“Bumper Tables” For Socially-Distant Dining Appear In Maryland Tyler Durden

Mon, 05/18/2020 – 21:05

Vistors are headed back to Ocean City, Maryland’s beach and boardwalk after Gov. Larry Hogan relaxes the stay-at-home order. At one restaurant over the weekend, a post-corona world was recognized with what is being called a socially distant dining experience, reported The Baltimore Sun.

Shaped like a giant donut with an outer perimeter lined with an inner tube, the socially distant tables were custom made for Fish Tales waterfront restaurant. The restaurant posted a Facebook Live video of employees unloading the new tables from a large box truck.

“It’s like a bumper boat, but it’s a table,” Fish Tales owner Shawn Harmon told Delmarva Daily Times, referring to the design of the table, which was created by a Baltimore-based design firm.

A customer stands in the center of the table surrounded by a rubber barrier that keeps patrons about six-feet apart. The tables have wheels and allow patrons to move around the restaurant.

Several months of lockdowns have led to restaurants and bars shuttering operations across Maryland — except for carryout and delivery service. The state inched into phase one of its Roadmap to Recovery, dining in could become a reality later this year, that is if a second virus wave doesn’t materialize.

Fish Tales is providing curbside and carryout service at the moment, with preparations to reopen its restaurant and bar when restrictions are lifted.

This restaurant in Maryland intends to use bumper tables to keep customers six feet apart once it begins to take seated diners. pic.twitter.com/ReCLbzcowF

Erin Cermak, the owner of Revolution, the firm responsible for designing and producing the tables, said: “we’re an event company, and events have taken a hard hit, so we’ve been trying to figure out a way that events and things can still happen.”

She said they’ve gotten an “incredible reaction” so far and are in discussions with other restaurants.

Hogan made the announcement last week to relax stay-at-home orders and reopen the state. Though reopening the state will not return Maryland nor any other part of the country back to 2019 growth levels. Businesses and households have been finally damaged because of lockdowns.

We noted last week, McDonald’s opened a prototype restaurant outfitted with a new social distancing layout. The move is to test new safety measures for guests and employees that will limit the spread of the virus once lockdowns are relaxed.

The restaurant industry will be severely impacted and might not return to 2019 activity levels for years.

via ZeroHedge News https://ift.tt/2WFGwW2 Tyler Durden

Nasdaq Imposes Restrictions On Chinese IPOs Tyler Durden

Mon, 05/18/2020 – 21:00

In a move that anyone who has ever invested in a Chinese fraud stock (which one can argue are most of them) will argue is long overdue, late on Monday Reuters reported that the Nasdaq is set to unveil new restrictions on initial public offerings, in a move that will make it more difficult for some Chinese companies to debut on its stock exchange.

While Nasdaq will not cite Chinese companies specifically in the changes, according to Reuters, the move is being driven by concerns about some of the Chinese IPO hopefuls’ lack of accounting transparency and close ties to powerful insiders.

And since the Nasdaq move, which may well be prompted by legitimate widespread concerns about shady Chinese accounting, comes just days after the Trump administration barred a government retirement fund from investing in Chinese equities, it will be seen by Beijing as another political intervention in soft capital controls imposed by the US vis-a-vis Chinese equities, inviting further retaliation from China against this “latest flashpoint in the financial relationship between the world’s two largest economies.”

Nasdaq also unveiled some restrictions on listings last year, seeking to curb IPOs by small Chinese companies. Their shares often trade thinly because most stay in the hands of a few insiders. Their low liquidity makes them unattractive to many large institutional investors, to whom Nasdaq is seeking to cater.

Whatever the reason behind the move, it has been a long time coming, considering the ease with which countless Chinese frauds are allowed to list in the US and soak up capital of gullible US investors. Last month, Luckin Coffee which had a U.S. IPO in early 2019, announced that an internal investigation had shown its chief operating officer and other employees fabricated sales deals.

The new rules will require companies from some countries, including China, to raise $25 million in their IPO or, alternatively, at least a quarter of their post-listing market capitalization, the Reuters sources said. This would represent the first time Nasdaq has put a minimum value on the size of IPOs. The change would have prevented several Chinese companies currently listed on the Nasdaq from going public. Out of 155 Chinese companies that listed on Nasdaq since 2000, 40 grossed IPO proceeds below $25 million, according to Refinitiv data.

And while it was not immediately clear how many of these IPOs were Chinese, Reuters notes that Chinese firms have historically pursued such small IPOs because they allow their founders and backers to cash out, rewarding them with U.S. dollars they cannot easily access because of China’s capital controls. And they have US bagholders, and lax exchange listing standards to thank. At the same time, these newly IPOed frauds would also use their Nasdaq-listed status to convince lenders in China to fund them and often get subsidies from Chinese local authorities for becoming publicly traded.

Finally, the proposed rules will also require auditing firms to ensure that their international franchises comply with global standards, and Nasdaq will also inspect the auditing of small U.S. firms that audit the accounts of Chinese IPO hopefuls, the sources added.

The news of the restriction hit S&P futures which slid to session lows on a day when there was no talk of trade war, and instead the market was obsessing over what in retrospect will end up being one giant “Made in the US” bait-and-switch by Moderna, which sold $1.25BN in stock after soaring earlier in the day on news of a “successful” Phase 1 coronavirus vaccine trial which involved eight “young and healthy” people.

Meanwhile, ahead of the Nasdaq news and perhaps sensing what was coming, China has been urging domestic companies to look at listing in London, Reuters also reported earlier in the day, as the country aims to revive deals under a Stock Connect scheme and strengthen overseas ties in the wake of the coronavirus crisis.

The Shanghai-London Stock Connect scheme, which began operating last year, aims to build links between Britain and China, help Chinese companies expand their investor base and give mainland investors access to UK-listed companies.

The original plan was for several companies to take part in the scheme in the first couple of years, but so far only one company — Huatai Securities — made the trip from Shanghai to London last June.

But now Chinese authorities have given the go-ahead for China Pacific Insurance and SDIC Power to move ahead with their London-listing plans, the sources said, after both deals were halted last year.

They also gave the nod to China Yangtze Power (600900.SS) to begin preparations for a secondary listing on the London Stock Exchange, the sources said, speaking on condition of anonymity as the matter is confidential.

The sources, including officials from banks, government and exchanges, said that the aim was to push for a resumption of listings under the Stock Connect scheme as China seeks to improve ties with the outside world and help to fund its post-lockdown recovery. “In the second half of this year, we could see one or maybe two Chinese companies list in London,” said one of the sources, who is closely involved in the process.

“China is among the first countries to come out of lockdown, and is keen to get back on track with plans to improve trade relations with the UK,” he added, by which he of course meant finding more gullible, naive investors to part with their money after investing in the next Chinese Luckin-like fraud, especially if the US window is closing.

via ZeroHedge News https://ift.tt/2zS33pr Tyler Durden

Various media outlets are struggling with recent polls that not only show President Trump at the same popularity as this time last year but actually rising in states like Ohio. When one poll found him leading by 7 points in battleground states, John King cautioned viewers to “be careful not to invest too much in any one poll” especially amid the coronavirus.

It was a CNN poll and, while Biden leads in other polls, it is not unique.

