India Test Fires ‘NextGen Hypersonic Weapon’ As Border Tensions With China Surge Tyler Durden

Mon, 09/07/2020 – 22:30

With a military standoff between India and China intensifying, the Indian military has decided to increase geopolitical instabilities in the region, on Monday, as it test-fired a new class of ultra-modern weapons that can travel at hypersonic speeds.

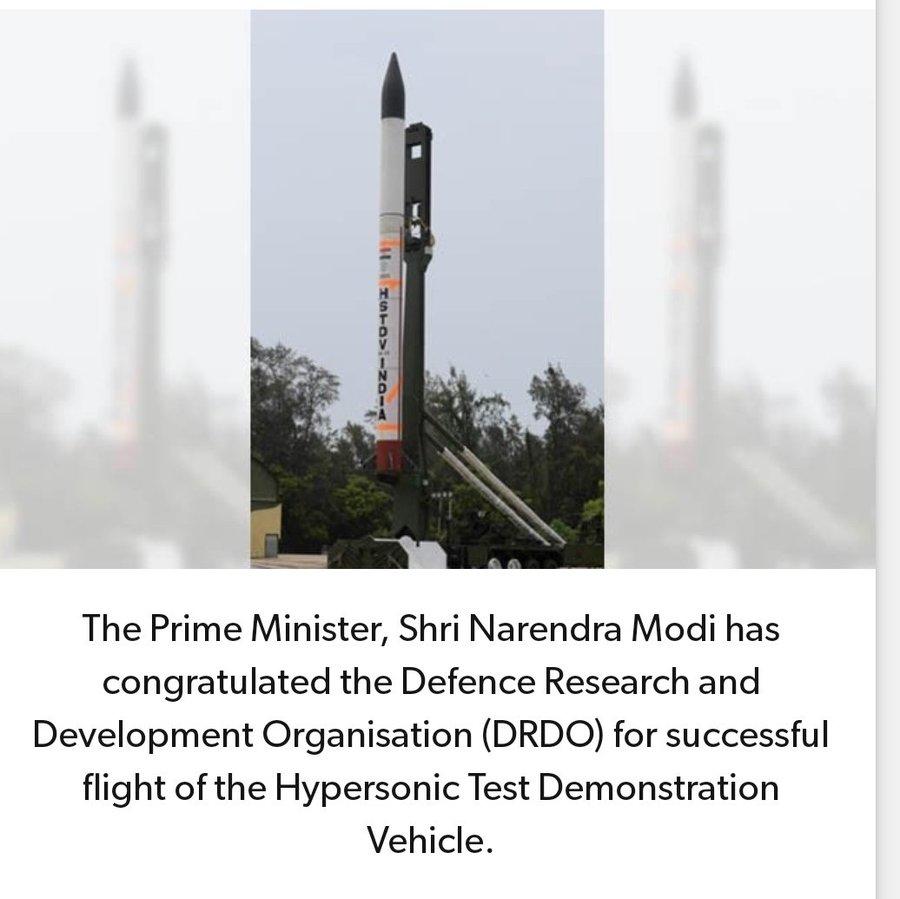

The Defence Research and Development Organisation (DRDO), an agency under the Indian Ministry of Defence, tasked with weapon development, released a statement Monday announcing it “successfully flight tested” a domestic hypersonic technology demonstrator vehicle (HSTDV) for the first-time.

DRDO with this mission, has demonstrated capabilities for highly complex technology that will serve as the building block for NextGen Hypersonic vehicles in partnership with industry.

Defense minister Rajnath Singh congratulated DRDO for the “successful” launch of the HSTDV, describing the advanced engine technology as a scramjet propulsion system. Singh said the vehicle hit speeds in excess of Mach 6 (4,600 mph).

Here’s a video of the HSTDV launch.

Successful flight test of Hypersonic Technology Demonstration Vehicle (HSTDV) from Dr. APJ Abdul Kalam Launch Complex at Wheeler Island off the cost of Odisha today. pic.twitter.com/7SstcyLQVo

— रक्षा मंत्री कार्यालय/ RMO India (@DefenceMinIndia) September 7, 2020

“The cruise vehicle separated from the launch vehicle and the air intake opened as planned. The hypersonic combustion sustained and the cruise vehicle continued on its desired flight path at a velocity of six times the speed of sound or nearly 2 km/second for more than 20 seconds,” the DRDO statement read. India’s first test of the HSTDV ended in failure in June 2019.

The successful test of the hypersonic vehicle is an important milestone for India as it now joins the US, Russia, and China in the hypersonic club.

“This has been some time in the making and the challenge now is to make a time-bound transition to the prototype testing phase. China is quite ahead in hypersonics and India cannot afford to lag behind,” Air Vice Marshal Manmohan Bahadur (Retired), additional director general, Centre for Air Power Studies, said.

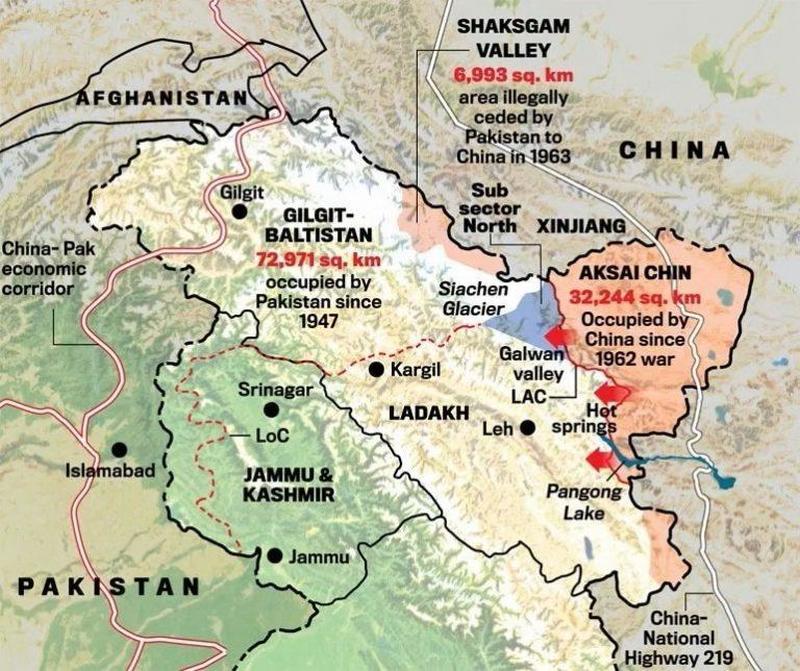

The timing of the launch comes as India and China are locked in a monthslong military standoff along the Line of Actual Control, a 2,175 mile disputed border between both countries, that stretches from the Ladakh region in the north to the Indian state of Sikkim.

In the event of an unintentional war along the heavily disputed border, and China already developing hypersonic weapons and deploying stealth fighter jets, India is now playing catch up as it must modernize it forces as a hot conflict may be inevitable.

via ZeroHedge News https://ift.tt/326iFkT Tyler Durden

When all else fails, Fake Republicans like Richard Nixon back in the day and Donald Trump today turn to “Law & Order” demagoguery to incite the electorate in their direction.

So doing, they conveniently abandon the real job of the Conservative Party in American democracy, which is to fight against the Government Party (usually the Dems) on behalf of free markets, fiscal rectitude, sound money, smaller government, federalism and maximum personal liberty.

Thus, when America was plagued with the short-term outbreak of riots in dozens of major American cities in 1968—Detroit, Cleveland, Newark, Gary, Chicago, Philadelphia—Tricky Dick Nixon put himself over the top at the polls in November by running for National Sherriff rather than as the scourge of Lyndon Johnson’s drastic ballooning of the state in the form of “guns and butter” finance and the eruption of Great Society spending programs.

As it happened, however, Nixon didn’t need an electoral mandate for Law and Order because the summer of 1968 eruptions in the urban ghettos quickly burned themselves out, while mainly harming the residents living therein.

More importantly, policing the big cities is not the job of the Federal government or the President, anyway; and is, in fact, one of the principal functions implicitly reserved to the states and their sub-units by the 10th Amendment to the Constitution.

Indeed, administration of local law and order is one of the main reasons we have 87,575 units of government separate from the Federal government, including the 50 states, 3,034 counties, 35,933 cities, towns, municipalities and townships and 48,558 other units including school districts and special purpose units of local government (e.g. police, fire, library districts etc).

Far more so than the giant Federal bureaucracies that have insinuated themselves into the law and order business, such as the FBI, DEA, BATF and the far-flung operations of the Homeland Security Department, the overwhelming share of these local government units are actually creatures of their respective electorates. If law and order breaks down or is wanting, therefore, the solution is to house clean at City Hall or the county courthouse, not import Federal money, laws, regulations and rhetorical posturing from Capitol Hill or the Oval Office.

