Two Baghdadi Associates Taken Alive In The Raid Along With “Trove” Of Intel

Two men believed close to the Islamic State’s top leadership were taken alive during the Saturday night US special forces raid which killed ISIS leader Abu Bakr al-Baghdadi.

“There were two adult males taken off the objective, alive,” Chairman of the Joint Chiefs of Staff Mark Milley announced Monday during a Pentagon briefing. “They’re in our custody and they’re in a secure facility,” Milley added, without revealing the identity of the captives.

US Defense Secretary Mark Esper and Joint Chiefs Chairman General Mark Milley. Image source: Reuters

“While clearing the objective, US forces discovered al-Baghdadi hiding in a tunnel. The assault forces closed in on al-Baghdadi and ended when he detonated a suicide vest,” said Milley.

This also as The New York Times reports Monday that intelligence recovered from the raid “could reveal a trove of ISIS clues”. No doubt this includes the human intelligence potentially gathered through interrogations of the newly captured ISIS operatives, which could reveal details of Baghdadi’s last days and months.

The Times report said “confiscated documents and electronic records” were found at the site where Baghdadi was hiding, which should “shed critical light on how the Islamic State operated.”

Gen. Milley also confirmed during the briefing that segments of the video imagery from the Baghdadi raid would be made public once it is subject to a declassification review, following prior comments made by President Trumps saying he’s mulling release of the video.

Milley mentioned that likely the video would be made public in the coming days after the declassification process.

In their joint press briefing Defense Secretary Mark Esper and Gen. Milley also addressed the issue of Baghdadi’s remains: “The disposal of his [al-Baghdadi’s] remains has been done and is complete and was handled appropriately,” Milley told reporters.

After the terror chief was described to have denoted a suicide vest as US forces were in pursuit while fleeing with his three children (also reported killed in the blast) in an underground tunnel, his DNA was reportedly quickly transported to a secure facility for testing. The Pentagon then said his identity was confirmed to be Baghdadi.

Whereas JPMorgan has been the unrelenting bull of this year’s 21% surge in the S&P500, Morgan Stanley has emerged as its bearish nemesis, and while JPM earlier today said its 2020 mid-year forecast of S&P 3,200 is doing so well, it could be hit as soon as this year, Morgan Stanley has once again doubled down on the bank’s bearish outlook, and in a report from its chief cross-asset strategist Andrew Sheets writes that it sees “a key divide. Some investors, like ourselves, remain cautious, focused on a variety of cyclical indicators that point to historically poor returns over the next 12-24 months.”

In framing the tensions, Sheets writes that “those with shorter-term investment horizons, are more optimistic” and notes that the optimists “cite two catalysts: i) Economic momentum, and PMIs, that are set to inflect; and ii) Already cautious sentiment means that growth concerns are already in the price.“

Why doesn’t Morgan Stanley agree with JPMorgan’s more optimistic take? Two reasons:

On the first issue, i.e., a rebound in economic momentum, Sheets points out the already large divide between asset prices (up) and US or global PMIs (down), as well as the fact that its US economists expect the next reading of ISM manufacturing PMI to see another decline. This PMI scenario does not bode well for risk assets.

However, it is the second point that is the emphasis of Sheets’ report, because as he writes, regarding sentiment three key factors have to be considered:

Tactically, while optimism does appear modest, measures of risk-aversion (Morgan Stanley’s Global Risk Demand Index, the Put/Call Ratio, the VIX) have rallied sharply following last week’s developments on trade and Brexit.

Strategically, the efficacy of investing based on ‘sentiment’ looks regime-dependent; it’s normal for investors to “get bearish in a bear market”. According to the strategist, “there’s above-average risk that we’re in such a regime.”

Third, and final, while overall positioning is arguably modest, relative positioning in equity sector and style is extreme. The ‘pain trade’ isn’t higher, it’s rotation.

Everyone has heard the saying “climbing the wall of worry”, which is basically a less refined way of saying that cautious sentiment is one of the most compelling reasons to be bullish (i.e. “buy when there is blood on the streets”). Sheets, however, disagrees for the reasons listed below.

There are a variety of ways to measure investor sentiment. For better and worse, many tend to focus on the US market, the world’s largest. Sheets begins his discussion with four indicators that he often sees cited as indicators for investor caution or greed.

AAII net bull-bear index: Per a weekly survey from the American Association of Individual Investors, this index shows the difference between those who are ‘bullish’ and ‘bearish’. The bank focuses on the four-week moving average to reduce noise.

Net length in S&P 500 futures from CFTC: Lower net exposure would, in theory, suggest more investor caution.

Equity fund flows from ICI: Weaker fund flows would, in theory, suggest more caution.

Hedge fund net exposure from our Morgan Stanley Prime Brokerage desk

The charts below summarize these four sentiment indicators over the most recent 18-month period, and as Sheets points out, “none suggest a great deal of optimism over the last 18 months, and such pervasive caution for an extended period of time is frequently cited as a helpful factor for markets.”

Yet whereas bulls will say the charts above are a clear indication to buy, one can easily present a counter argument. To wit, what happens if one looks at these measures over a different period – say the 18 months starting in January 2007: Similar to the charts above, these also saw below-average levels of sentiment over an extended period. But this wasn’t a signal to buy; it reflected investors (correctly) appreciating that the market environment was changing, for the worse.

Needless to say, anyone who used collapsing sentiment into the global financial crisis as a contrarian signal to buy was not very happy.

Fast forward to today, when “cautious” sentiment over the last 18 months hasn’t stopped global stocks (MSCI World) from falling over this time. This may be because that cautious sentiment was simply (correctly) responding to worsening market dynamics. And as shown above, 2007-08 saw a similar pattern, albeit with far more market weakness, which is to be expected: back then the Fed did not provide assurance it would step in any time there was a market spasm.

* * *

Another surprising finding: contrary to conventional wisdom, which holds that as of this moment most investors are skeptical and have limited exposure to risk assets, a proprietary Morgan Stanley indicator finds precisely the opposite.

As Sheets writes, the idea that sentiment indicators can be regime-dependent can be seen in something Morgan Stanley cites frequently – the Morgan Stanley Global Risk Demand Index, created and run by the bank’s FX strategy team (STGRDI on Bloomberg). This index looks at a variety of measures of cross-asset risk appetite; high readings suggest ‘greed’, low readings reflect ‘fear’.

From 2010 to 2017, what one has been supposed to do with those signals has been pretty straightforward. ‘Greed’ often reflected good sell signals and ‘fear’ good times to buy, something we can quantify by looking at 3-month forward returns based on different levels of the index.

A similar pattern was observed in the bull market prior to this one, 2004-07. In both cases, this sentiment measure worked ‘as expected’ in a trending bull market, according to Morgan Stanley.

But GRDI’s ‘signal’ changed dramatically in the time between, specifically the bear market of 2007-08: Running the same analysis during that internal reveals that the forward performance picture is almost completely reversed from the two bull market periods.

Why has sentiment been less effective in a time of market stress? Simple: it’s normal for investors to get bearish in a bear market!

This brings us to one of the biggest variations in opinion between Morgan Stanley and JPM, which has been pounding the table on bearish sentiment as a key catalyst for further upside (to be fair, JPM has been bullish when sentiment is bullish, as it confirms their thesis, and has been ever more bullish when sentiment is bearish, when it serves as a bullish contrarian signal). Here, Morgan Stanley asks if sentiment measures could be facing another shift in regime that could reduce their efficacy? And answers: “We think the risk is high” largely as a result of the “relatively light positioning over the last 18 months” which hasn’t prevented what our MS’s house uber-bear, Michael Wilson, has coined the “unsatisfying bear market” back in April 2018, an extended period of choppy markets, frustrating for bulls and bears.

