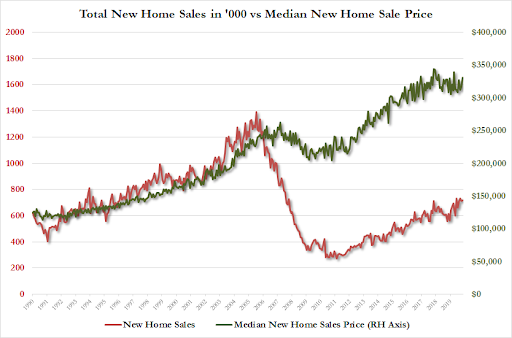

US New Home Sales Disappoint As Median Price Soars

Despite homebuilder sentiment soaring to 20-year highs, existing home sales slipped unexpectedly in November and new home sales are also expected to decline marginally MoM, but instead surprised to the upside with a 1.3% MoM.

However, the beat was due to a major downward revision from -0.7% MoM to -2.7% MoM for October.

Year-over-year, new home sales growth slowed to +16.9%…

Source: Bloomberg

Due to the downward revisions, new home sales are following the trend of existing home sales lower…

Source: Bloomberg

In the three months through November, purchases averaged a 720,000 pace, the strongest in 12 years.

Purchases of new homes rose in two of four U.S. regions, led by a 52.4% surge in the Northeast and a 7.5% gain in the West, which recorded its highest sales level in two years.

But, more problematically, the median home price soared 7.2% to $330.8k – the highest since April…

21% of new homes sold in Nov. cost more than $500,000, up from 19% prior month.

Flip on CNBC, pick up a financial paper, or scroll a financial website and you will find a great range of materials discussing the stock market, hot stocks, bad stocks, stock trading tips, and stock investment strategies.

Why? Because stocks are sexy, and the Wall Street casino — with all its flickering lights, screaming patrons, and carnival barkers — makes money for the purveyors of products ranging from IPOs to mutual funds and investment research.

On the other hand, you don’t hear much about bonds. Why? Because bonds are boring? Maybe so. Historically, however, discounting bonds has constituted an investment mistake, and the inevitable cooling down and possible volatility of the stock market in the next decade will make bonds a crucial part of your portfolio.

“A BNY Mellon Investment Management national survey on fixed-income investing was stunning: A measly 8% of Americans were able to accurately define fixed-income investments.

The 29-question online survey of just more than 2,000 adults, conducted in July, clearly shows that many Americans admit to having little knowledge about various fixed-income markets and how to invest in them. Here’s a rundown of those who answered “I do not understand it at all” with regard to the following types of bonds: Treasuries, 39%; municipal bonds, 45%; high-yield bonds, 46%; corporate bonds, 51%; structured products, 53%; Treasury Inflation Protected Securities, 63%. Of the 849 respondents who don’t own fixed income or don’t have any investment portfolio, 44% said they don’t buy bonds because they don’t understand the different types of securities.”

This is fascinating but not surprising. Since the financial media focuses only on headline-grabbing corporate news, the minute-by-minute price change of the markets, or what some investment guy with a product to sell you has to say, bonds don’t get much attention.

But, as BNY states, if you don’t understand what bonds are — and more importantly, what they can do for your portfolio — you may be missing out on something really big: And not just if you’re a retiree either.

Bonds can play a vital role for investors of any age because they reduce overall portfolio volatility. The less volatility a portfolio has, the less likely an investor will be to act emotionally during market declines and panic-sell investments to reduce losses.

Bonds also provide the third leg to the total return of a portfolio. Equities offer the first two legs, capital appreciation and dividends. Bonds offers stability by providing investors with both a safety-of-principal function (by returning the initial principal at maturity) and interest income.

Adding bonds to portfolios create better diversification and asset allocation for investors, which can lead to better returns over time, particularly during periods of increased volatility.

Is It The Right Time To Invest In Bonds?

Because interest rates are currently low, concerns about a recession in the U.S. economy have risen. This has led many media commentators to suggest the bonds are now wildly overvalued. For example:

“When evaluating the desirability of government bonds as a long-term investment, it’s imperative to compare the prevailing yields of bonds with the earnings yields for stocks.”

While this is a common comparison, it is also wrong.

Let’s compare the two:

Earnings Yield

“Earnings yield” is the inverse of P/E ratios and tells you only what the yield is currently, not what it will be in the future.

Investors do not “receive” an “earnings yield” from owning stocks. There is no “yield payment” paid out to shareholders; it is merely a mathematical calculation.

There is no protection of principal.

Treasury Yield

Investors receive a specific yield, calculable to the penny, which is paid to the holder.

Holders also have a government-guaranteed return of principal at maturity.

As we have written previously, it is essential to align expectations and investing requirements. Stocks have liquidity, and potential return (or loss), but no safety of principal. Treasuries have a stated return and a high degree of safety. However, to guarantee the stated return, Treasuries must be held to maturity and may not be liquid, if liquidity is part of your goal.

For most investors, completely discounting the advantage of owning bonds over the last 20 years has been a mistake. By reducing volatility and drawdowns, investors were better able to withstand the eventual storms that wiped out large chunks of capital.

Some may look at the graph below and see that bonds and stocks are at the same level. While this is true, bonds gave you the same amount of return as stocks with much less risk (and, needless to say, stress) during two major bear markets.

It is also worth pointing out that stocks are once again grossly overvalued, and a significant drawdown is probable in the coming years.

Over the next decade, the prospect of low stock market returns, possibly approaching zero, seems much less appealing than the positive return offered by risk-free asset.

Given that we are in the most extended bull market cycle in history, combined with high valuations and weakening fundamentals, it might be time to pay more attention to what bonds can offer you.

They could turn out to be one of the best-performing assets in your portfolio during the next cycle.

Tesla Picks Pockets Of Chinese Banks As It Borrows Another $1.4 Billion

Tesla, which supposedly has lots of cash in the bank and tons of working capital (just ask David Einhorn), is tapping a group of Chinese banks for a relatively small $1.4 billion USD, five year loan, for the company’s Shanghai plant. Part of the loan will be used to roll over an existing loan, according to Reuters.

