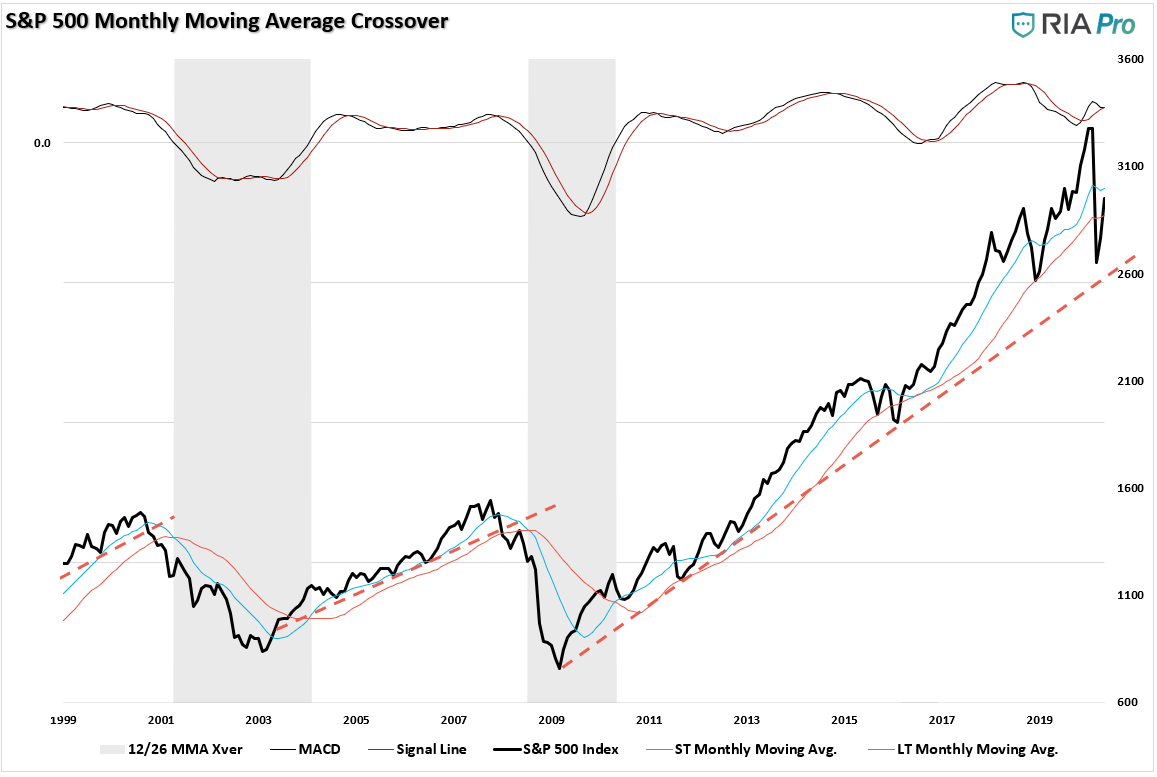

As noted last week,the markets remain stuck between the 50- and 200-dma. That remained the case this week once again, keeping any expansion of equity positioning on hold.

The shaded blue area shows the containment of the market between the two moving averages. With the market very overbought short-term (orange indicator in the background), there is downside pressure on prices short-term.

This past week, the current risk/reward ranges remain unfavorable. I have updated the levels from last week:

-7.6% to the 50-dma vs. +5% to the March peak.

-11.5% to -17.1% to the late March peak or early April low vs. +13.6% to all-time highs.

-24.7% to March 23rd lows vs. 13.6% to all-time highs.

For now, we remain “stuck in the middle.”

However, if the markets can break above the 200-dma, and maintain that level, it would suggest the bull market is back in play. Such would change the focus from a retest of previous support to a push back to all-time highs.

While such would be hard to believe, given the economic devastation currently at hand, technically, it would suggest the decline in March was only a “correction” and not the beginning of a “bear market.”

Was This A Correction Or A Bear Market?

Price is nothing more than a reflection of the “psychology” of market participants. A potential mistake in evaluating “bull” or “bear” markets is using a “20% advance or decline” to distinguish between them.

Such brings up an interesting question. After a decade-long bull market, which stretched prices to extremes above long-term trends, is the 20% measure still valid?

To answer that question, let’s clarify the premise.

A bull market is when the price of the market is trending higher over a long-term period.

A bear market is when the previous advance breaks, and prices begin to trend lower.

The chart below provides a visual of the distinction. When you look at price “trends,” the difference becomes both apparent and useful.

This distinction is important.

“Corrections” generally occur over very short time frames, do not break the prevailing trend in prices, and are quickly resolved by markets reversing to new highs.

“Bear Markets” tend to be long-term affairs where prices grind sideways or lower over several months as valuations are reverted.

Using monthly closing data, the “correction” in March was unusually swift but did not break the long-term bullish trend. Such suggests the bull market that began in 2009 is still intact as long as the monthly trend line holds.

However, I have noted the market may be in the process of a topping pattern. The 2018 and 2020 peaks are currently forming the “left shoulder” and “head” of the topping process. Such would also suggest the “neckline” is the running bull trend from the 2009 lows. A market peak without setting a new high that violates the bull trend line would define a “bear market.”

Valuations

Valuations also suggest the decline in March was just a correction and not a bear market.

The chart below shows the history of secular bull market periods going back to 1871 using data from Dr. Robert Shiller. The defining difference between bull and bear markets is valuations. Bull markets are defined by expanding valuations, while bear markets contract valuations. Market “corrections” tend to have minimal impacts on valuations.

During trending bull markets, valuations remain elevated even during corrective processes. However, during bear markets, valuations tend to compress as prices adjust to weaker earnings growth.

The surge in valuations in recent weeks suggests the markets remain in a “corrective” process rather than a “bear market.”

While monetary policy has kept the valuation reversion process from completing, it likely hasn’t eliminated the risk.

If March was indeed just a “correction,” then earnings will need to quickly recover back to previous levels to support current valuation levels. However, given the economic devastation, I suspect the “correction” was likely the beginning of a more protracted valuation reversion process and “bear market.”

