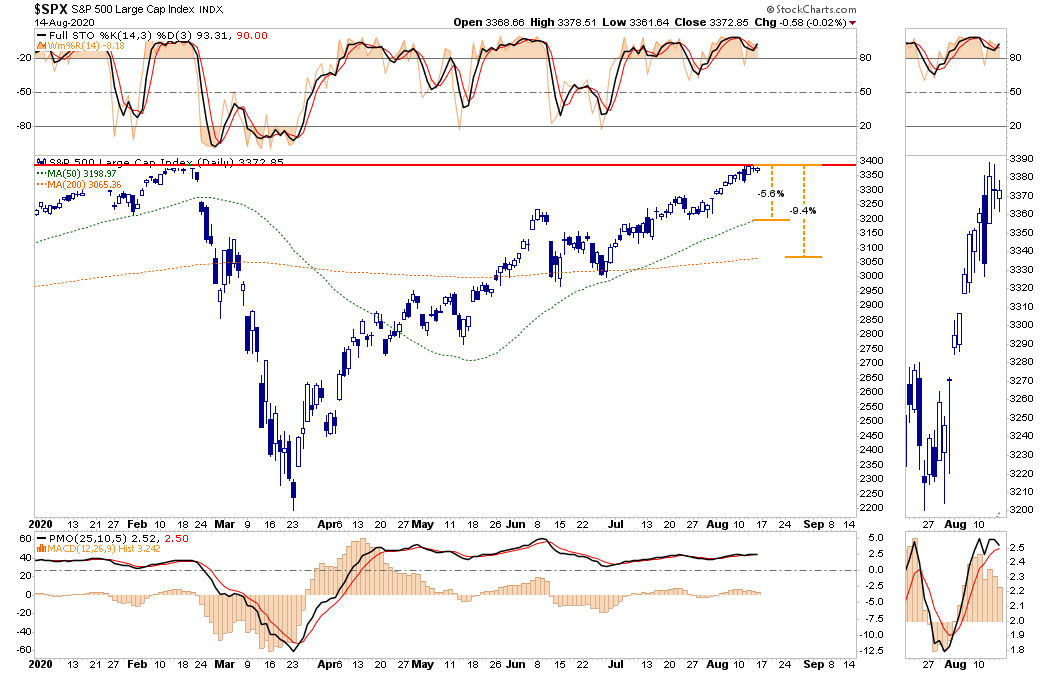

As discussed last week in “Bulls Chant,” the markets pushed toward all-time highs:

“While weaker economic data has not yet dented the “bullish sentiment” at this juncture, it doesn’t mean it won’t. However, as we have discussed over the last several weeks, a breakout of the consolidation range, which was capped by the June highs, would put all-time highs into focus.”

This week, despite repeated attempts, the bulls were unable to close above all-time highs solidly. As they say, “it was close, but no cigar.”

With options expiring next week, the bulls are going to attempt to push markets up. A breakout to all-time highs is entirely possible. However, the question is whether they will be able to maintain it?

A Normal Correction Is Likely

With the markets overbought on several measures, there is a downside risk heading into the end of the month. These risks come from several fronts we will discuss momentarily. However, from a technical perspective, the downside risk is about 5.6% to the 50-dma and 9.4% to the 200-dma. (Shown above)

A 5-10% decline in any given year is not outside of the norm. However, since investors have entirely forgotten what a drop feels like, a 5-10% slide will “feel” worse than it is.

As I stated, the market is overbought on multiple measures, which have typically coincided with short-term market peaks and corrections. With the S&P now trading more than 9% above the 200-dma, and all indicators back to overbought conditions, it is worth wary of potential short-term correction risks.

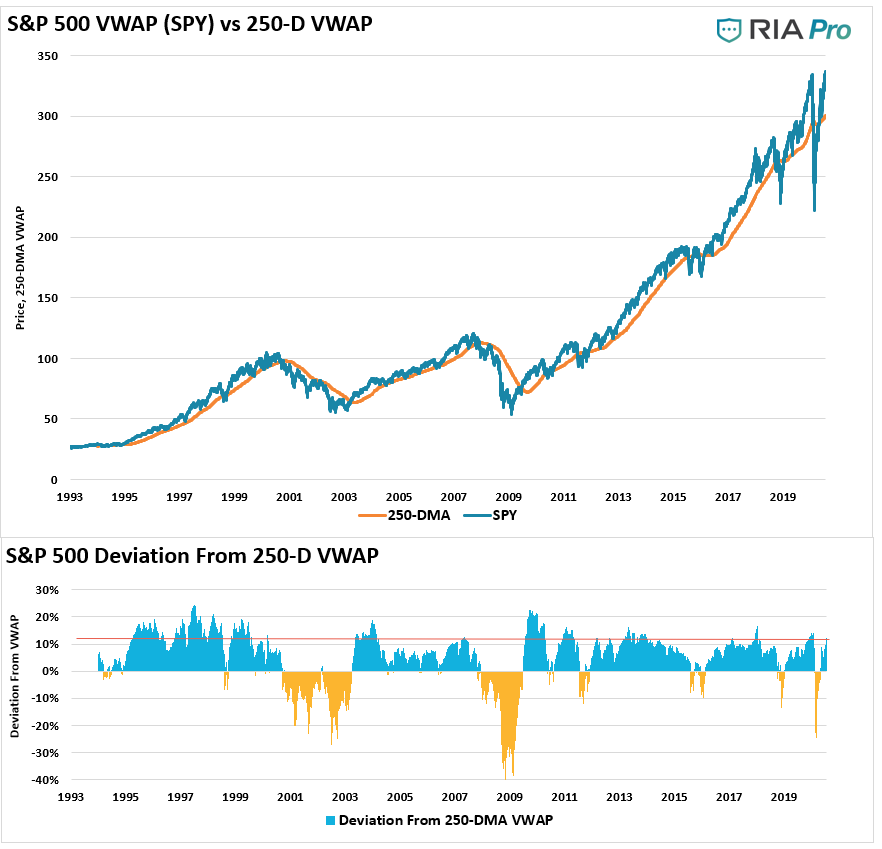

Another way to look at deviations is where the S&P 500 ETF (SPY) trades relative to its 250-day volume-weighted average price (VWAP.) While deviations have been more extreme in the past, this is currently the highest level since February.

All this indicator suggests it there is “fuel” for a correction in the markets short-term. What is needed, of course, is a “catalyst” to ignite sellers.

That is where our discussion of the “Income Cliff” comes in.

The Income Cliff

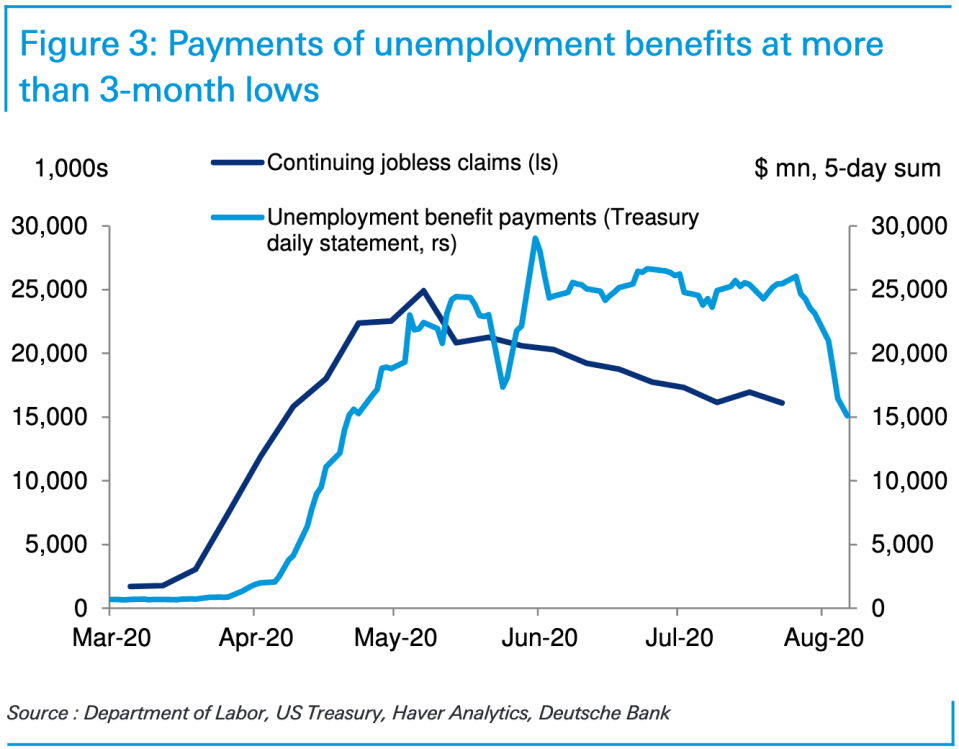

One of the significant risks facing the market over the next couple of months is the “income cliff” as extended unemployment benefits run dry.

“Last month, we argued that rapid and robust fiscal stimulus was a critical driver of the initial V-shaped recovery in consumer spending. Therefore, several benefits cliffs could endanger this momentum as the removal of government support was premature.

The evaporation of these benefits highlights near-term downside risks to consumer spending, particularly for lower-income households, which have been a critical engine of the recovery despite being disproportionately more likely to lose a job during the pandemic — a testament to the effectiveness of the income supplement.” – Matt Luzzetti, chief U.S. economist at Deutsche Bank.

While the White House announced last week it would take executive action to reallocate unused dollars from the CARES Act to supplement existing unemployment programs, there remain challenges. At this point, there are no additional $1200 checks going to households, and as shown below, other benefits are plunging.

The initial rebound in retail sales, and much of the economic data, came from $1200 checks and $600/week in additional benefits. With Congress now heading off to summer recess, and the pre-election rhetoric about to begin, there is a risk of delay in any additional relief. Importantly, even if the passage of additional relief occurs, it will be less than previous amounts, which will slow any economic recovery.

Since sales are what drives corporate earnings, you can see the stock market’s issue over the next few quarters.

While watching the “income cliff” carefully, my colleague Doug Kass lays out 10-other risks, which could also provide the catalyst for a correction.

10-Other Factors That Could Spark A Correction

“My view is that the period leading up to the November election holds a list of unique and potentially worrisome risks:

Fundamentals Remain Too Optimistic.