Among the banks participating in the loan are China Construction Bank, Agricultural Bank of China, Industrial and Commercial Bank of China and Shanghai Pudong Development Bank.

Earlier this year the banks had offered Tesla an even smaller 12 month facility of 3.5 billion yuan (about $475 million USD) that comes due in March of 2020. The new loan will help Tesla roll over the previous debt and the rest will be used on Tesla’s “China operations”.

Tesla broke ground on its Shanghai plant in January and has started vehicle production. The factory is the cornerstone to Tesla’s ambitions of expanding globally and avoiding higher import tariffs imposed on U.S. made cars. The Shanghai government has been supportive of the project, for whatever reason, which marks China’s first wholly foreign owned car plant.

The new loan’s interest rate will be 90% of China’s one-year benchmark, the same as the 12 month facility. It’s an attractive interest rate and one that Chinese banks offer to “their best clients”. it was not immediately clear how or why Tesla qualified for this preferential rate.

As we approach the end of 2019, gold is on track for a healthy yearly gain. To date, the yellow metal is up over 16% on the year.

It’s always interesting talking about gains in the price of gold because when you get down to it, it all depends on when you got into the market. If you bought an ounce of gold on Jan. 1 of this year and sold it this morning, you’d have pocketed around $208 (less any taxes and fees). But if you bought your gold at the peak price this year and sold it this morning, you’d be out about $68.

So, when we say gold is up or down, you always have to ask a second question: since when? The price can be simultaneously up and down at the same moment depending on the answer to that question.

I occasionally get comments on articles posted on the SchiffGold Facebook page by people complaining that they’ve lost a lot of money in gold because they bought when the market was at its absolute peak in 2011 and the yellow metal nearly hit $1,900. I can certainly understand their frustration, but I don’t buy their argument that their experience proves gold is a bad investment. While eight years seems like a long time, it’s not in the big scheme of things.

As I said, where you begin when you talk about a trend is key. Plucking an arbitrary date out of thin air doesn’t necessarily tell us a whole lot. It’s important to begin at a key moment in history.

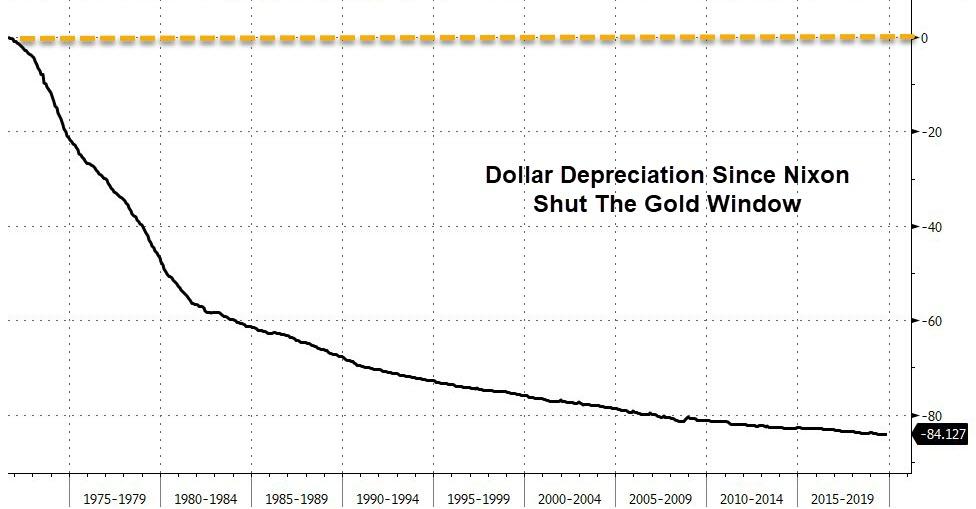

When it comes to gold, that key moment is August 15, 1971.

Source: Bloomberg

That’s the day that Richard Nixon slammed shut the gold window and eliminated the last vestige of the gold standard. From that date, the US — and the world — has been on a pure fiat money system. Governments have taken advantage of it by inflating the money supply relentlessly. As a result, the price of gold has skyrocketed from that moment.

What Exactly Happened in 1971?

Nixon ordered Treasury Secretary John Connally to uncouple gold from its fixed $35 price and suspended the ability of foreign banks to directly exchange dollars for gold. During a national television address, Nixon promised the action would be temporary in order to “defend the dollar against the speculators,” but this turned out to be a lie. The president’s move permanently and completely severed the dollar from gold and turned it into a pure fiat currency.

Nixon’s order was the end of a path off the gold standard that started during President Franklin D. Roosevelt’s administration. June 5, 1933, marked the beginning of a slow death of the dollar when Congress enacted a joint resolution erasing the right of creditors in the United States to demand payment in gold. The move was the culmination of other actions taken by Roosevelt that year.

In March 1933, the president prohibited banks from paying out or exporting gold, and in April of that same year, Roosevelt signed Executive Order 6102. It was touted as a measure to stop hoarding, but was, in reality, a massive confiscation scheme. The order required private citizens, partnerships, associations and corporations to turn in all but small amounts of gold to the Federal Reserve at an exchange rate of $20.67 per ounce. In 1934, the government’s fixed price for gold was increased to $35 per ounce. This effectively increased the value of gold on the Federal Reserve’s balance sheet by 69%.

The reason behind Roosevelt’s executive order and the congressional joint resolution was to remove constraints on inflating the money supply. The Federal Reserve Act required all Federal Reserve notes have 40% gold backing. But the Fed was low on gold and up against the limit. By increasing its gold stores through the confiscation of private gold holdings, and declaring a higher exchange rate, the Fed could circulate more notes.

While American citizens were legally prohibited from redeeming dollars for gold, foreign governments maintained that privilege. In the 1960s, the Federal Reserve initiated an inflationary monetary policy to help monetize massive government spending for the Vietnam War and Pres. Lyndon Johnson’s “Great Society.” With the dollar losing value due to these inflationary policies, foreign governments began to redeem dollars for gold.

