US “Geoblocks” BLS And Census Websites For Hong Kong Internet Users Tyler Durden

Tue, 10/13/2020 – 20:00

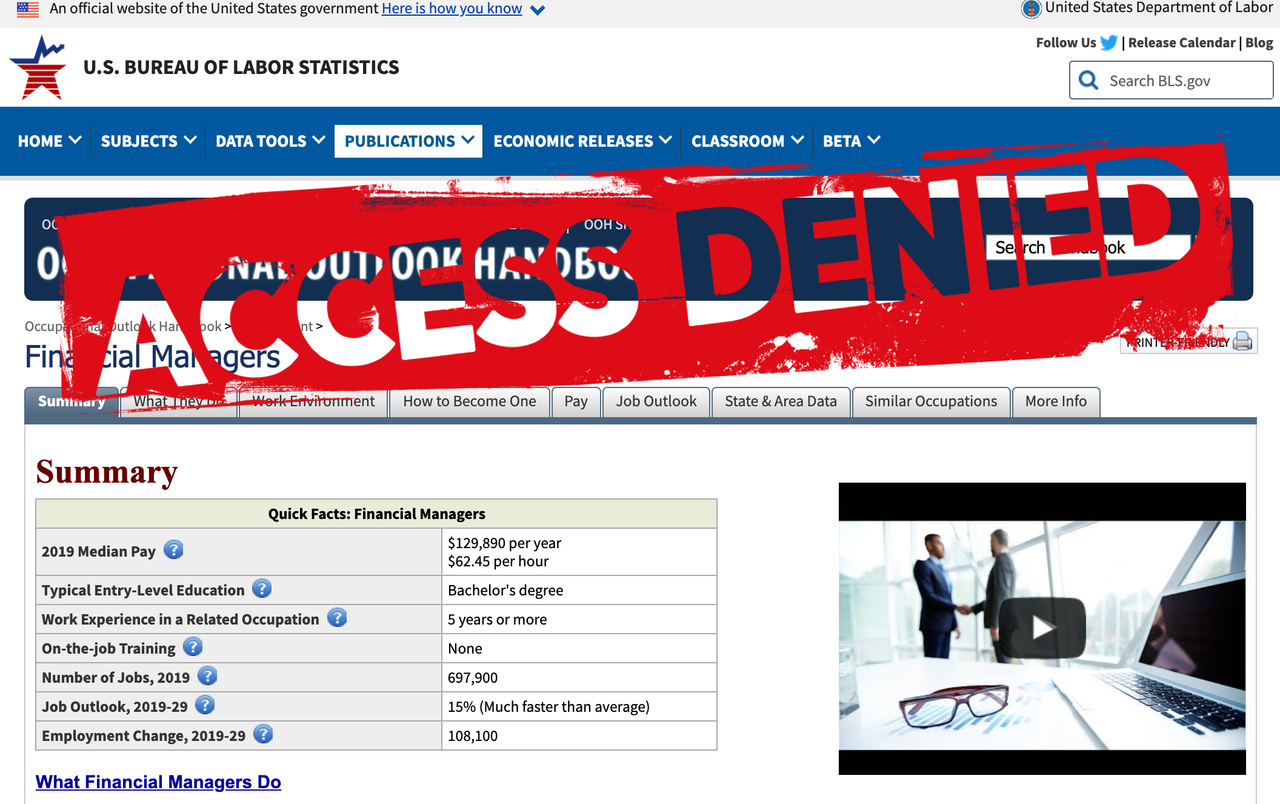

The US has terminated access to two very important US federal websites for Hong Kong internet users, reported FT.

The Websites, the Bureau of Labor Statistics and the US Census Bureau, provide critical economic data for investors, is fueling continued tensions between Washington and Beijing over the semi-autonomous territory.

FT spoke with several US government agencies about the blocked websites for Kong Kong residents but received very little information about the ongoing situation.

A spokesperson at the Department of Labor, which includes the Bureau of Labor Statistics, declined to comment on the “security procedures” but said, “agencies began implementing geoblocks that included Hong Kong in January 2018.”

“That would mean the measures started more than two years before the US punished the Asian financial center in response to Beijing’s introduction in June of a tough security law for Hong Kong. The US maintained that the security law meant Hong Kong was no longer sufficiently autonomous from mainland China,” FT said.

Considering Hong Kong is one of the world’s most important financial hubs, the blocking of both websites is not helpful for analyst and investors working in the area, though many are still able to access the US government data via a virtual private network, Bloomberg, Eikon, or FactSet terminal.

Cliff Tan, a Hong Kong-based analyst and former head of East Asian global markets research at Japanese bank Mitsubishi UFJ Financial Group, told FT that access to both websites have been blocked for the last couple of months.

“Non-farm payroll data is arguably the most important economic statistic in the world,” Tan said.

He said his VPN works just fine to access the websites.

“I have a VPN but didn’t ever think I would need it in Hong Kong,” he said.

A US government source, with direct knowledge about the situation, said more US federal government websites are expected to be blocked as Washington no longer recognizes Hong Kong as autonomous from mainland China.

US Cyber Command told FT it began geoblocking federal websites in 2017 to protect military websites and ensure “network availability” worldwide. The cyber agency wasn’t able to comment on why certain civilian websites were geoblocked.

Tensions between Washington and Beijing have been soaring under President Trump’s first term. The rift between both countries explode during the trade war and accelerated in 2020 following the virus pandemic. In July, Trump revoked Hong Kong’s special trading status after Beijing imposed national security law.

Tan summarizes the latest debacle: “If you interfere with information in a financial center, it’s like cutting off oxygen.”

via ZeroHedge News https://ift.tt/3dngihR Tyler Durden

Everyone knew the second quarter of 2020 was going to be a disaster, and it was. The U.S. economy fell by 31.4% (annualized) in the second quarter.

But, the expectation was that we’d have a V-shaped recovery with a sharp bounce-back in the third quarter, a reopening of closed businesses, rehiring of the unemployed and a rising stock market.

But so far, the economy is not following the script laid out for it by the politicians and experts.

The stock market did rally, but that was mainly because the stock index components are heavily weighted to companies least affected by the pandemic including Amazon, Apple, Netflix, Alphabet (Google), Facebook and Microsoft.

