Did we mention that Musk was also accused of having committed securities fraud? And that there’s vaguely odd options buying and accounting practices that appear to be driving his company’s value – and his net worth – higher at the same time?

But we digress. We guess, with all those things out of the way, we can congratulate Musk, who is now second only on the rich list to Jeff Bezos after passing Bill Gates, who Musk called a “knucklehead” back in September.

Musk’s wealth now stands at $127.9 billion after adding $100.3 billion to his net worth in just this year alone.

It isn’t just Musk who is making out like a bandit while the rest of the world forges through unprecedented economic turmoil as a result of the Covid-19 shutdowns. Thanks to the Fed’s unlimited QE bazooka in March of this year, members of Bloomberg’s Billionaire Index have seen their wealth rise 23% – or $1.3 trillion – since the beginning of the year, per Bloomberg.

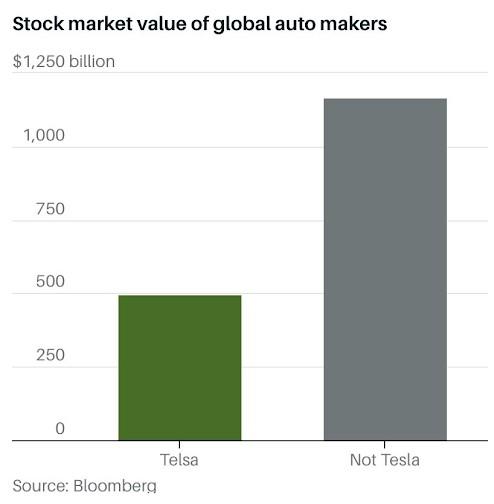

Meanwhile, the market’s relentless driving up of Tesla stock (for whatever reason it is happening) has taken Tesla’s perceived market value by the stock market to nearly half of all remaining global automakers.

Musk’s latest pay award comes as a result of Tesla reaching milestones for “adjusted EBITDA” (yes, there was a multi-billion dollar compensation plan award for an adjusted number) and market cap.

via ZeroHedge News https://ift.tt/3m1IA4Y Tyler Durden

The South Carolina mom who wants her kids’ elementary school to allow them to walk home alone could find herself facing an investigation.

Ominously, at the end of a local news story about Jessie Thompson’s quest to get her kids’ school to permit them to enjoy some fresh air, the anchorwoman said, “Social Services could be called if the children are left to walk home on their own.”

“Left” to walk home. As if the mom is abandoning her kids, rather than trusting them.

The story, chronicled here, involves Thompson, a mom of four. Her three youngest, ages 9, 10, and 11, attend Spann Elementary School in Summerville, South Carolina. They already walk alone in that neighborhood—and look both ways before crossing—on their way to extracurriculars. But the principal has said they can’t walk home from school without an adult present. Thompson must come pick up the kids, or the school will put them on the bus.

The school is situated off a four-lane highway, mistakenly identified as a six-lane highway by the TV reporter. (It has extra turning lanes.) “The Thompson family lives on one side of the parkway and Spann Elementary School is on the other,” intoned the reporter as the camera dramatically zoomed out to illustrate the intersection.

It has a crosswalk as well as Walk/Don’t Walk signs. If the school believes no child can traverse this safely, why not station a crossing guard there, rather than insisting that each and every parent come fetch their kids?

The bus ride takes longer than the walk: During COVID-19, it actually seems less safe than the fresh-air option. As for insisting a parent come pick up the kids, this is a burden on anyone who can’t afford to leave her job in the middle of the day. Presumably, child protective services has better things to do than investigate parents whose kids walk home from school.

For Thompson, the issue is simple: Why is the school allowed to dictate what kids do once they leave school property? A lawyer for the district, Christy Graham, said the school is wary of liability issues. An “additional concern of the district [is] for our students not to be harmed.”

But how far into the children’s home life does the school’s right to be concerned” extend? It doesn’t dictate where the kids can walk on evenings and weekends, after all.

“I’m not naïve,” says Thompson. “It’s a major intersection.” But just because it’s not 100 percent safe doesn’t mean it’s 100 percent dangerous. No intersection can be guaranteed safe, but neither can a car ride to or from the school. Indeed, car passenger deaths are the number one way children die in America. Yet no one stops parents from driving their kids home.

We aren’t really criminalizing danger—we’re criminalizing parents who don’t helicopter. Which means we are criminalizing childhood independence.

With any luck, South Carolina will pass the Reasonable Childhood Independence Bill that had passed the Senate unanimously and was working its way toward the House before the pandemic shut the legislature down. Parents know their kids best. If they believe their kids are ready for a time-honored independence milestone, they should not be threatened with an investigation for neglect. Not by schools, and not by the media.

from Latest – Reason.com https://ift.tt/2J151Zn

via IFTTT

The South Carolina mom who wants her kids’ elementary school to allow them to walk home alone could find herself facing an investigation.

Ominously, at the end of a local news story about Jessie Thompson’s quest to get her kids’ school to permit them to enjoy some fresh air, the anchorwoman said, “Social Services could be called if the children are left to walk home on their own.”

“Left” to walk home. As if the mom is abandoning her kids, rather than trusting them.

The story, chronicled here, involves Thompson, a mom of four. Her three youngest, ages 9, 10, and 11, attend Spann Elementary School in Summerville, South Carolina. They already walk alone in that neighborhood—and look both ways before crossing—on their way to extracurriculars. But the principal has said they can’t walk home from school without an adult present. Thompson must come pick up the kids, or the school will put them on the bus.

The school is situated off a four-lane highway, mistakenly identified as a six-lane highway by the TV reporter. (It has extra turning lanes.) “The Thompson family lives on one side of the parkway and Spann Elementary School is on the other,” intoned the reporter as the camera dramatically zoomed out to illustrate the intersection.

It has a crosswalk as well as Walk/Don’t Walk signs. If the school believes no child can traverse this safely, why not station a crossing guard there, rather than insisting that each and every parent come fetch their kids?

The bus ride takes longer than the walk: During COVID-19, it actually seems less safe than the fresh-air option. As for insisting a parent come pick up the kids, this is a burden on anyone who can’t afford to leave her job in the middle of the day. Presumably, child protective services has better things to do than investigate parents whose kids walk home from school.

For Thompson, the issue is simple: Why is the school allowed to dictate what kids do once they leave school property? A lawyer for the district, Christy Graham, said the school is wary of liability issues. An “additional concern of the district [is] for our students not to be harmed.”

But how far into the children’s home life does the school’s right to be concerned” extend? It doesn’t dictate where the kids can walk on evenings and weekends, after all.

“I’m not naïve,” says Thompson. “It’s a major intersection.” But just because it’s not 100 percent safe doesn’t mean it’s 100 percent dangerous. No intersection can be guaranteed safe, but neither can a car ride to or from the school. Indeed, car passenger deaths are the number one way children die in America. Yet no one stops parents from driving their kids home.

We aren’t really criminalizing danger—we’re criminalizing parents who don’t helicopter. Which means we are criminalizing childhood independence.

