Responding to comments, Jack tweeted “It will happen in the US soon, and so the world.”

It’s pretty clear that inflation will run hotter longer than the mainstream anticipated just a few months ago. The CPI came in higher than expected yet again in September. Year on year, the CPI was 5.4% last month. It was the fifth consecutive month that year over year inflation came in above 5%. And the rate rises to 6.5% if we project the inflation levels of the first 9 months of 2021 to the entire calendar year. This is based on government numbers. Keep in mind the methodology to derive CPI was deliberately designed to understate the true increase in the cost of living.

Even Federal Reserve Chairman Jerome Powell has been forced to admit that inflation isn’t looking so transitory. On the same day that Dorsey warned of hyperinflation, Powell conceded that inflation pressures “are likely to last longer than previously expected,” and projected that they could run “well into next year.”

Nevertheless, the mainstream by and large poo-pooed Dorsey’s warning.

Technically, hyperinflation means price increases of 50% per month. Stagflation — a combination of rising prices and low economic growth — already appears to be rearing its ugly head. But could we really see hyperinflation in the US?

Given the Federal Reserve’s monetary policy, it’s not out of the realm of possibility. Despite some fretting about rising prices and some taper talk, the Federal Reserve continues to run the same extraordinary quantitative easing program it launched at the onset of the coronavirus pandemic. Interest rates are locked at zero and there is no hint the Fed will raise them any time soon. While money supply growth has slowed, it continues to expand at an alarmingly high rate. M2 grew at the fastest rate since February last month. With inflation already hot, continuing this kind of loose monetary policy is a recipe for hyperinflation.

Peter Schiff has talked about the possibility of hyperinflation in the past, and he discussed Dorsey’s tweet on his podcast.

I’ve never said it’s going to happen for sure. I’ve always said that’s the worst-case scenario. But it certainly is a possible scenario. I have no way of knowing the exact probability. I still think it is a worse-case, not most-likely scenario.”

But again, the mainstream doesn’t see hyperinflation as a risk at all. Treasury Secretary Janet Yellen weighed in, saying she sees no risk of the Fed losing control of inflation and predicted CPI will return to “normal” by late 2022. Schiff wondered how she could say this.

Obviously, we know she’s just lying. But clearly, there is that risk. I mean, you can say, ‘I don’t think it’s going to happen,’ But the Fed really has no ability to rein in inflation if it gets out of control. So, this is just wishful thinking.”

The central bank has printed trillions of dollars — not just over the last 18 months but over the last several decades. There is already significant pent-up inflationary pressure in the economy.

And we’re unleashing more and more of it,” Schiff said. “And the Fed really has no ability with rate hikes – unless you think that raising interest rates from zero to 0.5% is really enough firepower to do anything. To me, it seems ridiculous. If we end up having the most inflation we’ve had, including even the 1970s, how is the Fed going to fight it with half a percent interest rates?”

Paul Volker had to push rates to 20% in order to tame the inflation of the 1970s. If we have an even bigger inflationary fire now, wouldn’t rates have to go even higher to put it out this time around?

And of course, higher rates would collapse this economy built on easy money and stimulus.

How is the Fed going to sit idly by and watch the entire house of cards that it spent the last couple of decades building completely implode?” Schiff asked.

“It’s not going to do that. … The only way that the Fed can contain inflation is just to hope that it never really becomes a problem. And that’s basically what it’s doing. It’s pinning everything on hope.”

As Schiff put it, it’s “open mouth operations.”

When you can only bark and you can’t bit, you’d better bark awfully loud. Because that’s all you’ve got.”

So, while hyperinflation may not be the most likely scenario, it’s certainly a scenario.

“Not Hyperbole” – Biden Warns House Dems That His Presidency Depends On New Spending Plan Vote

Update (1215ET): Having explained to the American public how “17 Nobel Prize winning economists” believe this new spending bill will not be inflationary and will not raise the deficit (seriously), it appears President Biden is rapidly realizing just how serious an inflection point he is approaching.

Bloomberg reports that, in a private meeting Thursday at the Capitol, Biden warned House Democrats that his presidency and their own political fortunes depend on them passing his multi-trillion-dollar economic agenda.

“I don’t think it’s hyperbole to say that the House and Senate majorities and my presidency will be determined by what happens in the next week,” Biden told the lawmakers, according to two people in the room and a third person familiar with the remark.

Given his record approval rating plunge since inauguration, perhaps that bird has already flown the coop, and backing a flailing president into the MidTerms may not be poitically palatable to each of their individual political careers.

* * *

Update (1145ET): Arriving roughly a half-hour late, President Biden spoke from the White House on Thursday to fill out the details of the Dems’ $1.75 trillion social spending and climate change plan, the president seemed to have a message to any Democrat who might vote against it: the bill represents an effective “compromise,” that won’t increase the deficit, according to “17 Nobel Prize winning economists.”.

While many Dem agenda items were left out, Biden said “that’s compromise…that’s consensus and that’s what I ran on,” he said of the bill, saying that, combined with the infrastructure bill, the package would amount to a “historic investment” that would “truly transform our nation.”

“No one got everything they wanted, including me. But that’s what compromise is,” Biden said, touting spending deal that includes climate and Medicaid coverage provisions but excludes paid leave and drug-price negotiations. “That’s consensus, and that’s what I ran on.”

He then went on to “lay out a few points”. “We face an inflection point as a nation” since the dominance America enjoyed during the 20th Century is already fading as we head deeper into the 21st.

“For most of the 20th Century, we led the world by a significant margin because we invested in our people. We didn’t just build an interstate highway system, we built a highway in the sky…we invested in the space race, and we won.

As for American leadership in public education, “we invested in education for all our children back in the late 18th century…that was a major part of why we were able to lead the world in the 20th century…but somewhere along the way…we stopped investing in our people.”

However, somewhere along the line, America “lost our edge as a nation.”

“We used to lead the world in educational achievement, now according to the OECD, the US ranks 35th…We can’t be competitive in the 21st century economy if we continue this side.”

Americans need to “build America from the bottom up not the top down.”

As for the theme of economic inequality, Biden said he “can’t think of a single time when the middle class has done well and wealthy haven’t done well…but I can think of times when the wealthy did well and the middle class didn’t.”

Ultimately, the social spending bill is “about expanding opportunity not letting the opportunity be denied.” “It’s about leading the world and not let the world pass us by

Many of the benefits of the bill are targeted at what Biden called the “sandwich generation who feel financially squeezed by raising a child and caring for an aging parent.”