And if the local electorate fails to clean house, it will bear the brunt of the adverse consequences of too many homicides, robberies or destructive attacks on private property within the jurisdiction in question. After all, most serious crime—especially homicides and violent assaults on persons and property—are the work of local residents, not regional or national crime rings.

Moreover, if the electorates of badly governed jurisdictions like Seattle, Portland, Minneapolis, Chicago, New York and Baltimore at the moment fail to remedy their own crime problems, the ultimate brilliance of Federalism comes powerfully into play: That is, on the margin residents and businesses vote with their feet, causing local economic decline and diminution of tax revenues, and thereby eventually generating electoral demands for corrective action.

At the same time, presidential Law & Order demagoguery by GOP presidents readily becomes a cover for betrayal on Federal policy matters that actually count. Until the Donald came along, of course, Tricky Dick Nixon was the poster boy for this kind of doctrinal perfidy.

The man’s policy sins are almost too egregious to reprise. Richard Nixon…

Famously abandoned sound money when he slammed the gold window shut at Camp David in August 1971;

Made a mockery of free markets when he imposed wage, price, rent and interest controls on the entire US economy shortly thereafter;

Fecklessly fueled the growth of Big Government by putting Federal bureaucrats in charge of domestic energy industries and employing subsidies and import controls to pursue the folly of national energy autarky;

Deeply wounded the cause of fiscal rectitude by adopting the specious Keynesian notion of “full employment budgeting”, which amounts to an excuse for chronic government deficits whenever an imaginary figure called “potential GDP” is not realized (most of the time);

Attempted to vastly expand the Welfare State through a guaranteed annual income (Family Assistance Plan) and an incipient form of national health insurance (Family Insurance Program);

Eroded Federalism through revenue sharing handouts from Washington and a vast expansion of federal grant-in-aid programs; and

Fueled a 50-year assault on the social and economic stability of the nation’s declining urban centers via the abomination of the the War on Drugs.

Needless to say, the latter betrayal gets us to the present moment. There is no more of a Law & Order crisis today that demands presidential attention and Washington intervention than there was in 1968.

The overwhelming bulk of the American electorate is not in any danger owing to the antics and defaults of the clowns running Portland, Minneapolis, Chicago or even New York City. In due time, their electorates will select better leadership or the citizens will flee for better governed environs.

But as we demonstrate below, there is an elevated and unnecessary level of friction between the police and citizens in the nation’s urban centers. The latter is overwhelmingly caused by and exacerbated by the War on Drugs and the criminalization of related social behaviors such as gambling, prostitution etc. that can be solved by repeal of bad laws, not costly and counter-productive efforts to get tough on crime; and most certainly not be sending Federal cops into cities which are wittingly or unwittingly abetting crime and riots and thereby bringing ruin upon themselves.

So just as in Nixon’s time, by relentlessly obsessing about crime ridden Democrat cities the Donald is abandoning his real job. If there is a real crisis in America, it is the crushing burden of debt and speculation on the main street economy, not any serious or long-lasting outbreak of serious crime.

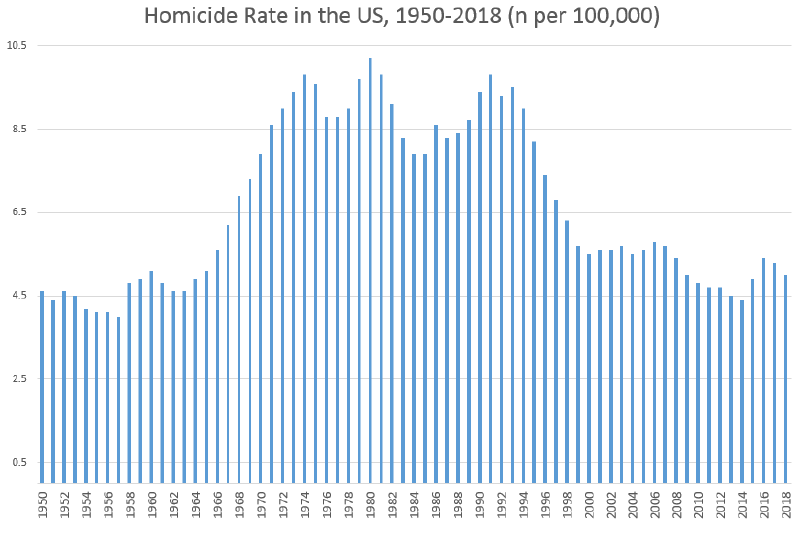

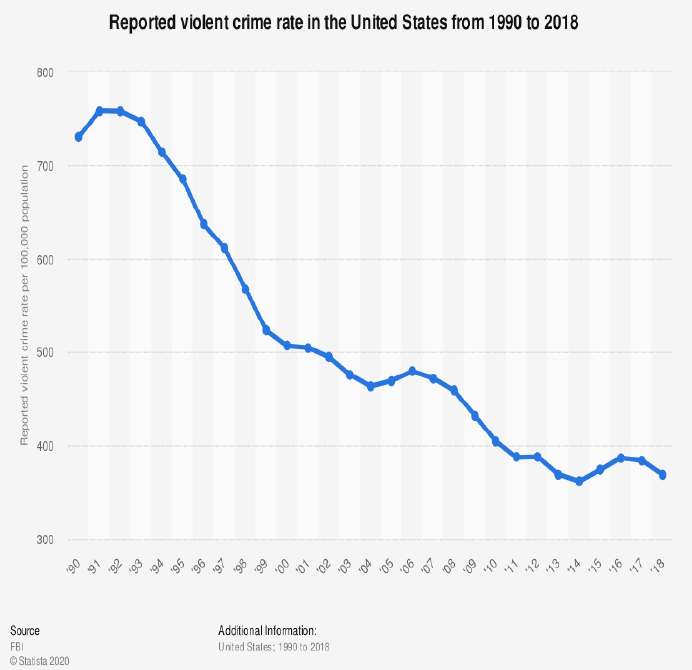

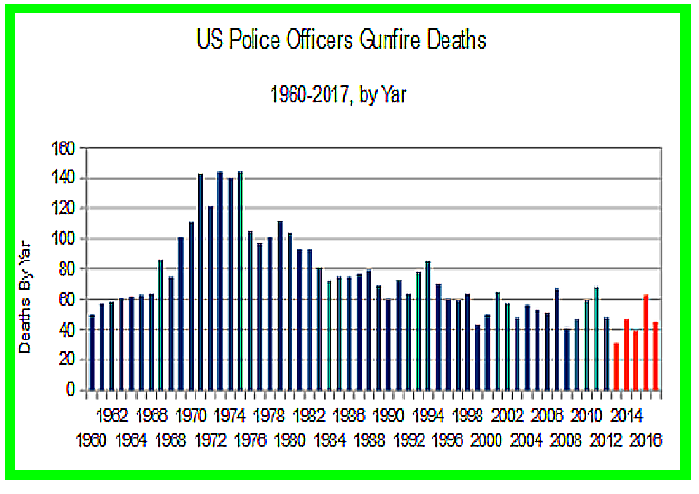

Obviously, when it comes to crime, it doesn’t get more serious than homicide. Yet as shown below, the homicide rate per 100,000 in recent years has been barely half of what prevailed during the 1970-1995 period, and has continued to edge lower.

The same is true of total violent crimes, which also includes rape, robbery and aggravated assault, as well as homicides. As shown below, the rate per 100,000 in the most recent year was about half the early 1990s level.

Moreover, although not shown, preliminary FBI statistics indicate that neither the homicide rate nor the total violent crime rate appreciably changed in 2019.

Violent Crime Per 100,000

While the last full year for which FBI statistics are available is 2018, the preliminary data from the FBI for 2019 indicates that all four categories of violent crime were down versus prior year:

Homicide: -3.9%;

Forcible rape: -7.3%;

Robbery: -7.4%;

Aggravated assault: -0.3%.

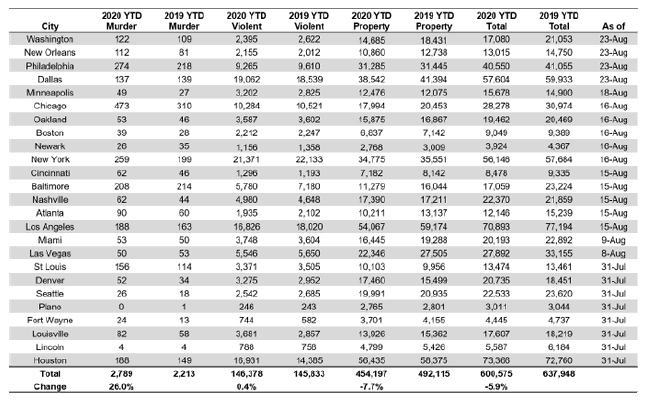

To be sure, during 2020 to date there has been an upsurge of homicides in a handful of big cities owing to the BLM demonstrations and riots after the late May murder of George Floyd by the police in Minneapolis.

