NOTE: THIS DAILY BRIEFING WAS FILMED THURSDAY, NOVEMBER 5. Fielding questions from Real Vision subscribers, senior editor, Ash Bennington, and managing editor, Ed Harrison, analyze how the various outcomes of the 2020 U.S. election will impact markets. Ash and Ed talk about the future of Real Vision content, price action across bitcoin, bonds, and equities, and the likely underperformance of the 60/40 portfolio should the economy enter a cyclical downturn. Ash and Ed analyze how the prospect of divided government (i.e., a Biden presidency coinciding with a Republican senate) will affect earnings potential and fiscal stimulus. They also share their views on potential cabinets picks for the next U.S. President.

via ZeroHedge News https://ift.tt/3nbRBIC Tyler Durden

Trump Admin Prepares “Flood” Of Iran Sanctions To Take Effect By Jan. 20 Tyler Durden

Mon, 11/09/2020 – 18:20

The Trump administration plans to throw everything it can against the Iranians before January 20 — the day Joe Biden would be inaugurated and take the White House.

According to Axios on Sunday Pompeo is preparing a “flood” of sanctions in an attempt to ensure the Biden administration would have many more hurdles if it hopes to restore the 2015 nuclear deal brokered under Obama, as Biden previously vowed during the campaign.

One unnamed Israeli source privy to discussions involving US Iran envy Elliott Abrams, Israeli PM Benjamin Netanyahu, and national security adviser Meir Ben-Shabbat told Axios’ Barak Ravid that “The goal is to slap as many sanctions as possible on Iran until Jan. 20.”

Elliot Abrams is in Israel Monday to coordinate new sanctions against Iran. File image: US State Department via Wikimedia Commons.

The detail which is sure to enrage leaders in Tehran the most is that sanctions targeting the Islamic Republic’s ballistic missile program will be done “in coordination with Israel and several Gulf states” — which is the result of the recent peace deals between Israel and Arab League member states, the foremost of which was struck with UAE.

The US administration has reportedly prepared a “target bank” of further entities to be sanctioned, after far-reaching sanctions have already been in place against everything from the auto to aviation to energy to banking sectors.

Instead of targeting Iran’s nuclear development capabilities directly, which it is believed will be easier for a future Biden administration to peel back, the new sanctions “flood” will focus on Iran’s ballistic missiles production and capability.

Last month the Trump White House lost its bid for the United Nations to extend a longtime conventional weapons embargo on Iran, which expired Oct. 18, now allowing the Islamic Republic to buy and sell arms without violating international law.

via ZeroHedge News https://ift.tt/3lfvxfR Tyler Durden

Fox’s Neil Cavuto Interrupts Trump Campaign Broadcast Over Election Fraud Claims ‘Without Proof’ Tyler Durden

Mon, 11/09/2020 – 18:00

Fox News host Neil Cavuto cut away from a Trump campaign press conference on Monday during which White House press secretary Kayleigh McEnany – speaking in her “personal capacity” – claimed that Democrats were ‘inviting fraud’ by disallowing GOP observers to watch the Pennsylvania ballot count.

“One party in America that opposes verifying signatures, citizenship, residency, eligibility. There is only one party in America trying to keep observers out of the count room – and that party, my friends, is the Democrat party.

“You don’t take these positions because you want an honest election. You don’t oppose an audit of the vote because you want an accurate count. You don’t oppose our efforts at sunlight and transparency because you have nothing to hide. You take these positions because you are welcome fraud, and you are welcoming illegal voting.“

“Our position is clear, we want to protect the franchise of the American people. We want an honest, accurate, lawful count. We want maximum sunlight. We want maximum transparency. We want every legal vote to be counted, and we want every illegal vote –“

“Woah, woah, woah,” Host Neil Cavuto then cut in, according to the Washington Examiner. “I just think we have to be very clear. She’s charging the other side is welcoming fraud and welcoming illegal voting. Unless she has more details to back that up, I can’t in good countenance continue showing you this.”

“I want to make sure that maybe they do have something back that up,” Cavuto added. “But that’s an explosive charge to make, that the other side is effectively rigging and cheating. If she does bring proof of that, of course, we’ll take you back. So far, she has started saying, right at the outset, welcoming fraud, welcoming illegal voting. Not so fast.”

