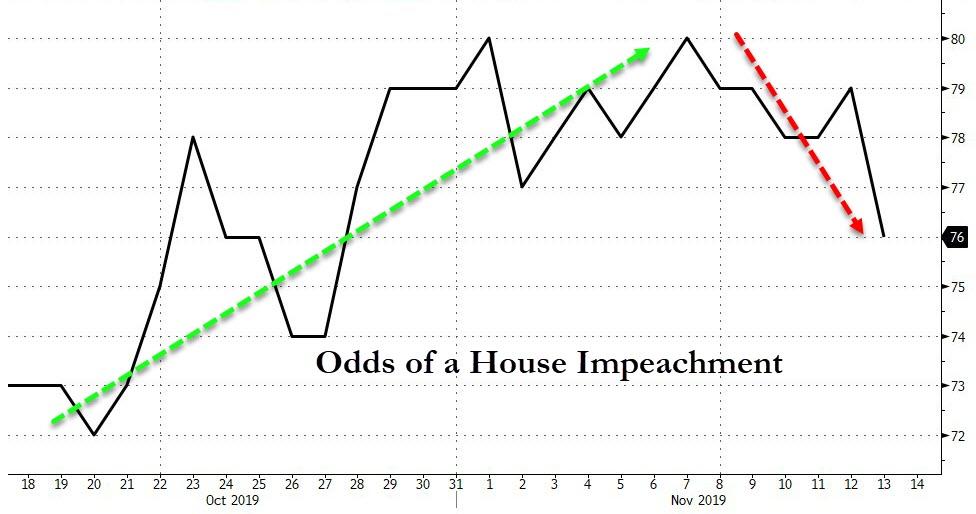

“We Sail For Europe!” – Environmental Savior Greta Thunberg Sets Sail For Madrid Surrounded By Youtubing Disciples

Greta Thunberg is a lot of things: teenager, climate activist, social media darling. And soon she might add ‘YouTube creator’ to her resume.

Thanks to Chile’s decision to cancel a United Nations climate gathering scheduled for December, Greta Thunberg, who has apparently been living in the US since arriving in September on a carbon-neutral vessel, unable to fly home because it would betray her principles.

Since simply flying coach apparently isn’t an option, Thunberg put the word out on social media that she was looking for somebody to sail with her to Madrid, where the December UN conference is now being held because of the riots in Chile. And who should answer her call but a couple of YouTube-famous Australians who live aboard their low-carbon catamaran, “La Vagabonde”.

Riley Whitelum and Elayna Carausu are their names. And during their four-week journey – a journey that will only barely get them there in time for Greta to catch the end of the conference – we suspect that the couple and Greta will extensively document their journey via social media and YouTube, as they’ve been doing.

So happy to say I’ll hopefully make it to COP25 in Madrid.

I’ve been offered a ride from Virginia on the 48ft catamaran La Vagabonde. Australians @Sailing_LaVaga ,Elayna Carausu & @_NikkiHenderson from England will take me across the Atlantic.

We sail for Europe tomorrow morning! pic.twitter.com/qJcgREe332

According to the Verge, the 40-foot catamaran in which they will be traveling is equipped with solar panels, a wind turbine, and hydro-generators, ensuring a “low carbon” journey.

Greta is clearly having a great time playing sailor.

Of course, by sailing across the Atlantic, one could argue that Greta is putting herself and others at risk. November isn’t the ideal month to sail across the North Atlantic. Hurricane season in the Atlantic runs from June to November.

Meanwhile, Thunberg is inviting her fans to follow her travels online.

Thunberg first became a sensation last year when she became the figurehead of the global school climate strike movement, where she encouraged kids to leave school en masse and take to the streets to demand their leaders do more to address climate change. She’s now apparently dedicating herself to traveling to every official ‘climate summit’ in search of a microphone to warn about the planet’s impending doom, and how it’s all the boomers’ fault.

In order for society to function properly, we need to be able to assume that most people are going to behave rationally. And when I was growing up, it was generally safe to make that assumption. But now things have completely changed. No matter how hard one may try, there is simply no avoiding the hordes of crazy people that seem to be taking over our society. It is almost as if millions of us never learned the basic rules for how civilized people should treat one another. Sometimes this manifests in behavior that is simply rude, other times it manifests in behavior that is actually dangerous, and if you are really unlucky you will personally encounter someone that has fully embraced depravity on a level that most of us never even want to think about.

Let me give you an example of crazy behavior that is simply rude. Not too long ago, a Reddit user posted a photograph that really freaked a lot of people out…

A female plane passenger took to Reddit this week to share a horrifying photo of a stranger performing a rude act during her flight.

The woman, who goes by WoodySoprano on the social media platform, posted an image of a traveler resting their bare feet on her headrest. Though the Reddit user’s face is cropped, her terrified eyes tell all.

“Going to be a long flight,” she captioned the photo.

This woman was never in any physical danger, but this type of behavior is incredibly rude.

Who would do something like that?

Of course sometimes crazy behavior does cross the line and actually becomes dangerous. For example, just consider what recently happened to one woman in Los Angeles…

Heidi Van Tassel was parked in Hollywood after having a pleasant evening out with friends at an authentic Thai restaurant. Suddenly a man randomly pulled her out of the car, dragged her out to the middle of the street, and dumped a bucket of feces on her head, Van Tassel said and public records confirm.

“It was diarrhea. Hot liquid. I was soaked, and it was coming off my eyelashes and into my eyes,” Van Tassel said. “Paramedics who came to treat me said there was so much of it on me, that it looked like the man was saving it up for a month.”

Nobody in their right mind would dump a bucket of warm diarrhea on some random woman.

But if you visit the major cities on the west coast, something like this could actually happen to you. In San Francisco alone, there have been more than 132,000 official complaints about human feces in the streets since 2008.

We have literally become a nation where hordes of people use the streets as a toilet.

What in the world has happened to us?

And if you are brave enough to go get something to eat at a local fast food restaurant, there is a chance that you might be viciously attacked by a complete nutjob…

A woman has been sentenced to seven years in prison for slashing a man’s throat in front of his family at a Taco Bell after he asked her to stop ranting at employees for taking too long on her food.

The victim, 48-year-old Jason Luczkow, told The Oregonian Thursday that he and his wife went to a Taco Bell along Highway 26 in July to pick up some food for the family when the errand took a horrifying turn, which was miraculously caught on video.

Have you noticed that people seem to get “triggered” a whole lot more easily than they once did?

These days, saying the wrong thing to one of these crazy people at the wrong time can result in violence very quickly…

A Twitter user received over 126,000 ‘likes’ after she bragged about stealing a “homophobic” white woman’s purse and spending her money on tacos.

Yes, really.

“A white woman spawned out of nowhere today and started being homophobic to me so I stole her purse and now miss thing’s ID is resting in a target trashcan and her money is paying for my tacos and rent,” tweeted a user called @yourholygaymom, who describes herself as “the high priestess of gay twitter.”

The most frightening thing about that story is the fact that more than 126,000 people decided to hit the like button.

Like I said, the crazy people are literally taking over our society.

Those of us that try to behave rationally still depend on the police to protect us, but the crazies are going after them too…

Video posted by CBS shows people deliberately covering an NYPD vehicle in trash on Halloween night, while a small group of residents sit by, laugh, and taunt the two officers that were left to clean up the mess.

One resident is heard saying “trick or treat”, followed by a slur.

The officers calmly show restraint as they are left to clean up trash filled boxes, broken eggs and rotting food. The officers were in the midst of responding to a domestic dispute call and were upstairs at a residence long enough for their vehicle to be vandalized.

