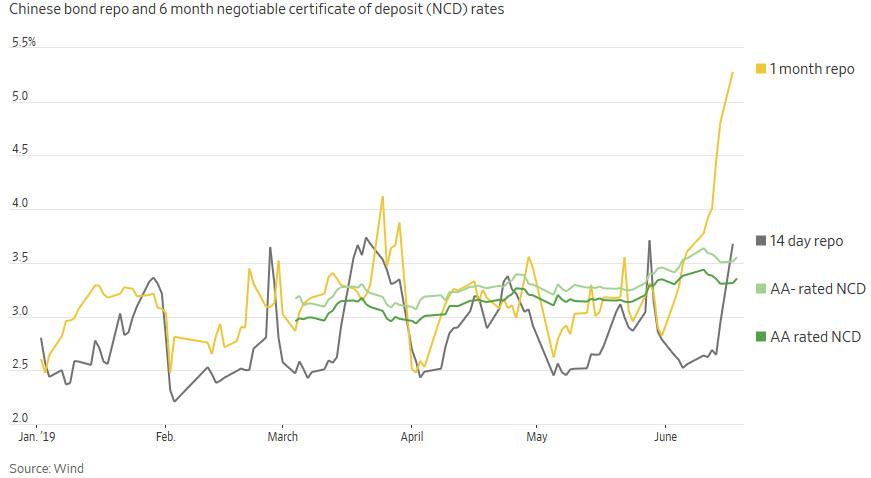

… China’s banking stress has taken a turn for the worse, and on Monday, China’s overnight repurchase rate dropped to its lowest level in nearly 10 years, after the central bank’s repeated liquidity injections to ease credit concerns in small-to-medium banks: The rate fell as much as 11 basis points to 0.9861% on Monday, before being fixed at exactly 1.000%.

Seeking to ease funding strains after the Baoshang collapse and to unfreeze the financial channels in the banking sector, the PBOC has been injecting cash into the financial system to soothe credit risk concerns in smaller banks following the seizure of Baoshang Bank, which sent shockwaves through China’s markets.

Also helping drive the rate lower is China’s move to allow brokerages to issue more debt, said ANZ Bank’s Zhaopeng Xing, quoted by Bloomberg. As a result, at least five brokerages had their short-term debt quotas increased by the People’s Bank of China in recent days, according to filings.

The improved access to shorter-term debt will cut costs for brokerages compared with alternative funding sources such as bond issuance. The flipside, of course, is that the lower overnight funding rates drop, the greater the investor skepticism that China’s massive, $40 trillion financial system is doing ok, especially since the last time overnight funding rates were this low, the near-collapse of the global financial system was still fresh and the S&P was trading in the triple-digits.

Commenting on the ongoing collapse in SHIBOR, Commodore Research wrote overnight that “low SHIBOR lending rates are supposed to be supportive and accommodative in nature — but rates are now at the lowest level seen this decade and are very likely an indication that China is facing significant banking stress at the moment. It is extremely rare for the overnight SHIBOR lending rate to be set as low as 1.00%. This previously had not all been seen this decade, and the last time it occurred was during the financial crisis in 2008 – 2009.”

Meanwhile, as the world’s biggest financial time bomb ticks ever louder, traders and analysts are blissfully oblivious, focusing instead on central banks admitting that the recession is imminent and trying to spin how a world war with Iran would be bullish for stocks.