With any luck, South Carolina will pass the Reasonable Childhood Independence Bill that had passed the Senate unanimously and was working its way toward the House before the pandemic shut the legislature down. Parents know their kids best. If they believe their kids are ready for a time-honored independence milestone, they should not be threatened with an investigation for neglect. Not by schools, and not by the media.

from Latest – Reason.com https://ift.tt/2J151Zn

via IFTTT

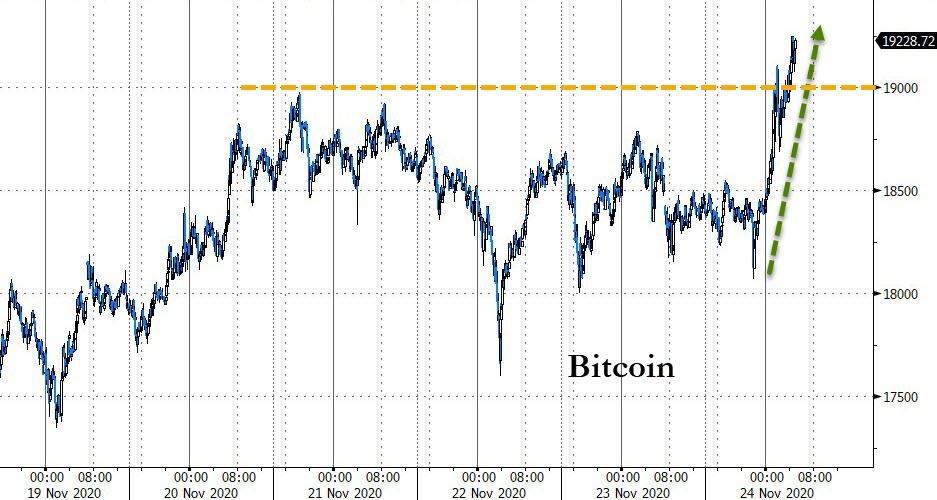

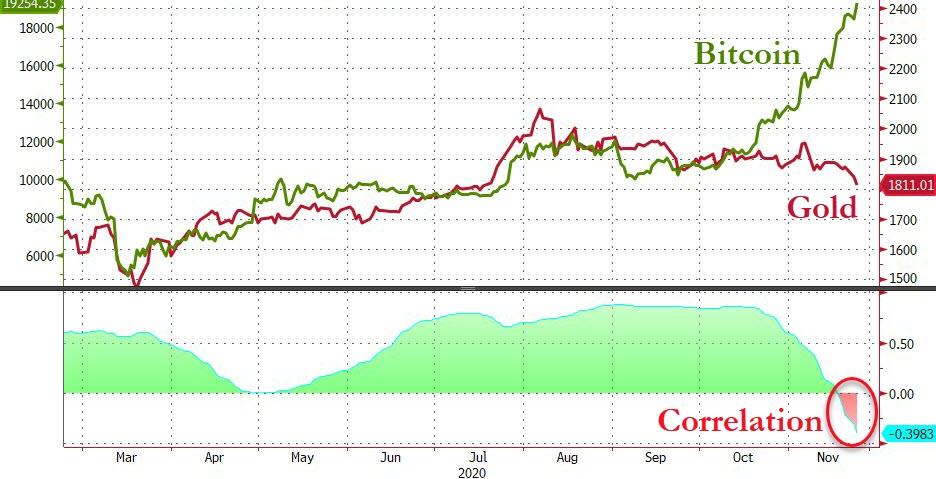

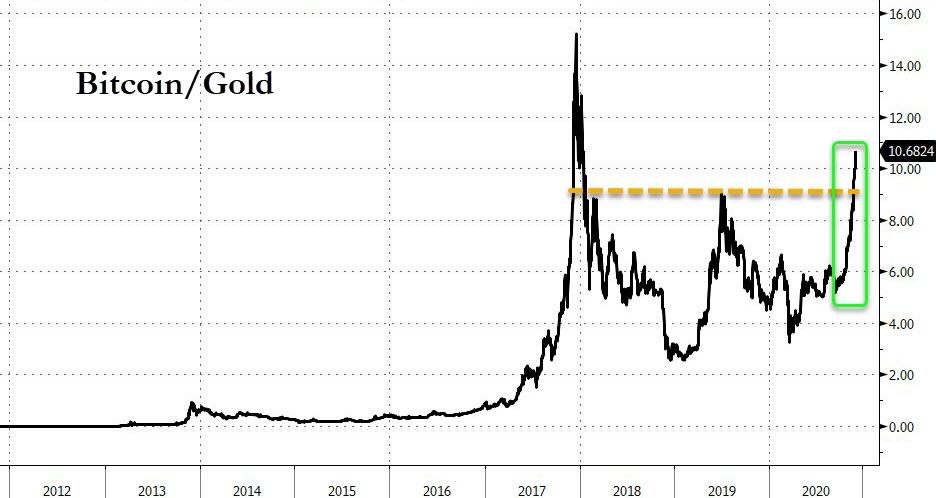

For the first time since 2017, Bitcoin price pushed above $19,000, and multiple indicators suggest the rally may continue. There’s less good news for lovers of more traditional economic-curmudgeon plays with gold dropping for a second day to trade at $1,815

Source: Bloomberg

Within $400 of the record high from Dec 2017…

Source: Bloomberg

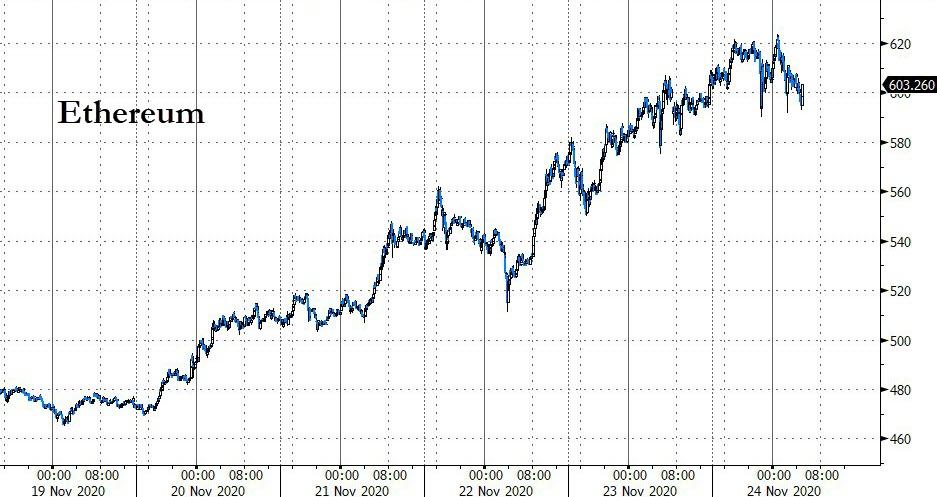

Ethereum is steady today after yesterday’s surge as Eth2’s beacon chain genesis has been confirmed for Dec. 1 following the transfer of 524,288 Ether (ETH) from 16,384 validators into the Eth2 deposit contract since it went live on Nov. 4.

