3/23/1870: Justice Joseph Bradley takes oath.

from Latest – Reason.com https://ift.tt/3rcEFUJ

via IFTTT

another site

3/23/1870: Justice Joseph Bradley takes oath.

from Latest – Reason.com https://ift.tt/3rcEFUJ

via IFTTT

Yield Curve Control: Another Recipe For Stagnation

Central banks do not manage risk, they disguise it. You know you live in a bubble when a small bounce in sovereign bond yields generates an immediate panic reaction from central banks trying to prevent those yields from rising further. It is particularly more evident when the alleged soar in yields comes after years of artificially depressing them with negative rates and asset purchases.

It is scary to read that the European Central Bank will implement more asset purchases to control a small love in yields that still left sovereign issuers bonds with negative nominal and real interest rates. It is even scarier to see that market participants hail the decision of disguising risk with even more liquidity. No one seemed to complain about the fact that sovereign issuers with alarming solvency problems were issuing bonds with negative yields. No one seemed to be concerned about the fact that the European Central Bank bought more than 100% of net issuances from Eurozone states. What shows what a bubble we live in is that market participants find logical to see a central bank taking aggressive action to prevent bond yields from rising… to 0.3% in Spain or 0.6% in Italy.

This is the evidence of a massive bubble.

If the European Central Bank was not there to repurchase all Eurozone sovereign issuances, what yield would investors demand for Spain, Italy or Portugal? Three, four, five times the current level on the 10-year? Probably. That is why developed central banks are trapped in their own policy. They cannot hint at normalizing even when the economy is recovering strongly, and inflation is rising.

Market participants may be happy thinking these actions will drive equities and risky assets higher, but they also make economic cycles weaker, shorter, and more abrupt.

Central banks have exhausted tools like repurchasing bonds and cutting rates, the diminishing returns are evident. Now they look to Japan, of all places, to look at yield-curve-control policies.

Many articles hail the Bank Of Japan’s curve control strategy as a big success. It has managed to keep bond yields inside a narrow range around 0%, since it adopted its yield curve control (YCC) policy in 2016.

However, all this has done is disguise risk and lead the economy to massively indebted stagnation.

Why? The central bank applies constant changes in its purchases of sovereign bonds with different maturities to prevent the yield curve from steepening and bond yields from rising above a certain level, which could cause an economic crisis as risk-off takes over.

There is a deeply flawed view of markets in this theory. YCC does not reduce the risk of a crisis, simply disguises it by manipulating the price of sovereign bonds, the alleged lowest risk asset. As such, market participants always take significantly more risk than what they want or should, because the price of risk and the shape of the curve is artificially managed by the central bank.

The idea behind YCC is that savers will stop purchasing or selling sovereign bonds when they perceive that the economic cycle is changing, and that investors’ funds will be directed to finance the productive economy and put to work to invest in industry and provide credit to households. However, that does not happen. Market participants know that the shape of the yield curve is manipulated, and that risk is hidden, so most of the funds go to liquid, short-term assets and to refinance zombie firms that are already in high debt. Overcapacity is perpetuated, risky asset inflation soars, those that are already indebted are refinanced eternally and low interest rates push high liquidity to the least productive parts of the economy. It is no coincidence that the number of zombie firms has soared in the period when YCC was implemented. It is even less of a coincidence that unproductive debt has ballooned.

Allowing rates to adjust to reality through free float would be more effective to transfer liquidity to the productive segments of the economy and strengthen the recovery. It would also reduce the incentive to overspend from governments. Central banks say they do not cut rates but just follow market demands. If that is the case, let them float freely. But they will not.

YCC will likely be openly implemented by the ECB and the Federal Reserve, but it is in place de-facto already. It will not solve anything. Just make bubbles larger and the economy weaker. Just like in Japan, it will not prevent a crisis nor make the economy better prepared to face it, it will not lead to stronger economic recoveries either. The only thing that YCC does is to perpetuate bloated government spending and zombify the economy at the expense of real wages and the productive sectors. Once YCC fails, like all other financial repression tools, central banks and governments will say that it did not work because they did not do enough. It is never enough when they use other people’s money.

Tyler Durden

Tue, 03/23/2021 – 06:30

via ZeroHedge News https://ift.tt/3r8P6IZ Tyler Durden

In January 2018, a powerhouse trio of megacorporations—Amazon, Berkshire Hathaway, and JPMorgan Chase—announced a new health care venture. It didn’t have a name or a CEO or a specific product, but it did have a mission: to fix America’s health-care mess and, in particular, to bring down costs, especially for companies and employees facing ever-rising medical bills.

“The initial focus of the new company will be on technology solutions that will provide U.S. employees and their families with simplified, high-quality and transparent healthcare at a reasonable cost,” the companies said in a joint press release, promising that the venture would be backed with extraordinary resources and “free from profit-making incentives and constraints.” The cost of providing health care represented “a hungry tapeworm on the American economy,” said Berkshire Hathaway CEO and famed investor Warren Buffett. The company’s goal was to put that tapeworm on a diet.

