Silver Futures Spike Above $23, “Has Long Way To Go” Tyler Durden

Wed, 07/22/2020 – 08:25

As European trading opened, it seems someone (cough Benoit cough) wanted silver prices lower, but as the US session gets started, futures prices have reaccelerated, crossing above $23…

Source: Bloomberg

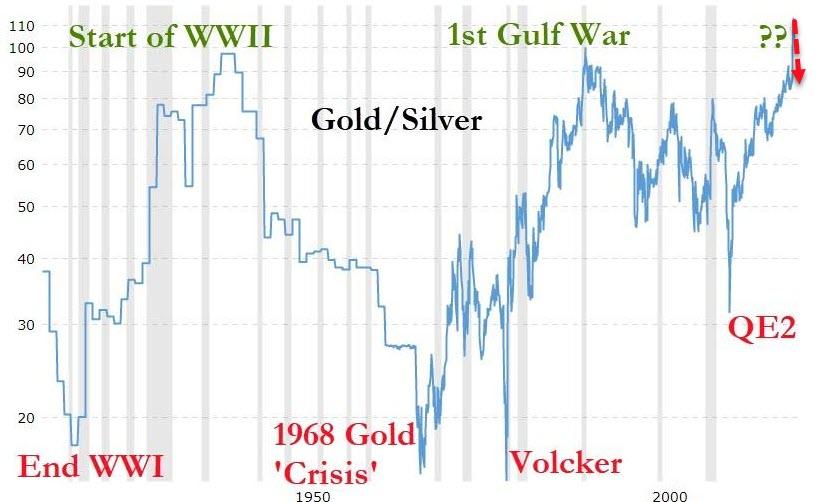

Gold is steady this morning (at cycle highs), which has pushed the gold-silver ratio down to its lowest since Sept 2019…

Source: Bloomberg

But, the ratio has a long way to go from its current 80x to its ‘average’ 50x-ish level…

Peter opened up the show talking about soaring stocks. NASDAQ in particular is booming. But most of the money is going into a handful of stocks that have benefited from coronavirus — as Peter called them, the stay at home stocks. But Peter said these companies are still going to be affected by COVID-19.

Because so many of their customers are about to be broke. Just because people have access to your products doesn’t mean they’re going to be able to buy your products. Just because they can buy your products from home doesn’t mean they’re going to do it if they don’t have any money.”

Peter said what investors should be doing is looking at gold, silver, gold stocks, and silver stocks.

Those are the real COVID plays because the way the government is trying to prop everything up and bail everybody out is by creating inflation. And the best hedge against inflation is not an overpriced social media company but extremely undervalued mining companies that are mining the money that the Federal Reserve can’t print, and the money that is likely to replace the US dollar in the global financial system as the primary reserve asset for central banks — and that is gold.”

The real action over the last few days has been in the gold and silver markets – particularly in silver. Peter has talked about the potential for silver for some time. But though silver has made a big move of late, Peter said this is not the big move that he’s been forecasting.

What I think is going to happen is going to be much bigger than today’s 7% gain at the peak.”

The white metal ended up closing up about $1.30 on July 21, and it eclipsed the $21 per ounce level. But keep in mind that silver was close to $50 in 2011.

That is the next stop. Believe it or not, that’s where the real resistance is and that’s where we’re going.”

But Peter said it won’t stop there. Once silver breaks through $50, he said it will go “much, much higher.”

Silver actually has a double-top around $50. It first got to that level in 1980 and then again in 2011.

Fifty-dollars looms very large. But there’s an old saying about these double-tops. I think they’re made to be broken, and silver is going to break this double-top. And the fact that it’s been there for so long means that when it does break — look out!”

Consider how far silver dropped. You could buy silver for $11 or $12 in March. Peter said he bought some silver coins himself.

Once 50 goes from being resistance to being support, it’s going to be massive support. And it is going to provide kind of like a launching pad for a massive move up in the price of silver.”

The silver-gold ratio has been historically high for months. It was well over 100-1 back in March. It’s dropped to about 84-1, but that is still high by historical standards, meaning silver remains undervalued compared to gold. Peter said he thinks we’re starting to unwind that spread and the unwinding of this silver-gold trade is important.

Once they’re finished unwinding, that bit of selling pressure on gold is going to be gone, but all the selling pressure on silver is going to be gone because no one’s shorting it anymore. They’re just going to be buying it. And silver has a long way to go.”

Peter said silver’s breakout is a good sign for gold too.

The fact that silver was never confirming the gold bull market, some people saw that as a non-confirmation, and so another reason not to believe in the gold bull market because silver wasn’t participating. Well, now it is. So, you can’t say that anymore.”

So what is the rally in silver telling us? It’s a prelude to the dollar collapse Peter has been predicting for a long time. And he said we don’t have a lot of time.

The bottom is going to drop out of the dollar any day. Gold could go through the roof any day. And so, this is really a race – a race to beat the clock and get people out of the dollar.”

