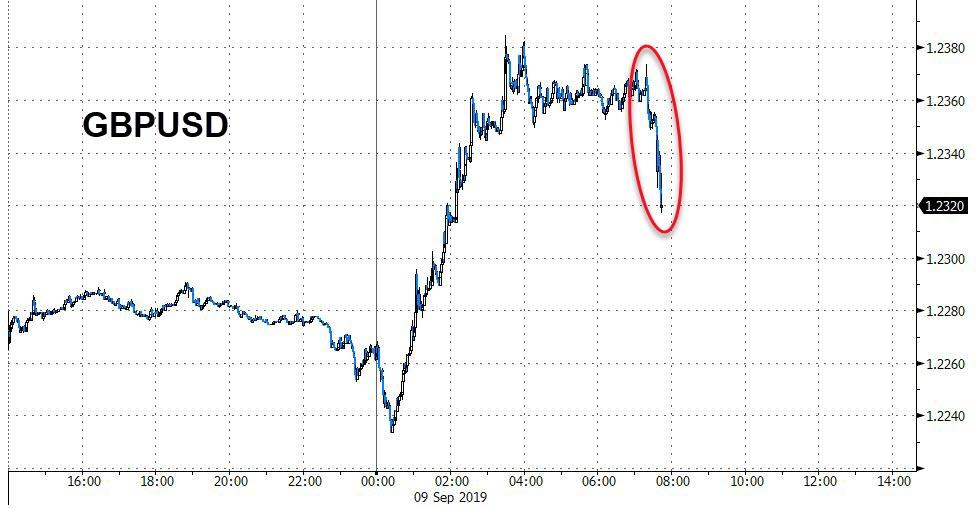

In the latest resignation announcement from a key figure in the UK government, Commons Speaker John Bercow, who has faced scrutiny and even an attempt by some of his fellow Toriesto oust him , said Monday afternoon (London Time) said he would stand down as Speaker by the end of October.

Bercow’s announcement prompted the pound to soften against the dollar.

Source: Bloomberg

The pound started to weaken earlier after the Queen assented to a law prohibiting a no deal Brexit.

Source: Bloomberg

Bercow said that if the Commons votes for an early general election, his tenure as Speaker and as an MP will end when this Parliament ends. And if MPs do not vote for an election, Bercow has concluded that the least disruptive option for him would be to stand down at the close of business on Oct. 31, according to the Guardian.

The votes on the Queen’s Speech are taking place early this week, and Bercow said it would make sense to have an experienced Speaker in the chair for those votes.

Globalization of natural gas markets, OPEC’s struggle to balance oil supply and price, and platinum coming to the fore as an investment vehicle are all covered in this week’s selection of essential charts from S&P Global Platts editors.

1. Global gas price differentials keep tightening…

What’s happening? Gas spot prices across regions have converged in recent weeks due to the continued gas glut in an increasingly globalized gas market, with surplus LNG cargoes struggling to find homes amid subdued demand in Asia. With limited European storage demand, coal-to-gas switching in Europe maximized and the global LNG surplus growing all the time, prices are now within a small $2/MMBtu range.

What’s next? With more US LNG set to come online over the next 12 months, the global gas glut could become even more severe, with a likely continuation of the gas price convergence into 2021 unless there is a significant supply disruption of some kind. And even then, prices could move together rather than diverge given the interconnected nature of the gas markets.

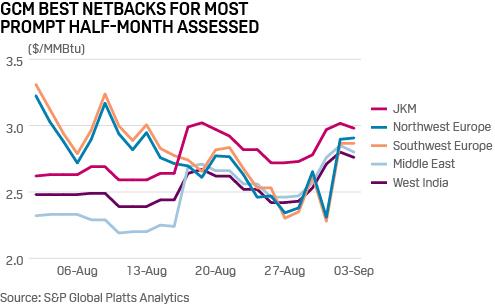

2. …and US LNG export economics start to favor Europe over Asia.

What’s happening? For prompt US Gulf Coast-loading spot LNG cargoes, price signals from Northeast Asia, represented by the Platts JKM, overtook those from Southwest Europe last month, as represented by the Platts SWE marker. US Gulf Coast netback price calculations take into consideration the cost of shipping to destination markets. In recent days, the trend has started to flip, favoring Europe.

What’s next? With six major US terminals now operating – four on the Gulf Coast and two on the East Coast – offtakers will be looking for the best bang for their buck heading into the fall and winter.

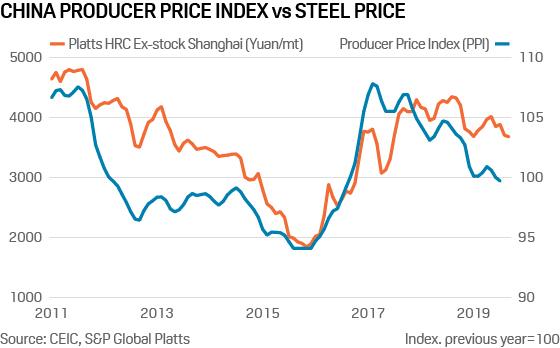

3. China steel prices suggest squeeze on manufacturers’ profits

What’s happening? Look out for the release of China’s producer price index (PPI) on Tuesday. In August, factory prices compared to the previous year fell for the first time in three years last month due to weaker domestic and export demand as a result of a slowing economy and no sign of respite in the ongoing trade tensions with the United States. Steel prices have historically been a good leading indicator and proxy for producer price inflation. If the past if any guide to the future, PPI data could show a further decline in August which is likely to be harbinger of weakening corporate profitability going forward.

What’s next? The Chinese government is determined to avoid the long term risk to the economy of excess credit. That means it’s unlikely we will see a major stimulus to boost demand. However, a modest credit injection in the coming months to offset the impact of weaker external demand, supporting domestic consumption and stabilizing factory gate prices, is a possibility.