Seniors on medicare they need some help…they don’t want to put them in nursing homes not because of the cost but because its a matter of dignity. you’re just looking for an answer so your parents can keep living independently with dignity…we’re going to expand services for seniors so families can get help from well-trained professionals.”

In a reference to how COVID has impacted the labor market, Biden said “30 years ago we ranked 7th in terms of women working…we’ve gone from 7th to 33rd. There are over 2MM women not working today because they can’t afford child care.”

Biden added that “we’re going to allow parents earning less than $300,000 a year well pay no more than 7% of their salary on childcare,” Biden said.

Moving on, Biden added the plan would “cut child poverty in half in a year.”

After this, he shifted to the climate side of the agenda, and infrastructure. The bill according to Biden will make climate friendly investments in infrastructure like renewable energy, public transportation (including trains, as Biden noted in a self-deprecating joke) while also investing in clean water for the next generation.

Circling back to the subject of how to pay for the bill, Biden insists that “in order to make these investments…the wealthy must pay their fair share.”

“If we make these investments, there will be no stopping Americans and the American people…that’s what these plans do, they’re about betting on America.”

He concluded without taking questions, saying only “see you in Rome” as he presumably left the podium to depart for the G-20 conference in Rome that starts later Thursday.

* * *

President Biden will attempt to explain to the nation just how awesome his administration’s new tax-the-rich-and-spend-spend-spend plan is (despite it being less than half the size that his progressive pals are still demanding)…

Remarks due to start at 1115ET:

* * *

Update (1010ET): President Biden’s brief trip to Capitol Hill to try and sell his new social spending and climate change framework to progressives is over. According to BBG, he has left the Dem caucus meeting with his top negotiators and Nancy Pelosi, whom he was seen chatting with as they departed. Biden will address the American people in a little over an hour.

Biden is pushing for a vote on the infrastructure bill Thursday (which seems more like a fantasy than an achievable goal) although that goal was parroted to the press by at least a few House progressives. Speaker Pelosi has confirmed that she wants to have the vote on the infrastructure bill on Thursday – as in today.

Meanwhile at least one progressive – Rep. Ilhan Omar – says she won’t support a spending bill until she sees the full text.

* * *

Update (0900ET): As President Biden prepares to meet with Congressional Democrats ahead of a 1130ET presser from the White House to officially unveil the plan, more details of the Dems’ new $1.75 trillion spending-and-climate plan are leaking out. Biden has reportedly struck an agreement with moderates like Manchin and Sinema on the deal (which encompasses an expansion of the social safety net, and elements of the ‘Green New Deal’).

Here’s CNBC with more specific details from the plan, some of which were previously known, and some of which are novel:

After months of negotiations, “the package contains a wide-ranging set of programs that, if enacted, will profoundly impact the lives of families with children, low-income Americans and the renewable energy economy,” per CNBC and Bloomberg.

The details include:

Universal preschool for all 3- and 4-year olds, which is funded for at least 6 years.

Subsidized child care that caps what parents pay at 7% of their income, which is funded for 6 years.

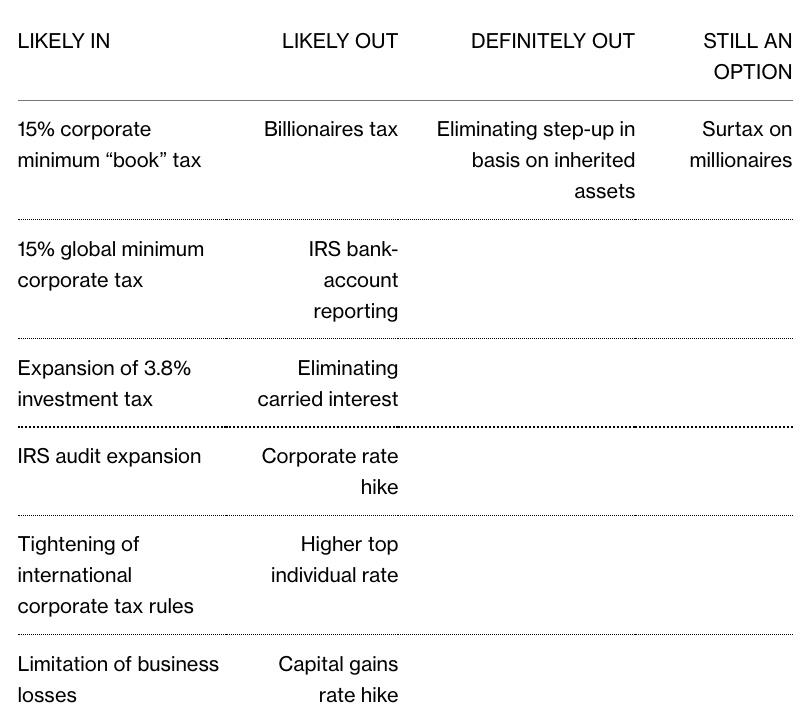

A 15% minimum tax on corporate profits for firms with earnings over $1 billion reported to shareholders, and a 1% surtax on stock buybacks

An additional 5% tax on incomes above $10 million, as well as an additional 3% on incomes above $25 million

$555 billion in clean energy and climate provisions

A one-year extension of the current expanded Child Tax Credit, which impacts approximately 35 million households nationwide.

Expanded tax credits for 10 years for utility and residential clean energy, including electric vehicles.

Extend the current, pandemic-related Affordable Care Act subsidies for 4 years.

Allow Medicare to cover the cost of hearing.

The framework also raises the possibility of immigration reform being included in the reconciliation package, but the scope isn’t clear. It forecasts a cost of $100 billion, in addition to the $1.75 trillion topline.

The framework is also notable for what the framework excludes, per CNBC:

A longstanding proposal to create a federal paid family and medical leave system was dropped from the bill on Wednesday afternoon after Sen. Joe Manchin, a key Democratic swing vote, said he did not believe the program belonged in the bill.

The primary purpose of Biden’s trip to the Hill Thursday morning is to convince progressives to back the plan, though Biden says “everybody” is already on board with the new plan. Per CNBC, the bigest challenge for Dems will be convincing the progressives to accept it, since the plan falls far short of “the Squad” and their allies’ grand vision for a $3.5 trillion reworking of the social safety net. Biden will deliver an address to the nation later this am after the meetings on the Hill.

