Imagine if, at a Q & A with Donald Trump, someone got up and said, “As an American Jew I am terrified at the unholy alliance AIPAC is forming with racist black activists, open borders extremists, Socialists and Communists, and no Republican should legitimize that type of globalist bigotry, and I’m wondering whether you will commit to boycotting it?” And Trump in response nodded agreeably and said yes. Now watch this clip with Elizabeth Warren regarding AIPAC, which involves equally inflammatory and tendentious allegations. Note that AIPAC has a huge membership (for an American Jewish organization of over 100,000, primarily Jews, and is, within the Jewish community, utterly mainstream, though of course (like the ADL, though AIPAC is much more bipartisan and centrist) it has critics both left and right.

from Latest – Reason.com https://ift.tt/2H5Riwd

via IFTTT

January Payrolls Soar By 225K, Smashing Expectations As Hourly Earnings Coming In Hot

For once the ADP private payrolls report was not that far off.

With Wall Street expecting a 165K print in this morning payrolls report, and with ADP coming in at almost 300K, the whisper number was obviously well above the official consensus, and the BLS did not disappoint, because just as Trump hinted a few days ago with his “jobs, jobs, jobs” tweet, in January the US created a whopping 225K jobs, smashing expectations, and well above last month’s upward revised 142K print.

The unemployment rate nudged higher by 0.1%, rising to 3.6%, above the 3.5% expected, yet still just barely above 50 year lows. Of note, the unemployment rate for both hispanics and blacks also rose to the highest since mid-2019.

Most notable, however, for markets was the rebound in hourly earnings, which rebounded from last month’s upward revised 3.0%, hitting 3.1%. Notably, after plunging in December to 3.2% from a decade high 3.8%, the average hourly earnings for production and nonsupervisory workers also staged a modest rebound, rising to 3.3% in January.

Royal Caribbean Ship With 12 Quarantined Passengers Docks In NJ; Ambulances, CDC On Scene

A Royal Caribbean cruise ship that has 12 passengers quarantined over fears of coronavirus has docked in Bayonne, New Jersey, this morning with ambulances on the scene.

The “Anthem of the Seas” arrived in New Jersey just hours ago, at about 6AM, in thick dense fog, according to ABC 6. Several ambulances were on standby at the scene.

The passengers in quarantine will all be tested by the CDC, who was also awaiting the arrival of the ship on the scene. The passengers of the ship are all Chinese nationals – many of whom started exhibiting symptoms while aboard the ship, which was coming back from the Bahamas.

#breaking Royal Carribean cruiseship docking now in Bayonne, NJ with roughly a dozen sick Chinese nationals on board. They will be tested for coronavirus. #abc7NYpic.twitter.com/RrupnawWo1

The NY Post reported that some of the passengers “have pulmonary issues”.

Royal Caribbean said in a statement:

“We are closely monitoring developments regarding coronavirus and have rigorous medical protocols in place onboard our ships. We continue to work in close consultation with the CDC, the WHO, and local health authorities to align with their guidance and ensure the health and wellbeing of our guests and crew.”

Robert Isaacson, whose 75 year old mother is on the ship, said that crew members have not alerted passengers to the sick people on board.

“We have been chatting throughout the cruise and she has not brought any mentions of the crew alerting the passengers of a potential situation involving sick passengers,” he said, referring to conversations with his mother.

This news follows last night’s news “Nightmare at Sea” news that 42 additional cases of coronavirus, including an infected passenger who got on the ship in Japan, had been discovered on the Diamond Princess cruise ship which is anchored in Yokohama, Japan.

Japan says 273 people on the cruise ship were tested and 61 were found positive, and the 41 new patients have been sent to hospitals in 5 separate prefectures.

Japanese PM Shinzo Abe said no foreigners on board the MS Westerdam, run by Holland America Liner, would be allowed to disembark in Japan. The ship is capable of carrying 3,000, but it’s unclear how many are on board. Passengers on the Westerdam say the ship has already been refused entry to the Philippines and Taiwan over the virus fears.

Stephen Hansen, one tourist onboard the ship, has express concerns that the ship could be quarantined for two weeks.

Traders Are Calling Central Bankers’ Bluffs… Again

Authored by Richard Breslow via Bloomberg,

The S&P 500 has, so far at least, been up every day this week. And achieved a new all-time high.

The Shanghai Composite, after Monday’s plunge, rose each day to finish out the week at levels seen only as far back as early December — when it began its big run.

During these moves, we have spent a lot of time trying to come up with suitable explanations for the strength, let alone resiliency, of these markets in the face of really disturbing news.

Obviously investors must be bullish. And are so despite some pretty eminent and respected economists warning that this is getting way out of control. And valuations making no sense given the forecast outlook. It’s making me think back to last Friday, when the stock market got whacked. What a buy-the-dip opportunity that turned out to be. A 3%-plus snip over the course of a single week is a home run on any occasion. Caveat: we still have to get through today.

The main reason we had that Jan. 31 sell-off (which seems like a long time ago, doesn’t it?) was uncertainty over where Chinese markets would open after their long hiatus. How orderly things would function. But also, and this is the point, what if there was more bad news while exchanges were closed for the weekend?

Bad news was assumed to be just that. We weren’t trying to explain it away with unsupportable arguments about this all being temporary and obviously contained. (Subtext: Over there.) This week the market has clearly reverted to the old “bad news is good news” playbook. I want to see which of these two assumptions holds true through this session. It will inform trading going forward.

There is, of course, the matter of non-farm payrolls to cloud the matter. But it still should be possible to get a sense of where we stand on this question, which is an important one. This afternoon will matter. Central banks will do what they have to when push comes to shove, but most of them don’t want to. Fed speakers are doing their best to stick to the on-hold mantra, which given U.S. numbers is appropriate. Chairman Jerome Powell’s congressional testimony next week is well-timed given how markets are trading.

ECB President Christine Lagarde isn’t a clone of Mario Draghi. Her comments this week about having few monetary stimulus options left after the years of fighting the financial crisis Europe is still struggling from are true. And, given the industrial production numbers we saw this morning, made all the more worrisome. But I couldn’t help thinking they were also meant to be a reminder to those buying the “undervalued” Stoxx 600, which itself is up 3% this week. The U.S. had its Iowa debacle. Germany had a scarier one in Thuringia.

In a very real sense, traders are trying to call their central bankers’ bluffs. And are building in rate cuts to prove their points. It’s worked before and as any Bayesian believes, it’s worth thinking it can work again. So the old adage of, “if you liked it up there, you’ll love it down here” remains the operative practice. And, that is what keeps those who might be tasked with cleaning up any major stumble up at night.

Ten-year Treasuries have failed miserably trying to get back above 1.70%. The technical resistance right in front of it proved too difficult to surmount. Remember how it traded there should we revisit that level at some point. It’s shaping up to be big. On the downside, 1.50% is equally huge support. Maybe even more powerful. And until either side breaks we will have a clear, and tradable, range.

A Stunning 400 Million People Are On Lockdown In China As Guangzhou Joins Quarantine

Guangzhou, the capital of China’s southwestern Guangdong Province and the country’s fifth largest city with nearly 15 million residents, has just joined the ranks of cities imposing a mandatory lockdown on all citizens, effectively trapping residents inside their homes, with only limited permission to venture into the outside world to buy essential supplies.