Monthly Moving Average Crossover

Lastly, from a purely technical perspective, we have not confirmed a “traditional” bear market. One of the key identifiers of a “bear market” versus a “correction” is the “bearish crossover” of the short and long-term moving averages.

In both 2001 and 2008, the moving average crossover delineated the start of a more protected “bear market” process. Despite the one month correction in March, the rebound in April and May have kept the moving average crossover from triggering.

Without a monthly moving average crossover, there is little historical precedent to suggest the decline in March was anything other than a deep corrective process.

However, if we are in the beginning stages of a longer-term valuation reversion process, then the crossover will occur in the months ahead.

Bear Markets Begin With Corrections

There is one crucial point that needs addressing.

Was the decline in March just a “correction” or the start of a “bear market?”

Only time will tell with certainty, but all “bear markets” begin with a “correction.”

Every bear market in history has an initial decline, a reflexive rally, then a protracted decline which reverts market excesses. Investors never know where they are in the process until the rally’s completion from the initial fall.

Given the deviation of the market, due to Fed stimulus, was so extremely deviated above long-term trends, the depth of the “correction” was not surprising. However, if this is the start of a “bear market,” confirmed by a change in trend, the depth of the decline will eventually be equally as great.

A Growing List Of Concerns

What we do know is there is a litany of warning signs which suggest risk greatly outweighs the reward of being aggressively invested in the markets. Here is a shortlist:

Frantic positioning and extreme readings in market internals.

Speculative positioning in options markets.

Small investors are incredibly bullish.

Put/Call ratios are massively elevated.

A lack of risk hedging.

Buying interest has hit extremes.

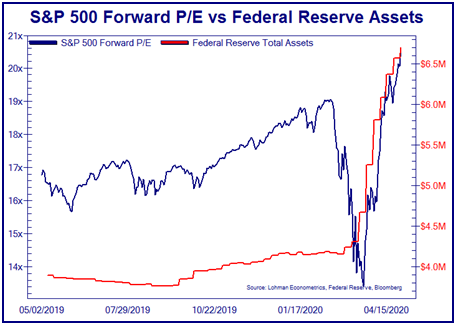

Forward P/E ratios are historically rich.

Value to Growth ratios are at some of the lowest levels in history.

The hope for a “V-shaped” recovery is likely to be disappointed.

Expectations for an earnings recovery remain overly exuberant.

Unemployment is likely to remain elevated longer than most expect.

Consumer confidence will likely not bounce back as fast as hoped.

Rising delinquencies, defaults, and bankruptcies will be problematic.

A resurgence of COVID-19 later this summer will set back recovery expectations.

Fed liquidity is likely much more limited than markets expect.

A resurgence of a “trade war” with China could not be more ill-timed.

Risk of acceleration of geopolitical tensions with China

Corporate profitability will plunge

I could go on, but you get the idea.

Don’t Fight The Fed

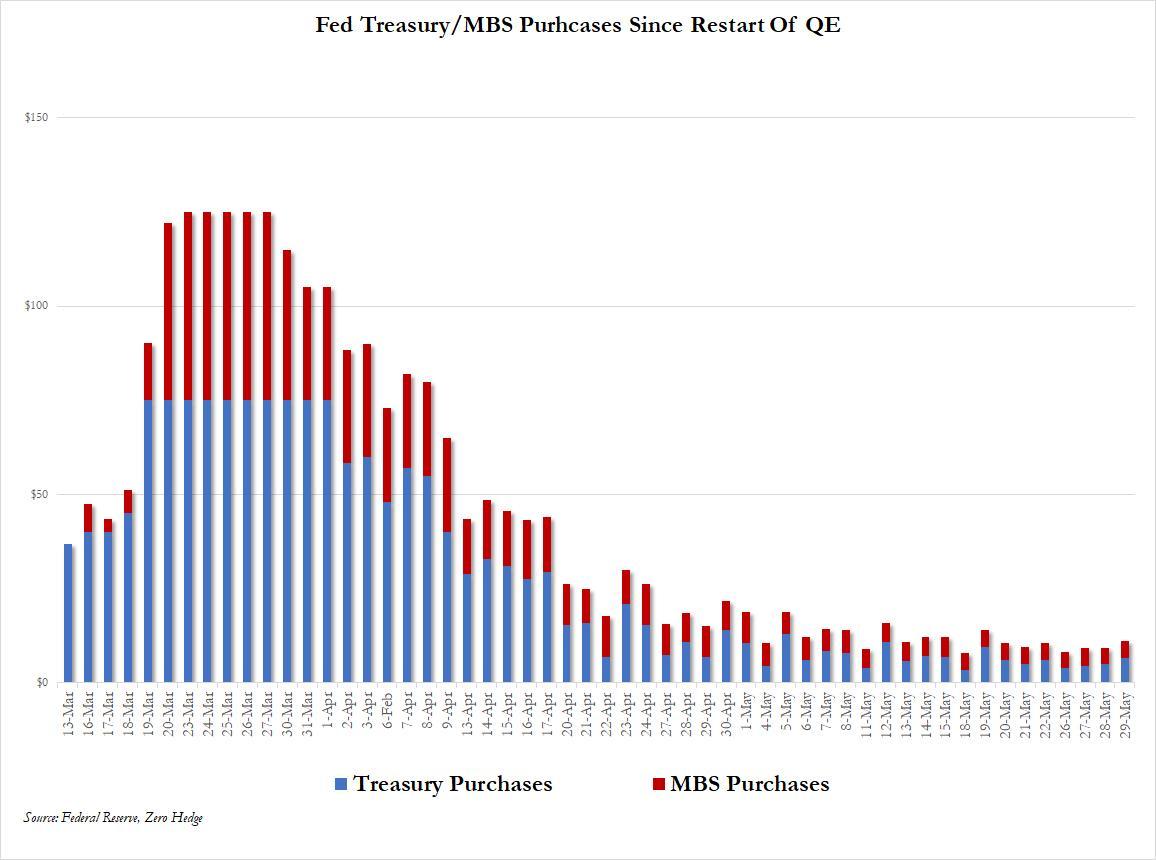

With the amount of economic devastation that is in process, and will likely continue for quite some time, it is hard to suggest the decline in March was only a “correction.” There are numerous headwinds that could derail markets in the months ahead despite the Fed’s liquidity.