Source: Bloomberg

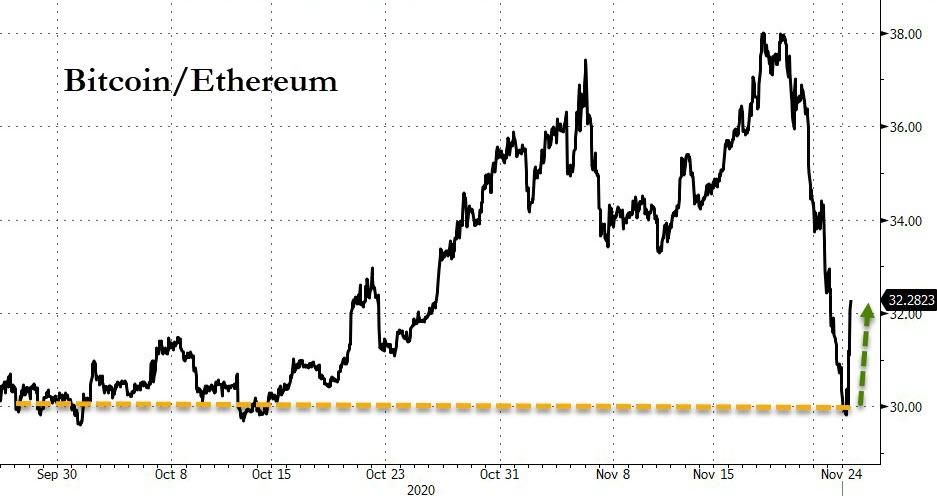

Bitcoin bounced off support versus Ethereum…

Source: Bloomberg

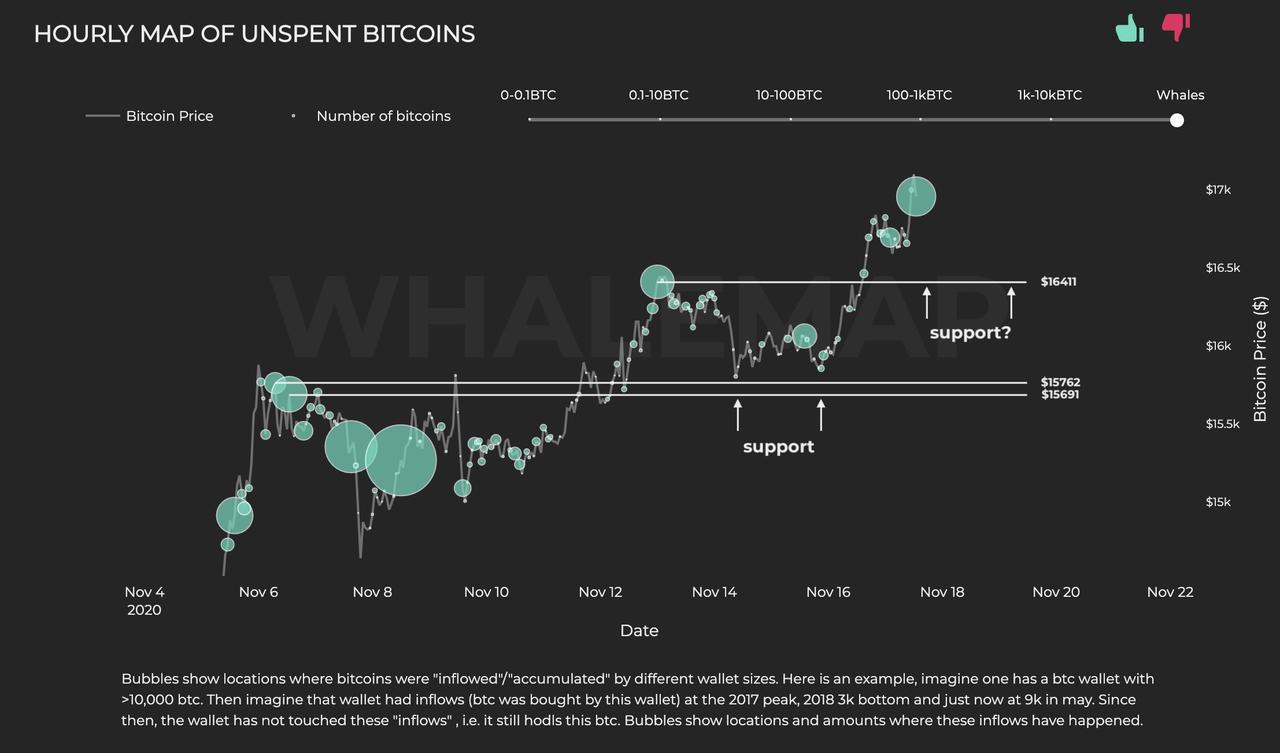

CoinTelegraph’s Ray Salmond points out that the main factors buoying BTC’s ongoing rally is whale accumulation, decreasing exchange supply and explosive volume trends.

All throughout November, Cointelegraph reported that whale clusters were steadily forming as the price of Bitcoin rallied.

These clusters emerge when Bitcoin whales buy BTC at a certain price point and do not move them. Analysts have interpreted this as a signal that whales are accumulating and that they have no intention of selling in the near term.

The difference between the ongoing Bitcoin rally and previous price cycles is that the recent uptrend has proven to be more sustainable. In fact, each whale cluster shows that every major support level BTC reclaimed was accompanied by whale accumulation.

Unspent Bitcoins at each whale cluster. Source: Whalemap

On Nov. 18, when Bitcoin dropped to as low as $17,200, analysts at Whalemap said that the new whale support is located at $16,411. They said:

“Bubbles indicate prices at which whales have purchased BTC that they are currently holding. Bubbles also visualize support levels. Last time we bounced from $15,762 and had a 15% price increase. Is the new bubble at $16,411 going to hold this time as well?”

Since then, Bitcoin has seen several more dips below $18,000 but has since recovered above $18,800, sustaining its strong momentum.

Furthermore, data from Santiment, an on-chain market analysis platform, shows a similar trend. Santiment researchers found that the number of BTC whales significantly increased in recent months. They explained:

“The amount of #Bitcoin whales with at least 10,000 coins (currently $185M or more) has ballooned to 114 the past couple days as prices soared above $18k. Additionally, the amount of holders with at least 1,000 $BTC ($18.5M) has hit an ATH of 2,449!”

Additionally, as Reuters reports, investors like Stanley Druckenmiller, founder of hedge fund Duquesne Capital, and Rick Rieder, BlackRock Inc’s chief investment officer of global fixed income, have recently touted bitcoin.

Retail investors though are still mostly sidelined due to the pandemic’s effect on the economy. But with the entry of Square and PayPal, Lennard Neo, head of research at crypto index fund provider Stack Funds, expects a deluge of retail demand more intense than in 2017.

Neo forecasts bitcoin to reach $60,000-$80,000 by the end of 2021., but that pales compared to Tom Fitzpatrick, a strategist at Citigroup, who forecast earlier this month the token could potentially reach as high as $318,000.

Going from $18,000 to $100,000 in one year is not a stretch, Brian Estes, chief investment officer at hedge fund Off the Chain Capital, said.

“I have seen bitcoin go up 10X, 20X, 30X in a year. So going up 5X is not a big deal.”

Estes predicts bitcoin could hit between $100,000 and $288,000 by end-2021, based on a model that utilizes the stock-to-flow ratio measuring the scarcity of commodities like gold.

That model, he said, has a 94% correlation with the price of bitcoin.

Bitcoin’s supply is drying up

One consistent trend throughout the 2020 bull cycle was the continuous drop in Bitcoin exchange reserves.

Investors and whales deposit BTC to exchanges when they want to sell BTC. Hence, the recent drop in exchange reserves means there are fewer sellers in the market.

A pseudonymous trader known as “Byzantine General” said that every time spot exchanges expand their BTC reserves, they get accumulated. He said:

“Everytime spot exchanges add to their $BTC reserves it gets depleted almost immediately. Don’t you get it? There’s literally not enough supply.”

Volume is surging

The volume of both institutional and spot exchanges has been increasing rapidly since September. Open interest on Bitcoin futures and options at CME surpassed $1 billion in November and Binance’s BTC/USDT pair has consistently delivered over $1.5 billion in daily volume.

Various data points also show that the spot market has been leading the rally, not derivatives or futures markets. This trend makes the rally more stable and reduces the risk of massive corrections.

When the futures market accounts for the majority of the volume during a Bitcoin uptrend, there is a large risk of cascading liquidations. This time, the spot market has been leading the rally, thus making it more sustainable.

‘Digital’ Gold

Finally, there is one more factor worth noting. It appears there is a preference for ‘digital gold’ over the barbarous relic as the correlation between the two crashes into negative territory..

Source: Bloomberg

As Tom Luongo recently noted, the current rally in bitcoin is telling us clearly that there is a new premier store of value asset because of the current state of the world. Maybe that’s really what Schiff is decrying, a world that has passed him by.

What’s becoming clear even to me is that gold will only be valued in relation to bitcoin going forward, not the other way around.

It’s sad but true. In my heart of hearts I wish it were different and not because of the structure of my portfolio or the name of my business.

It’s sad because it proves that we are moving into a different age where technology is depreciating the value of an asset which materially improved the life of billions for millennia towards its commodity extraction value limit.

And while many gold advocates don’t want to admit that they have stood by while the fortune of two lifetimes has passed them by. That’s the bad news.

via ZeroHedge News https://ift.tt/2UTse2i Tyler Durden

Other indexes, already released for September, suggest that an upward surprise is likely.

