The phrase “mid-cycle adjustment” sent shudders through risk markets yesterday, during Powell’s press conference. Mid cycle! When corporate debt to GDP is at extremes, earnings growth slowing, and the US manufacturing sector close to contraction, this really does not look mid-cycle to us.

By delivering a 25bp insurance cut, the Fed actually tightened financial conditions for Main Street US, making subsequent easing more likely. The march higher of the USD is the main problem the Fed has to deal with. This has pushed our estimate of the neutral nominal Fed Funds rate much lower this year to under 1.4% and, with yesterday’s move, it could well fall further.

The Fed had many opportunities to reduce market expectations for an easing cycle, but did not take them. In so doing they have repeated the December 2018 hike error, wasting ammunition, and long term US rates will rightly continue to fall from here. For the first time under Trump’s leadership, we see value in long end Treasuries here, as a Fed policy-error trade (for example as a 2s30s flattener).

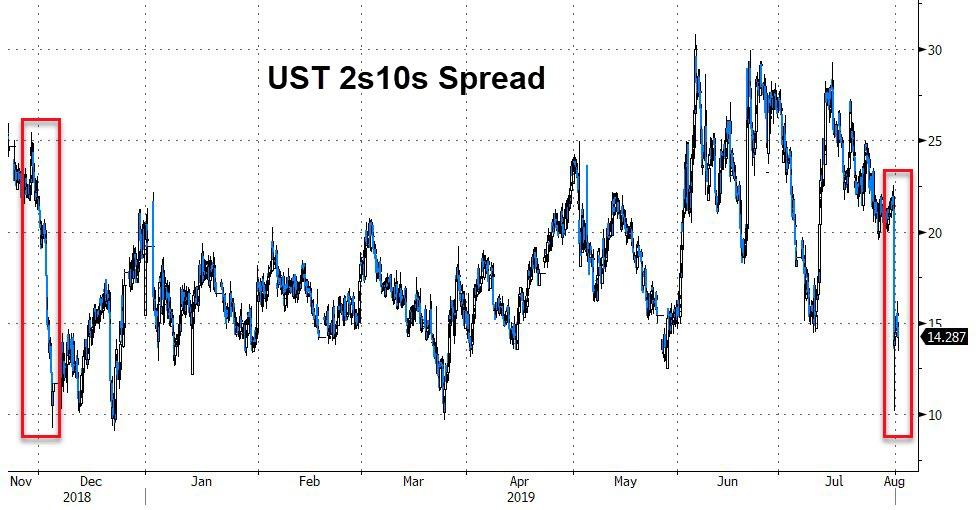

2s10s seems likely to invert in the near term, as the market digests the implications of a Fed which cut rates while simultaneously tightening financial conditions. Such a poor delivery of a cut puts the Fed closer to the zero lower bound, and therefore a liquidity trap. Inflation expectations should continue to fall in the US, and we would expect US corporate spreads and equities to see more selling flows.

Our conclusion is that the market will be proven correct- to prolong the cycle as the Fed is seeking, the Fed will need to ease further, by around 75bp from here just to reach neutral. Until then, expect long end Treasuries to be well bid, particularly as long-end carry just became a bit more favorable.

via ZeroHedge News https://ift.tt/2KeKEF0 Tyler Durden

MSNBC Host Joe Scarborough of MSNBC’s ‘Morning Joe’ complained in a tweet last night that the Democratic contenders onstage last night for Pt. 2 of the second Democratic debate spent more time attacking President Barack Obama’s policies than they spent attacking President Donald Trump.

He added that this is “politically stupid and crazy.”

These candidates are attacking Barack Obama’s policy positions more than Donald Trump. That is politically stupid and crazy.

Though Scarborough also inadvertently admitted something important: The Democratic Party of today isn’t the same party from 2016. Instead, even candidates who once believed themselves to be part of the mainstream have embraced policies that are much further to the left, largely thanks to the influence of “the Squad” and their fellow progressives, who have been gaining influence in Washington since the mid-terms.

Scarborough is probably also referring to the fact that Biden and Harris, the two front runners who participated in Wednesday night’s debate, were lightning rods for criticism. Bill de Blasio and others got into a huge debate with Biden over health-care reform, even prompting Biden to declare these criticisms of Obamacare “malarky”.

Biden was also attacked over the 800,000 deportations that occurred during the Obama Administration, which seemed to support the Trump Administration’s argument that Trump’s supposedly “draconian” border policies are merely a continuation of the Obama years.

While the “you’re playing into Republicans’ hands!” argument is certainly compelling to some, they should probably tell Scarborough not to say the quiet part out loud.

via ZeroHedge News https://ift.tt/2YAAUhs Tyler Durden

The Federal Reserve cut interest rates for the first time in over a decade Wednesday. And Jerome Powell left the door open for future cuts.

Peter Schiff broke it all down on his most recent podcast, saying this is the first interest rate cut on the short road to zero.

During his press conference after the FOMC meeting, Fed Chairman Jerome Power tried to straddle the fence. In the process, he ended up mixing his messages.

Powell called the 25 basis point cut a “mid-cycle adjustment.” When asked about future cuts, the Fed chair left that door propped open, saying “As the committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion.”

About midway through the Q&A session, Powell said the Fed wasn’t embarking on a long rate-cutting cycle like it would during a recession. But then he backtracked and sounded a little more dovish later on.

Let me be clear: what I said was it’s not the beginning of a long series of rate cuts. I didn’t say it’s just one or anything like that. When you think about rate-cutting cycles, they go on for a long time and the committee’s not seeing that.”

Of course, when the Fed pivoted to the “Powell Pause” last December, most analysts weren’t expecting a rate cut down the road. And here we are.

Peter Schiff predicted all of this. During his podcast, Peter called this the first step on the road to zero. And he said it was going to be a pretty short road.

Powell claimed the Fed was cutting rates as an insurance policy to ensure problems in the global economy don’t spill over into a healthy US economy. Peter called this a load of BS.

Either he is lying, or he’s a complete idiot. And I tend to believe its the former. And the reason he is lying is because if he told the truth, he would scare the sh** out of the markets.”

Peter reiterated something he’s been saying all along — a 25-basis point cut isn’t going to cut it. To underscore this point, he noted that the Dow fell over 300 points after the announcement. But Peter said Powell was right when he said this wasn’t the beginning of a long easing cycle. That’s because it won’t take long to get to zero.

It doesn’t have a lot of ammunition to cut rates, and so I think we’ll get to zero relatively quickly. And we’ll stay there until the Fed completely loses control of this thing.”

Keep in mind the last two times the Fed started cutting rates a recession quickly followed.

Peter said he thinks the stock market will continue to trend downward until the Fed significantly softens the position that it took yesterday.

He reiterated that it’s clear Powell is lying about this just being a temporary measure in a good economy.

The fact that there was so much contradictory statements made by Powell during this conference, I mean, it’s obvious that he’s lying, he’s making up excuses because he’s trying to pretend the economy is great, but he’s cutting rates anyway. So, he’s trying to defend, really, a ridiculous story. He contradicts himself. If you’re being honest, it’s easy not to contradict yourself because you just tell the truth. But when you’re lying, you weave a very tangled web. One lie contradicts another lie because you can’t keep your story straight. And that is the position he was in.”

Listen to the whole podcast for more analysis on the Fed’s latest move and what may lie ahead.

via ZeroHedge News https://ift.tt/2YgPdIJ Tyler Durden

World stocks and US index futures rebounded, even as the dollar charged to its highest in more than two years on Thursday after the Federal Reserve spoiled hopes of a run of U.S. interest rate cuts when Fed Chair Powell shocked when he said that the rate cut is a “mid-cycle adjustment” indicating it’s not the start of an extended series of cuts.

After the rate cut on Wednesday, Powell said in a press conference that the Fed’s quarter-point reduction amounted to a “mid-term policy adjustment.” Two Fed officials dissented to the decision, favoring no change. President Donald Trump said in a tweet “Powell let us down” with the size of the move.

While there was already a blizzard of global data and events going on, it was Fed Chair Jerome Powell’s remarks on Wednesday that set the markets running – literally – with the hour that contained Powell’s press conference seeing trading volumes explode to the highest level of the year; this is when Powell said the first U.S. rate cut in over a decade was “not the beginning of a long series of rate cuts” and the market tumbled.

Analyst hot takes on the Fed’s decision came hot and heavy: “That’s what a hawkish cut looks like,’’ Morgan Stanley analysts including Ellen Zentner wrote in a note to clients. “The minimal size of the cut, the dissents, and Powell’s press conference disappointed markets, and undercut our expectation.”