Of course, it didn’t hurt that the Federal Reserve printed $4 trillion of new money and backstopped money markets, corporate bonds, municipal bonds, foreign central banks and other facets of capital markets with direct purchases, guarantees or currency swaps.

Even at that, stocks have been struggling since hitting new highs on September 2.

And yes, there was growth in the third-quarter (the best estimate is that the economy will grow at about a 35% annualized rate, but we won’t have official figures until October 29).

The 35% third-quarter recovery was to be expected as Americans got back to work after the lockdown. That 35% rate might sound like the third quarter will basically make up for the second quarter, but it won’t.

Not as Good as It Sounds

The 35% gain is applied to the lower level of output resulting from the 31.4% loss. If you take 100 as a starting place, reduce it by 31.4% you get to a new level of 68.6. If you increase that level by 35% you get back to 92.6.

That still leaves you 7.4 percentage points in the hole, not counting the 5% drop in the first quarter. When you apply 7.4% to a $22 trillion economy, that means you still have $1.6 trillion of lost output on an annualized basis even after the 35% third-quarter recovery.

The V-shaped recovery looks more like an “L” with flattish growth beyond the third-quarter. Things will not necessarily get much better from there, and progress is very much in doubt.

The lockdown continues in many places. The virus has not gone away, and the caseload and fatalities continue to grow.

A second wave of layoffs has now begun as companies that were able to hang on thanks to Payroll Protection Plan loans find that the money has run out, and their businesses are still closed. They are now being forced to let go of workers who might have survived the first layoffs in March and April.

So the letter to describe the recovery isn’t a “V” or even an “L” but possibly a “W,” with another recession right around the corner.

Beyond the second wave of layoffs, there is a persistent problem of the long-term unemployed whose businesses are shut down or dead in the water with no prospect of any return of demand.

This is a combination of factors the economy has not seen since the 1930s. It’s worse than a technical recession, it’s a depression, and its effects will be felt for years, or even decades, to come.

When Will Output Return To 2019 Levels?

The U.S. will not regain 2019 output levels until at least 2022, and growth going forward will be even worse than the weakest-ever growth of the 2009–2020 recovery.

The post-2009 recovery produced only 2.2% growth. It was an L-shaped recovery. It was a real recovery, yet the output gap between the former trend and the new trend was never closed.

The U.S. economy suffered over $4 trillion of lost wealth based on the difference between the former strong trend and the new weaker trend.

That lost wealth was a serious problem for the U.S. before the New Great Depression. Now the prospect is for even lower growth than the weak post-2009 recovery.

The U.S. economy would have to grow 10% a year in 2021 and 2022 to return to 2019 levels of output.

First, is 10% growth even a reality? Past history says no.

Since 1943, U.S. annual real growth in GDP has never exceeded 10%. In fact, post-1980 recoveries averaged 3.2% growth. And since 1984, growth has never exceeded 5%.

So 10% is a very optimistic forecast to begin with. Here’s the problem:

Using 100 as a yardstick for 2019 output and assuming unrealistic back-to-back years of 10% real growth in 2021 and 2022, one still does not get back to 2019 output levels.

It would take the highest annual real growth in over 40 years, sustained for two consecutive years, to get close to 2019 output levels.

It’s far more realistic to assume real growth will be less than 10% per year. That puts the economy well into 2023 before reaching output levels last achieved in 2019.

Another “L”-shaped Recovery

The new recovery, far from the 10% growth discussed in the example above, may only produce 1.8% growth, even worse than the 2.2% growth before the pandemic.

It’s another L-shaped recovery, the second in a row. Now the bottom of the L is even closer to a flat line, and the output gap compared with the long-term trend is even greater.

All of this economic devastation was not caused directly by the virus. It was caused by the policy response to the virus, specifically the extreme lockdowns ordered by many state governors.

Was it all worth it? The likely answer is “no.”

90% of Lockdown Benefits at Only 10% of the Cost

Many top scientists agree that lockdowns don’t work. The virus will spread with or without a lockdown. Some measures make sense such as washing hands, keeping social distance and wearing masks in crowded spaces.

But there’s no evidence masks do any good at all when the wearer is alone, outdoors or at a reasonable distance from others.

We could have followed these basic rules and gotten 90% of the benefit of a lockdown at only 10% of the cost.

Those supporting lockdowns have ignored the costs of increased suicides, drug abuse, alcohol abuse, domestic violence and the depression and anxiety that result from lack of social interaction. There was never a good reason to close every bar, restaurant, salon, boutique and public space.

“We Destroyed the World’s Greatest Economy for No Good Reason”

Even the World Health Organization is coming out against lockdowns. Dr David Nabarro, the WHO’s special envoy on COVID-19, says:

We really do appeal to all world leaders: stop using lockdown as your primary control method… We in the World Health Organization do not advocate lockdowns as the primary means of control of this virus. The only time we believe a lockdown is justified is to buy you time to reorganize, regroup, rebalance your resources, protect your health workers who are exhausted, but by and large, we’d rather not do it.

We destroyed the world’s greatest economy for no good reason.

via ZeroHedge News https://ift.tt/34TsZNA Tyler Durden

Everyone knew the second quarter of 2020 was going to be a disaster, and it was. The U.S. economy fell by 31.4% (annualized) in the second quarter.

But, the expectation was that we’d have a V-shaped recovery with a sharp bounce-back in the third quarter, a reopening of closed businesses, rehiring of the unemployed and a rising stock market.

But so far, the economy is not following the script laid out for it by the politicians and experts.

The stock market did rally, but that was mainly because the stock index components are heavily weighted to companies least affected by the pandemic including Amazon, Apple, Netflix, Alphabet (Google), Facebook and Microsoft.

Of course, it didn’t hurt that the Federal Reserve printed $4 trillion of new money and backstopped money markets, corporate bonds, municipal bonds, foreign central banks and other facets of capital markets with direct purchases, guarantees or currency swaps.

Even at that, stocks have been struggling since hitting new highs on September 2.

And yes, there was growth in the third-quarter (the best estimate is that the economy will grow at about a 35% annualized rate, but we won’t have official figures until October 29).

The 35% third-quarter recovery was to be expected as Americans got back to work after the lockdown. That 35% rate might sound like the third quarter will basically make up for the second quarter, but it won’t.