Speaking of liquidity, the basis of the “Don’t Fight The Fed” mantra, has now shrunk from $75 billion/day in March to just $5 billion/day.

The most logical view is that we are in the midst of a torrid reflexive rally that seems to be losing steam. Such would be typical of a reflexive “bear market rally.,” Over the next couple of months the markets will have to come to grips with economic and fundamental realities.

The next leg lower will likely surprise most investors.

Positioning Update

This analysis is part of our thought process as we continue to weigh “equity risk” within our portfolios.

We remain focused on our positioning, and we again modestly increased our equity exposure during this past week. However, we also balanced that increase with matched weights in Treasury bonds to hedge our risk.

Taking profits in our trading positions also continues to be a “staple” in our management process. This past week we took profits in the Communications space that has gotten extremely extended. We also continue to rebalance portfolios regularly.

We don’t like the risk/reward of the market currently, and suspect we will have a better opportunity to increase equity risk later this summer. But, if things change, we will also.

What is essential is remembering one investing truth. Investing isn’t a competition of who gets to say “I bought the bottom.” Investing is about putting capital to work when reward outweighs the risk.

That is not today.

Bear markets have a way of “suckering” investors back into the market to inflict the most pain possible.

Such is why “bear markets” never end with optimism but in despair.

via ZeroHedge News https://ift.tt/2LUBjn5 Tyler Durden

Meet The Super Exclusive Family Office Investing Club Run By An Ex-Goldman Prop Trader Tyler Durden

Sun, 05/24/2020 – 09:55

Ex-Goldman Sachs prop trader Lex van Dam knows where his bread is being buttered: family offices. And what’s better than one family office? A whole bunch of family offices together.

Working for a single family office called Rinkelberg Capital, van Dam had the idea of group together more family offices and create a club to “bolster their dealmaking opportunities,” according to Bloomberg. So van Dam started the London-based SFO Alliance, which sets out to be “a forum to discuss common problems and find investment solutions to match [family office] idiosyncrasies.”

Keith Johnston, chief executive officer of SFO, said: “Single family offices are a unique set of long-term, often even multigenerational investors.”

The company is going to host private events where offices can come together to discuss things like private equity deals, real estate and direct investments in businesses. Family offices have been increasingly considering private debt, with the number of offices active in the asset class more than doubling since 2015.

Van Dam joined Goldman Sachs in 1992 and ran one of the bank’s prop desks before going to work at Rinkelberg. One might also recognize van Dam from the UK show “Million Dollar Traders“.

On SFO’s website, he is quoted as saying: “I have worked for a family office for over 15 years now. Most of us come across the same companies and funds and we could save ourselves a lot of time, effort and money if we had our own informal curated network of high quality single family offices where we share our experiences.”

And entry into the alliance seems to be exclusive. SFO’s website says of the alliance:

“We are successful by adhering to a strict membership policy. Each member is individually vetted by the SFO Alliance board. The vast majority of our members are personally referred by existing members.”

“Because our founding members are single family offices we understand the importance of peer-to-peer discussions, relevant external content, and a solicitation-free environment. We serve the interests of our member family offices only. The club is not for profit and free to members,” it says.

Family offices had, on average, $1.3 billion in assets last year and their investing setups are as sophisticated as any investment bank on Wall Street. In fact, months ago here on Zero Hedge, we reported about how some family offices were getting direct lines to the trading desks at investment banks.

via ZeroHedge News https://ift.tt/3geGyvX Tyler Durden

A report published by the European Commission in late 2019 reveals that the EU has been looking to increase the scope and power of vaccination programmes since well before the current “pandemic”.

The endpoint of the Roadmap is, among many other things, to introduce a “common vaccination card/passport” for all EU citizens.

This proposal will be appearing before the commission in 2022, with a “feasibility study” set to run from 2019 through 2021 (meaning, as of now, it’s about halfway through).

To underline the point: The “vaccination roadmap” is not an improvised response to the Covid19 pandemic, but rather an ongoing plan with roots going back to 2018, when the EU released a survey of the public’s attitude toward vaccines titled “2018 State of Vaccine Confidence”

In the 3rd quarter of 2019 these reports were all combined into the latest version of the the “Vaccination Roadmap”, a long-term policy plan to spread vaccine “awareness and understanding” whilst counteracting “vaccine myths” and combatting “vaccine hesitancy”.

You can read the entire report here, but below are some of the more concerning highlights [emphasis throughout is ours]:

“Examine the feasibility of developing a common vaccinationcard/passport for EU citizens“

“Develop EU guidance for establishing comprehensive electronic immunization information systems for effective monitoring of immunization programmes.”

“overcome the legal and technical barriers impeding the interoperability of national immunisation information systems”

On the 12th September 2019, at the joint EU-WHO “Global Vaccination Summit”, they announced the “10 Actions Towards Vaccination for All”, which cover much of the same ground.

For those who don’t know, Event 201 was a simulated pandemic exercise focusing on a zoonotic novel coronavirus originating in bats. It was sponsored by Johns Hopkins Center for Health Security, the World Economic Forum, and the Bill & Melinda Gates Foundation.

In November of 2019, these suggestions were published as a “call to action”.

One month later, China reported the first cases of Covid19.

To be clear here (and forestall any below-the-line arguments): this is not about vaccines, their effectiveness, safety or lack thereof.

The point is that proposed COVID countermeasures, which have been presented to the public as emergency measures thought up on the fly by panicking institutions, have in fact existed since before the emergence the disease.

They already wanted to monitor your vaccination records and tie that to your passport, introduce mandatory vaccinations and clampdown on “misinformation”. They just didn’t have a reason yet.

This was a situation which required a crisis and, fortuitously, it got one.

