Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/30TCqf0

via IFTTT

Billionaire financier and political puppeteer George Soros says he’s no longer invested in financial markets – admitting to Italy’s La Repubblica that we’re caught in a bubble fueled by Fed liquidity, and that ever since he shared his methodology in his book, “Alchemy of Finance,” he no longer has an advantage.

Soros explained that “two simple propositions” drove his investment strategy, according to MarketWatch.

“One is that in situations that have thinking participants the participants’ view of the world is always incomplete and distorted. That is fallibility,” he said, adding “The other is that these distorted views can influence the situation to which they relate and distorted views lead to inappropriate actions. That is reflexivity.”

He went on to say the market, which he no longer participates in, is sustained by the expectation of more fiscal stimulus along with hopes Trump will announce a vaccine before November. –MarketWatch

“We are in a crisis, the worst crisis in my lifetime since the Second World War. I would describe it as a revolutionary moment when the range of possibilities is much greater than in normal times. What is inconceivable in normal times becomes not only possible but actually happens. People are disoriented and scared. They do things that are bad for them and for the world,” he told the outlet.

Turning his attention to politics and the pandemic, Soros – who’s contributed $52 million towards political spending during the 2020 election cycle, said that the United States is better positioned to weather COVID-19, but President Trump “remains very dangerous” because “he’s fighting for his life and he will do anything to stay in power.“

“Even in the United States, a confidence trickster like Trump can be elected president and undermine democracy from within,” he said, adding “But in the U.S. you have a great tradition of checks and balances and established rules. And above all you have the Constitution. So I am confident that Trump will turn out to be a transitory phenomenon, hopefully ending in November.”

In May, Soros claimed that Trump would be a “dictator” without the US Constitution in place, according to Breitbart‘s Josh Caplan. “But he cannot be one because there is a constitution in the United States that people still respect. And it will prevent him from doing certain things. That does not mean that he will not try, because he is literally fighting for his life,” Soros told the Independent.

“I will also say that I have put my faith in Trump to destroy himself, and he has exceeded my wildest expectations.”

via ZeroHedge News https://ift.tt/2FmJXuD Tyler Durden

I feel a bit of rant coming on… Yesterday’s dismal UK numbers were not a surprise – unless you expected them to be even worse. A 20% quarter on quarter Q2 decline in GDP, deeper than anywhere else (except possibly Spain), and the deepest and fastest recession on record. Germany was down 12%, while US GDP was down a mere 10.5%. Sweden – which didn’t lockdown, was down 8.6%. Unemployment is going through the roof. Companies are planning redundancies, and no one is going to get Christmas holidays again. Ever. We have become addicted to government support – the papers say we face a house price collapse next year when stamp-tax holiday ends, and it’s a stark choice of putting everyone on permanent furlough or redundancy.

Why is the UK so shockingly bad?

There are probably good reasons for our miserable performance in terms of the detail of how our retail and services sector works, the density and health of our population, our genetics, even our habit of stopping to chat and greet friends and neighbours.. or it might have been issues like the length of lockdown. It might also be the way we record data – already the number of Covid Deaths has been revised downwards, and could go lower yet. What the UK did wasn’t so different to what other countries tried – the timing of when we started and finished lockdown was days rather than months, but it has been seized upon as critical evidence of government incompetence.

The result is going to be a witch-hunt. We need someone to blame.

Whatever the UK did right or wrong, somehow we managed to turn a mere economic catastrophe into a full blown apocalypse. If this was the Olympic COVID Pants Performance competition, we just scored a perfect set of 10s for our sheer crapness.

And it’s unlikely to get much better. Half the nation still believes the Virus is going to kill them given any chance – they have been properly scared. The other half has no interest in returning to work while there are still beaches with pubs on them… assuming their jobs are doomed, so they are enjoying their last furlough cheques before Winter comes a knocking…

It’s very easy to blame government – Boris’s shambolic nature means he’s going to be very easy to scapegoat. But consider the alternatives… it would hardly be fair to inflict even worse politicians on out poor benighted county. Her Majesty’s Loyal Opposition are braying for blood – but they would have done equally badly, if not worse.

And blaming government is exactly what the establishment is hoping for. Anything to deflect from the multiple failings of the UK’s bloated, self-serving and unaccountable establishment – the multiple bureaucracies of uncivil service. Poorly advised governments tend to underperform. If there was failure in the UK, then it occurred at the institutional level – not in parliament, but within the apparatus of state that advises and runs the country. If we want to sort it and avoid repeat.. then it’s time to shake the foundations of the state and introduce the concepts of responsibility and accountability. With prejudice.

Let’s give government some credit for the swift application of furlough and bailouts. It would be easy to blame the BBC for dramatizing crisis, but I stopped watching TV news months ago…. It was just too pointless and depressing.

The Pandemic triggered successive failures across the nation. Heads should be rolling – but not the ones we know.

I want to know why NHS England was so unprepared despite having gamed the Pandemic a few years ago.

I want the models investigated.

I want to know what idiot thought it was fine for care home staff to continue working in multiple homes – thus the example of a care home in Skye taking on agency staff from London as a virus vector.

I want to know who advised government on schools.

I want a public enquiry on every aspect of the successive mistakes and escalating cascade of stupidity that characterised the virus in the UK.

Let’s look back at this farrago from start to finish – and let’s have some real accountability. When it is done.. let’s put the guilty up against the proverbial wall.

The real problem might be even worse. Fish rot from the head down – and I wonder just how fundamentally broken the country is. Once we were the envy of the world. Today we are a nation of petty bureaucrats. This is the country that’s never been conquered (well not since 1066 and all that), that’s taken on every European despot from Louis, Phillipe, Napoleon, The German and Barnier – and bowled them all out no matter how sticky the wicket.

Yet, we now face a far greater enemy – ourselves…

We’ve got Menshevik teachers in revolt – they’re happy enough to go an sit and drink Lady Petrol on crowded Cornish beaches with the rest of the Garuniad intellectual woke brigades – but ask them to look at the evidence and go back to actually teach kids and it’s no chance… “far too dangerous” they say..