The media seems honestly confused. It was not supposed to work this way. With unrelentingly negative coverage of an impeachment, a pandemic, and an economic collapse, voters were supposed to be angry. There is even a psychological model for such social cognitive learning or conditioning called “Bobo the Clown” and, while this experiment by psychologist Albert Bandura, these polls suggest that conditioning does not work nearly as well in politics as it does on playgrounds.

In 1961, Bandura used a goofy inflatable clown named Bobo and had children watch adults as they acted aggressively toward it. Soon the children followed the adults’ example and beat the clown. Conversely, when children watched the clown being treated without aggression, they were less aggressive toward it.

For many voters, Donald Trump and Joe Biden are not so funny clowns, and voters are being conditioned by some in the media to treat one aggressively and the other not aggressively. It is not the first attempt at media conditioning: In 2016, when every poll indicated that voters wanted outsider candidates, Democratic leaders pushed through one of the two most unpopular presidential candidates in history, Hillary Clinton.

She was beaten by the other most unpopular figure on the Republican side, Trump. Yet, after largely positive treatment of Clinton and correspondingly negative coverage of Trump, the election results stunned experts who predicted an easy win for Clinton — and why not? Voters had been exposed to unyielding, continual media conditioning against Trump.

The conclusion of the media today appears to be that the scathing treatment in 2016 was not aggressive enough. Trump is routinely called an actual clown by some in the media. More importantly, there are now consistent attacks on Trump supporters. Washington Post “conservative columnist” Jennifer Rubin has declared that Trump supporters as a whole are racists. That common stereotyping of Trump supporters is uncontested, even as the media objects to Trump’s generalizations about other groups.

Columnist Leonard Pitts wrote a recent column entitled, “No, it’s not the economy, stupid. Trump supporters fear a black and brown America.” The narrative has moved beyond Clinton’s description of Trump supporters as a “basket of deplorables” to now portraying all Trump supporters as open racists. “Make America Great Again” hats are denounced by academics as the symbol of “modern day hitlerjugend” and hate speech.

It is all part of media-cognitive learning, and it is working in a curious way. Recent polls show Trump at the exact same spot as he was last year, with roughly 43 percent support. In Ohio he actually is ahead by 3 percentage points in a survey from Emerson College and Nexstar Media; he and Biden are in a statistical dead heat in Wisconsin. In other words, as in 2016, the media campaign is forcing Trump supporters into the closet, but not away from Trump.

Meanwhile, the media has been working hard at non-aggressive treatment of Biden. His frequent gaffes are quickly dismissed; when he was accused of sexual assault, the media reluctantly noted the story. Even when Biden recently espoused a conspiracy theory that Trump was going to halt the November election, the media called it a “prediction” and ignored that it was based on a fundamental misunderstanding of the Constitution.

At the end of last year, the Media Research Center found that network evening news was 96 percent negative against Trump. The drumbeat has only increased with impeachment and pandemic coverage this year. Despite such saturated messaging, polls show that the number of voters expressing strong “enthusiasm” for Biden is wallowing at just 24 percent, while Trump remains at 53 percent. Biden is just 3 points ahead of Trump in the most recent polls, actually behind where Clinton was in 2016. The reason may be that the anti-Trump narrative is so overwhelming that voters feel they are being played like the kids in the Bandura experiment.

Consider again the recent attack of the Post’s Rubin on most Republicans. Rubin lashed out at the immigration freeze ordered by Trump during the pandemic; however, she was not satisfied with denouncing the policy as a political stunt to appeal to the unemployed. She declared:

“No doubt Trump’s base is primarily motivated by racism. This is why Trump does this.”

The statement captures the accepted, unhinged bias against all Trump supporters in the mainstream media.

I did not vote for Trump, and I have regularly criticized him in columns and blog posts. However, I have watched the stereotyping of Trump supporters at media conferences for years. It suggests that roughly 63 million people in this country who voted for Trump in 2016 are knuckle-dragging racists. It ignores the fact that Hillary Clinton had record negative polling before the nomination and was widely viewed as pathologically inauthentic.

Recently, polls show 85 percent of Republicans support Trump. Thus, according to Rubin, 85 percent of Republicans (and roughly 10 percent of Democrats and 47 percent of independents) — in other words, almost half of America — are primarily motivated by racism. Does that track with any sense of reality? There are a host of reasons for these voters to support Trump other than racism.

What is not being discussed much in the media is that people might have non-racist reasons for supporting Trump. The fact is that Trump has a curious record: He has been repeatedly (and correctly) chastised for untrue statements, and yet he has one of the best records for actually keeping campaign promises — the crackdown on immigration, building of the border wall, pro-life policies and appointments, selection of conservative jurists, tax cuts, regulation rollbacks, opening up areas to oil drilling.

These and many other aspects of his administration are the most controversial but also are the long-held wish list of conservatives going back to Ronald Reagan. Indeed, while 85 percent of Republicans support Trump, a new poll shows that 23 percent would like to see someone else as their nominee. Yet, Rubin and others simply dismiss all Trump supporters as monolithic, pathological racists.

Thus, polls indicate that the unending attacks on Trump and his supporters in the media are not conditioning but, instead, are repelling voters. They are fulfilling his narrative that voters cannot trust the media. Many voters may still view both Trump and Biden as over-inflated clowns, but they resent being continually conditioned to hit one clown and hug the other.

Indeed, if Trump is reelected, he may have the media to thank.

via ZeroHedge News https://ift.tt/2zLqWzg Tyler Durden

Oil prices have surged to two-month highs on growing signs of a rebound in oil demand, as the easing of lockdowns spread worldwide. At its peak in April, global lockdown measures affected around 3.9 billion people. But an estimated 3.7 billion people are now living in areas that are experiencing some version of a “reopening,” according to an estimate from Raymond James.

Data from China has stoked some bullishness in oil markets, although there are some mixed signals. Traffic is back in many Chinese cities, and there are early signs that China’s oil demand is rising back close to pre-pandemic levels around 13 million barrels per day (mb/d).

At the same time, a new coronavirus cluster in China suddenly sparked another lockdown measure. While Wuhan and other regions may be opening up, roughly 108 million people in Jilin province just went into lockdown. It’s a sign that the fight against COVID-19 will likely be frustrated by repeated flare ups in new cases, which may ultimately lead to renewed lockdowns.

But for now, the markets apparently want to focus on the positive. On the global vaccine front, there appears to be some progress. Moderna said on Monday that its vaccine has shown to be safe in humans and has also demonstrated promising results in stopping COVID-19. Meanwhile, AstraZeneca said it could have 30 million doses of its vaccine ready by September.

Financial equities rejoiced, with the Dow Jones up roughly 3.5 percent during midday trading. WTI surged past $30 per barrel, up at one point on Monday by more than 10 percent.

Massive supply cuts go even further in explaining the recent jump in prices. Oil traders view the implementation of the OPEC+ cuts favorably, with the 9.7 mb/d cuts phasing in swiftly. Part of the reason is that some oil producers, including Saudi Arabia, began having difficulty finding a home for its oil, so a portion of the cuts arguably became involuntary.

Meanwhile, weeks of catastrophically low oil prices ravaged North American oil producers over the past two months. Shut ins could reach 2 mb/d in the U.S. by June, and Canada could lose 1 mb/d.

