Treasury Puts Financial Institutions “On Notice” Over “Very Powerful” New Turkey Sanctions

President Trump has again threatened more Turkey sanctions. In a surprise Treasury Department press briefing early Friday afternoon, Steven Mnuchin said the president has “authorized” new sanctions on NATO member Turkey over its ongoing assault on US-backed Syrian Kurdish groups in northern Syria, also as bipartisan legislation targeting Turkey has been introduced in both the House and Senate.

However, Mnuchin noted that the proposed sanctions have not been activated yet. “We are putting financial institutions on notice,” Mnuchin told reporters in the White House briefing room.

Treasury Secretary Mnuchin says POTUS is concerned about the ongoing military offensive by Turkey. Says President Trump has authorized significant authorities for new sanctions, but the US is not activating those sanctions yet. pic.twitter.com/1NfYRvu2vt

The treasury secretary further promised that any additional Turkey sanctions would be “very powerful”— this as the Pentagon in its own briefing on the same day tried to push back against the idea that the US had “authorized” Erdogan’s military operation, or that it had “abandoned” the Kurds.

The Turkish lira remained volatile on the news after selling off all day, still hovering near its weakest level since August, after a day earlier Turkish stocks and government bonds fell, combined with the great unknown of looming and now apparently ever closer Washington punitive sanctions.

This also after the Pentagon earlier of Friday condemned the Turkish assault on northeast Syria, despite US troops withdrawing from border positions deeper into bases in the country which enabled the Turkish offensive in the first place.

And in more bad news for Erdogan and Turkey’s economy, France announced on Friday that EU sanctions against Turkey are “on the table,” as other European nations led by Sweden are pushing an arms embargo on Ankara.

These matters assigned to the undersigned, where each plaintiff appears through Richard P. Leibowitz, Esq., come now before the court of its own initiative. Attorneys in good standing of the bar of a United States Court and the bar of the highest court of any state may practice in this court for a particular case in association with a member of the bar of this court. Local Civil Rule 83.1(e)(1). It appears Mr. Leibowitz’s standing has been called into question in the United States District Court for the Southern District of New York. Referred to as a “copyright troll,” in a case involving one of the plaintiffs named above, a district judge recently observed “Mr. Liebowitz has been sanctioned, reprimanded, and advised to ‘clean up [his] act’ by other judges of this Court.” Sands v. Bauer Media Grp. USA, LLC, No. 17-CV-9215 (LAK), 2019 WL 4464672, at *1 (S.D.N.Y. Sept. 18, 2019). Serious sanctions were imposed by the judge in that case on account of plaintiff’s discovery deficiencies, including requirement that Mr. Leibowitz personally pay defendant’s fees associated with advancing its motion to dismiss as a sanction for alleged discovery misconduct.

This judge joins the chorus of those telling this attorney to clean up his act. The dockets of each of the cases assigned to me, wherein this attorney represents a plaintiff, are littered with deficiency notices. This is a harbinger for troubled litigation ahead.

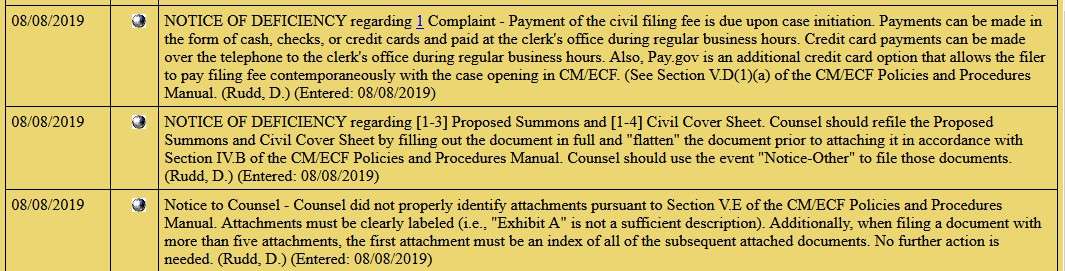

In Matthew Bradley, initiated by complaint filed June 18, 2019, Mr. Liebowitz was noticed June 19, 2019, to file notice of appearance. It took over two months for him to bring himself into compliance. In Steve Sands, filed August 8, 2019, he was noticed of numerous deficiencies at the case’s start including those noted below:

Counsel also was noticed of requirement in Steve Sands to associate local counsel:

The same notice was [repeated] August 27, 2019, and disregarded by the attorney. This court had to issue an order nearly two months after opening of the case, expressly drawing this deficiency to Mr. Liebowitz’s attention. If no appearance is made by the stated deadline of October 10, 2019, absent some showing of good cause, this case will be dismissed.

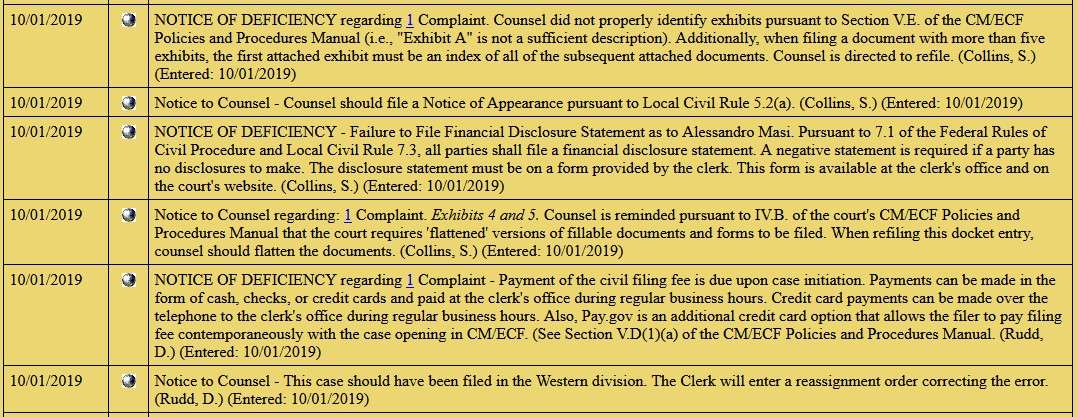

In Alessandro Masi, just filed September 30, 2019, a number of deficiencies immediately were noted by the clerk:

The problems described above appear rooted in a failure to read or understand the court’s CM/ECF Policies and Procedures Manual and the Court’s Local Civil Rules, and disrespect for the work of the clerk. There appears a failure to profit from the clerk’s work to bring issues to the attorney’s attention prompt attention. Many of the issues repeat themselves from case to case. See also Adlife Marketing & Communications Company, Inc. v. Carlie C’s Operation Center, Inc., No. 5:19-CV-405-BO (E.D.N.C. Sept. 16, 2019) (issuing deficiency notices concerning failure to pay civil filing fee; failure to identify attachments; issues with proposed summons and civil cover sheet; failure to associate local civil counsel; and failure to file financial disclosure statement have all been brought to counsel’s attention, in some instances more than one time and still, it appears, no remedial action on any noticed deficiency has been taken).

This attorney is noticed that he has until October 10, 2019, to cure any and every noticed deficiency in the three cases now assigned to me. If no address is made in accordance with this order, the cases at issue will be dismissed.

Filing mistakes, of course, happen; I’ve made my share. It generally takes an unusually substantial pattern of errors, though, for a judge to issue an order such as this one.

Dick’s Sporting Goods thinks it has found a solution to gun violence: destroying the company’s own inventory.

In an interview with CBS on October 6, CEO Edward Stack revealed that Dick’s had destroyed $5 million worth of “assault-style weapons” following the company’s 2018 decision to remove them from store shelves.

Stack’s stance on the issue began to take form in 2012, when he decided to stop selling the popular AR-15 rifle after Adam Lanza used one to kill 27 people at Sandy Hook Elementary School in Newtown, Connecticut. Stack initially planned to remove the guns from store shelves quietly, but outcry from the National Rifle Association, firearm enthusiasts, and gun companies led Stack to publicly defend his decision, saying he didn’t want “to sell…assault-style weapons that could inflict [the] kind of damage” seen at Sandy Hook.

After the 2018 shootings at Stoneman Douglas High School in Parkland, Florida, which left 17 people dead, Stack took his position a step further, announcing that Dick’s would no longer sell firearms of any type to anyone under 21 and that it would pull all the remaining “assault weapons” from its stores. Two months later, the CEO announced his plan to physically destroy Dick’s assault-weapon inventory. Stack claims these decisions were prompted by the fact that Nikolas Cruz, the Parkland shooter, had purchased a shotgun from Dick’s prior to his arrest. “Even though it wasn’t the gun he used. It could’ve been,” Stack said. (Yet Dick’s still sells shotguns.)

The backlash from the firearms industry was even bigger this time, with multiple gun companies, including O.F. Mossberg & Sons Inc., MKS Supply, and Springfield Armory, severing ties with the chain completely.

Destroying $5 million in gun inventory does not seem to be affecting Dick’s bottom line. This past August, Dick’s posted its best-earning quarter in three years.

It probably won’t affect crime much either. A 2018 analysis by the Rand Corporation “found no qualifying studies showing that bans on the sale of assault weapons and high-capacity magazines decreased any of the eight outcomes we investigated,” including mass shootings.

Those results shouldn’t be surprising. When people say “assault weapon,” they usually mean the guns banned by 1994’s Public Safety and Recreational Firearms Use Protection Act, which expired in 2004. That law classified certain weapons as “assault weapons” for reasons as simple as being a specific brand, such as Kalashnikov, or bearing a combination of certain physical characteristics, such as folding stocks and threaded barrels. As Reason‘s Jacob Sullum has noted, these features have no impact on a weapon’s lethality. The functional capabilities of an AR-15 and a standard hunting rifle are the same. Both are semiautomatic weapons, firing one bullet per pull of the trigger.

And yes, Dick’s still stocks and sells semiautomatic rifles that aren’t considered “assault weapons.” Unsurprisingly, those are sometimes used in mass shootings. The Ruger 10/22, available at Dick’s, was used in a massacre at Cascade Mall in Burlington, Washington, in 2016.

Stack acknowledged that the new policy won’t stop mass shootings, saying: “You’re probably right, it won’t. But if we do these things and it saves one life, don’t you think it’s worth it?” It’s unclear what life he thinks it saves to stop selling one arbitrarily defined group of weapons while continuing to offer mechanically identical products. Stack may need to brush up on how the guns he sells work.

from Latest – Reason.com https://ift.tt/2BfOUAd

via IFTTT

These matters assigned to the undersigned, where each plaintiff appears through Richard P. Leibowitz, Esq., come now before the court of its own initiative. Attorneys in good standing of the bar of a United States Court and the bar of the highest court of any state may practice in this court for a particular case in association with a member of the bar of this court. Local Civil Rule 83.1(e)(1). It appears Mr. Leibowitz’s standing has been called into question in the United States District Court for the Southern District of New York. Referred to as a “copyright troll,” in a case involving one of the plaintiffs named above, a district judge recently observed “Mr. Liebowitz has been sanctioned, reprimanded, and advised to ‘clean up [his] act’ by other judges of this Court.” Sands v. Bauer Media Grp. USA, LLC, No. 17-CV-9215 (LAK), 2019 WL 4464672, at *1 (S.D.N.Y. Sept. 18, 2019). Serious sanctions were imposed by the judge in that case on account of plaintiff’s discovery deficiencies, including requirement that Mr. Leibowitz personally pay defendant’s fees associated with advancing its motion to dismiss as a sanction for alleged discovery misconduct.