Meanwhile, the economic and cyclical risk looks above-average, with Morgan Stanley’s cycle model moving to ‘downturn’, itself a sign of a potentially different regime…

… and – what’s worse – investors are now facing a market with ~0% global earnings growth, falling margins, a flat yield curve, weak PMIs, weak commodity prices and defensive leadership, all things that are very different from the 2010-17 or 2004-07 regimes when sentiment indicators were most effective. All of this brings us to a conclusion which we have long believed is the right now, namely that…

The ‘pain trade’ isn’t higher

Framing the argument, agaion, Sheets writes that when discussing sentiment and positioning over the last 18 months, one often confronts the argument that, due to widespread caution, rising markets are actually more painful for investors than falling ones. While this is a small point, Morgan Stanley – and most rational traders – strongly disagree.

The main reason why the pain trade is never higher, is that being ‘flat’ one’s benchmark still means being outright long. There are US$47 trillion of equities in the MSCI ACWI index, and these are all owned by someone. The market rallying 10% means the world’s insurance companies, pension funds and individuals have US$4.7 trillion more wealth on paper. That’s hardly the more painful outcome.

Second, and even more important, while some parts of the system have deleveraged since the GFC, the world remains a highly indebted place. In a highly leveraged world, high (and rising) asset prices help to keep this cycle going. The alternative is far more painful.

This, in turn brings us to the (widely misunderstood) “paradox of positioning.”

As Sheets concludes, “one paradox of sentiment measures is that, during times of stress (when one relies on them most), their signals can flip.” But there’s another ‘paradox’ – while cautious sentiment is frequently cited these days as a support to the market overall, how investors express this view, in sector and style, remains unusually crowded. Or, as Morgan Stanley puts it, “Caution on stocks is seen as a reason to be bullish, but optimism on growth stocks? No problem!” That is the best summary of the often hypocritical assessment by bulls, whose market takes can be summarized as heads I win, and tails… I win (when in reality it’s all the Fed).

The Allure and Limits of Monetized Fiscal Deficits

With the global economy experiencing a synchronized slowdown, any number of tail risks could bring on an outright recession. When that happens, policymakers will almost certainly pursue some form of central-bank-financed stimulus, regardless of whether the situation calls for it.

A cloud of gloom hovered over the International Monetary Fund’s annual meeting this month. With the global economy experiencing a synchronized slowdown, any number of tail risks could bring on an outright recession. Among other things, investors and economic policymakers must worry about a renewed escalation in the Sino-American trade and technology war. A military conflict between the United States and Iran would be felt globally. The same could be true of “hard” Brexit by the United Kingdom or a collision between the IMF and Argentina’s incoming Peronist government.

Still, some of these risks could become less likely over time. The US and China have reached a tentative agreement on a “phase one” partial trade deal, and the US has suspended tariffs that were due to come into effect on October 15. If the negotiations continue, damaging tariffs on Chinese consumer goods scheduled for December 15 could also be postponed or suspended. The US has also so far refrained from responding directly to Iran’s alleged downing of a US drone and attack on Saudi oil facilities in recent months. US President Donald Trump doubtless is aware that a spike in oil prices stemming from a military conflict would seriously damage his re-election prospects next November.

The United Kingdom and the European Union have reached a tentative agreement for a “soft” Brexit, and the UK Parliament has taken steps at least to prevent a no-deal departure from the EU. But the saga will continue, most likely with another extension of the Brexit deadline and a general election at some point. Finally, in Argentina, assuming that the new government and the IMF already recognize that they need each other, the threat of mutual assured destruction could lead to a compromise.

Meanwhile, financial markets have been reacting positively to the reduction of global tail risks and a further easing of monetary policy by major central banks, including the US Federal Reserve, the European Central Bank, and the People’s Bank of China. Yet it is still only a matter of time before some shock triggers a new recession, possibly followed by a financial crisis, owing to the large build-up of public and private debt globally.

What will policymakers do when that happens?

One increasingly popular view is that they will find themselves low on ammunition. Budget deficits and public debts are already high around the world, and monetary policy is reaching its limits. Japan, the eurozone, and a few other smaller advanced economies already have negative policy rates, and are still conducting quantitative and credit easing. Even the Fed is cutting rates and implementing a backdoor QE program, through its backstopping of repo (short-term borrowing) markets.

But it is naive to think that policymakers would simply allow a wave of “creative destruction” that liquidates every zombie firm, bank, and sovereign entity. They will be under intense political pressure to prevent a full-scale depression and the onset of deflation. If anything, then, another downturn will invite even more “crazy” and unconventional policies than what we’ve seen thus far.

In fact, views from across the ideological spectrum are converging on the notion that a semi-permanent monetization of larger fiscal deficits will be unavoidable – and even desirable – in the next downturn. Left-wing proponents of so-called Modern Monetary Theory argue that larger permanent fiscal deficits are sustainable when monetized during periods of economic slack, because there is no risk of runaway inflation.

Following this logic, in the UK, the Labour Party has proposed a “People’s QE,” whereby the central bank would print money to finance direct fiscal transfers to households – rather than to bankers and investors. Others, including mainstream economists such as Adair Turner, the former chairman of the UK Financial Services Authority, have called for “helicopter drops”: direct cash transfers to consumers through central-bank-financed fiscal deficits. Still others, such as former Fed Vice Chair Stanley Fischer and his colleagues at BlackRock, have proposed a “standing emergency fiscal facility,” which would allow the central bank to finance large fiscal deficits in the event of a deep recession.

Despite differences in terminology, all of these proposals are variants of the same idea:large fiscal deficits monetized by central banks should be used to stimulate aggregate demand in the event of the next slump. To understand what this future might look like, we need only look to Japan, where the central bank is effectively financing the country’s large fiscal deficits and monetizing its high debt-to-GDP ratio by maintaining a negative policy rate, conducing large-scale QE, and pursuing a ten-year government bond yield target of 0%.

Will such policies actually be effective in stopping and reversing the next slump? In the case of the 2008 financial crisis, which was triggered by a negative aggregate demand shock and a credit crunch on illiquid but solvent agents, massive monetary and fiscal stimulus and private-sector bailouts made sense. But what if the next recession is triggered by a permanent negative supply shock that produces stagflation (slower growth and rising inflation)? That, after all, is the risk posed by a decoupling of US-China trade, Brexit, or persistent upward pressure on oil prices.

Fiscal and monetary loosening is not an appropriate response to a permanent supply shock. Policy easing in response to the oil shocks of the 1970s resulted in double-digit inflation and a sharp, risky increase in public debt. Moreover, if a downturn renders some corporations, banks, or sovereign entities insolvent – not just illiquid – it makes no sense to keep them alive. In these cases, a bail-in of creditors (debt restructuring and write-offs) is more appropriate than a “zombifying” bailout.

In short, a semi-permanent monetization of fiscal deficits in the event of another downturn may or may not be the appropriate policy response. It all depends on the nature of the shock. But, because policymakers will be pressured to do something, “crazy” policy responses will become a foregone conclusion. The question is whether they will do more harm than good over the long term.

