The tragedy of the COVID-19 pandemic appears to be entering the containment phase. Tens of thousands of Americans have died, and Americans are now desperate for sensible policymakers who have the courage to ignore the panic and rely on facts. Leaders must examine accumulated data to see what has actually happened, rather than keep emphasizing hypothetical projections; combine that empirical evidence with fundamental principles of biology established for decades; and then thoughtfully restore the country to function.

Five key facts are being ignored by those calling for continuing the near-total lockdown.

Fact 1: The overwhelming majority of people do not have any significant risk of dying from COVID-19.

The recent Stanford University antibody study now estimates that the fatality rate if infected is likely 0.1 to 0.2 percent, a risk far lower than previous World Health Organization estimates that were 20 to 30 times higher and that motivated isolation policies.

In New York City, an epicenter of the pandemic with more than one-third of all U.S. deaths, the rate of death for people 18 to 45 years old is 0.01 percent, or 11 per 100,000 in the population. On the other hand, people aged 75 and over have a death rate 80 times that. For people under 18 years old, the rate of death is zero per 100,000.

Of all fatal cases in New York state, two-thirds were in patients over 70 years of age; more than 95 percent were over 50 years of age; and about 90 percent of all fatal cases had an underlying illness. Of 6,570 confirmed COVID-19 deaths fully investigated for underlying conditions to date, 6,520, or 99.2 percent, had an underlying illness. If you do not already have an underlying chronic condition, your chances of dying are small, regardless of age. And young adults and children in normal health have almost no risk of any serious illness from COVID-19.

Fact 2: Protecting older, at-risk people eliminates hospital overcrowding.

We can learn about hospital utilization from data from New York City, the hotbed of COVID-19 with more than 34,600 hospitalizations to date. For those under 18 years of age, hospitalization from the virus is 0.01 percent per 100,000 people; for those 18 to 44 years old, hospitalization is 0.1 percent per 100,000. Even for people ages 65 to 74, only 1.7 percent were hospitalized. Of 4,103 confirmed COVID-19 patients with symptoms bad enough to seek medical care, Dr. Leora Horwitz of NYU Medical Center concluded “age is far and away the strongest risk factor for hospitalization.” Even early WHO reports noted that 80 percent of all cases were mild, and more recent studies show a far more widespread rate of infection and lower rate of serious illness. Half of all people testing positive for infection have no symptoms at all. The vast majority of younger, otherwise healthy people do not need significant medical care if they catch this infection.

Fact 3: Vital population immunity is prevented by total isolation policies, prolonging the problem.

We know from decades of medical science that infection itself allows people to generate an immune response — antibodies — so that the infection is controlled throughout the population by “herd immunity.” Indeed, that is the main purpose of widespread immunization in other viral diseases — to assist with population immunity. In this virus, we know that medical care is not even necessary for the vast majority of people who are infected. It is so mild that half of infected people are asymptomatic, shown in early data from the Diamond Princess ship, and then in Iceland and Italy. That has been falselyportrayed as a problem requiring mass isolation. In fact, infected people without severe illness are the immediately available vehicle for establishing widespread immunity. By transmitting the virus to others in the low-risk group who then generate antibodies, they block the network of pathways toward the most vulnerable people, ultimately ending the threat. Extending whole-population isolation would directly prevent that widespread immunity from developing.

Fact 4: People are dying because other medical care is not getting done due to hypothetical projections.

Critical health care for millions of Americans is being ignored and people are dying to accommodate “potential” COVID-19 patients and for fear of spreading the disease. Most states and many hospitals abruptly stopped “nonessential” procedures and surgery. That prevented diagnoses of life-threatening diseases, like cancer screening, biopsies of tumors now undiscovered and potentially deadly brain aneurysms. Treatments, including emergency care, for the most serious illnesses were also missed. Cancer patients deferred chemotherapy. An estimated 80 percent of brain surgery cases were skipped. Acute stroke and heart attack patients missed their only chances for treatment, some dying and many now facing permanent disability.

Fact 5: We have a clearly defined population at risk who can be protected with targeted measures.

The overwhelming evidence all over the world consistently shows that a clearly defined group — older people and others with underlying conditions — is more likely to have a serious illness requiring hospitalization and more likely to die from COVID-19. Knowing that, it is a commonsense, achievable goal to target isolation policy to that group, including strictly monitoring those who interact with them. Nursing home residents, the highest risk, should be the most straightforward to systematically protect from infected people, given that they already live in confined places with highly restricted entry.

The appropriate policy, based on fundamental biology and the evidence already in hand, is to institute a more focused strategy like some outlined in the first place:

Strictly protect the known vulnerable,

self-isolate the mildly sick, and

open most workplaces and small businesses with some prudent large-group precautions.

This would allow the essential socializing to generate immunity among those with minimal risk of serious consequence, while saving lives, preventing overcrowding of hospitals and limiting the enormous harms compounded by continued total isolation. Let’s stop underemphasizing empirical evidence while instead doubling down on hypothetical models. Facts matter.

* * *

Scott W. Atlas, MD, is the David and Joan Traitel Senior Fellow at Stanford University’s Hoover Institution and the former chief of neuroradiology at Stanford University Medical Center.

All we need are ankle bracelets and Americans would understand what it’s like to be sentenced to home confinement. In a short drive to a grocery store in town last week, I spotted six patrol cars that were out presumably to enforce the stay-at-home orders. Even without those bracelets, we’re essentially prisoners in our homes.

My house sits on six acres—and my dogs, goats and chickens are blithely unaware of the social-distancing requirements (although the cats are getting grumpy about all the extra attention). Life is fairly normal for my family, as we work from home and take breaks by doing chores at the barn.

Even in the nearby tract suburbs, life doesn’t seem that different—at least until we queue up along six-foot markers outside the grocery store. There’s traffic, activity and some semblance of normalcy. In San Francisco, it’s a different story. Life has ground to a halt, and we read ominous reports from Ground Zero—in Manhattan, Seattle, Seoul, and other cities where people live packed together.

For years, urban planners have been singing the praises of population density. In fact, California’ planning model over the past couple decades has revolved around something called New Urbanism. The idea is to set aside as much land as possible as open space—then require developers to build high-density projects in the existing urban footprint. The public still likes single houses with yards, but policymakers are trying to limit that option.

The new rules are justified as part of the state’s battle against climate change. When Jerry Brown was attorney general, he even sued San Bernardino County for permitting too many sprawling developments. The idea that urbanization helps the planet is debatable, given that packed urban centers create heat islands. But the concept fits neatly with existing urban-planning ideology, which decries suburbs as soulless and rural living as wasteful.

Yet after the dust clears from the lockdowns, more Californians will likely be tempted to rethink the high-density status quo. Obviously, diseases spread more quickly where people live cheek by jowl. When a health crisis spreads across the globe, people living in less-dense environs are better able to cope with the madness. My heart goes out to urban dwellers, stuck in their tiny apartments and risking arrest by going to the park for fresh air.

“Density is a factor in this pandemic, as it has been in previous ones,” wrote Richard Florida in the CityLab website. “The very same clustering of people that makes our great cities more innovative and productive also makes them, and us, vulnerable to infectious disease.” Some big cities have handled the crisis better than others. Some rural areas have high infection rates, too. But, as an urban studies professor, he’s distressed at big-city vulnerability.

I find it distressing, too. I like cities for the same reasons as these urbanists and plan on moving back to one after our time on the acreage is done. There’s something exhilarating about the variety and vibrancy in cities, even though urbanists can be overly dismissive of the thriving social connections and civic life that take place in suburban and rural areas. I’ve lived in big cities where no one knows their neighbors, as well as tightly knit “sprawl” suburbs filled with a sense of community.

In reality, the suburbs largely are a product of government planning and subsidy, so there’s no reason that the government should restrict the construction of mid-rises and other higher-density projects in these areas. Some opponents of recent state legislation to give developers the right to build such projects are just as meddlesome as the New Urbanists who want to use government to force only the construction of these projects. They want to legislate their preferences rather than let the market decide.

But while the “get off my lawn” suburban crowd can be awfully annoying, the “you will live in high-density housing” crowd is even worse, given that their prerogatives are in control on virtually every local planning board (not to mention at the state level). Those restrictive policies, by the way, are the most significant reason that so few Californians can afford to buy homes now. The restrictions have reduced housing supply and driven up building costs.