Watch:

Fox’s Neil Cavuto cuts away from WH Press Secretary Kayleigh McEnany at Trump campaign press conference talking about their legal challenges. “I can’t in good countenance continue showing you this,” he says, until they bring proof that Dems are welcoming fraud and illegal voting pic.twitter.com/VUeNdUY8M4

As a reminder, there have been multiple on-record allegations of voter fraud from USPS employees and poll workers, while GOP poll watchers claim they were prevented by Democrats from performing a meaningful observation of poll counts.

Is Fox News deliberately trying to get rid of its conservative audience by giving it the middle finger, or have Fox hosts just lost just any ability to hide their hatred of the 70 million Americans who don’t have Trump Derangement Syndrome? https://t.co/if4fvsHIbk

In Painful Flip-Flop Deutsche Says It “Was Wrong To Close Dollar Short”, Reinstates It… As Dollar Surges Tyler Durden

Mon, 11/09/2020 – 17:40

Last Wednesday, as the market gyrated in response to what appeared to be the collapse of “Blue Wave” expectations, Deutsche Bank jumped the gun when its chief FX strategist George Saravelos rushed to close out his dollar short position, saying that “with the US election outcome extremely uncertain” he changed his USD view and turning neutral as he “no longer sees a compelling narrative of dollar weakness into year-end for three reasons.”

First, whoever wins the White House, the odds of a structural shift towards easier fiscal policy in the US have dramatically declined. Should the Democrats lose the Senate (the risk of this now appears high) and unified government becomes impossible, this would make agreement on sizeable fiscal expansion more difficult. Wider twin deficits and reflationary steepening in the US yield curve was an important driver behind our negative dollar view and this has been put on hold.

Second, the risks of a protracted contested election outcome appear significant. The market is likely to be most concerned by genuine uncertainty on the vote margin rather than political uncertainty relating to a refusal to concede. At the time of writing, the margins on numerous key states are very narrow (Georgia, Nevada, Wisconsin) or uncertain (Pennsylvania, Michigan), leading to a risk of protracted recount and litigation battles. This could last well into December.

Third, and beyond the election, the COVID winter wave has proven quicker and bigger than we thought. Europe is already on “soft” lockdown and the US numbers are likely to get worse.

Ironically, and as we pointed out last week, shortly after DB reversed its position, the dollar reversed its brief jump and collapsed, suffering its biggest decline since August.

One day after Deutsche Bank closes its USD short, dollar has worst day since August

The US currency then continued to slide and dropped every single day since DB closed out its dollar short…

… bringing us to today, when in yet another delightful moment of Wall Street revisionism on par with that from JPMorgan, the Deutsche strategist flip-flopped on his last week all, writing “we were wrong to close our dollar short. We reinstate it.“

Here is why according to George, everything he said less than a week ago is dead wrong and in fact the opposite case is now in play:

For the last three months we have been arguing that a Biden election victory would be the single most important negative event for the dollar this year. We closed our bearish dollar view on Wednesday as it looked like the US election was going to be contested. We were wrong: Biden has emerged as the clear President-elect this weekend and the market is sending a strong message of looking through any remaining uncertainty. We were therefore wrong to close out our dollar short and we reinstate it. We believe the broad trade-weighted dollar has the potential to drop by another 3-5% into the end of the year with EUR/USD convincingly breaking 1.20, USD/JPY reaching 100 and USD/CNH 6.40, as highlighted by our Asia colleagues on Friday. It all boils down to three drivers:

The unwind of the Trump dollar risk premium. we have demonstrated the strong positive correlation between measures of global uncertainty and the dollar.

The two biggest drivers of this uncertainty have been President Trump’s foreign policy as well as the Coronavirus. A shift to a more multilateral approach under Biden and a probable end of diplomacy by Tweet is going to be an important structural shift for the market in coming months that will take time to price in. Additionally, any vaccine announcement that reduces the market’s perception of the Coronavirus “tail” is likely to further reduce uncertainty. In all, an unwind of global uncertainty to pre-2016 levels would be associated with another 5-10% drop in the dollar.

The return of carry and the dollar as a funder: a Blue Wave was the most dollar negative outcome in the scenario analysis we published last week: more fiscal spending under unified government and widening twin deficits would have been important structural headwinds for the dollar. Yet the flipside of (a likely) divided government is that the market no longer has to worry about higher US yields. We have long emphasized how extremely underweight the market is in EM FX, especially the high-yielders. As we argued last week, we are moving back into a “secular stagnation” regime of low growth, low inflation and low yields – with no trade wars and no Fed hikes like 2018-19. There is plenty of potential for the market to build dollar shorts and use the greenback as a funder.