“We believe the Fed is trying to thread the needle, balancing market jitters about slowing global growth with robust consumer spending and a strong job market in the U.S.,” said Nick Maroutsos, co-head of global bonds at Janus Henderson. In other words, by cutting just 25 bps, the Fed is trying to bolster market confidence while also keeping some dry powder in reserve in case of an economic shock.”

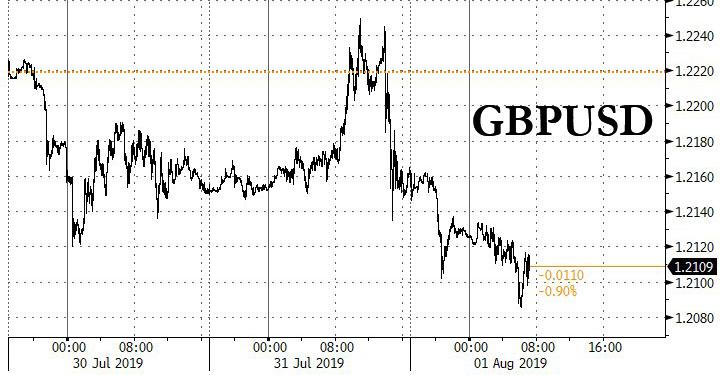

But it was the dollar’s reaction said it all: the DXY index surged to the highest in more than two years, euro/dollar dropped below $1.11 for the first time since May 2017, and Brexit-hobbled sterling hit 30-month lows just above $1.21. The Bloomberg dollar index jumped to the highest since 2018 as all bank clients who had been following short dollar trade recos were carted out feet first.

Ten-year Treasuries had rallied on Wednesday after the cut and when policy makers brought forward their plan to abandon the run-down in the bond portfolio.

“Markets interpreted the Fed’s communication as slightly hawkish and therefore further rate cuts in the immediate future were somewhat priced out,” said David Milleker, senior economic advisor at Union Investment. “And the dollar strengthened. All in all, the Fed did not achieve what it presumably wanted.” However, perhaps sensing that they had overreacted, world stocks rebounded modestly overnight as futures for all three main U.S. stock gauges nudged higher.

In Europe, the Stoxx Europe 600 Index rose 0.4% following a weak start, with financial services shares leading the rebound and banks also rising after upbeat results from the likes of Societe Generale and Barclays. Other top-performing European sectors included retail and telecom, while British American Tobacco, the top contributor in terms of index points, also extended its gain on better-than-expected earnings.

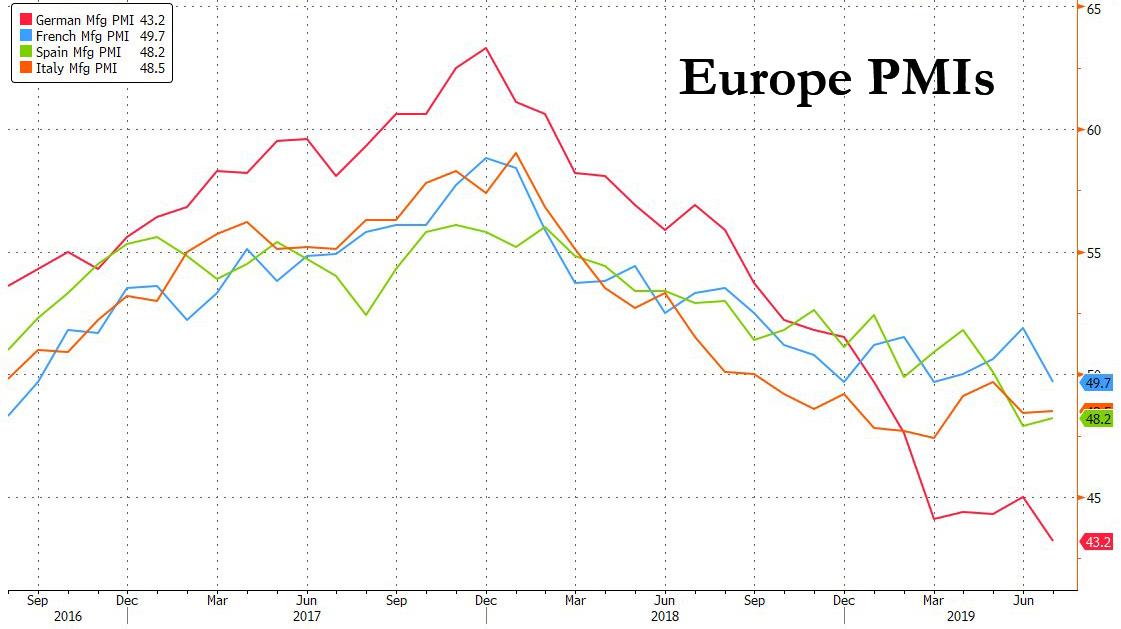

Most Asian equity gauges dropped earlier, though Japan’s benchmark recouped early losses as the yen slid. European bullishness was reinforced by disappointing European data, which saw the French manufacturing PMI slide back into contraction, while German Mfg PMI tumbled to a fresh multi-year low.

Europe reversed earlier losses in Asia where the MSCI index of Asian shares ex-Japan fell 0.8%, extending losses for a fifth day to the lowest since mid-June and posting its biggest one-day percentage drop in a month. The S&P BSE Sensex Index fell the most in the region, headed for its lowest level in five months on Thursday after completing its worst July in 17 years. Australian shares declined 0.4%. Losses by Chinese shares ended down 0.8%. Taiwan shares extended their losing streak to a fifth day as China imposed a ban on travel to the island. Japan stocks rebounded from early losses, helped by strong earnings at the country’s largest financial firms and a weakening in the yen. The nation’s banks and brokerages surged after Nomura and Mitsubishi UFJ reported large increases in quarterly profit.

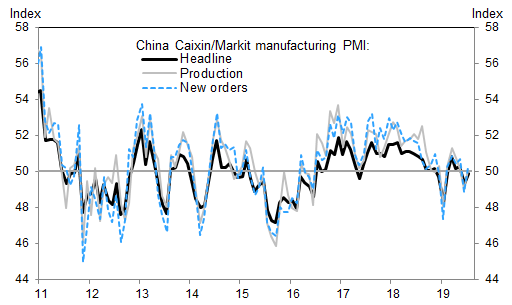

Downbeat data and factory surveys on Thursday had also pointed to further weakness for Asia’s trade-reliant economies. South Korea’s exports fell for an eighth straight month in July amid weak global demand and a dispute with Japan. New export orders shrank the most in about six years. South Korea, the world’s sixth-largest exporter, is the first major industrial economy to release trade data each month, providing an early assessment on the health of global demand. Pressure on Chinese factories eased slightly, but manufacturing activity continued to shrink according to the Caixin PMI which printed in contraction if modestly better than expected.

Specifically, China’s Caixin manufacturing PMI came in at 49.9 in July, above market expectations and also higher than June’s reading. The production sub-index increased by 1.1pp to 50.1, and the new orders sub-index went up to 50.2 from 48.8. Inventory indicators suggest a destocking trend — the raw material inventories sub-index was 0.4pp lower at 49.8, and the finished goods inventory index fell 0.7pp to 48.5. Employment growth deteriorated further — the employment sub-index was 0.3pp lower at 48.7, the lowest reading since February 2019.

“The broader global trade dynamic remains a challenge,” Morgan Stanley strategist Michael Zezas said. “Trade should continue to drag on corporate confidence, capex and global growth in the near term.”

U.S. Treasuries were sold off as investors scaled back their pre-Fed expectations for at least 100 basis points of cuts in the near term. Yields on 10-year notes climbed as high as 2.058% in Europe from a U.S. close of 2.007%, before recovering some of the losses. Core euro zone bond yields were rising, too, although -0.428% German Bund levels were still extraordinary.

Elsewhere in FX, as noted earlier the pound weakened, dropping below 1.21 and resuming its recent losing streak and staying lower as the Bank of England kept interest rates unchanged. Gilts pared a small gain. “Sterling remains vulnerable to a further escalation in Brexit tensions and we anticipate the market will likely discount higher risks of a ‘no deal’ outcome in the weeks ahead,” said Roger Hallam, currency chief investment officer at J.P. Morgan Asset Management.

Elsewhere, the Aussie dollar slipped below key chart support of $0.6832 to as low as $0.6828, a level not seen since an early January “flash crash”. The kiwi hit a six-week trough of $0.6535 on expectations the Reserve Bank of New Zealand will cut rates next week.