via ZeroHedge News http://bit.ly/2KDpXVZ Tyler Durden

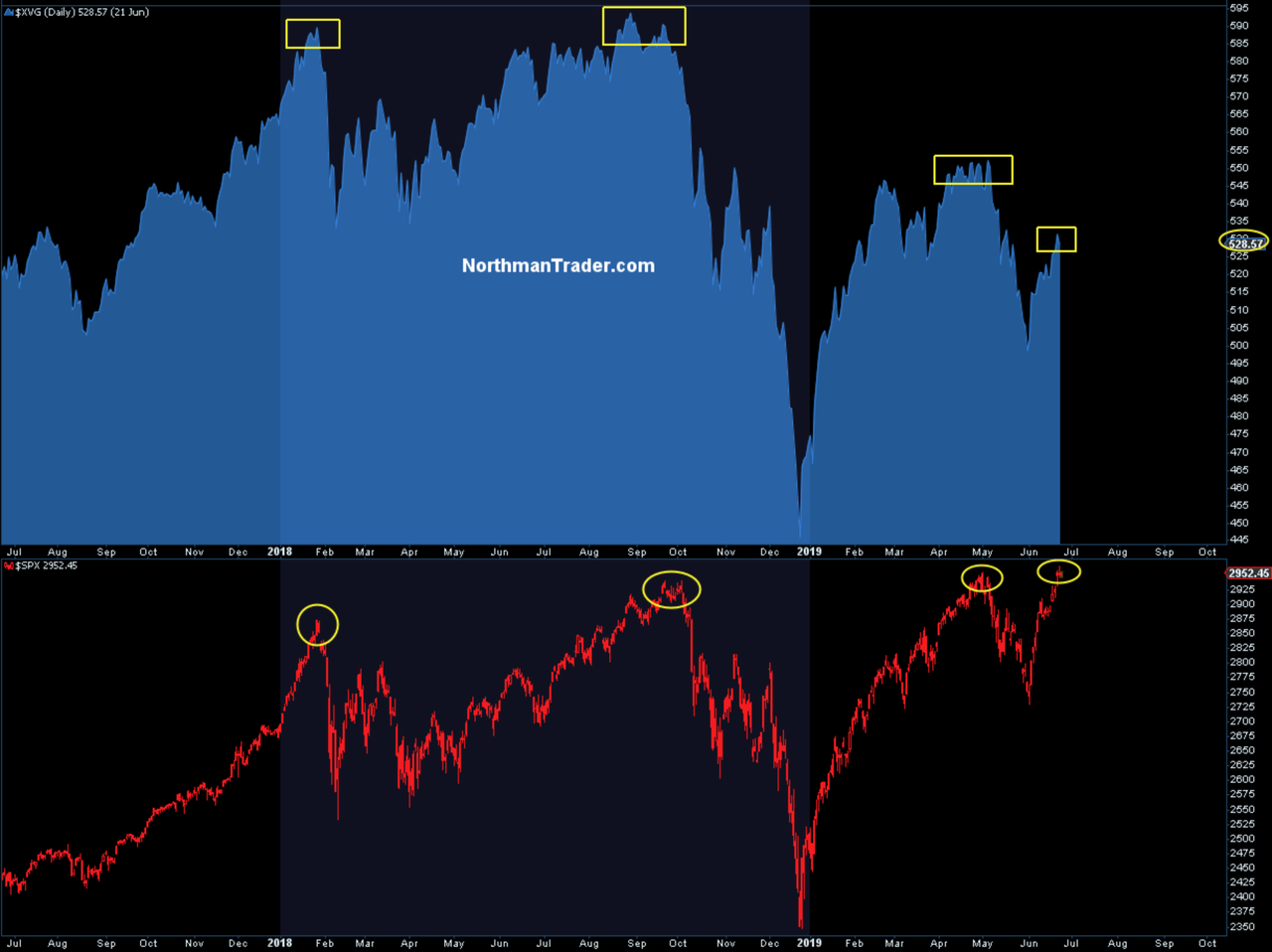

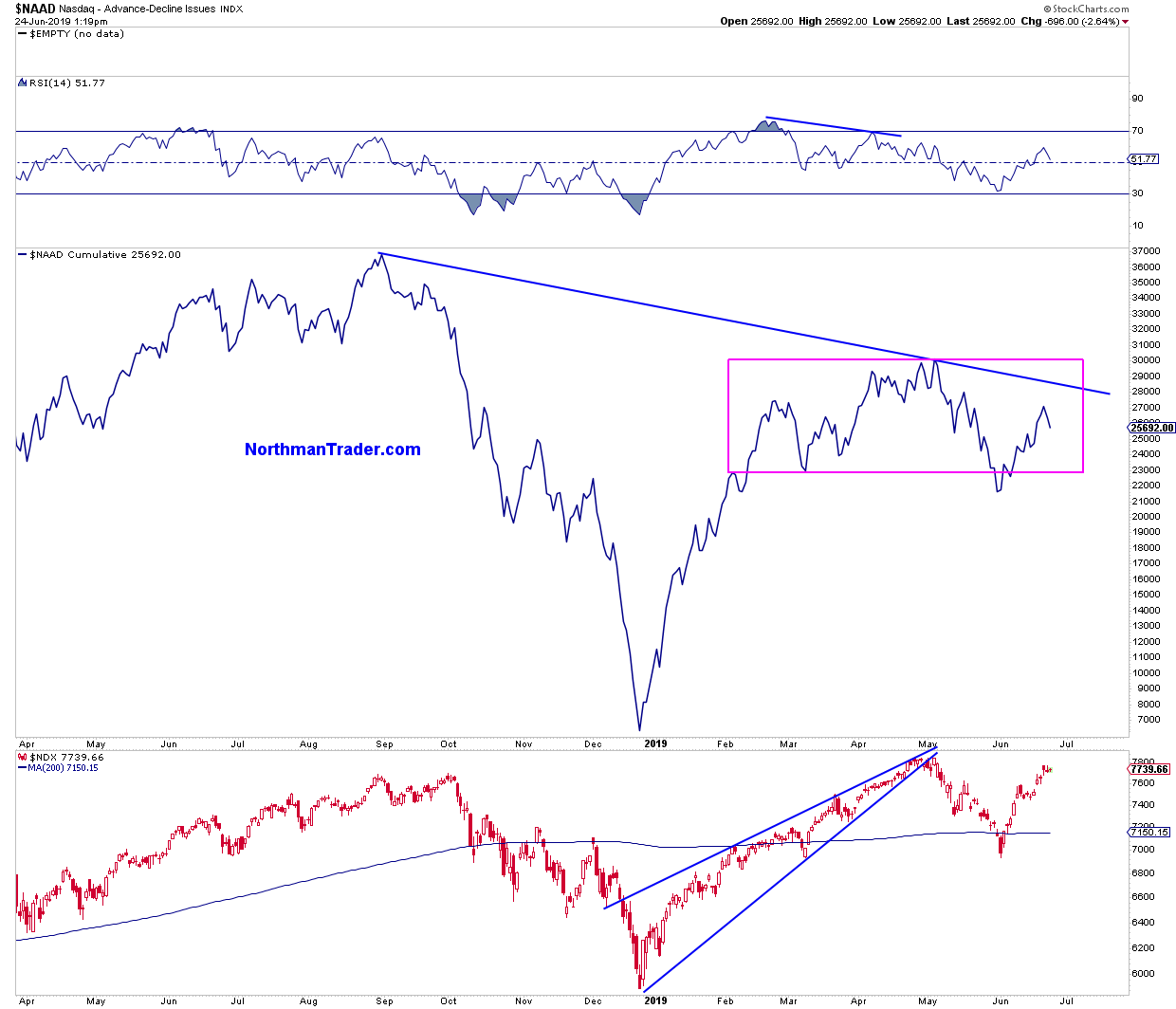

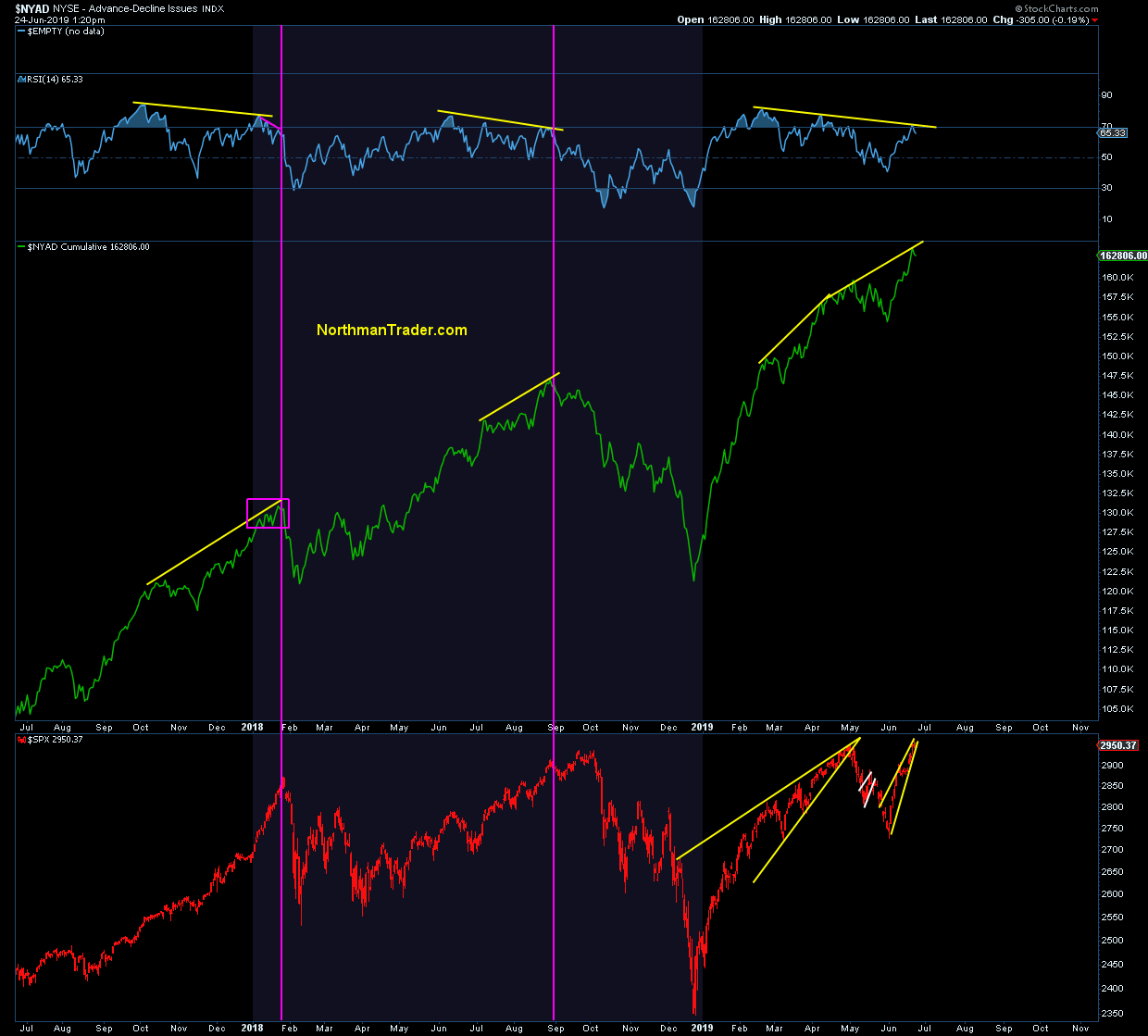

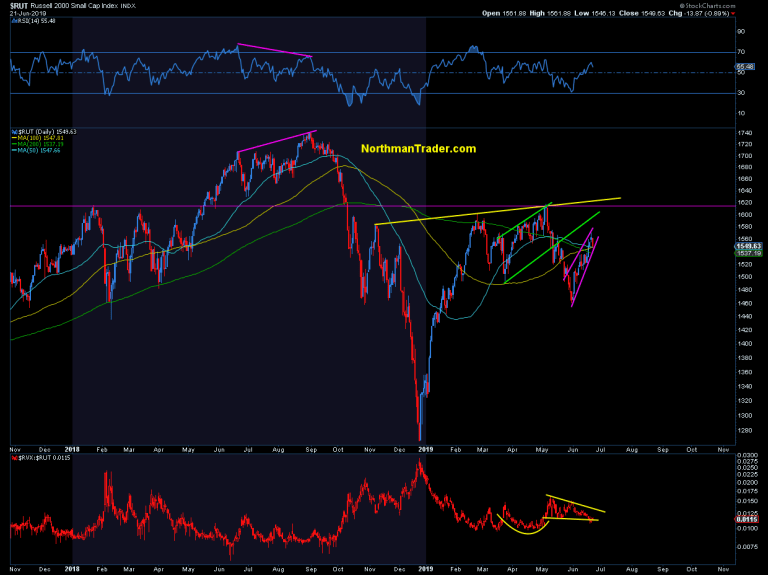

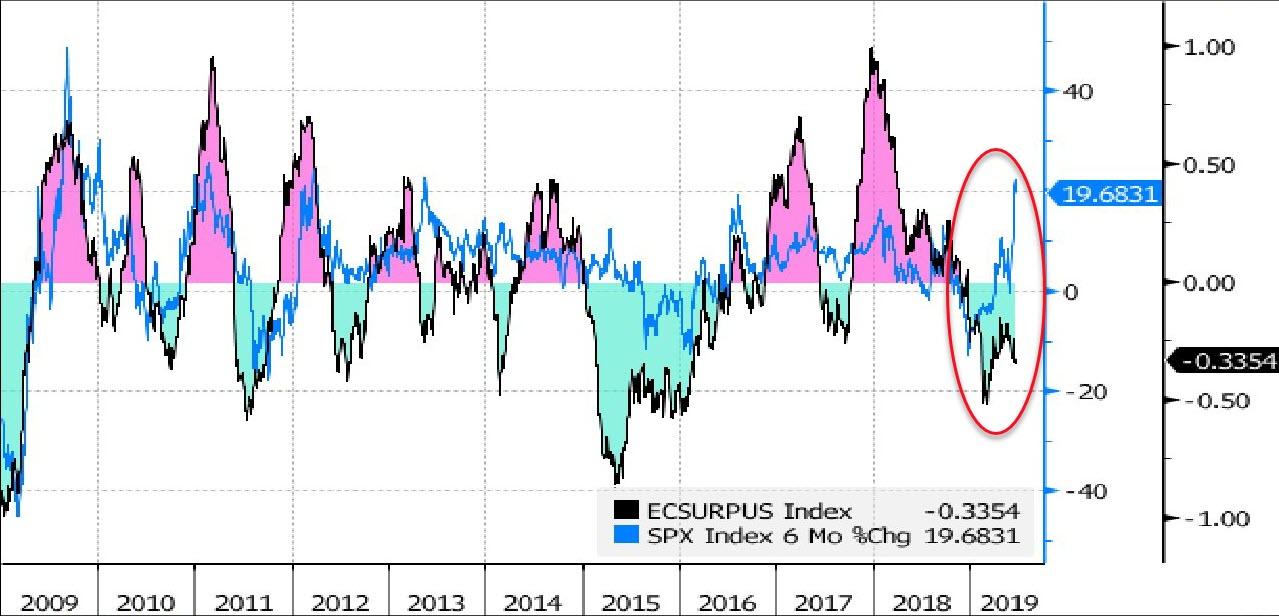

New highs are always informative from a technical perspective. What do the internals look like, are there divergences, positives or negatives, in short: How strong/sustainable are these new highs?

Well, $SPX made new highs last Friday and once again the rally looks the weakling. Central bank induced as all of June has been, the internal data just doesn’t scream conviction.

Nancy Pelosi infamously denounced walls as “immoral” during the 2018 midterms, and refused to acknowledge the legitimacy of the border crisis – dismissing it as a ‘made up’ emergency after Trump tried to bypass Congress and re-appropriate money to build his border wall from the Treasury and DoD budgets.

Now, the Speaker of the House is taking her hysterical pro-immigration/anti-Trump rhetoric to another level of hysterical inanity by insisting that just because somebody is in the country illegally doesn’t mean they should be deported.

During an event in New York, Pelosi told her audience about a recent phone call with President Trump, where she discussed Democrats’ desire to delay the mass roundups of illegal immigrants (a request to which Trump acquiesced). During the call, Pelosi said she told the president that “a violation of status is not a reason for deportation,” adding that there are over 10 million people who could face deportation because they are here illegally.

Instead of rounding these immigrants up, Pelosi said Washington should focus on creating a path to citizenship.

“I said ‘a violation of status is not a reason for deportation,’ that’s just not so,” Pelosi said she told Trump.

“If you have some case you want to make about somebody who’s been accused…that has nothing to do with violation of status, because then we’re talking about over 10 million people who may be subjected to this treatment, and what we need there is comprehensive immigration reform with a path to citizenship.”

Pelsoi then added that she told Trump his deportation rhetoric had scared “the children of America” – and not just the immigrant children.

“Look, I’m a mom, I have five kids…nine grandchildren, and you, children are scared,” Pelosi reportedly said to Trump.

“You’re scaring the children of America. Not just those families, but their neighbors and their communities. You’re scaring the children.”

Pelosi made the comments shortly after announcing on Sunday plans to introduce legislation in the House that would allocate more money to address ‘the humanitarian crisis’ at the border – something Trump discussed in this year’s State of the Union, and during the run-up to the midterms.

Watch the video of Pelosi’s comments below:

via ZeroHedge News http://bit.ly/2IEXUTQ Tyler Durden

The asymmetries are piling up and we’re cracking under the weight.

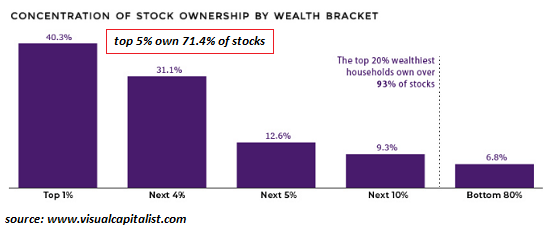