So, what does the silver and gold rally mean? Peter called it a canary in the coal mine.

And the canary is dropping dead.”

via ZeroHedge News https://ift.tt/2WM5u5D Tyler Durden

Gordon Johnson: 90% Chance Tesla Reports Q2 Profit, Helped By Regulatory Credits, Warranty Expense Reversals. & Deferred Revenue Tyler Durden

Wed, 07/22/2020 – 08:05

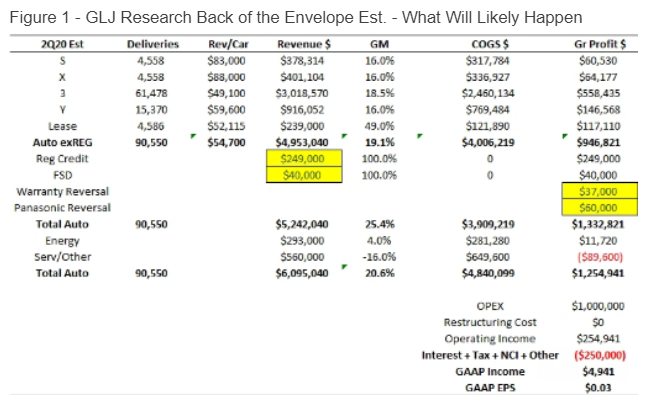

With S&P inclusion hinging on Tesla reporting a profit in Q2, analyst Gordon Johnson thinks that Tesla is likely to report a profit when it delivers earnings after the bell on Wednesday. The company will have several levers to pull in order to do so, Johnson says, laying them out in his latest report.

In a note published this week, Johnson predicts GAAP net income coming in at -$5.059mn, or a loss of -$0.03/shr. He bases his contention that the company will report a profit on several “levers” the company has to pull. First, he says Tesla will be recognizing deferred revenue from full-self driving (which we again remind readers, does not exist):

In short, as detailed in Ex. 1 below, our analysis is based primarily on the following assumptions: (1) on the 3Q19 call, TSLA’s CFO said the roll out of smart summon allowed them to recognize $30mn in deferred revenue; so that seems to be a good proxy for how much full-self-drive (“FSD”) revenue TSLA will recognize per the new feature rolled out in 2Q20 (i.e., red light recognition) – they had ~$600mn of FSD revenue as of 3/31/20, and have said a large chunk will be recognized when they reach full FSD, which they have not yet done.

Johnson also assumes that the company’s amended contract with Panasonic will allow the company to push unit costs lower, which will result in “an additional roughly 100bps in gross margin benefit”.

Regulatory credit sales will also play a key role in helping the automaker turn a profit, the note reads. Johnson says that “due to less cars sold in the EU in 2Q20, we assumed TSLA’s one-time (100% gross margin) regulatory credit sales are $249mn vs. $354mn last quarter”.

Finally, he thinks that Tesla will continue to game its warranty expenses:

Despite an increased incidence of product failure issues, we assume TSLA further, deceptively, reverses its warranty expense by $37mn (this is also a 100% margin “expense reversal”). Thus, with OPEX of ~$1bn, this gets one to -$0.03/shr in 2Q20 EPS. However, given how close this is to break-even, exacerbated by all the inorganic levers TSLA has in which it can pull, we see the probability of a 2Q20 profit/loss at 90:10.

Johnson raises the question at the end of his note whether or not the sell side consensus could be intentionally sandbagging Tesla’s forward estimates in order to create the “illusion” of perpetual outperformance.

Putting aside the fact that Wall Street has been known to do this across all sectors for as long as we can remember, Johnson makes a good point in saying that:

The current 2Q20 Consensus est. for TSLA’s 2Q20 earnings is -$1.20/shr. So what’s the big deal? Well, we see this as a demonstrably low low number given were this to prove accurate, TSLA’s near-term inclusion into the S&P 500 would disappear, and likely send the shares tumbling lower. Consequently, we see the lion’s share of sell-side analysts as intentionally sand-bagging forward ests. for TSLA.

In a matter of hours, we’ll know more…

via ZeroHedge News https://ift.tt/2WMComH Tyler Durden

Futures Slide After China Vows Retaliation To US Shutdown Of Houston Consulate Tyler Durden