The decision means 3 provinces, 60 cities and 400 million people are now facing China’s most-strict level of lockdown as Beijing struggles to contain the coronavirus outbreak as the virus has already spread to more than 2 dozen countries.

That’s more than 400 million people forcibly locked inside their homes for 638 deaths? Just think about that: If there was ever a reason to believe that Beijing is lying about the numbers (and not just because Tencent accidentally leaked the real data), this is it.

Meanwhile, in the US, the Trump Administration has directed researchers to investigate the ‘true origins’ of the virus, as ‘conspiracy theories’ and misinformation spreads online. We can’t help but wonder: What if the scientists discover something that the regime in Beijing doesn’t want them to see?

Elsewhere, Singapore raised its national disease response level to Orange, the second-highest level and the same level from the SARS epidemic, according to the city-state’s health ministry. It also confirmed three new coronavirus cases. While investigations are ongoing, none of the three appear to have a history of recent travel to China, suggesting they picked up the virus in Singapore.

‘Orange’ means the outbreak “is severe and spreads easily from person to person” but “has not spread widely in Singapore and is being contained,” according to the Disease Outbreak Response System Condition color-coded framework. Singapore has never invoked its highest level, red, per BBG.

Foreigners are complaining that the new hospitals in Wuhan are merely ‘quarantine centers’ without any medical resources.

Dear Gov’t of Uganda,

The famous makeshift “hospitalsh the Chinese Gov’t is bragging about are not hospitals, they are quarantine areas where patients are not receiving any treatment at all. Is this the place you’re saying is safer for us ? #EvacuateUgandansInWuhanpic.twitter.com/sLzdUHA24P

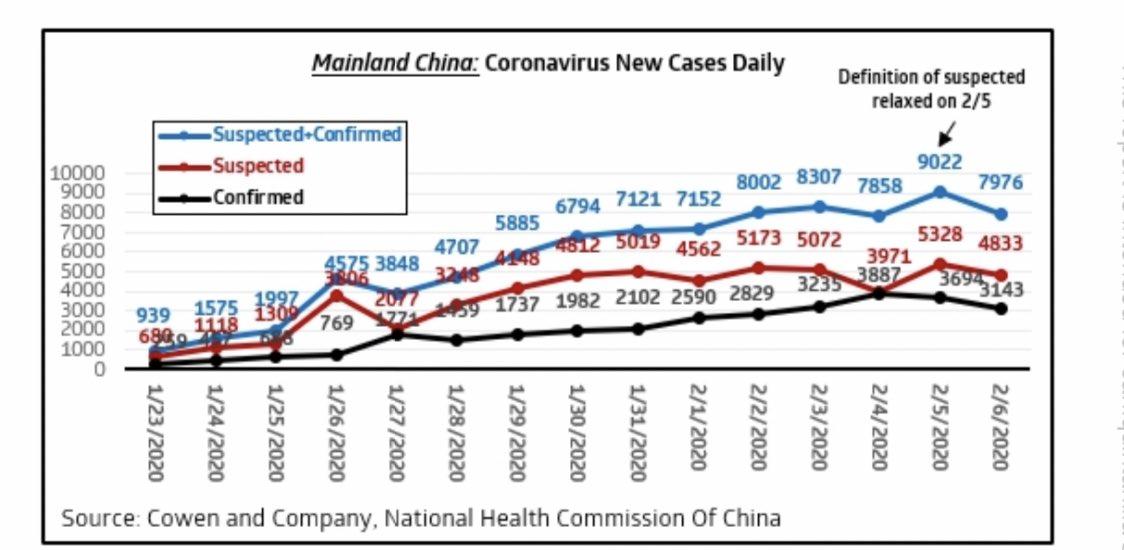

Yesterday, Beijing argued that the virus outbreak had ‘peaked’ as they cited a drop in the rate of new infections. However, others have suggested that the rate of new confirmed cases has more to do with Beijing’s limited resources.

It’s been said by others but I’ll say it too:

The way China is reporting almost an identical number of new coronavirus cases each day (approximately 3000) MUST be a reflection of its diagnosis capacity rather than the true caseload, which is likely much worse.

The WHO said during a press conference on Thursday that it’s too early to claim that the outbreak has peaked, even as the outlook for the global economy falls off a cliff.

Futures Slide On Fresh Virus Fears Ahead Of Payrolls As German Industrial Production Craters

Following a torrid 3% rally on “hopes” that the coronavirus epidemic is contained after last Friday’s plunge, coupled with even more “hopes” that trade relations with China are on the mend after Beijing slashed its duties on some US goods by up to 50%, overnight renewed coronavirus worries took a hit at world markets on Friday ahead of today’s payroll report (which will include major downward revisions), although the modest drop sparked by fears of a mini epidemic on board a Japanese cruise ship wasn’t going to stand in the way of the best week for stocks since June and the strongest for the dollar since August.

U.S. equity futures dropped and European stocks pared a week of big gains as doubt spread that the spread of the coronavirus was contained, while Treasuries and safe havens climbed before American jobs data.

Europe’s trading day began with stocks down and safe-haven government bonds up, a pattern that had been set in Asia where the death toll from the virus in China has more than doubled in less than a week, and stood at 638 on Friday, 636 in China (although doubt in the veracity in the official numbers is spreading just as fast as the underlying epidemic) and two abroad and it was also revealed that one of the first doctors to raise the alarm about the virus had died from it at a hospital in Wuhan, the outbreak’s epicenter. Drops in miners and carmakers led the Stoxx Europe 600 Index lower, while luxury retailer Burberry Group slipped scrapping guidance over the virus hitting China sales. Credit Suisse slumped after ousting its CEO. The mood turned more sour as the latest data showed German industrial production had the biggest monthly tumble since the financial crisis, crushing the narrative that Germany’s economy was on the mend.

Earlier in the session, equities slipped across most of Asia as news of further infections on a cruise ship off Japan offered another reminder that cases remain on the rise, even as China is scrambling to restore a sense ofcalm by reported a decline in the number of news cases.

And even though the World Health Organization has said it is too early to call a peak in the outbreak, the “data” out of China sufficient for some investors-turned epidemiologists who were all too eager to believe China’s bullshit statistics: “We are not that nervous, actually we are increasing our risk allocation,” said SEB investment management’s global head of asset allocation Hans Peterson, adding the risk of a massive worldwide epidemic seemed to have dropped. “We look more at this moment at the macro data in the U.S. which is really very good… and we presume we will get substantial support from central banks like we did in China on Monday.” So… win-win: bad news is great as it will only improve, but good news is even better as central banks will provide backstops. What’s not to like.

Not everyone shared the optimism that bankers will as usual save the day: expectations the outbreak will be contained and growth will rebound from the second quarter on the back of stimulus and pent-up activity are “probably somewhat optimistic,” Sue Trinh, macro strategist at Manulife Asset Management, told Bloomberg TV. “The very real risk is that this outbreak spreads, quite literally, into the second quarter and beyond.”