This is exactly how a gold standard is supposed to work. It puts limits on the amount the money supply can grow and constrains the government’s ability to spend. If the government “prints” too much money, other countries will begin to redeem the devaluing currency for gold. This is what was happening in the 1960s. As gold flowed out of the US Treasury, concern grew that the country’s gold holdings could be completely depleted.

Instead of insisting on fiscal and monetary discipline, Nixon simply severed the dollar from its last ties to gold, allowing the central bank to inflate the money supply without restraint.

So What About Gold?

When he announced the closing of the gold window, Nixon said, “Let me lay to rest the bugaboo of what is called devaluation,” and promised, “your dollar will be worth just as much as it is today.”

This was also a lie.

According to the Consumer Price Index data released by the Bureau Labor of Statistics, the dollar has lost more than 80 percent of its value since Nixon’s fateful decision. Meanwhile, the dollar value of gold has gone from $35 an ounce to nearly $1,500.

Source: Bloomberg

Looking at it another way, the purchasing power of gold has increased dramatically since Nixon closed the gold window. When Nixon made his announcement, gold was official $35 an ounce, but the actual market price was around $45 per ounce. If you take the recent price which has been hovering between $1,450 and $1,500 per ounce, the price has increased by 3122%.

That is not a typo.

This is much greater than the dollar prices of goods and services. The GDP deflator index has increased roughly five-fold since 1971. So, not only has gold served as an inflation hedge since the dawn of the pure fiat money era, it has actually outpaced prices.

By every measure—including stagnating wages and rising costs—things have been going downhill for the American middle class since the early 1970s. August 15, 1971, to be exact. This is the date President Nixon killed the last remnants of the gold standard. Since then, the dollar has been a pure fiat currency. This allows the Fed to print as many dollars as it pleases. And—without the discipline imposed by some form of a gold standard—it does precisely that. The U.S money supply has exploded 2,106 percent higher since 1971. The rejection of sound money is the primary reason inflation has eaten up wage growth since the early 1970s—and the primary reason the cost of living has exploded.”

Practically speaking, this means that if you stashed an ounce of gold worth $35 alongside thirty-five one-dollar bills under your bed in 1971. Today, you would be sitting on gold that would buy you an expensive tailored suit. The $35 in cash wouldn’t get you a pack of fancy boxer shorts.

This is a trend worth considering, given that there is zero chance that the fiat monetary regime is going to end any time soon.

In what was not entirely surprising, Boeing CEO Dennis Muilenberg has “resigned” and will be replaced by current Chairman David Calhoun.

Boeing shares are currently halted…

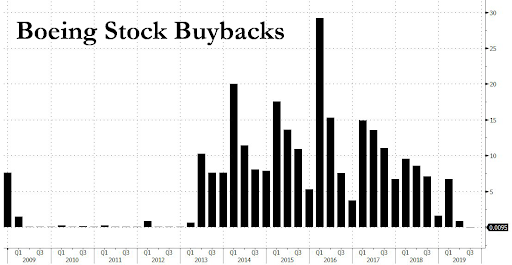

Over the 3-year period 2016 through 2018, Boeing employees received newly issued stock that’s worth $4.9 billion today. There was another $3.5 billion worth of stock issued to the Boeing pension plan, which was immediately sold into the open market.

Boeing announced today that its Board of Directors has named current Chairman, David L. Calhoun, as Chief Executive Officer and President, effective January 13, 2020. Mr. Calhoun will remain a member of the Board. In addition, Board member Lawrence W. Kellner will become non-executive Chairman of the Board effective immediately.

The Company also announced that Dennis A. Muilenburg has resigned from his positions as Chief Executive Officer and Board director effective immediately. Boeing Chief Financial Officer Greg Smith will serve as interim CEO during the brief transition period, while Mr. Calhoun exits his non-Boeing commitments.

The Board of Directors decided that a change in leadership was necessary to restore confidence in the Company moving forward as it works to repair relationships with regulators, customers, and all other stakeholders.

Under the Company’s new leadership, Boeing will operate with a renewed commitment to full transparency, including effective and proactive communication with the FAA, other global regulators and its customers.

“On behalf of the entire Board of Directors, I am pleased that Dave has agreed to lead Boeing at this critical juncture,” Mr. Kellner said. He added, “Dave has deep industry experience and a proven track record of strong leadership, and he recognizes the challenges we must confront. The Board and I look forward to working with him and the rest of the Boeing team to ensure that today marks a new way forward for our company.”

Mr. Calhoun said, “I strongly believe in the future of Boeing and the 737 MAX. I am honored to lead this great company and the 150,000 dedicated employees who are working hard to create the future of aviation.”

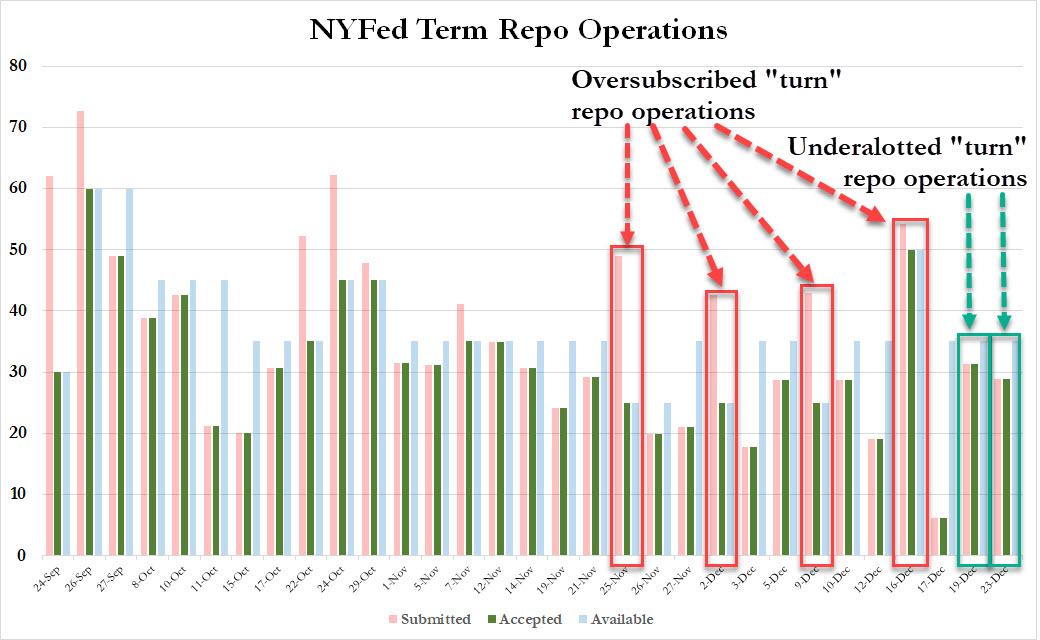

Repo Crisis Fades Away With Second “Undersubscribed” Turn Repo Even As Pozsar Doubles Down On Doomsday