Judging by the record-high stock market and the record-low unemployment rate, the “recovery” has reached new heights of prosperity. Academics and think-tankers viewing the global economy from 40,000 feet are brimming with policies to bring the remaining laggards into the booming economy.

You can imagine them rubbing their hands with glee as they quote statistics such as: the 53 metropolitan areas in the U.S. with populations of 1 million or more accounted for two-thirds of the GDP growth and three-quarters of the job growth. A staggering 93% of the population growth in the U.S. in the past decade occurred in these urban centers.

And this asymmetry is even greater if we separate the top 10 metropolitan areas from the rest: super-cities with super-charged economies, fueled by enormous influxes of capital and people, which just so happen to make life unbearable as overcrowded, aging infrastructure breaks down and costs for housing, rent, taxes, utilities, fees etc. skyrocket out of reach of the bottom 95%.

The well-paid pundits viewing glowing statistics of growth never get around to examining the human costs of this lopsided “recovery”: the “winners” in increasingly unlivable urban centers are cracking under the pressure-cooker stress, burning out, flaming out, crashing.

The residents of all the regions sucked dry of capital and talent–the “losers” of neoliberal globalization’s concentrations of mobile capital and talent in a few favored megalopolises–are also cracking under the weight of a loss of dignity and secure livelihood, the two being intimately bound, much to the dismay of the supporters of “just pay them to go away and not bother us” Universal Basic Income (UBI).

In other words, the “winners” are losing, too. They’re losing their sanity in 3-hour daily commutes on jammed freeways and equally jammed streets as thousands of other commuters seek a work-around to the endless congestion.

They’re losing their dreams of a better life, as all the average-wage worker can afford to rent is a bed in a cramped living room that has been converted into sleeping quarters for two workers who don’t make six-figure salaries and who don’t have stock options in a Unicorn tech company.

They’re fixated on FIRE–financial independence, retire early–because they hate their job, their career and the sector they toil in, and they count the days until they’re free, free, free of the pressure, the stress, the BS work, and the insanity of daily life in a teeming rat-cage.

No wonder the FIRE movement is spreading like (ahem) wildfire. Nobody in their right mind wants to do their job for another 10 years, much less 20 or 25 years. Everybody is bailing out the moment they can, or if they burn out and crash, when they’re forced to.

Let’s say you want to start a business in a super-progressive city that fulfills all your most cherished ideals: paying your employees good wages, providing customers with value, and paying all your taxes and fees, of course, as a responsible progressive citizen.

