This somewhat provocational act comes just hours after North Korea told a White House official that working-level meetings between the U.S. and North Korea will restart “very soon,” a Trump administration official told reporters Tuesday.

Developing…

via ZeroHedge News https://ift.tt/2ZjUtI0 Tyler Durden

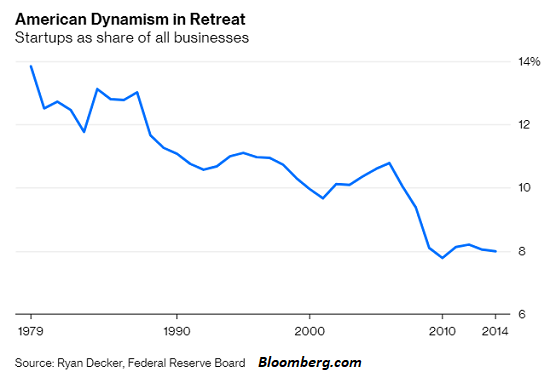

Small businesses on the precipice need only one small shove to go over the edge, and there won’t be replacements filling the fast-multiplying empty storefronts.

As a generality, the average employee (including financial pundits) has no real experience or understanding of what it takes to start and operate a small business in the U.S. Government employees in the agencies that oversee and enforce regulations on small businesses also generally lack any experience in the businesses they regulate.

A third generality is the endlessly promoted ethos of entrepreneurism cultivates the illusion that there is an essentially endless supply of entrepreneurs who are itching to start businesses and throw everything they have into the risky gamble.

All we ever hear when a restaurant owner is interviewed is how much they love their business, their work, their customers, their neighborhood, etc. etc. Sadly, enthusiasm isn’t enough to pay the rent when belt-tightening reduces sales while costs notch ever higher.

The story plays out the same everywhere; the only variation is the relative scale of the costs that are squeezing small businesses and the limits on how much they can raise prices:

For those of you who don’t read the entire article: one cafe owner reports that she netted a whopping $5,000 in a good year, her entrepreneurial payoff for working insane hours and putting up with the ceaseless grind of keeping her business afloat.

The reality is very few people have the drive, risk appetite, capital and experience to start and operate a small business. Once this pool of people has been exhausted or bankrupted, the number of new small businesses plummets and does not recover.

Another reality is a great many bricks-and-mortar Main Street businesses are on the precipice of closing. There are two primary drivers of this systemic vulnerability:

1. Costs are rising far faster than enterprises’ ability to raise prices for the goods and services they sell

2. Wages and salaries (earned income) has stagnated for the past 20 years for the lower 95% of households while costs of big-ticket expenses such as rent, healthcare, college, childcare and government services and taxes have risen sharply.

This leaves less discretionary income available to spend on non-essentials, i.e. “experience consumption.”

Simply put, small business expenses are rising while their customers’ stagnating income means there is little leeway to raise prices. Small business is in a vise.

There’s another dynamic in bricks-and-mortar businesses that must rent commercial space. The bubble in real estate valuations has spread to commercial real estate in many if not most urban areas, but certainly to every urban area with a vibrant job market–exactly the sort of place that attracts those willing to start a new business.

If a retail building was worth $1 million a decade ago, and now it sold for $3 million, the new owners naturally expect rents to cover all expenses and yield a 5% return on their investment.

The new owners don’t think of themselves as greedy; a 5% return on capital is conservative.

The higher price doesn’t just increase the size of the mortgage and the monthly payments; it also increases the property taxes due. Since the fees charged for government services are soaring, business licenses, permits, etc. have also increased far faster than official inflation.

For the investment to pencil out for the new owner who paid $3 million for the building, the rent for each space has to triple from $1,000 a month to $3,000 a month.

How many small businesses can afford a doubling or tripling of rent? Since wages, healthcare, licenses, permits, etc. have increased dramatically while the ability to raise prices has been constrained, many small businesses can’t afford even a 20% increase in rent, never mind 200%.

(Note on interest rates: even if the interest rate on the commercial-property mortgage declined a bit, that doesn’t offset the much larger principal payment required since the mortgage tripled in size, nor does it reduce the property taxes or other fixed costs. In other words, the interest part of the owners’ monthly expenses is not the key metric.)

Now let’s factor in a recession or slowdown, a period of consumer belt-tightening that causes revenues to drop.

A great many Main Street businesses paying market rents are only making money in the very best of times. Any slowdown, however modest, pushes them into the red.

If they expect revenues to pick up in a month or two, small business owners will absorb losses, cut the hours of employees, work longer hours, etc. But if the revenues don’t recover while expenses click higher, the entrepreneur eventually has no choice: either close down now or go broke via the drip of monthly losses.

Once the slowdown is undeniable, no one with any moxie is going to step up and pay market rent on the vacant space. The inexperienced souls who try their hand in the new space will be bankrupted in a matter of months by the high rent.

The building owners are loathe to drop the rent from $3,000 a month to $2,800, much less to $2,000 a month. Yet the reality is that no small business can afford more than $1,000 a month.

The building owners are caught in their own vise: they need rents close to $3,000/month to cover their expenses, and so dropping rents to what small businesses can afford will result in horrendous monthly losses. But leaving the spaces vacant generates losses, too.

The only way out is to default on the mortgage and abandon the building to the lender, who then faces enormous losses because the building is no longer worth $3 million since rents have crashed.

Neither the commercial building owners nor the small business tenants have any wiggle room. The only alternative to increasing losses each has is to close down the business / sell the building for a huge loss or default on the mortgage.

All the increasing costs are famously sticky: wages don’t go down, healthcare costs don’t go down, city fees don’t go down, and rent goes down only grudgingly, in increments too small to save small businesses operating in the red.

And since the pool of experienced entrepreneurs is small (and shrinking as people burn out, go bankrupt, retire, etc.), the empty storefronts will stay empty for a long, long time– until rents drop back to levels that enable small businesses to make a profit in recessionary times.

Nobody wants to see building valuations decline by 2/3 or more: cities, lenders and investors all want valuations to notch higher or at least remain stable. But bubble-era valuations lead to rents that are completely unaffordable, so small businesses will close, resulting in the rental income dropping to $0 per month.

Since all the costs are sticky and expectations are wildly unrealistic, there is no painless way forward.

Small businesses on the precipice need only one small shove to go over the edge, and there won’t be replacements filling the fast-multiplying empty storefronts. The hurdles, costs and risks of starting a new enterprise notch ever higher while the rewards diminish. No wonder startups are in systemic decline: we’ve made it so difficult to start and operate a small business that few have the skills, stamina and capital to survive, much less thrive.

Blowing a real estate bubble that crushed small business may well be viewed in hindsight as the Federal Reserve’s cruelest and most destructive policy error.