It certainly isn’t easy to be a police officer these days.

If those officers had lashed out against the residents that vandalized their vehicle, they would have probably been demonized by the mainstream media for committing “police brutality”.

And as I mentioned above, once in a while you run into a crazy person that has completely embraced depravity.

Today, the average American spends more than three and a half hours watching television each day, and the material on our televisions is becoming increasingly depraved…

A new study has a message for the many families who have said television content has grown coarser with each passing year: You’re right.

The study by the watchdog group Parents Television Council found a 28 percent increase in violence and a 44 percent increase in profanity over the past decade in shows rated TV-PG. It’s part of what the PTC calls “content creep” – that is, an increase in offensive content within a given rating compared to similarly rated programs a decade ago.

Unfortunately, the trends that are causing all of this crazy behavior in our society are likely to continue to intensify in the years ahead.

The thin veneer of civilization that we all rely on every day is steadily disappearing, and that means that things are going to become increasingly difficult for those of us that are still trying to behave rationally.

Google Slides After Antitrust Probe Expands Into Search And Android Businesses

Google shares are sliding into late session after a CNBC report states 50 attorney generals are expanding their investigation into the technology company’s search and Android businesses:

50 ATTORNEYS GENERAL PROBING GOOGLE PREPARING TO EXPAND ANTITRUST PROBE BEYOND CO’S ADVERTISING BUSINESS – CNBC

50 ATTORNEYS GENERAL INVESTIGATING GOOGLE PREPARING TO EXPAND ANTITRUST PROBE TO DIVE MORE DEEPLY INTO CO’S SEARCH & ANDROID BUSINESSES- CNBC

The investigation is being led by Texas Attorney General Ken Paxton, who has recently focused on investigating Google’s advertising business.

Several attorney generals in a recent meeting made the decision to expand the investigation into Google’s search and Android businesses, the sources said.

Google shares still ended higher on the day.

Investors clearly think Google is too-big-to-care.

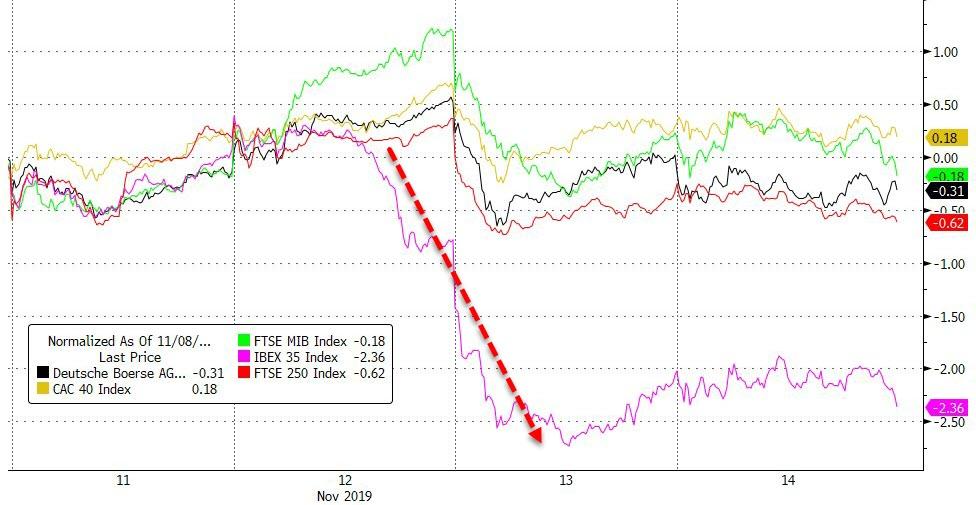

“The other thing that’s helped the bull is how poorly the rest of the world’s done. It sort of kept everyone here. If they are going to buy anything at all, they’d buy U.S.” Jim Paulsen, chief investment strategist at The Leuthold Group, told CNBC.

So why is the American consumer losing faith?

Source: Bloomberg

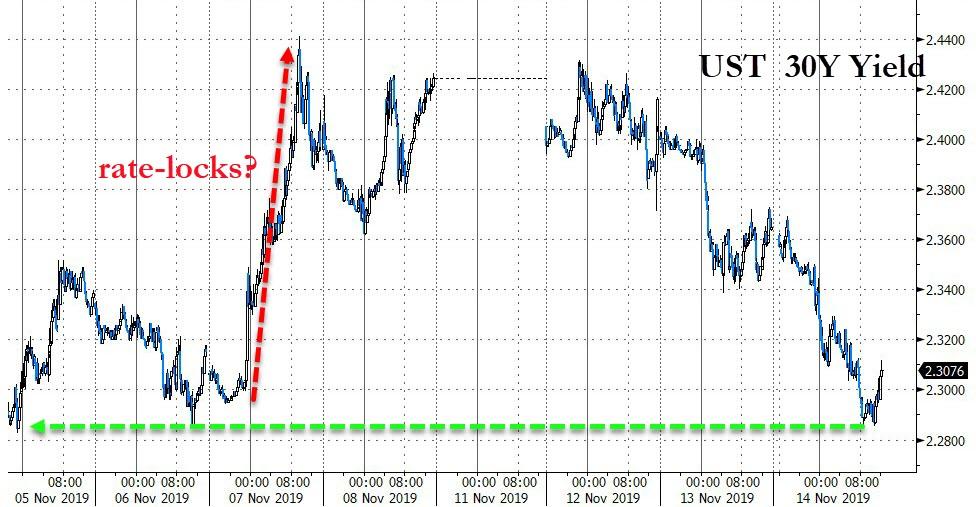

FEDSPEAK-FEST today – all singing from same songsheet – “We’re on hold unless world collapses”…

0900ET Clarida NEUTRAL – US Economy “at or close to” Fed’s goals

0910ET Evans – Cryptocurrency could cause “the business models of commercial banks to come under significant pressure”

1000ET Powell NEUTRAL – US is “star economy”, repeats baseline economic outlook remains favorable, policy is appropriate

1145ET Daly NEUTRAL – Monetary policy in good place given healthy momentum in the economy and consumer spending

1200ET Williams NEUTRAL – US economy and policy in good place, backs keeping rates steady

1220ET Bullard DOVISH – Positive yield curve is bullish for 2020, economy still faces downside risk

1300ET Kaplan NEUTRAL – US consumer in good shape, labor market tight, policy appropriate

Additional market movers were

1100ET Pelosi – USMCA by year-end, sent CAD higher, USD lower

1400ET U.S., CHINA STRUGGLE TO CLOSE PHASE-1 DEAL, FT SAYS

Disney’s new streaming service includes trigger warnings on old movies that caution the viewer about “outdated cultural depictions.”

The launch of the new Disney+ service in the United States made available many classic films, but they could not be presented without the need to genuflect to political correctness.

Movies including Dumbo, Lady and the Tramp, The Aristocats, Peter Pan and The Jungle Book all feature the trigger warning in their plot descriptions due to negative racial stereotypes like the Siamese cats in Lady and the Tramp, the Native American characters in Peter Pan, and the crows in Dumbo.

“This program is presented as originally created. It may contain outdated cultural depictions,” reads the disclaimer.

Movies deemed too controversial due to their stereotypical depictions of non-white people, such as the 1946 film Song of the South, are not included as part of the Disney+ service.

There is a constantly increasing number of movies and songs that are being forgotten or done over in order to conform to the ever changing social mores of progressivism.

John Legend and Kelly Clarkson recently released a re-recorded version of Baby, It’s Cold Outside, completely changing some of the supposedly “misogynistic” lyrics.