The Chinese yuan weakened to its lowest level in six weeks, slipping below 6.9 against a strengthening greenback. The onshore yuan fell to as low as 6.9150 per dollar on Thursday, the lowest since June 18, before paring the decline. “The Fed was less dovish than expected, so the dollar rebounded strongly across the board and against the yuan,” said Stephen Chiu, FX and rates strategist at Bloomberg Intelligence, adding that the yuan was expected to remain steady against the greenback in the near term while advancing against a basket of trading partners’ currencies. The People’s Bank of China set its daily yuan fix 0.14% weaker than Wednesday, but at a level stronger than 6.9 per dollar, which was considered its line in the sand for the currency. “I think the yuan will hover around the current level for a while, 6.85 to 6.95 for now,” said Tommy Xie, an economist at Oversea-Chinese Banking Corp. in Singapore. The PBOC is not likely to follow the Fed with a cut of its own, he added.

In commodities, U.S. crude futures fell 76 cents to $57.82 per barrel after comments on the rate outlook. Brent was down 71 cents at $64.34. Spot gold also fell, to $1,405.26.

With the Fed out of the way, and with traders now departing for their summer vacations, investors will continue to keep an eye on the ongoing earnings season amid even more abysmal liquidity, as well as Friday’s U.S. jobs data and trade developments. American and Chinese negotiators plan to meet again in early September, after the latest round of talks ended with few signs of concrete progress.

Expected data include jobless claims and PMI readings. Verizon, Veon and U.S. Steel are among companies reporting earnings

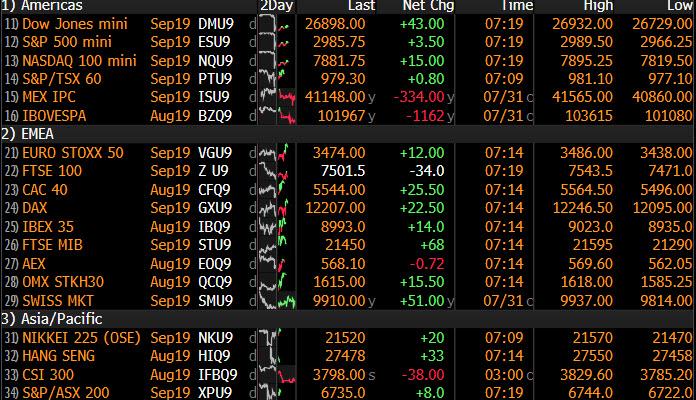

Market Snapshot

S&P 500 futures up little changed at 2,982.75

STOXX Europe 600 up 0.02% to 385.85

MXAP down 0.6% to 157.47

MXAPJ down 0.8% to 514.77

Nikkei up 0.09% to 21,540.99

Topix up 0.1% to 1,567.35

Hang Seng Index down 0.8% to 27,565.70

Shanghai Composite down 0.8% to 2,908.77

Sensex down 1.5% to 36,904.26

Australia S&P/ASX 200 down 0.4% to 6,788.93

Kospi down 0.4% to 2,017.34

German 10Y yield rose 2.1 bps to -0.419%

Euro down 0.3% to $1.1045

Brent Futures down 1.2% to $64.26/bbl

Italian 10Y yield fell 11.8 bps to 1.19%

Spanish 10Y yield rose 3.7 bps to 0.321%

Brent Futures down 1.1% to $64.45/bbl

Gold spot down 0.6% to $1,405.70

U.S. Dollar Index up 0.3% to 98.82

Top Overnight News from Bloomberg

Fed’s Powell hearkened back to the central bank’s 1990’s policy successes by suggesting he can sustain the record long U.S. economic expansion with just a modest reduction in interest rates. He said the cut this week shouldn’t be seen as a signal for extended easing

Manufacturing in the euro area shrank for a sixth month at the start of the third quarter, dragged down by Germany’s worst slump in seven years. The downbeat figures come in the wake of reports showing slower economic growth in France, Spain and the euro area, with Italy stagnating

China’s central bank refrained from immediately following the U.S. Federal Reserve in cutting borrowing costs, signaling its preference to continue with the current targeted easing approach for now.

President Donald Trump said Federal Reserve Chairman Jerome Powell “let us down” by delivering an interest-rate cut that’s not aggressive enough to fight the trade and currency battles his administration is waging

U.S. and Chinese trade negotiators plan to meet again in early September, as the latest round of negotiations ended with few signs of concrete progress. Chinese State media hails ‘transition’ role of Shanghai talks

The Trump administration on Wednesday imposed sanctions against Iranian Foreign Minister Javad Zarif in a provocative move that diminishes the prospects for a diplomatic solution to rising tensions that have brought the U.S. and Tehran to the brink of war

Joe Biden faced an onslaught from across the Democratic debate stage as his opponents sought to cut down the party’s front-runner on health care, immigration, women’s issues and criminal justice

Barclays Plc Chief Executive Officer Jes Staley said the bank cut 3,000 jobs in the second quarter as the firm sought to keep a tight grip on expenses and counter criticism over its ability to reach profitability targets

London Stock Exchange Group Plc agreed to snap up Refinitiv in a $27 billion blockbuster deal, betting on a future dominated by data that will extend its reach beyond Europe

Asian stocks traded lacklustre as the region reacted to the FOMC meeting. ASX 200 (-0.3%) and Nikkei 225 (U/C) were lower with notable weakness seen in gold miners after the precious metal slumped post-FOMC, although downside in Australia’s broader market was limited by resilience in its largest weighted financials sector, while the Japanese benchmark briefly turned positive as it found solace from a weaker currency and amid a heavy slate of earnings. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (-0.8%) conformed to the downbeat picture after the PBoC skipped liquidity operations again and participants digested more PMI data in which Chinese Caixin Manufacturing PMI topped estimates but remained below the 50 benchmark level, while there was also increasing concerns regarding the Chinese military intervening in Hong Kong. Conversely, participants had their first opportunity to react to the more constructive tone struck between US and China in trade talks. Finally, 10yr JGBs were lower and tracked the weakness seen in USTs following the less dovish than expected Fed, with further pressure seen after the 10yr auction results which attracted weaker demand.

Top Asian News

Tax Haven Crackdown Catches Asia Hedge Funds in Its Crosshairs

China Encourages Tencent to Boost Cooperation with SOEs

Iron Ore Falls as Samarco Close to Regaining License

Betting Like SoftBank Drives Toyota’s Value Up by $19 Billion

European stocks have nursed the losses seen at the open [Eurostoxx 50 +0.4%] and are somewhat consolidating following the downside seen post-FOMC. Major bourses are mixed with the FTSE 100 (Unch) faring slightly worse as its oil giant Shell (-4.6%) fell to the foot of the Stoxx 600 as the Co’s profits plunged on lower oil prices. This, coupled with an uninspiring energy complex sees the EU energy sector significantly underperforming, whilst other sectors (ex-materials) are broadly in positive territory. Notable movers today are largely on the back of earnings, with Altice (+23.7%), Capita (+21.0%), SocGen (+4.5%) and Standard Chartered (+4.5%) all bolstered by optimistic numbers. On the flip side, Barclays (-3.2%) is hit on a profit miss, while Siemens (-4.3%) narrowed its EBITA forecast and now sees it at the lower end of the previously guided range. Miners also took a hit from the FOMC-triggered downside in the metals complex. Finally, a special dividend announcement from Rio Tinto (-2.4%) did little to support their share price this morning.

Top European News

European Manufacturing Slump Keeps Economy Under Pressure

U.K. Allocates Extra $2.6 Billion to Prepare for No-Deal Brexit

Polish Central Bank Boss Signals No Response to Inflation Shock

Russia to Grant Some Visas to U.S.-Embassy Backed Moscow School

In FX, the Dollar is broadly firmer in wake of the FOMC and relatively hawkish guidance to accompany the 25 bp ease. The decision to cut rates was not unanimous and Fed Chair Powell stressed that the move was different to previous policy loosening heralding the start of a lengthy cycle by framing the reduction as a mid-cycle adjustment, albeit adding that it is not necessarily a case of ‘one and done’. Nevertheless, the markets were hoping for more and the index rallied to a new 2019 peak at 98.941 before losing momentum ahead of Friday’s NFP that may be pivotal for the rest of the year in terms of policy action.

AUD/NZD/NOK/SEK – Relative outperformers or at least recovering some lost ground, as the Aussie found support near early Feb 2016 lows around 0.6827 vs its US counterpart and has subsequently bounced to 0.6850+, while the Kiwi rebounded from 0.6535 to reclaim 0.6560+ status. Elsewhere, the Scandi Crowns are both benefiting from technical retracements against the Euro and seemingly independent of contrasting manufacturing PMIs given a bad Norwegian miss and sub-50 print vs firmer than forecast Swedish headline that was only partly offset by less upbeat components. Indeed, Eur/Nok is back down below 9.8000 and Eur/Sek under 10.7000.