Still, even in the 25 largest US cities shown below, total violent crimes in 2020 YTD are essentially flat with 2019 (up 0.4% during the first 7 months) and property crimes are actually down by -7.7% year-to-date.

As to the surge in homicides, 80% of the 576 increase in cases over 2019 is attributable to just eight cities including Chicago (+173), NYC (+60), Philadelphia (+56), St. Louis (+42), Houston (+39), Atlanta (+30), Louisville (+27). and Los Angles (+25). By contrast, a nearly equal number of big cities, including Dallas, Newark, Baltimore, Miami, Las Vegas, Plano and Lincoln have experienced little change or even declines from 2019.

In short, notwithstanding the cable TV tsunami of coverage of urban protests and riots and the Donald’s false characterization of Law & Order as a national crisis, there is no break-out of homicides and other violent crimes, even in the big cities. For the nation as a whole, the downward trend in crime rates which has been in effect for nearly 20 years remains in place.

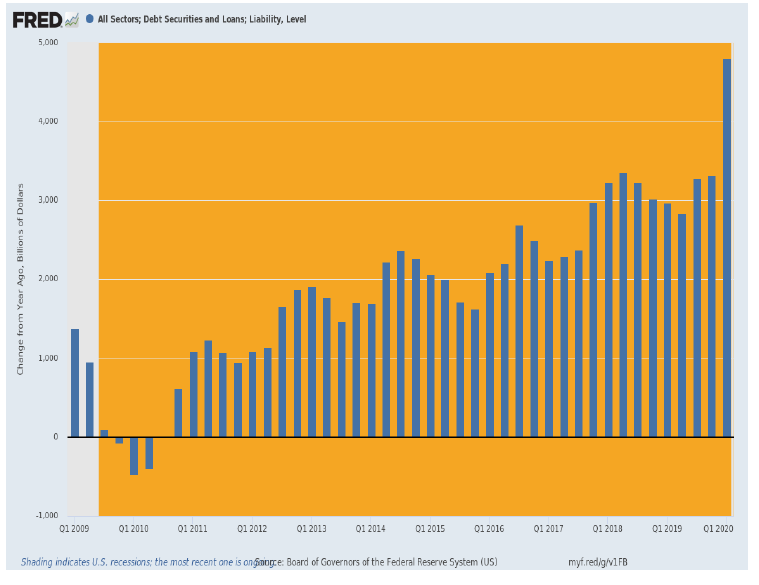

Needless to say, when it comes to the Donald’s real job as a Republican president, he has presided over what can only be described as a horror show. Owing to the total demise of fiscal rectitude and the last vestiges of sound money (the Fed’s belated, short-lived attempt at normalizing its balance sheet in 2017-2018) on his watch, the burden of total debt (public and private) grinding down the US economy has soared to $77.6 trillion.

In terms of of annual rates of gain, the blue bars below show that borrowing is again off to the races, vastly exceeding the egregiously large gains that were recorded during the Obama years, and at a time at the top of the longest business cycle in US history when the nation’s bloated burdens of debt should have actually been paid down.

The problem, of course, is that the Donald is not guided by anything which even remotely resembles policy or theosophical principles, let alone fundamentally conservative ones. For instance, he had a chance to appoint the majority of the Fed’s Board since taking office, but ended up putting Powell and other avid money-printers in the open Chairman’s role and other board seats.

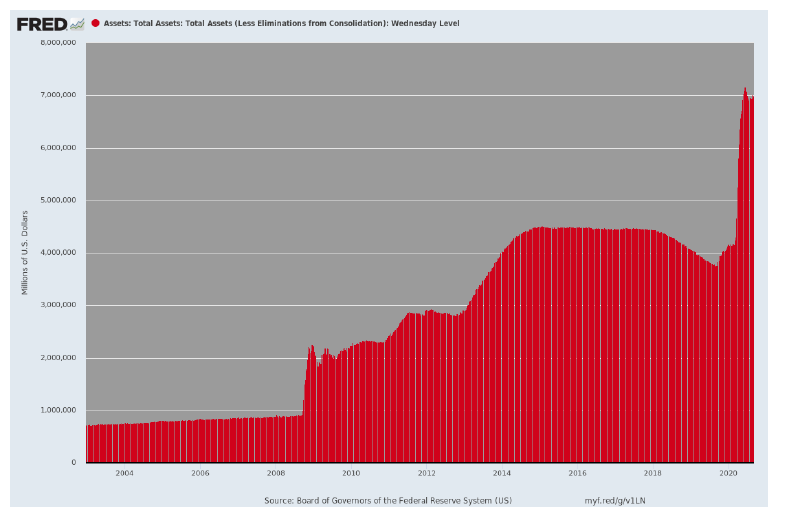

Not surprisingly, the bloated, elephantine $4 trillion balance sheet the Donald inherited and which was supposed to be drastically retrenched after the financial crisis ended has now exploded to $7 trillion, and the Donald self-evidently wants to to grow to $10 trillion and beyond.

That’s capitalism-destroying financial-fraud, yet it lies at the heart of the Trumpian economic program.

Balance Sheet of the Federal Reserve:

At the end of the day, the Donald simply views the Federal government as a larger-scale version of the Trump Organization; and that as its Maximum Leader-CEO, it is his prerogative to steer things in whatever direction promises (by the Donald’s lights) to redound to his greater glory (and presently, his re-election).

At the present moment that means wasting a good crisis on the shrill partisanship of his blustery campaign against crime, riots, looting and plunder in the “Dem-controlled” big cities of America.

In fact, however, there is a very particular and different crime problem in the big cities than the one the Donald excoriates owing to the misbegotten

War on Drugs and the excessive criminalization of social life.

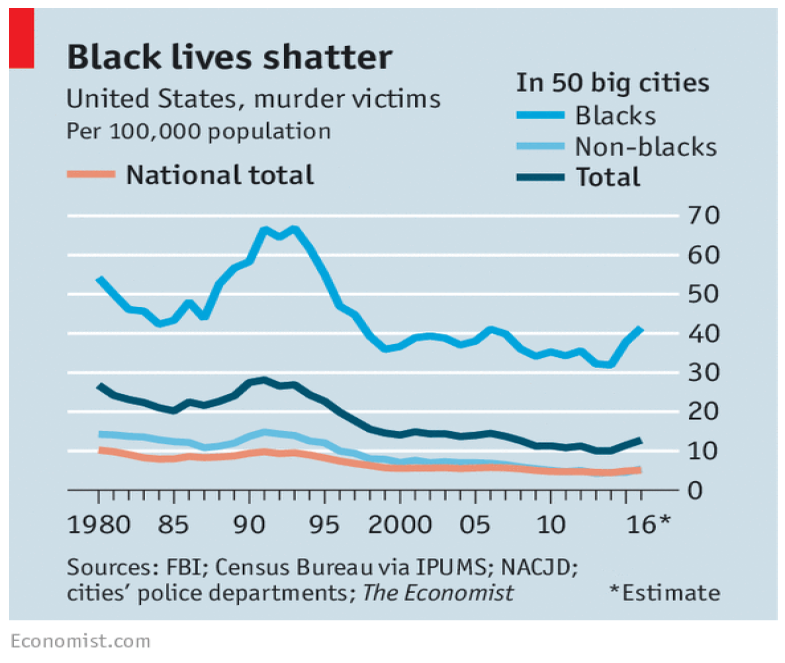

To wit, unlike the declining homicide rate in the US overall (brown line), the murder rate for black citizens in the 50 largest cities in the US has been flat since the turn of the century and has actually turned upward in recent yeas (dark blue line).

Needless to say, this unfortunate trend is not the result of systematic racism; it’s the consequence of bad laws and the resulting excessive friction between law enforcement officers and the urban neighborhoods where inappropriately criminalized activities are more prevalent owing to lack of jobs, the disaster of public education and the prevalence of broken homes, which now encompasses more than 70% of children born into black households.

Rather than overt racism or even simmering racial animosity, the real evil is the relentless aggrandizement of state power. Among its many ills is the rise of the Nanny State—a conflation of too many laws, crimes, cops, arrests and thereby opportunities for frictions between the state and its citizenry and for abuse by the gendarmes vested with legal use of violence.

The nation has now been enthrall for several months to an emotionally charged symptom of this rogue Nanny State—the unjustified murder of unarmed black citizens by the police. Among the most recent notorious cases, of course, are George Floyd for allegedly passing a counterfeit $20 bill, Eric Garner (NYC 2014) for selling un-taxed cigarettes, and Rayshard Brooks for falling asleep drunk in his car at a subsequently incinerated Wendy’s in Atlanta.

