Threats, propaganda and the Orwellian dissolution of social trust cannot stop a withdrawal from the status quo.

Longtime readers know I’ve had an active interest in what differentiates empires/nations that survive crises and those that collapse. There is a lively academic literature on this topic, and it boils down to three general views:

1. Collapse is typically triggered by an external crisis that overwhelms the empire’s ability to handle it. Absent the external shock, the empire could have continued on for decades or even centuries.

2. Crises that could have been handled in the “Spring” of rapid expansion are fatal in “Winter” when the costs of maintaining complex systems exceeds the empire’s resources.

3. Civilization is cyclical and as population and consumption outstrip resources, the empire becomes increasingly vulnerable to external shocks.

External shocks include prolonged severe drought, pandemics and invasion. In many cases, the empire is beset by all three: some change in weather that reduces grain harvests, a pandemic introduced by trade or military adventure and/or invasion by forces from far-off lands with novel diseases and/or military technologies and tactics.

More controversial are claims that political structures become sclerotic and top-heavy after long periods of success, and these bloated, brittle hierarchies lose the flexibility and boldness needed to deal with multiple novel challenges hitting at the same time.

We lack internal-political records for most empires that have collapsed, but those records that have survived for the Western and Eastern Roman Empires suggest that eras of stability breed political sclerosis which manifests as a bloated, parasitic bureaucracy or as ruthless competition between elites that were once united in the expansive “Spring” phase.

By the “Winter” phase, the elite hierarchy is willing to sacrifice the unity needed to survive for its own short-term advantage.

All of this applies directly to China, which is experiencing not just a public health crisis (Covid-19 pandemic) but a host of overlapping crises triggered by the epidemic.

The external shock of the coronavirus has revealed the fragilities and weaknesses of China’s social, political and financial orders. These include:

1. Healthcare system crisis. The system is a patchwork that leaves non-government workers largely on their own. One doctor in Wuhan reported that a pregnant woman in his care died when the family ran out of cash for her care. (The central government announced it would cover all costs shortly after the patient died.)

The for-profit nature of much of the healthcare system is not widely understood outside China. If you want high-quality care without long waits, you must have cash.

Additionally many of the “doctors” are trained only in traditional Chinese medicine, so there is a shortage of trained personnel and facilities.

2. Food system crisis. It’s not just Swine Fever that’s straining the system; shortages are widespread and rising costs have been crimping working-class household budgets for the past few years.

3. Economic crisis: consumption and exports. As employers slash wages or close down, incomes fall and the trauma of the pandemic doesn’t engender a mindset of rampant consumption. The authorities are desperate to ramp up new car sales, for example, but everyone who can afford a car in China already has one. Demand was stagnant even before the virus.

As for the export economy: companies were already relocating abroad as a result of the trade war with the U.S. There is no reason for production that leaves to ever return to China, and there is no other source of employment and revenue to replace the export production that leaves.

On top of that structural erosion, China has adopted the just-in-time supply chain, and so it’s unprepared to deal with the chaos as the supply chain is disrupted four layers deep.

4. Financial / debt crisis: local government debt, shadow banking defaults. China fueled its expansion since 2016 with unprecedented amounts of debt and speculation. Any activity dependent on debt and speculation is exceedingly vulnerable to disruption, as debt payments that can’t be made trigger defaults which then collapse the pyramid of speculation built on the shaky foundation of debt.

This is especially problematic in China, where the shadow banking system of informal, non-institutional credit is so vast and pervasive. Private debts that default trigger defaults in the formal banking sector as counterparties fail to make good: if I fail to make my private-loan payment to you, you can’t make your bank loan payment.

China’s central bank can print money but it can’t force bankrupt companies to borrow more or bankrupt lenders to issue loans to unqualified borrowers. The entire pyramid of debt in China could collapse even as the government prints money with abandon.

5. Social contract crisis: loss of trust in authorities and institutions. That the central government/Communist Party failed the citizenry is obvious. The Party betrayed the people to protect its own image, destroying the citizens’ trust.

As I’ve noted before, betrayal has consequences. There is no quick or easy way to restore what has been lost in terms of trust and faith that the social contract between parasitic rulers and the ruled is worth restoring.

6. Housing bubble popping, threatening household wealth. Household wealth in China is concentrated in housing, and so the bursting of the housing bubble will have an extraordinarily adverse impact on household wealth and the “wealth effect” of people spending freely because they feel wealthier as their home rises in value.

The hope that the housing sector, already stagnating before the epidemic, will quickly roar back to life is completely unrealistic. Bubbles always burst, and this external shock has the potential to pop China’s vast housing bubble.

7. High expectations dashed; confidence in the future dented. I’ve often written about the extremely high expectations of the Chinese people, which have only increased after three decades of uninterrupted growth. Low expectations prepare people for disappointment and are thus reservoirs of resilience; high expectations set people up for shattering losses of faith in institutions and the future.

