Landlords Are Reportedly Asking Broke Tenants To ‘Pay’ Rent With Sex

Desperate times call for desperate measures. And with the Fed in the process of destroying the monetary system as we know, we can’t say we were surprised to hear that some landlords were attempting to use the age-old system of barter to accept payments.

The problem? They’re reportedly asking their broke tenants for sex, according to BuzzFeed.

Citing the Hawaii State Commission on the Status of Women, the report details several complaints of sexual harassment since the coronavirus outbreak began.

One woman says when she texted her landlord about a more affordable property after being unable to pay her April rent, “he responded with a dick pic.” A different woman claimed that her landlord told her she could come over and “spoon him” instead of paying her April rent.

Khara Jabola-Carolus, the executive director of the commission said: “We’ve received more cases at our office in the last two days than we have in the last two years.”

She thinks the cases are becoming more egregious as tenants become unemployed, broke and more vulnerable. “Of course that’s not the root cause of why it’s happening, but it makes it easier because now [landlords] have access to people at their fingertips,” she said.

Sheryl Ring, the legal director at Open Communities, a legal aid and fair housing agency just north of Chicago said: “We have seen an uptick in sexual harassment. Since this started, they [landlords] have been taking advantage of the financial hardships many of their tenants have in order to coerce their tenants into a sex-for-rent agreement — which is absolutely illegal.”

She says sexual harassment complaints related to housing are up threefold in the last month. Ring was already working on six cases before the epidemic began and says that women of color and trans women are the most likely to be targeted. Ring advises women not to give in to trying to negotiate with landlords at all if the topic comes up.

“You can’t really negotiate how much illegality the landlord is willing to do,” she said. “We’ve heard some landlords are attempting to use the situation where a tenant falls behind to pressure a tenant into exchanging sex for rent,” she continued.

“It’s important to know what your rights are as quickly as possible. Even now, just because courts are closed to most things, it doesn’t mean you do not have recourse right now and can’t be protected,” Ring concluded.

“The conditions are ripe for sexual exploitation,” said Jabola-Carolus, noting that since Hawaii’s tourism industry has fallen apart, many immigrant and native Hawaiians are out of work.

Jabola-Carolus concluded: “The power dynamic goes without saying. All of us feel intimidated by our landlords because shelter is so critical.”

For this week’s round-up of articles, we noticed a theme: the most alarming articles are about governments going over-the-top, grabbing powers in the name of stopping the Coronavirus.

Here are some examples that we found absurd, and downright creepy:

WHO officials says next step could be separating families

A World Health Organization official said that the next step in controlling the spread of the virus could involve raiding homes, and separating families.

Here is what the Executive Director at the WHO Health Emergencies Program, Dr. Michael Ryan, said during an interview:

“In most parts of the world, due to lockdown, most of the transmission that’s actually happening in many countries now is happening in the household, at family level. In some senses, transmission has been taken off the streets and pushed back into family units. Now we need to go and look in families and find those people who may be sick and remove them, and isolate them, in a safe and dignified manner.”

Well that escalated quickly. Now we are talking about raiding homes and seizing family members who are sick.

Where is the limit on government powers during an emergency?

Watch the video here (skip to 50:00)…

Colorado County kicks out everyone who isn’t an official resident

Nonresidents in Gunnison County Colorado could face $5,000 fines and 18 months in prison if they don’t leave.

But it is not just vacation renters and temporary workers who the town has told to take a hike.

“Non-resident homeowners” are also now banned from stepping foot on their own property within county limits.

So even if someone owns a vacation home, or second house in the county, unless it is their official legal residence, the county claims the authority to arrest and imprison homeowners.

Prison. For simply being on your own private property.

Back in February, Chinese scientists were free to publish studies about the coronavirus with normal peer-review standards.

But now, any Chinese researcher looking to publish a study or paper tracing the origins of the CoronaVirus must first gain government approval.

What’s interesting is that even the order from the government, which mandates censorship over research, was itself censored!

Two universities (who were conducting research on the origins of the coronavirus) received a censorship order from the government.

The universities then posted the censorship order on their websites. Then, suddenly, poof… both their research, AND the censorship order, vanished.

(Fortunately the research still exists, and the censorship order was archived by web crawlers. Let that be a lesson: the Internet is forever.)

The order shows an announcement of new rules from the State Council called “Notice on the publication of academic papers related to the New Coronary Pneumonia Epidemic.”

In addition to extra academic scrutiny, the notice tells colleges to submit the papers to the government council. They will decide if it will be approved for publication, in China and abroad.

The Chinese government wants to give the impression that the reason for this is purely high academic standards– making sure false information doesn’t get out surrounding the virus.

