Just a few days after Morgan Stanley’s chief equity strategy, Michael Wilson, warned that “volatility is about to rise… a lot“, the executive director of Morgan Stanley’s institutional equity trading group, Chris Metli, has sent out an ominous warning of his own, cautioning the bank’s clients that “this week has been one of those markets where something just doesn’t feel right.”

What prompted this concern.

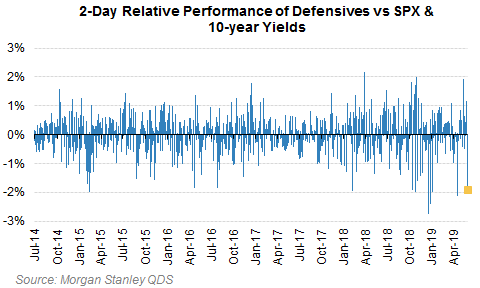

As Metli explains, “the underperformance of defensives in a down tape and with bonds bid is unusual,and this week defensives have posted the worst P/L relative to SPX and bonds of the last 5 years outside of December 2018 and the Healthcare selloff in April 2019 (using Staples/Utes/Real Estate/Healthcare for defensives).”

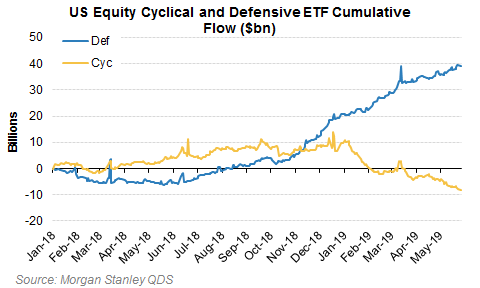

On one hand this could just be a little profit taking in Defensive areas, the MS strategist observes. There has been a strong rotation into Defensive sectors as well as Low Vol and High Div funds and out of Cyclicals and Value products.

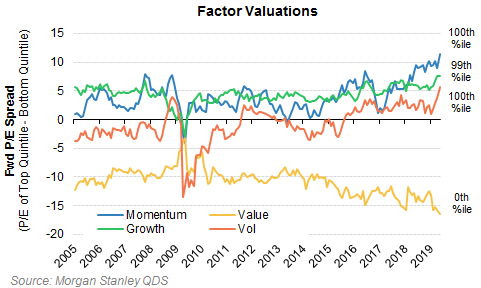

And valuation spreads are extreme in the factor space – Low Vol stocks have never been cheaper relative to High Vol stocks, while the opposite is true of Value.

The above shows that Momo and Growth are also rich, as they are the HF version of the ‘defensive’ rotation.

Momentum has tracked Growth over Cyclical performance nearly one-for-one over the last month as investors have fled cyclicals and sought the ‘safety’ of secular growth.

According to Metli, the above positioning could easily unwind on a positive stimulus, and that trades to play that outcome are pretty clear – i.e. if trade dispute is resolved, equities and bond yields go higher, cyclicals rally, defensives and growth stocks are a source of funds, etc. What is less clear is why these rotations would be happening in a down equity market. There are two possible explanations:

Equities are finally catching up to what the bond market has been saying for months – that growth is weak, and there is a limit to how bid defensive sectors can get in a negative growth environment. Investors are selling their passive holdings (which have a defensive bias).

This is the end of the defensive rotation and the beginning of a pro-cyclical / pro-growth rotation.

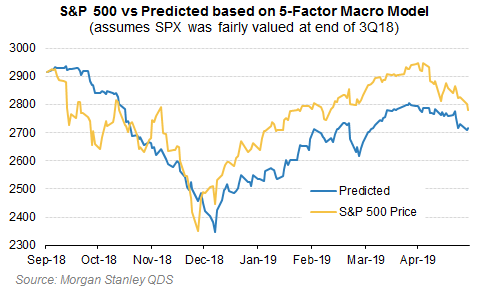

And this is where things get unpleasant, because according to the Morgan Stanley strategist, the former is more likely, in which case equities have further downside per a regression of SPX versus a “predictive” model based on 5 macro factors.

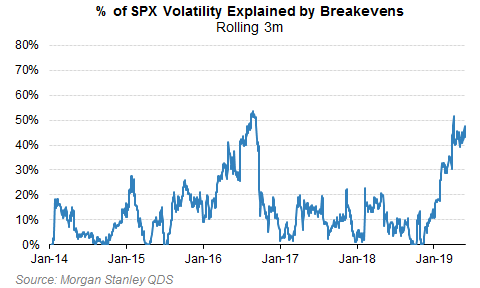

In this scenario the well owned Growth names and the long side of Momentum are most at risk going forward. That said the signals are still mixed – for example breakevens are up (modestly) and that same regression suggests SPX should be up 30 bps today, as breakevens have been explaining ~50% of SPX volatility over the last 3 months.

As Morgan Stanley concludes, “the future will tell which way it goes, but recent price action does suggest markets are at a turning point.“

via ZeroHedge News http://bit.ly/2WeJh1V Tyler Durden

As the trade war with China rages with no end in sight, President Trump has continued to spout optimistic rhetoric, even if it doesn’t have quite the same market-moving potential as it once did.

But over in Beijing, where President Xi recently warned his people to “prepare for a new Long March”, the trade-related rhetoric has grown increasingly belligerent and antagonistic since Washington decided to blacklist Huawei. The commentary from senior officials appears to undermine the prospects for Trump and Xi hammering out a sweeping deal on the sidelines of the upcoming G-20 summit in Osaka.

One senior Chinese diplomat lashed out at Washington on Thursday, denouncing the trade dispute as “naked economic terrorism” and “economic bullying,” and asserting that Beijing isn’t afraid of an enduring trade conflict.

Speaking to reporters in Beijing, Chinese Vice Foreign Minister Zhang Hanhui said China opposed the use of “big sticks” like trade sanctions, tariffs and protectionism.

“We oppose a trade war but are not afraid of a trade war. This kind of deliberately provoking trade disputes is naked economic terrorism, economic chauvinism, economic bullying,” Zhang said, when asked about the trade war with the United States.

During the press briefing, which was ostensibly called to answer questions about President Xi’s upcoming trip to Russia, where he will appear at the St. Petersburg Economic Forum, Zhang warned about the adverse impact on the global economy (perhaps a subtle clue that Beijing won’t come to the rescue with a ‘Shanghai Accord 2.0’).

Everyone loses in a trade war, he added, addressing a briefing on Chinese President Xi Jinping’s state visit to Russia next week, where he will meet Russian President Vladimir Putin and speak at a major investor forum in St Petersburg.

“This trade clash will have a serious negative effect on global economic development and recovery,” Zhang added.

“We will definitely properly deal with all external challenges, do our own thing well, develop our economy, and continue to raise the living standards of our two peoples,” he said, referring to China and Russia.

“At the same time, we have the confidence, resolve and ability to safeguard our country’s sovereignty, security, respect and security and development interests.”