Wed, 07/22/2020 – 07:56

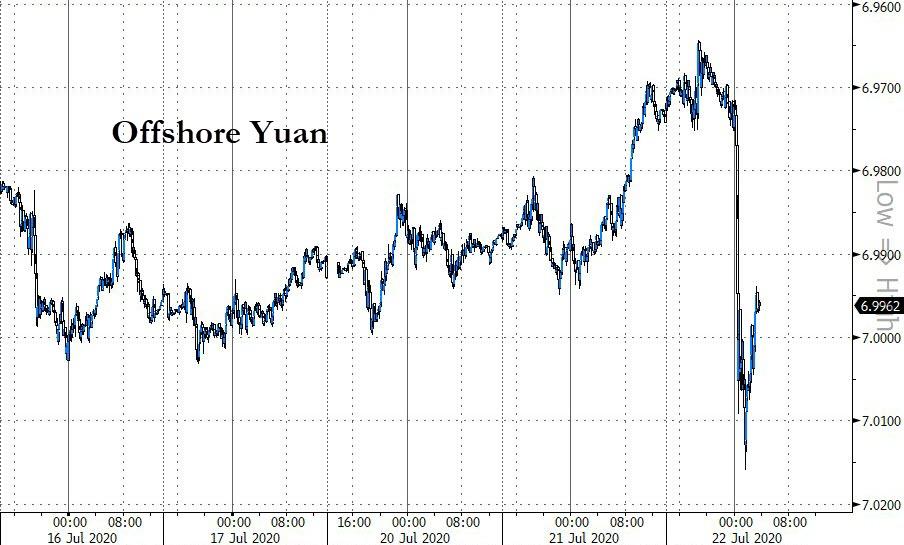

S&P futures slumped on Wednesday and European stocks fell after Washington ordered a shutdown of the Chinese consulate in Houston, citing a need to protect American intellectual property and information, amid a sharp deterioration in relations between the two countries (at least we now know why the Houston consulate was furiously burning all of its documents late on Tuesday). The State Department later said the order was to protect intellectual property and “private information” of Americans. Beijing in return vowed to “react with firm countermeasures”, and was reportedly considering the closure of the US consulate in Wuhan (of all places) escalating tensions between the world’s two largest economies and adding to concerns over the deteriorating relationship between the economic superpowers. Yields and the yuan fell, Hong Kong shares dropped and gold and silver dipped after soaring overnight on continued dollar weakness.

The U.S. Department of State confirmed the impending closure of the Houston consulate, after China’s foreign ministry reported it had been told to shut the mission. The closure had been ordered “in order to protect American intellectual property and American’s private information”, State Department Morgan Ortagus said in a statement.

“The United States will not tolerate the PRC’s violations of our sovereignty and intimidation of our people, just as we have not tolerated the PRC’s unfair trade practices, theft of American jobs, and other egregious behavior,” she added, referring to China by its official name, the People’s Republic of China.

In turn, China denounced the US order as an “unprecedented escalation”:

“The unilateral closure of China’s consulate general in Houston within a short period of time is an unprecedented escalation of its recent actions against China,” Chinese foreign ministry spokesman Wang Wenbin told a regular news briefing.

“We urge the U.S. to immediately revoke this erroneous decision. Should it insist on going down this wrong path, China will react with firm countermeasures,” he said.

The news comes after three straight sessions of gains for the S&P 500, driven by optimism about an eventual coronavirus vaccine, further fiscal support for the pandemic-hit economy and a batch of positive second-quarter reports. The index is less than 4% below its record closing high hit in February.

Some selling crept into stocks ahead of the Consulate news after Mitch McConnell warned that it is unlikely that a stimulus bill would be passed before the July 31 deadline when existing generous government handout programs expire.

Geopolitics aside, here are some company specific news:

Snap Inc declined 8.3% as it said a bump in user growth at the start of coronavirus-induced lockdowns petered out sooner than expected, and it forecast fewer current-quarter users than the Wall Street consensus.

United Airlines Holdings warned travel demand would remain suppressed until there was a widely accepted treatment or vaccine for COVID-19, which plunged the carrier to a deep quarterly loss. Its shares fell 0.1% in premarket trading.

Texas Instruments rose 4% rose after the company beat on the top and bottom line and guided to a higher Q3: EPS 1.48 (exp. 0.88/0.86 reported); Revenue 3.2bln (exp. 2.94bln); Q3 Revenue view 3.26-3.54bln (exp. 3.07bln); Q3 EPS view 1.14-1.34 (exp. 0.97)

Boeing 737 Max is unlikely to resumed widespread passenger flights until early next year, almost two months beyond prior guidance, amid regulatory delays, according to US officials cited by WSJ. Officials said the timetable could speed up and MAX operations could resume earlier, but it is not the expectations of those closely monitoring the process. Co. has a 4.5% weighting in the DJIA. Separately, a 737 craft has caught fire at the Shanghai airport, according to Xinhua.

Investors will also keep an eye out for quarterly results from Tesla and Microsoft after markets close.

“I’m more concerned going into the August, September period: what’s going to then be the next catalyst to take the broader market higher,” Andrew Sheets, a cross-asset strategist at Morgan Stanley, said on Bloomberg TV. It’s going to be “a tougher period for stocks,” he said.