Or perhaps they might be trying to control the narrative as rumors swirl and criticism mounts.

California Department of Justice raids private businesses to seize masks

The California Department of Justice is tight-lipped about a handful of raids last week.

In one of three locations, agents confiscated about 50,000 masks from a man they claim does not have a license to resell the masks.

The owner of one warehouse, however, claims he does in fact have a license to sell the masks, and acquired them legally. He was given a citation anyway.

Others in California have been arrested in sting operations for “price gouging” while selling N95 respirator masks. The state defines “price gouging” as selling an emergency item for more than a 10% mark-up during an emergency.

Watch Live: White House Coronavirus Task Force Holds Friday Briefing

The Democrats and Republicans are still battling over a bill to replenish the government’s tapped emergency lending program for small businesses, President Trump and the Pence-led White House Task Force are holding their first press briefing since delegating control of the economic reopening to the governors.

Hopefully, tonight’s briefing, which is slated to begin at 6pmET, will actually start on time, and not drag on for hours of repetitive guidance and tiresome sniping from the press.

Mexico Downgraded To Baa1 By Moody’s; “Negative Outlook” Means Junking Imminent

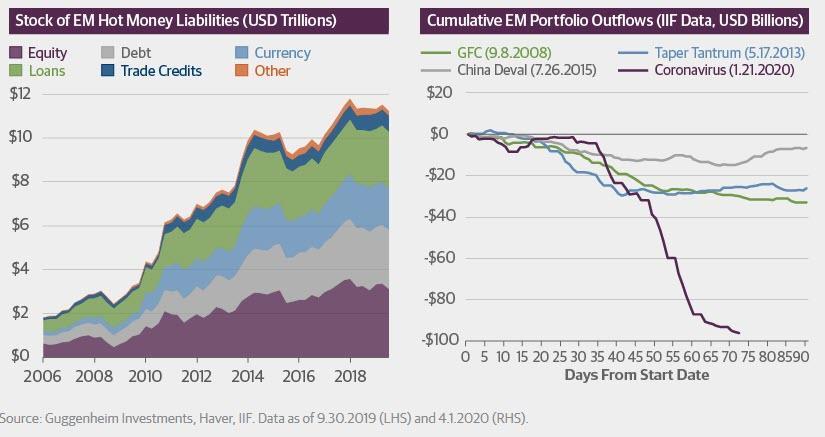

Just days after Scott Minerd warned of an emerging markets “apocalypse”, which he thinks would be the next shoe to drop in the ongoing global covid crisis as unlike developed nations emerging markets can’t just print their way out of a sharp recession at a time when EMs are suffereing massive FX reserve (read dollar) outflows…

… Fitch two days ago downgraded the one country many believe could be the ground zero of the next phase of the crisis, Mexico, to the lowest notch above junk, warning that “the economic shock represented by the coronavirus pandemic will lead to a severe recession in Mexico in 2020” and that “the outlook for the public finances is much less favorable than at the time of the last rating review in December 2019.”

But while Fitch’s new rating has a stable outlook, meaning a downgrade to junk isn’t imminent, Moody’s wasn’t as forgiving and moments after the close of FX trading (hardly a coincidence), the rating agency followed in Fitch’s footsteps, and also downgraded Mexico to the lowest investment grade rating, however this action had a negative outlook, meaning that a downgrade to junk can come at any moments, at which point the trickle of FX reserves out of Mexico would become a flood as foreign investors – prohibited by their mandate from investing in junk rated sovereigns – pull their capital.

Commenting on the action, Moody’s said that the key drivers behind the rating downgrade are: 1) Mexico’s medium term economic growth prospects have materially weakened; 2) The continued deterioration in Pemex’s financial and operational standing is eroding the sovereign’s fiscal strength, which is already pressured by slower revenue growth due to a weaker economy; and 3) Weakened policymaking and institutional capacity.

More importantly, this is why Moody’s kept a negative outlook:

The negative outlook captures the risk that the absence of effective measures to address the country’s economic challenges and contain the contingent liability stemming from Pemex could erode economic and fiscal strengths beyond what is contemplated by the downgrade to Baa1. In Moody’s view, the policy response has become less predictable and the spectrum of possible economic and fiscal policy outcomes has widened.

Mexico’s economic contraction in 2020 could be even deeper and the recovery could take longer than what Moody’s anticipates. If the pandemic worsens, pressures to increase government spending would add to the deteriorating fiscal and debt dynamics. Legislative as well as state and local elections in 2021 increase the risk that the federal government will boost spending ahead of the elections.

In short get out while you can, which will be less than welcome news for all those Mrs Watanabes who bought the MXN today after Fitch’s downgrade will simply because the currency had upward momentum. Newsflash: the Fed may be buying junk bonds, but they are domestic junk bonds. Nobody will buy Mexican junk.

