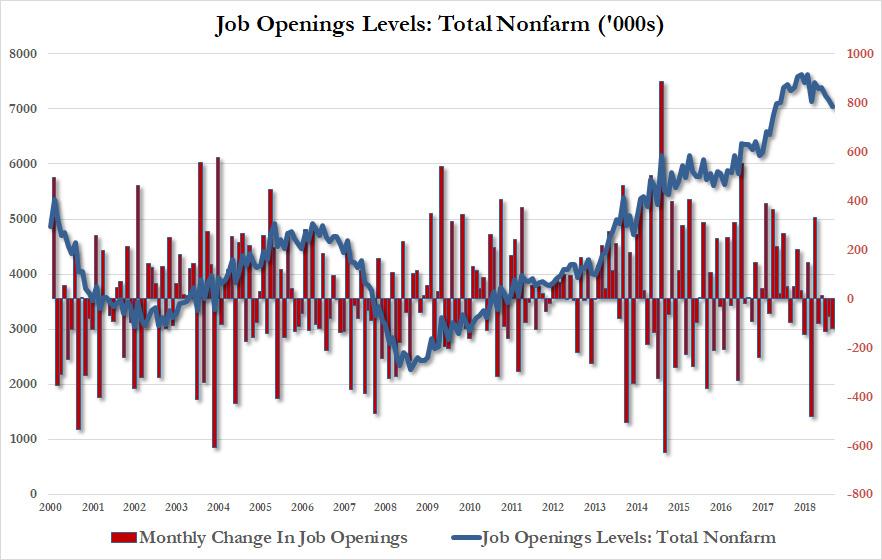

Job Openings Plunge To 17 Month Low As Slide In Hiring, Quitting Confirms Job Market Slowdown

Last month we concluded our analysis of the July Jolts by reminding readers that “JOLTS is 2 months delayed, so we wouldn’t be surprised if next month’s JOLTs is where the real ugliness lies.” That’s precisely what happened.

Just in case the last few disappointing payrolls reports weren’t sufficient to indicate that the US labor market is cooling rapidly, the latest JOLTS released today by the BLS confirmed that US workers are going through a decidedly rough patch, as the total number of job openings dropped again, sliding to 7.051 million, below the 7.250 million expected, and not only below the downward revised June print of 7.174 million (7.217 previously), but the lowest number in 17 months, since March 2018.

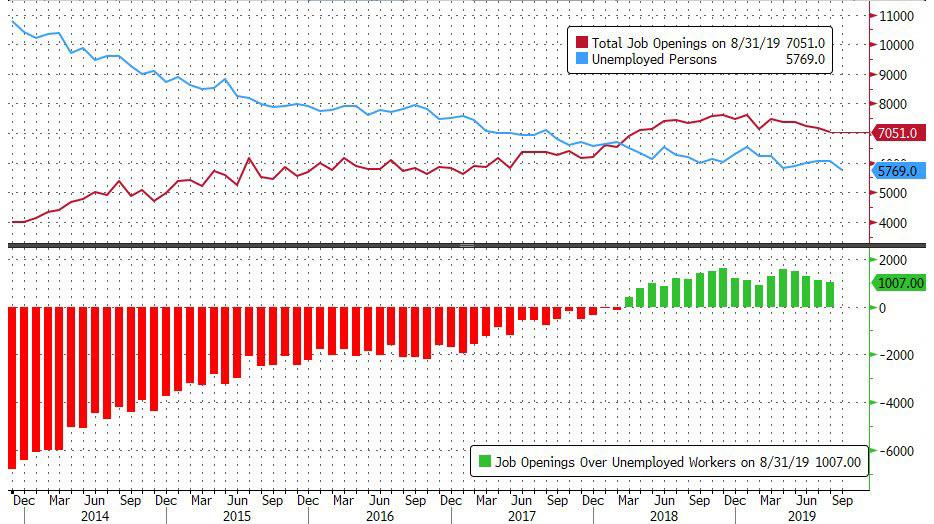

Yet even with the slowdown in job openings, there was still more than 1 million more job opening than unemployed workers; in fact there have now been more US job openings than unemployed workers for a record 18 consecutive months.