This judge joins the chorus of those telling this attorney to clean up his act. The dockets of each of the cases assigned to me, wherein this attorney represents a plaintiff, are littered with deficiency notices. This is a harbinger for troubled litigation ahead.

In Matthew Bradley, initiated by complaint filed June 18, 2019, Mr. Liebowitz was noticed June 19, 2019, to file notice of appearance. It took over two months for him to bring himself into compliance. In Steve Sands, filed August 8, 2019, he was noticed of numerous deficiencies at the case’s start including those noted below:

Counsel also was noticed of requirement in Steve Sands to associate local counsel:

The same notice was [repeated] August 27, 2019, and disregarded by the attorney. This court had to issue an order nearly two months after opening of the case, expressly drawing this deficiency to Mr. Liebowitz’s attention. If no appearance is made by the stated deadline of October 10, 2019, absent some showing of good cause, this case will be dismissed.

In Alessandro Masi, just filed September 30, 2019, a number of deficiencies immediately were noted by the clerk:

The problems described above appear rooted in a failure to read or understand the court’s CM/ECF Policies and Procedures Manual and the Court’s Local Civil Rules, and disrespect for the work of the clerk. There appears a failure to profit from the clerk’s work to bring issues to the attorney’s attention prompt attention. Many of the issues repeat themselves from case to case. See also Adlife Marketing & Communications Company, Inc. v. Carlie C’s Operation Center, Inc., No. 5:19-CV-405-BO (E.D.N.C. Sept. 16, 2019) (issuing deficiency notices concerning failure to pay civil filing fee; failure to identify attachments; issues with proposed summons and civil cover sheet; failure to associate local civil counsel; and failure to file financial disclosure statement have all been brought to counsel’s attention, in some instances more than one time and still, it appears, no remedial action on any noticed deficiency has been taken).

This attorney is noticed that he has until October 10, 2019, to cure any and every noticed deficiency in the three cases now assigned to me. If no address is made in accordance with this order, the cases at issue will be dismissed.

Filing mistakes, of course, happen; I’ve made my share. It generally takes an unusually substantial pattern of errors, though, for a judge to issue an order such as this one.

Dick’s Sporting Goods thinks it has found a solution to gun violence: destroying the company’s own inventory.

In an interview with CBS on October 6, CEO Edward Stack revealed that Dick’s had destroyed $5 million worth of “assault-style weapons” following the company’s 2018 decision to remove them from store shelves.

Stack’s stance on the issue began to take form in 2012, when he decided to stop selling the popular AR-15 rifle after Adam Lanza used one to kill 27 people at Sandy Hook Elementary School in Newtown, Connecticut. Stack initially planned to remove the guns from store shelves quietly, but outcry from the National Rifle Association, firearm enthusiasts, and gun companies led Stack to publicly defend his decision, saying he didn’t want “to sell…assault-style weapons that could inflict [the] kind of damage” seen at Sandy Hook.

After the 2018 shootings at Stoneman Douglas High School in Parkland, Florida, which left 17 people dead, Stack took his position a step further, announcing that Dick’s would no longer sell firearms of any type to anyone under 21 and that it would pull all the remaining “assault weapons” from its stores. Two months later, the CEO announced his plan to physically destroy Dick’s assault-weapon inventory. Stack claims these decisions were prompted by the fact that Nikolas Cruz, the Parkland shooter, had purchased a shotgun from Dick’s prior to his arrest. “Even though it wasn’t the gun he used. It could’ve been,” Stack said. (Yet Dick’s still sells shotguns.)

The backlash from the firearms industry was even bigger this time, with multiple gun companies, including O.F. Mossberg & Sons Inc., MKS Supply, and Springfield Armory, severing ties with the chain completely.

Destroying $5 million in gun inventory does not seem to be affecting Dick’s bottom line. This past August, Dick’s posted its best-earning quarter in three years.

It probably won’t affect crime much either. A 2018 analysis by the Rand Corporation “found no qualifying studies showing that bans on the sale of assault weapons and high-capacity magazines decreased any of the eight outcomes we investigated,” including mass shootings.

Those results shouldn’t be surprising. When people say “assault weapon,” they usually mean the guns banned by 1994’s Public Safety and Recreational Firearms Use Protection Act, which expired in 2004. That law classified certain weapons as “assault weapons” for reasons as simple as being a specific brand, such as Kalashnikov, or bearing a combination of certain physical characteristics, such as folding stocks and threaded barrels. As Reason‘s Jacob Sullum has noted, these features have no impact on a weapon’s lethality. The functional capabilities of an AR-15 and a standard hunting rifle are the same. Both are semiautomatic weapons, firing one bullet per pull of the trigger.

And yes, Dick’s still stocks and sells semiautomatic rifles that aren’t considered “assault weapons.” Unsurprisingly, those are sometimes used in mass shootings. The Ruger 10/22, available at Dick’s, was used in a massacre at Cascade Mall in Burlington, Washington, in 2016.