It looks like the year-end repocalypse that was predicted by Credit Suisse strategist Zoltan Pozsar is not going to happen this year after all.

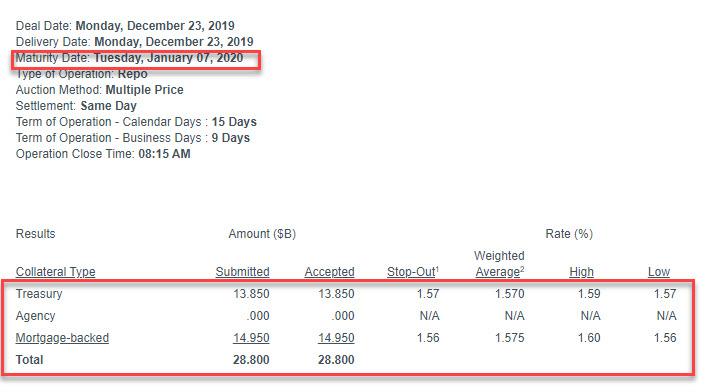

Today’s Term Repo which matures on January 7 saw $28.8BN in security submissions ($13.85BN in TSYs, $14.95BN in MBS), below the $35BN in total availability.

As such, this was the second term repo since the start of the Fed’s emergency repo program that covered the year-end “turn” with a maturity of Jan 2, and was not fully overalotted. As shown in the chart below, the first four “turn” term repos were all oversubscribed (boxed in red), while today’s was the second “turn” repo that saw a less than full allotment.

As such, it now appears that banks have reached their fill of what they believe will be sufficient year-end liquidity, and all subsequent “turn” repos will likely see a lower allotment as the Fed’s $500BN liquidity backstop bazooka ends up being underutilized, if not by much.

In his latest comment on the repo market, Curvature’s Scott Skyrm noted that “once the term RP operations switch to being undersubscribed, it either means most of the Street’s year-end funding need is fulfilled, or banks are close to their balance sheet limits.” His full comment below:

The Fed took out the bazooka last Thursday and proposed to flood the Repo market with liquidity. If needed. That’s the catch. The Primary Dealers might not take all of the cash the Fed is offering. Either they won’t need it or they won’t want it. So there are two scenarios as we get close to the end of the month. Either Primary Dealer banks do not take all of the Fed cash because their balance sheets are full or because they don’t need the cash. Wrightson estimates that only $300 billion to $350 billion* of the ~$500 billion will be taken by the Primary Dealers. We can see whether the Fed RP ops are oversubscribed or undersubscribed by watching the results. Back on November 25, the $25 billion term RP operation to January 6 was oversubscribed by $24 billion. The $50 billion operation to January 17 on Monday was only oversubscribed by $4.25 billion. Once the term RP operations switch to being undersubscribed, it either means most of the Street’s year-end funding need is fulfilled, or banks are close to their balance sheet limits.

This means that today’s repo is either good news, or bad news: good news if banks don’t need any additional liquidity for year end, but bad news if they are simply prevented from seeking more Fed reserves due to balance sheet limitations (and how many securities they can pledge), even as the overall funding in the repo market remains insufficient.

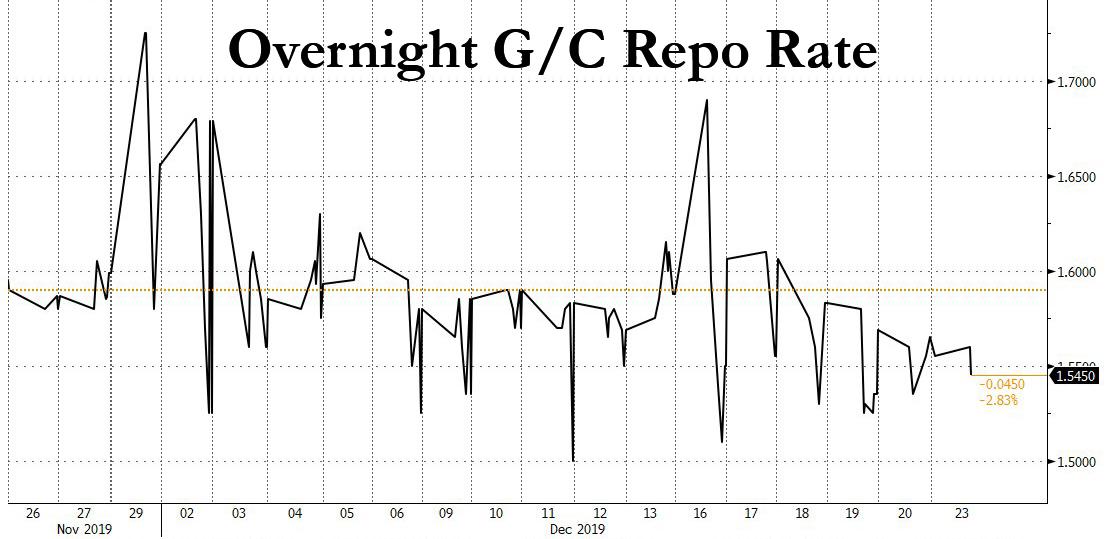

As usual, keep a track on the overnight repo rate for confirmation if things are getting better or worse. Incidentally, today the rate dropped 2bps to 1.545%…

… which suggests that all else equal, the tempest in the repo market – and the Fed’s expansion of QE4 as Pozsar predicted – may not happen after all.