4. OPEC struggles to lift oil prices despite cuts discipline

What’s happening? OPEC crude oil production edged up higher in August to 29.93 million b/d but is still 2.34 million b/d lower year on year. The cuts, along with US sanctions on OPEC members Iran and Venezuela, have contributed to tightening supplies, particularly of heavier and sour crudes. But the bloc is still struggling to move oil prices higher, with the market wary of a global economic slowdown.

What’s next? Several key OPEC members and their allies, including Russia, will gather Thursday in Abu Dhabi for a Joint Ministerial Monitoring Committee meeting, where traders will be watching closely for signals on potentially deeper cuts. OPEC, Russia and nine other oil producing countries are in the midst of a 1.2 million b/d in production curb agreement that runs through March 2020.

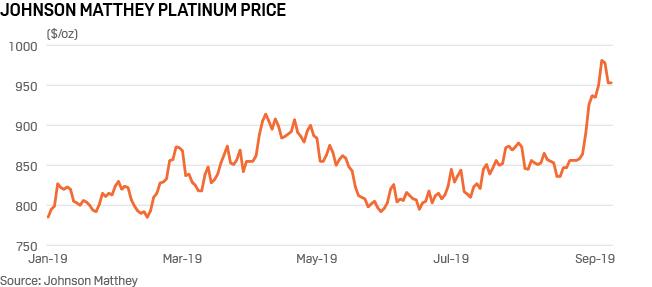

5. Platinum prices surge as investors look to new safe haven

What’s happening? Platinum has received a boost in recent weeks from the surge in gold prices, with spot bids around $940/oz on September 6. Negative interest rates have bolstered demand for gold and pushed prices sky-high in the process, driving investors towards platinum. In the first half of 2019, investment demand in platinum amounted to 855,000 oz, driven by a surge in exchange traded fund (ETF) holdings, which gained 720,000 oz, the World Platinum Investment Council said last week. That interest comes on top of a market that is much tighter than it was six months ago.

What’s next? Platinum’s fortunes may be closely tied to the outlook for palladium, which faces glaring deficits. In a 10 million oz palladium market, there was an 800,000 oz shortfall this year, and more than a 1 million oz potentially expected next year, according to WPIC. The metal is currently trading at more than $1500/oz The organization believes platinum will be considered as a serious substitute for palladium in ICE vehicles. That could mean there is potential for platinum prices to be pulled upwards.

6. German clean energy targets at risk as wind projects stall

What’s happening? German wind capacity additions have plunged after a record 20 GW was added over the past four years. Onshore wind is at a standstill with 10 GW of projects stuck in the permitting process due to aviation, military or ecological planning restrictions. Local opposition is growing in some regions, while coastal areas are already saturated causing grid bottlenecks.

What’s next? Germany targets a 65% share of renewables in the power mix by 2030 as coal is slowly phased out. Current growth trajectories lag behind that target, with market actors in crisis talks with the government ahead of climate policy decisions September 20. These could see offshore wind targets boosted, planning restrictions eased and the 52 GW solar ceiling cancelled.

Trump Gets Personal In Twitter Takedown Of GOP Challenger Mark Sanford

President Trump shredded former South Carolina Governor and congressman Mark Sanford, who announced his bid for the Republican presidential nomination on Sunday.

“When the former Governor of the Great State of South Carolina, @MarkSanford, was reported missing, only to then say he was away hiking on the Appalachian Trail, then was found in Argentina with his Flaming Dancer friend, it sounded like his political career was over,” tweeted Trump.

“but then he ran for Congress and won, only to lose his re-elect after I Tweeted my endorsement, on Election Day, for his opponent. But now take heart, he is back, and running for President of the United States. The Three Stooges, all badly failed candidates, will give it a go!“

…but then he ran for Congress and won, only to lose his re-elect after I Tweeted my endorsement, on Election Day, for his opponent. But now take heart, he is back, and running for President of the United States. The Three Stooges, all badly failed candidates, will give it a go!

Sanford made headlines in 2009 after it emerged that he had an extramarital affair with an Argentinian woman, which he and his wife, Jenny Sanford, attempted to cover up by fabricating a story that he was “hiking the Appalachians.”

The now-divorced father of four, who announced his run on “Fox News Sunday” with host Chris Wallace, became the third Republican challenge to Trump in 2020. The “Three Stooges” may find it tough sledding however after South Carolina and Nevada canceled their GOP primary contests for 2020, and committed all Republican delegates to Trump.

“We have a storm coming that we are neither talking about nor preparing for given that we, as a country, are more financially vulnerable than we have ever been since our Nation’s start and the Civil War,” Sanford wrote, adding “We are on a collision course with financial reality. We need to act now.”

Trump’s tweets on Monday morning targeting Sanders came minutes after the candidate concluded an interview on MSNBC’s “Morning Joe,” during which he defended his decision to take on the president.

Sanford declined to say whether he believes Trump is a Republican, pointed to polls he said showed roughly half of party members eager for a challenge to Trump, and claimed a robust primary debate would strengthen the GOP ahead of the general election. –Politico

“This is the equivalent of saying within the Republican Party, to all of those high school football teams across America, ‘Tell you what, guys: We are not going to scrimmage this week. We’ll be stronger by not scrimmaging. We’re just going to play on Friday night,” said Sanford. “And the coach would say, ‘Are you completely out of your mind?’ The American way is premised on competition.”

‘In 2014, 77.2 million workers age 16 and older in the United States were paid at hourly rates,representing 58.7 percent of all wage and salary workers. Among those paid by the hour, 1.3 million earned exactly the prevailing federal minimum wage of $7.25 per hour. About 1.7 million had wages below the federal minimum.

Together, these 3.0 million workers with wages at or below the federal minimum made up 3.9 percent of all hourly-paid workers. Of those 3 million workers, who were at or below the Federal minimum wage, 48.2% of that group were aged 16-24. Most importantly, the percentage of hourly paid workers earning the prevailing federal minimum wage or less declined from 4.3% in 2013 to 3.9% in 2014 and remains well below the 13.4% in 1979.’”