* * *

After abandoning a plan to strictly monitor Americans’ bank accounts in an effort to crack down on tax cheats following an outburst of popular opposition, Democrats finally came together yesterday and agreed on a corporate minimum tax that might offset at least some of the spending from President Biden’s “Build Back Better” initiative.

But given the fractiousness inherent to the Democratic Party, which has seen the House and Senate tax-writing committees and their leaders and members constantly bickering over what new taxes would and would not be acceptable – while Republicans stoke public resistance by warning that the Dems are trying to push through the biggest tax increase in decades – it looks like (after Sen. Kyrsten Sinema agreed to a minimum corporate tax rate) the Democratic caucus has finally ceded something that we at Zero Hedge have suspected all along.

1) the bulk of President Trump’s tax cuts will be left in place although

2) corporations will face a new slightly higher minimum tax.

But let’s put the tax side of the program aside for a moment, because WaPo and WSJ have just reported that President Biden is preparing to share a $1.75 trillion framework for his spending bill before he leaves for an extended trip abroad.

That would mean the size of the Dems’ social spending program has shrunk below $2 trillion to $1.75 trillion according to a report released minutes ago by WSJ . That’s down from the initial target of $3.5 trillion. Lawmakers are also waiting to pass a $1.2 trillion “bipartisan” infrastructure bill that passed the Senate back in August, but has been held up by progressive Democrats in the House, who are demanding that the social spending plan get a vote first, so to guarantee that it doesn’t fall by the wayside. Biden has indicated his supports this strategy.

After Treasury Sec Janet Yellen and other Dems hinted at the possibility of taxing unrealized capital gains – an idea that elicited horrified responses from Dems and GOPers alike – BBG says it looks like formerly “core” proposals to increase the top marginal income tax rate and the rate on capital gains tax have been abandoned while “more creative” measures like a minimum tax on the profits on corporate financial statements and a surtax on millionaires are still a possibility.

The new framework is expected to include funding for expanded health coverage, housing, universal prekindergarten and child care, and climate programs, among other provisions. WSJ says. Dems also abandoned a key push to mandate paid family leave on Wednesday.

After weeks of secretive discussions, Sen. Sinema has given the Biden admin a list of specific tax policies she will support in order to raise revenue for the social spending plan, per BBG’s sources on the Hill.

She would back the billionaires’ tax put forth by Senate Finance Committee Chairman Ron Wyden or a 3% income surcharge for earners above $5 million, as well as a 15% corporate minimum tax, the people said on condition of anonymity to discuss sensitive negotiations.

As Dems continue to debate what an acceptable tax and spend plan might look like, it appears Dems have also abandoned a plan to increase inheritance taxes, while a potential surtax on billionaires’ wealth has also started to gain their momentum.

But before President Biden leaves for a lengthy trip to Europe for the G-20 climate talks in Rome and the climate summit in Glasgow that will be the first major global climate summit since the Paris Accords in 2015, he’s expected to visit the Hill. Per WSJ, Biden’s also expected to make an address from the White House Thursday at 1130ET to explain to ‘average joe’ what the latest version of the Dems’ spending framework looks like.

Pelosi Pulls Trigger – Dares Progressives To Nuke Infrastructure Package With Thursday Vote

Update (1257ET): Challenge accepted…

House progressives have too many “No” votes to pass the infrastructure package, according to Rep. Pramila Jayapal (D-WA), sentiment echoed by Rep. Ilhan Omar (D-MN).

Will Pelosi – who said she’d never hold a vote that won’t pass – cancel?

* * *

House Speaker Nancy Pelosi is about to test whether progressive Democrats are full of hot air over their threat to nuke the $1.2 trillion bipartisan infrastructure package unless it’s paired with the yet-to-be finalized social spending package – which the White House capped at $1.75 trillion earlier Thursday.

If House progressives cave and pass the infrastructure package without the already-gutted ‘Build Back Better’ Act, they’ll give up whatever leverage they thought they had (and obviously don’t) towards achieving their spending goals.

Biden, meanwhile, said on Thursday that “We badly need a vote on both of these measures,” adding “I don’t think it’s hyperbole to say that the House and Senate majorities and my presidency will be determined by what happens in the next week.“

According to The Hill, Pelosi insists she’s “going to hold the vote open until we get a majority,” which – at least as of last night, didn’t seem within the realm of possibility based on Wednesday night statements by House progressive leaders.

Top progressives maintained Thursday that they still wanted legislative text for the social spending package before they’d feel comfortable backing the bipartisan infrastructure bill.

Rep. Pramila Jayapal (D-Wash.), the Congressional Progressive Caucus leader, planned to survey the 94 other members in her caucus but predicted that they’d need something more concrete than the White House framework.

“We have had a position of needing to see the legislative text and voting on both bills. And we’ll see where people are, but I think a lot of people are still in that place,” Jayapal told reporters after the meeting with Biden. –The Hill

“I’m still gonna be a ‘hell no’ [on infrastructure] unless I see both move,” said Rep. Rashida Tlaib (D-MI), a member of the progressive Squad, after the meeting.

I am not going to sell out my district for a bill that was written by the fossil fuel industry and championed by two Dem senators who bow down to Big Pharma & corporate polluters.

Yet, despite the above, Pelosi thinks she can convince House Democrats to give Biden a victory as he embarks on a Thursday trip to Europe where he will address the G20 and global climate summit in Glasgow.

“When the president gets off that plane we want him to have a vote of confidence from this Congress,” Pelosi reportedly said according to a source from the meeting.

“In order for us to have success, we must succeed today.“

“This Bill Now SUCKS” – Disappointed Dems Blast Biden, Bernie, & House Progressives Over New Spending Plan

Although they fought hard to preserve a vision of the biggest overhaul of the American social safety net – along with a revolutionary reworking of climate change policy – it appears that President Biden is preparing progressives in Congress for a major let-down by insisting that a scaled-back bill – the details of which are being shared with the public and press bit by bit – is better than no bill at all.

And while House progressives grumbled to the press following Biden’s Thursday morning visit to the Hill, the administration seems to think it has them convinced that it’s this bill, or no bill, as Nancy Pelosi says she’s hoping to hold a House vote on the “bipartisan” infrastructure package that progressives have been blocking for months.

Still, it’s worth noting that during the entire stretch of negotiations, President Biden has been insisting that he shares the progressives’ ideals, and that he has been on their side.

