Psychotherapist Dr Hugh Willbourn says lockdown zealots are displaying all the classic signs of cult members by doubling down on their beliefs despite having been proven wrong.

In an article on his website, Willbourn highlights the work of respected social psychologist Leon Festinger, who analyzed the beliefs of a UFO cult in the 1950’s who believed that a flying saucer would rescue them from the apocalypse.

However, after the catastrophic earthquakes and floods they expected to hit the United States never arrived and their beliefs were totally disproved, “the cult members would become not less but more convinced of their beliefs.”

Festinger identified five conditions that needed to be met in order for the cult members to double down on their beliefs and avoid cognitive dissonance.

1. There must be conviction

2. There must be commitment to this conviction

3. The conviction must be amenable to unequivocal disconfirmation

4. Such unequivocal disconfirmation must occur

5. Social support must be available subsequent to the disconfirmation.

“Festinger’s five conditions and the behaviour of the cult believers correspond closely to the situation with Brexit, Climate Change and Covid-19: a prophecy is made, believers invest themselves, their time, money and prestige in it, the prophecy fails and the believers become more fervent,” writes Willbourn.

The doctor notes how terrifying predictions of how many people COVID-19 would kill have fallen massively short and the models that produced these numbers have been thoroughly debunked. Despite warnings that coronavirus would kill 500,000 in the UK alone, the disease has only claimed 318,000 worldwide.

“To put this figure into perspective, the number of people who have died of, or with, Covid-19 in about four and half months is the same as the number who die in five days from cardiovascular disease,” writes Willbourn.

The doctor notes how “experts” are still doubling down anyway, warning of mass death if lockdown is lifted too early and a second wave of infections.

In reality, research suggests that the lockdowns had a minimal impact on infection numbers, and Sweden’s per capita death toll is lower than the UK’s and numerous other countries despite the Scandinavian country having imposed no hard lockdown.

“Don’t expect an apology from our Government, or any other Government, any time soon,” writes Willbourn.

“The Festinger effect is far, far more prevalent than a clear-sighted view of reality and the tragedy is all the greater.”

“Is this starting to sound familiar?” asks Toby Young. “As Willbourn points out, the sequence that Festinger wrote about more than 50 years ago is eerily reminiscent of what’s happening today: an apocalyptic prophecy was delivered from on high (“the science”), those who believed it radically altered their behaviour, the prophecy turned out not to be true, but instead of abandoning their doom-mongering the believers have become even more fervent, attacking anyone who points out the gap between fantasy and reality as dangerous heretics (“fake news”, “misinformation”, “conspiracy theories”, etc).”

“The difference, of course, is that Festinger’s UFO cult had a few dozen members, whereas the Covid cult seems to have infected half the world. If Festinger’s right, the bad news is we won’t be able to persuade people to stop social distancing if we prove that the danger posed by COVID-19 has been dramatically overstated. On the contrary, people’s opposition to returning to normal will intensify rather than diminish as the evidence mounts they were wrong.”

Meanwhile, Karens all over the world don’t show any signs of giving up on something that legitimizes their favorite thing in the world; Lecturing other people about their behavior.

via ZeroHedge News https://ift.tt/36fbI1x Tyler Durden

“You’ve Got 30 Days”: Trump Torches Tedros In Scathing Letter Slamming “Deadly” Failures Tyler Durden

Tue, 05/19/2020 – 09:04

President Trump fired off a scorching letter to World Health Organization Director-General Tedros Adhanom Ghebreyesus Monday night detailing 14 ways the WHO failed the world while kowtowing to China, and made clear that countless lives could have been saved had the organization refused to lie for Beijing.

“On April 14, 2020, I suspended United States contributions to the World Health Organization pending an investigation by my Administration of the organization’s failed response to the COVID-19 outbreak,” the letter begins.

“This review has confirmed many of the serious concerns I raised last month and identified others that the World Health Organization should have addressed, especially the World Health Organization’s alarming lack of independence from the People’s Republic of China.”

The letter lays out how the WHO and its director stood by while China lied, muzzled whistleblowers and destroyed samples – while ignoring evidence from Taiwan indicating “human-to-human transmission of a new virus,” after which the WHO “chose not to share any of this critical information with the rest of the world, probably for political reasons.“

This is the letter sent to Dr. Tedros of the World Health Organization. It is self-explanatory! pic.twitter.com/pF2kzPUpDv

Trump then lists several claims from the WHO about the coronavirus “that were either grossly inaccurate or misleading,” including:

• On January 14, 2020, the World Health Organization gratuitously reaffirmed China’s now-debunked claim that the coronavirus could not be transmitted between humans, stating: “Preliminary investigations conducted by the Chinese authorities have found no clear evidence of human-to-human transmission of the novel coronavirus (2019-nCov) identified in Wuhan, China.” This assertion was in direct conflict with censored reports from Wuhan.

• On January 21, 2020, President Xi Jinping of China reportedly pressured you not to declare the corona virus outbreak an emergency. You gave in to this pressure the next day and told the world that the coronavirus did not pose a Public Health Emergency of International Concern. Just over one week later, on January 30, 2020, overwhelming evidence to the contrary forced you to reverse course.

• On January 28, 2020, after meeting with President Xi in Beijing, you praised the Chinese government for its “transparency” with respect to the coronavirus, announcing that China had set a “new standard for outbreak control” and “bought the world time.” You did not mention that China had, by then, silenced or punished several doctors for speaking out about the virus and restricted Chinese

institutions from publishing information about it.

Travel ban double-standard

The letter points out that Tedros “strongly praised China’s strict domestic travel restrictions, but were inexplicably against my closing of the United States border, or the ban, with respect to people coming from China. I put the ban in place regardless of your wishes,” stating that the WHO director’s “political gamesmanship on this issue was deadly, as other governments, relying on your comments, delayed imposing life-saving restrictions on travel to and from China.”

Trump gets personal

Bringing it home, Trump slams Tedros as incompetent – writing that “Just a few years ago, under the direction of a different Director-General, the World Health Organization showed the world how much it has to offer. In 2003, in response to the outbreak of the Severe Acute Respiratory Syndrome (SARS) in China, Director General Harlem Brundtland boldly declared the World Health Organization’s first emergency travel advisory in 55 years, recommending against travel to and from the disease epicenter in southern China.

“Many lives could have been saved had you followed Dr. Brundtland’s example,” said Trump.

In closing, Trump gave the WHO 30 days to commit to “substantive improvements” or he will make the temporary freeze of US funding to the organization permanent, as well as “reconsider our membership in the organization.”

* * *

Entire letter below:

• The World Health Organization consistently ignored credible reports of the virus spreading in Wuhan in early December 2019 or even earlier, including reports from the Lancet medical journal. The World Health Organization failed to independently investigate credible reports that conflicted directly with the Chinese government’s official accounts, even those that came from sources within Wuhan itself.

• By no later than December 30, 2019, the World Health Organization office in Beijing knew that there was a “major public health” concern in Wuhan. Between December 26 and December 30, China’s media highlighted evidence of a new virus emerging from Wuhan, based on patient data sent to multiple Chinese genomics companies. Additionally, during this period, Dr. Zhang Jixian, a doctor from Hubei Provincial Hospital of Integrated Chinese and Western Medicine, told China’s health authorities that a new coronavirus was causing a novel disease that was, at the time, afflicting approximately 180 patients.

• By the next day, Taiwanese authorities had communicated information to the World Health Organization indicating human-to-human transmission of a new virus. Yet the World Health Organization chose not to share any of this critical information with the rest of the world, probably for political reasons.

• The International Health Regulations require countries to report the risk of a health emergency within 24 hours. But China did not inform the World Health Organization of Wuhan’s several cases of pneumonia, of unknown origin, until December 31, 2019, even though it likely had knowledge of these cases days or weeks earlier.

• According to Dr. Zhang Yongzhen of the Shanghai Public Health Clinic Center, he told Chinese authorities on January 5, 2020, that he had sequenced the genome of the virus. There was no publication of this information until six days later, on January 11, 2020, when Dr. Zhang self-posted it online. The next day, Chinese authorities closed his lab for “rectification.” As even the World Health Organization acknowledged, Dr. Zhang’s posting was a great act of “transparency.” But the World Health Organization has been conspicuously silent both with respect to the closure of Dr. Zhang’s lab and his assertion that he had notified Chinese authorities of his breakthrough six days earlier.

• The World Health Organization has repeatedly made claims about the coronavirus that were either grossly inaccurate or misleading.

• On January 14, 2020, the World Health Organization gratuitously reaffirmed China’s now-debunked claim that the coronavirus could not be transmitted between humans, stating: “Preliminary investigations conducted by the Chinese authorities have found no clear evidence of human-to-human transmission of the novel coronavirus (2019-nCov) identified in Wuhan, China.” This assertion was in direct conflict with censored reports from Wuhan.

• On January 21, 2020, President Xi Jinping of China reportedly pressured you not to declare the corona virus outbreak an emergency. You gave in to this pressure the next day and told the world that the coronavirus did not pose a Public Health Emergency of International Concern. Just over one week later, on January 30, 2020, overwhelming evidence to the contrary forced you to reverse course.