The song was a total flop, receiving almost twice the number of thumbs down than thumbs up on YouTube.

Get woke, go broke.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

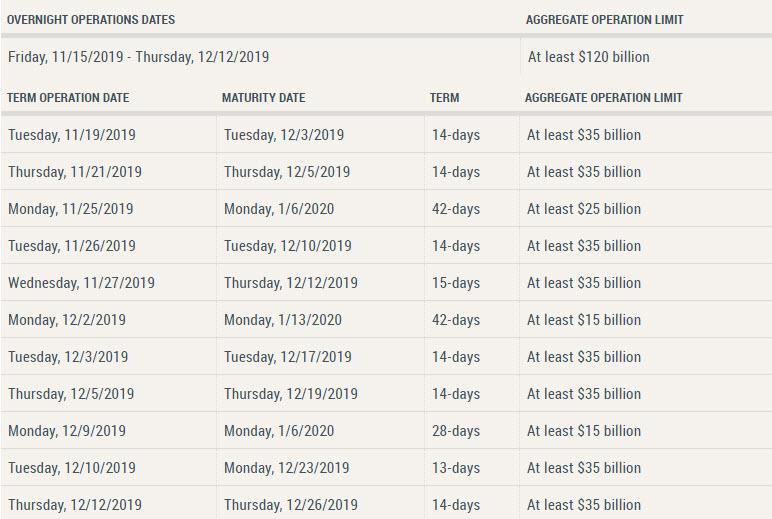

Fed Braces For Year End Repo Turmoil: Announces $55 Billion In 28, 42-Day Repos To Flood System With Cash

Just moments after we reported that according to Bank of America, the US financial system’s reliance on repos could “short-circuit the market’s ability to accurately price the supply and demand for leverage as asset prices rise”, and implicitly, facilitate the next financial crisis because “the Fed has entered unchartered territory of monetary policy that may stretch beyond its dual mandate”, the Fed confirmed just how reliant both it, and the entire US financial system is on the repo market, when it released its latest term repo schedule, one which for the first time included 28 and 42-day repos which would mature into the new, 2020 year, yet which amount to just a total of $55 billion collectively, an amount which we fear will be far too little to meet year-end liquidity demands, and represents just the first shot in the Fed’s scramble to flood the system with year-end liquidity. Meanwhile, the NY Fed is maintaining its $120BN in overnight repos indefinitely.

The Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York has released the schedule of repurchase agreement (repo) operations for the monthly period from November 15, 2019 through December 12, 2019. In accordance with the most recent FOMC directive, the Desk will continue to offer at least $35 billion in two-week term repo operations twice per week and at least $120 billion in daily overnight repo operations.

The Desk will also offer three additional term repo operations during this calendar period with longer maturities that extend past the end of 2019. These additional operations are intended to help offset the reserve effects of sharp increases in non-reserve liabilities later this year and ensure that the supply of reserves remains ample during the period through year end. They are also intended to mitigate the risk of money market pressures that could adversely affect policy implementation. The Desk will adjust the timing and amounts of repo operations as necessary to maintain an ample supply of reserve balances over time and based on money market conditions, consistent with the directive from the FOMC.

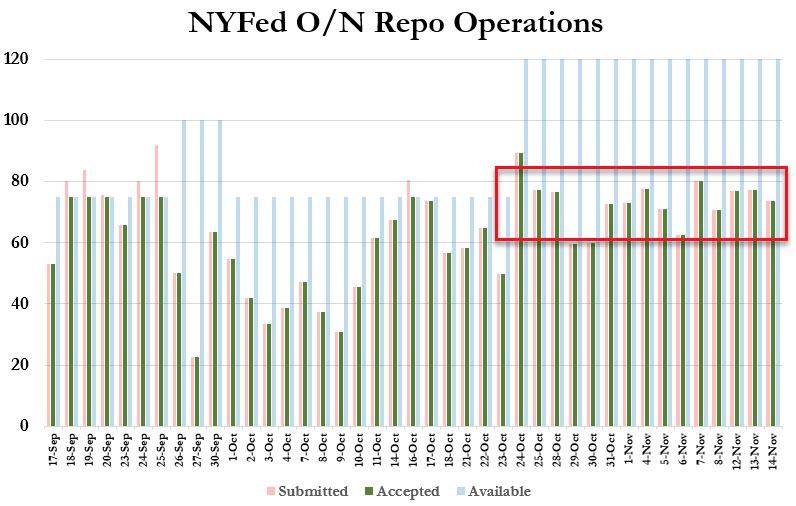

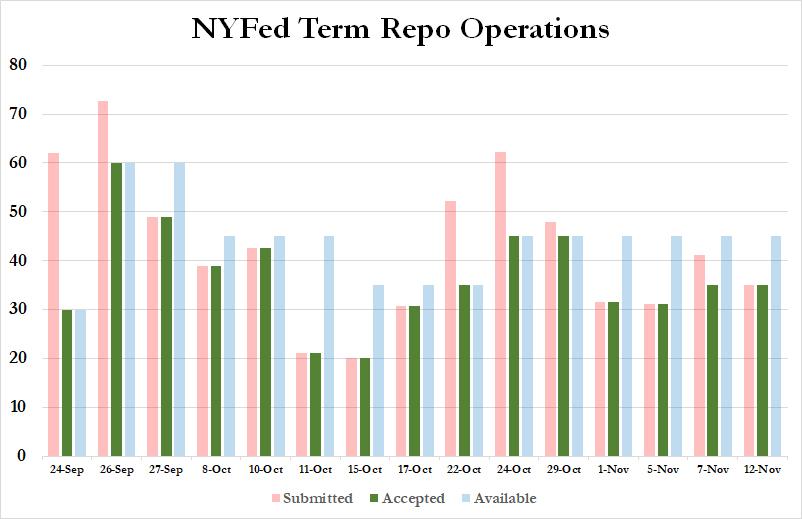

Indicatively, this is just how “temporary” the Fed’s overnight repos…

… and term repos have become:

Appropriately, the Fed admitted that it is starting to freak out about year-end liquidity just minutes after we published a scathing critique of the Fed’s “repo regime” by BofA, which among other things said the following:

Repo matters more than ever

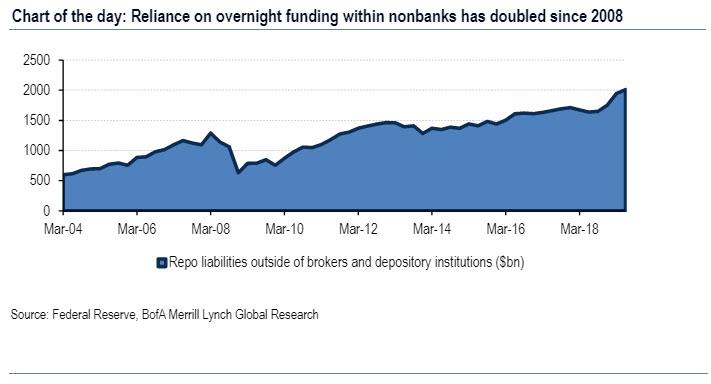

The repo channel, which is one ingredient within overall financial conditions, is becoming more important as reliance on overnight funding and leverage continues to rise. While banks and security brokers have greatly reduced reliance on overnight funding as a result of Dodd-Frank, the rest of the market has approximately doubled its reliance on overnight funding since the 2008 crisis.