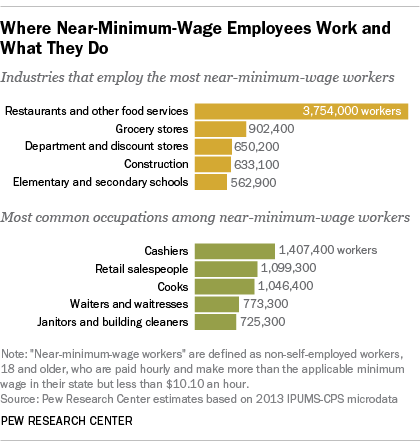

Hmm…3 million workers at minimum wage with roughly half aged 16-24. Where would that group of individuals most likely be found?

Not surprisingly, they primarily are found in the fast-food industry.

“So what? People working at restaurants need to make more money.”

Okay, let’s hike the minimum wage to $15/hr. That doesn’t sound like that big of a deal, right?

My daughter turned 16 in April and got her first summer job. She has no experience, no idea what “working” actually means, and is about to be the brunt of the cruel joke of “taxation” when she sees her first paycheck.

Let’s assume she worked full-time this summer earning $15/hour.

$15/hr X 40 hours per week = $600/week

$600/week x 4.3 weeks in a month = $2,580/month

$2580/month x 12 months = $30,960/year.

Let that soak in for a minute.

We are talking paying $30,000 per year to a 16-year old to flip burgers.

Now, what do you think is going to happen to the price of hamburgers when companies must pay $30,000 per year for “hamburger flippers?”

“Using a variety of methods to analyze employment in all sectors paying below a specified real hourly rate, we conclude that the second wage increase to $13 reduced hours worked in low-wage jobs by around 9 percent, while hourly wages in such jobs increased by around 3 percent.Consequently, total payroll fell for such jobs, implying that the minimum wage ordinance lowered low-wage employees’ earnings by an average of $125 per month in 2016.”

This should not be surprising as labor costs are the highest expense to any business. It’s not just the actual wages, but also payroll taxes, benefits, paid vacation, healthcare, etc. Employees are not cheap, and that cost must be covered by the goods or service sold. Therefore, if the consumer refuses to pay more, the costs have to be offset elsewhere.

For example, after Walmart and Target announced higher minimum wages, layoffs occurred (sorry, your “door greeter” retirement plan is “kaput”) and cashiers were replaced with self-checkout counters. Restaurants added surcharges to help cover the costs of higher wages, a “tax” on consumers, and chains like McDonald’s, and Panera Bread, replaced cashiers with apps and ordering kiosks.

“The workers who worked less in the months before the minimum-wage increase saw almost no improvement in overall pay — $4 a month on average over the same period, although the result was not statistically significant. While their hourly wage increased, their hours fell substantially.

The potential new entrants who were not employed at the time of the first minimum-wage increasefared the worst. They noted that, at the time of the first increase, the growth rate in new workers in Seattle making less than $15 an hour flattened out and was lagging behind the growth rate in new workers making less than $15 outside Seattle’s county. This suggests that the minimum wage had priced some workers out of the labor market, according to the authors.”

Again, this should not be surprising. If a business can “try out” a new employee at a lower cost elsewhere, such is what they will do. If the employee becomes an “asset” to the business, they will be moved to higher-cost areas. If not, they are replaced.

Here is the point that is often overlooked.

Your Minimum Wage Is Zero

Individuals are worth what they “bring to the table” in terms of skills, work ethic, and value. Minimum wage jobs are starter positions to allow businesses to train, evaluate, and grow valuable employees.

If the employee performs as expected, wages increase as additional duties are increased.

If not, they either remain where they are, or they are replaced.

Minimum wage jobs were never meant to be a permanent position, nor were they meant to be a “living wage.”

Individuals who are capable, but do not aspire, to move beyond “entry-level” jobs have a different set of personal issues that providing higher levels of wages will not cure.

Lastly, despite these knock-off effects of businesses adjusting for higher costs, the real issue is that the economy will quickly absorb, and remove, the benefit of higher minimum wages. In other words, as the cost of production rises, the cost of living will rise commensurately, which will negate the intended benefit.

The reality is that while increasing the minimum wage may allow workers to bring home higher pay in the short term; ultimately they will be sent to the unemployment lines as companies either consolidate or eliminate positions, or replace them with machines.

There is also other inevitable unintended consequences of boosting the minimum wage.

The Trickle Up Effect:

According to Payscale, the median hourly wage for a fast-food manager is $11.00 an hour.

Therefore, what do you think happens when my daughter, who just got her first job with no experience, is making more than the manager of the restaurant? The owner will have to increase the manager’s salary. But wait. Now the manager is making more than the district manager which requires another pay hike. So forth, and so on.

Of course, none of this is a problem as long as you can pass on higher payroll, benefit and rising healthcare costs to the consumer. But with an economy stumbling along at 2%, this may be a problem.

“By eliminating jobs and/or reducing employment growth, economists have long understood that adoption of a higher minimum wage can harm the very poor who are intended to be helped.Nonetheless, a political drumbeat of proposals—including from the White House—now calls for an increase in the $7.25 minimum wage to levels as high as $15 per hour.

But this groundbreaking paper by Douglas Holtz-Eakin, president of the American Action Forum and former director of the Congressional Budget Office, and Ben Gitis, director of labormarket policy at the American Action Forum, comes to a strikingly different conclusion: not only would overall employment growth be lower as a result of a higher minimum wage, but much of the increase in income that would result for those fortunate enough to have jobs would go to relatively higher-income households—not to those households in poverty in whose name the campaign for a higher minimum wage is being waged.”

This is really just common sense logic but it is also what the CBO recently discovered as well.