• On January 28, 2020, after meeting with President Xi in Beijing, you praised the Chinese government for its “transparency” with respect to the coronavirus, announcing that China had set a “new standard for outbreak control” and “bought the world time.” You did not mention that China had, by then, silenced or punished several doctors for speaking out about the virus and restricted Chinese

institutions from publishing information about it.

• Even after you belatedly declared the outbreak a Public Health Emergency of International Concern on January 30, 2020, you failed to press China for the timely admittance of a World Health Organization team of international medical experts. As a result, this critical team did not arrive in China until two weeks later, on February 16, 2020. And even then, the team was not allowed to visit Wuhan until the final days of their visit. Remarkably, the World Health Organization was silent when China denied the two American members of the team access to Wuhan entirely.

• You also strongly praised China’s strict domestic travel restrictions, but were inexplicably against my closing of the United States border, or the ban, with respect to people coming from China. I put the ban in place regardless of your wishes. Your political gamesmanship on this issue was deadly, as other governments, relying on your comments, delayed imposing life-saving restrictions on travel to and from China. Incredibly, on February 3, 2020, you reinforced your position, opining that because China was doing such a great job protecting the world from the virus, travel restrictions were “causing more harm than good.” Yet by then the world knew that, before locking down Wuhan, Chinese authorities had allowed more than five million people to leave the city and that many of these people were bound for international destinations all over the world.

• As of February 3, 2020, China was strongly pressuring countries to lift or forestall travel restrictions. This pressure campaign was bolstered by your incorrect statements on that day telling the world that the spread of the virus outside of China was “minimal and slow” and that “the chances of getting this going to anywhere outside China [were] very low.”

• On March 3, 2020, the World Health Organization cited official Chinese data to downplay the very serious risk of asymptomatic spread, telling the world that “COVID-19 does not transmit as efficiently as influenza” and that unlike influenza this disease was not primarily driven by “people who are infected but not yet sick.” China’s evidence, the World Health Organization told the world, “showed that only one percent of reported cases do not have symptoms, and most of those cases develop symptoms within two days.” Many experts, however, citing data from Japan, South Korea, and elsewhere, vigorously questioned these assertions. It is now clear that China’s assertions, repeated to the world by the World Health Organization, were wildly inaccurate.

• By the time you finally declared the virus a pandemic on March 11, 2020, it had killed more than 4,000 people and infected more than 100,000 people in at least 114 countries around the world.

• On April 11 , 2020, several African Ambassadors wrote to the Chinese Foreign Ministry about the discriminatory treatment of Africans related to the pandemic in Guangzhou and other cities in China. You were aware that Chinese authorities were carrying out a campaign of forced quarantines, evictions, and refusal of services against the nationals of these countries. You have not commented on China’s racially discriminatory actions. You have, however, baselessly labeled as racist Taiwan’s well-founded complaints about your mishandling of this pandemic.

• Throughout this crisis, the World Health Organization has been curiously insistent on praising China for its alleged “transparency.” You have consistently joined in these tributes, notwithstanding that China has been anything but transparent. In early January, for example, China ordered samples of the virus to be destroyed, depriving the world of critical information. Even now, China continues to undermine the International Health Regulations by refusing to share accurate and timely data, viral samples and isolates, and by withholding vital information about the virus and its origins. And, to this day, China continues to deny international access to their scientists and relevant facilities, all while casting blame widely and recklessly and censoring its own experts.

• The World Health Organization has failed to publicly call on China to allow for an independent investigation into the origins of the virus, despite the recent endorsement for doing so by its own Emergency Committee. The World Health Organization’s failure to

do so has prompted World Health Organization member states to adopt the “COYID-19 Response” Resolution at this year’s World Health Assembly, which echoes the call by the United States and so many others for an impartial, independent, and comprehensive review of how the World Health Organization handled the crisis. The resolution also calls for an investigation into the origins of the virus, which is necessary for the world to understand how best to counter the disease.

Perhaps worse than all these failings is that we know that the World Health Organization could have done so much better. Just a few years ago, under the direction of a different Director-General, the World Health Organization showed the world how much it has to offer. In 2003, in response to the outbreak of the Severe Acute Respiratory Syndrome (SARS) in China, Director General Harlem Brundtland boldly declared the World Health Organization’s first emergency travel advisory in 55 years, recommending against travel to and from the disease epicenter in southern China. She also did not hesitate to criticize China for endangering global health by attempting to cover up the outbreak through its usual play book of arresting whistleblowers and censoring media. Many lives could have been saved had you followed Dr. Brundtland’s example.

It is clear the repeated missteps by you and your organization in responding to the pandemic have been extremely costly for the world. The only way forward for the World Health Organization is if it can actually demonstrate independence from China. My Administration has already started discussions with you on how to reform the organization. But action is needed quickly. We do not have time to waste. That is why it is my duty, as President of the United States, to inform you that, if the World Health Organization does not commit to major substantive improvements within the next 30 days, I will make my temporary freeze of United States funding to the World Health Organization permanent and reconsider our membership in the organization. I cannot allow American taxpayer dollars to continue to finance an organization that, in its present state, is so clearly not serving America’s interests.

via ZeroHedge News https://ift.tt/3bKX2rZ Tyler Durden

“I don’t think I could stand another ten years of this fighting…”

Yesterday afternoon I set out to cure Coronavirus. I set up a new company, Splurgeldrug.Com, issuing our first press release about promising new drug trials, followed by another reporting how lab rats responded favourably to the first press release, and how confident of a vaccine in the near future we are. Splugeldrug.com stock went to $600 by teatime, and I currently negotiating the leveraged acquisition of a drug major…

It’s that kind of market. Rumour and sigh abounds..

As a wiser heads than I have noted… most drugs take years to get to market, and less than 1% are ever approved. We still don’t have an effective vaccine for the constantly evolving and mutating annual flu. To bet the farm on a successful vaccine would seem reckless…

Let’s be honest.. if we get a successful vaccine it will help speed global recovery, but it won’t undo the brutal economic damage that’s already been done. A vaccine will simply flatten the depth of the recession – not reverse it, and certainly not magically convert Q2 Earnings into positive numbers…

Markets are not thriving because they expect a vaccine miracle. They are simply arbing governments and central banks. When Powell says he’s “not out of ammunition by a long-shot”, that’s a massive buy signal. Any positive news helps.. and as the central banks have got out backs, just ignore the bad stuff…

(Oh dear… I suspect this will end badly…)

Yoorp – The Decline of the West, part 5826

Thankfully, I have something more significant and real(ish) to write about this morning… Yet again, for all the wrong reasons, it’s time to buy European distressed European Sovereign bonds. Wait for the them to tighten. Sell, then wait for the next crisis.

First, I have to say how hilarious I find it that Bloomberg insists on calling yesterday’s BIG EUROPEAN DEAL a $546 bln rescue package. Apparently, their American readers won’t have a clue what €500 bln means. (Confirmation that Yankee Cultural Imperialism doesn’t make them any smarter perhaps?)

Yesterday’s big moment was France and Germany announcing plans for a European Union Euro 500 bln Recovery Fund… Yawn… I struggled to contain my excitement… What is it?

Yet another solution that isn’t!

Yet again, we have the grand launch of more political mumbleswerve, cobbled together to extend the illusion Europe is a functional polity.

Yet again, a fudge allows Merkel to look like Germany gives a fig for the crisis across the rest of Europe, while simultaneously allowing Macron to look like the statesman he imagines himself to be.

Yet again, Europe remains a case of Eat, Sleep, Repeat…

All the above sound like bad things, but from a market perspective, they are good enough to put on your buying boots for peripheral European Sovereign Debt…

The latest Franco-German grand construction, announced with such Fanfare, is so embarrassingly trite the Europhile FT kept it off the front page and buried it in the international news section.

The proposal manages to neatly fly-tip the concepts of joint and several liability Eurobonds or Coronabonds. The fund, to be run by the EU – which has limited background of borrowing massive amounts – will borrow massive amounts to directly lend to stressed economies despite its dismal past lending record, failure to get its’ accounts signed off, and lack of agreement on a new post Brexit budget.

The whole thing screams…. FUDGE!

But this is Europe.. Fudge works… it comes in conveniently sized cans that are easily and repeatedly kicked down the road…

This can of fudge will allow Ms Merkel to grandstand to her electorate… telling them that backstopping an EU Euro 500 bln lending programme to struggling EU members is so obviously not the same as joint and several lending to struggling EU members. She will be able to tell German workers and savers that Euro 500 bln is a trifling matter compared to the importance of Germany remaining at the top part of Europe.. (It also conveniently glosses over the current ructions about the German constitutional court declaring itself superior to the European Court of Justice, but that’s a story for another day.)

What the agreement is…. is a commitment by France and Germany to allocate the European Union budget in the form of grants to the “worst-hit regions and sectors.” What Euro 500 bln of budget looks like – is a significant underspend. If the US is spending upwards of $3 trillion, then the years of austerity damage to Europe’s soft underbelly require a similar, if not greater amount.