Where do we start? How about the reality that virtually no one employed in the restaurant sector can afford to live in San Francisco unless they inherited a rent-controlled flat or scored one of the few subsidized housing openings?

The city’s solution–mandating a $15/hour minimum wage–doesn’t magically make healthcare or rent affordable; all it does is increase the burden on small businesses that are hanging on by a thread.

Working 100 hours a week couldn’t compensate for the crushing rent.

Even the well-paid are burning out. Astronomical household incomes (say, $300,000 annually) aren’t enough to buy a decayed bungalow for $1.3 million and pay for childcare, private-school tuition, healthcare, an aging parent and all the services the overworked wage-earners don’t have the time or energy to do themselves. Oh, and don’t forget the taxes. You’re rich, people, so pay up.

No wonder people who can afford to retire are bailing at 55 or 60, on the first day they qualify. Life’s too short to put up with the insane pressure and stress a day longer than you have to.

Not everybody feels it, of course. People who bought their modest house for $100,000 30 years ago can hug themselves silly that it’s now worth $1,000,000 (but with a still-modest property tax), and if they’re retired with a plump pension and gold-plated medical benefits, their biggest concern is finding ways to blow all the cash that’s piling up.

These lucky retirees wonder what all the fuss is about. “We worked hard for what we have,” etc. It’s easy to overlook being a lucky winner of the housing-bubble lottery and the equally bubblicious pension lottery, and easy not to ask yourself how you’d manage if you arrived in NYC, San Francisco, et al. now rather than 35 years ago.

The asymmetries are piling up and we’re cracking under the weight. When do we recover from the “recovery”? The answer appears to be “never.”

Without the quad-witch magic, stocks unable to hold gains as bonds, bullion, and bitcoin all see safe-haven bids…

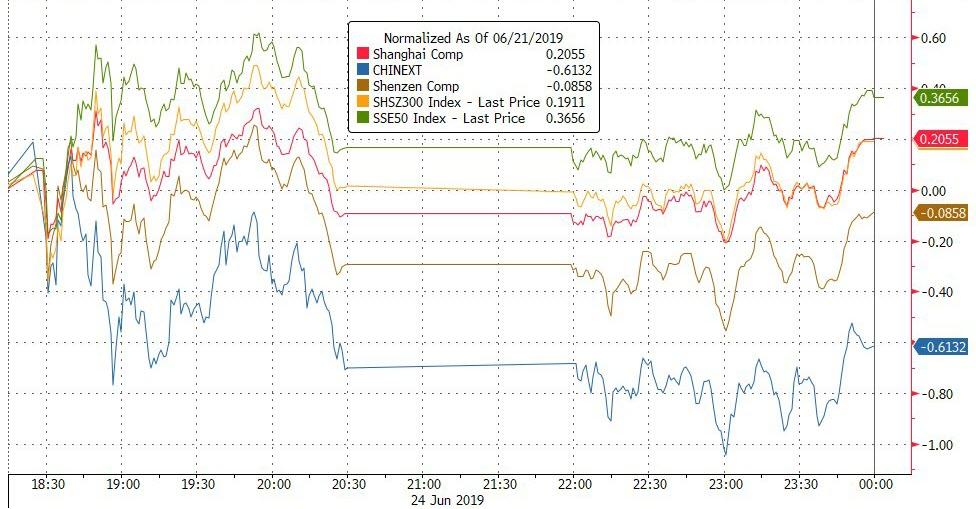

Chinese stocks trod water largely overnight after a big week, with tech and small caps leading the drop…

European stocks drifted lower for the 3rd day in a row, despite an excited open…

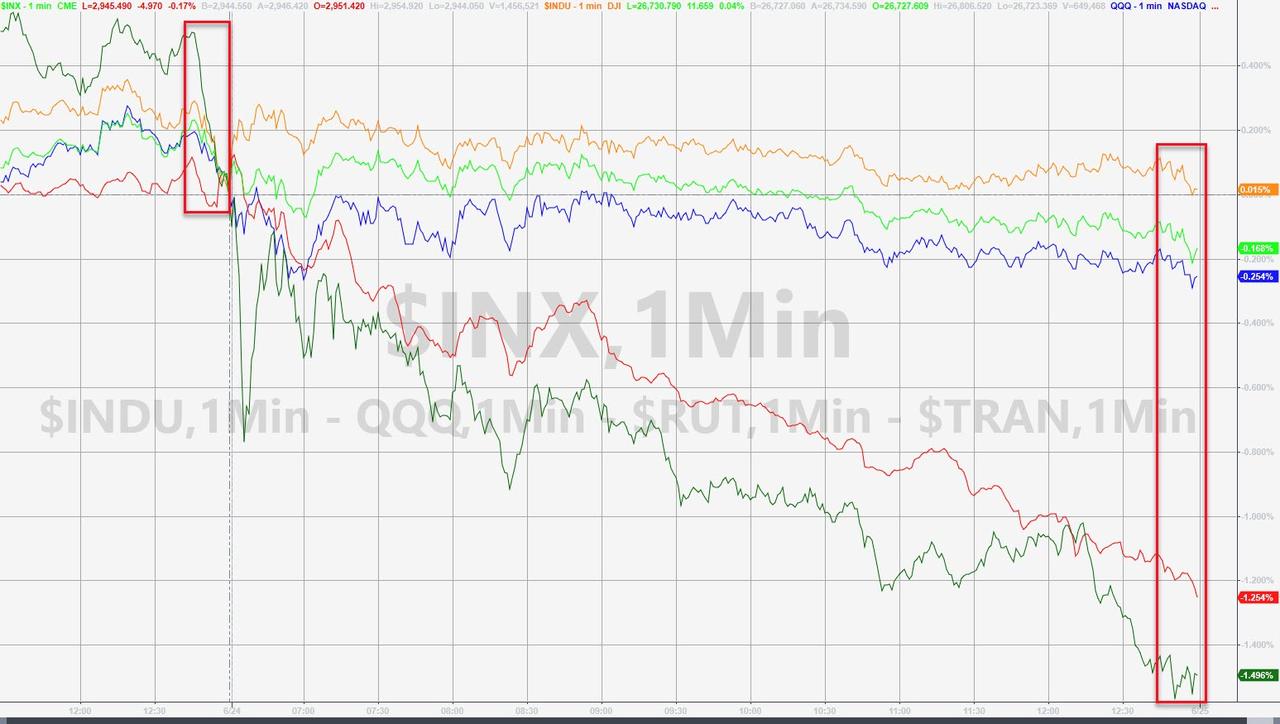

Ugly day for Trannies and Small Caps, Dow managed to cling to gains but S&P and Nasdaq scrambled around unch before a weak close (second in a row)…

The (cash) opening spike at the open could not hold…

Dow Industrials and Transports have notably decoupled…

It’s a serious decoupling…

Notably, the decoupling of Small Caps and Trannies occurred when the ammo for short-squeezes ran out…

VIX and Stocks remain decoupled…

While the so-called Fed model “shows” that stocks are relatively attractive to bonds, Bloomberg’s Ye Xie notes, the risk is that the equity market hasn’t priced in enough potential bad news on earnings and the economy.