But a reality check is in order. WTI at $30 per barrel is suddenly seen as “bullish,” but that price level is financially unsustainable for a vast swathe of global oil supply, including most of the U.S. shale complex.

Moreover, the physical oil market is not “out of the woods” just yet, according to Rystad Energy. “We still see a 13.7 million bpd implied liquids (crude, condensate, NGLs, others) stock builds in May-20,” the firm said in a statement. That is down by half from the peak of the glut (-26.7 mb/d in inventory builds in April), but a significant overhang remains.

Separately, Commerzbank argued that the oil market optimism may be running a little too far. “Despite all the euphoria, however, we believe that caution is still advisable: it will probably take some years before demand recovers to its pre-crisis level,” Commerzbank wrote on Monday.

U.S. Federal Reserve Chairman Jerome Powell warned that the American economy recovery could take until the end of 2021. “It could stretch through the end of next year. We really don’t know,” Powell said over the weekend. He noted that the economy might not return to normal simply because stay-at-home-orders are in the process of going away. “For the economy to fully recover people will have to be fully confident, and that may have to await the arrival of a vaccine,” Powell added.

In addition, the price rally may also be the result of speculative positioning – the physical market is trending towards rebalancing, but the rally can also be explained by overly exuberant speculative positioning. “Retail and institutional investors are also likely to have played a key part in the latest price rise. According to the CFTC, the latter expanded their net long positions in WTI on the NYMEX to around 352,000 contracts in the week to 12 May, putting them at their highest level since September 2018,” Commerzbank added. “Thus the positive trends (for the oil price) are largely expected and already priced in.”

The lockdowns are lifting, but there is nothing to suggest that the end of the pandemic is near, or that oil supply will remain shut in. “[T]here is significant downside risk related to two events, the resurgence in COVID-19 outbreaks, and deteriorating compliance to OPEC+ cuts as demand comes back,” Rystad warned.

via ZeroHedge News https://ift.tt/2ThvqVa Tyler Durden

Fearing An Imminent Top, Companies Flood The Market With Stock For Sale After The Close Tyler Durden

Mon, 05/18/2020 – 20:25

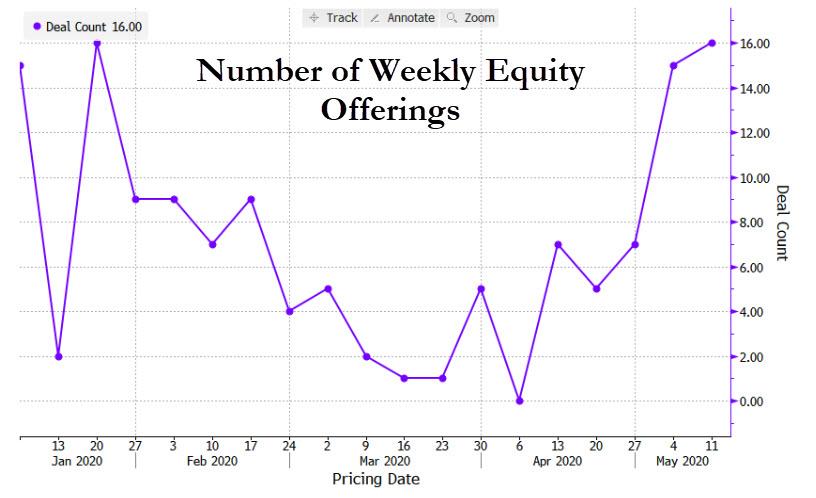

Last week was remarkable for the capital markets, not because the S&P did something crazy (it actually suffered its biggest weekly drop in months) but because the companies that comprise it appeared to make a collective decision that after its 30% rebound from the March 23 lows, that was as good as it gets and proceeded to flood the market with follow-on and secondary equity offerings.

As we reported before, in just the first three days of the week, public companies raised more cash from selling shares than in any week in eight years. According to Bloomberg calculations, investment banks conducted no less than 16 secondary offerings on U.S. exchanges in the Monday thru Wednesday interval in stocks such as Zillow, Equinix, MyoKardia, YETI Holdings, and Q2 Holdings Inc. Over that three-day interval, companies raised more than $17 billion from investors, the most since 2012, thanks largely to PNC selling $12.1 billion of its BlackRock shares in the second-largest offering since 2009. That made for the busiest week of 2020.

Buyers – mostly retail investors – have been undaunted by warnings from either Fed Chair Jerome Powell, who cautioned about unprecedented downside risk to the economy, from Goldman Sachs which we first reported said stocks could drop nearly 20% in the next three months, or by investing titans who say this is the most overbought market in history. No, these are retail investors who know better than even corporate management…

“Now’s the time to act. The rally is extremely fragile,” said Michael Purves, CEO of Tallbacken Capital Advisors, who spent 12 years advising companies on mergers and capital-raising. “When you’re a CFO or a board director of a company in a capital intensive industry, you raise money so that you don’t lose your job. That’s 100% the right thing to do now.”

More importantly, you raise money when you think the top is in so you don’t leave any on the table. Like now… because after last week’s torrid pace of equity offerings, at least thirteen equity offerings launched after the market closed Monday, the busiest evening of 2020 for such deals, as stocks that surged during the Covid-19 crisis thanks to a frenzy of retail buying, are now tapping the same retail investors for more cash, and follow on last week’s furious offering that raised more cash than in any week in eight years.

That said, unlike some prior share sales from distressed sectors, Bloomberg notes that almost all of Monday’s deals came from stocks that outperformed since the coronavirus began rattling U.S. markets in late February. Of the thirteen secondary offerings launched so far, all but two have outperformed the Nasdaq Composite Index since March 1.

Moderna for example, launched the largest of three stock offerings since going public in 2018 after Monday’s 20% rally capped off a more than 300% gain this year on very hasty speculation that the company’s Phase 1 trial which included 8 participants, was supposedly successful when it was, at best, noise. Fastly also sold shares after rising 69% since May 6, when it boosted its 2020 revenue forecast due to stay-at-home measures.

Below is a summary of the post-market launches of secondary offerings:

Avantor (AVTR) 45m shares, trades May 21

Bookrunners: Goldman Sachs, JPMorgan

Shares -7.0% post-market

Seller: Holders

Bellerophon (BLPH) Shares offered at $13 each

Bookrunner: Jefferies

Shares -15% post-market

Seller: Company

Cable One (CABO) $400m of shares, trades May 20

Bookrunners: JPMorgan, BoFA, Wells Fargo

Shares little changed post-market

Seller: Company

Carvana (CVNA) 5m shares at $93-$96

Bookrunners: Citi, Wells Fargo

Shares -4.8% post-market

Seller: Company

Clovis Oncology (CLVS) $85m of shares at $8.05-$8.50

Bookrunners: JPMorgan, BofA

Shares -6.9% post-market

Seller: Company

Fastly (FSLY) 6m shares, trades May 21

Bookrunners: Morgan Stanley, Citi, BofA, Credit Suisse, William Blair, Raymond James, Baird, Oppenheimer, Stifel, Craig- Hallum, DA Davidson

Shares -1.7% post-market

Seller: Company

Gamida Cell (GMDA) Shares offered at $4.50-$5.00

Bookrunners: Piper Sandler, Evercore Group, JMP

Shares -13% post-market

Seller: Company

Gossamer Bio (GOSS) Shares offered at $13.25- $13.75

At a time when the world is already being hit with major crisis after major crisis, our sun is behaving in ways that we have never seen before. For as long as records have been kept, the sun has never been quieter than it has been in 2019 and 2020, and as you will see below we are being warned that we have now entered “a very deep solar minimum”. Unfortunately, other very deep solar minimums throughout history have corresponded with brutally cold temperatures and horrific global famines, and of course this new solar minimum comes at a time when the United Nations is already warning that we are on the verge of “biblical” famines around the world. So we better hope that the sun wakes up soon, because the alternative is almost too horrifying to talk about.