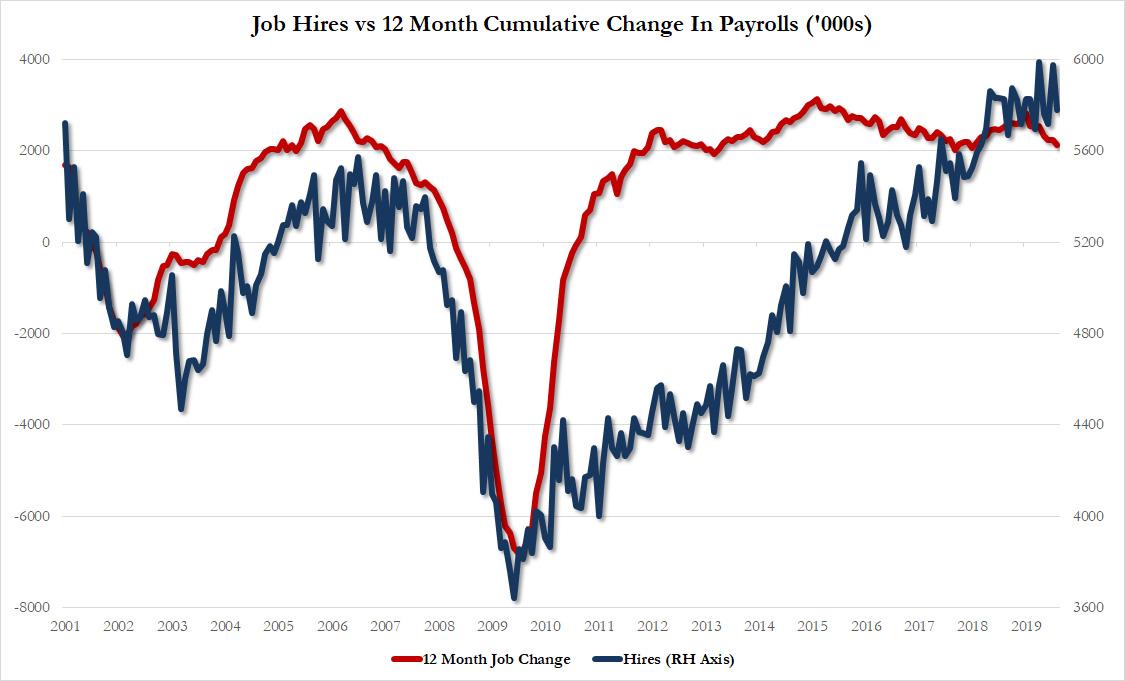

Unlike last month, though, when there was a modest improvement in the rate of hires and quits, in August the number of hires tumbled by 199K to 5.779 million, which still was modestly above where the payrolls implied number suggests:

The drop in hiring meant that from an annual expansion, hiring once again slumped into the red, dropping by -0.8% in August, down from a +2.5% increase in June.

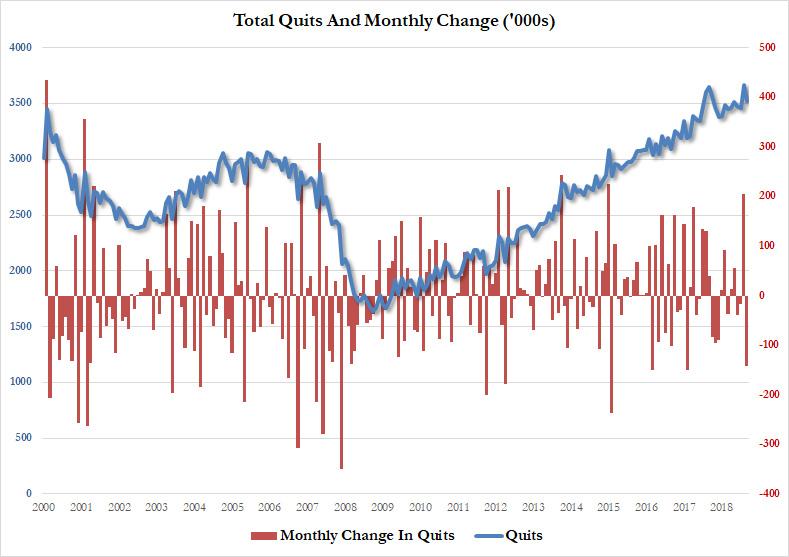

Finally, in the latest indication of the slowing labor market, we saw the so-called “take this job and shove it” indicator – the total level of “quits” which shows worker confidence that they can leave their current job and find a better paying job elsewhere – reversed from last month’s rebound, and in August the number of quits tumbled by 142K to 3.526MM from 3.668MM, and the biggest monthly drop since January.

Overall, this was the ugliest JOLTS report in more than year, which perhaps was to be expected in light of last week’s poor payrolls number.

Nasdaq Tightens The Noose On IPOs Of Small Chinese Companies

If you spoke to any research desk on Wall Street earlier this year, most were saying the trade war would be resolved by the end of summer, and stocks would hit new highs because the economy was roaring. But how the heck did so many Ivy League PhDs on Wall Street get the whole trade war and economy outlook so wrong?

We’re going, to be frank with you. The trade war is going nowhere — it’ll be around for years to come unless perhaps a new president removes the tariffs. The trade war is really about empire; the fight for the American empire is real, as China, the rising power has challenged the US, the status quo power of the world.

With that being said, one of the most significant moves currently underway is on Wall Street, perhaps forced by Washington, tightening the financial noose on China’s small businesses attempting to IPO on US exchanges.

New reports indicate Nasdaq is cracking down on IPOs of small Chinese firms by tightening the IPO approval threshold, according to m.21jingji.

The revision of listing rules has made “it more difficult in going public in the US,” said one person in charge of a Chinese financial technology company.

The company, who has been planning a $100 million IPO in the US, said the restrictions have now labeled them a small company. If they don’t raise $200 million to meet the new threshold, their IPO would likely be delayed or perhaps rejected. The company also said Nasdaq asked them to “delay” the IPO due to the high proportion of Chinese investors in the deal.