But the sense of defeat that progressives in both the House and Senate are grappling with Thursday was perhaps best encapsulated by comments from Sen. Bernie Sanders, the standard-bearer for the American far-left.

Sanders complained to reporters that “almost every sensible progressive revenue option that the president wants, the American people, that I want seem to be sabotaged.” As recently as Wednesday night, Sanders insisted that Dems were still far apart on a deal. President Biden seems to think he’s at the very least won the support of all the Dems in the Senate with the current package.

Meanwhile, in the House, Representative Ilhan Omar said that her position hasn’t changed, and she won’t support a vote on the infrastructure bill until the text of the spending-climate change package has been published in full.

Already, the liberalati on twitter are attacking progressives for failing to achieve their objectives, with one user accusing progressives of “gaslighting” Americans and that the “gutted spending bill..doesn’t even come close to meeting the moment we are in.”

The worst part is the Democrats will try to deceive and gaslight the people that this gutted spending bill is a big win for them when it doesn’t even come close to meeting the moment we are in. End this abusive relationship and do not give this corrupt party your vote ever again.

The biggest complaint it seems among progressive Dems was the decision to cut mandated family leave (at least four weeks), while taxes on billionaires’ unrealized capital gains has also been tossed, it appears, after Wall Street strenuously pushed back. Other tough cuts included a deal expanding Medicare to include dental AND vision coverage, along with agreements on prescription drug coverage. The Dems just couldn’t get the votes for a prescription drug plan of sufficient scope.

Biden appears to be confident the package has the support of all 50 Dem senators (and the tie-breaking vote from VP Kamala Harris) and enough votes to pass the House. Asked as he arrived on the Hill if the framework will get the support of progressives, Biden said, “Yes.”

Another high-profile progressive commentator, “Young Turks” Cenk Uygur urged progressives to “vote no” on the package, claiming “we have gotten nearly nothing.” In particular, he slammed Dems for cutting paid family leave from the bill.

Democrats drop paid family leave! This bill now SUCKS. Democrats are total losers. #VoteNo

The as more new details of the package came together, Uygur slammed progressive leaders in Congress, including House progressive caucus leader Pramila Jayapal and even Sen. Sanders. The reason, he said, is because Sen. Manchin is willing to kill the bill and Biden’s legacy, and Bernie isn’t.

Undeniable fact: Manchin and @BernieSanders are both Senators. But Manchin is getting everything he wants and Bernie is getting almost nothing. Why? Because Manchin is willing to kill the bill and Bernie isn’t. Progressives will have no power until they’re willing to kill bills.

However, he ultimately blamed Sens. Sinema and Manchin, whom he accused of being “corrupt”.

If you’re trying to figure out why Manchin and Sinema are trashing the entire Democratic agenda, it’s actually quite simple. They’re corrupt. They’re acting on behalf of their corporate donors. Silver lining here is that they made the corruption so obvious it can’t be ignored.

Every time you have to go back to work right after having a baby, know that Manchin and Sinema did that to you. Every time you pay unaffordable prices for your lifesaving drugs, know that Manchin and Sinema did that to you. They chose to cause you pain and suffering, for money.

Biden will unveil more details of the bill later on Thursday as he prepares to jet off to the G-20 Summit. But the president surely knows progressive activists are seriously unhappy with the plan – and that’s a major risk heading into the midterms. But more immediately, the big test will be a House vote planned on the “bipartisan” infrastructure bill that’s reportedly being set for Thursday.

We give the last words to Mike Shedlock who seemed to sum things up rather succinctly…

I wish Progressives would kill the bill.

They would then get what they deserve:

NOTHING https://t.co/QSqtceST8T

A Rutgers gender studies professor gave an interview in which she asserted that “white people are committed to being villains,” and, “we gotta take these motherfuckers out!”

Yes, really.

“Dr. Brittney Cooper, a professor in the Rutgers Women’s, Gender, and Sexuality Studies department that goes by the Twitter moniker “ProfessorCrunk,” appeared on a September YouTube interview with writer Michael Harriot of The Root to discuss Critical Race Theory and recent attempts to oppose it being taught in elementary and high schools,” reports the College Fix.

During an outburst about white people fearing retribution if they give up power to blacks, Cooper made it clear what needed to happen for whites to relinquish control.

“The thing I want to say to you is that we gotta take these motherfuckers out, but like, we can’t say that, right?,” Cooper screeched.

Rutgers professor: “White people are committed to being villains,” “We gotta take these MF’ers out.”

After uttering that call to action, which would be taken as an ominous violent threat if said by a white person, Cooper claimed she doesn’t believe “in a project of violence.”

The professor went on to call whiteness “an inconvenient interruption” in the history of the world and claimed that black societies were “being brilliant, and libraries, and inventions, and vibrant notions of humanity, and cross-cultural exchange long before white people showed up being raggedy and violent and terrible and trying to take everything from everybody.”

Cooper makes $112,000 a year to lecture everyone about how much she hates white people, a surprising opportunity given that she thinks America is still run by “white supremacy.”

The interview once again highlights the demented anti-white extremism that has come to dominate the social justice movement and academia.

Such disgusting rhetoric is the natural conclusion of Critical Race Theory programs that teach white people to hate themselves and that its normal for them to face institutionalized vitriol and condemnation for their skin color.

The interview remains on YouTube, fully monetized, with no restriction of any kind whatsoever.

The Root is the perfect platform for such vile rhetoric given that they published an article last year declaring that “Whiteness” is a “pandemic” and “the only way to stop it is to locate it, isolate it, extract it, and kill it.”

NYC Firefighters Union Tells Members To Defy Vaccine Mandate; NYPD Union Loses Bid To Halt

Members of New York’s finest are pushing back against Covid-19 vaccine mandates to the point of civil disobedience.

On Wednesday, the head of the New York City firefighters union said that he told unvaccinated members to report for duty regardless of an order from Mayor Bill de Blasio threatening to place them on unpaid leave if they refuse to take the jab, according to Reuters.

“I have told my members that if they choose to remain unvaccinated, they must still report for duty,” said Andrew Ansbro, president of the Uniformed Firefighters Association. “If they are told they cannot work, it will be the department and city of New York that sends them home. And it will be the department and the city of New York that has failed to protect the citizens of New York,” he added.