* * *

Full Moody’s downgrade below:

Moody’s Investors Service, (“Moody’s”) has today downgraded the Government of Mexico’s long-term foreign-currency and local-currency issuer ratings to Baa1 from A3. The outlook remains negative.

The key drivers behind the rating downgrade are:

1) Mexico’s medium term economic growth prospects have materially weakened

2) The continued deterioration in Pemex’s financial and operational standing is eroding the sovereign’s fiscal strength, which is already pressured by slower revenue growth due to a weaker economy

3) Weakened policymaking and institutional capacity

The Baa1 takes into account the country’s large and diversified economy, the lack of major macroeconomic imbalances, and its fiscal strength, which despite deteriorating, is comparable to that of Baa1-rated peers. The credit profile is also supported by a healthy financial system and a sound monetary policy setting.

The negative outlook reflects the risk that economic and fiscal strength deteriorate beyond what is captured in a Baa1 rating due to ongoing uncertainties related to policy direction in the medium term and policy responses that have been insufficient to effectively address both the country’s economic challenges and Pemex’s continued financial and operating problems.

Moody’s also downgraded Mexico’s long-term foreign-currency and local-currency senior unsecured debt ratings to Baa1 from A3, the senior unsecured MTN ratings to (P)Baa1 from (P)A3, and the foreign-currency senior unsecured shelf rating to (P)Baa1 from (P)A3.

All of Mexico’s long-term country risk ceilings were revised down by one notch. Its long-term local-currency bond and bank deposits ceilings were revised down to A1 from Aa3, and the long-term foreign-currency bond ceiling to A2 from A1. The short-term bond foreign-currency ceiling remained unchanged at Prime-1. Moody’s also lowered the long-term foreign-currency bank deposits ceilings to Baa1 from A3 and the short-term foreign-currency bank deposits ceiling was maintained at Prime-2.

RATIONALE FOR THE RATING DOWNGRADE TO Baa1

MEXICO’S MEDIUM TERM ECONOMIC GROWTH PROSPECTS HAVE MATERIALLY WEAKENED

Moody’s expects medium term growth to remain depressed, even when removing this year’s severe economic contraction due to the coronavirus shock, with the economy growing at best 2% on average in 2021-23. This represents a marked deterioration from the 2.7% average growth rate Mexico reported between 2010-19.

When Moody’s upgraded the ratings to A3 from Baa1 in 2014, the rating agency expected at that time that the implementation of a broad range of structural reforms would lead to an increase in Mexico’s potential growth north of 3%. Since then, however, implementation has been uneven at best, with the energy reform being de facto reversed and other reforms not yielding the anticipated impact on total factor productivity and potential growth, in some cases due to poor execution.

Economic policy decisions and mixed policy messages under the current administration have materially altered business sentiment and will likely continue to dampen private sector investment in the coming years, further lowering Mexico’s medium term growth prospects. The first policy decision was the cancellation of Mexico city’s new airport in October 2018, a political decision that dismissed clear warnings about negative economic ramifications. The lack of clarity over the role private investment will have in the electricity sector also poses risk to investment in renewable projects and natural gas pipelines, since the government has yet to define an agenda. More recently, the government’s cancelation of a large brewery project already under construction was considered a strong blow to investor confidence by business chambers in Mexico.

THE CONTINUED DETERIORATION IN PEMEX’S FINANCIAL AND OPERATIONAL STANDING IS ERODING THE SOVEREIGN’S FISCAL STRENGTH

The government’s change in Pemex’s business model is adding to the severe financial and operational challenges of the company. The government has discontinued and reversed many aspects of the energy reform of 2014. In the absence of private sector investment to help Pemex increase production and maintain reserves, support is coming from the government. The current oil price shock has further impacted Pemex’s profitability and increased its liquidity needs, adding to the need for ongoing sizable support that is pressuring government finances.

Moody’s believes that given Pemex’s negative free cash flow and upcoming debt obligations, supporting the company in 2020-22 for liquidity purposes will cost the sovereign up to 2% of GDP each year during that period. If in addition the government were to decide to provide the support needed to increase capital expenditures required to meet current oil production targets and fully replace reserves, the overall level of support would rise to up to 3% of GDP each year, according to the rating agency. Even though the government is cutting government spending to try to adhere to fiscal targets, the impact of higher support to Pemex, anemic government revenues amid weaker GDP growth and rising interest burden will lead to higher fiscal deficits and increased debt ratios. Under Moody’s baseline scenario, the debt burden is likely to increase 10 percentage points to 46.2% of GDP bu 2022 from 36.4% of GDP in 2019. If the impact of the coronavirus outbreak is more severe and the government responds with increased fiscal measures, debt burden would likely rise beyond the 50% mark by 2022, and even more so if in addition the government were to fully fund PEMEX’s capital expenditure needs.

