While the MSM peddled tin-foil Trump-Russian collusion conspiracies for more than two years, one pundit in particular stands head-and-shoulders above the rest; Rachel Maddow.

Night after night Maddow told lie after lie – promising her viewers Trump was finally, actually, definitively finished for one reason or another.

Maddow’s propaganda rants are too numerous to count – however The Nation‘s Aaron Maté is currently in the middle of a devastating Twitter takedown highlighting some of the MSNBC anchor’s most pathetic attempts to delegitimize the sitting president of the United States – after Maddow tweeted a Washington Post article about YouTube recommending an RT interview with Maté.

Enjoy – and be sure to click on Maté’s thread as it continues to unfold, and perhaps give him a follow.

1/ If YouTube were to recommend your show, it’d be recommending the leading purveyor of now debunked Trump-Russia conspiracy theories, falsehoods & innuendo of the last 2+ years. Here’s a sample:

3/ There was that time in Jan 2017 when you speculated that Putin may use the pee tape & other kompromat to force Trump into withdrawing US troops near Russia. How did that one turn out? pic.twitter.com/XuXXagyCNb

5/ Who could forget that time this past winter when you seized on life-threatening cold temperatures to fear-monger that Russia could kill Americans by knocking out their heat?pic.twitter.com/deo2H4SBBQ

7/ How about that time when you speculated — citing the Steele dossier — that Cohen billed Trump $50k for “tech services” to pay off Russian hackers? It was actually to pay a US firm (https://t.co/GGK6FQLvRJ). pic.twitter.com/TcqdN8mC4z

11/ Then there was that time when you lamented the suspension of US war games in Korea, and speculated that it was the fault of Putin: pic.twitter.com/cuDgHyDQPs

13/ Based on this sample alone, dare I say that your coverage of Trump-Russia very much amounts to the “deliberate trafficking in unreality”:pic.twitter.com/2OXbHhUDHa

15/ How about when you speculated that Maria Butina may have played a role in a secret Russian government plot to funnel money to the NRA in order to influence the 2016 election? How did that one pan out? pic.twitter.com/eaRgZdauty

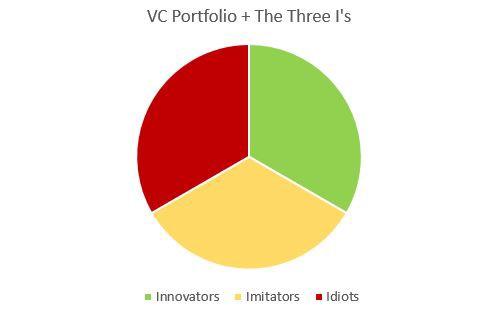

“First come the innovators, who see opportunities that others don’t. Then come the imitators, who copy what the innovators have done. And then come the idiots, whose avarice undoes the very innovations they are trying to use to get rich.”— Warren Buffet

A great deal of investing comes down to a process of identifying innovators, scrutinizing imitators, and screening out idiots.

This principle is applicable to everything from stock-picking to assessing management teams. Nowhere, however, is the concept more prevalent than in venture capital.

Every day, VC firms in Silicon Valley and beyond are inundated with pitches from startups touting innovative products and groundbreaking technology. Therefore, the clear determinant of a VC firm’s success lies in their ability to locate genius in a sea of mediocrity.

The obvious difficulty of this endeavor is reflected in the breakdown of a VC firm’s expected returns. As industry veteran Fred Wilson summarized it:

“I’ve said many times on this blog that our target batting average is ‘1/3, 1/3, 1/3’, which means that we expect to lose our entire investment on 1/3 of our investments, we expect to get our money back (or maybe make a small return) on 1/3 of our investments, and we expect to generate the bulk of our returns on 1/3 of our investments.” — Fred Wilson

To put it much more crudely:

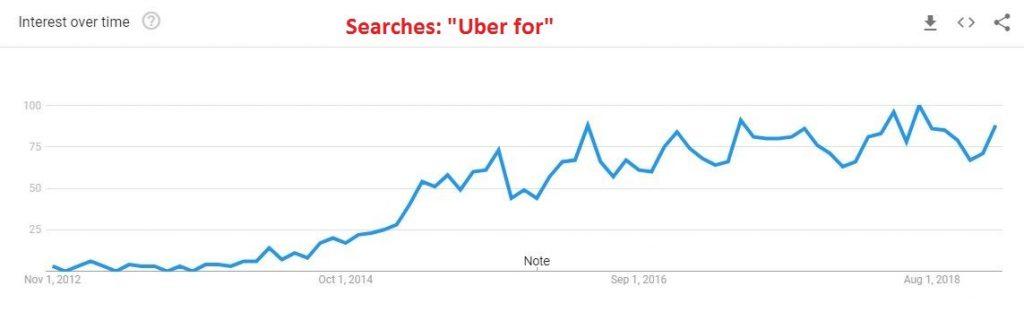

An already difficult process then becomes even harder after the wild success of a truly innovative company. For example, Uber’s dominance prompted an outbreak of “Uber for X” startups.

From a behavioral standpoint, it’s not easy for an investor to resist companies claiming to be the ‘Uber for X’ after witnessing Uber’s success.

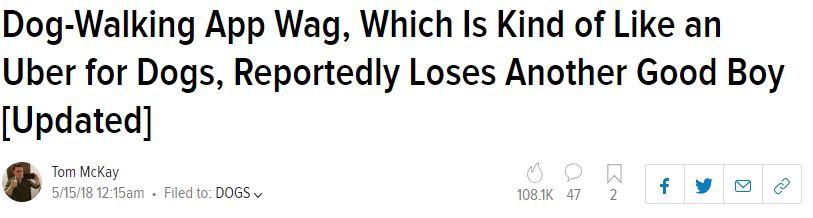

To be clear, there have been successful imitators. Wag!, the “Uber for Dogs”, being a prime example.

However, for every imitator like Wag! and Lyft, there is a longer list of failed imitators. Cherry, for instance, was the “Uber for carwashes” that eventually closed up shop.

That said, even the successful imitators aren’t perfect… poor Fluffy.

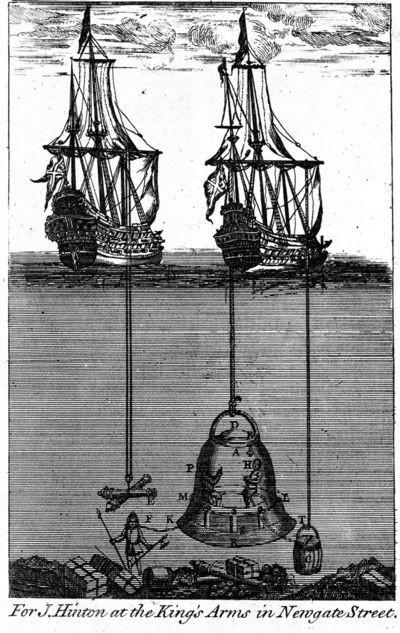

During the late 17th century, London’s nascent stock market experienced a wave of innovation. In 1687, only 15 public companies were listed on the London Stock Exchange. By 1695, however, that figure had increased tenfold.

The impetus for this investment boom is partially due to the Nine Years War, which restricted overseas trade with foreign powers. British investors were forced to deploy their capital into domestic investments as a result.

“A great many stocks have arisen since this war with France; for trade being obstructed at sea, few that have money were willing it should lie idle, and a great many that wanted employment studied how to dispose of their money…which they found they could more easily do in joint-stocks, than in laying out the same in lands, houses or commodities…” — John Houghton (1694)

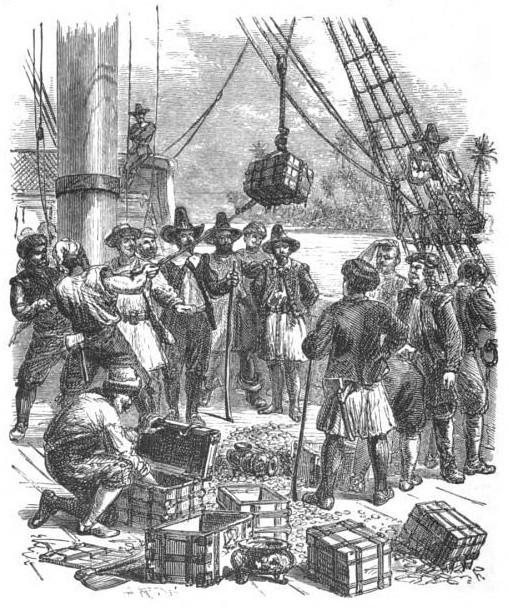

What truly kick-started this period of speculation and startup investments, however, was a successful treasure hunt.

The Innovator

“Thanks be to God! We are all made!”

— Sir William Phips (1687)

Sir William Phips was described by his contemporary, Daniel Defoe, as someone who “sought wealth and advancement through money-making schemes financed by others”.