Meanwhile, despite the lack of oversubscribed repo for two operations in a row, repo doomsayer Pozsar refuses to throw in the towel and in an interview posted by Bloomberg on Friday, the Credit Suisse analyst said “it’s not over” yet, saying that “if the yearend is less of a problem because of the repo bazooka we got from the Fed, and if the message of my report played a part in getting that bazooka, then that’s a nice way to be proven wrong.” However, he then added ominously that “now we’re getting into a point in the year when balance-sheet problems are going to flare up, and I think the system will get gummed up again.“

In other words, the world’s foremost repo expert expects more fireworks in the coming week.

He has two days in which to be proven right: there are two more term repos in 2019, one on Dec 26 and one on Dec 30. Absent some crisis on or around those days, it appears that the Fed managed to avoid the repo doomsday that Pozsar predicted two weeks ago.

Starr slams Pelosi: “There is an abuse of House power… It is wrong constitutionally.”

The judge who investigated Bill Clinton, leading to his impeachment after the Monica Lewinsky scandal, declared this past weekend that the Democrats’ impeachment of President Trump is ‘phony’.

Judge Ken Starr told Fox News that the process against Trump will be remembered in the history books with a “footnote” or an “asterisk.”

“There was a debate and there was a recorded vote. And that goes down in history. However… it’s an impeachment with a footnote or with an asterisk. By the way it never went over to the Senate, which I think means it’s a bit of a phony impeachment.” Starr noted.

Progressive law professor Noah Feldman says Trump may not actually be impeached yet, since Nancy Pelosi is holding the articles of impeachment. Ken Starr says meh… not so much. But Pelosi is committing “an abuse of House power.” And a quid pro quo? pic.twitter.com/pEdkuwH4Gg

When asked why Nancy Pelosi is delaying sending the articles of impeachment to the Senate, Starr replied “She appears to be intruding into the powers of the Senate which is ironic and extreme.”

“I think there is an abuse of House power in the way that this process unfolded in the House and riding roughshod over minority rights and ultimately the rights over the president.” Starr added.

“Now she is trying to essentially tell the Senate how to do its business: here’s the deal, Senator McConnell, leader McConnell — and it’s just wrong constitutionally. It’s not going to work. But it is wrong constitutionally.” Starr asserted.

Starr added that McConnell is doing the right thing in not going along with Democratic dirty tactics.

“He is doing it exactly the right way. I gather he’s going to say we are going to go forward with the business of the Senate and not play games.” Starr said.

Trump weighed in on the saga Sunday, suggesting that Democrats have realised they are driving off a cliff:

Crazy Nancy wants to dictate terms on the Impeachment Hoax to the Republican Majority Senate, but striped away all Due Process, no lawyers or witnesses, on the Democrat Majority House. The Dems just wish it would all end. Their case is dead, their poll numbers are horrendous!

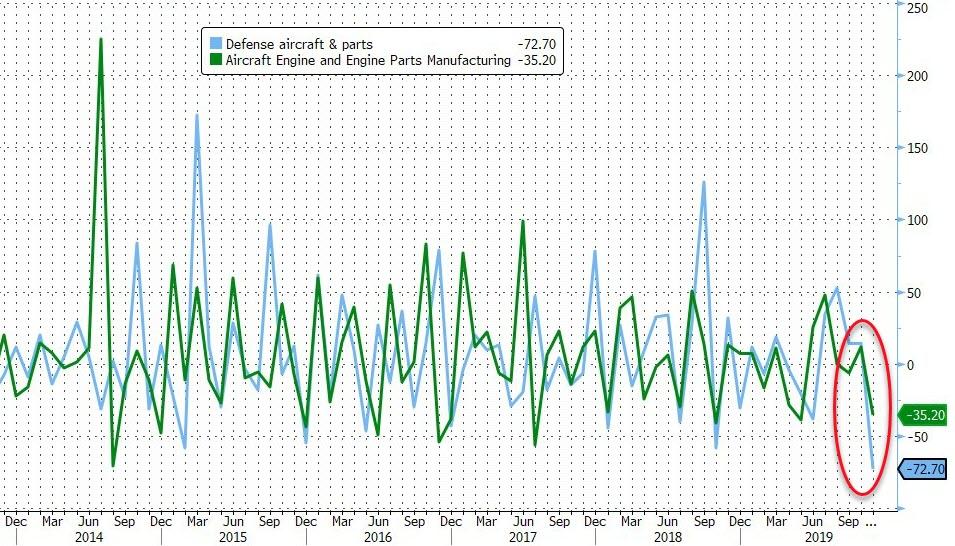

US Durables Goods Orders Unexpectedly Plunge In November As Boeing Backlash Hits

After a modest rebound in October (from September’s contraction), analysts expected a continued acceleration in durable goods orders in preliminary November data, but instead it collapsed!

Flash November Durable Goods Orders were expected to rise 1.5% MoM, but instead they tumbled 2.0% MoM, sending the year-over-year collapse to -5.7% – the worst since July 2016…

Source: Bloomberg

Core Durable goods orders (ex transports) were unchanged in November (worse than the 0.2% MoM expectation), indicating the headline drop was due to a slump in military aircraft and a drop in civilian planes.

The headline durable-goods figure was pressured by a decline in orders of commercial aircraft despite Boeing Co. reporting earlier this month that it received 63 orders in November compared with just 10 in October. Bookings for military hardware plunged 35.6%, the most since February 2017, while defense aircraft orders slid 72.7%.

Source: Bloomberg

The proxy for capex, Capital Goods orders ex-aircraft, spiked in October but slowed to just 0.1% MoM rise in early November data; and capital goods shipments ex-Air dropped 0.3% MoM (notably worse than the 0.0% expectation).

Combined with a decrease in core shipments, the figures highlight a lack of appetite for capital expenditures, with profit growth cooling and business sentiment still subdued amid global demand concerns.