The embattled new girl at the helm of the EU, Ursula von der Leyen, is a key figure behind the plan. She hasn’t been having an easy time of it in Brussels. She’s not an insider and she is a German. If the plan is unanimously approved, it will see the role of the EU elevated to effectively setting European industrial and regional policy as it distributes what amounts to a sticky-plaster aid fund.

Its bureaucracy cubed. The aim is to drive growth to countries devasted by the Coronavirus crisis. That requires money yesterday… not at some point in the future after all 27 member states have agreed the programme (which, incidentally, also requires them to approve the contentious post Brexit (no UK money) budget). (One could almost suspect the EU’s nomenklatura of bureaucrats have hatched up the whole thing to ensure their long-term security…?)

The last thing Europe needs is yet another round of EU infrastructure spending and motorways-to-nowhere proudly announcing they were paid for by the EU. Certain Italians will love it. Yet another EU grants package they can…. game and milk.

The very last way for Europe to recover from 10-years of misguided monetary policy and austerity budgets is through yet more centralised lending from Brussels. The best solution would be to magically undo the whole Euro construct, let countries run their own regional and industrial policy, and determine their own social polices within the single market of Europe. That would encourage nations to compete and optimise their economies within the single market. At some point – when nations were aligned – a common currency might even work. Instead, locking them into the Euro too early ensured European nations are increasingly beholden to Brussels.

European unity is no bad thing – but it’s how you arrive there that matters. The problem with the Euro is coercion – it traps and forces weaker members into increasingly onerous deals to remain members. Is there a workable solution for Europe? One that would allow Italy to restructure, reform and relaunch? Probably not.. which is why the next crisis is already coming just down the road (when are the next Italian elections?)

There are still risks with the Recovery Fund concept. It might not happen. Most commentators are looking at the Austrians or the Dutch throwing a spanner in the works. I’m wondering about the Italians themselves.. Why support a scheme that clearly demotes them to client state dependent on Brussels charity, and means Italy isn’t solving Italy’s problems itself, but has to beg the EU?

[ZH: Sure enough, as Bill projected above, European sentiment slumped after French Finance Minister Bruno Le Maire said that the European recovery fund proposed by France and Germany won’t be available until 2021 and still faces hurdles in “difficult” negotiations in coming weeks.

“It probably couldn’t be available before the start of 2021,” Le Maire says speaking at the National Assembly finance committee.

Le Maire says it will take time because procedures still need to be finalized and the fund will be linked to the EU budget. The finance minister also said Franco-German agreement on the fund was necessary but not sufficient and the two countries must still convince reluctant countries including Austria, Denmark, Sweden and the Netherlands.]

Whatever.. it has a long way to go, but today it’s a buy signal for Italian bonds.. (Just make sure you get short before the EU actually votes on it… )

via ZeroHedge News https://ift.tt/3cJjpQ4 Tyler Durden

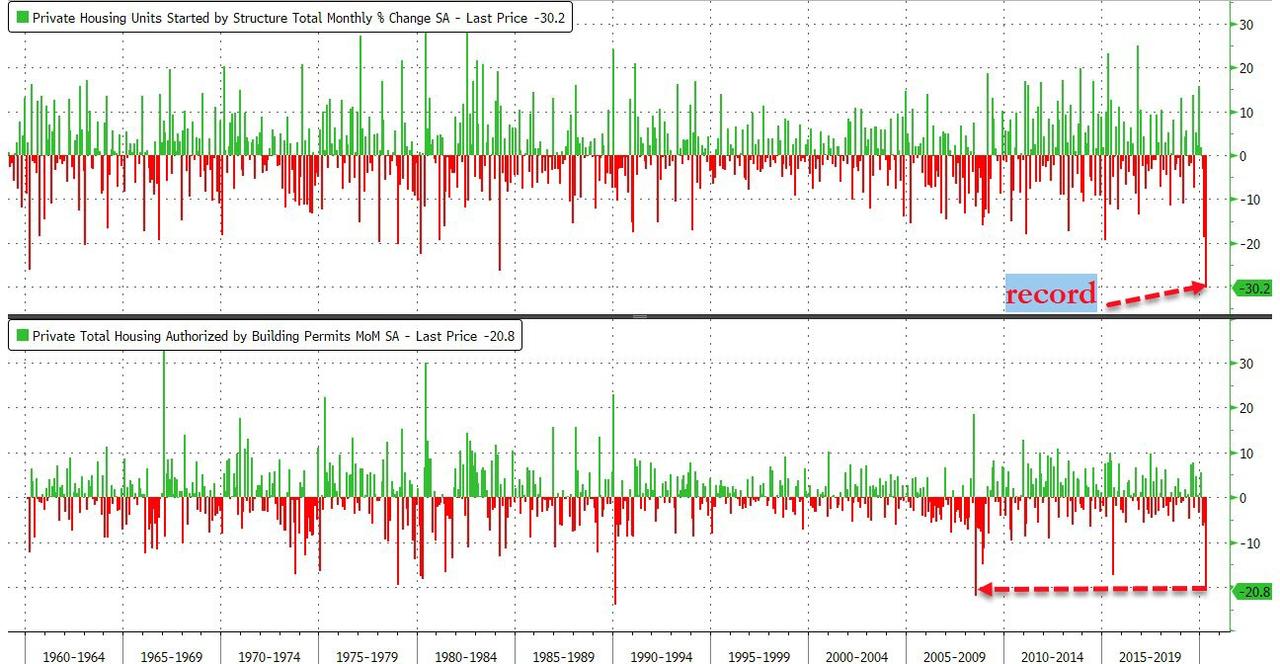

US Housing Starts, Permits Plunge To 5 Year Lows Tyler Durden

Tue, 05/19/2020 – 08:40

Having already collapsed in March, analysts expected further terrible weakness in both housing starts and building permits in April as the impact of lockdowns really escalated, and the data did indeed come in ugly.

Housing Starts fell 30.2% MoM in April (worse than the 26.0% drop expected and accelerating considerably from the 22.3% drop in March). This is a record drop.

Building Permits fell 20.8% MoM in April (better than the 25.9% expected)

Source: Bloomberg

The SAAR chart is a bloodbath with Starts at their lowest since Feb 2015 and Permits lowest since Jan 2015

Source: Bloomberg

Multi-family Starts dominated the drop… down over 40% to the lowest since April 2013, single family starts were down 25.4% to 650K, lowest since March 2015

Single-family permits plunged 24.3% to 669K, lowest since March 2015, and multi-unit permits dropped 12.4% to 373K, lowest since Feb 2017.

As a reminder, applications to build are a proxy for future construction, and the biggest drops were in the Northeast (-45.5% for single-family) and West (-33.2% for single-family).

via ZeroHedge News https://ift.tt/2LMB2Cp Tyler Durden

I have a new article posted for download. The article addresses the boooming literature on “administrative constitutionalism,” i.e., the role of administrative agencies in influencing, creating, and establishing constitutional rules and norms, and

governing based on those rules and norms.

Here is an execerpt:

Progressives such as Metzger, Ross, and Bagenstos seem drawn to broad versions of administrative constitutionalism to evade what some would argue is the inherent conservatism of the American constitutional system. Yet history does not support the assumption that administrative constitutionalism inherently promotes progressive values. This article has already discussed several examples where administrative flexibility in applying “constitutional principles,” particularly with regard to race and ethnicity, has led to illiberal policy.

Recall this article’s definition of shadow administrative constitutionalism-—”a process of agency-norm entrepreneurship and entrenchment that occurs without public consultation, deliberation, and accountability.” Other examples of illiberalism being the outcome of this sort of administrative constitutionalism are easy to come by. Consider, for example, local government administrators who vigorously enforced their states’ anti-miscegenation laws, including making their own innovations

regarding who was covered by such laws and how their race could be ascertained. Or consider the bureaucrats who put various procedural and other obstacles in the way of Jewish refugees seeking to flee Nazi-occupied areas in the late 1930s, ensuring that even meager immigration quotes would not be filled. Or consider southern voting registrars who took pains to limit or prevent African-American voter registration in the South, or zoning officials and road planners who tried to ensure that segregated housing patterns would be entrenched. Or consider the federal immigration officials who expelled tens of thousands of Mexicans from the United States in the early 1930s, including some who had America citizenship. Or consider federal Indian policy undertaken by executive branch bureaucrats in the nineteenth century, which involved “detention of Native peoples without any avenue for redress, forced separation of Native families, criminalization of religious beliefs, and a violent ‘civilizing’ process of Native adults and children.” For most of American history race-related administrative constitutionalism was mostly neglectful of, and

sometimes outright hostile to, the rights and interests of minorities.

The lesson of history is not that administrative constitutionalism leads to “good” or “bad” results from any given ideological perspective, but

that administrative agencies will, like other political/governmental actors, act according to circumstances and incentives.

from Latest – Reason.com https://ift.tt/2XePpoD

via IFTTT

Is remote work the future? Many think so, but the companies that build the tools to allow remote work did not have their own robust capabilities for off-site employment until a pandemic forced their hand. Isn’t that interesting?