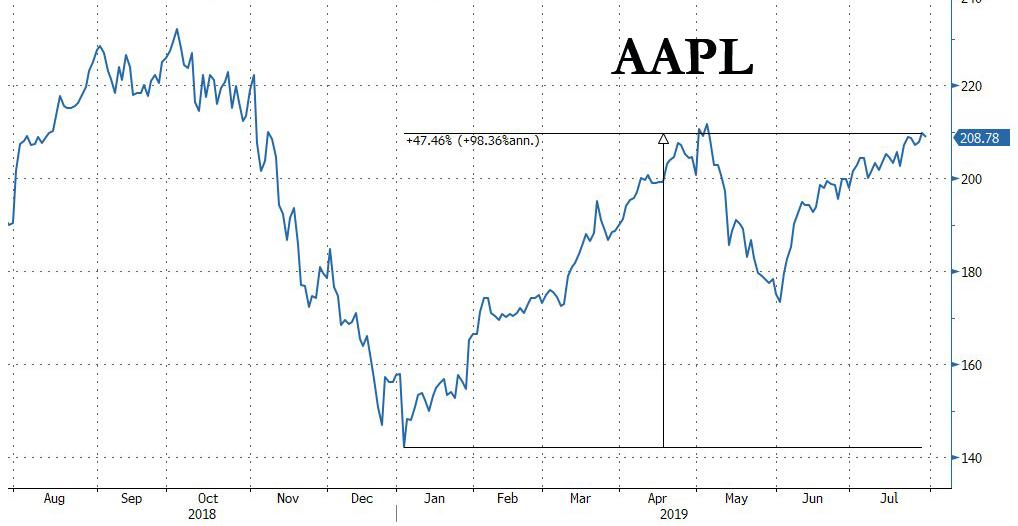

First, three quarters ago, Apple shocked investors when it said it would no longer disclose the number of iPhones it was selling – a clear signal that selling had slowed dramatically. Shocked investors sold off the stocks… then BTFD with gusto sending AAPL sharply higher. A few months later, on January 3 2019, Apple once again shocked the market when it slashed its revenue guidance by 8% for only the first time since this century (naturally, it blamed China). As AAPL stock tumbled, it reveberated across all capital markets, and even prompted a flash crash cascade in most yen and pound pairs. However, just like a quarter earlier, Apple’s “shock” was quickly overcome, and the after hours plunge actually marked the max pain for longs, and as the chart below shows, AAPL has soared 46%. And to think all it had to do was slash revenue guidance..

Then, last quarter, as largely expected, Apple reported that iPhone sales had indeed slumped, but the reason why the market kept bidding up the stocks, was the company’s effervescent outlook, which while declining on a year over year basis, was well above sellside consensus, dispelling fears of a growth slump and boosting hopes that Apple is successfully transitioning to a services company (the new $75 billion stock buyback repurchase authorization did not hurt). As a result, heading into its third quarter, AAPL stocks was trading near the highest levels of the year, and not too far from its all time highs.

So with US-China trade talks resuming today, Trump’s twitter rant notwithstanding, everyone’s attention was glued to the Apple earnings report at 430pm ET to see if all the optimism over the past 3 quarters would be justified. The answer appears to be yes, because moments ago, Apple reported that in fiscal Q3, it beat both revenue and EPS earnings:

Q3 EPS: $2.18, Exp. $2.10

Q3 Revenue: $53.8BN, Exp. $53.35BN

Q3 Gross Margin $20.23BN

Q3 Product revenue: $42.35 billion

Apple also announced that it had repurchased a whopping $17BN in stock in the quarter, and spent $3.6BN on dividends.

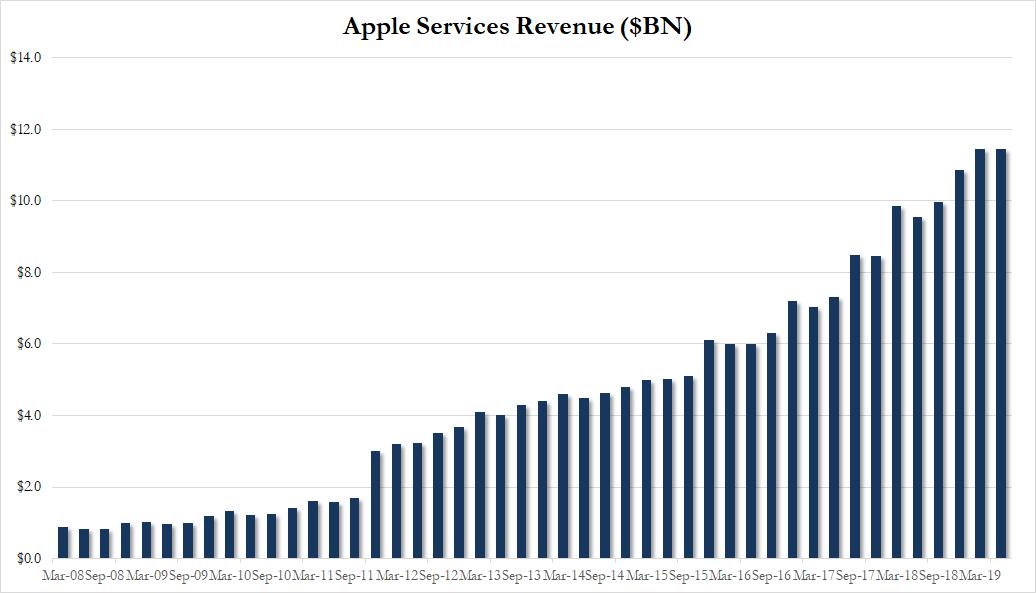

While Apple beating on earnings was great news (and the extravagant buyback certainly did not hurt), less impressive was Apple’s iPhone revenue, which came in at $25.986BN, below the $26.45BN expected, and well below the $29.5 billion from a year ago, as well as the slight miss in services revenue which came in at $11.46BN, below the $11.88BN consensus.

Another disappointing data point: China revenue came in at $9.16BN, down 4.1% Y/Y.

However, the reason why the stock is some 3% higher after hours was largely due to the company’s revenue and gross margin outlook, which came in well above the Sellside estimate:

Q4 revenue between $61 and $64 billion, exp. $61.04BN

Q4 gross margin between 37.5% and 38.5%, exp. 37.5%

Commenting on the earnings, Apple CFO Luca Maestri said that “Our year-over-year business performance improved compared to the March quarter and drove strong operating cash flow of $11.6 billion. We returned over $21 billion to shareholders during the quarter, including $17 billion through open market repurchases of almost 88 million Apple shares, and $3.6 billion in dividends and equivalents.”

Looking at the company’s increasingly important service revenue number, Apple reported $11.46BN in service revenue, up from $10.2BN a year ago, but below the $11.88BN expected by analysts, and virtually unchanged from the prior quarter.

So the bottom line: a modest profit beat, coupled with weaker than expected iPhone and Services revenue, offset by very strong guidance, which is enough to push AAPL stock 3.5% higher to $216 after hours.

via ZeroHedge News https://ift.tt/2GPM2x9 Tyler Durden

Oil rallied notably today as traders anticipated a growth jolt from The Fed tomorrow and tensions remain in the MidEast as Iran threatened to choke supplies.

“The crude oil market loves trade headlines,”

“Even if they were negative earlier in the day, at the end of the day the countries are trying to make a deal happen. They’re not there to fail, and that supports oil.”

API

Crude -6.024mm (-2.75mm exp)

Cushing -1.449mm

Gasoline -3.135mm

Distillates -890k

After the prior week’s shockingly large draw, crude inventories were expected to modestly drop further but once again surprised to the downside with a bigger-than-expected 6mm drop in stocks (and big draw in gasoline also)…

WTI had surged back above $58 ahead of the API print and extended gains after the surprise API Print

via ZeroHedge News https://ift.tt/2SW8auy Tyler Durden

Just one day before convicted pedophile Jeffrey Epstein was found in his jail cell with mysterious injuries, the accused child sex-trafficker was served with legal documentsclaiming that he forcibly raped a 15-year-old girl in his New York mansion in 2001, according to CNBC.

The accuser, Jennifer Araoz, plans to sue Epstein next month for claims of sexual assault, battery and rape, which she alleges he started committing when she was a New York high school student in 2001, according to a court filing earlier this month.

But first, Araoz is asking a judge to order Epstein to submit to a deposition, where he can be asked by Araoz’s lawyers the identity of a female “recruiter”who allegedly conspired with him to identify her “as a potential sexual abuse victim” and “facilitated the grooming” of Araoz. –CNBC

Araoz first detailed the alleged sexual assault on July 10, days after Epstein’s arrest.

Epstein gave her a tour of his mansion that culminated in a visit to what he described as his “favorite room in the house,” Araoz said. A massage table sat on the floor. A painting of a nude young woman hung from the wall.

Araoz would return to that room regularly over the next year, she said, manipulated into stripping down to her panties and giving Epstein massages that ended with him pleasuring himself to completion and her leaving with $300.

In the fall of 2002, Epstein pressured her to do more, Araoz said. He told her to remove her panties. Then he grabbed her 15-year-old body.