The CBO Study Findings

Overall

“Raising the minimum wage has a variety of effects on both employment and family income. By increasing the cost of employing low-wage workers, a higher minimum wage generally leads employers to reduce the size of their workforce.

The effects on employment would also cause changes in prices and in the use of different types of labor and capital.

By boosting the income of low-wage workers who keep their jobs, a higher minimum wage raises their families’ real income, lifting some of those families out of poverty. However, real income falls for some families because other workers lose their jobs, business owners lose income, and prices increase for consumers. For those reasons, the net effect of a minimum-wage increase is to reduce average real family income.”

Employment

First, higher wages increase the cost to employers of producing goods and services. The employers pass some of those increased costs on to consumers in the form of higher prices, and those higher prices, in turn, lead consumers to purchase fewer goods and services.

The employers consequently produce fewer goods and services, so they reduce their employment of both low-wage workers and higher-wage workers.

Second, when the cost of employing low-wage workers goes up, the relative cost of employing higher-wage workers or investing in machines and technology goes down.

An increase in the minimum wage affects those two components in offsetting ways.

It increases the cost of employing new hires for firms

It also makes firms with raise wages for all current employees whose wages are below the new minimum, regardless of whether new workers are hired.

Effects Across Employers.

Employers vary in how they respond to a minimum-wage increase.

Employment tends to fall more, for example, at firms whose sales decline when they raise prices and at firms that can readily substitute machines or technology for low-wage workers.

They might reduce workers’ fringe benefits (such as health insurance or pensions) and job perks (such as employee discounts), which would lessen the effect of the higher minimum wage on total compensation. That, in turn, would weaken employers’ incentives to reduce their employment of low-wage workers.

Employers could also partly offset their higher costs by cutting back on training or by assigning work to independent contractors who are not covered by the FLSA.

Macroeconomic Effects.

Reductions in employment would initially be concentrated at firms where higher prices quickly reduce sales. Over a longer period, however, more firms would replace low-wage workers with higher-wage workers, machines, and other substitutes.

A higher minimum wage shifts income from higher-wage consumers and business owners to low-wage workers. Because low-wage workers tend to spend a larger fraction of their earnings, some firms see increased demand for their goods and services, which boosts the employment of low-wage workers and higher-wage workers alike.

A decrease in the number of low-wage workers reduces the productivity of machines, buildings, and other capital goods. Although some businesses use more capital goods if labor is more expensive, that reduced productivity discourages other businesses from constructing new buildings and buying new machines. That reduction in capital reduces low-wage workers’ productivity, which leads to further reductions in their employment.

Don’t misunderstand me.

Hiking the minimum wage doesn’t affect my business at all as no one we employee makes minimum wage. This is true for MOST businesses.

The important point here is that the unintended consequences of a minimum wage hike in a weak economic environment are not inconsequential.

Furthermore, given that businesses are already fighting for profitability, hiking the minimum wage, given the subsequent “trickle up” effect, will lead to further increases in automation and the “off-shoring” of jobs to reduce rising employment costs.

In other words, so much for bringing back those manufacturing jobs.

Purdue Pharma Expected To File Bankruptcy Amid Settlement Negotiations “Hitting An Impasse”

The makers of Oxycontin, Purdue Pharma, are now expected to file for bankruptcy after settlement talks regarding the nation’s opioid crisis have “hit an impasse”, according to ABC News.

This impasse puts Purdue’s federal trial over the opioid epidemic on track to start next month and sets the stage for significant legal drama involving state and local governments.

Purdue had been working for months to try and avoid trial by determining the company’s responsibility for the crisis, which has cost over 400,000 Americans their lives. But an email from the attorneys general of Tennessee and North Carolina revealed that Purdue and the Sackler family had rejected two offers from the states over how payments would be handled as a result of a settlement.

Tennessee Attorney General Herbert Slatery and North Carolina Attorney General Josh Stein wrote in their message:

“As a result, the negotiations are at an impasse, and we expect Purdue to file for bankruptcy protection imminently.”

The failure to settle could set up “one of the most tangled bankruptcy cases in the nation’s history.” It would leave almost every state and 2,000 local governments that have sued the drugmaker to fend for themselves in bankruptcy court for the company’s remaining assets. Purdue had already threatened to file bankruptcy earlier this year, but was holding off while negotiations continued.

The Sackler family is being sued separately in at least 17 states, and its unclear what the bankruptcy means for them. Meanwhile, the family is believed to have transferred most of its multi-billion dollar fortune overseas.

Pennsylvania Attorney General Josh Shapiro says he will now sue the Sackler family, as other states have:

“I think they are a group of sanctimonious billionaires who lied and cheated so they could make a handsome profit,” he said. “I truly believe that they have blood on their hands.”

Purdue and the Sackler family had already settled for $270 million with the state of Oklahoma to avoid trial. Under one proposed settlement, the company would have entered into a structured bankruptcy that was said to have been worth $10 billion to $12 billion over time. This would have included $3 billion from the Sackler family, which would have given up its control of Purdue and contributed $1.5 billion more by selling Mundipharma, another company they own.

Shapiro has said that what the company was offering was not worth $10 billion to $12 billion. In their latest offers, the states looked to assure that the $4.5 billion from the Sackler family would be paid, but the family “refused to budge”.

Tennessee’s Slatery and North Carolina’s Stein said that states are already preparing to handle bankruptcy proceedings. They wrote:

“Like you, we plan to continue our work to ensure that the Sacklers, Purdue and other drug companies pay for drug addiction treatment and other remedies to help clean up the mess we allege they created.”

The nearly 2,000 cases filed have been consolidated under a single federal judge in Cleveland. Most of these lawsuits also name other opioid makers, distributors and pharmacies, some of whom are working on their own settlements.

Facing hundreds of other lawsuits in state courts, Purdue has sought a wide-ranging deal to settle all cases against it.

