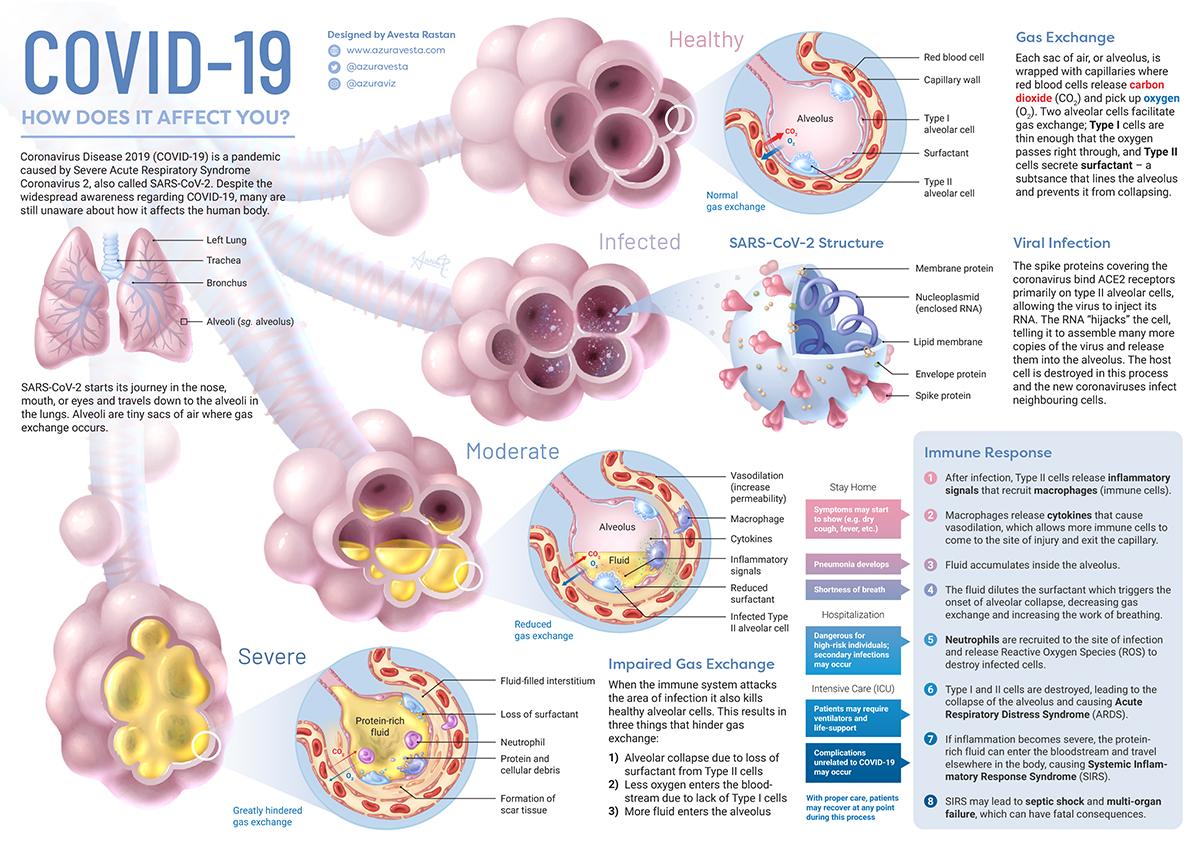

By now, researchers and health experts have gained a better understanding of the range of symptoms caused by COVID-19, which include fever, a dry cough, and of course, the dangerous inflammation of the respiratory system. Most of us know that COVID-19 can be much more severe than a typical flu, but, as Visual Capitalist’s Nick Routley explains below, lesser known are the mechanics behind how the virus causes pneumonia in its victims.

Today’s informative illustration, by scientific designer and animator Avesta Rastan, details the effects COVID-19 has on our lungs, from moderate to severe cases.

According to the World Health Organization (WHO), most people who contract COVID-19 only experience mild flu-like symptoms. Occasionally though, the infection can cascade into a severe case of pneumonia that can be lethal, especially for older people and those with underlying medical conditions.

Here’s what COVID-19 does to your body.

Infection

The virus, officially named SARS-CoV-2, enters the body – generally through the mouth or nose. From there, the virus makes its way down into the air sacs inside your lungs, known as alveoli.

Once in the alveoli, the virus uses its distinctive spike proteins to “hijack” cells. The primary genetic programming of any virus is to make copies of itself, and COVID-19 is no exception. Once the virus’ RNA has entered a cell, new copies are made and the cell is killed in the process, releasing new viruses to infect neighboring cells in the alveolus.

This process can occur initially without a person being aware of the infection, which is one of the reasons COVID-19 has been able to spread so effectively.

Immune Response

The process of hijacking cells to reproduce causes inflammation in the lungs, which triggers an immune response. As this process unfolds, fluid begins to accumulate in the alveoli, causing a dry cough and making breathing difficult.

For 80-85% of people infected by COVID-19, these symptoms will run their course much as they would with a case of the flu.

Severe Symptoms

In 15-20% cases, the immune system’s response to inflammation in the lungs can cause what’s known as a “cytokine storm”. This runaway response can cause more damage to the body’s own cells than to the virus it’s trying to defeat, and is thought to be the main reason for why the conditions of young, otherwise healthy individuals can rapidly deteriorate.

If enough alveoli collapse, acute respiratory distress syndrome (ARDS) can occur, requiring a patient to be placed on a ventilator for breathing assistance.

At this stage, the surfactant that helps keep alveoli from collapsing has been diluted, and fluid containing cellular debris is impairing the gas exchange process that supplies oxygen to our bloodstream.

In the most severe cases, systemic inflammatory response syndrome (SIRS) occurs as the protein-rich fluid from the lungs enters the bloodstream, resulting in septic shock and multi-organ failure. This is often the cause of death for people who have succumbed to a COVID-19 infection.

The Best Protection

Thankfully, COVID-19 isn’t a death sentence for most people who become infected, but the symptoms described above are not pleasant. Until a vaccine is developed, the best defense is avoiding infection altogether through frequent, thorough hand washing, and physical distancing as recommended by health authorities.

To see the full set of graphics, as well as other health and science related illustrations, visit Avesta Rastan’s website.