“I was terrified, and I was telling him to stop. ‘Please stop,’” Araoz, now 32, added.

“Upon identification of the recruiter, she will be added as a defendant to” Araoz’s pending lawsuit. “Further, the recruiter possesses critical evidence of [Araoz’s] sexual assault claims,” reads the filing.

The unnamed recruiter is undoubtedly Ghislaine Maxwell, who has been accused by several women of actively seeking out young women to satisfy Epstein’s sexual desires. Among others, Maxwell was accused by allgeged Epstein victim Virginia Giuffre of recruiting the then-15-year-old into sexual slavery while she was working at a towel girl at President Trump’s Mar-a-Lago club.

Araoz’s filing also requests that a judge order Epstein to produce records of who worked for him between 2000 and 2003, as well as logs of “everyone who entered or exited his” Upper East Side townhouse over the same period.

A New York City Sheriff’s Office official gave Epstein — a former friend of Presidents Donald Trump and Bill Clinton — copies of that request and related documents on July 22 at the Metropolitan Correctional Center, according to an affidavit filed Monday in Manhattan Supreme Court.

A day after he was given the court documents, Epstein was found injured and semi-conscious on the floor of his cell, with marks on his neck. He then was was put on suicide watch. –CNBC

According to a lawyer for one of Epstein’s victims, the financier may have been injured in an attempted ‘hit’ in order to prevent him from implicating powerful people who may have participated in his sexual deviance.

A lawyer for the now-32-year-old Araoz said “Jennifer endured unspeakable abuse by Jeffrey Epstein and his enablers, who robbed her of a piece of her childhood,” adding “She brought this action to hold those responsible accountable and deliver a simple message: she’s not afraid anymore.”

via ZeroHedge News https://ift.tt/2yrwTxj Tyler Durden

China stocks dipped in the afternoon after a morning buying panic…

UK stocks limped lower, outperforming the rest of Europe as its currency crumbled…

European Bank stocks dropped back into the red for 2019 again…

US markets were mixed with Small Cap soaring off early weakness but the rest of the majors ending red with Nasdaq worst…

NOTE – Trannies spiked at the close into the green barely.

Is a Fed rate-cut enough to make new highs in stocks… just like we did in 1987…

Small Caps were saved by another huge short-squeeze…

BYND was battered…

And Under Armor was hammered…

VIX is about to enter the riskiest part of the year…

Another extremely narrow range day in Treasuries that ended with yields down 1-2bps across the curve…

The Dollar Index trod water on the day

Cable continued its slide (down 7 of the last 8 days) – heading for its worst month since Oct 2016…

NOTE – this will be the lowest monthly close for sterling since Jan 1985

Cryptos rallied on the day led by Bitcoin Cash (Bitcoin remains below $10k)…

Oil prices spiked today as China trade talks and Iran tensions raised premia as copper crumbled, PMs both rallied…

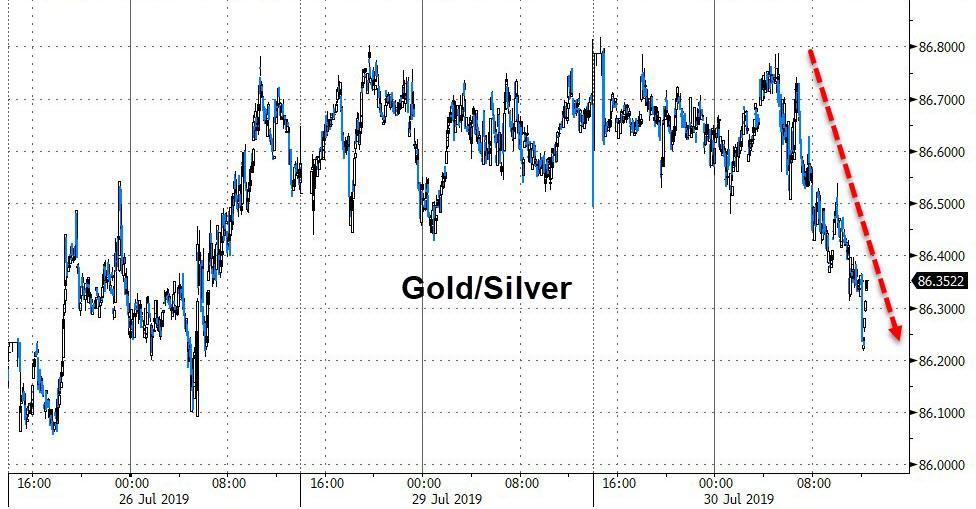

Silver outperformed Gold again…

Speculators are piling into the silver-options market as the precious metal returns to the limelight ahead of the Federal Reserve meeting, where policy makers are widely expected to cut borrowing costs.

As Bloomberg’s Nancy Moran and Michael Roschnotti notes, the combined volume of calls and puts has surged above 218,000 contracts this month, on course for the highest since November 2010. The bulls driving the trading are of the mind the commodity will catch up to the gains of its pricier cousin gold, while the bears are counting on weakening global manufacturing to hurt industrial demand.

WTI spiked back above $58 ahead of tonight’s API inventory data…

Finally, given the market’s expectations of at least a 25bps cut tomorrow, one wonders what the point is when global financial conditions are back at extreme easy levels…

Data-dependent my left nut!!

via ZeroHedge News https://ift.tt/2Yh2Jfq Tyler Durden

We’re thrilled to see the far-left in America has the same respect for the Democratic process as their forebears did (for a reference to their forebears, see here).

On Tuesday, Calif. Gov. Gavin Newsom signed a bill requiring President Trump to either release his tax returns or he won’t appear on the ballot in the state.

Calif Gov. Gavin Newsom

Under SB 27, called the “Presidential Tax Transparency and Accountability Act,” any candidate running for president or governor in California must file copies of their tax returns from the previous five years to the California secretary of State, or their names will be stricken from the ballot, the Hill reports.

Newsom argued that, as the largest economic engine within the US, California has a “responsibility” to demand this additional information (for the record: the Constitution doesn’t say anything about candidates releasing tax returns – though the federal income tax didn’t exist back on).

“As one of the largest economies in the world and home to one in nine Americans eligible to vote, California has a special responsibility to require this information of presidential and gubernatorial candidates,” Newsom said.

“These are extraordinary times and states have a legal and moral duty to do everything in their power to ensure leaders seeking the highest offices meet minimal standards, and to restore public confidence. The disclosure required by this bill will shed light on conflicts of interest, self-dealing, or influence from domestic and foreign business interest.”

A Trump campaign spokesman called the new law “unconstitutional,” and insisted that there was a good reason why California’s last governor, Jerry Brown, refused to sign the legislation.

In a statement, Trump campaign spokesman Tim Murtaugh called the move “unconstitutional.”

“There are very good reasons why the very liberal Gov. Jerry Brown vetoed this bill two years ago – it’s unconstitutional and it opens up the possibility for states to load up more requirements on candidates in future elections. What’s next, five years of health records?” he said.

Murtaugh said states cannot add requirements to presidential candidates’ qualifications for running.

“The Constitution is clear on the qualifications for someone to serve as president and states cannot add additional requirements on their own,” he said. “The bill also violates the 1st Amendment right of association since California can’t tell political parties which candidates their members can or cannot vote for in a primary election.”

Unsurprisingly, the bill was overwhelmingly passed by California’s assembly and the state senate earlier this month. Among its more appalling provisions, the bill includes an “urgency clause”, which would allow it to take effect before the 2020 vote, meaning any Californians who want to vote for President Trump might need to write his name in.

Though it has faded from the headlines somewhat, the battle over Trump’s tax returns continues to rage. The administration is already suing New York State, which recently passed a law allowing the state to request Trump’s tax returns, while in Congress, the Ways and Means Committee has filed a lawsuit over the administration’s refusal to release Trump’s returns, which is likely the beginning of a lengthy legal battle.

Surprisingly, Trump was joined in his outrage by some liberal pundits who have stood out for their opposition to Trump’s ideas.