The first steps were to give it a name, Haven, and a CEO, the well-known Harvard health policy and management professor Atul Gawande. Nearly a decade earlier, Gawande had penned an influential article for The New Yorker on “The Cost Conundrum.”

While researching that article, Gawande traveled to McAllen, Texas, a small city near the southern border that was one of the country’s most expensive health care markets on a per-capita basis. In McAllen, he noted, Medicare spent more than twice the national average on enrollees: almost $15,000 per person, a substantial increase from the early 1990s, when the city’s per-capita Medicare spending ran close to the national average. Why, he wondered, was McAllen now spending so much more?

The main reason for the cost inflation, Gawande decided, was a surfeit of unnecessary procedures: tests, scans, surgeries, and appointments that served no medical purpose and sometimes were actively harmful. Residents of McAllen were getting more care. But that didn’t make it better care.

From there, Gawande drew a theory of health policy reform: America needed to expand coverage, which was distributed unequally, and it could do so by reducing spending on unnecessary services. The country could have it both ways: more coverage and less spending—and perhaps even better care in the process.

When it passed a year after Gawande’s article, the Patient Protection and Affordable Care Act, widely known as Obamacare, was based at least partly on this theory. The law expanded coverage through Medicaid and subsidies for heavily regulated private insurance. A goal was “bending the cost curve down.”

By one measure, Obamacare slowed the growth of national health care spending from 5.6 percent a year between 2003 and 2010 to 4.4 percent a year between 2010 and 2018. But adjusted for general price inflation, the growth rate is essentially unchanged. And overall health spending increased from $2.6 trillion in 2010 to $3.6 trillion in 2018, representing an increased share of the country’s gross domestic product. Buffett’s hungry tapeworm had kept on eating.

Which brings us back to Haven. In May 2020, Gawande, who reportedly had served as more of an intellectual leader than a hands-on manager, left the company, citing a desire to focus more on policy and advocacy—not an auspicious sign for a company that set out to serve as a model for health care delivery. And despite the extraordinary resources at its disposal, the company’s actual work had been modest: a handful of pilot programs, according to The Wall Street Journal, including one that offered JPMorgan employees in two states a menu of health care services at a flat rate.

Despite its access to brainpower and financial backing, it had turned out to be harder than expected to disrupt the health care market. Haven would not get to try much longer. In January, the company announced that it would shut down entirely. The original dream—”simplified, high-quality and transparent healthcare at a reasonable cost”—had proven too vast and too difficult for even the most powerful players.

Haven’s failure is a genuine disappointment. Like Obamacare—which has sputtered along, frustrating the public with continued high costs and regulatory inflexibility—it serves as a lesson in the arduousness of ambitious health care reform. Regulatory and practical pressures, combined with the resources, innovative thinking, and ground-level administrative competence that are necessary, make major improvements very difficult to achieve. It might be possible to starve the tapeworm. But so far, no one has figured out how.

from Latest – Reason.com https://ift.tt/3ccWZJ9

via IFTTT

In January 2018, a powerhouse trio of megacorporations—Amazon, Berkshire Hathaway, and JPMorgan Chase—announced a new health care venture. It didn’t have a name or a CEO or a specific product, but it did have a mission: to fix America’s health-care mess and, in particular, to bring down costs, especially for companies and employees facing ever-rising medical bills.

“The initial focus of the new company will be on technology solutions that will provide U.S. employees and their families with simplified, high-quality and transparent healthcare at a reasonable cost,” the companies said in a joint press release, promising that the venture would be backed with extraordinary resources and “free from profit-making incentives and constraints.” The cost of providing health care represented “a hungry tapeworm on the American economy,” said Berkshire Hathaway CEO and famed investor Warren Buffett. The company’s goal was to put that tapeworm on a diet.

The first steps were to give it a name, Haven, and a CEO, the well-known Harvard health policy and management professor Atul Gawande. Nearly a decade earlier, Gawande had penned an influential article for The New Yorker on “The Cost Conundrum.”

While researching that article, Gawande traveled to McAllen, Texas, a small city near the southern border that was one of the country’s most expensive health care markets on a per-capita basis. In McAllen, he noted, Medicare spent more than twice the national average on enrollees: almost $15,000 per person, a substantial increase from the early 1990s, when the city’s per-capita Medicare spending ran close to the national average. Why, he wondered, was McAllen now spending so much more?

The main reason for the cost inflation, Gawande decided, was a surfeit of unnecessary procedures: tests, scans, surgeries, and appointments that served no medical purpose and sometimes were actively harmful. Residents of McAllen were getting more care. But that didn’t make it better care.

From there, Gawande drew a theory of health policy reform: America needed to expand coverage, which was distributed unequally, and it could do so by reducing spending on unnecessary services. The country could have it both ways: more coverage and less spending—and perhaps even better care in the process.