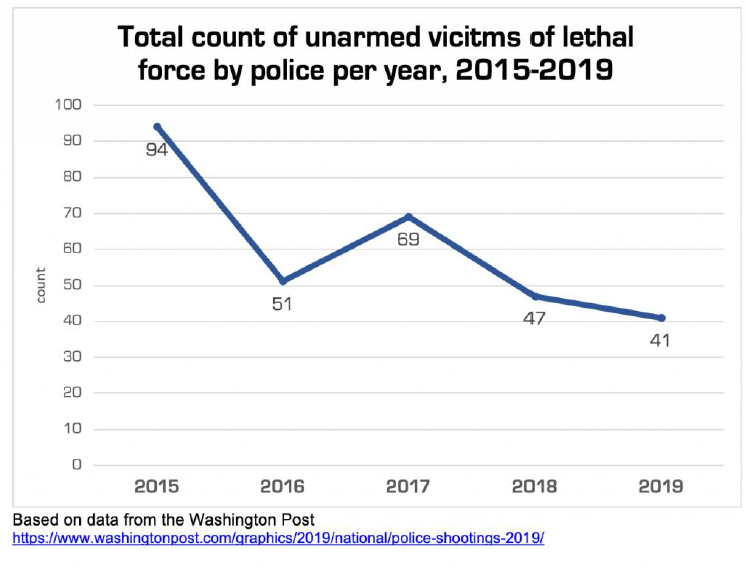

Nor are these notorious cases aberrations. During the recent past there were 38 such police killings of unarmed black citizens in 2015, and then 19, 21, 17 and 9 during 2016 through 2019, respectively. That’s 104 black lives lost to the ultimate abuse of police powers.

Of course, the number should be zero. There is no conceivable excuse for heavily armed cops—-usually working in pairs or groups—to murder lone, unarmed civilians, regardless of race or anything else.

And the fact is, being non-black is no guarantee against the same unjust fate. During the same period, a total of 127 unarmed white lives were wasted by the police, as well. That included 32 white killings in 2015 followed by 22, 31, 23 and 19 in 2016 through 2019, respectively.

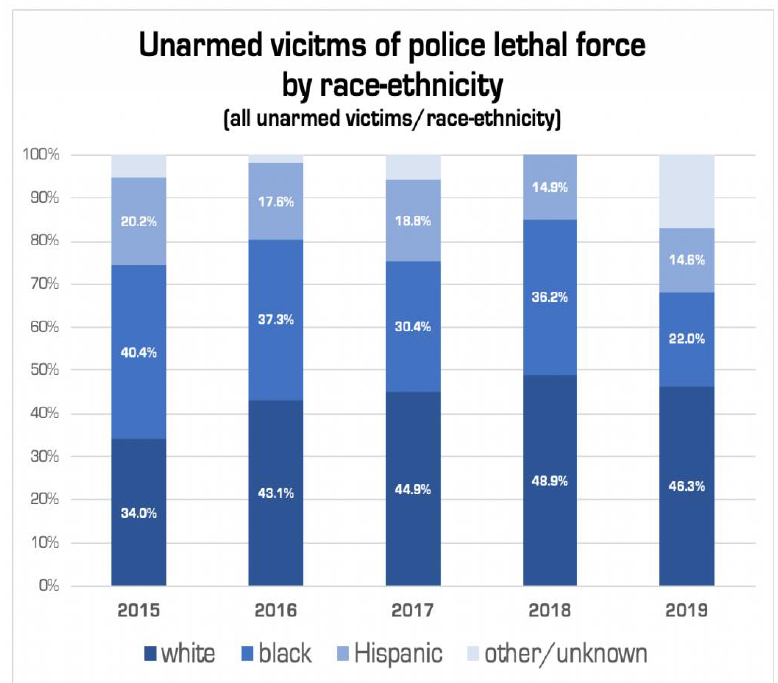

Overall, 302 unarmed citizens were killed by the police during the last five years, with the balance in the chart below accounted for by 71 deaths among Hispanic and other victims. That is, the real issue is illegal and excessive police violence, not racial victimization.

Indeed, the fact that 34% of these police killings involved black citizens compared to their 12% share of the population is not primarily a sign of racism among police forces. It’s actually evidence that the Nanny State, and especially the misbegotten War on Drugs, is designed to unnecessarily ensnare a distinct demographic— young, poor, often unemployed urban citizens— in confrontations with the cops, too many of which become fatal.

Alas, young black males are disproportionately represented among this particular in-harms’-way demographic, and that’s the reason they are “disproportionately” represented in the two charts below.

Stated differently, the Nanny State tends to be racist in effect, even if that is not necessarily the intent of the crusaders and zealots who have launched the state into anti-liberty wars on drugs, vice and victimless inequities and peccadillos.

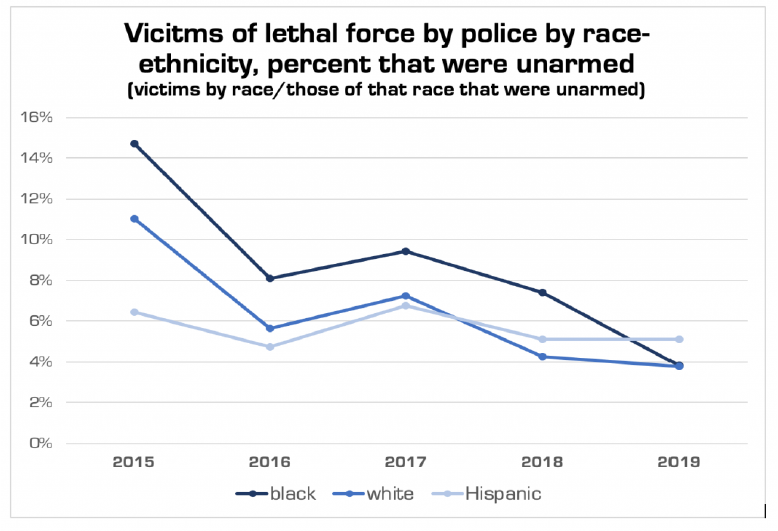

Then again, the charts above and below are only part of the story. As it happened, a total of 4,558 citizens were actually killed by police over that period, but according to the DOJ statistics, fully 93% or 4,256 of them were armed.

So viewed in context, the unarmed/I can’t breathe victims account for only a small fraction of lethal violence between citizens and police, and there really isn’t much difference in the unarmed/armed ratio among racial groups. To wit, over the 2015-2019 period as a whole—

1,164 black citizens were killed by police—of which 104 or just 8.9% were unarmed;

2,151 white citizens were killed by police—of which 127 or just 5.9% were unarmed;

1,243 Hispanic and other citizens were killed by police—of which 71 or just 5.7% were unarmed;

But here’s the thing. This data does not really support either the Sean Hannity/Law & Order fulminations of the Foxified Right or the 400 years of racism and victimization mantra of the CNN/progressive Left.

Contrary to the Left, 93.4% of the dead victims of police violence were themselves armed; and the 91.1% incidence among blacks is not meaningfully different than the 95% rate among whites and Hispanics. The chart below shows the inverse—the share of victims of police deaths who were not armed.

At the same time, the above statistics do not prove that the cops were mostly right or justified, either, as per the Donald’s Law and Order Howling.

As we shall explore below, the real issue is did 4,558 citizens end-up on the losing end of police fire because they were hardened criminals and sociopathic threats to society or were they set-up by an overreaching legal system that puts too many citizens and police officers alike in harms’ way?

But preliminary to that, it needs be said that the rightwing mantra about police as heroic victims of criminal violence doesn’t wash, either. They have the overwhelming firepower in these instances of police-on-citizen violence as attested to be the facts regarding felonious deaths of law enforcement officers during the same five year span.

It turns out that during 2015 through 2019 there occurred 256 police deaths in the line of fire, bringing the total of police and citizen deaths in these encounters to 4,814. That is to say, the cops won 95% of the time, as well they might given their overwhelming superiority in arms, training, back-up support and legal immunity from being too quick on the trigger finger.

In this context, it should be noted that police deaths are sometimes reported at much higher levels – a total of 492 over the last five years rather than the 256 indicated above. However, exactly half of that larger total is considered accidental or non-felonious and includes traffic cops stepping into the wrong lane and even heart attacks in the squad car resulting from too many stops at Dunkin’ Donuts.

So the question recurs as to why there were 4,814 fatal encounters between police and citizens during the past five years.

We think the answer starts with a staggering statistic. Namely, the fact that there were 10,310,960 arrests in the US during the most recent year (2018) excluding traffic violations.

That’s 3,153 arrests per 100,000 population including babies, grannies, toddlers, tweeners, the disabled, the infirm and religious leaders including nuns, priests, preachers, rabbis and imams.