“Right now, there’s no real inflation at play. But if we go further than we are currently, inflation is inevitably going to rise.” That’s from Alan Greenspan on CNBC this week. The “further” relates to US Federal deficit spending, the idea being that +$1 trillion annual budget shortfalls will eventually trigger price inflation.

It isn’t just Greenspan that is worried about rising US consumer price inflation; as we read through the most bearish market commentaries for 2020 this concern often has pride of place. Easy monetary and fiscal policy combined with a reaccelerating US/global economy late in a cycle is THE playbook for rising prices, so fair enough. The counterarguments are more structural (aging demographics, Internet price discovery, etc.), and while those work over the long term we can’t lean on them too hard in any given year. So do the inflation hawks have a case to make about 2020?

You know our methods for evaluating questions like this – a combination of market-based expectations and historical/real time data – so let’s get right to it:

Even during the period of Federal Reserve bond buying, TIPS spreads were reasonable proxies for market expectations about long-run future inflation. The lowest they ever got was 1.2% in early 2016 and they have often been +2.0% over the last decade, the Fed’s notional target (see chart below).

TIPS spreads were +2.0% for almost all of 2018, for example, only dropping in November along with US/global growth expectations.

Expected 10-year forward inflation as measured by the TIPS market hasn’t touched 2.0% in 2019 and currently sits at 1.73%.

Bottom line: after many years of holding out hope that US structural inflation could hold at 2.0%, TIPS spreads have thrown in the towel. The current TIPS spread of 1.73% is almost spot-on the 12 month average CPI of 1.82%. Even with the recently announced Phase 1 US-China trade deal and USMCA’s imminent passage, a late-year global equity rally, and a dovish Fed this market has resolutely refused to countenance the idea that US price inflation can make a comeback.

Here is the 10-year TIPS spread chart for the last decade:

Source: Bloomberg

#2: Core measures of inflation (PCE and CPI):

The Fed uses Personal Consumption Expenditures (PCE) data, while markets tend to look at the Consumer Price Index (CPI). Since 2000 core (ex-food and energy) PCE inflation has been lower than core CPI. We’ve included an explainer from the Cleveland Fed below if you want to learn more about why that’s the case.

The latest inflation readings for each: core PCE is at 1.6% as of October 2019 (latest data) but core CPI is higher at 2.3%.

Over the last 12 months core PCE has: 1) never hit 2.0% and 2) averaged 1.7%.

Over the last 12 months core CPI has: 1) always been 2.0% or greater and 2) averaged 2.2%.

Bottom line: inflation, like beauty, is in the eye of the index-focused beholder. By the Fed’s preferred measure (PCE) the US economy is still shy of their 2.0% inflation target. By the market’s primary metric (CPI), it is running slightly hot.

Since PCE is how the Fed makes policy, here is the 10-year chart for this measure’s core inflation rate for your review (and note how few times it breaches 2.0%):

Source: Bloomberg

#3: Owners’ Equivalent Rent (OER):

OER is how the BLS measures housing price inflation in the CPI calculation. It asks homeowners how much their house would rent for and tracks those responses over time.

OER is the single most important piece of core CPI, at 31% of the total. That makes it a more important contributor of measured inflation than any other single category by a wide margin.

OER inflation has not accelerated in over 4 years, trending consistently between 3.0% – 3.5% since mid 2015 (see chart below).

Bottom line: given that OER inflation shows no sign of acceleration (November’s 3.3% was the lowest since January’s 3.2%), this anchor in the CPI Index seems firmly set.

Here is the OER inflation chart:

Source: Bloomberg

Now, let’s wrap this up:

To believe in a 2020 inflation surge, one has to assume that the US economy is at a tipping point where marginal economic growth and/or fiscal and monetary stimulus has more of an effect on prices than any point in the last decade.

Bond markets do not see that happening. TIPS spreads say as much, and the Treasury market is among the most efficient in the world. In fact, this market is more worried about recession (witness the still paltry difference between 3 month and 10 year yields) and lower (not higher) price inflation.

Also worth noting: excluding the 1965-1970 experience when CPI inflation went from 1% to 6%, oil shocks are the proximate cause of every sudden ramp in core (ex-energy) consumer prices in the last 50 years. That was the case in 1974 (3% in 1973, 12% in 1975), 1979 (6% in 1978, 14% in 1980), and 1990 (4% in 1989, 6% at the start of 1991).

Our verdict: we simply cannot make a case for structurally higher inflation either in 2020 or the following several years. First, markets say it’s unlikely and investors already know about $1 trillion deficits, low unemployment, and positive catalysts like trade deals. Second, recent history (i.e. this year) exhibits little proof an inflection point is nigh. Lastly, the one thing that could shock the system into inflation – a sudden rise in oil prices – seems unlikely. That may not be a classic monetarist’s view of the world, but the data is clear enough.

Meltup Accelerates Into Christmas Break As Algos Run Wild In Illiquid Markets

After the decade’s last quad-witching came and went without any adverse incidents, and instead a massive short squeeze of the December Emini contract into its 930am Friday expiration repriced the entire market about 15 points higher…

… the relentless, QE4 inspired melt-up has only accelerated in today’s low volume session, as US equity futures pushed to fresh all time highs above 3,230…

… even as world stocks took a breather near record highs while currency and bond markets were little changed on Monday as trading volumes collapsed before the Christmas holiday.

On Friday, the S&P extended its record highs to seven straight sessions, its longest streak in more than two years, as all three major U.S. indexes – the S&P 500, Nasdaq and Dow – gained.

The MSCI ACWI index was flat, trading at Friday’s record high. It has risen nearly 3% this month as U.S.-China trade tensions eased and confidence grew that Britain would avoid a no deal exit from the European Union. The index is up 23% so far in 2019, set for its best year since 2009, with all of this upside thanks to multiple expansion as global earnings are down in 2019 compared to the prior year.

Trump did everything in his power to ensure a Monday spike after repeating – once again – on Saturday the United States and China would “very shortly” sign phase one a trade agreement, the same agreement he said in October would be signed in November. In response, China said on Monday it would lower tariffs on products ranging from frozen pork and avocado to some types of semiconductors next year.