Not as Good as It Sounds

The 35% gain is applied to the lower level of output resulting from the 31.4% loss. If you take 100 as a starting place, reduce it by 31.4% you get to a new level of 68.6. If you increase that level by 35% you get back to 92.6.

That still leaves you 7.4 percentage points in the hole, not counting the 5% drop in the first quarter. When you apply 7.4% to a $22 trillion economy, that means you still have $1.6 trillion of lost output on an annualized basis even after the 35% third-quarter recovery.

The V-shaped recovery looks more like an “L” with flattish growth beyond the third-quarter. Things will not necessarily get much better from there, and progress is very much in doubt.

The lockdown continues in many places. The virus has not gone away, and the caseload and fatalities continue to grow.

A second wave of layoffs has now begun as companies that were able to hang on thanks to Payroll Protection Plan loans find that the money has run out, and their businesses are still closed. They are now being forced to let go of workers who might have survived the first layoffs in March and April.

So the letter to describe the recovery isn’t a “V” or even an “L” but possibly a “W,” with another recession right around the corner.

Beyond the second wave of layoffs, there is a persistent problem of the long-term unemployed whose businesses are shut down or dead in the water with no prospect of any return of demand.

This is a combination of factors the economy has not seen since the 1930s. It’s worse than a technical recession, it’s a depression, and its effects will be felt for years, or even decades, to come.

When Will Output Return To 2019 Levels?

The U.S. will not regain 2019 output levels until at least 2022, and growth going forward will be even worse than the weakest-ever growth of the 2009–2020 recovery.

The post-2009 recovery produced only 2.2% growth. It was an L-shaped recovery. It was a real recovery, yet the output gap between the former trend and the new trend was never closed.

The U.S. economy suffered over $4 trillion of lost wealth based on the difference between the former strong trend and the new weaker trend.

That lost wealth was a serious problem for the U.S. before the New Great Depression. Now the prospect is for even lower growth than the weak post-2009 recovery.

The U.S. economy would have to grow 10% a year in 2021 and 2022 to return to 2019 levels of output.

First, is 10% growth even a reality? Past history says no.

Since 1943, U.S. annual real growth in GDP has never exceeded 10%. In fact, post-1980 recoveries averaged 3.2% growth. And since 1984, growth has never exceeded 5%.

So 10% is a very optimistic forecast to begin with. Here’s the problem:

Using 100 as a yardstick for 2019 output and assuming unrealistic back-to-back years of 10% real growth in 2021 and 2022, one still does not get back to 2019 output levels.

It would take the highest annual real growth in over 40 years, sustained for two consecutive years, to get close to 2019 output levels.

It’s far more realistic to assume real growth will be less than 10% per year. That puts the economy well into 2023 before reaching output levels last achieved in 2019.

Another “L”-shaped Recovery

The new recovery, far from the 10% growth discussed in the example above, may only produce 1.8% growth, even worse than the 2.2% growth before the pandemic.

It’s another L-shaped recovery, the second in a row. Now the bottom of the L is even closer to a flat line, and the output gap compared with the long-term trend is even greater.

All of this economic devastation was not caused directly by the virus. It was caused by the policy response to the virus, specifically the extreme lockdowns ordered by many state governors.

Was it all worth it? The likely answer is “no.”

90% of Lockdown Benefits at Only 10% of the Cost

Many top scientists agree that lockdowns don’t work. The virus will spread with or without a lockdown. Some measures make sense such as washing hands, keeping social distance and wearing masks in crowded spaces.

But there’s no evidence masks do any good at all when the wearer is alone, outdoors or at a reasonable distance from others.

We could have followed these basic rules and gotten 90% of the benefit of a lockdown at only 10% of the cost.

Those supporting lockdowns have ignored the costs of increased suicides, drug abuse, alcohol abuse, domestic violence and the depression and anxiety that result from lack of social interaction. There was never a good reason to close every bar, restaurant, salon, boutique and public space.

“We Destroyed the World’s Greatest Economy for No Good Reason”

Even the World Health Organization is coming out against lockdowns. Dr David Nabarro, the WHO’s special envoy on COVID-19, says:

We really do appeal to all world leaders: stop using lockdown as your primary control method… We in the World Health Organization do not advocate lockdowns as the primary means of control of this virus. The only time we believe a lockdown is justified is to buy you time to reorganize, regroup, rebalance your resources, protect your health workers who are exhausted, but by and large, we’d rather not do it.

We destroyed the world’s greatest economy for no good reason.

via ZeroHedge News https://ift.tt/34TsZNA Tyler Durden

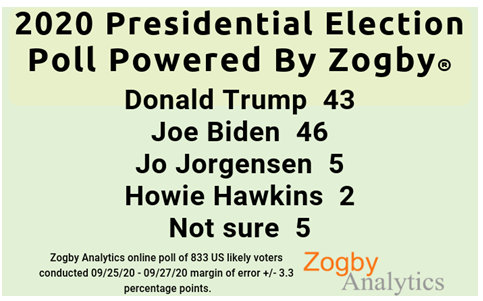

Trump Scores With Independents As Suburban Women Lean Left Tyler Durden

Tue, 10/13/2020 – 19:20

President Trump is closing the gap with former Joe Biden – scoring points with independent voters, while the former Vice President enjoys a healthy lead among suburban women, according to a recent poll by Zogby Analytics.

Overall, the poll has Trump leading Biden 46 to 43 in major battleground states – due in part to the fact that Zogby included third-party candidates Jo Jorgensen, Howie Hawkins and voters who are undecided.

“The race is close and is a far better representation when you include third parties,” said Jonathan Zogby, adding “Zogby Analytics will always include third parties in our polls. It’s a shame when you have a respected, intelligent woman as a party nominee, and the mainstream media is pretending she doesn’t exist. Now who is sexist? Don’t give us that business that ‘voting for a third party is a vote for Trump or Biden!’ So if you don’t fall in line with the duopoly you don’t have a voice? That’s not what the founders’ of our republic and Constitution ever intended to happen. Everyone has a voice: Democrats, Republicans, Libertarians, and Greens”

“The contest is also close in battleground states, with Trump narrowly winning against Biden 46% to 43%, while Jorgensen received 7% and Hawkins 1%,” said Zogby.