While one can argue that the proper metric is repo funding as a percentage of Treasuries and MBS outstanding, we think that such a ratio misses the bigger picture. The bigger picture is that if repo markets stopped functioning today, the amount of Treasury and MBS securities held outside of banks-dealers requiring liquidation (for lack of funding) would be about twice as large as 2008, and with today’s surprisingly low levels of liquidity in the “liquid markets” the impact could be massive. In this context, we view the Fed’s purchase program as integral to the promotion of easy financial conditions and supportive of asset prices, which is Chair Powell’s second criterion for QE.

Why is the above a problem? Because as BofA concluded, “Everything has a cost”

In our view, the most worrying part of the Fed’s current asset purchase program is the realization that an ongoing bank footprint in repo markets is required to maintain control of policy rates in the new floor system. While we are confident that beyond year-end, the additional reserves will have the required soothing effect, what is less clear is that the Fed can make sure the bank repo lending footprint is resilient to dips in the bank credit cycle. While repo is fully collateralized and therefore contains negligible counterparty credit risk, there may be a situation in which banks want to deleverage quickly, for example during a money run or a liquidation in some market caused by a sudden reassessment of value as in 2008. In this environment, it seems implausible to expect banks to maintain their level of repo lending. If repo lines were drawn down far enough and for long enough in time, it could lead to deleveraging at institutions that were otherwise healthy. The new monetary policy regime therefore may increase systemic financial risk by making repo markets more vulnerable to bank cycles. This increases interconnectedness, which is something regulators widely recognize as making asset bubbles and entity failures more dangerous.

Some have argued, including former NY Fed President William Dudley, that the last financial crisis was in part fueled by the Fed’s reluctance to tighten financial conditions as housing markets showed early signs of froth. It seems the Fed’s abundant-reserve regime may carry a new set of risks by supporting increased interconnectedness and overly easy policy (expanding balance sheet during an economic expansion) to maintain funding conditions that may short-circuit the market’s ability to accurately price the supply and demand for leverage as asset prices rise.

When the time comes for the Fed to unwind its “temporary” repos, we hope it will be more successful then when it tried to “renormalize” monetary policy, which lasted for a few months and then the Fed admitted defeat in a dramatic U-turn, and is now cutting rates instead.