An investment bank in the US said from now on, new restrictions on small and medium-sized Chinese firms via Nasdaq would make it extremely difficult to IPO.

“This is undoubtedly worse for China’s small and medium-sized financial technology platform to go public in the US,” the banker said.

Management teams of several Chinese financial technology firms said Nasdaq’s IPO restrictions have significantly “surged” in the last several months.

Another investment banker familiar with new restrictions said the amount of small to medium-sized Chinese IPOs on Nasdaq is expected to plunge in the coming quarters.

In the last six months, there have been several US investment banks rejecting IPOs of Chinese financial technology companies.

Another banker said the new restrictions had forced Chinese companies to raise additional funds to meet new thresholds, have at least 25%-30% of the funds raised from US investors, and add US citizens to the board of directors.

The restrictions have already delayed some IPOs that have to change their capital contribution plans to meet the new rules.

IPO restrictions of Chinese firms looking to IPO on Nasdaq could shift these firms to other exchanges, like the New York Stock Exchange (NYSE). There is also reason to believe that Chinese IPO restrictions will be enforced on other US exchanges in the months ahead, if not sooner. This would likely lead an exodus of Chinese investors in the US, as they shift their listings elsewhere.

Nasdaq’s curbs on small to medium-sized Chinese firms is the latest flashpoint between souring relations of the US and China.

“Those who cannot remember the past are condemned to repeat it.” – George Santayana

Current investors must be at least 60 years old to have been of working age during a sustained bond bear market. The vast majority of investment professionals have only worked in an environment where yields generally decline and bond prices increase. For those with this perspective, the bond market has been very rewarding and seemingly risk-free and easy to trade.

Investors in Europe are buying bonds with negative yields, guaranteeing some loss of principal unless bond yields become even more negative. The U.S. Treasury 30-year bond carries a current yield to maturity of 2.00%, which implies negative real returns when adjusted for expected inflation unless yields continue to fall. From the perspective of most bond investors, yields only fall, so there’s not much of a reason for concern with the current dynamics.

We wonder how much of this complacent behavior is due to the positive experience of those investors and traders driving the bond markets. It is worth exploring how the viewpoint of a leading investor archetype(s) can influence the mindset of financial markets at large.

Millennials

The millennial generation was born between the years 1981 and 1996, putting them currently between the ages of 23 and 38. Like all generations, millennials have unique outlooks and opinions based on their life experiences.

Millennials represent less than 25% of the total U.S. population, but they are over 40% of the working-age population defined as ages 25 to 65. Millennials are quickly becoming the generation that drives consumer, economic, market, and political decision making. Older millennials are in their prime spending years and quickly moving up corporate ladders, and they are taking leading roles in government. In many cases, millennials are the dominant leaders in emerging technologies such as artificial intelligence, social media, and alternative energy.

Their rise is exaggerated due to the disproportionately large baby boomer generation that is reaching retirement age and witnessing their consumer, economic, and political impact diminishing. An additional boost to millennials’ influence is their comfort with social media and technology. They are digital natives.They created Facebook, Twitter, Snapchat, Instagram, and are the most active voices on these platforms. Their opinions are amplified like no other generation and will only get louder in the years to come.

Given millennial’s rising influence over national opinion, we examine their experiences so we can better appreciate their economic and market perspectives.

Millennial Economics

In this section, we focus on the millennial experience with recessions. It is usually these trying economic experiences that stand foremost in our memories and play an important role in forming our economic behaviors. As an extreme example, anyone alive during the Great Depression is generally fiscally conservative and not willing to take outsized risks in the markets, despite the fact that they were likely children when the Depression struck.

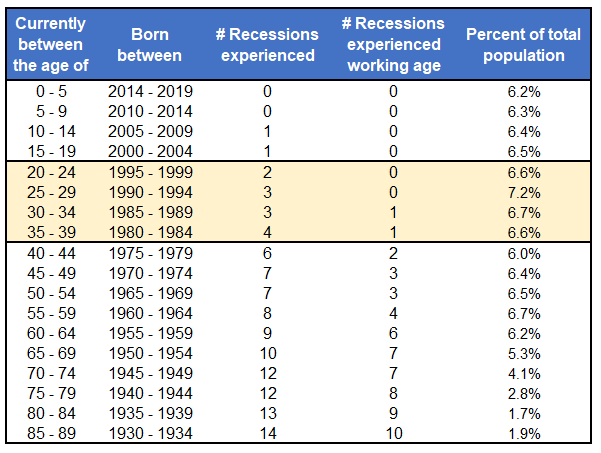

The table below shows the number of recessions experienced by population groupings and the number of recessions experienced by those groupings when they were working adults, defined as 25 or older.

Data Courtesy US Census Bureau – Millennial Generation 1981-1996

About two-thirds of the Millennials, highlighted in beige, have only experienced one recession as an adult, the financial crisis of 2008. The recession of 1990/91 occurred when the oldest millennial was nine years old. More Millennials are likely to remember the recession of 2001, but they were only between the ages of 5 and 20.