When it passed a year after Gawande’s article, the Patient Protection and Affordable Care Act, widely known as Obamacare, was based at least partly on this theory. The law expanded coverage through Medicaid and subsidies for heavily regulated private insurance. A goal was “bending the cost curve down.”

By one measure, Obamacare slowed the growth of national health care spending from 5.6 percent a year between 2003 and 2010 to 4.4 percent a year between 2010 and 2018. But adjusted for general price inflation, the growth rate is essentially unchanged. And overall health spending increased from $2.6 trillion in 2010 to $3.6 trillion in 2018, representing an increased share of the country’s gross domestic product. Buffett’s hungry tapeworm had kept on eating.

Which brings us back to Haven. In May 2020, Gawande, who reportedly had served as more of an intellectual leader than a hands-on manager, left the company, citing a desire to focus more on policy and advocacy—not an auspicious sign for a company that set out to serve as a model for health care delivery. And despite the extraordinary resources at its disposal, the company’s actual work had been modest: a handful of pilot programs, according to The Wall Street Journal, including one that offered JPMorgan employees in two states a menu of health care services at a flat rate.

Despite its access to brainpower and financial backing, it had turned out to be harder than expected to disrupt the health care market. Haven would not get to try much longer. In January, the company announced that it would shut down entirely. The original dream—”simplified, high-quality and transparent healthcare at a reasonable cost”—had proven too vast and too difficult for even the most powerful players.

Haven’s failure is a genuine disappointment. Like Obamacare—which has sputtered along, frustrating the public with continued high costs and regulatory inflexibility—it serves as a lesson in the arduousness of ambitious health care reform. Regulatory and practical pressures, combined with the resources, innovative thinking, and ground-level administrative competence that are necessary, make major improvements very difficult to achieve. It might be possible to starve the tapeworm. But so far, no one has figured out how.

from Latest – Reason.com https://ift.tt/3ccWZJ9

via IFTTT

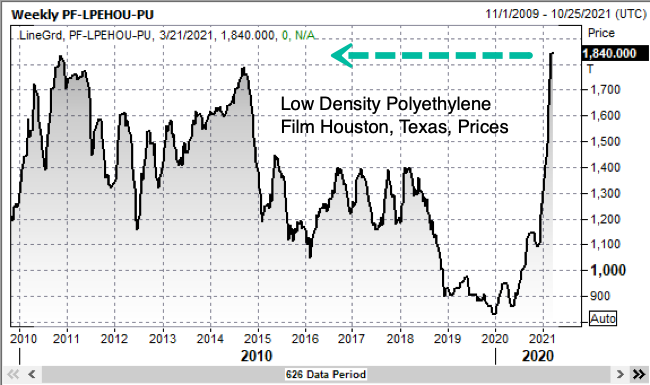

“Going To Get Ugly” – Global Plastic Shortage Triggered By Texas Deep Freeze

The cold snap that shut down oil fields and refineries across Texas last month has severely impacted several petrochemical plants caused a global shortage of plastics, according to WSJ. Plastics produced on the Gulf Coast are essential for carmaking, medical devices, homebuilding, and consumables.

Prices for polyethylene, polypropylene, and other plastics used to make automobiles, computers, and pipes have reached their highest prices in years due to the shortages produced by the shuttering of petrochemical plants across Texas and other Gulf Coast states due to cold weather in February.

On top of a shortage of almost everything and soaring prices, as we explained days ago, wide-scale supply chain pains are expected throughout 2021.

WSJ reports Honda Motor Co. will halt some of its U.S. and Canadian automobile factories this week due to supply chain issues from the winter storm last month.

Toyota Motor Corp. expects the shortage of petrochemicals to hurt production at its car plants. Paint maker PPG Industries Inc. said a number of its suppliers had been affected by the plastic shortage. Storage and shelving retailer, Container Store Group Inc., warned that the plastic shortage could impact profit margins.

John Schiegg, vice president of supply-chain services for David Weekley Homes, a Houston-based homebuilder, said a shortage of everything from siding to adhesives to insulation is quickly materializing – this could easily delay homebuilding projects, or in the meantime, result in higher costs.

It’s not just plastic in short supply; shortages have also been reported in lumber, steel, and semiconductors.

Several PVC piping manufacturers told Schiegg that they couldn’t fulfill his order because of the supply chain disruptions due to the crippling of petrochemical plants.

“We had no idea how much came from the Gulf Coast area,” Schiegg said. “I tell people it’s going to get ugly. There’s going to be a big fight for materials.”

It’s not just home building that’s being affected by the shortage. Hospitals are experiencing a lack of plastic medical equipment.

Kim Anders, a supply-chain executive at the hospital buying group Premier Inc., said the virus pandemic had caused a significant increase in demand for the use of needles but, at the moment, medical and disposable sharps containers (made out of plastic) are hard to obtain.