More virus divergence ahead of us: We noted a couple of weeks ago that what matters more for Europe is not the lockdowns but the second virus wave being brought under control. The virus case numbers are already peaking in the Netherlands and Spain, decelerating in Germany and there is evidence that the French positivity rate is peaking. North Asia continues to stand out for its superior virus and growth outcomes. In contrast, we not only worry the US virus numbers will get worse, but given the reluctance to impose more serious control measures in earlier waves it may take longer than Europe. This would be reminiscent of the first “virus divergence” episode of early summer.

Summing up DB’s latest position: “the removal of global uncertainty, a shift to dollar funding, and virus divergence against the US all favor a weaker dollar into the end of the year. China is emerging as the clear antipole of global growth and yield outperformance with CNH serving as an important anchor for broader dollar weakness. Our official forecasts already incorporate expectations of a weaker dollar into year-end so remain intact in line with the targets above.”

There was just one problem: having published this note overnight, it failed to account the latest market-moving Pfizer news which have sent Treasury yields surging, and bringing rate hike odds much closer to the present, as we noted earlier.

As a result, the market is starting to look through the entire deflationary phase of the next 2-3 years which had been fully priced in by now, and is instead starting to price in what may be Fed rate hikes as soon as 2023, or even 2022 (if note sooner) which – drumroll – has sent the dollar sharply higher!

One truly really couldn’t make this up, and for the sake of DB’s Saravelos, we can only hope that the spike in the dollar fades, or else the FX strategist will have no choice but to tell his whiplashed clients that he was wrong about being wrong about closing his dollar short.

via ZeroHedge News https://ift.tt/3n8NJbz Tyler Durden

Asset inflation benefits the super-rich more than anyone else because they own the vast majority of these assets.

With the reflation euphoria running full blast, maybe central banks will finally get all that inflation they’ve been pining for. So let’s ask cui bono–who will benefit from inflation?

The Super-Rich love inflation and the money-printing that generates it. Longtime correspondent Michael M. explains the dynamic behind billionaires’ adoration of inflation:

“Why does a game of Monopoly work? Because there is a zero-boundary for every player’s net worth.

If you were given endless credit (so negative net worth is allowed without limit), the game becomes pointless.

Is there also an upper bound at Monopoly?

Well, the bank at Monopoly can run out of money, I had that happen a few times while playing. But we didn’t treat it as an upper boundary, but wrote the richest player an IOU and took that amount of cash bills from him and put them back in the bank to continue.

Rolling it around in my head, how else could you solve that problem? Confiscate the same amount from every (remaining) player and put it back in the bank instead? That would be pointless if most wealth is with one player and you want the game to continue.

Another option is to go Keynesian [in its true practical implementation] and confiscate 10% of each player’s net worth to “re-liquidate” the bank. This is very similar to “printing money,” just more explicit. Now we’re getting somewhere.

But that’s linear (a fixed percentage), so why not go with progressive confiscation rates, and take a higher percentage of the wealthier players’ net worth?

Wait a second, did I just stumble over the reason why the filthy rich love Keynesian economics? Because printing money only “taxes” everybody linearly, which is much better for the rich than progressive taxation, which is the global standard in income tax policies.”

Let’s explore this profound insight a bit more. Modern Monetary Theory (MMT) holds that central banks/states can print as much money as they want without any adverse effects. From this, it’s a small step to sending every household a monthly stipend (Universal Basic Income–UBI) paid by freshly issued currency.

Given the unfairness of the income tax system, as the super-rich buy tax breaks, tax shelters and subsidies via lobbying and political contributions, it’s just one more tiny step to eliminating income taxes entirely and printing all the money the state needs.

Why would this enrich the super-rich and impoverish the rest of us? Printing money in excess of the goods and services being generated creates inflation, which is a “tax” on all cash and wages, both of which have been losing ground for decades.

Inflation is best defined as a loss of purchasing power. With 10% inflation, $1 only buys 90 cents of real-world goods and services. Thus it’s the exact equivalent of a 10% tax not just on wages but on all cash.

The super-rich don’t rely on wages or cash savings; they own productive assets whose yields rise with inflation. The super-rich own apartments, so they can jack rents up 10%, matching inflation. They own assets which tend to retain their purchasing power even as inflation reduces the purchasing power of cash and wages.

Markets place a premium on any assets that keep pace or outpace inflation, so the value of the assets owned by the super-rich soar, further enriching the few who own these assets.