WEAKENED POLICYMAKING AND INSTITUTIONAL CAPACITY

The third factor informing today’s rating action is Moody’s view that the quality of policymaking and the institutional capacity to respond to shocks, elements which the rating agency considers a governance factor under its ESG framework, have weakened.

Economic policy decisions over the last year and a half and mixed messages are dampening business sentiment and investment prospects. In addition, conflicting social, fiscal and energy sector policy objectives will make it increasingly difficult for the authorities to sustain the current policy stance over time, leading to uncertainty about the potential sovereign credit consequences of future policy shifts, according to the rating agency. Government measures intended to support Pemex, for instance, have been piecemeal and insufficient to effectively address the company’s longstanding financial and operational challenges, which give rise to the risk of abrupt policy changes.

In Moody’s view, broad based salary and benefit cuts across government ministries have weakened the government’s administrative capacity. Combined with the significant reduction in budget and governance changes to some autonomous regulatory institutions, Moody’s believes that the country’s institutional capacity has been eroded, impacting the capacity to respond and manage shocks effectively and reducing the predictability of the regulatory framework.

RATIONALE FOR A NEGATIVE OUTLOOK

The negative outlook captures the risk that the absence of effective measures to address the country’s economic challenges and contain the contingent liability stemming from Pemex could erode economic and fiscal strengths beyond what is contemplated by the downgrade to Baa1. In Moody’s view, the policy response has become less predictable and the spectrum of possible economic and fiscal policy outcomes has widened.

Mexico’s economic contraction in 2020 could be even deeper and the recovery could take longer than what Moody’s anticipates. If the pandemic worsens, pressures to increase government spending would add to the deteriorating fiscal and debt dynamics. Legislative as well as state and local elections in 2021 increase the risk that the federal government will boost spending ahead of the elections.

ENVIRONMENTAL, SOCIAL AND GOVERNANCE CONSIDERATIONS

Environmental risks are not material to Mexico’s credit profile. While some Mexican states in the coasts are exposed to extreme weather effects that may impact the finances of sub-sovereign states via reduced tourism, and disaster-relief and preparedness expenditure, they carry limited risk to the sovereign credit profile.

Social risks are material for Mexico. Moody’s considers the coronavirus outbreak to be a social factor under its ESG framework, given the substantial implications for public health and safety. The coronavirus crisis is likely to weigh significantly on employment levels in the short term, increasing social needs and therefore pressure on the government’s finances. Moreover, like other middle-income countries in Latin America, Mexico will be faced with a steadily ageing population in the coming decades. This ageing, in the context of a social security system that is both not universal and underfunded, will result in social demands that future administrations will have to contend with.

Governance risks are material for Mexico and, as noted above, a weakening policy framework and reduced administrative capacity contributed to today’s rating action. A deterioration in the decision making process is leading to economic policies that affect investment prospects and limit the government’s ability to respond to shocks. While the strength of key institutions such as the Central Bank supports macroeconomic stability, Mexico has scored poorly on institutional factors for more than a decade, as measured by the Worldwide Governance Indicators, with control of corruption and rule of law among its weakest areas.

FACTORS THAT COULD LEAD TO AN UPGRADE OR DOWNGRADE OF THE RATINGS

Although a rating upgrade is unlikely in the near future, a return to a stable outlook could result from regained confidence in the government’s ability to lay out and implement consistent policies and improve growth prospects in the medium term. A credible plan towards Pemex that would reduce the risk of recurrent and substantial government support to the company, while addressing the challenges facing the sector, would also support a return to stable outlook.

Further evidence that medium-term growth is in decline would put downward pressure on the rating. Rising fiscal deficits that cause the debt trajectory to shift upward beyond what we anticipate in our baseline scenario, whether due to recurrent financial support to PEMEX, a material increase in government spending or given a substantial decline in government revenues, could also lead to a downgrade. A continued deterioration in the policy framework would also add negative pressure to the rating.

GDP per capita (PPP basis, US$): 20,616 (2018 Actual) (also known as Per Capita Income)

Real GDP growth (% change): 2.1% (2018 Actual) (also known as GDP Growth)

Inflation Rate (CPI, % change Dec/Dec): 4.8% (2018 Actual)

Gen. Gov. Financial Balance/GDP: -1.8% (2018 Actual) (also known as Fiscal Balance)

Current Account Balance/GDP: -1.9% (2018 Actual) (also known as External Balance)

External debt/GDP: 36.6% (2018 Actual)

Economic resiliency: baa2

Default history: No default events (on bonds or loans) have been recorded since 1983.