It would be coherent with the ongoing improvement of fundamentals:

Buyers kept on benefiting from favorable market conditions with mortgage rates reaching the lowest level on record

Demand for second homes skyrocketed amid pandemic

Housing supply remained limited

1. Demand was resilient with mortgage rates falling to a record low for 13th time this year

Most of housing reports published over the period [July-September] confirmed that housing demand remained resilient and supported by low mortgage rates. This positive momentum should continue in the coming month in a context where, according to Freddie Mac, the average cost of a 30-year fixed-rate mortgage dropped to a new record low of 2.72 percent last week. It was the lowest in data going back almost 50 years.

Chief Economist @TheSamKhater: “While economic growth remains unstable, strong housing demand continues to have a domino effect on many other segments of the economy.”

2. Demand for second homes skyrocketed amid pandemic

In the meantime, Redfin highlighted that “in October, demand for second homes skyrocketed 100% from a year earlier—the fourth triple-digit increase in the last five months.” Redfin lead economist Taylor Marr noted that “with mortgage rates at all-time lows and offices shut down across the country, the dream of having a second home outside of the city is becoming a reality for many wealthy Americans.”

In October, demand for second homes skyrocketed 100% since last year.

In this context, in its October report, the National Association of Realtors reported that “total housing inventory at the end of October totaled 1.42 million units, down 2.7% from September and down 19.8% from one year ago (1.77 million). Unsold inventory sits at an all-time low 2.5-month supply at the current sales pace, down from 2.7 months in September and down from the 3.9-month figure recorded in October 2019.”

via ZeroHedge News https://ift.tt/2HBHYEg Tyler Durden

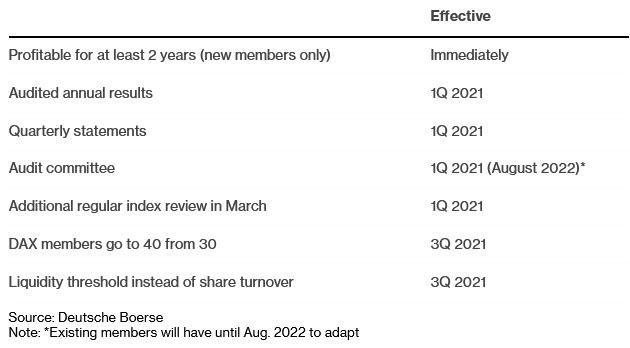

Germany’s DAX Index Announces Biggest Overhaul Since Inception, Expanding From 30 To 40 Companies Tyler Durden

Tue, 11/24/2020 – 08:21

Imagine if the Dow Jones just announced it would expand by a third, growing from 30 member stocks to 40. Well, that’s what happened overnight in Germany, when the operator of Germany’s DAX index announced its most sweeping overhaul since its inception, adding 10 new companies and new quality controls after the implosion of Wirecard rocked investor confidence in the gauge.

According to Bloomberg, the changes will trigger “billions of euros of passive flows for the new members” which are likely to come from the largest stocks in Germany’s MDAX gauge, which include Airbus SE, Siemens Healthineers AG, Sartorius AG and Zalando SE.

Qontigo, which operates the DAX index, said in a statement that it will boost the number of DAX members to 40 from 30 in the third quarter of next year, while reducing MDAX membership to 50 from 60 companies.

“In general, the larger volume, the slightly higher diversification and the slightly increased share of dynamically growing companies is positive for the DAX and should slightly improve the leading German index,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg Bank.

Qontigo, which is a unit of Deutsche Boerse AG, will also impose new criteria on both existing and prospective DAX members, including a requirement to publish quarterly statements and audited annual results, with a fast exit for those failing to release them on time (this begs the question why there wasn’t such a requirement in the past).

A roadmap of the new DAX rules which will begin taking place in 2021 is shown below:

The earnings reporting requirements will become effective during the first-quarter index review, along with a mandate for companies to include an audit committee on their supervisory board. Existing members that don’t yet have an audit committee will get until August 2022 to adapt to the new rule. The only proposal that was not adopted would have banned companies involved in “controversial weapons.” According to Qontigo, this would have affected one current member of the MDAX.

In addition to facilitating passive flows, the changes were prompted by the implosion of the Wirecard fraud, which was a DAX member for two years despite repeated allegations of irregularities. When it collapsed in June, pressure to overhaul the index mounted as existing rules didn’t allow for the benchmark’s first-ever insolvent member to be ejected right away. After that, the index makers undertook a four-week long consultation with more than 600 market participants before adjusting the rules.

The winners from this reshuffle, of course, as the new entrants: for prospective new members, the potential benefits are big, with about 14 billion euros ($17 billion) in exchange-traded funds tracking the index, according to data compiled by Bloomberg.

Entry will be based on market cap, a general liquidity threshold and the new qualitative criteria, with the index owner dropping its previous methodology of rankings which included the volume of shares traded. New members will also need to have been profitable for the past two years.

While the 10 new members has yet to be determined, possible new members include Airbus, Symrise AG, Zalando, Sartorius, Qiagen NV, Siemens Energy AG, LEG Immobilien AG, Brenntag AG, Siemens Healthineers and Hannover Rueck SE, according to Landesbank Baden-Wuerttemberg index analyst Uwe Streich. HelloFresh SE, Scout24 AG, Knorr-Bremse AG, Puma SE and TeamViewer AG are next in line, he added.

Delivery Hero joined the DAX in August to replace Wirecard, and some investors expressed unease about the fact that the Berlin food-delivery firm had never reported an annual profit (wait until they hear about Tesla). Had the new rules already been in place, it would not have been eligible to join.

One tangential benefit of the overhaul is that the change to 40 members brings Germany in line with France’s benchmark CAC index, and may help to minimize the impact of heavyweights on the gauge.

“Europe’s benchmark indexes are generally too narrow compared to U.S. equity indices,” said Frederik Hildner, Salm-Salm & Partner portfolio manager. “I very much like the fact that these are a better proxy for the economy, whereas narrow large-cap indices are oftentimes heavily impacted by sharp moves of large constituents.”

Most investors welcomed the changes and the new quality controls, but some expressed concern about the impact on the midcap gauge. Quoted by Bloomberg, Tarek Saffaf, Greiff Capital Management AG portfolio manager said that “due to the fact that small companies will join the DAX the weights of the bigger ones won’t change much and cluster risks remain. It is even more tragic for the MDAX index as the gauge will lose a lot of liquidity. The quality measures are a good step.”

via ZeroHedge News https://ift.tt/2UWhsbz Tyler Durden

Millions Defy CDC Travel Warnings; Hong Kong Shutters Bars, As Global COVID Cases Near 60MN: Live Updates Tyler Durden

Tue, 11/24/2020 – 08:06

No matter how many celebrities tweet or share Instagram posts imploring Americans to ‘just stay home’ this holiday season, more than a million Americans per day have continued to board planes, trains and automobiles as we reach the peak of the Thanksgiving travel season.

About 1 million Americans a day packed airports and planes over the weekend even as coronavirus deaths passed 250,000. Though traffic is down by roughly 50% compared with last year, it’s worth noting that millions of Americans – particularly younger millennials who are relatively new to the workforce – have been living with family since moving back in with mom and dad while working remotely this spring.

To be sure, the crowds are only expected to swell, with next Sunday likely to be the busiest day of the holiday period. To be sure, the number of people flying for Thanksgiving is down by more than half from last year because of the rapidly worsening outbreak.

The 3 million who went through US airport checkpoints from Friday through Sunday marked the biggest crowds since mid-March, when the COVID-19 crisis took hold in the US. According to Bloomberg, “many travelers are unwilling to miss out on seeing family and are convinced they can do it safely. Also, many colleges have ended their in-person classes, propelling students to return home.”