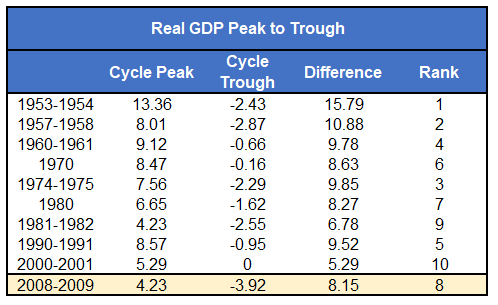

Unlike most prior recessions, the recession of 2008 was borne out of a banking and real-estate crisis. Typically, recessions occur due to an excessive buildup in inventories that cause a slowing of new orders and layoffs. While the market volatility of the Financial Crisis was disturbing, the economic decline was not as severe when viewed through the lens of peak to trough GDP decline. As shown in the table below, the difference between the cycle peak GDP growth and the cycle trough GDP growth during the most recent recession was only the eighth largest difference of the last ten recessions.

Data Courtesy St. Louis Federal Reserve

One of the reasons the 2008 experience was not more economically challenging was the massive fiscal and monetary stimulus provided by the federal government and Federal Reserve, respectively. In many ways, these actions were unprecedented. When the troubles in the banking sector were arrested, consumer and business confidence rose quickly, helping the economy and the financial markets. Although it took time for the fear to subside, it set the path for a smooth decade of uninterrupted economic growth. A decade later, with the expansion now the longest since at least the Civil War, the financial crisis is a fleeting memory for many.

The market crisis of 2008 was harsh, but it did not last long. It is largely blamed on poor banking practices and real-estate speculation issues that have been supposedly fixed. Most Millennials likely believe the experience was a black swan event not likely to be repeated. One could argue there’s a large contingent of non-millennials who feel likewise. Given the effectiveness of fiscal and monetary policy to reverse the effects of the crisis, Millennials might also believe that recessions can be avoided, or greatly curtailed.

Half of the millennial generation were teenagers during the financial crisis and have few if any, memories of the economic hardships of the era. The oldest of the Millennials were only in their early to mid-20s at the time and are not likely to be as financially scarred as older generations. In the words of Nassim Taleb, they had little skin in the game.

No one in the millennial generation has experienced a classical recession, which the Federal Reserve is not as effective at stopping. With only one recession under their belt, and minimal harm occurring as a result of their relatively young age, recession naivete is to be expected from the millennial generation.

Millennial Financial Markets

As stated earlier, the dot com bust, steep equity market decline, and the ensuing recession of 2001 occurred when the millennial generation was very young.

The financial crisis of 2008-2009 occurred when millennials were between the ages of 12 and 27. More than half of them were teenagers with little to no investing experience during the crisis. Some older Millennials may have been trading and investing, but at the time they were not very experienced, and the large majority had little money to lose.

What is likely more memorable for the vast majority of the generation is the sharp rebound in markets following the crisis and the ease in executing a passive buy and hold strategy that has worked ever since.

Millennial investors are not unlike bond traders under the age of 60 – they only know one direction, and that is up. They have been rewarded for following the herd, ignoring the warnings raised by excessive valuations, and dismissing the concerns of those that have experienced recessions and lasting market downturns.

Are they ready for 2001?

The next recession and market decline are more likely to be traditional in character, i.e. based on economic factors and not a crisis in the financial sector. Current equity valuations argue that a recession could result in a 50% or greater decline, similar to what occurred in 2008 and 2001. The difference, however, may be that the amount of time required to recover losses will be vastly different from 2008-2009. The two most comparable instances were 1929 and 2001 when valuations were as stretched as they are today. It took the S&P 500 over 20 years to recover from 1929. Likewise, the tech-laden NASDAQ needed 15 years to set new record highs after the early 2000’s dot com bust.

Those that were prepared, and had experienced numerous recessions were able to protect their wealth during the last two downturns. Some investors even prospered. Those that believed the popular narrative that prices would move onward and upward forever paid dearly.

Today, the narrative is increasingly driven by those that have never really experienced a recession or sharp market decline. Is this the perspective you should follow?

Summary

“Those who cannot remember the past are condemned to repeat it.”

We would add, “those who remember the past are more likely to avoid it.”

The millennial generation has a lot going for it, but in the case of markets and economics, it has lived in an environment coddled by monetary policy. Massive amounts of monetary stimulus have warped markets and created a dangerous mindset for those with a short time perspective.

If you fall into this camp, you may want to befriend a 60-year old bond trader, and let them explain what a bear market is.

Trump won’t comply with impeachment inquiry requests. On Tuesday, the president’s lawyer called the inquiry “partisan and unconstitutional” and told House Speaker Nancy Pelosi (D–Calif.) that the White House “cannot participate.”

In a letter to Pelosi and other Democratic leaders in the House of Representatives, Trump lawyer Pat Cipollone said he was writing on behalf of the president that the House’s impeachment inquiry “violates fundamental fairness and constitutionally mandated due process.”