“The Phase 1 (P1) agreement and UK elections have cleared up tail risks, but the market is now transcending that euphoria,” AxiTrader strategist Stephen Innes told Bloomberg. “While P1 is already reflected in stock prices, positioning is still relatively light, and with plenty of capital yet to be deployed, markets could even push significantly higher supported by the global growth rebound.”

The European Stoxx 600 index was flat, after starting off modestly lower before trading in positive territory. It hit a new record high in the Friday session.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan was near its highest since June 2018, up 0.05%, despite an unexpected hiccup in Chinese markets, where stocks posted their worst single-day drop in six weeks, weighed down by a correction in tech shares after a state fund announced plans to cut its stakes in some chip makers.

Asian shares were mixed with subdued volume ahead of the year-end holiday season. Health care stocks rose while material companies fell. The benchmark MSCI Asia Pacific Index was little changed, as gains in New Zealand stocks offset declines in China shares. The New Zealand Exchange 50 Gross Index jumped 0.6%, extending a new high on Monday, while China’s Shanghai Composite Index slumped 1.4% due to weak performance in financial shares. India’s S&P BSE Sensex Index dropped 0.3%. As we reported, on Monday the Chinese government said it will cut import tariffs for goods including frozen pork, pharmaceuticals, paper products and some high-tech components starting from Jan. 1, according to a statement from the Ministry of Finance.

As Bloomberg notes, all asset classes are on track for the best returns in a decade in 2019 after central banks around the world eased monetary policy.

“There is justification to say that the fundamentals are turning, but we haven’t seen confirmation in prices or data yet,” Kyle Rodda, an analyst at IG Markets Ltd., said on Bloomberg TV. “The risk is skewed to the upside, but I still think it’s a tentative picture at the moment.”

In FX markets, the euro was at $1.1083, up 0.05% after slipping 0.4% last week. Sterling tumbled again, sliding as low as 1,2930, a fresh 3 week low, extending its decline after seeing its worst week in more than two years. It remains on the back foot after U.K. Prime Minister Boris Johnson renewed hard-Brexit fears with an accelerated schedule for signing a trade deal with the European Union. It slid 2.6% last week for its worst weekly showing since October 2017. The safe-haven Japanese yen was down 0.08% at 109.35. And while the dollar was initially lower against most Group-of-10 peers in light holiday trading, it has since turned positive on the back of the pound’s latest mauling.

In commodities, Brent crude was down 23 cents to $65.95 a barrel. West Texas Intermediate crude slipped 24 cents to $60.2 a barrel, while gold rose to a 7 week high.

The U.S. personal consumption expenditure deflator for November, due on Friday, is the only major economic report this week.

Market Snapshot

S&P 500 futures little changed at 3,228.25

STOXX Europe 600 up 0.02% to 418.49

German 10Y yield fell 0.7 bps to -0.259%

Euro up 0.03% to $1.1082

Italian 10Y yield rose 2.4 bps to 1.237%

Spanish 10Y yield fell 0.7 bps to 0.436%

MXAP up 0.01% to 170.13

MXAPJ up 0.06% to 550.41

Nikkei up 0.02% to 23,821.11

Topix down 0.2% to 1,729.42

Hang Seng Index up 0.1% to 27,906.41

Shanghai Composite down 1.4% to 2,962.75

Sensex down 0.1% to 41,629.16

Australia S&P/ASX 200 down 0.5% to 6,785.14

Kospi down 0.02% to 2,203.71

Brent futures down 0.3% to $65.94/bbl

Gold spot up 0.4% to $1,484.27

U.S. Dollar Index little changed at 97.63

Top Overnight News from Bloomberg

China cut import tariffs on a wide range of goods including food, consumer items and parts for manufacturing smart-phones, continuing Beijing’s drive to lower trade barriers and spur domestic demand

Oil extended losses after the biggest decline in three weeks as Kuwait signaled a deal with Saudi Arabia to renew crude output along their border and as U.S. shale explorers increased drilling

One of Donald Trump’s top allies and his chief economic adversary are drifting closer, at least when it comes to trade

After money-laundering scandals involving hundreds of billions of euros rocked some of Europe’s biggest banks, the Baltic region has begun a fresh clampdown. This time, the target is payment-service providers

U.S. President Trump told Brazilian President Jair Bolsonaro he won’t reimpose tariffs on steel, aluminum from the Latin American nation, according to a person familiar

Satellite images show North Korea has added a structure to a factory linked to the production of intercontinental ballistic missiles, reports NBC News

Financial Times reports that traders at HSBC and JPMorgan Chase are among those who accessed a high-speed audio feed of Bank of England press conferences

Michel Barnier, European Commission chief negotiator for Brexit, says Britain must stick closely to Brussels’ standards on tax, state aid and environment to secure a trade deal with the bloc. Warns it will be “immensely challenging” to finish a deal by end of 2020 deadline, according to the Sunday Times

Asian equity markets traded somewhat mixed as the region once again failed to fully join in on the Christmas cheer which had propelled Wall Street to fresh record highs on Friday, with volumes light heading into the holidays. ASX 200 (-0.5%) and Nikkei 225 (+0.1%) were varied with Australia dragged by commodity-related losses and due to the adverse effects of its recent currency appreciation, while the Japanese benchmark remained afloat but with upside capped by an indecisive JPY and after Japanese Chief Cabinet Suga clarified that they have not eased export controls on South Korea. Hang Seng (+0.1%) and Shanghai Comp. (-1.4%) lacked conviction despite the announcement that China is to lower import tariffs for some products beginning January 1st and after the recent Trump-Xi call in which the leaders were said to have conducted a very good talk regarding the trade deal, although reports further noted that Chinese President Xi stated US interference is harming China’s interests and there were also downward revisions to November Chinese trade data including a wider contraction in Exports. Finally, 10yr JGBs languished firmly below the 152.00 level after the recent bear-flattening in USTs and with demand also dampened by the lack of BoJ presence in the market today.