Technical Deterioration. Market breadth and new highs (only 59 yesterday), investor sentiment is growing ebullient (put/call ratios at a multi-month lows), the National Association of Active Investment Managers (NAAIM) has its highest long exposure in years at 102.4.

Covid-19 Remains A Wildcard. Currently, the virus continues to spread, and fatalities are expanding. Travel restrictions are tightening, schools and universities closing or have a reduced schedule, and small business openings remain uncertain. The recent fragile rise in consumer and business confidence could be fleeting.

Speculation Is Beginning to Moderate. Losses in the “shiny objects” may now be accumulating.

The China/U.S. Rift Is Widening. China will likely play hardball in the face of a potential change of the Presidency.

For a Host of Reasons, Our Society is Fractured. An intensification of violence could shake confidence as social issues become more heated, leading into the November election.

The Social Safety Net Is Beginning to Fade. Federal unemployment benefits are getting extended but only a fraction of the $600. PPP is expiring in early August and is not being replaced or at a fraction of the previous level.

Market Structure Remains a Significant Risk. The intoxicating advance since March could easily move into reverse. “buyers live higher, but sellers live lower.”

A Democratic Sweep Will Result in More Distributional Policies.

Higher individual and corporate tax rates, a possible wealth tax, and potential threats to the tech market leaders’ monopolistic positions could undermine growth.

There Are Numerous Knock On Problems That Could Reverberate in Our Economic and Markets Systems. Let’s call this the “unknowable”.

Sitting Closer To The Exit

Point 10 in Doug’s list is the most critical.

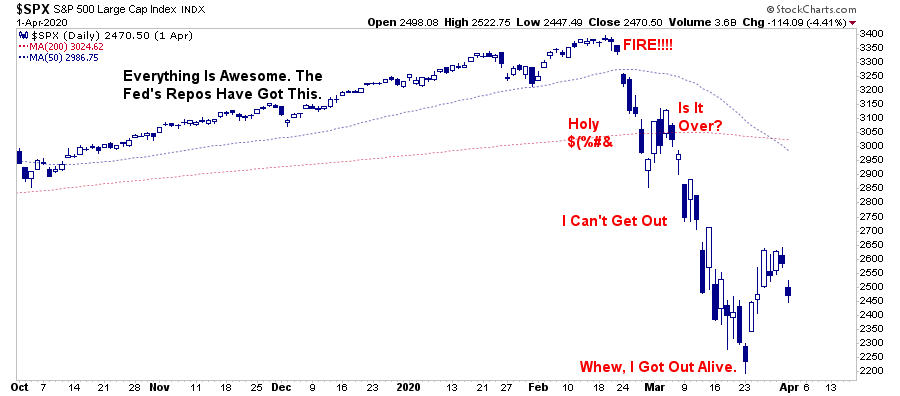

What eventually sparks a reversion is always the one thing no one is anticipating. Throughout history, the unexpected, exogenous event is what sends investors fleeing for the exits. After the damage occurs, the media’s excuse is always: “Well, no one could have seen that coming.”

As noted above, overbought, extended, overly bullish markets are by themselves “bullish.” These conditions represent the current “momentum,” which keeps pushing assets higher and dragging investors into the market.

It’s very much like a crowded theater. Everything is fine, until that point where someone yells “fire.”At that point, everyone tries to rush towards a very narrow exit. The same holds for the market.

“At some point, that reversion process will take hold. It is then investor ‘psychology’ will collide with ‘margin debt’ and ETF liquidity.

When the ‘robot trading algorithms’ begin to reverse, it will not be a slow and methodical process but rather a stampede with little regard to price, valuation n or fundamental measures. The exit will become very narrow.

Importantly, as prices decline, it will trigger margin calls, which will induce more indiscriminate selling. The forced redemption cycle will cause catastrophic spreads between the current bid and ask pricing for ETF’s. Such forces investors to dump positions to meet margin calls, the lack of buyers will form a vacuum causing rapid price declines. Such leaves investors helpless on the sidelines watching capital appreciation vanish in moments.”

No one believed me then. But it is what happened in March of 2020.

Hedging Risk

For all of these reasons, this is why we are sitting closer to exit.

Retail investors have packed themselves into the same theater under the belief that asset prices can only go higher. As noted, numerous things could spark a “fire.”

Furthermore, over the last couple of weeks, our portfolios remain weighted towards equity risk. Such makes us very uncomfortable, as “risk” controls are the backbone of our process.

Such remains the case this week.

Given we are now getting more extreme short-term overbought conditions, the risk of a short-term reversion has risen. Therefore, we continued making changes to portfolios last week.

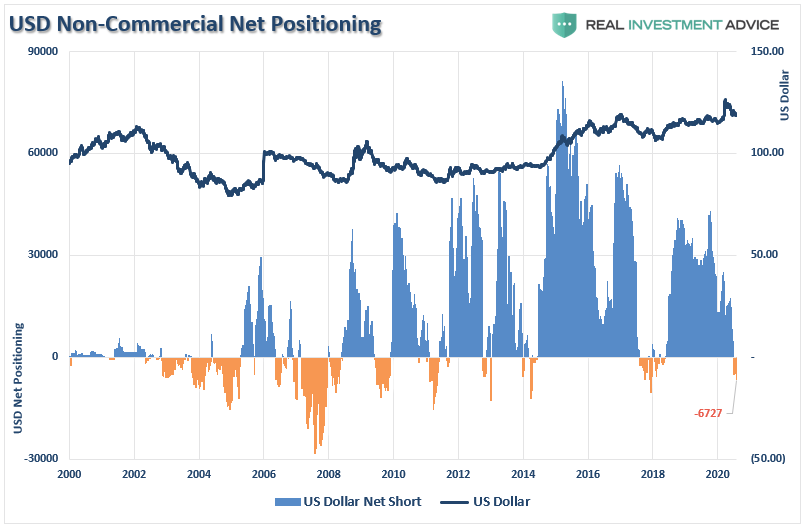

As noted previously in our “Commitment of Traders” report, the rather large short position in the US Dollar is a sign to hedge our dollar-based exposures (stocks, gold, and energy.) Therefore, we have been building a long-dollar position over the last two weeks and added to it again on Friday.

Furthermore, we added to our bond holdings, given the more extreme oversold condition. Just in case there is a correction, bonds should act as a hedge.

We are also beginning to add additional “value” positions to the portfolio. These positions carry high yields, have “fundamental value,” and have less downside currently. When the market begins to rotate towards safety, “value” may be a benefactor.

Consequently, the time has come to be more conservative in portfolios, even at the expense of short-term performance. When there is a more evident opportunity to take on risk, we will undoubtedly do so aggressively.

Sometimes, when you don’t know what to do, the best thing to do is not play.

via ZeroHedge News https://ift.tt/2Y4hrEk Tyler Durden

Mark Meadows And CNN’s Jake Tapper Clash In Heated Debate Over Mail-In Voting Tyler Durden

Sun, 08/16/2020 – 12:00

White House Chief of Staff Mark Meadows and CNN‘s Jake Tapper argued for more than 20 minutes on Sunday over a wide range of issues – including mail-in voting, with Meadows insisting that states which are sending ‘millions of ballots’ to registered voters is “just asking for a disaster.”

Via Axios:

MEADOWS: The problem that we have here is that a lot of people are looking at just sending out ballots. California is sending out ballots. When they just send out ballots, my home state of North Carolina —

TAPPER: California already did that for about 75% of its population. Now it’s 100%. But Utah has done it for years. Oregon has done it for years. Washington has done it for years. Now there are four states that are adding to the sending out ballots to every registered voter. I understand that that’s a concern that you’re claiming.

MEADOWS: “Isn’t it a concern to you? Do you realize how inaccurate the voter rolls are with just people just moving around? Let alone the people that die off. But sending ballots out based on a voter roll registration? Any time you move, you change your driver’s license but you don’t call up and say, by the way, I’m reregistering for — “

TAPPER: “But there’s no evidence of widespread voter fraud. “

MEADOWS: “There’s no evidence that there’s not either. That’s the definition of fraud, Jake.”

CNN’s @jaketapper: “There is no evidence of widespread voter fraud.”

Meadows said that reports of mail sorting machines being taken offline between now and the November election are “something that my Democrat friends are trying to do to stoke fear out there,” and a “political narrative by my Democrat colleagues.”

Tapper pushed back, saying “are you saying that sorting machines have not been taken offline and removed?” to which Meadows replied “Sorting machines between now and the election will not be taken offline.”

When asked if he thought Sen. Kamala Harris was eligibile to run for office due to her parents being non-US citizens when she was born in Oakland – which was recently questioned by Newsweek, Meadows said “sure,” noting “Jake – you and a number the media, y’all have spent more time on it than anybody in the White House has talking about this,” adding “I’m more concerned with Kamala Harris’s liberal ideas coming from San Francisco to the rest of America.”

White House chief of staff Mark Meadows says he accepts that Sen. Kamala Harris is eligible to be vice president. #CNNSOTUpic.twitter.com/kLcjgP4lYi

Over the last few months, it has been virtually impossible to do in-person speaking engagements. However, I have done quite a few online, and have more scheduled over the next few months. Here are videos of recent online talks I gave about my book Free to Move: Foot Voting, Migration and Political Freedom for the Cato Institute (with commentary by economist Bryan Caplan and immigration law scholar Peter Margulies), and the University of Torcuato Di Tella law faculty Seminar on Law, Economics, and Regulation (Argentina). Below is a list of all currently scheduled talks from now through the end of the year.

If you are a student, faculty, member or otherwise affiliated with one of the host institutions, you should be able to get information from them on how to sign on to listen to these talks. Some may also allow members of the general public to listen and ask questions. In some cases, there will also be video posted online.

And if you would like to invite me to give a “virtual” talk about any of my areas of expertise (described in more detail at my website here) at your own university, think thank, or other similar organization, please feel free to contact me! Virtual speaking events have some disadvantages relative to in-person ones. But they do have the benefit of being easier and cheaper to set up. If the talk is about one of my books, the organizer will get a free copy, and it might be possible to provide discount copies for at least some audience members.

Most of the talks below are about my new book Free to Move. But I’m more than happy to speak about other topics, as well.

September 14, 4-5:30 PM, Case Western Reserve University School of Law: “Immigration and the Constitution,” Constitution Day Conference.