Navy’s Oldest Warship Breaks Its Days-At-Sea Record While Avoiding Virus Tyler Durden

Sun, 05/24/2020 – 08:45

We previously reported that amid the coronavirus pandemic’s impact on military ranks, the US Navy began keeping warships withcrew deemed “clean” — that is, completely free of coronavirus cases— deployed for an additional length of time with no port calls and no deployment end date amid a worsening crisis aboard other ships.

Currently the US has multiple warships out at sea with no ‘return to shore’ dates. And now The Hill reports based on Navy statements, “The Navy’s oldest operational warship has broken its record for the most days at sea, the military branch said Thursday.”

USS Blue Ridge, via Military.com

The Pentagon wished to avoid another USS Theodore Roosevelt disaster of course, which US rivals and China and Russia kept a close eye on, no doubt taking note of just how quickly a state-of-the-art nuclear carrier was taken out by the virus.

The concern is simply that a return to shore brings greater exposure for the uninfected crew to become infected. The Navy said in its statement that the USS Blue Ridge has been at sea for 69 days as of Thursday. The previous record of 64 days was set during the Vietnam war, nearly 50 years ago.

The Blue Ridge is classified as naval command and control amphibious ship, and is the oldest operational ship in the Navy.

Blue Ridge’s previous record of 64 days was set during the Vietnam War when she left port April 5, 1972 and stayed at sea in and around the Gulf of Tonkin until June 2, 1972, when she moored in the Philippines.

The 2020 Blue Ridge patrol changed with the outbreak of COVID-19. The ship and crew have spent 65 consecutive days underway, and counting, an unusual length of time for a ship well-known for its frequent port visits.

“These times are uniquely challenging for the entire world, but it takes an extremely dedicated crew to maintain this old of a ship at sea for this long,” Blue Ridge commander, Capt. Craig Sicola, commander of the Blue Ridge, said in the statement.

The Blue Ridge has been conducting operations in the Philippine Sea for much of this month, again with no return date scheduled whatsoever.

via ZeroHedge News https://ift.tt/2TB2cAF Tyler Durden

As Americans emerge from their homes and try to return to some semblance of normal life, we have a small window of time to remove regulations that are nuisances in the best of times and deeply damaging in the worst.

We can start with child care. As parents begin to return to work, their old day care options are disappearing. The Washington Postreports that “one-third to half of child-care centers may not reopen at all.” It adds that even the surviving centers may operate at limited capacity for a time.

Those restrictions on supply will surely raise the cost of child care, exacerbating trends that were already underway before the COVID-19 pandemic. As of 2018, a study from the Economic Policy Institute put the average cost of day care in D.C. at $24,243 per infant each year. Despite those already staggering numbers, the nation’s capital decided to require college degrees for day care workers, increasing costs further. Those considering more informal arrangements had to tread carefully: D.C. has been known to crack down on large, semi-formal playdate groups.

Day care regulations don’t always make sense. It’s crucial to keep kids safe, of course, but some jurisdictions impose rules that have little or no rational connection to safety. Wisconsin, for example, imposes more than 400 requirements on licensed family child care providers, some of them as trivial as ensuring children not use “trampolines and inflatable bounce surfaces.” Oklahoma’s mandates specify the number of puppets that must be available per child. Is it any wonder that the number of small family child care providers declined by 35 percent from 2011 to 2017? Such vague and strange regulations hardly make the trade enticing, especially when child care providers already earn so little.

Senseless regulations can reach even further into home-based businesses, preventing people from working from home even when doing so has no impact on the neighborhood. The most absurd case might be the Georgia blogger who was shut down for uploading YouTube videos from his house, but there are plenty of other examples. Many localities prevent salons from operating out of their homes, while many state licensing laws prevent cosmetologists from practicing in the client’s home (or almost anywhere outside of a salon). This may have made sense during the coronavirus lockdowns, but as businesses reopen it makes no sense to maintain such rules. Indeed, allowing more people to work from home will give businesses and workers more flexibility during the reopening—and will be valuable for the many people who continue to socially distance themselves for health reasons.

Regulations also make it harder to help the homeless and needy. Several years ago, Arizona’s cosmetology board cracked down on a cosmetology student for cutting hair for the homeless without a license, until Gov. Doug Ducey stepped in to protect him. Even food donations to the homeless have been banned in some places; at other times, food provided by volunteers has been destroyed. Meanwhile, food banks across the nation are struggling.

One bright spot is MUST Ministries, a charity in Georgia that provides lunch for children during summer breaks. In summer 2018 alone, MUST fed over 250,000 hungry children. Despite this wonderful work, in 2019 health officials forced them to overhaul their procedures because it was being done in homes and churches instead of certified kitchens. MUST adjusted as well as it could, and earlier this year it partnered with the Cobb County School District to feed students in need. The original crackdown was needless, but when Georgia came asking for help in the early days of the pandemic, MUST stepped up.

The pandemic has exposed many of America’s destructive barriers to work. At a time when tens of millions of Americans are newly unemployed or otherwise struggling, regulatory reform is vital.

from Latest – Reason.com https://ift.tt/2LYkAPy

via IFTTT

As Americans emerge from their homes and try to return to some semblance of normal life, we have a small window of time to remove regulations that are nuisances in the best of times and deeply damaging in the worst.

We can start with child care. As parents begin to return to work, their old day care options are disappearing. The Washington Postreports that “one-third to half of child-care centers may not reopen at all.” It adds that even the surviving centers may operate at limited capacity for a time.

Those restrictions on supply will surely raise the cost of child care, exacerbating trends that were already underway before the COVID-19 pandemic. As of 2018, a study from the Economic Policy Institute put the average cost of day care in D.C. at $24,243 per infant each year. Despite those already staggering numbers, the nation’s capital decided to require college degrees for day care workers, increasing costs further. Those considering more informal arrangements had to tread carefully: D.C. has been known to crack down on large, semi-formal playdate groups.