8. Loss of international reputation/stature. The perceptions of China as a rising superpower on the move have been dismantled and replaced by a perception of autocratic incompetence, massive centralized bureaucratic failure, an elite willing to sacrifice its citizenry and a government that cannot be trusted, a government that will lie and fabricate whatever statistics it deems most salutary for its image.

The Party’s transparent efforts to improve the optics with ham-handed propaganda only strengthens the world’s perception of incompetence and bumbling, untrustworthy elites.

In sum, the loss to China’s so-called “soft power” is consequential. Whatever doubts other nations held about China’s reliability and oppressive demands have now been confirmed.

Ironically, China’s leaders are loathe to “come clean” as that would entail a loss of face. But maintaining a desperately thin charade of bogus propaganda and fabricated statistics only serves to destroy the last shreds of domestic and international legitimacy.

China’s leadership has proven adept at handling one crisis at a time during China’s “Spring” and “Summer” growth phases, but that is no guarantee that the leadership has the wherewithal to manage multiple overlapping crises in “Winter.”

The Communist Party leadership centered around President Xi has constructed a technological wonder of Orwellian social control, but this may well prove to be the leadership’s Maginot Line, a vast defense against a previous era’s violent social disorder that is incapable of controlling the erosion of legitimacy and confidence.

This technological wonder of Orwellian social control is defenseless against a population that simply opts out of returning to work and borrowing immense sums to gamble on future “growth.” Stalinist dependence on fear to compel political obedience does not create legitimacy, trust or confidence.

Threats, propaganda and the Orwellian dissolution of social trust cannot stop a withdrawal from the status quo. If workers opt out of returning to work, and households opt out of borrowing more money, that will undermine the economy and thus the social order. There is no police force large enough to force everyone to return to work and no mechanism to force people to borrow money to gamble in speculative ventures. A quiet withdrawal is a social movement that cannot be suppressed with traditional force or dissipated with propaganda no one believes.

This applies not just to China but to every nation struggling with the pandemic, a roster that will soon include virtually every major nation on Earth.

Plaintiff’s essential allegation is that Google violated Plaintiff’s First Amendment rights by temporarily suspending its verified political advertising account for several hours shortly after a Democratic primary debate. Plaintiff’s claim, however, “runs headfirst into two insurmountable barriers—the First Amendment and Supreme Court precedent.” Prager Univ. v. Google LLC, No. 18- 15712, 2020 WL 913661, at *1 (9th Cir. Feb. 26, 2020).

The First Amendment provides: “Congress shall make no law … abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble ….” “The First Amendment, applied to states through the Fourteenth Amendment, prohibits laws abridging the freedom of speech.” In effect, “the First Amendment means that government has no power to restrict expression because of its message, its ideas, its subject matter, or its content.”

Google is not now, nor (to the Court’s knowledge) has it ever been, an arm of the United States government. “The text and original meaning of those Amendments, as well as this Court’s longstanding precedents, establish that the Free Speech Clause prohibits only governmental abridgment of speech. The Free Speech Clause does not prohibit private abridgment of speech.” Manhattan Cmty. Access Corp. v. Halleck, 139 S. Ct. 1921, 1926 (2019) (emphasis in original).

Plaintiff alleges Google has become a state actor by virtue of providing advertising services surrounding the 2020 presidential election.

“Under [the Supreme] Court’s cases, a private entity can qualify as a state actor in a few limited circumstances—including, for example, (i) when the private entity performs a traditional, exclusive public function; (ii) when the government compels the private entity to take a particular action; or (iii) when the government acts jointly with the private entity.” Plaintiff’s argument is that, by regulating political advertising on its own platform, Google exercised the traditional government function of regulating elections. “To draw the line between governmental and private, this Court applies what is known as the state-action doctrine. Under that doctrine, as relevant here, a private entity may be considered a state actor when it exercises a function ‘traditionally exclusively reserved to the State.'”

Traditional government functions are defined narrowly. “It is not enough that the federal, state, or local government exercised the function in the past, or still does. And it is not enough that the function serves the public good or the public interest in some way. Rather, to qualify as a traditional, exclusive public function within the meaning of our state-action precedents, the government must have traditionally and exclusively performed the function.” “Under the Court’s cases, those functions include, for example, running elections and operating a company town.” There is no argument that webservices or online political advertising are traditionally exclusive government functions. Plaintiff argues that, by providing some restriction on political advertising on its platform, Google is in effect regulating elections.