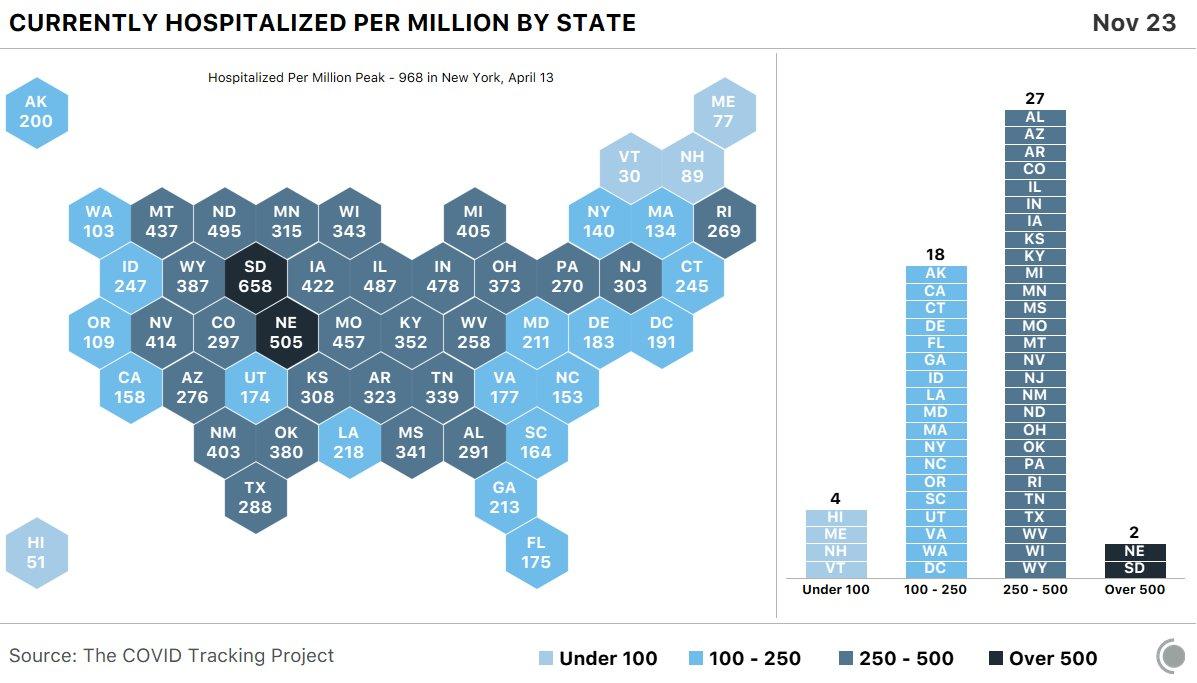

As hospitals across the Midwest struggle with overcapacity and New York reopens an overflow ward on Staten Island, it looks like new case numbers have started to trend lower, suggesting that numbers may have peaked, despite increasingly dire predictions for mortality heading into inauguration day.

Only 4 US states have fewer than 100 people per million hospitalized due to COVID.

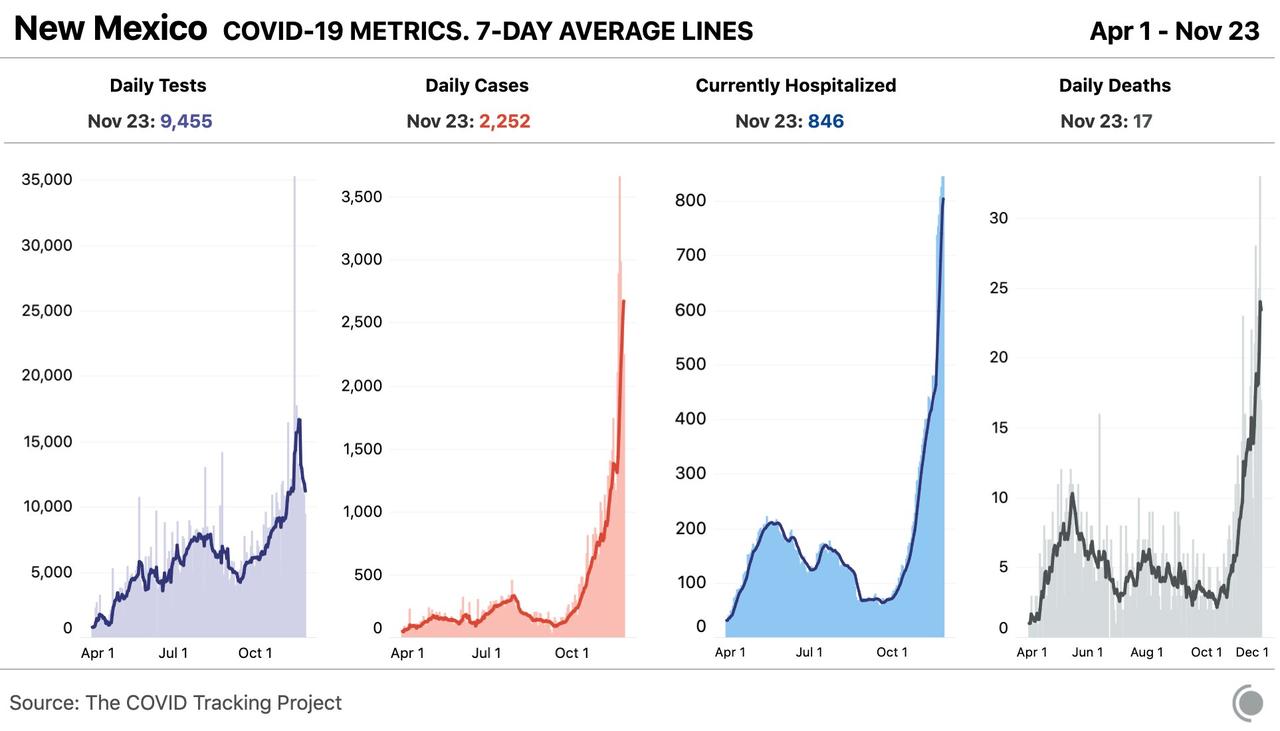

In the southwest, New Mexico is standing out as new cases, deaths and hospitalizations are all at all-time highs.

Looking abroad, Hong Kong authorities announced Tuesday that they would shut bars, nightclubs, and bathhouses from Thursday until Dec. 2 – a period of less than a week – as local coronavirus cases rise, Secretary for Food and Health Sophia Chan said during a briefing on Tuesday.

The number of tables allowed at banquets will be capped at 10, with four people per table. The 4-person public gathering limit, 4-per-table rule at restaurants and mandatory mask- wearing will remain in place even after the rest of the restrictions end. The news comes as Hong Kong reports 80 coronavirus cases, of which 69 are local, said Department of Health official Chuang Shuk-kwan.

Although the number of new cases being reported worldwide has slowed over the past week, the international total of confirmed COVID-19 cases stands just below 60 million, while deaths are on the verge of 1.4 million.

Here’s more COVID news from overnight and Tuesday:

North Carolina Gov. Roy Cooper issued an executive order Monday that extended a mask mandate and Covid-19 restrictions through Dec. 11, with one-fifth of the state’s counties seeing critical levels of spread. His order limits indoor gatherings to 10 people, closes indoor bar service and restricts occupancy for retail stores, restaurants and other public businesses (Source: Bloomberg).

Turkey reported a record number of deaths from the coronavirus, highlighting the dilemma facing policy makers who are trying to contain the current surge in new cases without shutting down the economy again (Source: Bloomberg).

France reported 4,452 Covid cases on Monday, the lowest number of confirmed new infections in 24 hours since Sept. 28. The seven-day average of cases fell to 21,918, the fewest in more than a month (Source: Bloomberg).

New York City residents received $40 billion in stimulus benefits that have been critical to the city’s recovery from the coronavirus, Mayor Bill de Blasio said (Source: Bloomberg).

via ZeroHedge News https://ift.tt/2J10mql Tyler Durden

Futures, Bitcoin And Brent Soar On Biden Transition, Yellen Return Tyler Durden

Tue, 11/24/2020 – 08:02

Futures surged above 3,600, oil jumped to a six month high, and bitcoin traded just shy of its 2017 record on Tuesday as the formal process for Joe Biden to begin his transition burnished a November already boosted by COVID-19 vaccines.