Top Asian News

Warburg-Backed ESR Is Said to Mull REIT IPO of Korean Assets

SoftBank, Naver Hike Line Offer as Son Takes on Google, Amazon

Rescuers Sought for India Shadow Bank Altico as Crisis Deepens

India BJP Trails in State Poll Signaling More Woes for Modi

Tentative and mixed trade for European bourses in the final full session before Christmas [Euro Stoxx 50 -0.1%] following on from a similar APAC handover amid a lack of conviction and participants. In terms of YTD performance in Europe – FTSE MIB stands as the winner with YTD returns of just over 30% followed by the CAC 40 (+27.3%), DAX (+26.0%) and Euro Stoxx 50 (+25.7%) whilst IBEX 35 (+13.1%) and FTSE 100 (+12.8%) reside towards the bottom end of the spectrum. State-side, Nasdaq (+34.5%) leads the YTD gains followed by S&P 500 (+28.5%) and DJIA (+22.0%). Back to today’s session, FTSE 100 (+0.4%) outpaced peers as exporters benefit from a softer Sterling. Sectors also reflect an indecisive risk tone with no major standouts. In terms of individual movers: Bayer (+3.0%) rose to the top of the German index after the US government said the USD 25mln verdict on Co’s Roundup case should be reversed. Lufthansa (-1.3%) shares are pressured after talks with the German Union UFO fell through and strikes are imminent, albeit the union will refrain from strike action during the busy Christmas period. Meanwhile, GSK (-0.4%) drifted off lows but remains subdued after the US FDA declined to approve Co’s long acting HIV injections after the regulator questioned the treatment’s chemistry, manufacturing and controls process but not its safety. Finally, NMC Health (+28.5%) spiked higher at the open, and have continued to strengthen, after the Co. stated it will be commencing an independent third-party review to provide additional reassurances to shareholders after activist short-seller Muddy Waters questioned the integrity of NMC’s reports. Note: tomorrows session sees Eurex and all its derivatives closer whilst cash DAX will be shut all day – the rest of the cash bourses will see an early finish.

Top European News

Consilium Soars More than 200% on Unit Sale to Nordic Capital

Germany Expects Gas Pipeline Delay Before Completion in 2020

Neste Jumps on Reinstatement of U.S. Blender’s Tax Credit

Benettons’ Atlantia to Confront Italy Government on Road Reform

In FX, AUD/NZD – The Aussie and Kiwi are still outpacing their G10 rivals and jostling for top spot in the major stakes having made firmer breaches of big figures against their US counterpart, with Aud/Usd up to 0.6920 and Nzd/Usd reaching 0.6625. Both have benefited from a mixture of short covering and technical buying after recent relatively upbeat data that has reduced or rolled back RBA/RBNZ rate cut expectations. In terms of next bullish chart targets, 0.6939 looms as long as the pair holds/closes above the 200 DMA (circa 0.6905) and 0.6636 respectively.

CHF/GBP – The Franc is in bronze position and eyeing 0.9800 vs the Buck as latest weekly Swiss sight deposits suggest less active currency intervention and the Greenback drifts down from best levels generally (DXY dipping within a narrow 97.708-578 range) amidst even thinner seasonal volumes and a softer/flatter Treasury yield curve. Similarly, Sterling is trying to take advantage of the Dollar’s dip and attempting to keep hold or sight of the 1.3000 level even though no deal Brexit risks have risen with the passing of the 1st parliament vote on PM Johnson’s WAB that includes a no transition delay clause.

EUR//JPY/CAD – All more narrowly mixed against the Usd, with the single currency mired between 1.1074-88 parameters, Yen meandering from 109.35-53 and Loonie pivoting 1.3150 ahead of Canadian GDP for the month of October that is forecast to be flat, but could disappoint given a string of bleak data since this month’s BoC meeting. Back to Eur/Usd, some option expiry interest could impact in the absence of anything else and the aforementioned quiet pre-Xmas trade, as almost 1 bn rolls off at 1.1070 and from 1.1100-10.

SCANDI/EM – The Swedish Crown has slipped after another test of resistance near 10.4150 against the Euro failed to propel the Sek higher, but its Norwegian peer is extending gains through 10.0000 towards 9.9150 on the back of the Norges Bank’s gently inclined depo rate path. Elsewhere, EMs are largely going through the motions in tight bands vs the Dollar.

In commodities, the energy complex remains flat/subdued amid holiday-thinned conditions after a lacklustre Asia session in light of a number of bearish supply-side factors including Friday’s increase in active rigs reported via the Baker Hughes rig count coupled with reports of a Saudi-Kuwaiti agreement to renew oil output in the shared neutral zone by year-end. WTI futures hover just above the USD 60/bbl mark whilst its Brent counterpart retains USD 66/bbl+ status at time of writing. Russian Energy Minister Novak failed to provide the complex with much impetus in early EU trade despite noting that the OPEC+ could discuss deeper oil output cut quotas at its March meeting (5th/6th) in 2020. This follows this month’s policy revision in which the cartel agreed to deeper cuts of 496k BPD starting from Q1 2020, with an extraordinary meeting in March for a review. Elsewhere, gold trades on a firmer footing with the yellow metal hovering around current session highs of ~USD 1485/oz ahead of reported trend-line resistance at ~USD 1487/oz. Copper also garnered some support from the initially softer Dollar with prices re-eying USD 2.80/lb to the upside, although the red metal’s 100 WMA rests just below the round figure at USD 2.7988/lb. Finally, Dalian iron ore rose in excess of 1.0% after key steelmaking cities in Northern China issued pollution alerts as air quality in the region deteriorates.

UIS Event Calendar

8:30am: Durable Goods Orders, est. 1.5%, prior 0.5%; Durables Ex Transportation, est. 0.2%, prior 0.5%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.2%, prior 1.1%; Cap Goods Ship Nondef Ex Air, est. 0.0%, prior 0.8%

8:30am: Chicago Fed Nat Activity Index, est. -0.3, prior -0.7

10am: New Home Sales, est. 730,000, prior 733,000; New Home Sales MoM, est. -0.41%, prior -0.7%