Day care regulations don’t always make sense. It’s crucial to keep kids safe, of course, but some jurisdictions impose rules that have little or no rational connection to safety. Wisconsin, for example, imposes more than 400 requirements on licensed family child care providers, some of them as trivial as ensuring children not use “trampolines and inflatable bounce surfaces.” Oklahoma’s mandates specify the number of puppets that must be available per child. Is it any wonder that the number of small family child care providers declined by 35 percent from 2011 to 2017? Such vague and strange regulations hardly make the trade enticing, especially when child care providers already earn so little.

Senseless regulations can reach even further into home-based businesses, preventing people from working from home even when doing so has no impact on the neighborhood. The most absurd case might be the Georgia blogger who was shut down for uploading YouTube videos from his house, but there are plenty of other examples. Many localities prevent salons from operating out of their homes, while many state licensing laws prevent cosmetologists from practicing in the client’s home (or almost anywhere outside of a salon). This may have made sense during the coronavirus lockdowns, but as businesses reopen it makes no sense to maintain such rules. Indeed, allowing more people to work from home will give businesses and workers more flexibility during the reopening—and will be valuable for the many people who continue to socially distance themselves for health reasons.

Regulations also make it harder to help the homeless and needy. Several years ago, Arizona’s cosmetology board cracked down on a cosmetology student for cutting hair for the homeless without a license, until Gov. Doug Ducey stepped in to protect him. Even food donations to the homeless have been banned in some places; at other times, food provided by volunteers has been destroyed. Meanwhile, food banks across the nation are struggling.

One bright spot is MUST Ministries, a charity in Georgia that provides lunch for children during summer breaks. In summer 2018 alone, MUST fed over 250,000 hungry children. Despite this wonderful work, in 2019 health officials forced them to overhaul their procedures because it was being done in homes and churches instead of certified kitchens. MUST adjusted as well as it could, and earlier this year it partnered with the Cobb County School District to feed students in need. The original crackdown was needless, but when Georgia came asking for help in the early days of the pandemic, MUST stepped up.

The pandemic has exposed many of America’s destructive barriers to work. At a time when tens of millions of Americans are newly unemployed or otherwise struggling, regulatory reform is vital.

from Latest – Reason.com https://ift.tt/2LYkAPy

via IFTTT

Why would an alleged GRU officer – supposedly part of an operation to deflect Russian culpability – suggest that Assange “may be connected with Russians?”

In December, I reported on digital forensics evidence relating to Guccifer 2.0 and highlighted several key points about the mysterious persona that Special Counsel Robert Mueller claims was a front for Russian intelligence to leak Democratic Party emails to WikiLeaks:

A considerable volume of evidence pointed at Guccifer 2.0’s activities being in American timezones (twice as many types of indicators were found pointing at Guccifer 2.0’s activities being in American timezones than anywhere else).

A couple of pieces of evidence with Russian indicators present had accompanying locale indicators that contradicted this which suggested the devices used hadn’t been properly set up for use in Russia (or Romania) but may have been suitable for other countries (including America).

On the same day that Guccifer 2.0 was plastering Russian breadcrumbs on documents through a deliberate process, choosing to use Russian-themed end-points and fabricating evidence to claim credit for hacking the DNC, the operation attributed itself to WikiLeaks.

This article questions what Guccifer 2.0’s intentions were in relation to WikiLeaks in the context of what has been discovered by independent researchers during the past three years.

Timing

On June 12, 2016, in an interview with ITV’s Robert Peston, Julian Assange confirmed that WikiLeaks had emails relating to Hillary Clinton that the organization intended to publish. This announcement was prior to any reported contact with Guccifer 2.0 (or with DCLeaks).

On June 14, 2016, an article was published in The Washington Post citing statements from two CrowdStrike executives alleging that Russian intelligence hacked the DNC and stole opposition research on Trump. It was apparent that the statements had been made in the 48 hours prior to publication as they referenced claims of kicking hackers off the DNC network on the weekend just passed (June 11-12, 2016).

On that same date, June 14, DCLeaks contacted WikiLeaks via Twitter DM and for some reason suggested that both parties coordinate their releases of leaks. (It doesn’t appear that WikiLeaks responded until September 2016).

[CrowdStrike President Shawn Henry testified under oath behind closed doors on Dec. 5, 2017 to the U.S. House intelligence committee that his company had no evidence that Russian actors removed anything from the DNC servers. This testimony was only released earlier this month.]

By stating that WikiLeaks would “publish them soon” the Guccifer 2.0 operation implied that it had received confirmation of intent to publish.

However, the earliest recorded communication between Guccifer 2.0 and WikiLeaks didn’t occur until a week later (June 22, 2016) when WikiLeaks reached out to Guccifer 2.0 and suggested that the persona send any new material to them rather than doing what it was doing:

[Excerpt from Special Counsel Mueller’s report. Note: “stolen from the DNC” is an editorial insert by the special counsel.]

If WikiLeaks had already received material and confirmed intent to publish prior to this direct message, why would they then suggest what they did when they did? WikiLeaks says it had no prior contact with Guccifer 2.0 despite what Guccifer 2.0 had claimed.

Here is the full conversation on that date (according to the application):

@WikiLeaks: Do you have secure communications?

@WikiLeaks: Send any new material here for us to review and it will have a much higher impact than what you are doing. No other media will release the full material.

@GUCCIFER_2: what can u suggest for a secure connection? Soft, keys, etc? I’m ready to cooperate with you, but I need to know what’s in your archive 80gb? Are there only HRC emails? Or some other docs? Are there any DNC docs? If it’s not secret when you are going to release it?

@WikiLeaks: You can send us a message in a .txt file here [link redacted]

@GUCCIFER_2: do you have GPG?

Why would Guccifer 2.0 need to know what material WikiLeaks already had? Certainly, if it were anything Guccifer 2.0 had sent (or the GRU had sent) he wouldn’t have had reason to inquire.

The more complete DM details provided here also suggest that both parties had not yet established secure communications.

Further communications were reported to have taken place on June 24, 2016:

@GUCCIFER_2: How can we chat? Do u have jabber or something like that?