Without the sun, life on Earth could not exist, and so the fact that it is behaving so weirdly right now should be big news.

Sadly, most mainstream news outlets are largely ignoring this story, but at least a few are covering it. The following comes from Forbes…

While we on Earth suffer from coronavirus, our star—the Sun—is having a lockdown all of its own. Spaceweather.com reports that already there have been 100 days in 2020 when our Sun has displayed zero sunspots.

That makes 2020 the second consecutive year of a record-setting low number of sunspots— which you can see (a complete absence of) here.

Our sun has gone into lockdown, which could cause freezing weather, earthquakes and famine, scientists say.

The sun is currently in a period of “solar minimum,” meaning activity on its surface has fallen dramatically.

Experts believe we are about to enter the deepest period of sunshine “recession” ever recorded as sunspots have virtually disappeared.

Yes, covering COVID-19 is important, but the fact that scientists are warning that we are potentially facing “freezing weather, earthquakes and famine” should be deeply alarming for all of us.

And since the mainstream media has been largely silent on this crisis, most Americans don’t even know that it exists.

Last year, there were no sunspots at all 77 percent of the time, and so far this year there have been no sunspots at all 76 percent of the time…

“This is a sign that solar minimum is underway,” reads SpaceWeather.com. “So far this year, the Sun has been blank 76% of the time, a rate surpassed only once before in the Space Age. Last year, 2019, the Sun was blank 77% of the time. Two consecutive years of record-setting spotlessness adds up to a very deep solar minimum, indeed.”

So why is this such a big deal?

Well, every once in a while a very deep solar minimum that lasts for several decades comes along, and when our planet has experienced such periods in the past the consequences have been quite dramatic.

For example, the New York Post is claiming that NASA scientists fear that we could potentially be facing “a repeat of the Dalton Minimum”…

NASA scientists fear it could be a repeat of the Dalton Minimum, which happened between 1790 and 1830 — leading to periods of brutal cold, crop loss, famine and powerful volcanic eruptions.

Temperatures plummeted by up to 2 degrees Celsius (3.6 degrees Fahrenheit) over 20 years, devastating the world’s food production.

Even worse would be a repeat of the Maunder Minimum which stretched from 1645 to 1715. It came as the globe was already in the midst of “the Little Ice Age”, and it caused harvest failures and famines all over the globe…

The Maunder Minimum is the most famous cold period of the Little Ice Age. Temperatures plummeted in Europe (Figs. 14.3–14.7), the growing season became shorter by more than a month, the number of snowy days increased from a few to 20–30, the ground froze to several feet, alpine glaciers advanced all over the world, glaciers in the Swiss Alps encroached on farms and buried villages, tree-lines in the Alps dropped, sea ports were blocked by sea ice that surrounded Iceland and Holland for about 20 miles, wine grape harvests diminished, and cereal grain harvests failed, leading to mass famines (Fagan, 2007). The Thames River and canals and rivers of the Netherlands froze over during the winter (Fig. 14.3). The population of Iceland decreased by about half. In parts of China, warm-weather crops that had been grown for centuries were abandoned. In North America, early European settlers experienced exceptionally severe winters.

Of course this would be an exceptionally bad time for such a cataclysmic climate shift, because African Swine Fever has already wiped out approximately one-fourth of all the pigs in the world, colossal armies of locusts the size of major cities are systematically wiping out crops across much of Africa, the Middle East and Asia, and fear of COVID-19 is greatly disrupting global food supply chains.

In fact, it is being reported that widespread shutdowns of meat processing facilities in the United States may force farmers to euthanize “as many as 10 million hogs by September”…

U.S. pork farmers may be forced to euthanize as many as 10 million hogs by September as a result of production-plant shutdowns brought on by the coronavirus pandemic, according to the National Pork Producers Council.

At least 14,000 reported positive COVID-19 cases have been connected to meatpacking facilities in at least 181 plants in 31 states as of May 13, and at least 54 meatpacking facility workers have died of the virus at 30 plants in 18 states, according to an investigation by the Midwest Center for Investigative reporting.

Global food supplies are getting tighter with each passing day, and many are warning that some areas of the globe will soon be dealing with severe food shortages.

What we really need are a few years of really good growing weather, but the behavior of the sun may not make that possible.

So let’s keep a very close eye on the giant ball of fire that we are revolving around, because if it remains very quiet that could mean big trouble for all of us.

via ZeroHedge News https://ift.tt/3bL1c32 Tyler Durden

Trump To Nominate New US Attorney For Swampy DC Office Tyler Durden

Mon, 05/18/2020 – 19:45

President Trump says he plans to nominate Justin Herdman to serve as US attorney for Washington DC – which has been at the center of the controversial prosecutions of Trump allies Michael Flynn and Roger Stone.

US Attorney Justin Herdman

Herdman – currently the US attorney for the Northern District of Ohio, would replace interim US attorney for Washington, Timothy Shea – whose appointment may not exceed 120 days by law and will expire next month, according to The Hill. Herdman’s appointment requires Senate approval. If rejected, the DC District Court will appoint a new interim US attorney until the position is eventually filled. He was confirmed in 2017 by voice vote for his current position.

Shea, meanwhile, has attracted controversy for his involvement in the DOJ’s request to drop charges against former Trump national security adviser Michael Flynn, as well as seek a lighter sentence for Stone.

Critics argue that Shea, who previously served as senior counsel to Attorney General William Barr, has been instrumental in the politicization of the DOJ.

After Shea and other top agency officials overruled career prosecutors earlier this year to request a more lenient sentence for Stone, the entire four-person prosecution team withdrew from the case, a stunning move taken in apparent protest.

One of those prosecutors, Jonathan Kravis, quit the department entirely. He broke his silence this month to excoriate what he described as political influence over the DOJ after Shea signed a motion to drop criminal charges against Flynn, despite his previously pleading guilty to lying to the FBI. -The Hill

Meanwhile, career prosecutor Brandon Van Grack – who was involved in securing Flynn’s ‘perjury trap’ plea agreement, withdrew from Flynn’s case without explanation an hour before the DOJ filed to drop the charges, according to the report. While he hasn’t resigned, he has reportedly also withdrawn from other cases.

via ZeroHedge News https://ift.tt/2LEFDqr Tyler Durden

The economic effects from COVID-19 will be devastating. Stock and asset prices will fall dramatically and will take years to recover. U.S. Treasury yields will turn negative. Sell “risk-on” assets, increase cash, and buy Treasury bonds.

