“Trump Should Not Rely on NATO”: The Once Formidable Alliance Has Turned Into A Gossip Circle

Authored by Nicholas Guy, originally posted in Human Events

In March, news that Germany refused to meet the financial obligations that come with membership to the North Atlantic Treaty Organization (NATO) was met with some ire by the general public. This shocked few national defense pundits, however.

For President Trump, who ran on a platform of holding our NATO allies accountable, the issue of membership dues is tantamount. In 2014, NATO members agreed to increase their contributions to the alliance to the amount of 2% of their respective GDPs; less than a quarter kept their promise. Since taking office, President Trump has pressured our allies to meet the standards they set themselves.

But the United States shouldn’t hold its breath. Germany—who had agreed, months back, to meet the 2% benchmark—announced in March that they will not do so. In an attempt to soften the blow, Germany suggested that it and the United States should only provide 16% of NATO’s operating budget—a reduction from the 22% that the United States had been burdened with. But this operating budget is distinct from the 2% of GDP that member states are obligated to contribute, per their own rules, and most members will continue to free-ride.

If European heads of state can laugh at and gossip about President Trump at a conference about the threats the Western world faces, America needs to be prepared to go it alone.

U.S. Army paratroopers assigned to 1st Squadron (Airborne), 91st Cavalry Regiment, 173rd Airborne Brigade. Nov. 20, 2019; Photo by Sgt. Henry Villarama.

THE ONCE-BOLD AMBITIONS OF THE POST-WAR COALITION

Seventy years after its formation, NATO is a shadow of its former self, a husk of the once-formidable alliance of anti-Soviet allies.

The Soviet menace was at the gate in the twilight of the 1940s. A world exhausted after years of total war was once again facing an existential threat. Communism was spreading like an untreated infection, and Western ideals were besieged. Since its inception, former Bloc states and weaker European nations have joined NATO to protect their autonomy. In theory, this should be a strong alliance, one well-funded and well-managed with immense institutional knowledge.

In practice, it’s a farce.

In the years since the fall of the Berlin Wall, member states have failed to pay their fair share of their obligations and forced the United States to shoulder the burden. Only a few members even bother to host military exercises for the alliance. Even when countries host their fellow members, the United States finds itself footing the bill for the massive costs associated with moving, coordinating, and executing the missions of other armies.

NATO’s member nations have done little to expand or modernize their military forces in recent years. Since 2001, Western militaries have focused their efforts at combating asymmetric threats, from terrorism, insurgencies, and non-state actors. The focus on unconventional warfare and counter-insurgency operations led Congress to steer defense monies to “overseas contingency operations.” This sterile, purposefully vague phrase describes what is essentially a slush fund, separate from the broader defense budget.

But while our military attention was focused on the mountains of Afghanistan, the streets of Iraq, and the deserts of Syria, new threats have emerged—threats that most of our Western allies are wholly unprepared for. Russia and China, fueled by chauvinism and motivated by dreams of imperialist grandeur, launched massive campaigns to expand their militaries and create robust intelligence apparatuses.

Army Rangers, assigned to 2nd Battalion, 75th Ranger Regiment. Photo Spc. Steven Hitchcock

THE BEAR AND THE DRAGON

Defense observers often sneer at Russia’s failures in their recent military technology ventures. Sukhoi’s new SU-57 lacks the latest stealth technology, and the Russian Federation has only been able to scrape together enough money to purchase 76 aircraft. Russian ground forces had also planned on acquiring 2,300 T-14 Armata main battle tanks by 2020—but had to push the timeline to 2025, which many experts still predict they’ll fail to meet. Russia’s Northern fleet sits docked, for the most part, rusting away while one official described the plans to modernize its hundreds of ships as a “fiasco.”

But these failures haven’t stopped Vladimir Putin from re-enacting the golden age of Soviet expansion. While the annexation of Crimea drew widespread media attention, Russia’s admittedly impressive involvement in Syria went largely unreported. Its naval base at Tartus is Russia’s only port to the Mediterranean sea, and they were not prepared to lose it. Russia sent thousands of advisers to train and fight alongside Assad’s forces against ISIS, the Syrian Democratic Forces, and the roughly dozen other non-state actors to claim territory in Syria. Russia mobilized a large air presence to enforce air space and harass coalition aircrafts, all while using its Special Operations capabilities to fortify regime territory and reclaim that which was lost. It proved that the regional power had achieved something we hadn’t seen from them since the 1980s: force projection—the key characteristic of a world power.

More alarming, though, is China. The sleeping dragon continues to smile for the cameras while it builds a military that rivals our own and is capable of dominating any regional opponent. Cold War-era equipment stocks and lackluster training curricula have been replaced by modern weapons systems, communications, body armor, and sophisticated exercises that dwarf those of most of their western counterparts.

Moreover, China is ahead of the curve when it comes to cyberwarfare. Its army invested heavily in the space years before the United States understood the value of defending critical systems against hacker attacks. In addition, China continues to project power throughout Africa, flooding eager third world countries with cash and military advisers, and have launched an island-hopping campaign to claim land without so much a protest in the region.

Green Berets assigned to 3rd Special Forces Group. Jan. 30, 2014. Photo by Sgt. Steven Lewis

AMERICA STANDS ALONE

The reluctant and half-hearted allyship of our NATO allies ultimately leaves the United States alone. NATO’s passivity over Russia and China has long established that they don’t take the threats seriously; indeed, it’s not clear they take their own sovereignty seriously. Of course, they’ll continue to lean on the military might of the United States. Why pull your weight when the last three decades have proven that Uncle Sam will foot the bill?

The United States is not the world’s police, and the American people are tired of endless war, sending our sons and daughters to die for reasons that are abstract at best. While we try and disentangle ourselves from the quagmire that is the Middle East and Western Asia, we must reconfigure our large conventional military to ensure a position of strength and readiness, prepared to engage the threats of China and Russia without the support of our NATO partners.