Yesterday my wife tried to speak to her bank re her business accounts. She waited over an hour listening to a voice telling her how unexpectedly busy the bank was at this time. It suggested she go online – but that’s not pertinent when you need to speak to someone urgently to trace cash that’s gone adrift. Of course the bank in question was Britain’s most embarrassing institution – the People’s Democratic State Bank of Hong Kong and Shanghai – which isn’t picking up the phone to customers because: 1) it doesn’t give a ****, 2) its busily sacking thousands of staff while lecturing clients on how to be ESG, 3) It still doesn’t give a **** and 4) its new masters in Beijing don’t give a **** either.

Or while trying to cheer yourself up and boost the local economy, you go into your favourite restaurant and you are faced with a limited menu – limited because of the requirement of the chefs to socially distance in the kitchens. But actually, the chain is delighted with the limited menu because they can bring in the cheap junior staff to serve stuff your kids will learn to cook in school – if there was any school to go to…. Cheap nosh at full price with half the staff in the hope you will be “understanding about the problems created by the Coronavirus.” It’s a rip.

Of course, there are moments of light humour… like the anxious pub landlady who threw us out her pub and asked us to shout orders from the other side of the road because she was worried by our “London accents”. (I don’t have a London accent… but wtf..) “I can’t take the risk.. I have to think about the staff..” she said.. Congratulations.. your pub will be bust by September, and your staff will all be redundant.. That’s one way of looking after them…

Sadly, the UK has become complicit in our own downfall…

And the clearest signal of the complete and utter collapse of the UK as going long-term concern is The Decline of Sticky-Toffee Pudding.

The decline of STP is symptomatic of where our once proud nation is headed. In my spare time I am publisher of the world renowned “Sticky-Toffee Pudding International”, the journal of record for STP fans everywhere. Each quarter the top STP features on the front page.

In recent weeks I’ve noted a terrifying trend. Even top STP restaurants are now producing a shallow false shadow of the STP – they are serving Sticky Toffee Cake. FFS!! It’s not a STP without dates. Last time I checked the supply of dates into this island set upon a silver sea was not blocked by the pandemic.. there is no reason to blame the virus for a lack of dates!!! It’s just an excuse… lazy chefs hiding behind pandemic to cut out dates – the core, the essence, the life and very soul of a proper, scrumptious STP!

I am willing, in extemis, to accept this modern fashion of having vanilla ice-cream instead of custard (frankly its daft, but if it leaves more custard for me, I’m delighted.) But STP without dates is like Christmas without Santa, Arsenal without losing, a wedding without a fight, or Eric without Ernie.. What is being served today is simply Sticky Toffee Cake – a travesty of the traditional STP.

It’s wrong and it needs to be stopped. Any chef with STP on the menu who serves up Sticky Toffee Cake should be boiled in their own caramel. I shall be shaming certain restaurants in the October edition of STPI. I have already written to my MP demanding action – but I’m told he’s on a Cornish beach….

via ZeroHedge News https://ift.tt/3iDEBtb Tyler Durden

Futures Drop From All Time High As Concerns Over Stimulus Stalemate Grow Tyler Durden

Thu, 08/13/2020 – 07:58

S&P 500 futures dipped along with European stocks on Thursday, one day after briefly rising above the previous record high and closing just a few points below its all time high close, as the global rally showed signs of faltering as stimulus talks in Washington remained deadlocked. Gold and Treasurys were flat, while the dollar fell before key unemployment data.

Wall Street indexes had rallied on Wednesday with gains across most sectors, bringing the S&P 500 about 0.4% below its intraday record high hit on Feb. 19 before shares faltered as investors continue to wonder when Congress will agree on the much needed fiscal stimulus. The concern is that government lifelines merely deferred even more unemployment.

Cisco Systems dropped 5.8% premarket after forecasting first-quarter revenue and profit below Wall Street estimates and laying out a restructuring plan.

“It seems that the markets have been in glass-half-full mode in the past couple of sessions,” said Jane Foley, a strategist at Rabobank in London. “Even if we did get a new record today, the lack of liquidity in August would detract from the credibility of such a move.”

European stocks fell, ending their largest four-day rally in two months, with insurers and mining stocks pulled down benchmarks. Dutch insurer Aegon NV tumbled after its profit missed estimates and as it withdrew financial targets over uncertainty from the pandemic. The Stoxx Europe 600 Basic Resources Index led declines, dropping as much as 2.1% the most among sectors in Europe, as the global rally in equities fades and copper, zinc trade lower although th gold rebound continues. Miners fall even as gold pares some of this week’s slump: Rio Tinto -2.9%, Anglo American -3%, BHP Group -2.3%, Glencore -2.3%, ArcelorMittal -2.8%, Antofagasta -2.1%.

Markets continued to hold on to hopes the Democrats and the White House would reach an agreement to pump more money into the economy, with unemployment benefits being a sticking point.

Attention now turns to the weekly U.S. jobless claims data which is expected to show the number of Americans filing for state unemployment benefits dipped slightly from the prior week, printing at 1.1 million, although the labor market continues to struggle due to the pandemic. Last week, the government’s July jobs report showed the economy has regained only 9.3 million of the 22 million jobs lost between February and April.

Meanwhile, as we noted several weeks ago, the most hard-hit U.S. states continued to show signs of improvement, with Texas and California reporting falling hospitalizations from the virus.

In rates, Treasuries were unchanged, reversing a modest gain during the Asian session despite a record $26BN 30-year auction at 1pm ET (WI 30-year yield at ~1.358% is ~3bp cheaper than last month’s, which stopped 2.7bp through the WI yield at the bidding deadline; yesterday’s 10- year auction stopped through by less than 1bp after a selloff). Yields declined during Asia session as demand emerged following two-day selloff, are edging higher in early U.S. trading as dealers prepare to underwrite final event of this week’s auction cycle. Yields richer by 0.5bp to 2bp with 10-year around 0.67%, outperforming bunds by 2.5bp, gilts by 1.5bp. According to Bloomberg, large short base may support a covering bid into the auction, while leaving the sector vulnerable to a squeeze.