GBP/EUR/JPY/CAD/CHF – The Pound has also largely shrugged off a better than expected UK manufacturing PMI amidst ongoing and increasing no deal Brexit risk as output hit circa 7 year lows and attention shifts to BoE super Thursday and the prospect of a more dovish/downbeat tone to the MPC minutes, QIR and Governor Carney presser. Indeed, Cable has now lost grip of the 1.2100 handle and Eur/Gbp is eyeing 0.9130 ahead of high noon and the 12.30BST news conference – full preview available via the Research Suite and Headline Feed. Mixed Eurozone manufacturing surveys have not really impacted the single currency either as Eur/Usd hovers towards the base of a 1.1080-33 range, while the Yen has regrouped from 109.30 lows to probe resistance at 109.00 and hefty option expiry interest from the big figure to 109.10 in 2 bn. Elsewhere, the Loonie has handed back all and more of its post-Canadian GDP data gains and is looking at offers said to be stacked between 1.3230-40, with the Franc pivoting 0.9950 and 1.1000 against the Euro.

EM – Amidst pronounced depreciation vs the Greenback, Turkey’s Lira has bucked the trend on further positive follow through from the latest CBRT inflation report and outlook, with Usd/Try remaining south of 5.6000 and hardly reacting to a more contractionary manufacturing PMI. However, the Real may underperform after a bigger than anticipated 50 bp BCB rate cut from a 3.8130 close post-FOMC.

In commodities, the energy complex remains subdued in the after-math of the disappointing FOMC forward guidance issued yesterday. WTI and Brent futures have since traded sideways below 58.00/bbl and 64.50/bbl respectively with little by way of fresh catalysts. Looking at technical levels to the upside, WTI sees the psychological 58/bbl mark ahead of its 200 DMA at 58.09/bbl, meanwhile its Brent counterpart sees clean air (ex-psych levels) between 63.50-65.00/bbl. In terms of geopolitics, US announced sanctions on Iranian Foreign Minister Zarif during the back-end of the US session, albeit the news did little to sway oil prices. Elsewhere, the metal market remains under pressure from the FOMC fallout in which gold plummeted over 20/oz since the release. The yellow metal remains under pressure (albeit above the 1400/oz level) as the Dollar index hovers near YTD highs. Meanwhile, copper remains lacklustre and firmly below the 2.7/lb as the red metal holds onto the Powell-induced losses.

US Event Calendar

8:30am: Initial Jobless Claims, est. 214,000, prior 206,000; Continuing Claims, est. 1.67m, prior 1.68m

9:45am: Bloomberg Consumer Comfort, prior 63.7

9:45am: Markit US Manufacturing PMI, est. 50, prior 50

10am: ISM Manufacturing, est. 52, prior 51.7

10am: Construction Spending MoM, est. 0.3%, prior -0.8%

Wards Total Vehicle Sales, est. 16.9m, prior 17.3m

DB’s Jim Reid concludes the overnight wrap

So welcome to August with July ending with a bit of a bang for markets. Indeed yesterday’s Fed meeting was the obvious main event, and it certainly did not disappoint even if Mr Powell did for many. As we discussed yesterday the risk/reward set up isn’t great ahead of this easing cycle and last night showed us how difficult it’s going to be for central banks to keep up with market expectations.

The Fed did cut interest rates by 25bps as broadly expected, albeit with two dissents from regional Fed presidents. Equities fell, the yield curve flattened worryingly and the dollar strengthened. Initially the moves seemed to just be a mechanical reaction to the fact that the interest rate cut was 25bps instead of 50bps, given the market had priced in around a 16% chance for a larger move. However, the adverse moves accelerated during Chair Powell’s press conference after he characterised the move as “a mid-cycle adjustment to policy” and said it was not “the beginning of a lengthy cutting cycle.”

The market certainly interpreted that as a signal of a hawkish cut, possibly with Powell signaling reduced odds for further cuts. The price moves across asset classes certainly seemed to be consistent with higher odds of a policy mistake. At one point during the presser, the S&P 500 and NASDAQ were down as much as -1.83% and -1.98%, respectively, while two-year yields rose as much as +11.5bps (+15bps from just before the announcement), taking the 2y10y yield curve -10.8bps flatter to 10.2bps at one point.

The curve ultimately ended -7.1bps flatter at 13.9bps (14.9bps this morning), the lowest level since May and towards to bottom of the YTD range. Ten-year yields rallied to end -4.7bps lower (but are up +2.1bps this morning), while two-year yields moderated to close +2.2bps higher (are up a further +1.4bps this morning). This flattening was in contrast to the +9.1bps of steepening that occurred after the June Fed meeting, when the FOMC signaled the impending rate cut with the curve hitting a seven month high of around +29bps. As a reminder I place a high degree of weight on the 2s10s curve when trying to work out where in the US cycle we are. With us almost getting back into single digits at one point last night we’re no more than a few bad days away from inverting. This for me is the biggest worry from last night.

In the end, the S&P 500 declined -1.10%, which was the worst day for the index since 31 May. The NASDAQ and DOW ultimately closed -1.19% and -1.23%, respectively, as well. The dollar rallied +0.58% to its strongest level in over two years. President Trump tweeted after markets closed that “Powell let us down” because “what the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle.” There was no immediate reaction to the tweet, but is certainly raises the political heat on the Fed.

Even before that tweet, Powell seemed to be feeling the heat and used his final comments to specifically address and reframe his earlier remarks which had driven the selloff. He clarified that “I didn’t say it’s just one (cut) or anything like that (…) what I said was it’s not a long cutting cycle, in other words, referring to what we do when there’s a recession or a very severe downturn. That’s really what I was ruling out.” So he tried to emphasize that the FOMC does not expect a recession or a downturn, but that they are ready to cut rates more than once as needed. He also referred one reporter to look at history for prior examples of “mid-cycle adjustments,” tacitly signaling that he views the current environment as similar to the 1995 and 1998 episodes, when the Fed cut rates 75bps each time. So a bit of a mixed message with the market a bit confused. However the reality is that it had probably gone over its skis a bit in expectations.

To recap the Fed’s actual policy statement, which came with two dissents from Kansas City’s George and Boston’s Rosengren, the only major additions were a reference to “global developments” and a new comment saying that the Committee will “contemplate the future path of the target range for the federal funds rate.” The statement still said that they “will act as appropriate to sustain the expansion.” The Fed also opted to end its balance sheet runoff effective today, rather than the end of September as originally planned, though this move will have only a marginal impact on markets.

Before the Fed decision, a pretty bad MNI Chicago PMI for July did help to justify the Fed’s decision to cut. The index fell to 44.4 (vs. 51.0 expected), the lowest reading since December 2015. Before that, every single one of the 68 instances of a Chicago PMI at or below the 44.4 level over the last 50 years has been associated with a recession. The index was this low in mid-1967 without prompting a recession, however. On an ISM-adjusted basis, the index fell -4.5pts to 47.5, and the details were broadly weak as well. The production and employment components were both the weakest since 2009 at 41.4 and 42.9, respectively. The print presents downside risks to today’s ISM manufacturing report, as well as tomorrow’s jobs report.

With the ongoing uncertainty over global trade being a major factor behind yesterday’s rate cut, it’s worth noting that the latest round of trade talks between the US and China finished yesterday. A White House statement following the talks described the meetings as “constructive”, and said that the discussions included “forced technology transfer, intellectual property rights, services, non-tariff barriers, and agriculture.” Regarding future talks, it said they “expect negotiations on an enforceable trade deal to continue in Washington, D.C., in early September,” though staff-level discussions will continue in August. So this won’t get resolved soon but at this stage it’s a positive that they’ve agreed to meet again. In the meantime we are obviously susceptible to a Trump tweet on the matter.

Again on the theme of the lower interest rate world, it was interesting that the FT reported yesterday that UBS have decided to pass on negative interest rates to its wealthy clients as banks start to appreciate that low or negative rates are not going to be the temporary phenomenon they had previously thought. In itself, it might not be a big deal but it may mark the start of a period where banks try to pass on more of the cost of central bank’s policies. What depositors do on this will be interesting. To exaggerate, if I have 100 units with a bank and I’m going to see this erode in value now I can either hoard cash (after recent building works I won’t need a big mattress), buy assets (risky), spend more as why bother to save (a bit extreme), or accept a steady reduction in my wealth, be grumpy and maybe save more to compensate. I haven’t got my head around which theme will dominate if this practise become more widespread.