This impasse comes about six weeks before the scheduled start of the first federal trial under the Cleveland litigation. Filing for bankruptcy would “most certainly” remove Purdue from the trial and the bankruptcy judge would have wide discretion on how to proceed.

It’s not a secret: OPEC has painted itself into a corner by relying exclusively on supply control to be able to manipulate international oil prices in a way that is favorable for its members.

Right now, prices are depressed and that has nothing to do with supply. Could OPEC’s grip on oil prices be slipping irreparably?

When OPEC first announced that its members had agreed to put a cap on their production to reverse a steep drop in prices, it worked. Prices had been pushed to lows last seen more than a decade ago by the U.S. shale boom and OPEC’s own attempt to halt it by turning the taps on to maximum flow. When OPEC said it would reduce this flow, prices rebounded, providing much-needed relief to oil-reliant economies in the Gulf—it also provided relief to oil producers around the world, including the U.S. shale patch.

The shale patch recovered so well that now U.S. oil production is at an all-time high with the country last year becoming the world’s largest producer. Meanwhile, OPEC and its partners led by Russia decided to cut again. This time, however, the cuts didn’t work. Prices remained subdued save the occasional short-lived rally. While it’s true Brent and WTI are both higher than they were before the second round of cuts was announced, the international benchmark is much lower than OPEC’s largest producers, notably Saudi Arabia, need it to be.

The reason these cuts aren’t working is that market movers are not watching them. They are watching the tariff match between Washington and Beijing—a match that could hurt global oil demand. According to forecasters, it is already hurting it and as a result, it is hurting prices.

“OPEC’s burden is to show that it still has the appropriate tools to arrest price declines driven in no small part by White House policy,” RBC’s head of commodity strategy, Helima Croft, said in a note to clients as quoted by CNBC this week.

“It may prove easier to clean up the physical market than to overcome skepticism about the ultimate efficacy of its strategy in the age of Trump,” Croft added.

“The recent crash of 2014-16 demonstrated the reduced impact that OPEC now has on oil prices. While OPEC was announcing production cuts, the US onshore shale boom easily counteracted any upward price pressure. Currently, sanctions on Iran and Venezuela continue to undermine the influence of OPEC,” Jason Lavis, partner at oil industry platform Drillers.comtold Oilprice.

When OPEC+ met last December, the partners agreed to take off a combined 1.2 million bpd from the global oil market. This July, they agreed to extend the cuts to the end of the year or even early 2020. Yet the cartel’s total production is actually down by more than 1.2 million bpd: U.S. sanctions on Venezuela and Iran have hurt these countries’ production rates severely. Even so, Brent is stubbornly hovering around $60 a barrel. The trade war worry, coupled with the relentless rise in U.S. production, has played a bad trick on OPEC.

It seems the only way to achieve higher prices would be to cut deeper. It is the only way that would make sense seeing as the maximum-production strategy failed spectacularly. However, deeper cuts would mean loss of market share, and any change in prices might not be substantial enough to justify this loss. In this context, it is highly doubtful that some OPEC members—and Russia, too—would agree to reduce their oil production by much more. This means OPEC might just need to sit on the sidelines and watch the trade war developments hoping for a deal: that could be the miracle the cartel needs to get the higher prices its members’ economies rely on. Whether a trade deal would push prices up to the $80 level Saudi Arabia needs is doubtful but in the end, anything higher would be better.

Hezbollah Shoots Down Israeli Surveillance Drone Over South Lebanon

Two weeks after the first significant Israel-Hezbollah exchange of fire since the 2006 war, Hezbollah announced Monday it has downed another Israeli drone in southern Lebanon, The Washington Postreports.

A Hezbollah media statement said the group had “confronted” the Israel drone with “appropriate weapons” near the southern town of Ramiyeh, indicating the small drone was shot down. The paramilitary group now has the drone in its possession.

However, the Israeli Defense Forces (IDF) denied its surveillance drone was shot down, only saying it had crashed in the pre-dawn hours of Monday morning. The IDF affirmed it had been conducting a reconnaissance mission in the area.

File image: Hezbollah flag and fighters in south Lebanon.

Simultaneously a separate IDF statement claimed Iran’s elite Quds Force had fired multiple rockets from Syria toward Israel, but noted all failed to hit their targets. While no proof or video was immediately offered to back it, the statement added, “We hold the Syrian regime responsible for events taking place in Syria” — which strongly suggests Israeli could be preparing to retaliate on sites in or near Damascus, or on positions in southern Syria.

Hezbollah has recently vowed to shoot down any Israeli aircraft violating Lebanese airspace after late last month twin Israeli drones mounted an attack on Hezbollah offices in south Beirut, and after another drone assassinated the commander of a Palestinian militant group (PFLP-GC) in the Bekaa Valley.

“I tell the Israeli army on the border — be prepared and wait for us,” Hezbollah Secretary-General Hassan Nasrallah said in a subsequent address. Indeed a week ago on Sunday Hezbollah’s retaliation began with an anti-tank missile attack on an Israeli military vehicle near the border, which video of the operation shows suffered a direct hit.

Many analysts have read the mounting tensions and new exchanges of fire as holding the potential to escalate into a renewed all-out Israeli-Lebanese war, similar to the month-long 2006 war.

Meanwhile, also on Monday there are as yet unconfirmed reports of possible Israeli airstrikes targeting Iranian forces in eastern Syria, specifically in the city of Albukamal on the Iraq border. A number of explosions were heard inside Albukamal city overnight; however, it’s unclear if foreign aircraft or drones were behind it.

Syrian opposition media outlets are reporting casualties from the alleged attack. As Haaretz summarizes of the unconfirmed reports:

Eighteen Iran-back militia members were killed in the strike, the British-based watchdog said on Monday. The Assad regime and Syrian state media didn’t report the incident.

If true we could be preparing to witness yet more build-up to major war between Israel and Iranian allies in the Middle East.