European stocks slumped on the latest diplomatic spat, the Stoxx 600 sliding as much as 1.2% shortly after the news, while Asian stocks also fell, led by communications and health care, after rising in the last session. Most markets in the region were down, with Hong Kong’s Hang Seng Index dropping 2.3% and Singapore’s Straits Times Index falling 1.3%, while Taiwan’s Taiex Index gained 0.6%. The Topix declined 0.6%, with Access and Land Co falling the most. The Shanghai Composite Index rose 0.4%, with Junzheng Energy and Ningxia Xinri Hengli Steel Wire posting the biggest advances.

Elsewhere, treasuries edged higher and the dollar briefly rose on the latest geopolitical scandal.

The Bloomberg dollar index briefly erased a decline as haven demand picked on news that the U.S. abruptly ordered China to close its consulate in Houston. Earlier, the greenback came under pressure after President Donald Trump warned that the coronavirus crisis in the U.S. will probably worsen before improving. The Australian dollar and euro led gains, both rising for a fourth day against the greenback; the Aussie saw strong demand from exporters, real money and reserve managers, while the euro touched the highest since October 2018. The pound led losses, weighed down by a report that ministers believe the U.K. and EU may fail to sign a post- Brexit trade deal.

The euro gained a fourth day and touched its strongest level since October 2018 as investors chase the price action higher. In evidence of its strong momentum, the currency dipped twice during the London session toward 1.1510 and it was quickly bought both times; initially, it was unable to take out offers at 1.1550, especially after news that the U.S. abruptly ordered China to close its consulate in Houston. The common currency’s strength corners the Bloomberg Dollar Spot Index, which is testing a key support that has held since mid-2018; President Donald Trump’s warning that the coronavirus crisis in the U.S. will probably worsen before improving weighs on the currency.

In rates, Bunds outperformed Treasuries on haven demand, though Italian debt led gains in Europe following the EU’s recovery fund deal. Treasuries bull-flattened with yields lower by as much as 2bp across 20- to 30-year sectors, trailing long-end-led gains for German curve. U.S. session highlights include 20-year bond auction. Treasuries only marginally richer across front-end and belly, flattening 2s10s, 5s30s by 1bp and 1.7bp; 10-year yields around 0.587%, richer by 1.3bp while bunds outperform by 1bp.

In commodities, WTI and Brent futures have experienced some modest selling this morning. At present, the session low for WTI Sep’20 stands just above the USD 41/bbl mark and almost USD 1/bbl lower on the day. The downside stemmed from an escalation in reports relating to the US asking China to close their Houston consulate, which has been confirmed by both sides and seen China threaten to take retaliatory action unless this demand is rectified. For the complex itself newsflow has once again been very quiet, as a reminder the private inventory report last night showed an unexpected build of 7.54mln compared to consensus for a draw of 2mln going into the release, a release which placed the crude benchmarks under pressure. Turning to metals, where price action for spot gold has been comparatively quieter in the context of APAC price action. Overnight, the yellow metal extended on gains above the USD 1850/oz mark to a high of USD 1866.44/oz; price action which seemingly followed similar upward action in silver. In terms of a catalyst, no one driver has been attributed to the move but desks note COVID-19 reports alongside Fed nominee Shelton, a gold standard supporter, advancing at the Senate Banking Committee amongst factors.

Looking at the day ahead, the data highlights include the US existing home sales for June, the FHFA house price index for May, along with Canada’s June CPI reading. From central banks, we’ll hear from ECB President Lagarde and Vice President de Guindos. Finally, earnings out include Microsoft, Thermo Fisher Scientific and Tesla.

Market Snapshot

S&P 500 futures down 0.6% to 3,230.50

STOXX Europe 600 down 0.9% to 373.43

MXAP down 0.8% to 166.73

MXAPJ down 1% to 551.81

Nikkei down 0.6% to 22,751.61

Topix down 0.6% to 1,572.96

Hang Seng Index down 2.3% to 25,057.94

Shanghai Composite up 0.4% to 3,333.16

Sensex down 0.4% to 37,791.32

Australia S&P/ASX 200 down 1.3% to 6,075.06

Kospi down 0.01% to 2,228.66

German 10Y yield fell 1.4 bps to -0.474%

Euro down 0.07% to $1.1519

Italian 10Y yield fell 1.0 bps to 0.968%

Spanish 10Y yield fell 0.3 bps to 0.353%

Brent futures down 1.2% to $43.78/bbl

Gold spot up 0.5% to $1,851.26

U.S. Dollar Index up 0.2% to 95.33

Top Overnight News from Bloomberg

The dollar briefly erased adecline as haven demand picked on news that the U.S. abruptly ordered China to close its consulate in Houston. Earlier, the greenback came under pressure after President Donald Trump warned that the coronavirus crisis in the U.S. will probably worsen before improving

The Australian dollar and euro led gains, both rising for a fourth day against the greenback; the Aussie saw strong demand from exporters, real money and reserve managers, while the euro touched the highest since October 2018