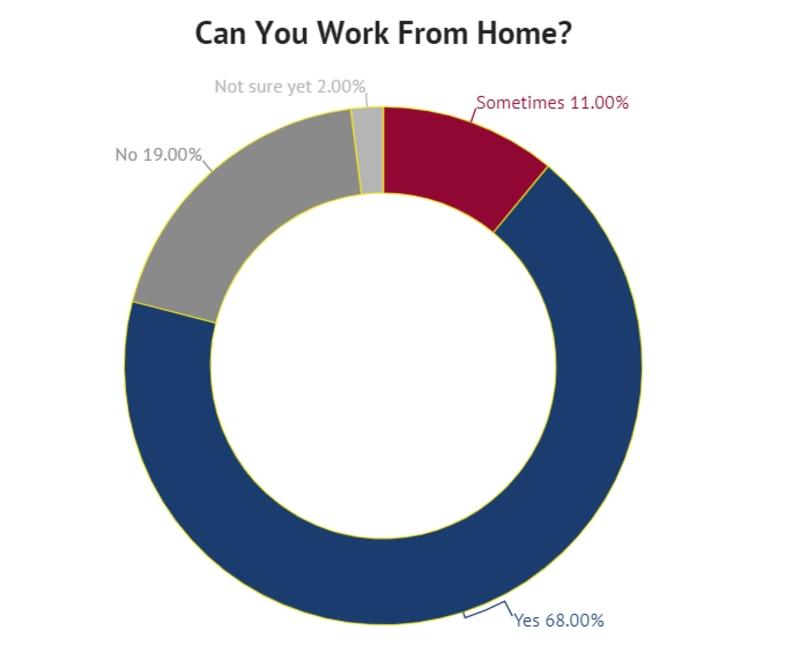

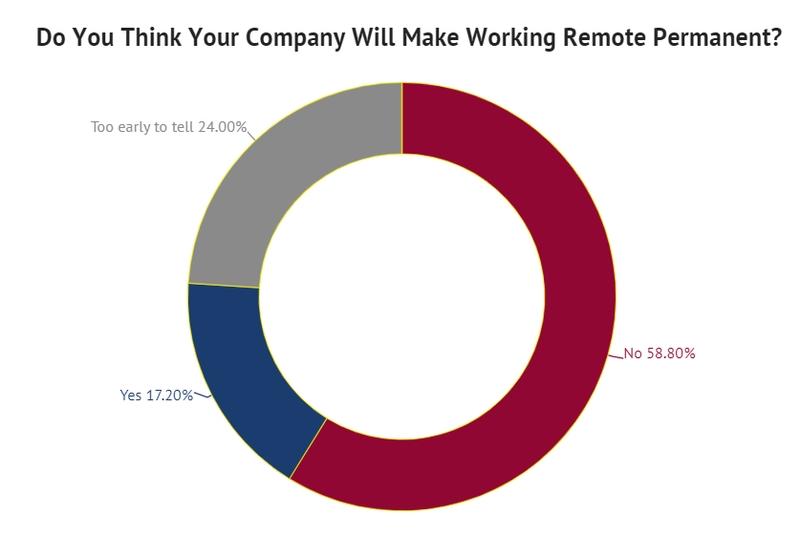

Two thirds of all American workers are able to work from home

75% of baby boomers want to work from home forever

Half of all Americans want to continue working from home following the coronavirus

The coronavirus, or COVID-19, has more people than ever working from home. With many states and cities closing down nonessential businesses, and others sure to follow, the number of workers working remotely will continue to grow in the coming days.

For many companies and workers that have never worked remotely this is all completely new. Companies hastily threw together guidelines and crossed their fingers in hopes that nothing would break. Workers wondered if it would all work.

We surveyed over 500 Americans to see how this unprecedented event is impacting the American worker. The survey found out how the coronavirus has affected Americans’ work lives– and if this event will fundamentally change how we work in the future.

Zippia found more than half of American workers prefer working from home and want to continue working from home when all this is over.

Below are some more highlights from Zippia’s survey:

Half of millenials want to work from home permanently

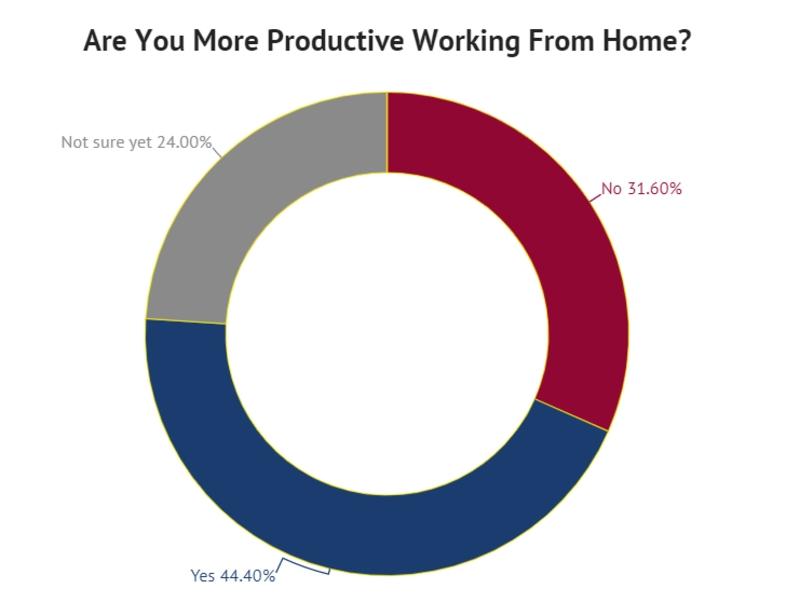

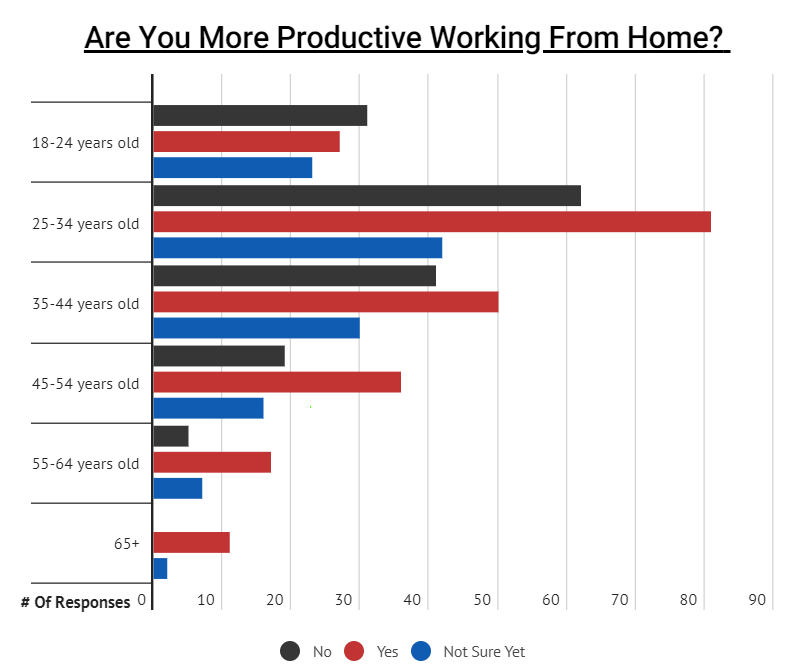

While most people feel more productive, older people feel significantly more productive working from home than younger workers

51% would rather work-from-home full-time than go into the office

More than half of Americans don’t believe their work will make remote work permanent

17% of Americans DO believe their work will let them work remotely following the crisis

Closing Thoughts On Remote Work During The Coronavirus

The coronavirus has launched a national work from home experiment of unprecedented size. Many Americans are finding that not only can they work from home– they are actually more productive than in the office.

While it is too soon to say how much this will change the way the American workforce works, many feel optimistic that their company will let them continue working remotely even after the threat is gone.

PC Shipments Plunge Most In Four Years As ‘Global Recession Begins’

A new report from research firm Canalys shows global PC shipments plunged 8% YoY for the first quarter, a drop of 4.6 million units from 58.3 million in 1Q19 to 53.7 million in 1Q20. The decline in PC shipments was the steepest since the global economy slowed in early 2016 when the research firm recorded a 12% decline.

We suspected that electronic manufacturers would take a sizeable hit from China shutdowns in 1Q20. Shortages of semiconductor parts and labor over the quarter didn’t help factories boost output.

Canalys said the top vendor for the global PC market was Lenovo, who shipped 12.8 million units, down 4.4% over the same quarter last year. HP was second with 11.7 million units shipped, or down 13.8%, followed by Dell with 10.5 million units, an increase of 1.1%. Apple suffered the sharpest decline in unit sales, down 20% to 3.2 million over the quarter.

Despite annual growth trends pointing down, Canalys research director Rushabh Dosh said there was some positive news as lockdowns across the world forced many people to work at home and upgrade PCs.

“The PC industry has been boosted by the global COVID-19 lockdown, with products flying off the shelves throughout Q1,” Doshi said. “But PC makers started 2020 with a constrained supply of Intel processors, caused by a botched transition to 10nm nodes. This was exacerbated when factories in China were unable to reopen after the lunar new year holidays.”

Canalys analyst Ishan Dutt warns that, while the production constraints will probably ease in 2Q, PC demand in 1Q won’t be sustained for long, and the outlook on the year is negative:

“As we move into Q2, the production constraints in China have eased. But the spike in PC demand seen in Q1 is not likely to be sustained and the rest of the year looks less positive. Few businesses will be spending on technology for their offices, while many homes will have been freshly equipped.

A global recession has begun – businesses will go bankrupt with millions of newly unemployed. Even governments and large corporations will have to prioritize spending elsewhere. Many parts of the tech industry have benefited from the early part of this extraordinary lockdown period, but we expect to see a significant downturn in demand in Q2 2020. With factories now reopened and virtually up to full speed in China, PC vendors will face a challenge to manage supply chain and production correctly over the next three to six months.”

Migrant-background youths staged a riot in Anderlecht, Belgium during which they trashed police vehicles and fired guns despite the city being under a coronavirus lockdown.

The unrest was triggered by an incident in which a 19-year-old identified as ‘Adil’ killed himself by colliding with a police van after running through a checkpoint on his scooter.

This prompted calls for a “protest” which quickly turned into a violent riot as the youths smashed up the police vehicle using bricks and concrete slabs.

An individual wearing a balaclava subsequently fired a handgun that had been stolen from police.

Brave bejaarden worden beboet als ze met twee te dicht bijeen op een bank durven zitten maar DIT blijft onbestraft? Zet het leger in… pic.twitter.com/a8czSgm9iv

“There was a new spike in violence, a more limited one, around 10 p.m., with stones thrown at a police station (windows were broken), but this was rapidly repressed by police, said local mayor Fabien Cumps.

Cumps said the mob had gathered not to pay respect to their dead friend but in order “to be violent.”

Police chief Patrick Evenepoel admitted that authorities didn’t initially intervene despite the illegal gathering and only acted “when we saw that groups of young people were arming themselves with rocks taken from construction sites in the area.”

All of this was in complete violation of Belgium’s coronavirus lockdown law, which bans gatherings of more than two people.

Twitter users pointed out the difference between the police’s approach to the initial gathering and them fining people for walking in the park.

There was a lightning-fast response on Belgian social media to the Anderlecht riots, with memes pointing at criminals paying zero for destroying police vans, while law-abiding citizens walking in the park get fined for breaking COVID-19 restrictions. pic.twitter.com/sGv0k4v0Ol

As we previously highlighted, lockdown laws are being ignored in numerous migrant ghettos across Europe.

The lockdowns are deemed so pointless that one French official even suggested opening up all the shops in migrant areas to prevent riots.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Private Army: Mark Zuckerberg’s Security Cost Facebook A Whopping $23 Million Last Year

Mark Zuckerberg, like a number of wealthy CEOs desiring to recieve “humble” compensation, has an official salary of just $1 a year.

However, according to a financial filing published last Friday, Facebook racked up a whopping $23 million for the company founder’s personal security and travel costs in 2019.

This includes “approximately $10,463,717” for “costs related to personal security for Zuckerberg at his home and during his personal travel.”

Getty Images

“Mr. Zuckerberg is one of the most-recognized executives in the world, in large part as a result of the size of our user base and our continued exposure to global media, legislative, and regulatory attention,” said the filing,

“He is synonymous with Facebook and, as a result, negative sentiment regarding our company is directly associated with, and often transferred to, Mr. Zuckerberg,” it continued.