This remains a terrible, anti-democratic idea and California should be embarassed. https://t.co/dYHAEtrnE5

We imagine California won’t be the last state to pass such a bill, but given Trump’s deep unpopularity throughout most of the state, he was unlikely to win any delegates from California: Imagine what will happen when swing states like Colorado and New Hampshire start trying to pass these types of laws?

And finally….

via ZeroHedge News https://ift.tt/2GAjF5W Tyler Durden

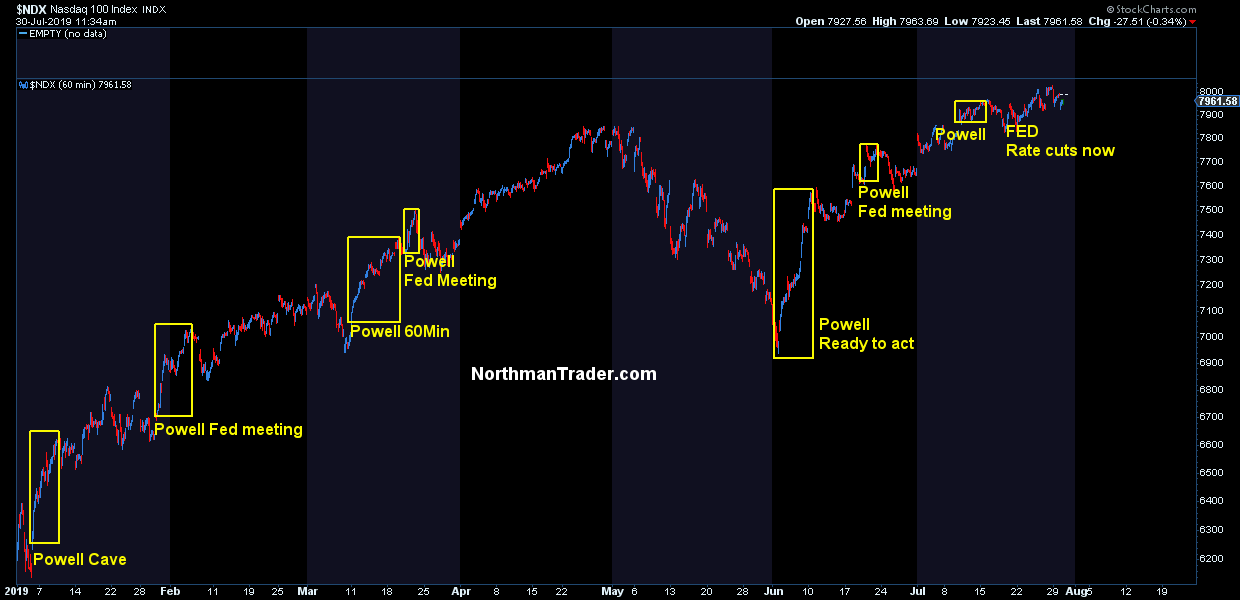

The circus is back in town and it’s putting on a major show, the rate cut show.

Some thoughts for your consideration:

Firstly, the expectation is for a 25bp rate cut. That’s what all signaling by the Fed has led to. That’s the market’s expectation. There is no way, no how, that they will not cut. The risk of stock market carnage would be to high. They can simply not afford to disappoint markets. Fact is a market sell-off of size would virtually set the stage for a massive reversal in confidence which in turn could be self fulfilling given slower growth.

One other piece of evidence: The Fed’s in a blackout period. Cute then that they paraded out Greenspan and Yellen in the past couple of days to give cover for a rate cut. Don’t think this was not done without behind the scenes approval and encouragement. Everything is a big game of managing expectations.

Powell has already declared that their goal is to extend the business cycle which, by the way, is a monumentally bad idea in my view because the only way they can extend the business cycle is by deepening the market bubble.

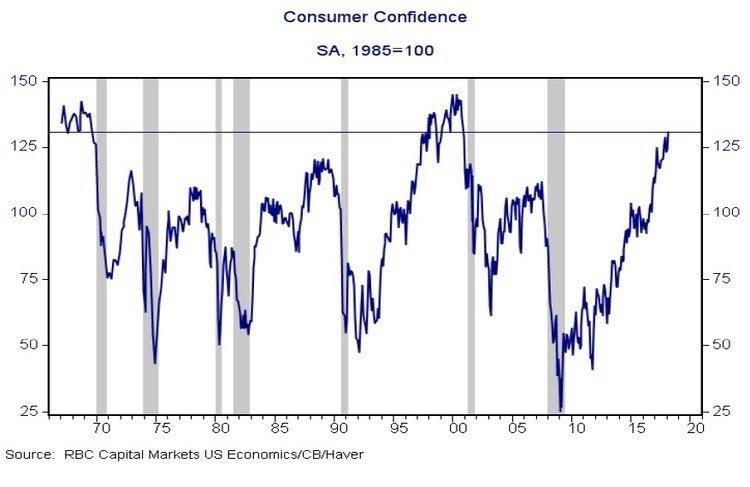

Cut rates here with consumer confidence at 135.7?

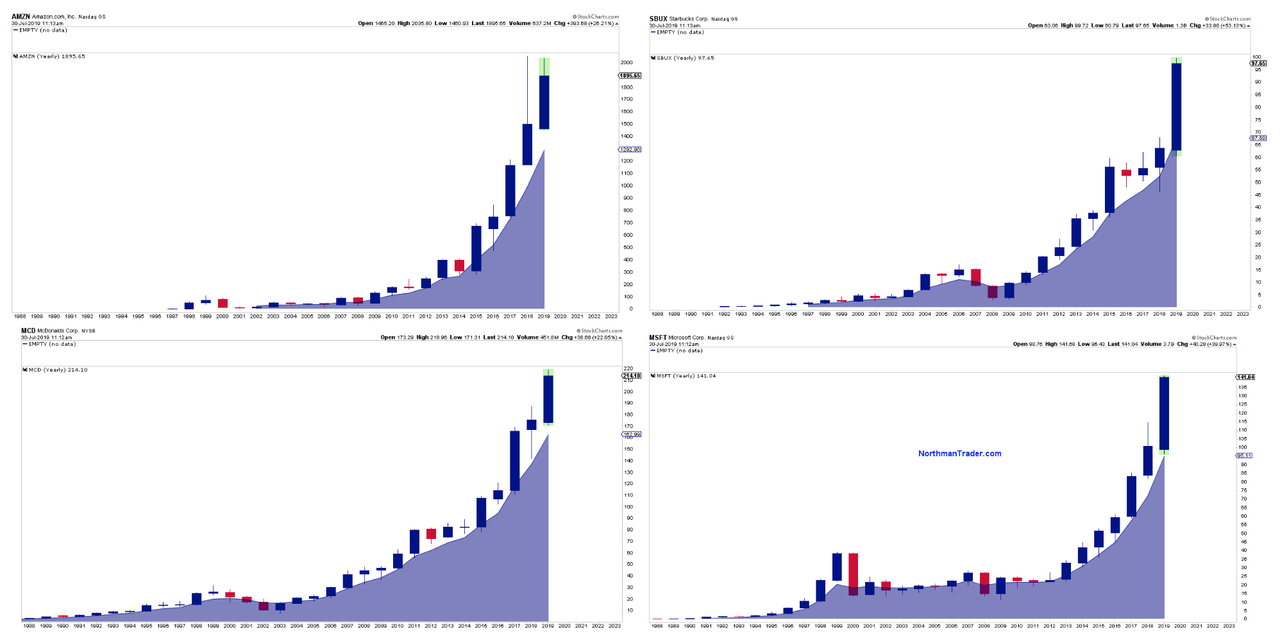

Cut rates here with key market cap stocks massively and historically extended after having rallied virtually non stop for 10 years?