A trader and seafarer by nature, Phips commanded boats making frequent trips to the West Indies. In the course of these journeys, Phips heard rumors of a sunken ship in the Caribbean , the Concepción, which held unimaginable treasures.

Though many would scoff at such gossip today, the rumors were not unfounded. The Spanish had transported scores of precious metals from Mexico for over a century, and many of these ships did not make it home.

Before long, Sir Phips decided to try his luck at locating the Concepción. Just as the modern founder ventures to Silicon Valley in search of funding on Sand Hill Road, Sir Phips returned to London in search of an investor.

Phips found his 17th century venture capitalist in the Duke of Albemarle, and his syndicate of investors. The group of financiers quickly formed a small joint-stock company for funding the expedition. This joint-stock company could be considered a VC firm equivalent.

This was truly ad-venture capital.

Eventually, the Duke of Albermarle proved to be one savvy venture capitalist. After endlessly searching for the sunken Concepción, Sir Phips finally located his treasure in 1687.

In the wake of his incredible discovery, Phips and his crew spent over two months hauling up 32 tonsof treasure from the ocean floor.

32 tons

Upon the treasure hunter’s return, the Duke of Albemarle and others received an astronomical 10,000% return on investment.

As for the captain himself, Phips took an 11% cut of the profit, which amounted to £12,000. This was an absolute fortune, as the average income for a merchant in 1688 was £400.

Sir William Phips represents a true Innovator. The treasure hunter had a bold, and risky business proposal, but offered an extremely enticing return if it proved successful.

The Imitator

“[Wreck-recovery companies] made much noise at this time, and shares for them were presented to persons of distinction to give reputation to the affair and to draw on others. So the patentees were sure to be gainers but the sharers under them lost all they paid in, some of whom, it seems, were men of good understanding but were allured by the hopes of getting vast sudden wealth without trouble.”- Anonymous (1692)

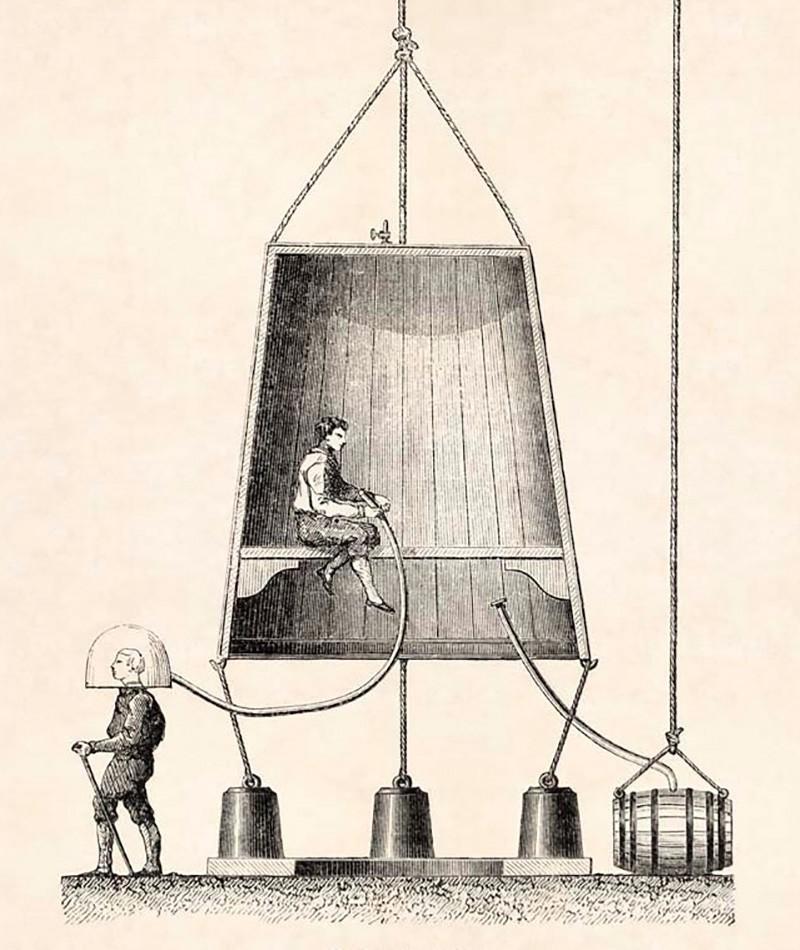

Reflecting the excitement surrounding new technologies and inventions, there were a record number of patents filed in London between 1691–1693,

The speculation in treasure hunting specifically is evidenced by the increase in patents related to diving and shipwrecks during the 1690s.

Over a 19-year period (1672–1689), there were 5 patents filed for ‘diving engines’. In just two years, however, there were 17 patents filed for diving engines from late 1691 to late 1693.

In this period, patents provided a level of status and credibility that investments from prestigious VC firms similarly offer startups today. One Londoner commented in 1695, “Oh, a patent gives a reputation to it, and cullies in [i.e. takes in] the company”.

While it’s unclear whether Phips had used a similar device himself, these new products captivated British investors. In response to investor’s thirst for a 10,000% return, new companies advertised diving engines for salvaging sunken treasure off the ocean floor.

The prospectus of one such company promised investor’s a 100% return.

Just as the success of modern companies like Uber led to an outburst of “Uber for X” companies, Sir Phips’ expedition sparked the formation of numerous diving and treasure hunting companies.

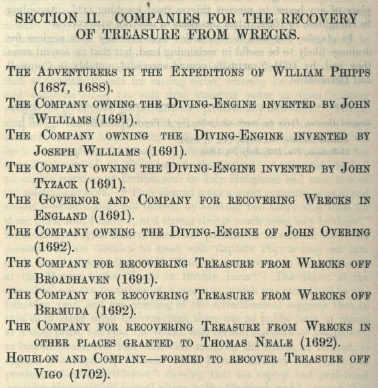

The below is only a partial list of such companies:

Despite the number of new companies formed to emulate Sir Phips’ success, “none of these expeditions were successful — indeed the only ‘finds’ consisted of a few cannons”.

The Idiot

“So I have seen shares in Joint-Stocks, Patents, Engines, and Undertakings, blown up by the air of great words, and the name of some man of credit…and many families been ruin’d by the purchase [of these shares].” — Daniel Defoe (1697)

In this bizarre treasure hunting bubble of the late 17th century there were plenty of idiots. On the funnier side, there were those that sought patents for ideas like “catching fish with lights”, and the “sea-crab” apparatus.

However, investors were just as idiotic. Typically sensible Londoners embraced their inner idiocy as the cravings for profits grew stronger. The bubble even drew in former critics:

“Captain Poyntz came forward with a petition on April 20th, in which he stated that persons who had secured patents for wrecks, sold shares at ‘extravagant rates and had as yet done nothing’. He too obtained a patent on April 29th.”

There were also many that suffered a fate similar to Daniel Defoe, who had invested and lost £200 in John Williams’ diving engine company. Later, he complained that Williams had only “pretended to be a skillful engineer in retrieving wrecks”.

Defoe, unable to identify Williams as an Idiot, was forced to deal with the consequences. Despite his best efforts to sue Williams, he eventually lost every penny of his investment.

Every investor wants to put their money in the Phips Treasure Hunt. However, finding Sir Phips is a treasure hunt in itself.

If you can identify Sir Phips before he embarks on his expedition, then the risk is worth the return.

Should you miss out on such a successful investment, however, ensure that you carefully scrutinize future opportunities borne out of its success. While imitators can certainly provide an attractive investment, you may end up holding shares in the “sea-crab” company.

Venture capital firms today acknowledge the difficulty of identifying the Innovator in how they construct their portfolios. The average investor should similarly ensure that they have a check in place.

Fail to identify the idiot in advance, and pretty soon you become the idiot yourself.

