Donald Trump took Joe Biden behind the proverbial bleachers this weekend and gave him a twitter beating the likes of which shant be soon forgotten.

In case you missed it, Trump tweeted on Sunday that “African Americans” would not be able to vote for “anyone associated with the 1994 crime bill” which Biden authored (and bragged about as recently as 2007) – largely blamed for contributing to the mass incarceration of black Americans for low-level drug crimes during the USA’s infamously failed war on drugs.

Anyone associated with the 1994 Crime Bill will not have a chance of being elected. In particular, African Americans will not be able to vote for you. I, on the other hand, was responsible for Criminal Justice Reform, which had tremendous support, & helped fix the bad 1994 Bill!

….Super Predator was the term associated with the 1994 Crime Bill that Sleepy Joe Biden was so heavily involved in passing. That was a dark period in American History, but has Sleepy Joe apologized? No!

Biden furiously shook his cane, as his campaign copped some serious holier-than-thou faux shock that Trump would talk shit “on foreign soil, on Memorial Day, and to side repeatedly with a murderous dictator against a fellow American and former Vice President,” referring to Trump’s downplay of North Korea’s short-range rocket test, and subsequent tweet calling Biden “a low IQ individual” and “swampman.”

North Korea fired off some small weapons, which disturbed some of my people, and others, but not me. I have confidence that Chairman Kim will keep his promise to me, & also smiled when he called Swampman Joe Biden a low IQ individual, & worse. Perhaps that’s sending me a signal?

The Trump campaign had none of Biden’s jibber-jabber, as 2020 campaign communications director Tim Murtaugh shot back in a statement “That’s rich coming from Joe Biden, who bashed President Trump while standing on foreign soil earlier this year in Germany.”

That’s rich coming from Joe Biden, who bashed President Trump while standing on foreign soil earlier this year in Germany.

In February, Biden slammed the Trump administration’s foreign policy and immigration stance while speaking during the Munich Security Conference.

“From the Iraq war to the Russia reset, Joe Biden has been wrong on virtually every foreign policy call in the last four decades,” said Murtaugh. “Just ask former Obama Defense Secretary Robert Gates.”

via ZeroHedge News http://bit.ly/2KiJPwL Tyler Durden

Paul Rosenzweig leads off with This Week in China Tech Fear – an enduring and fecund feature in Washington these days. We cover the Trump Administration’s plan to blacklist up to five Chinese surveillance companies, including Hikvision, for contributing to Uighur human rights violations in the West of China, DHS’s rather bland warning that commercial Chinese drones pose a data risk for US users, and the difficulty US chipmakers are facing in getting “deemed export” licenses for Chinese nationals.

We delve deeper into a remarkably shallow and agenda-driven New York Times article by Nicole Perlroth and Scott Shane that blames NSA for Baltimore’s ransomware problem without ever asking why the city failed for two years to patch its systems. David Kris uses the story to take us into the Vulnerabilities Equities Process – and its flaws.

There may be a lot – or nothing – to the Navy email “spyware” story, but David points out just how many of today’s cyber issues it touches. With the added fillip of a “Go Air Force, Beat Navy” theme not usually sounded in cybersecurity stories.

Paul expands on what I have called Cheapfakes (as opposed to Deep Fakes) – the Pelosi video manipulated to make her sound impaired. And he manages to find something approaching good news in the advance of faked video – it may mean the end of (video) blackmail.

But not the end of “revenge porn” and revenge porn laws. I ask Gus Hurwitz whether those laws are actually protected by the Constitution, and the answer turns out to be highly qualified. But, surprisingly, media lawyers aren’t objecting that revenge porn laws criminalizing the dissemination of true facts are on a slippery slope to criminalizing news media. Only a bit more persuasively, though, that is the argument they’re making about the expanded charges of espionage against Wikileaks founder Julian Assange. David offers his view of the pros and cons of the indictment.

And Gus closes us out with some almost unalloyed good news. Despite my suspicion of any bipartisan bill in the current climate, he insists that the Senate-passed anti-robocalling bill is a straight victory for the Forces of Good. But, he warns, the House could still screw things up by adding a private right of action along the lines of the Telephone Consumer Protection Act, which has provided the plaintiffs bar with an endless supply of class actions without actually benefiting consumers.

As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of the firm.

from Latest – Reason.com http://bit.ly/2EFhkWl

via IFTTT

All across America, U.S. farmland is being gobbled up by foreign interests. So when we refer to “the heartland of America”, the truth is that vast stretches of that “heartland” is now owned by foreigners, and most Americans have no idea that this is happening. These days, a lot of people are warning about the “globalization” of the world economy, but in reality our own soil is rapidly being “globalized”. When farms are locally owned, the revenue that those farms take in tends to stay in local communities. But with foreign-owned farms there is no guarantee that will happen. And while there is plenty of food to go around this is not a major concern, but what happens when a food crisis erupts and these foreign-owned farms just keep sending their produce out of the country? There are some very serious national security concerns here, and they really aren’t being addressed. Instead, the amount of farmland owned by foreigners just continues to increase with each passing year.

Prior to seeing the headline to this article, how much U.S. farmland would you have guessed that foreigners now own?

Personally, I had no idea that foreigners now own nearly 30 million acres. The following comes from NPR…

American soil.

Those are two words that are commonly used to stir up patriotic feelings. They are also words that can’t be be taken for granted, because today nearly 30 million acres of U.S. farmland are held by foreign investors. That number has doubled in the past two decades, which is raising alarm bells in farming communities.

How did we allow this to happen?

And actually laws regarding land ownership vary greatly from state to state. Some states have placed strict restrictions on foreign land ownership, while in other states it is “a free-for-all”…

“Texas is kind of a free-for-all, so they don’t have a limit on how much land can be owned,” say’s Ohio Farm Bureau’s Ty Higgins, “You look at Iowa and they restrict it — no land in Iowa is owned by a foreign entity.”

Ohio, like Texas, also has no restrictions, and nearly half a million acres of prime farmland are held by foreign-owned entities. In the northwestern corner of the state, below Toledo, companies from the Netherlands alone have purchased 64,000 acres for wind farms.

But even in states where there are restrictions, foreign entities can get around that by simply buying large corporations that own land.

For example, when the Chinese purchased Smithfield Foods in 2013 they instantly gained control over 146,000 acres of prime farmland. The following comes from Wikipedia…

Smithfield Foods, Inc., is a meat-processing company based in Smithfield, Virginia, in the United States, and a wholly owned subsidiary of WH Group of China. Founded in 1936 as the Smithfield Packing Company by Joseph W. Luter and his son, the company is the largest pig and pork producer in the world.[4] In addition to owning over 500 farms in the US, Smithfield contracts with another 2,000 independent farms around the country to grow Smithfield’s pigs.[5] Outside the US, the company has facilities in Mexico, Poland, Romania, Germany, and the United Kingdom.[6]Globally the company employed 50,200 in 2016 and reported an annual revenue of $14 billion.[2] Its 973,000-square-foot meat-processing plant in Tar Heel, North Carolina, was said in 2000 to be the world’s largest, processing 32,000 pigs a day.[7]

Then known as Shuanghui Group, WH Group purchased Smithfield Foods in 2013 for $4.72 billion, more than its market value.[8][9] It was the largest Chinese acquisition of an American company to date.[10] The acquisition of Smithfield’s 146,000 acres of land made WH Group, headquartered in Luohe, Henanprovince, one of the largest overseas owners of American farmland.[a]

Of course this hasn’t happened by accident.