We’re in the final few days of Reason‘s annual webathon, during which we ask our readers, viewers, and listeners to support our original, influential, and principled libertarian journalism with tax-deductible gifts (a perk of being published by a 501[c]3 nonprofit). Go here to donate and to learn about the great swag we’re giving out this year. The webathon ends Tuesday, so don’t delay!

For extra motivation, I’m excited to tell you that an anonymous donor is currently matching all donations, dollar-for-dollar, until we reach $50,000 in new gifts. Any amount you give today—$50, $100, $1,000, or even $5,000—will be instantly doubled until we reach $50,000! Make your donation go twice as far by giving right now.

One of the things for which we use your money is to develop new ways to bring our journalism—articles, videos, and podcasts—to different and bigger audiences. Since our founding in 1968, we’ve always been on the hunt not just for stories about what comes next in American politics and culture but for how to get our stories out into the world in new and interesting ways. The result is a pretty cool history of innovation, gambles, and publishing firsts.

Reason.com’s logo, mid-1990s.

The first few issues of Reason were cranked out on an old mimeograph machine, the do-it-yourself (DIY) tech of the day. We launched our website in 1994, when most print publications were either ignoring online publishing completely or shrilly denouncing the web as the end of all that was good and decent when it came to media.

In 2004, we published the first-ever mass-produced personalized cover in magazine history. Employing cutting-edge printer technology and publicly available databases, we were able to send out about 45,000 unique covers illustrated with a high-quality aerial photograph of the recipient’s house. Each subscriber was named on the cover too, and four pages of the issue were personalized by ZIP code and congressional district. Even some of the ads were personalized. The image to the right is for the newsstand edition, which wasn’t personalized, though it was for me in a way: The house that’s circled was my address at the time.

In 2007, we launched Reason TV, one of the first “pivots” to video by an existing journalism outfit. I recounted the origins of Reason TV in a previous webathon post (short version: Thanks, Drew Carey!) so I won’t go into that here, other than to note that our pioneering efforts in online video proceed directly from our vision of a world in which creative destruction is not only tolerated but actively encouraged.

In 2010, we released a series of videos about the national debt that were filmed in amazingly crisp 3D! Our thinking was that conventional two-dimensional footage just couldn’t capture the full horror of rapidly mounting debt. Below is the series, which includes a Dadaesque cameo by former Alaska Sen. Mike Gravel, in old-fashioned 2D. (If you have 3D glasses, you can watch the videos in their original format by going here.) We also published a special 3D companion issue of the print magazine that came with Reason-branded glasses.

In 2016 we went long on podcasts, and just a few weeks ago we reorganized our efforts and launched three new streams: The Reason Roundtable, a weekly, rollicking, no-holds-barred discussion featuring Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me; The Reason Interview with Nick Gillespie, weekly in-depth interviews with activists, artists, authors, entrepreneurs, newsmakers, and politicians; and The Soho Forum Debates, a debate series recorded monthly before a live audience in New York City in which Nobel laureates, radical thinkers, and other public intellectuals face off over bitcoin, electric vehicles, government debt, illegal drugs, robotics, sex work, and other controversial topics. Go here to learn more and to subscribe to our podcasts.

These sorts of fun, exciting, and ongoing efforts are just some of the ways Reason is using your tax-deductible donations to create a future that is more interesting, more innovative, and more engaging.

We can’t do any of this without your support, both as consumers and as patrons. And remember, right now, your gift will be doubled by our $50,000 challenge grant. Please give what you can by going here.

from Latest – Reason.com https://ift.tt/2Ryeols

via IFTTT

We’re in the final few days of Reason‘s annual webathon, during which we ask our readers, viewers, and listeners to support our original, influential, and principled libertarian journalism with tax-deductible gifts (a perk of being published by a 501[c]3 nonprofit). Go here to donate and to learn about the great swag we’re giving out this year. The webathon ends Tuesday, so don’t delay!

For extra motivation, I’m excited to tell you that an anonymous donor is currently matching all donations, dollar-for-dollar, until we reach $50,000 in new gifts. Any amount you give today—$50, $100, $1,000, or even $5,000—will be instantly doubled until we reach $50,000! Make your donation go twice as far by giving right now.

One of the things for which we use your money is to develop new ways to bring our journalism—articles, videos, and podcasts—to different and bigger audiences. Since our founding in 1968, we’ve always been on the hunt not just for stories about what comes next in American politics and culture but for how to get our stories out into the world in new and interesting ways. The result is a pretty cool history of innovation, gambles, and publishing firsts.

Reason.com’s logo, mid-1990s.

The first few issues of Reason were cranked out on an old mimeograph machine, the do-it-yourself (DIY) tech of the day. We launched our website in 1994, when most print publications were either ignoring online publishing completely or shrilly denouncing the web as the end of all that was good and decent when it came to media.

In 2004, we published the first-ever mass-produced personalized cover in magazine history. Employing cutting-edge printer technology and publicly available databases, we were able to send out about 45,000 unique covers illustrated with a high-quality aerial photograph of the recipient’s house. Each subscriber was named on the cover too, and four pages of the issue were personalized by ZIP code and congressional district. Even some of the ads were personalized. The image to the right is for the newsstand edition, which wasn’t personalized, though it was for me in a way: The house that’s circled was my address at the time.

In 2007, we launched Reason TV, one of the first “pivots” to video by an existing journalism outfit. I recounted the origins of Reason TV in a previous webathon post (short version: Thanks, Drew Carey!) so I won’t go into that here, other than to note that our pioneering efforts in online video proceed directly from our vision of a world in which creative destruction is not only tolerated but actively encouraged.