Asset inflation benefits the super-rich more than anyone else because they own the vast majority of these assets. So money-printing and the inflation it generates is a win-win for the rich. The “tax” rate of inflation / money-printing barely touches their incomes or wealth, both of which are tied to assets that rise along with inflation. All that money-printing pushes the value of their assets higher, making them even richer, which the inflation “tax” impoverishes everyone who depends on wages and cash.

No wonder the super-rich love MMT, money-printing and Keynesian giveaways of freshly printed currency – inflation makes them richer while it makes everyone else poorer. Going back to Michael’s analogy of a Monopoly game: inflation takes 10% of every player’s cash, but doesn’t touch their property holdings. So the wealthiest players’ net worth is barely dinted while players with fewer assets will find it difficult to survive as their cash is “taxed” away by inflation.

Fed Warns Assets Could Suffer “Significant Declines” If Covid Is Not Contained Tyler Durden

Mon, 11/09/2020 – 16:59

While it’s a little odd to read about market and economic risks on the day the every major index hit an all time high (then slumped) amid expectations the economy is on its way to a full recovery thanks to some vaccine which may or may not be available in early 2021 and which half the population have sworn they will not take, moments ago the Fed published its latest semi-annial Financial Stability Report, in which it emphasized that risk assets could be hit if the coronavirus pandemic’s economic impact worsens in coming months, to wit: “the COVID-19 shock highlighted how vulnerabilities related to leverage and funding risk at nonbank financial institutions could amplify shocks in the financial system in times of stress.”

While “asset prices have generally increased since May, and, when adjusted for low interest rates, valuation pressures appear roughly in line with their historical norms”, the Fed warned that “uncertainty remains high, and investor risk sentiment could shift swiftly should the economic recovery prove less promising or progress on containing the virus disappoint.”

So worried is the Fed about the impact of covid that it dedicated the entire first section in its “near-term risk” section to covid, in which it said that “investor risk appetite and asset prices have increased in recent months but could suffer significant declines should the pandemic take an unexpected course or the economic recovery prove less sustainable.” The Fed also also warned that “the leverage of some nonbank financial institutions, such as life insurance companies and hedge funds, is high, exposing them to risks stemming from sharp drops in asset prices and funding illiquidity risks.“

The effects of the pandemic have increased the vulnerabilities of the financial system to future shocks, including additional waves of substantial COVID-19 outbreaks

Most forecasters expect a moderate recovery in economic output in the United States and abroad following a global recession, but uncertainty surrounding this outcome is unusually high. The sharp slowdown in economic activity has disproportionately affected some businesses and households, and a further weakening in the balance sheets of those that are especially vulnerable could affect the financial system. Furthermore, monetary and fiscal policy tools have limited ability to moderate some dimensions of what is fundamentally a public health shock.

If the pandemic persists for longer than anticipated—especially if there are extended delays in the production or distribution of a successful vaccine—downward pressure on the U.S. economy could derail the nascent recovery and strain financial markets and financial institutions, particularly if many businesses are shuttered again and many workers are laid off and left without a normal income for a long period. If that were the case, a number of the vulnerabilities identified in this report could grow further, making them more likely to amplify negative shocks to the economy.

Investor risk appetite and asset prices have increased in recent months but could suffer significant declines should the pandemic take an unexpected course or the economic recovery prove less sustainable.Given the generally high level of leverage in the nonfinancial business sector, prolonged weak profits could trigger financial stress and defaults. In addition, a protracted slowdown could further harm the finances of even high-credit-score households, which could lead to defaults and place financial pressure on banks and other lenders. Broader solvency issues could impair the ability of some financial institutions to lend or induce increased asset sales and redemptions of withdrawable liabilities.

Although leverage remains at modest levels at banks, broker-dealers, and other financial institutions, the leverage of some nonbank financial institutions, such as life insurance companies and hedge funds, is high, exposing them to risks stemming from sharp drops in asset prices and funding illiquidity risks. Furthermore, prime MMFs and fixed-income mutual funds remain vulnerable to funding strains and sudden redemptions, as demonstrated during the acute period of extreme market volatility and deteriorating asset prices earlier this year. While government support has lowered the risk of adverse events associated with vulnerabilities in the nonbank sector, this sector would be vulnerable to funding risk should the government support be withdrawn.

Indicatively, the Fed is eyeing the following chart which shows that despite a record number of daily cases in the US, the number of corona-linked deaths have barely budged.

The smartest academics in the room also warned that “some segments of the economy, such as energy as well as travel and hospitality, are particularly vulnerable to a prolonged pandemic.” Furthermore, “within CRE, retail, office, and lodging properties exhibit the highest vulnerability” while commercial property values which have been especially sensitive to the pandemic, have already begun falling.