September 15, 5-6 PM, Miller Center of Public Affairs, University of Virginia, Charlottesville, VA: “Free to Move: Foot Voting, Migration, and Political Freedom”

September 22, University of Calgary, Calgary, Alberta, Time TBD: “Free to Move: Foot Voting Migration and Political Freedom” (this event is still tentative)

September 24, University of Alberta, Edmonton, Alberta, Time TBD: “Free to Move: Foot Voting Migration, and Political Freedom.”

September 29, noon-1:30 (approximate time), Yale Law School, New Haven, CT: “Free to Move: Foot Voting, Migration and Political Freedom” (with commentary and moderation by Yale Law School Dean Heather Gerken). Sponsored by Yale Federalist Society.

October 6, noon-1:30 (approximate time), Duke Law School, Durham, NC: “Free to Move: Foot Voting, Migration and Political Freedom” (with commentary by Duke law Prof. Guy Charles). Sponsored by Duke Federalist Society.

October 8, Time TBD, Sandra Day O’Connor College of Law, Arizona State University, Tempe, AZ: “The Free Market Conservative Case for Open Borders Immigration” (tentative title). Sponsored by the Arizona State Federalist Society

Date TBD, Harvard Kennedy School of Government, Cambridge, MA: “Free to Move: Foot Voting, Migration, and Political Freedom” (moderated by Harvard economics Prof. Edward Glaeser). Co-sponsored by the Taubman Center for State and Local Government and the Rappaport Center for Greater Boston.

Date TBD, Georgia State University, Atlanta, GA: “The Case for Foot Voting” (tentative title). With commentary by Prof. Michael Evans.

I will update this post regularly, over the next few weeks, as additional information about speaking engagements comes in.

from Latest – Reason.com https://ift.tt/3iIwg7F

via IFTTT

Over the last few months, it has been virtually impossible to do in-person speaking engagements. However, I have done quite a few online, and have more scheduled over the next few months. Here are videos of recent online talks I gave about my book Free to Move: Foot Voting, Migration and Political Freedom for the Cato Institute (with commentary by economist Bryan Caplan and immigration law scholar Peter Margulies), and the University of Torcuato Di Tella law faculty Seminar on Law, Economics, and Regulation (Argentina). Below is a list of all currently scheduled talks from now through the end of the year.

If you are a student, faculty, member or otherwise affiliated with one of the host institutions, you should be able to get information from them on how to sign on to listen to these talks. Some may also allow members of the general public to listen and ask questions. In some cases, there will also be video posted online.

And if you would like to invite me to give a “virtual” talk about any of my areas of expertise (described in more detail at my website here) at your own university, think thank, or other similar organization, please feel free to contact me! Virtual speaking events have some disadvantages relative to in-person ones. But they do have the benefit of being easier and cheaper to set up. If the talk is about one of my books, the organizer will get a free copy, and it might be possible to provide discount copies for at least some audience members.

Most of the talks below are about my new book Free to Move. But I’m more than happy to speak about other topics, as well.

September 14, 4-5:30 PM, Case Western Reserve University School of Law: “Immigration and the Constitution,” Constitution Day Conference.

September 15, 5-6 PM, Miller Center of Public Affairs, University of Virginia, Charlottesville, VA: “Free to Move: Foot Voting, Migration, and Political Freedom”

September 22, University of Calgary, Calgary, Alberta, Time TBD: “Free to Move: Foot Voting Migration and Political Freedom” (this event is still tentative)

September 24, University of Alberta, Edmonton, Alberta, Time TBD: “Free to Move: Foot Voting Migration, and Political Freedom.”

September 29, noon-1:30 (approximate time), Yale Law School, New Haven, CT: “Free to Move: Foot Voting, Migration and Political Freedom” (with commentary and moderation by Yale Law School Dean Heather Gerken). Sponsored by Yale Federalist Society.

October 6, noon-1:30 (approximate time), Duke Law School, Durham, NC: “Free to Move: Foot Voting, Migration and Political Freedom” (with commentary by Duke law Prof. Guy Charles). Sponsored by Duke Federalist Society.

October 8, Time TBD, Sandra Day O’Connor College of Law, Arizona State University, Tempe, AZ: “The Free Market Conservative Case for Open Borders Immigration” (tentative title). Sponsored by the Arizona State Federalist Society

Date TBD, Harvard Kennedy School of Government, Cambridge, MA: “Free to Move: Foot Voting, Migration, and Political Freedom” (moderated by Harvard economics Prof. Edward Glaeser). Co-sponsored by the Taubman Center for State and Local Government and the Rappaport Center for Greater Boston.

Date TBD, Georgia State University, Atlanta, GA: “The Case for Foot Voting” (tentative title). With commentary by Prof. Michael Evans.

I will update this post regularly, over the next few weeks, as additional information about speaking engagements comes in.

from Latest – Reason.com https://ift.tt/3iIwg7F

via IFTTT

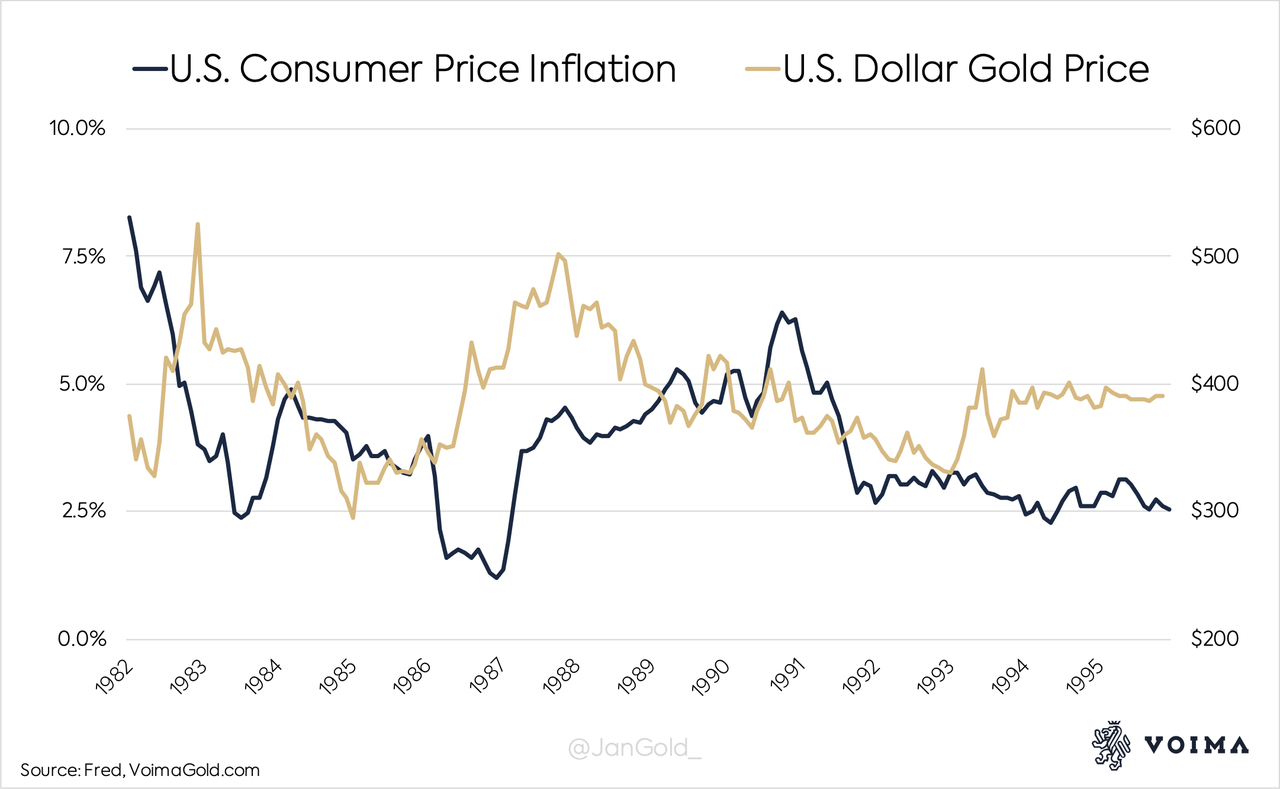

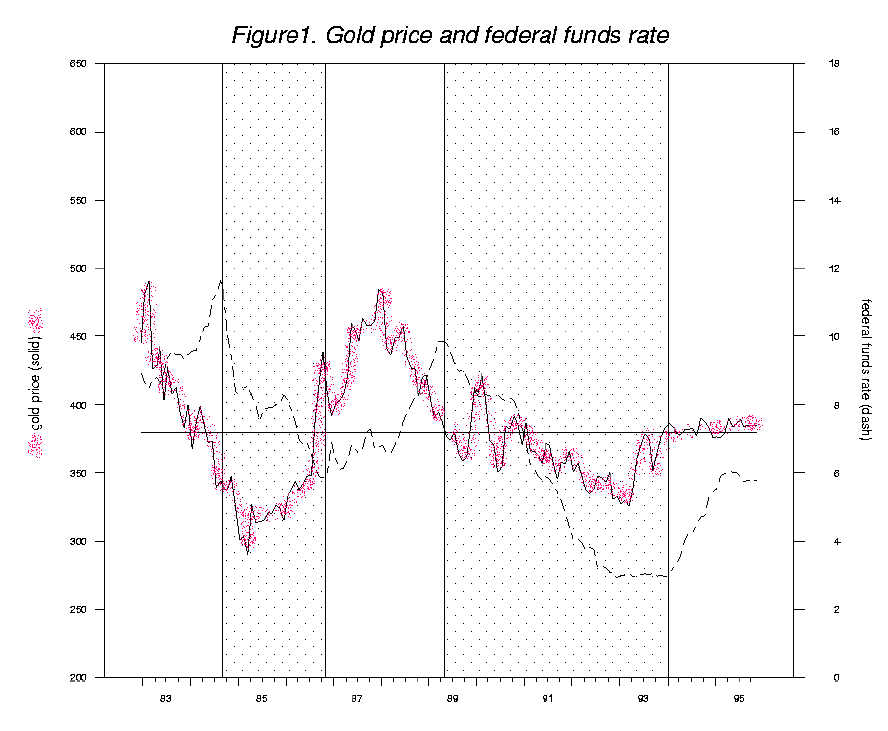

An academic study published in 1996 shows evidence that the Federal Reserve was influencing the price of gold over the observed period. The Fed used one of its main interest rate tools, the federal funds rate, to stabilize both the gold price and consumer price inflation.