Stack acknowledged that the new policy won’t stop mass shootings, saying: “You’re probably right, it won’t. But if we do these things and it saves one life, don’t you think it’s worth it?” It’s unclear what life he thinks it saves to stop selling one arbitrarily defined group of weapons while continuing to offer mechanically identical products. Stack may need to brush up on how the guns he sells work.

from Latest – Reason.com https://ift.tt/2BfOUAd

via IFTTT

A transgender attendee at last night’s LGBTQ town hall accused host Nia Mikayla Henderson of perpetrating “violence” after the CNN host got the pronunciation of her name wrong.

Yes, really.

Henderson introduced the trans person as Shea Diamond, pronouncing the first name ‘shay’.

“Erm, it’s Shea Diamond,” responded the trans person, pronouncing the first name ‘she-a’.

“Put that on record,” said Diamond, to which Henderson responded, “It’s on the record.”

A black trans woman said it’s “violence” to misgender or alter a trans person’s name after Nia Mikayla Henderson mispronounced her name at the #EqualityTownHall. pic.twitter.com/JqXQjlwsD0

“Yes honey, it’s violence to misgender or to alter a name of a trans person, so let’s always get that right first” asserted Diamond.

As we reported earlier, this was by no means the only highlight of the night.

Get woke, get humiliated.

I used to think CNN town halls were a tragedy, but now I realize they’re a comedy.

Honk honk.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

FAA Safety Certification Of Boeing 737 MAX Was “Inadequate”, Report Finds

Capping offwhat has been a difficult week for Boeing, the Joint Authorities Technical Review (JATR), an international panel of air safety regulators, slammed the aerospace giant on Friday over its allegedly inadequate review of the 737 MAX 8’s safety systems that were tied to the two deadly crashes that killed 346 people.

Reuters and the New York Times obtained draft copies of the report, which is expected to be released on Friday.

The agency was asked by the FAA back in April to look into the oversight and approval process for the 737 MAX 8, which, thanks to a flood of leaks that have emerged between now and then, has been shown to have involved several serious lapses. Particularly where the MCAS anti-stall system was involved.

That system has been connected to the crashes in the months since the second plane went down in March, triggering the worldwide grounding of the 737 MAX.

JATR confirmed that the FAA’s oversight of MCAS was seriously lacking.

“The JATR team found that the MCAS was not evaluated as a complete and integrated function in the certification documents that were submitted to the FAA,” the 69-page series of findings and recommendations said. “The lack of a unified top-down development and evaluation of the system function and its safety analyses, combined with the extensive and fragmented documentation, made it difficult to assess whether compliance was fully demonstrated.”

The report comes as regulators around the world look into Boeing’s software changes and training revisions, and more claim they might delay the plane’s return to service to carry out additional screening even after the FAA has given Boeing the green light.

The plane, which is Boeing’s workhorse and its top-selling model, has been grounded since March 10, after an Ethiopian Airlines flight crashed minutes after taking off from the Addis Ababa airport, killing all 157 people on board. Six months earlier, a 737 MAX operated by Indonesia’s Lion Air crashed into the Java Sea minutes after taking off.

US airlines have pushed back their expectations on when the planes might return to service to next year as the true extent of the FAA’s oversight becomes apparent. Here’s more from the JATR report, which questioned the FAA’s “limited staffing” and “inadequate number of FAA specialists” involved in the certification process.

“With adequate FAA engagement and oversight, the extent of delegation does not in itself compromise safety,” the report said.

“However, in the B737 MAX program, the FAA had inadequate awareness of the MCAS function which, coupled with limited involvement, resulted in an inability of the FAA to provide an independent assessment of the adequacy of the Boeing-proposed certification activities associated with MCAS.”

The report added that there were signs FAA employees “faced undue pressure…which may be attributed to conflicting priorities and an environment that does not support FAA requirements.”

To sum up, the FAA simply wasn’t able to assess whether MCAS was safe or unsafe.

“The F.A.A. had inadequate awareness of the MCAS function,” which means the agency wasn’t even equipped to evaluate the system.

The report also confirmed that, at times, FAA employees often faced conflicts of interest in certifying the 737 MAX 8.

Watch Treasury Secretary Mnuchin’s Ad Hoc Press Briefing

In a last-minute announcement, the Treasury Department said early Friday afternoon that Secretary Steven Mnuchin would hold an impromptu press conference.

However, not wanting to front-run President Trump, Mnuchin clarified that the briefing won’t pertain to the talks with Chinese Vice Premier Liu He over a US-China trade deal. Instead, Mnuchin will focus on “an unrelated issue.” Though he will inevitably be asked about reports that a “skinny deal” was reached.

So, what could it be about? It’s possible that Mnuchin plans to address the effort to force the turnover of Trump’s tax returns.

As Michael Every, senior strategist at Rabobank, explained in a Thursday research note, the rumors about a US-China currency accord probably aren’t accurate.

A recession is emerging with interest rate curves inverted, the end of the business cycle at hand, world trade falling, and consumers and businesses beginning to pull back on spending. The question is: will monetary or fiscal stimulus turn around a recession?

In this post, we find both stimulus alternatives likely to be too weak to have the necessary economic impact to lift the economy out of a recession. Finally, we will identify the key characteristics of a coming recession and the implications for investors.

Our economy is at the nexus of several major economic trends formed over decades that are limiting monetary and fiscal options. The monetary policy of central banks has caused world economies to be abundant in liquidity, yet producing limited growth. Central bankers in Japan and Europe have been trying to revive growth with $17 trillion injections using negative interest rates. Japan can barely keep its economy growing with an estimate of GDP at .5 % through 2019. The Japanese central bank holds 200 % of GDP in government debt. The European Central Bank holds 85 % of GDP in debt and uses negative interest rates as well. Germany is in a manufacturing recession with the most recent PMI in manufacturing activity at 47.3 and other European economies contracting toward near-zero GDP growth.