Ministry of Commerce Spokesman Gao Feng warned during a different news conference that China “will fight to the end”, and that Beijing wouldn’t tolerate its rare earth metals being used against it – the latest threat to curb exports of the critical rare earth metals, a “nuclear option” that Beijing has readily embraced following the latest round of escalation.

At the same time, Beijing has reportedly asked state media companies to tone down their rhetoric, and what was expected to be a heated “trade war debate” between Fox Business host Trish Regan and a popular Chinese news commentator instead took the form of an amicable discussion.

Taking this into consideration, it would appear that Beijing is sending Washington a message: Trump and his senior officials aren’t the only ones who can play ‘good cop, bad cop’ on trade.

via ZeroHedge News http://bit.ly/30XGc5g Tyler Durden

President Donald Trump’s top trade advisor, Peter Navarro, tried to make the case in The Wall Street Journal yesterday that free trade advocates should hop aboard Trump’s trade agenda.

Instead, he ended up highlighting a crucial blind spot in his, and the president’s, understanding of the issue—an error that shows exactly why Congress should not trust him, or Trump, with greater powers to reshape global trade.

Most of the op-ed is premised on the idea that lowering tariffs all around the world would be beneficial to the United States’ economy. And that’s probably true. Trade isn’t a zero-sum game, so more trade and fewer tariffs would generally benefit everyone. This isn’t a novel idea—it’s basically been the consensus among the nations of the developed world for decades, and it’s been pretty phenomenally successful—but it is good to hear the Trump administration admitting as much. While Trump has at times talked about trying to get to a point where there are no tariffs at all, his actions (and his general “trade is bad” worldview) make it difficult to take that seriously.

But Navarro is playing a bait-and-switch here. To get to that world of lower tariffs, he says, Congress should give Trump more power to increase tariffs. As a negotiating tactic only, of course. Specifically, Navarro is calling for the so-called Reciprocal Trade Act, which Trump asked Congress to pass at the State of the Union address earlier this year. As I wrote at that time, this bill would effectively give the president more excuses to raise trade barriers and impose tariffs, which are really just taxes paid by American importers.

For example, the European Union currently charges 10 percent tariffs on cars imported from America while America charges only 2.5 percent on car imports from Europe. If the Reciprocal Trade Act were to become law, Trump could circumvent Congress and raise car tariffs to 10 percent—something that he’s already threatened to do via a different mechanism, and something that would be disastrous for America’s auto dealers and car buyers.

Should Congress trust Trump with those powers? Maybe you believe Navarro’s claim that Trump would only use it to negotiate for lower tariff rates for American exports. But even then you should ask—as with all delegations of authority from Congress to the executive—whether you’d want the next president to have that same unchecked power.

You should also examine the argument Navarro makes at the end of the op-ed, where he suddenly shifts into protectionist mode—and ends up undermining his own argument for expanding presidential trade powers by demonstrating how little the current administration understands about trade.

Here’s what Navarro writes (bolding mine, italics his):

For a ballpark estimate of the jobs impact from lowering the U.S. trade deficit through a reciprocal tariff policy, the Economic Policy Institute provides this yardstick: For every $1 billion deficit reduction, U.S. employment increases by approximately 6,000. This suggests a [Reciprocal Trade Act] jobs boost ranging between 350,000 and 380,000.

That last claim may disconcert free-trade economists, who insist higher tariffs always result in slower growth and less employment. But because imports don’t contribute to gross domestic product, unfair trade reduces growth, and narrowing the trade deficit through higher exports and lower imports boosts growth.

There are two fallacies at play here.

First: Navarro is only half-right when he says that imports don’t contribute to gross domestic product, and he’s fully wrong to imply that imports harm growth. (In fact, they don’t influence the calculation of GDP at all, but they do have a positive correlation with economic growth.) Second: Running a trade deficit or a trade surplus has virtually no bearing on how quickly a country’s economy grows. Navarro uses these two errors to build a backdoor case for restrictions on imports that is not grounded in either economic theory or empirical evidence.

Let’s start with the first mistake: that imports do not affect GDP, either positively nor negatively. Here’s how economists Tyler Cowen and Alex Tabarrok explain this exact error in their book Modern Principles of Economics:

Here is a mistake to avoid. The national spending approach to calculating GDP requires a step where we subtract imports but that doesn’t mean that imports are bad for GDP! Let’s consider a simple economy where [Investment], [Government spending], and [Exports] are all zero and [Consumption]=$100 billion. Our only imports come from a container ship that once a year delivers $10 billion worth of iPhones. Thus when we calculate GDP we add up national spending and subtract $10 billion for the imports, $100-$10=$90 billion. But suppose that this year the container ship sinks before it reaches New York. So this year when we calculate GDP there are no imports to subtract. But GDP doesn’t change! Why not? Remember that part of the $100 billion of national spending was $10 billion spent on iPhones. So this year when we calculate GDP we will calculate $90 billion-$0=$90 billion. GDP doesn’t change and that shouldn’t be surprising since GDP is about domesticproduction and the sinking of the container ship doesn’t change domestic production.

But not only do imports (or the lack of them because all the container ships sank) not harm GDP, they likely add to it. Cowen and Tabarrok continue:

If we want to understand the role of imports (and exports) on GDP and national welfare. We have to go beyond accounting to think about economics. If we permanently stopped all the container ships from delivering iPhones, for example, then domestic producers would start producing more cellphones and that would add to GDP but producing more cellphones would require producing less of other goods. If we were buying cellphones from abroad because producing them abroad requires fewer resources then GDP would actually fall—this is the standard argument for trade that you learned in your microeconomics class.

This is all a bit technical, to be sure, but it applies to the real world. Last week, I spoke with Alex Camara, the CEO of AudioControl, a Seattl- based manufacturer of speakers and headphones. Although all his company’s products are designed and built in the United States, about 30 percent of the component parts are imported from China—and are now subject to 25 percent tariffs. Navarro wants you to believe that those imports are a drag on GDP, but a business like Camara’s might not even exist without them.

“Domestic production would not be as strong as it is without access to global supply chains, which reduce costs, raise productivity, expand the global market share of U.S. firms, and allow the United States to focus on what it does best: innovating, researching, and designing the cutting edge goods and services of the future,” write Theodore Moran and Lindsay Oldenski, researchers at the Peterson Institute for International Economics. “The data show that when US firms expand abroad they end up hiring more workers in the United States relative to other firms, not fewer.”

The second mistake is the more important one, but it builds on the first. Navarro is trying to argue that reducing imports will cut the trade deficit and boost economic growth.

As the Harvard economist N. Gregory Mankiw explained in The New York Times last year, countries run trade deficits because their governments and people spend more on consumption and investment than on the goods and services they produce. The way to reduce a trade deficit is to reduce public and private spending—which is why America’s trade deficit has typically fallen during recessions, when spending drops—not by attacking the countries that are trading with you.

“To be sure, I would be happy to have balanced trade,” Mankiw writes. “I would be delighted if every time my family went out to dinner, the restaurateur bought one of my books. But it would be harebrained for me to expect that or to boycott restaurants that had no interest in adding to their collection of economics textbooks.”