So when you talk about the subset of the population which actually get arrested with high frequency and accounts for most of these arrest totals–—young men between 16 and 35 years—the true arrest rate is far higher; it’s upwards of 15,000 per 100,000 population.

Either way, these arrests rates are far out whacko. Americans are not nearly that lawless, even when you allow for the chronic rotten apples in the population and the anti-social propensities of some young men.

And that hints at the real problem: We have way too many crimes and way too many cops who are way too heavily armed attempting to enforce laws that are not really the business of the state in the first place. In the most egregious kind of example, Eric Garner was apprehended and killed for selling “loosies”, or cigarettes one a time.

In fact, there are an estimated 300,000 Federal laws and regulations whose violation can lead to prison time; and when you throw in state and local jurisdictions, which historically have had an affinity for outlawing victimless crimes and the infinite forms of human vice, the total number of criminal offenses in America is surely well into the millions.

That’s why a disaggregation of the FBI’s UCR (Uniform Crime Reports) arrest statistics for 2018 tell you all you need to know about why the nation’s police forces are way over-funded and why a huge amount of confrontation and friction—including violent encounters––between citizens of all races are unnecessary.

In a word, some citizens sometimes can’t breathe their last breath because in far too many instances liberty can’t breath in today’s unhinged Nanny State, either.

Self-evidently, the legitimate law enforcement function of the state is protection of the life and property of its citizens. But when you look at the FBI’s own national arrest data for 2018, it appears that only about one-quarter of arrests were clearly pursuant to those core functions, meaning that the overwhelming bulk of arrests–-7,621,232-–were for drugs, gambling, prostitution, disorderly conduct and the like.

Among the core law enforcement functions, the 26% of all arrests broke out as follows:

521,103 arrests for violent crimes against persons (5% of total);

1,000,329 arrests for driving under the influence (DUI), a clear threat to the lives and property of other drivers (9.7%);

1,167,296 arrests for crimes against property (11.3% of total)

Even when you drill down in these categories, however, the reality of way too many cops is evident. There were just 11,970 arrests for murder and negligent manslaughter in 2018 across the entire USA at all levels of law enforcement. Clearly, these are the most violent and heinous of violent crimes, yet they amounted to just 2.2% of all “violent crimes” reported via the UCR and a mere 0.1% of all arrests by the police.

Next in order of severity were arrests for rape, armed robbery under threat of violence to persons and aggravated assault. There were 25,205, 88,128 and 395,800 arrests in these categories, respectively, amounting to 0.2%, 0.9% and 3.9% of all 10.3 million recorded arrests.

Thus, these four categories are the core of violent crime arrests and totaled 521,103 arrests in 2018 or just 5.0% of total arrests That compares to 850,000 sworn law enforcement officers in the USA, of which about 750,000 are employed by the 18,000 units of state and local government.

To be sure, nearly 1.6 cops for every annual arrest in these four core functions sounds more than a bit lop-sided, but there are some additional arrests that add to the legitimate work loads of the police. These include the following crimes and their share of total arrests:

burglary: 178,611 (1.7%);

larceny-theft: 887,622 (8.6%);

motor vehicle theft: 91,676 (0.8%);

arson: 9,387 (0.09%).

DUI: 1,167,296 (11.3%)

Needless to say, these are all serious crimes that need to be enforced for the protection of life and property. But by their very nature, the vast bulk of the arrests in the above five categories do not ordinarily involve violent criminals, nor does their enforcement require combat-strength arms and tactics among police forces.

DUI arrests, for example, overwhelmingly involve citizens engaging in socially reckless behavior, but not habitual criminal activity. A detailed study awhile back, for example, showed that 65% of arrests resulted in no correctional supervision at all and another 27% of cases consisted of individuals sentenced to probation or jail who had no prior arrest records for crimes other than DUI. By contrast just 8% of DUI arrestees had prior non-DUI criminal records, and even then most of them were for lesser offenses.

Likewise, the FBI’s UCR system defines larceny-theft as follows:

The unlawful taking, carrying, leading, or riding away of property from the possession or constructive possession of another. Examples are thefts of bicycles, motor vehicle parts and accessories, shoplifting, pocket-picking, or the stealing of any property or article that is not taken by force and violence or by fraud.

Nevertheless, larceny-theft accounts for 76% of all crimes against property reported in the UCR arrest data for 2018.

So the question recurs. If the nation’s huge and heavily armed police forces are involved in the arrests of core criminal in just 5% of their apprehensions and are dealing with serious but mainly non-violent criminals in another 21% of arrests dealing mainly with burglaries, drunk drivers, car thieves and arsonists, what are they doing the rest of the time?

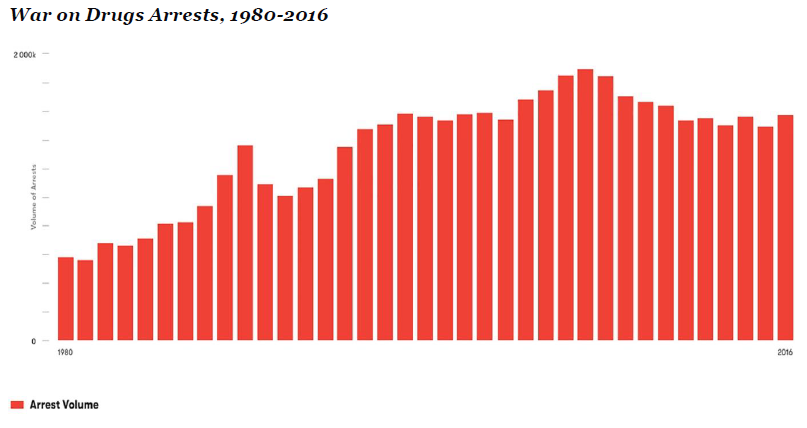

Here is a spoiler alert. The single largest category of arrests in 2018 was for drug abuse violations, which totaled 1,654,282.

In fact, while total arrests in 2018 were no higher than they were in 1977 despite a 100 million/50% growth in the US population, and had actually dropped from a peak of nearly 13 million in 2006, the opposite trend was extant in the case of War on Drugs arrests.

As shown by the chart below, arrest in 2018 were nearly at peak levels and were up by more than 171% since 1977—the vast majority of which are made for drug possession generally, and marijuana possession most often.

War on Drugs Arrests, 1980-2016

Not surprisingly, the next largest arrest category after drugs is one called “other assaults” for which 1,063,535 arrests were made in 2018. Yet the FBI’s own definitions raise considerable doubts as to why these are even a matter of law enforcement by the state:

Other assaults (simple)―Assaults and attempted assaults where no weapon was used or no serious or aggravated injury resulted to the victim. Stalking, intimidation, coercion, and hazing are included.

Then, of course, we have all the victimless and vice crimes, including the following number of arrests::

Prostitution and commercialized vice: 31,147;

Sex offenses excluding rape and prostitution: 46,937;

Gambling: 3,323;

Liquor law offenses: 173,152;

Curfew and loitering law violations: 22,031;

Vagrancy: 23,546;

Public drunkenness: 328,772;

Disorderly conduct: 329,152;

Forgery and counterfeiting: 50,072;

Weapons carrying and possession: 168,403;

All other offenses: 3,231,700.

The latter huge number tells you all you need to know. The UCR lists 27 enumerated categories of crime including all of those itemized above–plus the usual suspects like fraud and embezzlement for which there were about 135,000 arrests in 2018. Yet when the whole lists is exhausted, 32% of arrests occurred for crimes that are so minor even the FBI is embarrassed to enumerate them:

All other offenses—All violations of state or local laws not specifically identified as Part I or Part II offenses.

So, yes, we do think there is way, way to many crimes and cops, and that de-criminalizing and de-funding law enforcement are the only route to reducing police violence.

Indeed, over the past four decades, the constant dollar cost of policing in the U.S. has almost tripled, from $42.3 billion in 1977 to $114.5 billion in 2017, according to an analysis of U.S. Census Bureau data conducted by the Urban Institute. Yet that 171% gain compares to only a 20% increase in violent crimes from 1.0 million in 1977 to 1.2 million in 2017.

That is, real police spending per violent crime is up from $42,300 in 1977 to $95,400 in 2017.

Better that police did not spend 90% of their time on matters other than protecting the life and property of the citizenry; and in the process turning the Nanny State into an instrument of violence against citizens, and especially the young, poor and minorities who become ensnared in its vast over-reach.

Wealthy 20-Year-Old Arrested For Role In Black Lives Matter Riot That Caused $100,000 In Damage Tyler Durden

Mon, 09/07/2020 – 21:30

A 20 year old from a wealthy family is being charged for her role in participating in a 3 hour Black Lives Matter “protest” in Manhattan that resulted in nearly $100,000 worth of damage being done to businesses.

Clara Kraebber was arrested after a barrage of destruction in Manhattan’s Flatiron district last Friday. The group was spotted chanting “Every city, every town, burn the precinct to the ground!” , according to RT. Her group carried signs saying “Death to America” and “Free All Prisoners”.