Overnight in Asia markets are following Wall Street’s lead with the exception of Japan which is making modest gains (after paring early losses) on a weaker Japanese yen (-0.39% this morning). Other than that, the Hang Seng (-0.68%), Shanghai Comp (-0.78%) and Kospi (-0.18%) are all down. Elsewhere, futures on the S&P 500 are up a marginal +0.04%. The US dollar has continued to strengthen with the index being up +0.33% this morning after advancing +0.48% yesterday. In terms of overnight data releases, China’s Caixin manufacturing PMI surprised on the upside at 49.9 (vs. 49.5 expected). The accompanying statement suggested that new export orders stayed in contractionary territory but saw a rise while components of output and new orders returned to expansion. A slightly better message than yesterday’s official PMIs. Elsewhere Japan’s final July manufacturing PMI came in two-tenths lower than the initial read at 49.4 (vs. 49.3 last month).

In other overnight news, Bloomberg has reported that the Bank of Korea Governor Lee Ju-yeol considers “Japan’s recent export restrictions against South Korea are a big risk,” while adding that Japan may decide as early as this week to take South Korea off the “white list” of nations it deems to be safe buyers of sensitive materials. If Japan goes ahead with the move then it is likely to affect South Korea’s automobile, steel, aviation and electronics industries. The foreign ministers of both nations are meeting today in Bangkok after the US urged them to calm rising trade tensions that are threatening global supply lines. Meanwhile, here in the UK, the government has doubled spending to £4.2bn on no-deal Brexit preparations this financial year while bringing the total cash allocated to £6.3bn. For this, the Chancellor of the Exchequer Sajid Javid has set aside £2.1 bn of new cash including an immediate £1.1bn pounds to improve key border and customs infrastructure and ensure access to critical medical supplies. The remainder will be made available to government departments if needed.

Ahead of the Fed, the main story in European markets yesterday were the new record lows for sovereign bond yields. 10-year bunds fell -4.0bps to an all-time closing low of -0.440%, and now comfortably below the ECB’s deposit rate of -40bps. It was the same direction for French 10-year debt, down -4.3bps to close at -0.184%. And perhaps most eye watering of all, Swiss 10-year yields fell -3.0bps to close at -0.805%. Even 30-year Swiss debt now trades at a yield of -0.186bps and the longest bond, maturing in 2064, now yields -0.081%. Equities were mixed, with the STOXX 600 up +0.17%, with the DAX (+0.34%), CAC 40 (+0.14%) and the FTSE MIB (+0.56%) all making gains before the FOMC. Once again the FTSE 100 was the outlier, falling -0.78%, as it traded inversely to a rallying sterling.

The moves in Europe came as GDP figures confirmed the ongoing slowdown in the Eurozone economy, with Q2 growth of +0.2% (as expected), down from +0.4% in Q1. The decline in Q2 growth brings the yoy growth rate to +1.1%, the lowest since Q4 2013. Separately, inflation readings showed Eurozone CPI fell to +1.1% in July, the lowest since February 2018, while core inflation fell to +0.9% (vs. +1.0% expected). In terms of the country details we got yesterday, growth in Spain was at +0.5% (vs. +0.6% expected), which was the slowest quarterly growth there since Q2 2014. Italy saw growth come in above expectations however, with a flat 0.0% reading in Q2 (vs. -0.1% contraction expected), and unemployment in the country fell to 9.7%, the lowest since January 2012. Nevertheless, Italian inflation data showed HICP at +0.4% in July (vs. +0.5% expected), the lowest since November 2016. In spite of the lower than expected inflation readings, Euro five-year forward five-year inflation swaps ended the session up +2.5bps.

Continuing the big week for central banks, having already heard from the BoJ and the Fed, the Bank of England’s MPC will be making their latest policy decision today, and we’ll also have the release of the Bank’s quarterly inflation report and a press conference from Governor Carney. In their preview last Friday (link here ) our UK economists wrote that although they expect the MPC will vote to keep Bank Rate on hold, they think that they will drop their tightening bias, “with the MPC becoming more sensitive to a deteriorating economic outlook vis-à-vis the ongoing trade wars and an increasing risk of a no deal Brexit.” Since the MPC’s last meeting of course, sterling has weakened noticeably, although yesterday it was the best-performing G10 currency versus the dollar, trading flat despite broad strength for the greenback.

Wrapping up, in terms of other data yesterday in the US, the ADP Employment Change said that 156k jobs had been added in July (vs. 150k expected), while June’s reading was revised up by +10k. Although better than expected, this brought the 3-month moving average down to its lowest level since 2010. Elsewhere, the employment cost index for Q2 was +0.6% (vs. 0.7% expected).

Looking to the day ahead, the Bank of England will be announcing its latest monetary policy decision, with Governor Carney giving a press conference afterwards. In terms of data, the manufacturing PMIs will be the highlights, with Italy, France, Germany, the Eurozone and the UK all reporting this morning, before the US in the afternoon. From the US, there’ll also be the July ISM manufacturing data as well as June construction spending. Earnings releases today include Royal Dutch Shell, Barclays, Verizon Communications, General Motors, Rio Tinto and Siemens, and in the UK, there’s a parliamentary by-election taking place which will have implications for the new PM with his majority at risk of dropping to two.

via ZeroHedge News https://ift.tt/2ZmLyWt Tyler Durden

Wednesday night’s Democratic debate Pt. II allowed a smattering of underdog candidates a chance to try and raise their profile by taking shots at two of the race’s frontrunners – Vice President Joe Biden and Sen. Kamala Harris.

But it was Joe Biden who took the most heat Wednesday night, taking fire from all sides regarding his record on abortion rights, crime and immigration. Many also questioned whether a candidate like Biden, who is out of touch with progressive base voters who favor an agenda set by the “Squad,” could successfully mobilize the base and boost turnout.

Biden and Harris led in terms of speaking time, with the vice president commanding 20 whole minutes (while Harris came in second with 17.7 minutes).

The night’s most-tweeted moment was this exchange between Sen. Cory Booker and Biden, where Booker accused Biden of hypocrisy after the VP questioned Booker’s embrace of tough-on-crime policing tactics like stop-and-frisk, as well as the hiring of a former Giuliani advisor during his time as mayor of Newark.

Of course, Biden’s record involves helping write the controversial 1994 crime bill that dramatically widened sentencing disparities between black and white inmates.

“If you want to compare records, and I’m shocked that you do, I’m happy to do that,” Booker said to Biden Wednesday.

Another widely discussed moment from the debate on Twitter was this exchange between Rep. Tulsi Gabbard and Sen. Harris, where Gabbard took Harris to task for jailing thousands of offenders for low-level marijuana-relaed offenses: “I’m concerned about this record of Senator Harris. She put over 1,500 people in jail for marijuana violations and laughed about it when she was asked if she ever smoked marijuana.”

But perhaps the most embarrassing moment of the night for either frontrunner was this gaffe involving Biden, where the former vice president during his closing statement told viewers “If you agree with me, go to Joe 30330 and help me in this fight.” However, that site didn’t exist, and viewers soon concluded that Biden had meant to say “Text JOE to 30330.”

Joe Biden ended his debate night with a viral gaffe. He stared straight into the camera and said: “If you agree with me, go to Joe 30330 and help me in this fight.” Cue immediate confusion. (Viewers concluded Biden meant to tell his supporters to text his name to the number.) pic.twitter.com/vsYm4eHkgG

But rival campaigns were quick to strike: Domains like ‘www.joe30330.com‘ were soon redirecting people to Buttigieg’s campaign site.

Another one of the most tweeted moments from last night’s debate came courtesy of Sen. Kirsten Gillibrand, who said that “the first thing I’m going to do when I’m president is I’m going to Clorox the Oval Office.”

Those were the top moments according to Twitter. And while Harris and Biden, the two leading candidates in the debate, were busy defending more centrist positions like private health care and keeping border-crossing illegal, critics and left-wing media personalities alike soon noted that the tone of the Democratic debates is moving increasingly leftward.

CNN’s Chris Cuomo notes that the Democrat presidential candidates do not represent the party’s voters:

“In the party … 8 of 10 say, ‘We are center left, not far-left.’ … that’s not what you are getting on these debate stages” pic.twitter.com/hhPtQAJo90

With the pound tumbling below 1.21 ahead of today’s BOE announcement, traders indicated a virtual certainty that the central bank would be dovish, and why not when even the Fed had cut rate less than 24 hour earlier. So it was perhaps a modest surprise – even if the outcome was as consensus expected – that the BOE did not cut rates, and instead voted unanimously to keep rates at 0.75% and to keep asset purchases unchanged, while noting that it is less confident than usual about the outlook for the economy because of Brexit while offering little new insight into the impact of how it would react to a “no deal” outcome.