“The president is also coming back with independents,” though Biden still leads 39% to 34%.

Trump is winning voters aged 30-49, 51% to 38%, and Generation X, 50% to 42%.

70% of swing voters who chose Barack Obama and then Trump in 2016 back the president.

Positives for Biden:

Older voters choose him over Trump, 58%-38%.

He’s winning the suburbs, 47% to 39%.

Biden leads Trump among suburban women, 52% to 33%.

Yet, while Zogby conducts what appears to be minimally biased polls which includes a more realistic playing field (as people will write in third-party candidates), Rabobank’s Michael Every points out (and we noted earlier), polls can be wrong. Especially when it is harder and harder to find people who have the time and energy to answer a survey, a process that naturally leans towards the wealthier and more politically active.

As Pew research notes in a looong election note today, different polling agencies conduct their surveys quite differently; the barriers to entry in the field have disappeared; a poll may label itself “nationally representative,” but that’s not a guarantee that its methodology is solid; the real margin of error is often double that which is reported (and they are already quite large at +/- 3%); huge sample sizes sound impressive, but don’t mean much as this can mean cheap and problematic sampling; evidence suggests if the public hears a certain candidate is likely to win, they are less likely to vote; public estimates of policies are generally trustworthy, but estimates of who will win are less so; all good polling relies on statistical adjustment; not adjusting for education is a disqualifying shortfall (as we saw in 2016); more transparency on how a poll was taken is better; polling is not broken, despite 2016; the evidence for “shy” Trump voters is actually quite shy; yet a systematic miss in election polls is more likely than people think, especially on the electoral college outcome.

Every notes that RealClearPolitics‘ polling aggregator fails to include Zogby and Democracy Institute in their polling average benchmark.

* * *

In short, trust polls at your own risk.

via ZeroHedge News https://ift.tt/34RU8Aw Tyler Durden

IMF Urges Governments To “Ensure Corporations Pay Fair Share Of Taxes” Tyler Durden

Tue, 10/13/2020 – 19:00

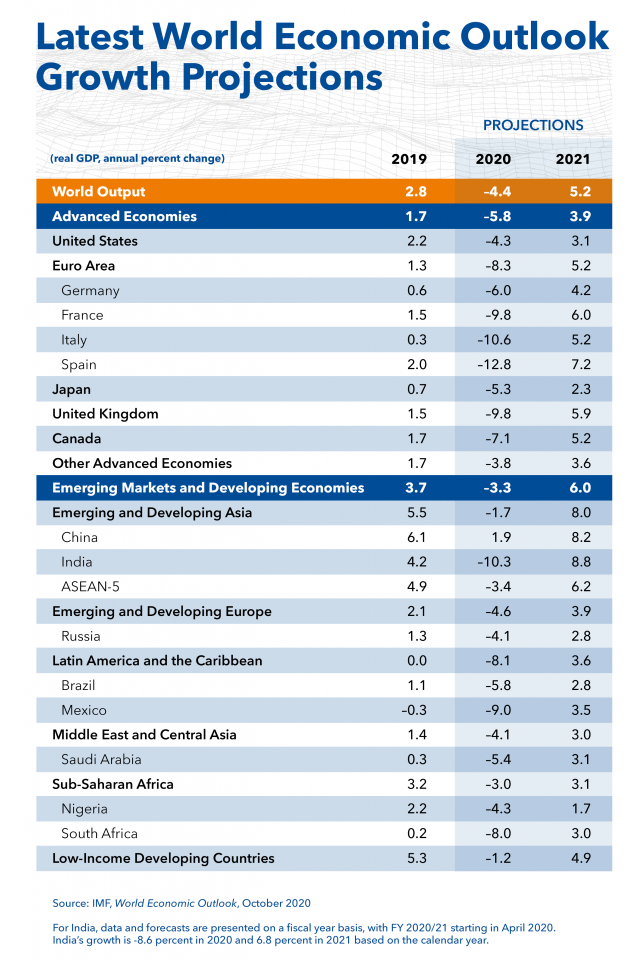

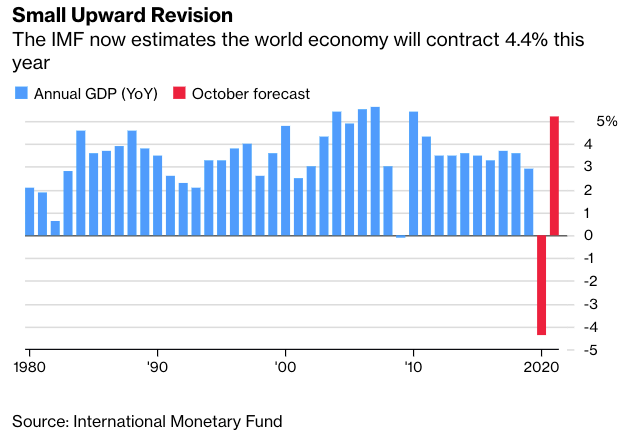

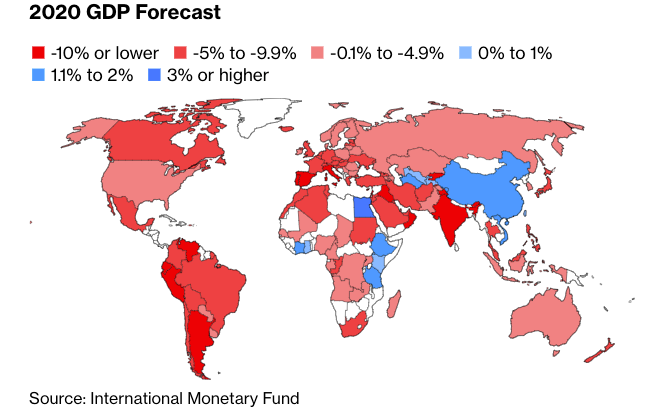

In its latest batch of projections about the global economy, the International Monetary Fund has again projected a “deep recession” in 2020, which would be one of the worst annual plunges since the Great Depression of the 1930s.

The report, released Tuesday, shows the agency expects global growth to plunge 4.4% this year, an upward revision of 0.8 percentage points compared with the June estimates in the World Economic Outlook report, said IMF chief economist Gita Gopinath. For 2021, the IMF sees world growth at 5.2%, down from June’s 5.4% projection.