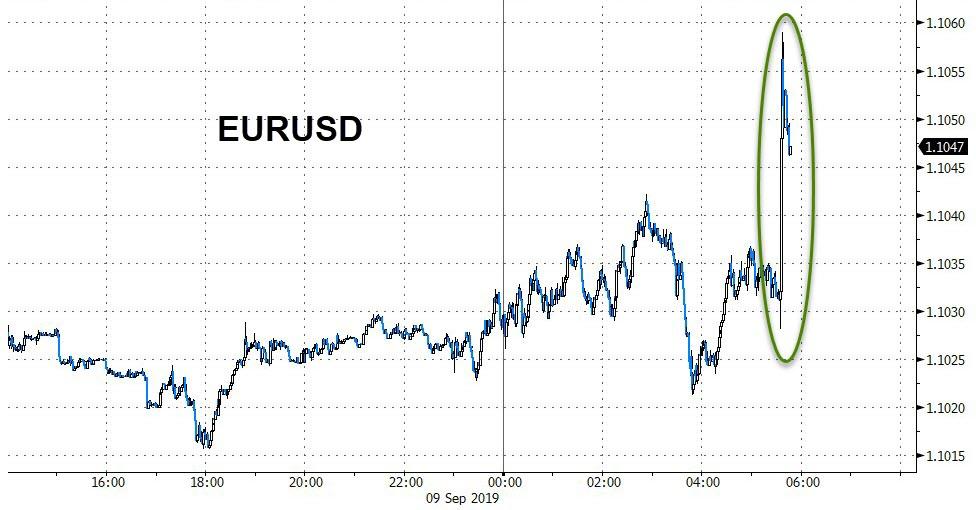

The euro and bund yields are rising this morning following Reuters headlines suggesting Germany is considering a “shadow budget” with the aim to increase public investments beyond restrictions of national debt rules.

Government officials are flirting with the idea of setting up independent public entities that would seize the historic opportunity of zero borrowing costs and take on new debt to increase investment in infrastructure and climate protection, said the officials, who all spoke on condition of anonymity.

The debt-financed spending of those independent public bodies would not be accounted for under the strict fiscal rules of Germany’s constitutionally enshrined debt brake, but only under the more lenient rules of the European Union’s Stability and Growth Pact, the sources said.

Which raised more than a few eyebrows (as @ljzaz summed up perfectly):

“What’s to stop Italy from creating their own ‘shadow budget’ then? (said everyone with half a brain)”

Additionally, as Bloomberg reports, deputy finance minister, Bettina Hagedorn, confirmed that the German government’s 2020 budget and financial planning through 2023 foresees balanced budgets with no new debt:

“Should there be a need for adjustment because of overall economic developments or external factors, it will be decided in the context of the budget planning and taking the coalition agreement into account.”

Perhaps it is this official statement (that merely echoes the same rhetoric Germany has used for years) that explains the market’s lack of enthusiasm…

Bund yields briefly rose…

Source: Bloomberg

But Euro is up 20-30 pips and fading back…

Source: Bloomberg

Notably, these headlines come ahead of the German lower house of parliament debating the 2020 budget and finance plan through 2023 on Tuesday.

Blain: Trump Picked A Great Moment To Declare Trade War Against China

Blain’s Morning Porridge, submitted by Bill Blain of Shard Capital

“There is a time to every purpose under heaven…”

It feels like Autumn has arrived. There is a chill in the air and cold rain, and that’s a real shame as I’m taking some very important clients out for a day’s sailing. The sun never shines on the righteous! Not only will they get cold and wet, but will have to listen to me blather on all day..

Is the changing of the seasons the theme for the coming week? Could be. Step back and look past the noise, and the global picture is all about long-term change.

In the US I’d argue the numbers show an economy slightly wobbled by the global trade ructions, but broadly on course. Trump may scream at the Fed to for ease – but is it needed? There are bigger long-term issues to address: themes such as income inequality, infrastructure, social programmes and education to resolve – but these have all been identified. If it wasn’t the partisan division in Washington and the chaotic leadership, they’d probably get addressed. They will in the future.

Is the US economy going to collapse on the back of trade war with China? No. There will be manageable inflation, some supply chain uncertainty and long-term the US will suffer a slowing effect from the Chinese economy no longer driving global growth. Addressing the long-term bubbles that have developed in equity markets, corporate and zombie debt, are going to be challenges. A turn around in the bond market will really hurt! A stock market reversal – they happen, and the sun comes up the next day.

China is in a more difficult position. Attitudes against it are polarising. Trump picked his moment to declare a trade war – just a time when poorly managed debt diplomacy was exposing the inequity of China’s plans to create its own global trade ecosystem. The fact China is now perceived as a global power makes it easier for the US to contain them – it’s not some poor third world nation they are looking to corral! The next few years will be as much about how China is increasingly contained, as about slowing growth. What the US really wants now is a Great Wall of China to keep them in as trade war morphs to cold-war.

China isn’t going to suffer and economic collapse on US tariffs, but it is sub-optimal and likely to push China growth lower earlier than the party strategists hoped, reducing the likelihood the nation can get rich before it gets old. The implications of a slowing China will be felt across whole globe. If China isn’t growing 6%, then that’s going to slow global growth. It will be felt most obviously in nations like Australia and other primary suppliers, but also elsewhere.

I’m tempted to say political risks may rise in China as it attempts to become increasingly self-reliant behind the walls the US will try to erect around them – the issues of the party delivering wealth, prosperity and critically, a clean environment, will be challenging, and could result in more aggressive China moves externally. Does that mean its time to invest in the US military industrial complex? Maybe.

What about Europe? This week the market is expecting big things from the ECB – I can’t imagine what they think they are going to change by further juicing the market? Sure, another boost to bonds, and infinity buying appetite? Whatever the ECB does in terms of a) cutting rates, b) reopening buy programmes, or c) promising to do (a) and (b) next month, will have precisely zero effect on European growth prospects. On the basis doing the same thing and expecting different results is just daft – the ECB needs to try something new.