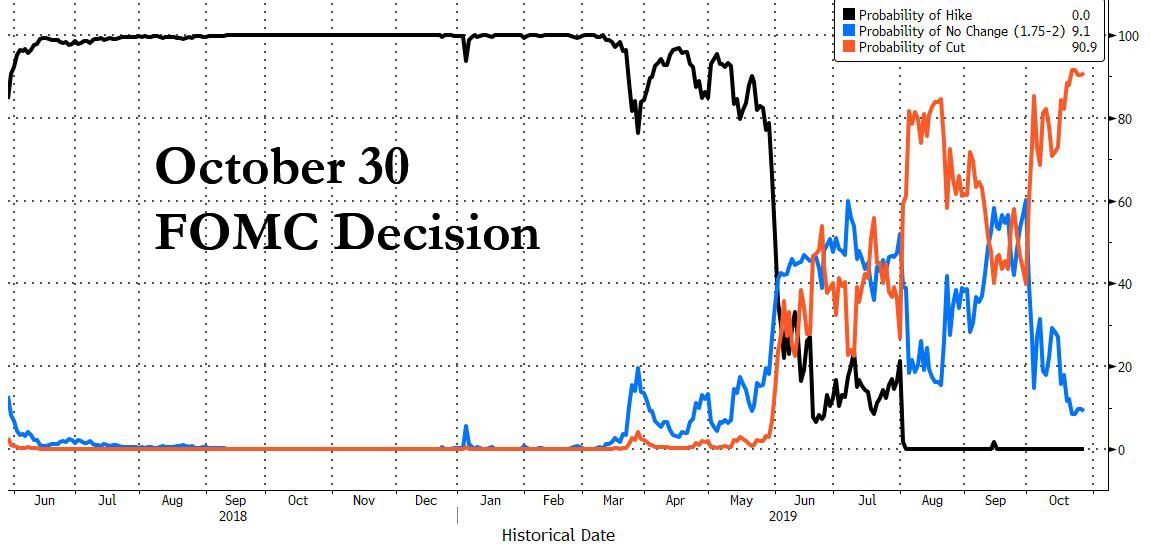

Brace For A Market Tantrum: Why One Bank Expects The Fed To Disappoint This Wednesday

When it comes to the Fed’s next rate decision, the market has made up its mind: as of this morning, the fed funds futures market is pricing in a probability of 91% that the Fed announces another 25bps rate cut at 2pm on Wednesday, with odds of no cut at just 9%.

So certain are strategists that the Fed will deliver another “insurance” cut – the third in a row – that discussion has now firmly shifted to what the Fed will do in its next, December, meeting with the FT writing that the “Federal Reserve faces the thorny decision of whether to signal an interruption to its monetary easing after it delivers what is widely expected to be a third consecutive cut to its main interest rate this week.”

If the Federal Open Market Committee presses ahead with a new rate reduction on Wednesday afternoon, it will have already notched up 75 basis points of monetary stimulus this year — and to some economists and Fed officials that should be sufficient to accomplish the goal.

Needless to say, the prevailing consensus is that Powell will cut, with Scott Anderson, chief economist at Bank of the West, summarizing it best: “I think they will end up cutting another 25 basis points [this week] and then pause for the rest of this year.”

Yet not everyone agrees.

According to Jefferies money-market economist Thomas Simons, the headwinds that pushed the central bank to cut rates in July and September have “abated somewhat” as U.S.-China trade tensions and Brexit uncertainty have also diminished, while the gap between the Fed’s policy stance and that of other central banks has narrowed.

As a result, Simon takes on the wildly contrarian view that the Fed will keep rates unchanged this week while leaving a December cut on the table; in doing so, the Fed would spark a “temper tantrum” in markets, while pushing back against aggressive Fed pricing and cement the idea of a mid-cycle policy adjustment.

“If they continue with so many consecutive rate cuts, they can never break the cycle of market expectations thinking more are coming,” Simons said in a Bloomberg interview, adding that “it’s time for the Fed to take a step back and see if the prior cuts are going to have an effect before moving forward with another one.”

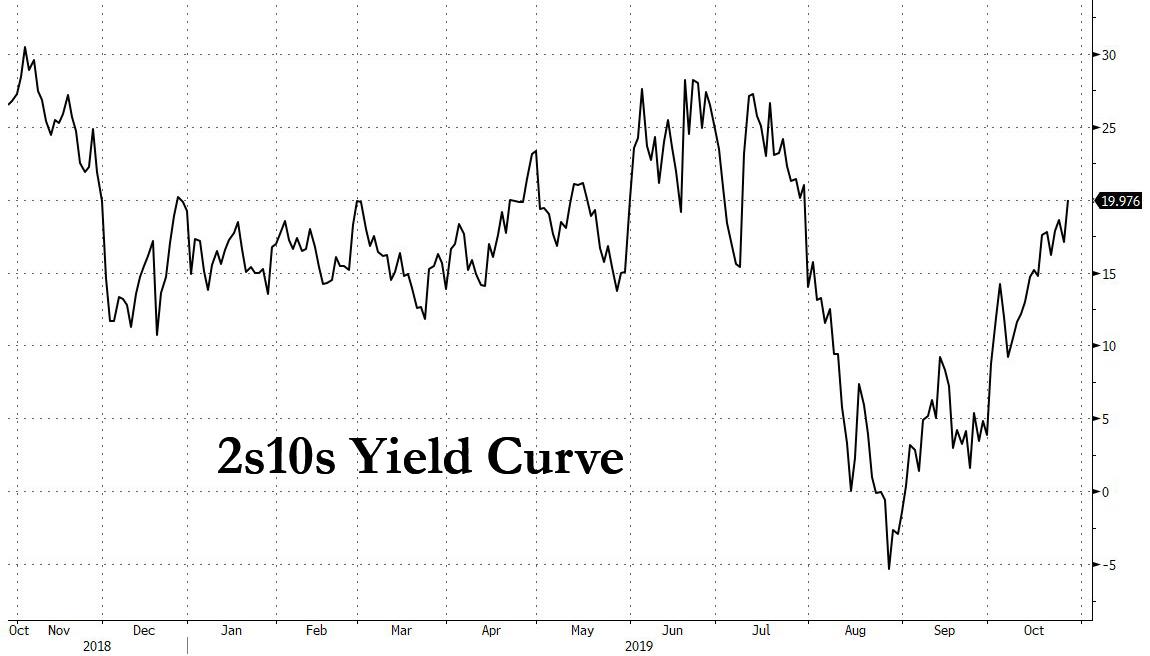

Holding fire on more rate cuts will likely have the added benefit of further steepening the yield curve, a critical condition for US banks to return to profit growth: with yields on the short-end depressed thanks to the Fed’s “Not QE”, which will soon spill over from purchasing merely Bills into the 2Y (if not longer maturity) sector, longer-dated yields will likely jump should the Fed surprise markets by not cutting rates in 48 hours. This would serve to further steepen the 2s10s yield curve, which after inverting briefly in August is back to level last seen at the start of the year (here we ignore the discussion that it is the re-steepening of the yield curve following an inversion that is the true recession signal, as it is a topic we have covered extensively in the past).

Helping the steeper yield curve is the recent rise in 10-year Treasury yields which printed a six-week high of 1.86% on Monday as President Trump touted trade progress and the EU granted the U.K. a three-month Brexit delay. Meanwhile, rates on 2-year Treasuries climbed a more modest 3 bps.

To be sure, it is unclear if Powell would be willing to risk a market tantrum just to prove that he is not at the mercy of the market. As Jefferies points out, a knee-jerk response to the Fed standing pat would likely see U.S. stocks sink and the yield curve “twist.” Or, as Bloomberg explains, “while the Fed’s bill purchases and lower inflation expectations should continue to suppress short- and long-dated yields, 3- to 7-year Treasuries may sell off, he said.”

“There will be a little bit of a temper tantrum, but I think the volatility will be short-lived,” Simons said. “Stocks won’t like it, but it isn’t exactly going to set off a prolonged sell-off.”

There is another reason why Simons’ view is in the minority: as the FT noted over the weekend, the drumbeat of relatively soft economic data, and fears of a negative market reaction, could make Mr Powell and other Fed policymakers wary of indicating that this round of “insurance” cuts is already over. Furthermore, the latest truce in the US-China trade war is only tentative, and even if it is signed by Trump and Xi Jinping, in Chile next month, many of the tariffs and the tensions in transpacific trade are set to linger.

“The Fed runs the risk of an unnecessary tightening of financial conditions. We are hopeful that Chair Powell avoids such a mistake,” said Natixis economist Joe Lavorgna.

As such, whereas most dismiss Jefferies’ suggestion, all will be focused on whether the FOMC statement changes it pledge to “act as appropriate to sustain the expansion” widely seen as an indicator of future rate cuts, to wording that appears less committed to further easing.

“Keeping the forward guidance as is is the path of least resistance. If they take it out they are being unintentionally hawkish,” said Michelle Meyer, an economist at Bank of America Merrill Lynch. “The data now is softening so I think they have to give some nod in that direction.”