On 14 April 2020, a rating committee was called to discuss the rating of the Mexico, Government of. The main points raised during the discussion were: The issuer’s economic fundamentals, including its economic strength, have materially decreased. The issuer’s fiscal or financial strength, including its debt profile, has materially decreased. Other views raised included: The issuer’s institutions and governance strength, has deteriorated.

No “Buy American” This Time: Munger Warns Berkshire “Will Shutter Some Businesses”

On Oct 16, 2008, in what seemed America’s darkest hour at least until a Chinese manmade virus escaped a Wuhan lab and killed thousands of Americans, forcing the Fed to nationalize capital markets and preserve social order by artificially inflating stock prices to idiotic levels based on the complete collapse in earnings, Warren Buffett came to America’s rescue by frontrunning a multi-trillion taxpayer bailout of US banks when he penned a NYT Op-ed “Buy American. I am” in which he wrote “The financial world is a mess, both in the United States and abroad….So, I’ve been buying American stocks.” And sure enough, Berkshire spent tens of billions of dollars investing in General Electric, Goldman Sachs Group, and many others as well as buying Burlington Northern Santa Fe outright.

And yet, for all his pompous poseur patriotism, the Omaha billionaire knew he was exposed to zero risk as US taxpayers would bail out the companies he was buying if it all came crashing down. In other words, what Buffett did not say at the time, is that he only “bought stocks” because he was frontrunning the largest bailout in US history.

Until now… when a newly merged Fed and Treasury have unleashed helicopter money which will amount to tens of trillions in “bailout” funds and liquidity injections, which are really meant to spark hyperinflation and inflate away the world’s record amount of debt.

So will Berkshire step up now to “Buy American” again in a repeat attempt to spark a wave of patriotic buying by retail investors? Don’t count on it.

In an interview with the WSJ’s Jason Zweig, best known for calling gold – whose price is now just shy of all time highs – a “pet rock” in 2015, Buffett’s right hand man, Charlie Munger explained that Berkshire’s patriotic buying would be far more muted this time… if at all:

“I would say basically we’re like the captain of a ship when the worst typhoon that’s ever happened comes. We just want to get through the typhoon, and we’d rather come out of it with a whole lot of liquidity. We’re not playing, ‘Oh goody, goody, everything’s going to hell, let’s plunge 100% of the reserves [into buying businesses].’”

He added, “Warren wants to keep Berkshire safe for people who have 90% of their net worth invested in it. We’re always going to be on the safe side. That doesn’t mean we couldn’t do something pretty aggressive or seize some opportunity. But basically we will be fairly conservative. And we’ll emerge on the other side very strong.”

Something else odd: unlike 2008 when every CEO was begging Buffett for a bailout, this time executives have learned that they can just go to the Fed. Asked if “hordes of corporate executives” are calling Berkshire begging for capital, Munger said “No, they aren’t. The typical reaction is that people are frozen. Take the airlines. They don’t know what the hell’s doing. They’re all negotiating with the government, but they’re not calling Warren. They’re frozen. They’ve never seen anything like it. Their playbook does not have this as a possibility.”

He repeated for emphasis, “Everybody’s just frozen. And the phone is not ringing off the hook. Everybody’s just frozen in the position they’re in.”

As Zweig correctly (this time) notes, “with Berkshire’s vast holdings in railroads, real estate, utilities, insurance and other industries, Mr. Buffett and Mr. Munger may have more and better data on U.S. economic activity than anyone else, with the possible exception of the Federal Reserve. But Mr. Munger wouldn’t even hazard a guess as to how long the downturn might last or how bad it could get.”

“Nobody in America’s ever seen anything else like this,” said Munger. “This thing is different. Everybody talks as if they know what’s going to happen, and nobody knows what’s going to happen.”

Which is an interesting – if hypocritical – observation since if “nobody knows what’s going to happen” how is everyone also saying it won’t be a depression, Munger included?

“Of course we’re having a recession,” said Mr. Munger. “The only question is how big it’s going to be and how long it’s going to last. I think we do know that this will pass. But how much damage, and how much recession, and how long it will last, nobody knows.”

He added, “I don’t think we’ll have a long-lasting Great Depression. I think government will be so active that we won’t have one like that. But we may have a different kind of a mess. All this money-printing may start bothering us.”

Finally, can the government reduce its role in the economy once the virus is under control?

“I don’t think we know exactly what the macroeconomic consequences are going to be,” said Mr. Munger. “I do think, sooner or later, we’ll have an economy back, which will be a moderate economy. It’s quite possible that never again—not again in a long time—will we have a level of employment again like we just lost. We may never get that back for all practical purposes. I don’t know.”