The ones that think gold hasn’t played a significant role in economics in the past decades, might want to reconsider their assumption. Until this day gold has been pivotal in international economics—although since 1971 different phases can be identified. In today’s article we will focus on the period from 1982 until 1995 with respect to U.S. monetary policy and the price of gold.

The Gold Price and Inflation Expectations

In the early 1990s it appeared that the Federal Reserve was tracking the gold price to get a sense of inflation expectations. On February 22, 1994, the Chairman of the Fed, Alan Greenspan, testified for the semiannual monetary policy report to Congress. He began by explaining that low consumer price inflation was key to long-term growth and low unemployment. From Greenspan (emphasis mine):

Lower inflation and inflation expectations reduce uncertainty in economic planning and diminish risk premiums for capital investment.

It follows that price stability, with inflation expectations essentially negligible, should be a long-run goal of macroeconomic policy.

The Fed’s aim was to subdue inflation and therefore inflation expectations, because the latter is what feeds into inflation. When people expect inflation to rise there will be a flight from fiat currency, which leads to higher inflation.

Greenspan elaborated that inflation data, such as the consumer price index (CPI), could only be known with a significant lag. And for monetary policy to affect inflation, an additional lag is added to the process. The full cycle to tame inflation could take a year or more. Ideally, the Fed had a real-time indicator of inflation expectations. In his testimony, Greenspan mentioned gold as “especially sensitive to inflation concerns,” which, next to other indicators, “can give important clues about changing [inflation] expectations.”

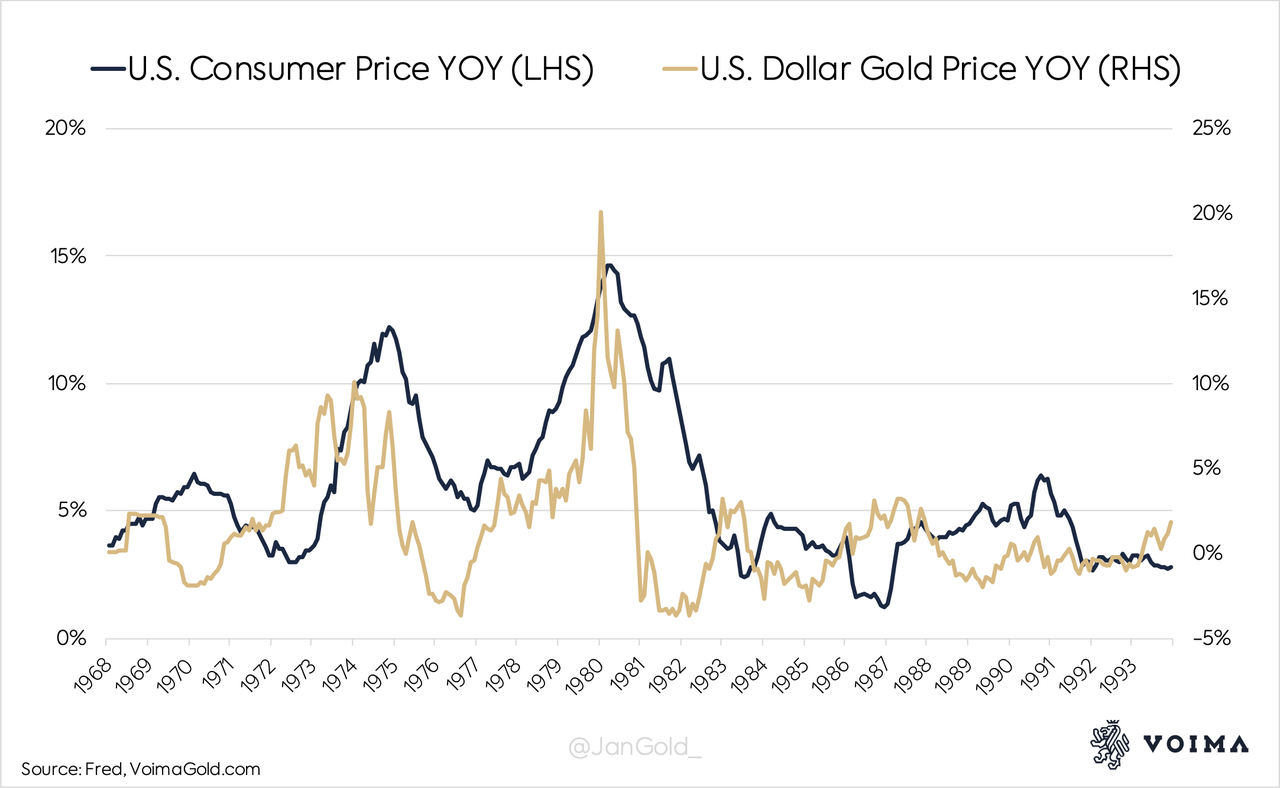

Greenspan’s analysis was probably based on the data displayed in the chart below. We can see that in 1968, 1970, 1976, 1982, and 1985, an increase in the gold price preceded an uptick in inflation. Hence, gold price movements could (and still can) be used as an indicator of inflation expectations.

Greenspan stated that in 1970s the Fed failed to timely respond to inflation. He said that during his tenure, which started in 1987, an information base that included gold, made the Fed adjust the federal funds rate to adequately react to inflation expectations. Reacting to early inflation concerns, was effective for targeting inflation itself.

To a question from Congressman LaFalce regarding gold, Greenspan replied:

I think that what the price of gold reflects is a basic view of the desire to hold real hard assets versus currencies. … [Gold] is a store of value measure which has shown a fairly consistent lead on inflation expectations and has been over the years a reasonably good indicator, among others, of what inflation expectations are doing. It does this better than commodity prices or a lot of other things.

Enter George Selgin and Bill Lastrapes

My guess is that Greenspan’s testimony in 1994 made the economists George Selgin and William D. Lastrapes, wonder for how long and to what extent the Fed was conducting monetary policy based on the price of gold. In 1996, they published a paper on the subject titled “The Price of Gold and Monetary Policy.”

In their study, Selgin & Lastrapes examined the co-movement of gold prices and the fed funds rate, and scanned the minutes form Federal Open Market Committee (FOMC) meetings. (They also used an econometric model, but for the sake of simplicity I will leave that out.) The paper concludes: “Our evidence … supports the claim that gold has played an independent role in formulating monetary policy.”

Let’s start with what Selgin & Lastrapes call anecdotal evidence from the FOMC minutes. At the May 18, 1993, meeting of the FOMC, the significance of movements in “sensitive commodity prices” were discussed (emphasis mine):

[T]he potential for a sustained increase in the rate of inflation could not be dismissed…. Indeed, in one view sensitive commodity prices and other key measures of inflation already indicated the need for a prompt move toward restraint….

In addition to new information on prices and costs, such signs could include developments in markets affected by inflation psychology, such as those for bonds, foreign exchange, and sensitive commodities, all of which need to be monitored carefully.

According to Selgin & Lastrapes the “sensitive commodity” in this quote is gold.

In the FOMC minutes from December 21, 1993, we can read beyond a doubt that a rising price of gold signaled the Committee to tighten monetary policy (emphasis mine):

[I]n the view of some members, the rise in long-term interest rates and in gold prices might well have been caused in part by heightened inflation concerns….

Looking forward, many of the members commented that the Committee probably would have to firm reserve conditions [move the fed funds rate] at some point to adjust monetary policy from its currently quite accommodative stance to a more neutral position, and that such a policy move might have to be made sooner rather than later to contain inflation….

In addition, Selgin & Lastrapes used their econometric model based on monthly data from December 1982 through November 1995. They found, as an example, that when the gold price escalated the fed funds rate was increased roughly 12 months later. The Fed responded to the gold price by adjusting the fed funds rate. Of course, the fed funds rate then influenced inflation, but also the price of gold.

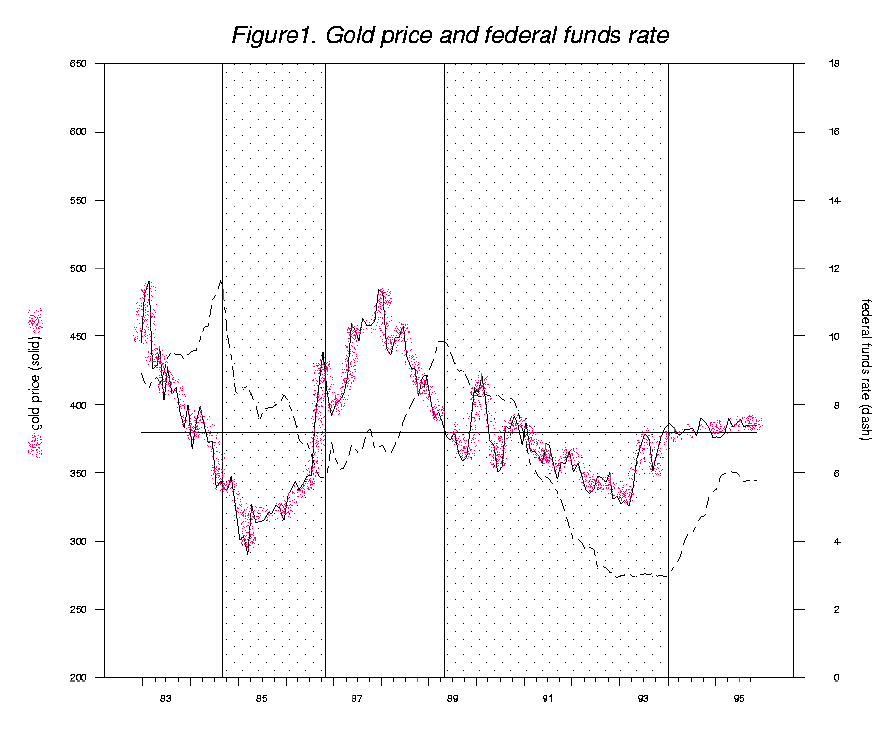

With respect to the chart below, which shows the interaction between the gold price and the fed funds rate, they write: “The figure shows that each [fed funds rate] turning point follows a similar turning point in the price of gold, albeit with a lag of a year to a year and a half.”

Courtesy Selgin & Lastrapes. I have added the purple spray for more clarity. In shaded periods the fed funds rate was declining.