The long-term economic effects of the coronavirus shutdown on the nation’s housing markets is far from clear, of course. Ultimately, it could alter buying patterns, as more people flee tightly packed cities for suburban, exurban, and rural areas that are less susceptible to societal breakdown when pandemics or other crises unfold. Unfortunately, California’s urban-planning rules restrict the ability of people to make those choices.

At the very least, I’d hope that California planners rethink their belief that density always is a good in and of itself—and realize the best way to move forward is to allow builders and buyers as many housing choices as possible.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2VwZmOC

via IFTTT

Lysol Maker Begs Public Not To Inject Its Cleaning Products After Bizarre Trump Advice

Love him or hate him, we believe many would agree that President Trump has made some pretty wild comments during his tenure in office, largely because he often insists on speaking extemporaneously, with little in the way of prep or review (remember when Trump sent markets reeling after mistakenly saying the US would cut off trade with Europe to fight the virus? That was only like six weeks ago).

Is this the most responsible approach to leading the country? Probably not, but it’s definitely a huge part of Trump’s appeal, adding an extra sheen of authenticity to everything he says. And though he has made the occasional slip, the liberal fever dreams about Trump accidentally sparking a devastating trade war or military conflict via gaffe have never materialized, and the president’s press office has grown adept at clarifying and walking back Trump’s comments.

And so it happened that during last night’s press briefing, President Trump made some confusing remarks about a new treatment involving ‘sunlight’ and ‘bleaching’ of the lungs to combat the virus. It appeared that during Thursday night’s presser, Trump was publicly spitballing about these treatments, which he said involved “a very powerful light”, or “heat”. He even said people should consider calling their doctors to ask whether possibly injecting “light”, “heat” or maybe Lysol or bleach.

The unhinged comments followed a presentation by William Bryan, the Department of Homeland Security’s undersecretary for science and technology. Bryan shared some data showing concentrated exposure to light and heat could help degrade the virus more quickly. Trump took that to mean that maybe his initial theory that the virus would ‘go away’ with the warmer weather might have some merit after all (though it has already been put to the test in places like South America and Singapore, which have seen the number of coronavirus cases explode regardless).

Suddenly, Trump had an idea…

“Supposing we hit the body with a tremendous…whether it’s ultraviolet or very powerful light…and I think you said we’re going to test it,” Trump said, looking toward Bryan. “Supposing you brought the light inside the body, which you can do, either through the skin or some other way … and I think you said you’re going to test that, too. That sounds interesting.”

…and then another, even crazier idea.

“And then I see the disinfectant where it knocks it out in a minute,” Trump said. “One minute! And is there a way we can do something, by an injection inside or almost a cleaning? Because you see it gets in the lungs and it does a tremendous number on the lungs, so it’d be interesting to check that. So, that you’re going to have to use medical doctors with, but it sounds interesting to me.”

It’s already obvious that Trump simply can’t resist parroting any scrap of information that he feels validates something he said or did that was widely panned by the press. And so, somewhere deep within his brain, he clearly saw an opening to possibly vindicate his claim that the virus would “go away with the warmer weather.”

Trump noted that he previously hypothesized that “maybe (coronavirus) goes away with heat and light. The fake news didn’t like it at all. But it seems like that’s the case.”

However, when he asked Dr. Deborah Birx, the White House coronavirus task force coordinator, about “the heat and the light” as potential treatments, she replied: “Not as a treatment.”

Of course, anybody who tries to inject bleach is an idiot: ingesting bleach in any form is extremely toxic and consuming it will likely kill a human. The fact that the president even suggested this probably says more about his current state – for instance, he’s probably so exhausted, that his usually freewheeling style is giving way to a near-delirium – than anything else, though his critics are feasting on the soundbite, and rightfully so.

Trump didn’t help the situation when he lashed out at a reporter for questioning the wisdom of saying ‘sunlight’ can fight the virus during a national lockdown.

Unfortunately, the reality is that there are many people out there who, if the president suggests that drinking bleach might be helpful, will go out and drink bleach, despite the fact that it is obviously toxic. The same goes with Lysol, which is why Lysol and Dettol maker Reckitt Benckiser issued a warning on Friday advising people against using disinfectants to treat the coronavirus, warning that “under no circumstances” should anybody ingest bleach.

“Under no circumstance should our disinfectant products be administered into the human body (through injection, ingestion or any other route),” the company said.

The company said that it had actually been asked via ‘recent social media activity’ whether injecting cleaning products might have some previously unknown salubrious health effects.

Several ‘public health experts’ quickly jumped on the bandwagon, warning “the public” not to inject disinfectant, or subject themselves to harmful doses of UV light. Robert Reich, a professor of public policy at the University of California at Berkeley, former secretary of labor under Clinton, and well known liberal wingnut, tweeted that Trump’s briefings were “actively endangering the public health.”

This, even as the MSM insists that the briefings are ‘unwatchable’ and should be canceled since nobody watches them and they only serve to create confusion.

Walter Shaub, a former director of the Office of Government Ethics, added: “It is incomprehensible to me that a moron like this holds the highest office in the land and that there exist people stupid enough to think this is OK. I can’t believe that in 2020 I have to caution anyone listening to the president that injecting disinfectant could kill you.”

Watch the clip from last night’s press briefing below:

After hearing presentation President Trump suggests irradiating people’s bodies with UV light or injecting them with bleach or alcohol to deal with COVID19. pic.twitter.com/cohkLyyl9G

For anybody who is still curious about the effects of bleach in treating/preventing the coronavirus, we’d urge you to check out this infographic…then maybe seek out psychological help.

“Watch what you say or they’ll be calling you a radical, liberal, oh fanatical, criminal…”

It says it all when the market pays far more attention to a failed test of Gilead’s drug Remdesivir than it does to the 4.4 million American workers who joined the 22 million already queuing on the unemployment lines.

4 little stories about hope: Spot the odd one out…

i) The report on the Gilead drugs test – which was quickly pulled from the WHO website after being posted by “mistake” – indicated it doesn’t work as a treatment for Covid-19. Gilead were quickly on the case saying earlier tests elsewhere were more positive – you can read the story here: Gilead Tumbles After Latest Data Leak on Virus Drug Trials. Gilead has become one of the most talked about stocks on the market.

ii) UK headline news last night was the first vaccine test in the UK. Two volunteers got jabs – one got a control, the other got the vaccine. If it works (still a big if), the Government has said Britons will be prioritised – something other nations looking to protect their own key workers might not forget quickly should the British effort flounder. It’s a race, an all or nothing effort – UK Health Minister Matt Hancock said: “the upside of being the first country in the world to develop a successful vaccine is so huge that I am throwing everything at it.” No doubt some big American PE fund has already called Tory HQ demanding to invest….

iii) In Madagascar – yeah! lemurs and penguins (you sure about the penguins??) – the President has launched his own company “COVID-Organics” – marketing a herbal tea which prevents and cures the virus. Madagascar pupils expelled for refusing Covid-19 remedy distributed by president. Armed Troops are selling it door to door around the country. Surprisingly, Covid-organics is not attracting as much real money as Gilead. (US readers…. mild sarcasm alert.)

iv) Meanwhile millions of American’s, including the world’s smartest man, still believe you can cure C-19 with Hydroxychloroquine, a relatively effective anti-malaria drug. It’s completely unproven – but for full disclosure, President Trump does own stock in the manufacturer; Sanofi.

Gilead, the UK vaccine and both snake oil stories neatly illustrate one driver of market sentiment: finding a quick fix! The investors who piled into Gilead’s drug and the column kilometres written about it, all support the narrative economies are going to reopen and get back to normal faster than expected. A quick cure, a miracle drug, a vaccine – they are all about hope.

As I’ve said so many times Hope is Never A Strategy.

I’m more concerned by the real news. The reality of deepening global recession.. How deep it goes depends on the virus. Can end lockdowns early or not. There is lots of conflicting news out there. They now reckon 20% of New Yorkers have been infected – meaning its closer to herd immunity, and the death rate was 0.5%. An Israeli team are claiming the virus has a limited shelf life – extinguishing itself after around 70 days. But other epidemologists are concerned how quickly the virus mutates – which may explain why some countries seem to have been hit by relatively mild flu-like versions, while others, including the UK have been hit by an all-in body-wrecker.

Boris Johnson is going back to work next week, but I hear Dominic Cummings is still bedridden. I have three close friends who have had the full-on virus. All three report the same things – they are still exhausted, their lungs are wrecked “going up a hill is impossible”, and 2 of them have kidney issues. The other has a constant headache. They’ve been told they will recover – but it could take months.