It’s true that Silicon Valley firms were among the first to take the big leap. While the leaders of major East Coast metropolises were telling city dwellers to live, laugh, and take the subways to jam-packed events, tech companies like Google, Microsoft, and Salesforce were telling employees to start working from home and cancel conferences and non-essential travel in early March.

The tech industry’s short-term experiment in remote work may extend to the indefinite future. Facebook and Google, for instance, recently announced that their originally months-long remote work plans will go on until the end of the year. Jack Dorsey’s Twitter, ever the dark horse, doubled down and announced last week that the company will permanently transition to a remote-first workplace.

This is big deal, though it got little attention in the mainstream news. Twitter is a huge company, and should its foray into an almost completely remote-first tech company prove successful, others will surely follow.

This has some people very excited. The dream of remote work never really panned out the way many in Silicon Valley might have hoped. The technologies that they developed would in theory allow employees to work from anywhere in the world. This would sever the need for people to uproot from preferred locations just to commute to an office every day, thereby expanding the possible pool of talent that any company could attract. Maybe COVID-19 will be just the kick in the rear that tech firms need to put their employees where their cloud is—everywhere.

Many implications follow. For starters, this would free tech workers from the expensive shackles of San Francisco real estate. No longer would young computer science grads be forced to pay several thousand dollars a month to have the privilege to live in a shoebox and ride company buses into luxurious campuses just to sit in front of a computer.

They could move to cheaper areas or even stay in their hometowns, keeping the bonds of family-of-origin and friendships intact, and remain a part of the fabric of these communities. The combination of stronger communities and lower cost of living could make it much easier for younger folks to affordably form their own families. Or maybe they would decide to strike it out as digital nomads, converting a van or a boat to live in exotic locales, or just flying about every few months. Whether attracted to roots or rootlessness, remote work gives employees more freedom and perhaps more dignity.

It might give a certain kind of employee just as much productivity, too, with a better quality of life. Salesforce recently surveyed a sample of the roughly 30 percent of the workforce that is currently working from home. Most people reported that they were about as productive as usual, and some even felt they were more productive. (As a longtime remote worker, I remember fondly those early days of hyper-productivity when I was released from the burden of constant meetings for the first time.)

Of course, this survey measures self-reporting. Without the risk of a colleague catching a glimpse of our multiple screens far down a Wikipedia rabbit hole, spending time understanding the contours of the Spanish claims to Alaska under the papal bull of 1493 may appear more directly justifiable in one’s role as, say, a technology analyst. As more companies invest in remote productivity surveillance technologies, employers will get a better idea of whether their employees’ perceptions match their own expectations.

Bigger cities could theoretically become more affordable. If knowledge workers are no longer forced to live in one of five big cities to make the big bucks, the political quagmire that prevents new housing supply could naturally become moot. With lower demand comes lower prices, assuming a fixed supply. Service and retail workers who saw much of their paychecks go to insane rental prices might get a little more breathing room (although this assumes their own employment is not jeopardized by a flight from the cities). Residential and commercial property owners who bought at the top of the market, on the other hand, would be clear losers.

Companies stand to benefit too. They might get away with paying new employees less since they would no longer need to subsidize the San Francisco area’s insane housing restrictions. Businesses could furthermore save money by not having to pay the full army of office managers, janitors, chefs, and other support staff that currently keep these palatial office parks running smoothly. Of course, this is bad news for the hardworking support staff that could find themselves out of work.

Remote also provides a way around immigration barriers. No longer would tech firms need to spend time and money lobbying Congress to protect or expand programs like H1-B that fast-track lower cost foreign programmers to move to the United States. They could simply hire them as remote workers—at least until this practice too became another political issue.

So why has it taken so long for Silicon Valley to use the tools they developed for others? It’s not because they’re stupid.

The financial analyst Byrne Hobart has a great run-down of the many reasons why firms have balked at a remote-first future despite the many apparent benefits. In addition to the distractability problem, there are obvious culture benefits to working in a physical office. People just like to feel like they are part of a team. It’s easier to build team morale with the kinds of spontaneous office hijinks and conversations that just can’t be scheduled through Zoom.

My husband and I are both remote workers: I started in the office for many years and moved off-site later, while my husband was hired by a remote-first company from the start. We both have different experiences with the comradery issue: I knew my team well at the time when I first moved, but it’s more difficult (though not impossible) to form relationships with new hires whom I have yet to meet—so I travel to the home office every so often mostly for socializing purposes. My husband’s company builds team spirit with quarterly retreats that pack in months’ worth of socializing into a week-long extravaganza. This works well in our experiences, and we are happy and productive in our remote-work world, but it might be more difficult to scale such scheduled socializing for a Google or a Facebook.

More cynically, the notoriously opulent campuses of big tech fixtures serve as a kind of golden spider’s web to keep employees clocking in for longer than they otherwise would because everything they need is already right there in Mountain View.

For these reasons, the future of remote work may only be quasi-remote—at least for major employers. Yes, knowledge economy workers who can do their job just as well at home may be free to live “anywhere.” But they might find that this “anywhere” is still pretty close to top tier American cities because they will be regularly called upon to visit satellite offices for some real life facetime.

The pandemic has already forced many firms to join the remote work revolution whether they liked it or not. This will undoubtedly create inertia and many businesses will find it makes more sense to keep some staff remote rather than expand their office footprints. Yet culture bonds are sticky and (for now) fairly physically-dependent.

The Silicon Valley dream of a fully decentralized workspace won’t come in the near future, as admirable as Twitter’s foray may be. No wonder virtual reality is the Next Big Thing in tech.

from Latest – Reason.com https://ift.tt/2TAMJAP

via IFTTT

S&P Futures Fail A Breakout Above 3,000 As Triple-Top Forms Tyler Durden

Tue, 05/19/2020 – 08:19

US equity futures tried, and failed, to stage a major breakout into 3,000 overnight, with the E-mini rising as high as 2,976 ahead of the European open (on virtually zero volume), before paring all gains alongside a drop and European stocks as investors weighed the return of the trade war against positive coronavirus news, while disappointing results from Home Depot weighed on sentiment and not even a huge beat by Walmart managed to reverse the mood.

What is more concerning is that now that the S&P has tried, and failed, to break out above the 2950 resistance level, a triple-top appear has formed, which suggests that the most likely next move is a retest of the support.

The Stoxx Europe 600 Index remained lower however as investors shrugged off both news of a $546 billion recovery fund for the region and a surprise jump in German investor confidence, with the ZEW Economist Sentiment surging to 51 from 28.2, beating expectations of a 32.0 print and far above the deeply negative print just two months ago.

European sentiment slumped after French Finance Minister Bruno Le Maire said that the European recovery fund proposed by France and Germany won’t be available until 2021 and still faces hurdles in “difficult” negotiations in coming weeks. “It probably couldn’t be available before the start of 2021,” Le Maire says speaking at the National Assembly finance committee. Le Maire says it will take time because procedures still need to be finalized and the fund will be linked to the EU budget. The finance minister also said Franco-German agreement on the fund was necessary but not sufficient and the two countries must still convince reluctant countries including Austria, Denmark, Sweden and the Netherlands.

Earlier in the session, Asian stocks were green across the board lifted by momentum from the US, and led by materials and industrials, after rising in the last session. All markets in the region were up, with South Korea’s Kospi Index gaining 2.2% and Hong Kong’s Hang Seng Index rising 1.9%. The Topix gained 1.8%, with Soshin Electric and Sony Financial rising the most. The Shanghai Composite Index rose 0.8%, with Fujian Start Group and Shanghai Lingyun Industries Development posting the biggest advances.

Stock started off the week with a bang after Moderna fueled hopes for a coronavirus vaccine, but investors are struggling to maintain the optimism as they continue to monitor efforts to both contain the pandemic and restart economies. Federal Reserve Chairman Jerome Powell is scheduled to speak on the state of the recovery Tuesday, amid expectations he’ll press for further fiscal support to address the steepest downturn since the Depression.

“Short-lived bounces in stock prices even while markets establish new lows are not unheard of,” Ashwin Alankar, head of global asset allocation at Janus Henderson, said in a note. “Forward-looking metrics such as earnings revisions and options prices, on the other hand, sound a more cautious tone both for the economy and stock prices.”

Meanwhile, headwinds remain for stocks, not least a deteriorating U.S.-China relationship. In a further sign of tightening scrutiny on capital flows to the Asian nation, Reuters reported late on Monday that the Nasdaq is set to unveil new rules for initial public offerings including tougher accounting standards that will make it more difficult for some Chinese companies to list on the exchange.

In rates, the 10Y Treasury was unchanged after yields blew out on Monday, while European government bonds were mixed, with peripheral yields falling on the recovery fund news.

In FX, the Bloomberg Dollar Spot Index fell; the euro and European peripheral bonds extended gains in the wake of a proposal by France and Germany to distribute money to member states. The yen fell to a one-week low against the dollar after the news that the Bank of Japan will discuss details of a funding program to demonstrate its resolve to support struggling businesses. The New Zealand dollar advanced, supported by purchases against the Aussie. Sterling strengthened after the U.K. announced plans for 30 billion pounds ($37 billion) in tariff cuts after Brexit.