Munger may not know, but Buffett does and explains why this time he will not only not be buying, but in fact shuttering:

“This will cause us to shutter some businesses,” Munger said. “We have a few bad businesses that…we could be tolerant of as members of the family. Somebody else would have already shut them down. We’ve got a few businesses, small ones, we won’t reopen when this is over.”

Finally, here is what Berkshire thinks stocks will do in the future. “I don’t have the faintest idea whether the stock market is going to go lower than the old lows or whether it’s not.” The coronavirus shutdown is “something we have to live through,” letting the chips fall where they may, he said. “What else can you do?”

Trump Slams Cuomo: “Spend Less Time Complaining And More Time Doing”

Here’s a message for Andrew Cuomo: When the president delegates, he delegates.

President Trump has apparently realized that the process of reopening this country might be more complicated than he initially anticipated, and affirmed that the ball is now in the governors’ court – and that includes the hard-hit states like New York.

Because after tweeting messages about “Liberating” various states, he has turned his attention to Gov. Andrew Cuomo who earlier was repeating demands that the Feds fork over more money to help his state finance a massive statewide testing initiative.

Trump responded with a valid point that some might find callous, but remains nevertheless true: the Feds handed over plenty of additional resources to NY including beds and equipment and a floating hospital ship. And many of those resources went unused.

Now, Cuomo is demanding more money to test millions of people who probably haven’t had the opportunity to contract the virus over the last 3 weeks. But regardless, it appears Trump has drawn a line in the sand: He has delegated the responsibility to the states. Other than doling out money in stimulus packages, the White House is taking a back seat and letting the governors get to work, just like all of Trump’s critics wanted.

Governor Cuomo should spend more time “doing” and less time “complaining”. Get out there and get the job done. Stop talking! We built you thousands of hospital beds that you didn’t need or use, gave large numbers of Ventilators that you should have had, and helped you with….

….testing that you should be doing. We have given New York far more money, help and equipment than any other state, by far, & these great men & women who did the job never hear you say thanks. Your numbers are not good. Less talk and more action!

And as the information war with China continues, Trump commented on the latest ‘revision’ to Wuhan’s death toll and total case count, echoing past tweets accusing the Chinese of lying about their numbers.

China has just announced a doubling in the number of their deaths from the Invisible Enemy. It is far higher than that and far higher than the U.S., not even close!

To sum up: If nothing else, these tweets suggest that Trump understands that trying to barge back in and seize back control at this point would be a terrible political miscalculation.

American justice is built to a disturbing degree on fining citizens, often very poor ones, for petty crimes. In the COVID-19 age of unprecedented unemployment, paying those fines has become harder than ever for many.

The Fines and Fees Justice Center is keeping track of states’ reactions to the pandemic age. Some good news: The $1,200 checks from the federal government are being protected from garnishment for outstanding fines across the board.

Decent actions taken by states and localities when it comes to COVID-19 include:

• California is, on the state level, suspending criminal justice and most other government-owed debt collections via “wage garnishments, bank levies, and tax intercepts” (including a cessation of levies and license suspensions for child support payments) and some California localities are doing the same for their citizen-owed fines.

• Delaware has “suspended the active collection of payment for criminal, civil and traffic assessments”; Louisiana has also “suspended the requirement to make scheduled payments of fines, fees and court costs until further notice”; Oregon has similarly stopped imposing “late fees, suspending driver licenses for nonpayment, sending delinquency notices, imposing collection fees/referring new cases to collections, and issuing new garnishments.”

• Florida is suspending most fine-triggered drivers license suspensions and Miami Dade County has decided that those “whose criminal, misdemeanor, or traffic payment plans are cancelled due to non payment during the timeframe that the courthouses are closed to the public, can re-enroll without any penalty or additional fees.”

• Idaho is giving two-month extensions on hearings regarding fines; a couple of Georgia counties are giving 90-day extensions on municipal fines and fees; various Illinois cities and counties are giving varied length extensions or halts in interest accrual on fines due or the time they’ll be turned over to collection agencies; Iowa is also suspending delinquency fees on fines owed for more than 30 days; Minnesota is acting similarly.

• Maine is “vacating warrants for unpaid fines, restitution, court-appointed counsel fees, failure to appear for unpaid fine hearings, and other failure to appear warrants”; Brooklyn, New York, has also declared “no warrants or civil judgments will be issued for unpaid court debt” for 60 to 90 days; Kentucky is also “prohibiting the arrest or detention of any person served with a warrant for nonpayment of court costs, fees, or fines, or with a warrant for a failure to appear on a violation”; Nebraska is doing similarly.

• Reading, Pennsylvania, in an attempt to cease creating new debt slaves to the city, has done a lot to make things easier, including ending late penalties, extending deadlines for challenging citations; ending new parking tickets entirely (including at meters) and no more booting cars for now.