The idea that trade deficits are tied to economic growth also fails in practice.

In 2017, for example, the United States recorded GDP growth of 2.22 percent and ran a trade deficit of about $502 billion—”with a b,” as Trump would say. But look at other countries that had similar growth rates. France grew at 2.16 percent but had a trade deficit of $18 billion. Germany grew at 2.16 percent too, but ran a trade surplus of $274 billion.

The same is true at the higher end of the growth scale. Ireland grew by 7.22 percent and had a $101 billion trade surplus in 2017; India grew by 7.17 percent with a $72 billion trade deficit. It’s also true at the bottom. Italy’s economy grew by a mere 1.57 percent with a $60 billion trade surplus; the United Kingdom grew by 1.82 percent despite a $29 billion trade deficit.

If Navarro were truly interested in building a world with freer trade and lower tariffs, his influence on “Tariff Man” Trump would be welcomed. But his Wall Street Journal argument looks more like a deliberately deceptive attempt to push for greater executive powers over trade, which could be wielded to limit imports into America under the false premise that doing so will boost economic growth.

from Latest – Reason.com http://bit.ly/2EHqIsg

via IFTTT

President Donald Trump’s top trade advisor, Peter Navarro, tried to make the case in The Wall Street Journal yesterday that free trade advocates should hop aboard Trump’s trade agenda.

Instead, he ended up highlighting a crucial blind spot in his, and the president’s, understanding of the issue—an error that shows exactly why Congress should not trust him, or Trump, with greater powers to reshape global trade.

Most of the op-ed is premised on the idea that lowering tariffs all around the world would be beneficial to the United States’ economy. And that’s probably true. Trade isn’t a zero-sum game, so more trade and fewer tariffs would generally benefit everyone. This isn’t a novel idea—it’s basically been the consensus among the nations of the developed world for decades, and it’s been pretty phenomenally successful—but it is good to hear the Trump administration admitting as much. While Trump has at times talked about trying to get to a point where there are no tariffs at all, his actions (and his general “trade is bad” worldview) make it difficult to take that seriously.

But Navarro is playing a bait-and-switch here. To get to that world of lower tariffs, he says, Congress should give Trump more power to increase tariffs. As a negotiating tactic only, of course. Specifically, Navarro is calling for the so-called Reciprocal Trade Act, which Trump asked Congress to pass at the State of the Union address earlier this year. As I wrote at that time, this bill would effectively give the president more excuses to raise trade barriers and impose tariffs, which are really just taxes paid by American importers.

For example, the European Union currently charges 10 percent tariffs on cars imported from America while America charges only 2.5 percent on car imports from Europe. If the Reciprocal Trade Act were to become law, Trump could circumvent Congress and raise car tariffs to 10 percent—something that he’s already threatened to do via a different mechanism, and something that would be disastrous for America’s auto dealers and car buyers.

Should Congress trust Trump with those powers? Maybe you believe Navarro’s claim that Trump would only use it to negotiate for lower tariff rates for American exports. But even then you should ask—as with all delegations of authority from Congress to the executive—whether you’d want the next president to have that same unchecked power.

You should also examine the argument Navarro makes at the end of the op-ed, where he suddenly shifts into protectionist mode—and ends up undermining his own argument for expanding presidential trade powers by demonstrating how little the current administration understands about trade.

Here’s what Navarro writes (bolding mine, italics his):

For a ballpark estimate of the jobs impact from lowering the U.S. trade deficit through a reciprocal tariff policy, the Economic Policy Institute provides this yardstick: For every $1 billion deficit reduction, U.S. employment increases by approximately 6,000. This suggests a [Reciprocal Trade Act] jobs boost ranging between 350,000 and 380,000.

That last claim may disconcert free-trade economists, who insist higher tariffs always result in slower growth and less employment. But because imports don’t contribute to gross domestic product, unfair trade reduces growth, and narrowing the trade deficit through higher exports and lower imports boosts growth.

There are two fallacies at play here.

First: Navarro is only half-right when he says that imports don’t contribute to gross domestic product, and he’s fully wrong to imply that imports harm growth. (In fact, they don’t influence the calculation of GDP at all, but they do have a positive correlation with economic growth.) Second: Running a trade deficit or a trade surplus has virtually no bearing on how quickly a country’s economy grows. Navarro uses these two errors to build a backdoor case for restrictions on imports that is not grounded in either economic theory or empirical evidence.

Let’s start with the first mistake: that imports do not affect GDP, either positively nor negatively. Here’s how economists Tyler Cowen and Alex Tabarrok explain this exact error in their book Modern Principles of Economics:

Here is a mistake to avoid. The national spending approach to calculating GDP requires a step where we subtract imports but that doesn’t mean that imports are bad for GDP! Let’s consider a simple economy where [Investment], [Government spending], and [Exports] are all zero and [Consumption]=$100 billion. Our only imports come from a container ship that once a year delivers $10 billion worth of iPhones. Thus when we calculate GDP we add up national spending and subtract $10 billion for the imports, $100-$10=$90 billion. But suppose that this year the container ship sinks before it reaches New York. So this year when we calculate GDP there are no imports to subtract. But GDP doesn’t change! Why not? Remember that part of the $100 billion of national spending was $10 billion spent on iPhones. So this year when we calculate GDP we will calculate $90 billion-$0=$90 billion. GDP doesn’t change and that shouldn’t be surprising since GDP is about domesticproduction and the sinking of the container ship doesn’t change domestic production.

But not only do imports (or the lack of them because all the container ships sank) not harm GDP, they likely add to it. Cowen and Tabarrok continue:

If we want to understand the role of imports (and exports) on GDP and national welfare. We have to go beyond accounting to think about economics. If we permanently stopped all the container ships from delivering iPhones, for example, then domestic producers would start producing more cellphones and that would add to GDP but producing more cellphones would require producing less of other goods. If we were buying cellphones from abroad because producing them abroad requires fewer resources then GDP would actually fall—this is the standard argument for trade that you learned in your microeconomics class.

This is all a bit technical, to be sure, but it applies to the real world. Last week, I spoke with Alex Camara, the CEO of AudioControl, a Seattl- based manufacturer of speakers and headphones. Although all his company’s products are designed and built in the United States, about 30 percent of the component parts are imported from China—and are now subject to 25 percent tariffs. Navarro wants you to believe that those imports are a drag on GDP, but a business like Camara’s might not even exist without them.

“Domestic production would not be as strong as it is without access to global supply chains, which reduce costs, raise productivity, expand the global market share of U.S. firms, and allow the United States to focus on what it does best: innovating, researching, and designing the cutting edge goods and services of the future,” write Theodore Moran and Lindsay Oldenski, researchers at the Peterson Institute for International Economics. “The data show that when US firms expand abroad they end up hiring more workers in the United States relative to other firms, not fewer.”

The second mistake is the more important one, but it builds on the first. Navarro is trying to argue that reducing imports will cut the trade deficit and boost economic growth.