The gold price and the fed funds rate constantly reacted to each other.

Conclusion

One might interpret the above as being in contradiction to my previous article “EuropeHas Been Preparing a Global Gold Standard Since the 1970s,” in which I wrote, among other things, that in the 1970s the U.S. tried to phase gold out from the international monetary system. But there is no contradiction. As I have pointed out, America’s goal was the dollar hegemony.

What happened is that in the early 1980s the global dollar standard was firmly established, and the U.S. sought to sustain its position by stabilizing the dollar. Ironically, they did so by stabilizing the dollar price of gold. Still, through the 1980s and 1990s, the United States’ trade and fiscal deficits persisted, so its political needs were met through its exorbitant privilege.

Some economists, like Nathan Lewis, view the period covered by this article as a “pseudo-gold standard.” Others disagree, because strictly speaking the Fed was targeting inflation and not the price of gold—the fact the gold price was stabilized was a side effect. Alan Greenspan himself wrote in 2017:

When I was Chair of the Federal Reserve I used to testify before U.S. Congressman Ron Paul, who was a very strong advocate of gold. We had some interesting discussions. I told him that US monetary policy tried to follow signals that a gold standard would have created. That is sound monetary policy even with a fiat currency. In that regard, I told him that even if we had gone back to the gold standard, policy would not have changed all that much.

Greenspan labels the Fed’s monetary policy during his tenure as a pseudo-gold standard.

Selgin & Lastrapes write in their paper that the Fed did not specifically target the gold price, although they also write that, “Fed behavior does seem to have served to limit variations in the price of gold.” What stands out is that Greenspan achieved consumer price stability, which was enforced by a stable gold price. In the chart below you can see how the gold price stabilized in 1990 at around $390 dollars per ounce, and inflation stabilized two years later at 2.5%.

What hasn’t been addressed yet is gold leasing. Staring in the 1980s there was a buildup of central banks’ gold on lease causing downward pressure on the gold price. Simply, when central banks lend their gold (usually to bullion banks), physical supply in the market increases, which puts pressure on the gold price. However, when the loans need to be repaid physical demand increases, and the initial downward pressure is undone. Leasing has a temporary impact on the market.

The peak of central banks’ gold “in the market” is thought to have been in 2000 at 5,000 tonnes (of which European central banks contributed 2,119 tonnes). So, leasing suppressed the price of gold until 2000, after which the price jumped back up. To what extent gold leasing distorted inflation expectations and U.S. monetary policy from 1982 til 1995 is unknown.

Kindly note that nowadays the Fed is not inclined to raise rates although the gold price is rising, because of the massive debt overhang. Currently, inflation is seen as a cure rather than a poison, with all due consequences.

via ZeroHedge News https://ift.tt/3l0iXBw Tyler Durden

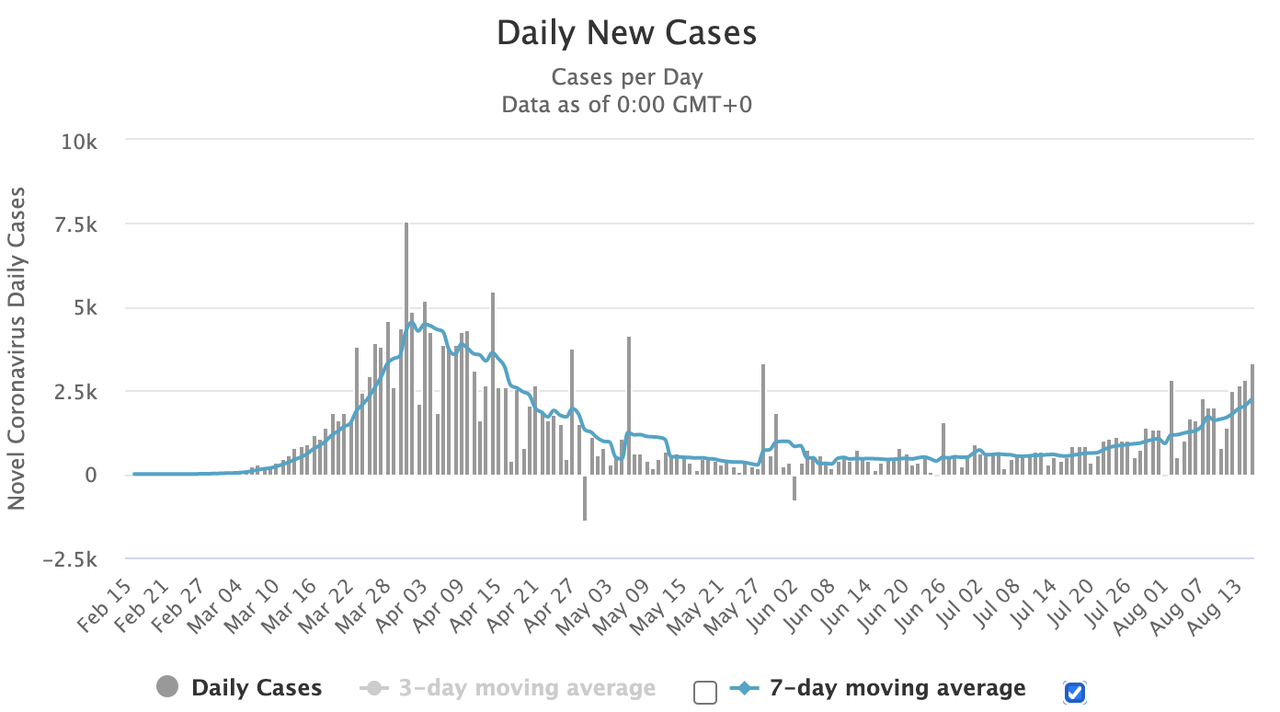

New COVID-19 Cases Hit 5-Month High In South Korea, France Smashes Post-Lockdown Record: Live Updates Tyler Durden

Sun, 08/16/2020 – 11:03

After reviving mandatory mask orders in Paris, French officials on Sunday proposed making face masks mandatory in shared work-spaces as the country continued to grapple with a coronavirus rebound.

The health ministry reported 3,310 new infections on Sunday, marking a post-lockdown high for the fourth day in a row, while the number of clusters being investigated has increased by 17 to 252. The spike in new cases prompted the UK to impose a mandatory 14-day quarantine on any travelers returning from France.

While France drew most of the attention in Europe Sunday morning, South Korea triggered anxieties in Asia after reporting a staggering 279 new cases on Sunday, breaking above 200 for the first time in five months, with a set of clusters in the greater Seoul area contributing most of the new cases.

Of these new cases, 146 were in Seoul and 107 were linked to Sarang Jeil Church, which is led by Reverend Jun Kwang-hoon, a controversial pastor and an outspoken government critic. SK Health ministry officials said they would file a complaint against the leader of the church for violating social distancing rules.

Meanwhile, South Korea and the US said they would delay the start their annual joint military drills until Tuesday after a South Korean officer tested positive. That marked a 2 day delay.

Chinese state media reported that the number of people in Xinjiang with coronavirus who have recovered far exceeded the number of newly reported cases for the 9th day in a row, a sign that the outbreak in the far-flung region dominated by an oppressed Muslim ethnic group is finally starting to wane.

Only 4 new cases were reported across the vast region on Sunday, down from 19 new cases across the entire country on Sat.

Worldwide, total cases have passed 21.35 million after another roughly 260,000 cases were added yesterday…

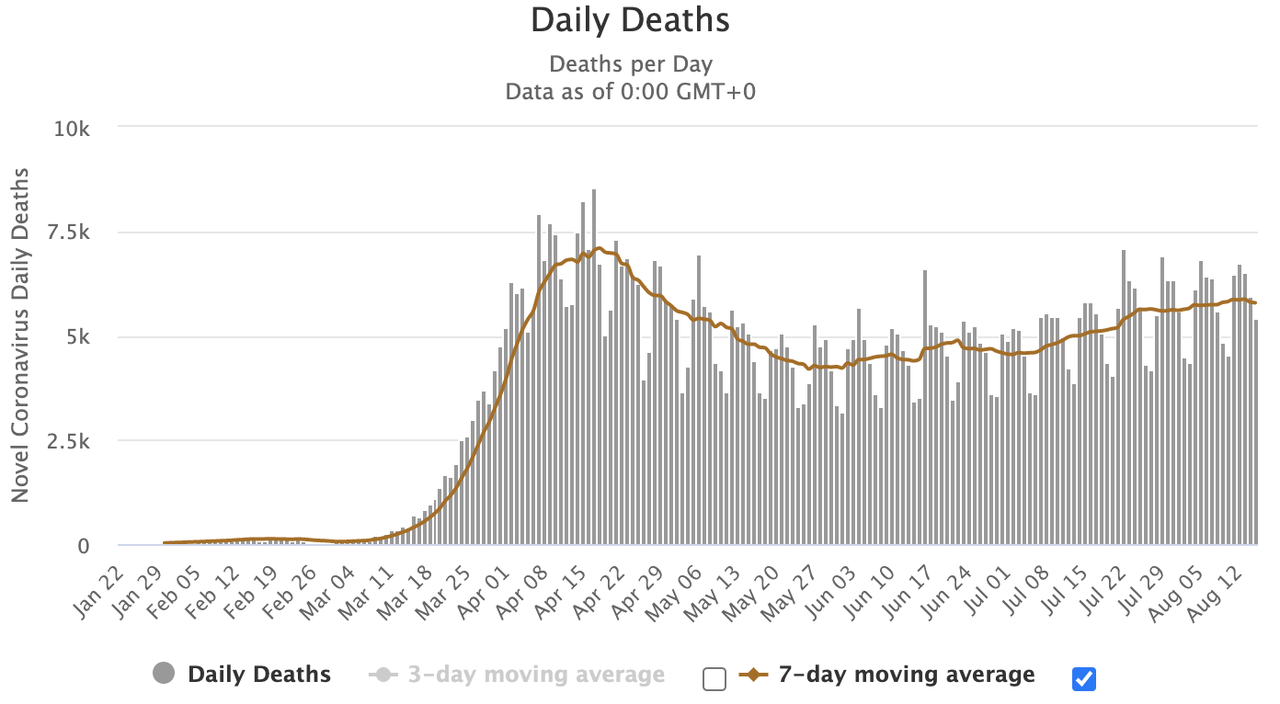

…while deaths have topped 769,000, after another 5,000 were reported.