Prices for low-density polyethylene film in Houston, Texas, have nearly doubled since the beginning of the pandemic, reaching a decade high this month. LDPE plastic film is used for dry cleaner bags, bread bags, paper towel overwrap, and shipping sacks.

Prices for linear low-density polyethylene in Houston, Texas, have reached highs not seen since 2015. LLDPE is used for plastic wrap, stretch wrap, pouches, toys, covers, lids, pipes, buckets, containers, cables, geomembranes, and flexible tubing.

While the plastic shortage has sent specific plastic prices to decade highs, demand appears to be an overwhelming supply at the moment. Even before last month’s deep freeze, the Gulf Coast’s chemical industry was hurting from a super active hurricane season. On top of this all, the Federal Reserve is setting off a historical experiment to run the economy extremely hot via low rates and massive fiscal stimulus.

“We could also see upward pressure on prices if spending rebounds quickly as the economy continues to reopen, particularly if supply bottlenecks limit how quickly production can respond in the near-term,” Fed Chairman Jerome Powell said last week. “However, these one-time increases in prices are likely to have only transient effects on inflation.”

Supply bottlenecks of plastics, lumber, steel, chips are already dragging on specific industrial production. We’re only finding out how vulnerable global supply chains are, and the other is how crucial plastic is to the economy.

Respondents to the most recent mfg ISM revealed just how bad supply chain disruptions truly is:

Goldman Sachs told clients last week that supply chain woes might not be resolved until 2022.

Tyler Durden

Tue, 03/23/2021 – 05:45

via ZeroHedge News https://ift.tt/3lFvefg Tyler Durden

Climate Change Won’t Be Stopped By 593 Pages Of Green Tape

Submitted by Huw van Steenis,

Financing an innovative low-carbon economy is one of the defining challenges of our age, as Bill Gates argues in his new book. Energy transition will require $3.5 trillion annually — for decades. As we emerge from the pandemic, defining what counts as a green investment around the world will take on even greater significance. It’s crucial to ensuring we really do create a better future from this crisis and avoid falling into the greenwashing trap.

In the race to net zero, the European Union should have a head start in setting those standards given many years of investor interest. Its new rules requiring asset managers to disclose the environmental, social and corporate governance features of their funds started to take effect this month. But the bloc still hasn’t agreed on the list of categories and definitions of what’s green and what’s not – known as the green taxonomy – that’s supposed to underpin the effort, and to become a global standard.

Brussels has gotten bogged down in the details and a noble, but self-defeating desire to create an exhaustive, one-size-fits all solution. Debate over what should qualify as green, especially around gas, has become a political hot potato. Investors and companies are beginning to fret about how they will put into action technical guidance that runs to 593 pages so far.

The green tape, if you will, puts the bloc at risk of being overtaken by a freshly emboldened U.S. And like with its botched vaccination campaign, the EU risks being upstaged by the U.K., which has moved ahead in mandating new climate reporting by companies based on existing guidelines.

A universal classification system feels intuitively appealing, but it’s extremely challenging to assess the sustainability of every economic activity and then apply the results consistently everywhere. There are good arguments for why a single green taxonomy is a bad idea, as Ben Caldecott, director of the Oxford Sustainable Finance Programme, argues. Even ratings agencies that score sustainability agree with each other only 60% of the time — compared to over 90% for credit ratings, according to an MIT Sloan School of Management study.

The EU’s taxonomy in particular poses several challenges.

First, it’s too binary in supporting only what is the purest shade of green. Take green bonds, an increasingly important way to fund energy-efficient real estate at attractive rates. They’ve flourished under private-sector standards set by the International Capital Market Association and Climate Bond Initiative. These use the top 15% of housing stock in each country as a proxy and look to tighten it over time. By contrast, the EU proposals would only permit the 1% of properties to have an “A” energy rating certificate — against the advice of the Commission’s own expert group.

As a result, almost all European green bonds would fail to make the cut, potentially closing the market at a stroke. Without major changes to the standards, even the EU’s pandemic recovery fund probably wouldn’t be able to issue the 250 billion euros ($300 million) of green bonds it has earmarked.

Second, the methodology is, by turns, too strict and too broad. A fifth of the revenues generated by companies in the Euro Stoxx 50 index are broadly aligned to the EU taxonomy’s principles, but only 2% could be considered as strictly aligned, a study by ISS ESG found. Not even all forms of renewable energy are considered green enough: Wind is in, but hydropower is not, to the frustration of the Danes and Swedes. Elsewhere, the responsibility to “Do no significant harm” raises legal issues around the due diligence to vet such a sweeping commitment.

Third, there’s no category for firms in transition. Yet it’s incredibly important to understand how firms are adapting and to incentivize them to move in the right direction. To achieve that, many green ratings advisers use a more nuanced color-coding system. Static binary standards will not serve the economy or investors well.