Lance Roberts notes that the world economy is not running on a solid economic foundation if there is $17 trillion in negative-yielding debt in his blog, Powell Fails, Trump Rails, The Failure of Negative Rates. He questions the ability of negative interest policies to stabilize world economies,

“You don’t have $17 Trillion in negative-yielding sovereign debt if there is economic and fiscal stability.”

Negative interest rates and extreme monetary stimulus policies have distorted financial relationships between debt and risk assets. This financial distortion has created a significantly wider gap between the 90 % and the top 1 % in wealth.

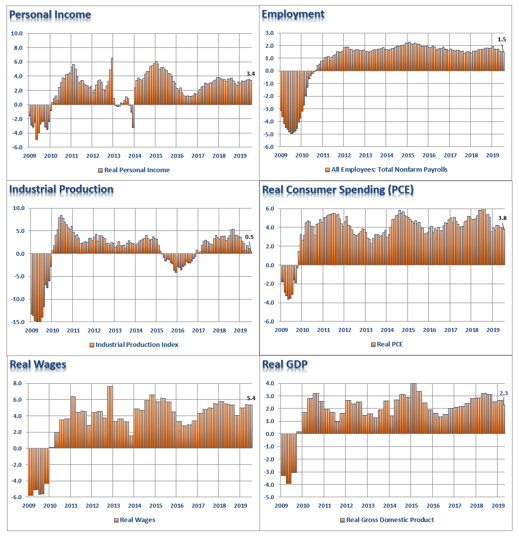

Roberts outlines in the six panel chart below how personal income, employment, industrial production, real consumer spending, real wages, and real GDP are all weakening in the U.S.:

Source: RIA – 8/23/19

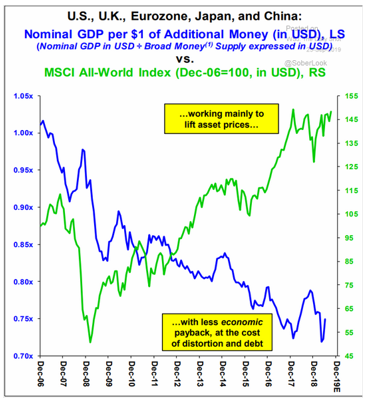

Trillions of dollars of monetary stimulus have not created prosperity for all. The chart below shows how liquidity fueled a dramatic increase in asset prices while the amount of world GDP per money supply declined by about 25 %:

Sources: The Wall Street Journal, The Daily Shot – 9/23/19

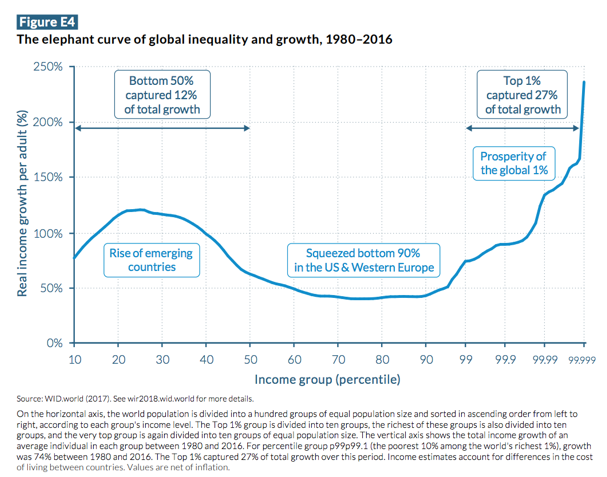

Low interest rates have not driven real growth in wages, productivity, innovation, and services development that create real wealth for the working class. Instead, wealth and income are concentrated in the top 1 %. The concentration of wealth in the top one percent is at the highest level since 1929. The World Inequality Report notes inequality has squeezed the middle class between emerging countries and the U.S. and Europe. The top 1 % has received twice the financial growth benefits as the bottom 50 % since 1980:

Source: World Inequality Lab, Thomas Piketty, Gabriel Zucman et al – 2018

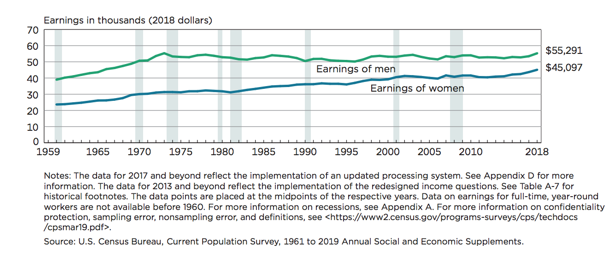

There are several reasons monetary stimulus by itself has not lifted the incomes of the middle class. One of the big causes is that stimulus money has not translated into wage increases for most workers. U.S. real earnings for men have essentially been flat since 1975, while earnings for women have increased though basically flat since 2000:

Source: U.S. Census Bureau – 9/10/19

If monetary policy is not working, then fiscal investment from private and public sectors is necessary to drive an economic reversal. But, will the private and public sector sectors have the necessary tools to bring new life to an economy in decline?

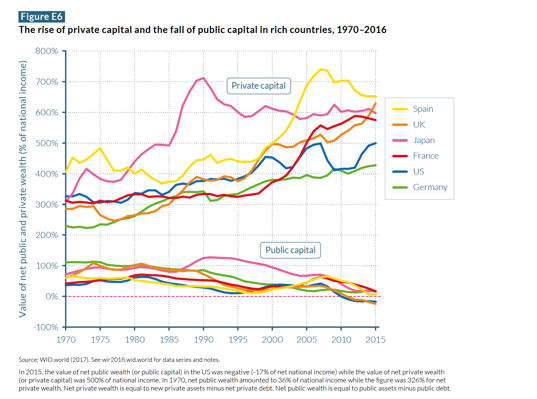

Wealth Creation Has Gone to the Private Sector

The last 40 years have seen the rise of private capital worldwide while public capital has declined. In 2015, the value of net public wealth (or public capital) in the US was negative -17% of net national income, while the value of net private wealth (or private capital) was 500% of national income. In comparison to 1970, net public wealth amounted to 36% of national income, while net private wealth was at 326 %.