The hope is we get back to normal faster – which is why the stock market rallies so hard on good news. The reality may yet be more shocks to come.

I must admit to some concerns about Europe. They have agreed to fudge address the funding crisis in Italy and Spain via a new massive recovery fund linked to the newly agreed European Budget. EC President Ursula von der Leyen said “The budget is time tested. Everybody knows it. It is trusted by all member states.” Would that be the same budget that hasn’t been signed off by the auditors in years, and has a gaping hole which the British used to fill?

FRIDAY RANT TIME – Blain Blain versus the Financial Media

As its Friday, I have contractually entitled myself to a rant about something.. Today I hope my chums in the financial media won’t be too offended if I express a degree of unhappiness at the Fourth Estate.

Earlier this week I wrote a piece about Fixed Income ETFs. It was highly critical of an article in the FT about how ETFs saved the bond market. A good number of replies to the Porridge on Wednesday said I’d nailed it – agreeing it was the prospect of QEI (QE Infinity) of investment grade and junk by central banks that pulled bonds from the edge of a credit meltdown. I might have been a bit blunt when I wrote it read like puff for ETF sponsors and promoters.

Later a reader alerted me to the FT comments page on the story. There were about 60 comments, and most (80% plus) agreed with my take that the article was wrong. Someone had posted a link to the Morning Porridge on the page – which is excellent. The journalist, Robin Wigglesworth, personally responded to it.

He defended himself vigorously – as it his right. He also got personal.

Mr Wigglesworth described the Morning Porridge as a “bit of a dogs dinner” – which, to be honest could pass as fair comment. I write the Morning Porridge fresh every morning, and I don’t have an army of sub-editors at my command to correct and edit it. I don’t spend the rest of the day figuring what to write next or which press release to rewrite – I literally have a day job in alternative assets which more than fills the hours.

Mr Wigglesworth went on to tell readers I don’t understand ETFs, and accused me of lying when I said it was impossible to gets bids on some ETFs during the crisis in March. Because I raised the “old trope” about the relative numbers of asset managers with experience of previous crisis, he wrote that I’m the comical “grizzled expert” who regards anyone with less experience as a “callow child”. To finish me off he accused me of intellectual dishonesty because of my stance on ETFs.

Whoa… I am not an “ETF hater”. I am personally invested – including in a high yield ETF I could not sell in March. (Holding it has proved profitable.) I am many things, (and at this pre-shave moment, that includes grizzled), but I am not dishonest nor unprofessional. To accuse me of being dishonest Mr Wigglesworth, gets an invite to Shooters Hill – old London’s premier duelling site.

Or maybe.. we don’t need to get overly dramatic.

Over the past few years trolls have called me just about everything on comment pages – there is a great one up there on a recent Shard Lite-Bite YouTube video calling me: “Blain the Bland Bloviating Fat Lefty Socialist know-nothing”. What a marvellous word – bloviating!

I am more than happy to receive direct criticism of the Morning Porridge. I welcome readers to post comments – good or bad. Please use the comment section on the Porridge or email me direct. Any feedback is constructive. I accept being called an idiot to my face by clients and competitors.

I don’t have any problem with ETFs – but its fair comment to be critical if someone states something as outrageous as “they saved the bond market”. I certainly don’t have a problem with the FT. It’s the first thing I read each day. Some of writers and features are superb. My two impossible dreams are being on Desert Island Discs and doing Lunch with the FT!

I don’t want to pick a fight with the FT – I know who would lose….

But I am disappointed at the journalist. Many years ago, a much younger Bill Blain was a financial journalist – Euromoney and Bloomberg. The experience and what I learnt proved critical to my subsequent career back in fixed income – and made me a better financier. I might have been young and naïve, but as a journalist, I’m pretty sure my first reaction to hearing about someone disagreeing with a story would have been to phone them, listen, and attempt to convert them into a contact.

Bottom line is no harm really done, and I’d welcome a dialog with Wigglesworth or any other journalist who thinks I write nonsense… I don’t always get it right, and I’d like to learn what I’m doing wrong from them.

There is a lot to report and comment on in Finance. It worries me that regulations, including MiFid, restrict access. It worries me that the thoughts and comments of the large incumbent Investment Banks, the largest assets managers and the wealthiest hedge fund managers always take precedence to anyone below them in the financial food chain the media thinks exists.

That’s potentially a problem – big financial firms are compromised by their relationships. They can’t say anything without first checking they’re not restricted by client relationships.

The one thing I can guarantee you about the Porridge is complete independence. I say and write it exactly as I see it. I don’t need to pull or hold my comments because “relationships” might be at risk. Unlike my bigger rivals – I can offend everyone!

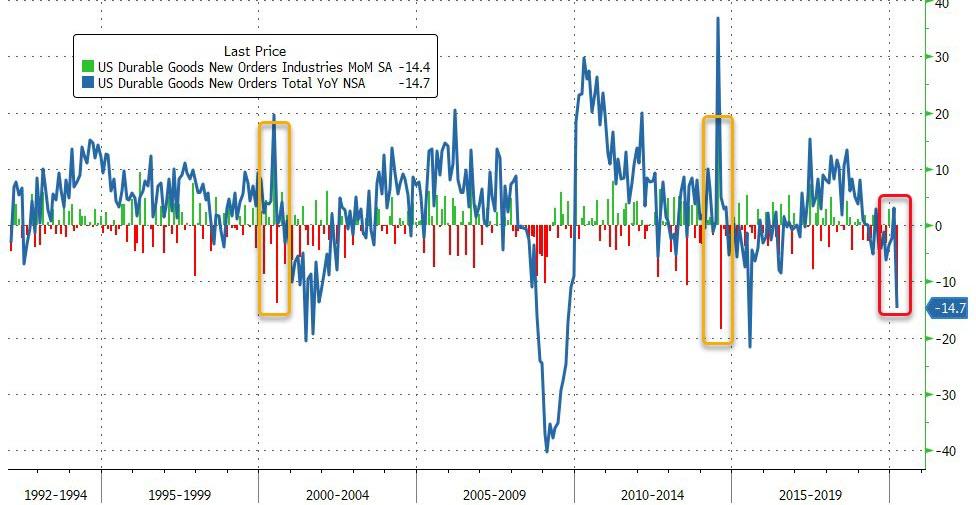

US Durable Goods Orders Collapse In Early March Data

After an armada of ugly data this week, US Durable Goods orders were expected to be the piece de resistance and it was – with preliminary March orders crashing 14.4% MoM (far worse than the already bad 12% decline expected), sending year-over-year durable goods orders down 14.7% – the worst since the great financial crisis..

Source: Bloomberg

The biggest driver of the drop was Boeing order cancellations (New orders ex-defense fell 15.8% in March after 0.2% fall)… four times worse than during the great financial crisis.

Source: Bloomberg

Outside of extreme swings in airline orders that distort the data drastically, this is the worst MoM drop ever.

There is a lot of noise in these numbers so one must be careful with Orders ex-Transports only down a measly 0.2% MoM (against expectations of 6.5% plunge) and the Business Investment proxy (Cap Goods Shipments non-Defense, ex-Aircraft) fell just 0.2% MoM (against expectations of a 7.0% collapse).

We suspect by the time the final March data comes in, this will be a bloodbath.

Futures Rebound From Earlier Losses As Corona Optimism Returns

S&index futures reversed earlier losses as the U.S. House of Representatives passed a $484 billion coronavirus aid package, while China’s central bank cut another policy rate as expected. Sentiment was helped after US Covid-19 infections rose at the slowest pace in three weeks, and the potential easing of lockdowns in Europe.

Europe did not share US enthusiasm and the Stoxx 600 dropped after the region’s leaders failed to agree on a long-term stimulus package and news the Remdesivir coronavirus drug was a flop. Food and beverages was the only gaining industry group to advance after food giant Nestle reported its fastest sales growth since 2015 as consumers loaded up on frozen food. Travel, oil and bank shares led the decline. The banking index led the declines in European stocks after S&P cut Commerzbank’s credit rating by a notch and lowered its outlook for Deutsche Bank to negative from stable.

German’s Ifo Business Climate index plunged in April to 74.3, below the 79.7 expected and down sharply from prev 85.9 previously. The Ifo Expectation print came in at an apocalyptic 69.4 (exp 75.0; R prev 79.5), while the Current Assessment was a bit stronger at Apr: 79.5 (exp 80.5; R prev 92.9).