For the record, impeachment is one of the rare things the U.S. Constitution explicitly gives Congress the power to do, doling out to the House “the sole power” to start impeachment inquiries and to the Senate “the sole power to try all impeachments.” It does not, however, specify what exactly this should look like.

Trump seems to think that as the House is trying to determine whether impeachment is even warranted—and before the White House answers any questions at all or submits to any information requests—he is entitled to the same rights as a defendant in a criminal trial. The letter accuses House Democrats of denying Trump “the right to cross-examine witnesses, to call witnesses, to receive transcripts of testimony, to have access to evidence, to have counsel present, and many other basic rights,” and asserts that this is one of the reasons Trump will not cooperate.

But as lawyer and national security analyst Mieke Eoyang points out, “the White House doesn’t get to tell Congress how to conduct impeachment.” Indeed, the president’s “due process rights kick in when the proceedings move to the Senate” and the trial phase of impeachment begins. Any “due process concerns raised by the WH counsel’s letter” can be negotiated at that stage.

“Impeachment in the House is akin to a grand jury & indictment,” notes Eoyang, and the House has already made allowances beyond what’s permitted for the targets of a grand jury. In a grand jury proceeding, for instance, witnesses can’t bring in personal lawyers and “the target’s counsel does not get to sit and hear the evidence.” But the House is allowing personal counsel for witnesses and letting all sides hear witness testimony. Overall, they’re “being quite fair,” tweeted Eoyang, adding:

This is all to say that the WH counsel’s screed is premature, mistakes the nature of the proceedings, and is attempting to distract from the underlying accusations of wrongdoing.

Also, WH counsel has no legal basis for what he’s arguing, and he knows it.

But reality has never stopped Trump or his staff from flinging wild accusations.

Trump’s lawyer’s letter insists “there was nothing wrong with the call” between Trump and the Ukrainian president and asserts that the impeachment inquiry is simply a ploy to “overturn the results of the 2016 election” and “influence the next election.” Declaring the impeachment inquiry “unconstitutional,” “unprecedented,” and “naked political strategy,” the letter informs House leaders that “President Trump and his Administration cannot participate” in the impeachment inquiry.

“Even for the Trump White House, this memo is breathtakingly disconnected from all law, constitutional provisions, history, and facts,” tweeted attorney and author Mike Godwin.

“my initial reaction upon reading White House Counsel Cipollone’s letter to the House is – adapting a line from the great legal scholar Tom Cruise (A Few Good Men)—to wonder whether the White House counsel was sick the day they taught law at law school.” @IlyaSomin on FB

“This is best understood as a political document,” suggests Keith Whittington at The Volokh Conspiracy (hosted at Reason):

Cipollone, on behalf of the president, has thrown down the gauntlet. The White House will not offer documents or testimony that might put the president’s or the administration’s conduct in a better light. The House can either choose to impeach the president based on what it knows or can discover without the president’s cooperation, or it can move on. The president has dared the House to impeach him, and he has now chosen to mount his defense against possible removal in the Senate and in the court of public opinion.

This sets a bad precedent, even if the House is overreacting about Ukraine.

In the event that there is not “much of a fire beneath the smoke surrounding the Ukraine matter,” that’s for the House to investigate first, the Senate to judge, and the voters to respond to on election day, writes Whittington. But “if this president can simply issue a blanket refusal to cooperate with any congressional oversight of executive branch activities, then Congress should expect that future presidents will try to build on that example.”

The White House should be warned that continued efforts to hide the truth of the President’s abuse of power from the American people will be regarded as further evidence of obstruction.

Mr. President, you are not above the law. You will be held accountable.”

BREAKING NEWS: The FBI's use of a controversial foreign surveillance tool violated Americans' constitutional privacy rights, FISA Court finds, dealing a rare rebuke to U.S. spying activities. https://t.co/Fz3kO8SuWS

FiveThirtyEighttakes a look at why the Kamala Harris campaign is faltering:

At least four 2020 candidates—Beto O’Rourke, Cory Booker, Buttigieg and Harris—have run campaigns that echo Barack Obama’s 2008 run: a youthful candidate without much Washington experience runs on charisma and personality more than a defined ideology or particular policy stands. Obama isbeloved by Democrats, and his 2008 campaign was iconic, so it’s natural that 2020 candidates would try to emulate him. But Harris, Booker, Buttigieg and O’Rourke are at 14 percent combined in national polls, suggesting that Democratic voters aren’t looking for an Obama re-run.

In some ways, Harris has the same problem that Ted Cruz and Marco Rubio had in the 2016 Republican primary, when they (wrongly) thought that the GOP would be excited about nominating a youngish, non-white standard-bearer with a solid conservative record.”

But writer Perry Bacon Jr. also offers a caveat:

It’s entirely possible that in December or January, Democrats feel like Biden is not inspiring enough but also that Sanders and Warren have taken too many left-wing positions and are risky bets in the general. In such a scenario, Harris, along with Buttigieg, are the best positioned candidates to rise.

But a lot would have to happen for Harris to pull off such a comeback. Right now, she seems more likely to finish behind Andrew Yang than to win the Democratic nomination.