The U.S., if not the world’s, economy was primed for a serious recession coming into 2020. I argued in an article published on January 13 that, based on economic indicators, a U.S. recession would begin sometime before the end of 2020 and likely by March. In this context, COVID-19 was just the catalyst (albeit, a transcendent one) that tipped the world into it. Pandemic or not, the world was oversupplied and due to flush-out bad debt, weak companies and inequality. It only needed a push. China hadn’t had a recession in 42 years (since modern records have been kept in 1978), Australia in 28 years, and the U.S. in 10 years. Creative destruction had been waiting a long time.

And what a push it was. Just 10 days later (on January 23), I wrote an e-mail to my clients with an article from The Washington Post about emerging issues in Wuhan saying, “I get the sense that this is a bigger story than we are aware of.” In the ensuing months, COVID-19 has become everything.

The health side of the story is bad enough, but the economic one is worse. The combined economic effects of the global simultaneous lock-down, nine or more months of social distancing/rolling lock-down until a potential vaccine/treatment is available (the “90% Economy” as The Economist has termed it), as well as the normal deleveraging side of the business cycle (the “knock-on” effects or mentality change that usually is the recession) make for an economic contraction that will be deep (severe), wide (pervasive), and long (time).

And yet, stock markets are pricing a quick return to normal. It won’t happen. We are still in the first (dare I say, “denial”) stage; something akin to the spring of 1930 when the stock market had rallied back to be down just 19% from the 09/03/1929 peak. I suspect there are many years and chapters of COVID-19 yet to come.

At the same time, it isn’t the end of the world. If one can appreciate how it works, there are investments that will do well; but just a few.

The virus is going to be here for a while

Many prominent people and publications are saying serious things about this virus’ severity and duration:

Bill Gates, “It is impossible to overstate the pain that people are feeling now and will continue to feel for years to come.” 4/23/2020

German Chancellor Angela Merkel, “We are not living in the final phase of the pandemic, but still at the beginning.” 4/23/2020

CDC Director Robert Redfield, “There’s a possibility that the assault of the virus on our nation next winter will actually be even more difficult than the one we just went through.” 4/21/2020

WHO Special Envoy David Nabarro, “We think it’s going to be a virus that stalks the human race for quite a long time to come until we can all have a vaccine to protect us…” 4/12/2020

Former CDC Director, Tom Frieden, “As bad as this has been so far, we’re just at the beginning.” 5/7/2020

New York Magazine, “The FDA has never approved a vaccine for humans that is effective against any member of the coronavirus family, which includes SARS, MERS, and several that cause the common cold.” 4/20/2020

A vaccine requires several steps past finding the right formula. Once a promising discovery is made, there is animal testing, human testing, dose finding, regulatory approval, large-scale production, distribution and the issue of who pays for it. You cannot inject all humans with something until there is relative certainty it is not going to have adverse effects. Experts seem to agree that this cannot be done faster than nine months. Under the best case scenario, the world will be forced into the “90% economy” until sometime in 2021.

COVID-19 is still mysterious to scientists. It has several phenomena that make it problematic:

Contagious without symptoms;

A relatively long incubation period;

Symptoms throughout the body (i.e., blood clotting, COVID toe, organ failure);

Unknown immunity duration after recovery; and

Uneven virulence across strains, the population, and within an infection.

COVID-19 hit the developed world first; presumably in places where there is greater international travel. And because of that, most developed nations are now seeing a plateau or decrease in new infections (in the first wave at least). But seemingly, many developing economies are just starting their first wave. Developing economies generate the lion’s share of global GDP (estimated to be 60-70%) and thus have a large impact on the developed world.

The economic picture is serious

The economic damage already done from the lock-down as well as the idea that the world was near to a recession will result in a secular change in spending mentality that favors saving over spending.

Beyond lock-downs, the social distancing required until a potential vaccine is available has direct ramifications to economic activity. Gatherings with less density imply less demand for goods and services. Common examples are flights with empty middle seats or stadiums half-filled. Social distancing policies will enforce less economic output until a vaccine can be found and distributed broadly.

Economic data releases have been “off the charts” bad but dismissed by investors as aberrations. And as yet economists are increasingly clear that even if the economy has already bottomed (I doubt it), it will be a years-long recovery back. But the stock market is priced for a V-shaped recovery (more on this below). Investors are imagining that the new infections curve (of a given country) to be inversely correlated to its economic curve. As the new infections rate falls, the economy will come back in the same proportion. But the economic indicators are “off the charts” in the same proportion to how severe this incident is. In other words, they are real numbers and they are commensurately scary.

In any past recession, there were geographical areas or industries that were somewhat unaffected and could mitigate the heavily affected areas. In this case, whole aspects of the global economy were turned off simultaneously in a very specialized and optimized (“just-in-time”) global economy. Also, unlike older historical pandemics when it took days or weeks for news to travel, humanity knew about it at the same time, changing our economic behavior (a little or a lot) all at once. This is unprecedented in human history.

With reduced tax revenue, U.S. state, local, and municipal governments are strugglingand will likely need a stimulus package of their own. If this is happening in the United States, imagine the fiscal crises that will strike less wealthy economies.

Countries that have not locked down (Sweden) or countries well on the other side of the infections curve (South Korea, China) are showing depressed economies even without the lock-down.

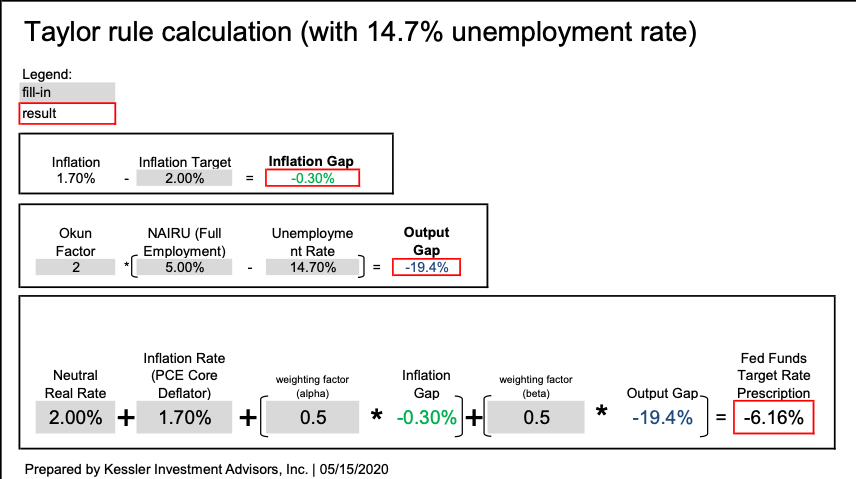

With the U.S. unemployment rate at 14.7%, the Taylor Rule implies the Fed funds rate should be less than minus -6% to be stimulating the economy. If the unemployment rate were to rise to 25% in May (per Treasury Secretary Steven Mnuchin on 05/10/2020), the Taylor Rule would suggest the Fed funds rate should be below minus -16% to be stimulative. I’m not suggesting the Fed will get to these levels, but it illustrates the scale of the crisis.