In FX, the dollar dipped and the euro and pound both advanced against the greenback, mostly helped by sustained dollar weakness. Sterling was stable against the euro, but it remains vulnerable to the common currency, according to Rabobank’s head of FX strategy Jane Foley.

In commodities, oil steadied after rising earlier on signs of improving demand while gold resumed its advance after the Monday crash.

Looking at the day ahead now, the data highlights include the weekly initial jobless claims from the US along with the final July CPI reading from Germany. Fed speakers include Bostic and Brainard, while the Mexican central bank will also be deciding on rates. Tapestry and Applied Materials are among companies reporting earnings.

Market Snapshot

S&P 500 futures little changed at 3,369.25

STOXX Europe 600 down 0.5% to 373.17

MXAP up 0.5% to 171.17

MXAPJ up 0.09% to 564.39

Nikkei up 1.8% to 23,249.61

Topix up 1.2% to 1,624.15

Hang Seng Index down 0.05% to 25,230.67

Shanghai Composite up 0.04% to 3,320.73

Sensex down 0.1% to 38,331.48

Australia S&P/ASX 200 down 0.7% to 6,091.00

Kospi up 0.2% to 2,437.53

Brent futures little changed at $45.41/bbl

Gold spot up 1% to $1,935.22

U.S. Dollar Index down 0.3% to 93.14

German 10Y yield fell 1.4 bps to -0.461%

Euro up 0.4% to $1.1830

Italian 10Y yield rose 1.8 bps to 0.836%

Spanish 10Y yield fell 0.3 bps to 0.3%

Market Snapshot

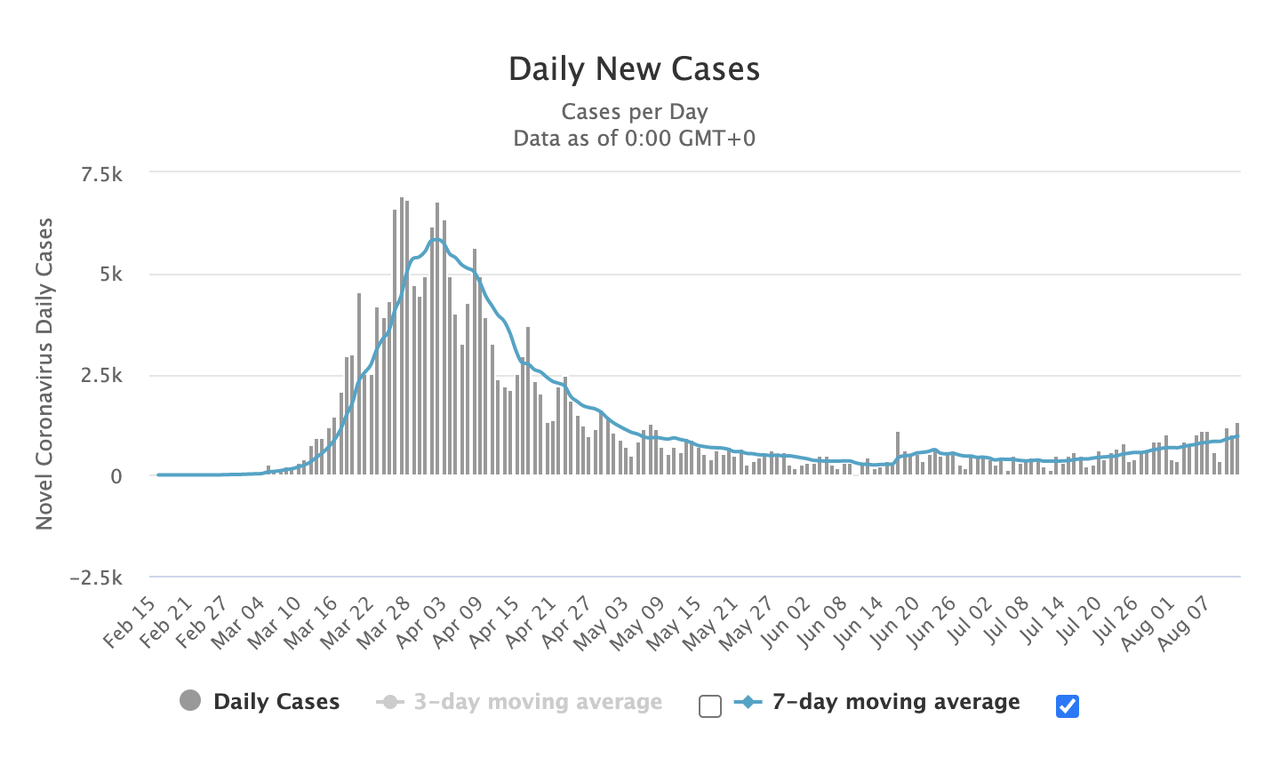

Virus resurgence across Europe continues with Germany recording the highest number of new cases in more than three months, with daily infections topping 1,000 for three days in a row. Meanwhile two Chinese patients test positive again several months after having recovered, raising fears that the virus could linger and reappear in people previously infected.

Around 3.4 million people in England — or 6% of the population — have caught coronavirus, according to a large-scale antibody study. The rate in the capital is twice as high, with 13% of Londoners having contracted the virus.

Australian employment rebounded in July, with an additional 114,700 jobs added to the economy, beating estimates. Unemployment lowered to 7.5%.

Sweden’s controversial virus policy may have saved the economy from a further 4% drop in GDP, according to Capital Economics. Sweden did not impose a strict lockdown, and the country suffered a higher death rate than comparable countries which did impose a lockdown. The Swedish economy contracted 8.6% in the second quarter.