Apparently this “negative sentiment” is such that it requires something akin to a private army or Zuck’s own secret service, given the massive personal security cost is approaching that of some heads of small foreign countries.

By comparison, Facebook spent $9.1 million for his security in 2017, and $20 million in 2018. The 2018 security expenditures broke down to about $20,000 a day to protect him.

The Facebook co-founder jogging accompanied by a ‘secret service’-style team of private security, via EPA.

The filing also shows Zuckerberg required $2.95 million for private aircraft costs. He spent $2.59 million on private air travel in 2018 and $1.52 million on it in 2017.

All of the expenses are filed under “Other compensation” for Zuckerberg.

Some reports have pointed to a series of “non-stop scandals” of the past two years which have put even more of a spotlight on Zuckerberg.

“It has been under fire for everything from personal privacy issues following revelations that data-firm Cambridge Analytica collected information on 87 million Facebook users, to enabling the spread of white supremacy and hate speech on the platform,” CNN notes. “Those events have drawn a large amount of exposure for the company and its 34-year-old co-founder.”

COO Sheryl Sandberg took home ~$875K in base pay last year, up from $843K the previous year, and she received a bonus of more than $902K, up from $638K in 2018, and $19.6M in stock awards, vs. $18.4M in stock awards in 2018.

Sandberg’s personal security cost $4.37M in 2019, up from $2.9M in 2018, and her use of private aircraft cost Facebook $1.3M in 2019 vs. $908K in 2018.