Meanwhile, in poll results:

New Quinnipiac NATIONAL poll (counts for the November debate) Warren 29% Biden 26% Sanders 16% Buttigieg 4% Harris 3% Yang 3% Everyone else at or below 2 percent https://t.co/2skJmUGBSD

BREAKING: US State Dept. announces visa restrictions on Chinese government and Communist Party officials "who are believed to be responsible for, or complicit in, the detention or abuse of Uighurs, Kazakhs, or other members of Muslim minority groups in Xinjiang, China."

Trump won’t comply with impeachment inquiry requests. On Tuesday, the president’s lawyer called the inquiry “partisan and unconstitutional” and told House Speaker Nancy Pelosi (D–Calif.) that the White House “cannot participate.”

In a letter to Pelosi and other Democratic leaders in the House of Representatives, Trump lawyer Pat Cipollone said he was writing on behalf of the president that the House’s impeachment inquiry “violates fundamental fairness and constitutionally mandated due process.”

For the record, impeachment is one of the rare things the U.S. Constitution explicitly gives Congress the power to do, doling out to the House “the sole power” to start impeachment inquiries and to the Senate “the sole power to try all impeachments.” It does not, however, specify what exactly this should look like.

Trump seems to think that as the House is trying to determine whether impeachment is even warranted—and before the White House answers any questions at all or submits to any information requests—he is entitled to the same rights as a defendant in a criminal trial. The letter accuses House Democrats of denying Trump “the right to cross-examine witnesses, to call witnesses, to receive transcripts of testimony, to have access to evidence, to have counsel present, and many other basic rights,” and asserts that this is one of the reasons Trump will not cooperate.

But as lawyer and national security analyst Mieke Eoyang points out, “the White House doesn’t get to tell Congress how to conduct impeachment.” Indeed, the president’s “due process rights kick in when the proceedings move to the Senate” and the trial phase of impeachment begins. Any “due process concerns raised by the WH counsel’s letter” can be negotiated at that stage.

“Impeachment in the House is akin to a grand jury & indictment,” notes Eoyang, and the House has already made allowances beyond what’s permitted for the targets of a grand jury. In a grand jury proceeding, for instance, witnesses can’t bring in personal lawyers and “the target’s counsel does not get to sit and hear the evidence.” But the House is allowing personal counsel for witnesses and letting all sides hear witness testimony. Overall, they’re “being quite fair,” tweeted Eoyang, adding:

This is all to say that the WH counsel’s screed is premature, mistakes the nature of the proceedings, and is attempting to distract from the underlying accusations of wrongdoing.

Also, WH counsel has no legal basis for what he’s arguing, and he knows it.

But reality has never stopped Trump or his staff from flinging wild accusations.

Trump’s lawyer’s letter insists “there was nothing wrong with the call” between Trump and the Ukrainian president and asserts that the impeachment inquiry is simply a ploy to “overturn the results of the 2016 election” and “influence the next election.” Declaring the impeachment inquiry “unconstitutional,” “unprecedented,” and “naked political strategy,” the letter informs House leaders that “President Trump and his Administration cannot participate” in the impeachment inquiry.

“Even for the Trump White House, this memo is breathtakingly disconnected from all law, constitutional provisions, history, and facts,” tweeted attorney and author Mike Godwin.

“my initial reaction upon reading White House Counsel Cipollone’s letter to the House is – adapting a line from the great legal scholar Tom Cruise (A Few Good Men)—to wonder whether the White House counsel was sick the day they taught law at law school.” @IlyaSomin on FB

“This is best understood as a political document,” suggests Keith Whittington at The Volokh Conspiracy (hosted at Reason):

Cipollone, on behalf of the president, has thrown down the gauntlet. The White House will not offer documents or testimony that might put the president’s or the administration’s conduct in a better light. The House can either choose to impeach the president based on what it knows or can discover without the president’s cooperation, or it can move on. The president has dared the House to impeach him, and he has now chosen to mount his defense against possible removal in the Senate and in the court of public opinion.

This sets a bad precedent, even if the House is overreacting about Ukraine.

In the event that there is not “much of a fire beneath the smoke surrounding the Ukraine matter,” that’s for the House to investigate first, the Senate to judge, and the voters to respond to on election day, writes Whittington. But “if this president can simply issue a blanket refusal to cooperate with any congressional oversight of executive branch activities, then Congress should expect that future presidents will try to build on that example.”

The White House should be warned that continued efforts to hide the truth of the President’s abuse of power from the American people will be regarded as further evidence of obstruction.

Mr. President, you are not above the law. You will be held accountable.”

BREAKING NEWS: The FBI's use of a controversial foreign surveillance tool violated Americans' constitutional privacy rights, FISA Court finds, dealing a rare rebuke to U.S. spying activities. https://t.co/Fz3kO8SuWS

FiveThirtyEighttakes a look at why the Kamala Harris campaign is faltering:

At least four 2020 candidates—Beto O’Rourke, Cory Booker, Buttigieg and Harris—have run campaigns that echo Barack Obama’s 2008 run: a youthful candidate without much Washington experience runs on charisma and personality more than a defined ideology or particular policy stands. Obama isbeloved by Democrats, and his 2008 campaign was iconic, so it’s natural that 2020 candidates would try to emulate him. But Harris, Booker, Buttigieg and O’Rourke are at 14 percent combined in national polls, suggesting that Democratic voters aren’t looking for an Obama re-run.