In 2010, we released a series of videos about the national debt that were filmed in amazingly crisp 3D! Our thinking was that conventional two-dimensional footage just couldn’t capture the full horror of rapidly mounting debt. Below is the series, which includes a Dadaesque cameo by former Alaska Sen. Mike Gravel, in old-fashioned 2D. (If you have 3D glasses, you can watch the videos in their original format by going here.) We also published a special 3D companion issue of the print magazine that came with Reason-branded glasses.

In 2016 we went long on podcasts, and just a few weeks ago we reorganized our efforts and launched three new streams: The Reason Roundtable, a weekly, rollicking, no-holds-barred discussion featuring Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me; The Reason Interview with Nick Gillespie, weekly in-depth interviews with activists, artists, authors, entrepreneurs, newsmakers, and politicians; and The Soho Forum Debates, a debate series recorded monthly before a live audience in New York City in which Nobel laureates, radical thinkers, and other public intellectuals face off over bitcoin, electric vehicles, government debt, illegal drugs, robotics, sex work, and other controversial topics. Go here to learn more and to subscribe to our podcasts.

These sorts of fun, exciting, and ongoing efforts are just some of the ways Reason is using your tax-deductible donations to create a future that is more interesting, more innovative, and more engaging.

We can’t do any of this without your support, both as consumers and as patrons. And remember, right now, your gift will be doubled by our $50,000 challenge grant. Please give what you can by going here.

from Latest – Reason.com https://ift.tt/2Ryeols

via IFTTT

US Shocks With Inflated Claim Of 1,000 Iranian Protesters “Murdered” By Regime

The Trump administration has issued an assessment of the recent unrest in Iran which had raged for a couple weeks after protests in some 100 cities were triggered by a sudden fuel price hike on Nov. 15 when government subsidies were slashed. Though international reports and human rights monitoring groups have consistently cited a little over 200 killed (with the UN and Amnesty saying 208 or more), US figures are multiple times higher.

In a Thursday press briefing, the State Department said it has counted a whopping 1,000 protesters killed by Iranian security forces. Partly using local video as evidence, spokesman Brian Hook said, “As the truth is trickling out of Iran, it appears the regime could have murdered over 1,000 Iranian citizens since the protests began.”

He said the White House will urge Congress to impose further harsh sanctions on officials overseeing security forces, especially the IRGC-connected Basij paramilitary force, thought responsible for“mowing down” demonstrators.

Special Envoy for Iran Brian Hook

Hook also charged the regime with killing “at least a dozen children” and wounding many thousands in a crackdown involving torture among some of the over 7,000 arrested.

Though there’s widespread acknowledgement, even among some Iranian official sources, that the security crackdown has been harsh and in some instances involved ‘live fire,’ the US administration’s figure appears inflated for political purposes, as even The Washington Postacknowledges:

The State Department’s casualty numbers are much larger than estimates provided so far by independent groups. Amnesty International, for example, has confirmed about 200 deaths, though it said the number was likely to be much higher.

While showing a sample video of police attacking protesters — one among the32,000 videos and photos reportedly sent inafter Pompeo’s earlier public call for ‘crackdown’ footage — Hook described, “The IRGC tracked them down and surrounded them with machine guns mounted on trucks”.

“It appears the regime could have murdered over 1000 Iranian citizens since the protests began.”

Brian Hook, U.S. Special Representative for Iran, says “hundreds more” Iranian protesters have been killed than originally thought, including at least a dozen children pic.twitter.com/cGocA6QA4j

“Between the rounds of machine gun fire, the screams of the victims can be heard,” he said further of one dramatic scene. “In this one incident alone, the regime murdered as many as 100 Iranians and possibly more. When it was over, the regime loaded the bodies into trucks.”

And in emotionally jarring claims which resemble Washington talking points within the first years of proxy war in Syria (which were clearly geared toward regime change), the Post reports further:

Hook said that when families tried to recover the bodies, the IRGC demanded they pay the cost of the ammunition and extracted their promise not to hold public funerals.

Evidence for this and some of the other dramatic and harrowing details of torture and human rights abuses were not forthcoming, however, in what appears to be an active US policy of continued ‘overthrow the regime’ efforts targeting Tehran.

But the United Nations Human Rights commission did issue a special report on Friday which alleges Iranian security forces were “shooting to kill” in their deadly crackdown, which also primarily cited local video as evidence. Again the UN’s casualty count was just over 200 — some800 less than the now official administration figures.

Meanwhile, Iranian leaders have claimed (also without evidence) that hostile external powers like the CIA and Israel’s Mossad have hijacked protests by sending “thugs” to initiate mayhem, resulting in the burning of hundreds of banks, gas stations, and security bases.

The protests in Hong Kong, which started in early June, were sparked by a bill that would have allowed China and Taiwan to extradite suspected criminals residing in Hong Kong. But the protests are about much more than that. The extradition bill was inspired by Chan Tong-kai, a 19-year-old accused of strangling his pregnant girlfriend to death in Taiwan and then fleeing. That such a deeply unsympathetic suspect launched a protest movement watched around the world illuminates the extent to which Hong Kong residents fear the influence of the Chinese Communist Party.

Save for four years of occupation by Japan during World War II, Hong Kong was a British territory from 1841 to 1997. Its political culture is distinctly British, in that Hong Kong has clear due process rights, quasi-democratic representation, and a healthy respect for civil liberties. In 1997, when the U.K. gave the island back to China, it stipulated that Beijing needed to preserve Hong Kong’s political culture under a “one country, two systems” model. The agreement says China must allow Hong Kong to maintain its system of semi-autonomy through 2047.

Privately operated newspapers in Hong Kong run scathing critiques of politicians without political reprisal. This does not happen in Shenzhen. While mainland China claims to have freedom of association and expression, it also has vague anti-subversion laws that let the authorities target dissidents. “The extradition bill would have blurred the line between the Hong Kong and mainland justice systems,” says Hong Kong–based journalist and lawyer Antony Dapiran.