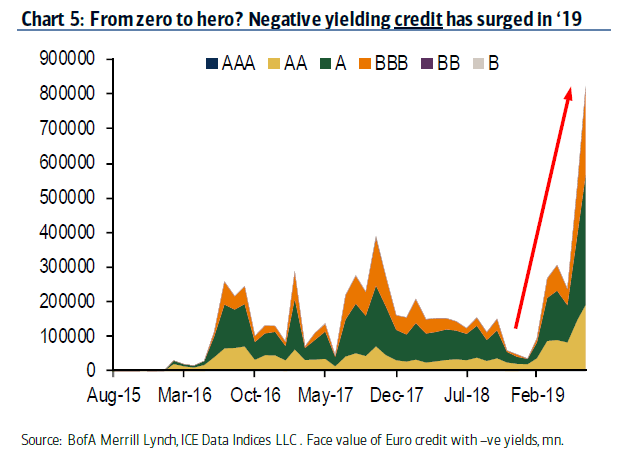

Everything is distorted and propped up by central banks and it’s causing massive dislocations, look no further than European bonds:

About €825bn of corporate debt in Europe now trades with negative yields, a chunk of that is rated triple-B.

When markets do extreme things that are completely outside the norm of history everybody better pay attention. Dislocations lead to relocations.

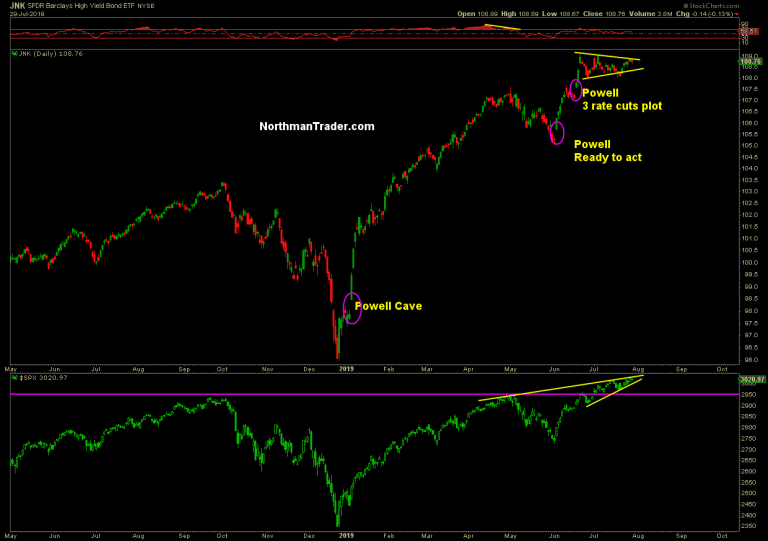

And let’s be clear without the surge in high yield credit this year stock markets wouldn’t be anywhere near here.

For the Fed it has to be all about not disappointing and managing market expectations. What if they cut 25bp and they have 1,2 or even 3 dissenters on the vote?

Markets don’t like an internal Fed fight. Rosengren wants to wait he said on Friday.

And you know what? Cutting in my view is a mistake here from a managing the economy perspective. From a managing the stock market perspective it makes sense to cut, from an economy perspective it’s a mistake. Why? Again, the Fed has limited ammunition, it should use it judiciously and not waste it on insurance. If you have limited ammunition, make it count, a big bang, shock and awe if you will.

If the slowdown is persisting, and CAPEX, business investment and global PMIs are telling you that a recession is coming and not an expansion, then you better have all the ammunition available to you to combat that. But US data has been beating on some key reports, so why diddle with a 25bp cut here? Because you are beholden to the market’s reaction and can’t disappoint. Well, that’s just pitiful.

But if the threat is real, and suppose you even have a peek at Friday’s job’s numbers ahead of time and you see bad news coming down the pike, then it may make sense to shock the market right here and there and do a 50bp cut even though you dialed back expectations for a 50bp rate cut following the William’s speech.

Here’s the evil alternative: Maybe, just maybe, the Fed wanted to surprise markets with a 50bp rate cut and Williams bollixed it up when he gave his speech and expectations were moving in the 50bp direction. In this context suddenly it made sense why the Fed came out and dialed back expectations. Now 80% think it’s a 25 bp rate cut so mission accomplished.

But there’s a problem with a 50bp rate cut, while perhaps causing another market rally on the surprise the underlying message is one of panic. Things are worse than they seem, the ghosts of 2001 and 2007 would make their presence felt and that could be damaging to confidence, and when you damage confidence you lose buyers or, worse, invite sellers.

Bottomline:

If it’s a decision to manage markets they need to cut either 25bp or 50bp.

If it’s a decision to manage the economy they shouldn’t cut yet. Why? Because they have limited ammunition & need to make it count when it matters.

They can’t afford frivolous cuts.

The irony: If they don’t cut to appease marktes, markets would sell off hard resulting in an adverse economic reaction & loss of confidence forcing to Fed to cut rates.

Nice circle jerk they got themselves into.

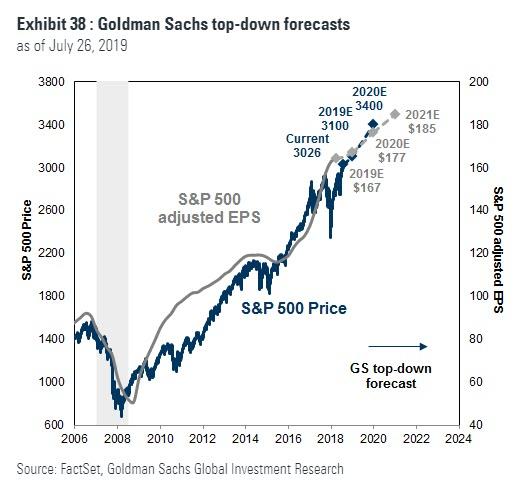

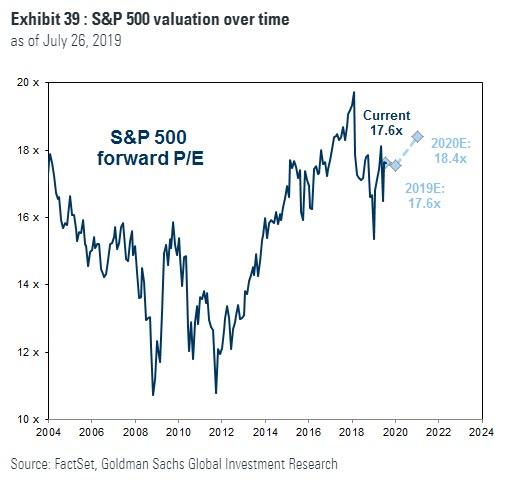

But no worry, Wall Street sees no downside either way, only multiple expansion. Case in point: Goldman raised its price target today for $SPX, 3,100 in 2019 and 3,400 in 2020. Their rationale: Not earnings expansion, no Sir, rather it’s earnings growth reduction and multiple expansion courtesy the Fed:

“David Kostin, the bank’s chief U.S. equity analyst raised his target for the S&P 500 stock index despite lowering his estimate for 2019 earnings-per-share growth from its November estimate of 6% to 3% today, resulting in a higher expected price-to-earnings ratio.

“Our target implies a 3% appreciation through year-end 2019, implying a 24% fully year-gain,” Kostin wrote. “Valuation models have expanded by 22% year-to-date, and the S&P 500 trades at roughly fair value relative to interest rates and profitability.”

Goldman analysts now predicts the S&P 500 forward price-to-earnings multiple will end the year at 17.6 times earnings, a marked increase from the 16 times predicted in their 2019 outlook published in November.

The bank sees Federal Reserve policy as a key driver of higher valuations, as it earlier predicted the Fed would raise interest rates 100 basis points in 2019, but now see the fed funds rate ending the year 50 basis points lower.”

As I’ve said many times: The Fed is the market’s primary price discovery mechanism and looks like Goldman implicitly agrees.

And it is very much self evident in investor behavior:

Whatever decision the Fed will make on Wednesday be sure it will be keeping 3 data points in mind: $SPX, $NDX & $DJIA.