The pound led losses, weighed down by a report that ministers believe the U.K. and EU may fail to sign a post- Brexit trade deal

Bunds outperformed Treasuries on haven demand, though Italian debt led gains in Europe following the EU’s recovery fund deal

APAC stocks traded mixed following a similar handover from Wall Street, in which the three indices saw downside in the latter part of the session as the US stimulus bill hit a bump amid differences over the size of the package and whether payroll tax cuts should be included. ASX 200 (-1.3%) lagged as cases stayed on an upward trajectory in Australia’s second largest state of Victoria, although miners saw a boost from the rally in precious metals. Nikkei 225 (-0.6%) failed to nurse opening losses as several large-cap stocks remained in the red, whilst recent JPY strength further weighed on exporters in the index. Conversely, Shanghai Comp (+0.4%) outperformed following yesterday’s pause, whilst Hang Seng (-2.5%) initially took a breather and remained in positive territory as oil giants kept the index afloat; before succumbing to the overall deterioration in sentiment. Finally, JGB futures ticked higher overnight after reports that that the Tokyo Governor is mulling stay-at-home orders, whilst the BoJ’s Rinban operations saw sizes for the 1-3yr, 3-5yr and 5-10yr buckets unchanged.

Top Asian News

China Central Bank to Pause Further Monetary Policy Easing: Rtrs

China Huarong Is Said to Buy BEA’s Tewoo Debt at 80% Discount

Hong Kong Sees Record 105 Local Cases in ‘Most Severe Moment’

European equities have started the session off on the backfoot (Eurostoxx 50 -0.8%) following a mixed handover from the US and Asia with action exacerbated on increasing US-China tensions regarding the Houston consulate in EU hours. From a European perspective, little has fundamentally changed since yesterday’s close amid the fallout from the agreement in Brussels other than some rumblings from Parliamentary groups in the EU that do not accept the Multiannual Financial Framework as its stands; ahead of tomorrow’s plenary session to assess the Council conclusions. In terms of sectoral performance, auto names are lagging their peers after a solid session yesterday with Valeo (-9%) acting as a weight on the sector after its H1 update. Energy names are also seen lower this morning with WTI and Brent front-month futures having dipped below 41.50/bbl and 44/bbl respectively. For stocks specific developments, Kingfisher (+11.4%) sit at the top of the Stoxx 600 with the Co. anticipating HY adj. pretax profit to be above Prev. due to strong Q2 sales and cost reductions. Elsewhere, other gainers include Fresnillo (+9.1%) despite cutting gold production guidance as investors appear satisfied with the accompanying beat on silver production. ABB (+2.3%) are also seen higher after the Co. beat on both top and bottom lines, whilst to the downside Melrose (-17.5%) are a laggard in Europe after announcing a 27% decline in H1 revenues.

Top European News

Fiat-Peugeot Deal Faces Delay as EU Stops Clock on Review

Bailey Hires First Woman for BOE’s ‘Unofficial Governor’ Role

Twitter Alerts Irish Privacy Regulator About Hacker Attack

In FX, the Dollar has bounced broadly on risk-off positioning and some profit taking after sustaining more heavy losses vs rival currencies, as US-China tensions ratchet up further over the closure of the Chinese Consulate in Houston by US ‘request’. In response, China’s Foreign Ministry has issued a warning about retaliation if the outrageous edict is not reversed and Usd/Cnh has rebounded firmly from circa 6.9640 to around 7.0160 awaiting further developments. Meanwhile, the DXY has pared more losses following another skirmish with 95.000, at 95.061 vs 95.043 at one stage on Tuesday to trade at 95.419 amidst a deeper pull-back in high beta/cyclicals that have gleaned most at the Greenback’s expense.

GBP – Sterling never really took advantage of the aforementioned Dollar drubbing, with Cable only extending advances beyond the 200 DMA (around 1.2705) to 1.2740 at best before reports emerged in the UK press suggesting that the Government is resigned to life post-Brexit transition period without an EU trade deal. The Pound has subsequently given up 1.2700+ status and Eur/Gbp is testing 0.9100 from a few pips off 0.9000 only yesterday.

CHF/AUD/NZD/EUR/CAD/JPY – All conceding ground to the recovering Buck, but not much in the grand scheme, as the Franc flits between 0.9314-37, Aussie remains above 0.7100 and not far from Fib resistance that was breached on the way up towards 0.7167 and Kiwi pivots 0.6650. Elsewhere, the Euro ran into reported fund supply at 1.1550, but is holding above 1.1500 after Tuesday’s big figure break despite potentially damaging news on the EU Budget as main EP groups back a motion of non-acceptance of the deplorable deal. Separately, Eur/Usd may be deriving a degree of underlying support from decent 1.27 bn option expiry interest at the round number. The Loonie is straddling 1.3450 in the run up to Canadian CPI and the Yen has drifted down to 107.00 or so following a break above that faded just ahead of near double top resistance at 106.67-65.