Disclosure: I have represented Google as a lawyer, including in writing a white paper arguing that the First Amendment protects search engine results, though that is a different question than the one I’m discussing here; I have not been asked to blog about this, and I am speaking entirely for myself here.

from Latest – Reason.com https://ift.tt/2TFH77n

via IFTTT

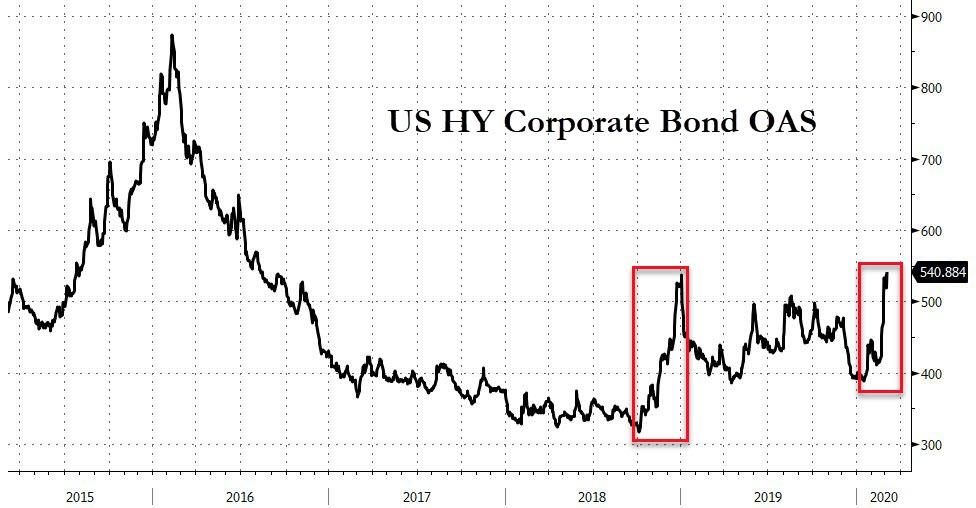

Fed Is Now Trapped: If Powell Fails To Taper “Not-QE”, He Will Admit It Was “QE 4” All Along

The unexpected scramble by dealers to obtain repo funding in recent days has taken the market, and especially STIR traders by surprise: after all, the primary catalyst behind the Fed’s decision to (emergency) cut by 50bps was to ease financial conditions. And yet the record oversubscribtion in both term and overnight repos in the past few days confirms that contrary to the Fed’s expectations, market liquidity has in fact deteriorated sharply.

And yet, as liquidity gets worse in response to the coronavirus market shock and, paradoxically, the Fed’s rate cut, the Fed faces a conundrum: will it continue tapering its repo operations and the permanent purchases of T-Bills, as it promised previously it would… or will the Fed capitulate and no only no longer taper, but in fact boost the availability of these products.

Herein lies the rub: if the Fed does in fact capitulate as most expect it to do, it will be effectively admitting that “Not QE” was in fact QE4 all the time, as this website and a handful of other Fed critics have claimed all along, and will make yet another mockery of all those finance hacks who, living in their mom’s basement, claimed that the Fed’s QE4 was not in fact QE4.

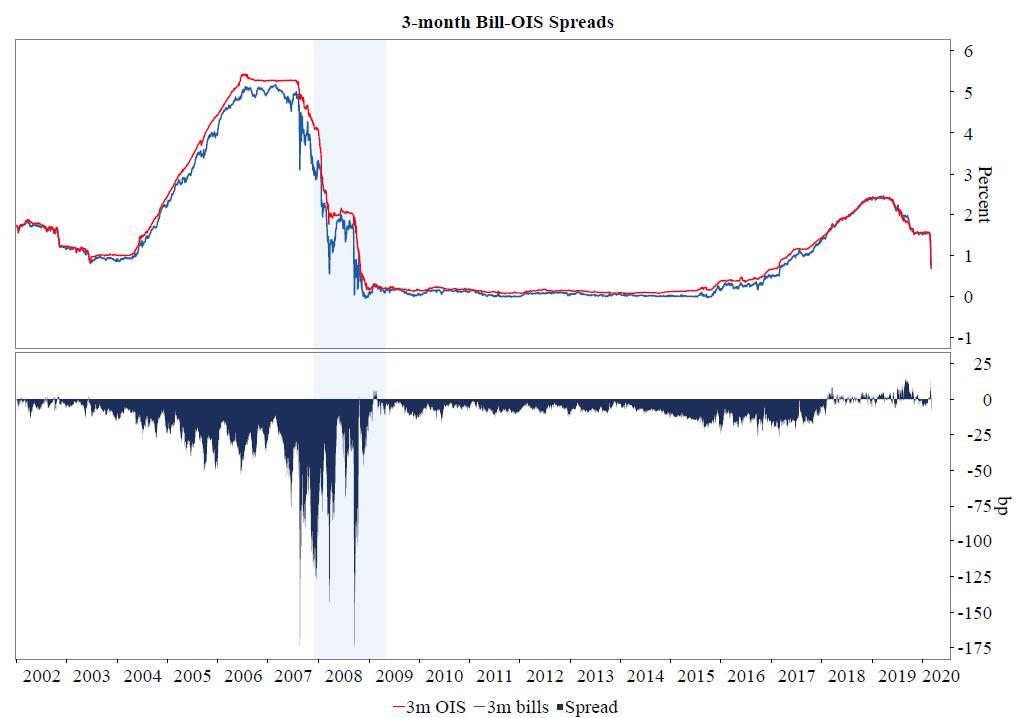

Addressing precisely this issue, on Thursday morning BMO’s rates strategist Jon Hill discusses the recent divergence in the 3M Bill-OIS spread…