Enjoy the rate cut show.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2ypIixA Tyler Durden

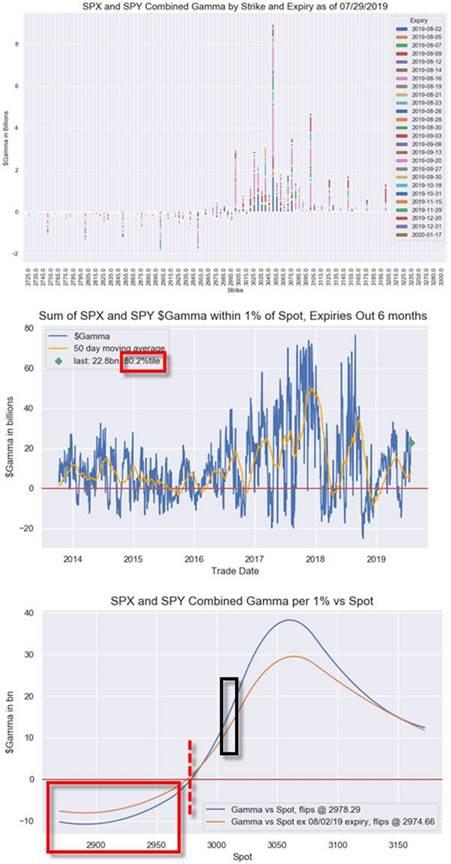

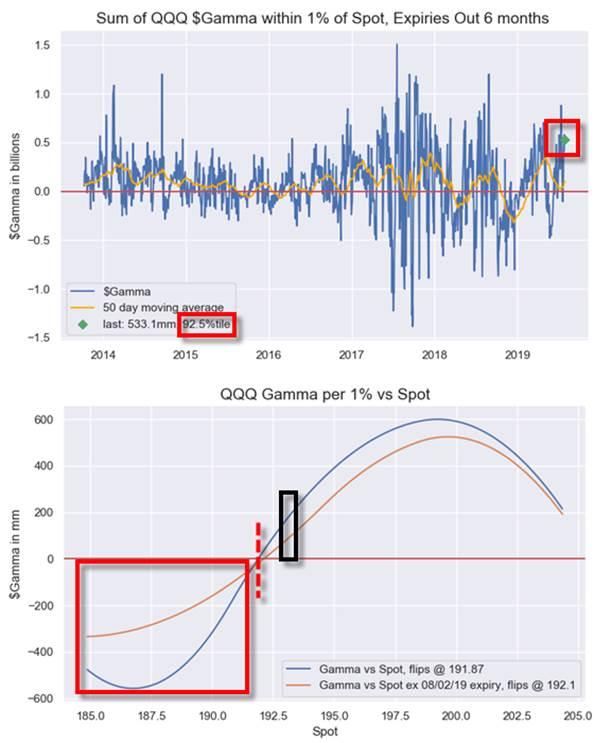

With all eyes focused on whether Jay Powell will go 25, 50, and/or end QT, Nomura’s Charlie McElligott notes that dealers are generally positioned aggressively long and additionally ‘long gamma’. However, given the potential for some serious volatility tomorrow, what levels should investors be watching for chaotic unwinds to begin.

Via Nomura,

Our analysis shows that Dealers are currently “long Gamma” across combined SPX / SPY options, with $Gamma at 80th %Ile since 2013.

However, we would see that position “flip” to “Short Gamma” down at 2978, or 2974 ex the 8/2/19 expiry

Strikes that matter: 3050 ($9.375B), 3100 ($5.000B) and 3000 ($4.507B)

Also worth noting is the VERY long positioning in crowded Nasdaq.

This leaves QQQ too nearing a flip from current Dealer “Long Gamma” positioning to the “Short Gamma” flip-zone at 191.87 / 192.10 (ex 8/2/19 expiry)…

Particularly relevant at the $Gamma is currently extreme at 92.5 %ile since 2003.

Trade accordingly.

via ZeroHedge News https://ift.tt/2YcehAB Tyler Durden

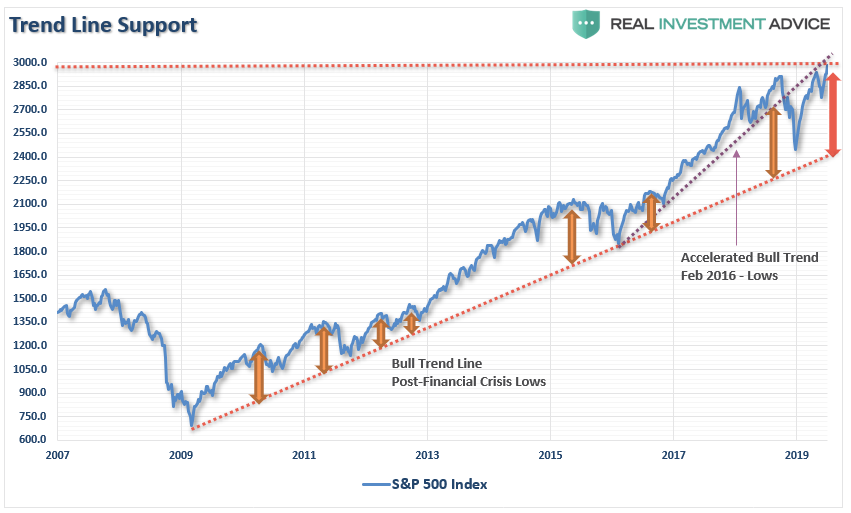

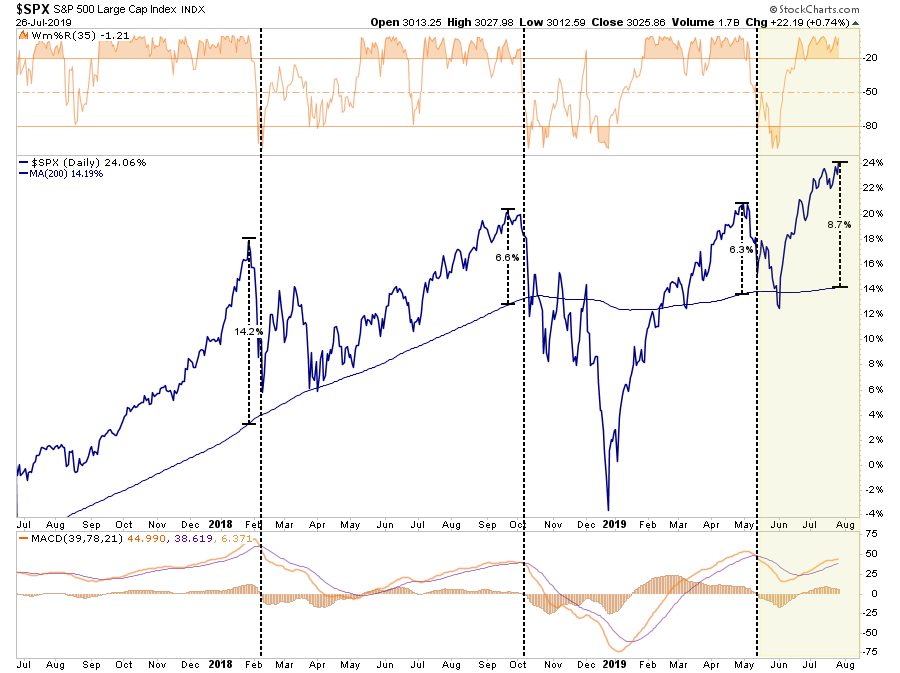

In this past weekend’s newsletter, I discussed the rather severe extensions of the market above both the longer-term bullish trend and the 200-dma. To wit:

There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

“As shown below, while the market is on a near-term “buy signal”(lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.”

Of course, discussing the potential of a market correction is almost always perceived as being “bearish.” Therefore, by extension that must mean that I am either all in cash or shorting the market. In either case, it is assumed I “missed out” on previous advances.