Futures for the S&P 500 rose 0.7% in early European trading hours, trading around the “call wall” that is 3,600 and putting the 49-country MSCI world stocks index on course to set a new record high later. Dow futures jumped 1% in early trading, outperforming Nasdaq 100 futures as investors set up to again rotate out of the technology heavyweights that were seen as safe bets during the recession.

After weeks of legal challenges to the election results, U.S. General Services Administration chief Emily Murphy wrote to Biden on Monday informing him the formal handover process could begin. Minutes later, President Trump tweeted that he had told his team “do what needs to be done with regard to initial protocols”, an indication he was moving towards a transition.

“Markets have been constrained by very high levels of uncertainty on the U.S. political front and around vaccines for weeks, so with those two going away investors are considering the prospect of a return to normality in 2021,” said Emmanuel Cau, head of European equity strategy at Barclays.

Additionally, reports that Biden plans to nominate former Federal Reserve Chair and uberdove Janet Yellen to be the next Treasury Secretary further boosted U.S. stocks on expectations she would pursue “more conventional policies” than the outgoing Steven Mnuchin, according to Reuters which is bizarre because what it really means is that Yellen will buy stocks after the next 20% drop.

“Progress on developing and distributing a vaccine de-risks the path back to normal for oil markets,” said Stephen Innes, chief global markets strategist at financial services firm Axi.

Finally, signs that a working COVID-19 vaccine could be available before the end of the year put the benchmark S&P 500 on course for its best November since 1980 and rekindled demand for cyclical sectors such as industrials and financials after a virus-led crash earlier this year. Energy stocks continued their storm higher on the back of higher oil prices.

Shares of Tesla Inc jumped 4.2% in premarket trading, putting the stock on track to hit $500 billion in market capitalization at the opening bell, and just shy of Berkshire’s market cap.

European markets tracked gains in Asian and U.S. equities, with the broad-based STOXX 600 index climbing 0.6% led by energy stocks, while the Eurostoxx 50 rallied 1.2%; FTSE MIB jumped over 1.5% to outperform peers, while Italian 10Y bonds rallied to fresh record low yields. Oil & gas, autos and basic resources were the best performing sectors. Adding to the positive near-term tone in markets was better than expected economic news from Germany, where gross domestic product grew by a record 8.5% in the third quarter as household spending recovered. The reading marked an upward revision to an earlier flash estimate of 8.2% growth. The Ifo institute’s survey of business morale pointed to fears of a recession to come, however, as the business climate index fell to 90.7 from a downwardly revised 92.5 in October.

Earlier in the session, Asian stocks also jumped with Asia-Pac shares ex-Japan ticking up 0.4%. Australia’s S&P/ASX 200 was 1.26% stronger, touching its highest level in almost nine months, with energy stocks leading the pack there. Japan’s Nikkei jumped 2.5% to its highest level since May 1991 overnight, with energy, real estate and financial shares leading the advance. Seoul’s Kospi was 0.6% higher as was Hong Kong’s Hang Seng which rose 0.4%. China blue-chips were an outlier however, edging down 0.6%, as investors booked profits following recent strong gains.

In FX, the Bloomberg Dollar Spot Index fell by as much as 0.5% as sentiment remained constructive before recovering some of its losses; high-beta currencies extended gains as the dollar broadly fell after European stock markets opened higher, The euro advanced, yet failed to rise beyond $1.19. The pound rose for a third session, extending gains from Monday when it reached the highest in more than two months, on optimism for the prospect of a trade deal between the U.K. and European Union. Market positioning and sentiment in pound options suggest traders see a relatively low risk that the currency will sustain a move above its 2019 highs on a Brexit trade deal.

Elsewhere, the kiwi and Australian dollar both rallied by more than 1% versus the dollar in European hours; New Zealand’s dollar advanced to 70 cents per dollar for the first time in over two years, and the nation’s bond yields rose after the RBNZ said house prices, which have been storming higher this year, could be included in its inflation basket while Finance Minister Grant Robertson released a letter to the central bank expressing concerns over how low rates have stoked home prices, prompting the market to price out the possibility of negative borrowing costs.

In rates, Treasury futures were little changed in early U.S. trading. Yields remain higher by more than 1bp at long end of the curve, 10-year around 0.87%; though still more than 10bp below its November high, 10-year yield had bearish moving-average cross, with 50-day exceeding 200-day for first time since January 2019. Another record 7-year note sale ($56BN) takes place at 1pm ET, and concludes this week’s Treasury auction cycle for holiday-shortened week. Three-month dollar Libor jumped 2.58bp, triggering a flood of sales in Dec20 eurodollar futures. Germany’s 10-year yield was up 1 basis point to -0.57% in early trade, while Bund curves also bear-steepened modestly, with peripheral spreads tightening with 10y BTP/Bund near 118bps.

In commodities, spurred on by the vaccine hopes oil reached levels not seen since March, before the coronavirus began to spread rapidly and decimated demand. Brent crude futures rose 45 cents, or 1%, to $46.51 a barrel to add to a more than 20% surge this month, while U.S. West Texas Intermediate crude added 46 cents, or 1.1%, to $43.52.

The rapid rise of Bitcoin continued this morning, passing $19,000 for the first time in three years, and just shy of its all time high just under $20,000. The rally has been accompanied by the usual collection of further price rises, with Tom Fitzpatrick, a strategist at Citigroup saying earlier this month the token could potentially reach as high as $318,000, while JPMorgan hinting at a price target above $160,000. There was less good news the traditional safe haven gold, which dropped for a second day to trade at $1,811 an ounce by 7:30 a.m. ET, while spot silver dropped over 1.5%.

Investor attention will be on consumer confidence data for November due later in the day, although trading volumes are expected to be light in a week shortened by the Thanksgiving holiday on Thursday. We will also get the Richmond Fed’s manufacturing index, along with the FHFA’s house price index for September. Central bank speakers include ECB President Lagarde, the ECB’s Lane, Schnabel and Rehn, the Fed’s Bullard and Williams, and the BoE’s Haskel.

Market Snapshot

S&P 500 futures up 0.7% to 3,602.00

STOXX Europe 600 up 0.7% to 391.43

MXAP up 1% to 191.45

MXAPJ up 0.4% to 632.41

Nikkei up 2.5% to 26,165.59

Topix up 2% to 1,762.40

Hang Seng Index up 0.4% to 26,588.20

Shanghai Composite down 0.3% to 3,402.82

Sensex up 1% to 44,494.55

Australia S&P/ASX 200 up 1.3% to 6,644.07

Kospi up 0.6% to 2,617.76

Brent futures up 0.8% to $46.41/bbl

Gold spot down 0.7% to $1,825.82

U.S. Dollar Index down 0.4% to 92.19

German 10Y yield rose 0.5 bps to -0.576%

Euro up 0.4% to $1.1883

Italian 10Y yield fell 0.9 bps to 0.513%

Spanish 10Y yield fell 1.0 bps to 0.061%

Top Overnight News from Bloomberg

President-elect Joe Biden’s selection of Janet Yellen as Treasury secretary signals that he plans to act aggressively to revive the world’s biggest economy, putting a former Federal Reserve chair who’s not shied away from stimulus at the helm of his economic policy

Prime Minister Boris Johnson confirmed England’s national lockdown will end next week, to be replaced by a tougher three-tier system of regional restrictions designed to last until spring next year

A German expectations gauge by the Ifo institute fell to 91.5 in November from 94.7 the previous month, a steeper drop than economists forecast. The outlook is particularly bad in services, where temporary business closures and rules affecting social activities erode profits and threaten bankruptcies

The EU is gearing up for its third sale of social bonds, capitalizing on huge investor interest in securities designed to finance the bloc’s economic recovery. The 15-year debt offering kicked off Tuesday, following sales earlier this year that attracted some of the largest orderbooks on record