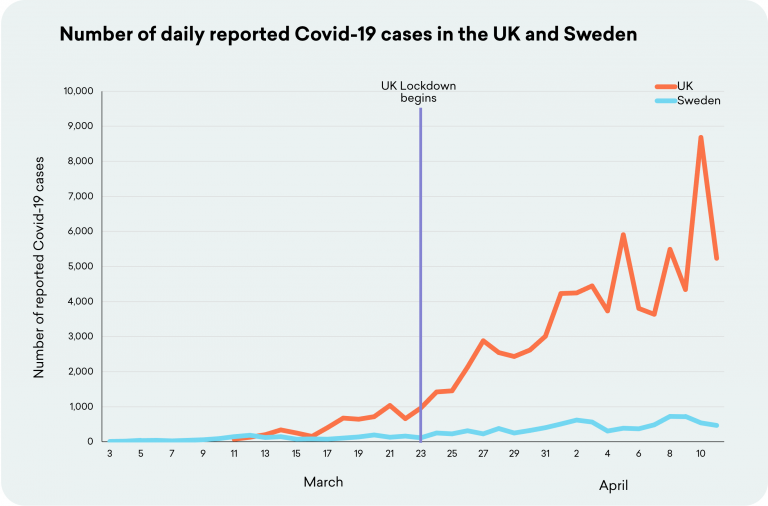

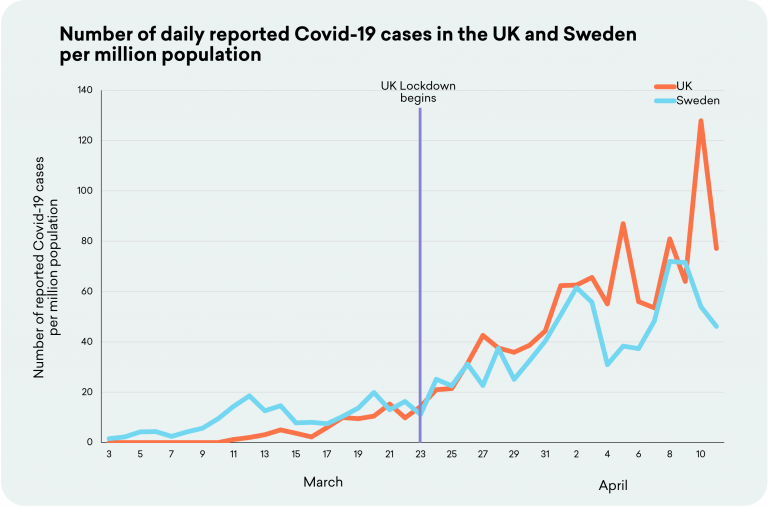

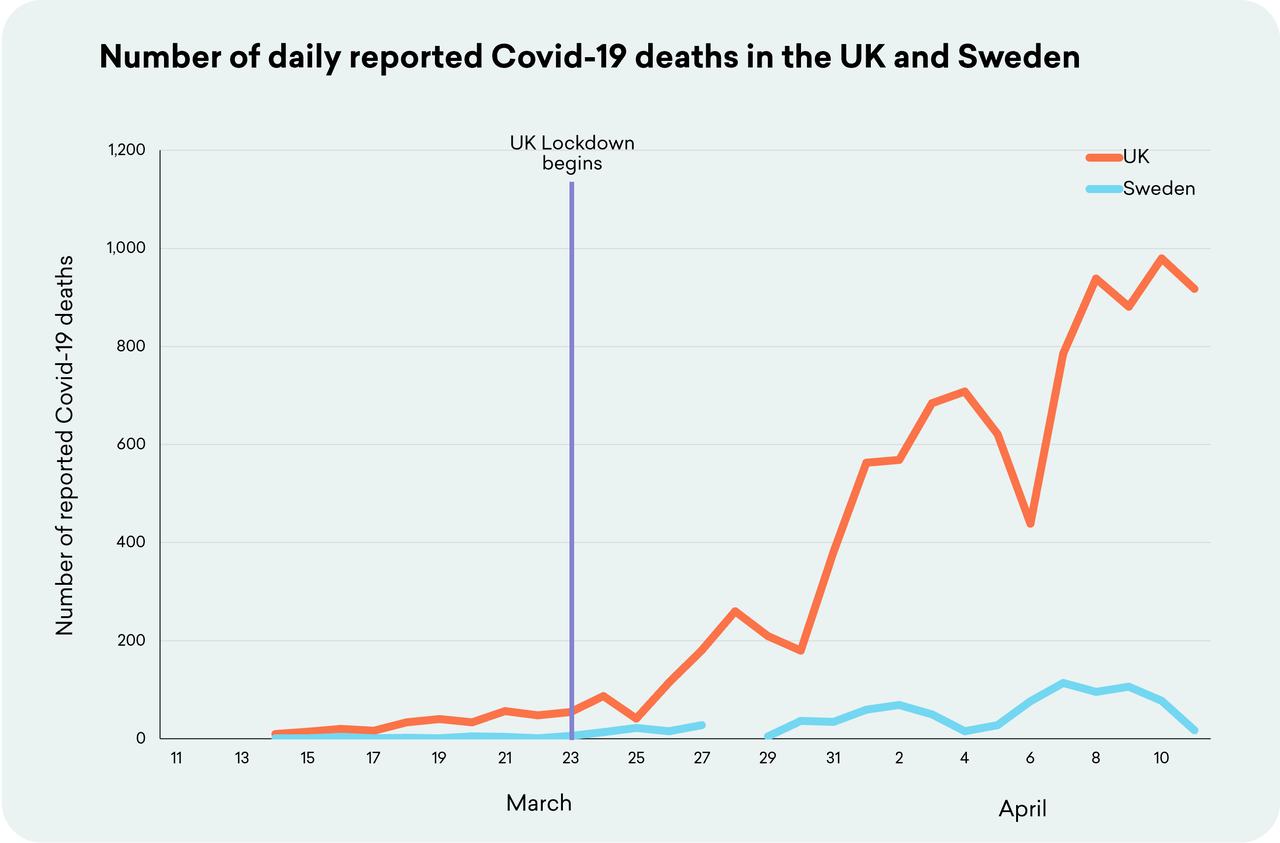

A Comparison Of Lockdown UK With Non-Lockdown Sweden

Update (0400ET): Stefan Lofven, Sweden’s prime minister, said today that after taking a “flexible” approach to restricting movements within its borders, the country’s coronavirus measures were “not good enough.”

Lofven, who has been PM since 2014 as part of a various coalitions, said previous governments and parties were responsible for the lack of equipment.

“All parties have a responsibility in that, because [civil defence] was something that was phased out gradually after the Cold War, so that’s three decades we’re talking about. Since then, many governments have contributed to this.”

A spokesman for the prime minister said last week:

“We want measures that work in the long run, since this pandemic likely will continue for months.”

So far as I am aware, Sweden remains the only major Western country that has not imposed a strict lockdown on its citizens to deal with the Covid-19 outbreak. Other than a ban on gatherings of 50 or more people, and advice such as over-70s being urged to stay at home, Swedish schools, shops, restaurants and pubs all remain open. It almost seems to me that the Government there has decided to treat grown adults like they are … well grown adults.

However, despite being a sovereign nation, with the right to set its own policy, it appears that this is not acceptable to the “international community”, and the Swedish Government is coming under huge pressure to change course. The World Health Organization (WHO), for instance, recently called for the nation to impose more restrictions, saying that it is “imperative” that Sweden:

“increase measures to control spread of the virus, prepare and increase capacity of the health system to cope, ensure physical distancing and communicate the why and how of all measures to the population.”

Donald Trump also felt the need to give his two cents as well:

“Sweden did that, the herd, they call it the herd. Sweden’s suffering very, very badly.”

But is Sweden really suffering very, very badly in comparison to other countries that have imposed severe restrictions? Is it really imperative that they change course and fall in line with what most other countries have done? Or do these calls proceed from a different motive entirely: a fear that Sweden’s comparatively measured approach of dealing with Covid-19 without introducing the most draconian civil restrictions ever seen and without crashing its economy might actually work and in so doing show the response of other countries to have been wildly disproportionate?

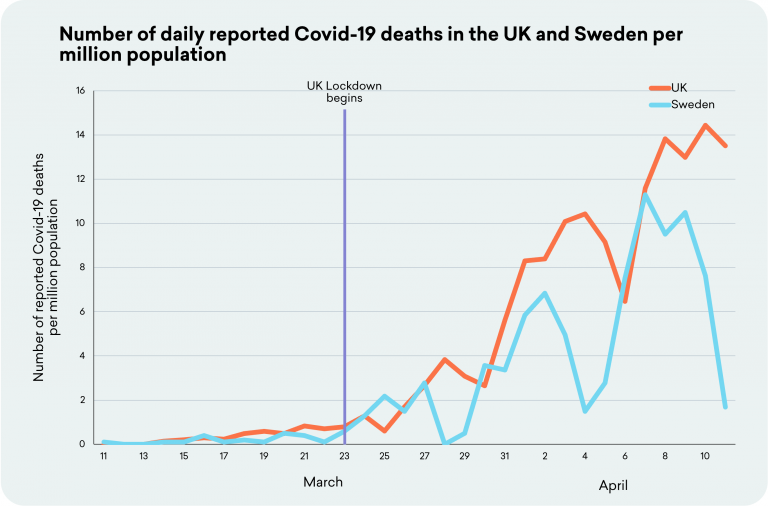

This is not something we should leave to a matter of opinion, so let’s instead look at what the data tells us. Below are four charts comparing the UK, which went into lockdown on 23rd March, with Sweden and its far more relaxed approach. All the data on these charts comes from the official reports from both countries up to and including 11th April (here and here). It comes with the caveats that of course this is by no means final and the situation may well change to produce a very different picture in the coming weeks, nor is it possible to know with any certainty whether both countries are counting their cases and deaths in a way that is consistent with one another. Nevertheless, since it is from official data sources, it is the best guide we currently have to what is happening in both countries.

(Note: Charts 1 and 3 compare cases and deaths in absolute terms. Charts 2 and 4 take into account the relative population sizes (UK = 67.9 million; Sweden = 10.10 million) by looking at the number of cases per million people).

Chart 1

Chart 2

Chart 3

Chart 4

(Note: In terms of timelines, Sweden reported its first Covid-cases eight days before the UK (15 on 3rd March, compared with 77 on 11th March in the UK), whilst the UK recorded its first deaths two days before Sweden (10 on 14th March, compared with 4 for Sweden on 16th March)).

Looking at these charts, particularly charts 2 and 4 which are a like-for-like comparison, as at 11th April, I think we can say the following:

In terms of reported cases, the data shows no evidence that the UK lockdown approach has been any more successful than the Swedish approach. In fact, per million people, Sweden has had fewer cases than the UK.

In terms of recorded deaths, again there is no evidence so far that the UK lockdown approach has been any more successful than the Swedish approach. In fact, per million people, Sweden has had fewer deaths than the UK.