If you have been reading our work for long, you already know we have remained primarily invested in the markets, but hedge our risk with fixed income and cash, despite our “bearish” views. I am reminded of something famed Morgan Stanley strategist Gerard Minack said once:

“The funny thing is there is a disconnect between what investors are saying and what they are doing. No one thinks all the problems the global financial crisis revealed have been healed. But when you have an equity rally like you’ve seen for the past four or five years, then everybody has had to participate to some extent.

What you’ve had are fully invested bears.”

While the mainstream media continues to misalign individuals expectations by chastising them for “not beating the market,” which is actually impossible to do, the job of a portfolio manager is to participate in the markets with a predilection toward capital preservation. This is an important point:

“It is the destruction of capital during market declines that have the greatest impact on long-term portfolio performance.”

It is from that view, as a portfolio manager, the idea of “fully invested bears” defines the reality of the markets that we live with today. Despite the understanding the markets are overly bullish, extended and overvalued, portfolio managers must stay invested or suffer potential “career risk” for underperformance.What the Federal Reserve’s ongoing interventions have done is push portfolio managers to chase performance despite concerns of potential capital loss.

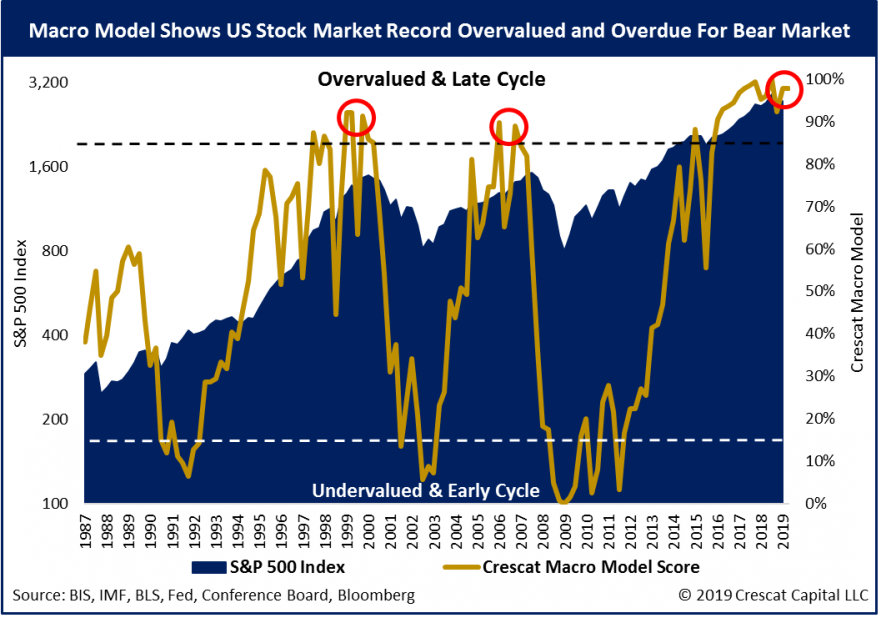

Managing portfolios for both risk adjusted returns while protecting capital is a delicate balance. Each week in the Real Investment Report(click here for free weekly e-delivery) we discuss the risks and challenges of the current market environment and report on how we are adjusting our exposures to the market over time. I wanted to share these charts from our friends at Crescat Capital which are all sending an important message. Currently, these are “risks” the market is ignoring, but eventually they will matter, and they will matter a lot.

Valuations

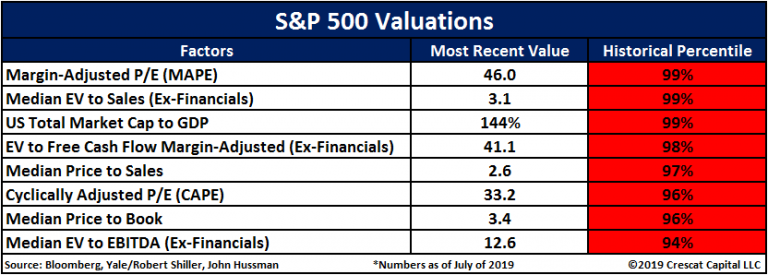

One of the consistent drivers behind the bull market over the last few years has been the idea of the “Fed Put.”As long as the Federal Reserve was there to “bailout” the markets if something went wrong, there was no reason NOT to be invested in equities. In turn, this has pushed investors to not only “chase yield,”due to artificially suppressed interest rates but to push valuations on stocks back to levels only seen prior to the turn of the century. As Crescat notes:

“ The reality is that stocks have never been this expensive for how low the 10-year Treasury yield is today. It’s true that all else equal, low interest rates justify higher valuations. However, the lowest interest rates historically haven’t corresponded to the highest P/E markets because extremely depressed yields also signal fundamental problems in the economy. Ultra-low rate environments are often marked by highly leveraged economies where future growth is likely to be weak.”

Given that valuations are all in the 90th percentile of historical values, it suggests that a reversion to the mean is increasingly likely.

Given these valuations are occurring against a backdrop of deteriorating economic growth and corporate profits, the risk to investor capital is high.

Divergences

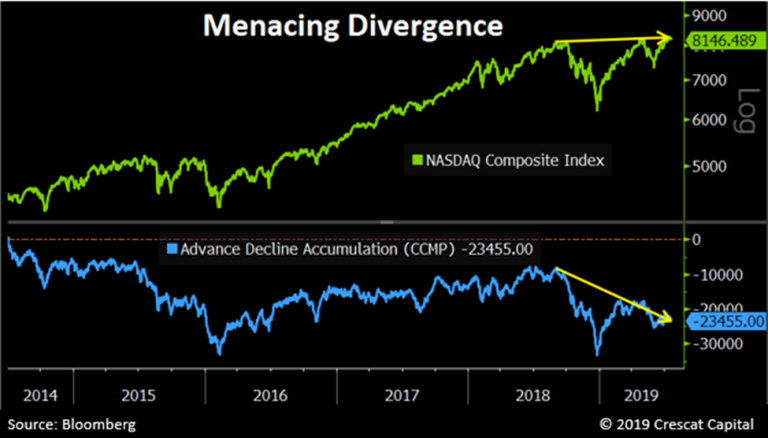

I have previously addressed the narrowing of participation in the markets. Much of the advance in the markets this year alone can be solely accounted for by a handful of mega-capitalization stocks. Since those mega-cap reside in both the Nasdaq and the S&P 500 index, the lack of breadth is worth noting. As Crescat points out:

“While many US equity indices have marginally broken out to new highs recently, they have done so in the face of weakening market internals. Equity indices are being propped up by a narrowing group of leaders. The deteriorating breadth is most evident in the NASDAQ Composite, home to today’s leading growth stocks. While the overall index has reached record levels, the number of declining stocks has significantly outpaced the number of advancing stocks since last September. The collapsing internals point to an exhausted bull market.”

Volume & Participation

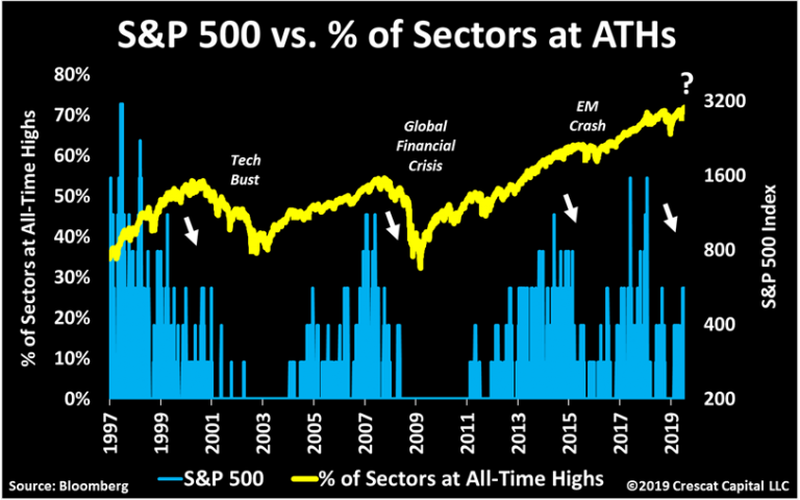

Another warning sign is that volume and participation have have also weakened markedly. These are all signs of a market advance nearing “exhaustion.” Back to Crescat:

“Stocks are also rising in defiance of extremely low volume. On July 16th, the SPDR S&P 500 ETF (SPY) had its lowest daily volume in almost 2 years. In a 15-daily average terms, volume is now as low as it was at the peak of the housing bubble and prior to the last two selloffs in 2018. Unusual calmness and breadth deterioration are not a good set up for record overvalued stocks.”