Goldman Sachs Group Inc. is planning a European stock trading platform to ensure its clients can still buy and sell shares even without a post-Brexit agreement to allow dealing in London

A quick look at global markets courtesy of NewsSquawk

Asian equity markets were mostly positive as the region digested several bullish factors including ongoing vaccine hopes, strong US PMI data and reports that President-elect Biden is to pick former Fed Chair Yellen for Treasury Secretary. In addition, the General Services Administration informed Biden’s team that the transition can formally begin and President Trump’s recommendation for the GSA and his team to adhere to initial protocols, despite his continued legal challenge to the election, also stoked risk appetite. ASX 200 (+1.3%) was led higher by outperformance in energy and its largest-weighted financials sector, with sentiment also helped by preliminary trade data which mostly showed an improvement, as well as the reduced restrictions with Queensland set to reopen its border with New South Wales from December 1st. Nikkei 225 (+2.5%) surged at the open to print its best levels since May 1991 as it played catch up from yesterday’s holiday closure and with exporters cheering a weaker currency, while KOSPI (+0.5%) notched a fresh record high after stronger Consumer Confidence added to the recent encouraging trade data. Hang Seng (+0.4%) and Shanghai Comp. (-0.3%) were less decisive after reports the White House was mulling new actions against China and a new alliance to retaliate against Chinese economic coercion, with the mood in Hong Kong also hindered by the announcement to further tighten social distancing rules and close more indoor entertainment venues. Finally, 10yr JGBs were lower with prices subdued by the outperformance in Japanese stocks and after the bear steepening in USTs, although the downside was cushioned by the BoJ’s presence in the market for over JPY 1.3tln of JGBs with 1yr-10yr maturities.

Top Asian News

York Capital to Spin Off $2.7 Billion Asia Hedge Fund Firm

Hong Kong to Close Bars, Nightclubs From Thursday Due to Virus

Negative Rate Bets Are Passe in New Zealand as No Cut View Grows

Major European bourses hold onto gains seen at the cash open (Euro Stoxx 50 +1.1%) as the mostly positive sentiment from the APAC region reverberated into the region, whilst Chinese markets lagged on idiosyncratic factors. Price action thus far has been somewhat contained across European cash/futures alongside US futures amid a lack of fresh catalysts for the complex in this holiday-shortened week. Amid quietened trade, it’s worth pondering over potential future bullish/bearish catalysts that could materialise in the coming weeks/months, with upside risks including accelerated vaccine progress, larger fiscal support, fixed income outflows into equities whilst some desks also suggest US investors returning to European stocks amid more favourable EPS growth. Conversely, potential downside catalysts include renewed/re-imposition of lockdown measures, an adverse Brexit outcome and a snag in fiscal responses with eyes on the EU budget/recovery fund developments. Back to Europe, broad-based gains are seen across the most majors, whilst CAC 40 (+1.2%) narrowly outperforms as Total (+4.8%) is propelled by gains in crude prices alongside news that the giant is mulling a voluntary redundancy plan in France whilst also halting operations in its loss-making Donges refinery. Gains in Total also support the broader Oil & Gas sector which stands as the outperformer in the region for a second straight session this week. Delving deeper into sectors, the cyclical vs defensives bias is again experienced as Autos, Banks, Travel & Leisure, and Telecoms are some of the top performers, whilst Healthcare, Staples and Utilities reside as straddlers. The Travel & Leisure sectors sees renewed tailwinds on vaccine optimism alongside reports that England is to introduce new COVID-19 testing scheme for passengers arriving from high-risk countries that could reduce self-isolation by a week or more and passengers will not need to self isolate if they test negative. As such, Tui (+11%), Air France-KLM (+10.5%), Carnival (+10.2%), easyJet (+5.7%) and IAG (+5.0%) post firms gains. Elsewhere, despite the broader losses in Healthcare, Novartis (+0.4%) holds onto mild gains having had seen a firm open as the group announced the initiation of share buybacks of up to USD 2.5bln whilst emphasising confidence in future operations.

Top European News

Johnson Ends England’s Lockdown But Hits Regions With New Rules

Germany’s DAX to Get Bigger, Stricter After Wirecard Fiasco

Germany’s Business Outlook Worsens After Short-Lived Rebound

In FX, the Kiwi is cresting 0.7000 vs its US counterpart in wake of considerably better than forecast NZ deficit and debt outturns for the 2019/20 fiscal year and assertions from Finance Minister Robertson that house prices may be included in the RBNZ policy remit pending consultations. However, Aud/Nzd has rebounded from 1.0475 overnight lows as the Aussie corrects higher and Aud/Usd breaches 0.7350 on the way to circa 0.7365 amidst stops and technical buying after mixed trade data and relatively innocuous comments from RBA Deputy Governor Debelle. Conversely, and only in part due to the exertions of the Antipodeans, Monday’s recovery momentum has all but reversed for the Buck as the index recoils further through 92.500 to 92.138. To recap, the DXY only just survived a test of 92.000 yesterday before rebounding sharply following robust Markit PMIs that appeared to spark a stop-fuelled short squeeze and perhaps some early month end positioning given Thanksgiving at the end of this week and an early close on Thursday when the spot date for currency markets if November 30.

CAD/EUR/GBP – All taking advantage of the Greenback’s fall from grace, with the Loonie back within striking distance of 1.3000 with assistance from strong oil prices rather than remarks from BoC Assistant Governor Gravelle who underlined a willingness to restart QE and reopen liquidity facilities if widespread stress in the financial system reappears. Similarly, the Euro has regrouped to reclaim 1.1850+ status irrespective of a somewhat divergent German Ifo survey against expectations and the Pound is eyeing 1.3400 again on the back of Brexit deal hopes underpinned by reports that the 2 sides could be on the cusp of a trade agreement.

JPY/CHF – Not quite so eager or able to recoup declines vs the Dollar on overall risk considerations, as the Yen hovers below 104.00 and Franc under 0.9100 in the run up to Swiss investor sentiment on Wednesday.

EM/PM – The Lira has wiped out even more of its post-CBRT gains to revisit sub-8.0000 lows with little help from a deterioration in Turkish manufacturing confidence or the Banking Watchdog preannouncing that it will terminate calculating assert requirement ratios for banks from year end. Elsewhere, Gold is also struggling to arrest its relapse towards Usd 1800/oz having suffered stop losses on a break beneath Usd 1850 and several tech levels. However, crude and commodity currencies are doing well to the extent that the Rouble and Rand have not been adversely impacted by the worsening COVID-19 situation of SARB noting that SA’s finances are a source of concern.

In commodities, WTI and Brent front-month futures continue on the upward trajectory seen overnight as the key themes for the complex (i.e. expectations for OPEC cut extension alongside vaccine optimism) continue to feed into prices, with WTI Jan back above USD 43.50/bbl (vs. low USD 42.82/bbl) and Brent around USD 46.50/bbl (vs. low 45.89/bbl). The widening of the WTI-Brent arb reflects expectations surrounding the OPEC/OPEC+ confab at month-end, although it is worth noting that a number of technical meetings will occur prior to this, including the OPEC economic board to meet tomorrow and Thursday, whilst OPEC/Non-OPEC experts will convene on Friday, according to EnergyIntel. On that note, it’s also worth flagging some scepticism across participants that the recent crude price rally could translate to several oil producers being reluctant to roll over cuts, albeit this in itself could increase the risk of another price war. Elsewhere, precious metals continue to trend lower despite a softer Dollar, but more-so in lockstep with the constructive risk appetite, with spot gold inching closer towards USD 1800/oz (vs. high 1839/oz) to the downside ahead of its 200 DMA around 1796/oz, whilst spot silver continues to lose ground below USD 23.50/oz (vs. high 23.63/oz). Finally, copper prices are bolstered by Dollar weakness and risk sentiment.