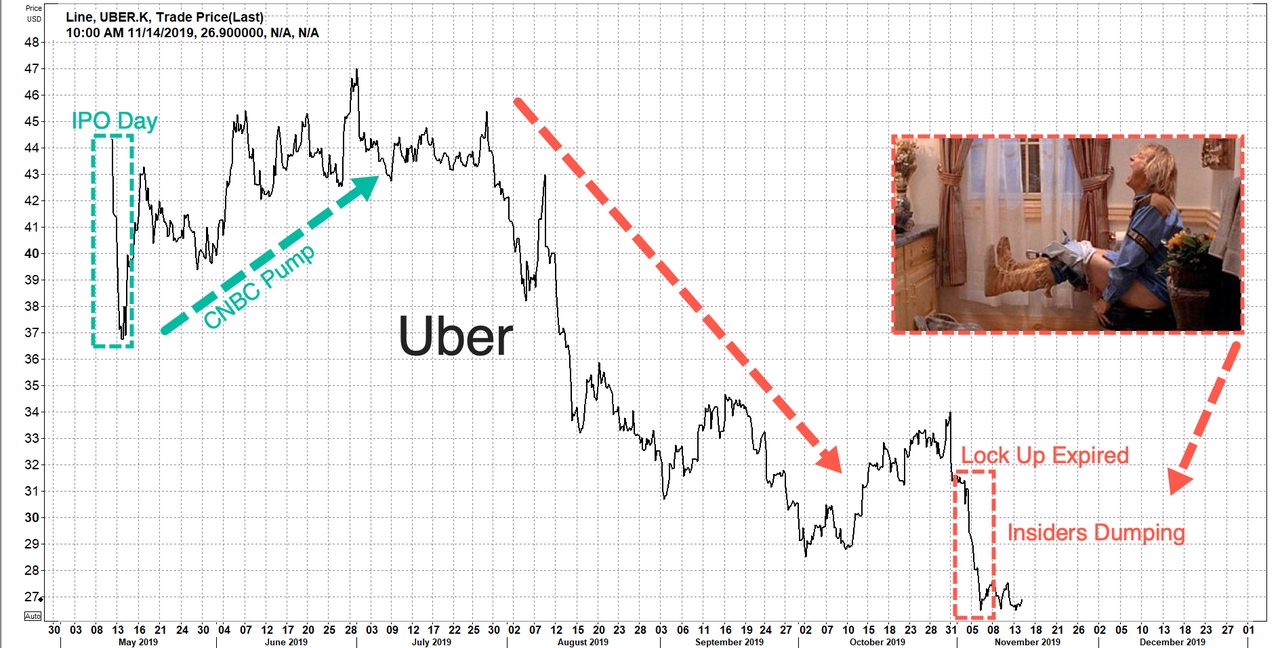

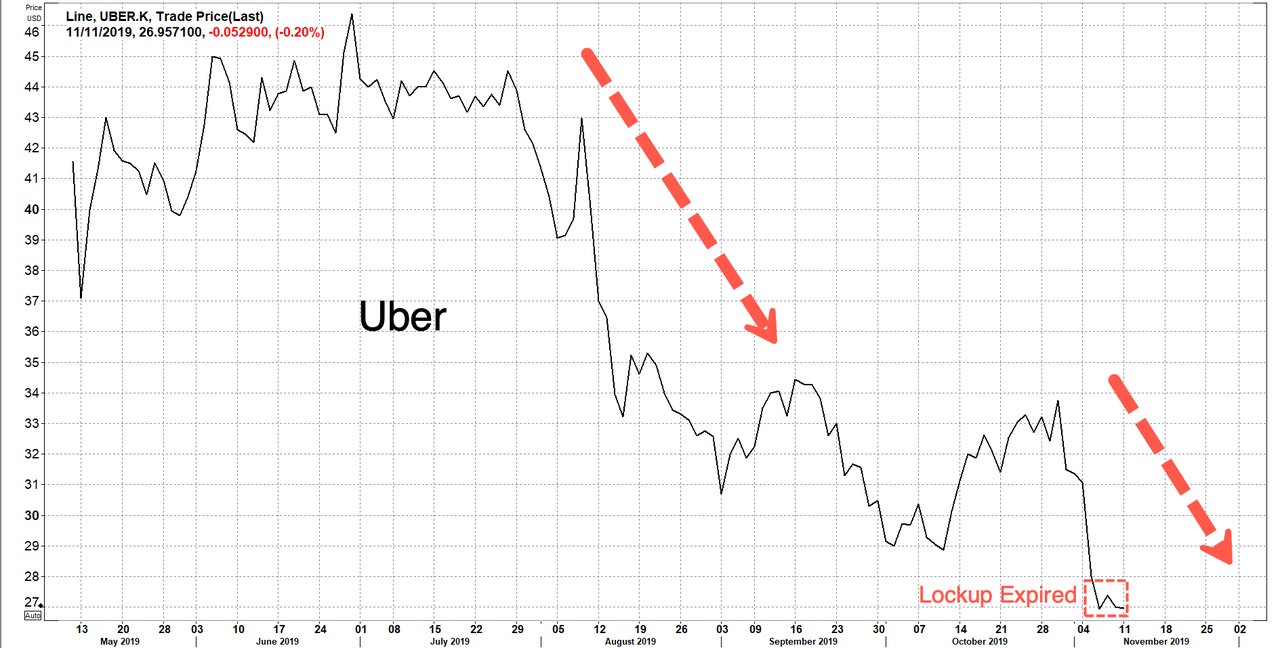

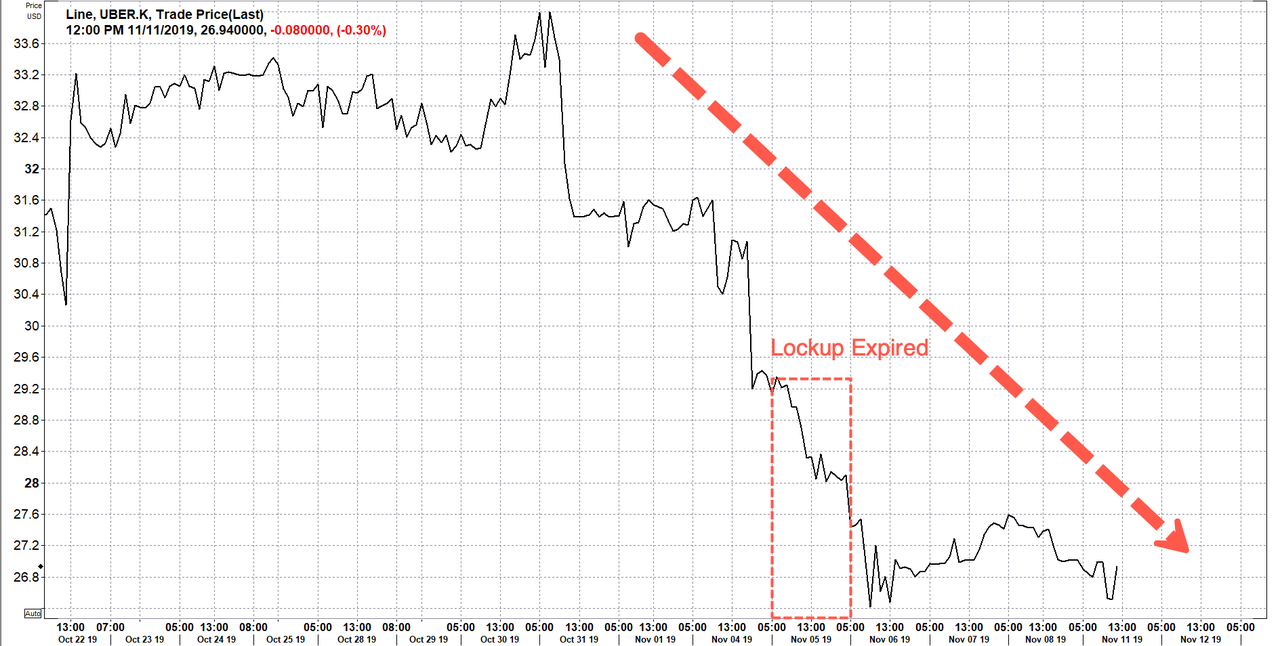

Travis Kalanick Is Dumping Even More Of His Uber Stake After Lockup

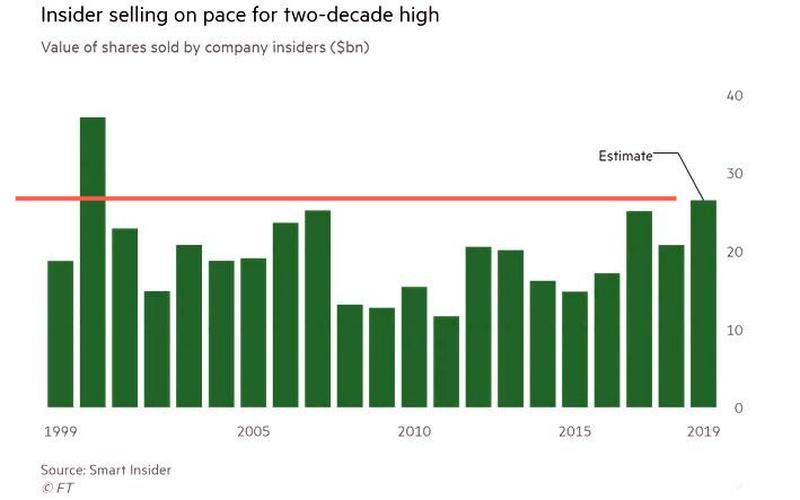

Update (Nov. 14): Earlier this week, we reported that Wall Street insiders are dumping stock at a record pace as the bull market in equities could be nearing an end.

We also said Travis Kalanick, Uber’s ousted co-founder, sold 20.3 million shares worth $547 million last week. Now a new filing shows Kalanick continues to dump stock this week.

The filing shows Kalanick dumped another $164 million of his Uber holdings, bringing the total amount sold since the 180-day lockup expiration on Nov. 6 to $711 million.

Kalanick still serves on Uber’s board and continues to maintain a 4.2% stake worth $1.9 billion. He’ll likely continue dumping shares as the company loses billions of dollars and records the slowest-ever revenue growth.

Investors fear that the money-losing technology company could face severe financial headwinds ahead of the next recession, which is why Kalanick isn’t sticking around and dumping his shares as fast as possible.

In the last 20 weeks, shares have plunged 42% as investors see no turnaround in the ride-hailing company.

* * *

As we detailed previously, Travis Kalanick, Uber’s ousted co-founder, has followed down the path of every other Wall Street insider this year: dump stock amid concerns the longest bull market in equities could be nearing an end.

Insiders are dumping stock at the fastest pace in two decades. Bloomberg reports Kalanick sold 20.3 million shares worth $547 million last week, according to a Friday filing.

Uber’s 180-day lockup period restricting insiders and pre-IPO investors from selling expired last Wednesday.

Uber shares in the last five months have plunged 43% to the 26-handle.

Shares have dropped 22% over the previous seven days ahead of the expiration, which underlines how investors steer cleared of the stock ahead of insider dumping.

Kalanick still serves on Uber’s board; he owns 78 million shares, or about a 4.6% stake, worth $3.5 billion.

Kalanick disposed of stock through a Rule 10b5-1 plan, which allows him to sell a certain amount of shares within a pre-determined timeframe to avoid controversy.

Across all of Wall Street, insiders dumped $19 billion of stock in their companies through mid-September. Annualized, this puts insiders on track to hit $26 billion for the year, would be the highest dollar amount on insiders dumping since right before the Dot Com bust in 2000.

Kalanick is dumping stock like every other insider on Wall Street. What do they know?

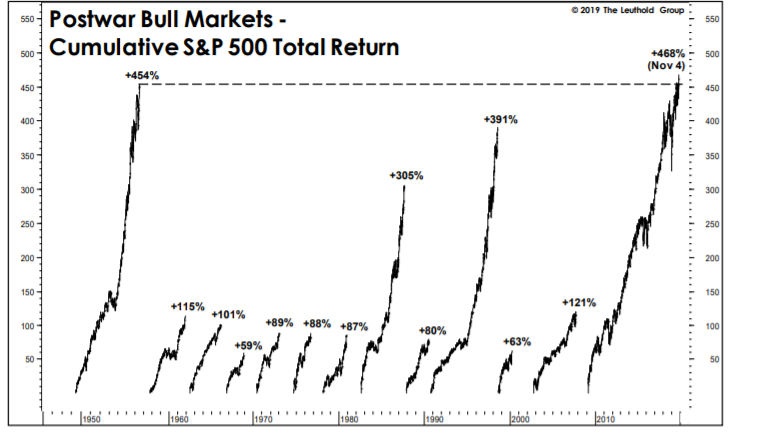

We’ve outlined pretty much the entire bull case for US/global stocks over the last few days. It comes down to:

Easing of US-China trade tensions going into an American election year.