Hundreds of thousands of Hongkongers have taken to the streets, smashed lamp posts (which are suspected of having surveillance capabilities), and stormed government buildings to keep China from encroaching on Hong Kong’s freedoms prematurely. The protesters have, in turn, been on the receiving end of increased police brutality—a possible harbinger of life under Communist rule.

Most protesters don’t want secession, but they do want to preserve the Hong Kong they know—a wealthy metropolis with high economic freedom and low corruption. Dapiran notes that “the vast majority, if not all, Hongkongers want ‘one country, two systems’ to continue indefinitely.” It is “anxiety” over the 2047 deadline, he says, that’s powering the protests. Hongkongers realize winning full autonomy is unrealistic. But Chinese rule would ruin the freedoms they cherish, and it’s unlikely those freedoms would be restored in their lifetimes.

Hong Kong’s revolutionaries just want to keep what they have. They’re fighting for nothing more, and they will settle for nothing less.

from Latest – Reason.com https://ift.tt/2s453qW

via IFTTT

The protests in Hong Kong, which started in early June, were sparked by a bill that would have allowed China and Taiwan to extradite suspected criminals residing in Hong Kong. But the protests are about much more than that. The extradition bill was inspired by Chan Tong-kai, a 19-year-old accused of strangling his pregnant girlfriend to death in Taiwan and then fleeing. That such a deeply unsympathetic suspect launched a protest movement watched around the world illuminates the extent to which Hong Kong residents fear the influence of the Chinese Communist Party.

Save for four years of occupation by Japan during World War II, Hong Kong was a British territory from 1841 to 1997. Its political culture is distinctly British, in that Hong Kong has clear due process rights, quasi-democratic representation, and a healthy respect for civil liberties. In 1997, when the U.K. gave the island back to China, it stipulated that Beijing needed to preserve Hong Kong’s political culture under a “one country, two systems” model. The agreement says China must allow Hong Kong to maintain its system of semi-autonomy through 2047.

Privately operated newspapers in Hong Kong run scathing critiques of politicians without political reprisal. This does not happen in Shenzhen. While mainland China claims to have freedom of association and expression, it also has vague anti-subversion laws that let the authorities target dissidents. “The extradition bill would have blurred the line between the Hong Kong and mainland justice systems,” says Hong Kong–based journalist and lawyer Antony Dapiran.

Hundreds of thousands of Hongkongers have taken to the streets, smashed lamp posts (which are suspected of having surveillance capabilities), and stormed government buildings to keep China from encroaching on Hong Kong’s freedoms prematurely. The protesters have, in turn, been on the receiving end of increased police brutality—a possible harbinger of life under Communist rule.

Most protesters don’t want secession, but they do want to preserve the Hong Kong they know—a wealthy metropolis with high economic freedom and low corruption. Dapiran notes that “the vast majority, if not all, Hongkongers want ‘one country, two systems’ to continue indefinitely.” It is “anxiety” over the 2047 deadline, he says, that’s powering the protests. Hongkongers realize winning full autonomy is unrealistic. But Chinese rule would ruin the freedoms they cherish, and it’s unlikely those freedoms would be restored in their lifetimes.

Hong Kong’s revolutionaries just want to keep what they have. They’re fighting for nothing more, and they will settle for nothing less.