🇺🇸 President van de Uniformed Firefighters Association in New York, Andrew Ansbro :”Putting people out of work for making a personal health choice is something that we can never accept.” pic.twitter.com/87gQ7FdTcz

According to Ansbro, firefighters who have put their lives on the line during the pandemic feel “insulted” by de Blasio’s order, and New Yorkers will be the ones to suffer if the mayor carries out his threat.

“Fires are going to burn longer. Heart attack victims are going to be laying on the floor longer,” Ansbro told Fox News Radio.

“People in stuck elevators are going to be stuck there for hours if not days.” (h/t Summit News)

Ansbro also predicted that 30 to 40% of firehouses in NYC will be closed down if the mandate remains, as up to 45% of the workforce remains unvaccinated.

“On Friday, when they’re tallying the numbers of who complied and who didn’t, they’re going to be faced with a stark reality that they’re going to have to close firehouses down,” he said, adding “The mayor is going to be faced with either sending us home or sticking to his guns,” Ansbro continued, adding “And his guns are going to get New York City residents killed.”

NYPD loses bid to halt mandate

Meanwhile, a Staten Island Judge denied the Police Benevolent Association’s bid to temporarily halt the implementation of the city’s vaccine mandate set to take effect Nov. 1, according to CBS News.

The largest police union in the city had argued that de Blasio’s policy does not make clear their policy on potential exceptions, including for medical or religious reasons, and does not allow unvaccinated cops enough time to apply for said potential exemptions – which were required to be submitted just one week after the mandate was announced.

“Today’s ruling sets the city up for a real crisis. The haphazard rollout of this mandate has created chaos in the NYPD,” said PBA President Patrick J. Lynch in a statement. “City Hall has given no reason that a vaccine mandate with a weekly testing option is no longer enough to protect police officers and the public, especially while the number of COVID-19 cases continues to fall.”

The union plans to appeal, calling the mandate “arbitrary and capricious” in court documents.

The policy requires police officers, firefighters and other municipal workers get at least their first dose of the COVID-19 vaccine by Friday or be placed on unpaid leave. Correctional officers on Rikers Island — a New York City prison that has been grappling with staffing shortages and unsafe conditions — will be subject to the mandate on December 1.

The NYPD’s vaccination rate has lagged behind the rest of the city — as of Tuesday, the NYPD’s vaccination rate is 73%, compared with the 78.2% of adults who have been vaccinated in New York City. The PBA, which represents over 24,000 current NYPD officers, contends that getting the vaccine is a personal medical decision.

The NYPD has about 36,000 officers and about 19,000 civilian staff employees. -CBS News

We noticed nobody’s leading with the natural immunity argument, considering that thousands of NYPD officers have recovered from Covid-19.

Years (and years) ago, I was an unskilled 17- year-old who needed a job. So I drove out to a “foundry” (a factory that makes things out of molten metal) on the edge of town and asked if they needed any more workers. They said yes, hired me on the spot, and enrolled me in the local United Steelworkers union.

The work was hard, the conditions dirty and sometimes scary, but I made adult money and got to know men (it was all men) who supported their families with that single 8-hour-a-day job.

We even went on strike once. The union rep called each of us one evening and told us not to show up until further notice. After about a week, having gotten some of what they wanted, they called us back in. Very civilized and unremarkable, completely normal for the time and place.

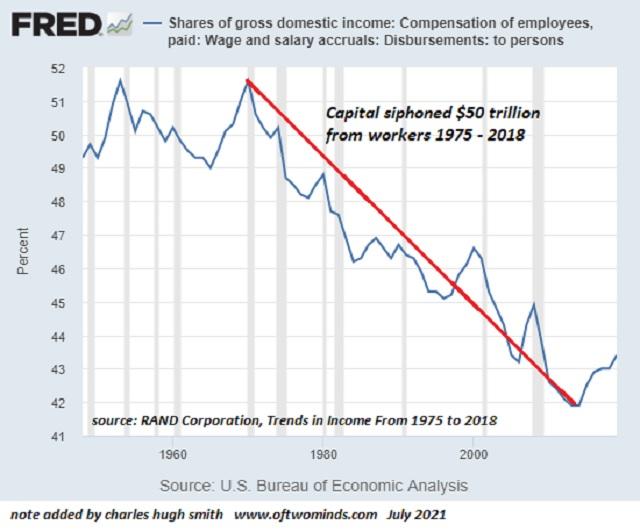

Then the whole concept of striking as a collective bargaining strategy disappeared. Factories began moving to China or Mexico, and the kinds of people who worked in foundries or assembly plants lost the power to negotiate with their bosses. No longer able to support families on one salary, they took ever crappier jobs, and – even with multiple family members working — fell from lower-middle-class to working poor. As a group, their share of national income crashed.

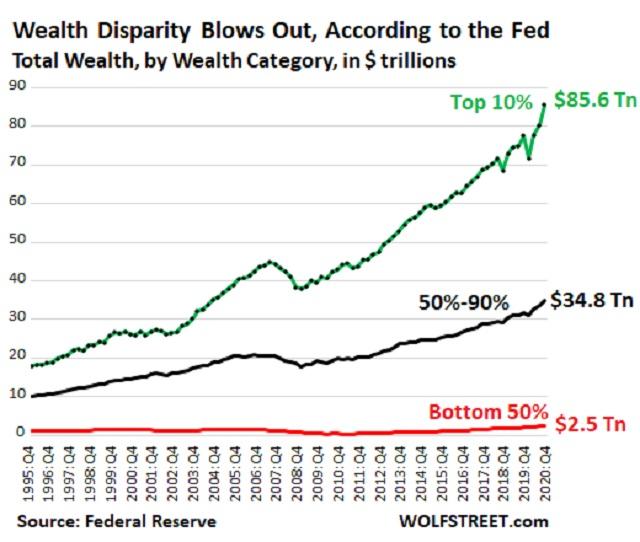

Meanwhile, the people who run those foreign factories — along with the bankers who structure the off-shoring deals and the politicians who enact free trade laws in return for generous campaign contributions — have done considerably better, rolling their ever-higher incomes into ever-growing stock, bond, and real estate portfolios. Today the richest 10% own the vast bulk of national wealth.

The Pendulum Swings Back

If this kind of trend seems unsustainable in a world where the 90% outnumbers the 10% (that is, in any world), well, it clearly is. There’s a limit to how rapacious an aristocracy can become before the pendulum starts swinging back towards the serfs.

(Reuters) – Thousands of workers remain on strike across the United States demanding higher pay and better conditions despite Hollywood make-up artists and camera operators reaching a deal over the weekend to avoid a walkout, and the tight jobs market has only emboldened them.