US Event Calendar

9am: FHFA House Price Index MoM, est. 0.8%, prior 1.5%

9am: House Price Purchase Index QoQ, prior 0.8%

9am: S&P CoreLogic CS 20- City MoM SA, est. 0.7%, prior 0.47%; CS 20-City YoY NSA, est. 5.3%, prior 5.18%

10am: Richmond Fed Manufact. Index, est. 20, prior 29

DB’s Jim Reid concludes the overnight wrap

At last! Golf will be back on again from the middle of next week here in England. Ever since Bryson DeChambeau returned from lockdown 1 with a huge increase in muscles in an attempt to hit the golf ball further I’ve been doing a weights and core strength program for absolutely no other reason than to hit the golf ball further. Then 3 weeks ago I started a speed training program. It’s based around the same concept as HIT (high intensity training) training or interval training where you incorporate sprinting into your fitness training in order to get quicker even for long distance training. This speed training involves swinging 3 different weighted sticks as fast as you possibly can in different ways over a period of 10 minutes three times a week. I even bought a speed gun to measure it. I have absolutely no idea whether it will work. All I know is that my wife thinks I’m crazy and obsessed and that I’ve now got back spasms again!

Speed of execution will now be the key for vaccines as for the third Monday in a row we had important news from a leading candidate. This time it was the one from the University of Oxford and AstraZeneca, where interim trial data from the Phase III trials found it to be 70.4% effective when combining the data from the two dosing regimens. Though this is below the figures for the Pfizer/BioNTech and the Moderna vaccines we already have trial data for, one of the dose regimens in which there was a halved first dose and a standard second dose had a higher efficacy of 90%, which is much closer to the other two. And in further good news, this vaccine only needs to be stored at a fridge temperature of 2-8C, unlike the other two which require the far lower transportation and storage temperatures of around -70C for Pfizer/BioNTech and -20C for Moderna, so that’s another positive when it comes to distribution, particularly for EM countries. See our CoTD yesterday here for how the G10 could see herd immunity by mid-year. A reminder that if you want CoTD in your email every day around U.K. lunchtime email jim-reid.thematicresearch@db.com.

In spite of the good news, global equity markets struggled to build on the initial good news even if there continued to be rotation into cyclicals. By the close, the S&P 500 was up +0.56% with the NASDAQ up a lesser +0.22% as some of the biggest components in the index including Apple (-2.97%), Netflix (-2.38%) and Alphabet (-0.50%) saw notable declines. Interestingly the equal weight S&P 500 index was up a very healthy +1.48% and thus further illustrating the continued post vaccine theme away from the mega-caps. In Europe, the STOXX 600 fell from an intraday high of +0.86% shortly after the open to close -0.20% lower. One notable bright spot on both sides of the Atlantic were energy stocks thanks to the rise in oil prices. Brent crude was up another +2.45% yesterday to close at a post-pandemic high of $46.06/bbl. Banks were the other common winner with European banks up +1.67% while their US counterparts gained +2.50% as the reflation trade continues.

Core sovereign bonds sold off yesterday, with yields on 10yr Treasuries (+2.9bps), bunds (+0.2bps) and gilts (+1.6bps) all moving higher. They weren’t the only safe havens to struggle, as gold prices fell -1.77% to a 4-month low of $1,838/oz. That said, it was yet another record day for 10yr BTPs, with yields falling to an all-time low of 0.62%.

Moving on to US politics and overnight the General Services Administration acknowledged Joe Biden as the apparent winner of the presidential election with Mr Trump calling on his agencies to cooperate with this transition. However he said that he would continue to contest the outcome of the election. This triggering of a formal transition process is boding well for risk assets though with S&P 500 futures up +0.80% while yields on 10y USTs are up +1.1bps to 0.866%. Asian markets are also making advances this morning with the Nikkei (+2.52%) higher as it reopened post a holiday while the Hang Seng (+0.13%), Kospi (+0.46%) and ASX (+1.26%) are also up. The Shanghai Comp (-0.17%) is trading down. In FX, the New Zealand dollar is up +0.64% after an overnight letter from Finance Minister Grant Robertson to the central bank expressed concerns over how low rates have stoked home prices. Elsewhere, gold prices are down -0.66% while oil prices are up a further c. 1%.

Staying with US politics, yesterday we began to get news of some US cabinet nominations and other appointees from President-elect Biden. One headline that seemed to help US equity prices was news that President-elect Biden is planning to nominate former Fed Chair Janet Yellen to serve as his Treasury Secretary. The S&P rose +0.45% in the c.15 minutes after the story hit later in the session. She had been viewed as one of the front runners for the position and is likely to be welcomed by both wings of the Democratic party. She is also likely to try to closely align fiscal and monetary policy, which could mean quickly reversing the decision of current Treasury Secretary Mnuchin to shutter the Fed facilities that we highlighted last week.

The president-elect’s other announcements pulled heavily from his time as Vice President. His team announced plans to nominate Avril Haines to be Director of National Intelligence and Alejandro Mayorkas to lead the Department of Homeland Security. Haines was a White House Deputy National Security Advisor under President Obama, while Mayorkas led the US Citizenship and Immigration Services agency during that time as well. Linda Thomas-Greenfield will be nominated as the US ambassador to the UN, after she spent nearly four decades at the State Department and served as assistant secretary for African affairs – a post she left shortly into the Trump administration. Lastly, former Secretary of State John Kerry is slated to return as President-elect Biden’s “Climate Czar” to work in an inter-agency role. The move signals that the incoming administration is going to put far more emphasis on the issue going forward.

Meanwhile in the UK with the year-end Brexit transition deadline approaching, the Times Radio’s chief political commentator reiterated a Telegraph story from the previous night that a phone call, or possibly even a face-to-face meeting, would be set up between Prime Minister Johnson and Commission President Ursula von der Leyen later this week.

Staying with the U.K., yesterday PM Johnson announced that the second lockdown in England would end on December 2 and would instead be replaced by a return to the system of three regional tiers but with likely stricter tiers than before. The government hasn’t actually said which region will be in which tier yet. The government said that they’re seeking to allow more social contact over Christmas, but haven’t yet announced details on what that will mean. Today we can expect another address from French President Macron on the latest changes to lockdown rules.

The main data release yesterday came from the flash PMIs, where all the European countries saw their composite PMIs decline from their October levels. The Euro Area composite PMI fell to 45.1 (vs. 45.6 expected), which puts it back below the 50-mark that separates expansion from contraction for the first time since June, while the composite PMI in France sunk to an even-lower 39.9 (vs. 42.0 expected). Germany held up relatively better at 52.0 (vs. 50.5 expected), though this was also its lowest since June, and the UK slumped back below 50, albeit with a stronger-than-expected 47.4 reading (vs. 42.5 expected). The US was the exception to this pattern, and the composite PMI actually rose to 57.9.

This came even as US Covid-19 hospitalisations hit their highest levels since April 9, with over 12% of hospital beds filled with Covid-19 patients across the country. The Governor of North Carolina issued an order extending the state’s mask mandate and kept restrictions in place until December 11. Meanwhile New York State is a reopening an emergency centre on Staten Island where hospital capacity is strained. The issues across the US highlight how while the vaccine offers much promise for normalisations by the summer, the intervening months could see the economy strained further. Across the other side of world despite still low number of new infections, Hong Kong’s Chief Executive Lam has said that the city will shutter more indoor entertainment venues to control the spread of the virus. Hong Kong reported 63 new cases yesterday. In Japan, Osaka city will ask some bars and restaurants in its nightlife districts to close at 9pm for 15 days starting Friday while the country is also temporarily suspending a campaign to spur domestic travel.

To the day ahead now, and the data highlights include the Ifo business climate indicator from Germany for November. From the US, we’ll also get the Conference Board’s consumer confidence indicator for November, the Richmond Fed’s manufacturing index, along with the FHFA’s house price index for September. Otherwise, central bank speakers include ECB President Lagarde, the ECB’s Lane, Schnabel and Rehn, the Fed’s Bullard and Williams, and the BoE’s Haskel.

via ZeroHedge News https://ift.tt/33cGCal Tyler Durden