As a result, “uncertainty remains high, and investor risk sentiment could shift swiftly should the economic recovery prove less promising or progress on containing the virus disappoint.” Furthermore, some segments of the economy, “such as energy as well as travel and hospitality, are particularly vulnerable to a prolonged pandemic. Within CRE, retail, office, and lodging properties exhibit the highest vulnerability.”

As such, a vaccine that lessens the virus’s threat is vital to commercial real estate, which has much to gain if people begin working, shopping and traveling again at pre-Covid levels, the Fed said.

Besides covid, the Fed listed risks in the following categories:

Disruptions in global dollar funding markets remain an important source of risk

Stresses emanating from Europe also pose risks to the United States because of strong transmission channels…

… and adverse developments in emerging market economies with vulnerable financial systems could spill over to the United State

Additionally, as part of its market intelligence gathering for this report, the Federal solicited views from a wide range of contacts on risks to U.S. financial stability. From early September to mid-October, the staff surveyed 24 contacts at banks, investment firms, academic institutions, and political consultancies. As shown in the figure, respondents frequently cited concerns about U.S. political uncertainty as well as the risk of a COVID-19 resurgence generating renewed restrictions. Relatedly, a large share of respondents highlighted uncertainty surrounding the likelihood and efficacy of a policy response to economic weakness as well as concerns over the potential for increased insolvencies among nonfinancial corporates and small businesses.

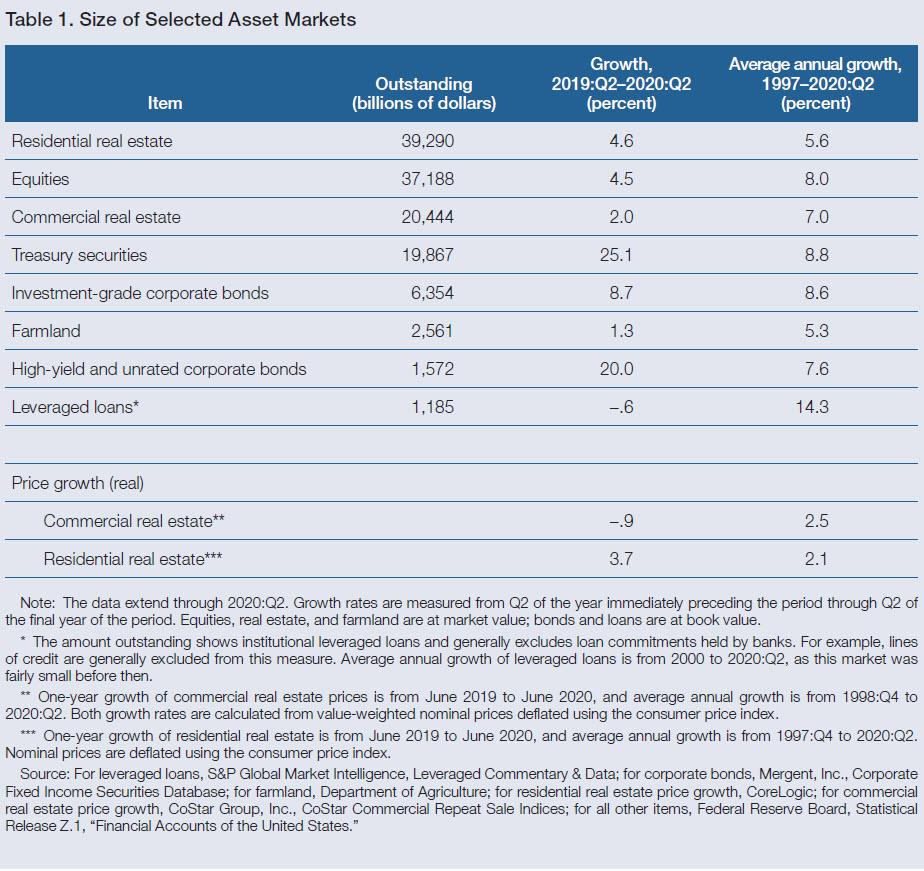

The Fed also showed the size of the various asset markets discussed, with the largest asset markets are those for residential real estate, corporate public equities, CRE, and Treasury securities:

In what may be the most accurate thing it has ever said, the Fed warned that that vulnerabilities tend to build up over time – like for example the 11 years since the launch of QE – and are “the aspects of the financial system that are most expected to cause widespread problems in times of stress.” As a result, the Fed’s framework focuses primarily on monitoring vulnerabilities and emphasizes four broad categories based on research which include i) elevated valuation pressures, ii) excessive borrowings by businesses and households, iii) excessive leverage in the financial sector; and iv) funding risks.