Kevin Bradshaw is an employee at Kellogg Co’s (K.N) cereal plant in Memphis, Tennessee, where most of North America’s Frosted Flakes are made. He feels anything but great about cuts to healthcare coverage,

retirement benefits and vacation time that union officials say the company is pushing for from about 1,400 workers on strike since Oct. 5 at plants in Michigan, Nebraska, Pennsylvania and Tennessee.

“Enough is enough,” said Bradshaw, vice president of Bakery, Confectionary, Tobacco Workers and Grain Millers International Union Local 252G at the Memphis plant. “We can’t afford to keep giving away things to a company that financially has made record-breaking returns.”

Some 60,000 behind-the-scenes workers on movies and TV shows on Saturday avoided joining the Kellogg strikers, but the near-walkout was the latest demonstration of force by union members who say they are fed up with meager or no raises and other givebacks. Kellogg officials could not be reached for comment but have said the company’s compensation is among the industry’s best.

So far, at least 176 strikes have been launched this year, including 17 in October, according to Cornell University’s Labor Action Tracker.

“Workers are on strike for a better deal and a better life,” Liz Shuler, president of the AFL-CIO, the nation’s biggest labor federation, said last week at a SABEW journalism conference.

“The pandemic really did lay bare the inequities of our system and working people are refusing to return to crappy jobs that put their health at risk,” she added, noting that the term #Striketober was trending on Twitter.

“We have entered a new era in labor relations,” said Harley Shaiken, professor emeritus of labor at the University of California Berkeley. “Workers feel they’re in the driver’s seat and there’s plenty of lost ground to make up.”

Financial Earthquake

This long-overdue wealth rebalancing will change a lot of things, including:

Rising inflation and monetary policy tightening. When stocks, bonds and real estate go up, the Federal Reserve doesn’t count that as inflation. But when wages rise, the Fed finds that alarming. So expect the trend towards higher wages to generate scary CPI numbers which in turn lead the Fed to at least try to raise interest rates.

Near-term financial instability. Higher interest rates are good for retirees and savers who earn more money on their bank accounts and money market funds, but bad for the stocks, bonds and real estate that now dominate the economy. So expect the financial assets that account for the bulk of the 10%’s wealth to be “repriced” via bear markets.

Easy money ever after. Crashing financial assets would wipe out big parts of the global financial system, which the aristocracy will find completely unacceptable. So expect the Fed – as it has in every crisis since the 1990s – to reverse course and go back to aggressive monetary stimulus. Whether this “works” remains to be seen. One of these times it won’t. But so far, Fed capitulation has always been good for safe haven assets like gold and silver, making the investment implications pretty obvious.

The Sixth Circuit is considering a very interesting gun case; unfortunately, I haven’t been following it closely, largely because it’s a technical statutory and regulatory case rather than a Second Amendment case—but Prof. Robert Leider (George Mason), who guest-blogged here on a different subject a few months ago, has been, and kindly offered this analysis:

In gun control debates, the Second Amendment usually takes center stage. But more mundane questions of statutory interpretation and administrative law can have more impact on gun owners.

On Tuesday, the U.S. Court of Appeals for the Sixth Circuit heard oral argument in one such case, Gun Owners of America, Inc. v. Department of Justice. The appeal relates to a March 3, 2020 declaration by the Bureau of Alcohol, Tobacco, Firearms, and Explosives (ATF) that Michigan’s concealed pistol license holders are no longer exempt from the national instant background check before the sale of a firearm because the Michigan State Police do not adequately research previous criminal convictions to determine whether a license applicant is prohibited from possessing a firearm. (ATF also undertook a similar action against Alabama pistol permit holders.)

Under the Brady Handgun Violence Protection Act, a federal firearms licensee (e.g., a gun store) must initiate a background check through the National Instant Check System before transferring a firearm. The law contains some exceptions, the most important of which is that a licensee may transfer a firearm to a person who has a permit that “was issued not more than 5 years earlier by the State in which the transfer is to take place” if that permit “allows such other person to possess or acquire a firearm” and “the law of the State provides that such a permit is to be issued only after an authorized government official has verified that the information available to such official does not indicate that possession of a firearm by such other person would be in violation of law.”

Traditionally, ATF has declared whether state permits qualify as instant check alternatives by publishing a “Permanent Brady Permit Chart” online and in a “Public Safety Advisory” to a state’s federal firearm licensees. In regulating through these informal mechanisms, ATF is doing one of two things, and both are procedurally problematic under the Administrative Procedure Act.

The first possibility is that despite ATF’s portrayal of the letters and permit charts as binding, they actually constitute non-binding sub-regulatory guidance from ATF to Federal Firearm Licensees. If that is the case, Michigan gun stores could just ignore ATF’s letter and continue accepting Michigan concealed pistol licensees as alternatives if they were certain that the licenses met the requirements of the Brady Act.

The second possibility—what ATF is likely doing—is issuing binding rules (or conducting binding adjudication) without public notice and comment and without the opportunity of affected stakeholders to participate. ATF’s letter, which announces “an important change to the procedure [federal firearms licensees] must follow to comply with the Brady [law],” suggests that when ATF determines that a permit does not qualify, ATF considers its determination as legally binding. If so, ATF’s determination is “one by which rights or obligations have been determined, or from which legal consequences will flow.”

Yet, before making changes to the Brady Permit Chart, ATF does not engage in notice and comment, nor does it engage in adjudication in which federal firearms licensees and permit holders—the affected stakeholders—may participate. Regardless of the merits of ATF’s actions, ATF is flouting the Administrative Procedure Act, and I was surprised that the Sixth Circuit panel did not press the government on this issue.

Two other major issues came up during oral argument that deserve further comment.

Standing: Why ATF’s Actions Have Significant Real-World Impact

The Sixth Circuit is apparently struggling with whether the plaintiffs have standing under Article III. Although the federal government has revoked the federal legal effect of their state-issued firearm licenses, the plaintiffs have another ready alternative to purchase firearms by submitting to the federal instant check system. The government contends that submission to the instant check does not create sufficient real-world injury to constitute injury-in-fact.