… and touches on the various factors that he thinks would have an impact on a possible compression of the front-end Treasury/OIS spread, where he highlights “the possibility the Fed calls off tapering the bill purchase program”, although as noted above, he admits doing so would signal the Fed’s critics were right all along, and would be a prelude to the Fed losing even more credibility. To wit:

We still believe that the Fed will follow through on its forward guidance and taper its non-QE program. In their minds (and ours) this is not a facility designed to ease financial conditions, but rather one to address a reserve scarcity that emerged in September last year. To deviate from their tapering schedule would be to either tacitly acknowledge that it’s been shadow QE this whole time or further capitulate to some in the market’s interpretation of what the demand represents. That said, the probability that the tapering never occurs is clearly non-zero, if only because of the Committee’s extreme reticence to startle the market at this extremely precarious moment.

While in BMO’s mind, this facility may have been designed to address reserve scarcity, in “our mind” we have made it abundantly clear that the Fed’s non-QE POMO, i.e., T-Bill monetization, was meant to goose stocks all along, even if the Fed would never dare admit it. In other words, it was QE-4 all along. And we are certain that when the time comes in a few weeks, the Fed will prove us right by refusing to taper, as doing so would result in another market crash catalyst, an outcome the Fed is doing everything in its power to avoid.

“Project Kennedy” Escalates: JPMorgan Splits Trading, Sales Teams In Virus Response

As we detailed yesterday, America’s largest bank is going on lockdown…

And today has seen JPMorgan escalate their resiliency plan by sending some of its New York and London sales and trading staff to backup locations in response to the coronavirus.

“We are starting to shift people as a precautionary measure at this stage,” the bank said Thursday in a memo to staff.

“Dividing our workforce into different locations improves our ability to serve clients continuously while reducing the health risks associated with physical contact should a case arise.”

Reuters reports that Brian Marchiony, a bank spokesman, confirmed the plans and said they are “precautionary.”

And this comes after we noted yesterday that, according to Bloomberg, JPMorgan is asking thousands of US-based employees to work from home in test of “virus contingency plan” for closing domestic offices should the coronavirus spread. As part of the test, managers have requested that about 10% of staff across its consumer bank work remotely as part of the plan’s resiliency testing, which has been code-named “Project Kennedy” (it wasn’t clear why JPM picked that name for the project). And since JPMorgan’s consumer bank has 127,137 employees, the most of any of the firm’s divisions, that means that over 12,000 workers will be working from home for the foreseeable future.

As the coronavirus spreads, banks around the world have been scrambling ensure they can keep their businesses running and avoid a worst-case scenario by restricting travel, splitting up teams and traders amid different locations, and quarantining staff. As Bloomberg notes, some are also “dusting off regulatory plans for keeping “critical operations” open through a potential pandemic, some of which describe things like how far apart traders should sit from each other, or how many can work remotely.”

The key test for JPM’s will assess its telecommuting policy on a sampling of employees across businesses to ensure kinks are worked out before the plan needs to be rolled out more broadly in the event of a pandemic, one of the people said.

In other words, JPMorgan thinks it’s just a matter of time before it gets… worse.

It wasnt exactly clear how JPM’s client-facing bank tellers will do their job by teleconference. While technology has made it possible for more professionals to do their jobs remotely, working from home generally isn’t an option for branch workers like tellers and bankers who deal directly with customers. JPMorgan had 4,976 branches around the country as of the end of December that are filled with thousands of employees who have to show up to work for business to run.

JPMorgan’s leaders have been double-checking contingency plans to be sure the firm can continue to serve customers in the event of widespread disruptions. The moves are part of broader resiliency planning at the bank. The firm last week followed the lead of major US corporations in restrictring non-essential international travel for all employees and has been urging workers to test their remote-access capabilities. JPMorgan has also been testing systems at backup trading sites over the past few days in case workers need to be moved off of the main trading floors in New York and London.

There is a silver lining: with hand sanitizer sold out virtually everywhere, the bank is providing that precious commodity – extra hand sanitizer – to customer-facing branch workers and taking extra steps to sanitize offices, branches and equipment, including elevator call buttons and door handles, according to a memo from Co-President Gordon Smith to consumer bank staff on Friday.

And just to nip any potentially viral problems at the bud, JPMorgan has been encouraging consumers to access bank services and products through digital channels instead of walking into branches when they can.

“This can make their life easier all the time,” Smith wrote.

An Iranian military leader has suggested that the coronavirus is not a naturally occurring disease, and that it is a manmade bioweapon cultivated and released against China and Iran by a ‘hostile state’.