The communist Chinese government has actually made the purchase of foreign agricultural assets a top national priority in recent years, and this has been reflected in a series of key documents…

The strategy is reflected in encouragements to invest abroad by various documents and articles issued by Chinese leaders. For example, a series of annual “Number one documents” from China’s communist party authorities stating rural policy have contained increasingly specific strategies for investment. A general exhortation to invest in agriculture overseas, issued in 2007, was followed by an initial surge in overseas farming ventures. In 2010, authorities called for supportive policies to encourage investment abroad.

The 2014 document included a more specific mandate to create large grain-trading conglomerates, designed to give Chinese companies greater control over oilseed and grain imports. That was the same year COFCO acquired Nidera and Noble Agri, making COFCO one of the largest trading companies in the world based on value of assets. The 2015 document specifically called for policies to support facilities, equipment, and inputs for agricultural production in foreign countries. The 2017 document broadened the encouragement to include all types of agricultural conglomerates. The 2018 document repeated the general endorsement of overseas investment and instructions to create multinational grain-trading and agricultural conglomerates.

In the end, how much Chinese ownership of our farmland would we be comfortable with?

If they owned 20 percent of our farmland, would we be okay with that?

Well, what if that figure surged to 30 or 40 percent?

Would that still be okay?

We need to start asking these sorts of questions, because foreigners are buying up more of our farmland with each passing day, and this is a very real national security threat.

And after this absolutely disastrous year, thousands more U.S. farmers will be forced out of business and it is anticipated that more U.S. farmland will be up for sale than ever before.

I extensively discussed the problems that farmers in the middle of the country are currently having yesterday, and today I would like to share with you a portion of an email that a friend in Missouri just sent me…

I work for a farmer in West-Central Missouri who raises corn, soybeans, and cattle and to say it’s been a challenging Spring would be the understatement of the year!!! We managed to get some corn planted in April but it started to rain and rain and rain and we still have more corn to plant. My boss doesn’t like to plant corn after May 15 and here it is May 27 and we still are not done planting corn. With each late day that passes by the yield goes down so what do you do??? Do we start planting soybeans if or when it dries up even though the price of soybeans is at a record low or do we plant corn that has risen in price but will have a reduced yield??? From April 28 through today (May 27) we have had 10 inches of rain. One day we had 4.5 inches with roads and basements flooded. Last week we had rain 4 out of those 7 days!!! It’s raining again today as I write this!!! We need warm, sunshine, dry, windy days and we get mostly cool, cloudy, rainy days. Next Thursdays low is supposed to be 57!!! If the weather pattern doesn’t change I don’t see how we can ever get the soybeans planted and we have 1,300 acres to plant. There are large farmers in my area that don’t have anything planted.

This truly is a “perfect storm” for U.S. farmers, and many believe that what we have witnessed so far is just the beginning.

Farm bankruptcies are already at the highest level that we have seen since the last recession, and do we really want foreigners gobbling up even more of our farmland from farmers that are incredibly desperate to sell?

Our founders never intended for America to be for sale to the highest bidder, and hopefully more states will start passing laws that will make sure that U.S. farms stay in the hands of U.S. farmers.

via ZeroHedge News http://bit.ly/2XcGNNS Tyler Durden

Paul Rosenzweig leads off with This Week in China Tech Fear – an enduring and fecund feature in Washington these days. We cover the Trump Administration’s plan to blacklist up to five Chinese surveillance companies, including Hikvision, for contributing to Uighur human rights violations in the West of China, DHS’s rather bland warning that commercial Chinese drones pose a data risk for US users, and the difficulty US chipmakers are facing in getting “deemed export” licenses for Chinese nationals.

We delve deeper into a remarkably shallow and agenda-driven New York Times article by Nicole Perlroth and Scott Shane that blames NSA for Baltimore’s ransomware problem without ever asking why the city failed for two years to patch its systems. David Kris uses the story to take us into the Vulnerabilities Equities Process – and its flaws.

There may be a lot – or nothing – to the Navy email “spyware” story, but David points out just how many of today’s cyber issues it touches. With the added fillip of a “Go Air Force, Beat Navy” theme not usually sounded in cybersecurity stories.

Paul expands on what I have called Cheapfakes (as opposed to Deep Fakes) – the Pelosi video manipulated to make her sound impaired. And he manages to find something approaching good news in the advance of faked video – it may mean the end of (video) blackmail.

But not the end of “revenge porn” and revenge porn laws. I ask Gus Hurwitz whether those laws are actually protected by the Constitution, and the answer turns out to be highly qualified. But, surprisingly, media lawyers aren’t objecting that revenge porn laws criminalizing the dissemination of true facts are on a slippery slope to criminalizing news media. Only a bit more persuasively, though, that is the argument they’re making about the expanded charges of espionage against Wikileaks founder Julian Assange. David offers his view of the pros and cons of the indictment.

And Gus closes us out with some almost unalloyed good news. Despite my suspicion of any bipartisan bill in the current climate, he insists that the Senate-passed anti-robocalling bill is a straight victory for the Forces of Good. But, he warns, the House could still screw things up by adding a private right of action along the lines of the Telephone Consumer Protection Act, which has provided the plaintiffs bar with an endless supply of class actions without actually benefiting consumers.

As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of the firm.

from Latest – Reason.com http://bit.ly/2EFhkWl

via IFTTT

With every passing day that the US China trade war is not resolved, it appears that Morgan Stanley’s bearish equity strategist, Michael Wilson, will be Wall Street’s most accurate forecaster for the second year in a row, because unlike various quants from JPMorgan who shall remain unnamed, he did not erroneously assume that trade war will be resolved quickly, and instead of slapping a lazy 3,000 S&P year-end price target, Wilson – despite being mocked by the likes of Bloomberg – remained stubborn in the face of the April market melt up, and said that it is only a matter of time before stocks rerate sharply lower.

So just to remind Morgan Stanley clients that unlike most of his peers who are nothing but lagging indicators, their calls flip-flopping every several weeks depending on which way the S&P moves, Wilson has published a report today in which he makes three rather bold calls:

Trade is not the only risk to growth.

Adjusting the yield curve for QE and QT shows a persistent inversion for the past ~6 months, suggesting recession risk is higher than normal.

volatility is about to rise…a lot.

The first of three should be intuitive to anyone who has been following the market in the past month. As Wilson notes, looking at the most recent disappointing macro data including poor durable good, capital spending and Markit PMIs, “recent data points suggest US earnings and economic risk is greater than most investors may think.”