Notably though, equity risk has entirely decoupled from the risk of bonds and bullion – some suggest this as a simple way to quantify the ‘value’ of the ‘Fed Put’ – around equity 25 vol points compression

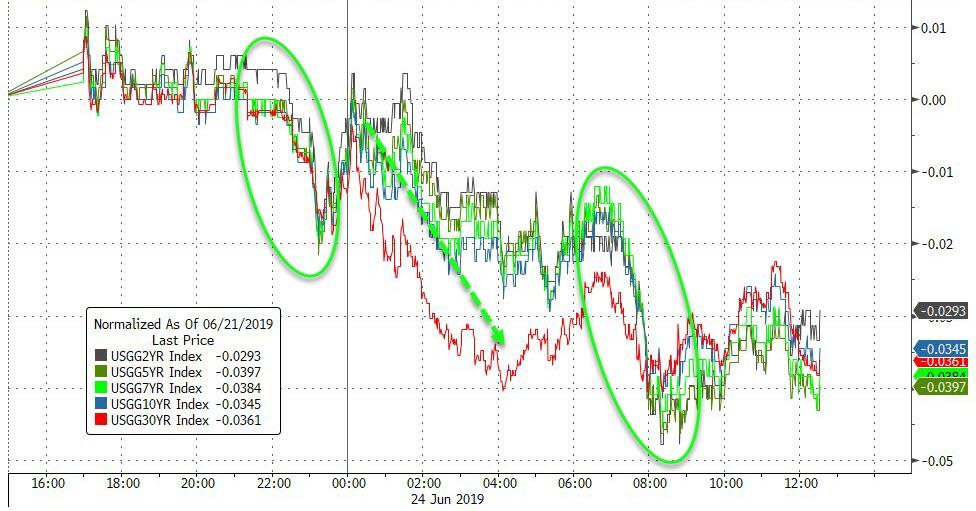

Treasury yields were down a pretty uniform 3-4bps or so across the curve…

10Y dropped back to a 2.01% handle once again…

And the yield curve flattened…now inverted for 22 days straight…

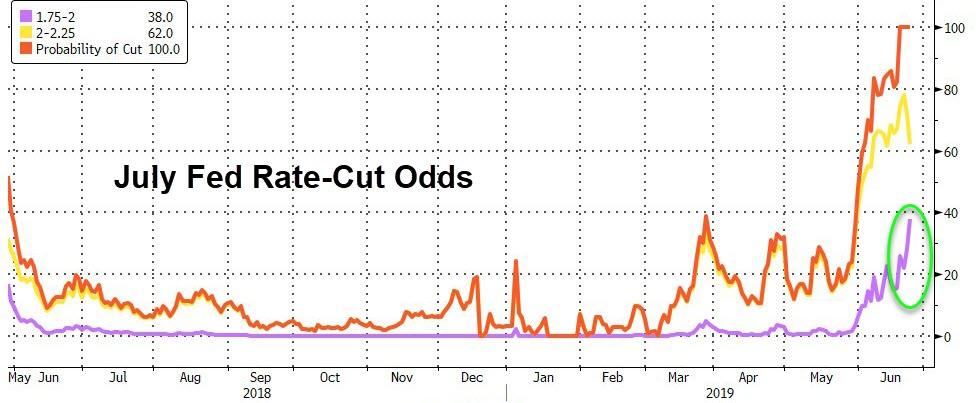

Expectations for a big (50bps) rate-cut in July are surging (now 38%!)

Before we leave bondland, this is worth noting – the US yield curve collapse has tracked the same move in the mid to late 1990s… all of which culminated with the collapse and bailout of LTCM (where leveraged bets on correlations exploded)

The Dollar Index extended its decline…

Falling well below its 200DMA now…

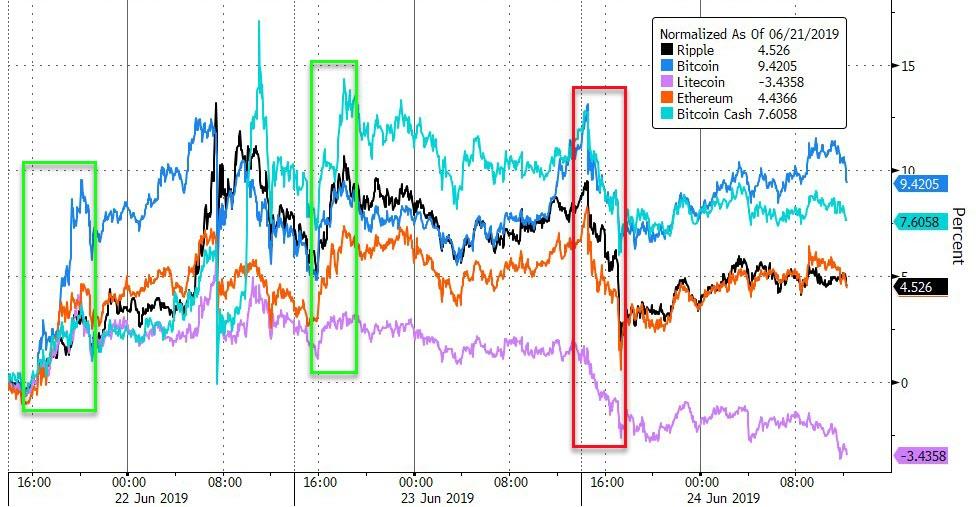

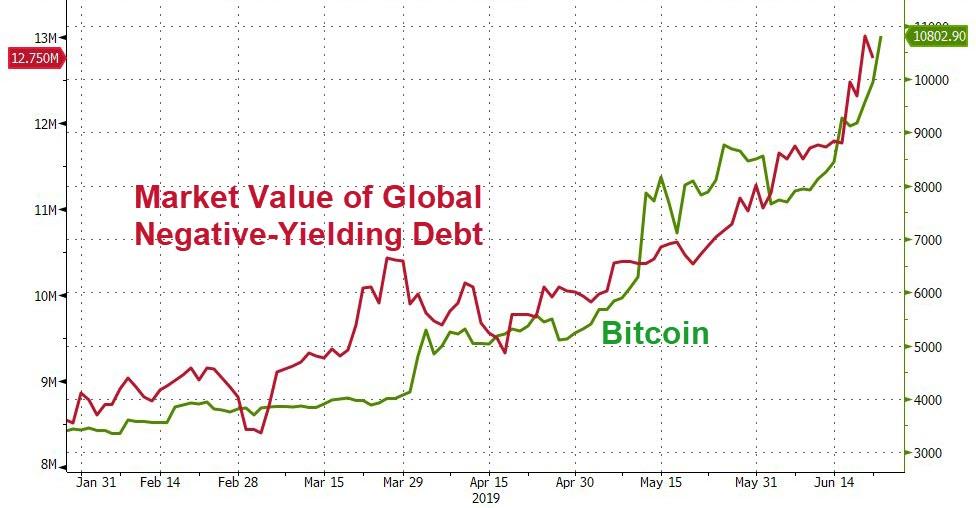

A big weekend for crypto saw some selling early today (Litecoin weakest)…

Bitcoin was bid multiple times back above $11,000…

Bitcoin is tracking the amount of crazy in the world…

Gold and Bitcoin have recently become seriously correlated…

Gold was the best performing commodity on the day with oil playing a bg catch up into its close…

WTI rebounded off $57 once again…

Another big day for gold, with futures spiking up to almost $1425…

Gold continues to outpace silver…

Finally, when everything is yielding below zero, a zero-yielding asset has more value…

“World-Gone-Mad” premium soars.

via ZeroHedge News http://bit.ly/2Y6XbQy Tyler Durden

As the first of 12 presidential debates blows in at mid-week like an evil patch of bad summer weather, twenty candidates vie for the position of Ole Massa on the Democratic Party plantation, and the air is gravid with bad vibes.

One highly-favored entry, Mayor Pete (Buttigieg) of charming South Bend, Indiana, stepped into (and tripped over) a big fresh patty of mule poop over the weekend at a “town hall” meeting that was called to address the June 16 shooting of one Eric Logan, 54, by a police officer dispatched to check out “a suspicious individual going through cars” at 2:30 a.m. The officer said the suspect came at him with a knife. The officer failed to switch on his body-cam, or so the police department said. Conclusions were jumped to. Then, in the wee hours just before Mayor Pete’s June 24 town hall, another black man was killed and 10 other people wounded in the shoot-up of a watering hole called Kelly’s Pub.

God knows what that was about — no police were involved in the shoot-up — but Mayor Pete caught the blame for it, of course, and the Sunday town hall meeting turned into a shriek-in by outraged “community” members. He was hardly allowed to admit his failures, issue apologies, and promise to do better. After the ordeal, Mayor Pete struggled to hold in his tears talking to the media. No doubt he will be pressured to keep ‘splainin’ these matters until either his campaign folds up its tent or he is anointed at the national convention in Milwaukee.