As the Harvard economist N. Gregory Mankiw explained in The New York Times last year, countries run trade deficits because their governments and people spend more on consumption and investment than on the goods and services they produce. The way to reduce a trade deficit is to reduce public and private spending—which is why America’s trade deficit has typically fallen during recessions, when spending drops—not by attacking the countries that are trading with you.

“To be sure, I would be happy to have balanced trade,” Mankiw writes. “I would be delighted if every time my family went out to dinner, the restaurateur bought one of my books. But it would be harebrained for me to expect that or to boycott restaurants that had no interest in adding to their collection of economics textbooks.”

The idea that trade deficits are tied to economic growth also fails in practice.

In 2017, for example, the United States recorded GDP growth of 2.22 percent and ran a trade deficit of about $502 billion—”with a b,” as Trump would say. But look at other countries that had similar growth rates. France grew at 2.16 percent but had a trade deficit of $18 billion. Germany grew at 2.16 percent too, but ran a trade surplus of $274 billion.

The same is true at the higher end of the growth scale. Ireland grew by 7.22 percent and had a $101 billion trade surplus in 2017; India grew by 7.17 percent with a $72 billion trade deficit. It’s also true at the bottom. Italy’s economy grew by a mere 1.57 percent with a $60 billion trade surplus; the United Kingdom grew by 1.82 percent despite a $29 billion trade deficit.

If Navarro were truly interested in building a world with freer trade and lower tariffs, his influence on “Tariff Man” Trump would be welcomed. But his Wall Street Journal argument looks more like a deliberately deceptive attempt to push for greater executive powers over trade, which could be wielded to limit imports into America under the false premise that doing so will boost economic growth.

from Latest – Reason.com http://bit.ly/2EHqIsg

via IFTTT

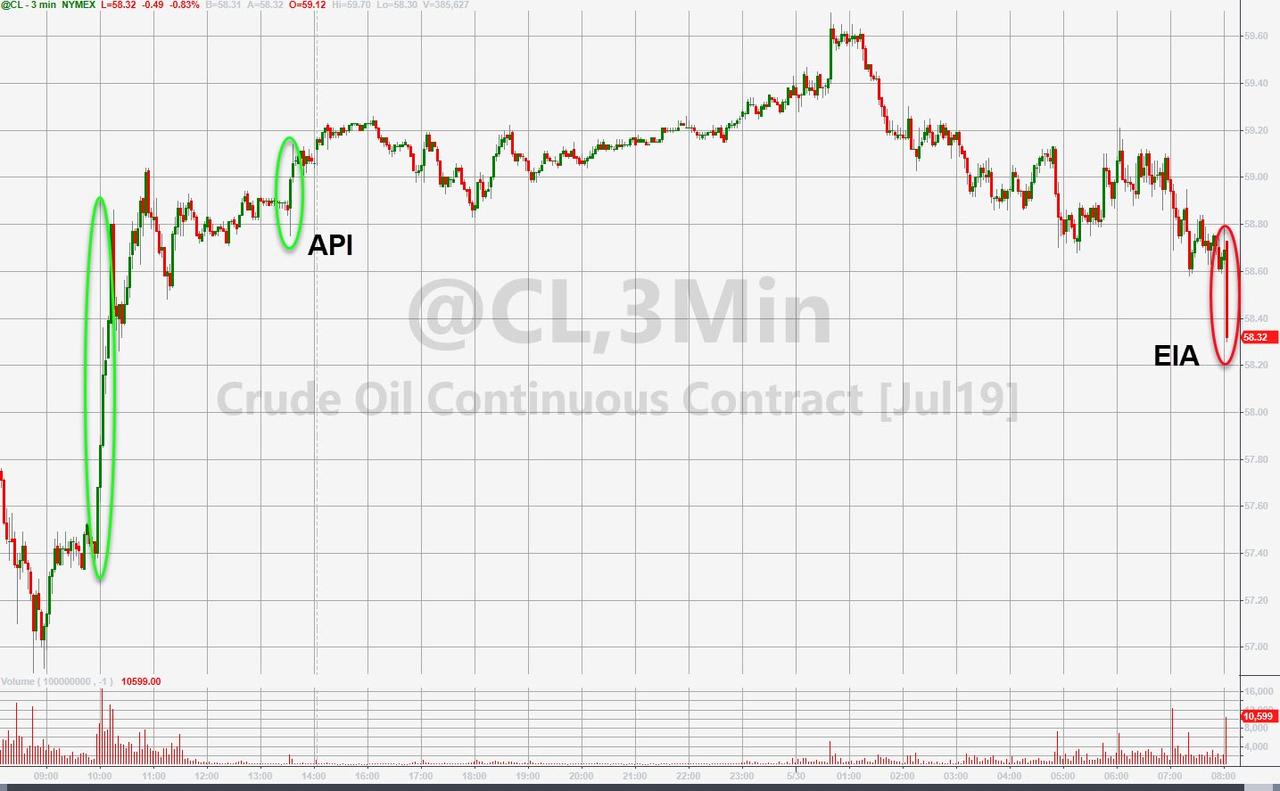

U.S. crude inventories were expected to fall for the first time in three weeks, with investors will focus on refinery consumption, which dropped unexpectedly in last EIA report.

“As those refiners come back in, we’re probably going to see demand really rip higher in the U.S.,” says Michael Loewen, a commodities strategist at Scotiabank in Toronto.

As Bloomberg also notes, heavy rains and flooding in the Midwest and Great Plains last week meant that a number of refiners had to pull back from their typical summer demand pick-up plans.

API

Crude -5.265mm (-500k exp)

Cushing -176k

Gasoline +2.711mm

Distillates -2.144mm

DOE

Crude -282k (-1.4mm exp)

Cushing -16k

Gasoline +2.204mm

Distillates -1.615mm

Following last night’s solid crude draw, EIA reported a tiny 282k draw (well below expectations) and at the same time gasoline stocks rose notably for the 2nd week in a row…

US Crude production continues to hover near record highs, rebounding modestly last week…

WTI fell back below $59 ahead of the EIA data (after rallying overnight following the API data) but slipped on the lower than expected EIA draw…

Finally, as Bloomberg reports, the WTI put skew grew to the most bearish since mid-December on Wednesday, while gauges of volatility for both the U.S. benchmark and global equivalent Brent swelled

Bloomberg Intelligence Senior Energy Analyst Vince Piazza cpncludes:

“The market is coalescing around our view of softer global demand growth affecting the petroleum value chain, with WTI retreating below $60. We highlight sustained U.S. crude output, despite waning growth. Prolonged periods above $60 in the U.S. would likely invite an acceleration in well completions, even amid pressure for capital discipline. Indecision among OPEC and its partners about capacity curbs, along with geopolitical turmoil, clouds the fundamental backdrop.”

via ZeroHedge News http://bit.ly/2QCA1Pg Tyler Durden

When Uber Technologies ended years of speculation by holding its hotly anticipated initial public offering on May 11, CEO Dara Khosrowshahi tried to appease nervous investors by claiming that the rather low asking price of $45-a-pop was a fair reflection of a lackluster IPO environment. Well, apparently, he underestimated just how treacherous and unreceptive the market has become to newbies deemed as being all flash and little substance.