“It’s a negative session,” said François Savary, chief investment officer at Swiss wealth manager Prime Partners. “The market for the last week has been under consolidation after a strong rally. A lot of good news has already been priced in and news that the number of deaths had increased in the U.S. was also a warning sign for investors.”

In the latest European failure to resolve the coronacrisis, EU leaders agreed on Thursday to build a trillion euro emergency fund to help recover from the coronavirus pandemic, while leaving divisive details until the summer. French President Emmanuel Macron said differences continued between EU governments over whether the fund should be transferring grant money, or simply making loans.

“The risk exists that a concrete decision on the creation of the recovery fund may not occur before September, thereby not being operational before early 2021,” Goldman Sachs European economist Alain Durre wrote in a note.

Earlier in the session, Asian stocks also fell, led by IT and industrials, after rising in the last session. Most markets in the region were down, with Jakarta Composite dropping 2.1% and South Korea’s Kospi Index falling 1.3%, while Australia’s S&P/ASX 200 gained 0.5%. The Topix declined 0.3%, with Legs and Meiji Shipping falling the most. The Shanghai Composite Index retreated 1.1%, with Jumpcan Pharma and Jiangsu Jiangnan High Polymer Fiber posting the biggest slides. There was limited reaction to the Chinese central bank’s partial roll-over of maturing medium-term funding to banks, at a lower interest rate.

The MSCI All Country World Index was down 0.3% and heading for its worst week in three, while MSCI’s broadest index of Asia-Pacific shares outside Japan fell 0.9%.

“The recent price action in global markets has highlighted the fragility of the risk rally in the face of deteriorating global economic data and weak commodity prices,” Valentin Marinov, the head of G10 FX strategy at Credit Agricole CIB in London, wrote in a note to clients. Still, “the recent global monetary and fiscal stimulus measures have put a ‘floor’ under the risky assets,” he said.

On Thursday, the S&P 500 and the Nasdaq turned negative at the close on Thursday in the wake of a report that Gilead Sciences’s antiviral drug remdesivir had failed to help severely ill COVID-19 patients in its first clinical trial. Gilead said the findings were inconclusive because the study conducted in China was terminated early. The markets’ sensitivity to news related to the medical treatment of COVID-19 reflected investors’ desperation for a sign of when the global economy might start returning to normal, said Tim Ghriskey, chief investment strategist at New York-based wealth management firm Inverness Counsel.

“Any piece of bad news is likely to rattle the market,” Ghriskey said. “Investors are keen for a semblance of hope that they can soon crawl out of their homes and get on with some form of normal life, even if with trepidation and fear.

Business activity in the US plumbed record lows in April, mirroring dire figures from Europe and Asia as strict stay-at-home orders crushed production, supply chains and consumer spending, a survey showed. Optimism, however, was boosted after the U.S. House of Representatives on Thursday passed a $484 billion bill to expand federal loans to small businesses and hospitals overwhelmed by patients. President Donald Trump, who has indicated he will sign the bill, said late Thursday he may need to extend social distancing guidelines to early summer.

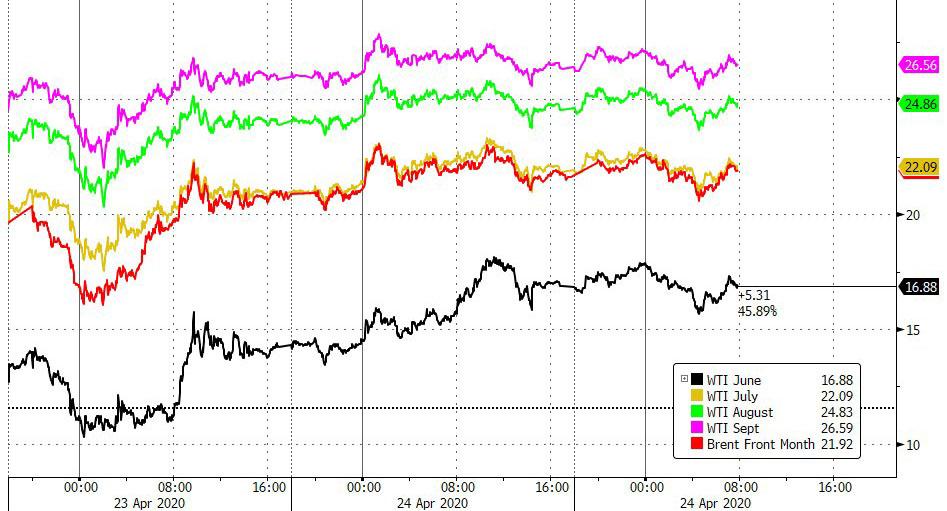

In commodities, retained their recovery from a price collapse this week that pushed U.S. crude futures into negative territory for the first time ever, helped by producers such as Kuwait saying they would move to cut output. Brent crude was up 18 cents, or 0.9%, at $21.51, after jumping 5% on Thursday. U.S. oil was steady at $16.87 a barrel, having surged 20% in the previous session.

But prices were headed for their third weekly loss and the outlook remains dim because global energy demand has evaporated due to business closures and travel curbs aimed at slowing the pandemic. In addition, some countries are running out of space to store the crude oil that they are not using.

In rates, Italian bonds dropped while bunds lead euro-area gains after EU heads fail to agree on how to finance an economic aid package to fight the pandemic. Focus is on S&P’s review of Italy’s rating later Friday, while Germany releases IFO figures. BTP-bund spread widens 12bps to 253bp, below this week’s high at 272bps. Bunds bull flattened, outperform Treasuries by 2bps. Gilts may look to an announcement at 12pm to see if BOE buyback buckets will be changed from the current GBP1.5b per operation, after Thursday’s revised bond remit was increased to GBP180b from May to July.

In FX, dollar reversed an earlier advance to trade flat as risk sentiment improved with stocks recovering ground. The Bloomberg Dollar Spot index was little changed and still set for a weekly gain of 0.9%; U.S. equity futures gained and European stocks pared losses. The euro recovered from dipping to a one-month low vs the dollar to trade up 0.1% at $1.0789; it was still set for a weekly drop of 0.8%. “USD switches between minor losses and minor gains,” said Shaun Osborne, chief FX strategist at Scotiabank, in a client note. “We look for relatively quiet trading on the session but equity trends will continue to shape intraday trading; if U.S. markets pick up, the USD should slide somewhat”

Looking at the day ahead, we get the US preliminary March durable goods orders and non-defence capital goods orders ex air, along with the final April University of Michigan consumer sentiment index. Meanwhile, the Russian central bank will be deciding on interest rates, and earnings releases include Verizon Communications, T-Mobile and American Express.

Market Snapshot

S&P 500 futures up 0.2% to 2,788.25

STOXX Europe 600 down 1.3% to 328.93

MXAP down 0.7% to 141.58

MXAPJ down 0.9% to 456.34

Nikkei down 0.9% to 19,262.00

Topix down 0.3% to 1,421.29

Hang Seng Index down 0.6% to 23,831.33

Shanghai Composite down 1.1% to 2,808.53

Sensex down 1.2% to 31,467.29

Australia S&P/ASX 200 up 0.5% to 5,242.62

Kospi down 1.3% to 1,889.01

German 10Y yield fell 3.9 bps to -0.463%

Euro down 0.2% to $1.0754

Italian 10Y yield fell 9.2 bps to 1.81%

Spanish 10Y yield rose 0.2 bps to 1.051%

Brent futures down 1.7% to $20.96/bbl

Gold spot little changed at $1,729.60

U.S. Dollar Index up 0.3% to 100.71

Top Overnight News

The U.S. House of Representatives passed a $484 billion package, replenishing funding to aid small businesses and provide support for hospitals and virus testing. U.S. infections rose at the slowest pace in three weeks, and China reported no deaths for a ninth straight day

German Ifo Insitute’s business confidence dropped to 74.3, more than economists predicted and a record low

Germany’s sick beds continued to empty, and France and Italy showed progress in slowing the coronavirus spread in a welcome sign for European leaders ahead of further steps to ease lockdowns

Stress in the commercial paper market is continuing to ease as prime fund inflows accelerate. The funds saw a third straight week of inflows through April 22. Total assets jumped by $19 billion — the most since October 2015 — helping to push rates lower and tighten spreads

With the Bank of Japan accumulating bonds at a slower pace than its 80 trillion yen ($745 billion) target for years, it has faced criticism for keeping the guideline in its policy statement

U.K. Prime Minister Boris Johnson plans to return to Downing Street as early as Monday following his bout with Covid-19, the Telegraph newspaper reported