In some ways, Harris has the same problem that Ted Cruz and Marco Rubio had in the 2016 Republican primary, when they (wrongly) thought that the GOP would be excited about nominating a youngish, non-white standard-bearer with a solid conservative record.”

But writer Perry Bacon Jr. also offers a caveat:

It’s entirely possible that in December or January, Democrats feel like Biden is not inspiring enough but also that Sanders and Warren have taken too many left-wing positions and are risky bets in the general. In such a scenario, Harris, along with Buttigieg, are the best positioned candidates to rise.

But a lot would have to happen for Harris to pull off such a comeback. Right now, she seems more likely to finish behind Andrew Yang than to win the Democratic nomination.

Meanwhile, in poll results:

New Quinnipiac NATIONAL poll (counts for the November debate) Warren 29% Biden 26% Sanders 16% Buttigieg 4% Harris 3% Yang 3% Everyone else at or below 2 percent https://t.co/2skJmUGBSD

BREAKING: US State Dept. announces visa restrictions on Chinese government and Communist Party officials "who are believed to be responsible for, or complicit in, the detention or abuse of Uighurs, Kazakhs, or other members of Muslim minority groups in Xinjiang, China."

American Airlines Joins Southwest In Abandoning Hope 737 MAX Will Fly Again This Year

Even as Boeing still tells anyone who will listen that it is confident the infamous 737 MAX plane will fly again this year, its biggest clients are giving up hope, and earlier today American Airlines abandoned expectations it would resume flights with the Boeing Co. 737 Max this year, pulling the troubled plane from the carrier’s schedule beyond the end of 2019, at least through January 15, 2020.

As Bloomberg notes, the world‘s largest airline, which previously removed the aircraft through Dec. 3, is canceling 140 flights per day as its two dozen Max jets remain grounded indefinitely. With its announcement that it won’t fly a 737MAX until 2020 at the earliest, American follows Southwest Airlines which in July said that it wouldn’t fly the plane before Jan. 6. Southwest is the largest Max operator, with 34.

United Airlines remains the major outlier, and still has the Max set to return to its schedule on Dec. 19, while Air Canada has removed the plane until Jan. 8.

The narrow-body aircraft was grounded by authorities worldwide in March after crashes at Lion Air and Ethiopian Airlines killed 346 people. Boeing has targeted this quarter for the plane’s return, but the new software and other changes meant to avoid a repeat of the disastrous malfunctions first must be approved by regulators.

Once flights are allowed to resume, it is unclear what happens next: while carriers will need weeks or even months to train pilots and prepare stored aircraft for service, it still remains unclear if the general public will be willing to fly in a plane which we have now learned was manufactured with the explicit goal of minimizing cost even at the expense of passenger safety.

American said it expects to phase in the Max slowly and will increase flights throughout January and into February. In July, the company forecast a $400 million drag on this year’s pretax earnings from the Max’s grounding; the final number will likely be far greater.

From Baumgarten v. EOTFR, a California Superior Court libel sued filed last Friday:

On or around August 15, 2019, defendant Ballard insinuated that Baumgarten had defecated on the bathroom floor of the New York office and interrogated Baumgarten about the defecation incident in the restroom in front of Santos. Defendant Ballard insinuated Baumgarten was responsible for the defecation because the defecation was reported after Baumgarten used the restroom. Later, word spread throughout the ICM offices that attributed Baumgarten to the defecation incident, and then subsequently, outside of ICM, including to other agencies and major studios.

Defendant Ballard wrongfully accused Baumgarten of these outrageous allegat[ions] knowing that once she leaked the mere subject matter that Baumgarten would be terminated and his reputation would be eviscerated.

Defendant ICM has a pattern and practice of defaming employees that they target and want to separate from the company, in order to ensure that the employee’s reputation

in the industry is tarnished so that they will be unable to compete with Defendant ICM. Defendant ICM defames such employees in front of other company employees, the press, competitors and others in the entertainment community. There have been dozens of employees who have been subjected to this treatment….

Recall that this is just the plaintiff’s side of the story; see the article in the Hollywood Reporter (Rebecca Sun) for more. Thanks to Glen Whitman for the pointer.

from Latest – Reason.com https://ift.tt/2MtmjfI

via IFTTT

China Takes Aim At Apple For “Betraying The Feelings Of The Chinese People”

It’s only a matter of time before the Chinese Communist Party punishes Apple as the trade war escalates. Late Tuesday night, China’s official newspaper, the People’s Daily, criticized Apple for allowing an app on its app store that tracks the movement of the Hong Kong Police Force.

Apple has “betrayed the feelings of the Chinese people” by approving the app HKmap.live, which crowdsources real-time locations of police in Hong Kong.

The People’s Daily said Apple shouldn’t provide apps for people conducting illegal activity, and it also questioned whether the US technology company was “thinking clearly.”