Kraebber is the daughter of an architect and child psychiatrist and comes from a family who owns homes in both the Upper East Side and Connecticut. She was demonstrating with groups calling themselves the “Revolutionary Abolitionist Movement” and the “New Afrikan Black Panther Party”.

EXCLUSIVE: As protestors take to the streets of New York, a small group of troublemakers are seen smashing windows. We know of at least 8 arrests tonight. One store worker says he understands the protests, but doesn’t get the destruction of property – 11p @NBCNewYorkpic.twitter.com/vr4z76ZqQn

She is currently an undergraduate at Rice University, where tuition averages about $50,000. According to RT, her family paid $1.8 million for their Upper East Side home and their second home – in Connecticut – features four fireplaces.

Eight people in total were arrested and charged with rioting – some were also charged with having weapons and burglary tools. Protesters lit trash cans on fire and wrote graffiti, including the word “abolition” near Foley Square.

A law enforcement source stated: “This is the height of hypocrisy. This girl should be the poster child for white privilege, growing up on the Upper East Side and another home in Connecticut. I wonder how her rich parents feel about their daughter. How would they feel if they graffitied their townhouse?

Revolutionary Abolitionist Movement protesters geared up in Black Bloc take over NYC Streets carrying a “Death to America” and “Free All Prisoners” banners

“No Recovery In Sight”: Container Volumes At The Port Of Los Angeles Flatline Tyler Durden

Mon, 09/07/2020 – 21:00

Submitted by Christopher Dembik, head of macro analysis at Saxo Bank

In today’s edition, we focus once again on global trade and the U.S. economy in these unusual circumstances.

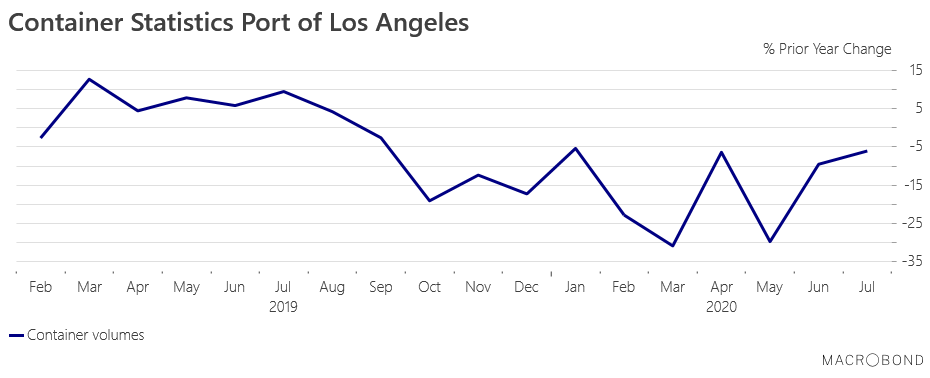

One of our favorite coincident trade indicators is the evolution of container volumes at the Port of Los Angeles. As it is the number one port in the U.S. in terms of container volume and value and the busiest entryway for ocean trade with China, any major change in data could be of great significance for the global and U.S. outlooks.

The least we can say is that the economic panorama has hardly improved in recent months if we rely on shipping data.

YoY statistics about container volumes are still in contraction with the latest figure for July out at minus 6.11% after a lowest point reached at minus 30.94% at the start of the outbreak in March. If we look at the below chart, there is no V-shaped or U-shaped recoveries in sight for the shipping industry but rather a W-shaped recovery.

Despite the effective containment of the outbreak in China, the global supply chain has not fully-recovered and global trade remains hampered by the resurgence of the virus in many countries, notably in some U.S. states, and related economic uncertainty.

The shipping industry will certainly take years to recover from coronavirus. Statistics for the month of August, that should be released around September 15, should confirm the Port of Los Angeles is not out of the woods yet and the economic recovery has reached a plateau in many developed countries, including the U.S., in August, as pointed out by numerous high-frequency data.

via ZeroHedge News https://ift.tt/3h8MKET Tyler Durden

Dear Gavin Newsom, Explain This $hit!!! Tyler Durden

Mon, 09/07/2020 – 20:30

We are sure, somewhere deep down in the bureaucracy of banality that is California’s representative government, there is good reason for each of these ‘policies’… but seriously, one could be forgiven for thinking that the Golden State’s massive liberal majority is just making it up as they go along to punish the most undeserving people the most vociferously.

“It Was Like Stepping On My D*ck”: Jake Tapper Reamed Buzzfeed Ben For Steele Dossier Upstage Tyler Durden

Mon, 09/07/2020 – 20:00

Hours after CNN reported the existence of the now-infamous Steele Dossier on January 10, 2017 – choosing to withhold key details because they hadn’t been “independently corroborated,” BuzzFeed’s Ben Smith decided to kick the door in – publishing the salacious and unverified document funded by Hillary Clinton and the DNC.

The decision seriously pissed off CNN‘s Jake Tapper – who emailed Smith later that day, writing “I think your move makes the story less serious and credible[.] I think you damaged its impact,” according to emails released Friday and reported by the Daily Caller‘s Chuck Ross.

The emails were released in response to a federal judge’s order to unseal documents from a lawsuit against BuzzFeed, which was sued in February 2017 by a Russian businessman who was accused in the dossier of being a Russian agent.

Lawyers for the Russian, Aleksej Gubarev, picked out the Tapper-Smith exchange in hopes of showing BuzzFeed failed to do its due diligence before publishing the dossier, which was funded by Democrats and compiled by former British spy Christopher Steele. –Daily Caller

“That was pretty uncollegial[.] Not to mention irresponsible[.] No one has verified this stuff,” Tapper continued.

Smith replied, saying that publishing the dossier was “not an easy call,” to which Tapper responded “Collegiality wise it was you stepping on my dick,” adding “You could have waited til morning.”

“Professionally this is unverified info[.] Your guys unlike us don’t even seem to know who the former agent i[s],” Tapper continued, seemingly referring to dossier author Christopher Steele.

Smith replied that “of course” he knew who wrote the dossier.

Three years and many investigations later, the Dossier was proven to be a hoax, the FBI was revealed to have spied on Trump’s campaign, manipulated evidence, and lied to the FISA court – and Democrats pivoted to Ukraine in their unsuccessful attempt to remove Trump from office.

via ZeroHedge News https://ift.tt/327F4OU Tyler Durden

Beijing Delays Visas For Journalists From WSJ, CNN & Bloomberg As President Xi Cracks Down On Dissent Tyler Durden

Mon, 09/07/2020 – 19:35

In its latest attack on Western journalists that’s part of both a broader “New Cold War” with the US, and a crackdown on dissent in the aftermath of the pandemic, engineered by President Xi, Beijing is throwing up new roadblocks to stop western journalists from Bloomberg, CNN & WSJ from remaining in China.

The delays were couched as retaliation for the Trump Administration’s latest limitations on visa term limits for reporters working in the US on behalf of state-controlled Chinese press. These organizations have been subjected to myriad new requirements by Trump and the administration in a push to limit electoral interference from Beijing.

Chinese authorities delayed renewing the press credentials of some journalists working for American media outlets, including Bloomberg News, CNN and the Wall Street Journal, in response to the Trump administration limiting visa terms for Chinese reporters in the US.

The journalists in Beijing were told their residence permits will at this stage be extended until Nov. 6, which appears to coincide with the date when the 90-day visas given to Chinese press in the U.S. will need to be renewed. Two non-Americans at Bloomberg News received a letter allowing them to work and stay in the country in lieu of having official press credentials, which in the past were normally good for 12 months.

An organization for foreign correspondents put out a statement slamming Beijing’s decision.

A Bloomberg spokesperson declined to comment. The Foreign Correspondents’ Club of China called on Beijing to reverse the move.

“These coercive practices have again turned accredited foreign journalists in China into pawns in a wider diplomatic conflict,” the group said in a statement Monday. “The FCCC calls on the Chinese government to halt this cycle of tit-for-tat reprisals in what is quickly becoming the darkest year yet for media freedoms.”

A spokesperson for China’s Foreign Ministry played down the delays, saying all the reporters affected would be allowed to stay in China for an extended period.

@StateDept@statedeptspox: You should be honest to tell people since 2018 StateDept has delayed&denied visas of about 30 Chinese journalists&expelled 60 in Mar, limited visas for all Chinese journalists to a max 90-day stay in May&has not approved visa extension of any of them.

#CNN journalist and a few other #US journalists’ visa extension applications are being processed, during which they can continue to live and work here with no problems at all. We’ve made it very clear to your colleagues in Beijing.

As per usual, Beijing denounced the Trump Administration’s latest crackdown on Chinese state media with characteristically aggressive rhetoric.