Brigadier General Gholam Reza Jalali, an Iranian officer in charge of the country’s Civil Defense Organization claimed Tuesday that:

“A study of the consequences of the virus in terms of tolls or the extent of the epidemic and the type of media propaganda over this issue that is aimed at increasing fear and panic among people strengthens the speculations that a biological attack has been launched against China and Iran with economic goals.”

Strongly hinting that the the virus is a bio-attack by the US, Jalali told Iranian Fars News Agency, state media, that he is seeking “laboratorial investigations and comparing the genome of the primary virus and the new genomes” to confirm his theory.

Iran has been accused of covering up the real extent of the outbreak within its borders. At time of writing it has officially recorded only 92 deaths from 2,922 cases, but those numbers are significantly lower than what independent reports and claims from dissident groups within the country suggest. The real number of deaths is thought to be in the high hundreds or thousands.

Videos uploaded to YouTube by the dissident groups purport to show people collapsing in the streets of Tehran from the effects of the virus, and are reminiscent of previous videos from China:

The BBC published footage that is said to be from Iran, showing hundreds of bodies in bags at a local morgue in Qom. Mideast-based correspondent Joyce Karam commented that “If these are confirmed to be from Corona as videos claim, death toll is higher than the government claims.”

Horrific thread of BBC obtained Videos from #Iran shows bagged bodies in Qom from moment of death till burial.

If these are confirmed to be from Corona as videos claim, death toll is higher than Gov. claims (77): pic.twitter.com/vxmTren3Lt

Other videos show preparations for mass graves, and health workers in full Hazmat gear burying victims:

قبرستان سرخحصار، شهر قدس، استان تهران؛ تدفین با تمهیدات بهداشتی ویژه ناظران، مقامات ایران را به پنهانکاری در مورد ابعاد شیوع ویروس کرونا متهم میکنند اما آیتالله خامنهای، رهبر ایران امروز گفت که اطلاعرسانی درباره ویروس کرونا در ایران شفاف و صادقانه است. pic.twitter.com/YzcGEBMo8u

گلزار شهدای مرودشت، فارس، ۱۱ اسفند ۹۸؛ تمهیداتی مربوط به آمادهسازی برای تدفین ویژه جانباختگان احتمالی کرونا از جمله تلی از آهک دیده میشود.

مقامات بیمارستانی در ایران اعلام کردهاند تنها از بیماران با علائم حاد تست کرونا میگیرند، از جمله آنها که به بخش مراقبتهای ویژه رفتهاند pic.twitter.com/ZM2YLd67Z6

A new video with translation, a dire situation in Iran (Video by @HeshmatAlavi), Translated by my friend, an Iranian journalist, can’t publish journalist’s name due to concerns for safety of her family in Iran. There’s no freedom of press in that country. pic.twitter.com/bHqUZQqLwR

Iranian dictator Ayatollah Khamenei issued a statement Tuesday urging that the “jihad” against coronavirus is proving successful, and that the outbreak “is not such a big tragedy.”

“I don’t want to say it’s unimportant, but let’s not exaggerate it either. The Coronavirus will affect the country briefly & leave. But the experience it brings, and the actions of the people & the govt sectors, are like a public exercise that will remain as an achievement,” Khamenei said.

Mike Adams joins Alex Jones live via Skype to confirm that the coronavirus is a bioweapon released by the Chinese Communist government to destroy the United States’ economy.

One US official who hasn’t shied away from probing the bio-weapon angle is Arkansas Sen. Tom Cotton, who has stated several times that Beijing needs to address the questions, and that the “burden of proof” is on “the communists” to explain where the virus came from.

.@ambcuitianki, here’s what’s not a conspiracy, not a theory:

Cotton has noted that “Wuhan has China’s only biosafety level 4 super laboratory that works with the worlds most deadly pathogens that include the coronavirus.”

Other officials, such as senior White House advisor Peter Navarro have admitted that they are not ruling out any possibilities:

How bad is COVID-19? That is far too complex a question for a blog post, so let’s focus on a much simpler question: What would an answer to the previous question look like? COVID-19 will cause deaths and illness, and attempts to reduce the deaths and illness will themselves impose economic costs. We could use a metric like QALYs (quality-adjusted life years) to aggregate the burden of COVID-19. Then, in assessing public policy interventions, such as closing schools and limiting travel, we could at least informally perform some sort of cost-benefit analysis, assessing the economic cost of an intervention and comparing it with the benefit in reduced deaths and illness.

Yet the QALY does not seem to enter into discussions of COVID-19. We see a great deal of discussion of mortality rates among those infected by the novel coronavirus, including reports of how those rates vary by age band. The question, though, is not just the age of those who have died, but how much longer they would have lived. I have not seen any systematic attempt to convert these mortality rates into a QALY number, let alone any formal cost-benefit analyses assessing how different interventions might save QALYs. Perhaps the government or some private citizens have created such analyses, but if so, they don’t seem to show up on Google or Twitter.