Leader-of-the-Pack (in the polls, anyway) Joe Biden steeped into it perhaps even deeper than Mayor Pete last week when he bragged about how well he was able to work with the old southern segregationist fossils, Herman Talmadge (GA) and James O. Eastland (MS), who were still around in the senate when “Uncle Joe” first came on the scene decades ago. “We didn’t agree on much,” the former Veep said, “but we got things done.” What’s more, the candidate averred, going perhaps a bridge too far, Senator Eastland “never called me ‘boy,’ he always called me ‘son,’” as if Mr. Biden might have been mistaken for a waiter in the senators’ dining room, with its old fashioned-ways and renowned bean soup.

Senator Cory Booker (NJ), a.k.a. “Spartacus,” aiming to “speak truth to power,” as gladiators are wont to do, jumped on the remarks as “hurtful and harmful to African Americans.” Mr. Biden, something of a political fossil himself now, shot back that Senator Booker should apologize to him for imputing he had racist proclivities. The rest of the pack joined the feeding frenzy. Bernie Sanders backed up Mr. Booker’s call for a Biden apology. Senator Elizabeth Warren (MA), criticizing her leading rival said, “I’m not here to criticize other Democrats, but it’s never okay to celebrate segregationists. Never.” Senator Kamala Harris piled on, calling Mr. Biden “misinformed and wrong.”

The week’s doings left the impression that the Democratic Party has turned into one big race hustle, with reparations for slavery as the centerpiece on the banquet table and recriminations for “white privilege” as the main course. Senator Warren added a gender hustle amuse bouche to the menu over the weekend with demands for “reparations for gay and lesbian couples” who had to file income taxes as individuals in the pre-gay-marriage days.

African Americans comprise about 12.3 percent of the US population and about 4.5 percent “identify as” LGBTetc. The Hispanic demographic is 18.1 percent and the Democratic Party has already got them covered with its official opposition to the immigration laws – though there is evidence that Hispanic US citizen-voters are not uniformly on-board with that pander.

Now the party will be hard put to come up with some goodies for the rest of the US population. But it appears that it has only punishments and persecutions in mind for them. This may be the way the world ends for the party first consolidated by Andy Jackson, the old white slavemaster rascal, whose sins were later redressed with the election of Barack Obama.

Hustling their way to an election disaster in 2020, they play right into the small-ish hands of Mr. Trump, the Golden Golem of Greatness.

via ZeroHedge News http://bit.ly/2X1SNpv Tyler Durden

With US stocks back in the red for the day, Global Times editor Hu Xijin, one of Beijing’s favorite English-language mouthpieces and perhaps the most obvious candidate for ‘anti-Trump’ Twitter foil, has offered a stern warning to keep the market’s frothy enthusiasm in check.

One day before leaders of each side’s trade delegation are expected to begin meeting in Osaka ahead of this week’s G-20 summit (and long-anticipated meeting, Hu warned that the “current atmosphere” between Washington and Beijing is “not good”.

Current atmosphere between China and the US is not good. What I have learned about China’s stance now is: holding constructive and positive attitude toward upcoming China-US summit, but fully preparing for its failure and an escalating trade war.

According to Hu, China’s attitude going into the summit is “positive”, but “fully preparing for its failure and an escalation” of the trade war.

Furthermore, Hu had some particularly harsh words for Secretary of State Mike Pompeo, labeling the Secretary of State a “troublesome” figure in US-China relations and insisting that Pompeo “can no longer play the role of a top US diplomat between the two countries.”

.@SecPompeo has become the most troublesome US official for China. He can no longer play the role of a top US diplomat between the two countries. To China, he is still a CIA director who takes over State Department.

“When one buys life insurance, you don’t win when you die” – Harley Bassman

A few weeks ago, in his latest commentary, “Can’t You Hear Me Knocking” which we discussed here on the last day of May, the creator of the MOVE bond volatility index, noted “the strange configuration of the Yield Curve and how it likely presaged a macro-political or -economic disturbance.”

Since then, his view has not changed and while the exact timing and nature of a financial reversal is above his pay-grade, Bassman writes in his latest freebie note (now that he is retired, having quit PIMCO a few years ago), that historically such events occur about eighteen months after the first inversion: “as a rough prediction, I would target a date in mid-2020, serendipitously in the middle of the election cycle.“

With that in mind, Bassman – who for much of the 1990s and 2000s was seen as one of Wall Street’s most ingenious structured products traders – has published a report which details “a terrific strategic trading opportunity.” Alas, this is not for retail: as Bassman writes, “the structure of this investment involves a rather complex derivative product whose supporting concepts require a bit of concentration. Moreover, only professionals (or those with an ISDA) can execute this transaction – I apologize. If you have an interest in high-level finance, please continue; otherwise, save a tree and don’t print this commentary” (incidentally, he also discloses that has a position in this trade).

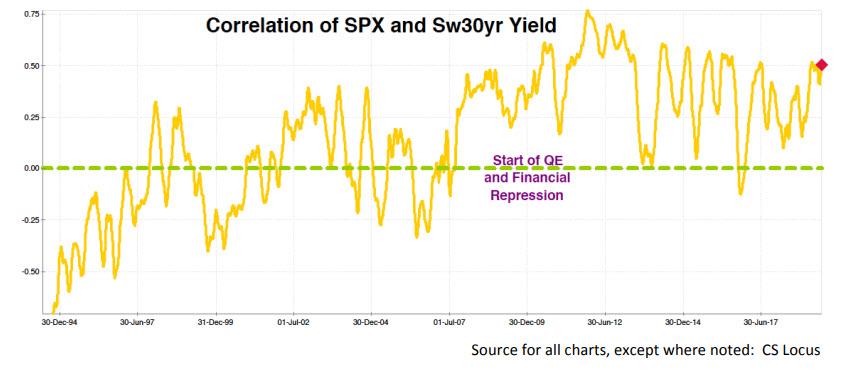

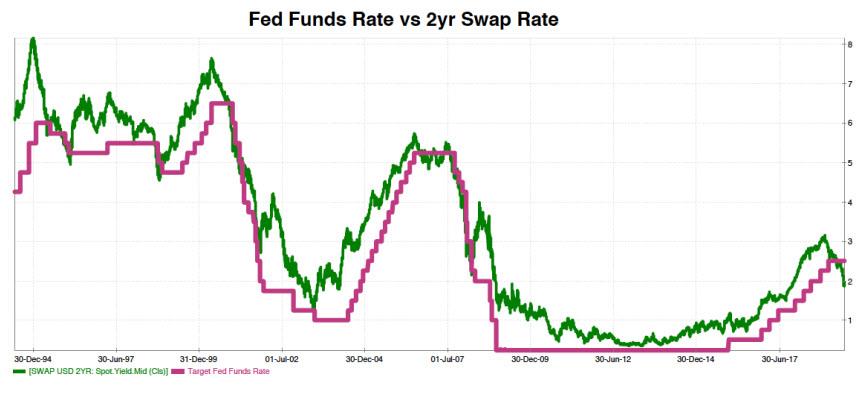

As I first detailed in “How Will I Know” – since the implementation of Quantitative Easing (QE) and Financial Repression as Great Financial Crisis (GFC) unfolded, stocks and bonds have moved in opposite directions. The line below is the three-month moving average of the three-month correlation between the SPX price change and the Sw30yr yield change.

(Note: this would be a negative correlation if we measured the price change of both stocks and bonds.)

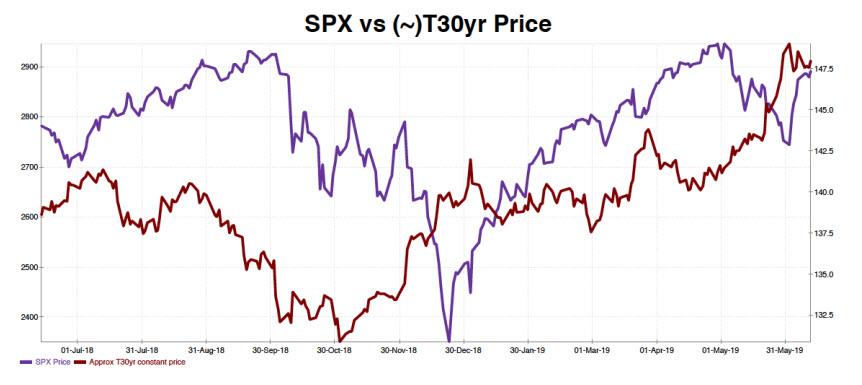

What is curious is that despite a decade of moving in opposite directions, the prices of both the violent line- S&P 500 (SPX) and the red line, Thirty year UST bond, are approaching their all-time highs.