from Latest – Reason.com https://ift.tt/2s453qW

via IFTTT

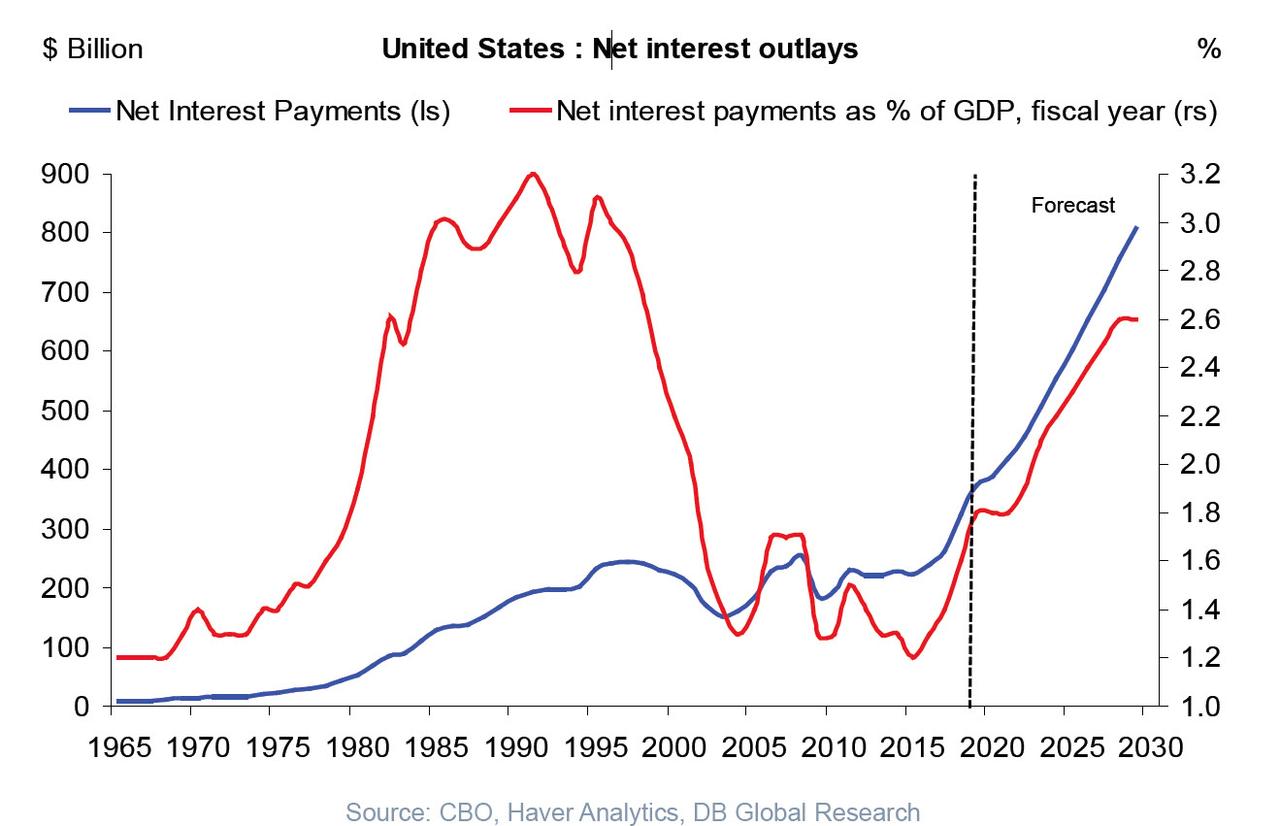

The David Einhorn Podcast: The Fed Is Monetizing Debt Again

It was back in 2012 that famed contrarian and value investing hedge fund icon, David Einhorn, first took aim at the pinnacle of market manipulation when he slammed the Fed for creating the ultimate toxic cocktail: something he called the Jelly Donut Policy. As the Greenlight founder wrote in May 2012, the Fed is “presently force-feeding us what seems like the 36th Jelly Donut of easy money and wondering why it isn’t giving us energy or making us feel better. Instead of a robust recovery, the economy continues to be sluggish.”

Seven years later, the recovery is just as sluggish and yet nothing has changed; in fact, just two months ago, the Fed launched what Fed Chair Powell sternly refuses to admit is QE4 but… is QE4. And while Einhorn has been right that the Fed is ultimately destroying the very fabric of not only the US economy, but taking down society with it as the growing wealth and income disparity chasm will eventually culminate in civil war, by fighting the Fed, Einhorn has seen his AUM plummet in recent years, his hedge fund a shadow of what of what it once was, largely due to the relentless ascent of the so-called “bubble basket” of stocks, those names which benefit entirely due to the Fed’s monetary generosity, and which have seen their stocks prices explode in the past decade.

Which brings us to another Jelly Donut – that’s the name of a new podcast service, which in recent weeks has interviewed, Julian Brigden, Ben Hunt, Miles Kimball, and others. Most notably, among those interviewed is that man responsible for the concept in the first place: David Einhorn.

While David Einhorn has recently been in the press for yet another feud he is currently waging, this time with Elon Musk, in which he first accused the Tesla CEO of “Significant fraud”, followed up with even more specific accusations of accounting irregularity profiled here, in the podcast with Ryan – which marked the Greenlight CEO’s first appearance in two years – Einhorn goes back to his roots and takes on his primary nemesis, the Federal Reserve, which is why among the topics covered are QE, ZIRP, MMT, fiscal and central bank stimulus. Oh, and gold, because seven years after the “Jelly Donut policy” was first coined, Einhorn remains just as bullish on the precious metal as the following excerpt confirms:

We’re running a very high deficit to GDP. And this is many years into an economic recovery with something that’s very close to full employment… In the event that the economy weakens, there’s going to be an enormous, both natural fiscal stimulus that comes from higher benefits, and less tax revenue, as well as an urge for Congress to do things to help people out in tougher economic times. So, what you have is a deficit right now that is very high and then you combine that with an accumulation of debt. You have a situation where the debt to GDP is much higher going into whatever the next down cycle is, and where we’ve had before similarly you have of monetary policy, which has been very aggressive. The balance sheet is much larger than it used to be and the rates going into down cycle are much lower than they used to be. There will be enormous pressure on the central bank to be very aggressive. And, so when you combine aggressive fiscal policy with aggressive monetary policy, historically that can lead to a problem with the currency and then when you realize that the same dynamic is essentially in place and in some cases worse in all of the other major developed currencies, it seems to me it’s a situation where sooner or later it might be good to have a fraction of your assets in gold, which is not subject to appropriation by the whim of the central banks.

Or rather, it is not yet subject to appropriate by central banks. Because all it takes is another Executive Order 6102 for all that to change.

All this and much more in the podcast below (phonetic transcript attached below):

Transcribed:

Ryan: David welcome to the podcast.

David: Hi Ryan. Thanks for having me.

Ryan: Well, it’s great to have you here. Really appreciate you coming on. First off, I wanted to explain a little bit to the audience of why we have you here, and when I decided to launch this podcast, I was trying to think of a great name that captured the subject of the show everything related to macro and monetary policy and I immediately thought about your article. So, going back to 2012 you wrote an article called The Fed’s Jelly Donut Policy in The Huffington Post and used a story about The Simpsons to explain a long periods of QE and zero interest rates may actually be harmful to the real economy. And it turns out a lot of what you said, they’re panned out inefficient allocation of Capital stock Buybacks with no urgency for corporations to invest to reach for yield from all investors, especially to Retirees so a lot has happened since then take us back to the feedback you got from the article and if your views have changed since.

David: Well honestly, I think the best feedback I got from the article is somebody’s naming their podcast after it. How can how can you beat that? And I’m honored to be here for the first one of these and I expect after I speak today, you’ll probably get all kinds of feedback and I will hopefully learn from listening to the feedback you get because I’m not a trained Economist. I’m not a macro-economist, I’ve never worked in the plumbing of the fed or any of these things. I’m basically an equity Market investor, and I think I have a few observations on some of these things from time to time, but I don’t profess to be a technical expert in all the mechanics of everything.