“The upward revision in the IMF’s 2020 growth forecast reflects in particular better-than-projected second-quarter growth in the U.S. and the euro area, a stronger-than-anticipated return to growth in China and signs of a more rapid recovery in the third quarter,” said Bloomberg.

Ahead of today’s release, Bloomberg quoted Gopinath as saying:

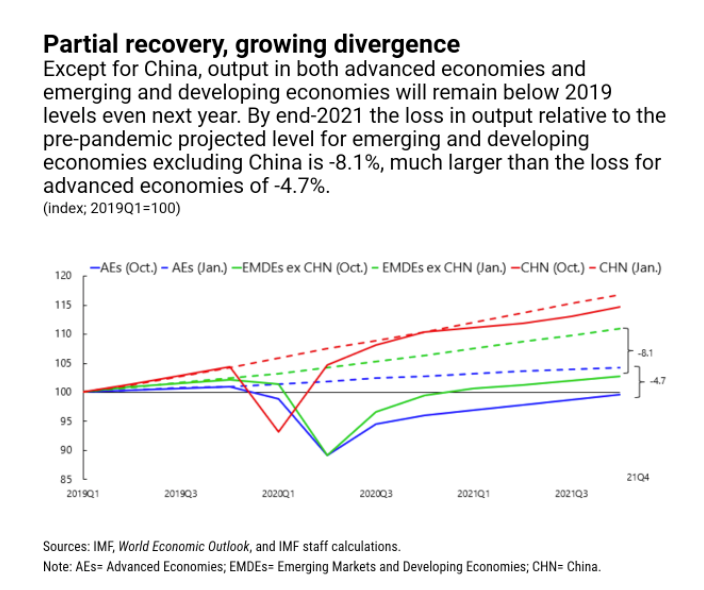

“So we continue to project a deep recession in 2020 with global growth projected to be -4.4%. This is a small upgrade relative to our June numbers. We expect growth to rebound partially in 2021, coming back to 5.2 percent. However, with the exception of China, all advanced economies and emerging and developing economies, excluding China we are projecting output will remain below 2019 levels well into 2021. Therefore, we see that the recovery from this catastrophic collapse will likely be long and even highly uncertain,” she said.

In today’s report, Gopinath said that “the global economy is climbing out from the depths to which it had plummeted during the Great Lockdown in April… But with the COVID-19 pandemic continuing to spread, many countries have slowed reopening and some are reinstating partial lockdowns to protect susceptible populations.”

She said the crisis is “far from over.” This year’s contraction will be the deepest since the Great Depression, with COVID-19 killing more than one million people and collapsing the global economy.

As we’ve explained in recent weeks, severe wealth inequality imbalances are developing, as the poor are getting poorer, and the rich are getting richer – the imbalance is directly connected with how governments and central banks distribute monetary and or fiscal stimulus, with much of it flowing to mega-corporations. IMF estimates at least 90 million people worldwide are set to fall into “extreme poverty” this year.

Gopinath wrote in the report that economic recoveries “everywhere face difficult paths back to pre-pandemic activity levels.”

The IMF said a speedy recovery in China had been a surprise, but warned the global rebound remains vulnerable to setbacks. It noted that “prospects have worsened significantly in some developing countries where infections are rising rapidly.”

“Preventing further policy setbacks,” the IMF said, “will require that policy support is not prematurely withdrawn.” It warned that sovereign debt loads are set to rise sharply:

“The global easing of monetary policy, while essential for the recovery, should be complemented with measures to prevent build-up of financial risks over the medium term, and central bank independence should be safeguarded at all costs. Needed fiscal spending and the output collapse have driven global sovereign debt levels to a record 100 percent of global GDP,” the report said.

As analysts on Wall Street reasses whether a Biden victory and Democratic Senate sweep would truly be such a negative for the market, the IMF has highlighted the importance of keeping the money tap flowing – at least in the near term.

“While low interest rates alongside the projected rebound in growth in 2021 will stabilize debt levels in many countries, all will benefit from a medium-term fiscal framework to give confidence that debt remains sustainable. In the future, governments will likely need to raise the progressivity of their taxes while ensuring that corporations pay their fair share of taxes, alongside eliminating wasteful spending,” the report said.

That wording seems extremely similar to Democratic Party talking points…

via ZeroHedge News https://ift.tt/3nPZll1 Tyler Durden

Real Vision senior editor Ash Bennington welcomes Tony Greer of TG Macro back to the Daily Briefing to make sense of big moves today in equities, bonds, and the dollar. Greer analyzes the latest CPI reading through the lens of the ECB’s piggy-back announcement that it too would let inflation run hot. Greer then breaks down today’s bond rally as the dollar retracement coincided with significant sector rotations in the S&P 500. Bennington and Greer then analyze the latest newsflow from Washington D.C, including the status of President Trump’s health, the progress of stimulus talks in Congress, and the outcome of the upcoming presidential election. In the intro, Ash speaks to editor Jack Farley about the latest earnings reports from U.S. banks JPMorgan Chase and Citigroup.

via ZeroHedge News https://ift.tt/3dnd265 Tyler Durden

Federal Judge Allows Clinton Foundation Whistleblower Complaint To Proceed, Rules IRS ‘Abused Its Discretion’ Tyler Durden

Tue, 10/13/2020 – 18:40

A US tax court judge is allowing a whistleblower complaint to proceed against the Clinton Foundation after finding that the IRS “abused its discretion” when it attempted to dismiss allegations of wrongdoing by the nonprofit, according to Just The News.

Judge David Gustafson found that whistleblower John Moynihan – a former Drug Enforcement Agency (DEA) official, and Larry Doyle, a corporate tax compliance expert “provided ‘specific credible documentation’ supporting their allegations” of potential legal violations by the Arkansas-based charity.

John Moynihan and Larry Doyle testify before Congress in December, 2018

Gustafson, who struck down the IRS’s request for a summary motion, said that the agency’s Whistleblower Office wrongly denied the pair’s claims on the basis of the IRS’s Criminal Investigation (CI) office saying in an email that the complaint was closed.

The judge said he had reason to believe from the evidence that the IRS and the FBI engaged in some investigative activity.