After losing his full investment in a sham diving company, Defoe lamented:

“I could give a very diverting history of a patent-monger…whose cully [fool] was nobody but myself” — Daniel Defore (1697)

via ZeroHedge News http://bit.ly/2LcJy08 Tyler Durden

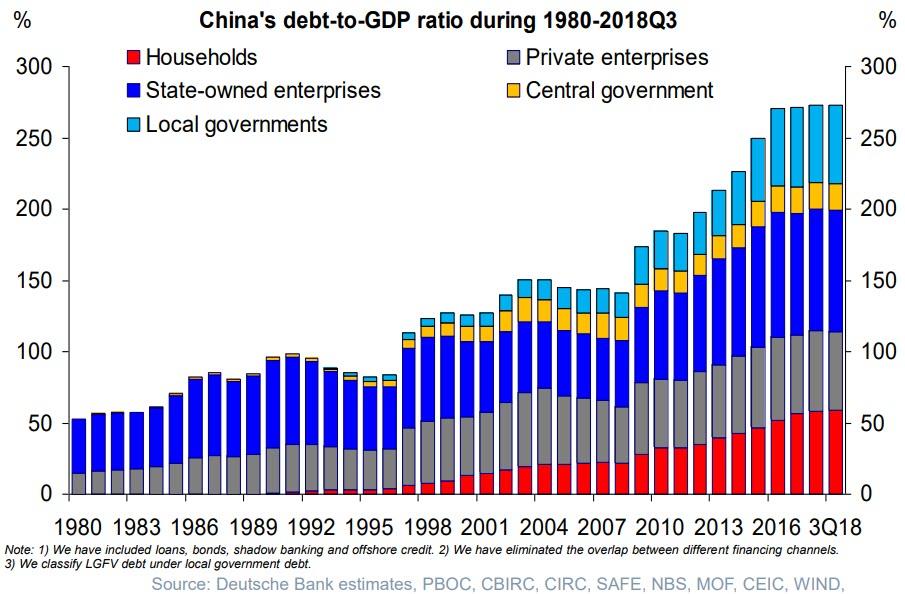

Back on January 9, when the S&P500 was just inches away from its Christmas Day bear market lows, we asked a simple question: is the Shanghai Accord 2.0 coming? Now, with the S&P back at all time highs, China unleashing a historic torrent of new credit after launching monetary and fiscal easing that shocked even the most cynical China skeptics and sent Chinese stocks soaring, and every central bank in the world reversing in the Fed’s footsteps and scrambling to cut rates as the global race to the currency bottom entered what may be its final lap, we have the answer.

Or do we?

For those who are rightfully confused, because while there are countless similarities between the “2016 scenario” and current markets, there are also some very specific differences, here is a great recap of the similarities and differences, excerpted from the latest weekend note by One River asset management’s CIO, Eric Peters:

Deja Vu

“Everyone’s thinking it’s 2016 all over again,” said the CIO. A global growth scare, equity weakness, dollar strength and commodity declines prompted central bankers to hash out the Shanghai accord in early 2016 that dramatically reversed these trends. “They’ve seen China ease this year, the Fed pivot, equities rebound,” he said. By late-April in 2016, the S&P 500 had jumped 17% from the Jan 2016 lows (this year it rallied +20%), and by late-April 2016, Chinese stocks rose +16% (this year +40%). “They’ve looked at this and said green light, risk on.”

“Pulling out the 2016 playbook, people piled into reflation trades,” continued the same CIO. “Short dollar trades, crap beats quality, dash for trash, EM equities and FX, commodities.” By late-April 2016, oil had surged +70% from the Jan 2016 lows (this year +50%), copper rallied +20% then (this year +18%). The dollar index had fallen -6% in 2016 (but this year DXY is up +1%), gold surged +23% (but this year flat). “The dollar and gold are saying 2019 is different from 2016, and if that’s right, people need to exit their reflation trades.”

“China doesn’t appear to have the stomach for a massive stimulus above what they’ve already done,” said the CIO. “At a certain level, the efficiency of each additional dollar of credit you pump into a system declines to the point where new debt is almost entirely used to service old debt.” By late-April 2016, emerging market equities had rallied 28% from the Jan lows (this year just +17%), and Baltic Dry shipping rates surged 160% (+26%). “This year’s response lacks the oomph of the 2016 rally, which was itself weaker than the 2009 explosion.”

All this can be seen in the feeble rebound in China’s Credit Impulse which despite the record injection of credit in Q1, has barely pushed off its all time lows.

RMS:

“As long as we’re negotiating, it seems good for stocks,” said the investor. On Mar 1st, 2018, Trump announced 25% steel tariffs and said, ‘Trade wars are good and easy to win.’ From those levels, the S&P 500 has traded both 10% higher and lower and is now at a record. In the meantime, the administration put our CEOs on notice that China is not a great link in their global supply chains. “We want a US exodus from China, but at a pace that doesn’t sink the ship. If you’re on a lifeboat on the Titanic, you give yourself some distance before it goes down.”

“The challenge we face is that in the process of our politicians attempting to disentangle the US from China, our financiers are sending them widow and orphan money,” said the investor. The April 1st MSCI inclusion of Chinese bonds into its index is the latest example of moves that will passively shift $150bln-$200bln+ a year in US retirement savings to China. “Without these flows, Beijing has a real problem. They need Wall Street’s help. They’re no longer running a current account surplus. And Washington is going after their trade surplus.”

“The lure of China has proved irresistible,” he said. “But when you climb aboard, remember their rules are different. Take Alipay, the world’s largest payment platform. Jack Ma woke up one morning and told Alibaba shareholders he was taking it.” That was in 2011, at an estimated $2bln value. There was no lawsuit. No recourse. It’s now worth $150bln. “When people buy BABA stock today, they don’t even own Alibaba. They own an American Depository Receipt (ADR) on a Cayman company with rights to Alibaba cash flows. Good luck with that.”

via ZeroHedge News http://bit.ly/2UOl653 Tyler Durden

Every year, thousands of people in need of kidney transplants endure greatly suffering because there are not enough organs available to satisfy the demand. They can survive—for a time—only by going through the difficult and time-consuming process of kidney dialysis A recent Canadian Broadcasting Corporation article effectively conveys the pain involved:

Blair Waldvogel wishes he didn’t have to spend so much time in his basement. But if he doesn’t, he’ll die.

The 52-year-old Winnipeg father has been on Manitoba’s kidney transplant list for the past eight years. His Type O blood means Blair can only receive a kidney from a Type O donor and he hasn’t been able to find a match.

So, four days a week, Blair Waldvogel goes downstairs to the guest bedroom, hooks himself up to his home dialysis machine, and sits there for four hours while the machine cleans his blood.

“I never imagined I’d get to eight years,” said Blair…..

If you include the time it takes to set up the machine and to clean up afterwards, Blair has spent the equivalent of 348 days in his basement on dialysis.

“There have been some scary, scary times along the way,” said [Blair’s wife] Irene. She has had to call paramedics more than once after Blair passed out in his dialysis room because his blood pressure dropped too low.

As the article describes, kidney dialysis makes it extremely difficult to continue to live a normal life. Blair Waldvogel, for example, has had to quit his job as the president of the North American recycling program for an international steel company. The article also correctly notes that many dialysis patients endure even greater suffering than the Waldvogel family. And, every year, thousands die because organs do not become available in time to save them. Indeed, Mr. Waldvogel is somewhat fortunate to have survived for eight years on kidney dialysis, because the average life expectancy of dialysis patients who cannot get a transplant is only 5-10 years. The case described in the CBC article is in Canada. But the situation in the United States is no better.

In addition to the pain endured by patients and their families, society loses as well, due to patients’ reduced productivity and the enormous expense of dialysis treatment (much of it subsidized by federal and state governments).

Nearly all of this death, suffering, and waste could be eliminated if only the US and Canadian governments would legalize organ markets, thereby increasing the supply of kidneys. For reasons I summarized here, laws banning organ markets are the moral equivalent of actively killing innocent people:

The injustice of status quo policy is more than just a matter of failing to help people in need. It is the equivalent of actively killing them. Consider a situation where Bob needs to buy food in order to keep from starving. Producers are willing to sell him what he needs at market prices, but the federal government passes a law saying that it is illegal to sell food for a profit. Bob is only allowed to acquire such food as producers are willing to give him for free. If Bob starves as a result, the government is actively culpable for his death. It cannot claim that it was merely an innocent bystander who refused to help him in his time of need. The same point applies if the government (or anyone else) uses coercion to prevent people from selling organs that ESRD patients need to live.

Unlike in the case of food, it is unlikely that ESRD patients would buy what they need directly from sellers. Most likely, the actual purchases would be done by hospitals, health insurance companies, and other specialized enterprises, which could screen them for quality and then offer them to patients (as is the case with many other types of transplants and complex medical supplies). But that does not change the morality of the situation.

By legalizing organ markets, we can save thousands of lives and greatly curtail the kind of suffering now needlessly endured by the Waldvogel family and thousands of others. As an extra bonus, we can also increase economic productivity and reduce health care costs in the process. Few if any other policy reforms can achieve such enormous gains at so little cost.

from Latest – Reason.com http://bit.ly/2UN1o9I

via IFTTT

“Ignoring MMT’s rising popularity would be about as smart (and effective) as a dog barking at the waves in the ocean.”

–KEVIN MUIR, author of the avant garde financial newsletter, The Macro Tourist

“I believe that all good things taken to an extreme become self-destructive and that everything must evolve or die. This is now true for capitalism.”

–RAY DALIO, founder of hedge fund behemoth, Bridgewater Associates

INTRODUCTION

The final lap. It’s hard to believe that as recently as February, when I first brought up the concept of a new economic model that was poised to radically alter the world we’re living in, MMT was as obscure as an extra in an old Cecil B. DeMille bible film. Yet, a mere two months later, you have to try extremely hard to ignore Modern Monetary Theory and its swelling number of disciples.