Source: World Inequality Lab, Thomas Piketty, Gabriel Zucman et al – 2018

Essentially, world banks and governments have built monetary and fiscal economic systems that increased private wealth at the expense of public wealth. The lack of public capital makes the creation of public goods and services nearly impossible. The development of public goods and services like basic research and development, education and health services are necessary for an economic rebound. The economy will need a huge stimulus ‘lifting’ program and yet the capital necessary to do the job is in the private sector where private individuals make investment allocation decisions.

Why is building high levels of private capital a problem? Because, as we have discussed, private wealth is now concentrated in the top 1 %, while 70 % of U.S GDP is dependent on consumer spending. The 90 % have been working for stagnant wages for decades, right along with diminishing GDP growth. There is a direct correlation between wealth creation for all the people and GDP growth.

Corporations Are Not In A Position to Invest

Some corporations certainly have invested in their businesses, people, and technology. The issue is the majority of corporations are now financially strapped. Many corporate executives have made profit allocation decisions to pay themselves and their stockholders well at the expense of workers, their communities and the economy.

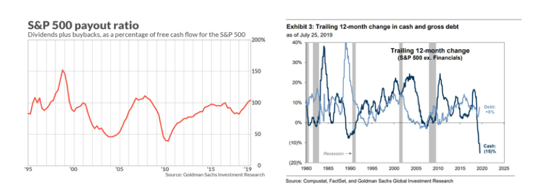

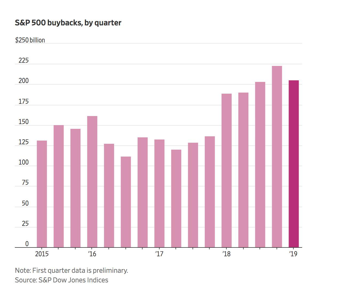

S & P 500 corporations are paying out more cash than they are taking in, creating a cash flow crunch at a – 15 % rate (that’s right they are burning cash) to maintain stock buyback and dividend levels:

In 2018 stock buybacks at $1.01 trillion were at the highest level they have ever been since buybacks were allowed under the 1982 SEC safe harbor provision decision. It is interesting to consider where our economy would be today if corporations spent the money they were wasting on boosting stock prices and instead invested in long term value creation. One trillion dollars invested in raising wages, research, and development, cutting prices, employee education, and reducing health care premiums would have made a significant impact lifting the financial position of millions. This year stock buybacks have fallen back slightly as debt loads increase and sales fall:

Source: Dow Jones – 7/2019

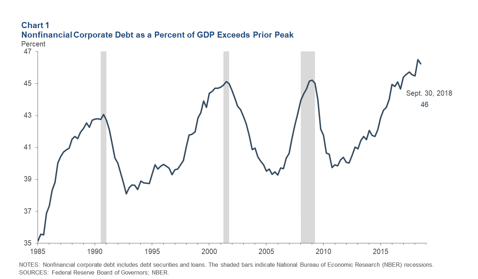

Many corporations with tight cash flows have borrowed to purchase shares, pay dividends and keep their stock price elevated causing corporate debt to hit new highs as a percentage of GDP (note recessions followed three peaks):

Source: Federal Reserve Bank of Dallas – 3/6/2019

Corporate debt has ballooned to 46 % of GDP totaling $5.7 trillion in 2018 versus $2.2 trillion in 2008. While the bulk of these nonfinancial corporate bonds have been investment grade, many bond covenants have become weaker as corporations seek more funding. Some bondholders may find their investment not as secure as they thought resulting in significantly less than 100 % return of principal at maturity.

In a recession, corporate sales fall, cash flow goes negative, high debt payments become hard to make, employees are laid off and management tries to hold on. Only a select set of major corporations have cash hoards to ride out a recession, and others may be able obtain loans at steep interest rates, if at all. Other companies may try going to the stock market which will be problematic with low valuations. Plus, investors will be reluctant to buy stock in negative cash flow companies.

Thus, most corporations will be hard pressed to invest the billions of dollars necessary to turnaround a recession. Instead, they will be just trying to keep the doors open, the lights on, and maintain staffing levels to hold on until the day sales stop falling and finally turn up.

Public Sector is Also Tapped Out

In past recessions, federal policy makers have turned to fiscal policy – public spending on infrastructure projects, research development, training, corporate partnerships, and public services to revive the economy. When the 2008 financial crisis was at its peak the Bush administration, followed by the Obama government pumped fiscal stimulus of $983 billion in spending over four years on roads, bridges, airports, and other projects. The Fed funds interest rate before the recession was at 5.25 % at the peak allowing lower rates to have plenty of impact. Today, with rates at 1.75-2.00 %, the impact will be negligible. In 2008, it was the combined massive injection of monetary and fiscal stimulus that created a V-shaped recession with the economy back on a path to recovery in 18 months. It was not monetary policy alone that moved the economy forward. However, the recession caused lasting financial damage to wealth of millions. Many retirement portfolios lost 40 – 60 % of their value, millions of homeowners lost their homes, thousands of workers were laid off late in their careers and unable to find comparable jobs. The Great Recession changed many people’s lives permanently, yet it was relatively short-lived compared to the Great Depression.