At a regular news briefing later Monday, Foreign Ministry spokesman Zhao Lijian accused the U.S. of “kidnapping” journalists and taking “hostages” in the dispute. “For China, all options are on the table,” he said, noting that the U.S. had also refused to rule out any actions.

“If the U.S. truly cares about American journalists in China, it should extend the visas for all Chinese journalists as soon as possible instead of kidnapping Chinese and American journalists out of selfish political purposes,” Zhao said.

Beijing has said the U.S. has expelled more than 60 Chinese media personnel and denied visas to more than 20 others. Meanwhile, the FCCC said the Chinese government had forced a record 17 foreign correspondents to leave in the first half of this year and put at least a dozen more on visas as short as one month.

The Trump Administration has frequently taken the lead on curbing the influence of Chinese state-backed media in the US. Social media companies like Twitter have often been more focused on censoring the President and his allies.

California Gov. Gavin Newsom quietly signed a law on Sept. 4 repealing parts of an unpopular law that put independent contractors in the state out of work and limited the earnings of freelancers, including visual artists, musicians, writers, translators, and film support crews by classifying them as employees.

The enactment of the new measure, which came after months of political and legal pressure from the trucking industry, companies such as Uber and Postmates, and groups such as the American Society of Journalists and Authors Inc. and the National Press Photographers Association, is a rare defeat for the labor movement in solidly progressive California.

The new law, known as AB 2257, passed both chambers of the state legislature unanimously on Aug. 31.

The Democratic governor announced on his website Sept. 4 that he had signed the measure but offered no explanation for why he had done so. The governor’s office could not immediately be reached for comment.

The new law took effect immediately upon signing.

AB 2257 amended AB 5, which attempted to determine who is a contractor and who is an employee and forced companies to reclassify their freelancers as employees. The new law provides greater flexibility to freelancers.

When AB 5 took effect Jan. 1, that law made it hard for so-called gig-economy companies to classify people who work for them as independent contractors instead of employees. The idea being the measure was to prevent freelancers from being unfairly exploited by employers.

Assemblywoman Lorena Gonzalez, a San Diego Democrat, wrote AB5 to implement a 2018 California Supreme Court decision known as Dynamex Operations West Inc. v. Superior Court, that deemed many freelancers to be employees, a status that entitled them to the minimum wage, overtime pay, unemployment insurance, and health benefits.

Employees in California are entitled to benefits not available to contractors, such as the minimum wage, health insurance, and paid time off. AB 5 was strongly backed by labor organizations critical of hard-to-unionize freelance jobs. Unions hoped the law would give them an edge in recruiting new members.

AB 5 was enacted ostensibly to help workers by preventing their “misclassification” as non-employees.

It adopted the so-called “ABC” test to determine employee status, according to the Economic Policy Institute (EPI). The test stipulates that workers may only be considered independent contractors when a business proves the workers:

“a. Are free from control and direction by the hiring company;

b. Perform work outside the usual course of business of the hiring entity;

and c. Are independently established in that trade, occupation, or business.”

But mere weeks after the enactment of AB 5, which is still being challenged in the courts, the law ran into headwinds as freelance workers and others in a state with many independent contractors suddenly found themselves out of work or with their ability to earn a living severely restricted.

It stopped freelance writers from accepting more than 35 assignments from a single publisher and hindered the ability of musicians to accept regular paying gigs. Companies outside California stopped using freelancers in the state as they feared financial penalties for violating the law.

Gonzalez admitted there were problems back in February.

Gonzalez wrote in a Feb. 6 tweet that she was willing to consider easing the restriction affecting journalists. “Based on dozens of meetings with freelance journalists & photographers, we have submitted language to legislative counsel that … will cut out the 35 [articles] submission cap & instead more clearly define freelancer journalism,” she wrote.

Later in the month she reported progress on writing what turned out to be AB 2257.

“Having heard additional feedback from a variety of freelance writers, photographers and journalists, we are making changes to Assembly Bill 5 that accommodate their needs and still provide protections from misclassification,” she said February 27.

AB 2257 abolishes the 35 item submission limit for writers and photographers contained in AB 5. It also exempts translators, appraisers, and registered foresters from the restrictions.

Gig-economy companies are supporting a state ballot initiative this Nov. 3, Proposition 22, that would treat app-based drivers as independent contractors, not as employees.

via ZeroHedge News https://ift.tt/3ic5Jj9 Tyler Durden

Goldman Warns Of “Near-Term Setback” For Stocks As Record Bullish Nasdaq Sentiment Suffers Near-Record Shock Tyler Durden

Mon, 09/07/2020 – 18:45

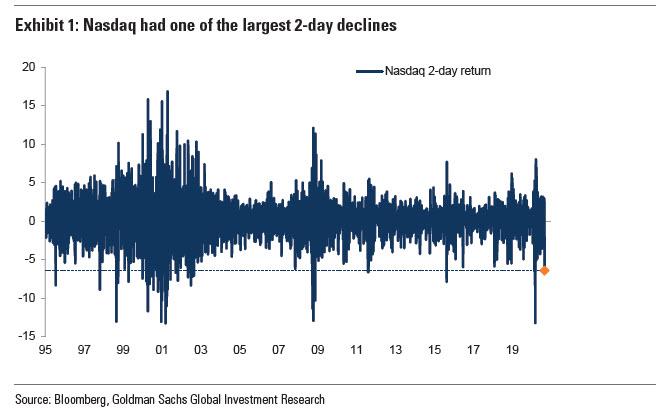

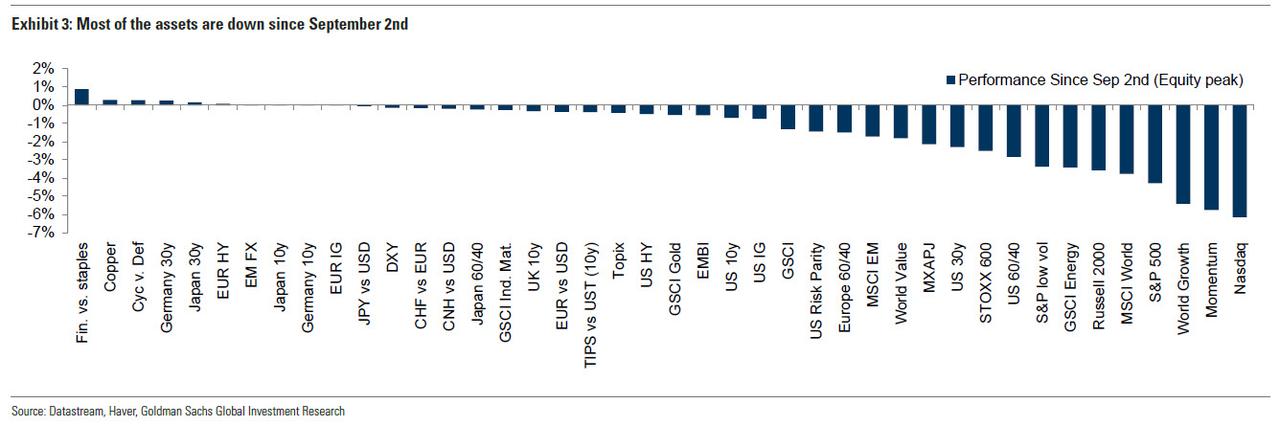

In a stark reminder of the market excesses reached last week, Goldman writes that the Nasdaq had one of the largest 2-day declines in the last 30 years after the SoftBank gamma trade was exposed.

Meanwhile, the sheer buying frenzy into this plunge was unprecedented, and was characterized by a significant increase in options positioning into US equity and US Tech in particular, with the put/call ratio in the US reaching a historical low, the single stock skew back to pre-Covid levels and the spot-vol correlation turned into positive territory. “Such stretched option positioning has historically highlighted a negative asymmetry of near-term equity returns”, Goldman writes, pointing out that Nasdaq net equity future positioning at the peak was close to historical highs.

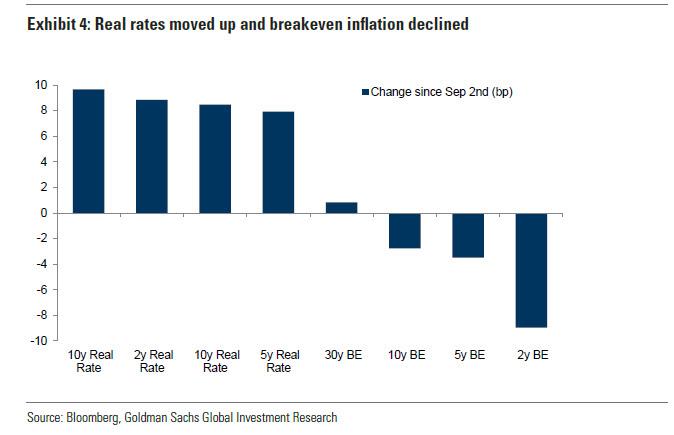

The silver lining is that as the meltup breadth was relatively narrow, so was the selloff, and here a key catalyst in addition to merely positional unwind is that the US 10y real rates increase (+8bps since the lows) “has likely triggered a rotation out of longer duration equities such as ‘Growth’ and Tech.”