Specifically, when it comes to its view on Brexit, the MPC specifically excluded the possibility of no deal, assuming a smooth Brexit and reiterated that interest rates will need to gradually rise to bring inflation to target. while noting that evidence suggests that uncertainty over the UK’s future trading relationship with the EU has become more entrenched.

Among its other underlying assumptions of projections, the BOE’s MPC notes that projections are impacted by an inconsistency between the Bank’s smooth Brexit assumption underpinning the forecasts and the prevailing market asset prices on which the forecasts are also conditioned.

On rates, the BOE maintained the view that on the basis of the assumption of a smooth Brexit and some recovery in global growth (new inclusion), the MPC continues to judge that increases in interest rates, at a gradual pace and to a limited extent, would be appropriate to return inflation sustainably to the 2% target. The response to Brexit, whatever form it takes, will not be automatic and could be in either direction

On domestic growth, the BOE maintained the view that Q2 growth is expected to be flat. On the basis of current Brexit assumptions, underlying output growth is expected to be subdued in the near-term. Thereafter, GDP is expected to accelerate to robust growth rates as Brexit-related uncertainties dissipate.

On Global Growth, the BOE noted that global trade tensions have intensified since May and global activity remains soft

On inflation, after falling in the near-term, CPI is expected to rise above the 2% target, with CPI to reach 2.4% by the end of the three-year forecast period.

On labor/wages, the central bank said that the Labur market remains tight and annual pay growth has been relatively strong

These comments were the bank’s first since Boris Johnson became prime minster on a mission to leave the European Union on Oct. 31 with or without new trading arrangements in place. If there’s no deal, the BOE merely noted again that the pound will fall, inflation will accelerate and growth will slow.

While that BOE’s non-committal forecast and lack of Brexit discussion meant Governor Mark Carney avoids a political headache, it disappointed others who are looking for more clues as to how the BOE might respond to no deal.

That communications problem has dogged the governor for some time. To account for the market currently pricing in a rate cut because of the greater chance of a bumpy departure from the EU, the BOE gave some stylized forecasts based on higher pound and interest rates. They show much slower inflation than the central scenario.

“The increased uncertainty about the nature of EU withdrawal meant that the economy could follow a wide range of paths over coming years,” the BOE said. “The appropriate path of monetary policy would depend on the balance of the effects of Brexit on demand, supply and exchange rate.”

Meanwhile, as Brexit keeps the BOE in wait-and-see mode, the world’s biggest central banks are turning dovish as global growth cools and trade tensions persist. The Federal Reserve on Wednesday delivered a quarter-point cut and suggested there’s more to come. The European Central Bank is looking at adding more stimulus as early as September.

Acknowledging the weaker global backdrop, the BOE lowered its forecast for economic growth this year, sees slower export growth and weak business investment persisting into 2020. In the stylized forecasts, one quarter-point rate hike over the next three years brings inflation below the 2% target. That compares with a central forecast, based on the market’s expectation of a quarter-point cut, for inflation to pick up to 2.4%. The forecast also sees excess demand at a whopping 1.75%. As Bloomberg notes, in normal circumstances, that would imply that the BOE should be raising rates soon. But given the uncertainty around Brexit, all nine policy makers deemed the current stance appropriate.

With cable having collapsed by a record amount heading into today’s decision, the pound barely moved after the announcement of the decision not to cut rates.

via ZeroHedge News https://ift.tt/3360SZw Tyler Durden

Given the rising tension in the Strait of Hormuz, and the mysterious spate of seemingly random attacks on tankers that some have blamed on Iran, it’s no surprise that more captains transporting shipments of crude and LNG through one of the busiest corridors for the global energy trade feel the need to keep a low profile, according to Bloomberg.

Which is apparently why more ships are turning off their transponders – “going dark”, in industry jargon – a technique that is typically used by smugglers and those hoping to avoid American sanctions.

But this time, ships are going dark mostly as a precaution. Following a buildup of military personnel in the region, most carriers fear the prospects of open war between Iran and a coalition of the Americans and the Saudis, or at the very least, more sporadic attacks on vessels that are still simply trying to scratch out a living.

In at least one way, the fact that ships are “going dark” is ironic: Because Iranian ships pioneered the technique while trying to bypass the American sanctions regime.

Copying from Iran’s own playbook, at least 20 ships turned off their transponders while passing through the strait this month, tanker-tracking data compiled by Bloomberg show. Others appear to have slightly altered their routes once inside the Persian Gulf, sailing closer than usual to Saudi Arabia’s coast en route to ports in Kuwait or Iraq.

Some ships are also trying out new routes that involve spending less time, or no time, in Iran’s territorial waters.

Before the latest increase in tensions with Iran, ships were more consistent about signaling their positions as they passed through a waterway that handles a third of seaborne petroleum. Once inside the Gulf, shipping routes took them fairly close to the Iranian coast, skirting the offshore South Pars/North gas field shared by Iran and Qatar. Most still do, but a growing number appear to be trying something new.

It’s little surprise that ships are doing everything possible to minimize risk. The Gulf region has witnessed a spate of vessel attacks, tanker seizures and drone shoot-downs since May, all against the backdrop of U.S. sanctions aimed at crippling Iran. War-risk insurance soared for tanker owners seeking to load cargoes in the region.

Two British warships are now stationed in the region, and stand ready to assist tankers flagged for Britain. The Norwegian Maritime Authority recently warned its vessels to avoid taking unnecessary risks by minimizing transit time in Iran’s territorial waters. All of this is making tanker captains increasingly nervous about the risks of getting caught in the crossfire between Iran and the US, and some ships have been looking at alternate routes that don’t involve going anywhere near the Strait.

By Bloomberg‘s count, at least 12 tankers loaded in Saudi Arabia and shut off their transponders while passing through the strait within the past month, including the supertanker Kahla, which turned off its transponder on July 20 before passing through the strait. At least eight vessels that loaded in Iraq and Kuwait went dark while leaving the Strait of Hormuz. A vessel shipping from the UAE also dropped off tracking systems.

And as long as tankers keep getting attacked, or captured, expect this trend to continue.

via ZeroHedge News https://ift.tt/2OAutY2 Tyler Durden

Despite termination of the Intermediate-Range Nuclear Forces (INF) Treaty soon, deployment of new missiles is unlikely but a disrupted security environment may give rise to provocative incidents “inviting” Russia to “partake.”

Given that there is a low probability that the US will change its stance of issuing ultimatums to Russia, the treaty will be terminated in August.

Although the INF didn’t reflect the current global order as it applied only to the US and the successor states of the Soviet Union, European nations perceived it as a security guarantee against dangerous military buildups on their soil. Hence, its ripples may affect Europe.

However, the development and deployment of ground-launched ballistic and cruise missiles with ranges of 500-5500km is ruled out in the short-term.

And here are the reasons…

Potential reluctance of the energy dependent European countries

According to data from Eurostat, the EU’s statistical office, in 2018 Russia was the largest supplier of natural gas and petroleum oils to the EU with a 40.2% and 27.3% share respectively. Moreover, in 9 NATO member states (Bulgaria, Czech Republic, Estonia, Latvia, Hungary, Poland, Romania, Slovenia, and Slovakia) Russia’s share of total national imports of natural gas was reportedly more than 75%.

The NATO states, that have been “entrusted” to play a key role in “countering” Russia, such as Poland, Bulgaria, Romania, and the Baltic nations, are in varying degrees dependent from it.

According to Gazprom, 9,861bcm of natural gas was sold to Poland in 2018. The Polish state-controlled oil and natural gas company PGNiG may continue to import Russian gas until 2022 under the Yamal contract with Gazprom.

Although Bulgaria has planned to diversify its supply routes by importing LNG and Caspian gas, Russia has served as the sole exporter of natural gas to the country. Bulgaria has also played a key role in transit of Russian gas. Furthermore, as the President of Bulgaria Rumen Radev mentioned recently during the plenary session of the St. Petersburg International Economic Forum, Sofia would expect even more Russian gas to flow to Central Europe through Bulgaria.

Gazprom numbers indicate that Russian exports to Romania increased in 2018.

In addition to Russian gas supplies, the Baltic countries are also dependent on Russian electricity as their power grids are connected with the Soviet-era BRELL (Belarus, Russia, Estonia, Latvia and Lithuania) ring. This dependency will continue until 2025 when it is expected that full synchronization with Europe’s electricity grids will occur.