Uber shares have tanked 12 percent in its short public life, dropping nearly $10 billion from its valuation in less than three weeks in what is shaping up to be yet another disastrous listing. Driving the massacre are hordes of short-sellers, with shares sold short surging 160 percent to 36 million from 13.6 million at the time of its IPO.

Uber is facing a fate even worse than that by its close peer Lyft, Inc.(NYSE:LYFT), with the value of short positions surpassing Lyft’s for the first time.

Wrong timing

Maybe the ride-hailing company was being a little naïve for expecting the red carpet treatment at a time when the market had clearly soured on unprofitable startups.

Just a few months earlier, shareholders had raked Lyft shares over the coals for its lack of profits. Yet, Uber is the real champion in that department, with the company having lost $4 billion last year alone and nearly $7 billion cumulatively in its 10-year lifespan. Lyft’s $900 million loss last year certainly pales in comparison with that.

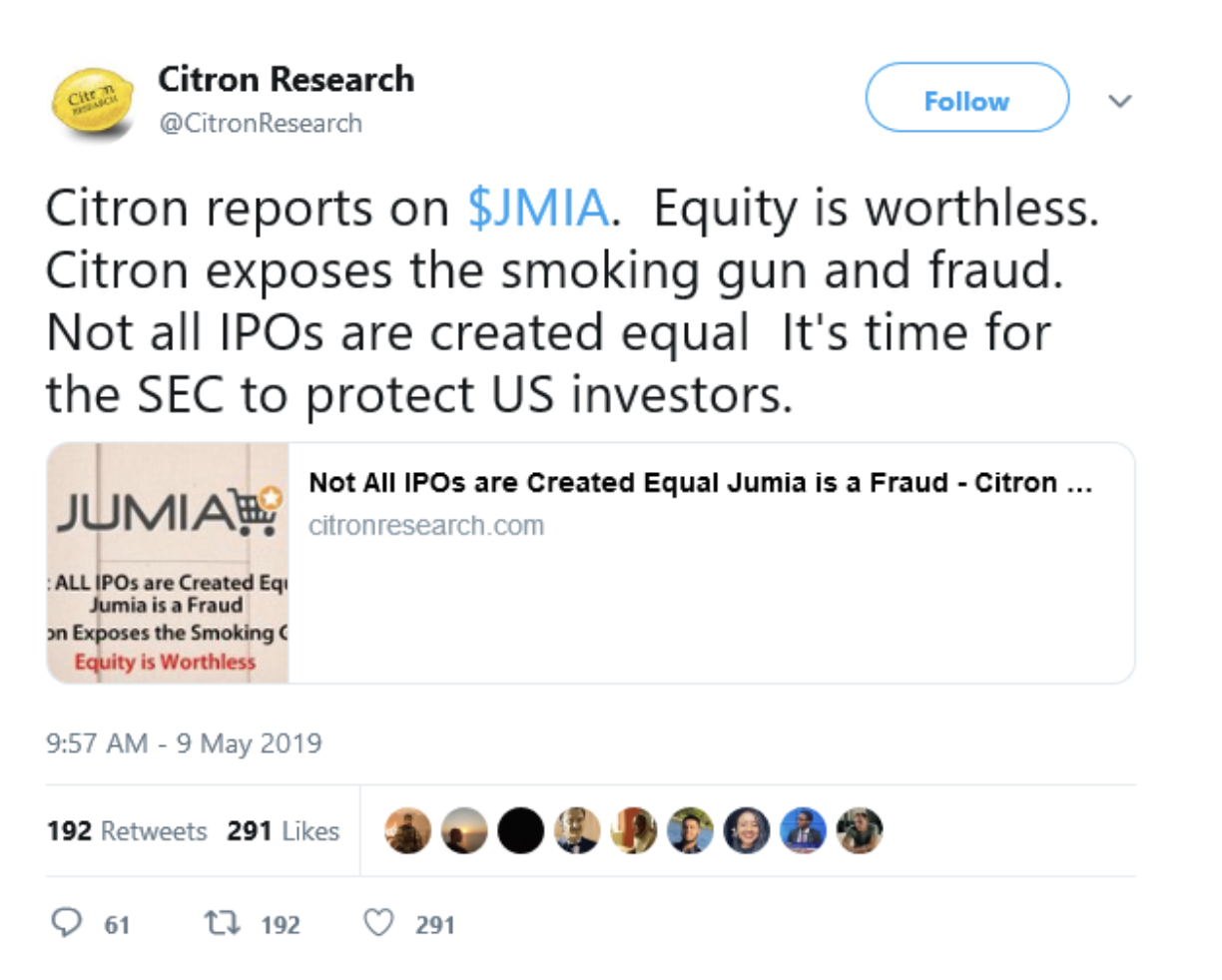

There’s a clear trend developing here with the market going out on a limb to punish startups with nothing to show at the bottom line. After a Cinderella run that saw its shares climb 75 percent post-IPO, Jumia Technologies(NYSE:JMIA), Africa’s first unicorn to list on NYSE, has tanked nearly 50 percent in May after famous Wall Street short-seller Citron Research, took to Twitter and laid in on the company accusing it of fudging its numbers to give the impression of a far more stable business. Citron alleges these are material discrepancies and labeled the shares “worthless”. Citron’s Andrew Left has evenreleased a video to back-up claims of the said fraud.

Jumia had accumulated losses of close to a billion dollars by the end of 2018.

(Click to enlarge)

The shorts are clearly having a field day here.