More than 13.36 million people have recovered worldwide.

Cases in the US climbed by 47,813, or 0.9%, less than the 1% increase over the previous week, data compiled by JHU and Bloomberg showed.

That’s below the 1% increase over the previous week, according to data compiled by Johns Hopkins University and Bloomberg. It was the smallest increase since Tuesday.

Deaths related to Covid-19 rose by 1,046 nationwide, the fifth-consecutive day with more than 1,000, though almost 300 fewer than the previous day, according to the data.

On the vaccine front, the CFO from CureVac told the FT it wouldn’t sell its coronavirus vaccine candidate at cost, but would instead ask for an “ethical margin”. Considering that experts have widely accused Moderna and others of pricing their still-unapproved vaccines at exorbitant prices.

via ZeroHedge News https://ift.tt/345dG5F Tyler Durden

Fake News: Kansas City Southern Shares Stung By Mysterious Disappearing Buyout Report Tyler Durden

Sun, 08/16/2020 – 10:45

Kansas City Southern stock rocketed higher last week on news of a possible increased buyout bid for the company, published by a little known Spanish media website called El Negocio. That news now appears to be fake.

The company had already been the subject of a late July report by the WSJ that claimed Blackstone could bid for the company at a valuation of $21 billion. This week’s El Negocio report claimed that the valuation of such a transaction could be $3 billion higher than expected, sending shares on a tear higher.

But shortly thereafter, analysts began to cast a light of doubt on the source of the information, according to Bloomberg. The day after the second report was released, it had been taken down from the website where it was published.

Credit Suisse analyst Allison Landry said: “We’re not really sure what to make of this. What we are struggling with is why a Spain-based media outlet is reporting on this; it would make more sense to us if it were a Latin American news source.”

Blackstone spokeswoman Paula Chirhart said Wednesday: “While we never comment on deal speculation, this appears to be a fake news website. We’ve never heard of this organization and they did not contact us ahead of publication.”

Bloomberg tried to reach out to El Negocio and said that when they called the “news organization” that “a man who said his name was Albert answered and asked the reporter to call back in an hour.”

The organization’s Twitter account in unverified and its Facebook page lists a well known street in Madrid as its location, without providing an address. The link to its address sends users “to a Google maps page giving directions between the cities of Madrid and Cordoba,” Bloomberg reported.

The incident is the latest in a string of fake news reports and fake buyout offers that have been published online or, even in some cases, submitted to EDGAR, to temporarily manipulate the price of a security. In many recent cases, like the fake acquisition bid made for BlueLinx holdings, there doesn’t appear to be regulatory follow up from the SEC.

And so if you’re a Kansas City Southern shareholder that was stung by this “report”, we wouldn’t hold out hope for justice. Rather, it was likely a worthy learning experience and lesson in exactly what our public markets have now become.

via ZeroHedge News https://ift.tt/2Y7pW1B Tyler Durden

Never before have I seen a market so highly valued in the face of overwhelming uncertainty. Yet today the U.S. stock market stands at nosebleed-inducing levels of multiple, whilst the fundamentals seem more uncertain than ever before. It appears as though the U.S. stock market has drunk from Dr. Pangloss’ Kool-Aid – where everything is for the best in the best of all possible worlds. It is as if Mr. Market is taking a tail risk (albeit a good one) and pricing it with certainty.

Now let me be clear, I don’t claim to know the answers to any of the deep imponderables that face the world today. I have no idea what the shape of the recovery will be, I have no idea how easy it will be to get all the unemployed back to work. I have no idea if we will see a second wave of Covid-19 or what we will do if we do encounter such an event. But I do know that these questions exist. And that means I should demand a margin of safety – wriggle room for bad outcomes if you like. Mr. Market clearly does not share my view.

Instead, as best I can tell, the driving narrative behind a V-shaped recovery in the stock market seems to be centered on “The Fed” or, even more vaguely, “liquidity creation.” It is tricky to argue for any direct linkage from the Fed’s balance sheet expansion programs to equities. The vast majority of QE programs have really been about maturity transformation (swapping long debt for very short-term debt). Nor can one claim a good link between QEs to yields to equities. In fact, during each of the three previous waves of QE, bond yields actually rose. In addition, yields around the world are low but you don’t see other equity markets sporting extreme valuations. So, I think that Fed-based explanations are at best ex post justifications for the performance of the stock market; at worst they are part of a dangerously incorrect narrative driving sentiment (and prices higher).

The U.S. stock market looks increasingly like the hapless Wiley E. Coyote, running off the edge of a cliff in pursuit of the pesky Roadrunner but not yet realizing the ground beneath his feet had run out some time ago.

Investing is always about making decisions under a cloud of uncertainty. It is how one deals with the uncertainty that distinguishes the long-term value-based investor from the rest. Rather than acting as if the uncertainty doesn’t exist (the current fad), the value investor embraces it and demands a margin of safety to reflect the unknown. There is no margin of safety in the pricing of U.S. stocks today. Voltaire observed, “Doubt is not a pleasant condition, but certainty is absurd.” The U.S. stock market appears to be absurd.

From Bull to Bear

Just a few short months ago I was bullish and penning my thoughts on the fear and psychology of bear markets. Little did I know I would find myself writing about the opposite situation in such a short space of time. However, since those dark days of late March, the U.S. equity market has rallied some 47%, other world markets nearly 38%, and even my much beloved emerging markets have turned in a 36% increase.

Both the speed and scale of the U.S. equity market decline and its rebound are rare events. In terms of the scale of decline and its speed I have been able to find only a few other examples to offer as comparison to determine whether sharp declines are often followed by sharp rebounds. We saw similar declines over roughly the same time period in 1987 (obviously, October 1987), late in the Global Financial Crisis (December 2008), and early on during the Great Depression (November 1929). Of the three, only the Global Financial Crisis experienced a similar, very sharp recovery (and this ignores the fact that the market had already declined by 40% before the period of the very sharp sell-off).

It would, of course, be foolhardy in the extreme to extrapolate any conclusions from a sample size of just these events. But I do believe I can say that a market does not have the divine right to display a sharp bounce-back after a sharp decline.

EXHIBIT 1: V–SHAPED RECOVERY IN PRICES IN THE S&P 500 (AND SOME HISTORICAL COMPARISONS)

Source: Global Financial Data

As is often the case, it now appears as though most market participants – I hesitate to use the term investors – are back in full swing with Ian Dury and the Blockheads’ “Reasons To Be Cheerful” echoing through their heads. I have written countless times over the years that overoptimism and overconfidence are a particularly heady and potently dangerous combination because they lead to the overestimation of return and the underestimation of risk.

This combination strikes me as the best description of our current juncture.

It is really the latter trait – the lack of appreciation for risk – that will be the subject of this short missive. One of my favorite definitions of risk comes from Elroy Dimson of Cambridge University who noted, “Risk means more things can happen than will happen.” I find this helps reinforce the unknowable nature of the future and highlights that history is just a series of discrete branches on a much larger tree.

So, when I look at a very sharp recovery like the one we have all just observed, I can’t help but wonder if the world has forgotten about risk. It appears to be as if the U.S. equity market in particular has priced in a truly Panglossian future where everything is for the best in the best of all possible worlds.

It is certainly true in theory that the stock market is meant to be a forward-looking device, capable of seeing through short-term issues. However, as an erudite soul1 once opined, “In theory there is no difference between theory and practice. But, in practice, there is.” History teaches us that the market is usually a master of double-counting, attaching peak multiples to peak earnings, and trough multiples to trough earnings.

For instance, in 1929 the U.S. market P/E was 37% above its long-term average, and earnings relative to 10-year earnings were 46% above their normal level. Similarly, in 2000 the market P/E was 98% above its average, and earnings relative to 10-year average earnings were 37% above their normal level. Peak multiples on peak earnings. In comparison, in 1932 the market was just 64% of its average valuation, and earnings relative to their 10-year average level were just 54% of the average – trough multiples on trough P/Es.

As Exhibits 2 and 3 show, today we see something different. Valuations on a Shiller P/E basis are in the 95th percentile (right up there in terms of one of the most expensive markets of all time), and economic growth measured as real GDP is in the 4th percentile based on pretty generous assessments of this year’s growth (which is one of the worst economic outcomes we have ever seen).

EXHIBIT 2: SHILLER P/E PERCENTILE 1881-2020

Source: Shiller

EXHIBIT 3: ECONOMIC GDP PERCENTILES (ASSUMES THIS YEAR WILL SEE -6% FOR THE FULL YEAR) 1881-2020

Source: Global Financial Data

Perhaps today’s market is truly “looking over the valley,” but it would be one of the few times in history when Mr. Market managed such foresight. Even if this is the case, the certainty with which a V-shaped recovery is being priced in reflects a potentially dangerous level of overconfidence.

Now, to be clear, I have no idea what the shape of any recovery is going to be. How one begins to choose between W, L, swoosh (like the Nike symbol, apparently), or perhaps something more exotic from the Cyrillic alphabet remains beyond my ken.

However, it strikes me that it is likely to be much harder to get the U.S. economy going again post Covid-19 than the market is implying. I don’t think for one second that it is simply a matter of flicking a switch back to the “On” position, which makes the V perhaps one of the least likely outcomes.

The shape of the recovery ultimately depends on a large number of frankly unknowable things such as a household’s ability and willingness to spend. In February there were 6 million unemployed people in the U.S.; today there are more than 30 million! One study from the University of Chicago estimates that up to 40% of the layoffs related to Covid-19 could be permanent! If these projections are even close to accurate about the permanent nature of some of the these losses, then households may be unable or unwilling to spend as they had before the virus struck.

The impact on business in terms of bankruptcies and lower investment will also be key. It is easy to imagine that in the wake of the virus, entrepreneurs may be hesitant to try and start new businesses, which are often said to be the lifeblood of the U.S. economy. Sadly, many businesses will have failed due to the effects of the pandemic, and even those that do survive may likely find their animal spirits dampened significantly.

Now add in other causes for uncertainty relating to the continued developments surrounding Covid-19. What happens if there is a second wave in the Fall? As lockdown restrictions are lifted does it roar back? Exhibit 4 presents a frightening, real-time answer to the second concern as the U.S. is clearly struggling to contain the first wave of the virus.