As a result, the EU green taxonomy is not going global in the way Brussels had hoped. As countries race to establish green investing frameworks, most acknowledge the EU principles, but then shape their own far simpler ones drawing on established building blocks. Most recently, Singapore proposed a systemto encourage transition with a ratings spectrum across red, amber and green.

When Securities and Exchange Commission Acting Chair Allison Herren Lee created a climate and ESG finance task force to prosecute misconduct and embraced a new sustainable standards initiative from the International Organization of Securities Commissions, she emphasized the need for creating a regime that’s flexible enough to keep up with the science and the markets.

The EU’s failure to agree on the taxonomy provides an opportunity for re-assessment. To keep ahead globally, it should prioritize improving company climate-related disclosures by building on existing frameworks. High quality, comparable data that allows investors, consumers, pressure groups and regulators to assess risks and hold companies to account is a powerful tool. The Financial Stability Board’s Task Force on Climate-Related Financial Disclosures has become the gold standard for reporting, and the bloc should follow the U.K.’s lead in mandating them for corporates and funds.

The bloc should use its head start to fashion workable standards and building blocks that can work across all jurisdictions. Some 18 central banks, following the Bank of England’s lead, have created exploratory stress tests for climate change of financial institutions. They will need robust data to do this. This is equally important for mainstreaming the inclusion of climate risks in credit ratings.

Finally, the bloc must develop a richer framework: “50 shades of green,” as former BOE governor Mark Carney, who’s working on climate finance reform for the United Nations, puts it. For instance, there’s interest in shaping portfolios along the UN’s broader Sustainable Development Goals. Care must be taken to avoid a regime that could disincentivize the development of a range of funds that cater to a wide spectrum of investor preferences.

For Europe’s Green Deal to succeed, it will need to channel the “bold, persistent experimentation” of Franklin Roosevelt’s New Deal. To keep the ambition intact and be a global role model, the EU must move away from a one-size-fits-all approach and shape disclosure standards to give a shot in the arm to sustainable innovation, finance and transition.

* * *

Huw van Steenis is the chair of the sustainable finance committee at UBS. He formerly served as senior adviser to Mark Carney at the Bank of England.

Tyler Durden

Tue, 03/23/2021 – 05:00

via ZeroHedge News https://ift.tt/3d02Mkd Tyler Durden

In Australia, Judge Salvatore Vasta jailed a man for 12 months during a routine property dispute between the man and his ex-wife. Vasta repeatedly accused the man of not divulging all of his financial information. The man kept insisting he had. Finally, Vasta jailed the man, who claims he contemplated suicide while locked up. The man is now suing Vasta, claiming the judge had no right to jail him without first finding he had violated a court order. Vasta admits he jailed the man “by error,” believing another judge had previously found him guilty of violating a court order. But Vasta says he is protected from being sued by judicial immunity.