@WikiLeaks: Yes, we have everything. We’ve been busy celebrating Brexit. You can also email an encrypted message to office@wikileaks.org. They key is here.

and June 27, 2016:

@GUCCIFER_2: Hi, i’ve just sent you an email with a text message encrypted and an open key.

@WikiLeaks: Thanks.

@GUCCIFER_2: waiting for ur response. I send u some interesting piece.

Guccifer 2.0 said he needed to know what was in the 88GB ‘insurance’ archive that WikiLeaks had posted on June 16, 2016 and it’s clear that, at this stage, secure communications had not been established between both parties (which would seem to rule out the possibility of encrypted communications prior to June 15, 2016, making Guccifer 2.0’s initial claims about WikiLeaks even more doubtful).

There was no evidence of WikiLeaks mentioning this to Guccifer 2.0 nor any reason for why WikiLeaks couldn’t just send a DM to DCLeaks themselves if they had wanted to.

(It should also be noted that this Twitter DM activity between DCLeaks and Guccifer 2.0 is alleged by Mueller to be communications between officers within the same unit of the GRU, who, for some unknown reason, decided to use Twitter DMs to relay such information rather than just communicate face to face or securely via their own local network.)

Guccifer 2.0 lied about DCLeaks being a sub-project of WikiLeaks and then, over two months later, was seen trying to encourage DCLeaks to communicate with WikiLeaks by relaying an alleged request from WikiLeaks that there is no record of WikiLeaks ever making (and which WikiLeaks could have done themselves, directly, if they had wanted to).

@GUCCIFER_2: hi there, check up r email, waiting for reply.

This was followed up on July 6, 2016 with the following conversation:

@GUCCIFER_2: have you received my parcel?

@WikiLeaks: Not unless it was very recent. [we haven’ t checked in 24h].

@GUCCIFER_2: I sent it yesterday, an archive of about 1 gb. via [website link]. and check your email.

@WikiLeaks: Wil[l] check, thanks.

@GUCCIFER_2: let me know the results.

@WikiLeaks: Please don’t make anything you send to us public. It’s a lot of work to go through it and the impact is severely reduced if we are not the first to publish.

@GUCCIFER_2: agreed. How much time will it take?

@WikiLeaks: likely sometime today.

@GUCCIFER_2: will u announce a publication? and what about 3 docs sent u earlier?

@WikiLeaks: I don’t believe we received them. Nothing on ‘Brexit’ for example.

@GUCCIFER_2: wow. have you checked ur mail?

@WikiLeaks: At least not as of 4 days ago . . . . For security reasons mail cannot be checked for some hours.

@GUCCIFER_2: fuck, sent 4 docs on brexit on jun 29, an archive in gpg ur submission form is too fucking slow, spent the whole day uploading 1 gb.

@WikiLeaks: We can arrange servers 100x as fast. The speed restrictions are to anonymise the path. Just ask for custom fast upload point in an email.

@GUCCIFER_2: will u be able to check ur email?

@WikiLeaks: We’re best with very large data sets. e.g. 200gb. these prove themselves since they’re too big to fake.

@GUCCIFER_2: or shall I send brexit docs via submission once again?

@WikiLeaks: to be safe, send via [web link]

@GUCCIFER_2: can u confirm u received dnc emails?

@WikiLeaks: for security reasons we can’ t confirm what we’ve received here. e.g., in case your account has been taken over by us intelligence and is probing to see what we have.

@GUCCIFER_2: then send me an encrypted email.

@WikiLeaks: we can do that. but the security people are in another time zone so it will need to wait some hours.

@WikiLeaks: what do you think about the FBl’ s failure to charge? To our mind the clinton foundation investigation has always been the more serious. we would be very interested in all the emails/docs from there. She set up quite a lot of front companies. e.g in sweden.

@GUCCIFER_2: ok, i’ll be waiting for confirmation. as for investigation, they have everything settled, or else I don’t know how to explain that they found a hundred classified docs but fail to charge her.

@WikiLeaks: She’s too powerful to charge at least without something stronger. s far as we know, the investigation into the clinton foundation remains open e hear the FBI are unhappy with Loretta Lynch over meeting Bill, because he’s a target in that investigation.

@GUCCIFER_2: do you have any info about marcel lazar? There’ve been a lot of rumors of late.

@WikiLeaks: the death? [A] fake story.

@WikiLeaks: His 2013 screen shots of Max Blumenthal’s inbox prove that Hillary secretly deleted at least one email about Libya that was meant to be handed over to Congress. So we were very interested in his co-operation with the FBI.

@GUCCIFER_2: some dirty games behind the scenes believe Can you send me an email now?

@WikiLeaks: No; we have not been able to activate the people who handle it. Still trying.

@GUCCIFER_2: what about tor submission? [W]ill u receive a doc now?

@WikiLeaks: We will get everything sent on [weblink].” [A]s long as you see \”upload succseful\” at the end. [I]f you have anything hillary related we want it in the next tweo [sic] days prefable [sic] because the DNC is approaching and she will solidify bernie supporters behind her after.

@GUCCIFER_2: ok. I see.

@WikiLeaks: [W]e think the public interest is greatest now and in early october.

@GUCCIFER_2: do u think a lot of people will attend bernie fans rally in philly? Will it affect the dnc anyhow?

@WikiLeaks: bernie is trying to make his own faction leading up to the DNC. [S]o he can push for concessions (positions/policies) or, at the outside, if hillary has a stroke, is arrested etc, he can take over the nomination. [T]he question is this: can bemies supporters+staff keep their coherency until then (and after). [O]r will they dis[s]olve into hillary’ s camp? [P]resently many of them are looking to damage hilary [sic] inorder [sic] to increase their unity and bargaining power at the DNC. Doubt one rally is going to be that significant in the bigger scheme. [I]t seems many of them will vote for hillary just to prevent trump from winning.

@GUCCIFER_2: sent brexit docs successfully.

@WikiLeaks: :))).

@WikiLeaks: we think trump has only about a 25% chance of winning against hillary so conflict between bernie and hillary is interesting.

@GUCCIFER_2: so it is.

@WikiLeaks: also, it’ s important to consider what type of president hillary might be. If bernie and trump retain their groups past 2016 in significant number, then they are a restraining force on hillary.