Perhaps at this point, some of you who have read the three previous installments of our month-long series on MMT wish I’d never brought it your attention. You might even think it’s such a zany idea that it will never see the light of day. If so, you could be right—but I doubt it.

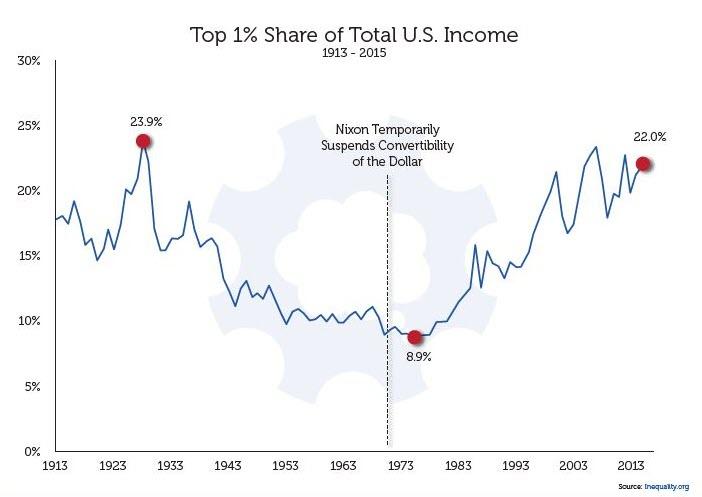

Prior issues of this series have made the point that ultra-low and, even, negative interest rates have led to a boom in asset prices at the expense of the real economy. This has created the most lop-sided income distortion since 1929.

Source: Grant Williams, TTMYGH (2/10/2019)

Even after 10 years of a long and sluggish expansion—which happily has driven unemployment down to 50-year lows–there is an unmistakable whiff of outrage in the air. The non-1% or, perhaps more accurately, the non-5%, are coming to believe they’ve been stiffed by the reality revealed in the above chart.

Perhaps that’s why a number of the uber-rich (with thousands more of those soon to be created when Uber goes public) are suggesting MMT as a viable solution to this seemingly intractable problem of secular stagnation (i.e., a long period of sub-par economic growth) and income/wealth disparity. This realization has also caused Wall Street billionaires like Ray Dalio to openly warn of class warfare, including of the violent variety. As noted in the April 12th EVA on MMT, a number of Wall Street’s finest (is that an oxymoron?) are endorsing it as a way to break out of the current quagmire of low inflation and economic lethargy. But of course they would! After all, who is better on figuring out how to profit from a game-changing economic model like MMT than the Wizards of Wall Street.

That’s a good segue to this week’s MMT issue written by Charles Gave. Long-time EVA readers are well aware that Charles is one of my favorite economic thinkers. In his piece on MMT, he goes back in time to review some of the much earlier dalliances with the alluring theory that governments can spend almost at will. He particularly examines the experience his native country of France has had in this regard. What you will read is that the well-connected elites (the Wizards of Wall Street of their era) were able to make a killing—at least for those who managed to avoid being killed themselves–during the booms and inevitable busts that accompany such policies.

Ronald Reagan used to say that there are two kinds of economists. The first, usually disliked by politicians, believe like Milton Friedman that there is no such thing as a free of lunch. The second, very much liked by politicians, believe that if only the government were to spend more, growth would accelerate for the greater good of all. Reagan would then go on to say that the first kind tend to believe in God, and the second kind believe in Santa Claus. Unfortunately, Santa Claus doesn’t exist.

With all the talk about Modern Monetary Theory, we appear to be back in Santa Claus territory. Even the name is a complete misnomer; the proposed policy is neither modern, nor is it truly about money, nor is it much of a theory.

MMT is not modern

Financing government spending by printing money is as old as paper money itself. The Song Dynasty did it. The Weimar Republic did it. And Robert Mugabe and Nicolás Maduro both did it. But perhaps the closest historical parallels to today’s MMT proposals are to be found in 18th century France— two of them in the same century!

The first attempt at what we might call Early Modern Monetary Theory came after John Law fled to France to escape justice in Britain (perhaps Perfidious Albion sent him to France to ruin what was then the predominant economic power in Europe?). John Law was a brilliant Scot and a professional gambler, with the mental ability to calculate all sorts of odds in a flash. Through gambling circles, he came to meet the Duke of Orleans, the young Louis XV’s uncle and Regent. This gave Law the opportunity to present what he called his “system”.

It worked like this. First, the French Treasury would issue paper money convertible on demand into gold. Second, a bank would be created (one of the first central banks in history) and this bank would issue shares allowing holders to participate in the guaranteed growth of a French colony in North America called Louisiana (at the time Louisiana stretched from New Orleans to the borders of French Canada). The shares could be subscribed for using the government debt at par (while the debt traded at 30% of face value, since it paid no interest). Or shares could be purchased using the paper money issued by the French Treasury and backed by a gold inventory (which would disappear over time).

The Regent was quick to catch on and realized that, with Law’s system, France’s debt (which had gone through the roof following years of over-spending under Louis XIV), would quickly evaporate. The system was launched. The share price of the central bank rocketed, and soon the whole of Paris was caught up by a speculative mania unprecedented in French history.

Unfortunately, Louisiana never paid a dividend and the share price collapsed. The French middle class, having traded government debt worth 30% of its face value for shares worth nothing, was wiped out. But at least the French government was solvent again.

Not everybody lost out. Richard Cantillon, an Irish economist living in France, made a fortune (it’s not every day that an Irishman gets to take all the money from a Scotsman’s wallet). Cantillon had sold short the shares of the bank, and for good measure also sold the French currency against sterling. In his Essay on Commerce (a must-read), Cantillon became the first scholar to explain the difference between the creation of money and the creation of wealth, and that the first did not automatically lead to the second.

Cantillon further understood and explained that if the government is intent on destroying the local currency, then those who are the closest to the central bank will make money, while the rest of the population will end up on the losing side. Since dubbed “the Cantillon effect”, this understanding foreshadowed the Wall Street versus Main Street debate ignited by the era of zero interest rate policies over the past decade.

France’s second attempt at EMMT took place during the French Revolution. Facing a cash crunch triggered by the upheaval in France’s institutions, the new revolutionary government elected to nationalize the assets (mostly land) of the French Catholic church and print “assignats” whose values were backed by the church lands. However, the temptation to print proved too strong. In short order the number of assignats grew far above the value of the underlying assets, triggering a collapse in the value of assignats.

Still, if one was connected to the new revolutionary government, one could buy the old church assets either in gold, or at the face value of the assignats. This provided a live example of the Cantillon effect in action. The connected bourgeoisie of Paris and other French metropolitan centers bought the former assets of the French church at one-tenth of their value. Eventually, when there were no more church assets left to buy, and when the value of assignats had collapsed to near zero, the revolutionary government organized a “bankruptcy of the two-thirds”. The government announced that France’s debt would not be paid back at face value. Instead, the holder of the debt would receive a perpetual piece of paper worth one-third of the original value of his holdings, paying a fixed rate of 4%.

Needless to say, ahead of the announcement, those “in the know” rushed to buy up the paper, which was trading at 5% of its face value or less, in massive volumes. Once again, the well-connected made a fortune, when the paper was exchanged at 33%. Again, the Cantillon effect, and again the objective was achieved: the French state was restored to solvency. And in the process a whole class of nouveaux riches had been conjured into existence, while the rest of the population, especially the middle class, was left much poorer.

Funnily enough, this appears to be the outcome of every historical example of massive monetary printing: a solvent state, a new class of nouveaux riches, and a wiped-out middle class. These examples lead to my second point: MMT cannot be described as a monetary theory. The reason is simple: its proponents do not understand what money is.

It’s not really about money

MMT proponents seem to believe that issuing money is, and will always remain, a state monopoly. But when one considers money, one looks at it first as a means of payment (which can be, and often is, organized by the state). And second, one looks at the value of this money. This second aspect (at least outside totalitarian communist states) can never be determined by the state. The value of money is, and has always been, determined by myriads of transactions, each taking place freely between two or more individuals. Thus, the supply of money can be controlled by the government, but its value cannot. This implies that money is a common good, and can never be a tool of the government.

In fact, of the three functions of money—means of payment, unit of account, and store of value—the only one that MMT proponents seem to consider is the means of payment, which the government guarantees by using brute force. This probably explains why previous examples of MMT—Venezuela, Zimbabwe, the Weimar Republic, Revolutionary France—have tended to lead to tyranny or economic collapse, or both.