Treasury Secretary Steven Mnuchin will require public companies deemed critical to national security that seek a share of $17 billion in virus-related relief to offer an equity stake to the government

China’s central bank rolled over some of the targeted funds due Friday while cutting interest rates on the loans, the latest in a string of measures aimed at ensuring sufficient liquidity. China’s 2020 economic growth is seen sliding below 2% in survey

Oil continued to claw back losses as attention turned to output cuts in response to the demand hit from coronavirus lockdowns. New York futures for June delivery rose for a fourth day to above $17 a barrel

New Zealand Finance Minister Grant Robertson has downplayed the prospect of the central bank monetizing government debt, saying its approach to quantitative easing is working

Asian equity markets traded mostly negative following the lacklustre handover from US where the major indices retraced their initial oil-inspired gains as sentiment soured following weak data and with anti-viral hopes dashed by disappointing results for Gilead’s Remdesivir drug in a clinical trial. ASX 200 (+0.5%) and Nikkei 225 (-0.9%) were mixed with energy front-running the gains in Australia after similar outperformance of the sector stateside due to the continued rebound in oil and as state governments are set to begin releasing a list of projects next week to spur the rebound in the domestic economy, while sentiment in Tokyo was subdued as exporters suffered from recent adverse currency flows and ongoing COVID-19 disruptions. Hang Seng (-0.6%) and Shanghai Comp. (-1.0%) conformed to the regional glum amid weak financial earnings from the likes of China Life Insurance and Ping An Insurance, while the PBoC’s CNY 56.1bln 1-Year Targeted Medium-term Lending Facility and respective 20bps rate cut failed to spur upside given that the injection was less than the CNY 267.4bln maturing and with the rate cut inline with the recent similar reductions in the 1-year MLF and PBoC Loan Prime Rate. The biggest losses in the region were seen in the Philippines PSEi (-2.2%) after President Duterte extended the lockdown for the national capital region to May 15th and warned the country was running out of funds which the Finance Secretary suggested was not the case, while India’s NIFTY Index (-1.2%) also slumped with financials pressured following the decision by Franklin Templeton Mutual Fund to wind up six of its credit funds in India. Finally, 10yr JGBs were higher amid the downbeat overnight risk tone and following recent source reports that suggested the BoJ could consider unlimited bond buying at next week’s policy meeting. Furthermore, the BoJ were present in the market today for a total of JPY 180bln of JGBs concentrated in the long to super-long end, while the Chinese 10yr yield also dropped to its lowest in 10yrs as markets had widely anticipated the PBoC’s TMLF actions.

Top Asian News

China Cuts Another Policy Rate, Replaces Some Maturing Loans

HSBC Pushes Back Against Claims the Yen Has Lost Haven Status

BOJ Has Perfect Cover to Ditch 80 Trillion Yen Bond Purchase Aim

Biotech Firm Akeso Surges 58% on Hong Kong Trading Debut

The downbeat APAC sentiment intensified as European players entered the fray (Euro Stoxx 50 -0.8%), with the failure of EU leaders to agree on a recovery package coupled with the Gilead Remdesivir pessimistic reports prompting an unwinding of recent gains. That being said, US equity futures outperform Europe after the latest coronavirus bill made smooth passage through the House. European bourses see broad-based losses, but have clambered off lows, albeit Spain’s IBEX (-1.3%) sees more pronounced downside after the country’s hopes for a grant and a joint EU debt issuance were dashed out the window at yesterday’s EU Summit. Sectors are in the red with the exception of Consumer Staples (amid Nestle earnings) and feature Energy as the laggard given the pullback in the complex. The breakdown also paints a downbeat picture as Oil & Gas, Banks, Autos, and Travel & Leisure all post losses of over 2%. Nestle’s (+3.0%) numbers see shares on a firmer footing after organic revenue topped estimates, FY20 was maintained and the Co. is exploring options for its Yinlu Peanut Milk and Canned Rice Porridge businesses in China, including a potential sale. The group expects continued improvement in organic sales growth and underlying trading operating profit margin and sees underlying EPS to increase in constant currency. As Nestle carries a 16.3% weighing in the SMI (+0.3%), the Swiss index fares better than its regional peers. Other movers are largely earnings-oriented: Air Liquide (+0.4%), Casino (-0.4%), Saint Gobain (-3.6%) and Sanofi (-0.6%); the latter conforming to the broad losses across health names induced by Gilead (-0.8% pre-mkt), despite a boost to earnings from COVID-19 stockpiling and an increase in Business EPS. Although Italy’s DiaSorin (+2.5%) bucks the trend on the back of its competitor’s failure in the COVID-19 antibody market. Signify (+14.3%) leads the gains the Stoxx 600 after announcing a strong cash position against the backdrop of the pandemic.

Top European News

Merkel’s Stimulus Vow Sets Up EU Battle for Recovery Funds

Italy Bonds Slide as EU Inaction Deepens Gloom Before S&P Review

German Business Confidence Plummets Further as Lockdowns Persist

Britons Under Lockdown Turn to Alcohol in Record Splurge

In FX, the single currency has pared some losses vs the Dollar after falling to fresh mtd lows and through a key Fib retracement level (1.0757), but remains weak overall following no breakthrough on an EU-wide fiscal recovery fund and yet more evidence of the fallout from COVID-19 via the keenly watched Ifo survey, as all metrics missed consensus and the institute described the mood of German businesses as ‘catastrophic’. Moreover, firms are said to be more pessimistic about the outlook for coming months than ever, while Germany’s IAB Labour Market Research group believes that unemployment could rise in excess of 3 mln this year. However, Eur/Usd is clinging to 1.0760, while Eur/Gbp holds above 0.8700 amidst a pull-back in the Pound from Thursday’s recovery peaks in wake of weak UK retail sales data and a broadly firmer Greenback, in part on the demise of others. Indeed, Cable has tested 1.2300 as the DXY rebounds from post-US jobless claims and Markit PMI lows to notch a new recent high at 100.860, closer to April’s best so far (100.931 on April 6).

CAD/AUD/NZD/JPY – All softer vs the Buck, but off worst levels as aversion and disappointment over the failure of Gilead’s Remdesivir coronavirus treatment at clinical trial abates. The Loonie is holding the bulk of it’s crude induced momentum on the 1.4000 handle alongside oil, while the Aussie is pivoting 0.6350 after failing to sustain 0.6400+ status yesterday and Kiwi is hovering close to 0.6000. Elsewhere, the Yen has returned to tight confines between 107.75-55 following knee-jerk depreciation on no holds barred BoJ QE with little independent impetus from in line Japanese inflation data overnight.

SCANDI – Somewhat mixed fortunes for the Crowns, as Eur/Sek maintains a downward bias close to 10.8500 ahead of the Riksbank policy meeting on the grounds that the repo rate looks set rigid regardless of more adverse nCoV contagion highlighted by the Swedish Finance Ministry downgrading its already recessionary assessment of Q2 GDP. Conversely, Eur/Nok is back up near 11.5000 as Stats Norway slashed its 2020 growth forecast with the entire economy already in contraction over Q1.

EM – Aside from the ongoing vigil for the Rouble in terms of tracking Brent, the looming CBR rate verdict will be in focus along with the post-meeting press conference amidst expectations that the benchmark will be lowered to 5.5% from 6%. Usd/Rub roughly flat in the run up circa 74.6750.

Mexico Central Bank Governor said will hold usual meeting on May 14th despite this week’s off-schedule cut and central bank will continue to evaluate as well as take actions it deems necessary, while he added the challenge is overcoming the short-term crisis and it will be important to provide liquidity and financing to those that need it as economy gradually returns to normal. (Newswires)

In commodities, WTI and Brent front month futures have yielded their gains seen in the APAC session, with both benchmarks extending losses as the final session of the week goes underway, but the complex has seen a recent pickup in-line with a improving overall risk tone. WTI posted +40% gains over the last two days as geopolitical risk premium pricing was induced by a ramp-up in US-Iranian tensions, while some argue prices were squeezed higher amid liquidation-only restrictions by some brokers. Again, there is little by way of any fresh fundamental developments to support a sustained move higher, but a relief rally may have been due given the recent detrimental losses across the complex. In terms of OPEC, despite reports of Algeria and Kuwait following the lead from Saudi to cut output early, desks believe this will do very little in the short term to offset the surplus in the market. ING analysts believe that “there is more downside risk to prices in the short term.” WTI futures rose to a whisker away from USD 18.00/bbl before receding to a current intraday low at USD 15.64/bbl, whilst its Brent counterpart printed an intraday roof at USD 22.70/bbl and base at USD 20.50/bbl thus far. Elsewhere, spot gold retraces some of its recent gains, but prices remain comfortably above USD 1700/oz at the time writing. The yellow metal is pressured by the rising Buck and sits within a USD 1721-31 intraday band, with much of the session spent at the lower end of this. Copper prices see similar price action amid the overall risk aversion across the market, alongside Dollar woes. The red metal threatens a break below USD 2.3/lb vs. yesterday’s 2.3505/lb high.