[Note: This was over a week after the Brexit referendum had taken place, so this will not have had any impact on the results of that. It also doesn’t appear that WikiLeaks released any Brexit content around this time.]

On July 14, 2016, Guccifer 2.0 sent an email to WikiLeaks, this was covered in the Mueller report:

It should be noted that while the attachment sent was encrypted, the email wasn’t and both the email contents and name of the file were readable.

The persona then opted, once again, for insecure communications via Twitter DMs:

@GUCCIFER_2: ping. Check ur email. sent u a link to a big archive and a pass.

@WikiLeaks: great, thanks; can’t check until tomorrow though.

On July 17, 2016, the persona contacted WikiLeaks again:

@GUCCIFER_2: what bout now?

On July 18, 2016, WikiLeaks responded and more was discussed:

@WikiLeaks: have the 1 Gb or so archive.

@GUCCIFER_2: have u managed to extract the files?

@WikiLeaks: yes. turkey coup has delayed us a couple of days. [O]therwise all ready[.]

@GUCCIFER_2: so when r u about to make a release?

@WikiLeaks: this week. [D]o you have any bigger datasets? [D]id you get our fast transfer details?

@GUCCIFER_2: i’ll check it. did u send it via email?

@WikiLeaks: yes.

@GUCCIFER_2: to [web link]. [I] got nothing.

@WikiLeaks: check your other mail? this was over a week ago.

@GUCCIFER_2:oh, that one, yeah, [I] got it.

@WikiLeaks: great. [D]id it work?

@GUCCIFER_2:[I] haven’ t tried yet.

@WikiLeaks: Oh. We arranged that server just for that purpose. Nothing bigger?

@GUCCIFER_2: let’s move step by step, u have released nothing of what [I] sent u yet.

@WikiLeaks: How about you transfer it all to us encrypted. [T]hen when you are happy, you give us the decrypt key. [T]his way we can move much faster. (A]lso it is protective for you if we already have everything because then there is no point in trying to shut you up.

@GUCCIFER_2: ok, i’ll ponder it

Again, we see a reference to the file being approximately one gigabyte in size.

Guccifer 2.0’s “so when r u about to make a release?” seems to be a question about his files. However, it could have been inferred as generally relating to what WikiLeaks had or even material relating to the “Turkey Coup” that WikiLeaks had mentioned in the previous sentence and that were published by the following day (July 19, 2016).

The way this is reported in the Mueller report, though, prevented this potential ambiguity being known (by not citing the exact question that Guccifer 2.0 had asked and the context immediately preceding it).

Four days later, WikiLeaks published the DNC emails.

Later that same day, Guccifer 2.0 tweeted: “@wikileaks published #DNCHack docs I’d given them!!!”.

Guccifer 2.0 chose to use insecure communications to ask WikiLeaks to confirm receipt of “DNC emails” on July 6, 2016. Confirmation of this was not provided at that time but WikiLeaks did confirm receipt of a “1gb or so” archive on July 18, 2016.

Guccifer 2.0’s emails to WikiLeaks were also sent insecurely.

We cannot be certain that WikiLeaks statement about making a release was in relation to Guccifer 2.0’s material and there is even a possibility that this could have been in reference to the Erdogan leaks published by WikiLeaks on July 19, 2016.

Ulterior Motives?

While the above seems troubling there are a few points worth considering:

Guccifer 2.0’s initial claim about sending WikiLeaks material(and that they would publish it soon) appears to have been made without justification and seems to be contradicted by subsequent communications from WikiLeaks.

If the archive was “about 1GB” (as Guccifer 2.0 describes it) then it would be too small to have been all of the DNC’s emails (as these, compressed, came to 1.8GB-2GB depending on compression method used, which, regardless, would be “about 2GB” not “about 1GB”). If we assume that these were DNC emails, where did the rest of them come from?

Assange has maintained that WikiLeaks didn’t publish the material that Guccifer 2.0 had sent to them. Of course, Assange could just be lying about that but there are some other possibilities to consider. If true, there is always a possibility that Guccifer 2.0 could have sent them material they had already received from another source or other emails from the DNC that they didn’t release (Guccifer 2.0 had access to a lot of content relating to the DNC and Democratic party and the persona also offered emails of Democratic staffers to Emma Best, a self-described journalist, activist and ex-hacker, the month after WikiLeaks published the DNC emails, which, logically, must have been different emails to still have any value at that point in time).

On July 6, 2016, the same day that Guccifer 2.0 was trying to get WikiLeaks to confirm receipt of DNC emails (and on which Guccifer 2.0 agreed not to publish material he had sent them), the persona posted a series of files to his blog that were exclusively DNC email attachments.

It doesn’t appear any further communications were reported between the parties following the July 18, 2016 communications despite Guccifer 2.0 tweeting on August 12, 2016: “I’ll send the major trove of the #DCCC materials and emails to #wikileaks keep following…” and, apparently, stating this to The Hill too.

As there are no further communications reported beyond this point it’s fair to question whether getting confirmation of receipt of the archive was the primary objective for Guccifer 2.0 here.

Even though WikiLeaks offered Guccifer 2.0 a fast server for large uploads, the persona later suggested he needed to find a resource for publishing a large amount of data.

Despite later claiming he would send (or had sent) DCCC content to WikiLeaks,WikiLeaks never published such content and there doesn’t appear to be any record of any attempt to send this material to WikiLeaks.

Considering all of this and the fact Guccifer 2.0 effectively covered itself in “Made In Russia” labels (by plastering files in Russian metadata and choosing to use a Russian VPN service and a proxy in Moscow for it’s activities) on the same day it first attributed itself to WikiLeaks, it’s fair to suspect that Guccifer 2.0 had malicious intent towards WikiLeaks from the outset.

If this was the case, Guccifer 2.0 may have known about the DNC emails by June 30, 2016 as this is when the persona first started publishing attachments from those emails.