Setting aside the small detail that daily volatility offers sparse information about the final destination of an asset; clearly the Equity market did not receive the email from the Bond market that a storm is brewing. It is an interesting juxtaposition that short-term interest rates (the Reds) declined by 37bps in a week while the SPX closed last Friday a mere 2% below its forever peak.

A quick glance at the table below might offer becalming comfort since the one-year rate of 2.08% is almost equal to the ten-year rate of 2.035%.

Yet a closer look of forward two-year swap rates highlight a deep contortion in the belly of the Yield Curve.

To spare your eyes, while the effective Fed Funds rate is presently 2.375%, the two-year swap rate is 51.7bp lower at 1.858%; and as will be important soon, the two-year rate six months forward is 1.696%, or 16.2bps lower.

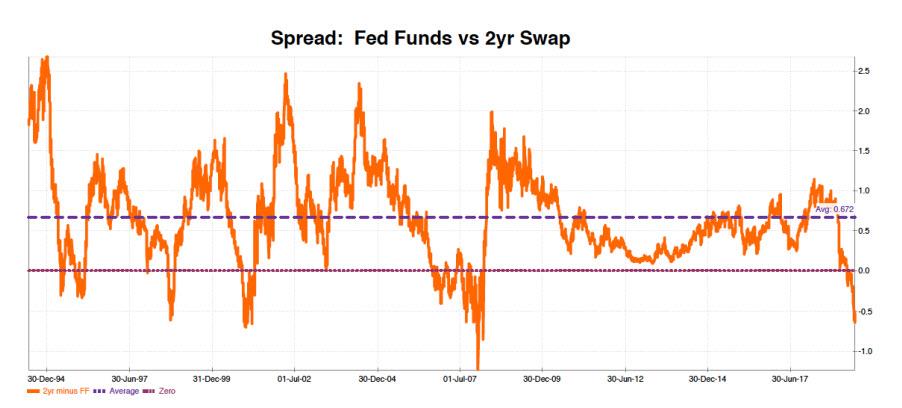

Let’s pause for moment and consider why the relationship between the Fed’s Target rate and the two-year rate is important. Below, the green line is the two-year swap rate while the pink line is the effective Fed Funds rate; this difference is generally a positive spread.

For clarity, the orange line is this spread. Since 1994, it has averaged about 74bps, and since the start of the GFC, the gap has been about 62bp

Employing only grade school math, a reversion to the decade average would entail the need for the Federal Reserve to cut its target rate five times in 25bp increments by the end of the year. [1.696% minus 62bp equals 1.076%; and 2.375% minus 1.076% equals ~130bps]

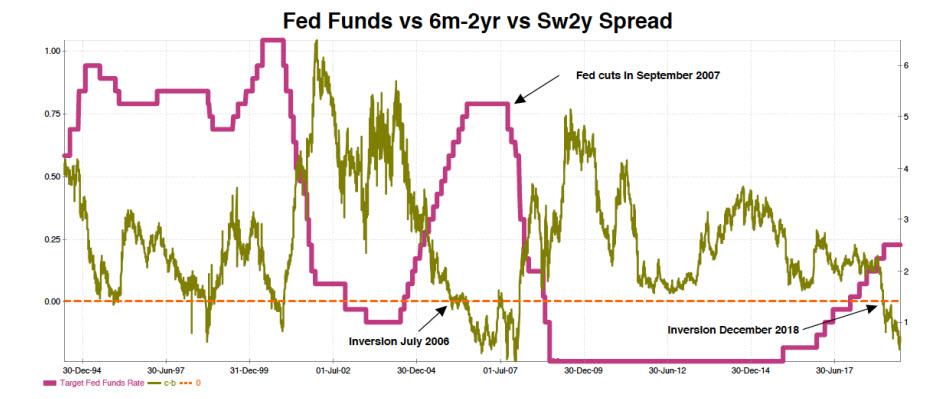

Unless you are a newbie, you know my favorite saying is: “It’s never different this time”. And indeed, the green lin- forward spread does invert prior to green line representing Fed rate cuts. However, one might note it is not an instantaneous event. In the last rate cut cycle, this spread inverted in July 2006 yet Fed rate cuts did not commence until 14 months later in September 2007.

The bottom line is not that the bond market is wrong, rather only a bit too early. It could be fears of a Trade War or an Immigration meltdown, or perhaps twitter has finally become fully weaponized. In any event, except for interest rates, fundamental economics presently do not support an immediate rate cut by a “data dependent Fed”; and certainly not four rate cuts by December.

If you have read this far, it is time for your reward…. (Hat tip to my friends at MS)

As noted, the two-year forward swap rate is 1.696%, 16.2bps below the spot rate. If one believes rate cuts will not be as speedy or as often as implied by market rates, the simple ticket is to short the forward and earn the 31cents of “roll up carry” as the forward grinds up to the spot.

I don’t like this trade because of the potential for unlimited loss. Of course the easy alternative is to buy a six-month expiry payer swaption (similar to a put option on the UST two-year note), but this option would cost about 46 cents upfront, a fee greater than the pure carry of 31cents.

Another way to reduce the price is via an option spread. One could buy an at-the-money (ATM) option struck at 1.696% and sell an option struck 25bps (1.946%) or 50bps (2.196%) OTM for a total net cost of 26cents and 36cents respectively. This is better, but the fee still eats up the carry profits.

Here is the clever idea:

Buy the ATM option struck at 1.696% and sell the 50bp out-of-the-money option struck at 2.196%

But: Make it contingent upon the SPX being 5% lower than today’s price. This reduces the cost by 78% to only 8cents.

If the rates market is unchanged, and the SPX backs up by 5% to 2743, this position would produce a 3.75x pay out. And if the bond market realizes it is over its skis and spot rates increase just a bit, the pay out can be much higher.

The hook is that you need to have some confidence that stocks can decline over the next six months, without rates sinking further. While I am not a super bear, a small pull back is more than just possible. Corporations purchasing their own stock have been largest buyers of equities, and this buying has just passed its seasonal peak. Also, the recent rate move may shake out out a few sellers who want to cash in their chips before election politics begins to heat up.

I absolutely love this trade as it offers a near-the-money option at the price of a tail hedge. Moreover, it is well suited for any portfolio that is constructed to use interest rate risk to partially offset equity risk. (Clever eyes will notice that Closed-end Funds, which I own in abundance, exhibit this sort of exposure.)

The massive discount of this Hybrid option is sourced from the high correlation between rates and stocks, as described above. This trade is effectively a sale of that correlation.

There is no free lunch, but I have a 16.2bps wind at my back via the curve inversion, and the SPX is near its local top. If I am right, this is a convexity monster; and you know I love that.

via ZeroHedge News http://bit.ly/2IH09Gd Tyler Durden

The past few years have been a feeding frenzy for most major asset classes. Stocks blew through previous highs, as did trophy real estate, fine art, and, most recently, Treasury bonds.

A big part of the reason for what came to be called the everything bubble was the sense that with everyone else making easy money, the worst possible fate was to be stuck on the sidelines, a sentiment known as “fear of missing out,” or FOMO.