SCANDI/EM – The latest strains in relations between Washington and Beijing and associated aversion has undermined the Sek and Nok especially as oil prices recoil, but EMs are also suffering due to their more risk sensitive nature. Nevertheless, the Rand is still deriving some traction from Gold reaching fresh multi-year peak and only appearing to wane beyond Usd 1850/oz amidst speculation about hedging from bullion producers.

In commodities, WTI and Brent futures have, alongside broader market performance, experienced risk-off moves this morning. At present, the session low for WTI Sep’20 stands just above the USD 41/bbl mark and almost USD 1/bbl lower on the day. The downside stemmed from an escalation in reports relating to the US asking China to close their Houston consulate, which has been confirmed by both sides and seen China threaten to take retaliatory action unless this demand is rectified. For the complex itself newsflow has once again been very quiet, as a reminder the private inventory report last night showed an unexpected build of 7.54mln compared to consensus for a draw of 2mln going into the release, a release which placed the crude benchmarks under pressure. Attention now turns to the EIA report later today for confirmation of such a build in stocks; currently, the EIA report is expected to show a crude draw of 2.088mln which would be smaller than last week’s 7.5mln draw and in contrast to last night private inventory build. Turning to metals, where price action for spot gold has been comparatively quieter in the context of APAC price action. Overnight, the yellow metal extended on gains above the USD 1850/oz mark to a high of USD 1866.44/oz; price action which seemingly followed similar upward action in silver. In terms of a catalyst, no one driver has been attributed to the move but desks note COVID-19 reports alongside Fed nominee Shelton, a gold standard supporter, advancing at the Senate Banking Committee amongst factors. For reference, the next level to watch out for is USD 1885.72/oz which is the high from September 9th 2011 and the ATH at USD 1921.17/oz.

US Event Calendar

7am: MBA Mortgage Applications, prior 5.1%

9am: FHFA House Price Index MoM, est. 0.3%, prior 0.2%

10am: Existing Home Sales, est. 4.75m, prior 3.91m; Existing Home Sales MoM, est. 21.36%, prior -9.7%

DB’s Jim Reid concludes the overnight wrap

The best thing about working I can find other than to pay the mortgage and constant renovation bills is that I didn’t have to go to Peppa Pig world yesterday with my family. It was chaos apparently. However this trip may have pushed back retirement plans even further as they came back with more Peppa Pig merchandise than Hamleys stock at Xmas.

Christmas came early yesterday in markets with numerous asset classes reaching their strongest levels since financial markets reacted to the global spread of the pandemic back in March. Having said that, US stocks came off their highs on stimulus doubts in the last hour of trading. Nevertheless the S&P 500 advanced by +0.17% to reach its highest level since 21st February, which was the Friday before the weekend when Italian cases surged into triple digits and sent markets into a tailspin. The rise in the S&P was led by Energy (+6.15%) and Banks (+3.55%) as the growth over value trade had a rare reversal. In fact, Energy stocks led the rally on both sides of the Atlantic (+2.37% for STOXX 600 Oil and Gas sector) against the backdrop of a surge in oil prices with Brent crude (+2.40%) and WTI (+2.82%) both climbing to their highest levels since early March. Tech underperformed with the NASDAQ falling -0.81%.

In a further sign of normalisation though, Bloomberg’s index of US financial conditions closed in positive territory for the first time since the pandemic began or more specifically 26 February (meaning financial conditions are marginally more accommodative now than at their pre-GFC average from 1994 to July 2008). Over in Europe, equities earlier also gave up some of their gains towards the end of the session with the STOXX 600 (+0.32%) similarly reaching a post-pandemic high. At one point in trading the DAX (+2.04% at the highs) actually ventured into positive territory on a YTD basis, before ending the session up +0.96%.

The corollary of this risk-on move was a broad dollar breakdown, with the dollar index down by -0.75% to its lowest level in over 4 months, having weakened for 7 of the last 8 sessions now. The move saw the euro rise to $1.153, finally breaching the $1.145 high back in March that means the single currency is now at its strongest level against the dollar since January 2019. As a reminder, our FX strategists see the euro heading up to $1.20 by year-end, partly supported by an expected divergence in the Europe data relative to that in the US as the resurgence in cases knocks confidence.

Speaking of the US, Republican leaders in Congress and the White House met to finish off the party’s opening bid to House Democrats for the latest round of stimulus. Treasury Secretary Mnuchin and White House Chief of Staff Meadows seem to agree that an additional round of stimulus checks directly to individuals, a more tailored extension of supplemental unemployment benefits, and additional funding for covid-19 testing would all be included. However, the party still sees some dissent for the payroll tax cut that the President has advocated for. Congress has already approved $2.9tr in fiscal stimulus this year, and now Republicans are trying to keep the current bill to another $1tr vs the House passed bill for $3.5tr. The timeline is getting tight for Congress as much of the original stimulus is set to expire within the next few weeks but with US lawmakers on recess in the second week of August. Late in the session, it was reported that Senate Majority leader McConnell does not expect stimulus to get done in two weeks as the White House had wanted. Overnight, Bloomberg has reported that Senate Republicans are considering whether to cut the unemployment insurance subsidy to 70% of the $600 weekly addition to state-run unemployment programs provided by the last round of economic aid, or pushing for 70-75% of prior wage replacement, a smaller benefit. Final details on this are likely to be out today.