Here, the plaintiffs have unnecessarily convoluted the standing question by not articulating to the court the practical significance of ATF’s revocation. The use of a license as a substitute for the instant background check confers two important benefits upon license holders. First, it prevents the possibility that a gun purchaser will face significant delays in acquiring a firearm. About 10% of “instant” checks are not actually instant, and just under 1% take longer than three business days to resolve. Once a check is initiated, federal law permits the firearm to be transferred after three business days have elapsed. But that means individuals could still face delays of up to five days before they can take possession of their firearm. Those delays may not be a significant burden if the gun store is local. But if a person is traveling a substantial distance to a gun store or gun show, that delay could require a second, long trip to retrieve the firearm. When individuals seek to purchase a firearm, having a permit removes all uncertainty about the transaction being delayed.

Second, the permit allows individuals to engage in intrastate mail-order firearm sales. In response to the assassinations of John F. Kennedy and Martin Luther King, Jr., Congress banned the interstate mail-order sale of firearms in 1968. But Congress allowed intrastate mail-order sales to continue if allowed by state law, and there has been renewed interest in intrastate mail-order sales because the coronavirus pandemic has limited access to gun stores.

In 1993, the Brady Act effectively stopped most intrastate mail-order sales because the Act required individuals to present photo identification before the gun store may initiate the instant check. When an individual has a permit exempting the person from the Brady Act’s instant check requirement, however, then the Brady Act’s requirement to provide photo identification at the gun store also does not apply. Instead, the purchaser may submit a Firearm Transaction Record (Form 4473) by mail along with a copy of their permit. The gun store may then transfer the firearm by mail after contacting the purchaser’s local law enforcement agency and observing a lengthy waiting period. When ATF determines that a state’s permit does not exempt the permit holder from the Brady law, ATF also cuts off the ability to use that permit to facilitate a mail-order sale.

Should the Court Defer to the Michigan Attorney General’s Understanding of State Law?

Michigan law (§ 28.425b(6)) provides that the “department of state police shall verify” whether a person is qualified under law to receive the license by using information accessible “through the law enforcement information network and the national instant criminal background check system.” When the Michigan State Police receives ambiguous criminal history records, they have refused to conduct exhaustive investigations into whether the applicant is prohibited from having a license. The refusal to conduct such investigations prompted ATF’s withdrawal of concealed pistol licenses as an alternative to the instant check system. During oral argument, the panel (particularly Judge Sutton) seemed troubled that ATF was deferring to some unnamed person in the state police to authoritatively determine what Michigan law requires the state police to do when conducting a background check. He suggested asking the Michigan Attorney General for her views. In this case, however, deferring to the Attorney General’s understanding of the law would be a mistake.

The Michigan Attorney General should not be viewed as a neutral, authoritative source to determine the meaning of Michigan law. The Michigan Attorney General is a strong proponent of gun control. Gun control groups seek to narrow the exceptions of the federal instant check system because of the possibility that information could grow stale between the time that the permit was issued and when a person seeks to buy a gun. In this case, the Michigan Attorney General is incentivized to opine that Michigan law does not require the state police to conduct exhaustive background checks to prevent concealed pistol licenses from being acceptable alternatives to the federal background check.

Federal courts sometimes face difficult state-law interpretive questions. But no less than in federal-law cases, a federal court’s job is to interpret state law, not to try to delegate its task to a state executive official. That is particularly true in this case, in which the Attorney General would not be a neutral arbiter of state law. If the panel insists on having the state interpret its own laws, the more appropriate course of action would be to certify the question to the Michigan Supreme Court.

More broadly, this case raises difficult questions concerning what properly constitutes “the law of the State.” The federal Gun Control Act exempts state permits if “the law of the State” requires an adequate background check. What is the “law of the State”? The statute? The statute as implemented by binding executive regulations? Or does the real-world practice of state officials constitute “the law of the State,” even if that practice violates state statutes?

Here, I think the statutes should have primacy over executive practice. The plain statutory text of Michigan law indicates its concealed pistol licenses should qualify as alternatives to the national instant check system. Although executive agencies may engage in unlawful behavior when they implement the law, neither they, nor the Attorney General, has the power to rewrite the law passed by the legislature. And the Brady Act contains no language disqualifying all state permits just because some licensing official implements the law in a faulty manner.

from Latest – Reason.com https://ift.tt/3Et6Qpc

via IFTTT

Kao Lee Yang, a Hmong American neuroscience PhD student, was recently nominated for a prestigious fellowship for students who are members of “groups historically excluded from and underrepresented in science.” The fellowship committee determined that as an Asian American, Yang was not from an “underrepresented” group. The committee therefore refused to even consider her application.

Yang took to Twitter to vent: “While some Asian Americans are academically successful, others like the Hmong are underrepresented in STEM and academia in general… name me just one Hmong American woman you know who is a neuroscientist. I would love to connect with her if she is out there.” She added, “I am an example of the consequences resulting from the continued practice of grouping people with East/Southeast/South Asian heritages underneath the ‘Asian American’ umbrella.”

Yang blamed her predicament on the “model minority myth.” Her ire would have been better targeted at the federal Department of Education. For over forty years, its Office of Civil Rights has required educational institutions to collect and report demographic data about “Asian Americans,” with no differentiation among the many national-origin groups. The educational establishment, in turn, has grown used to treating Asian Americans as a uniform racial group.

Of course, one can object that no minorities should be given special consideration for fellowship. Or that only African Americans should be given such consideration, but not groups composed mostly of post-1965 immigrants and their descendants. But it’s pretty hard to argue that an Argentine American of Italian descent should be eligible for a minority fellowship because she is “Hispanic,” but a Hmong American should not because she is “Asian.”

You can read more about how our modern racial and ethnic classifications developed in my recently published article, The Modern American Law of Race, or you can wait for my book, Classified: The Untold Story of Racial Classifications in America, forthcoming July 2021.

from Latest – Reason.com https://ift.tt/3Bicysg

via IFTTT

Democrats appear likely to abandon plans to include an expensive new federal entitlement program—paid family leave—as they try to trim the overall cost of President Joe Biden’s “Build Back Better” plan proposal.

Biden’s plan called for a federal paid leave program that would replace up to 85 percent of a worker’s pay (with that percentage falling for higher-paid workers) for up to 12 weeks per year. Workers could access the paid leave program if they were having a baby, taking care of an elderly or sick relative, or recovering from a serious illness of their own.

There has not been an official Congressional Budget Office assessment of how much the paid leave program would cost, but a similar stand-alone proposal drawn up by Democrats in 2019 carried a $547 billion price tag over 10 years. That made the paid leave proposal one of the more expensive heaves in Biden’s proposal. Even after Democrats tried to trim the benefits by reducing the timeframe to just four weeks instead of 12, the price tag was still over $300 billion, Politicoreported earlier this month.