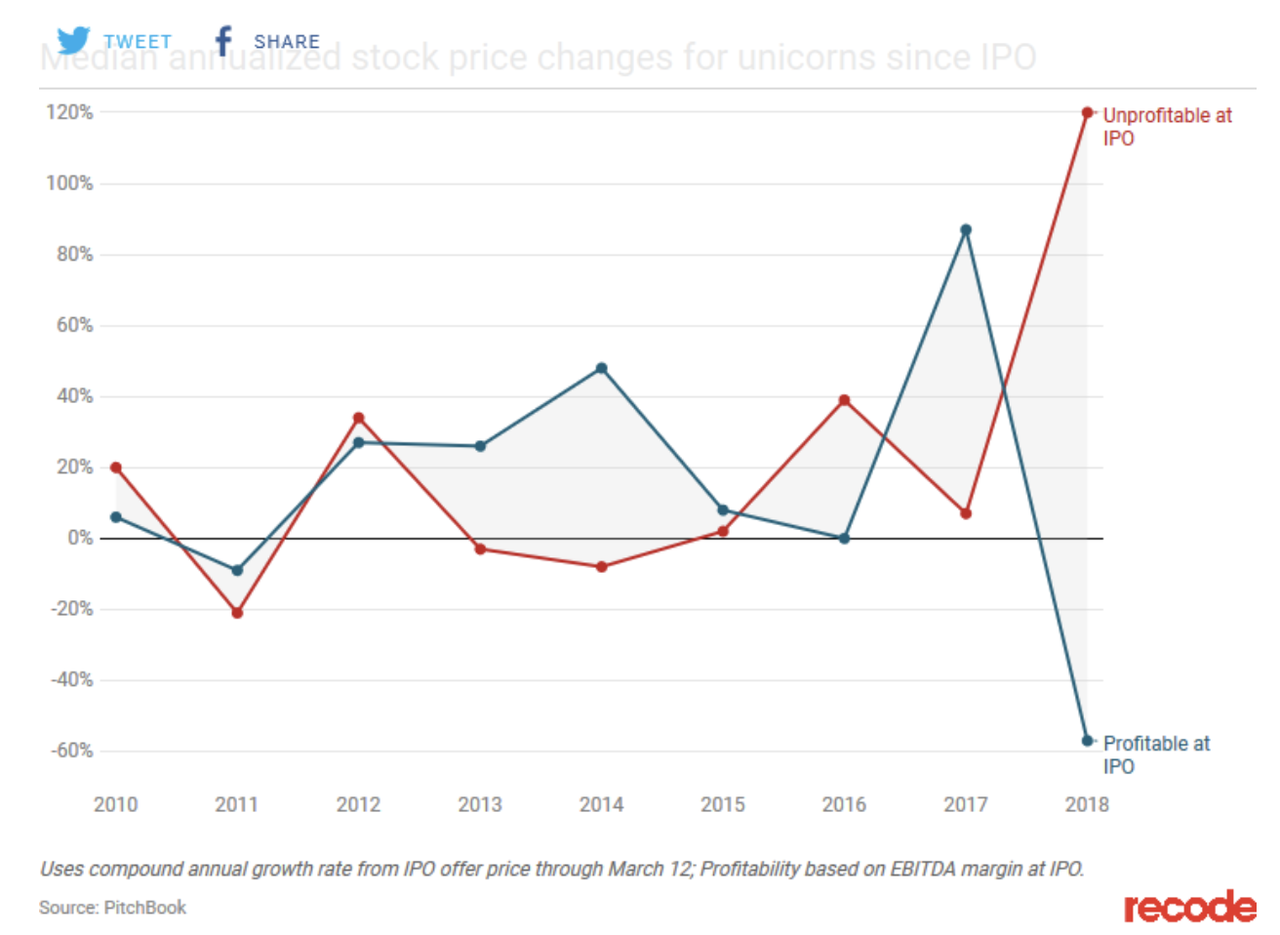

Yet, Uber, Lyft and Jumia should have known better. Stock markets can be incredibly capricious, with investor sentiment in a state of constant flux. Just last year, shares of unprofitable companies that IPO’d performed much better than those by their profitable peers.

However, experts were already warning earlier in the year that the mood had started to sour and the market was less likely to tolerate companies printing red ink.

(Click to enlarge)

Source: Vox

Mark Cuban, the billionaire investor and an early-stage Lyft investor to the tune of $1 million, told CNBC he thinks that both companies would have fared much better had they listed at the peak of their growth. Notably, Uber’s top line growth has slowed considerably, with 25 percent growth during the final quarter of 2018 being only a fraction what it used to be a few years ago.

Mark has even lambasted Silicon Valley’s venture capitalists, questioning their ability to accurately price pre-IPO companies.

Earnings on deck

Yet, Uber’s fate could get a lot worse when the company presents its first ever earnings scorecard to hostile shareholders after the close tonight.

“While investors have been expecting take rate compression as competition pushes irrationality and rider incentives in the near-term, we expect a focus on a path to improvement and accelerating revenue growth over the remainder of 2019 and into 2020, particularly as Lyft noted on its 1Q call that it believes the domestic rideshare market is becoming increasingly rational.’’

Uber has provided guidance for Q1 revenue of $3.0B-$3.1B and a net loss of $1.0B $1.1B. It’s going to be interesting to see whether investors will be willing to take Ives’ cue and play the long game. Just, don’t bet on it.

via ZeroHedge News http://bit.ly/2MjZDSl Tyler Durden

The group takes issue with three of the university’s policies: its restrictions on political leaflets, its bias reporting system, and the no-contact orders it issues to students accused of bias.

The first of these is the most obviously suspect from a First Amendment perspective. Students who wish to post leaflets or materials about candidates “for non-campus elections” must first receive permission from the administration.

“The University has no compelling interest in imposing a prior restraint on this category of political speech nor would this prohibition be narrowly tailored to any such interest,” the lawsuit says. “This rule chills protected speech and expression and forces students who do not wish to submit to this prior restraint to engage in self-censorship.”

The lawsuit also argues that because the university defines “bias incidents” very broadly—as any action orexpression motivated by hostility toward a protected group—its bias reporting system has the effect of chilling constitutionally protected speech. The no-contact directive empowers administrators to place limits on the rights of students involved in behavioral disputes; Speech First says this permits the university to punish students for mere expression. The lawsuit cites an example:

In November 2017, a graduate assistant, Tariq Khan, got in a shouting match with two students at an “anti-Trump” rally and subsequently broke one student’s phone. Two days later, another student, Andrew Minik—who was not at the event—wrote an article about the incident for the online publication Campus Reform. The article shared a video of the incident and described what had occurred at the rally.

Shortly after the article was published, Khan sought a No Contact Directive against Minik. The University issued the directive—even though Minik was not present when the dispute occurred and merely wrote an article about the dispute for Campus Reform. The No Contact Directive against Minik stated: “The Office for Student Conflict Resolution has become aware of a problem involving you and another student….Therefore, I am directing you to have NO CONTACT with Tariq Kahn (oral or written, directly or through any third party) until further notice.” The order warned that “[a]ny violation of this directive may result in charges before the appropriate Subcommittee on Student Conduct. Violations of no contact directives are taken very seriously and can have very significant consequences, including dismissal from the university.”

Speech First previously sued the University of Michigan, which prompted administrators to revise the wording of an overly broad harassment policy that had stated “the most important indication of bias is your own feelings.”

The University of Illinois did not immediately respond to a request for comment.

from Latest – Reason.com http://bit.ly/2VX7GnD

via IFTTT

The group takes issue with three of the university’s policies: its restrictions on political leaflets, its bias reporting system, and the no-contact orders it issues to students accused of bias.

The first of these is the most obviously suspect from a First Amendment perspective. Students who wish to post leaflets or materials about candidates “for non-campus elections” must first receive permission from the administration.

“The University has no compelling interest in imposing a prior restraint on this category of political speech nor would this prohibition be narrowly tailored to any such interest,” the lawsuit says. “This rule chills protected speech and expression and forces students who do not wish to submit to this prior restraint to engage in self-censorship.”