“The developers of the map app had not hidden their malicious motive in providing ‘navigation’ for the rioters,” The People’s Daily wrote. “Apple chose to approve the app in the App Store in Hong Kong at this point. Does this mean Apple intended to be an accomplice to the rioters?”

The newspaper also slammed Apple for promoting “Hong Kong independence” music in the Apple Music Store.

Apple is the latest US company to stumble into the firing line of the Chinese government in relation to supporting the protestors in Hong Kong.

On Tuesday, China’s state broadcaster, CCTV, canceled broadcasts of NBA games in China after Daryl Morey tweeted (then swiftly deleted) a message of support for the Hong Kong protesters.

The political crisis intensified last weekend when protestors took to the streets on Saturday and Sunday in another round of violent clashes with police.

Hong Kong Apple removed HKmap.live last Wednesday. A message on the app told users: “Your app contains content — or facilitates, enables, and encourages an activity — that is not legal . . . Specifically, the app allowed users to evade law enforcement.”

Several days later, right before weekend protests flared up, Apple reapproved the app on Friday.

Apple’s resistance against China’s demands to stop aiding protestors will get it in trouble. As the US blacklists top Chinese technology firms on Tuesday and imposed visa restrictions on Chinese government officials, China could likely strike back at Apple.

Apple shares are higher in the pre-market, but there are some oddly negative prints coming through…

From Baumgarten v. EOTFR, a California Superior Court libel sued filed last Friday:

On or around August 15, 2019, defendant Ballard insinuated that Baumgarten had defecated on the bathroom floor of the New York office and interrogated Baumgarten about the defecation incident in the restroom in front of Santos. Defendant Ballard insinuated Baumgarten was responsible for the defecation because the defecation was reported after Baumgarten used the restroom. Later, word spread throughout the ICM offices that attributed Baumgarten to the defecation incident, and then subsequently, outside of ICM, including to other agencies and major studios.

Defendant Ballard wrongfully accused Baumgarten of these outrageous allegat[ions] knowing that once she leaked the mere subject matter that Baumgarten would be terminated and his reputation would be eviscerated.

Defendant ICM has a pattern and practice of defaming employees that they target and want to separate from the company, in order to ensure that the employee’s reputation

in the industry is tarnished so that they will be unable to compete with Defendant ICM. Defendant ICM defames such employees in front of other company employees, the press, competitors and others in the entertainment community. There have been dozens of employees who have been subjected to this treatment….

Recall that this is just the plaintiff’s side of the story; see the article in the Hollywood Reporter (Rebecca Sun) for more. Thanks to Glen Whitman for the pointer.

from Latest – Reason.com https://ift.tt/2MtmjfI

via IFTTT

Fed Takes $31 Billion Securities In Overnight Repo As “Not A QE” Looms

The NY Fed announced that it accepted $30.8BN in securities ($26.25BN in TSYs and $4.550BN in MBS) in its latest overnight repo operation, shortly after the latest overnight G/C repo rate printed at an “unstressed” 1.90% this morning.

This was down from Tuesday’s $37.5BN and was the lowest repo allotment since Sept 27.

Of course, after Tuesday’s speech in which Powell preannounced the return of POMOs, confirming that these “temporary” operations are set to become “not temporary” as the Fed grows permanently grows its balance sheet by purchases of Treasurys, reportedly Bills at first, the overnight POMO has now become just a placeholder until November when the new “not a QE” is set to begin and expand the Fed’s balance sheet by about $20BN in 10 Year equivalents every month.

As such, predictably the stress in the repo market is now effectively gone and the only question is what the final framework of the new POMO will look like, and specifically what the Fed will announce how many Treasuries the Fed will have to buy.

But wait, didn’t Powell say not to confuse what is coming with QE? Alas, as we first explained and then as Capital Economics confirmed, the Federal Reserve “will struggle to convince markets that a resumption of Treasury purchases to avoid future money-market turmoil is not another round of quantitative easing” according to Capital Economics chief U.S. economist Paul Ashworth: “Hard to communicate that effectively when the Fed’s organic balance sheet growth will be half the size of the ECB’s newly unveiled QE,” Ashworth wrote in note Tuesday

According to CapEcon, the Fed will need to buy $120b of additional Treasury securities per year to prevent any further decline in reserve balances. On top of that, Fed could also buy another $100b-$300b of Treasury securities in first year, to avoid mismatch of demand/supply in repo market like mid-September’s.

So yes, just as we first had “not a flamethrower” which was, for all intents and purposes, a flamethrower, we now have “not a QE”, which is, for all intents and purposes, QE.

Alas, in this “brave new world” where one is no longer allowed to call a spade a spade (especially if it risks jeopardizing Chinese investments, right NBA?), what one has to remember is that the return of QE is anything but. No matter what one calls it however, the Fed’s overnight repo no longer matters as the turmoil in the funding market has been stabilized for now, and certainly until POMO returns. The bigger problem is if we still have repo turmoil after “not a QE” is back. In that case, all bets will officially be off as the Fed loses its last shred of credibility.