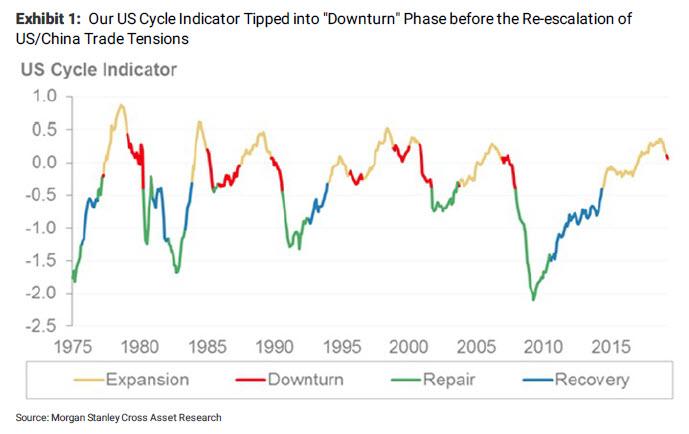

Supporting that claim is the fact that our US Cycle indicator moved into a downturn phase based on the April data which was before the trade talks broke down in early May (Exhibit 1). The OECD leading indicator also fell to its lowest level since the last recession. In addition, we are now hearing from many leading semiconductor (INTC, MCHP) and industrial companies (CAT, DE) that the second half recovery many are counting on is looking less likely. Like the weaker macro data in April, we don’t think these softer outlooks are the result of the uncertainty in the US/China trade negotiations. In the past week, our economists have lowered their 2Q US GDP forecast to 0.6% from 1.0%. We suspect this could deteriorate further if trade negotiations don’t improve soon.

And since all of these reflect April data – which means it weakened before the re-escalation of trade tensions – the latest trade war will only make a dismal economic picture worse. In addition, Wilson claims, “numerous leading companies may be starting to throw in the towel on the second half rebound”, something the Morgan Stanley strategist has repeatedly warned about even though “many investors are not.”

In short, “get ready for more potential growth disappointments even with a trade deal.”

* * *

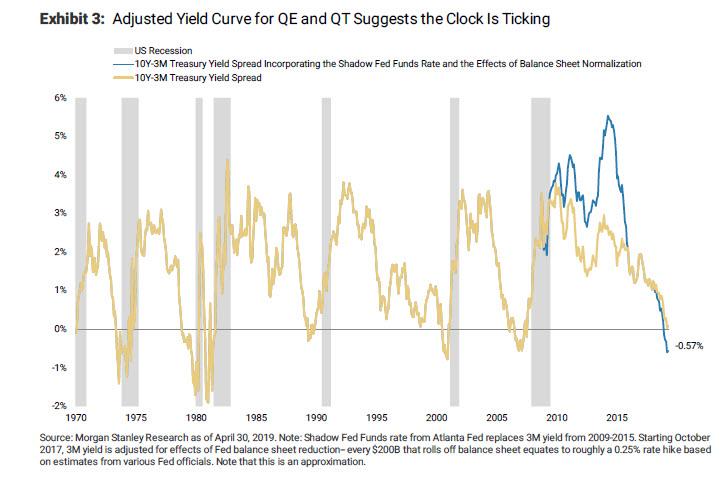

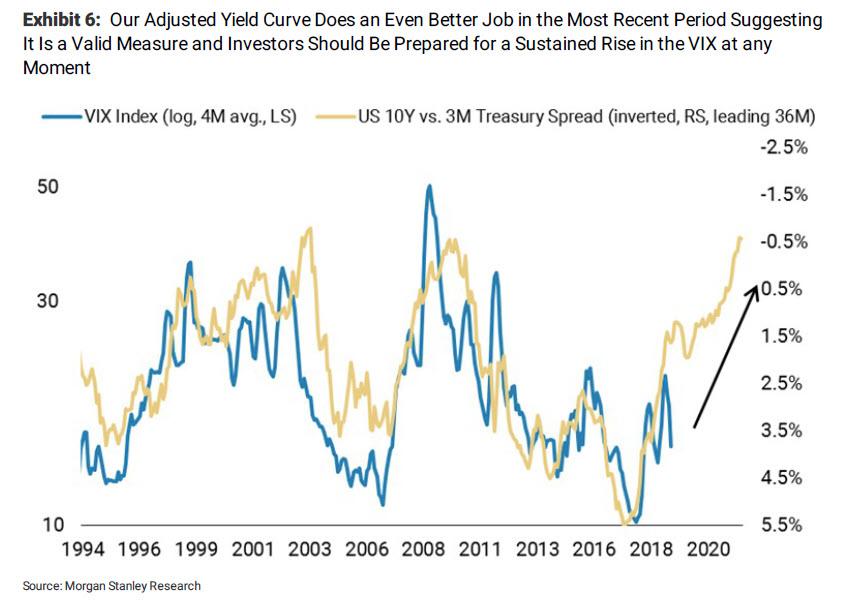

Wilson’s second, and even more important point is that whereas in the past 6 months the yield curve has been flirting with inversion, “adjusting the yield curve for QE and QT shows an inversion began at the end of last year and persisted ever since.” As the strategist notes, when the 10-year vs. 3-month yield curve inverted in March there was a lot of noise about what it meant for markets. However, it didn’t stay inverted very long and the noise dissipated. That’s only half the story, thought, because Morgan Stanley “adjusted the traditional yield curve for QE and QT and the results are interesting.”

A quick note on how said “adjustment” of the yield curve took place: First, to adjust for QE, MS took the Atlanta Fed’s work on the shadow Fed Funds rate. It then took the Fed’s estimate that every $200B of QT is worth an additional rate hike and added it to the Fed Funds rate. The result is shown below, with the darker line showing the impact of QE and QT on the raw Fed Funds rate.

Some observations on the chart above: As Wilson notes, it’s interesting that the adjusted Fed Funds rate touches the lower end of the well defined channel that has contained the Fed Funds rate going back to the early 1980s. Secondly, when adjusting for QT, the adjusted Fed Funds rate breaks the channel to the upside arguing the Fed may have exceeded r* last fall and helping to provide an explanation for the very difficult 4Q for the financial markets. It also explains why the US economy is now slowing more than perhaps many economists and investors expected. Given that monetary policy typically works with a lag of 12-18 months, it’s unlikely that a pause by the Fed will be enough to reverse the impact of the significant tightening that occurred by the Fed over the past few years.

Another observation: earlier today we noted that the nominal 3M-10Y yield curve has inverted the most since 2007, screaming recession.

Well, it gets worse. According to Wilson, when translating the adjusted Fed Funds rate into the yield curve by making the exact same adjustment to the 3 month T-Bill given the historical nearly 100 percent correlation, the result can be seen below.

The light blue line is the unadjusted 10 year – 3 month yield curve and the dark blue line shows what it would look like fully adjusted for QE and QT. The adjusted curve shows record steepness in 2013 as the QE program peaked, which makes sense as it took record monetary support to get the economy going again after the great recession. The amount of flattening thereafter is commensurate with a significant amount of monetary tightening that is perhaps underappreciated by the average investor.

More importantly, unlike the unadjusted curve which only flipped negative in March, the adjusted yield curve inverted last November and has remained in negative territory ever since, surpassing the minimum time required for a valid meaningful economic slowdown signal. It also suggests the “shot clock” started 6 months ago, putting us “in the zone” for a recession watch, according to Wilson. As a result, Morgan Stanley thinks the bond market has it right to suggest the next move for the Fed will be a cut. Incidentally, the equity market is also right, given how defensively it has traded since last summer. Furthermore, the curve inverted about the same time the trade truce happened in late November and has stayed inverted despite all the positive rhetoric earlier this year around a trade deal. This means the US economic slowdown and rising recession risk is happening regardless of the trade outcome

The adjusted yield curve inverted last December rather than in March, and it’s remained well below 0% even since.

It looks like it may be bottoming which is typically the beginning of the end for the economic cycle.