China’s yuan fell to a two-month low against a basket of trading partners’ currencies, as the central bank’s reference rate stays close to the weakest since 2008. The Bloomberg replica of the CFETS RMB Index — which tracks the yuan against 24 currencies — declined 0.27% to 93.5, the lowest level since March 12. That comes as the People’s Bank of China kept the yuan’s fixings versus major exchange rates low. The authorities cut its reference rate versus the euro by the most in seven weeks Tuesday, while the fixing against the dollar was close to the weakest since 2008. But the yuan has been steady in the spot market, with the currency fluctuating within a narrow band of less than 0.85% on either side this month. That’s partly because traders expect the Chinese exchange rate to be stable ahead of the annual parliamentary meeting, which starts this week

In commodities, West Texas crude’s ascent kept it well above $32 a barrel, rising for a 4th day, though it came off highs touched in Asian trade. West Texas Intermediate crude increased 2.9% to $32.73 a barrel. In terms of underlying fundamentals, on the demand side, participants continue to eye reopening economies for any signs of potential risk of reclosures. Meanwhile looking at supply, OPEC+ cuts are underway, with eyes on the June 8th JMMC meeting for further details as to whether current cuts will be extended as per source which floated potential extension to year-end as opposed to a wind-down of agreed curbs. Meanwhile, unsurprisingly, OPEC+ cut oil exports sharply in the first half of May, according to trackers – which boils down to a function of lower supply and lower demand. WTI July meanders around 31.50/bbl whilst its Brent counterpart failed to reclaim USD 35/bbl to the upside, with both contracts contained within ~USD 2/bbl intraday bands. Elsewhere, spot gold trades flat in recent trade after failing to nurse some of yesterday’s sentiment-induced losses, with the yellow metal now waiting for the Powell/Mnuchin double testimony as a scheduled potential catalyst. Copper prices have given up overnight gains as the sentiment in Europe somewhat soured as US-Sino tensions remain elevated, whilst the EU still has to overcome obstacles before launch of their Recovery Fund, touted to be implemented January 2021.

Home Depot and Walmart are among companies reporting earnings

Market Snapshot

S&P 500 futures down 0.4% to 2,937.75

STOXX Europe 600 down 0.7% to 339.38

MXAP up 1.7% to 148.14

MXAPJ up 1.7% to 477.86

Nikkei up 1.5% to 20,433.45

Topix up 1.8% to 1,486.05

Hang Seng Index up 1.9% to 24,388.13

Shanghai Composite up 0.8% to 2,898.58

Sensex up 0.8% to 30,281.28

Australia S&P/ASX 200 up 1.8% to 5,559.52

Kospi up 2.3% to 1,980.61

German 10Y yield fell 2.1 bps to -0.488%

Euro up 0.1% to $1.0925

Italian 10Y yield fell 18.8 bps to 1.5%

Spanish 10Y yield fell 8.2 bps to 0.651%

Brent futures little changed at $3479/bbl

Gold spot up 0.1% to $1,734.98

U.S. Dollar Index down 0.1% to 99.56

Top Overnight News

President Donald Trump escalated a spat with the World Health Organization, threatening to permanently freeze U.S. funding unless there’s sweeping reform. An experimental vaccine from Moderna Inc. showed early signs it can create an immune-system response to fend off the virus

Nasdaq is set to unveil new rules for initial public offerings including tougher accounting standards that will make it more difficult for some Chinese companies to list on the exchange

Federal Reserve Chairman Jerome Powell said the central bank is prepared to use its full range of tools and leave the benchmark lending rate near zero until the economy is back on track

New Zealand’s central bank sees no need to adjust its monetary stimulus in the wake of the government’s stronger-than-expected fiscal spending package in last week’s budget

Australia’s central bank board held a further discussion on risks to financial stability including a briefing on the resilience of households during its May policy meeting, when both the cash rate and bond-yield target were kept unchanged at 0.25%

Oil’s rally extended to a fourth day as a combination of recovering demand, production cuts and promising test results for a coronavirus vaccine brightened the outlook for energy prices

Argentina’s Exchange Bondholder Group is recommending the government give investors who hold discount bonds a contingent recovery instrument linked to the nation’s GDP, the group said on its website

The U.K. set out its post-Brexit tariffs plan, cutting import duties on many products while protecting industries such as automotive and agriculture in global trade beyond Europe

Optimism that economies may recover faster than expected should boost European stocks, tighten Mediterranean bond spreads and buoy the euro; yet options pricing and technical charts show these currency gains may prove fleeting, with developments in the crisis yet to prove game-changers

Patients who test positive for the coronavirus weeks after recovering from Covid-19 probably aren’t capable of transmitting the infection, research from South Korea shows

Asian equity markets were higher across the board as the region took impetus from the global stock rally spurred by several bullish factors including the reopening of economies, coronavirus vaccine hopes and stimulus efforts after Germany and France proposed a EUR 500bln recovery fund. As such, ASX 200 (+1.8%) shrugged off the increasing Aussie-Sino tensions from China’s import duties on Australian barley and briefly climbed above the 5600 level with upside led by the energy sector after the gains in oil prices and as its top-weighted financial sector also outperformed. Nikkei 225 (+1.5%) coat-tailed on the recent favourable currency moves which helped participants overlook the weak earnings from the likes of Panasonic, while SoftBank shares eventually slumped as plans to tap into its Alibaba and T-Mobile stakes to raise funds failed to offset selling pressure from a record FY loss. Hang Seng (+1.9%) and Shanghai Comp. (+0.8%) conformed to the upbeat tone as China continued to tout more favourable policies including SOE reforms, interest rate liberalization, further opening up and lower tariffs, with the gains in Hong Kong exacerbated after rule changes in the Hang Seng Index which paves the way for the inclusion of Chinese internet giants such as Alibaba, Xiaomi and Meituan Dianping. Finally, 10yr JGBs are lower amid spillover selling in T-notes as the demand for safe havens was sapped by the heightened global risk appetite, while the BoJ presence in the market for JPY 770bln also did little to inspire a turnaround in JGBs.

Top Asian News

China Mulls Relief as Deadline Nears on $211 Billion in Bad Debt

China Mulls Targeting Australian Wine, Dairy on Virus Spat

Sony Plans to Take Finance Arm Private for About $3.7 Billion

Mitsui Is Said to Weigh Stake Sale in Indonesia’s Paiton Energy

European equities have shaved gains since the open and now reside in a sea of red [Euro Stoxx 50 -0.9%] – as the strained relations between US and China continue to hover as a grey cloud on investor sentiment. Meanwhile, despite Germany and France proposing a EUR 500bln European Recovery Fund, the unanimous approval itself could prove to be complex. Netherlands, Austria, Denmark, and Sweden are not fond of the fund being distributed as grants, whilst the touted launch in 2021 may further strain peripheries hit harder by the pandemic such as Italy and Spain. On that note, FTSE MIB (-1.4%) and IBEX (-2.3%) are the marked underperformers thus far whilst core indices see broad-based losses between 0.1-0.4%. Trade updates aside, today marks the first session since the European short-selling ban was remove, as per yesterday’s announcements, potentially providing price action with some influence. Sectors are mostly in the red; breakdown also sees broad-based losses across most sectors, but financials fare better on initial optimism on the EU recovery fund. In terms of individual movers: Thyssenkrupp (+5.4%) holds onto opening gains after it said it is mulling the sale of their steel and warships divisions. Sources also noted that talks with Tata Steel never broke off and both the Cos is still in talks about consolidation. Handelsblatt reported that SSAB and Baoshan Iron & Steel were interested in a majority of the steel unit. Meanwhile, Wirecard (-1.6%) extended on losses amid source reports Germany’s accountancy watchdog FREP last year opened a probe into the Co. following allegations of accounting fraud. Carnival (-0.5%) is weighed on after being downgraded to Junk at Moody’s.

Top European News

European Lockdowns Knock Car Sales Into Record Monthly Drop

German Investor Confidence Jumps on Hopes Worst of Pandemic Over

U.K. Catering Firm Compass Plans $2.5 Billion Share Sale

Sweden Plans Record 30-Fold Jump in Borrowing to Fight Crisis

In FX, the Kiwi has extended recovery gains in wake of commentary from RBNZ Deputy Governor Bascand indicating no rush to deliver more monetary stimulus via an expansion of QE or adopting NIRP, as the Bank waits so see how data pans out before deciding whether it needs to adjust policy further. Nzd/Usd topped out just shy of 0.6100 and Aud/Nzd has retreated sharply through 1.0800 as Aud/Usd respects resistance at recent peaks around 0.6570 and the Aussie reflects on reports that China may add more exports to the higher tariff list on top of barley. Note, no added insight on the RBA front from minutes overnight that merely reiterated the grounds for maintaining rates and asset purchases at present levels while monitoring the impact or recent actions including the introduction of YCC. Meanwhile, the Pound has regained some poise across the board following latest negative interest rate chat from the BoE via Tenreyro and irrespective of UK data revealing a bigger than forecast jump in the claimant count alongside slightly softer than expected wages, with Cable back up above 1.2200 and briefly nibbling stops at 1.2266 and Eur/Gbp easing from 0.8950+ even though the Euro remains elevated independently on additional fiscal support to combat the adverse effects of COVID-19.