Boosting the dovish case, it is likely that just hours before the Fed’s announcement, the US will announce that Q3 GDP rose just 1.6%, which would be the slowest pace so far this year; In fact, since the Trump election, there has been just one quarter of GDP growth below 2%, and analysts will be looking out for what this might mean for the economy heading into next year’s election. And then there is the October US jobs report on Friday, where consensus expects a paltry +90k print following the previous month’s +136k increase. If accurate, that would be the weakest pace of monthly jobs growth since May but the recent GM strike complicates the analysis with a 46k hit expected from this. Explanations aside, however, Trump will be sure to put the squeeze on the Fed to cut rates even more after such a poor number, and for Powell the question will be whether he wishes to do so after he has just cut again for the third time, or after giving himself some breathing space by not cutting rates this week, even if it means a modest “tantrum.”

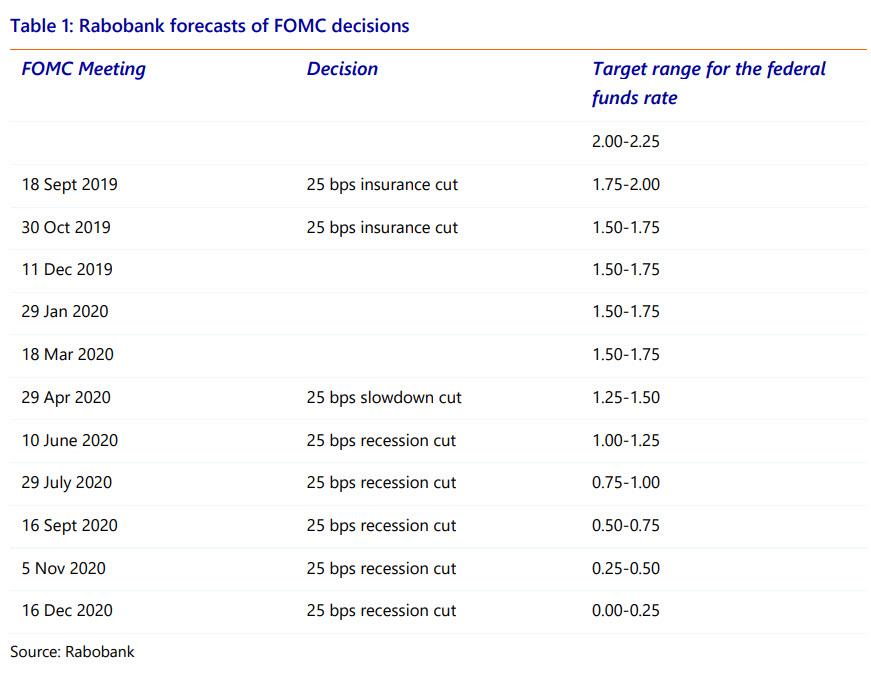

While it is unknown what Powell will decide on Wednesday, the best summary of the choices facing the Fed chair comes from the former head of the NY Fed’s market team, Brian Sack, who is currently director of global economics at DE Shaw, and who two weeks ago told an Institute of International Finance conference that “we either stabilize with one more cut, or I think we’re going to go all the way to the lower bound.”

The problem for the Fed is that even if it cuts on Wednesday, the probability of a quick “stabilization” is virtually nil, for one simple reason: China refuses to join the global reflation party, which has resulted in its credit impulse barely rebounding from cycle lows.

As long as Beijing refuses to lend a helping hand to the global reflation effort, it will be up to the Fed. And should Powell use up his last “insurance” cut for nothing – because after three cuts as Sack said, the Fed will likely have no choice but to cut all the way to zero, something which Rabobank predicted some time ago, the Fed chair will have no choice but to capitulate.

And, as an added consideration, this will be Trump’s preferred outcome, because what better way to ensure that the S&P is at all time highs and the US economy avoids recession ahead of the Nov 2020 election, than the Fed cutting rates to 0% by December 2020.

What happens then?

Well, with “Not QE” already active, and the Fed out of ammo when it comes to more rate cuts, what happens in 2021 will depend on one simple choice: will the Fed follow Europe and Japan into negative rates, or will the long delayed recession finally arrive.

As LME week kicks off, S&P Global Platts editors take a closer look at the current drivers of copper prices. US oil and refined products trade, UK political parties’ energy policies, and a glut of Russian coal on the European market round out this week’s selection.

1. Upturn in copper prices a key talking point for LME Week

What’s happening? 2019 has proved a turbulent year for metals, with the continued trade dispute between the US and China – and the associated economic malaise – one of the biggest drivers. For copper it has been a kick in the teeth, as the metal dropped from around $6,600/mt in April to a low of $5,520/mt in September, although it is currently trading somewhat higher at around $5,895/mt. As LME Week begins, there is renewed optimism for copper prices headed into 2020. The recent pick-up has been prompted by talk of a possible partial trade resolution, and strikes in major producing nation Chile, part of a wave of protests over rising living costs and high levels of inequality in the country.

What’s next? Citi bank expects copper to rebound. Max Layton, an analyst at the bank, is placing bullish bets on the metal in 2020. “We forecast $6,500/mt by H2 2020, targeting $6,300/mt on a 6-month view, on the back of sustained supply disruptions and an anticipated rebound in macroeconomic sentiment,” Layton said. Others see a more moderate adjustment. S&P Global Market Intelligence commodities analyst Tom Rutland expects prices to stay similar to 2019 levels, averaging around the $6,000/t mark. “In 2020, we estimate that global copper demand will grow at similar levels to refined production, maintaining a balanced market,” he said.

2. US headed for net petroleum exports through 2020

What’s happening? As US shale production continues to grow and petroleum exports climb, the country has become a net total petroleum exporter this month, the latest figures from the US Energy Information Administration show. The US was a net exporter of 621,000 b/d of total petroleum the week ending October 18. That followed two weeks of net exports to the tune of roughly 30,000 b/d. The recent shift has also been driven by a sharp 438,000 b/d decline in crude imports to 5.86 million b/d the week ending October 18.

What’s next? Crude imports are likely to rise again, as the 438,000 b/d decline in the third week of October could have been the result of loading delays related to Tropical Storm Nestor. US Census data shows imports, particularly from Mexico, rising following the storm. Also, a combined 2.2 million b/d of distillation capacity is currently down for maintenance in the Midwest and USGC, according to S&P Global Platts Analytics, but most of this will be back online by end-November, which would imply higher crude imports. Still, the longer term trend is for the US to be a net exporter of total petroleum through 2020, according to the EIA, although this will be driven primarily by a rise in refined products and other liquid fuels exports. The EIA’s Short-Term Energy Outlook shows the US as a net exporter of 1.53 million b/d by December 2020, while remaining a net importer of crude.

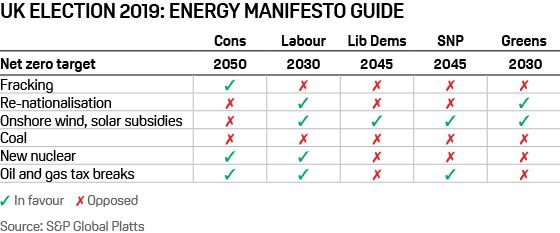

3. Energy policy in spotlight as UK general election looms

What’s happening? The UK’s opposition Labour Party has set out a radical low-carbon energy planahead of a possible general election. Some 30 recommendations, put together by a team of independent experts, urge an immediate, vast expansion of offshore and onshore wind and solar, and all new buildings to be net zero carbon from 2020.

What’s next? Distinct differences between the UK’s various political parties on climate and energy policy will come in to focus if/when General Election manifestos are published. One key area of uncertainty is Labour’s position on oil and gas tax breaks. It has to square the circle of supporting jobs and investment with its decarbonisation strategy. Our assumption is Labour’s focus will be on raising corporation tax rather than removing E&P tax breaks.