* * *

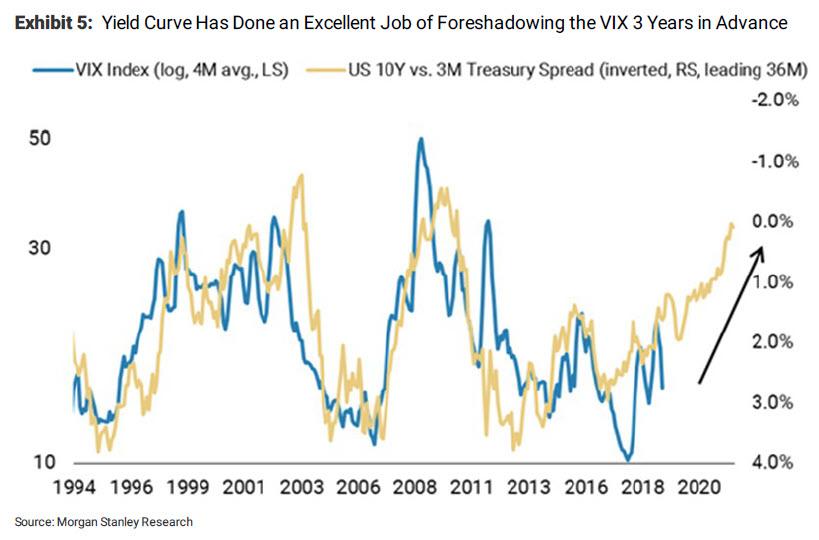

The third, and final point, may be of most significance to traders. Here, Wilson makes the controversial claim that whether or not an economic recession occurs in the US in the near term may not be the most important signal from the yield curve for investors. Why? Because, we are already in what will soon be revealed to be an especially volatile zone.

To be sure, we’ve shown the relationship between the yield curve and the lagged spot VIX on many times in the past, first in 2017. And now, according to Morgan Stanley, it’s time to look at it again (SocGen’s complaints about this correlation notwithstanding), because “the yield curve has done a remarkably good job of forecasting the direction of the VIX 3 years in advance until recently when it appears to have not predicted the severe decline in the VIX a few years ago.”

However, if analysts use the adjusted yield curve as revised above, its predictive power remains very much intact.

To Wilson this means two things:

First, Morgan Stanley’s adjusted yield curve is right (over the objections of the peanut gallery), and

Investors need to get ready for a potentially much higher level of equity volatility in the near term and on a sustained basis.

Incidentally, this is precisely the same conclusion that another Morgan Stanley strategist, Michael Zezas reached over the weekend, when he warned that if the trade war does not end soon, it will cause enough economic erosion to crash markets. Same conclusion, two different ways of getting there.

Wilson’s conclusion also touches on the recently discussed topic of differences and similarities between 2019 and 2018. Specifically, he says that “while last fall’s equity volatility was driven by higher rates, the next bout of equity volatility will be driven by weaker growth and earnings misses from stocks that are not priced for it.“

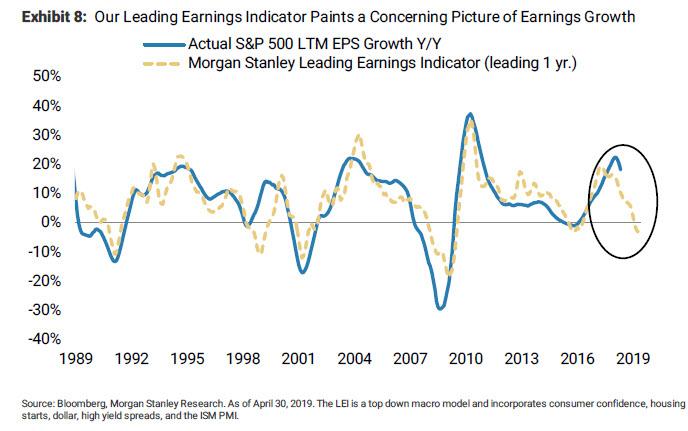

Finally, speaking of disappointing earnings, Wilson writes that contrary to incorrect reports that an earnings contraction was narrowly avoided in Q1, with 95% of S&P 500 companies done reporting we are on track to see 1Q earnings growth come in at -43 bps. And, as a reminder, a key part of Wilson’s call for 2019 is for an earnings recession which is defined as two or more quarters of flat or negative growth. Wilson’s conclusion:

We think 1Q19 will mark the beginning of the earnings recession and think that full year 2019 earnings estimates still need to fall by 5-10 percent. A lot of the growth that is still expected for 2019 is being packed into the fourth quarter and that looks unrealistic to us, with or without a trade deal. We saw companies that did poorly in the first quarter hold on to strong fourth quarter guidance and maintain optimism. We don’t buy this story and our leading earnings indicator (LEI) is still pointing to a significant deceleration in earnings growth over the back half of the year.

In other words, the sequence of events is roughly as follows:

Companies guide down sharply in the coming several weeks ahead of the second half as trade war escalated further

(Adjusted) yield curve turns even more inverted.

VIXplosion

via ZeroHedge News http://bit.ly/2Wxxgnq Tyler Durden

The dawning may have begun, the realization that growth again has been overstated.