Several others have stern warnings about the economic severity of COVID-19:

Chairman and CEO of BlackRock Larry Fink, surreptitiously, “Mass bankruptcies, empty planes, cautious consumers and an increase in the corporate tax rate to as high as 29% were part of a vision Fink sketched out on a call this week.” 05/06/2020

Minneapolis Federal Reserve Bank President Neel Kashkari, “Large banks are eager to be part of the solution to the coronavirus crisis. The most patriotic thing they could do today would be to stop paying dividends and raise equity capital, to ensure they can endure a deep economic downturn.” 4/16/2020

Sam Zell, “Sam Zell, the billionaire known for buying up troubled real estate, said the coronavirus pandemic will leave the same kind of impact on the economy and society as the Great Depression 80 years ago, with long-lasting changes in human behavior that imperil many business models.” 05/05/2020

Nouriel Roubini, “The Coming Greater Depression of the 2020s,” 04/28/2020

Warren Buffett “I don’t know that three, four years from now people will fly as many passenger miles as they did last year.” 05/02/2020

Scott Minerd, CIO of Guggenheim Investments, “To think that the economy is going to reaccelerate in the third quarter in a V-shaped recovery to the level where gross domestic product (GDP) was prior to the pandemic is unrealistic. Four years from now the economy will most likely recover to the same level of activity that it was in January.” 4/26/2020

Historian Niall Ferguson, “It will take much longer than people assume for the economy to recover.” 05/06/2020

Global stock markets will fall to new lows

Prominent publications have come out with specific warnings about the stock market:

The Economist, “A one-month bear market scarcely seems enough time to absorb all the possible bad news from the pandemic and the huge uncertainty it has created. This stock market drama has a few more acts yet.”

Financial Times, “Equities generally are still priced for a near-perfect bounce-back from the coronavirus crisis. Lockdowns may last longer than planned. Exits may prove bumpier. Hopes that the virus can be eradicated quickly, and a second wave of infections avoided, may be proven wrong. A quick rebound to the status quo ante looks increasingly implausible. Amid so many unknowns, a further market correction looks more than likely.”

Despite it seeming as though the Federal Reserve and Treasury have spent infinite amounts of money to prop things up, it is still less than the money lost. In a general sense, if the stimulus funds were as big as the problem, economic indicators wouldn’t be weakening. Politicians never accidentally make people more than whole (in the aggregate). No matter how much liquidity there is, stocks are still ultimately beholden to corporate earnings.

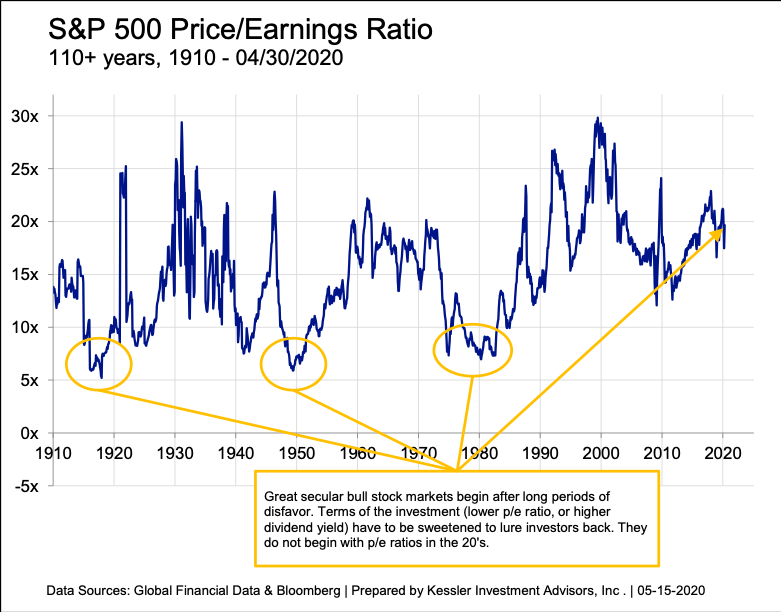

The stock market is fundamentally expensive. The price earnings ratio (trailing) of the S&P 500 is near 20. Prices will need to come down a great deal before stocks look secularly attractive. They will have to come down even further if earnings weaken materially. Multi-decade secular bull markets have begun when these ratios are below 10 (see chart below).

This is a big enough demand shock (an economic “earthquake”) that virtually any company (U.S. or international) will struggle for years. Even after the virus and economy improve, paying the huge public debt bills that economies have amassed will become the focus. Higher taxes will ultimately weigh on profitability for decades. There will be exceptions (say Clorox or Netflix, so far), but the majority will struggle.

Because COVID-19 has only been known for four months (really just three, as the markets are concerned), investors can still imagine a V-shaped recovery.

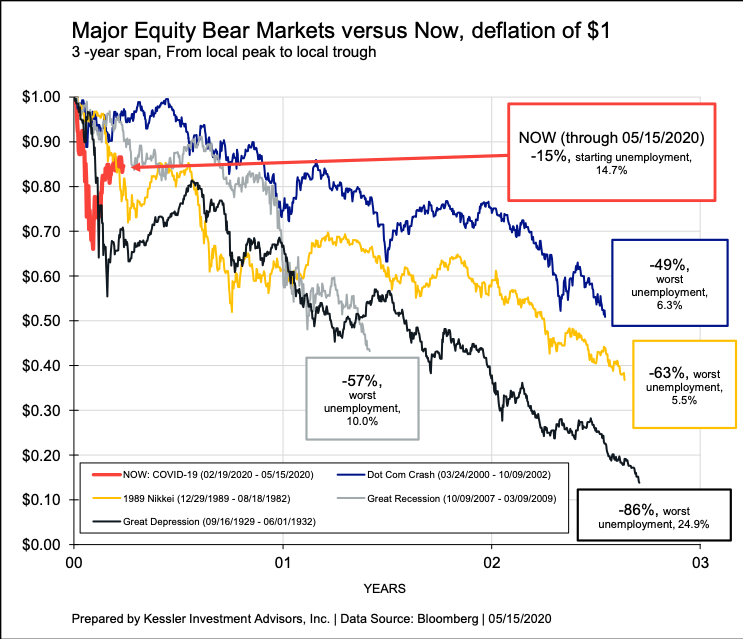

The chart below puts the U.S. stock market’s (S&P 500) performance from its recent peak in the context of past major bear markets. In this view, things have only begun. For instance, in the Great Depression, it took nearly three years from the peak to the trough. We are just four months into this.

The stock markets went down through alternating waves of hopes (prices higher) and fears (prices lower). There will be many chapters to COVID-19. We are in the first one.

The table below shows all of the bear-market rallies greater than 10% in the cycles identified above. There were several strong rallies. The average length of those rallies was about two months (1.8). The current rally has lasted a very similar 1.2 months (assuming 04/29/2020 was the peak).

What to invest in?

There is nothing wrong with cash. Today, we call money not being invested “cash,” but at one time, it was just called “savings.” The importance of savings is that the money is there more than it is growing. Japan has rediscovered this dynamic in the last 30 years. Despite cash earning nothing (and it won’t again for years), if you are in cash and the stock market falls, you get to buy it back cheaper. Having cash gives an investor the freedom to invest in opportunities as they arise and be the “buyer” in a buyer’s market. Don’t think you have to invest all your money to be productive.