Economic collapse follows because, in such a system, the unit of account function breaks down, leaving the population to resort to barter. But economic collapse also happens because the main damage is sustained by the store of value function, especially when it comes to international transactions. It’s as safe a bet as you can make that foreigners will not be very keen to stockpile the bank notes (or government debt) of a country openly embracing MMT.

As a result, any country implementing MMT will have to maintain a current account surplus at all times. Very likely, international trade with the country will tend to drift towards barter. Inside the MMT country, a black market in foreign bank notes, gold and diamonds will spring up almost immediately. And corruption will go through the roof, because when civil servants are in charge of awarding import permits, the first thing any importer has to buy is the civil servant.

For proponents of MMT, money is simply the unit of payment they program into their computers to build their theoretical model of the flows in the economy. Like typical Keynesians, they pay no attention to the balance sheet effects of their policies. Unfortunately, a real economy, or a business, is not the end sum of positive “rates of change” differentiations in the short term, but the result of “area under the curve” integrations over the long term. This brings us to the theory aspect of MMT.

MMT is not much of a theory

Frédéric Bastiat used to say that, when it comes to economics, there is always “what you see, and what you don’t see”. In this respect, any theory which looks solely at a country’s, or a company’s, income statement, without also looking at the potential damage done on the balance sheet side of the equation, is not much of a theory at all. Such a “theory” would focus solely on the “what you see”, and moreover on the “what you see right now”.

Take a decline in interest rates as an example. At first glance, lower interest rates should be good for economic activity. They lead to more consumption, more capital spending, and so on. But if that were really all there was to it, wouldn’t our ancestors have figured things out long ago, and adopted ZIRP forever? And wouldn’t Medieval Europe, with its laws against usury, have been a hotbed of economic dynamism?

Perhaps the answer is that abnormally low interest rates destroy the long-term savings industry. And since, in a closed economy, savings equals investment, low interest rates lead to a collapse in capital spending, which leads to a collapse in productivity, which in turn implies a lower standard of living. Meanwhile, because of the Cantillon effect, the rich get richer, while the poor do not. In a democracy, this usually results in the replacement of the ruling elite by somebody else, even by somebody described as a “populist”. And populists sometimes do things that are even stupider than economists’ recommendations, such as increasing the weight of government spending in GDP.

All of which brings us to the populists advocating today’s MMT. True MMT believers aim to manage something they call “aggregate demand” by guaranteeing incomes for all. This will eliminate poverty and restore humanity to the Garden of Eden. In short, the solution to all our economic problems is to pay people not to work, with money that didn’t exist a week ago. It is amazing that no one ever thought of this before. Undeniably, such a scheme will boost demand.

The problem will be supply. Efficient supply comes through a mechanism described by Joseph Schumpeter and called Creative Destruction. But in our MMT paradise, no destruction will be allowed. And no destruction means little, if any, creation. The result will be something akin to North Korea, Maoist China, or even France, where government spending as a proportion of GDP has been going up relentlessly for 40 years under the direction of people who specialize in managing aggregate demand.

The conclusion is simple:MMT proponents know nothing about economic history, do not understand the nature of money, which is not a state monopoly but a common good, and believe unquestioningly in their theories without pursuing them to their logical conclusions.

via ZeroHedge News http://bit.ly/2DGbOSS Tyler Durden

Every year, thousands of people in need of kidney transplants endure greatly suffering because there are not enough organs available to satisfy the demand. They can survive—for a time—only by going through the difficult and time-consuming process of kidney dialysis A recent Canadian Broadcasting Corporation article effectively conveys the pain involved:

Blair Waldvogel wishes he didn’t have to spend so much time in his basement. But if he doesn’t, he’ll die.

The 52-year-old Winnipeg father has been on Manitoba’s kidney transplant list for the past eight years. His Type O blood means Blair can only receive a kidney from a Type O donor and he hasn’t been able to find a match.

So, four days a week, Blair Waldvogel goes downstairs to the guest bedroom, hooks himself up to his home dialysis machine, and sits there for four hours while the machine cleans his blood.

“I never imagined I’d get to eight years,” said Blair…..

If you include the time it takes to set up the machine and to clean up afterwards, Blair has spent the equivalent of 348 days in his basement on dialysis.

“There have been some scary, scary times along the way,” said [Blair’s wife] Irene. She has had to call paramedics more than once after Blair passed out in his dialysis room because his blood pressure dropped too low.

As the article describes, kidney dialysis makes it extremely difficult to continue to live a normal life. Blair Waldvogel, for example, has had to quit his job as the president of the North American recycling program for an international steel company. The article also correctly notes that many dialysis patients endure even greater suffering than the Waldvogel family. And, every year, thousands die because organs do not become available in time to save them. Indeed, Mr. Waldvogel is somewhat fortunate to have survived for eight years on kidney dialysis, because the average life expectancy of dialysis patients who cannot get a transplant is only 5-10 years. The case described in the CBC article is in Canada. But the situation in the United States is no better.

In addition to the pain endured by patients and their families, society loses as well, due to patients’ reduced productivity and the enormous expense of dialysis treatment (much of it subsidized by federal and state governments).

Nearly all of this death, suffering, and waste could be eliminated if only the US and Canadian governments would legalize organ markets, thereby increasing the supply of kidneys. For reasons I summarized here, laws banning organ markets are the moral equivalent of actively killing innocent people:

The injustice of status quo policy is more than just a matter of failing to help people in need. It is the equivalent of actively killing them. Consider a situation where Bob needs to buy food in order to keep from starving. Producers are willing to sell him what he needs at market prices, but the federal government passes a law saying that it is illegal to sell food for a profit. Bob is only allowed to acquire such food as producers are willing to give him for free. If Bob starves as a result, the government is actively culpable for his death. It cannot claim that it was merely an innocent bystander who refused to help him in his time of need. The same point applies if the government (or anyone else) uses coercion to prevent people from selling organs that ESRD patients need to live.

Unlike in the case of food, it is unlikely that ESRD patients would buy what they need directly from sellers. Most likely, the actual purchases would be done by hospitals, health insurance companies, and other specialized enterprises, which could screen them for quality and then offer them to patients (as is the case with many other types of transplants and complex medical supplies). But that does not change the morality of the situation.

By legalizing organ markets, we can save thousands of lives and greatly curtail the kind of suffering now needlessly endured by the Waldvogel family and thousands of others. As an extra bonus, we can also increase economic productivity and reduce health care costs in the process. Few if any other policy reforms can achieve such enormous gains at so little cost.

from Latest – Reason.com http://bit.ly/2UN1o9I

via IFTTT

President Trump bailed on the White House Correspondents Association Dinner Saturday night – instead heading to Wisconsin to deliver a fiery speech to a packed Green Bay arena.

“There’s no place I’d rather be than right here in America’s heartland… and there’s no one I’d rather be with than you, the hardworking patriots that make our country run so well,” said Trump.

Meanwhile, a sad trombone could be heard whomp-whomping at the Trump-less WHCA dinner – where instead of the traditional comedian, association president Olivier Knox balled up his fists and gave a fear-mongering sermon about poor MSM reporters who Trump has endangered with his rhetoric.

It’s hard to accurately convey the somber tone in the room post-Mueller report, as the room full of journalists who have peddled Trump-Russia conspiracy theories for more than two years cried into their wheaties.

This sums up the WHCA dinner

“I don’t want to dwell on the president,” said Knox. “This is not his dinner. It’s ours, and it should stay ours. But I do want to say this. In nearly 23 years as a reporter I’ve been physically assaulted by Republicans and Democrats, spat on, shoved, had crap thrown at me. I’ve been told I will never work in Washington again by both major parties.”

“And yet I still separate my career to before February 2017 and what came after,” Know continued. “And February 2017 is when the president called us the enemy of the people. A few days later my son asked me, ‘Is Donald Trump going to put you in prison?” At the end of a family trip to Mexico he mused if the president tried to keep me out of the country, at least Uncle Josh is a good lawyer and will get you home”

“I’ve had to tell my family not to touch packages on our stoop,” Knox bemoaned. “My name is on a statement criticizing the president for celebrating a congressman’s criminal assault on a reporter. I’ve had death threats, including one this week. Too many of us have. It shouldn’t need to be said in a room full of people who understand the power of words but fake news and enemies of the people are not punch lines, pet names or presidential. And we should reject politically expedient assaults on the men and women whose hard work makes it possible to hold the powerful to account.” (h/t Grabien).