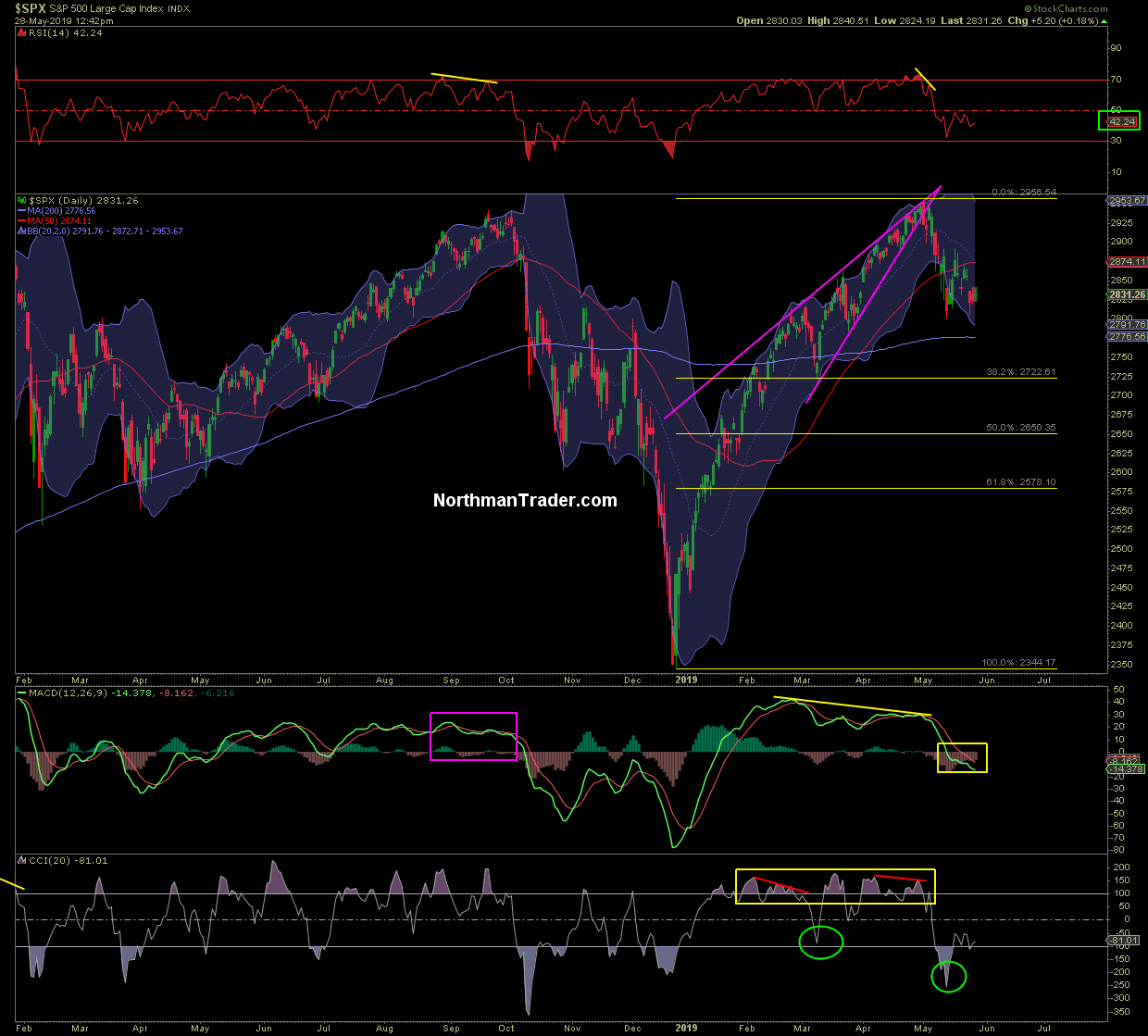

Be it a China deal that’s dragging on with no clear path to resolution, and/or economic data that keeps disappointing. With index charts showing signs of potential topping patterns, yet support holding at the moment, I wanted to briefly follow up on some technical observations I made on CNBC this morning:

While I referenced the equal weight issue, I honed in on current price action being a battle for control, bears need to break 2800, bulls need to get back above 2900, in the meantime we’re stuck in a chop range with buyers and sellers fighting it out.

Let’s look at some specific technical levels and how they may go a long way in helping identify when and where we have a clearer sense about who’s winning the battle for control.

In the interview I mentioned 2640 as potential target should we break 2800 AND 2776.

Why these numbers?

For one $ES is engaged in a potential head and shoulders pattern that targets 2640 precisely:

That level would also coincide with the .5 fib offering confluence support.

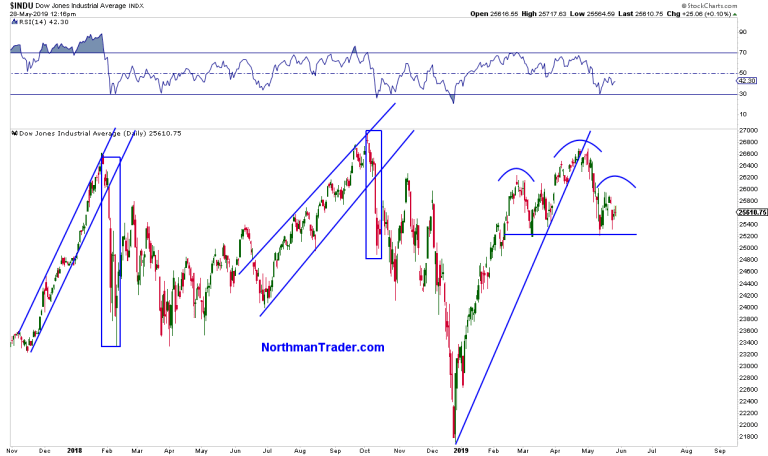

Note $ES is not the only index chart with a potential H&S pattern, here’s the $DJIA:

$DJIA, like many other indices, never sustained a move back above the January 2018 highs. Holding the May lows then is critical to avoid a technical trigger break.

And let’s be clear, without a break of 2800 bears have nothing, but a nice May pullback.

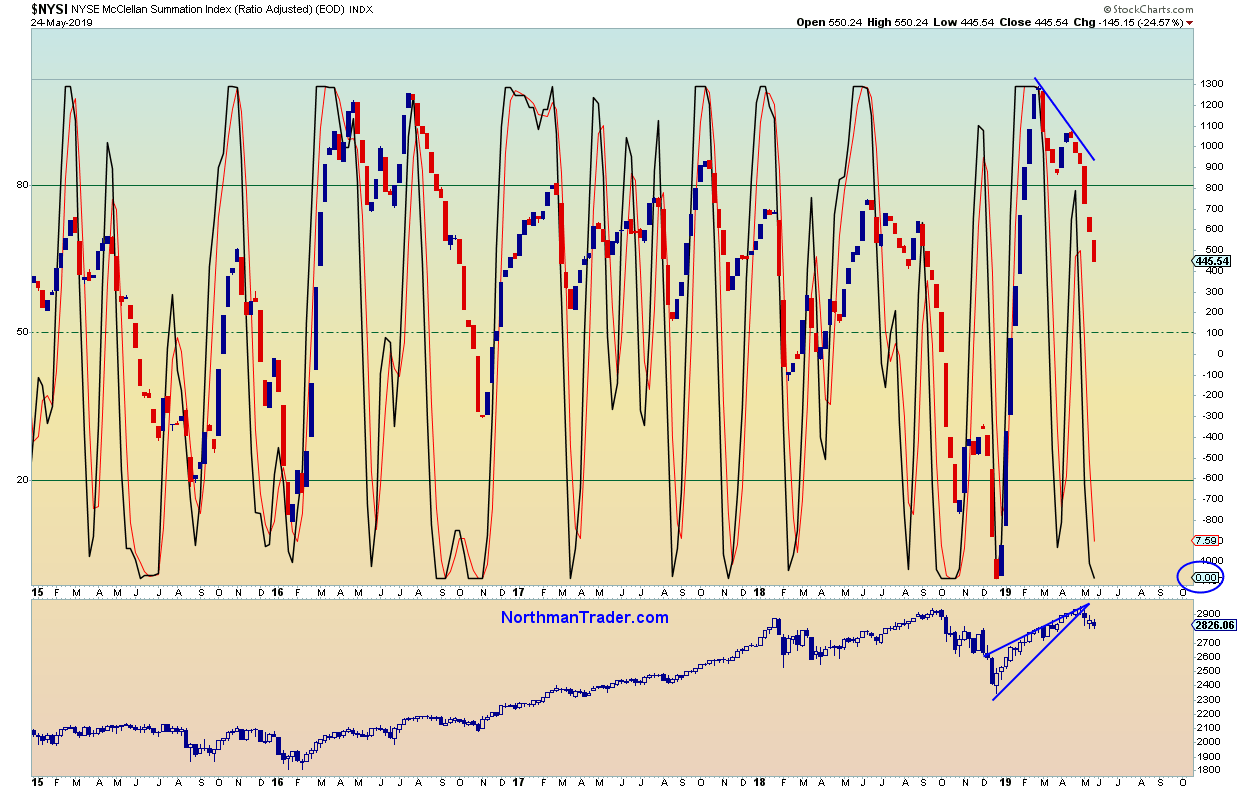

As I also indicated in the interview we’re currently seeing some oversold conditions emerging, example the stochastic on the $NYSI is max oversold at the moment:

That does not preclude new lows, but it also puts bears on notice: A rally is coming, question is from where.

I mentioned seasonality in the interview as well, but pointed out that turning markets in May can also bring sizable further downside risk for June.