from Latest – Reason.com https://ift.tt/3lSAUCZ

via IFTTT

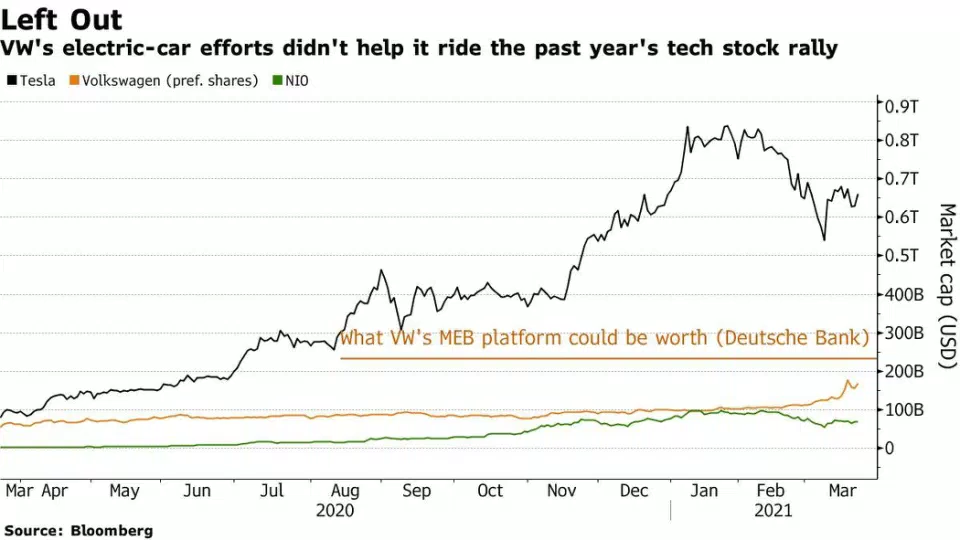

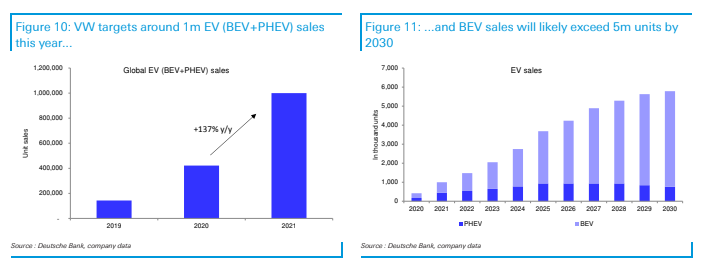

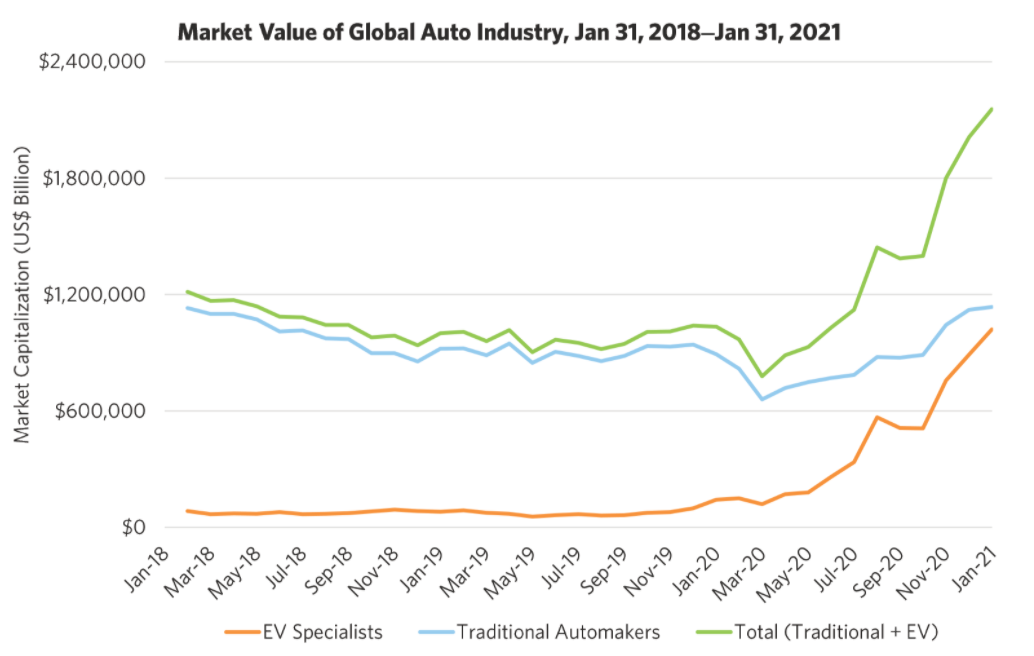

Volkswagen’s EV Business Could Be Worth $230 Billion Alone, Deutsche Bank Says

Certainly one of the more exciting stories in the world of EV investing over the past several weeks has been Volkswagen. We have documented the legacy automaker’s stock during a rapid ascent over the last few trading sessions, on the heels of the company positioning itself as a direct competitor to Tesla.

The move has been part of a broader reversion to the mean in EV valuation that we think is likely to continue.

Of course, the lingering question remains: what is VW’s business actually worth, given the new pivot to EVs? Deutsche Bank weighed in early this week stating that the company’s EV business along could be worth $230 billion.

Analysts led by Tim Rokossa lifted their price target for VW shares by 46% to 270 euros, according to Yahoo Finance. The company’s stock was up as much as 14% to start the week on the news. Last week, VW surpassed SAP as the largest member of the DAX.

Rokossa said there is a “good chance VW’s EV deliveries surpass Tesla’s in short order as its ID.4 compact SUV is rolled out globally”. Meanwhile, VW has said that it plans on turning its factory outside Barcelona into an EV hub with goals of making more than 500,000 vehicles per year.

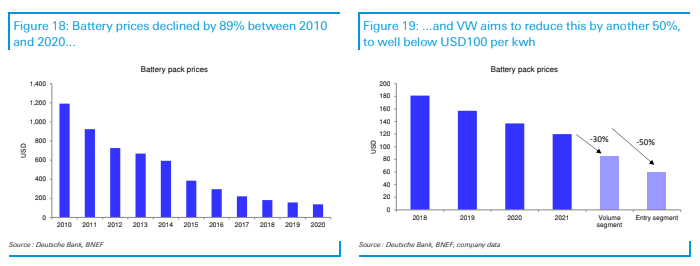

He also pointed to reduction of cost in items like batteries as key drivers of the financial bull case for VW:

VW’s truck unit, Traton SE, also said it was boosting investments into electric technology from 1 billion euros to 1.6 billion euros in 2025. Traton Chief Executive Officer Matthias Gruendler commented: “The future of commercial vehicles won’t be shaped by diesel anymore but by electric trucks.”