U.S. Treasury bonds will appreciate. They appreciate in price when yields fall and depreciate when yields rise. The more that yields move lower, the more that prices move higher. As an example, if the current 30-year Treasury’s yield were to drop from where it currently yields 1.33% (5/15/2020), to 0.75%, this bond would appreciate by 15%. If it dropped to a zero yield, it would appreciate 40%. These aren’t small returns. But bond prices decrease in the same proportion if rates were to rise.

As has already happened in Japan and Germany, U.S. Treasury interest rates will fall well below zero as this crisis intensifies. This is why:

Deflation will be the theme of the “90% economy” because it implies a 90% price. Meaning that if the economy is expected to operate 10% lower than before, supply and demand would suggest that prices (inflation) would be 10% lower too. I am not suggesting a one-time drop of 10%, but rather that there will be tremendous pressure towards lower prices (in aggregate that-is; individual sectors may have higher prices). But, it isn’t just the initial shock, there will continue to be deflationary pressure as long as the output gap is negative. That is going to take years and years to close. Deflation implies lower Treasury yields, because if prices are deflating at say 5% per year, a minus 4% yield on a Treasury would be valuable (as saving 1% over the alternative). Because of this, there is no limit to how negative Treasury rates can go, they are a function of inflation/deflation.

Given the scale of COVID-19, the Fed (and other developed economy central banks) will need to cut short-term rates deeply negative. This will pull all Treasury yields lower. I can already hear the chorus of arguments (“it hasn’t worked!”, “it creates a liquidity trap!”, “it creates hyperinflation!”) Yes, there will be tremendous resistance, but a threshold exists where the importance of protecting an industry (money market managers, banking) will pale in comparison to the economic needs of the whole country. In other words, there is a point where the Fed will alienate creditors at-large for the bigger picture. There are two prominent voices calling for negative rates so far (below), but I suspect these voices will grow in number:

Professor of Economics and Public Policy at Harvard University Ken Rogoff, “…the Fed could push most short-term interest rates across the economy to near or below zero. Europe and Japan already have tiptoed into negative rate territory. Suppose central banks pushed back against today’s flight into government debt by going further, cutting short-term policy rates to, say, -3% or lower.” 5/4/2020

Former President of the Minneapolis Federal Reserve Bank, Naranya Kocherlakota, “Unprecedented situations require unprecedented actions. That’s why the U.S. Federal Reserve should fight a rapidly deepening recession by taking interest rates below zero for the first time ever.” 4/24/2020

But “yield curve control” is the Fed’s next-biggest tool and I suspect it will be used before negative rates because it is more palatable to the banking and money-market industries. “Yield curve control” is a fancy way of saying that the Fed could control longer-term interest rates like they do with short-term rates. Japan is currently doing it and the U.S. did it in the 1950s. The idea is to force term rates down to, or below, a certain threshold to encourage lending. For instance, the Fed could target the 10-year Treasury yield to be 0.25% and ensure it by committing to buy enough 10-year Treasury bonds to take it there. “Committing” is the key word because if the central bank is credible enough, it doesn’t always have prove it with real capital; the threat is enough for the market to take it there. Assuming the mortgage market was functioning normally, it could help get mortgage rates down to 1%. Anyone with a mortgage can imagine how helpful that would be.

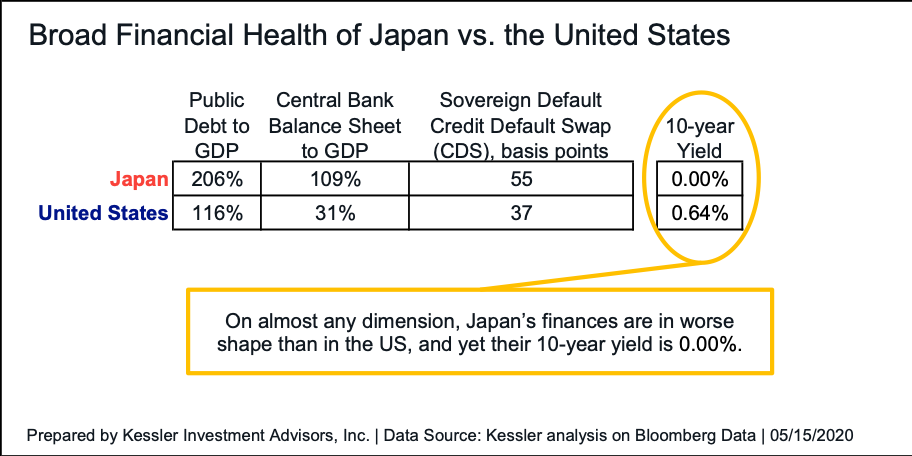

Some worry that the amount of stimulus the U.S. is spending will lead to hyper-inflation or equivalently, a weakened currency. The fiscal/monetary picture of the U.S. isn’t as extreme as it is made to be. Japan’s finances are a useful example of how far a super-power’s credit stretches. On almost any dimension, Japan’s finances are in worse shape than in the US, and yet their 10-year yield is 0.00% (see table below). Credit risk should show up first in Japan before we would see it in the U.S. They are the canary in the coal mine on this issue.

All of these things combined portend a continuing U.S. Treasury bull market (lower yields) for a few more years.

Then, once everyone has given up on the stock market and P/E ratios are in the single digits, it will be time to buy stocks.

COVID-19 is the equivalent of a 300-year flood. It will be the theme of financial markets for an enduring horizon.

Canadian Jet Doing COVID ‘Flyover Tribute’ In Fiery Crash Onto Residence, Killing One Tyler Durden

Mon, 05/18/2020 – 19:05

“We live six or seven miles away from the crash and we heard a really loud boom,” a local eyewitness said of a horrific military plane crash in British Columbia. “You could see the smoke so we decided to walk toward it. The smell was really strong. You could start to smell the burning fuel.”

Over the weekend a Canadian Air Force jet crashed into a residential neighborhood in an area 220 miles northeast of Vancouver just before noon. The jet was part of Canadian Forces Snowbirds, an aerial demonstration team akin to America’s ‘Blue Angels’, and was in the midst of performing a flyover of cities as a tribute frontline coronavirus health workers and other virus responders.

The event typically features nine jets flying in tight formation with white smoke trailing, but quickly turned tragic after one aircraft veered off and spiraled down, ending in a massive boom. Capt. Jenn Casey, a spokeswoman for the Canadian Forces Snowbirds, died in the crash while her copilot survived with serious injuries after parachuting out.

The Snowbirds flying over Montreal on May 7th, via AFP.

The white and red jet took off alongside another and did a wide turn once in flight, according to a video posted on Twitter. Shortly after, the plane could be seen heading downward.

It appeared that two people ejected from the plane in a plume of dark smoke before the aircraft nose-dived into a house in the Brocklehurst neighborhood of Kamloops, which is about 220 miles northeast of Vancouver.

The Canadian Forces Snowbirds last month announced Operation Inspiration. The mission consisted of the squadron flying over cities across Canada in a nine-jet formation with trailing white smoke. The Snowbirds were scheduled to start in Nova Scotia and work their way west throughout the week.

Shocking video recorded by onlookers showed the plane attempted to gain altitude before entering a dramatic nosedive — all which took a mere seconds.

The two pilots were then seen ejecting already perilously close to the ground — so close that it was unclear whether the parachutes even opened.