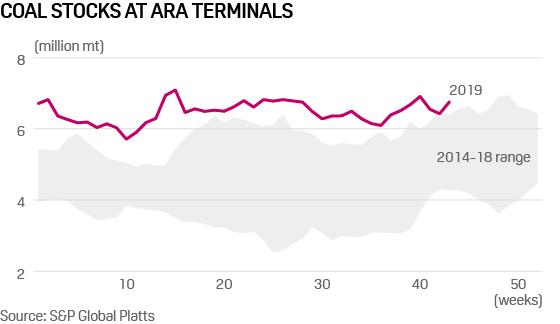

4. Russian thermal coal floods European market

What’s happening? The European coal market is being inundated with Russian thermal coal, keeping stockpiles at Dutch terminals close to record highs and more than one million mt above the five-year average. This is reducing spot demand as the winter season gets underway, and placing firm downward pressure on CIF ARA coal prices, which have struggled to hold above the $60/mt level for the last six months.

What’s next? Russian coal exports show little sign of significantly reducing, which will likely see ARA stocks remain close to 7 million mt over winter. A strong winter coal burn could alleviate the pressure, but this seems unlikely given recent competitive natural gas prices, which have so far left coal out of the money in Europe. This has kept price expectations for the first half of 2020 similarly bleak to the low pricing environment which has defined 2019 so far, and the multi-years low of $45/mt may soon be tested.

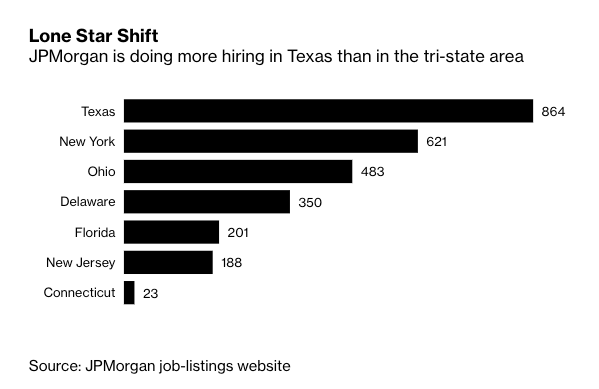

JPMorgan Prepares For Next Recession By Shifting Jobs From NYC To Texas

A new report via Bloomberg details how JPMorgan Chase & Co. is preparing for the next economic downturn by weighing the option to relocate its Manhattan headquarters to lower-cost financial hubs such as ones in Plano, Texas; Columbus, Ohio; and Wilmington, Delaware.

JPM spokesman Joe Evangelisti told Bloomberg the bank’s new headquarters (likely to be in Texas), will house twice the number of employees than its Manhattan office.

Sources told Bloomberg that hundreds of credit-risk employees have already transferred to Texas. Other sources have said Manhattan will no longer be the location for the bank’s compliance.

Bloomberg noted that other large financial institutions had been exiting NYC for lower-cost commercial hubs across the country.

Deutsche Bank expanded operations in Jacksonville, Florida; Goldman Sachs has built officers in Salt Lake City; and AllianceBernstein Holding LP announced plans to move its headquarters to Nashville, Tennessee.

While JPM CEO Jamie Dimon told investors the bank would build a new headquarters at 270 Park Ave, in Midtown Manhattan, it has also quietly constructed a new building that can house 4,000 employees in the Dallas suburb of Plano. Already, JPM has 25,000 employees in Texas, and if the next recession strikes, it seems that the bank has a clear choice to move operations to a low-cost hub to weather the financial storm.

Dimon mentioned in an investor call last year that the Plano site could be the company’s next headquarters.

“There are more JPMorgan Chase employees in Texas than any other state outside of New York,” he said. “I’m sure it will be No. 1 soon.”

Evangelisti said, “Location strategy is not simply about costs…We build in places to be close to local talent such as Palo Alto, to better serve clients and for business resiliency reasons.”

JPM’s location strategy is a response to streamline the bank before the next economic downturn.

The cost to run a company in NYC has skyrocketed in the last decade. Also, regulations and taxes in the city are some of the highest in the country.

In total, the bank has 37,000 employees across NYC, at least half are bank branch workers, a source told Bloomberg. Once construction at 270 Park Ave is completed, expected in 2023, JPM could consolidate employees across the entire metro area.

As for the next big trend in business, Wall Street banks are already making their exit plans out of NYC to lower-cost financial hubs across the country.

Judging by the volume of intemperate emails and angry social media blasts that come my way, the party of impeachment seems to be inhaling way too much gas from the smoking guns it keeps finding in the various star chambers of its inquisition against you-know-who. You’d think that the failure of Mr. Mueller’s extravaganza might have chastened them just a little – a $32 million-dollar effort starring the most vicious partisan lawyers inside-the-Beltway, 2,800 subpoenas issued over two years, 500 search warrants exercised, and finally nothing whatever to pin on Mr. Trump – except the contra-legal assertion that now he must prove his innocence.

When you state just that, these frothing hysterics reply that many background figures – if not the Golden Golem of Greatness himself – were indicted and convicted of crimes by Mr. Mueller’s crew. Oh yes!

The Russian troll farm called the Internet Research Agency was indicted for spending $400,000 on Facebook ads (and never extradited or tried in a court-of-law). Pretty impressive victory there!

The hacking of Hillary Clinton’s emails by “Russia”? Still just alleged, never proven, with plenty of shady business around the search for evidence.

Paul Manafort, on tax evasion of money earned in Ukraine, 2014? We’ll see about that as the whole filthy business of the 2014 Ukraine regime change op under Mr. Obama gets reviewed in the months ahead.

George Papadopoulos for lying to the FBI? Stand by on that one, too; still a developing story.

General Michael Flynn, for ditto? You may have noticed that General Flynn’s case is shaping up to be the biggest instance of prosecutorial misconduct since the Dreyfus affair (France, 1894-1906, which badly-educated Americans most certainly know nothing about).

To set the record straight I’m forced to repeat something that these New Age Jacobins seem unable to process: you don’t have to be a Trump cheerleader to be revolted by the behavior of his antagonists, which is a stunning spectacle of bad faith, dishonesty, incompetence, and malice — and is surely way more toxic to the American project than anything the president has done. Every time I entertain the complaints of these angry auditors, I’m forced to remind myself that these are the same people who think that “inclusion” means shutting down free speech, who believe that the US should not have borders, who promote transsexual reading hours in the grammar schools, and who fiercely desire to start a war with Russia.

That’s not a polity I want to be associated with and until it screws its head back on, I will remain the enemy of it. In fact, in early November I’m traveling to New York City, where the Jacobin city council has just made it a crime to utter the phrase illegal alien in a public place, with a $250,000 penalty attached. I challenge their agents to meet me in Penn Station and arrest me when I go to the information kiosk and inquire if they know what is the best place in midtown Manhattan to meet illegal aliens.

The volume of Jacobin hysteria ratcheted up to “11” late last week when the news broke that the Attorney General’s study of RussiaGate’s origins was upgraded to a criminal investigation, and that a voluminous report from the DOJ Inspector General is also about to be released. What do you suppose they’re worried about? Naturally the Jacobins’ bulletin board, a.k.a The New York Times, fired a salvo denouncing William Barr — so expect his reputation to be the next battle zone for these ever more desperate fanatics. Talk of preemptively impeaching him is already crackling through the Twitter channels. That will be an excellent sideshow.

Meanwhile, how is Rep, Adam Schiff’s secret proceeding going?

Last week he put out a narrative that US Chargé d’Affaires to Ukraine Bill Taylor fired a gun-that-smoked fer sure in testimony. Except, of course, as per Mr. Schiff’s usual practice, he refused to issue any actual transcript of the interview in evidence, while there are plenty of indications that Mr. Taylor’s second-hand gossip was roundly refuted under counter-questioning by the non-Jacobin minority members of the House intel Committee. Mr. Schiff’s pattern lo these many months of strife has been to claim ultimate proof of wrongdoing only to have it blow up in his face. It’s a face that many Americans are sick of seeing and hearing from, and I am serenely confident that before this colossal scandal is resolved, the Congressman from Hollywood will be fatally disgraced, as was his role-model, Senator Joseph McCarthy, before him.