The lawsuit also argues that because the university defines “bias incidents” very broadly—as any action orexpression motivated by hostility toward a protected group—its bias reporting system has the effect of chilling constitutionally protected speech. The no-contact directive empowers administrators to place limits on the rights of students involved in behavioral disputes; Speech First says this permits the university to punish students for mere expression. The lawsuit cites an example:

In November 2017, a graduate assistant, Tariq Khan, got in a shouting match with two students at an “anti-Trump” rally and subsequently broke one student’s phone. Two days later, another student, Andrew Minik—who was not at the event—wrote an article about the incident for the online publication Campus Reform. The article shared a video of the incident and described what had occurred at the rally.

Shortly after the article was published, Khan sought a No Contact Directive against Minik. The University issued the directive—even though Minik was not present when the dispute occurred and merely wrote an article about the dispute for Campus Reform. The No Contact Directive against Minik stated: “The Office for Student Conflict Resolution has become aware of a problem involving you and another student….Therefore, I am directing you to have NO CONTACT with Tariq Kahn (oral or written, directly or through any third party) until further notice.” The order warned that “[a]ny violation of this directive may result in charges before the appropriate Subcommittee on Student Conduct. Violations of no contact directives are taken very seriously and can have very significant consequences, including dismissal from the university.”

Speech First previously sued the University of Michigan, which prompted administrators to revise the wording of an overly broad harassment policy that had stated “the most important indication of bias is your own feelings.”

The University of Illinois did not immediately respond to a request for comment.

from Latest – Reason.com http://bit.ly/2VX7GnD

via IFTTT

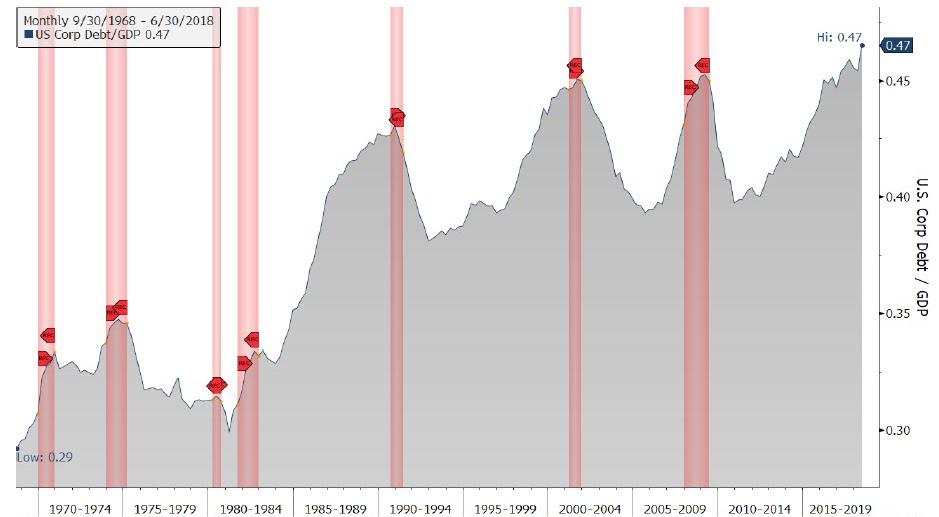

It seems the warnings from PIMCO’s Scott Mather that: “We have probably the riskiest credit market that we have ever had” in terms of size, duration, quality and lack of liquidity, Mather said, adding that the current situation compares risk to mid-2000s, just before the global financial crisis,”are being reflected in pricing and flows.

“We see it in the build up in corporate leverage, the decline in credit quality, and declining underwriting standards – all this late-cycle credit behavior we began to see in 2005 and 2006.” One way of visualizing what Mather was referring to is the following chart of corporate debt to GDP which has never been higher. As for the lack of creditor protections, well, just wait until the screams of fury begin after the next wave of bankruptcies.

While stocks have slowly woken up to the realities of the ‘recovery’, credit-markets have started to flash warnings that all is not well…

With some concerned that summer 2019 is echoing the risk-off deluge from Q4 2018…

And, as Bloomberg reports,traders yanked almost $429 million from State Street Corp.’s SPDR Bloomberg Barclays High Yield Bond ETF on Tuesday, the biggest withdrawal since December.

Mather’s rather ominous conclusion:

“I think that’s what you’re seeing now in markets. People are starting to come to a more realistic outlook about the forward-looking growth prospects, as well as the power of central banks to pump up asset prices.“

Considering that the S&P is about a few hundred percent higher than where it would be without central banks “pumping up prices”, the market is about to go through a lot of pain in the near future if the world’s largest bond manager is correct.

via ZeroHedge News http://bit.ly/2QCmU0f Tyler Durden

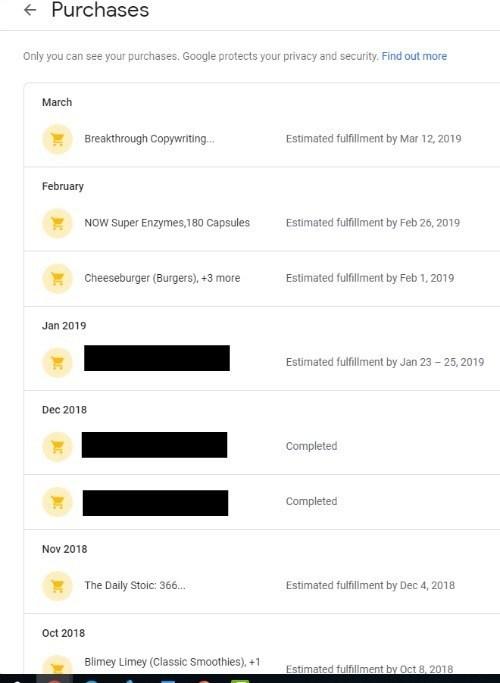

Google is very interested in your shopping habits – so much that the tech giant is collecting and saving your purchase history.

The company has been quietly keeping track of your online (and sometimes, offline) purchases for years, according to a recent report from CNBC.

In that report, writer Todd Haselton explains that he was looking around in his Google account and found something alarming:

A page called “Purchases ” shows an accurate list of many — though not all — of the things I’ve bought dating back to at least 2012. I made these purchases using online services or apps such as Amazon, DoorDash or Seamless, or in stores such as Macy’s, but never directly through Google.

But because the digital receipts went to my Gmail account, Google has a list of info about my buying habits.

Google even knows about things I long forgot I’d purchased, like dress shoes I bought inside a Macy’s store on Sept. 14, 2015. It also knows:

I ordered a Philly cheesesteak on a hoagie roll with Cheez Whiz and banana peppers on Jan. 14, 2016.

I reloaded my Starbucks card in November 2014.

I bought a new Kindle on Dec. 18, 2013, from Amazon.

I bought “Solo: A Star Wars Story” from iTunes on Sept. 14, 2018.

I decided to check my own Purchases page to see what kind of data Google has been collecting there and found this:

My purchase history goes back to October 2014 (!) but I decided not to share it all here in the interest of saving space (and sparing myself some embarrassment). I blacked out three personal items for, well, privacy reasons – as if privacy is even a thing these days.

I don’t shop online very often, I rarely opt-in to receiving email receipts, and I usually pay with cash when I shop or go out to eat, so I suspect that is why there isn’t much in my purchase history. Nonetheless, I find this disturbing, as someone who is becoming increasingly annoyed by the growing barrage of privacy invasions we all face.