Asian equity markets began mostly higher as the region took impetus from the tech-led gains on Wall St where the S&P 500 and Nasdaq moved to within close proximity of record highs, fuelled by strength across the big tech names and with Tesla front-running the advances following the recent announcement of a 5-for-1 stock split. However, some of the elation gradually waned overnight as focus turned to the deluge of earnings. ASX 200 (-0.7%) and Nikkei 225 (+1.8%) were mixed with price action for the biggest movers in Australia dictated by results, in particular the worst performers AGL Energy and Telstra after both posting weaker bottom lines for the full year, while the Japanese benchmark outperformed on a breakout above 23,000 to print its highest level since February. Hang Seng (Unch.) and Shanghai Comp. (Unch.) were indecisive with only minimal support seen from another substantial PBoC liquidity injection as geopolitical tensions remain in the background and tentativeness ahead of US-China talks on Saturday to assess the Phase-1 deal in which China will reportedly bring up WeChat and TikTok issues. Furthermore, Hong Kong was also kept indecisive amid choppy trade in index heavyweight Tencent which was eventually pressured despite topping earnings estimates as it refrained from an interim dividend and as it faces the impending WeChat ban in US. Finally, 10yr JGBs traded marginally higher after rebounding from yesterday’s floor and despite the strength in Japanese stocks, while the BoJ were also present in the market today for nearly JPY 1.2tln of JGBs in 1yr-10yr maturities.

Top Asia News

China Investors Pick Winners From Xi’s New Economic Mantra

Duterte to Use Russian Vaccine After Philippine Human Trials

Modi’s Key Ministers Hit by Coronavirus as Pandemic Grips India

Australia Employment Surges as Economy Absorbs Victoria Relapse

European equities have largely seen modest broad-based losses [Euro Stoxx 50 -0.2%] after a mixed APAC lead as earnings take focus amid a lack of fresh catalysts. UK’s FTSE 100 (-1.1%) sees more pronounced losses vs. the region amid currency dynamics, but more notably due to a slew of large-cap ex-dividends including the likes of AstraZeneca (-1.5%), BP (-2.4%), Diageo (-1.1%), GSK (-2.4%) and Shell (-2.5%) – together equating to just under a quarter (~24%) of the FTSE 100 by weighting. Sectors are mixed with no clear risk profile to be derived – Energy underperforms, IT remains somewhat afloat after its underperformance yesterday, whilst Telecom names see a firm performance on the back of Deutsche Telekom’s (+2.1%) earnings, which topped revenue and adj. EBITDA forecasts whilst the Co. also raised its FY20 adj. EBITDA AL guidance. In terms of individual movers, Airbus (-1.4%) shares remain pressured after the US maintained tariffs on the European aviation sector. Thyssenkrupp (-14.3%) shares tumbled at the open amid dismal numbers, whilst Wirecard (-13.8%) follows a close second after Deutsche Boerse has announced that subsequent to approving new rules in light of the Wirecard scandal, the new composition of the DAX will be published on August 19th, the review will see Wirecard removed from the index. Separate reports also noted that the Philippines government is mulling criminal charges for Wirecard executives forging travel data. Other earnings-related movers include RWE (+1.4%), Deutsche Wohnen (Unch), Lanxess (-1.1%), Swisscom (-0.3%) and Carlsberg (-4.8%).

Top European News

Zurich Insurance Sticks With Outlook as Virus Hits Profit

Sweden May Be Facing a Much Milder Recession Than First Feared

Wirecard’s Jan Marsalek Added to Interpol’s Most Wanted List

In FX, the Dollar remains depressed following another dead cat bounce and failure to reach 94.000 in index terms with the aid of firm US inflation data, and a retreat in Treasury yields amidst re-flattening across the curve is not helping the Greenback sustain gains as the DXY slips closer to the round number below. Meanwhile, bouts of risk-off trade due to the lack of progress on fiscal stimulus to replace maturing COVID-19 relief are fleeting and not providing the Buck any safe-haven sustenance, as 2nd wave concerns linger alongside global trade, diplomatic and geopolitical threats to the economic recovery. Ahead, initial claims will be monitored in context of the latter and recent signs that the re-opening return to employment is waning.

EUR/GBP/CHF/JPY – All benefiting at the expense of the Dollar, and technically in the case of the Euro as it builds a firmer base above the 200 HMA around 1.1800 eyeing 1.1850 next on the upside, while Sterling has recovered well from successive retreats towards 1.3000, albeit with Cable unable to reach 1.3100 again. Elsewhere, the Franc is probing 0.9100 and Yen has bounced a bit further from 107.00 to sit within a 106.92-57 range on the aforementioned less bearish UST yield/curve backdrop.

CAD/AUD/NZD – The Loonie has lost some impetus from crude, but meandering between 1.3256-26 parameters and the Aussie is holding above 0.7150 after better than expected jobs data, albeit mainly due to a jump in temporary workers keeping the overall unemployment rate relatively steady, but the Kiwi is lagging again following an attempt to revisit 0.6600 as the NZ pandemic resurgence continues and PM Ahern warns that the situation could get worse before slowing down again. Moreover, RBNZ Deputy Governor Bascand acknowledges a big risk to the outlook due to the growing cluster and a policy response in the event of an extended lockdown likely in the form of NIRP in tandem with a funding for lending facility.

SCANDI/EM – Some consolidation after recent volatile trade, and little reaction from the Nok or Sek to mixed Norwegian consumer sentiment, firmer Swedish 1-year CPIF expectations and NIER’s less recessionary 2020 GDP forecast. However, the Zar may respond to SA Gold and mining production as Eskom projects more load-shedding and the Brl has Brazilian services sector growth to digest.