After to a $400 billion wipeout on Monday, Shanghai is poised for its worst week in eight months. But the other Asian indexes are ahead and the pan-European FTSEurofirst is heading for its best week since late 2016.

Also overnight, Singapore lifted its national disease response to the second-highest level, the same one for the SARS epidemic. Apple’s Chinese iPhone maker Foxconn told employees not to return to work at its Shenzhen facility when the extended Lunar New Year break ends Feb. 10. Meanwhile, the presidents of China and the U.S. reaffirmed their commitment to the implementation of a phase-one trade deal in a phone call Friday.

Yields on 10Y TSYs dropped back to 1.61%, and have failed to breach a key technical resistance amid slowdown fears.

In FX, the euro fell to its lowest since October in early European trading after German industrial output recorded its biggest decline in a decade (see chart above) and strong U.S. employment numbers on Thursday had primed the dollar for monthly payrolls later. The yen halted a slide that has it set for its worst week in 18 months, leaving the currency sitting just above a two-week low at 109.85 per dollar. The Australian dollar, often seen as a proxy for China, weakened 0.5% to $0.6699 after the Reserve Bank of Australia slashed growth forecasts in its quarterly economic outlook, blaming its bushfires and the coronavirus. The Aussie was still on track for its first weekly gain this year, whereas Singapore dollar and Thai baht have been trampled in a rush from emerging market currencies into majors.

Owing to much greater exposure to Chinese demand and less access to the benefits of monetary stimulus, commodity prices have been more sensitive to conditions on the ground. Oil and metal prices fell hard as the coronavirus outbreak gained pace and have been slow to recover. Brent crude was a touch firmer on Friday at $55.17 per barrel, but is heading for its fifth back-to-back weekly drop having lost over 16% this year. A rally in copper – often seen as a barometer of global economic health because of its wide industrial use – stalled at $5,695 per tonne though it has been its strongest week since the start of December.

“We think that demand could come back strongly as opposed to gradually in Q2 2020,” said Commonwealth Bank commodities analyst Vivek Dhar. “But the risk in the near term is that (Chinese) provinces take longer to return to work in order to contain the spread of the virus.”

Expected data include non-farm payrolls, unemployment, and wholesale inventories. AbbVie, Avantor, and Canada Goose are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.3% to 3,336.50

STOXX Europe 600 down 0.2% to 424.57

MXAP down 0.5% to 169.76

MXAPJ down 0.8% to 547.76

Nikkei down 0.2% to 23,827.98

Topix down 0.3% to 1,732.14

Hang Seng Index down 0.3% to 27,404.27

Shanghai Composite up 0.3% to 2,875.96

Sensex down 0.3% to 41,172.95

Australia S&P/ASX 200 down 0.4% to 7,022.58

Kospi down 0.7% to 2,211.95

German 10Y yield fell 1.8 bps to -0.388%

Euro down 0.2% to $1.0960

Italian 10Y yield unchanged at 0.798%

Spanish 10Y yield fell 1.7 bps to 0.278%

Brent futures little changed at $54.91/bbl

Gold spot up 0.2% to $1,569.30

U.S. Dollar Index up 0.1% to 98.61

Top Overnight News

China’s January trade data was scheduled to be released Friday, but will instead be announced together with February data, according to the customs administration

Germany is facing a possible recession again after industrial production plunged by the most since the global financial crisis

A nascent recovery in Indonesian exports is under threat, with the coronavirus outbreak set to sap Chinese demand for commodities including palm oil, coal, paper and pulp

The death of a 34-year-old doctor on Friday has unleashed a wave of fury that is sparking a rare crisis of confidence in the Chinese Communist Party and its handling of the coronavirus outbreak

A Chinese doctor who was initially sanctioned for warning about the deadly Wuhan coronavirus outbreak in early January has died, stoking fresh anger online at the Communist Party-led government. The number of infections on China’s mainland climbed to more than 31,000

President Trump and China’s President Xi Jinping “agreed to continue extensive communication and cooperation between both sides,” White House says in readout of leaders’ call

OPEC expects Russia to respond in days, rather than weeks, to a production-cut proposal as the cartel confronts a price rout triggered by the collapse in petroleum demand from China, according to a delegate. U.S. weighs sanctions on Rosneft but is wary of oil market chaos

European Union Trade Commissioner Phil Hogan had a “useful and constructive” meeting in Washington on Thursday with his U.S. counterpart, according to an EU official

Pete Buttigieg holds a razor-thin lead over Bernie Sanders in the Iowa caucus with 100% of precincts reporting. Buttigieg had 26.2% to Sanders’ 26.1%, according to official results. Elizabeth Warren had 18%, Joe Biden had 15.8% and Amy Klobuchar had 12.3%. Other candidates were far behind

Declines in Japan’s household spending worsened in December, signaling that government measures to ease the shock of October’s sales tax hike may not be working as well as economists and policy makers expected

Asian equity markets were mostly subdued as the momentum from Wall St, where all major indices posted record levels and tech outperformed, was clouded by coronavirus fears and cautiousness heading into the latest Chinese trade data and US Non-Farm Payrolls. ASX 200 (-0.4%) was dragged lower by weakness in energy and miners amid ongoing demand concerns triggered by the outbreak in China, while Nikkei 225 (-0.2%) was indecisive with focus in Tokyo on a deluge of earnings, weaker than expected Household Spending and reports of 41 additional coronavirus cases onboard the cruise ship off Yokohama, although it wasn’t all gloom and doom as SoftBank gapped higher by 8% after Elliot Management acquired a USD 2.5bln stake. Elsewhere, Hang Seng (-0.3%) and Shanghai Comp. (+0.3%) declined amid the ongoing coronavirus fears and tentativeness ahead of the trade figures which are expected to show exports and imports slipped into contraction territory, although officials have remained supportive including the PBoC’s Beijing branch which directed banks to cap interest rates offered to key enterprises at 100bps below the Loan Prime Rate. Finally, 10yr JGBs benefitted from the risk averse tone which lifted prices back above the 152.50 level, while the BoJ were also present in the market for over JPY 1.1tln of JGBs with 1yr-10yr maturities.

Top Asian News

Japan Lawmakers Call on BOJ to Mull Digital Yen to Counter China

China Delays January Trade Data to Merge With February Release

Taiwan Exports Plummet as Coronavirus Threatens Trade Recovery

Toyota, Honda Extend China Shutdowns as Virus Gathers Pace

A relatively subdued session thus far for European equities [Eurostoxx 50 -0.3%], with participants on guard amid virus jitters ahead of the release of the key US labour market report later today. APAC bouses ended the week on a mixed footing following a mostly subdued session – Mainland China eked mild gains after reports of supportive steps by the PBoC to cope with downward pressures arising from the coronavirus outbreak. Back to Europe, bourses are mostly subdued with no clear standouts. Sectors are largely in negative territory with defensives faring modestly better than cyclicals. In terms of individual movers, Credit Suisse (-2.5%) slipped to the foot of the SMI (~3% weighting) following the departure of CEO Thiam following the spying scandal. Thiam will be leaving his post on February 14th and is to be replaced by Thomas Gottstein, the current head of the bank’s Swiss business. Note: Credit Suisse will be reporting its results on February 13th. Elsewhere, Burberry’s (-1.3%) withdrawal of guidance and bleak demand outlook for the luxury market (amid the virus outbreak) has prompted sympathy play from European peers including Richemont (-1.3%), Swatch (-0.9%), LVMH (-1.0%) and Kering (-1.5%). Fiat Chrysler (-2.2%) slid to the foot of the FTSE MIB after warning that its European plants may see closures within weeks if China closures are extended as a result of the outbreak as factories will find it difficult to source key parts. In terms of earnings, L’Oreal (+1.2%) leads the gains in the CAC amid an all-round solid report and a 10% annual increase to its dividend, although the Co. did highlight a temporary slowdown from its Chinese beauty market, a key driver of its growth. Finally, Ericsson (+4.8%) and Nokia (+6.7%) see renewed tailwinds from US AG Barr’s endorsement in Cos for 5G technology as opposed to Huawei.