The resultant rebound from lackluster corporate earnings growth this year, led by increasing business confidence and investment.

Global central banks remaining more inclined to stimulate than constrain their local economies.

Yes, there will be bumps in the road, and this year’s Q4 rally is stealing some of 2020’s thunder, but history shows US equity markets do tend to add to gains after a strong year.

Today we will play devil’s advocate and consider 3 issues that could derail that upbeat story.

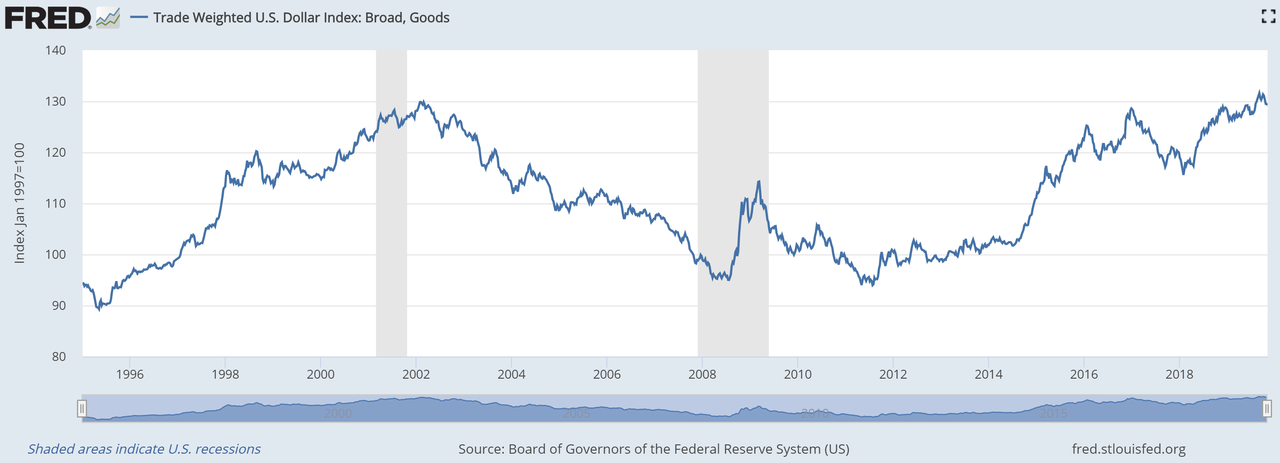

#1: Continued dollar strength.

The Fed’s Trade Weighted Dollar Index remains stubbornly near all-time highs. We use the Broad/Goods version of the index (chart below) because it’s more inclusive than other measures.

As much as other capital markets have embraced an optimistic view of the world of late, the dollar’s continued strength does not fit that framework. Not only is the trade-weighted dollar index still strong, but even the narrower DXY Index is still only 1% off its multiyear highs of September 30th.

A stronger dollar in 2020 would not only cast doubt on the global recovery story, but it would also crimp 2020 US corporate earnings. The S&P 500 derives 38% of its revenues from non-dollar markets.

Bottom line: a weaker dollar is an important (but still missing) link in the current 2020 recovery story. It helps turbo charge global growth by making export-driven economies/companies more profitable and also makes energy (oil is priced in dollars) cheaper for those markets. If the dollar continues to strengthen next year, that will certainly slow any global recovery.

#2: US Corporate leverage in a rising rate environment:

US corporate debt currently sits at all-time high levels: 46% of GDP.

However, because interest rates are low and corporate profit margins are high, cash flow coverage ratios remain within normal ranges.

But if interest rates begin to rise as global economies recover in 2020, then it will be quite a horse race to see if incremental corporate cash flows will grow as quickly as interest expense.

Bottom line: so far the only real sign of trouble here is in the US collateralized loan obligation (CLO) market, where managers bundle subprime loans into risk tranches, but this could spread to traditional corporate debt markets in 2020. The Wall Street Journal had a good piece on the CLO market’s troubles just yesterday (link below), pointing out that these buyers have been over half of the demand for leveraged loans in recent years. Our best source in the leveraged loan market also reports real stress in many credits.

That makes single B and CCC corporate spreads the indicators to watch. Single B spreads are still fairly tight to Treasuries just now (418 basis points, at the lower end of the 1-year range). But as you can see in the 5-year chart below, CCC spreads are certainly moving higher.

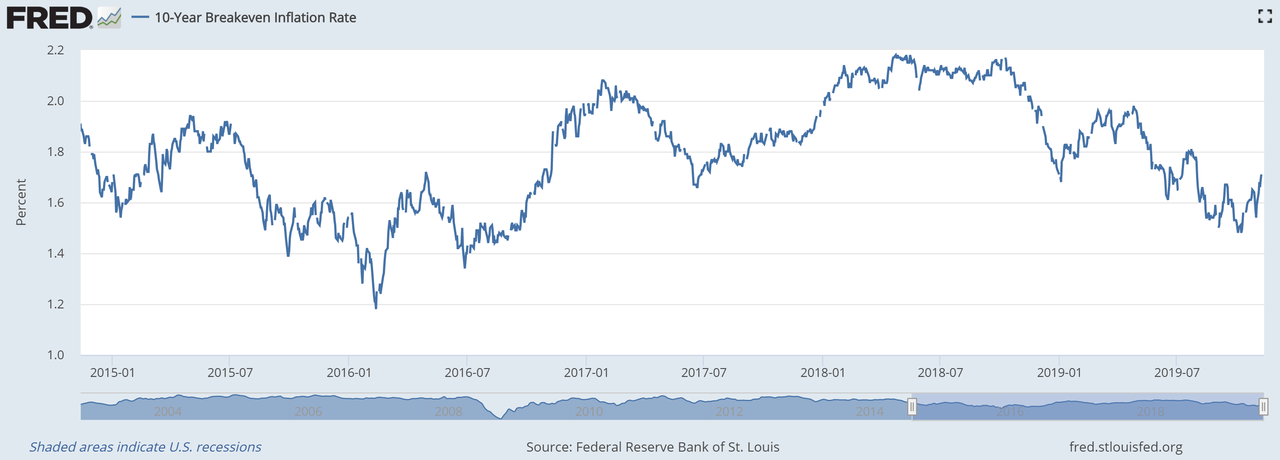

#3) Structural inflation expectations:

Treasury Inflation Protected securities are another market that hasn’t really signed off on the current bullishness over 2020 economic and business conditions.

10-year TIPS spreads are currently 171 basis points, closer to their 1-year lows (148 bp) than their 1-year highs (207 bp).

Over the last 5 years, the only time TIPS spreads have expressed confidence that expected future inflation similar to the Fed’s target of 2% was in 2018.

If fixed income markets do fully embrace the notion of a hotter US economy in 2020, then inflation expectations will rise and long term interest rates will follow along.

Here is the chart of the 10-year TIPS inflation breakeven over the last 5 years for reference:

Bottom line: a piece of the bull case relies on a stealth-dove Fed, worried as they are about inflation expectations (Powell highlighted this at his last presser). But in the sort of faster-growth economy that equity markets are increasingly discounting, that could flip to a stealth-hawk Fed fairly quickly.

Final thought: bullish as we may be, we see the merits of each of these points. At the very least, they are three large bricks in the wall of worry markets will have to climb.