In commodities, WTI September and Brent October futures eke modest gains after a flat APAC session, with prices on either side of 42.75/bbl and 45.50/bbl respectively. The IEA monthly report trimmed its 2020 demand growth forecast by 140k BPD, citing poor jet fuel demand, whilst also cutting the 2021 metric by 240k BPD. The report chimes more with the OPEC’s monthly report as opposed to the EIA’s STEO, as OPEC also trimmed its 2020 global demand forecast view in light of second wave fears, although IEA specifically mentioned poor jet fuel demand. The IEA and OPEC do however differ in their 2021 view as latter left its forecast unchanged. Elsewhere, Russian Energy Minister Novak pushed back against some speculation that OPEC+ could taper their cuts sooner than agreed on. Novak stated that there has not been any proposals to alter the OPEC+ deal and added the JMMC will not discuss changes to the OPEC+ deal this month when they meet on August 18th. Elsewhere, spot gold remains firmer within recent ranges having had found some interim support at USD 1925/oz, whilst spot silver remains somewhat capped by mild resistance near 26/oz. In terms of base metals, LME copper trades softer despite Shanghai September copper futures closing higher, as the former tracks European stock performance. Shanghai Stainless steel futures also saw a session of gains amid robust demand and recent slump in inventories.

US Event Calendar

8:30am: Import Price Index MoM, est. 0.6%, prior 1.4%; Import Price Index YoY, est. -3.05%, prior -3.8%

8:30am: Export Price Index MoM, est. 0.4%, prior 1.4%; Export Price Index YoY, prior -4.4%

8:30am: Initial Jobless Claims, est. 1.1m, prior 1.19m; Continuing Claims, est. 15.8m, prior 16.1m

9:45am: Bloomberg Consumer Comfort, prior 44.9

DB’s Jim Reid concludes the overnight wrap

Normal service appears to have resumed in markets again with the S&P 500 (+1.40%) doing its best to prove that Tuesday’s move was all but a small blip on its one-way ascent to new record highs. The index momentarily hit new highs yesterday but a move of just +0.18% or more today is all it will take to get it there on a closing basis now. Unlike previous days it was a rotation back into tech stocks which did most of the hard work yesterday, with the NASDAQ (+2.13%) recouping a decent chunk of the move lower in the three days into Tuesday.

To be honest there wasn’t a huge amount for markets to get stuck into. Democratic House Speaker Pelosi reiterated for the umpteenth time that the two sides were “miles apart” on some of the issues in stimulus talks – although markets once again turned a blind eye. Treasury Secretary Mnuchin reiterated the Republican offer of just over $1 trillion in stimulus, telling Fox Business Network that Democratic demands for higher spending could always be done later in the year or in January, and that “we don’t have to do everything at once.” Fed speakers also waded in, with Rosengren saying it would be very bad news it there isn’t additional stimulus. The bottom line is that the main negotiators haven’t spoken since Friday and it’s not clear when talks will resume.

Risk also survived a bumper US inflation print. In fact, the +0.6% mom core CPI reading was the largest monthly rise in almost 3 decades and was well above the +0.2% reading anticipated. In response, US 10-year breakevens rose to 1.666% (up to 1.684% overnight), putting them back at their mid-February levels before worries about the global spread of the pandemic gathered pace. The Treasury curve had already bear steepened prior to the data and in fact if anything, some of the wind was taken out of the sails with 10y yields ending just +3.4bps higher – a record 10y auction also being absorbed with ease – and the 2s10s curve +2.3bps higher at 51.2bps (it did touch 52.7bps at the intraday highs).

Meanwhile, the USD struggled with the Dollar index ending -0.20% (is down a further -0.21% overnight) while the Japanese Yen was the worst-performing G10 currency for a second day running. A host of dovish comments from Fed officials did little to help the Dollar’s case. Gold was one of the exceptions to this safe-haven selloff, seeing a modest recovery from its worst day in 7 years on Tuesday to move +0.21% higher, and silver was also up +2.90%. Gold and silver are building up on yesterday’s advances by being up +0.86% and +0.96% respectively this morning too. Elsewhere in the commodities sphere though, oil prices reached new post-pandemic highs, with Brent crude up +2.09% to reach $45.43/bbl.

In terms of Asia this morning, it’s been a more mixed trading session with Nikkei (+1.87%) leading the advance and the Kopsi (+0.80%) also up but the ASX (-0.76%) and Hang Seng (-0.12%) are down and the Shanghai Comp unchanged. Futures on the S&P 500 are also flat. The only data out this morning came from Japan where July PPI came in at -0.9% yoy (vs. -1.1% yoy expected).

As for the latest on the virus, overnight New Zealand saw another 13 new cases in its fresh outbreak while Singapore quarantined 800 migrant workers after a case was discovered in a dormitory that had been cleared. Meanwhile, in the US, new cases grew by 1.1% in the past 24 hours. Hospitalizations in Texas dropped to a six week low and in New Jersey, Governor Murphy gave the state’s public schools the option of all-remote classes.

Back to markets yesterday, where in Europe the STOXX 600 rallied +1.11% to post its fourth consecutive daily gain. European banks faded into the close but still finished up +0.31% with bonds selling off. Indeed yields on 10yr bunds (+2.9bps), OATs (+2.8bps) and gilts (+3.8bps) all moved higher. However, the tightening of peripheral spreads in Europe continued, with the spread of Italian (-1.3bps) and Spanish (-0.5bps) 10yr yields over bunds falling to their tightest level in almost 6 months.

In terms of other data yesterday, here in the UK, the economic impact of the pandemic was made clear by the Q2 GDP reading showing a -20.4% contraction, a number considerably worse than that already seen for the US, France, Germany and Italy. It was also the largest quarterly contraction since the series begins back in 1955, and comes off the back of a -2.2% decline in Q1. Looking forward however, the June GDP reading did show a month-on-month increase of +8.7%, stronger than the +8.0% reading expected, which continues the recovery from the trough back in April. Furthermore, as our UK economist Sanjay Raja writes (link here ), Q3 is poised for a strong recovery, with high frequency data showing a sizeable rebound in many industries.

The final data point yesterday came from Euro Area industrial production, which missed estimates with a +9.1% increase in June (vs. 10.3% expected). That said, the rebound from the nadir in April continued, with the year-on-year decline now “only” at -12.3%, a long way above the -28.6% yoy fall back in April.