Top European News

Nordea Fixes Bonus Culture After Investor Lambastes Bank

Calisen Gains After Raising $426 Million in London IPO

Carbon Pollution Costs Are Likely to Rise Again in Europe

Short Sellers’ Nordic Nightmare Attracts a $130 Billion Fund

In FX, it remains gradual and measured, but relatively resolute as the Greenback maintains positive momentum and on track to extend its winning streak amidst widespread if not universal gains vs currency rivals. Indeed, DXY pull-backs are becoming increasingly shallow and short-lived with the index now building a platform around 98.500 and just posting a fresh peak at 98.639 ahead of the next bullish chart resistance level at 98.885 (higher Fib retracement from 2019 peak to December trough). US jobs data may present a fundamental hurdle, but in the current constructive climate the bar appears high in terms of an upset to stall the Buck’s rally or halt the bull run altogether.

AUD/NZD – The clear G10 underperformers, as the Aussie recoils further from Tuesday’s post-RBA peaks and the Kiwi retreats partly in sympathy towards 0.6680 and 0.6400 respectively vs their US counterpart. Aud/Usd gleaned little if any traction via the SOMP or latest rhetoric from Governor Lowe as the former revealed lower GDP forecasts based on the assumption that rates will be reduced by another 25 bp. Moreover, news of a delay to Chinese trade data and the ongoing spread of the coronavirus are weighing on risk sentiment in general, as the YUAN slips back to 7.0000 against the US Dollar.

EUR/CAD/CHF – Also unable to resist the Greenback’s advances, with the Euro also blighted by more dire German/Eurozone data and increasingly bearish technical impulses having fallen through a sub-1.1000 Fib (1.0964) and now testing the resolve of bids around 1.0950 ahead of last October’s pre-2019 full year low (1.0941). Similarly, the Loonie has lost grip of the 1.3300 handle, but could yet be saved from a worse fate and stops said to be poised on a break of 1.3320 by decent option expiry interest between 1.3290-1.3300, if not impending Canadian payrolls. Meanwhile, the Franc is still somewhat mixed given weakness vs the Buck below 0.97500 in contrast to strength through 1.0700 against the Euro.

JPY/GBP – The Yen is paring losses amidst a partial reversal in risk-on flows and renewed safe-haven positioning, with Usd/Jpy back down to circa 109.70 from just above 110.00 even though media reports suggest official GPIF sponsored selling of the Japanese unit alongside PBoC OMOs. However, the Pound is also holding up fairly well in the circumstances, as Cable hovers above 1.2900 and the post-UK GE trough, and Eur/Gbp remains capped around 0.8500.

NOK – Disappointing Norwegian data and another downturn in oil prices have combined to propel Eur/Nok above 10.1600 even though the single currency has its own negative factors to contend with, as noted above.

In commodities, WTI and Brent front-month futures remain choppy as focus remains on OPEC’s move following a three-day meeting by the group’s JTC. In terms of the fallout, the committee reportedly proposed a 600k supply cut to start immediately which will continue through to June if agreed by all members and they expect Russia to respond in a matter of days according to sources, while there were twitter reports of unconfirmed chatter OPEC+ are proposing extending current cuts into year-end. That said, Russian Energy Minister Novak continued to push back against these cuts stating that Russia needs a few days to analyse situation on oil market and will come up next week with its position for OPEC+ meeting due next month, although Russian Foreign Minister Lavrov that he supports the panel’s proposal of cutting oil output – but did not specify a preferred magnitude of reductions. WTI and Brent futures have largely traded on either side of USD 51/bbl and USD 55/bbl respectively before prices moved lower in tandem with sentiment. Elsewhere, spot gold treads water just under USD 1570/oz with the yellow metal’s 21 DMA seen around 1564/oz. Meanwhile, copper prices saw brutal losses after hitting resistance at USD 2.6/lb (low USD 2.55/lb) with reports noting that Chinese copper traders, the metal’s largest market, asked miners to cancel or halt shipments of the red metal as the virus outbreak takes its toll on demand.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 165,000, prior 145,000

Average Hourly Earnings YoY, est. 3.0%, prior 2.9%

Change in Private Payrolls, est. 155,000, prior 139,000

Change in Manufact. Payrolls, est. -1,500, prior -12,000

Unemployment Rate, est. 3.5%, prior 3.5%

Average Hourly Earnings MoM, est. 0.3%, prior 0.1%

Average Weekly Hours All Employees, est. 34.3, prior 34.3

Labor Force Participation Rate, est. 63.15%, prior 63.2%

Underemployment Rate, prior 6.7%

10am: Wholesale Inventories MoM, est. -0.1%, prior -0.1%; Wholesale Trade Sales MoM, est. 0.1%, prior 1.5%

3pm: Consumer Credit, est. $15.0b, prior $12.5b

DB’s Jim Reid concludes the overnight wrap

Being in Dubai this week I’ve learnt something new about the climate here. The area is a significant user of cloud seeding and frequently uses the technology to encourage precipitation and also to cool down the temperatures. I wasn’t aware it could be done at such an industrial level. I’ve been doing a bit of reading on geo-engineering recently in my work on climate change and boy this is a controversial topic. I suspect it will get more attention in the years ahead as we try to fight climate change and the technology improves. Given that my last two rounds of golf at home have been cancelled due to a sodden course this is starting to influence my opinions on the topic! Looking at the stormy weather forecast for this Sunday in the U.K. and many parts of Europe I suspect I’ll be in even less control of my golf ball than usual. If you’re reading from this region then maybe make the most of Saturday this weekend!!

The storm clouds have certainly been swept away in markets this week even if the wind direction has slightly changed in the Asia session. Attention today will turn to US payrolls. In terms of what to expect from the announcement, DB’s US economists are looking for a +160k increase in nonfarm payrolls, which is basically in line with the consensus +163k call. They assume a 10k boost from temporary government hiring for the decennial census, so investor focus should be on private payrolls instead, where we’re expecting a +150k reading. Some might look for optimism given the ADP’s report of private payrolls on Wednesday, which saw a +291k increase, the most since May 2015. However the ADP reports have actually proved somewhat wide of the mark recently, with the previous month’s ADP reading overestimating the private payrolls number by +60k. Furthermore, the ISM non-manufacturing employment reading earlier this week fell to 53.1, the lowest since September.