Staying with the US Congress, the Senate Banking Committee heard a pair of Fed confirmation votes. Judy Shelton has been a contentious pick by President Trump for the Federal Reserve’s Board of Governors, but yesterday she won confirmation by a party-line vote, 13-12, of the Senate Banking Committee. Shelton has drawn criticism in the past for being an informal adviser to the Trump campaign in 2016, which might affect the image of her independence. She has also held more unorthodox monetary policy views including a return of the US to the gold standard and questioning a need for a central bank controlled benchmark rate. With far less contention, Christopher Waller, who is currently the director of research at the St. Louis Fed passed 18-7 through his own confirmation vote. Both Shelton and Waller will now be voted on by the entire Senate in order to join the Fed Board. Senate Majority leader McConnell will likely only bring votes to the floor once he knows he has at least 50 votes and so it will be notable if the chamber votes on Waller, clearly the far less controversial candidate, well ahead of Shelton.

In terms of the latest on the coronavirus, California has overtaken New York overnight to become the most infected state in the US in terms of total infections since the start of the pandemic as it reported 14,369 new cases (vs. 7-day average of 8790) or a 3.6% daily rise (vs. 7-day average of 2.5%). California’s total infections now stand at 409,305 versus 408,181 in New York. Governor Newsom noted that California is likely to have adequate hospital capacity, with Covid-19 patients occupying just 17% of available beds across the state. In Florida, cumulative hospitalizations rose 2.4%, to 21,780, while the daily increase of 517 is the most on record. Cases rose by just over 9400 (vs. 7-day average of 11,172) yesterday in the state or 2.6% (vs. 7-day average of 3.5%), but Tuesday has routinely been lower than the rest of the week and so should be taken with a degree of caution. According to the Texas Medical Center, the number of covid-19 patients in Houston-area hospitals, which at one point were using surge beds to deal with the overflow of patients, should decline for at least the next two weeks, given recent admission stats. New York continues to add to its “Quarantine list”, with 10 new states including Alaska, Delaware, Indiana, Maryland, Missouri, Montana, North Dakota, Nebraska, Virginia and Washington, but Minnesota has been removed. Meanwhile, President Donald Trump has rebooted his coronavirus briefings and warned yesterday that the coronavirus crisis will probably worsen before improving.

There are also concerning reports from Asia, as both Hong Kong and Tokyo are seeing a rise in cases. Tokyo has seen more than 1,600 coronavirus cases in the past week with between 230 to 240 cases today, and Governor Yuriko Koike is considering urging residents to avoid unnecessary trips outdoors during an upcoming four-day weekend. Australia’s Victoria state also registered 484 new cases setting a nation record while State Premier Daniel Andrews said that the lockdown may be extended unless people comply with restrictions.

The Nikkei (-0.47%) and the ASX (-1.28%) are the notable underperformers this morning following the latest virus data, while in contrast the Hang Seng (+0.08%), Kospi (+0.11%) and most notably the Shanghai Comp (+1.20%) are all up. Futures on the S&P 500 are up +0.35% and in commodities spot silver and gold prices are up a further +4.93% and +0.72% respectively. In terms of data releases, Japan’s preliminary June manufacturing PMI came in at 42.6 (vs. 40.1 last month) while the service PMI printed at 45.2 (vs. 45.0 last month) bringing the composite reading to 43.9 (vs. 40.8 last month).

Over in Europe, we just caught the news in yesterday’s edition that EU leaders had agreed a final deal on the recovery fund, made up of €390bn in grants and €360bn in loans. Our European economists have now put out an in-depth note looking at the final deal (link here), where they argue that there are two key positives from a financial market point of view. The first is the precedent it sets as the EU’s first common counter-cyclical instrument. The second is that it has an optimal design in that it is large enough for the scale of the crisis, it is targeted at the most growth-enhancing opportunities, and it incentivises structural reforms.

In line with the broader risk-on move yesterday, the market reaction in Europe continued to be positive. 10yr yields on Italian (-1.1bps) debt over bunds narrowed to their lowest levels in over 4 months. Credit default risk also fell, with the iTraxx Europe falling by -1bp to its lowest level since late February, with the iTraxx Crossover (-3bps) at its lowest since early March. Nevertheless, inflation expectations fell back, in spite of reaching a 4-month high on an intraday basis with 5yr5yr inflation breakeven swaps for the Euro Area closing down -1.2bps at 1.12%.