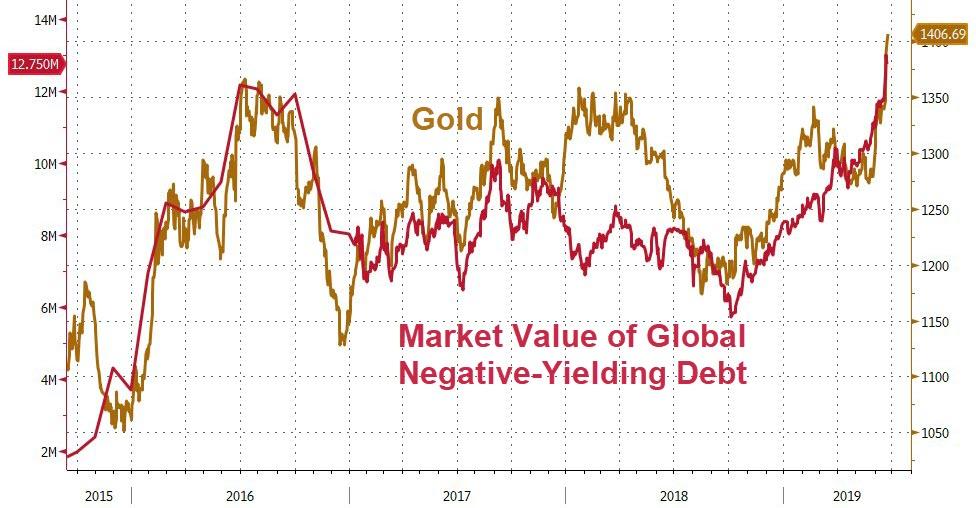

Gold, alas, wasn’t invited to this party and has languished far below its 2011 high, while bouncing off resistance at the $1,360 level five (!) times over the past five years.

That may have changed this month. As central banks move back into easing mode – with interest rates already at historic lows, implying that future cuts will take even more of the world into negative territory – and the US blunders ever-closer to a major shooting war, safe haven assets are suddenly in vogue. And gold has popped.

Now the emotional tone of the precious metals market borders on giddy, with dozens of recent headlines quoting analysts on their upwardly-revised gold price targets and new buy ratings on precious metals mining stocks.

In other words, where just a few weeks ago would-be gold and silver buyers thought they had plenty of time and feared being stuck in a dead-money asset, they now feel like time is running out. FOMO has become their dominant impulse.

Here’s an excerpt from a King World News interview with Michael Oliver, a technical analyst who has been predicting a sharp, quick upward move in precious metals for the past few months and was – sharply and quickly – proven right in June. Not surprisingly, he thinks the current move has very long legs:

This is a new massive gold bull leg that’s an extension of the bull market that began in the 1970s…Most price chart analysts are looking at this and are thinking ‘I have to be in this or I’m’ going to miss it.’ We’ve rapidly taken out the highs of the past five years. Money managers who have not been in gold are being jolted into the sense that they have to be part of this. Especially with the gold miners, which are rising at double the rate of the metals. When these folks start to move assets into this sector it can have a dramatic effect. They’ll move explosively higher.

Most people will be shocked where the next rest stop for the gold miners. GDX was $20 recently and could be above $30 in short order. It’s a new dynamic and all the price-related technical indicators that most people look at will be shattered to the upside. Ignore those overbought signals.

By the end of the year we should see $1,700 in gold. That’s not the end, it’s just where it will be at year-end. We’re in a major situation.

Silver, meanwhile, is about to slingshot to catch up with gold. It will do twice as well as gold, too quickly to allow time for committee meetings to decide whether or not to buy. You won’t get a measured move – expect a move from the mid $15s to over $20 in a matter of weeks. But that will be just the beginning.

If you’re not there you’re going to miss it.

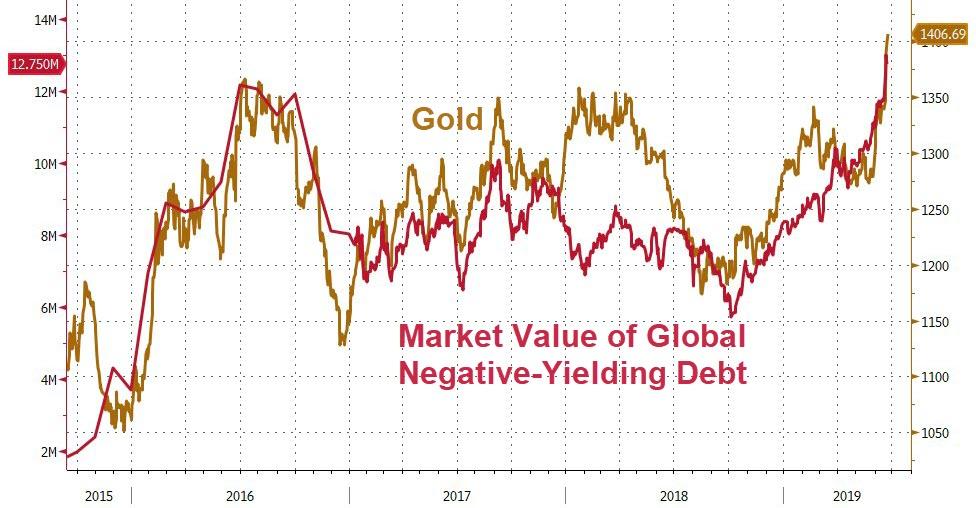

[ZH: Finally, while we are well aware that correlation does not imply causation, the following chart of the extremely close relationship between zero-yielding gold and the amount of negative-yielding debt in the world suggests the precious metal is acting just as it should – as a hedge against a world gone mad]

So, don’t fight the global central bank credibility collapse, buy gold.

via ZeroHedge News http://bit.ly/2IGmcgb Tyler Durden

As President Trump prepares to move ahead with plans to slap new sanctions on Iran – which he promised over the weekend – the Iranians are doubling down on their own threatening language, warning that their armed forces wouldn’t hesitate to shoot down more US surveillance drones if Washington continues to press them.

Late last week, the Trump administration reportedly called off a planned military strike after Iranian forces shot down the drone, which was worth more than $100 million, and furthermore warned that they could have shot down an American spy plane carrying dozens of people (according to the Iranians) but they chose not to (an indication of their benevolence before the Trump administration).

Iranian President Hassan Rouhani

But even as Washington continues to lather its belligerent rhetoric with offers to engage with Tehran, the Iranians remain extremely wary, and have followed up mostly with threats of their own, according to the AP, Iran’s naval commander, Rear Admiral Hossein Khanzadi, warned Washington that Tehran is capable of shooting down other American spy drones that drift into Iranian airspace (Washington contends that the drone was flying over international waters when it was shot down).

“We confidently say that the crushing response can always be repeated, and the enemy knows it,” Khanzadi was quoted as saying by the semi-official Tasnim news agency during a meeting with a group of defense officials.

Meanwhile, Tehran has rebutted reports that Washington launched a cyberattack against Iran late last week by warning that the attack wasn’t successful. In a number that sounds slightly exaggerated, Iran’s minister for information said Iran ‘neutralized’ 33 million attacks with its firewall last year.

“They try hard, but have not carried out a successful attack,” Mohammad Javad Azari Jahromi, Iran’s minister for information and communications technology, said on Twitter.

“Media asked if the claimed cyber attacks against Iran are true,” he said. “Last year we neutralized 33 million attacks with the (national) firewall.”

As tensions with the Iranians flared, Secretary of State Mike Pompeo traveled to Saudi Arabia over the weekend. During a meeting with King Salman in Jeddah on Monday, Pompeo said he wanted to build a “global coalition” to push back against Tehran, according to Reuters.

“We’ll be talking with them about how to make sure that we are all strategically aligned, and how we can build out a global coalition, a coalition not only throughout the Gulf states, but in Asia and in Europe, that understands this challenge as it is prepared to push back against the world’s largest state sponsor of terror,” Pompeo said about Iran.

But even as Pompeo kept up the belligerent train of remarks, he emphasized that Washington is still open to talks with Tehran, though Tehran has indicated that it won’t abandon plans to start stockpiling enriched uranium again until the US backs off on its crude-oil export ban.

“They know precisely how to find us,” Pompeo said.

Next, the secretary of state will travel to Abu Dhabi for a similar round of meetings.

via ZeroHedge News http://bit.ly/2IH44mx Tyler Durden