EUR – The single currency is consolidating towards the top of a circa 1.0956-03 range vs the Dollar and contributing to a depressed DXY around 99.500 in advance of US housing data, testimony from Fed chair Powell and comments from Rosengren. As noted above, another financial recovery fund for the Eurozone and agreement between Germany and France to issue joint EU debt as a means of paying for the Eur500 bn pot has given the Euro a boost amidst formative signs of an improvement in ZEW’s forward-looking economic sentiment indices.

JPY – A previously unscheduled BoJ meeting to discuss bank funding measures preannounced in April and timetabled for this Friday prompted a bit more Yen weakness against the Greenback within 107.60-30 parameters, but the headline pair may be capped ahead of decent option expiry interest between 107.65-75 in 1.5 bn into the NY cut.

NOK – The Norwegian Krona has pared gains alongside crude prices and waning risk appetite, with perhaps some acknowledgment of remarks from Norges Bank Governor Olsen repeating that the depo rate has likely reached its lower bound, but there is more room in terms of economic policy.

EM – Usd/Try has now breached 6.8000 to the downside and reports that the CBRT has arranged swap lines with the BoE and BoJ are helping the Lira continue its retracement, while the Idr has been very volatile following the BI’s unchanged rate decision that confounded consensus for a 25 bp cut.

RBA Minutes stated that members assessed the best course of action was to maintain current policy setting and monitor economic and financials outcomes closely as support package had been introduced only recently, while it noted that the board determined it would not raise cash rate until progress is made towards full employment and inflation targets. Furthermore, the RBA agreed that policy package was working broadly as expected but is prepared to scale up government bond purchases again if necessary, to achieve the yield target. (Newswires)

RBNZ Deputy Governor Bascand said RBNZ could extend and expand asset purchase programme further but added they will see how data plays out and provide more stimulus if required. Bascand added no decision has been made to buy foreign assets or launch negative rates which are among the many options available to the committee, while he reiterated they asked banks to be ready to transact negative rates in wholesale markets by year-end. (Newswires)

In commodities, WTI and Brent futures trade mixed after intially eking mild gains in what seems to be a breather from yesterday’s pronounced upside – whilst WTI June heads into its futures expiry with its head above USD 30/bbl. In terms of underlying fundamentals, on the demand side – participants continue to eye reopening economies for any signs of potential risk of reclosures. Meanwhile looking at supply, OPEC+ cuts are underway, with eyes on the June 8th JMMC meeting for further details as to whether current cuts will be extended as per source which floated potential extension to year-end as opposed to a wind-down of agreed curbs. Meanwhile, unsurprisingly, OPEC+ cut oil exports sharply in the first half of May, according to trackers – which boils down to a function of lower supply and lower demand. WTI July meanders around 31.50/bbl whilst its Brent counterpart failed to reclaim USD 35/bbl to the upside, with both contracts contained withing ~USD 2/bbl intraday bands. Elsewhere, spot gold trades flat in recent trade after failing to nurse some of yesterday’s sentiment-induced losses, with the yellow metal now waiting for the Powell/Mnuchin double testimony as a scheduled potential catalyst. Copper prices have given up overnight gains as the sentiment in Europe somewhat soured as US-Sino tensions remain elevated, whilst the EU still has to overcome obstacles before launch of their Recovery Fund, touted to be implemented January 2021.

US Event Calendar

8:30am: Housing Starts, est. 900,000, prior 1.22m; Housing Starts MoM, est. -25.99%, prior -22.3%

8:30am: Building Permits, est. 1m, prior 1.35m; Building Permits MoM, est. -25.93%, prior -6.8%

DB’s Jim Reid concludes the overnight wrap

Hopes that the virus will be well and truly beaten surged yesterday as markets got very excited about the potential for a vaccine. There was also the encouragement of new solidarity over the recovery fund in Europe but there wasn’t a lot of new news here but markets just used it as a good excuse to extend the rally. On the vaccine hopes, Moderna announced yesterday that they’d found a promising candidate in their trials. They said that their vaccine produced antibodies that can help with Covid-19 in all eight initial participants. They also said that there weren’t any major safety issues and that the company expects to start a Phase 3 trial in July. In response, the company’s shares ended the day up +19.96%, the eighth best performer in the Russell 1000 index. United Airlines, TripAdvisor, and Park Hotels, who would all benefit greatly from a vaccine, were a few of the small number of companies ahead of them in the index.

The other major news yesterday came from Chancellor Merkel and President Macron, who agreed to support a €500bn recovery fund, which Merkel said would have the ability to borrow money. Macron indicated that the fund would not be reimbursed by the beneficiaries, which would mean that the fund would be financed through grants rather than loans or that the fund would directly invest in member states, thereby acting as grants. The mix of grant and loans was a point of contention at the last meeting and so we will see what support for such an arrangement looks like when the full European Commission comes together next week. I don’t think it’s any surprise that Merkel and Macron support such a fund so it shouldn’t be huge news, but the market liked it. As noted, there are other players to convince but a show of unity here is no bad thing.

All of the major equity indices rallied on both sides of the Atlantic, with the S&P 500 up +3.15% in its best performance in over a month and back above recent closing highs after the difficulties last week. In addition the Dow Jones (+3.85%) and the NASDAQ (+2.44%) also advanced. It was a broad-based rally, with every sector and over 92% of the companies in the S&P moving higher. The covid laggards clearly outperformed on the day with autos (+9.23%), Energy (+7.55%) and Banks (+7.18%) leading the way.

Over in Europe meanwhile, the STOXX 600 (+4.07%) and the DAX (+5.67%) both had their strongest days in over a month. Energy stocks led the rally, buoyed by the strong performance of oil prices as both WTI (+8.12%) and Brent (+7.11%) climbed to 2-month highs of $31.82/bbl and $34.81/bbl respectively. Copper was also up +2.62% while palladium rose by +6.15% to just under $2,000/oz. Gold came off its 7-year high however, down -0.64%, while the dollar index (-0.73%) had its worst day in over a month.

The momentum has continued for the most part in Asia this morning with the Nikkei (+1.81%), Hang Seng (+1.79%), ASX (+1.96%) and Kospi (+2.02%) all posting decent gains. That being said, in China the Shanghai Comp (+0.53%) and CSI 300 (+0.64%) have underperformed while futures on the S&P 500 are flat. That could be in response to the news that Nasdaq is expected to tighten IPO rules including tougher accounting standards that may make it difficult for companies from countries including China to list according to a story on Bloomberg. Elsewhere this morning, yields on 10y USTs are down -2.7bps to 0.70% while in commodities oil is trading flat.

Over in sovereign bond markets yesterday, there was a major narrowing of peripheral spreads in Europe that accelerated late in the day after the news of the recovery fund came out. The spread of Italian ten-year yields over bunds fell by -25.4bps to 214bps, the largest one-day tightening since mid-March after the ECB unveiled their Pandemic Emergency Purchase Programme. There was similarly a tightening in the spread of Spanish (-9.1bps), Portuguese (-9.1bps) and Greek (-13.9bps) yields over bunds. Sovereign bond yields in core countries saw notable rises however, with yields on 10yr Treasuries up +8.3bps to climb back above 0.7% again, while yields on 10yr bunds were also up +6.4bps. In a further positive sign, Bloomberg’s index of US financial conditions eased to its most accommodative level since early March.

In terms of other news yesterday, UK overnight interest-rate swaps began to price in the chance of rates going below zero by the Bank of England’s December meeting. It comes after the BoE’s chief economists’ comments over the weekend, who said that the BoE was looking at further unconventional monetary policies such as negative rates. Like the US, the UK didn’t experiment with negative rates after the financial crisis, so such a move would be unchartered territory in the history of the Bank of England, which dates all the way back to 1694. Later on, we got some comments from the MPC’s Silvana Tenreyro, who said that the longer the lockdown was in place, the longer stimulus would be needed and didn’t close the door on negative rates. For reference, our economists are expecting a further £125bn of QE at the June meeting.

In terms of other central bank speakers yesterday, the Atlanta Fed’s Bostic added to his colleagues’ comments that the second quarter was likely going to be “tough”, but that a number of the job losses would be temporary. He espoused the need for the reopening of the economy to be thoughtful, and that the eventual recovery would hinge on consumer confidence returning. He also indicated that he would not be looking to penalize the decisions of banks during the crisis, saying that banks have been encouraged by the Fed to deploy capital during this time and “reduce the stresses” businesses and people are feeling.

There was barely any economic data to speak of, though the NAHB’s housing market index from the US for May did show a recovery from the 7-year low it reached in April, rising to 37 (vs. 35 expected). We’ll get some more hard data on the US housing market for April today though.