US Economic Calendar

8:30am: Durable Goods Orders, est. -12.0%, prior 1.2%; Durables Ex Transportation, est. -6.5%, prior -0.6%

8:30am: Cap Goods Orders Nondef Ex Air, est. -6.7%, prior -0.9%; Cap Goods Ship Nondef Ex Air, est. -7.0%, prior -0.8%

10am: U. of Mich. Sentiment, est. 68, prior 71; Current Conditions, prior 72.4; Expectations, prior 70

DB’s Jim Reid concludes the overnight wrap

European leaders won’t be able to afford a lie down anytime soon as there is still much unfinished business to sort out post the leaders’ summit yesterday. Mark Wall published a blog last night (Link here) on the outcome. While he wasn’t expecting a full agreement on the EU recovery Fund yesterday, the progress was slower than feared. Mark remains confident there will be a Recovery Fund, but beyond that, the size, speed and structure remains undecided and unclear. What is clear is that the key battleground won’t be “joint bonds”. It will be the ratio of grants vs loans. See the note for what has been agreed but with 3-4 weeks now until the EC come up with a proposal, that leaves plenty of time for events to take over here. A notable positive was Conte’s positive reaction though. If activating the ESM is politically viable in Italy it could unlock more unlimited sub 3-year buying of BTPs by the ECB.

During these deliberations, Bloomberg reported that ECB President Lagarde had warned that the Euro Area economy could shrink by 15% this year in an extreme scenario, with her baseline scenario a 9% drop in output. Furthermore, she said that the leaders risked doing too little, too late in terms of their response.

The poor data (woeful PMIs, bad as expected US jobless claims) didn’t stop markets rallying for most of yesterday but the shine was taken off the session with the EU summit failing to agree on an immediate deal and also on news that a virus treatment did not do well in phase 1 trials. Equities earlier got a boost ahead of the summit by reports of Chancellor Merkel saying that the European response must be huge, which initially boosted the Euro before it fell (-0.43%) after the disappointing end to the summit – the fourth straight daily weakening of the currency. Equities peaked just before Europe went home, with the S&P 500 falling from +1.62% to close basically flat at -0.05%. This meant that the S&P 500 did not rise for the 5th Thursday in a row of multi-million jobless claim numbers. The retreat was also potentially on news that Gilead’s antiviral Remdesivir drug did not perform well in its first randomised covid-19 clinical trial. Before the US slip and the summit conclusion the STOXX 600 was up +0.92% with the FTSE MIB +1.45%.

Sovereign debt also had a strong day, with yields on 10yr Treasuries and bunds down by -1.8bps and -1.7bps respectively. Furthermore, European spreads narrowed ahead of the summit, with the gap between Italian (-7.6bps), Spanish (-7.1bps), Portuguese (-6.5bps), and Greek (-20.7bps) yields over bunds all falling, even if they still remained at elevated levels. Oil had a relatively quiet session by the standards set this week. WTI was up +19.74% to 16.50/barrel. Brent Crude was also up by +4.71% at $21.33/barrel, while the Russian Ruble powered forward, seeing its biggest 2-day gain against the US dollar (+3.25%) since December 2016.

While US equities reacted to the failure of a possible covid-19 treatment, we saw some interesting information out of New York State yesterday. The region has been one of the hardest hit in the entire world, with just over 10% of all confirmed cases globally. The state has also been very aggressive in ramping up testing capabilities over the past month. Yesterday, Governor Cuomo announced the results of testing roughly 3,000 people across 19 counties and 40 localities. In this survey, 13.9% of individuals tested positive for antibodies of covid-19. New York City had the highest rate, with 21.2% testing positive. The Governor cautioned that this may not be entirely representative of the state, because the survey was done at grocery stores and other big box stores and therefore was not necessarily fully random. Healthcare workers particularly, could have different and potentially higher rates. Also no one under the age of 18 was tested in this study. Regardless, if the infection rate is closer to 14%, then the number of New Yorkers infected would be near 2.7 million, bringing the overall mortality rate much lower than currently cited and closer to the 0.50% that we highlighted in our pandemic piece yesterday ( link here). This is closer to that of the recent Imperial College London study we mentioned which projected this kind of fatality rate if the virus were allowed to spread unmitigated. Many epidemiologists had cited a likely mortality rates of 0.5%-1% by the time the virus has run through, but seeing evidence of this sort of number may be encouraging to those that fear it’s far higher. Still a lot of studies and testing to back this up though.

Staying with the US, Treasury Secretary Steven Mnuchin said overnight that he is considering the creation of a government lending program for US oil companies following the huge decline in the price of oil. Mnuchin said that “investment-grade companies will be able to either access the normal capital markets or will be able to access the Fed’s investment-grade facility. That’s the priority” but for companies that aren’t IG, Mnuchin said that he is discussing “alternative structures with banks.” Bloomberg has reported that the program will run out of the Fed while the administration is also considering taking financial stakes in exchange for some loans, and some firms might be asked to reduce production. Separately, the Treasury Department said, in the 10-page loan application posted on its website overnight that public companies deemed critical to national security that seek a share of $17bn in virus-related relief may be required to offer an equity stake to the government while for private companies the department “may, at its discretion, accept senior debt instruments” or other financial interests.

A quick refresh of our screens show that most Asian markets are trading lower this morning with the Nikkei (-0.66%), Hang Seng (-0.28%), Shanghai Comp (-0.63%) and Kospi (-1.04%) all down. Elsewhere, futures on the S&P 500 are down -0.54% while June WTI oil prices are up a further +7.82% this morning to $17.80. In other news, the Nikkei reported that BoJ policy makers are likely to discuss unlimited JGB purchases at their meeting on Monday. The report has also added that the BoJ would double targets for purchases of commercial paper and corporate bonds at the meeting.

Onto the data and we got another truly dire set of PMI releases yesterday, especially in Europe with the indicators once again falling right across the board. As we have discussed, because it’s a diffusion index it will always look even more extreme on the down and upside in circumstance like this. In fact we could get a PMI in the 70s or 80s at some point this year without activity being anything close back to normal.

However for completeness, the Euro Area composite PMI fell to a record low of 13.5 (vs. 25.0 expected), with the services reading at 11.7 (vs. 22.8 expected) also at a record low. The manufacturing PMI was relatively stronger at 33.6 (vs. 38.0 expected), since it’s services sectors like hospitality and restaurants that have been the biggest victim of compulsory shutdowns, but it was still deep in contractionary territory and at its own lowest level since February 2009. The country-by-country breakdown didn’t provide much respite, with the composite PMIs in Germany (17.1), France (11.2) and the UK (12.9) all falling to record lows as well. The US composite PMI was “only” as bad as 27.4 however, suggesting that for now their economy has managed to hold up slightly better than their European counterparts with shutdowns less widespread.

Against this backdrop, the initial weekly jobless claims fell to 4.427m in the week up to April 18, slightly below the expected 4.5m reading and down from the revised 5.237m the previous month. If you’re looking for the bright spot amidst the gloom, this was actually the 3rd consecutive week that the number of claims has declined, down from its peak of 6.867m, so a sign that perhaps we’re past the most rapid period of job losses. Nevertheless, this brings the total number of claims over the last 5 weeks to a cumulative 26.453m, which compares to peak nonfarm employment back in February of 152.5m. So it’s looking likely that unemployment could get close to 20% when released on May 8th.

Wrapping up with the other data releases now. In France, the INSEE’s business climate composite indicator fell to 62 in April, its lowest level since the start of the series in 1980. Meanwhile, in Germany, the GfK’s consumer confidence reading for May fell to an all-time low of -23.4. Finally in the US, new home sales in March fell to an annual rate of 627k, with the -15.4% monthly decline being the largest since July 2013.