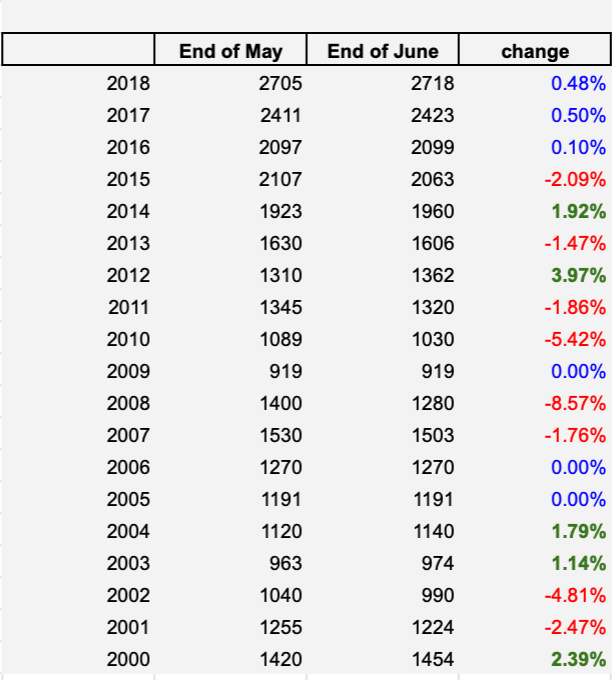

As we’re approaching the end of May this week and are heading into June next week here’s a historic look $SPX performance between the end of May and the end of June since 2000:

What’s that tell us? In 5 years markets were basically flat between the end of May and the end of June. 5 years were up between 2%-4%. 8 years were down between 2%-8%.

Hate to call this a coin toss, but fact is sizable downside can emerge in a June month and the 2640 target zone then wouldn’t be such a crazy target. That’s nearly 11% off the highs and most likely to produce a major rally from there into end of June/early July. So theoretically one could see that drop and then a bounce from there into month end making the overall decline from end of May to end of June much more muted, ie 3%-6% for example.

However, and this is why also I mentioned 2776 as a key level, the 200MA, should markets drop below 2800, the 200MA zone and quarterly 5 EMA zone would also offer intermittent support:

As long as bulls can defend this area, should we get there, bulls may be fine.

But let’s be clear: There’s been no break of 2800 yet, and for now all this remains theoretical, but keep these levels in mind in case we do get a break.

In the meantime, how do we know when bulls are regaining control? Simply put, they need to close a week above the weekly 5 EMA:

This weekly chart, simple as it is, is actually quite interesting.

Firstly note how the May highs stopped at the 2016 trend line resistance dating back to the US election low, hence this minor correction here actually reacted technically quite cleanly.

Also note the weekly 50MA is also coinciding with the daily 200MA I outlined earlier offering further confluence support on a break below 2800. So for all the ethnical pattern targets I would expect a further price battle in the 2750-2780 zone on a break below 2800.

Finally note how the weekly 5 EMA has been resistance and a point of rejection in the past 2 weeks. In Q1 it was support, now it’s resistance. To get to 2900 again, bulls need to close a week above the weekly 5 EMA. It’s currently sitting at 2856. And also note $SPX also need to regain its 50MA which is currently at 2874, bulls also need to recapture that price one to regain control.

So there you go: The battle for control is cleary defined. Bulls must get above 2856 at least and stay above and bears need a break below 2800 and stay below. In the meantime: Chop.

But as I said this morning in the interview: The longer this trade war drags on the more the pressure on economic indicators that are already at risk of signaling a cycle turn. It is entirely possible to trade war oneself into a recession.

The premise: The pressure to make a trade deal would come from lower, not from 5% below all time highs. And that realization may be dawning on market participants as well.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News http://bit.ly/2JM8XMz Tyler Durden

China and Russia appear to be flexing their muscles in the Middle East, as both announced early this week they would boycott a major economic summit on Israel-Palestine peace sponsored by the United States set for late June in the Bahrain capital of Manama. The White House has touted that the US will unveil economic aspects of its long-awaited Middle East peace plan which aims to achieve economic prosperity for Palestinians, or Trump’s so-called “Deal of the Century”.

Crucially, the Chinese statement emphasized a bilateral Russian-Chinese agreement to boycott the talks. Chinese Ambassador to Palestine Guo Wei on Monday visited the West Bank city of Ramallah, where in a meeting he said, “Boycotting the Bahrain conference comes within the framework of a bilateral Russian-Chinese agreement not to participate in it.”

Via Los Angeles Times

During the statements Wei emphasized Beijing’s position “in support of the Palestinian cause and people, including their right to self-determination and the establishment of an independent state of Palestine within the 1967 borders with East Jerusalem as its capital”.

At the same time Palestinian Authority President Mahmoud Abbas commented Monday, lashing out specifically at the White House-backed Bahrain conference for the first time. Abbas said:

Trump’s ‘deal of the century’ will go to hell, as will the economic workshop in Bahrain that the Americans intend to hold and present illusions.

It’s not only a big victory for the Palestinian side, given it’s rallied countries not to show up, but comes amidst the continuing proxy war in Syria where Russia is ramping up airstrikes in support of Damascus over Idlib, as well as the ongoing US-China trade war. However, as Axios notes the decision “is mainly driven by Russian and Chinese tensions with the U.S. rather than by Palestinian interests.”

The Palestine Liberation Organization (PLO), which is the largely secular backbone of the Palestinian National Authority headquartered in the West Bank, has said it wasn’t even notified of the Bahrain conference before it was announced.

PA president Mahmoud Abbas, via the AFP

And interestingly, it’s none other that President Trump’s own son-in-law and senior adviser Jared Kushner who will chair the summit. Al Jazeera reports:

Early last week, the US announced plans to hold a landmark conference in Manama, where Trump administration officials are expected to unveil economic aspects of the “Deal of the Century”, a US backchannel Palestine-Israel peace plan, the terms of which have yet to be made public.

The Manama meeting will reportedly be chaired by Jared Kushner, US President Donald Trump‘s senior adviser and son-in-law, and Jason Greenblatt, Trump’s Middle East envoy.

Last week, Palestinian Prime Minister Mohammad Shtayyeh slammed the planned meeting for neglecting the core issues of “final borders, the status of Jerusalem, or the fate of Palestinian refugees.”

“Any solution to the conflict in Palestine must be political… and based on ending the occupation,” he said. And separately, Axios reports that PLO secretary general Saeb Erekat was told by both Russian and Chinese foreign ministry officials that both countries “support the Palestinian position regarding the Bahrain conference and therefore will not attend it.”