As I say, the situation may well change as the days and weeks go by, but so far, according to the official data from both countries, the approach taken in the UK of keeping people in their homes and closing down huge swathes of the economy, has not had any more positive effect on reducing Covid-19 cases or deaths than the Swedish approach. Yet it will put millions out of work, it will destroy thousands of businesses, it will lead to a massive deterioration of mental health, it will lead to an increase in suicides, it will lead to old people dying on their own without their carers, and it already has led to an increase of state power on a scale never seen before. There is that!

COVID-19 Could Push An Extra Half A Billion People Into Poverty

Charity group Oxfam has warned that a global recession caused by Covid-19 could push an extra half a billion people into poverty – 8 percent of the world’s population – unless urgent action is taken.

Conducted by King’s College London and the Australian National University, the researchgauged the short-term impact of containing the coronavirus on global monetary poverty based on the World Bank poverty lines of $1.90, $3.20 and $5.50 a day.

As Statista’s Niall McCarthy details below, global poverty levels would increase under all three scenarios for the first time since 1990 according to the analysis with up to a decade of progress lost globally.

The impact is set to be even worse in some hard-hit parts of the world such as North Africa, Sub-Saharan Africa and the Middle East where up to 30 years of progress could be wiped out.

The most serious scenario involves a 20 percent fall in income which would result in an additional 548 million people earning less than the World Bank poverty threshold of $5.50 per day. The United Nations has warned that $2.5 trillion is needed to support developing countries during the crisis and that nearly half of all Africa’s jobs could be lost.

G20 ministers, The World Bank and the IMF met this weekend to discuss debt relief for poorer countries. Oxfam has urged them to agree to a global rescue package and mobilize the sum cited by the UN to avert a global economic collapse. Possible measures to raise the money could include the immediate cancellation of $1 trillion in debt, the IMF issuing a further $1 trillion in Special Drawing Rights, an increase in aid flows to struggling countries as well as the adoption of emergency solidarity taxes.

In fact, as we detailed earlier, hours after Pope Francis on Easter Sunday morning said the debt burden on the most impoverished countries should be forgiven (aka debt jubilee), the Financial Times is now reporting that the G20 group is nearing a critical “action plan” to freeze debt servicing payments for poor countries to stave off an emerging-market meltdown.

The new relief program could be finalized on April 15 on a videoconference of finance ministers and central bank governors. The plan would “freeze on sovereign debt repayments for six or nine months, or possibly through to 2021,” the official told the Times.

The official said developed countries and multilateral institutions would use this period to write up “very clear criteria, country-by-country of what exactly is going to happen. Is it debt relief totally? Is it just a deferment, a rescheduling?”

“For debt relief to happen, it would take time for it to be co-ordinated,” the official said.

“But what is immediately needed is to give these people space so they don’t need to worry about the cash flow and debt servicing going to other countries, and they can use that money for their immediate needs,” the official said, who did not want to be named due to the sensitivity of the discussions.

A police force in the UK has bragged that its officers may be ‘hiding in the shadows’ ready to catch people who have picnics in rural locations.

The Central Community Team, which represents Bedfordshire Police, tweeted out an ominous message that sounds like it could have been ripped straight from the pages of George Orwell’s 1984.

“If you think that by going for a picnic in a rural location no one will find you, don’t be surprised if an officer appears from the shadows! We are covering the whole county,” states the tweet.

— Central Community Team (@CentralBedsCPT) April 11, 2020

The message was accompanied by a photo of two officers literally standing in the shadows.

Respondents to the tweet were nonplussed.

“If you think that by going to burgle in a rural location no one will find you, don’t be surprised if an officer appears from the shadows! We are covering the whole county – SAID NO POLICE FORCE EVER,” tweeted one.

“Stop it. Just stop it. If you could compose a Tweet more likely to make me want to go for an isolated picnic, I can’t think of it,” said Philip Sinclair.

The Central Community Team later partially walked back the original tweet, stating, “We’re aware of some concerns in relation to this tweet. Please rest assured that it was well intentioned,” while claiming they are only trying to “save lives.”

We appreciate the weather is lovely but picnics aren’t essential so we’d encourage you to enjoy the sun from home instead. Please remember we’re all just doing what we can to help save lives in a difficult situation. More info: https://t.co/jjD2tLpJ3J 2/2

— Central Community Team (@CentralBedsCPT) April 12, 2020

This is by no means the first time a UK police force has received flak for its overzealous enforcement of lockdown measures.

Last week, the government was forced to clarify that police officers shouldn’t be checking the contents of grocery baskets after a police force suggested they would be looking for “non-essential” items.

The government also clarified that it is not illegal for people to be outside in their own gardens following the release of a video which showed a female South Yorkshire Police officer telling a family it was against the rules for their children to be playing in their own front garden.

While current polls show support for the lockdown measures in the UK is very high, expect those numbers to slip if police forces continue to act in an unreasonable and predatory manner.

Meanwhile, comedian Andrew Lawrence did an impersonation of a UK lockdown cop that wasn’t far removed from reality

— Andrew Lawrence, next show: No clue (@andrewlawrence) April 12, 2020

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

We noted on Thursday, Americans have resorted to “watching porn, drinking beer, smoking pot, and or devouring chocolate” to cope with their fears of a pandemic. In the report, we noted how cannabis sales in California, Colorado, Oregon, and Alaska jumped 50% during the March 16-22 period, but it was hard for us to quantify overall national trends.

Apparently, ripping bongs and eating edibles hit an all-time high in March as lockdowns across the country were only in the beginning stages, according to Bloomberg, citing a consumer report via Cowen & Co.

The survey, conducted in March of 2,500 consumers, found about 33% had tried smoking pot, a record high, and that 12.8% had used cannabis within the past month compared to the 2019 average of 12.5%

Sales spiked in mid-March as people rushed to stock up ahead of potential dispensary closures, Cowen said, using data from cannabis analytics firm Headset Inc. Weekly sales growth peaked at 64% in the week ended March 16, the highest rate of increase since at least the beginning of 2019.

However, sales decelerated during the last two weeks of the month to the mid- to the high-single-digit range. This may be linked to a “more pronounced deterioration in job security for past-month cannabis consumers relative to the general population,” according to analysts led by Vivien Azer.