The record “fails to support the WBO’s conclusion that CI had not proceeded with any action based on petitioners’ information. Accordingly, we deny the motion on the grounds that the WBO abused its discretion in reaching its conclusion, because not all of its factual determinations underlying that conclusion are supported by that record,” Gustafson wrote. –Just The News

The judge also suggested that the FBI was involved in an IRS investigation – citing nonpublic information in his ruling which was contained within IRS records in which the whistleblowers relay their exchanges with law enforcement.

“The FBI in [redacted] has thanked us profusely and praised our report excessively. As one individual close to the investigation commented to me, ‘you and your colleagues have saved numerous federal agents thousands of hours of work.'”

Meanwhile, it was reported in late September that US Attorney John Durham is looking into the Clinton Foundation’s alleged tax issues.

The pair of whistleblowers are financial forensic investigators who believe that the Clinton Foundation may have violated IRS codes relating to the Organization and Operational Tests for a 501c3 public charity with specific details addressing Misrepresentations and Misuse of Donated Public Funds. On top of that, they also addressed their probable cause assertion that the Clinton Foundation acted as an agent in violation of IRS code and the Foreign Agent Registration Act. These whistleblowers also highlighted that private foundations, including the Gates Foundation, that have donated to the Clinton Foundation are themselves subject to taxation based on IRS codes relating to Donors’ Responsibilities. Ultimately, Doyle and Moynihan maintained that the Clinton Foundation could be subject to paying tax on anywhere from $400mm to potentially as much as $2.5 billion of revenue.

Doyle and Moynihan have amassed 6,000 documents in their nearly two-year investigation through their private firm MDA Analytics LLC.

“The investigation clearly demonstrates that the foundation was not a charitable organization per se, but in point of fact was a closely held family partnership,” said Doyle, who formerly worked on Wall Street and has been involved with finance for the last ten years conducting investigations.

“As such it was governed in a fashion in which it sought in large measure to advance the personal interests of its principals as detailed within the financial analysis of this submission and further confirmed within the supporting documentation and evidence section. –The Hill

And so, with Gustafson’s ruling, the case moves forward – with Moynihan and Doyle’s latest filing asking the court permission to take a deposition from the chief of accounting compliance for the state of Arkansas, Jimmy Corley. According to JTN, the court has sealed the request.

via ZeroHedge News https://ift.tt/2T4UzC5 Tyler Durden

Countries that are in the decline stages tend to lose their best and brightest.

What happens is that, as a country becomes more socialistic, it attracts thousands of new residents who are seeking free stuff.

They wish to cash in – to live off the state.

But someone has to pay for that free stuff. And of course, that means that the more productive people in the country are handed the tab.

As a country grows more socialistic, an ever-larger number of dependent people must be paid for by those who are productive. This, of course, diminishes the retained earnings of those who have been productive.

What happens then is that a quiet exodus begins to take place. The very people who are ordered to pay the bill for everyone else tend to look for greener pastures.

In most every case, the first inclination is to look for a better corner of the country in which to live. Generally, it’s a location – a state, a city, a town – where the taxes are less, the crime is lower and the level of freedom is greater.

After all, you don’t really want to leave your country; you just want to free yourself from the burdens your government is placing upon you.

Unfortunately, it’s that last bit that ultimately inspires expatriation.

Those who choose a partial exit – say to Florida, Texas, or even Puerto Rico – at some point discover that the government that had treated them as a cash cows, ready to be milked to pay for government’s increasing entitlements, does not wish to lose its herd of cows.

Sooner or later, the temporary relief of living in a location that’s a partial solution becomes a lesser relief. The trouble is: Once a government has been in the habit of treating its productive class as cash cows – and has put in place the laws that allow it to milk them – it rarely relinquishes its grip on them for long.

Essentially, this means that at some point, the light is switched on in the mind of a particular cow – the realisation that the ultimate objective is to get beyond the borders of governmental control.

I’ve found, over the years, that those who are planning an exit tend to do it quietly.

But why should this be so?

Well first, they realise that their move will not be popular and they don’t wish to be explaining themselves to others. Second, they want it to go smoothly and they’d rather slip away than have anyone try to get in their way.

Therefore, the early exiters tend not to be noticed. Their numbers are small in comparison to the numbers of incoming largesse-seekers.

So, what happens to those who are now becoming aware that their government is bleeding them dry? Since they tend not to be aware that others have exited before them, they’re likely to feel quite alone, which is a great deterrent to their own inclination to leave. Since they don’t know anyone else who’s made an exit, it’s understandable if they feel that leaving simply isn’t an option.

What, then, is the tendency in such people? How do they deal with the situation?

Well, for the most part, they tend to tolerate the injustice, even though further weight continues to be added to the millstone around their necks.

But they do say, “This isn’t fair. We’re not going to take much more of this.”

And the key here is in those last four words. For the great majority of those who are oppressed by an overreaching government, the trigger never quite gets pulled. Instead, with every new burden, they tend to say, “Not much more.”

And governments recognise that, as long as the burden is added gradually, most people are foolish enough to tolerate the increases endlessly.

As Desmond Tutu said, “If you are neutral in situations of injustice, you have chosen the side of the oppressor.”

Quite so. People can only be dominated if they accept domination.

The numbers that actually pull the trigger and leave are therefore quite low.

And in this there’s an advantage: Although thousands are now leaving the US every year and their numbers are growing, they are not at present in the millions or even in the hundreds of thousands.

It’s for this reason that those who choose to cease being milk cows may still make a fairly quiet exit.

At present, there’s an exit tax, but its threshold is relatively high. And although the government has begun to disallow travel offshore, those who are persistent can still find an opportunity to do so.

However, this possibility may cease in the near future.

As economic woes worsen in the US, more people will decide that they don’t wish to have their government lessen the ability to make a living and raise taxes to pay for the government’s loss in revenue.

Even now, the exit door is beginning to close, as the government realises that the trend has begun.

Unknown to most Americans, all of the restrictions needed to literally close the doors on the departure of both wealth and people have been passed into law, primarily under the USA PATRIOT Act of 2001 and the National Defense Authorization Act of 2011.

These restrictions are not yet implemented. They’re intended to be implemented automatically, should a president declare a national state of emergency for any reason.