To the day ahead now, where the data releases include UK retail sales for March, Germany’s Ifo business climate indicator for April, the US preliminary March durable goods orders and non-defence capital goods orders ex air, along with the final April University of Michigan consumer sentiment index. Meanwhile, the Russian central bank will be deciding on interest rates, and earnings releases include Verizon Communications, T-Mobile and American Express.

Even after an impressive bull run on the stock market, state pension funds across the country were facing more than $1 trillion in unfunded debts even before the COVID-19 pandemic struck.

Now, the gap between what pension funds have promised to current workers and retirees and the funds available to make those payments is expected to grow—perhaps quite dramatically.

With some investment returns likely declining by as much as 15 percent this year, thanks to the COVID-19 pandemic, states are going to face a cumulative pension debt of between $1.5 trillion and $2 trillion by the end of the year. That’s according to separate estimates released this week, first by Reason Foundation (which publishes this Reason) and shortly after by the Pew Charitable Trusts.

But the aggregate numbers are only so useful. Some state pension systems were nearly fully funded before the current crisis, and therefore figure to be in better shape to survive it without major problems. States like Kentucky, Illinois, and New Jersey were already in terrible shape are now facing a serious crisis.

“Worse, this is coming after a decadelong bull run in the markets where pensions failed to gain much, if any, ground in terms of funding after the last downturn,” says Len Gilroy, managing director of the Reason Foundation’s pension integrity project. “It’s becoming apparent that we’ve just experienced a Lost Decade for public pension solvency and that policy makers will need to abandon the failed myth that they can invest their way out of this problem.”

We won’t know for sure how badly state pension systems got whacked by the coronavirus-induced economic crash until later in the year, but a new tool released by the Reason Foundation’s pension integrity project offers a glimpse into the potential damage. Using current data from state pension plans and forecasted investment losses, the tool estimates how much more debt states could be facing by the end of the year.

If its investments lose 15 percent this year, for example, New Jersey’s teachers’ pension system would find itself with a mere 30 percent of the assets necessary to cover its long-term costs, and with an unfunded liability of more than $40 billion. Illinois’ teachers pension plan would be more than $75 billion in the red if it sees similar losses this year.

The economic downturn creates a one-two punch for state pensions. Because of the way most public pension funds are structured, lower-than-anticipated investment returns must be made up with tax dollars. But, now, states are also expecting steep drops in tax revenue.

Already, those prospects are causing some state officials to seek a federal bailout. New Jersey State Senate President Stephen Sweeney has called for the feds to offer low-interest loans to states facing severe pension problems.

But federal taxpayers shouldn’t be on the hook to pay for states’ mistakes. There have been plenty of warning signs that public pension systems were in trouble.

“Public pension systems may be more vulnerable to an economic downturn than they have ever been,” Greg Mennis, Susan Banta, and David Draine, three researchers at the Harvard Kennedy School, concluded in a 2018 analysis that “stress tested” each state’s pension system.

Even if annual returns averaged 5 percent, they found, some deeply indebted pension plans in places such as Kentucky and New Jersey would face insolvency. A major economic downturn would be enough to force middle-of-the-road states like Colorado, Ohio, and Pennsylvania to require taxpayer-funded contributions that “may be unaffordable” to avoid insolvency, they wrote.

For years, states have been warned to stop making unrealistic promises about investment returns—a trick used to make shortfalls look smaller than they really are—and to fully fund their retirement systems instead of deferring payments to later years. Both strategies are widespread in state pension systems, and both have contributed to the mess that states now face. Policy makers have clung to the belief that reforms were unnecessary because future investment growth would close the funding gaps.

That idea should now be dispelled. Even a decade of growth wasn’t enough for many pensions to fully recover from the last recession—and that should have been a warning right there, if policy makers were paying attention. Now, the deluge.

from Latest – Reason.com https://ift.tt/2x8jVHK

via IFTTT

All we need are ankle bracelets and Americans would understand what it’s like to be sentenced to home confinement. In a short drive to a grocery store in town last week, I spotted six patrol cars that were out presumably to enforce the stay-at-home orders. Even without those bracelets, we’re essentially prisoners in our homes.

My house sits on six acres—and my dogs, goats and chickens are blithely unaware of the social-distancing requirements (although the cats are getting grumpy about all the extra attention). Life is fairly normal for my family, as we work from home and take breaks by doing chores at the barn.

Even in the nearby tract suburbs, life doesn’t seem that different—at least until we queue up along six-foot markers outside the grocery store. There’s traffic, activity and some semblance of normalcy. In San Francisco, it’s a different story. Life has ground to a halt, and we read ominous reports from Ground Zero—in Manhattan, Seattle, Seoul, and other cities where people live packed together.

For years, urban planners have been singing the praises of population density. In fact, California’ planning model over the past couple decades has revolved around something called New Urbanism. The idea is to set aside as much land as possible as open space—then require developers to build high-density projects in the existing urban footprint. The public still likes single houses with yards, but policymakers are trying to limit that option.

The new rules are justified as part of the state’s battle against climate change. When Jerry Brown was attorney general, he even sued San Bernardino County for permitting too many sprawling developments. The idea that urbanization helps the planet is debatable, given that packed urban centers create heat islands. But the concept fits neatly with existing urban-planning ideology, which decries suburbs as soulless and rural living as wasteful.

Yet after the dust clears from the lockdowns, more Californians will likely be tempted to rethink the high-density status quo. Obviously, diseases spread more quickly where people live cheek by jowl. When a health crisis spreads across the globe, people living in less-dense environs are better able to cope with the madness. My heart goes out to urban dwellers, stuck in their tiny apartments and risking arrest by going to the park for fresh air.

“Density is a factor in this pandemic, as it has been in previous ones,” wrote Richard Florida in the CityLab website. “The very same clustering of people that makes our great cities more innovative and productive also makes them, and us, vulnerable to infectious disease.” Some big cities have handled the crisis better than others. Some rural areas have high infection rates, too. But, as an urban studies professor, he’s distressed at big-city vulnerability.

I find it distressing, too. I like cities for the same reasons as these urbanists and plan on moving back to one after our time on the acreage is done. There’s something exhilarating about the variety and vibrancy in cities, even though urbanists can be overly dismissive of the thriving social connections and civic life that take place in suburban and rural areas. I’ve lived in big cities where no one knows their neighbors, as well as tightly knit “sprawl” suburbs filled with a sense of community.

In reality, the suburbs largely are a product of government planning and subsidy, so there’s no reason that the government should restrict the construction of mid-rises and other higher-density projects in these areas. Some opponents of recent state legislation to give developers the right to build such projects are just as meddlesome as the New Urbanists who want to use government to force only the construction of these projects. They want to legislate their preferences rather than let the market decide.

But while the “get off my lawn” suburban crowd can be awfully annoying, the “you will live in high-density housing” crowd is even worse, given that their prerogatives are in control on virtually every local planning board (not to mention at the state level). Those restrictive policies, by the way, are the most significant reason that so few Californians can afford to buy homes now. The restrictions have reduced housing supply and driven up building costs.

The long-term economic effects of the coronavirus shutdown on the nation’s housing markets is far from clear, of course. Ultimately, it could alter buying patterns, as more people flee tightly packed cities for suburban, exurban, and rural areas that are less susceptible to societal breakdown when pandemics or other crises unfold. Unfortunately, California’s urban-planning rules restrict the ability of people to make those choices.

At the very least, I’d hope that California planners rethink their belief that density always is a good in and of itself—and realize the best way to move forward is to allow builders and buyers as many housing choices as possible.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2VwZmOC

via IFTTT

Even after an impressive bull run on the stock market, state pension funds across the country were facing more than $1 trillion in unfunded debts even before the COVID-19 pandemic struck.

Now, the gap between what pension funds have promised to current workers and retirees and the funds available to make those payments is expected to grow—perhaps quite dramatically.

With some investment returns likely declining by as much as 15 percent this year, thanks to the COVID-19 pandemic, states are going to face a cumulative pension debt of between $1.5 trillion and $2 trillion by the end of the year. That’s according to separate estimates released this week, first by Reason Foundation (which publishes this Reason) and shortly after by the Pew Charitable Trusts.

But the aggregate numbers are only so useful. Some state pension systems were nearly fully funded before the current crisis, and therefore figure to be in better shape to survive it without major problems. States like Kentucky, Illinois, and New Jersey were already in terrible shape are now facing a serious crisis.