The survey found that the percentage of cannabis consumers working full time fell by 290 basis points to 42.4% in March from February, a bigger decline than the general population. They also tended to be less comfortable with their financial situation. – Bloomberg

America is getting high, melting in their couches as “Netflix and quarantine” become the hottest trend during the pandemic.

“We Weren’t Prepared” For COVID-19: Macron Admits A French Disaster

Update (0200ET): France will remain locked down until at least May 11, PM Emmanuel Macron has revealed, calling on citizens to continue to respect the rules his government has imposed to slow the spread of coronavirus.

L’épidémie commence à marquer le pas. Les résultats sont là, plusieurs ont pu être épargnées, depuis quelques jours, les entrées en réanimation diminuent.#Coronavirus

Admitting the country had not been prepared for the outbreak, the PM nevertheless praised those in front-line occupations for working overtime to save lives and called on the French to continue to stay home and maintain social distancing.

On April 9, in France, one of the three European countries most affected by COVID-19 — the others being Spain and Italy, 1,341 people died from the Chinese Communist Party virus. For Italy, the main European country affected so far, the figure on April 9 was 610 deaths; for Spain 446, and for Germany 266. While the pandemic has been stabilizing in Italy and Spain — and in Germany seems contained — in France it seems still expanding.

Extremely bad decisions taken by the authorities created a situation of contagion more destructive than it should have been.

The first bad decision was that, in contrast to European Union fantasies, borders apparently do matter. France never closed them; instead it allowed large numbers of potential virus-carriers to enter the country. Even when it became clear that in Italy the pandemic was taking on catastrophic proportions, France’s border with Italy remained open. The Italian government, by contrast, on March 10, prohibited French people coming to its territory or Italians going to France, but to date, France has put no controls on its side of the border.

The situation is the same on France’s border with Spain, despite the terrifying situation there. Since March 17, it has been virtually impossible to go from France to Spain, but coming to France from Spain is easy: you just show a police officer your ID. The same goes for France’s border with Germany. On March 16, Germany closed its border with France, but France declined to do the same for its border with Germany. When, on February 26, a soccer match between a French team and an Italian team took place in Lyon, the third-largest city in France, 3,000 Italian supporters attended, even though patients were already flocking to Italy’s hospitals.

France never closed its airports; they are still open to “nationals of EEA Member States, Switzerland, passengers with a British passport, and those with residence permits issued by France” and healthcare professionals. Earlier, until the last days of March, people arriving from China were not even subject to health checks. French people in Wuhan, the city where the pandemic originated, were repatriated by a military plane, and, upon their arrival in France, were placed in quarantine. While Air France interrupted its flights to China on January 30, Chinese and other airlines departing from Shanghai and Beijing continue to land in France.

French President Emmanuel Macron summarized France’s official position on the practice: “Viruses do not have passports,” he said. Members of the French government repeated the same dogma. A few commentators reminded them that viruses travel with infected people, who can be stopped at borders, and that borders are essential to stop or slow the spread of a disease, but the effort was useless. Macron ended up saying that the borders of the Schengen area (26 European states that have officially abolished all passport and border control with one another) could not be shut down and raged at other European leaders for reintroducing border checks between the Schengen area member countries. “What is at stake,” he said, seemingly more concerned with the “European project” than with the lives of millions of people, “is the survival of the European project.”

Other bad decisions the disastrous management of the means of fighting the pandemic.

In early March, when people in large numbers started to arrive ill at hospitals, doctors and caregivers warned that they did not have enough masks and said that working without any protective equipment put them at high risk. Journalists quickly discovered that in 2013, France had possessed a reserve of several million masks, but that the government had decided to destroy them to reduce storage costs. In January 2020, a few hundred thousand masks were still available, but on February 19, President Macron decided to send them to Wuhan, as a “gesture of solidarity with the Chinese people”.

The French government then announced that masks would be available soon, but by the end of March, most doctors and caregivers still had no masks. Several doctors fell ill. As of April 10, eight have died from COVID-19 and several others are in critical condition. On March 20, the government’s spokeswoman, Sibeth N’Diaye, incorrectly said that “masks are essentially useless”.

At the end of February, France had almost no tests available, and no means of manufacturing them. The government decided to buy tests from China, but by March 19, the number of tests was still insufficient. While Germany performed 500,000 screening tests per week, France was only able to only perform 50,000.

Rather than admit that tests were unavailable, or that the government had mismanaged situation, the France’s minister of health, Olivier Veran, announced that large-scale screening was useless, and that France had chosen to “proceed differently”.

Municipal elections, scheduled for March 15, took place despite the virus and despite the fact that many doctors warned that polling stations were places of contagion. Sure enough, in the days that followed, hundreds of people in charge of polling stations flocked to the hospitals. On March 16, President Macron delivered a speech declaring that “France is at war” and that on the following day, March 17, France would be placed on lockdown.

Lockdown is still in place and the French government has decided to extend it indefinitely. The rules are strict. The French can only leave home, within a radius of one kilometer, for one hour a day, to buy food, and must have written authorization to present to the police who patrol the streets. Anyone who is on a street without authorization is fined 135 euros ($145) the first time, 1,500 euros ($1,630) the second time, and after three offenses, can be subject to a sentence of six months in prison. Any meeting with a person not sharing the same place of lockdown is prohibited.

Most of the population has complied, except in the no-go zones. The police have been ordered to turn a blind eye to what happens there. The no-go zone in Seine Saint Denis, for instance, has a fatality rate 63% higher than in the rest of the country.

It was not exactly a secret that before the pandemic that the French economy had also not been doing that well. Growth was barely above zero and unemployment high. Now, the French economy has effectively stopped. It is hard to imagine what the situation will be after the pandemic.

Now, almost all the French hospitals are full; patients wait on beds in the halls. On March 18, France had only 5,000 ventilators, so “triage” procedures began: some patients survived, others, for lack of treatment, did not.

A scandal erupted. Agnes Buzyn — who was Minister of Health until February 16, then a candidate for mayor of Paris; then, on March 15, defeated — said on March 18: “I knew a tsunami [presumably meaning a deadly pandemic] was going to hit France”. She added that she had told everything to President Macron in January. Immediately, Marine Le Pen, President of the National Rally, the main opposition party in France, said that “by staying silent about a worrying situation, Agnes Buzyn behaved in an unconscionable manner”. Le Pen added, “if Agnes Buzyn is speaking the truth, the government and President Macron have seriously failed in their duties, and the case will have to be brought before a Court of Justice”.