Staying with the US, Democratic candidates will be gathering in New Hampshire for their latest TV debate tonight, which comes ahead of that state’s primary on Tuesday. We’ve seen a remarkable shift in the betting odds this week. Joe Biden, who still leads in national polling averages, has seen his PredictIt odds crash to 16%, the lowest reading of this cycle (c.35% last week). The majority of his numbers seems to have been siphoned to Buttigieg (seemingly the narrowest of winners in Iowa) and Bloomberg, as the market seems to being looking for an alternative moderate. Sanders is now up to 45%, with the more liberal wing of the party coalescing around him as Warren is down to 6%, after being over 50% back in October. The most recent polling data either omits or only partially includes days after the Iowa caucuses, but we should know in a few days how performances there and in the aftermath have affected national and regional numbers. Finally fivethirtyeight.com’s model forecasting the Democratic primary now has Sanders with a 49% chance of winning the nomination, with “no one” or a contested convention coming in second at 24%. Betting markets and polling currently look good for Sanders winning the nomination. However, equity markets do not seem to be pricing that in or – as the EMR survey from January shows – market participants do not believe in Sanders’s (or any Democrat’s) ability to beat President Trump in November. We’ll be doing our latest market survey next week so we’ll see how markets feel about the race then.

Back to yesterday now, and for the time being at least, markets seem to be taking the coronavirus in their stride, as the S&P 500 rose +0.33% to a new record, while the STOXX 600 also reached a fresh high with a +0.44% advance. Positive earnings releases supported the advance, with Twitter +15.03% and the top performer in the S&P 500 after the company reported quarterly revenue over $1bn for the first time, beating expectations. Over in Europe meanwhile, ArcelorMittal was up +11.04% as the company reported the lowest net debt since their 2006 merger and struck a positive note on the 2020 outlook.

Other asset classes continued to join in the rebound with copper, a key bellwether for global economic demand, powering forward for a 3rd consecutive session yesterday, up +0.84%, and after 13 straight days of declines before that. 10yr Treasury and Bund yields both fell around 1bps.

Coronavirus fears are resurfacing a little this morning as Japan found an additional 41 coronavirus cases (bringing the total tally to 61) on a quarantined cruise ship. It is the biggest outbreak number outside of China and the number could potentially jump higher as only 273 of the 3700 passengers on the ship have been tested so far. Meanwhile Japan has banned a separate cruise ship from berthing at a port in the country, saying a person onboard was suspected of having contracted the virus. In other related news, Japanese PM Shinzo Abe has said that Japan will put together emergency spending measures next week to address the coronavirus crisis, tapping budgeted reserves.

Back in China, the total number of infected cases now stands at 31,161 (vs. 24,324 yesterday) with the death toll at 636 (vs. 490 yesterday). Meanwhile, Pan Gongsheng, a deputy governor at the PBoC, said overnight that the central bank will give higher priority to economic growth as the virus outbreak is intensifying downward pressure on the economy, but also pledged to consider other factors such as controlling debt and the yuan exchange rate. Markets are increasingly expecting the PBoC to lower the MLF rate by 10bps around the middle of the month after it has already lowered the short term repo rates by the same amount earlier this week.

Asian markets are trading lower this morning with the Nikkei (-0.21%), Hang Seng (-0.87%), Shanghai Comp (-0.80%) and Kospi (-1.15%) all down. Elsewhere, futures on the S&P 500 are down -0.21% and the yield on 10yr USTs are down -2.1bps. Brent crude oil prices are trading up +0.18% after yesterday’s news that technical experts from OPEC+ recommended a further supply curb of 600,000 barrels a day until June even as Russia’s response over this is awaited. In addition they recommended that the current 2.1 mn barrel/day cut already in place be extended until the end of the year, rather than expiring in March as originally planned. As for overnight data releases, Japan’s December household spending came in at -4.8% yoy vs. -1.7% yoy expected and real cash earnings came in line with consensus at -0.9% yoy.

In other news, the US President Trump spoke overnight with Chinese President Xi Jinping and both sides reaffirmed their commitment to the implementation of Phase 1 deal. Elsewhere, Bloomberg reported that the US is weighing whether to sanction Russia’s biggest oil producer, Rosneft, for maintaining ties with Venezuela.

Back to the Coronavirus and yesterday our China economists released their latest update on the impact (link here), where they write that it is still too early to call it a turning point. Although the outbreak appears to be plateauing outside of Hubei province, the situation in Wuhan and Hubei may still be very difficult, and they write that the disruption to China’s economy is likely to continue in the short term. The two biggest keys to watch for according to our economists are: (1) How the virus spreads after the new round of travel post the elongated Chinese New Year and (2) How long it takes for production to get back to full capacity.

On central banks, we heard yesterday from ECB President Lagarde, who appeared before the European Parliament’s Economic and Monetary Affairs Committee. In her testimony, she highlighted the coronavirus, saying that the uncertainty from its impact was “a renewed source of concern”, and came as the Euro Area economy was showing “tentative signs of stabilisation”. Notably, she also explicitly warned of the ECB’s diminishing ability to respond to future negative shocks, saying that the “low interest rate and low inflation environment has significantly reduced the scope for the ECB and other central banks worldwide to ease monetary policy in the face of an economic downturn.” Her remarks came as we got more poor data from Germany, with factory orders surprising to the downside thanks to a -2.1% decline in December (vs. +0.6% expected). The reading brings the year-on-year decline to -8.7%, the lowest since September 2009. That said, data yesterday also showed the country’s construction PMI rising to 54.9 in January, its highest level since March.

The data from the US was somewhat better yesterday, with weekly initial jobless claims falling to 202k (vs. 215k expected), their lowest level since April, which also sent the 4-week moving average down to its lowest since April as well. We also got the preliminary nonfarm productivity data for Q4, which was up +1.4% qoq (vs. +1.6% expected), bouncing back from the first quarterly decline since 2015 in Q3. Though the reading was less than forecast, the full-year figure for 2019 was up +1.7%, the fastest increase since 2010.

Wrapping up now, and yesterday the new state premier of the German state of Thuringia stood down and called for fresh elections after one day in office. It follows an outcry after the FPD politician got the job thanks to the backing of both the CDU and the AfD, which marks the first time that the AfD have acted as kingmakers in Germany. While the story hasn’t had much of a market impact, it has roiled domestic German politics, where the major parties have all previously rejected any cooperation with the AfD. Chancellor Merkel said the vote yesterday, which also was supported by the CDU in the state, marked “a day that broke with the values and the convictions of the CDU”.

To the day ahead now, and as well as the aforementioned US jobs report, today’s data highlights include both Germany and France’s industrial production and current account balance for December, along with December retail sales from Italy. On the other side of the Atlantic, there’ll be Canada’s employment report, as well as the final US wholesale inventories figure for December. From central banks, the Fed will be releasing their semi-annual Monetary Policy Report to Congress, and we’ll also get a monetary policy decision from the Russian central bank. There isn’t much in the way of earnings today, though AbbVie is scheduled to report. Finally, ahead of New Hampshire’s primary on Tuesday, there’ll be a TV debate taking place there tonight between the Democratic candidates.