The note concludes:

“While we keep our existing valuation model, we increase the applied multiple that we think the market will deem fair and introduce a blue-sky valuation of the BEV business separately with this note. Applying the multiples of EV pure plays such as Tesla or NIO on sales generated by the MEB platform would yield a value of almost EUR400 per share (DBe) and we even ignore the premium PPE and luxury J1 platform in that calculation. We also ignore the potential value creation from a Porsche IPO (DBe: worth >EUR60bn). Overall, given the earnings momentum and the greater credibility of its EV story, we remain on Buy and increase our TP to EUR270.”

Recall, last week VW upgraded its profit guidance laid out plans for expanding the company’s EV offering out through 2030 which also includes dethroning Tesla as the reigning EV world champ. VW hosted its “Power Day” yesterday and revealed plans to build six “gigafactories” with a total capacity of 240 gigawatt hours per year.

“The company is aiming to achieve an operating margin between 7% and 8% after 2021. VOW also confirmed it is looking to finish the year at the upper and of a 5% – 6.5% range in 2021. Higher profitability will be achieved through lower costs with as much as 2 billion euros savings identified for 2023 compared to 2020,” the company said yesterday, according to StreetInsider.

Chief Executive Herbert Diess said on CNBC: “This period is probably the most crucial for the whole industry. Within the next 15 years we will see a total turnover of the industry. Electric cars are taking the lead and then software really becomes the core driver of the industry.”

“Electric cars already today are very, very competitive and they’re becoming more competitive over time. that gives us the certainty that this is the right way going forward. Electric cars actually will bring down the cost of individual mobility further,” he continued.

VW also disclosed yesterday that it was working on a “new unified battery cell” to be launched in 2023. Diess said: “The one size fits almost all cell design will radically reduce battery costs … by up to 50% compared to today. Lower prices for batteries means more affordable cars, which makes electric vehicles more attractive for customers.”

Also probably contributing to its ascent is the fact that VW is a “less liquid” share listing, as Bloomberg notes that it is “owned by major shareholders Porsche SE, the German state of Lower Saxony and Qatar”.

The move is also part of a general hysteria surrounding EV stocks. Recall, we wrote days ago that Rob Arnott of Research Affiliates referred to it as a “big delusion”. Arnott’s predictions could eventually rope in valuations across the board in EVs, not just for any one player.

Current valuations in EVs are due to “pricing delusion”, Arnott said in a new paper calling EVs the “Big Market Delusion” last week. “The electric vehicle industry, with its astronomical growth in market-cap over the 12 months ending January 31, 2021, is a prime example of a big market delusion,” he wrote.

In his paper, he defines a big market delusion as “when all the firms in an evolving industry rise together, despite that fact that they are competing against each other.” He used airlines as an example of the BMD in the past. Technology “does not translate into great fortunes for investors unless it is associated with barriers to entry that allow a company to earn returns significantly in excess of the cost of capital for an extended period,” he argued.

Tyler Durden

Tue, 03/23/2021 – 04:15

via ZeroHedge News https://ift.tt/2NMIwKy Tyler Durden

In Australia, Judge Salvatore Vasta jailed a man for 12 months during a routine property dispute between the man and his ex-wife. Vasta repeatedly accused the man of not divulging all of his financial information. The man kept insisting he had. Finally, Vasta jailed the man, who claims he contemplated suicide while locked up. The man is now suing Vasta, claiming the judge had no right to jail him without first finding he had violated a court order. Vasta admits he jailed the man “by error,” believing another judge had previously found him guilty of violating a court order. But Vasta says he is protected from being sued by judicial immunity.

from Latest – Reason.com https://ift.tt/3lSAUCZ

via IFTTT

Five Ways In Which The EU Mismanaged Vaccine Policy

Submitted by Peter Cleppe, editor-in-chief of Brussels Report

Whatever the reason, not as many Covid vaccines were delivered to the EU in the last few months as compared to the deliveries to Israel, the United States and the United Kingdom. Even proponents of greater EU centralization, like Renew MEP Guy Verhofstadt, have criticized the EU for this, saying that the reason for the EU’s lackluster performance is because of “the contracts Europe negotiated with the pharmaceutical companies”, which he thinks are “extremely unbalanced. They are precise on pricing and liabilities but weak and vague on supply and on timing, and offer escape routes to the contractual obligations of the pharmaceutical companies involved.”

The EU Commission has come up with all kinds of excuses for this, even accusing one of the vaccine producers, AstraZeneca, of having violated its contractual obligations with the EU, but when the contracts were made public, it was not clear at all that this was the case. What we know, is that the EU closed the deal with AstraZeneca three months later than the U.K. and that it was four months slower than the U.K. and the U.S. in signing the contract with Pfizer. Also, there would be provisions in the U.S. contract with J&J that the U.S. would enjoy priority for its J&J vaccine. Furthermore, Israel would have paid 2.3 times the EU’s price, thereby obtaining 40 percent more vaccine doses than Germany, even if the country’s population size is 12 percent of Germany’s.

In a nutshell: after Angela Merkel forced her Minister of Health to hand the initiative to negotiate contracts for vaccine procurement to the European Commission in June 2020, the Commission failed to do the job well. This doesn’t stop the supranational bureaucracy from calling for even more powers over health policy. One lesson that can already be drawn, is that this is not a good idea.