In an interview with Nieuwsuur that was posted the same day, Julian Assange explained that the reward was for a DNC staffer who he said had been “shot in the back, murdered”. When the interviewer suggested it was a robbery Assange disputed it and stated that there were no findings.

When the interviewer asked if Seth Rich was a source, Assange stated, “We don’t comment on who our sources are”.

When pressed to explain WikiLeaks actions, Assange stated that the reward was being offered because WikiLeaks‘ sources were concerned by the incident. He also stated that WikiLeaks were investigating.

Speculation and theories about Seth Rich being a source for WikiLeaks soon propagated to several sites and across social media.

On that same day, in a DM conversation with the actress Robbin Young, Guccifer 2.0 claimed that Seth was his source (despite previously claiming he obtained his material by hacking the DNC).

Why did Guccifer 2.0 feel the need to attribute itself to Seth at this time?

[Note: I am not advocating for any theory and am simply reporting on Guccifer 2.0’s effort to attribute itself to Seth Rich following the propagation of Rich-WikiLeaks association theories online.]

Special Counsel Claims

In Spring, 2019, Special Counsel Robert Mueller, who was named to investigate Russian interference in the 2016 U.S. general election, delivered his final report.

It claimed:

Guccifer 2.0 contradicted his own hacking claims to allege that Seth Rich was his source and did so on the same day that Julian Assange was due to be interviewed by Fox News (in relation to Seth Rich).

No communications between Guccifer 2.0 and Seth Rich have ever been reported.

Suggesting Assange Connected To Russians

In the same conversation Guccifer 2.0 had with Robbin Young where Rich’s name is mentioned (on August 25, 2016), the persona also provided a very interesting response to Young mentioning “Julian” (in reference to Julian Assange):

The alleged GRU officer we are told was part of an operation to deflect from Russian culpability suggested that Assange “may be connected with Russians”.

Guccifer 2.0’s Mentions of WikiLeaks and Assange

Guccifer 2.0 mentioned WikiLeaks or associated himself with their output on several occasions:

July 22nd, 2016: claimed credit when WikiLeaks published the DNC leaks.

August 12, 2016: It was reported in The Hill that Guccifer 2.0 had released material to the publication. They reported: “The documents released to The Hill are only the first section of a much larger cache. The bulk, the hacker said, will be released on WikiLeaks.”

August 12, 2016: Tweeted that he would “send the major trove of the #DCCC materials and emails to #wikileaks“.

September 15, 2016: telling DCLeaks that WikiLeaks wanted to get in contact with them.

October 4, 2016: Congratulating WikiLeaks on their 10th anniversary via its blog. Also states: “Julian, you are really cool! Stay safe and sound!”. (This was the same day on which Guccifer 2.0 published his “Clinton Foundation” files that were clearly not from the Clinton Foundation.)

October 17, 2016: via Twitter, stating “i’m here and ready for new releases. already changed my location thanks @wikileaks for a good job!”

Guccifer 2.0 also made some statements in response to WikiLeaks or Assange being mentioned:

June 17, 2016: in response to The Smoking Gun asking if Assange would publish the same material it was publishing, Guccifer 2.0 stated: “I gave WikiLeaks the greater part of the files, but saved some for myself,”

August 22, 2016: in response to Raphael Satter suggesting that Guccifer 2.0 send leaks to WikiLeaks,the persona stated: “I gave wikileaks a greater part of docs”.

August 25, 2016: in response to Julian Assange’s name being mentioned in a conversation with Robbin Young, Guccifer 2.0 stated: “he may be connected with Russians”.

October 18, 2016: a BBC reported asked Guccifer 2.0 if he was upset that WikiLeaks had “stole his thunder” and “do you still support Assange?”. Guccifer 2.0 responded: “i’m glad, together we’ll make America great again.”.

Guccifer 2.0 fabricated evidence to claim credit for hacking the DNC, covered itself (and its files) in what were essentially a collection of “Made In Russia” labels through deliberate processes and decisions made by the persona, and, then, it attributed itself to WikiLeaks with a claim that was contradicted by subsequent communications between both parties.

Guccifer 2.0 then went on to lie about WikiLeaks, contradicted its own hacking claims to attribute itself to Seth Rich and even alleged that Julian Assange “may be connected with Russians”.

While we are expected to accept that Guccifer 2.0’s efforts between July 6 and July 18 were a sincere effort to get leaks to WikiLeaks, considering everything we now know about the persona, it seems fair to question whether Guccifer 2.0’s intentions towards WikiLeaks may have instead been malicious.

via ZeroHedge News https://ift.tt/2zorgnu Tyler Durden

Global Tourism To Suffer Crushing Blow In 2020 Tyler Durden

Sun, 05/24/2020 – 07:35

While few industries have been spared by the impact of the COVID-19 pandemic, even fewer have been hit harder than the tourism sector. And while it is impossible to gauge the full extent of disruption brought on by COVID-19, Statista’s Feliz Richter notes that the World Tourism Organization (UNWTO) published estimates on how the pandemic will affect international tourist arrivals in 2020 under three different scenarios.

Unfortunately, the pandemic’s impact on the tourism industry is expected to be devastating, even under the most optimistic of the three scenarios.

Assuming the opening of borders and the gradual lifting of travel restrictions begins in early July, the UNWTO expects international tourist arrivals to drop by 58 percent to 610 million this year. That would set the global travel industry back to 1998, when the number of international travelers was last so low.

It could get worse, however, if travel restrictions remain in place until later in the year.

Assuming they are eased as late as December, the UNWTO sees international tourist arrivals fall as low as 320 million, a level last seen in the mid-80s and possibly costing the industry $1+ trillion.

Prior to the coronavirus outbreak, the global tourism industry had seen almost uninterrupted growth for decades. Since 1980, the number of international arrivals skyrocketed from 277 million to nearly 1.5 billion in 2019.

As our chart shows, tourist numbers only dipped twice in the past two decades: in 2003, when the SARS outbreak led to a 0.4 percent drop in arrivals, and in 2009, when the global financial crisis caused a 4 percent drop in international travel.

via ZeroHedge News https://ift.tt/3ebVbOA Tyler Durden

{kind=link}