One Bank Finally Admits The Fed’s “NOT QE” Is Indeed QE… And Could Lead To Financial Collapse

After a month of constant verbal gymnastics (and diarrhea from financial pundit sycophants who can’t think creatively or originally and merely parrot their echo chamber) by the Fed that the recent launch of $60 billion in T-Bill purchases is anything but QE (whatever you do, don’t call it “QE 4”, just call it “NOT QE” please), one bank finally had the guts to say what was so obvious to anyone who isn’t challenged by simple logic: the Fed’s “NOT QE”, is really “QE.”

In a note warning that the Fed’s latest purchase program – whether one calls it QE or NOT QE – will have big, potentially catastrophic costs, Bank of America’s Ralph Axel writes that in the aftermath of the Fed’s new program of T-bill purchases to increase the amount of reserves in the banking system, the Fed made an effort to repeatedly inform markets that this is not a new round of quantitative easing, and yet as the BofA strategist notes, “in important ways it is similar.”

But is it QE? Well, in his October FOMC press conference, Fed Chair Powell said “our T-bill purchases should not be confused with the large-scale asset purchase program that we deployed after the financial crisis. In contrast, purchasing Tbills should not materially affect demand and supply for longer-term securities or financial conditions more broadly.” Chair Powell gives a succinct definition of QE as having two basic elements: (1) supporting longer-term security prices, and (2) easing financial conditions.

Here’s the problem: as we have said since the beginning, and as Bank of America now writes, “the Fed’s T-bill purchase program delivers on both fronts and is therefore similar to QE,” with one exception – the element of forward guidance.

The upshot to this attempt to mislead the market what it is doing according to Bank of America, is that:

the Fed is continuing to “ease” even though rate cuts are now on hold, which is supportive of growth, higher interest rates and higher equities, and

the Fed is loosening financial conditions by increasing the availability of, and lowering the cost of, leverage, which broadly supports asset prices potentially at the cost of increasing systemic financial risk.

Putting the Fed’s “NOT QE” in context: so far the Fed has purchased $66bn of Tbills and may purchase $60bn per month through June 2020, which could result in an increase in the Fed’s Treasury holdings by about $500bn.

While we have repeatedly written in the past why we think the Fed’s latest asset purchase program is, in fact, QE, below we present BofA’s argument why we are right.

As Axel writes, there are two basic mechanisms how T-Bill purchases support longer-term security prices: the increase in cash assets and deposit liabilities on bank balance sheets, and the reduction of funding risk for leveraged buyers of Treasuries, MBS and other financed securities.

For those who have forgotten how the “asset reflation” pathway works, recall that the Fed either buys T-bills from investors such as money market funds, or from primary dealers who do not hold T-bills, but can buy them at auction to sell to the Fed. Buying from investors converts their T-bill holdings into new Fed cash, which in turn winds up on deposit in the banking system. If instead a primary dealer buys a Tbill at auction and sells it to the Fed, the transaction results in new Fed cash placed in the Treasury’s cash account, while the dealer balance sheet is unchanged, and the banking system balance is also unchanged. But once the Treasury spends the new Fed cash on a social security payment or a medical insurance bill, etc, the cash enters the banking system and increases the aggregate balance sheet of banks.

Either way, bank balance sheets expand and banks will need to (1) hold more HQLA (high quality liquid assets) against those deposits, and (2) put some of their new cash to work in longer-term securities such as mortgage-backed securities (or even stocks)? Although banks can be flexible in how they deploy the new cash, it is likely that a portion of it will go into bonds similar to what banks already hold (currently $1.8TN in MBS securities and $770bn in Treasuries, according to Fed H.8 data). And once bonds are bid, other investors have no choice but to reach for even riskier securities, such as stocks.

Meanwhile, while the Fed does not directly lend to leveraged investors, some of the increased cash on hand at banks will likely go into repo markets to fund overnight loans to potential buyers of long-term securities in Treasuries and mortgages. This, as BofA explains, is how the increase in reserves is designed to calm repo markets. The amount of bank lending in repo has increased by about 50% since the end of 2017.

Focusing just on the increasingly more important repo channel, which is one ingredient within overall financial conditions, is becoming more important as reliance on overnight funding and leverage continues to rise. This is because, as BofA shows in its “chart of the day”, while banks and security brokers have greatly reduced reliance on overnight funding as a result of Dodd-Frank, the rest of the market has approximately doubled its reliance on overnight funding since the 2008 crisis.

And while one can argue that the proper metric is repo funding as a percentage of Treasuries and MBS outstanding, the bigger picture is that if repo markets stopped functioning today, the amount of Treasury and MBS securities held outside of banks-dealers requiring liquidation (for lack of funding) would be about twice as large as 2008, and as BofA warns, “with today’s surprisingly low levels of liquidity in the “liquid markets” the impact could be massive.” In this context, BofA views the Fed’s purchase program as integral to the promotion of easy financial conditions and supportive of asset prices, which as Chair Powell himself admitted, is the second key criterion for QE.

At this point it is worth considering a critical, if tangential question: Why is the Fed so concerned about not signaling QE, and why are so many Fed fanboys desperate to parrot whatever Powell is saying day after day?

Simply said, there are several reasons why the Fed is making a great effort to let the world know that its security purchases are not QE and are not reflective of any change in monetary policy stance. The first is the obvious issue of signaling concern around the economic outlook which would run counter to its cautiously optimistic and often upbeat assessment. After all, why do QE if the economy has “never been stronger”, and the Fed was hiking rates as recently as a December. Included here are the concerns about running out of ammunition at the zero lower bound of rate policy. With negative rates increasingly off the table – until push comes to shove of course and the Fed is forced to cut below zero – QE is meant to be reserved as dry powder for a rainy day when conventional tools are exhausted (even if QE is in fact taking place this very instant).

A less obvious concern for the Fed is connecting monetary policy to bank demand for Fed liabilities, which as BofA admits, “is not something that fits neatly within its dual mandate”: last January, the Fed made a “momentous decision” to run an “abundant reserve regime” also known as a floor system, where the central bank decided not to return to its pre-crisis days of zero excess reserves. As such, the central bank now views the proper level of excess reserves (a Fed balance sheet liability) not in terms of its dual mandate for inflation and employment, but in terms of how banks prefer to meet regulatory liquidity requirements and how this preference impacts repo and other markets.

In short, the Fed’s dual mandate has been replaced by a single mandate of promoting financial stability (or as some may say, boosting JPMorgan’s stock price) similar to that of the ECB.

Here BofA adds ominously that “by deciding to dynamically assess bank demand for reserves and reduce the risk of air pockets in repo markets, we believe the Fed has entered unchartered territory of monetary policy that may stretch beyond its dual mandate.” And the punchline: “By running balance-sheet policy to ensure overnight funding markets remain flush, the Fed is arguably circumventing the most important brake on excess leverage: the price.“

So if NOT QE is in fact, QE, and if the Fed is once again in the price manipulation business, what then?

According to BofA’s Axel, the most worrying part of the Fed’s current asset purchase program is the realization that an ongoing bank footprint in repo markets is required to maintain control of policy rates in the new floor system, or as we put it less politely, banks are now able to hijack the financial system by indicating that they have an overnight funding problem (as JPMorgan very clearly did) and force the Fed to do their (really JPMorgan’s) bidding.

While it is likely that beyond year-end, the additional tends of billions in reserves will have the required soothing effect, what is less clear is that the Fed can make sure the bank repo lending footprint is resilient to dips in the bank credit cycle.

And this is where BofA’s warning hits a crescendo, because while repo is fully collateralized and therefore contains negligible counterparty credit risk, “there may be a situation in which banks want to deleverage quickly, for example during a money run or a liquidation in some market caused by a sudden reassessment of value as in 2008.”