The Marshall Project reports some of the not-so-good news for those burdened with petty fines: Cops in Tulsa, Oklahoma, for example, are continuing “to arrest people for failing to pay court debts—even ones more than a decade old.”

Courts and governments have a strong incentive to show no mercy to poor Americans trapped in their fines and fees machinery, since, as The Marshall Project notes, “Two main sources of revenue—sales taxes from now-shuttered restaurants and bars, and traffic tickets from now-empty highways—have cratered. This comes at a time when officials are straining to pay for, among other things, desperately needed medical equipment and unemployment benefits for record numbers of laid-off workers.” Some are thus in the COVID-19 age adding new reasons to fine citizens, including “for violating orders to stay at home and wearmasks.“

Such fines are enough to crush many poor Americans even in better times, but localities almost always think they need their payoff. More than $50 billion in such fines are due in America for either actual crimes or merely for related late fees. court costs, and interest.

One looming problem is a lot of those prophylactic measures have short time limits, and the likelihood that most Americans who owe fines for petty crimes will be in a better position to pay them in 60 to 90 days seems very small. The courts will soon either need to rethink their policies or see lots of new fines, warrants, and court cases, in a time when fines will be harder than ever to pay and shoving more citizens in jails and prisons is particularly cruel.

from Latest – Reason.com https://ift.tt/2VC04sB

via IFTTT

Between 48,000 and 81,000 residents of Santa Clara County, California are likely to have already been infected by the coronavirus that causes COVID-19, suggests a new study by researchers associated with Stanford University Medical School. The researchers tested a sample of 3,330 residents of the county using blood tests to detect antibodies to determine whether or not they had been exposed to the coronavirus. If the researchers’ calculations are correct, that’s really good news. Why? Because that data will help public health officials to get a better handle on just how lethal the coronavirus is, and if researchers are right it’s a lot less lethal than many have feared it to be.

Currently, the U.S. case fatality rate, that is, the percent of people with confirmed diagnoses of COVID-19 who die, is running at 5.2 percent. But epidemiologists have known that a significant proportion of people who are infected are going undetected by the medical system because either they don’t feel sick enough to seek help or are asymptomatic. For example, recent research in Iceland suggests that about 50 percent of people infected with the virus have no symptoms.

In the new study, the researchers sought residents through Facebook to whom they could administer the antibody tests. The results were an unadjusted prevalence of coronavirus antibodies of 1.5 percent. After making various statistical and demographic adjustments, researchers calculated the likely prevalence ranged from 2.49 to 4.16 percent. At the time that these tests were administered, there were about 1,000 confirmed COVID-19 cases and 100 deaths from the disease in Santa Clara County. The upshot is that “these prevalence estimates represent a range between 48,000 and 81,000 people infected in Santa Clara County by early April, 50- 85-fold more than the number of confirmed cases.”

Using these data, the researchers calculated the infection fatality rate, that is, the percent of people infected with the disease who die: “A hundred deaths out of 48,000-81,000 infections corresponds to an infection fatality rate of 0.12-0.2%,” they report. That’s about the same infection fatality rate the Centers for Disease Control and Prevention (CDC) estimates for seasonal influenza.

The researchers conclude:

While our study was limited to Santa Clara County, it demonstrates the feasibility of seroprevalence surveys of population samples now, and in the future, to inform our understanding of this pandemic’s progression, project estimates of community vulnerability, and monitor infection fatality rates in different populations over time. It is also an important tool for reducing uncertainty about the state of the epidemic, which may have important public benefits.

Assuming that their findings are happily confirmed, among the important public benefits would be a quicker end to the pandemic lockdown we are all experiencing. It’s high time the CDC gets it act together and conducts similar antibody population screening to determine the prevalence of the disease across the nation.

from Latest – Reason.com https://ift.tt/2wO0hk1

via IFTTT

The Labor Department reported yesterday that nearly 5.25 million Americans filed for unemployment over the last week. This brings the total over the last month to more than 22 million Americans. As bad as these numbers are, it’s likely they’re severely underreported as many people continue to have trouble accessing their state’s unemployment websites.

The SBA’s website said it is “unable to accept new applications for the Paycheck Protection Program based on available appropriations funding. Similarly, we are unable to enroll new PPP lenders at this time.”

The onus is now on Congress to quickly expand the amount of fund’s available for the program. Besides the obvious reason that small businesses money, why is this so imperative?

Small businesses employ about 47% of all American workers and 7.5 million of them could permanently go out of business over the next few months if the effects of COVID-19 persist.