To the day ahead now, and the highlight is expected to be Fed Chair Powell’s testimony before the Senate Banking Committee. The text of his speech was released last night and didn’t contain too many surprises and is more a reflection of what the Fed has done but the Q&A will probably be the most interesting part. Other speakers include the Fed’s Rosengren and Kashkari, as well as the ECB’s chief economist Lane, while the Indonesian central bank will be deciding on interest rates. In terms of data, there’ll be Germany’s ZEW survey for May, UK employment data for the three months to March, and US housing starts and building permits for April. Finally, we’ll get earnings releases from Walmart and Home Depot.

via ZeroHedge News https://ift.tt/3g3BScc Tyler Durden

Chinese Ambassador Says “Independent” WHO Investigation Is “A Joke”: Virus Updates Tyler Durden

Tue, 05/19/2020 – 08:07

Summary:

Chinese ambassador in Canberra says notion that WHO investigation satisfies Australia’s call for “independent” probe is “a joke”

Trump threatens to permanently pull funding and end membership of WHO

Brazil overtakes UK to become world’s 3rd-largest outbreak

India’s case total passes 100k

Navajo Nation now home to “biggest outbreak in the US” per CNN

Singapore plans to start phased reopening on June 2

Jerusalem’s Al-Aqsa mosque set to reopen after Eid

* * *

The big news on Tuesday is the meeting of the World Health Assembly, which is expected to back a WHO-sponsored inquiry into China’s handling of the early days of the coronavirus outbreak. Last night, President Trump delivered a threatening letter where the US warned it could permanently cut funding and even cancel its membership in the WHO.

In response, China accused the US of trying to divert the world’s attention from President Trump’s handling of the outbreak by playing a “blame game” with Beijing. The White House has leveled similar accusations at Beijing. But even more tellingly, China’s ambassador in Canberra slammed Australia’s call for an independent investigation into China’s handling of the early days of the outbreak as “a joke”. The ambassador claimed the the investigation about to be authorized by the WHA doesn’t resemble the type of inquiry that Australia has called for. This gloating comes after President Xi said he’d welcome a comprehensive review, but only after the outbreak has subsided.

“To claim the WHA’s resolution a vindication of Australia’s call is nothing but a joke,” the ambassador said.

After passing the 1.5 million confirmed case threshold yesterday, globally, there have now been more than 4.8 million confirmed cases of COVID-19 and more than 318,500 people have died, according to Johns Hopkins University. Nearly 1.8 million people have recovered.

Some of the latest local updates include Russia, which reported 9,263 new cases and 115 new deaths on Tuesday morning, bringing its case total to 299,941 and 2,837 deaths. In Germany, where the gradual economic reopening has continued unabated, public health officials reported just 513 news cases, bringing Germany’s total to 175,210 cases, while reporting another 72 deaths, bringing the total to 8,007 deaths. Last night, Brazil passed the UK to become the country with the third-largest outbreak in the world after reporting another ~13k cases.

Additionally, India passed the 100k official-case threshold just days after extending its extremely stringent lockdown for another 2 weeks. Health officials reported 4,970 new cases, bringing India’s total to 101,139 cases and 132 deaths, bringing the death toll to 3,163. While India has overtaken China on the ‘official’ numbers, it’s widely believed the outbreak in the mainland was much worse than the official numbers reflect, and more than 40 new cases have been reported in Wuhan and the northeastern Jilin province over the past couple of weeks, resulting in intense new shutdown measures.

As western European states continue to loosen their travel restrictions, Spain has lifted a ban on all direct flights and ships from Italy, though travelers from Italy will have to comply with a two-week quarantine like other foreign visitors until Spain’s state of emergency is officially lifted.

Over in the US, CNN has apparently decided to focus on the plight of the Navajo Nation out west, claiming in a piece published last night that the Native American community is now home to the biggest outbreak in the country (a designation CNN once used to describe a meatpacking plant in South Dakota).

The Navajo Nation reported 69 new coronavirus cases and two additional deaths on Monday, according to a news release from the Navajo Nation president and vice president, which brought the nation’s case total to 4,071, along with 142 deaths, out of a population of roughly 200k. Of course, the rate of ~2,035 infections per 100k would put the nation’s infection rate well above that of most US states. But we suspect this isn’t really an apples-to-apples comparison.

Moving on to the big news in Washington DC on Tuesday: Treasury Secretary Steven Mnuchin and Fed Chairman Jerome Powell will testify before the Senate on the coronavirus response: Treasury Secretary Steven Mnuchin and Federal Reserve Chairman Jerome Powell will testify starting at 10amET before the Senate Banking Committee, where they will deliver “The Quarterly CARES Act Report to Congress” – testimony that’s mandated as per the $2.2 trillion stimulus bill.

Meanwhile, Ivanka Trump will meet with industry leaders, including Apple CEO Tim Cook, Lockheed Martin CEO Marilyn Hewson and IBM executive Ginni Rometty, via Zoom on Tuesday.

As the outbreak in his country rages out of control, Russian PM Mikhail Mishustin has returned to his post after taking nearly 3 weeks off to recover from the virus, during which time the outbreak in his country has careened out of control.

We haven’t heard much from Singapore in a few days as the city-state’s strict new lockdown and testing campaigns appeared to finally cut down on the number of migrant workers falling ill from the virus. Singapore reported just 451 (higher than Monday’s lower but well below the city-state’s peak) new coronavirus cases on Tuesday, as the dissipation of this second wave of migrant worker infections faded. However, Singapore’s government has issued a warning about the increased risk of patients catching dengue fever due to the lockdown, the latest indication of how the shutdown in non-emergency health services could lead to ancillary health crises around the world.

Singapore also apologized to 357 COVID-19 patients who received an erroneous text message saying they had again tested positive for the virus, when they hadn’t. Singapore’s leadership also announced on Tuesday plans to begin a 3-stage reopening on June 2.

In Jerusalem, the Al-Aqsa Mosque will reopen to worshippers after the Eid holiday, according to a statement from its governing body.

“The council decided to lift the suspension on worshippers entering the blessed Al-Aqsa Mosque after the Eid al-Fitr holiday,” according to a statement from the Waqf organisation said.

Finally, in Hong Kong, Chief Executive Carrie Lam said Tuesday that social distancing measures prohibiting gatherings of more than eight people would be extended in a transparent attempt to quash resurgent anti-Beijing protests, which have reemerged as the coronavirus outbreak in the autonomous region have subsided.

via ZeroHedge News https://ift.tt/2TlpjPt Tyler Durden

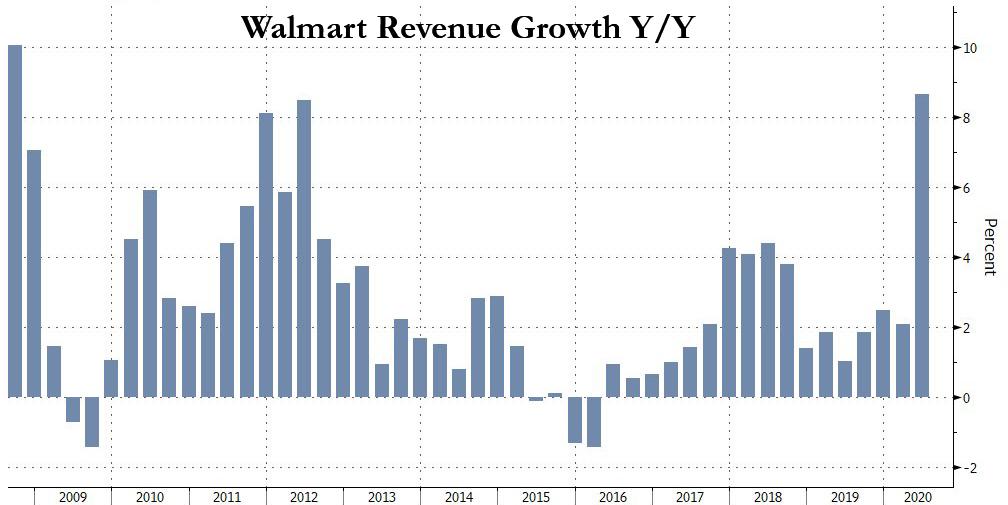

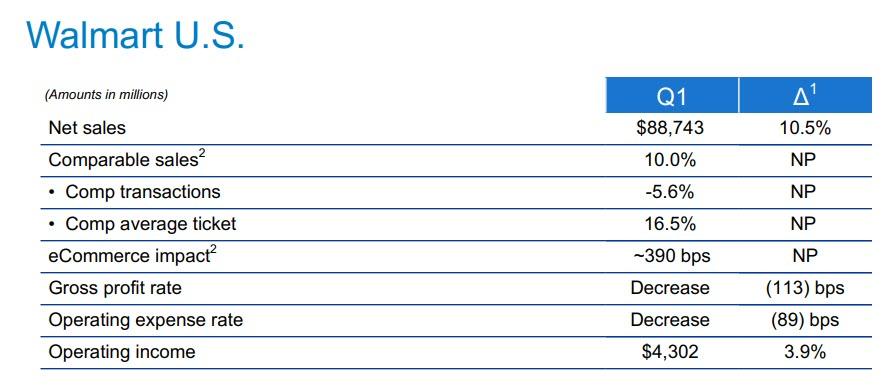

Walmart Hits All Time High On Blowout Earnings From Coronavirus-Linked Stockpiling Tyler Durden

Tue, 05/19/2020 – 07:55

Walmart reported blowout Q1 results, boosted not only by record high pickup and delivery as a result of the coronavirus pandemic, but also a 74% increase in online sales, as US consumers scrambled to stockpile products during the pandemic lockdown.