Why? Some possible explanations:

(1) Too many unknowns. Cost-benefit analysis, the argument goes, is a process that we can undertake only when we have sufficient time to accomplish it with care. There are many unknowns concerning COVID-19, including how many people carry the virus with mild symptoms or asymptomatically. It is difficult to construct a baseline case of how many people might become infected and die absent government intervention, so any cost-benefit analysis would largely be guesswork.

(2) Real option theory. A more sophisticated version of the previous hypothesis is that a cost-benefit analysis might be too simplistic and in particular might understate the value of extraordinary efforts to contain the virus while we develop better information about its dangers. For example, a cost-benefit analysis based on current assumptions of mortality might suggest that many interventions to reduce the spread of the virus are with high probability not cost-benefit justified, but that with low probability the pandemic will be so bad that such interventions are critical. In theory, we might assume some distribution of how deadly the virus is and simulate the effects of interventions now, taking into account that our information will improve in the future and thus allow better decisions then. But this means that the cost-benefit analysis must account for many more unknowns, plus it is difficult to aggregate the results into a single punchy conclusion.

(3) Lost QALYs. Discussion of QALYs almost always focuses on QALYs saved by interventions. The first step in a COVID-19 analysis would focus on the QALYs that would be lost in baseline. We frequently see reports of how many people die from cancer, but few reports of how many QALYs are lost to cancer. There are exceptions, such as this one measuring the global burden of disease with the related measure of DALYs (disability-adjusted life years). An explanation for the general lack of discussion is that the baseline burden of disease doesn’t matter for policy as much as lives saved from particular interventions. Because we are not used to thinking about disease burdens in QALYs or DALYs, we don’t seek to measure the burden of some new disease in those terms, even though we need to do that before we can assess interventions.

(4) Not medical treatments. Typically, QALYs are used to measure life-years saved by new medical treatments. Here, the question is the expected QALY savings from quarantines, canceling sporting events, and the like. We have standard methodologies for conducting randomized trials of medical treatments, and these methodologies can be used to generate QALY numbers. We may not have standard methodologies for measuring QALYs for government actions that are not medical treatments. In principle, however, we could use epidemiological models to estimate morbidity and mortality and translate that to QALYs.

(5) Prospect theory. The value of a QALY may differ based on whether we focus on a QALY saved or a QALY lost. Because our baseline is the pre-COVID-19 world, whether we are focusing on the burden of disease or the effectiveness of interventions, we frame the new suffering as losses rather than gains. Thus, arguably we should assign a higher value to a QALY with COVID-19 than when focusing on treatments of more familiar diseases. But questions of what a QALY is worth are second-order questions, worth asking when we want to compare QALYs to economic costs of particular interventions. It would be nice to have estimates of QALYs saved by interventions even if we might reasonably disagree about the trade-off between QALYs and economic costs.

I have no idea which steps to slow the spread of COVID-19 are cost-justified and which steps are not. My own ignorance doesn’t matter, but I worry that health organizations and governments may not even be trying to compare costs and benefits in any systematic fashion. Overreaction in the form of an availability cascade is especially likely at the beginning of a crisis, yet there is also a danger of complacency. There may be some good reasons not to base policy decisions solely on comparisons of QALYs and costs, but production of at least back-of-the-envelope estimates could be useful in anchoring serious policy discussion, even in or maybe especially in times of crisis.

from Latest – Reason.com https://ift.tt/39CxTQh

via IFTTT

How bad is COVID-19? That is far too complex a question for a blog post, so let’s focus on a much simpler question: What would an answer to the previous question look like? COVID-19 will cause deaths and illness, and attempts to reduce the deaths and illness will themselves impose economic costs. We could use a metric like QALYs (quality-adjusted life years) to aggregate the burden of COVID-19. Then, in assessing public policy interventions, such as closing schools and limiting travel, we could at least informally perform some sort of cost-benefit analysis, assessing the economic cost of an intervention and comparing it with the benefit in reduced deaths and illness.

Yet the QALY does not seem to enter into discussions of COVID-19. We see a great deal of discussion of mortality rates among those infected by the novel coronavirus, including reports of how those rates vary by age band. The question, though, is not just the age of those who have died, but how much longer they would have lived. I have not seen any systematic attempt to convert these mortality rates into a QALY number, let alone any formal cost-benefit analyses assessing how different interventions might save QALYs. Perhaps the government or some private citizens have created such analyses, but if so, they don’t seem to show up on Google or Twitter.

Why? Some possible explanations:

(1) Too many unknowns. Cost-benefit analysis, the argument goes, is a process that we can undertake only when we have sufficient time to accomplish it with care. There are many unknowns concerning COVID-19, including how many people carry the virus with mild symptoms or asymptomatically. It is difficult to construct a baseline case of how many people might become infected and die absent government intervention, so any cost-benefit analysis would largely be guesswork.