To the day ahead now, and data highlights include the weekly initial jobless claims from the US along with the final July CPI reading from Germany. Fed speakers include Bostic and Brainard, while the Mexican central bank will also be deciding on rates.

via ZeroHedge News https://ift.tt/2DVjOlQ Tyler Durden

Germany Reports Biggest COVID-19 Tally In 3 Months As Outbreak Spreads “All Over The Country”: Live Updates Tyler Durden

Thu, 08/13/2020 – 07:55

Summary:

Germany sees new cases hit 3-month high

6% of England has been infected

Rural Indians grow weary of wearing masks

Philippines joins Brazil, UAE etc in planning Russian vaccine trials

South Korea sees cases hit 1-month high

Oxford-Astrazeneca vaccine produces “immune response” in test subjects

* * *

As schools reopen in Berlin and elsewhere, Germany has reported another day of 1,000+ COVID-19 cases and the biggest single-day reading in three months, with the health minister warning of outbreaks across the country, blaming the spread on partiers and holiday travelers.

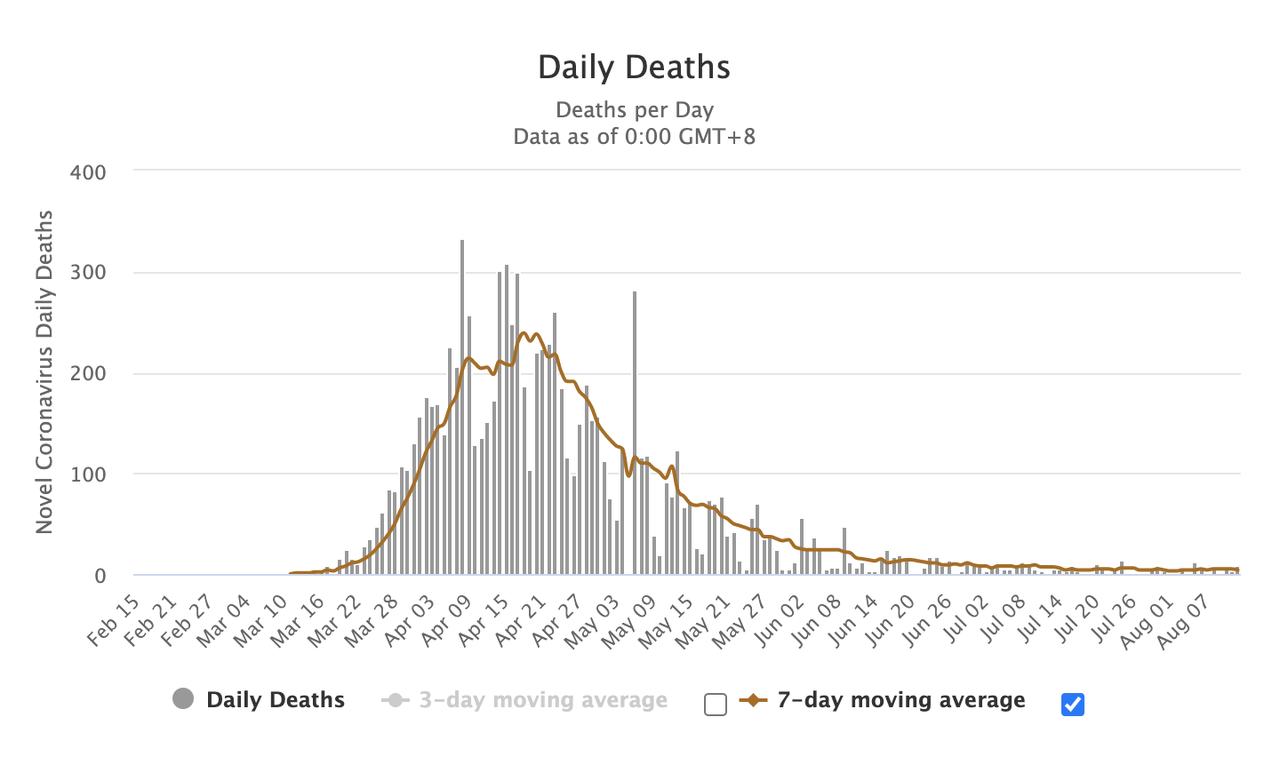

In the country of 83 million, the number of confirmed coronavirus cases climbed by 1,226 to 218,519, according to data from the Robert Koch Institute. That’s the biggest daily increase since May 9. Meanwhile, the number of deaths remained relatively low, increasing by six to a total of 9,207.

Chancellor Angela Merkel and the 16 state governments decided in May to start gradually easing coronavirus restrictions, a balancing act to allow public life and business activity to recover while trying to keep the infection rate low. Though the rate remains low relative to the US and other countries struggling with raging outbreaks, keeping cases at a manageable level requires a careful balancing act.

“This is, no doubt, very worrying,” said Health Minister Jens Spahn during an interview with Deutschlandfunk radio. He added that Germans must remain “very cautious” to avoid spread of the virus.

The fate of the European economy could very well hinge on a V-shaped rebound that economists say might be possible if another round of damaging lockdowns can be avoided. In Spain and the UK, local measures have been favored, like ‘partial lockdowns’ in parts of Manchester and in Catalonia, efforts that the WHO has applauded.

In other news out of Europe, the FT reports that roughly 6% of people in England have been infected already, which is roughly 1/10th of the minimum level of penetration experts believe would be necessary for ‘herd immunity’ to slow the virus.

About 6% of people in England had the virus by the end of June, equating to roughly 3.4 million, a study by Imperial College London found. London was found to have the highest rate of infection in the UK, at 13%, while the South West had the lowest, at 3%. The findings were part of the REACT study, commissioned by the Department of Health and Social Care.

That study incorporated antibody test results from more than 100,000 Britons. The data was roughly in line with surveillance data published by the ONS, which showed that 6.8% of people in England received antibody tests. In Black, Asian and minority ethnic people were 2-3x as likely to have had the virus than white people.