We’re deep into another presidential election. It’s a time when a few of the wealthiest, most cossetted and least appealing members of society try to convince us that America basically is an impoverished wasteland, filled with untold suffering and blight. The nation won’t heal itself until we put one of them in charge of its behemoth government.

“The United States has more people living in poverty than at almost any time in the modern history of our country,” intoned leftist Democratic candidate Bernie Sanders. He’s so out of touch with reality that he hired a top adviser who once praised the “economic miracle” in socialist Venezuela, which is one of the most genuinely miserable places on Earth.

The populist Right isn’t much better. Trump-supporting pundits have spread wild tales of misery afflicting the Rust Belt and the nation’s middle class, with Fox News’ Tucker Carlson last year engaging in an infamous critique of free-market capitalism. Their policy prescriptions (more government) aren’t remarkably different from those championed on the Left.

Obviously, in a land of 329 million flawed human beings one can always find stories of people who are living on the streets, lacking proper healthcare, addicted to drugs and whatnot. Some people are sick, unhappy, out of work and living crummy lives. The only thing lacking from these analyses is a little perspective about the human condition—and about the limits of government uplift.

The data shows that poverty is diminishing rapidly, which no doubt explains why the doom-mongers focus mainly on anecdotes. Conservatives (including President Trump) point to progressive San Francisco as a foreboding place filled with homeless encampments and crime. I’m in the city frequently. It has lots of self-imposed problems, but remains one of the wealthiest and most beautiful cities in the world. It’s easy to forget that crime rates are near-record lows in most of America.

I recently returned from rural Appalachia, another place that politicians point to as a sea of despair. The region is in decline, but it’s mostly a middle-class place. (Don’t tell Trumpsters this, but the best thing that could happen to these hard-edged towns—with their low-cost real estate and aging populations—is an influx of immigrants.) I’m not downplaying enduring problems in cities and the countryside, but the nation is doing well by almost any measure.

The world’s doing pretty well, too. Microsoft founder Bill Gates last year tweeted an infographic showing how much living conditions have improved over time. The number of people in extreme poverty has fallen from 94 percent in 1820 to under 10 percent today. Child mortality rates have dropped like a rock, while literacy rates have soared. Instead of welcoming this good news, commentators chided Gates for pointing it out.

Politicians and policy wonks of all stripes have a vested interest in depicting the world as far worse than it really is. It’s not hard to understand. No one follows a leader, or pays much attention to their policy proposals, if they argue that life is pretty good and mostly getting better.

Before we get taken in by grandiose political promises or radical political platforms, it’s worth recognizing this point made by the Brookings Institution: “Something of enormous global significance is happening almost without notice. For the first time since agriculture-based civilization began 10,000 years ago, the majority of humankind is no longer poor or vulnerable to falling into poverty.” Consider, also, that poverty today is a far cry from what it was in the past given the level of technological innovation that permeates every part of society.

There’s an entertaining little book from 1974 called “The Good Old Days—They Were Terrible!” It reminds Americans of the days of sweat shops, tenements, widespread opium addiction, of rampant crime and cities where horse poop (in the days before automobiles) was piled high on nearly every corner. We worry about air quality now, but it’s nothing compared to the Industrial Revolution. I was just in a museum in Pittsburgh, Pa., and was astounded by the dark-as-night daytime photos of the pollution-clogged city.

The first step in reducing poverty is understanding the fundamental nature of it. “(I)f we say that they’re poor because we rich people stole everything then the correct policy is going to be rather different from if we acknowledge reality,” argues Tim Worstall of the Adam Smith Institute in London. “Which is that abject poverty is the natural state of mankind and it’s wealth that is the thing that needs to be created to end it.”

Of course, we should try to fix problems and make life even better for more people, but we need to start with some real-world understanding. That begins with recognizing that freedom and the free marketplace are the sources of wealth—and that politicians who peddle doom and gloom are likely only to make us poorer and miserable.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2Ovlyon

via IFTTT

We’re deep into another presidential election. It’s a time when a few of the wealthiest, most cossetted and least appealing members of society try to convince us that America basically is an impoverished wasteland, filled with untold suffering and blight. The nation won’t heal itself until we put one of them in charge of its behemoth government.

“The United States has more people living in poverty than at almost any time in the modern history of our country,” intoned leftist Democratic candidate Bernie Sanders. He’s so out of touch with reality that he hired a top adviser who once praised the “economic miracle” in socialist Venezuela, which is one of the most genuinely miserable places on Earth.

The populist Right isn’t much better. Trump-supporting pundits have spread wild tales of misery afflicting the Rust Belt and the nation’s middle class, with Fox News’ Tucker Carlson last year engaging in an infamous critique of free-market capitalism. Their policy prescriptions (more government) aren’t remarkably different from those championed on the Left.

Obviously, in a land of 329 million flawed human beings one can always find stories of people who are living on the streets, lacking proper healthcare, addicted to drugs and whatnot. Some people are sick, unhappy, out of work and living crummy lives. The only thing lacking from these analyses is a little perspective about the human condition—and about the limits of government uplift.

The data shows that poverty is diminishing rapidly, which no doubt explains why the doom-mongers focus mainly on anecdotes. Conservatives (including President Trump) point to progressive San Francisco as a foreboding place filled with homeless encampments and crime. I’m in the city frequently. It has lots of self-imposed problems, but remains one of the wealthiest and most beautiful cities in the world. It’s easy to forget that crime rates are near-record lows in most of America.

I recently returned from rural Appalachia, another place that politicians point to as a sea of despair. The region is in decline, but it’s mostly a middle-class place. (Don’t tell Trumpsters this, but the best thing that could happen to these hard-edged towns—with their low-cost real estate and aging populations—is an influx of immigrants.) I’m not downplaying enduring problems in cities and the countryside, but the nation is doing well by almost any measure.

The world’s doing pretty well, too. Microsoft founder Bill Gates last year tweeted an infographic showing how much living conditions have improved over time. The number of people in extreme poverty has fallen from 94 percent in 1820 to under 10 percent today. Child mortality rates have dropped like a rock, while literacy rates have soared. Instead of welcoming this good news, commentators chided Gates for pointing it out.

Politicians and policy wonks of all stripes have a vested interest in depicting the world as far worse than it really is. It’s not hard to understand. No one follows a leader, or pays much attention to their policy proposals, if they argue that life is pretty good and mostly getting better.

Before we get taken in by grandiose political promises or radical political platforms, it’s worth recognizing this point made by the Brookings Institution: “Something of enormous global significance is happening almost without notice. For the first time since agriculture-based civilization began 10,000 years ago, the majority of humankind is no longer poor or vulnerable to falling into poverty.” Consider, also, that poverty today is a far cry from what it was in the past given the level of technological innovation that permeates every part of society.

There’s an entertaining little book from 1974 called “The Good Old Days—They Were Terrible!” It reminds Americans of the days of sweat shops, tenements, widespread opium addiction, of rampant crime and cities where horse poop (in the days before automobiles) was piled high on nearly every corner. We worry about air quality now, but it’s nothing compared to the Industrial Revolution. I was just in a museum in Pittsburgh, Pa., and was astounded by the dark-as-night daytime photos of the pollution-clogged city.