According to Bloomberg, Fed Governor Lael Brainard, who has led the central bank’s stability reporting efforts and who is rumored to be Joe Biden’s top choice for Treasury Secretary, said the report shows that some of the same nonbank financial sectors that were troublesome in the 2008 meltdown are posing dangers in this crisis, which “highlights the importance of a renewed commitment to financial reform” although it is unclear how the Fed is reforming the system when it keeps injecting $120BN in liquidity every month.

“If the pandemic persists for longer than anticipated — especially if there are extended delays in the production or distribution of a successful vaccine — downward pressure on the U.S. economy could derail the nascent recovery and strain financial markets,” the report said. “Given the generally high level of leverage in the non-financial business sector, prolonged weak profits could trigger financial stress and defaults.”

And while there is much more in the full report (embedded below and linked here), including a lot of pretty charts one thing to note is that for the first time ever, the Fed included a section discussing the “implications of climate change for financial stability.” In other words, it’s not the Fed’s fault there is a massive bubble: blame the weather.

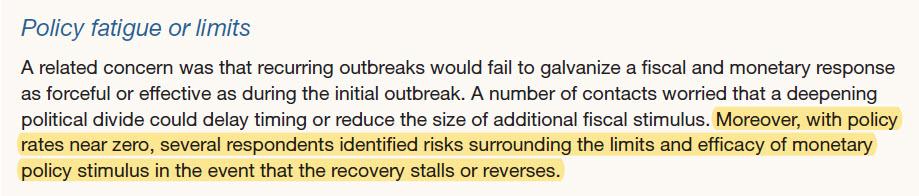

One final point: in perhaps the most ominous note in the report, the Fed warned that its own tools may soon be useless:

via ZeroHedge News https://ift.tt/32sbbIV Tyler Durden

Parler Becomes Most Downloaded App As Conservative-Driven Revolt From Twitter Intensifies Tyler Durden

Mon, 11/09/2020 – 16:41

Conservative politicians from President Trump to Senate members have railed against social media companies for their brazen censorship and de-platforming of conservative social media users. In recent weeks, Republicans on the Senate Commerce Committee grilled Facebook’s Mark Zuckerberg, Google’s Sundar Pichai, and Twitter’s Jack Dorsey over their content-moderation practices.

Lately, Republican social media users, who have been censored or de-platformed, have embarked on a great migration to a new platform, that is, Parler, bills itself as a Twitter rival with “an unbiased social media focused on real user experiences and engagement.”

According to radio host Dan Bongino, who has an “ownership stake” in Parler – the platform has “exploded” with new users:

“We’re adding thousands of users per minute, and we’re working out the glitches as a result.”

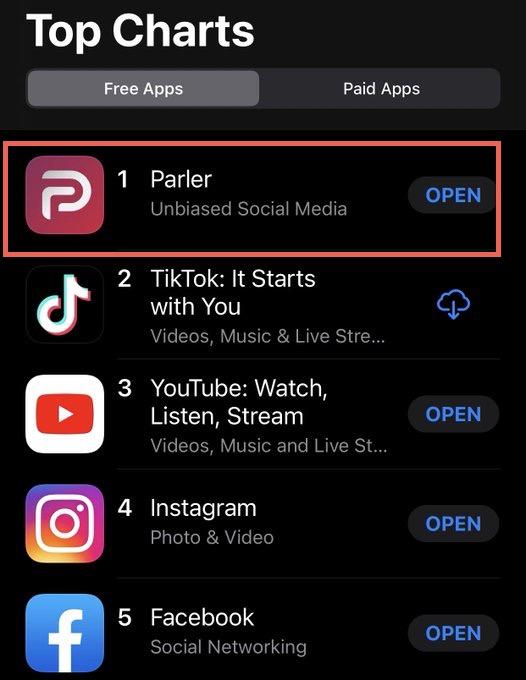

The influx of new users, likely ex-Twitter/Facebook Republican folks, who have had their content censored or have been banned from the platform or are just fed up with liberals censoring their every tweet/post, have made Parler the “most downloaded application in the US on Google Play, overtaking such platforms as TikTok, Instagram, and Twitter,” said RT News.