To sum up, the formation of a ‘sound’ anti-Russian coalition would not be as easy as it may be perceived from the rhetoric, and news about the US’ or NATO’ ramped-up military presence, increased military aid, and plans to establish or modernize military bases in the aforementioned countries.

Taking into account the energy dependence and economic interests, it would be at least irrational if those allies decide to host missiles or ensure an unnerving military posture.

Public disapproval

The unwillingness of the European leaders to provoke a new arms race would be effectively supported by public criticism.

Nowadays, people in Europe are more sensitive to threats, considering the rise of violence in the continent, and have more tools at their disposal to allow them to protest. Widespread protests would be quite challenging for European leaders given the existing issues over Brexit, migrants, and the deteriorating situation over Iran.

Fear of the reaction from Moscow

Any drastic shifts that could pose a threat to the national interests of Russia could cause an unexpected response from it.

In his 2019 address to the Federal Assembly, President Putin, mentioned the deployment of launchers which can accommodate Tomahawk cruise missiles in Romania and Poland, as an open violation of the treaty clauses. He warnedthat Russia would “respond with mirror or asymmetric actions.” He stated that Russia would have to target the decision-making centers of the missile systems.

US decision makers and policy planners are well informed about the nature of a possible Russian response which has been tested in the past in the case of Georgia and Ukraine.

Upcoming elections in the US

The Trump administration would refrain from radical foreign policy decisions ahead of the presidential elections in 2020.

Although US foreign policy is not believed to be as important in US elections as issues such as healthcare, immigration, and gun laws, any dramatic geopolitical event for the US would definitely affect voting behavior.

While the US has been concerned about Russia’s alleged development of a ground-launched cruise missile since 2013, it is unclear what triggered Washington’s abrupt move. However, it is known from the U.S. Nuclear Posture Review 2018, that the US had already started “research and development by reviewing military concepts and options for conventional, ground-launched, intermediate-range missile systems,” as part of military measures to respond to Russia.

The explanation of the incentives of the withdrawal decision is further complicated in view of the above listed circumstances which would essentially limit the potential willingness of the US to deploy such missiles.

The move could be related to US concerns regarding China, which is not bound by the Cold War-era treaty. This is challenging for Russia too. But Russia could deploy those missiles in the East as a counterbalance against the potential US deployment to the Asia-Pacific.

Nevertheless, the US decision to walk away from the treaty will impact European security and worsen relations between the US and Russia.

Apparently, the vulnerable security situation and the lack of contacts within the NATO-Russia and US-Russia channels may give rise to incidents and provocations based on miscalculations or errors of information.

The risk of this happening has increased due to NATO’s and the US’ enhanced military presence.

As NATO Secretary General Jens Stoltenberg noted at a press conference ahead of a meeting of NATO foreign ministers in Washington in April, a 50% increase was seen in the number of days NATO ships spent in the Black Sea in 2018 compared with 2017.

It is worth mentioning the incident of a Russian Su-27 intercepting the US EP-3 Aries aircraft flying over the Black Sea. While Russia’s Defense Ministry said the crew “followed all necessary safety procedures,” the US Navy warned “unsafe actions increase the risk of miscalculation and potential for midair collisions”. Another such incident occurred last month over the Mediterranean Sea when a US P-8A Poseidon aircraft was intercepted by a Russian SU-35.

Provoking Russia to become involved in such incidents could make European leaders recalculate their strategic choices and boost military cooperation with the US and within NATO. It would also stimulate further attempts to harm Russia’s strategic energy plans, such as the Nord Stream 2 project, in order to reduce Russian leverage against Europe and open the way for LNG imports for the sake of US business interests.

via ZeroHedge News https://ift.tt/2MrvVtb Tyler Durden

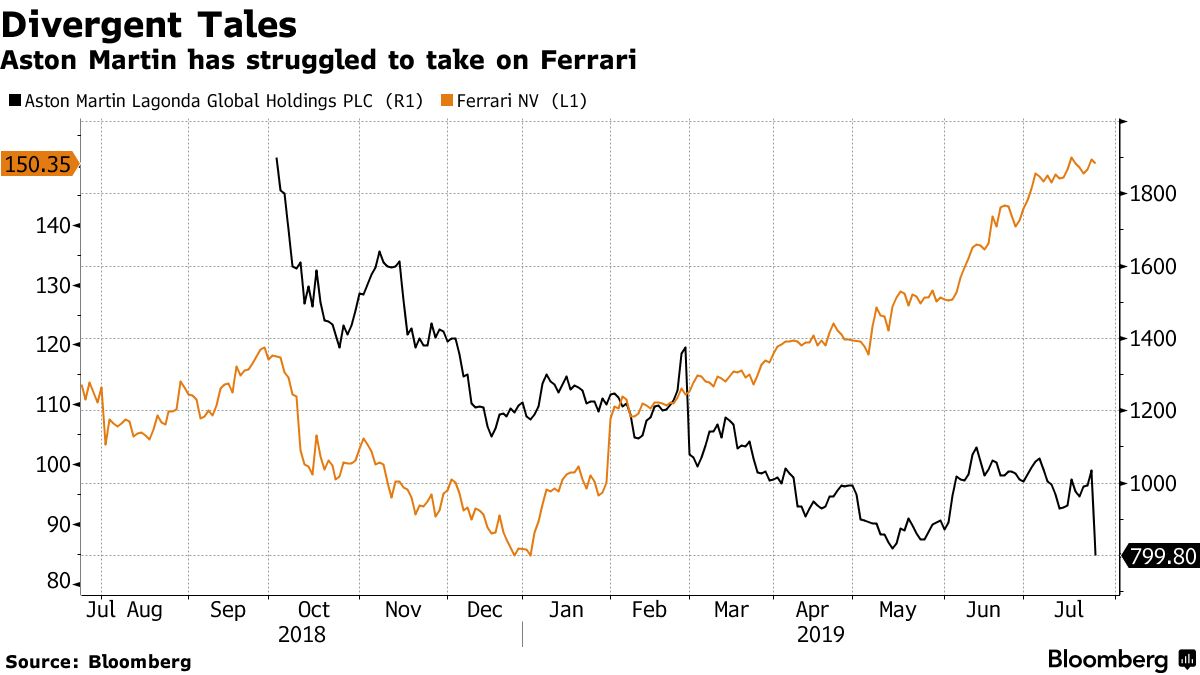

The questions are starting to pile up for Aston Martin after the company’s ugly first half of the year, where it swung to a loss, according to Bloomberg.

Recall, just days ago, we reported that the newly-listed company had slashed its sales forecast and saw its shares tumble as a result. The stock’s fall since its listing in October, combined with its operational challenges, have prompted speculation about capital raises and potentially becoming a takeover target.

The company’s Chief Executive Officer Andy Palmer said on Wednesday: “It’s been a tough time for all of us, but we still believe that what we’ve done is the right thing for the brand.”

The company cut its outlook on sales to dealers by more than 10% last week and reported a 1H adjusted operating loss of 35.2 million pounds, versus a 64.4 million pound profit last year. The company blamed higher costs of expansion and lower vehicle pricing as pressures on its operations. It also noted that uncertainty over Brexit continues to loom over the head of the automaker.

As the U.K. leaving the EU without an exit deal becomes likely, the company is preparing to face supply chain issues going forward.

Bernstein analyst Max Warburton said:

“The company is now on a financial knife-edge. There’s now very, very little room for error or further external pressures, a serious worry given the potential trouble that could come from Brexit.”

The company now sports a 1 billion pound market valuation, nearing the amount of its 723 million pounds in debt. Bank of America said on Tuesday that the company should consider a rights offering of up to 500 million pounds or cut its medium term outlook.

The struggles also open the door for a potential buyer, like InvestIndustrial, who is one of its largest shareholders.

Chief Financial Officer Mark Wilson said Wednesday:

“If we require some additional financing from sources with which we’re familiar, particularly in the debt market to maintain that capacity, then that’s what we’ll go out and do.”

A lot of the company’s success going forward will hinge on its new SUV, the DBX, which is set to launch next year.

It’ll be built at a new plant in Wales and is a key part of the company’s goal to raise annual production to 14,000 per year by 2023.

via ZeroHedge News https://ift.tt/2yqITPw Tyler Durden

“We are facing the biggest wave of migration in history. If we open the floodgates, no European government will be able to survive for more than six months. We advise them not to try our patience.” — Turkish Interior Minister Süleyman Soylu.

“Turkey is fully committed to the objective of EU membership… The finalization of the Visa Liberalization Dialogue process which will allow our citizens to travel to the Schengen area without a visa, is our first priority.” — Statement released by the Turkish Foreign Ministry, May 9, 2019.