For some, however, Google’s collection of purchase data could be quite embarrassing, as Bryan Clark explains in an article for TNW:

My girlfriend’s purchase history is a lot more interesting — our Amazon account is linked to her Gmail address. It’s there that Google could potentially find some intimate details, if it so chose. Not in our case, of course, as we’re both supremely boring individuals. But generally speaking this purchase data could reveal a lot about a person. It could point to an affair, for example (hotel receipts, clothing or gifts never given to a spouse), or let the cat out of the bag on an unannounced pregnancy. Google’s ledger, and the data within it, could track everything from mental illness to a woman’s menstrual cycle, all based on purchase data. (source)

Google won’t say why it is collecting purchase data or how long it has been doing so.

Google claims to care a great deal about privacy (ironically, at the top of the Purchases page, there is a note that says “Only you can see your purchases. Google protects your privacy and security. Find out more“), but the company sure is collecting an awful lot of data on folks, and is being pretty damn secretive about it.

CNBC reached out to Google to ask about purchase tracking. Here’s what a spokesperson told them:

“To help you easily view and keep track of your purchases, bookings and subscriptions in one place, we’ve created a private destination that can only be seen by you. You can delete this information at any time. We don’t use any information from your Gmail messages to serve you ads, and that includes the email receipts and confirmations shown on the Purchase page.” (source)

How long has Google been collecting purchase data? I can’t find an exact answer to that question, but it appears to be at least 9 years. In an article for The Verge, Nick Statt wrote:

Because I made my Gmail account nearly a decade ago, my purchase history stretches back as far as 2010, including purchases I made while I was a college student and those through Apple’s App Store, which has been linked to my Gmail account since its inception. It also includes some real-world transactions made using my credit card, thanks to point-of-sale software providers like Square and others that link your credit card number and name to an associated email account to deliver receipts, offer rewards programs, and, in some cases, collect valuable purchase data. (source)

Clark makes some additional (and disturbing) points:

Google has also proven unwilling to tell us how long this feature has existed, or why it’s logging offline purchases using certain point-of-sale terminals, like Square — meaning, it’s not just tracking purchases made online — but not others.

Before we jump to conclusions, however, it’s important to note that Google said back in 2017 that it would stop using collected Gmail data to serve personalized advertisements to its users. What’s troubling though, is that it might no longer need to. A 2018 Bloomberg report revealed that Google and Mastercard had reached a deal that would pay the latter millions for coughing up purchase data on its card holders. Google itself claims to have access to the purchase data of “approximately 70 percent” of US credit or debit card holders.

Regardless of how Google is using the data, if it’s using the data, the idea that this kind of ledger exists should be enough to give shoppers pause. (source)

Google says it doesn’t use your Gmail to show you ads and promises it “does not sell your personal information, which includes your Gmail and Google Account information,” and does “not share your personal information with advertisers, unless you have asked us to.”

Why, then, is the company collecting all this data?

Google wants us to believe this purchase tracking feature is for our benefit if we are to believe the explanation the company spokesperson provided to CNBC.

I am not buying it. Are you? If the company is providing this feature as a benefit to Google users, why not notify us that it exists?

We have plenty of reasons to distrust Google with our private data.

Google doesn’t exactly have a reputation for being upfront about data mining, as Statt points out:

This particular tool is not outright nefarious in an obvious way, but it does highlight Google’s struggle to transparently communicate its privacy policies and ad-tracking methods as Silicon Valley at large grapples with a more sensitive atmosphere around data privacy and security. The idea that this tool, and the technology to collect and present the data it provides, has existed quietly without a majority of Gmail users aware it exists echoes similar issues Google has faced over the last few years.

Those include a controversy over third-party app developers pulling data from the contents of Gmail messages, an auto-login feature for Chrome that would sync web browsing with your Gmail account, and reports that Google supplemented its ad-targeting tools with Mastercard purchase history data to provide advertisers a link between online ad impressions and real-world purchases. All of these situations contribute to a common theme: Google offers users a compromise that involves trading products and web services in exchange for data that the company will collect through a variety of means you may not know about and have little to no control over. That data is then used to help Google target ads, a division of its business that’s largely responsible for it becoming one of the most valuable corporations on Earth. (source)

Earlier this year, it was revealed that Google’s Nest Secure home security and alarm system has an embedded microphone system that the company conveniently failed to disclose to users. And, late last year, it was revealed that the Google app tracks users and sells their information.

Cybersecurity experts are expressing concern over the data collection.

David Shipley, CEO of Beauceron Security, told CBC he has three worries when it comes to Google tracking purchases: consent, the potential for abuse, and the amount of power that tech companies continue to collect:

“When people signed up for GMail years ago, Google never said that someday they’re going to do a super-creepy project where they’re going to collect all your receipts,” Shipley said.

Shipley said people should have been able to choose whether they wanted Google to collect their purchasing information in the first place.

“That’s the core of privacy and maintaining our digital rights online.”

He said the feature threatens people’s right to privacy online and offers an easy way for people to take advantage of others online.

“From an attackers standpoint, if they can hack into your GMail account, they now know where you buy from, and so they can now send scams and targeted attacks specifically to products and services you bought in the past,” Shipley said to CBC’s Shift.

“It is, from an information, privacy and control standpoint, absolutely staggering to realize just how far into everyone’s life Google reaches … If you’re using the web, you’re touching Google at some point in your day.” (source)

It is very difficult to delete your purchase history.

Haselton tried to delete his purchase history and had no luck:

But there isn’t an easy way to remove all of this. You can delete all the receipts in your Gmail inbox and archived messages. But, if you’re like me, you might save receipts in Gmail in case you need them later for returns. There is no way to delete them from Purchases without also deleting them from Gmail — when you click on the “Delete” option in Purchases, it simply guides you back to the Gmail message.

Google’s privacy page says that only you can view your purchases. But it says “Information aboutyour orders may also be saved with your activity in other Google services ” and that you can see and delete this information on a separate “My Activity” page.

Except you can’t. Google’s activity controls page doesn’t give you any ability to manage the data it stores on Purchases.

Google told CNBC you can turn off the tracking entirely, but you have to go to another page for search setting preferences. However, when CNBC tried this, it didn’t work — there was no such option to fully turn off the tracking. It’s weird this isn’t front and center on Google’s new privacy pages or even in Google’s privacy checkup feature. (source)

According to CNET, here is how to delete your purchase data:

To delete something, you can click on a purchase, which will bring up an itemized list of everything you bought in that transaction. You can then click the “i” button for information, and then on “where’s this from?”

Google will tell you if the purchase was found in your Gmail, after which you can either click “got it” or “view email.” You’ll then be taken to your Gmail account, the email will load, and you can delete it entirely.

Only then will the transaction disappear from your purchase history. (source)

Will you check to see if your data is being collected on a Google Purchases page?

via ZeroHedge News http://bit.ly/2EIFb7w Tyler Durden

{kind=link}