The Palestinian Authority has boycotted any and all US peace talks following last year’s extremely controversial move to give formal US recognition of Jerusalem as the Israeli capital, further buttressed by the US moving its embassy there. Though a number of American gulf allies have predictably said they will attend, the absence of Russia and China is sure to doom any momentum or attempt at international consensus from the start.

via ZeroHedge News http://bit.ly/2X9GNhz Tyler Durden

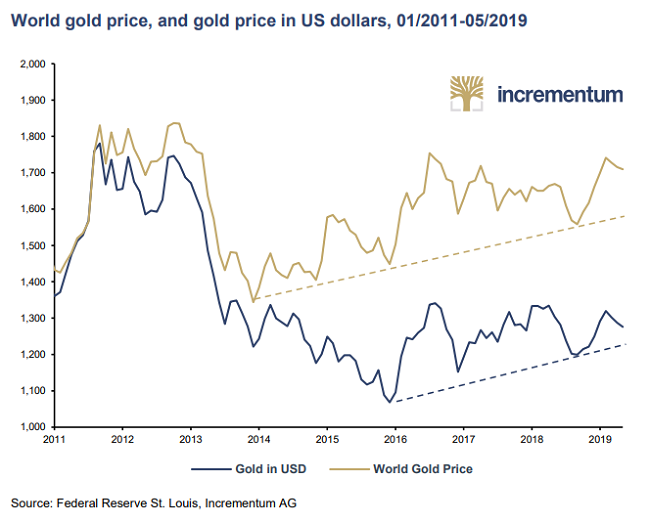

Investors need to look past gold’s current summer doldrums and focus on the yellow metal’s safe-haven potential as trust in society and financial markets continues to erode, according to one fund manager.

“We have seen an erosion of trust in many parts of our lives; we’ve lost trust in the media, in democracy, in geopolitical alliances and monetary policy,” said Stoeferle.

“There is still some trust in the U.S. economy and the U.S. dollar, which is hurting gold, but we don’t think this will last.”

Stoeferle said that the trust in the U.S. financial system is already being tested following the performance in the fourth quarter, which saw large-cap U.S. equities fall 13.5%, small-cap stocks fall more than 20%, gold prices rise more than 8% and gold equities rise nearly 14%.

“For the first time in many years, the seemingly untouchable competitive advantage of stock markets has been seriously questioned. Gold has outperformed all major domestic equity markets,” the firm said in its report.

Although the perception is that the U.S. economy is “the least dirty shirt in the laundry,” Stoeferle said that the economy is built on debt, which is not sustainable in the long run.

The report noted that next year, “U.S. government debt will exceed the combined debt of Japan and the eurozone, despite the fact that absolute U.S. and Japanese debt were at similar levels until 2011, rising almost in step.”

Stoeferle added that it’s not just government debt that is growing out of control; he said that corporate debt with about $600 billion in bonds at risk of being rated as junk.

“I think we are seeing a little bit too much confidence in the U.S. economy and the U.S. dollar and that will come back to bite investors,” he said.

Stoeferle added that confidence in the U.S. dollar is already starting to weigh as it struggles to push higher from its already lofty valuation. Incrementum AG noted that last year the U.S. dollar rose only 4.3%.

“Given the numerous economic, political, and social trouble spots in the EU – Brexit, Italy’s open rebellion against the Stability and Growth Pact (SGP), the yellow vest protests in France, the economic slowdown in Germany – it is remarkable how little the USD has appreciated,” the firm said.

“A further indication that the U.S. dollar could slowly but surely lose its status as a classic safe-haven currency is the fact that in the course of the sharp correction of the stock markets in Q4/2018 the greenback strengthened only marginally. We regard this as a prime indication of a U.S. dollar bear market, whose starting signal has not yet been apprehended by the majority of investors.”

While the U.S. dollar gold price dominates investor perceptions of the yellow metal, Stoeferle said that it is also important to pay attention to the health of the global market. Gold prices are up in other currencies like the Australia dollar, the euro, the Swiss franc and the Japanese yen, the firm said in its report.

“We think it’s only a matter of time before we start to see higher gold prices in the U.S. dollar.”

But Stoeferle added that the real test will come when the inevitable recession hits.

According to the report, most economists are not expecting to see a recession in the next three years, but the investment firm also noted the terrible track record economists have at predicting a recession.

“According to a study by Fathom Consulting, the IMF has correctly predicted only 4 of 469 downturns since 1988,” the report said.

According to the Federal Reserve’s own indicators last month there is a nearly 28% chance of a recession by 2020.

“In the past 30 years, this figure has never been so high if there was no recession in the following two months,” the report said.

Although the gold market is suffering from a lack of investor interest, Stoeferle said that this sentiment could quickly shift if financial markets start to deteriorate. He added that investors need to watch last year’s highs at $1,360 an ounce. He said that if this price level breaks, then investors will flood back into the market.

“We are sticking to our statement from last year that gold is in the early stages of a new bull market – a bull market that could soon pick up momentum on a U.S. dollar basis as well,” the firms said.

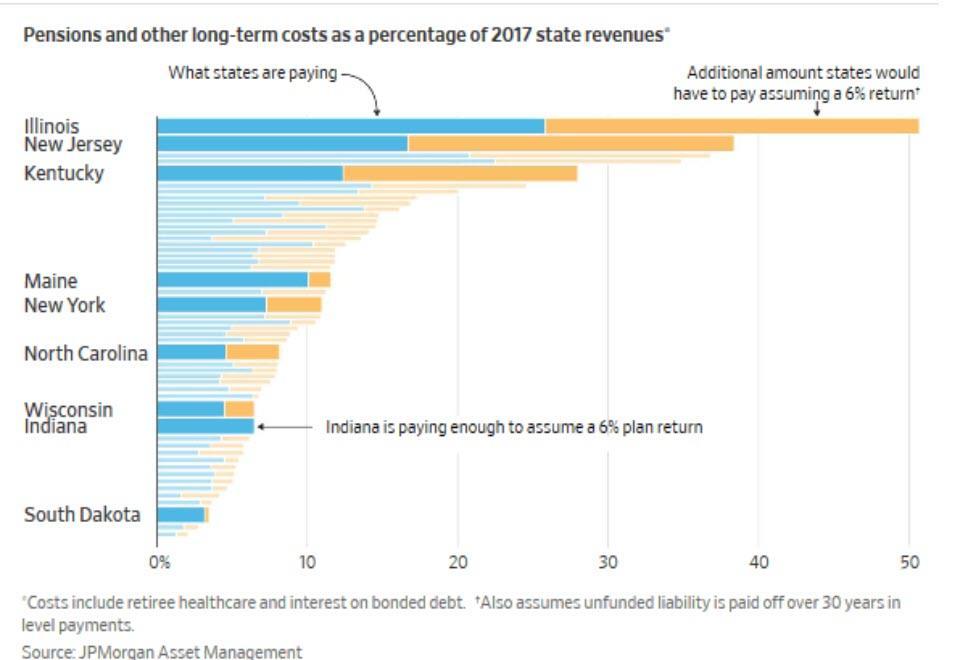

Cash-strapped Illinois is one step closer to passing a new income tax with the potential to seriously accelerate the exodus of high-earning taxpayers from the most financially dysfunctional state in America.

Lawmakers in the Illinois House of Representatives on Monday approved a constitutional amendment aiming to get rid of the state’s flat income tax, clearingthe way for the amendment to be included on the November 2020 ballot for ratification by the voters. Governor JB Pritzker is widely expected to sign it the amendment, which has already been passed by the State Senate.

According to the Democrats who backed it, the tax will help fix the state’s recurring deficits by creating a sorely needed new revenue source: The higher taxes on those earning more than $250,000 would raise more than $3 billion annually while leaving taxes on 97% of the state’s residents unchanged.

There’s no question that more revenue (or, perhaps, less spending) is badly needed. Chronic budget shortfalls, drastically underfunded pensions (to the tune of $134 billion) and $7 billion in unpaid bills have left Illinois’ finances in terrible shape. Illinois’ credit rating being pushed to one level above junk, the lowest in the country, Bloomberg reports.