Watch:

via ZeroHedge News http://bit.ly/2GD3QdM Tyler Durden

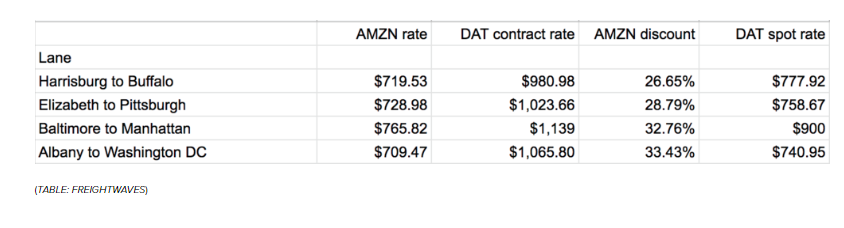

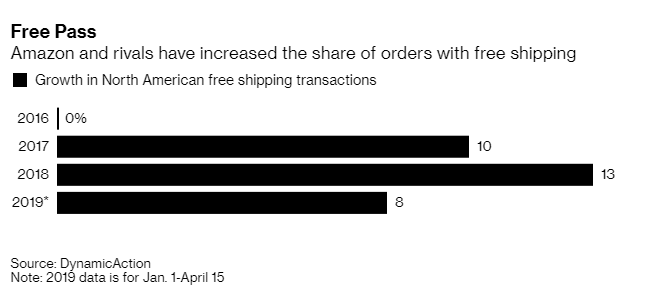

In what is being called a “nightmare come true” for freight brokers and carriers, Amazon did what it traditionally does every time it enters a new market, and took its own digital freight brokerage platform live while undercutting prevailing market prices by 26% to 33% in the latest deflationary race to the pricing bottom in order to grab market share, according to FreightWaves.

Late last week, Morgan Stanley equities analyst Brian Nowak had predicted this was going to happen, stating: “We see AMZN’s 1-day Prime shipping raising consumer expectations and increasing the cost to compete in e-commerce. Over the long term, we also see this as a Trojan horse for Amazon to grow its next disruptive business… a third party logistics network.”

Amazon already has an extensive network of trucking carriers as it moves an enormous amount of freight across the country. Having their own third-party logistics network was just an obvious next step for the behemoth of a company that relies so much on shipping. The benefits are plentiful for Amazon: they get to hedge against the volatile price of trucking capacity and they get to expand their infrastructure, while turning part of their costs into revenue. Amazon is already a top 10 international freight forwarder for Asian ocean freight inbound to North America.

Amazon explained the company’s strategy by stating: “The advantages that then come from disintermediation and the monetization of those capabilities are secondary to the immediate need of self-preservation, but then serve to feed very critical needs of Amazon’s ability to continue to succeed. This innovation and growth then manifests as continuously evolving towards the ability to sell everything and anything that is or can be sold. That’s the true Amazon flywheel: disintermediate to survive; monetize to fund innovation; innovate to grow; disintermediate to survive…”

Amazon’s entry into freight brokerage is an attempt to re-accelerate its top line, which has slowed from 30% annually three years ago to less than 15% this year. The company is trying to not allow trucking capacity to constrain its growth and, for now, it is coming in at price points that are far below market prices. This indicates that Amazon is not trying to realize enormous gross margins at first. The company’s new portal is intended for those who want Amazon‘s rates for full truckload dry van freight in Connecticut, Maryland, New Jersey, New York, and Pennsylvania. Based on these rates, the company is essentially a “free, marginless brokerage”.

Eventually, down the road, the company will monetize this. But for right now, the company is focused on deploying a massive amount of capital to rapidly scale up its network on thin margins to get started. Prices will eventually creep up once Amazon has penetrated the market (read obliterated the competition), not unlike Amazon’s original business model decades ago.

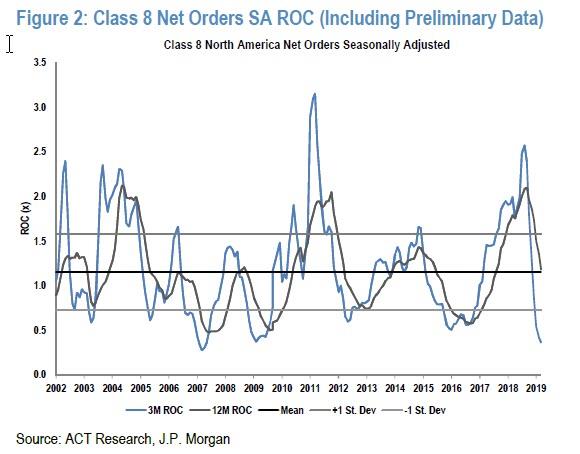

Amazon’s new business will surely result in even more carnage in the Class 8 “heavy duty” order industry, where as we reported a few weeks ago, order for Class 8 trucks collapsed an astounding 66%, which decline is attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term, however it is also likely that concerns about the economic slowdown are also playing a major part in the latest collapse. Specifically, March Class 8 net orders were just 15,700 units (16,000 SA; 192,000 SAAR), down 66% YoY from 49,600 a year ago and down 6.7% sequentially.

“March marks the fourth consecutive month of orders meaningfully below the current rate of build,” said Steve Tam, vice president of ACT. During that four-month period, Class 8 orders have been booked at a 194,000 seasonally adjusted annual rate, or SAAR. This is down significantly from 489,000 SAAR for the same period a year earlier, Tam said.

And it’s only going to get worse now that Amazon is taking over. The company spent $7.3 billion on transportation in the first quarter of 2019, which is lumped together with sortation and delivery costs in its “shipping cost” line item. Amazon’s shipping costs for the year, annualized, are approximately $87.6 billion and FreightWaves predicts that it could be years before investors start asking about margins on this business.

Building out this network could also allow Amazon to “blowout retail peak season”. By sacrificing margins up front, the company will have capacity locked up to move record breaking volumes during the holiday season. This is also another step Amazon is taking to try and get a leg up against competitors like Walmart. We just reported hours ago that Walmart was looking to get into one day shipping without a membership fee to compete with Amazon. Now, it looks as though Amazon has volleyed that ball right back into Walmart’s court.

Walmart has offered free two-day shipping on orders of $35 or more since early 2017, which helped it keep up with Amazon. And while Amazon still accounts for about half of all e-commerce spending in the United States, this $35 threshold has also been taken on by other retailers, like Target, to help offset the cost of delivery.

Total retail transactions with free shipping were up 13% in North America last year and were up 8% through April 15 of this year. Amazon Prime now charges customers monthly and annual fees, amounting to about $119 in the US for a year. Prime customers get shipping discounts and free two day delivery on most items.

via ZeroHedge News http://bit.ly/2VrqVtq Tyler Durden

The final phase of a bull cycle is the most deceiving. It is the time when things are at their best, optimism runs wild, equities can do no wrong and any warning signs are dismissed as equity price action valiantly defies the reality that is to come.

It is also a time when complacency makes a comeback as big rallies emerge following initial larger corrections. 2018 was a year of big corrections. 10% in February, 20% in Q4. Now a 25% rally. Not signs of a stable bull market. It is precisely the aggressive counter rallies near the end of cycles that can be the most awe-inspiring and reason defying, yet they can also be the most dangerous while being the best opportunities to sell at the same time.

Let’s get real: The liquidity machine can hide reality only for so long and that is: Things keep slowing down. Cycles don’t turn on a dime, they take time and that is what we are seeing unfold and the signs are plentiful. From Japanese industrial production going negativethe past 3 months to home sales in the Hamptons slowing to the slowest level in 7 years. I’m using these couple rather random examples to illustrate a point: The slowdown is as broad as it global:

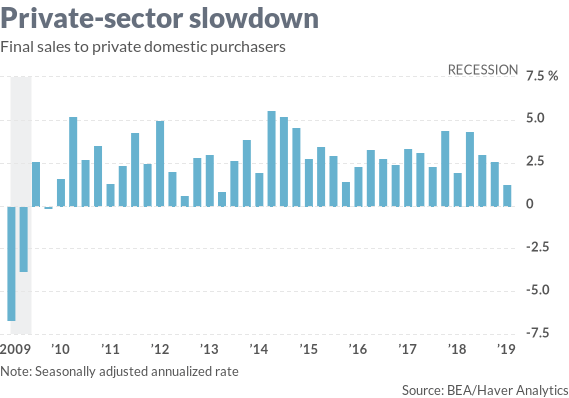

Oh yes, even Friday’s Q1 GDP report reeked of deceit and the headline is hiding theslowdown in plain sight:

“The economy isn’t doing nearly as well as that 3.2% annual growth rate for gross domestic product reported Friday by the Commerce Department.

The heart of the real economy — private-sector consumption and investment — slowed sharply in the first quarter to a 1.3% annual rate, the slowest growth in nearly six years.

“On the outside, it looks like a shiny muscle car. Lift the hood, however, and you see a fragile one-cylinder engine.”

Consumer spending rose only 1.2% in the first quarter, after healthy 2.5% growth the previous quarter. Spending on durable goods plunged 5.3%, the worst since 2009.