(2) Real option theory. A more sophisticated version of the previous hypothesis is that a cost-benefit analysis might be too simplistic and in particular might understate the value of extraordinary efforts to contain the virus while we develop better information about its dangers. For example, a cost-benefit analysis based on current assumptions of mortality might suggest that many interventions to reduce the spread of the virus are with high probability not cost-benefit justified, but that with low probability the pandemic will be so bad that such interventions are critical. In theory, we might assume some distribution of how deadly the virus is and simulate the effects of interventions now, taking into account that our information will improve in the future and thus allow better decisions then. But this means that the cost-benefit analysis must account for many more unknowns, plus it is difficult to aggregate the results into a single punchy conclusion.

(3) Lost QALYs. Discussion of QALYs almost always focuses on QALYs saved by interventions. The first step in a COVID-19 analysis would focus on the QALYs that would be lost in baseline. We frequently see reports of how many people die from cancer, but few reports of how many QALYs are lost to cancer. There are exceptions, such as this one measuring the global burden of disease with the related measure of DALYs (disability-adjusted life years). An explanation for the general lack of discussion is that the baseline burden of disease doesn’t matter for policy as much as lives saved from particular interventions. Because we are not used to thinking about disease burdens in QALYs or DALYs, we don’t seek to measure the burden of some new disease in those terms, even though we need to do that before we can assess interventions.

(4) Not medical treatments. Typically, QALYs are used to measure life-years saved by new medical treatments. Here, the question is the expected QALY savings from quarantines, canceling sporting events, and the like. We have standard methodologies for conducting randomized trials of medical treatments, and these methodologies can be used to generate QALY numbers. We may not have standard methodologies for measuring QALYs for government actions that are not medical treatments. In principle, however, we could use epidemiological models to estimate morbidity and mortality and translate that to QALYs.

(5) Prospect theory. The value of a QALY may differ based on whether we focus on a QALY saved or a QALY lost. Because our baseline is the pre-COVID-19 world, whether we are focusing on the burden of disease or the effectiveness of interventions, we frame the new suffering as losses rather than gains. Thus, arguably we should assign a higher value to a QALY with COVID-19 than when focusing on treatments of more familiar diseases. But questions of what a QALY is worth are second-order questions, worth asking when we want to compare QALYs to economic costs of particular interventions. It would be nice to have estimates of QALYs saved by interventions even if we might reasonably disagree about the trade-off between QALYs and economic costs.

I have no idea which steps to slow the spread of COVID-19 are cost-justified and which steps are not. My own ignorance doesn’t matter, but I worry that health organizations and governments may not even be trying to compare costs and benefits in any systematic fashion. Overreaction in the form of an availability cascade is especially likely at the beginning of a crisis, yet there is also a danger of complacency. There may be some good reasons not to base policy decisions solely on comparisons of QALYs and costs, but production of at least back-of-the-envelope estimates could be useful in anchoring serious policy discussion, even in or maybe especially in times of crisis.

from Latest – Reason.com https://ift.tt/39CxTQh

via IFTTT

Indian Government Nationalizes 4th Largest Bank As Shadow Banking Crisis Looms

Two years ago we first noted the building crisis in the Indian banking system, and now, as Bloomberg reports, the Indian government has stepped in to organize a rescue plan for the nation’s fourth largest private bank as a long-running crisis among shadow lenders threatened to spill over into the banking system.

“After 18 months of shadow banking crisis, the government did not want another major turmoil to hit the financial sector,” said Ravikant Anand Bhat, a senior analyst at Indianivesh Securities Ltd.

The government’s plan – to create a State Bank of India-led consortium to inject new capital into Yes Bank Ltd – would throw a lifeline to the embattled lender, which has been struggling to raise capital to offset a surge in bad loans.

Moody’s Investors Service cut the bank’s credit ratings in December and in January said its “standalone viability is getting increasingly challenged by its slowness in raising new capital.”

“Yes Bank is currently in the intensive care unit, and a State Bank capital injection will provide much needed oxygen,” said Kranthi Bathini, a director at WealthMills Securities Ltd.

Additionally, the finance ministry imposes a limit of 50,000 rupees on withdrawals (around US$650) from accounts held in Yes Bank, according to a gazette notification.

But the market does not seem reassured as India’s sovereign credit risk has recently spiked as virus fears and this banking system crisis comes to a head…

The RBI has superseded the board of Yes Bank for a period of 30 days “owing to serious deterioration in the financial position of the Bank,” the central bank says in a statement.

Yes Bank is not the first – The government took over IL&FS in 2018 in an effort to reassure creditors after the defaults. And last year, the Reserve Bank of India seized control of another struggling shadow lender, Dewan Housing Finance Corp., and said it will initiate bankruptcy proceedings – and we suspect it will not be the last.