The first step in reducing poverty is understanding the fundamental nature of it. “(I)f we say that they’re poor because we rich people stole everything then the correct policy is going to be rather different from if we acknowledge reality,” argues Tim Worstall of the Adam Smith Institute in London. “Which is that abject poverty is the natural state of mankind and it’s wealth that is the thing that needs to be created to end it.”

Of course, we should try to fix problems and make life even better for more people, but we need to start with some real-world understanding. That begins with recognizing that freedom and the free marketplace are the sources of wealth—and that politicians who peddle doom and gloom are likely only to make us poorer and miserable.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/2Ovlyon

via IFTTT

I travel a lot. Every year I speak at about 50 law schools and lawyers groups across the country. On average, I fly approximately 100,000 miles per year (almost entirely on United). And I spend roughly 80 nights a year in hotels (almost exclusive at Marriott properties.) I recognize this schedule is not for everyone, but I have developed a system that makes it manageable. In short, I maximize my waking hours at home, and minimize my waking hours on the road. Here are ten tips I abide by, that may make your travels easier.

1. Where feasible, choose early morning flights over late-night flights the day before.

Virtually all of my trips are same-day jaunts. I recognize this option is not feasible for everyone, but it works well for me. I can take an early morning flight (usually before 7:30 a.m.) to just about anywhere in the country, and arrive in time for a lunchtime event. And I can usually catch an early afternoon return flight (usually around 3:00 p.m.), and be home in time for dinner. This schedule minimizes my time on the road. Often, groups will invite me out to lunch, or dinner after the event. Where feasible, I propose brunch instead. That is, we eat after I land at the airport, and before the event begins. That scheduling option allows me to quickly get out of town once I am done speaking. There is a huge difference between getting home at 7 p.m., and getting home at 9:00 p.m.

Only in rare circumstances will I fly in the night before, and spend a night in a hotel on the road. First, some invitations require me to speak in the morning–a noon arrival time is not sufficient. Second, some flights will not arrive early enough in the morning to make it work. For example, I cannot get to Boston in time for a noon talk. The flight-time is too long. And I cannot make it to Seattle or Portland in time–even with the time-zone changes, the flight is too long. Fortunately, Houston is roughly in the middle of the country–I can make it to New York, Chicago, and Los Angeles in three to four hours.

2. Avoid connecting flights where feasible.

I will only take a connecting flight in rare circumstances. Too much can go wrong. You have to worry about the inbound flight in your starting airport, and your inbound flight in the connecting airport. And if there is a delay, you have the stress of knowing you will have to run through the terminal. Flight attendants will often tell you “they’ll hold the flight.” They won’t. I once got stuck in Phoenix after I missed a connection on American. The door closed about a minute before I got to the gate.

I am fortunate to live near an intercontinental airport. Indeed, one of the biggest perks of teaching in Houston is the airport. I recognize people who live near smaller airports will have to take connections.

3. For early morning flights, consider staying at the airport hotel in your home city

Early morning flights are rough. A flight that leaves at 7:00 a.m. will board at 6:30 a.m. Delays in the morning can be mitigated by signing up for TSA-Pre, as well as Clear. These options allow you to zoom through security at most hours of the day. I seldom wait more than 5 or 10 minutes at any airport I visit with these features. Even so, getting to the airport at 6 a.m. is not easy. (I will discuss my approach for airport travel in the next section). About a year ago, I figured out a method to minimize the stress of an early-morning flight.

The George Bush Intercontinental Airport in Houston has a Marriott hotel on property. The interterminal train stops at the hotel. When I have an early morning flight, I usually spend the night at the Houston hotel. Specifically, around 10 or 11 p.m., around when I would usually go to sleep, I head to the hotel. I arrive at the hotel, and go right to sleep. (I have no problem sleeping at hotels.) This option lets me shift the commute from early in the morning (when I am half-asleep) to late at night (when I am wide awake). Let’s assume boarding is at 6:30 a.m. If I am staying at home, I would usually wake up around 4, leave for the airport around 5, arrive at the airport around 5:30, and clear security by about 5:45. But if I am staying at home, I can wake up at 5:30 for a 6:30 boarding time. So long as I am on the interterminal train by 6:00, I can get to my gate well before boarding. And with this option, I don’t need to worry about traffic or last minute delays in leaving the house. The bulk of my 80 hotel stays every year are in Houston.

Many international airports have hotels on property: Philadelphia, Atlanta, Detroit, San Francisco, O’Hare, Newark, to name a few. Some of these hotels require taking a bus shuttle. I do not prefer those hotels, because busses run on irregular schedules early in the morning (maybe every 15 minutes). The ideal hotels are those you can walk to through the terminal, or take an automated transportation system.

4. Do not drive to the airport. Uber there, and taxi back.

Over the past two years or so, I have more-or-less gone full Uber. I Uber to and from work, and most other places. I can easily work in the back of the car on my laptop, or take a nap if I’m tired. This approach, which is not cheap, has helped me generate between five and ten hours a week of found time. Even if you aren’t willing to take the plunge, I encourage you to consider avoiding the drive to the airport. The process of finding a garage spot can often be stressful, especially if lots are full. And that search may add 10 or 15 minutes to your commute. Ubering to the airport eliminates all of those problems.

But, I would not recommend taking an Uber from the airport. Invariably, the wait times are more than 10 minutes. And far too many Uber drivers engage in a scam: (1) you call an Uber, (2) they do not move, and call you ask where you are going, (3) then they say they will not drive you, and ask you to cancel the ride. I don’t bother anymore. I simply hop in a taxi from the cab line. They are always available, and will take you wherever you want to go. The price is more, though it becomes more reasonable during surge times (early in the morning, and during rush hour).

5. Take a risk: don’t get your destination too early, and don’t wait too long at the airport.

TSA recommends arriving at the airport two hours before your flight. This recommendation creates an absolute waste of time. I try to arrive at the airport about 30 minutes before boarding. In some cases, I’ve arrived 15 minutes before boarding, and was fine. (TSA Pre and Clear are essentials for this approach.) Taking a risk on this front will allow you to spend more time at home.

Moreover, I try to arrive at my destination with about an hour to spare. For example, if my event starts at noon, and there is a 15 minute ride from the airport to the destination, I will try to land around 10:45. But what about delays, you ask? Generally, flights that leave first thing in the morning have the fewest delays. Those airplanes are generally parked overnight from late-night arrivals. You do not have to worry about a delayed inbound. Flights later in the day are more likely to be delayed, because of delays that occurred throughout the course of the day. I have been using the one-hour rule for nearly a decade; it caused me to be late for an event only once. Several years ago, on a trip to Detroit, we waited on the tarmac an hour for de-icing. Even then, I managed to arrive at my event around 12:20. Not the end of the world.

6. Do not check bags, and limit what you carry through the terminal

When I travel alone on short deadlines, I never check bags. It takes additional time to check a bag at the terminal, and then additional time to wait for the bag upon arrival. Some smaller regional jets have limited overhead space that will not fit standard roller-boards. For those flights, bring a smaller roller-board. Waiting on the jet-bridge (where there is no climate control) is a waste of time.