“Prior to June, Parler was averaging about 2,000 downloads. Its user base doubled that month, to about 1.5 million, after Twitter’s banning of conservative meme creator Carpe Donktum sparked an anti-censorship backlash. Parler is now reportedly adding as many users per minute as it used to gain in a day,” RT said.

Bongino tweeted that “liberal lunatics” running social media platforms such as Facebook and Twitter “have awakened a sleeping giant. We gave a collective middle finger to the tech tyrants just now as Parler became the NUMBER ONE most downloaded app in the world.”

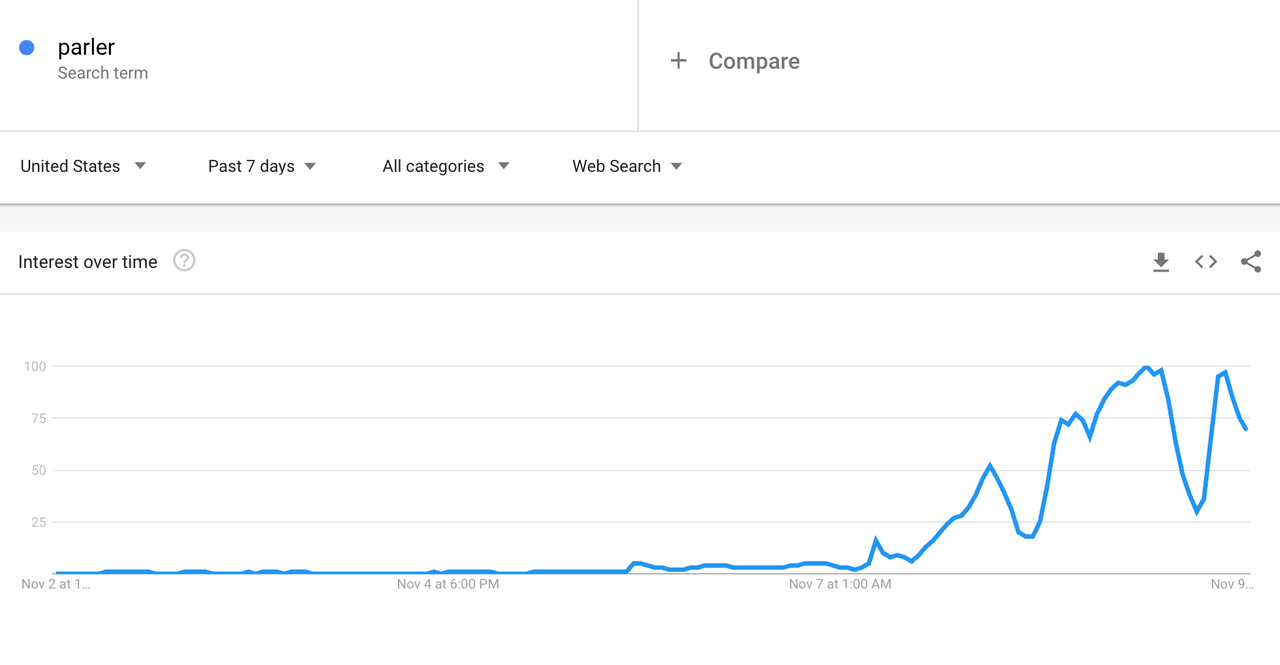

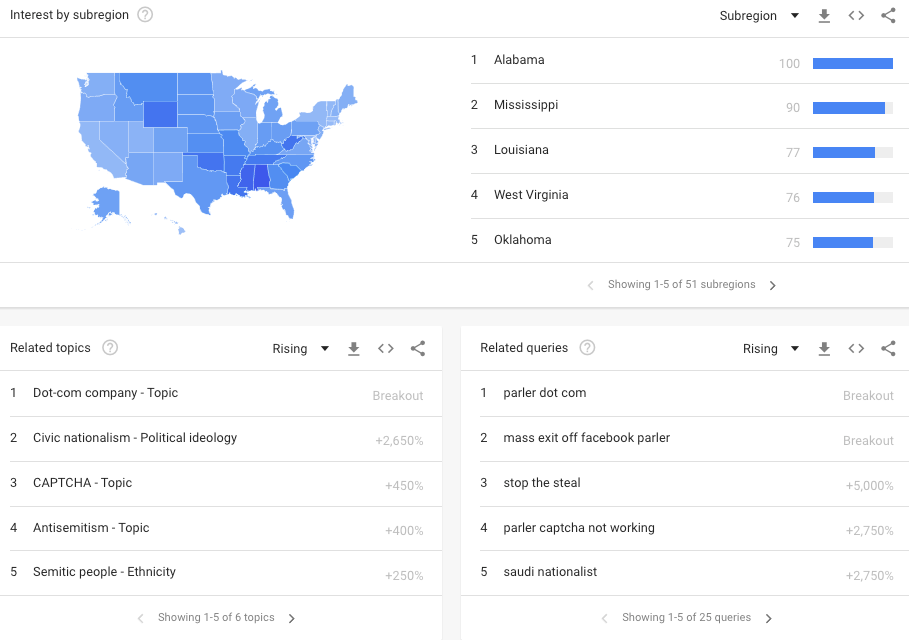

Internet searches for “Parler” have exploded in the last few days.

Many of the folks searching for “Parler” are based in conservative states, including Alabama, Mississippi, Louisana, West Virginia, and Oklahoma.

The exodus of Republicans from Twitter and Facebook to Parler appears to have begun shortly after NYPost’s Hunter Biden story was censored by social media giants in mid-October.

via ZeroHedge News https://ift.tt/3eGvkQe Tyler Durden

President-elect Joe Biden has promised to fully reinstate the DACA program as one of his first steps, once he formally becomes president on January 20. DACA is the Obama-era program suspending deportation of some 800,000 undocumented immigrants who came to the United States as children. It allows such migrants (often referred to as “Dreamers,” after the Dream Act, which failed to pass Congress) to stay in the U.S. as long as they arrived in the country when they were 15 years old or younger, were 30 or younger when the program began in 2012, have not been convicted of any crimes as of the time they apply for the program, and have either graduated from a U.S. high school, are currently enrolled in school, or have served in the armed forces. In addition to suspending deportation, the program also allows DACA recipients to obtain authorization for work in the US and accrue “lawful presence.”

Biden’s plan to fully reinstate DACA will almost certainly be challenged in court by red state governments and others, who will argue that it exceeds the legal scope of presidential power. The most vulnerable point of the program is the grant of “lawful presence” to recipients. For reasons I summarized here, this provision doesn’t actually do very much. It is not necessary to protect Dreamers from deportation, and all it really does is enable them to accrue eligible time for the receipt of Social Security and Medicare benefits that, however, they are unlikely to ever actually collect unless their status is genuinely legalized at some point in the future, and they remain in the US until after retirement age. If the latter were to happen, the legislation granting legal status could easily also grant lawful presence for the entire period Dreamers spent in the United States, regardless of whether the DACA executive action previously did so.