If, for example, an economic crisis were to unfold, as it’s presently doing, it’s likely that a state of emergency would be declared.

Therefore, for any milk cow who is considering an exit to greener pastures, the window of opportunity may well close relatively soon.

Those who may love their country, but do not love what it’s become, may choose to leave the herd whilst greener pastures remain an option.

* * *

The prospect of a disputed US presidential election amid the global pandemic is not only a possible scenario but a likely one. It could lead to enormous and unprecedented effects, such as mass unrest in American cities, stock market convulsions, a dollar collapse, and much more. That’s precisely why making the right moves in today’s turbulent political, financial, and social environment is absolutely crucial. For the first time, legendary investor Doug Casey is joining the world’s top economists, geopolitical analysts, investors, military experts, historians, and Washington, DC insiders to bring you actionable information on what comes next, including what you can do right now to prepare. Click here for all the details.

via ZeroHedge News https://ift.tt/371znoD Tyler Durden

Airbus-Boeing Ruling: WTO Greenlights EU Tariffs On $4 Billion In US Goods Tyler Durden

Tue, 10/13/2020 – 18:00

The European Union has won the right to impose tariffs on about $4 billion in Boeing jets and other U.S. goods annuallyunder an almost unprecedented World Trade Organization (WTO) ruling on Tuesday.

It follows last year’s WTO ruling that gave Washington a green light to impose tariffs on $7.5 billion in EU goods over state support for Airbus from European countries.

Via Reuters

Top US trade negotiator Robert Lighthizer reacted by saying the EU has “no lawful basis to impose tariffs” given that subsidies for Boeing were already repealed.

While the European Commission is not expected to move forward with tariffs immediately, now expressing strong support for a negotiated settlement to the WTO’s longest such dispute since the trade body’s inception (at 16 years), Lighthizer warned, “Any imposition of tariffs based on a measure that has been eliminated is plainly contrary to WTO principles and will force a U.S. response,” as quoted in The Wall Street Journal.

Airbus said it supports any action the EU takes. Meanwhile Airbuse responded that the company is “ready to support a negotiation process that leads to a fair settlement,” but remains supportive of any EU action on the matter. “It is time to find a solution now so that tariffs can be removed on both sides of the Atlantic,” Airbuse Chief Executive Guillaume Faury said.

Brussels has held out of the possibility that it’s ready to move on tariffs without negotiations, hoping to leverage pressure and urgency just three weeks before the US presidential election.

Reuters noted that “It has already drawn up an extensive list of U.S. products it could target including wine, spirits, suitcases, tractors, frozen fish, and a range of agricultural produce from dried onions to cherries.”

“We welcome the publication of the @wto decision on the countermeasures the EU can impose in respect of US subsidies to Boeing as a necessary, final step in the Airbus/Boeing litigation.”

“European sources have said the EU could also add tariffs on a further $4 billion of U.S. products left over from an earlier WTO case, giving it firepower similar to that Washington won in last year’s WTO ruling,” Reuters added.

Tuesday’s ruling will no doubt inflame White House criticism of the Geneva-based trade body, given it’s a massive and almost unprecedented penalty, and given the impossible to ignore geopolitical angle baked into the relationship between the two aviation giants on either side of the Atlantic.

via ZeroHedge News https://ift.tt/2SReK6f Tyler Durden

JPMorgan’s Kolanovic Has A Warning For Those Expecting A Crushing Biden Victory Tyler Durden

Tue, 10/13/2020 – 17:40

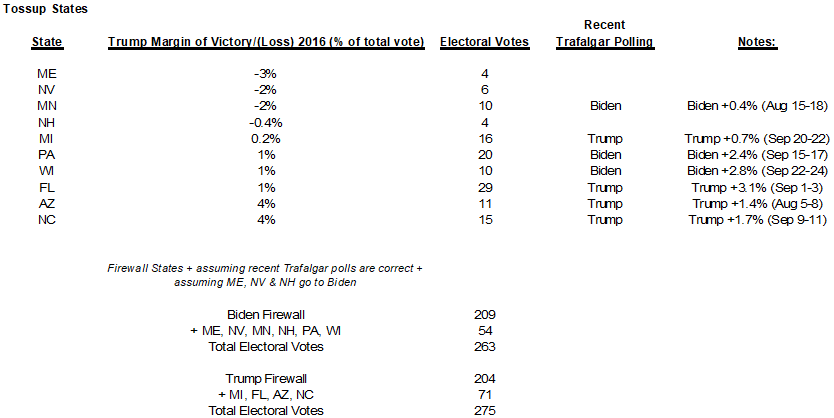

Perhaps it was our article from last Friday which showed that contrary to most popular polls predicting a Blue Wave sweep on Nov 3, a recent analysis by the Trafalgar Group (which correctly called the outcome of the 2016 election) found that a Trump victory and Republicans holding the Senate were the two most likely outcomes on election day. Or perhaps it was just general nerves over the upcoming election, which will be contested according to the latest BofA Fund Manager Survey …

… but whatever the reason, JPMorgan’s top quant Marko Kolanovic wrote and interesting note yesterday in which he said that clients have been asking him “what data in addition to polls are available to assess possible US election outcomes in various states.”

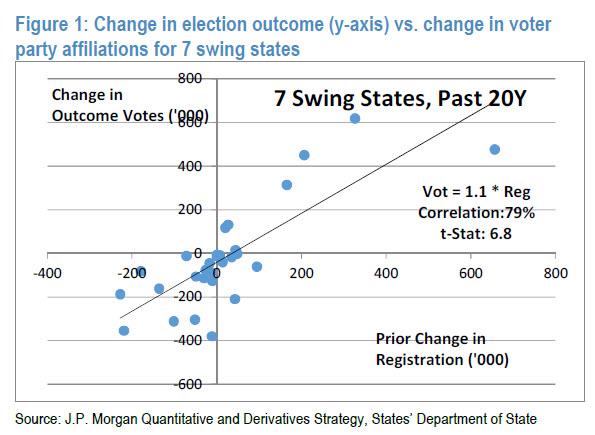

To answer this question, Kolanovic said that he looked at the historical changes in voter registration data and back-tested their relevance to election outcomes.