Echoing what we said in our discussion of the unprecedented divergence between real rates and breakevens, Goldman points out that with nominal yields being anchored by central banks, “breakeven rates and real rates are more likely to move in opposite direction” adding that “while phases of increasing breakeven rates coupled with lower real rates are usually very friendly for both risky assets and safe assets, lower breakeven rates and higher real rates tend to be very negative for markets as all assets typically decline.” In line with this framework, since Sep. 2 most assets are down and multi-asset investors struggled to diversify the correction.

This also means that amid the gamma trade unwind, the dollar performance, usually positive in this environment, was mixed given the resilience of EM FX.

Nonetheless, despite conceding that the risk of corrections remains elevated, and warning that “a near-term setback” is likely, Goldman expects the current bull market to continue “as the improved growth outlook coupled with supportive monetary policies should maintain the search for yield elevated and foster a compression of the ERPs.” Specifically, Goldman lists the following ten reasons why despite one of the biggest 2-day crashes in the Nasdaq on record, the levitation will continue:

We are in the first phase of a new investment cycle, following a deep recession. The ‘Hope’ phase – the first part of a new cycle, which usually begins in a recession as investors start to anticipate a recovery, is typically the strongest part of the cycle. That is what we have been seeing this year.

The economic recovery looks more durable as vaccines become more likely.

Goldman economists have recently made upward revisions to their economic forecasts and it is likely that analysts’ expectations will follow.

The bank’s Bear Market Indicator (which was at very elevated levels in 2019) is pointing to relatively low risks of a bear market despite very high valuations.

Policy support remains very supportive for risk assets. There is both a central bank ‘put’ – a belief that central banks will be there to provide as much liquidity as is required – and a fiscal ‘put’ as governments have scaled up their willingness to support growth.

The Equity Risk Premium has room to fall.

The resumption of zero nominal interest rate policy in the recent past, together with the extended forward guidance, has created an environment of greater negative real interest rates. This should be highly supportive to risk assets in an economic recovery.

Equities offer a reasonable hedge to higher inflation expectations.

Equities look cheap relative to corporate debt, particularly for strong balance sheet companies (60% of US companies and 80% of European companies have dividend yields above the average corporate bond yield).

The digital revolution continues to gather pace. We think this transformation of the economy and stock markets has further to go. These companies could continue to drive valuations and returns in this bull market.

via ZeroHedge News https://ift.tt/3jVzoxE Tyler Durden

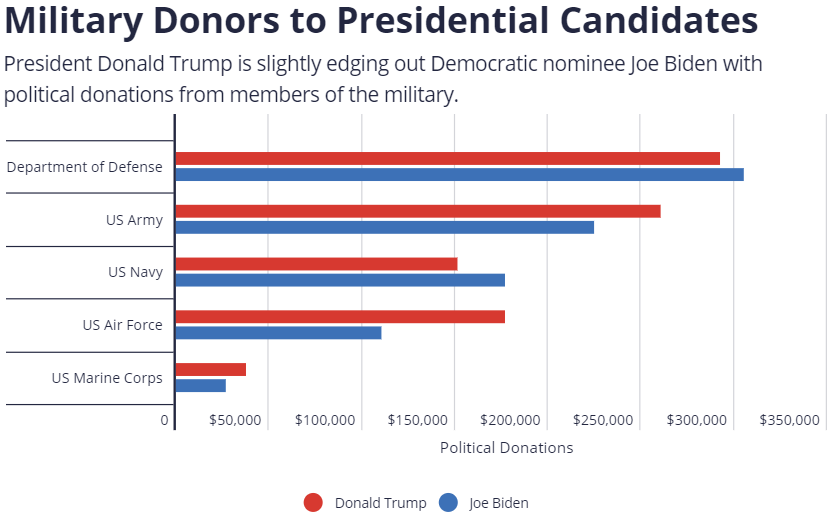

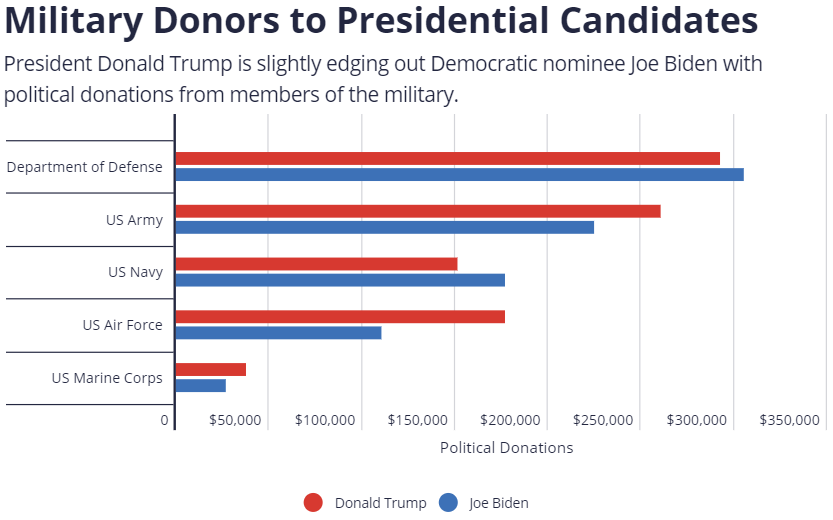

President Donald Trump is edging out Democratic nominee Joe Biden in political donations from members of the military, even as more U.S. troops say they would vote for Biden over their current commander in chief.

Trump has raisednearly $1.1 million from military members, compared to roughly $859,000 for Biden. Trump receives far more campaign cash from members of the U.S. Air Force and beats out Biden among members of the U.S. Army and U.S. Marine Corps. Biden fares better with members of the Department of Defense and U.S. Navy.

President Donald Trump salutes graduates at the U.S. Air Force Academy-Falcon Stadium in Colorado Springs, Colo. last year. Image: Official White House Photo

The president’s campaign cash lead with military donors was much higher when earlier this cycle when he had a larger overall fundraising advantage over Biden. That narrow lead could continue to slip when the campaigns officially report their August fundraising figures, as Biden raised record money last month.

Trump has claimed he has strong support from the military, touting pay raises he and Congress authorized for active-duty troops. But a recent Military Times poll found that Biden leads Trump by 4 points among active-duty troops. Roughly 38 percent of active-duty troops said they had a favorable view of Trump, compared to 50 percent holding an unfavorable view of the president.

The president’s support with the military has declined during the course of his presidency. A 2016 Military Times poll found that Trump had a 2-to-1 lead over then Democratic nominee Hillary Clinton. At the start of his presidency, Trump’s approval with troops sat at 46 percent. His decline has come amid criticism from former high-ranking defense officials. The most shocking rebuke came from former Secretary of Defense James Mattis, who described the president as a threat to the Constitution after Trump sent troops into Washington, D.C., to quell protests.

Via OpenSecrets.org

Citing anonymous officials at the Defense Department and U.S. Marine Corps, The Atlantic reported last week that Trump described dead American troops as “losers” and “suckers.”

Trump strongly denied the report, calling it “Fake News.” Trump has previously disparaged military heroes in front of large audiences, including the late Sen. John McCain (R-Ariz.), saying in 2015, “I like people who weren’t captured.” He’s also publicly feuded with Gold Star families.

Biden does best compared to Trump with donors from the U.S. Navy. Trump clashed with Navy leadership and fired Navy Secretary Richard Spencer over the department’s handling of a Navy Seal accused of war crimes who was pardoned by Trump. Trump also fired a Navy captain who wrote a letter to military leadership asking for help with a COVID-19 outbreak on his warship. That captain, Brett Crozier, received a roaring applause from his crew when he left the ship.

TRUMP: “I’m not saying the military’s in love with me. The soldiers are. The top people in the Pentagon probably aren’t because they want to do nothing but fight wars, so all of those wonderful companies that make the bombs and make the planes and make everything else stay happy”

Biden has sought to make inroads with former military officials who have expressed disgust with Trump’s presidency. More than 70 former senior national security officials, all Republicans, endorsed Biden last month, calling Trump “unfit to lead.”

Former Secretary of State and four-star general Colin Powell endorsed Biden during the Democratic National Convention, calling the Democrat “a president we will all be proud to salute.” Trump responded on Twitter by calling Powell “a real stiff who was responsible for getting us into the disastrous Middle East Wars.”

via ZeroHedge News https://ift.tt/3lYKOT1 Tyler Durden

{kind=link}

{kind=link}