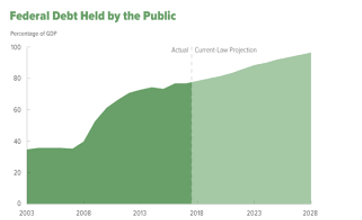

As noted in the chart above, public sector wealth has actually moved to negative levels in the U.S. at – 17 % of national income. Our federal government is running a $1 trillion deficit per year. In 2007, the federal government debt level was at 39 % of GDP. The Congressional Budget Office projects that by 2028 the Federal deficit will be at 100 % of GDP

Source: CBO – 4/9/19

We are at a different time economically than 2008. Today with Federal debt is over 100% of GDP and expected to grow rapidly. The Feds balance sheet is still excessive and they formally stopped reducing the size (QT). In a recession federal policymakers will likely make spending cuts to keep the deficit from going exponential. Policy makers will be limited by the twin deficits of $22.0 trillion national debt and ongoing deficits of $1+ trillion a year, eroding investor confidence in U.S. bonds. The problem is the political consensus for fiscal stimulus in 2008 – 2009 does not exist today, and it will probably be even worse after the 2020 election. Our cultural, social and political fabric is so frayed as a result of decades of divisive politics it is likely to take years to sort out during a recession. Our political leaders will be fixing the politics of our country while searching for intelligent stimulus solutions to be developed, agreed upon and implemented.

What Will the Next Recession Look Like?

We don’t know when the next recession will come. Yet, present trends do tell us what the structure of a recession might look like, as a deep U- shaped, slow recovery measured in years not months:

Corporations Short of Cash – Corporations already strapped are short on cash, will lay off workers, pull back spending, and are stuck paying off huge debts instead of investing.

Federal Government Spending Cuts – The federal government caught with falling revenues from corporations and individuals, is forced to make deep cuts first in discretionary spending and then social services and transfer funding programs. The reduction of transfer programs will drive slower consumer spending.

Consumers Pull Back Spending – Consumers will be forced to tighten budgets, pay off expensive car loans and student debt, and for those laid off seeking work anywhere they can find a job.

World Trade Declines – World trade will not be a source of rebuilding sales growth as a result of the China – US trade war, and tariffs with Europe and Japan. We expect no trade deal or a small deal with the majority of tariffs to stay in place. In other words, just reversing some tariffs will not be enough to restart sales. New buyer – seller relationships are already set, closing sales channels to US companies. New country alliances are already in place, leaving the US closed out of emerging high growth markets. A successor Trans Pacific Partnership (TPP) agreement with Japan and eleven other countries was signed in March, 2018 without the US. China is negotiating a new agreement with the EU. EU and China trade totals 365 billion euros per year. China is working with a federation of African countries to gain favorable trade access to their markets.

Pension Payments in Jeopardy – Workers dependent on corporate and public pensions may see their benefits cut from pensions, which are poorly funded today with markets at all-time highs. GE just announced freezing pensions for 20,000 employees, the harbinger of a possible trend that will reduce consumer spending

Investment Environment Uncertain – Uncertainty in investments will be extremely high, ‘get rich quick’ schemes will flourish as they did in 2008 – 2009 and 2000.

Fed Implements Low Rates & QE – The Fed is likely to implement very low interest rates (though not negative rates), and QE with liquidity in abundance but the economy will have low inflation, and declining GDP feeling like the Japanese economic stasis – ‘locked in irons’.

Implications for Investors

The following recommendations are intended for consideration just prior or during a recession with a sharp decline in the markets, not necessarily for today’s markets.

Cash – It is crucial to maintain a significant cash hoard so you can purchase corporate stocks when they cheapen. The SPX could decline by 40 – 50 % or more when the economy is in recession. Yet, good values in some stocks will be available. At the 1500 level, there is an excellent opportunity to make good long term growth and value investments based on sound research.

CDs – as Will Rogers noted during the Depression, “I’m more interested in Return of my Capital than Return on my Capital”, a prudent investor should be too. CDs are FDIC insured while offering lower interest rates than other investments. Importantly, they provide return of capital and allow you to sleep at night.

Bonds – U.S. Treasuries certainly provide safety, return of principal, and during a recession will provide better overall returns than high-risk equity investments. Corporate bonds may come under greater scrutiny by investors even for so-called ‘blue chips’ like General Electric. The firm is falling on hard times with $156 billion in debt. GE is seeking business direction and selling off assets. The major conglomerate’s bonds have declined in value by 2.5 % last year with their rating dropped to BBB. Now with new management the price of GE bonds is climbing up slightly.

Utilities – are regulated to have a profit. While they may see declining revenues due to less energy use by corporations and individuals, they still will pay dividends to shareholders as they did in 2008. Consumer staple companies are likely to be cash flow strained; most did not pay dividends to investors during the 2008 – 2009 recession. REITs need to be evaluated on a company by company basis to determine how secure their cash streams are from leases. During the 2008 – 2009 downturn, some REITs stopped paying dividends due to declining revenues from lease defaults.

Growth & ValueEquities– invest in new sectors that have government support or emerging demand based on social trends like climate change: renewables, water, carbon emission recovery, environmental cleanup. From our Navigating A Two Block Trade World – US and China post, we noted possible investments in bridge companies between the two trade blocks; services, and countries that act as bridges like Australia. Look for firms with good cash positions to ride out the recession, companies in new markets with sales generated by innovations, or problem solving products that require spending by customers. For example, seniors will have to spend money on health services. Companies serving an increasingly aging population with innovative low cost health solutions are likely to see good demand and sales growth.