Why? Because according to Marko, it is intuitive that “if more voters register for a party, that they will also vote for that party.” However, being a quant, Kolanovic immediately focused on the causative, not correlative aspects of this observation, and as he puts it, “the question is how significant the relationship is and what is the “beta” of additional registered voters to actual votes.” The chart below shows data for seven battleground states that provide these data and presidential elections over the past 20 years.

Looking at the chart above, Kolanovic finds that changes of voter registration (change in registered D, R, D-R), is a significant variable in predicting the voting outcomes, a critical observation which virtually no existing polls takes into account since it would indicate that Republicans have a high likelihood of winning virtually all battleground states!

The regression above indicates that the change in D-R (Democrats less Republicans) registrations highly correlates with the subsequent change in D-R voting outcomes. Kolanovic also notes that historically, the “beta” was averaging 1.1 across states, a relatively high number which can be explained by large pools of independent voters (in fact, there is positive correlation between the registration “beta” and fraction of independent voters in a state).

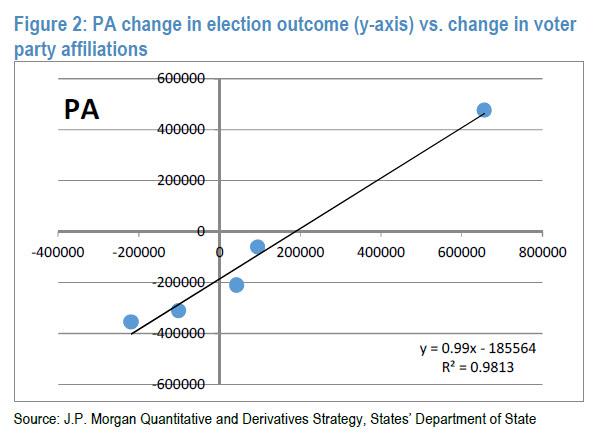

The JPM strategist next looks at an example of this analysis in the case of arguably the most important swing state for the upcoming election: Pennsylvania (PA). PA has a particularly strong relationship between voter registration and election outcome, according to Kolanovic, and in Figure 2 below he shows the relationship between changes in voter registration (D-R) and subsequent changes in election outcome (D-R vote count).

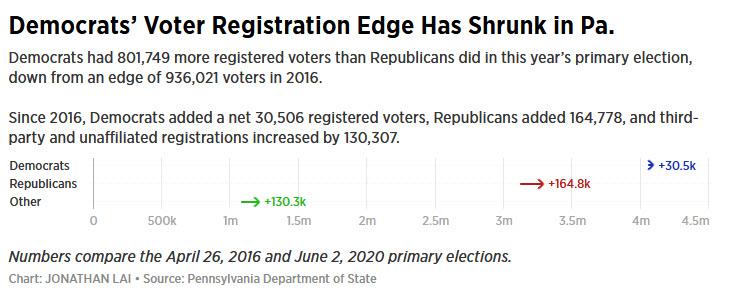

Three months ago, the Philadelphia Inquirer conducted a similar analysis when it found that “since the 2016 primary election, Republicans have added about 165,000 net voters, while Democrats added only about 30,000. Democrats still maintain an 800,000-voter edge over Republicans. But that’s down from 936,000 in 2016, when Trump still won the state by less than 1%.”

“Look, the president won our state by 44,000-plus votes in 2016,” said Lawrence Tabas, chair of the Pennsylvania Republican Party. “We have since picked up and narrowed the gap between us and the Democrats [by 135,000]. So we were already ahead 44,000, and look what we’ve picked up. I predict we’re going to narrow the gap further between now and November.”

While the other swing states with available data typically show a weaker relationship, in most cases it is significant from a statistical standpoint.

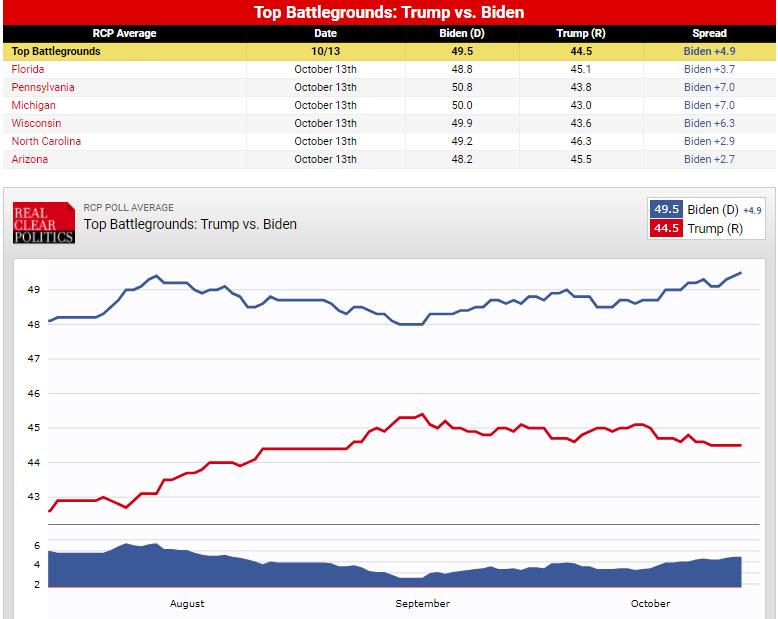

Finally, the punchline: what is the current change in voter registration over the past four years in swing states? This is shown in the table below.

Needless to say, if Kolanovic’s assumption is accurate, the change in voter registration data shown above would immediately invalidate all polls such as this one from Real Clear Politics showing Biden sweeping across the Battleground states. In fact, while he does not say it, the implication from the Kolanovic analysis is that Trump may well end up winning the critical trio of Pennsylvania (20 Electoral votes), Florida (29 votes) and North Carolina (15 votes).

Even more remarkable, the Kolanovic analysis means Trump could win Pennsylvania, something which not even the Trafalgar analysis of tossup states assumed.

Of course, lest he be seen as predicting Trump victory based on these data (something which last month prompted Nate Silver to have a hilarious meltdown on twitter), Kolanovic caveats that voter registration is only one variable in determining the election outcome, and “these results should not be taken as a prediction of state election outcomes.”

via ZeroHedge News https://ift.tt/33RNIC2 Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}