Another scandal, however, even more important, had erupted before that. On February 25, a celebrated French epidemiologist, Professor Didier Raoult, President of the Marseille University Hospital Institute for Infectious Diseases (Méditerranée Infection), one of the main European research centers on epidemics and pandemics, published a video, “Coronavirus: Towards a way out of the crisis”. In it, he said that he had found a treatment to infected people quickly: hydroxychloroquine (a drug used against malaria since 1949) and azithromycin (a commonly used antibiotic), that had already cured 24 patients.

Immediately, Olivier Veran, the new French minister of health, said that Professor Raoult’s statements were “unacceptable”. A harsh medical and political battle began. Many doctors close to President Macron agreed with Veran and denounced Raoult. Some even claimed he was a “charlatan”, apparently forgetting that, until then, Professor Raoult had been considered by many France’s most prestigious epidemiologist. Other doctors said that Dr. Raoult was right and supported his findings.

In an attempt to quell the controversy, the French government, by decree, authorized Professor Raoult’s treatment in “military hospitals” for “patients reaching the acute phase of the disease” — but prohibited family doctors from prescribing hydroxychloroquine. Professor Raoult replied that the treatment was only effective if administered “before the disease reaches its acute phase“. [Emphasis added]

A clinical trial was launched by the government but Professor Raoult said that “the trial is not based on the treatment I use and is destined to fail.”

On April 10, Professor Raoult published data showing that he had treated and cured 2,401 patients. A recent international poll of thousands of doctors rated hydroxychloroquine the “most effective therapy” for combating COVID 19. The U.S. Food and Drug Administration (FDA) has authorized widespread “compassionate use” of hydroxychloroquine, while awaiting the results of scientific tests, projects to be complete in “a year or a year and a half”.

Philippe Douste Blazy, Professor in Medicine, former French Minister of Health, said that “the obstructive behavior of Emmanuel Macron and the French government ‘was “criminal'”. He added that “the treatment proposed by Professor Raoult has positive results” and that “France will soon be the last country to refuse the use by doctors of hydroxychloroquine.” He then launched a petition calling on the government to stop obstructing the use of the treatment. The text was signed by thousands of doctors, professors of medicine and other former ministers of health.

The treatment recommended by Professor Raoult still cannot be prescribed by French family doctors. A decree promulgated by President Macron on March 28 authorized doctors to use Rivotril (clonazepam) to “alleviate the suffering of patient in a state of respiratory distress”. Clonazepam slows breathing and can lead to respiratory arrest. Dr. Christian Coulon, a renowned anesthesiologist, tweeted:

“Euthanasia of our elders suffering from respiratory failure. Yes, they decided [to do] it. As a doctor, I suffer deeply”.

Dr. Serge Rader explained on radio on April 3 that many senior citizens living in retirement homes and who get Covid-19 are not sent to a hospital because the hospitals are overwhelmed; instead they receive an injection of Rivotril and die alone in their rooms. Many other doctors expressed their horror on social media, but added that they were powerless.

The result is that anxiety and anger have increased sharply in the population and add to the distress arising from the pandemic and the strict lockdown.

A French lawyer, Regis de Castelnau, wrote in Marianne, a center-left magazine:

“The behavior of our leaders has been marked by unpreparedness, casualness, cynicism, and many of their acts imply the enforcement of the criminal law. Deliberate endangerment of the lives of others and failure to provide assistance to people in danger are obvious… In war, generals who are judged incompetent are sometimes shot. The President and other officials are well aware of this and have to know that they will be held accountable.”

Economists expect the GDP of France in the second quarter of 2020 to be in free fall. One economist, Emmanuel Lechypre, said, “France will experience a very severe recession…. What is happening has never been seen in the past and the country will never be the same.”

A recent survey shows that 70% of French people think that the government is not telling the truth, and 79% think that the government and the President do not know where they are going.

Before the pandemic, France was on the edge of chaos. From the moment President Macron was elected, not a single week in France has passed without demonstrations. The uprising of the “yellow vests” lasted 70 weeks and was accompanied by riots. A strike against a reform of the bankrupt French pension system that began in December 2019 lasted until the appearance of the pandemic.

On March 27, Macron said in a threatening tone that those who criticized his handling of the pandemic were “irresponsible” and that he would remember “those who did not live up to his expectations”.

On April 1, the columnist Ivan Rioufol wrote in Le Figaro:

“The president is not only wrong, but he lied and let others lie. He and his team are guilty. The official speech was unable to assess the seriousness of the situation. It denied, to the point of absurdity, the usefulness of national borders… It is the government that repeated, before claiming the contrary, that masks and tests are useless. It is the State that maintains an incomprehensible confusion around chloroquine… The law of silence that Macron would like to impose is completely untenable.”

Those who hold power in France seem more clueless today than before the pandemic. Sadly, a debacle in France seems increasingly closer.

In the French mainstream media, China is treated extremely politely. No journalist will remind the public that that the pandemic began in Wuhan, China. Reporters say that the United States is in a difficult situation and show New York hospitals, as if showing the suffering of Americans would alleviate the suffering of the French.

France’s mainstream media would do well to fight harder for physicians to be able supply hydroxychloroquine with azithromycin and zinc sulfate. The French media would also do well to be more aware of the dirty game China is playing. On April 5, reports started coming in that in January, before China had let the world know there was a problem, it had begun deliberately lying about it. On January 14, 2020, in a tweet, the World Health Organization repeated China’s lie:

“Investigations conducted by the Chinese authorities have found no clear evidence of human-to-human transmission of the novel #coronavirus (2019-nCoV) identified in #Wuhan, #China”

Meanwhile, Maria Bartiromo disclosed on Fox News, that, before alerting the world about the coronavirus crisis, China had begun cornering the market in medical supplies. It bought $2 billion worth of medical masks — China makes half the world’s supply; why would it buy them? — as well as hundreds of millions of dollars’ worth of other medical gear. Now, reports are stating that China is demanding payment from Italy for donated medical equipment that Italy had donated to China and that China now wants Italy to buy back.

Finally, it would not hurt the French media to show more compassion, to pay more attention to what they say, to watch with more care their own society, and to think about ways to find remedies to the economic and political dysfunction that unleashed such an unimaginable horror.

{kind=link}

{kind=link}

{kind=link}