But, despite its substantive insignificance, the grant of “lawful presence” is easily attacked as going beyond a mere exercise of prosecutorial discretion not to deport migrants, and instead extending an “affirmative benefit.” This idea was emphasized by lower court decisions striking down the larger DAPA program in 2016, and by the conservative dissenters in last year’s Supreme Court case.

The incoming Biden administration can easily eliminate this vulnerability simply by omitting “lawful presence” from its new order reinstating DACA. Alternatively, Biden could include a severability provision in the order, clearly indicating that the rest of the order will remain in force if the lawful presence element gets invalidated in court. Such “severability clauses” are given great deference by courts when they are included in congressional legislation. It is less clear that courts will respect a severability clause in an executive order. But there is at least a substantial likelihood they will.

The grant of work permits can also be attacked as an “affirmative benefit.” In this case, however, the benefit in question does have congressional authorization, based on a 1986 law that specifically permits employment of aliens who are “authorized … to be employed … by the attorney general.” There is no such unambiguous legislative authority for a grant of “lawful presence.”

There are other arguments against the legality of DACA. I addressed them in some detail here and here. But they are much weaker than the attack on “lawful presence.” Excising the latter could well make the difference between victory and defeat in court.

In the long run, the best way to institutionalize DACA would be for Congress to pass legislation to that effect. Even if Biden reinstates the policy through executive action, and it survives legal challenge, a future administration could potentially rescind it later, so long as it gets its administrative-law ducks in line. Not every GOP administration is likely to be as shambolic as Trump’s often is.

In the meantime, however, a successful executive reinstatement of DACA can provide much-needed protection for hundreds of thousands of vulnerable immigrants who would otherwise be subject to the threat of deportation through no fault of their own. That’s good for both them and the US economy, which benefits greatly from their many contributions. Dropping the questionable “lawful presence” element of DACA (or at least making it clearly severable) is a small price to pay for achieving that goal.

from Latest – Reason.com https://ift.tt/35ey1Wk

via IFTTT

{kind=link}