— Victor Mario Kaisar (@supermario_47) May 17, 2020

The flame-engulfed jet reportedly landed directly on a residential house, but there were no reports of injuries or deaths on the ground, with an elderly couple surviving — one had been in the basement at the moment of impact, with another in the backyard.

Debris was seen scattered across lawns and the neighborhood as firefighters responded.

The RCAF has suffered another tragic loss of a dedicated member of the RCAF team. We are deeply saddened and grieve alongside Jenn’s family and friends. Our thoughts are also with the loved ones of Captain MacDougall. We hope for a swift recovery from his injuries. – Comd RCAF pic.twitter.com/8U41bdVqcU

— Royal Canadian Air Force (@RCAF_ARC) May 18, 2020

Local eyewitnesses in the residential area said they were shocked and didn’t initially know what had happened:

Kerri Turatus, 30, who lives in the neighborhood where the plane went down, said the aircraft hit a house, engulfing it in flames.

It “sounded like a gunshot outside my window,” Turatus said.

She saw a “big black circle ring of smoke” in the sky, she said, adding that part of the plane’s wreckage was in the street and that she could see a wing sticking out of a neighbor’s garage.

Parts of the aircraft could be seen scattered and in flames across a neighborhood block, with a parachute being found on the roof of a house. It seems a miracle that the copilot survived.

Via local British Columbia media reports.

Another eyewitness, Rose Miller, told the AP: “It looked to me like it was mostly on the road, but it just exploded. It went everywhere.” She added, “In fact, I got a big, huge piece in my backyard. The cops said it was the ejection seat.”

The tragedy brings up serious questions of safety as well as how necessary such high-risk, high-cost endeavors are as well as their frequency.

Ongoing campaigns in the United States involving major flyovers of cities by The Blue Angels and Thunderbirds as “tribute” and “inspiration” amid COVID-19 lockdowns have grown increasingly controversial given the huge expense to taxpayers, at $500,000 per flyover, according to some estimates.

The weekend tragedy in British Columbia presents another criticism: the unnecessary dangers both the pilots and on the ground spectators are subject to in what remains fundamentally high-risk aerial demonstrations and maneuvers.

via ZeroHedge News https://ift.tt/3e2bdKH Tyler Durden

If Donald Trump wants to get re-elected as President of the U.S. he’s going to have to take out former President Barack Obama. At this point Obama is the person who most stands in his path for a second term.

Former Vice President Joe Biden may well wind up being the nominee but that’s only because he is Obama’s stand in since Obama can’t run for a third term thanks to the only part of the U.S. Constitution anyone seems to give a damn about anymore.

But, make no mistake, the current flap about the unmasking of Trump’s first (and short-lived) National Security Adviser Gen. Michael Flynn is all about Trump finally going on the offensive after more than three years of fighting rear-guard actions just to stay in power.

Obama was the ring leader in the operation to spy on Trump and anyone with half a brain knows it. The unmasking of the unmaskers in the Obama administration is to tarnish his legacy and dishearten any centrist voters who may be tiring of Trump’s mistakes and the worsening economic collapse engineered by the shutdown of the economy during the peak of the COVID-19 hysteria.

This is why it is imperative for Trump to take Obama out of this election cycle as quickly as possible.

With Hillary finally bending the knee to Obama when she publicly endorsed Biden that was the signal that she’s acknowledging she’s lost the fight for control over the Democratic Party, which she and her husband have ruled with a closed fist for decades.

Now Obama is free and clear to begin campaigning openly on Biden’s behalf. And don’t for a second think that the trial balloons of his wife Michelle being Biden’s running mate are the fanciful wishes of hopeless Democrats. Michelle is absolutely one of the top candidates for that job.

Because with Trump surviving everything thrown at him to this point the only chance Biden has this fall is his second coming as the Left’s political messiah. Take nothing away from Obama, he is an excellent campaigner.

With Michelle as his running mate that puts Obama right where he needs to be, hounding Trump on all the issues that are supposed to be weaknesses for him – the economy, COVID-19 deaths, unemployment, etc.

So, the timing of Trump having his acting ODNI Director Richard Grenell pick a public spat with the hapless Head of the House Intelligence Committee Adam Schiff and get the transcripts of the impeachment interviews released to the public isn’t coincidence, folks. These transcripts confirm that Obama’s inner circle all lied through their teeth in the media for years about the RussiaGate collusion story.

This comes on the heels of Trump’s somewhat cleaned up Dept. of Justice dropping the case against Flynn which then opens up the opportunity to resurrect the timeline of events which led up to his firing and indictment by the very people now revealed as bald-faced liars and conspirators.

Trump then goes directly to the people and coins the term of the year, “Obamagate.”

He’s telling the entire world who his target is. He knows that if he loses this election any chance of reforming any part of the D.C. swamp vanishes as Biden steps aside for health reasons after sweeping everything under the rug and Obama rules the White House from the shadows as First Lady.

And it’s clear that this is the real reason behind the Democratic governors defying their people and Trump on opening up their cities and states. They are purposefully trying to destroy the country to regain control over it.

These people are vandals.

But Trump’s biggest obstacle at this point isn’t the Democrat-controlled House or the Media, it is the Republicans in the Senate who have proven repeatedly to be spineless when it comes to anything substantive.

Obama is guilty of the highest crimes a President can be guilty of, utilizing Federal law enforcement and intelligence services to spy on a political opponent during an election. This is after eight years of ruinous wars, coups both successful and not, drone-striking U.S. citizens and generally carrying on like the vandal he is.

Thankfully Rand Paul (R-Ky) has been activated by Trump to go after Graham directly and force him to back peddle. Paul is already calling for hearings in the Senate, using his Chairmanship of the Government Oversight Committee to end run around Light in the Loafers Lindsey.

The FBI is now going after people like Richard Burr (R-NC), head of the Senate Intelligence Committee for potential insider trading violations. This is a pure power play to make sure Burr doesn’t let this die in committee.

If this tweet isn’t clear enough that Trump wants Obama’s head on a platter and he’s now willing to go scorched earth on him and anyone trying to protect Obama to get it I don’t know what is.

If I were a Senator or Congressman, the first person I would call to testify about the biggest political crime and scandal in the history of the USA, by FAR, is former President Obama. He knew EVERYTHING. Do it @LindseyGrahamSC, just do it. No more Mr. Nice Guy. No more talk!

Things are spiraling out of control in D.C. quickly. A reader noted to me recently that one of Trump’s strengths is that he thrives in chaos, that he’s most comfortable stirring the pot and getting everyone around him ‘on tilt’ as the poker players say.

That’s what he’s doing now with #Obamagate. He’s doing what he does best, forcing his opponents to ab react to him and leaving them vulnerable to his next attack. He’s in pure campaign mode now, which we haven’t seen in four years.

But this time he’s campaigning with a lot more resources at his disposal especially if he has them all nailed. Trump wouldn’t be going after Obama if he didn’t have proof of Obama’s guilt. He’s a limbic creature but he’s not random.

Obama’s people will spin this as desperation over the mishandling of COVID-19, but it won’t matter. With a Justice Dept. that looks ready to get to work for the first time in decades, Trump just well be ready to finally do something right.

via ZeroHedge News https://ift.tt/2Tl2jQR Tyler Durden

{kind=link}

{kind=link}

{kind=link}