According to a survey of 5,850 small business owners conducted by Main Street America, nearly one-third of small businesses would go out of business if current conditions persisted for up to two months. The number jumps to two-thirds of small businesses going out of business if current conditions persisted for up to five months.

In terms of how many small businesses that could affect, the numbers indicate 3.5 million small businesses going out of business within two months and 7.5 million within five months.

Eight in ten of those surveyed have already temporarily closed their businesses, with more than half of them seeing their company’s revenues fall by at least 75%. More than 90% of those surveyed have seen their company’s revenues fall, while only 1.5% of business owners have seen their company’s revenues increase.

While small businesses remain temporarily closed without access to any more small business loans, Amazon has clearly been the beneficiary. With limited shopping options for consumers who are confined to their homes, shares of Amazon have hit fresh all-time highs for the last three days. Shares are now up more than 30% year-to-date, adding nearly $300 billion to its market capitalization.

With jobs being lost at an unprecedented pace and many small businesses facing an imminent threat of having to close for good, the ramifications of the economy remaining closed are getting more dire by the day for many

American justice is built to a disturbing degree on fining citizens, often very poor ones, for petty crimes. In the COVID-19 age of unprecedented unemployment, paying those fines has become harder than ever for many.

The Fines and Fees Justice Center is keeping track of states’ reactions to the pandemic age. Some good news: The $1,200 checks from the federal government are being protected from garnishment for outstanding fines across the board.

Decent actions taken by states and localities when it comes to COVID-19 include:

• California is, on the state level, suspending criminal justice and most other government-owed debt collections via “wage garnishments, bank levies, and tax intercepts” (including a cessation of levies and license suspensions for child support payments) and some California localities are doing the same for their citizen-owed fines.

• Delaware has “suspended the active collection of payment for criminal, civil and traffic assessments”; Louisiana has also “suspended the requirement to make scheduled payments of fines, fees and court costs until further notice”; Oregon has similarly stopped imposing “late fees, suspending driver licenses for nonpayment, sending delinquency notices, imposing collection fees/referring new cases to collections, and issuing new garnishments.”

• Florida is suspending most fine-triggered drivers license suspensions and Miami Dade County has decided that those “whose criminal, misdemeanor, or traffic payment plans are cancelled due to non payment during the timeframe that the courthouses are closed to the public, can re-enroll without any penalty or additional fees.”

• Idaho is giving two-month extensions on hearings regarding fines; a couple of Georgia counties are giving 90-day extensions on municipal fines and fees; various Illinois cities and counties are giving varied length extensions or halts in interest accrual on fines due or the time they’ll be turned over to collection agencies; Iowa is also suspending delinquency fees on fines owed for more than 30 days; Minnesota is acting similarly.

• Maine is “vacating warrants for unpaid fines, restitution, court-appointed counsel fees, failure to appear for unpaid fine hearings, and other failure to appear warrants”; Brooklyn, New York, has also declared “no warrants or civil judgments will be issued for unpaid court debt” for 60 to 90 days; Kentucky is also “prohibiting the arrest or detention of any person served with a warrant for nonpayment of court costs, fees, or fines, or with a warrant for a failure to appear on a violation”; Nebraska is doing similarly.

• Reading, Pennsylvania, in an attempt to cease creating new debt slaves to the city, has done a lot to make things easier, including ending late penalties, extending deadlines for challenging citations; ending new parking tickets entirely (including at meters) and no more booting cars for now.

The Marshall Project reports some of the not-so-good news for those burdened with petty fines: Cops in Tulsa, Oklahoma, for example, are continuing “to arrest people for failing to pay court debts—even ones more than a decade old.”

Courts and governments have a strong incentive to show no mercy to poor Americans trapped in their fines and fees machinery, since, as The Marshall Project notes, “Two main sources of revenue—sales taxes from now-shuttered restaurants and bars, and traffic tickets from now-empty highways—have cratered. This comes at a time when officials are straining to pay for, among other things, desperately needed medical equipment and unemployment benefits for record numbers of laid-off workers.” Some are thus in the COVID-19 age adding new reasons to fine citizens, including “for violating orders to stay at home and wearmasks.“

Such fines are enough to crush many poor Americans even in better times, but localities almost always think they need their payoff. More than $50 billion in such fines are due in America for either actual crimes or merely for related late fees. court costs, and interest.

One looming problem is a lot of those prophylactic measures have short time limits, and the likelihood that most Americans who owe fines for petty crimes will be in a better position to pay them in 60 to 90 days seems very small. The courts will soon either need to rethink their policies or see lots of new fines, warrants, and court cases, in a time when fines will be harder than ever to pay and shoving more citizens in jails and prisons is particularly cruel.

from Latest – Reason.com https://ift.tt/2VC04sB

via IFTTT