Business investment also slowed, to 2.7% from 5.4%. Investments in structures, such as factories, offices, stores and oil wells, fell for the third straight quarter. Investments in equipment — computers, airplanes and machinery — barely grew, rising 0.2%.:

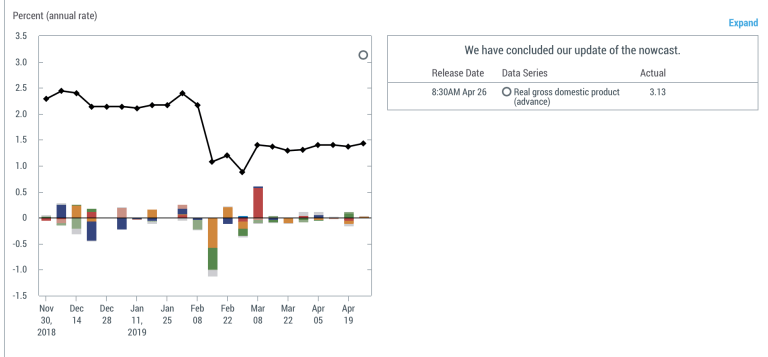

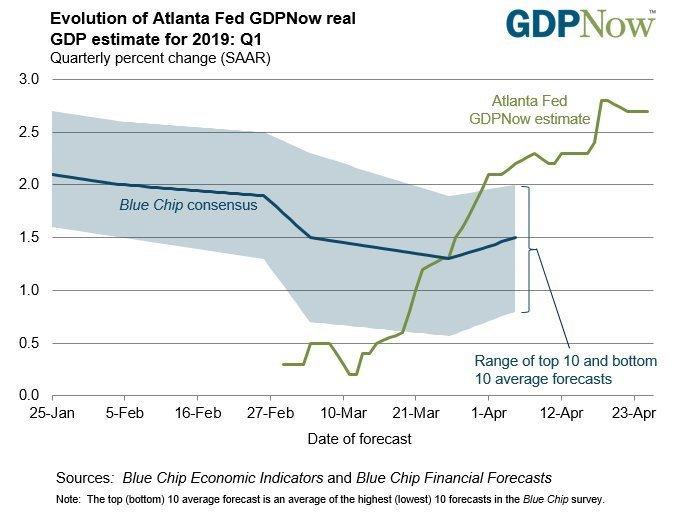

A GDP print so outsized to reality it made made a mockery of the NY Fed GDP model:

Forecast 1.5% but see a 3.2% result. Sure.

For added entertainment I present the Atlanta Fed model which projected 0.4% growth just 7 weeks ago:

This is banana republic like GDP forecasting. Blue chip consensus was 1.5% but the 3.2% result was “boosted by one-off factors big improvement in the trade balance, a big build-up in inventories, and a big pop in state and local government spending”

Not sustainable and not reflective of the true state of the economy. Yet we still see earnings beats from lowered expectations, but earnings will also have to catch up with the slowing reality:

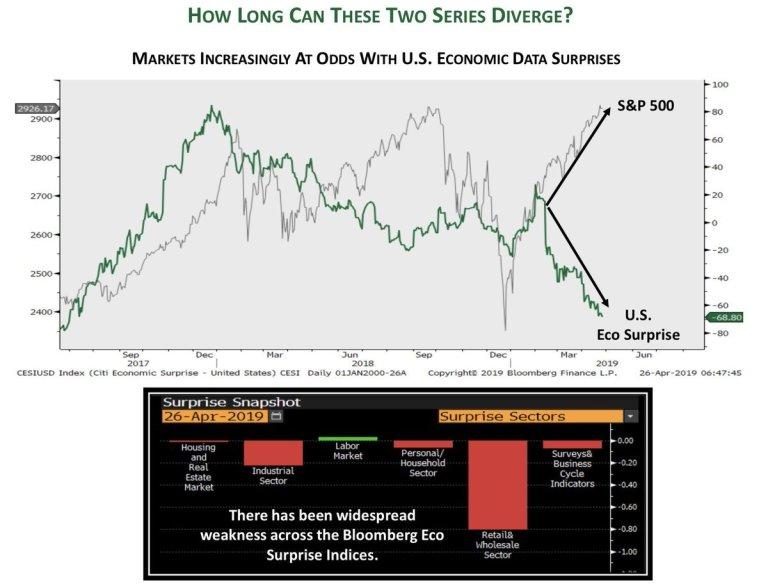

So far investors haven’t cared about that emerging reality, they have cared about liquidity, dovish central banks, buybacks and a China deal.

The prevailing fantasy: We can keep this up forever because the Fed has our back and a China trade deal will solve all problems:

Get real:

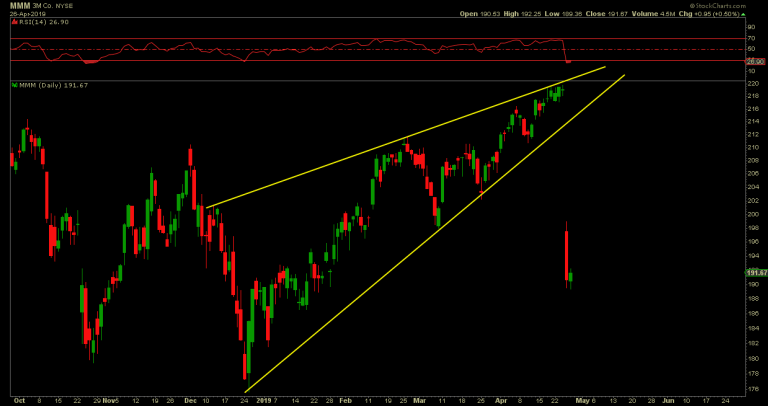

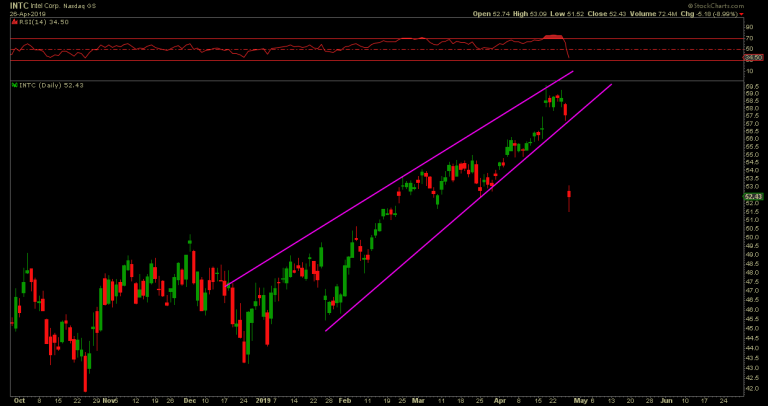

$MMM:

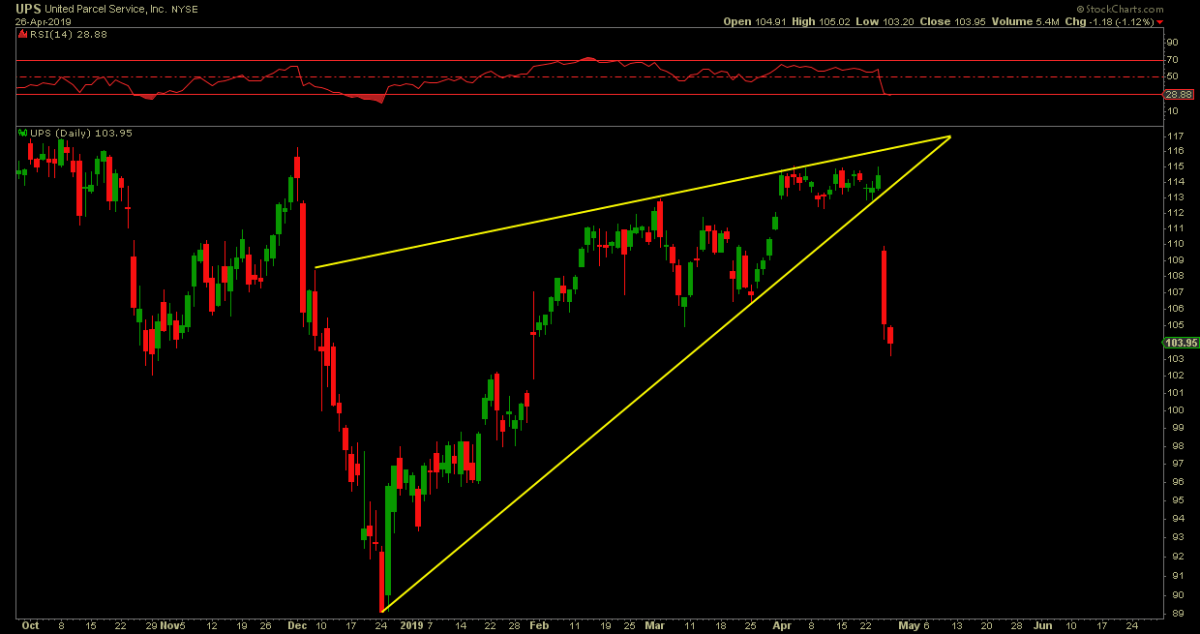

$UPS:

$INTC:

Oh yes, rising wedges do matter.