Ryan: Right and what was considered unconventional monetary policy over decade ago is really now seen as normal not just for the FED but central banks around the world and these policies seem to only be going on for longer and longer and uh others talked about using these tools and definitely what’s your view on these policies as far as do you ever imagine that balance sheet still being over $4.5T, you know taking up towards there right now and before the crisis was $800B. Did you see this still going on this long? And what’s your thoughts on the Fed using these tools and definitely?

David: Yeah. I don’t know how to predict what the FED is going to do with the size of the of the balance sheet, you know, basically, I think there’s two main parts of fed uh policy one is the interest rate policy and then the uh other is the balance sheet size the main thrust of the jelly donut thesis is that the interest rate policy by setting rates too low at some point you have a diminishing return from lower rates and eventually ultimately a marginally negative return from low rates, which is kind of separate from what you just raised which has to do with the size of the FED balance sheet and the monetary base and how they choose to implement that.

Ryan: Yes, so separating those out a little bit, obviously with the all the easing, you know, short-term rates, they’re able to target and bring down low and now we’re having some issues in the repo Market obviously some change some things change with paying interest on excess reserves and there’s been some other issues that brought up as far as the tax bill and things like this. What’s your thoughts right now on the current issues with the repo market and can the Fed really keep a hold of rates at this point?

David: Well, I think the FED ultimately can control whatever chooses to control within certainly within rates or whatever markets it’s willing to intervene in because it has unlimited fire power in order to enforce whatever policies that it wants . Sometimes eventually if the fed or a central bank over overdoes it, then people can take it out on the currency, which would be the normal reaction, but within the domestic economy in terms of control…. The Fed can set any rate that wants actually almost anywhere on the curve by, you know directly intervening in the market with unlimited firepower.

Ryan: Right, and going back to a Bloomberg interview did in 2014, you told a story about how you ask Ben Bernanke and a private dinner about QE and he talked about how these policies would lead to higher inflation talking about usually it only happens after a war and he talked about Japan has done a lot more QE than the US and they don’t have inflation. Recently Fed officials have said it’s kind of a mystery why. CPI claims inflation hasn’t gone up more but we have seen inflation in certain pockets: Healthcare, Housing, College tuition and you mentioned the currency piece. So what’s your thoughts as far as, where inflation goes and how long it can actually stay where it is right now?

David: When the Fed creates money and whether it’s from what you would call money printing or what they want to call quantitative easing, and most recently they’re doing the same thing and they want to tell us that it’s not quantitative easing. I don’t really know what the difference between all of these things is except for semantics and messaging in an attempt to, kind of control things. When the Fed increases the money the money has to go somewhere. It doesn’t have the same impact that it did when there were fewer excess reserves in the system, but we can come back to that later. I’ll just skip over that for the moment, but when they create money, the money does have to go somewhere. Now, the thing is, they don’t have any control over where that is. So it could be that the price of corn goes up or it could be the price of healthcare goes up or it could be the price of stocks go up or the price of bonds or art or Real estate or oil or what not but it doesn’t have to be any of those particular things. So as price levels in general go up it may or may not be prices that are measured within the CPI basket, which is only, you know, its a subset of possible places where new money can go.

Ryan: That makes sense. And you mentioned kind of the mechanics of how QE works. So one camp says that this is just an asset Swap and that this is a swap for bank reserves for Treasuries, and this is kind of normal operations. Where the other camp says this is something more like money printing and really something like debt monetization since all the interests gets remitted back to the Treasury and the so far a lot of these assets haven’t actually rolled off. How do you actually view that piece?

David: Yeah. I think it’s a little bit of a semantic game. By only looking at one side of a transaction, in other words, like what happens after a treasury is issued, you can decide, you know, that this isn’t money printing. But when you think about it in the totality how do treasuries get issued, a treasury is issued because the government needs to borrow money. And when the government needs to borrow money, there’s two places they can borrow it. They can borrow it in the private sector or effectively they can borrow it from the central bank. Now, there’s a rule that says they can’t sell the debt directly to the central bank, so they instead issue a T-bill to a leading commercial bank and then the central bank can buy the T-bill and you’re kind of in the same place. What’s happened is that the Federal government has borrowed money and ultimately that loan is held by the central bank which increases the central bank’s balance sheet size and thereby in there for the monetary base. So it’s the equivalent of a debt monetization. When you question whether its quantitative easing whether the current Fed chairman says it’s something different from that , whether it’s money printing, it’s really all the same things because all it is, it’s the Fed increasing the size of its balance sheet by buying Treasuries in one form or another. The difference is some people want to look at it as a two-step thing where the treasuries are issued by the Treasury Department to the private sector and then the Fed buys it as opposed to the Treasury issuing it directly to the Fed which is illegal, but the fact that there’s two steps in the transaction—I don’t think it makes any economic relevance. So think you have to look through it and when you look through it, when the Fed buys Treasuries, they’re increasing the balance sheet. They’re increasing the monetary base and effectively its debt monetization.

Ryan: Right, that makes a lot of sense. Now going back to interest rates and kind of what your article focused on, it’s arguable that interest rates are really the price of money and the price of money has been manipulated. Now, as far as rates rising on the longer end, you mentioned the Fed can kind of control not just the short-end, but also the longer-end. We saw recently when the repo market spiked up to a 10 from 2, that people said, okay, the price of money is not really what the Fed says is it is the price should be this. So, the question is, could the Fed lose control as far as people losing faith in their ability to just start tinkering and really micromanage. And will that show up maybe on the long end of the curve or how could that crisis of confidence happen?