Pritzker, who took over from unpopular Republican Gov. Bruce Rauner in January, has tried to spin the tax as a “fair tax”, while ignoring the state’s Republicans, who have accused Democrats of refusing to accept responsibility for the state’s dire fiscal situation, and instead seeking to tax their way out of the problem.

But anybody who thinks the new tax will make a meaningful difference in the state’s finances is sadly mistaken.

As Mark Glennon of WirePoints explained in a post published last month, the $3.4 billion in revenues expected to be raised by the new tax will cover barely one-third of the “hole” in the state’s pension obligations.

Here’s the central message now being blasted across the state by proponents of a $3.4 billion state income tax increase on high earners: “Illinois is in a $3.2 billion financial hole. A Fair Tax could fix that and reverse the damage.” That’s an epic lie. The “hole” isn’t $3.2 billion. It’s roughly a quarter of total revenue according to this work, which is consistent with our own numbers – about $10 billion – and that’s just at the state level. The new $3.4 billion will go down a nearly bottomless pit.

The follow chart shows just how dire Illinois’ pension situation truly is.

And while the new taxes might make up for some of this shortfall, at least in the short term, once the new taxes start to bite, those wealthy residents saddled with the new tax will almost inevitably start looking for greener pastures – and sun-belt states like Arizona and Florida offer several advantages over chilly Illinois.

via ZeroHedge News http://bit.ly/2XbI5sF Tyler Durden

If you want to identify tomorrow’s superpowers, overlay maps of fresh water, energy, grain/cereal surpluses and arable land.

The status quo measures wealth with “money,” but “money” is not what’s valuable. “Money” (in quotes because the global economy operates on intrinsically valueless fiat currencies being “money”) is wealth only if it can purchase what’s actually valuable.

As the world slides into an era of scarcities, what will matter more than “money” are the essentials of survival: fresh water, energy, soil and the output of those three, food. The ability to secure these resources will separate nations that fail and those that survive.

In a world of abundance, it’s assumed every essential resource can be bought on the open market. Surpluses are placed on the market and anyone with “money” can buy the surplus.

Things work differently in scarcity: “money” buys zip, zero, nada because nobody with what’s scarce can afford to give it away for “money” which can no longer secure what’s scarce.

Parachute into a desert with gold, dollars, euros, yen and yuan, and since there’s nothing to buy, all your money is worthless. Once you’re thirsting to death, you’d give all your money away for a liter of fresh water. But why would anyone who needs that liter for their on survival trade it for useless “money”?

Imagine the longevity of a regime which sold the nation’s food while its populace went hungry. Not very long once the truth comes out.

Having resources is only one component: consumption is the other half of the picture. Having 4 million barrels a day of oil (MBPD) is nice if you’re only using 3 MBPD, but if you’re consuming 8 MBPD, you still need to import 4 MBPD.

Water and soil are not tradable commodities. Nations which share water resources (rivers and watersheds) have to negotiate (or fight wars over) the division of that scarce resource, but as a generality, fresh water and fertile soil can’t be bought and sold like grain and oil.

The number of nations with surplus energy and food to export is small. As I noted in Superbugs and the Ultimate Economic Weapon: Food, there are contingencies in food production which could quickly erase surpluses and exports and trigger widespread shortages that have the potential to unleash social unrest.

Energy exports are also a natural economic weapon with which to reward needy friends or punish desperate enemies (no oil or natural gas for you!).

But energy exports are also contingent: natural gas and oil pipelines can be blown up by non-state players, shipping chokepoints can be closed or mined, regimes can change overnight and so on.

The value of a nation’s currency can be understood as a reflection of its essential resources, what I have called the FEW resources (food, energy, water) which I would now amend to FEWS (food, energy, water, soil).

Nations which are frugal about creating currency (either via printing/issuance or borrowing it into existence) while prudently managing their fresh water, energy, soil and food will in effect be “backing” their currency with their surpluses of what will be increasingly scarce.

Nations which borrow into existence or emit currency profligately while having scarce FEWS resources and enormous needs for imported food and energy will find their currency rapidly loses value.

When there’s not enough energy and food to go around, who will trade what’s scarce and valuable for what’s abundant and worthless (“money”)? The answer is no one.

If you want to identify tomorrow’s superpowers, overlay maps of fresh water, energy, grain/cereal surpluses and arable land: those nations with abundances that can yield sustainable surpluses in food and energy while taking care of domestic needs will have wealth and power.

Those with diminishing resources that are inadequate to meet domestic demand will have very little wealth, no matter how much “money” they print or borrow into existence or how much consumerist “stuff” they produce.

There are two other attributes that matter: being able to defend your FEWS resources from would-be thieves and a widely shared national sense of purpose that enables shared sacrifice for the common good. Without that shared source of unity, the elites with wealth and power will grab more and more, bringing down the house around them with their limitless greed.

Sacrifice either starts at the top or it means nothing. Forcing commoners to suck up sacrifices only exacerbates disunity and national dissolution.

There are no guarantees that any nation will be able to assemble all that it will take to survive an era of scarcity. But some have better odds than others. Place your bets accordingly.

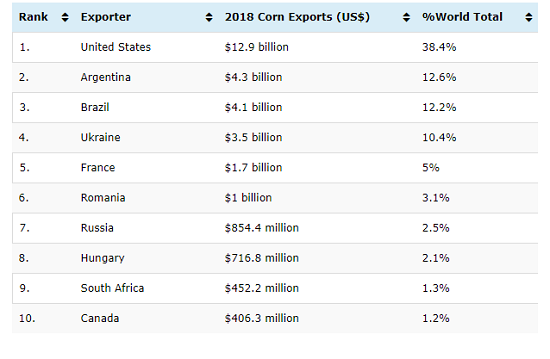

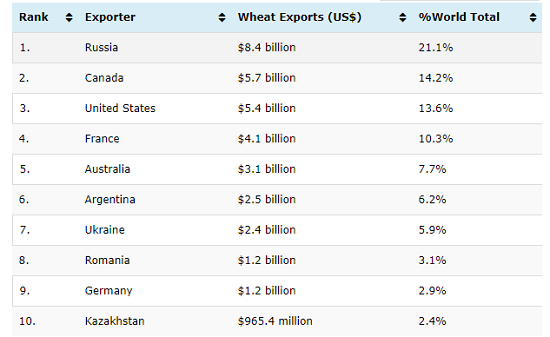

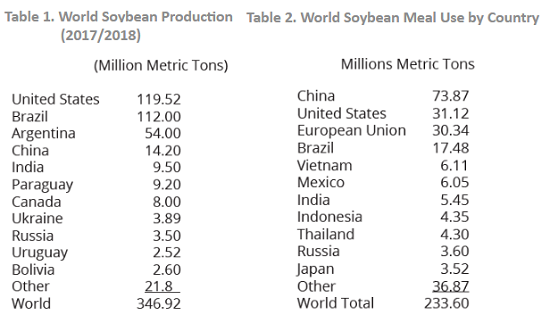

I’m reprinting these charts to emphasize how few nations have geopolitically meaningful surpluses of food.

Corn is often the primary food for livestock. No corn, not much meat.

The exportable surpluses of wheat are concentrated in a few hands.

The same is true of soybeans, a source of protein in Asia and livestock feed everywhere. This chart shows the top producers and the top consumers.

{kind=link}

{kind=link}