Just how different will be the new Legarde regime at the ECB? Draghi must be thanking the gods he did a good job holding the Euro together – but didn’t face the impossibility of moving it forward politically with some form of fiscal agreement on how to genuinely reflate Europe. If they don’t then Europe sinks into increasing economic irrelevance. Speaking to a US hedge fund last week they told me they see Zero opportunities in Europe worth chasing.. they are waiting for a new crisis to buy it cheap.

And then there is the UK…

There is nothing more I can usefully add about the parliamentary Brexit shambles. Who resigns next? What will Boris surprise us with? Which Ditch? (Best suggestion on that one so far is HMP Ford (the open prison). Jeremy Corbyn anyone? Or the end of UK Politics?

What is more worrying is the long-term effect on the investibility of the UK as a result of the current shambles. I was speaking to a good chum who is a very successful real economist at a proper University last week. He asked about the risks of the UK losing its quasi-reserve/hedge status. That’s actually a really scary thought. At the moment the UK is perceived to be a reserve asset far out of proportion to our small population and low productivity economy.

The UK’s position in the global economy is boosted by factors such as London being the global centre of finance, our mercantile history, the fact English is the basis of contract and business law, the UK winning more than its fair share of Nobel prizes and our reputation for invention, and the fact the UK still owns the keys to money printing presses. (Europe does not – the ECB does.)

What happens to the UK’s above market weight if the currency continues to collapse on the back of the Brexit stramash, and the government starts to borrow heavily to cover the costs? Currency tumbles and deficits rise – not attractive. Could it ultimately result in the UK being seen as a failing state, and cost Sterling its reserve status? That could get very nasty….

As Deutsche Bank’s Jim Reid puts it, “If last week was back to school with a bang with Brexit and a bond market sell-off the highlights, this coming week has plenty more potential ‘boom’ moments.” The main highlight will be the ECB’s rate cut/QE restart on Thursday but today’s trip to Dublin from UK PM Johnson and the subsequent election vote later in Parliament (highly likely to be defeated) will be a “riveting” watch, especially with UK parliament set to be suspended later today; in data terms the highlights are US CPI (Thursday) and Friday’s US retail sales and UoM consumer confidence which last month fell to the lowest since October 2016.

With regards to what the ECB is expected to do, Reid reminds us that this will be President Draghi’s penultimate press conference before his term comes to an end. Deutsche economists expect the ECB to cut interest rates by 10bps at Thursday’s policy meeting, and they also anticipate a new system of reserve tiering, where some subset of reserves are exempted from the cost of negative interest rates, plus an enhanced version of forward guidance. While a shift to a symmetric inflation target or to a price level target would almost certainly be too radical for them to consider without a deeper policy review, they are likely to commit to some form of “lower for longer” rate guidance. There are also risks that they cut by more than 10bps, given the apparent lack of pushback by hawkish members of the Governing Council against a rate cut. There was more public pushback over the last few weeks against asset purchases, so that may be harder to agree on. DB’s economists nevertheless think a €30 billion per month purchase program is possible, though they could also see a more generous form of TLTROs if the ECB wants to focus on credit easing instead of measures that may flatten the curve.

Turning to Brexit, events are expected to continue to journey into the unknown this week. A vote in the House of Commons to hold an election will likely get defeated on Monday, with the opposition parties trying to force Johnson into asking the EU for an extension. The weekend papers were full of talk about the government working out whether they could sidestep the law with the Sunday Times reporting that the PM wants to even use the Supreme Court as an option. There was also talk of a PM resignation as one option being considered and even talk of the PM actively disobeying the law and perhaps facing a potential prison sentence if he does. As for the polls, after a torrid time in Westminster for the PM last week and over the weekend with another cabinet and party resignation, the Conservation Party have generally maintained their lead (between 3 and 14pts lead over 6 polls) but one poll suggested that if Brexit didn’t happen by October 31st then the lead would reverse and Labour would take a 2 point lead. This highlights why the opposition are gambling on denying an election this side of that date. The polls also show that hard tactics in Westminster are not necessarily damaging the governments support. However, the collateral damage to the party is significant so it’s high stakes for everyone.

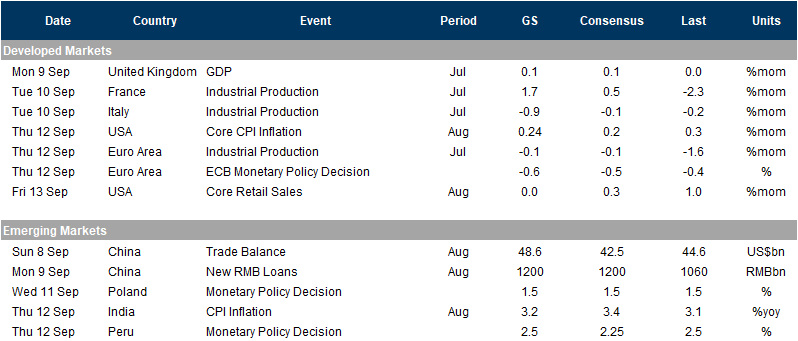

Below is a daily breakdown of key global events, courtesy of Goldman Sachs:

Monday: United Kingdom, GDP (Jul). GS +0.1%, consensus +0.1%, last 0.0%, all %mom. We expect GDP growth of +0.1%mom in July, a touch above growth in June. We see this marginal pickup as largely driven by services. Construction may contribute positively sequentially, while manufacturing is expected to decline, given recent PMI reports.