Think these 3 companies are not reflective of global growth? They sure are.

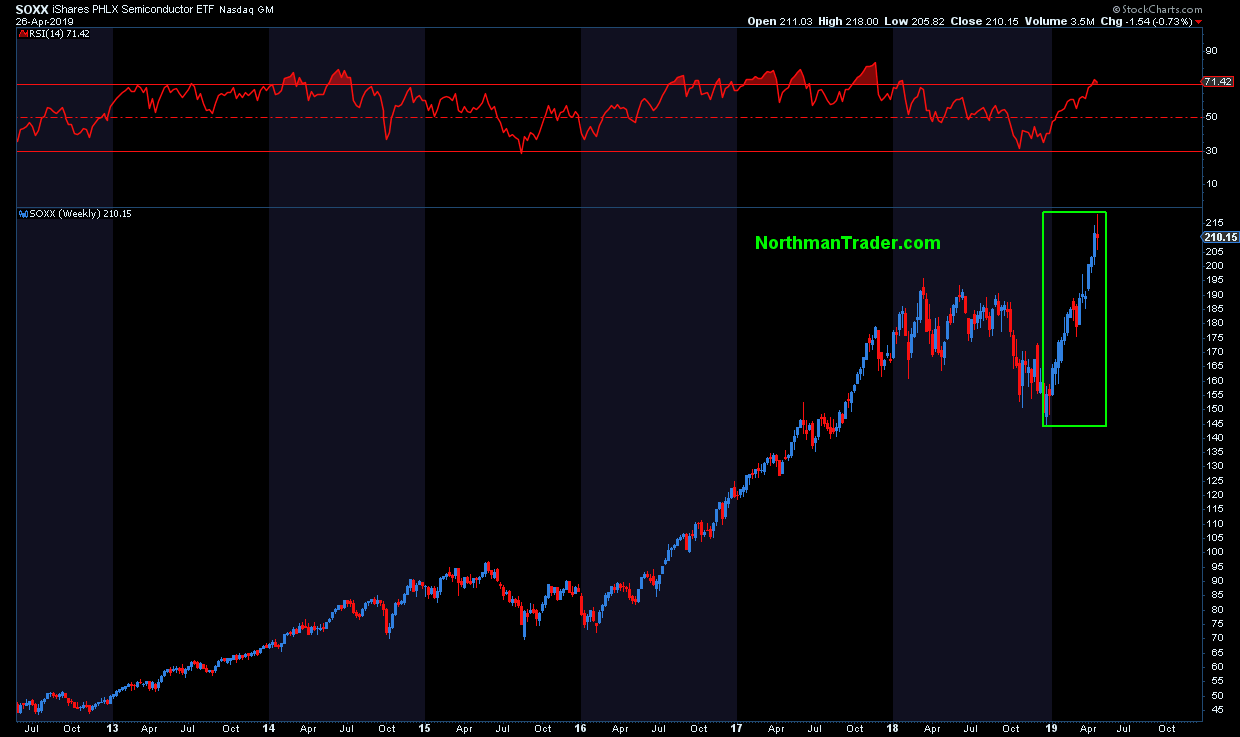

But they just had to jam into semis all year ignoring this reality:

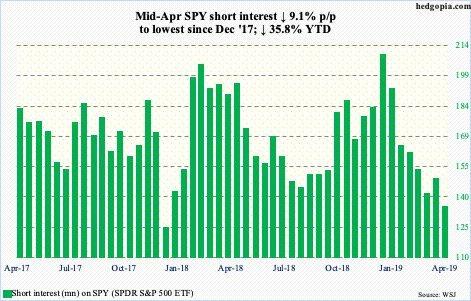

In process forcing capitulation in equity shorts:

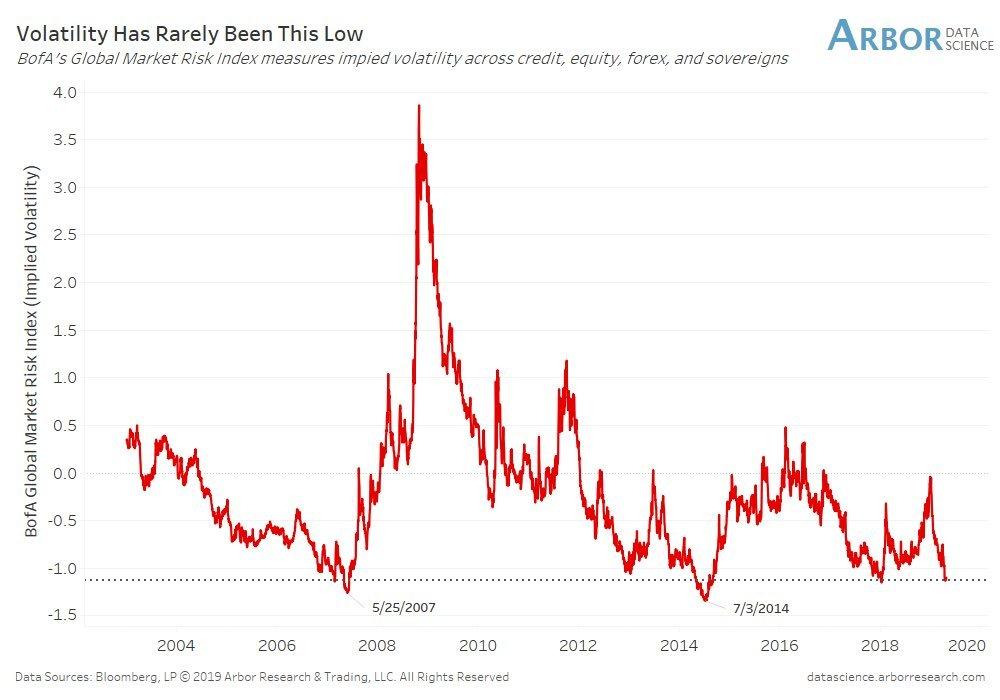

Right at the moment of historic low volatility across asset all classes:

…while believing volatility will never be great again:

Get real.

This is a dangerous combination that sets up for another volatility event to emerge.

For now the relentless 2019 market trend remains fully intact, individual stock bombs notwithstanding. Are we ready to blow-off as I asked this week? It looks so at the moment, but if that is so the sustainability of any such move has to be carefully evaluated as indices such as $NDX are highly overbought and confined to ever tightening rising wedge patterns:

In the spirit of keeping things real some key technical observations and charts in the video below:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel.

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News http://bit.ly/2ZHcSiz Tyler Durden

More than a dozen suspected jihadis (and a few civilians) died during a fierce gun battle on Friday between Sri Lankan police and terror suspects as dozens of suspected ISIS-affiliated jihadis from domestic terror organizations National Thawheedh Jamaath and Jammiyathul Millathu Ibrahim were rounded up in a crackdown meant to stave off any additional terror attacks.

According to a Reuters report from Friday, among the 15 dead were the father and two brothers of the mastermind of last week’s Easter Sunday bombings, which left 253 dead and another 500 injured. As we reported on Friday, a radical preacher named Zahran Hashim has been identified as the primary architect of the series of bombings at three churches and three luxury hotels. Hashim was a leader of the National Thawheedh Jamaath, and had been arrested over his involvement in the defacing of Buddhist statues. In a series of videos posted to YouTube, the radical Imam had called for violence against all non-believers.

Zahran Hashim

In one of these videos, Zainee Hashim, Rilwan Hashim and their father Mohamed Hashim, all of whom were killed by police, could be seen calling for war against nonbelievers. The attack occurred when police raided a suspect terrorist hideout on Sri Lanka’s east coast not far from one of the bombings in Batticaloa.

A family member confirmed to Sri Lankan police the identities of Hashim’s brothers and fathers. As comments from Hashim’s sister that circulated in the press suggest, not all of his family members shared his extreme, violent views.

“Even if he is my brother, I cannot accept this. I don’t care about him any more,” his sister said.

Nearly 10,000 soldiers have been deployed across the island to hunt down members of the Islamist groups who carried out the attacks. Police have already detained more than 100 people, including foreigners from Syria and Egypt, in the wake of the bombings.

In one of the videos that circulated online, Rilwan Hashim can bee heard calling for jihad and the deaths of non-believers.

“We will destroy these non-believers to protect this land and therefore we need to do jihad,” Rilwan said.

“We need to teach a proper lesson for these non-believers who have been destroying Muslims.”

However, authorities have warned that more terrorists might be on the loose. Though so far, there haven’t been any more incidences of violence since Friday.

via ZeroHedge News http://bit.ly/2WaVXmz Tyler Durden

{kind=link}