The bear market rally probably didn’t persuade anyone the coronavirus crisis is over – but a few will wonder if we’ve passed “the end of the beginning” stage..! Time to stop the panic, and focus on timing for the upside? For instance, there are a surprising number of articles saying manufacturing production is recovering rapidly in China – although the same weather satellites I mentioned yesterday do show rising NoX levels, but they are still massively lower than they should be, inferring Chinese industry is about 50% of where it was this time last year!

A number of market talking-heads are saying there is no reason there should not be a swift V shaped recovery from this crisis – but I think they underestimate timing effects on sentiment, confidence in central bankers to keep juicing markets, and on supply chain resilience. Long-term, I reckon the global economy will emerge stronger, but timing is rather in the hands of “what the virus does next,” than the hopes of market sages! (Hopes are never a good strategy.) Perhaps we do get recovery, but I expect the second leg, the upward V, will be jerky and disjointed as more bad, and good, news emerges and is digested.

Markets also took some reassurance on the Chinese pledging $16 bln to fight the virus, and the American’s nearly $ 8bln – its clear East and West are taking the disease seriously. Read some of the articles about how bad it’s been in Wuhan, and it’s quite distressing.

However, the real issue is what are governments and central banks going to do about addressing the economic issues and damage?

Tuesday’s 50 bp emergency Fed cut conclusively demonstrated monetary policy is not going to address a global supply shock.

Solving the Coronovirus shock effects is going to be about practical politics and fiscal policy. Investors want to see what Governments are going to do in terms of hard dosh and real support being put on the table. Interest rates at zero are as relevant as painting a sinking ship.

This is the major reason I’m negative on Europe at the moment. The ECB under Lagarde is trying to join the 21stCentury, and realises that tinkering with rates and even QE is not the solution. It requires Fiscal policy to juice decaying economies. But fiscal spending is a government political decision. The ECB does not have any political mandate, and in any sane world will never be given one. Her best hope is for the ECB to support nations calling for the rules to be eased to allow fiscal policy – it won’t help Italy was the fist to the lending window, but even Berlin is making positive noises about combatting the effects of the virus.

The issue for markets remains recessionary threats, and these are multiple. One of the major ones is the prospect of an escalating cascade of defaults as companies start to go to the wall triggering wider financial contagion on the back of broken supply chains and lost orders.

I wasn’t that surprised UK Regional Zombie Airline Flybe finally went to the wall last night – Coronavirus was but the final nail in its coffin.

However, what does its collapse say about the UK’s Government intervening across business (and especially SMEs) to stop them going bust over Coronavirus fears? I am heartened to read new BOE Governor Andrew Bailey is greatly in favour of SME support to get them through the crisis. (I’ve decided I like Bailey – anyone who is a target of the self-confabulated Gina Miller is a friend of mine!)

But letting Flybe go bust raises a host of issues. For a start, I can’t believe the Boris government is using the excuse it can’t bail out Flybe because we are still subject to EU rules. FFS! This means the government could not cut domestic passenger taxes – which would have saved the airline, nor can they make it an emergency loan of £100mm. Both would upset Yoorp. Apparently!

There is a great argument to be made that Flybe is vital to UK infrastructure. If you want to fly from any of the regions to another you really have had no alternative. Driving is an option – if you fancy hours stuck in jams caused by our decaying infrastructure – and don’t even suggest the railways.

I’m particularly peeved about Southampton. The railway to anywhere is just appalling. The roads are most blocked – they are converting the motorways into “Smart Motorway” death-traps. And now the airport is closed – over 95% of the flights were Flybe.

Here is a great Business Investment Idea: Buy Southampton Airport

Let me tell you a story. A few years ago we were in Frankfurt on business. It was a Thursday night, and we were having dinner with German clients. I decided to fly directly home to Southampton the following morning, while Jimbo was going to Heathrow. But something came up, and we were both needed back in the office. It was too late to change flights. My flight to Southampton was 20 mins after the Heathrow flight. When I landed at Southampton, I walked across and caught the train to London Waterloo, and then the tube to the office. I arrived 30 mins before Jimbo who’d caught the earlier Heathrow flight.

There is a message in that story. Southampton airport is empty. It lies at the hear of Southern England in one hours drive of 20 million affluent people. It was a small airport under Flybe. It could be massive.

(And if you are wondering why there is a blue Spitfire on the Photo this morning, its because the guard plane at Southampton is a model of the original prototype Spit that first flew from the Airport in 1936!)

Back in the USSR USA

Meanwhile, the other big story this morning is the market not taking fright at the likelihood Joe Biden will win the Democrat Nomination, and even could/might win against Trump. That was utterly inconceivable just a week ago… All Trump had to do was wait for the Democrats to lose the election.

But a week is a long time in politics!

With the prospect of slower flatline growth or a weaker economy into the 3rd/4th quarter – timing and recessions are the secret of all good comedy – Trump could face a real battle with Biden. You might have expected the market to react badly to the prospect of a Biden win, but even health stocks went higher..

Over the next few days I’m looking for pro and con arguments on what a Democrat Win in November will do the global economy.