Walmart reported EPS of $1.18, beating expectations of $1.12, on Revenue of $134.622BN, also well above the $132.79BN expected, even as the company withdrew its full-year guidance due to the “significant uncertainty” surrounding the length and intensity of the coronavirus’s impact.

The retailer reported revenue growth of 8.6% in the quarter, the highest since the financial crisis.

Even though total transactions declined by 5.6%, the surge in the average ticket by 16.5% meant that comp sales rose by a whopping 10.0%, smashing expectations of 8.6% and the highest in almost two decades. It was “as a result of the health crisis and related stay-at-home mandates, customers consolidated store shopping trips with larger average baskets and shifted more purchases to eCommerce.”

As the company details, while February comp sales grew 3.8%, in mid-March, stock-up trips surged with March comp sales increased 15.4%. Store sales slowed during the first half of April but reaccelerated mid-month as customers spent government stimulus money resulting in a 9.5% April comp sales increase.

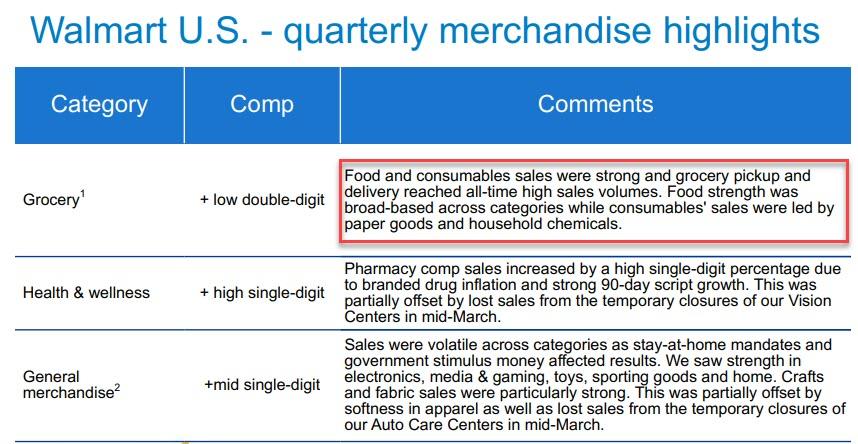

E-commerce sales were strong growing 74% and contributed approximately 390 basis points to segment comp sales growth. The company also reported that “food and consumables sales were strong and grocery pickup and delivery reached all-time high sales volumes” and store pickup and delivery, ship to home, ship from store, and marketplace channels were strong throughout the quarter.

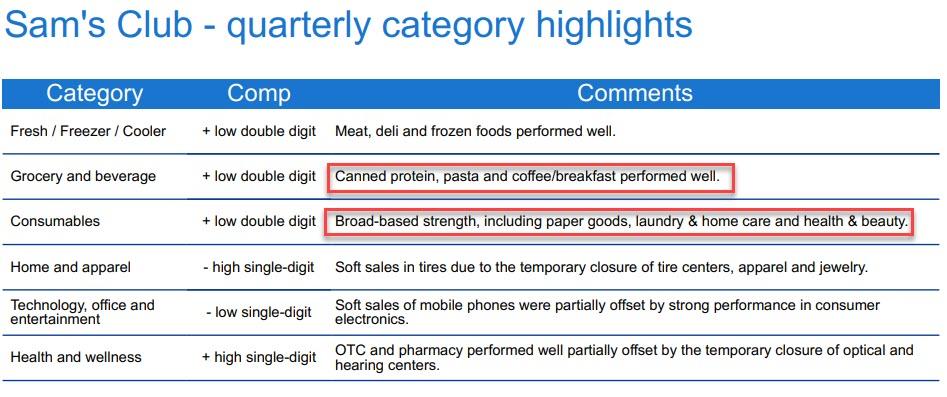

Sam’s Club Q1 US comparable sales ex-gas were also impressive, rising +12%, and smashing the estimate of +7.8%. According to a breakdown of the key performance highlights, in addition to the record stockpiling of paper ” Broad-based strength, including paper goods, laundry & home care and health & beauty”, the company saw a surge in spam sales as “canned protein, pasta and coffee/breakfast performed well.”

Some other observations from the report, via Bloomberg:

Walmart will shutter the Jet.com online business, which it acquired four years ago, an unsurprising move as Walmart has been integrating Jet into its broader web unit over the past year.

While Walmart’s sales are up, there’s concern that everyday items like food and toilet paper are less profitable than merchandise like clothing. Fulfillment costs also erode the profitability of online orders. Walmart said gross profit margins narrowed due to a shift to lower-margin categories and web sales along with markdowns and other investments to lower prices. But the e-commerce business lost less money than it did in the year-ago quarter.

The “significant uncertainty” surrounding the length and intensity of the coronavirus’s impact prompted the retailer to withdraw its full-year guidance, given just three months ago. Still, Walmart said its “business fundamentals are strong.” Walmart incurred about $1.1 billion in additional expenses related to the coronavirus — from worker bonuses to additional cleaning and purchases of protective gear — according to Jefferies analyst Christopher Mandeville.

The safety of Walmart’s massive U.S. workforce is also under scrutiny amid reports that some employees have died from Covid-19. Walmart started requiring all store employees wear masks in late April after earlier measures included social-distancing, plexiglass “sneeze guards” and limits on the number of customers allowed in the store at one time. The company’s executives will share more details on their response to the pandemic on a call with analysts this morning.

The CFO said that “The decision to withdraw guidance reflects significant uncertainty around several key external variables and their potential impact on our business and the global economy, including: the duration and intensity of the COVID-19 health crisis globally, the length and impact of stay-at-home orders, the scale and duration of economic stimulus, employment trends and consumer confidence.”

Finally, the company said it generated a whopping $5.3BN in free cash flow in the quarter, with operating cash flow doubling to $7BN compared to year ago, and while dividends were unchanged from a year ago, stock buybacks tumbled by 66%

On net, however, the quarter blew out expectations as can be seen in the stock price, which jumped over 3% from Monday’s close and is set to surpass the all-time high price set on April 16 of $132.33.

via ZeroHedge News https://ift.tt/3bKDtA3 Tyler Durden

Is remote work the future? Many think so, but the companies that build the tools to allow remote work did not have their own robust capabilities for off-site employment until a pandemic forced their hand. Isn’t that interesting?

It’s true that Silicon Valley firms were among the first to take the big leap. While the leaders of major East Coast metropolises were telling city dwellers to live, laugh, and take the subways to jam-packed events, tech companies like Google, Microsoft, and Salesforce were telling employees to start working from home and cancel conferences and non-essential travel in early March.

The tech industry’s short-term experiment in remote work may extend to the indefinite future. Facebook and Google, for instance, recently announced that their originally months-long remote work plans will go on until the end of the year. Jack Dorsey’s Twitter, ever the dark horse, doubled down and announced last week that the company will permanently transition to a remote-first workplace.

This is big deal, though it got little attention in the mainstream news. Twitter is a huge company, and should its foray into an almost completely remote-first tech company prove successful, others will surely follow.

This has some people very excited. The dream of remote work never really panned out the way many in Silicon Valley might have hoped. The technologies that they developed would in theory allow employees to work from anywhere in the world. This would sever the need for people to uproot from preferred locations just to commute to an office every day, thereby expanding the possible pool of talent that any company could attract. Maybe COVID-19 will be just the kick in the rear that tech firms need to put their employees where their cloud is—everywhere.

Many implications follow. For starters, this would free tech workers from the expensive shackles of San Francisco real estate. No longer would young computer science grads be forced to pay several thousand dollars a month to have the privilege to live in a shoebox and ride company buses into luxurious campuses just to sit in front of a computer.

They could move to cheaper areas or even stay in their hometowns, keeping the bonds of family-of-origin and friendships intact, and remain a part of the fabric of these communities. The combination of stronger communities and lower cost of living could make it much easier for younger folks to affordably form their own families. Or maybe they would decide to strike it out as digital nomads, converting a van or a boat to live in exotic locales, or just flying about every few months. Whether attracted to roots or rootlessness, remote work gives employees more freedom and perhaps more dignity.

It might give a certain kind of employee just as much productivity, too, with a better quality of life. Salesforce recently surveyed a sample of the roughly 30 percent of the workforce that is currently working from home. Most people reported that they were about as productive as usual, and some even felt they were more productive. (As a longtime remote worker, I remember fondly those early days of hyper-productivity when I was released from the burden of constant meetings for the first time.)