“This doesn’t mean that I have anything against the Turks…. But if we begin to explain it — that Turkey is in Europe — European school students will have to be told that the European border lies in Syria. Where’s common sense? … Can Turkey be regarded a European country culturally, historically, and economically speaking? If we say that, we want the European Union’s death.” — Former French President Nicolas Sarkozy.

If the EU approves the visa waiver, tens of millions of Turks will gain immediate and unimpeded access to Europe’s passport-free zone. Critics of visa liberalization fear that millions of Turkish nationals may end up migrating to Europe. The Austrian newsmagazine, Wochenblick, reported that 11 million Turks are living in poverty and “many of them are dreaming of moving to central Europe.”

Turkey has threatened to re-open the floodgates of mass migration to Europe unless Turkish nationals are granted visa-free travel to the European Union. The EU agreed to visa liberalization in a March 2016 EU-Turkey migrant deal in which Ankara pledged to stem the flow of migrants to Europe.

Pictured: The Adiyaman refugee camp in Turkey. (Image source: UNHCR)

European officials insist that while Turkey has reduced the flow of migrants, it has not yet met all of the requirements for visa liberalization. Moreover, EU foreign ministers on July 15 decided to halt high-level talks with Ankara as part of sanctions over Turkish oil and gas drilling off the coast of Cyprus.

In an interview with Turkish television channel TGRT Haber on July 22, Turkish Foreign Minister Mevlut Çavuşoğlu said that Turkey was backing out of the migrant deal because the EU had failed to honor its pledge to grant Turkish passport holders visa-free access to 26 European countries.

“We have suspended the readmission agreement,” he said. “We will not wait at the EU’s door.”

A day earlier, Turkish Interior Minister Süleyman Soylu accused European countries of leaving Turkey alone to deal with the migration issue. In comments published by the state news agency Anadolu Agency, he warned:

“We are facing the biggest wave of migration in history. If we open the floodgates, no European government will be able to survive for more than six months. We advise them not to try our patience.”

The migration deal, which entered into force on June 1, 2016, was hastily negotiated by European leaders desperate to gain control over a crisis in which more than one million migrants poured into Europe in 2015.

Under the agreement, the EU pledged to pay Turkey €6 billion ($6.7 billion), grant visa-free travel to Europe for Turkey’s 82 million citizens, and restart accession talks for Turkey to join the EU. In exchange, Turkey agreed to stop the flow of migrants to Europe as well as to take back all migrants and refugees who illegally reach Greece from Turkey.

Turkey currently hosts an estimated 3.5 million migrants and refugees — mainly Syrians, Iraqis and Afghans. Many of these people presumably would migrate to Europe if given the opportunity to do so.

Responding to Çavuşoğlu’s remarks, EU spokesperson Natasha Bertaud insisted that Turkey’s continued enforcement of the EU-Turkey deal remains a condition for visa liberalization.

Turkish officials have repeatedly accused the EU of failing to keep its end of the bargain, especially with respect to visa liberalization and accession to the EU.

Under the agreement, European officials promised to fast-track visa-free access for Turkish nationals to the Schengen (open-bordered) passport-free zone by June 30, 2016 and to restart Turkey’s stalled EU membership talks by the end of July 2016.

To qualify for the visa waiver, Turkey had until April 30, 2016 to meet 72 conditions. These include: bringing the security features of Turkish passports up to EU standards; sharing information on forged and fraudulent documents used to travel to the EU, and granting work permits to non-Syrian migrants in Turkey.

European officials say that although Turkey has fulfilled most of their conditions, it has failed to comply with the most important one: relaxing its stringent anti-terrorism laws, which are being used to silence critics of Turkish President Recep Tayyip Erdoğan.

Since Turkey’s failed coup on July 15, 2016, more than 95,000 Turkish citizens have been arrested and at least 160,000 civil servants, teachers, journalists, police officers and soldiers have been fired or suspended from various state-run institutions.

Responding to the purge, the European Parliament on March 13, 2019 called for EU accession negotiations with Turkey to be suspended. “While the EU accession process was at its start a strong motivation for reforms in Turkey, there has been a stark regression in the areas of the rule of law and human rights during the last few years,” according to the adopted text.

Turkey was first promised EU membership in September 1963, when it signed an “Association Agreement” aimed at establishing a customs union to pave the way for eventual accession to the EU. Turkey formally applied for EU membership in April 1987 and membership talks began in October 2005.

Turkey’s EU accession talks stalled in December 2006 after the Turkish government refused to open Turkish ports and airports to trade from Cyprus. Since then, talks have continued on and off, but the process has been stalled due to political opposition from France and Germany, among others.

If Turkey were to join the EU, it would overtake Germany to become the EU’s largest member in terms of population. Consequently, the EU’s largest member state would be Muslim. Some European officials have warned that Turkish accession would cause Europe to “implode” and be “Islamized.”

Former French President Nicolas Sarkozy has said that Turkey has no place in the EU. In a February 2016 interview with the French news channel iTélé, he expressed sentiments that presumably are shared by many Europeans:

“Turkey has no place in Europe. I have always adhered to this position, it is based on common sense. This doesn’t mean that I have anything against the Turks. We need them, they are our allies in NATO. But if we begin to explain it — that Turkey is in Europe — European school students will have to be told that the European border lies in Syria. Where’s common sense?

“It’s not just that. What’s the idea behind Europe? Europe is a union of European countries. The question is very simple, even in a geographical sense, is Turkey a European country? Turkey has only one shore of the Bosporus in Europe. Can Turkey be regarded a European country culturally, historically, and economically speaking? If we say that, we want the European Union’s death.”

On May 9, 2019, Erdoğan said that Turkey was committed to joining the EU. A statement released by the Turkish Foreign Ministry noted:

“Turkey remains committed to its objective of EU membership and continues its efforts in this respect…. Our expectation from the EU is to treat Turkey on equal footing with other candidate countries and to remove political barriers on the way of negotiations which is supposed to be a technical process…

“Although our accession negotiations are politically blocked, Turkey decisively continues its efforts for alignment with the EU standards. In the meeting today, we have set out the current developments in Turkey and agreed on the steps to be taken in the forthcoming period.

“The finalization of the Visa Liberalization Dialogue process which will allow our citizens to travel to the Schengen area without a visa, is our first priority.”

Even if Turkey complies with all of the EU’s demands, it seems unlikely that Turkish nationals will be granted visa-free travel anytime soon. On July 15, EU foreign ministers formally linked progress on Turkish-EU relations to Cyprus. A measure adopted by the European Council on July 15 states:

“The Council deplores that, despite the European Union’s repeated calls to cease its illegal activities in the Eastern Mediterranean, Turkey continued its drilling operations west of Cyprus and launched a second drilling operation northeast of Cyprus within Cypriot territorial waters. The Council reiterates the serious immediate negative impact that such illegal actions have across the range of EU-Turkey relations. The Council calls again on Turkey to refrain from such actions, act in a spirit of good neighborliness and respect the sovereignty and sovereign rights of Cyprus in accordance with international law….

“In light of Turkey’s continued and new illegal drilling activities, the Council decides to suspend … further meetings of the EU-Turkey high-level dialogues for the time being. The Council endorses the Commission’s proposal to reduce the pre-accession assistance to Turkey for 2020.”

European officials may be justified in taking a hardline stance against Turkey, but Ankara is well positioned to create chaos for the European Union if it chooses to do so. Indeed, Europe appears to be trapped in a no-win situation.

If the EU approves the visa waiver, tens of millions of Turks will gain immediate and unimpeded access to Europe’s passport-free zone. Critics of visa liberalization fear that millions of Turkish nationals may end up migrating to Europe. The Austrian newsmagazine, Wochenblick, reported that 11 million Turks are living in poverty and “many of them are dreaming of moving to central Europe.”

Others believe that Erdoğan views the visa waiver as an opportunity to “export” Turkey’s “Kurdish Problem” to Germany. Markus Söder, the head of the Christian Social Union, the Bavarian sister party to German Chancellor Angela Merkel’s Christian Democratic Union, warned that millions of Kurds are poised to take advantage of the visa waiver to flee to Germany to escape persecution at the hands of Erdoğan: “We are importing an internal Turkish conflict. In the end, fewer migrants may arrive by boat, but more will arrive by airplane.”

On the other hand, if the EU rejects the visa waiver, and Turkey retaliates by reopening the migration floodgates, potentially hundreds of thousands of migrants from Africa, Asia and the Middle East could once again begin flowing into Europe.

via ZeroHedge News https://ift.tt/2OtVJaD Tyler Durden