Lebanon Bans Removal Of Large Dollar Sums From Country Amid Bank Run “Panic”

Eleven days into banks across Lebanon being shuttered due to mass anti-government corruption protests which have gripped the nation, in numbers estimated at one million people taking to the streets simultaneously (a stunning quarter of the population), authorities have just put a temporary ban on removing any large sum of physical dollar currency from out of the country.

The order was issued Sunday by Public Prosecutor Ghassan Oueidat who imposed the ban on all air and land borders, in effect “until the central bank determines a new mechanism for regulating such transfers.” Previously a customs permit was required to take large cash amounts out of the country, but there’s now concern that a potential run on the banks could crash the economy the moment they finally do open.

Finance Minister Fouad Siniora has been target of tax protests and anger over corruption in the popular protests. Image via AFP.

We reported last week that the country’s banking association claimed it was necessary for the banks to close due to “safety concerns”. The association has since been reportedly engaged in crisis meetings over how to preventa “panic mode” scramble on the part of the public to remove all deposits.

Over the course of the protests, which have been mostly peaceful but at times involved clashes with police and blockage of major roadways, banking operations have been “limited to paying out customer and employee salaries via ATMs” in a situation which has also hit war-torn Syria, given many Syrians rely on the neighboring Lebanese banking system to hold dollars and savings following the collapse of Syria’s currency.

It’s still unclear when banks will actually open, with the chairman of the Association of Banks in Lebanon saying last week that banks are to re-open “once normalcy is restored.”

The most potent case for cryptocurrencies: banks are never there when you need them. And they are trying to bully the public so they avoid accountability and profit disbursements.

Bankers are legal crooks.#bottomup#bitcoin#Lebanonhttps://t.co/Fp3QPFFkJQ

In recent years the country has suffered a severe slowdown in capital flows, and difficulty of importers securing dollars at the pegged exchange rate, as well as periodic collapse of public services – due to frequent strikes, work stoppages, and lack of public funding. As Reuters describes further:

Lebanon, where the Lebanese pound currency is pegged to the dollar, is one of the world’s most heavily indebted states.

Capital inflows needed to finance the state deficit and pay for imports have been slowing down, generating financial pressures not seen in decades, including the emergence of a parallel market for dollars.

At the heart of the crisis and of the protests is extreme lack of confidence in the local currency and corrupt officials which oversee the depleted system.

As Asia Timespointed out last week, “Lebanon’s credit rating was downgraded to junk in August, with the global ratings agency Fisk raising the possibility the Eastern Mediterranean nation could default on its debts.”

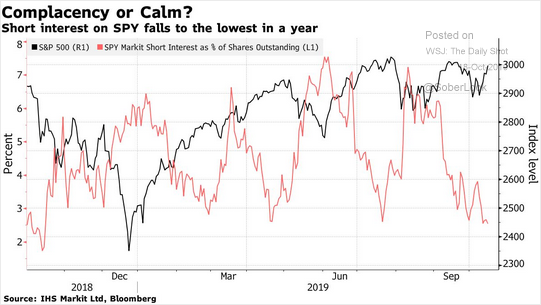

In a recent weekly newsletter (Subscribe for free e-delivery), I discussed the rather dramatic decline of short-interest in the S&P 500 which suggests a high degree of complacency by investors.

As Wolf Richter recently noted:

“Of the total shares outstanding of the SPDR S&P 500 ETF, only 2.6% were out on loan to short-sellers this week, the lowest since early October 2018, and down from 7% during the summer, according to IHS Markit data cited by Bloomberg. Meaning that short-sellers who want to short the entire market, and not specific companies, are worried that the market will break out, powered by a Brexit deal or a miraculous US-China trade deal as per presidential tweet, or whatever, and rip their faces off if they’re short the market.”

In other words, optimism about the “bull market” continuing is actually rather high, despite seemingly negative sentiment from headlines.

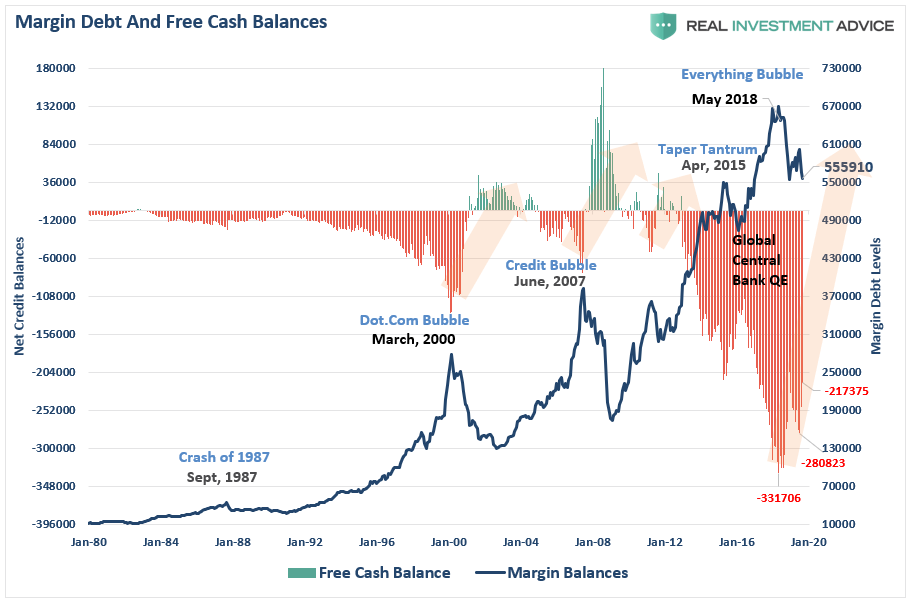

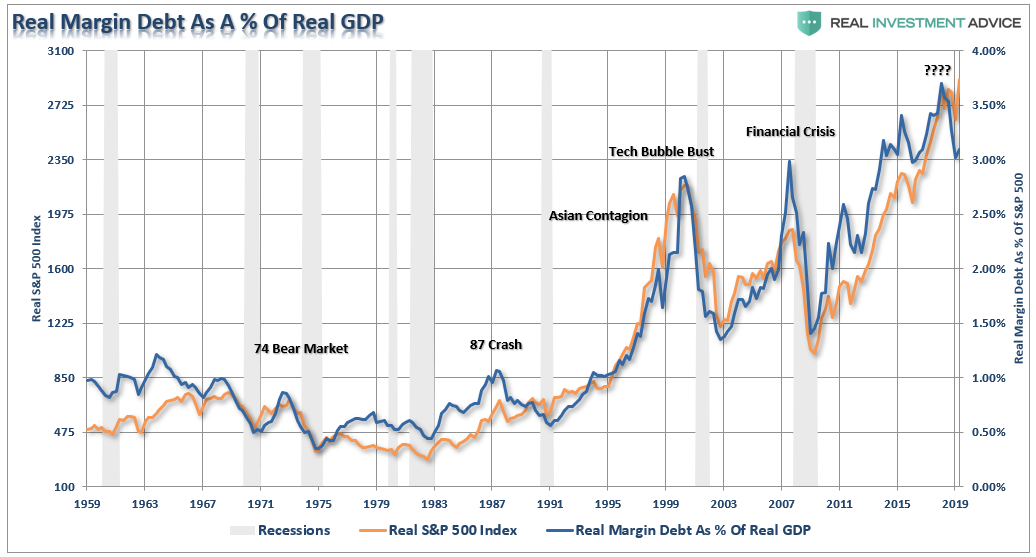

As Wolf goes on to note, short-sellers are “speculators” in the purest form. They are also leveraged investors who have been deleveraging as of late. The chart below shows margin debt as reported by FINRA, as compared to the “free cash balance” of investors.

You can see that since May 2018, the level of “negative cash balances” has improved as margin debt has declined. However, we need to keep this in perspective as even with the recent improvement, negative cash balances are still twice as high as any other point in history.