David: I don’t know that you’ll have a crisis of confidence. But when you think about what just happened in the repo Market essentially, there wasn’t a huge amount of active intervention in the exact moment that it spiked. It spiked and the Feds saw what was happening relatively quickly after and announced new programs with extraordinary firepower in order to make sure that the problem doesn’t persist and that’s what I mean by their having the ability to control the rate. So, it spiked for a moment, but beyond that, you know, they managed to put it back together. As for Relating to the long end the curve, it has to do with how much intervention this the Fed is willing to do. Presently, I don’t know that they’re doing a lot of intervention on the long-end, but if you look at other central banks around the world, Japan and Europe and so forth, there’s huge amounts of intervention at the long-end of the curve and those banks have effectively cornered and controlled those rates as well.

Ryan: Yeah, that’s interesting when you look at Japan buying up huge amount of the JGBs is outstanding and obviously buying ETFs and things like Apple stock and seemingly distorting markets and doing so. Now, going back to the article again, the thesis laid out talking about with the Simpsons, it was actually really enjoyable to read for people who are trying to understand how this is all working. And, I think when you look at retirees, when you look at savers and obviously pension plans and insurance companies, a lot of these types of things have really caused a big problem as far as rates being low, and obviously for all investors going out on the curve to bid up risk assets. Do you see a path to normalization as far as rates or concerned? And what should the Fed be doing right now, and can they normalize rates or should they right now?

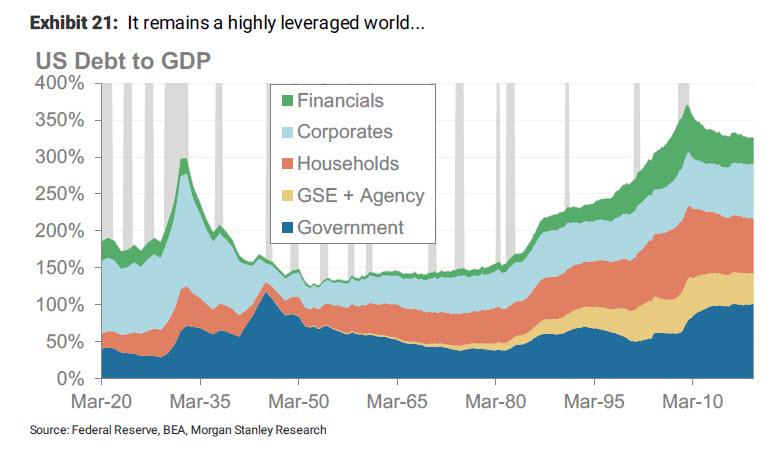

David: Well, I think it depends on what one thinks about as normalized rates. We’re certainly in a situation that there’s a lot more leverage in the financial system than 20 or 30 years ago, which means that the debt that’s in the system can’t support nominal rates that are higher than a certain amount, you know, if you think about what the deficit looked like when Volcker raised the short rates up into the teens, the debt to GDP was nowhere near what it is today. So you didn’t create a question about the government’s ability to repay the even in as rates went even a short rates went up at a at a good clip and ultimately even cost for long bonds. They wanted to sell at the time became quite expensive right once you have debt to GDP or incorporate case debt to EBITDA at higher ratios. It becomes much more sensitive to increase rates in terms of, from a solvency perspective. And so the situation is much different today than it used to be.

Ryan: Yeah, I’m looking at equity markets, especially here in the U.S., when you look at share buybacks and other things that have been going on. How are you looking at this the market based on these share buybacks uh and a lot of people have been talking about it. We’ve seen this many times before and it’s only a matter of time until the cycle has turned and you’ve talked a little bit about this over the past couple of years, but it really seems we’re almost kind of out of breaking point. How do you feel about the market right now?

David: I have no opinion as to whether the market is anywhere near a breaking point. Not the type of forecasting or thinking about things that I think about, you know, and in terms of things like share repurchases from my perspective, they are a tax efficient way to return capital and businesses to their owners and to the extent that there aren’t investment opportunities at better returns than returning capital to their owners, I think it’s a perfectly appropriate thing for businesses to do.

Ryan: Okay, that makes sense and you mentioned as far as going back to 2008 and even previous with the derivatives and all the debt built up in the system. How are you looking at the current environment compared to 2008. Obviously, it was built up more so in the mortgage market. How are you looking at the market now compared to back then. We now have some of these banking regulations after Dodd-Frank and others. Are we actually worse off or more levered up?

David: Well, there’s leverage, but the leverage is in a different place than it was last time last time. I believe (in 2008) that the leading part of the leverage was in the real estate market both commercial and residential and I think today it’s more in the public market meaning sovereign debt, municipal debt, and also corporate debt.

Ryan: Right and we’ve seen corporates levered up to some of the highest they’ve been…The last thing to touch on is, you’ve held a position in physical gold for a while now. Other investors have talked about hedging against inflation or even a “Black Swan” type event with real assets. How are you seeing a position in real assets as far as hedging against inflation?

David: Yeah. I don’t know that it’s a hedge against inflation or a particular Black Swan event. But, our theory relating to gold is that monetary and fiscal policies combined are very aggressive. Just take the United States as an example right now. We’re running a very high deficit to GDP. And this is many years into an economic recovery with something that’s very close to full employment… In the event that the economy weakens, there’s going to be an enormous, both natural fiscal stimulus that comes from higher benefits, and less tax revenue, as well as an urge for Congress to do things to help people out in tougher economic times. So, what you have is a deficit right now that is very high and then you combine that with an accumulation of debt. You have a situation where the debt to GDP is much higher going into whatever the next down cycle is, and where we’ve had before similarly you have of monetary policy, which has been very aggressive. The balance sheet is much larger than it used to be and the rates going into down cycle are much lower than they used to be. There will be enormous pressure on the central bank to be very aggressive. And, so when you combine aggressive fiscal policy with aggressive monetary policy, historically that can lead to a problem with the currency and then when you realize that the same dynamic is essentially in place and in some cases worse in all of the other major developed currencies, it seems to me it’s a situation where sooner or later it might be good to have a fraction of your assets in gold, which is not subject to appropriation by the whim of the central banks.