Early data from trials of three potential vaccines showed promise of fighting COVID-19 without serious side effects, while leaders in the United States and European Union pushed for massive stimulus to cushion the economic blow from the pandemic. Coronavirus cases in Spain have risen three-fold over the last three weeks as authorities struggle to contain a rash of fresh clusters. Sweden is changing its contact tracing guidelines to make more of the information gathered self-reported by the infected.

In India, where antibody testing run in the slums has, in at least a few instances, turned up positivity levels north of 50%, many in rural areas, where the virus has largely died out, are growing weary of social distancing requirements like wearing masks, creating a parallel to the mask debate in the US.

In two dozen small towns and villages visited by Reuters reporters in recent weeks, people have largely given up on social distancing and masks after months of sticking to the rules, believing the virus is not such a serious threat.

Harmahan Deka doesn’t wear a mask anymore to avoid the novel coronavirus nor does he try to keep a safe distance from others.

For the 25 men and women he works with in his construction materials business near the small town of Baihata Chariali in India’s Assam state, life is more or less as it used to be, Deka says.

“The virus can’t attack me, it’s weakened,” the 50-year-old diabetic said. “I often hang out at a busy neighbourhood grocery store – without masks, nothing. Both the store owner and I are fine. Maybe we’ve had it already without symptoms.”

In two dozen small towns and villages visited by Reuters reporters in recent weeks, people have largely given up on social distancing and masks after months of sticking to the rules, believing the virus is not such a serious threat.

Though incidence rates are low, the virus remains a threat, and the poor health infrastructure in the countryside makes following social distancing rules all the more critical, the public health officials said.

The change in behaviour in rural India – where two-thirds of its 1.3 billion people live, often with only the most basic health facilities – has come as infections in the countryside have surged.

Health officials are exasperated.

“Sometimes people take it too lightly, as if nothing will happen to them just because they’re breathing fresh air and eating fresh vegetables,” said Rajni Kant, a member of a rapid response team of the state-run Indian Council of Medical Research (ICMR) set up to fight the pandemic.

“Health infrastructure is poor in rural areas, that’s why they have to strictly follow social distancing norms, wear masks, avoid crowded areas and keep washing hands. Otherwise they’ll suffer.”

As we reported earlier, the Philippines has joined a growing list of countries preparing to hold clinical trials for the Russia-approved COVID-19 vaccine developed by the world-renowned Gameleya Institute. As news about the Russian vaccine dominated headlines this week, the usual patter of updates from Western companies working on their own candidates has continued. Here’s a rundown of some recent vax news courtesy of Reuters:

An experimental vaccine being developed by AstraZeneca and Oxford University against the new coronavirus produced an immune response in early-stage clinical trials.

German biotech BioNTech and U.S. drugmaker Pfizer Inc said data from an early-stage trial of their experimental coronavirus vaccine showed that it prompted an immune response and was well-tolerated.

A vaccine developed by CanSino Biologics Inc and China’s military research unit has shown to be safe and induced immune responses in most of the recipients who got one shot.

Finally, moving east, China and Hong Kong have seen infection numbers continue to decline following flareups earlier this month, but in South Korea, health officials reported 47 new locally transmitted cases, a one-month high amid concerns about a new batch of potential clusters.

via ZeroHedge News https://ift.tt/2CojA6p Tyler Durden

“A Vaccine Or Nothing” – Philippines Plans Russian Vaccine Trials To Begin In October Tyler Durden

Thu, 08/13/2020 – 07:00

A couple of days after Philippines President Rodrigo Duterte volunteered to take a test dose of the Russia-approved vaccine (after President Vladimir Putin claimed one of his two adult daughters received a course of the vaccine during “the experiment”), the Philippines has officially agreed to run clinical trials of “Sputnik V”, and if successful, it would be registered for use within the country by April 2021.

A spokesman for Duterte said on Thursday that trials would begin in October and, if they were successful, the “Sputnik V” vaccine would be registered for public use by April or May 2021, according to the FT.

This, even after Dr. Scott Gottlieb, the former head of the FDA who quit to “spend more time with family” just months before the outbreak began (thereby missing out on the star turn of a lifetime), said on CNBC that he “wouldn’t take it”, referring to the Russian vaccine, explaining that the “adenovirus vector” favored by the Ruskies is similar to CanSino’s candidate, which, Gottlieb claimed, hasn’t produced much promising data.

Though he will need to wait until the spring, according to his spokesman Harry Roque, Duterte will indeed be one of the first injected with the vaccine in the country: “It’s not a metaphorical statement,” said Mr Roque in an online briefing with journalists. “He is willing to undergo it.”

Pundits told the FT that, as the country’s outbreak roars back amid economic reopenings ordered by Duterte, which inspired him to revive restrictive lockdowns in the capital, Manila, it’s clear his strategy is to bring a vaccine to market as quickly as possible.

“I think Duterte’s strategy is a vaccine or nothing,” said Richard Heydarian, a political analyst and author of a book on the leader. “This guy has gone from typical populist dismissiveness toward the crisis to becoming one of the world’s biggest supporters of lockdowns.”

To be sure, the advent of the vaccine in the Philippines will likely be met with a mix of skepticism and hope, since the country has a history of being burned by vaccines: As the FT points out, the country suspended Sanofi’s Dengvaxia dengue vaccine in 2018 after Philippines officials connected it to a spate of illnesses and deaths, even as Sanofi has insisted that the vaccine is “safe”.

Russian doctors and teachers start getting vaccinated, advanced trials are set to start Wednesday that will involve “several thousand people” and span several countries, including the UAE, Saudi Arabia and possibly Brazil.

via ZeroHedge News https://ift.tt/3fVuFcN Tyler Durden

Failure To Reach Deal On Federal Stimulus Plan Risks Consumer Spending Recession Tyler Durden

Thu, 08/13/2020 – 06:00

Submitted by Joseph Carson, former chief economist at AllianceBernstein

Failure to reach a compromise on a broad federal stimulus plan creates a big “hole” in consumer’s cash flow. The “hole” is so big it raises the risk of substantial reduction, if not a recession, in consumer spending in the coming months.