More importantly, note the events related to increases in margin debt. Clearly, a decade of ultra-low interest rates, ongoing liquidity infusions by Central Banks, and surging levels of stock buybacks have emboldened speculators to take on ever-increasing levels of “risk” through leverage.

This deleveraging process over the last year, combined with the sharp drop in “short interest,” suggests the speculative investors have become much more cautious on the market.

However, is this more negative positioning a contrarian signal for the markets?

Are The Bulls In The Clear?

Maybe not.

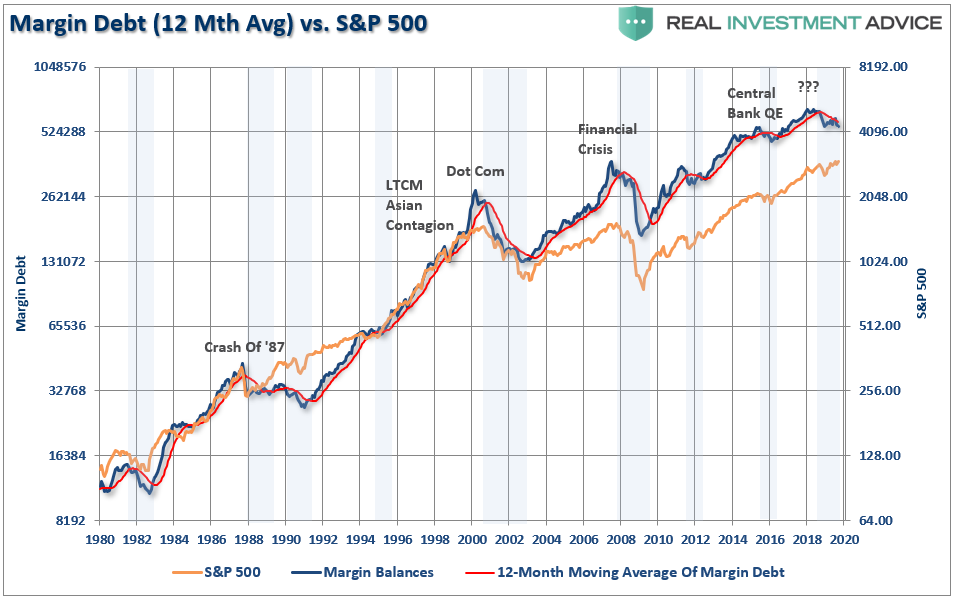

“According to research conducted in the 1970s by Norman Fosback, then the president of the Institute for Econometric Research, there is an 85% probability that a bull market is in progress when margin debt is above its 12-month moving average, in contrast to just a 41% probability when it’s below.”

Currently, margin debt has crossed below the 12- month average. If we take a longer-term look at the data we find that breaks of the 12-month moving average have indeed provided a decent signal to reduce equity risk in portfolios (blue highlights).Yes, as with any indicator, there are times that it doesn’t work, but more often than not, it has provided a reasonable assessment of elevated risk.

Importantly, margin debt is not a technical indicator which can be used to trade markets. Margin debt is just additional “gasoline” to lift asset prices higher as the leverage provides for additional purchasing power. However, “leverage” also works in reverse as it provides an accelerant for larger declines as lenders “force” the liquidation of assets to cover credit lines without regard to the borrower’s position.

That last sentence is the most important. The issue with margin debt, in particular, is that the unwinding of leverage is NOT at the investor’s discretion. It is at the discretion of the broker-dealers that extended the leverage in the first place. (In other words, if you don’t sell to cover, the broker-dealer will do it for you.)When lenders fear they may not be able to recoup their credit-lines, they force the borrower to either put in more cash or sell assets to cover the debt. The problem is that “margin calls” generally happen all at once as falling asset prices impact all lenders simultaneously.

Margin debt is NOT an issue – until it is.

It is when an “event” causes lenders to “panic” that margin becomes problematic. As I discussed previously:

“If such a decline triggers a 20% fall from the peak, which is around 2340 currently, broker-dealers are likely going to start tightening up margin requirements and requiring coverage of outstanding margin lines.

This is just a guess…it could be at any point at which ‘credit-risk’ becomes a concern. The critical point is that ‘when’ it occurs, it will start a ‘liquidation cycle’ as ‘margin calls’ trigger more selling, which leads to more margin calls. This cycle will continue until the liquidation process is complete.

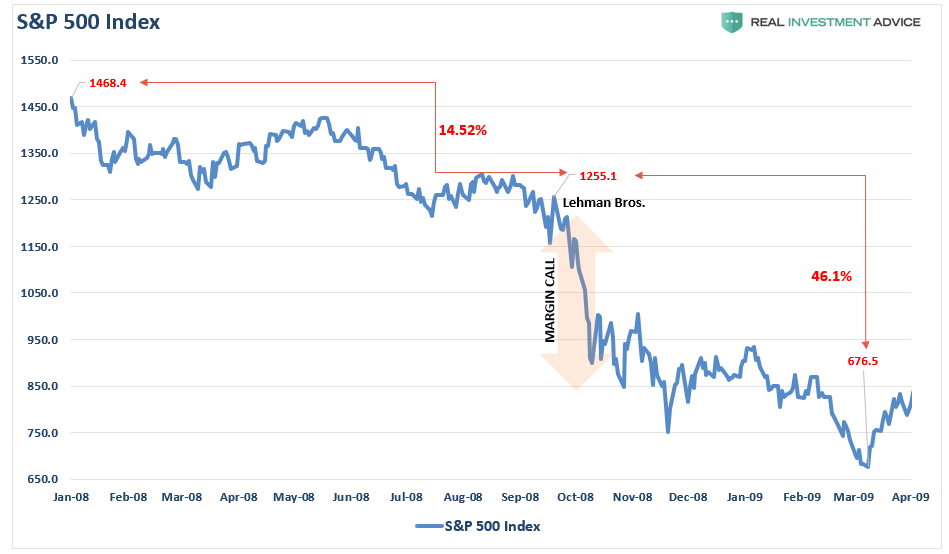

The last time we saw such an event was here:”

Note in the chart above the market had two declines early in 2008, which ‘reduced’ margin debt but did NOT trigger “margin calls.” The event which caused lenders to panic was when Lehman Brothers was forced into bankruptcy and concerns over counter-party risk caused banks to dramatically reduce their “risk exposure.”

We never know what the catalyst will be which forces lenders to become concerned about “default” risk, but there is more than sufficient leverage in the market, with deteriorating credit quality, to supply an “event.”

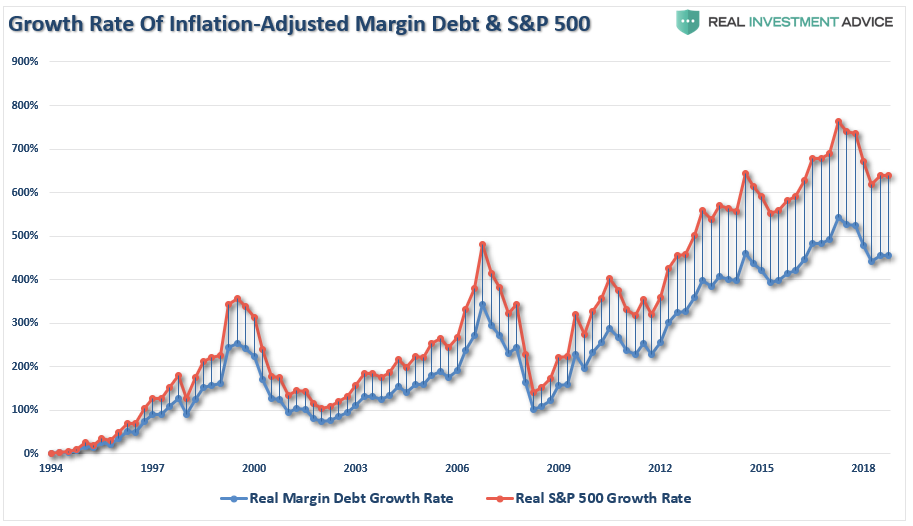

History, going back to 1959, also suggests the “bulls” should not be overly complacent with the modest pullback in “margin debt.”