The intelligent investor will do well to ‘hope for the best, but plan for the worst’ in terms of portfolio management in a coming recession. Asking hard questions of financial product executives and doing your own research will likely be keys to survival.

In the end, Americans have always pulled together, solved problems, and moved ahead toward an even better future. After a reversion to the mean in the capital markets and an economic recession things will improve. A reversion in social and culture values is likely to happen in parallel to the financial reversion. The complacency, greed, and selfishness that drove the present economic extremes will give way to a new appreciation of values like self-sacrifice, service, fairness, fair wages and benefits for workers, and creation of a renewed economy that creates financial opportunities for all, not just the few.

“This is going to be one forum where you’re going to hear very little disagreement between the candidates,” former Vice President Joe Biden observed. He was absolutely correct.

The event was a CNN town hall in Los Angeles Thursday night, where nine Democratic candidates were interviewed about their stances on LGBT issues. Those who tuned in for the four-and-a-half-hour show were treated, with few exceptions, to each candidate answering variations of the same questions in the same ways. What will they do about any continued discrimination against LGBT? They’ll fight against it and support the Equality Act. What will they do about improving access to HIV drugs and preventative medication? They’ll go after those greedy pharmaceutical companies, and all the drugs will be covered under their health care plans. What will they do about hate crimes? They’ll unleash the Department of Justice against them, and hate crimes will definitely be exempted from any push to make federal sentencing less punitive. What will they do about other countries who treat arrest or execute LGBT people? They’ll withhold aid and possibly even trade. What will they do about people who invoke their religious beliefs to justify discriminating against LGBT people? They won’t let them, and they’ll strip churches and nonprofits of their tax-exempt status if they try. What will they do about conversion therapy? Ban it. What will they do about bullying in schools and teen suicide? Get rid of Education Secretary Betsy DeVos. (Seriously, her name was invoked more frequently than Donald Trump’s.)

The too-long, didn’t-watch version of last night’s summit: Tell us who did you wrong and we’ll go punish them.

The moment that’s produced the biggest waves in the media is when candidate Beto O’Rourke promised to strip tax-exempt status from churches and religious schools not just for actually discriminating against LGBT people but for simply speaking in opposition to same-sex marriage. The audience applauded, and he added, “There can be no reward, no benefit, no tax break for anyone, any institution, or any organization that denies the full human rights and full civil rights of every single one of us.”

Here’s the clip:

Beto O’Rourke on religious institutions losing tax-exempt status for opposing same-sex marriage: "There can be no reward, no benefit, no tax break for anyone … that denies the full human rights and the full civil rights of every single one of us" #EqualityTownHallpic.twitter.com/tjwVGqv5h0

Needless to say, punishing churches for their positions, not just their actions, is thoroughly, unquestionably unconstitutional. It should be absolutely abhorrent to anyone concerned with freedom of speech or freedom of religion.

It shouldn’t come as much of a surprise that the candidate who thinks he’s somehow going to force Americans to turn in their guns also has little grasp that his tax-exemption plan will get him laughed out of court. If you care about LGBT rights, you should be glad O’Rourke doesn’t have a shot: The backlash against him as a nominee would be massive. His response didn’t go viral because it’s worth praising; it went viral because it’s a horrifyingly bad idea that will lead to terrible government abuses.

But this is what you get when the country is locked in a culture war driven by a desire to punish people you disagree with—and when millions of people believe that the president’s role is to lead this war. Donald Trump is a symptom, not the cause, of the problem.

Almost every answer to every questioner featured a call for more federal involvement in people’s lives. Thursday morning before the town hall, three candidates—Sen. Elizabeth Warren (D–Mass.), Sen. Kamala Harris (D–Calif.), and South Bend Mayor Pete Buttigieg—all released lengthy plans offering not a chicken in every pot for LGBT Americans, but an entire chorus of federal bureaucrats, lawyers, and regulations overseeing every problem. No candidate even gently suggested that any LGBT issue would best be handled locally and not by the inhabitant of the White House. Indeed, when CNN’s Chris Cuomo noted that the states, not the federal government, controlled many of these laws and regulations, Harris condescendingly explained that federal laws take precedence over state and local laws.

Of course, for Harris (or any of these candidates) to fulfill promises like passing the Equality Act (which every candidate onstage supported), they’ll have to sway Congress. Biden and Sen. Amy Klobuchar (D–Minn.) both called for voters to flip control of the Senate to the Democrats in order to make sure they can get these laws passed. Several candidates talked up the importance of controlling the next Supreme Court nominations. All the candidates promised to overturn Trump’s executive orders pushing transgender troops out of military service and permitting some government contractors to discriminate against LGBT people, but nobody wanted to consider the possibility that Trump’s ability to make such sweeping changes without oversight is an indication that the office of the president is itself too powerful.

Members of the LGBT community should know better than this. After decades of fighting to be treated as equal members of society, we shouldn’t be trying to put the boot of the federal government on the neck of anybody who is not violating our individual liberty. Not getting a wedding cake, or not getting to teach at a Catholic school, is not enough to justify the boot.

Ultimately, the Democratic candidates offered LGBT voters whatever they wanted—so long as what they wanted was more meddling in people’s lives. This is not a path to peace or an end to this bipartisan culture wars. It’s an escalation. Those of us in the LGBT community who want less government involvement in our lives and want to be left alone to deal with cultural conflicts through voluntary engagement with our opponents—we’re all out of luck. There was nobody at this town hall, either among the candidates or the carefully vetted questioners, to represent us.

from Latest – Reason.com https://ift.tt/33mIcEo

via IFTTT