EXHIBIT 4: COVID-19 CASES (5-DAY ROLLING AVERAGE) 10 MOST AFFECTED COUNTRIES

Source: Johns Hopkins University

I don’t know the answers to these questions, and I am going to refrain from participating in the very popular trend of becoming an armchair epidemiologist or virologist, but I do know that these questions and many others exist. I am also certainly not in the business of trying to second-guess how the future will unfold, but I do know that anyone claiming certainty of foresight is likely to be sorely disappointed. And yet, Mr. Market appears to be doing exactly that.

Howard Marks of Oaktree Capital often talks about there being two kinds of investors. The two groups can be broadly distinguished by their attitudes toward the future.

The first camp is best described as “I know” investors. They think that knowledge of the future course of events such as growth and interest rates is vital to investing. They are confident that such knowledge is attainable, and they “know” they can forecast accurately. They are very comfortable investing on the basis of their views. They freely admit that others will be trying to do the same thing, but their insight is better: it is their edge. Such investors are very popular at dinner parties because they will chatter on about pretty much any subject.

In contrast, the second group of investors studied at the “I don’t know” school. They hold some very different beliefs about the way you should approach investing. They believe you can’t know the future, and, in fact, you don’t need to know the future in order to invest. Driven by this explicit embrace of uncertainty, they insist on a margin of safety when investing: valuation is front and foremost in their approach. This group is not particularly popular at dinner parties (or maybe it’s just me) as the frequent refrain of “I don’t know” in response to questions is not amazingly stimulating on the conversation front.

As should be obvious, I firmly identify with the “I don’t know” school, having already stated that I don’t know several times in response to some very important questions raised earlier in this missive. Naturally, when Mr. Market acts with what looks to me like extreme certainty, I get nervous. Even if my caution is completely misplaced, it does not change my view that the U.S. market has priced in all the good news it possibly can, suggesting very little upside from a fundamental point of view.

Now, of course many will argue that focusing on the fundamentals is a quaint, old-fashioned idea just as they had done during all the great bubbles we have witnessed and studied. They will argue that this is all about the Fed and then blather on about “liquidity creation,” usually in the vaguest of hand-waving fashion. Such protestations are sometimes accompanied by a visual aid such as Exhibit 5, as if it offers some proof of concept.

EXHIBIT 5: FED BALANCE SHEET AND THE S&P 500

Source: Datastream

I find it strange that proponents of the narrative implicit in this exhibit didn’t speak up when the S&P soared during the 4 years from 2016 to 2020, when the Fed’s balance sheet was either flat or shrinking.

From a fundamental (there I go again, set in my old ways) perspective, it is tricky to argue for any direct linkage from the Fed’s balance sheet to equities. Most of the expansion of the balance sheet has been due to the various QE programs. And QE is really just a maturity transformation (i.e., purchasing long-term debt and replacing it with the ultimate form of short-term debt, excess reserves). The clue is in the term “balance sheet”: for every asset there must be a liability and vice versa. Hopefully, Exhibit 6 makes this very clear.

EXHIBIT 6: FED’S BALANCE SHEET – QE IS JUST MATURITY TRANSFORMATION

Source: U.S. Federal Reserve

To provide some context, the following is a breakdown of the Fed’s balancing act through the years shown in the exhibit. You should be able to match each of the phases to Exhibits 5 and 6 and trace their evolution through time.

QE1: $2.3 trillion in assets. The Fed’s first QE program ran from January 2009 to August 2010. The cornerstone of this program was the purchase of $1.25 trillion in mortgage-backed securities (MBS).

QE2: $2.9 trillion in assets. The second QE program ran from November 2010 to June 2011 and included purchases of $600 billion in longer-term Treasury securities.

Operation Twist (Maturity Extension Program). To further decrease long-term rates, the Fed used the proceeds from its maturing short-term Treasury bills to purchase longer-term assets. These purchases, known as Operation Twist, did not expand the Fed’s balance sheet and were concluded in December 2012.

QE3: $4.5 trillion in assets. Beginning in September 2012, the Fed began purchasing MBS at a rate of $40 billion/month. In January 2013, this was supplemented with the purchase of long-term Treasury securities at a rate of

$45 billion/month. Both programs were concluded in October 2014.

Balance Sheet Normalization Program: $3.7 trillion in assets. The Fed began to shrink its balance sheet in October 2017. Starting at an initial rate of $10 billion/month, the program called for a $10 billion/month increase every quarter, until a final reduction rate of $50 billion/month was reached.

QE4: $7 trillion in assets. In October 2019, the Fed began purchasing Treasury bills at a rate of $60 billion/month to ease liquidity issues in overnight lending markets. On March 15, 2020 the Fed announced it would buy at least $500 billion in Treasury securities and $200 billion in government guaranteed MBS over “the coming months.” On March 25 it made the purchases open-ended in size. On June 10 the Fed said it would buy at least $80 billion/month in Treasuries, and $40 billion in RMBS/CMBS. A raft of other measures was also announced but pale into insignificance in terms of the Fed’s balance sheet. U.S. Treasuries held outright account for 64% of the Fed’s assets, and MBS almost 30%.

It is very hard to see how maturity transformation should engender massive enthusiasm for equities. You might be sitting there reading this, screaming silently that I am a moron and that the missing link is interest rates. To wit, by performing QE the Fed lowers the bond yield and, because this serves as the discount rate for other assets, it drives up the stock market.

I have several issues with this viewpoint. First, as long-term readers will know, I am very skeptical of a clear link between bond yields and equity valuations. A little international perspective helps illustrate one of the reasons for my skepticism. Japan and Europe both have exceptionally low interest rates, mirroring the U.S., but they aren’t witnessing stock market valuations at nosebleed-inducing levels. Second, even if I accepted the link, there is the problem still that if the interest rate is low because growth is low, then the valuation is unchanged in a simple DDM framework (see “Role of Interest Rates”). And third (and in my humble opinion the killer blow for this argument), QE hasn’t actually managed to lower bond yields, which truly emasculates the argument. As Exhibit 7 shows, all three of the completed cycles of QE have actually ended with yields higher than they were when the QE began!

EXHIBIT 7: U.S. 10-YEAR BOND YIELD (QE PROGRAMS SHADED)

Source: Datastream

This all suggests there is a good chance that Exhibit 5 is just the result of spurious correlation. That is to say that two series happen to move together despite their being no underlying connection between them. When one studies statistics (as I did many, many moons ago) one is repeatedly taught that correlation does not equal causation for this very reason. One of my personal favorite examples, Exhibit 8, comes from Tyler Vigen and shows a 94.7% correlation between per capita cheese consumption and the number of people who die by becoming tangled in their bedsheets!

EXHIBIT 8: SPURIOUS CORRELATION AT ITS BEST PER CAPITA CHEESE CONSUMPTION CORRELATES WITH NUMBER OF PEOPLE WHO DIED BY BECOMING TANGLED IN THEIR BEDSHEETS

Source: tylervigen.com

Sadly, we humans are prone to love a story. Hence, when we see a correlation (even a spurious one) it is tempting to make up a story to explain the relationship. I think this is exactly what we see when people start talking about equities, the Fed, and “liquidity creation.”

Because I don’t think there is any fundamental relationship between the stock market and the Fed’s actions, I would suggest that this is either ex post justification or, at best, a driver of the ever-slippery concept of sentiment.

One final word of warning when it comes to markets and authorities. I am old enough to have been around when the Japanese engaged in their price-keeping operations from 1992 to 1993 with the aim of keeping the Nikkei 225 above a certain level. These attempts failed both in the short term and the long term and serve as a salutary tale as to the limits on the ability of official bodies to control prices in even the most direct fashion.

In conclusion, it appears to me, at least, that the U.S. stock market has priced in a truly Panglossian outcome with essentially a 100% probability. It is as if the market is taking a (good) tail risk and pricing it as the central case. This strikes me as extreme overconfidence, especially given the vast and imponderable questions that define today’s environment.

The current dominant narrative seems to center on the irrelevance of these questions and favors a “Fed-based” explanation. I think this is dangerous. Ignoring the fundamentals is rarely a good strategy for the longer term, and the evidence seems at odds with the notion of the “Fed” explanation, suggesting this is more ex post justification and not a genuine driver of returns.

Investing is always about making decisions while under a cloud of uncertainty. It is how one deals with the uncertainty that distinguishes the long-term value-based investors from the rest. Rather than acting as if the uncertainty doesn’t exist (the current fad), the value investor embraces it and demands a margin of safety to reflect the unknown. There is no margin of safety in the pricing of U.S. stocks today. Voltaire observed, “Doubt is not a pleasant condition, but certainty is absurd.” The U.S. stock market appears to be absurd.

* * *

A Note on the Role of Interest Rates

I am no longer unique in my questioning of the role of interest rates. The good people at AQR Capital released a paper in May 2020 entitled “Value and Interest Rates: Are Rates to Blame for Value’s Torments?” In it they say, “As the risk-free interest rate is one component of the discount rate, when interest rates go up, the discount rate increases and the asset price falls – if everything else stays constant. Hence, if expected cash flows are unchanged and if the risk premium associated with those cash flows is unchanged (where the risk premium is determined by both the amount of risk exposure the cash flows have and the price of aggregate risk to those exposures in the economy), then the formula tells us how prices will change when riskless interest rates change. However, in the case of stocks, these other components rarely stay constant. Changes in real or nominal interest rates are often accompanied by (or are often a response to) changes in expected inflation and/or changes in expected economic growth, and hence expected cashflows are often changing as well. There may also be a change in the required risk premium, which is the other (and often larger) component of the discount rate. All of these components have their own dynamics and are likely simultaneously being affected by macroeconomic conditions in possibly different ways.

Barack Obama Has “Privately Expressed Grave Concerns” About Joe Biden’s 2020 White House Run Tyler Durden

Sun, 08/16/2020 – 09:45

President Obama sure did take a long time to finally endorse Joe Biden for his 2020 run. The world couldn’t help but notice that Biden’s former partner in crime didn’t exactly hop at the chance to endorse Biden after it was clear that Biden would be the Democratic candidate for 2020.

Now, we might know why…

President Obama has “privately expressed grave concerns” about Biden’s run for the White House, according to a stunning new report from Politico. Obama reportedly said of Biden:

“Don’t underestimate Joe’s ability to f–k things up.”