“Worse, this is coming after a decadelong bull run in the markets where pensions failed to gain much, if any, ground in terms of funding after the last downturn,” says Len Gilroy, managing director of the Reason Foundation’s pension integrity project. “It’s becoming apparent that we’ve just experienced a Lost Decade for public pension solvency and that policy makers will need to abandon the failed myth that they can invest their way out of this problem.”

We won’t know for sure how badly state pension systems got whacked by the coronavirus-induced economic crash until later in the year, but a new tool released by the Reason Foundation’s pension integrity project offers a glimpse into the potential damage. Using current data from state pension plans and forecasted investment losses, the tool estimates how much more debt states could be facing by the end of the year.

If its investments lose 15 percent this year, for example, New Jersey’s teachers’ pension system would find itself with a mere 30 percent of the assets necessary to cover its long-term costs, and with an unfunded liability of more than $40 billion. Illinois’ teachers pension plan would be more than $75 billion in the red if it sees similar losses this year.

The economic downturn creates a one-two punch for state pensions. Because of the way most public pension funds are structured, lower-than-anticipated investment returns must be made up with tax dollars. But, now, states are also expecting steep drops in tax revenue.

Already, those prospects are causing some state officials to seek a federal bailout. New Jersey State Senate President Stephen Sweeney has called for the feds to offer low-interest loans to states facing severe pension problems.

But federal taxpayers shouldn’t be on the hook to pay for states’ mistakes. There have been plenty of warning signs that public pension systems were in trouble.

“Public pension systems may be more vulnerable to an economic downturn than they have ever been,” Greg Mennis, Susan Banta, and David Draine, three researchers at the Harvard Kennedy School, concluded in a 2018 analysis that “stress tested” each state’s pension system.

Even if annual returns averaged 5 percent, they found, some deeply indebted pension plans in places such as Kentucky and New Jersey would face insolvency. A major economic downturn would be enough to force middle-of-the-road states like Colorado, Ohio, and Pennsylvania to require taxpayer-funded contributions that “may be unaffordable” to avoid insolvency, they wrote.

For years, states have been warned to stop making unrealistic promises about investment returns—a trick used to make shortfalls look smaller than they really are—and to fully fund their retirement systems instead of deferring payments to later years. Both strategies are widespread in state pension systems, and both have contributed to the mess that states now face. Policy makers have clung to the belief that reforms were unnecessary because future investment growth would close the funding gaps.

That idea should now be dispelled. Even a decade of growth wasn’t enough for many pensions to fully recover from the last recession—and that should have been a warning right there, if policy makers were paying attention. Now, the deluge.

from Latest – Reason.com https://ift.tt/2x8jVHK

via IFTTT

Fitch Warns Of Record Loan Defaults In April As Economy Implodes

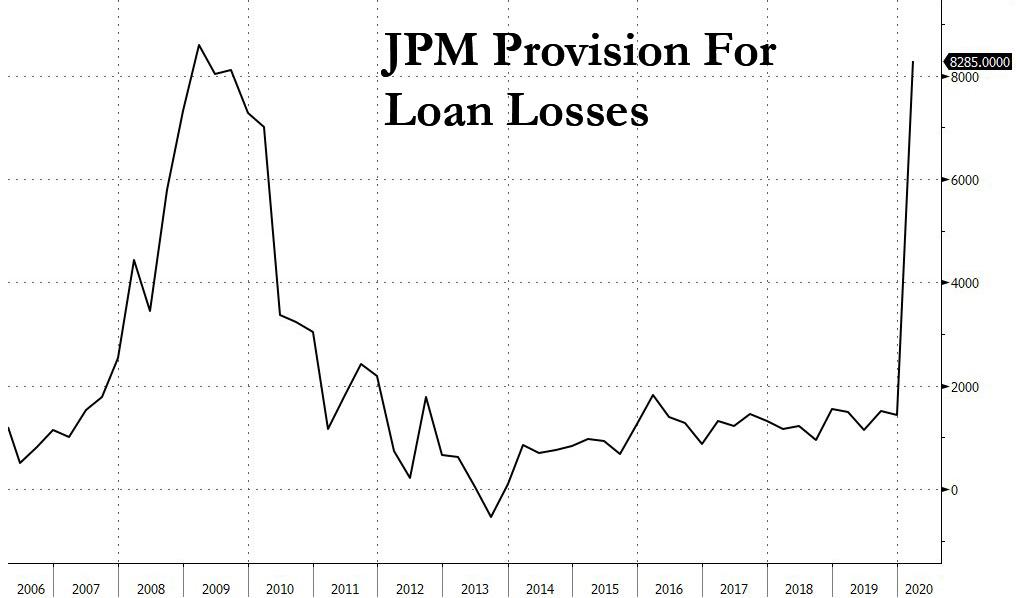

Over the past two weeks, we have observed several very ominous tactical shifts from the largest US commercial bank: after it first announced it would halt all non-government insured loan issuance for the foreseeable future, traditionally the bank’s “bread and butter” business, JPMorgan then said it would raise its mortgage standards, stating that customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value, a dramatic tightening since the typical minimum requirement for a conventional mortgage is a 620 FICO score and as little as 5% down. Then late last week, JPMorgan also said it was had stopped accepting new home equity line of credit, or HELOC, applications.

All this, of course, was happening around the time JPMorgan unveiled a 5x increase to its loan loss provisions, confirming that the bank was expecting a surge in loan defaults.

Overnight, Fitch validated all of Jamie Dimon’s worst fears – and his decision to effectively shut down JPM’s loan issuance machinery – when it warned that it expects the number of institutional term loan defaults in April to top the record of 15 set in 2009.

“Fitch anticipates the default rate will exceed 3% in May, which would be the highest since March 2015,” said Eric Rosenthal, Senior Director of Leveraged Finance. “The $7 billion of April default volume propelled the TTM default rate to 2.6% from 2.2% at March end.”

The 14 defaults registered this month impacted 10 separate sectors, led by three in healthcare/pharmaceutical which is perhaps a little odd with everyone focusing on the tsunami about to sweep through the energy sector. At least another $3 billion is projected to occur this month, with Neiman Marcus Group Inc. and Akorn Inc. expected to default imminently.

As reported previously, several other large companies have missed corresponding bond interest payments earlier this month and are likely to file bankruptcy including Intelsat Investments, JC Penney, and Ultra Resources.

According to Fitch, Neiman’s and JC Penney’s defaults would together lift the retail rate to 13% from the current 7% level. The default rate for retail is then forecast to jump to 19% by year end, led by anticipated defaults for Serta Simmons Bedding, J Crew, Ascena Retail Group, and Jo-Ann Stores.

Meanwhile, the energy default rate stands at 5.5%, but sizable expected defaults from Seadrill Partners, California Resources and Chesapeake Energy would push the rate to 18.0% by year end.

The telecommunications default rate reached 4.0% following Frontier Communications’ bankruptcy and would rise above 7.5% once Intelsat – which also missed a coupon payment – also files.

Fitch’s Top and Tier 2 Loans of Concern’s combined lists total $258.5 billion, exceeding 18% of the loan index. This is up from $233.6 billion last month and two and a half times above the $102.1 billion of February’s pre-pandemic total. The Top Loans of Concern total jumped to $69.4 billion from $54.8 billion in March. Retail, energy, healthcare/pharmaceutical and telecommunications together account for 60% of the Top Loans of Concern’s outstandings.

Last month, Fitch raised its 2020 default forecast to 5%-6% from 3%, equating to roughly $80 billion of volume which would top the record $78 billion from 2009. In addition, Fitch projects an 8%-9% default rate for 2021. If the expected recession becomes prolonged, a double-digit default rate is conceivable for 2021.

In a similar report last week, Moody’s warned that an “unprecedented jump” in its “B3 Negative and Lower” tally underscores the “sharp deterioration in credit conditions.”

Our B3 Negative and Lower Corporate Ratings List (B3N list) soared to its highest tally ever of 311 companies (see Exhibit 1), topping its old peak of 291 companies hit during credit crisis of 2009 and commodity-related downturn in April 2016. This spike is the result of the confluence of a coronavirus outbreak, tanking oil prices, and mounting recessionary conditions, which combined created severe and extensive credit shocks across many sectors, regions and markets, the effects of which are unprecedented.

Ironically, even as cash flows collapse, and a wave of bankruptcies hits corporations, which will add millions in unemployed workers to the tens of millions already laid off due to the coronavirus, stocks remains within spitting distance of all time highs. We only note that in case anyone still harbors any delusion that markets reflect anything but the trillions in liquidity that the Fed is injecting at any given moment.