Ryan: Right, that makes a lot of sense. Well David, thank you so much for coming on, I really appreciate it.

David: You’re welcome and good luck with the whole podcast series.

Nancy Pelosi is a bitch. And in saying that I’m actually being sexist against female dogs, since every one of them I’ve ever met is a higher quality individual than Pelosi.

So, my apologies to dogs everywhere.

Just when you thought this power-mad harpy couldn’t sink any lower she responds to a simple question from a reporter with the kind of lame, stuttering virtue-signaling that has become her signature move, to attack when confronted with the truth.

This screed is a masterclass in diversion and doublespeak. Her self-righteous anger is a dead giveaway that she was lying about her motivations for proceeding with this impeachment while scolding the CSPAN reporter who asked the question like he was an impudent child.

If there is one thing Nancy Pelosi hates it is being called a liar.

She’s the ultimate keeper of the status quo, of the political order as she sees it and she has determined it shall be.

But she damns herself by wrapping herself in the false flag of her Catholicism. The false flag of her love for humanity. She is so desperate to deflect away from the truth that she does, in fact, hate the president and all that his election represents, she uses that to debunk the idea that she can hate anyone.

You know, except for all those unborn children that she advocates murdering or the people overseas she spends zero time stopping from being bombed by the administration.

So, we all have to suffer because of this outrageous woman’s all-consuming love for humanity? That’s what she’s trying to sell now?

In a word, yes. The mask slipped when she had to run back to the podium to look into the camera and unconvincingly proclaim her love of children. And that she’ll fight anyone who gets in her way, clutching her rosary the entire time.

Yup, that’s love all right.

The tough broad act plays well with the bi-coastal shitlib set but the rest of us just look at her and shake our heads wondering who in the holy hell does she think she’s fooling with this stuff?

Please, I’ve seen more believable acting in your average 1990’s porn flick.

That thin veneer of compassion masks a cold and cruel calculation and psychopathology which is abhorrent to anyone with any shred of a soul left.

The sad truth is that Pelosi in her near-dementia might actually now believe some of this stuff she’s spouting. Here she does a CNN Town Hall in which she parrots the current climate hysteria saying that civilization itself depends on removing Donald Trump from the White House.

Even if this is true, and this is how she sees herself, acting out of a love for humanity rather than her own narrow interests, then she’s simply a classic villain archetype who is willing to break a few eggs to make her omelette.

And Pelosi, like the people she ultimately represents, are telling us that they will ‘love us all to death‘ to achieve their goals. It’s the most sick and twisted form of manipulation possible.

She’s morphed from the tough broad from San Francisco to the epitome of Toxic Femininity, the over-bearing mother archetype. And any threat to her power will be met with the cruelest counter-attack.

She’s Nurse Ratched with Botox.

And Donald Trump is her R. P. McMurphy.

And in every way Pelosi knows that she’s locked in an existential battle for control over the future of America. She knows that she’s been tasked with delivering results on destroying Trump and if she doesn’t she’ll be cast aside.

No rational person can actually think the world is going to end in twelve years when they take even a cursory look at the climate data. But Pelosi is an order-taker not an order-maker in the hierarchy of political dominance.

And the call has come from above her pay-grade to sell this climate hysteria as the way to keep the program on track to finish the globalist’s dream of universal serfdom for us and perpetual power for them.

That’s your tell that Pelosi simply does what she’s told. It’s her job to sell whatever it is she’s been told to sell.

Every religion has it’s apocalypse story and the latest one from the Climate Crazies is this insane notion that time has run out and we need to act now or face extinction.

You know someone is lying to you when they only present you ultimatums, which are always a false binary choice. Follow our prescriptions or we’re all going to die!

And Pelosi truly is the enforcer of this edict.

In her heart she knows this impeachment process is a sham. She knows the premise is faulty and the results for the Democratic Party will be catastrophic. She can see the poll numbers.

But in her single-mindedness to save the world from itself, Pelosi will do everything she can to force us wayward and mentally-ill citizens back into her institution because her cause is righteous.

That’s why it’s now a life or death struggle to get rid of Trump. That’s why she’s willing to sell Climate hysteria and that’s why she lost her mind when asked the simplest of questions which she could have brushed off with a wave and a “No.”

Her vehement denial is her admission of guilt. For a moment, Speaker Ratched lost control and the results were a glimpse into the depths of her evil.

In 2004, we published

In 2004, we published .jpg) In 2016 we went long on podcasts, and just a few weeks ago we reorganized our efforts and launched three new streams: The Reason Roundtable, a weekly, rollicking, no-holds-barred discussion featuring Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me; The Reason Interview with Nick Gillespie, weekly in-depth

In 2016 we went long on podcasts, and just a few weeks ago we reorganized our efforts and launched three new streams: The Reason Roundtable, a weekly, rollicking, no-holds-barred discussion featuring Katherine Mangu-Ward, Peter Suderman, Matt Welch, and me; The Reason Interview with Nick Gillespie, weekly in-depth  interviews with activists, artists, authors, entrepreneurs, newsmakers, and politicians; and The Soho Forum Debates, a debate series recorded monthly before a live audience in New York City in which Nobel laureates, radical thinkers, and other public intellectuals face

interviews with activists, artists, authors, entrepreneurs, newsmakers, and politicians; and The Soho Forum Debates, a debate series recorded monthly before a live audience in New York City in which Nobel laureates, radical thinkers, and other public intellectuals face .jpg) off over bitcoin, electric vehicles, government debt, illegal drugs, robotics, sex work, and other controversial topics. Go

off over bitcoin, electric vehicles, government debt, illegal drugs, robotics, sex work, and other controversial topics. Go

{kind=link}

{kind=link}

{kind=link}

{kind=link}