“The following chart is yet another illustration of how this recent rally in equities is running on empty, and again lacking substance. On July 15th, S&P 500 reached record levels, but only three sectors were at all-time highs. Market breadth today is faltering just as much as it did ahead of the last two recessions. In 2015, this was also the case, but back then only 20% of the yield curve was inverted. Now it’s close to 60%!”

Deviation

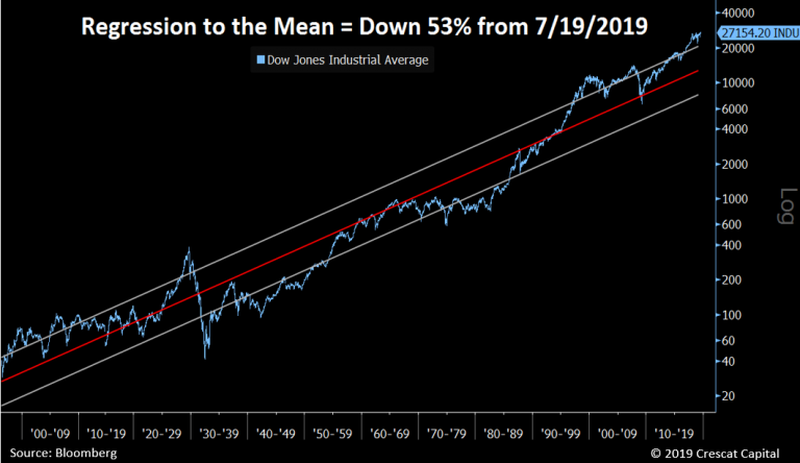

I have written many times in the past that the financial markets are not immune to the laws of physics. As I started out this missive, the deviation between the current market and long-term means is at some of the highest levels in market history.

There is a simple rule for markets:

“What goes up, must, and will, eventually come down.”

The example I use most often is the resemblance to “stretching a rubber-band.” Stock prices are tied to their long-term trend which acts as a gravitational pull. When prices deviate too far from the long-term trend they will eventually, and inevitably, “revert to the mean.”

As Crescat laid out, a “mean reverting” event would currently encompass a 53% decline from recent peaks.

Does this mean the current bull market is over?

No.

However, it does suggest the “risk” to investors is currently to the downside and some caution with respect to equity-based exposure should be considered.

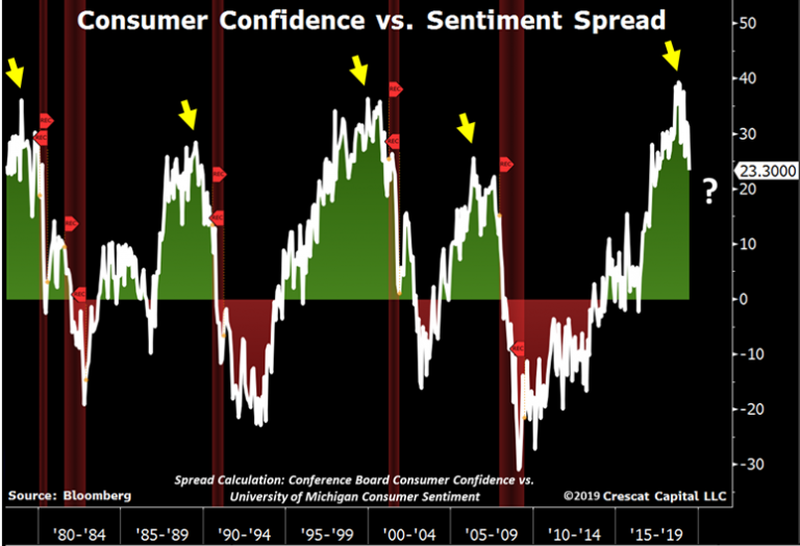

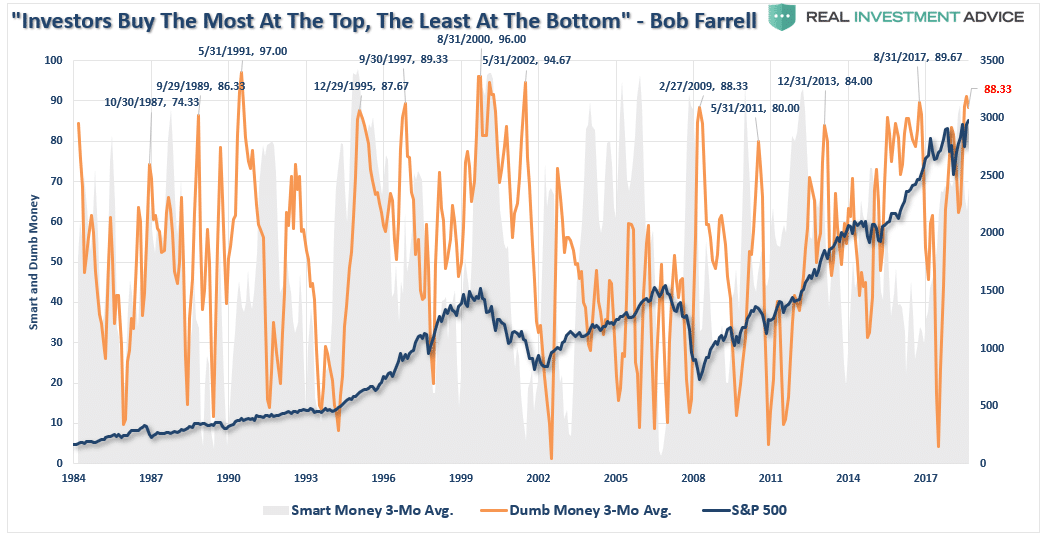

Sentiment

Lastly, is investor sentiment. When sentiment is heavily skewed toward those willing to “buy,” prices can rise rapidly and seemingly “climb a wall of worry.” However, the problem comes when that sentiment begins to change and those willing to “buy” disappear.

This “vacuum” of buyers leads to rapid reductions in prices as sellers are forced to lower their price to complete a transaction. The problem is magnified when prices decline rapidly. When sellers panic, and are willing to sell “at any price,” the buyers that remain gain almost absolute control over the price they will pay. This “lack of liquidity” for sellers leads to rapid and sharp declines in price, which further exacerbates the problem and escalates until “sellers” are exhausted.

With sentiment currently at very high levels, combined with low volatility and excess margin debt, all the ingredients necessary for a sharp market reversion are present. Am I sounding an “alarm bell” and calling for the end of the known world?

Of course, not.

However, I am suggesting that remaining fully invested in the financial markets without a thorough understanding of your “risk exposure” will likely not have the desirable end result you have been promised. All of the charts above have linkages to each other, and when one goes, they will all go.

So pay attention to the details.

The markets currently believe that when the Fed cuts rates this week, the bull market will continue higher. Crescat, and history, suggest a different outcome.

As I stated above, my job, like every portfolio manager, is to participate when markets are rising. However, it is also my job to keep a measured approach to capital preservation.

Yes, I am bearish on the longer-term outlook of the markets for the reasons, and many more, stated above.

Just make sure you understand that I am an “almost fully invested bear.”

At least for now.

But that can, and will, rapidly change as the indicators I follow dictate.

What’s your strategy?

via ZeroHedge News https://ift.tt/2GEonPQ Tyler Durden