While not always immediately coincident, there is a significant correlation between the growth rate in margin debt relative to the growth rate of the S&P 500 (both adjusted for inflation). Over the last year, the S&P 500 has struggled to make advances as margin debt growth has weakened.

Furthermore, if we look at real, inflation-adjusted margin debt as a percent of GDP, the declines have also been coincident with both weaker economic and market outcomes.

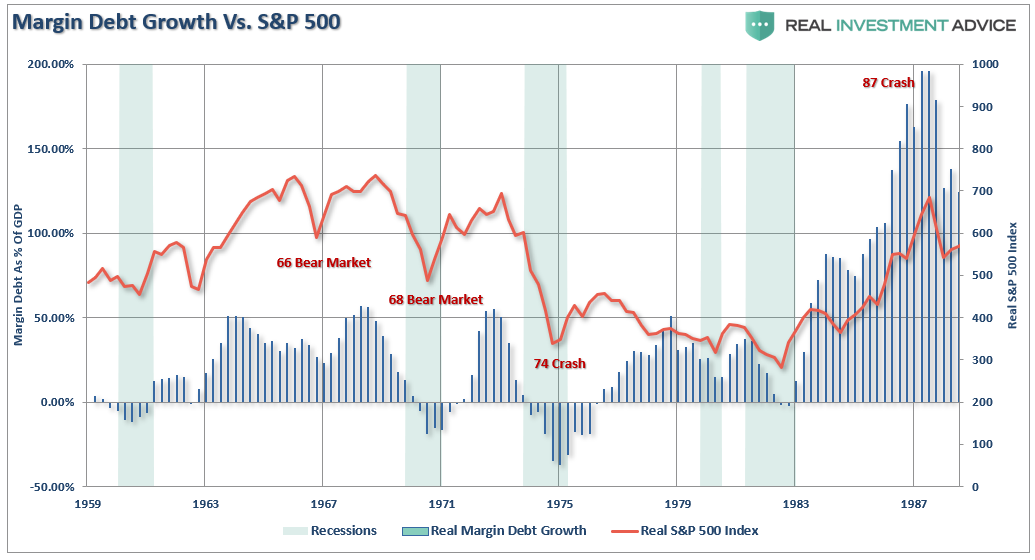

It is hard to see what was happening prior to 1980. The next chart shows margin debt growth from 1959-1987.

(Most people have forgotten there were three back-to-back bear markets in 1960’s-1970’s as interest rates were spiking higher. The 1974 bear market was the one that simply wiped everyone out!)

Again, what we find is a correlation between asset prices and margin debt. When margin growth occurs extremely quickly, which coincides with more extreme investor exuberance, corresponding unwinds of the debt have been brutal.

This time is not likely any different.

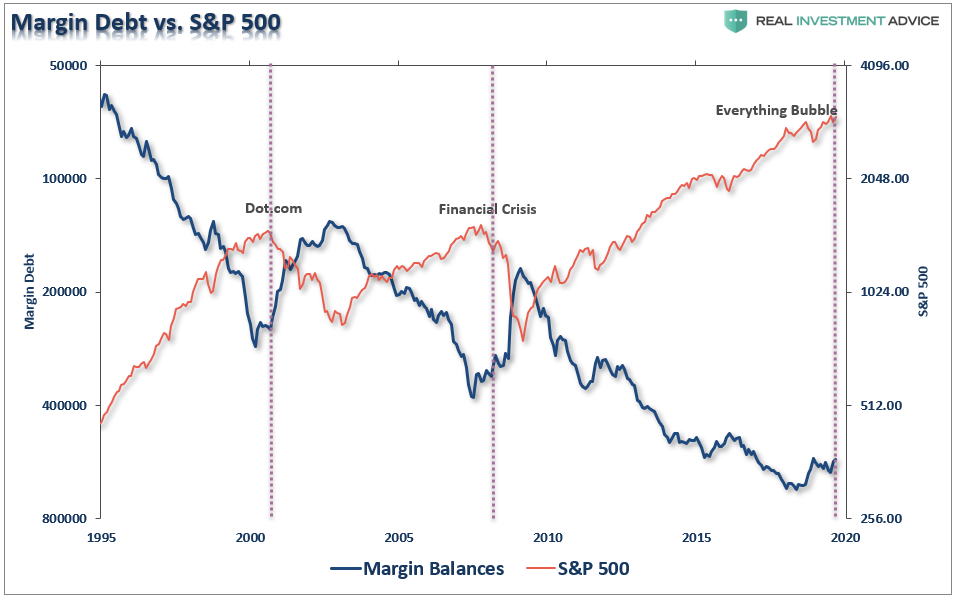

As shown, it is not uncommon for margin debt to start to unwind (margin debt inverted for clarity) before the bear market begins.

It’s All Coincident

When it comes to “margin debt,” it is a “coincident” indicator. Such should not be surprising since rising levels of margin debt are considered to be a measure of investor confidence. Investors are more willing to take out debt against investments when shares are rising, and they have more value in their portfolios to borrow against. However, the opposite is also true when falling asset prices reduce the amount of credit available and assets must be sold to bring the account back into balance.

I both agree and disagree with the idea that margin debt levels are simply a function of market activity and have no bearing on the outcome of the market.

By itself, margin debt is inert.

Investors can leverage their existing portfolios and increase buying power to participate in rising markets. While “this time could certainly be different,”the reality is that leverage of this magnitude is “gasoline waiting on a match.”

When an event eventually occurs, it creates a rush to liquidate holdings. The subsequent decline in prices finally reaches a point that triggers an initial round of margin calls. Since margin debt is a function of the value of the underlying “collateral,” the forced sale of assets will reduce the value of the collateral further triggering further margin calls. Those margin calls will trigger more selling forcing more margin calls, so forth and so on.

As I noted above, it will likely take a correction of more than 20%, or a “credit related” event, which sparks broker-dealer concerns about repayment of their credit lines. The risk to the market is “when” those “margin calls” are made.

It is not the rising level of debt that is the problem; it is the decline which marks peaks in both market and economic expansions.

Currently, the “bullish bias” remains intact, and the recent volatility in the market has not shaken investors loose as of yet. Therefore, it is certainly understandable why so many are suggesting you should ignore the recent drop in margin debt.

Trump Mulls Partial Video Release Of Baghdadi Raid

President Trump on Monday said he could release segments from a video recorded during a dramatic US raid which resulted in the suicide of ISIS founder and leader, Abu Bakr al-Baghdadi in Syria.

The ‘austere religious scholar‘ detonated an explosive vest after being cornered by US soldiers in a tunnel – killing himself and three children, and wounding a US military canine.

“We may take certain parts of it and release it,” Trump told reporters on departure from Washington to Chicago, according to AFP.

He died “like a dog,” Trump said in his comments, which differed sharply in tone from similar announcements by presidents in the past.

A report in The New York Times, quoting military and intelligence officials, cast doubt on some of Trump’s descriptions, including his repeated claim that Baghdadi was “whimpering and crying” in the tunnel. –AFP

In recent comments, Trump said the raid looked like “a movie,” however according to the NYT he wouldn’t have had access to real-time audio or video.

A senior Turkish official said Baghdadi had arrived at the site of the U.S. raid some 48 hours before it took place, adding that Turkey’s military – which has been waging its own offensive against Kurdish fighters in northern Syria – “had advance knowledge of the U.S. operation in Idlib.” Meanwhile, Newsweek, which first reported news of the raid, said it had been told by a U.S. Army official briefed on the raid that Baghdadi was dead.

Baghdadi led the Islamic State since 2010, when it was still an underground offshoot of al Qaeda in Iraq. Baghdadi had long been believed to be hiding somewhere along the Iraq-Syria border – evading justice despite a $25 million reward offered by the United States for his capture.

{kind=link}

{kind=link}