Despite the endorsement and the former Obama administration painting a rosy picture of the relationship between the two, the Post describes their relationship as being “fraught with tension”.

Former White House communications director Jen Psaki commented of their relationship:

“You could certainly see technocratic eye-rolling at times.”

The attitude reportedly is what led Obama to endorse Hillary Clinton, instead of Joe Biden, in the 2016 Presidential race.

“The president was not encouraging,” Biden said of Obama’s support in 2016.

And while Obama was keeping his distance from Biden after his 2020 announcement he was “talking him down” behind the scenes.

Obama finally caved and endorsed Biden in April of this year, stating:

“I believe Joe has all the qualities we need in a president right now. He’s someone whose own life has taught him how to persevere,”

But speaking about Biden’s presence in Iowa during the caucuses Obama said:

Interestingly, Jim Rickards recently suggested , admittedly a prognostication at best, that Biden won’t even make it to The White house and will soon be replaced as the nominee soon.

Democratic insiders will probably force him out of the race in the next week or so.

They don’t want to risk exposing him to the American people before the election. For Democrats, the stakes are simply too high.

One public incident or serious slip-up is all it could take to kill his chances in the election. The American people simply aren’t going to elect someone who they feel is mentally unfit for office.

Many voters obviously dislike Trump. But, no one could credibly argue that he’s suffering from cognitive decline.

So what’s going to happen?

The Democrat power brokers (Tom Perez, Donna Brazile, Valerie Jarrett, Philippe Reins, AOC, John Podesta and a few others) will get in a room and pick a new nominee.

Biden will “release” his delegates, and party leadership will direct the super-delegates to support that choice. This will start a stampede among the former Biden delegates.

The Bernie Sanders delegates will already be onboard because they’ll be part of the consultation. Then the new nominee will pick a VP and the “convention” will tidy things up. The race will continue from there.

Alternatively, the power brokers could allow Biden to get the nomination and then remove him as nominee before the debates. That’s even easier because there are no delegates involved. It’s just an executive committee decision the candidate cannot refuse.

Still, the process will be a shock to millions of Americans who’ve been expecting a Biden candidacy.

How much of a surprise would that really be?

via ZeroHedge News https://ift.tt/3aus3Bp Tyler Durden

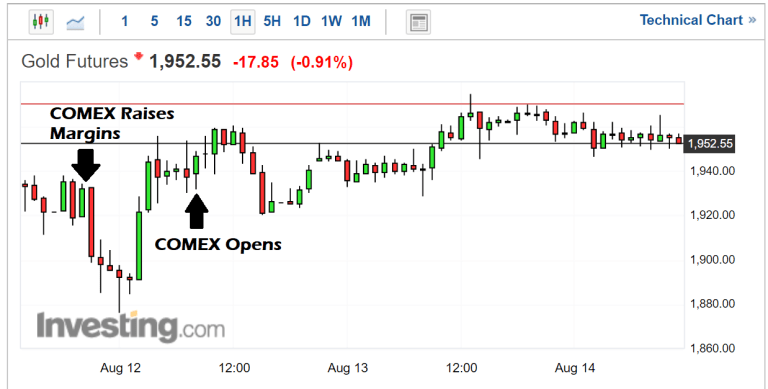

There’s been a lot of speculation in the Gold community about what’s happening in the market this year. 2020 has been wracked with unprecedented gyrations in the gold market.

It’s also seen gold finally breach the $2000 level and, this week after a nasty correction, is still holding onto most of its recent gains.

This rally in gold and the persistent supply tightness which has kept gold futures in backwardation for most of the year are indicators that something has fundamentally shifted in the gold market.

And now, the question on a lot of people’s minds is whether we’ll see the end of the fiction of the paper gold market as epitomized by the futures market on the COMEX.

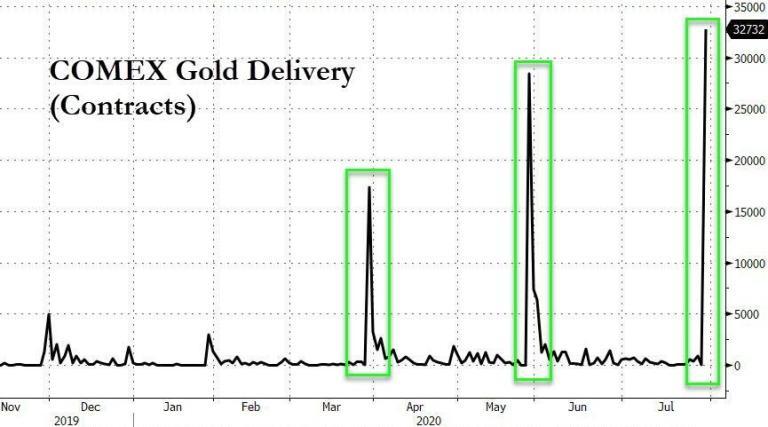

His detailed the use of open interest on the COMEX to push and pull the price of gold and how the market changed after March 23rd when the futures premiums blew out to a high of $70 over the cash price in the forex markets.

Using mass liquidation to crater the price of gold and force thinly-margined, weak longs off their positions is a classic COMEX raid on the gold and silver markets.

And if you look closely at this chart you’ll see a few moments where dramatic drops in open interest didn’t result in big price drops. So, either longs ponied up the cash to stay in their positions or the buying into those ‘raids’ so intense that attempt failed to break the psychology of the gold market.

This is especially true at the end of July, where the attempts to crash the price saw the backwardation premium contract sharply to force longs into unprofitable positions just before the delivery period opened up to try and get them to settle up in cash rather than stand for delivery.

An important change in the global gold market occurred on March 23, 2020. On that day the price of gold futures in New York started drifting higher than the price for spot gold in London. Ever since, the spread has persisted, though it continuously widens and narrows. The reason for this disturbance in the market can be read in my previous article “What Caused the New York vs. London Gold Price Spread and Why it Persists.”

For years folks have talked about that ultimate dramatic moment where the COMEX stands naked in front of the gold community unable to source the physical metal and defaulting on its obligations.

We saw the opposite version of that in oil earlier this year when the May contract closed at $-40.57 per barrel because there was no place to send the oil the contracts represented.

There was so much open interest which needed to settle that the speculators couldn’t resolve the positions without paying through the nose to find a place to put the oil they’d just bought.

And a lot of people feel the same thing will happen in gold in reverse. In this scenario there won’t be enough gold to deliver to those who want the metal. Normally, gold futures are settled in cash.

It’s not a producer/consumer hedging platform. It’s a currency hedging/speculator platform.

But in 2020 it’s now a source of physical gold supply for someone and the COMEX isn’t happy about it at all.

The latest raid on gold began on Friday and continued through Tuesday. When all was said and done more than $200 got knocked off the price, peak to trough.

It should have been enough to dampen gold bull enthusiasm given the strength of the rally off the March low. And during the worst of the raid gold moved back into contango.

But once the raid was over and a new low established gold moved right back into backwardation and with that an explosion off the low and a move right back to challenge $2000 again on Thursday.

What’s even more impressive is that the COMEX, after Monday’s follow-through beat down, did what it always does to protect itself, it raised margin requirements on both gold and silver to force even more liquidations from now exposed and under-water longs.

But it didn’t work!

There was weakness in the overnight Asian markets but once Europe opened the price rebounded and by the time the COMEX opened gold was trading at a higher price than the previous close.

What’s important here isn’t that gold may be moving into a longer-term correction, which is highly likely and a bit overdue, it is that dramatic washouts in price are having little effect on bullish sentiment.

The bulls know that the old market structure is breaking down. They know that London is being drained of gold supply through persistent backwardation, creating arbitrage opportunities while investors are rightfully nervous about the future.

Someone is standing for hundreds of tonnes of delivery in gold while pushing the price higher against the wishes of the exchange.

Here’s a question for you…. who would that be?

Regardless of that, the current scenario can only last for so long.

If there’s one thing I’ve come to accept after over two decades of watching markets it is that the House always wins. The exchanges will always move to protect themselves in the event of a run on their business.

And in the case of the COMEX I fully expect the current gold futures contract to go the way of the U.S. dollar, decoupled completely from physical redemption.

Some folks seem to think this will drive the price to zero. It might, but only after driving the price to infinity.

The more likely scenario is that there won’t be any gold available at any price. Once that occurs, then the value of the contract could vaporize.

What the COMEX doesn’t want to admit to the market is that its gold futures contract isn’t a real futures market but rather a speculation/hedging platform as I said earlier.

The fiction of a gold-settled futures contract keeps the fiction that supply and demand for gold are in balance at these prices. But are they really? If so then gold wouldn’t be hoarded the way it is. Gresham’s Law would reverse and gold would move into the market at a much higher clearing price.

In a regime where central bank credibility is under fire as well as complete political dysfunction in both D.C. and Brussels, the desire to keep gold from making headlines is key to extending that credibility through the crisis period.

As a last resort, then, when cornered by bulls, things have become truly crazy and the exchange cannot make good on its ability to deliver physical gold the COMEX will go to a fully cash-settled contract and that will be that.

And it will happen long before the market goes ‘ask-less.’ The COMEX will step in, in my opinion, before the end of the year to make this critical shift.

Because I think they are fighting people with deeper pockets than they’ve ever fought before.

Will that destroy the COMEX’s credibility? Yes. Will it end the market? No. There is a reason why the COMEX can write hundreds of contracts against the amount of gold in its vaults, because there is demand for a cash-settled ‘paper’ gold futures contract.

That demand will not go away just because some users of the platform are cock-blocked from taking physical delivery. The COMEX gold futures contract will just morph into a highly-liquid contract-for-difference (CFD) and the world will move on.

But it will upset the structure of the gold market in general. It will free the gold market from the fiction of the COMEX gold delivery system and, for the first time in ages, allow real price discovery unburdened by fears over physical delivery forcing ridiculous positioning by bullion banks back-stopped by the Fed’s Magic Money Tree.

That, to me, is what is so very important about what is happening now. Because that begs the question, cui bono?

Who benefits from breaking the price control system of the fake, paper gold market?

Once you sort through the answer to that, China and Russia, then what’s been happening in gold and silver should make a whole lot more sense.

And why gold seems to have decoupled not only from the COMEX but gyrations in the U.S. dollar.

{kind=link}