Some EU countries have already broken ranks with the EU. Austria and Denmark closed a deal with Israel on vaccine production, to “no longer be dependent only on the EU”, while also Poland, Hungary, Slovakia, and the Czech Republic have opted to go alone in various ways, exploring deals with Russia and China.

Perhaps EU governments jointly negotiating with big pharma made sense, but then some kind of technical team directly steered by 27 national governments, rather than a politicized supranational bureaucracy should have been made responsible.

For those in doubt that the EU Commission is a deeply politicized institution, it suffices to take a look at how the Commission reacted when the poor results of its actions become apparent. It’s one thing to make a mistake. It’s yet another not to admit it.

In between accusing one of the vaccine producers that had just managed to come up with an incredibly successful vaccine at record speed of “breach of contract”, EU Commission President Ursula von der Leyen attempted to blame her Trade Commissioner, Valdis Dombrovskis. After dragging her feet, in the end she did issue a half-hearted admission that “mistakes were made” but that “in the end, we got it right.” Also her deputy, EU Commission vice-President Frans Timmermans, has now admitted “errors”, however without much explanation how and not without a sneer towards member states.

In a weird turn of events, EU leaders – or at least some of them – appeared to start badmouthing the vaccine they first were clamoring for. Again EU Commission chief von der Leyen suggested that the U.K. had compromised vaccination “safety and efficacy”, unlike of course the EU. A similar tactic had been used by Belgian Prime Minister Alexander De Croo, when he stated in December that the UK was merely faster in approving the Pfizer vaccine because “they have used their population as [guinea pigs] over there.” Perhaps French President Macron went the farthest of them all, when he stated that the AstraZeneca vaccine was “‘quasi-ineffective” for older people. This flatly contradicted the science, according to which there simply wasn’t sufficient data to conclude it would also protect the elderly. It also contradicted the advice of the European Medicines Agency (EMA), which claimed that despite the lack of data, “protection is expected” also for those over 55 years old – something that has been confirmed by now.

A child could predict such statements by the EU Commission President and EU leaders, clearly made in a bid to divert attention from the EU’s own failures, wouldn’t exactly strengthen support for vaccines among the many “vaccine skeptics” in the EU. In practice, these look to have played a role in the low take-up of the vaccine, even if this would also be due to logistical failures of national governments. It also complicates the work to convince people vaccines are safe when actual legitimate worries arise, for example in recent days, when a number of EU member states suspended use of the AstraZeneca vaccine, despite reassurances by the European Medicines Agency (EMA).

Another questionable response was to set up a so-called “export certification” mechanism, which allows curbs on exports of vaccines if drug makers fail to meet delivery targets. This was used for the first time by the government of new Italian PM Mario Draghi, when a batch of 250.000 AstraZeneca vaccines destined for Australia were denied an export permit from Italy.

The move was cleared by the European Commission, but may end up hurting the EU. Non-EU countries may retaliate, with or within the context of the WTO. This is also a headache for the EU vaccine industry, which is strongly reliant on imports from North America. Most companies at the forefront of vaccine effort have production capacity in EU to serve the world. Vaccine producers have testified their production capacity was already being slowed down due to these new bureaucratic hurdles.

On the longer term, this kind of politically inspired populist protectionism may also make the EU a less attractive place for investment into this innovative industry for which EU member states are so renown. Long gone are the days – a mere few months ago – when Ursula von der Leyen was pontificating not to engage in costly “vaccine nationalism”. One estimate puts the cost of such “vaccine nationalism” at $9 trillion, because of hampered international cooperation and reduced trade.

The one thing that seems to have enabled countries to avoid economically devastating lockdowns were travel restrictions. Among Western nations, Finland and Norway, not Sweden, should really be the poster childs of the global “anti- lockdown” movements. They were both even more liberal than Sweden throughout 2020, and nevertheless managed to suppress the spread of Covid successfully, unlike Sweden. Their travel restrictions were key to help avoid the need for lockdowns after Spring, when everybody had been surprised by the virus. The travel checks they imposed weren’t all that burdensome and closely linked to virus infection risk data.

Perhaps it would be harder for countries in the middle of Europe to enforce such restrictions than for those in the periphery, but then well-traveled countries also have more scope to reduce infection risk by limiting non-essential travel. Belgium did so, in any case. Despite all the evidence that it works, in the middle of February, the EU Commission expressed concerns about such bans on non-essential travel. That’s not to say it shouldn’t be the job of the Commission to push for a relaxation when infection rates allow, and of course, it’s good to be mindful about such restrictions, but when the alternative is to inflict much more harm to the domestic economy, it’s obvious what the priority should be.

Tyler Durden

Tue, 03/23/2021 – 03:30

via ZeroHedge News https://ift.tt/3raCXD5 Tyler Durden