Also, limit what you carry through the terminal. I have one roller-board, and my laptop bag. The laptop bag has a special flap, that allows you to put the handle of the roller-board through it. In other words, the two elements come one. I can hold onto the handle, and wheel both items through the terminal at a quick speed. That approach leaves my other hand free. I much prefer a roller-board with two big wheels, rather than the four small wheels. The latter are easier to navigate around sharp turns, but are harder to walk with at a fast clip. Also, the four-wheeled versions take up more space, and give you less room to pack.

When you are in the terminal, do not carry extra items in your hand. You will put them down somewhere, and forget them. Any food I buy goes either in my laptop bag, or in a plastic bag I drape over the roller-board handle. Everything is together. I always keep my jacket in the suitcase. It is too tempting to put a jacket down on a chair, and walk away without it. But doesn’t my jacket get wrinkled?

7. Do not worry about wrinkled clothing

When I first started traveling, I took steps to ensure that my clothes would not be wrinkled. I would carry a separate valet, where my suit and shirts were neatly folder. I would have to check this additional carry-on. Or I would gently lay my suit jacket on the overhead bin. (Invariably, someone put their suitcase on top of my spot). At a certain point, I said “forget it.” My clothes will be wrinkled, and I will be fine. I do ask the cleaners to fold up shirts, and place them in plastic wraps, rather than put them on hangers. This process makes transporting shirts easier. But suit jackets, ties, and pants are wrinkled. I’m okay with it.

8. Consolidate your flights and hotel stays to accrue loyalty status

I am fortunate to live in a city with a United hub. Almost 90% of the flights I take are on United. As a result, I maintain what is known as Premier 1K status. The biggest benefit is that I can board early. And, in theory at least, I can clear for upgrades (though those upgrades are increasingly rare.) There is another benefit that is less well-known. When a flight is cancelled, United will rebook you on another flight, and you leapfrog to the top of the standby line. That perk has ensured that I get home in time, versus spending the night in a random city.

I also primarily stay at Marriott Bonvoy properties. Here, the biggest parks are early check in (around noon) and late-checkout (around 4:00 p.m.). These features allow you to maximize flexibility of travel. If I need a late checkout at a non-Marriott property, I am usually able to pay an additional amount, or simply book a second night.

9. Where it saves time, consider mixing and matching airports/airlines

In the previous tip, I urged you to consolidate all of your travels on a single airline and hotel chain. But in some cases, it is useful to mix and match. For example, if I have a lunchtime event in Salt Lake City, I take a 6:00 a.m. flight on Delta, but return home on a 3:00 p.m. flight on United. Or if I am flying to Chicago, I may fly inbound on Southwest to Midway, and outbound from O’Hare on United. (This option requires ubering to the airport, as I take off and land at different airports in Houston.) And if I am staying at a conference hosted at a Hilton or Hyatt property, I book that brand–you save time coming and going from the airport. Get creative with your booking. You can minimize how much time you spend on the road.

10. Don’t stress

Travel can be stressful. If your flight is delayed, nothing you can do will eliminate the delay. Nothing you say to the flight attendant will remove the delay. If your flight is so delayed that you will miss your event, simply walk off the plane (if the door is open) and reschedule. People understand bad things happen. But don’t get irate at things. Don’t mutter and complain. Everyone on the plane is in the same boat. Use that additional time to get work done, or focus on some other matters. Don’t stress.

from Latest – Reason.com https://ift.tt/2vg2IuM

via IFTTT

If Donald Trump could shoot somebody in the middle of Fifth Avenue and get away with it, what brazenness might we expect from his fellow septuagenarian Manhattanite presidential candidate, Michael Bloomberg?

The then–mayoral candidate gave us a glimpse back in 2001, when he was dumping his first tranche of $74 million into a late-in-life political career and a reporter asked him whether he had ever smoked marijuana. “You bet I did,” the media mogul enthused, at a time when politicians tended to be much more reticent about such things. “And I enjoyed it.”

Talk about do as I say, not as I did. During Bloomberg’s three terms as mayor, the Big Apple became the marijuana arrest capital of the world, thanks to the notorious stop-and-frisk searches conducted largely in neighborhoods where billionaires rarely venture.

Hizzoner’s conscience has never been noticeably troubled by such obvious disparities under the law. If anything, the disproportionate impact of his policy preferences on poorer folk has been the point.

In an April 2018 conversation with Christine Lagarde, then the managing director of the International Monetary Fund, Bloomberg defended his fondness for taxing treats, such as sugary sodas and trans fats, that are mostly enjoyed by the non-rich.

“Some people say, well, taxes are regressive,” he said. “But in this case, yes they are! That’s the good thing about them, because the problem is in people that don’t have a lot of money. And so, higher taxes should have a bigger impact on their behavior and how they deal with themselves….The question is, do you want to pander to those people, or do you want to get them to live longer?”

Rules may be important for “those people” but are much less so for the eighth-richest man on the planet. He is the leading financier of gun control advocacy in America—and one of the few people allowed to have an armed security detail in Bermuda. He has been positively Trumpian about releasing his tax returns, snapping at the mere suggestion that such political traditions should apply to him. And as recently as January 2019, even as the rest of the Democratic Party was finally evolving toward getting rid of federal prohibitions on the marijuana Bloomberg once enjoyed, the former mayor called pot legalization “perhaps the stupidest thing we’ve ever done.”

If George W. Bush and Barack Obama ushered in the return of the imperial presidency, Trump represents a further devolution toward the imperious presidency. There was an audacity in Obama’s pen and phone, and there was an expansive theory of executive branch autonomy spearheaded by former Vice President Dick Cheney. Trump’s contribution has been more vulgar, more direct, more New York: “I dare you to stop me” mixed with “I can say anything I want.”

Bloomberg’s manners are more refined, but only just. There’s the locker room talk about women, which he pre-emptively apologized for in advance of his presidential run. Trump may troll people about seeking a legally proscribed third term, but Bloomberg actually went there, changing New York City law near the end of his second mayoral term in order to run for a third, and then switching it back soon after winning. As TheNew York Times noted dryly upon the latter occasion, “Bloomberg thinks that being able to serve three terms in office is a good idea—just not for anyone else.”

Bloomberg’s above-the-law demeanor might seem preferable to Trump’s appetite for corruption, but their approaches to how the law applies to the lowly are distressingly similar. To Trump, constitutional limits to executive power are speed bumps slowing down his policy goals, especially concerning immigration. To Bloomberg, policy ends can justify means that judges have explicitly ruled unconstitutional. “I think people, the voters, want low crime,” he told the Times in September 2018, defending the practice of stop and frisk. “They don’t want kids to kill each other.”

It seems implausible that, in an era of resurgent Democratic populism, primary voters will reward the kind of bluenose who has appeared in skits as “King Michael.” But seeing Bloomberg even in fifth place extends a worrying trend. We’ve stacked up so much power at 1600 Pennsylvania Avenue that billionaires with insatiable ambitions are eyeing the address greedily and finding market share among understandably disgruntled voters.

“The president,” lawyer Alan Dershowitz said on Fox News host Laura Ingraham’s show last year, “has the power that kings have never had.” Until we start denuding the Oval Office, we will continue getting the royals we deserve.

from Latest – Reason.com https://ift.tt/2UyCMEY

via IFTTT