Tuesday: France, Industrial Production (Jul). GS +1.7%, consensus +0.5%, last -2.3%, all %mom. After a sharp decline of French industrial production in June, we expect a rebound in July in line with recent survey data pointing to an increase in sales and orders against decrease in inventories on the month; Italy, Industrial Production (Jul). GS -0.9%, consensus -0.1%, last -0.2%, all %mom. We expect Italian industrial production to contract further in July, given a sharp contraction in German industrial production and Italy’s trade links with Germany, notably in transport equipment. We expect the fall in Italian IP to reflect lower export orders in the auto industry, as noted by PMI reports last month.

Thursday: USA, CPI Inflation (Aug). GS Core CPI Inflation +0.24%, consensus +0.2%, last +0.3%, all %mom-sa. We estimate a 0.24% increase in August core CPI (mom sa), which would boost the year-on-year rate by two tenths to 2.4% on a rounded basis. Our monthly core inflation forecast reflects a modest further boost from the tariffs implemented in May and June, which we expect to manifest in the household furnishings, auto parts, and personal care categories. We also expect a large rise in the apparel category related to methodological changes earlier this year. On the negative side, we expect a pullback in airfares reflecting lower oil prices, and we expect a further deceleration in monthly used car inflation, which we nonetheless expect to remain positive. We estimate a 0.11% increase in headline CPI (mom sa), reflecting lower gasoline prices;

Euro Area, Industrial Production (Jul). GS -0.1%, consensus -0.1%, last -1.6%, all %mom. We expect Euro area industrial production (ex-construction) to show a small contraction on the month in July, in line with consensus. We expect the drop in German production as well as the expected contraction in Italian and Spanish production to weigh upon area wide IP;

Euro Area, ECB Monetary Policy Decision. Deposit Facility Rate: GS -0.6%, consensus -0.5%, last -0.4%. We expect ECB officials to deliver a three-pronged easing package at this meeting. First, we look for a 20bp deposit rate cut, flanked by a tiered reserve system, which we expect to focus on excess reserves. Second, we expect a QE programme within the current constraints and a clear time limit. Third, the Governing Council is likely to enhance its forward guidance with a stronger link to inflation and an emphasis on the symmetry of the inflation aim.

Friday: USA, Retail Sales (Aug). GS Core Retail Sales flat, consensus +0.3%, last +1.0%, all %mom. We estimate that core retail sales (ex-autos, gasoline, and building materials) were flat in August (mom sa), reflecting mean reversion in the non-store category following a record Amazon Prime Day in July. We also estimate a flat reading in the headline measure, and a 0.1% decline in the ex-auto measure, reflecting a rebound in auto sales but lower gas prices.

And visually:

Finally, focusing on the US, Goldman notes that the key economic data releases this week are the CPI report on Thursday and the retail sales report on Friday. There are no scheduled speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, September 9

There are no major economic data releases scheduled today.

Tuesday, September 10

06:00 AM NFIB small business optimism, August (consensus 103.5, last 104.7)

10:00 AM JOLTS Job Openings, July (consensus 7,311k, last 7,348k)

Wednesday, September 11

08:30 AM PPI final demand, August (GS flat, consensus flat, last +0.2%); PPI ex-food and energy, August (GS +0.1%, consensus +0.2%, last -0.1%); PPI ex-food, energy, and trade, August (GS +0.1%, consensus +0.2%, last -0.1%): We estimate a flat reading in headline PPI in August, reflecting relatively soft core prices as well as weaker energy prices. We expect a 0.1% increase in the core measure excluding food and energy, and also a 0.1% increase in the core measure excluding food, energy, and trade.

10:00 AM Wholesale inventories, July final (consensus +0.2%, last +0.2%)

Thursday, September 12

08:30 AM CPI (mom), August (GS +0.11%, consensus +0.1%, last +0.3%); Core CPI (mom), August (GS +0.24%, consensus +0.2%, last +0.3%); CPI (yoy), August (GS +1.81%, consensus +1.8%, last +1.8%); Core CPI (yoy), August (GS +2.37%, consensus +2.3%, last +2.2%): We estimate a 0.24% increase in August core CPI (mom sa), which would boost the year-on-year rate by two tenths to 2.4% on a rounded basis. Our monthly core inflation forecast reflects a modest further boost from the tariffs implemented in May and June, which we expect to manifest in the household furnishings, auto parts, and personal care categories. We also expect a large rise in the apparel category related to methodological changes earlier this year. On the negative side, we expect a pullback in airfares reflecting lower oil prices, and we expect a further deceleration in monthly used car inflation, which we nonetheless expect to remain positive. We estimate a 0.11% increase in headline CPI (mom sa), reflecting lower gasoline prices.

08:30 AM Initial jobless claims, week ended September 7 (GS 220k, consensus 215k, last 217k); Continuing jobless claims, week ended August 31 (consensus 1,678k, last 1,662k); We estimate jobless claims increased by 3k to 220k in the week ended September 7, after increasing by 1k in the prior week.

Friday, September 13

08:30 AM Retail sales, August (GS flat, consensus +0.2%, last +0.7%); Retail sales ex-auto, August (GS -0.1%, consensus +0.1%, last +1.0%); Retail sales ex-auto & gas, August (GS +0.1%, consensus +0.3%, last +0.9%); Core retail sales, August (GS flat, consensus +0.3%, last +1.0%): We estimate that core retail sales (ex-autos, gasoline, and building materials) were flat in August (mom sa), reflecting mean reversion in the non-store category following a record Amazon Prime Day in July. We also estimate a flat reading in the headline measure, and a 0.1% decline in the ex-auto measure, reflecting a rebound in auto sales but lower gas prices.

08:30 AM Import price index, August (consensus -0.5%, last +0.2%)

10:00 AM University of Michigan consumer sentiment, September preliminary (GS 89.5, consensus 90.4, last 89.8); We expect the University of Michigan consumer sentiment index declined by 0.3pt to 89.5 in the preliminary September reading, as recent economic misses could weigh on sentiment.

10:00 AM Business inventories, July (consensus +0.3%, last flat)

{kind=link}