Ultimately, the high cost is what seems to have doomed that aspect of Biden’s plan.

???? Senate Democrats have decided to drop paid family and medical leave, a key cornerstone of Joe Biden’s presidential campaign, from their mammoth social spending package Wednesday after attempts to drastically pare it down were deemed insufficient, three sources tell me.

The problem facing Democrats right now is rooted in basic budget math of the kind that usually gets ignored in Washington. Sen. Joe Manchin (D–W.Va.) has said he is worried about the trajectory of the national debt and will not support a social spending plan that relies on more borrowing. Without his support, Democrats do not have a majority in the Senate. So the plan has to include enough revenue offsets to pay for the proposed new spending—or, at least, pay for them sufficiently to satisfy Manchin.

But Democrats keep backing away from the sorts of large-scale tax increases necessary to pay for a $3.5 trillion spending plan—like the proposed “billionaire tax” on unrealized capital gains that reportedly got axed on Wednesday. As Reason’s Peter Suderman explains, that tax was a terrible idea (and maybe even an unconstitutional one), but discarding it reveals something about the underlying negotiations over Biden’s plan:

It is certainly possible that some deal will still be negotiated, that some other tax mechanism or mechanisms will be found that can raise sufficient revenue to make the tax-and-spending math work. But even if something eventually passes, Democrats’ down-to-the-wire struggle highlights the inherent political difficulty of raising taxes, even within a party that is nominally devoted to the idea that higher taxes, especially on the rich and well-off, are a popular political good. And the reason for that difficulty is not the intransigence of tax-hating Republicans, or the existence of the Senate filibuster, but the fact that Democrats are having trouble mustering sufficient support from elected Democrats.

So, to review: Manchin won’t vote for more borrowing. Democrats can’t find the votes for big tax increases. The only remaining option, at that point, is to start hacking away at the spending side of the legislation. Which is exactly what Democrats are doing, and that’s why paid leave appears to be heading for the cutting committee room floor.

Manchin on Wednesday stressed that his opposition to new benefits was rooted in concern for the country’s long-term fiscal status, noting in comments to reporters both the nearly $29 trillion national debt and the looming insolvency of the trust funds for Social Security and Medicare. “In good conscience, I have a hard time increasing benefits—which, all of us can agree we’d love to have this and love to have that—when you can’t even take care of what you have,” Manchin said.

Manchin talks to us on billionaires' tax: “I don’t like the connotation that we are targeting different people"

On Medicare expansion: "I have hard time increasing" benefits

On paid leave, Manchin said given the debt: “It doesn’t make sense to me. … I just can’t do it" pic.twitter.com/mMZfW20Gk5

Here’s the real kicker for progressives: A paid leave proposal, expensive though it may be, is politically popular even among Republicans. If Sen. Kirsten Gillibrand (D–N.Y.), who has been championing the policy, were able to bring a stand-alone bill for a paid leave program to the Senate floor (along with a mechanism to pay it), it is at least theoretically possible that such a bill would pass. Sure, there would be negotiations, amendments, and arguments over it. Legislators would have to legislate, in other words. But there are almost certainly 60 votes in the Senate for some form of federal paid leave program.

Instead, there will likely be no federal paid leave program. And that’s at least in part due to the fact that Democrats are trying to cram all their big ideas into a single piece of legislation, rather than trying to find agreement for individual items and moving them one at a time.

Congress is gradually moving toward having only one bill per year, with everything stuffed into it, negotiated by just a few congressional leaders, completely behind closed doors, with no floor amendments permitted.

Where does that leave Biden’s bill on the eve of the latest deadline for a Senate vote that seems nowhere close to happening? The president is supposed to meet with congressional Democrats on Thursday to present a new framework that The Washington Post promises will “win the support of all Democrats.” Meanwhile, The New York Times says the revamped plan “is likely to leave some critical issues unresolved, including how to pay for it.”

So, yeah.

One of the cardinal rules of politics—and political media, especially—is that nothing is ever as bad (or as good) as it seems. These are professions where overreacting is a way of life. That said, here’s something White House Chief of Staff (and longtime Biden confidant) Ron Klain retweeted on Wednesday night. Judge for yourself how things are going right now over at 1600 Pennsylvania Ave.

Normal stuff, just the White House Chief of Staff retweeting a description of the emerging BBB package as a "grab-bag of ill-designed, underfunded programs that are all set to self-destruct during the second Trump administration" pic.twitter.com/LcVvIJlUAZ

Sen. Tom Cotton (R–Ark.) penned a wildly inaccurate piece for National Review defending qualified immunity. Reason‘s Billy Binion helpfully offers some corrections:

Misconception #1: Qualified immunity is "essential to effective policing."

QI allows gov't officials to violate your rights with little fear of liability in civil court. To say it's essential is to say that cops need to be able to violate your rights to do their jobs. /2 pic.twitter.com/M6czw0sOZJ

How to eat for an entire year on $150—as long as your stomach can handle it:

It all started on the first day of his internship in 2014, when Dylan noticed the rollicking coasters of Six Flags Magic Mountain from the windows of his new office. Fresh out of college and something of a coaster-fanatic already, Dylan was perusing the options for Six Flags’ annual pass when he stumbled upon what might be the deal of his lifetime — for a one-time fee of $150, he could eat two meals a day, every day at the park for an entire year. Since his office was just a five-minute drive away, it was a no-brainer.

“That entire first year, I don’t think I ever went to the grocery store,” he says. “I timed it so I was able to go there during my lunch break, go back to work, then stop back for dinner on my way home.”

Over the course of seven years of eating at the Six Flags food court, Dylan claims he saved enough to pay off his student loans, get married, and buy a house. Read the whole saga in MEL Magazine.

• Hong Kong approved a new censorship law prohibiting content that Chinese officials believe “might endanger national security.”

• America is in desperate need of more workers, but federal officials wasted at least 400,000 visa slots during the fiscal year that ended in September.

• Hall of Fame quarterback Brett Favre repaid $600,000 in welfare he improperly received from Mississippi.

• You’re gonna need a bigger….whatever you keep scorpions in?

As if small scorpions weren’t scary enough, scientists have discovered an ancient fossil of a sea scorpion that was 16 times larger than the present-day scorpion—almost as big as a dog!