Got that? Going forward please refer to any market crash as a “sudden reassessment of value”, something which has become impossible in a world where “value” is whatever the Fed says it is… Well, the Fed or a bunch of self-serving venture capitalists, who pushed the “value” of WeWork to $47 billion just weeks before it was revealed that the company is effectively insolvent the punch bowl of endless free money is taken away.

Going back to repo, in such a crashy, pardon, “sudden value reassessmenty” environment, it seems implausible to expect banks to maintain their level of repo lending. And if repo lines were drawn down far enough and for long enough in time, it could lead to deleveraging at institutions that were otherwise healthy, precisely what happened during the financial crisis when the lock up of Lehman’s various overnight funding lines instantly cascaded across the financial system, resulting in an overnight paralysis of the US shadow banking system, and resulting in the near- bankruptcy of the largest US bank.

Therefore, to Bank of America, this new monetary policy regime actually increases systemic financial risk by making repo markets more vulnerable to bank cycles. This, as the bank ominously warns, “increases interconnectedness, which is something regulators widely recognize as making asset bubbles and entity failures more dangerous.“

Think of this as Europe’s infamous doom loop, only in the US and instead of sovereign debt, it uses repo as a risk intermediary to keep the system functioning.

In short, not only is the Fed pursuing QE without calling it QE, but by doing so it is implicitly raising the odds – more so than if it simply did another QE and rebuilt reserves to abour $4.5 trillion or more by purchasing coupon bonds – of another market crash.

It is, however, BofA’s conclusion that we found most alarming: as Axel writes, in his parting words:

“some have argued, including former NY Fed President William Dudley, that the last financial crisis was in part fueled by the Fed’s reluctance to tighten financial conditions as housing markets showed early signs of froth. It seems the Fed’s abundant-reserve regime may carry a new set of risks by supporting increased interconnectedness and overly easy policy (expanding balance sheet during an economic expansion) to maintain funding conditions that may short-circuit the market’s ability to accurately price the supply and demand for leverage as asset prices rise.“

In retrospect, we understand why the Fed is terrified of calling the latest QE by its true name: one mistake, and not only will it be the last QE the Fed will ever do, but it could also finally finish what the 2008 financial crisis failed to achieve, only this time the Fed will be powerless to do anything but sit and watch.

The anti-social carnage unleashed by Corporate America’s “lock-in” / negative network effects has no real limits.

Here’s the U.S.economy in a nutshell: Corporate America is an anti-social Black Plague, gorging on cartel-monopoly profits reaped from negative network effects running amok, enriching the few at the expense of the many and concentrating political power in the hands of the most rapacious, anti-democratic corporate sociopaths.

Let’s start with network effects: the conventional definition is “When a network effect is present, the value of a product or service increases according to the number of others using it.”

So for example, when telephone service was only available to a few users, its value was limited. As more people obtained telephone service, the value of the network increased to both its owners and to users, who could reach more people and conduct commerce more easily as a result of having telephone service.

In the conventional analysis, negative network effects occur from “congestion,” i.e. the network is adding new users so quickly that “more users make a product less valuable.”

But this superficial analysis misses the fatally anti-social consequences of corporate negative network effects, a dynamic described by analyst Simons Chase in this essay. Here is an excerpt:

Even the most imaginative and far-reaching narratives about non-obvious economic fragility and off balance sheet risks are mere rants without constructive ideas about causes and solutions.

Consider network effects, the popular economic construct applied to market concentration and increasing returns for strategies pursued by some leading tech companies. This dynamic economic agent is also known as demand side economies of scale.

W. Brian Arthur, the economist credited with first developing the theory, described the condition of increasing returns as a game of strategic positioning and building up a user base to the point where ‘lock in’ of dominant players occurs. Companies able to tap network effects have been rewarded with huge valuations and highly defensible businesses.

But what about negative network effects? What if the same dynamic applies to the U.S.’s pay-to-play political industry where the government promotes or approves of something through a policy, subsidy or financial guarantee due to private sector influence.

Benefits accrue only to the purchaser of the network effects, and consumers, induced by the false signal of large network size, ultimately suffer from asymmetric risk and experience what I’m calling a loss of intangible net worth for each additional member after the ‘bandwagon’ wares off.

If this were the case, then you would see companies experience rapid revenue growth (out of line with traditional asset leverage models), executives accumulating huge fortunes and political campaign coffers swelling.

But the most striking feature would be the anti-social outcomes, the ones not available without the instant critical mass of government-supported network effects, the ones that, at scale, monetize a society’s intangible net worth.

Some products tied to these metrics include: prescriptions drugs, junk food targeting children, mortgages, diplomas, and social media. The list of industries that are likely to have gained through the purchasing of network effects in D.C. maps closely to the decay that is visible in U.S. society.

The loss of intangible capital and other manifestations of non-obvious economic fragility (to use Simons’ apt phrase) is the subject of my latest book,Will You Be Richer or Poorer? Profit, Power and A.I. in a Traumatized World, in which I catalog the anti-social consequences of negative network effects and other forces eroding our nation’s intangible capital.

The full social cost of social media’s negative network effects are difficult to tally, but studies have found that loneliness and alienation are correlated to how many hours a day individuals spend on social media. (An Internet search brings up dozens of reports such as NPR’s Feeling Lonely? Too Much Time On Social Media May Be Why.)

Facebook is trying to leverage its social media “lock-in” to issue its own global currency and both Facebook and Google are trying to offer banking services without any of the pesky regulations imposed on legitimate banks. (Will $10 million in lobbying do the trick? How about $100 million? We’ve got billions to “invest” in corrupting and controlling public agencies and political power.)

Once Corporate America locks in cartel-monopoly power, i.e. you have to use our services and products, the corporate sociopaths use their billions in market cap and profits to buy the sociopaths in government.Pay-to-play is the real political machinery; “democracy” is the PR fig-leaf to mask the private sector “lock-in” (monopoly) and the public-sector “lock-in” (regulatory influence, anti-competitive barriers to entry, the legalization of corporate fraud, cooking the books, embezzlement, etc.)

Consider Boeing, an effective monopoly which used $12 billion in profits to buy back its own shares and “invested” millions in buying political influence so it could minimize public-sector oversight.

Rather than spend the $12 billion designing a new safe aircraft, Boeing cobbled together a fatally flawed design dependent on software, as described in The Case Against Boeing (The New Yorker) to maximize the profitability of its “lock-in”.

The anti-social carnage unleashed by Corporate America’s “lock-in” / negative network effects has no real limits. Consider the essentially limitless private and social damage caused by Big Tech: Child Abusers Run Rampant as Tech Companies Look the Other Way (New York Times).

Then there’s the opioid epidemic, whose casualties run into the hundreds of thousands, an epidemic that was entirely a creature of Corporate America seeking to maximize “lock-in” profits by buying regulatory approval and pushing false claims that the corporate products were safe and non-addictive.

Note the media sources of these reports: these are the top tier of American journalism, not some easily dismissed alt-media source.

What does this tell us? It tells us the anti-social consequences are now so extreme and so apparent that the corporate media cannot ignore them. Once Corporate America locks-in market, financial and political power, it acts as a virulent Black Plague on the social order, legitimate democracy, and an entire spectrum of intangible social capital including the rule of law.

As Simons put it:

“The ethical dimension underpinning the whole system is this: what’s moral is what’s legal and what’s legal is for sale.” Where does this Black Plague pathology take us? To a collapse of the status quo which enabled it, cheered it, and so richly rewarded it.