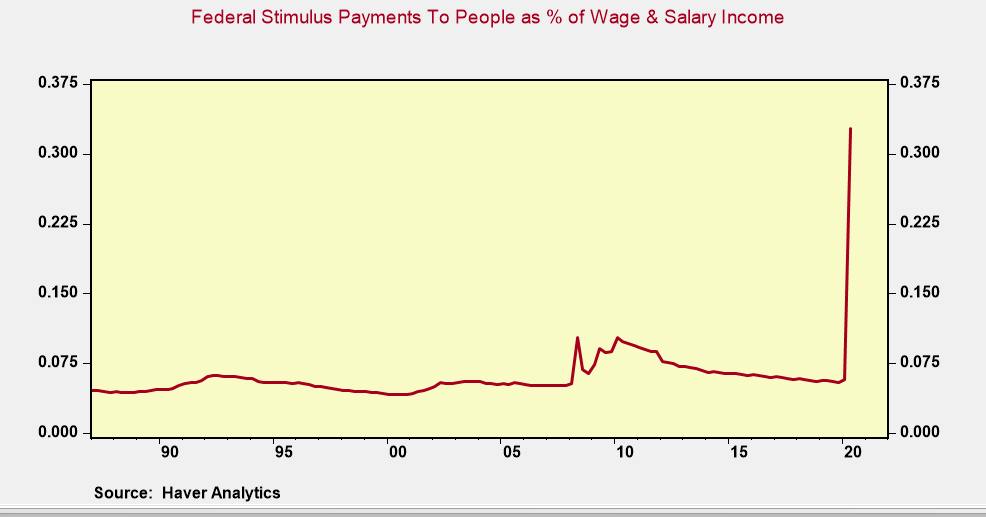

Record Federal Stimulus In Q2

According to the Bureau of Economic Analysis (BEA), special federal payments to individuals (and small businesses) in Q2 totaled more than $ 3.2 trillion annualized. That boost to personal income resulted in a 7% quarterly gain in Q2, wiping out what would have been a 10% reduction based on record job losses, and reduction in hours worked and pay.

Included in those numbers are the direct stimulus payments to people, a weekly supplemental payment for unemployment, expanded unemployment payments to individuals who are not usually eligible for unemployment, forgivable loans to small businesses and non-profits to help cover payroll and other expenses, suspension of reimbursements paid to Medicare and suspension of interest payments on federally held student loans.

In Q2, the special federal payments to people (including small businesses) amounted to 25% of wage and salary income earned in the quarter. In other words, for every $4 of wage and salary income, people working and idled (and small business owners) received another $1 from the federal government.

According to the payroll employment data from the Bureau of Labor Statistics, there were 133.7 million people employed in Q2. That means the record federal stimulus payments were the equivalent of 33 million jobs.

The abrupt and sharp loss of income has not been lost on economic experts, even those that occupy the White House. Fearing a sharp drop in spending due to the loss of record federal stimulus payments the Administration’s economic team recommended the president sign executive orders to provide a temporary extension but smaller scale of unemployment compensation and a three month holiday in payroll taxes.

This band-aid plan is too small to fill the “holes” and also too slow in getting monies to people fast. That’s because the additional unemployment program will take several weeks to set-up and also require states to pay for one-fourth of the plan. But most states don’t have the monies to comply so some unemployed people might not see any benefit at all.

Businesses are undecided on the payroll tax holiday. That’s because it will be difficult for them to implement since it only applies to part of their workforce, and it needs to be repaid at some point in 2021. As a result, many companies may opt-out, resulting in little or no short-term boost to consumer cash flow.

With each passing day, failure of Congress and the Administration to reach a deal on the federal stimulus plan raises the risk of a hard fall in consumer spending. Millions of people have not paid rent or mortgages over the last few months and the federal stimulus payments offered them a short-term “lifeline” just to sustain minimum household spending.

I have never been a believer in double-dip recessions. But the sharp drop in consumer income may make it a reality for investors.

via ZeroHedge News https://ift.tt/2PKVAxg Tyler Durden

Mnuchin Begs For Coins Amid Shortage; Avoid Depositing These Pennies Tyler Durden

Thu, 08/13/2020 – 05:30

Treasury Secretary Steve Mnuchin urged his Twitter followers on Tuesday to swap out their spare coins for cash at banks amid a continuing nationwide coin shortage that appears to be worsening.

If you have extra coins at home, please use them to make purchases— or deposit them at the bank or exchange them for cash. Help get coins moving! 🇺🇸

There’s currently a shortage of pennies, nickels, dimes, and quarters caused by the coronavirus pandemic, which led the Federal Reserve to start rationing coins in June.

Community banks have asked customers to deposit spare change to pump more coins into circulation. Because of the shortage, major retailers have told consumers to pay in cards or exact change.

“Until coin circulation patterns return to normal, it may be more difficult for retailers and small businesses to accept cash payments,” the US Mint said in late July. “For millions of Americans, cash is the only form of payment and cash transactions rely on coins to make change.”

Now, before readers start rummaging through their homes, underneath sofa cushions, and under car seats for spare coins to help the country in these challenging times, there are certain coins in circulation that are worth more in scrap than face value.

According to Coinflation.com, pennies from 1909-1982 are approximately 95% copper and have a metal value of about $0.0185. In this instance, once could almost double their money if they took these pennies to a scrapper than the bank. Here’s the complete list of what coins are worth in terms of face value versus metal value.

Another coin to watch is the nickel. It has been nine years since Kyle Bass first suggested the ‘nickel trade’, and the metal value is about 82% of face value. Though the trade is underwater, it’s not far off from the face value breakeven when considering other coins in circulation.

While Bass’ nickel trade underperforms, readers should think twice before depositing pennies from 1909-1982 at the bank because they’re worth way more in scrap.

via ZeroHedge News https://ift.tt/3fUnn9g Tyler Durden