Aside from the dollar, a number of safe havens actually recorded a strong performance, with the precious metal rally we mentioned yesterday gathering further steam. By the close, gold had risen a further +1.33% to a fresh 8-year high of $1842, while silver surged by +7.01% to surpass its 2016 peak and reach a 6-year high. The +21.39% advance for gold since the start of the year makes it one of the few major assets to have seen big positive returns in 2020 so far. US Treasuries also advanced, with 10yr yields down -1.0bps to 0.60%.

It was another day of fairly light data releases, though from the US we did get the Chicago Fed’s national activity index which saw a rise to 4.11 in June (vs. 4.00 expected). Elsewhere, Canadian retail sales rose by +18.7% in May (vs. +20.0% expected), and the UK’s main measure of public borrowing rose to £35.5bn in June (vs. £38.0bn expected), a move which took the debt-to-GDP ratio to 99.6%, the highest since the financial year ending March 1961. While we’re on the UK public finances, it’s worth noting that Chancellor Sunak launched the Comprehensive Spending Review for 2020 yesterday, which will be published in the autumn. Notably it warned of “tough choices” that lie ahead given the economic impact of the pandemic. Overnight, the British Chambers of Commerce has said in a report that Sunak should reduce social security contributions by GBP500 per employee as it will help to “protect businesses and preserve jobs.”

To the day ahead now, and the data highlights include the US existing home sales for June, the FHFA house price index for May, along with Canada’s June CPI reading. From central banks, we’ll hear from ECB President Lagarde and Vice President de Guindos. Finally, earnings out include Microsoft, Thermo Fisher Scientific and Tesla.

via ZeroHedge News https://ift.tt/2CSFiPM Tyler Durden

US Strikes $2 Billion Deal To Buy COVID-19 Vaccine From Pfizer Tyler Durden

Wed, 07/22/2020 – 07:35

In the latest deal involving a (clearly anxious) government and a (clearly greedy) pharmaceutical giant peddling an as-yet-unfinished remedy or vaccine, the US Department of Health and Human Services and the DoD have announced a deal with Pfizer to buy 100 million doses of a vaccine candidate – once it has been tested and approved and all that.

We received the latest update from German biotech firm BioNTech and US-based Pfizer, who are jointly developing a vaccine, earlier this week. They released the results of an early-stage trial purporting to establish that the vaccine is safe for human consumption. The virus remains on track to begin anticipated Phase 2B/3 safety and efficacy trial later in July. The US government has pledged $1.95 billion for an initial order of 100 million doses of the vaccine.

The deal also includes an option for the government to purchase an additional 500 million doses, contingent on the drug being granted regulatory approval.

The US government said it aims to make the vaccine free to all Americans.

We expect to learn more about the “arrangement” when DHHS Secretary Alex Azar joins the “Squawk Box” crew for an interview in an hour.

As the FT reminds us, several governments have signed agreements with some of the 24 groups currently testing a coronavirus vaccine on humans, including the candidate being developed by Oxford University in partnership with AstraZeneca.

Here’s more on the history of governments striking vaccine deals. In the UK, HMG was aiming to strike deals to distribute each of the four main vaccine technologies being explored. These include: genetic vaccines, viral vectors, inactivated whole virus and protein-based vaccines.

The US move comes after the UK government ordered 30m doses of BioNTech’s vaccine and 60m doses of another vaccine from Valneva of France, which is less advanced in clinical development. But it did not disclose financial details of the agreements. Kate Bingham, head of UK government’s vaccines task force, said the country was aiming for a total of at least eight deals — two for each of the four main vaccine technologies (genetic vaccines, viral vectors, inactivated whole virus and protein-based vaccines). “We initially talked to the government about going up to 12 vaccines but it’s more likely to around eight, at least initially,” said Ms Bingham. “That would give us a broad and diverse portfolio.” Ugur Sahin, co-founder and chief executive of BioNTech, said: “We are also in advanced discussions with multiple other government bodies and we hope to announce additional supply agreements soon.” BioNTech said it had also expressed an interest in supplying the COVAX programme, which aims to enable equitable access to a vaccine. It is run by Gavi, the Coalition for Epidemic Preparedness Innovations (Cepi), and the World Health Organization. The Mainz-based company is one of several using messenger RNA (mRNA) technology to develop a Covid-19 vaccine — a process that is faster than traditional methods. However, there is as yet no certified mRNA product on the market.

Though most other details haven’t revealed the price per dose. The White House’s “Operation Warp Speed” aims to deliver 300 million doses of a certified vaccine by January. The program has already spent more than $2 billion on investments in vaccines being developed by Moderna and JNJ.

via ZeroHedge News https://ift.tt/2ZQHTmw Tyler Durden

Apparently, the incident occurred just as the US was ordering the abrupt closure of China’s consulate in Houston, citing a need to protect American intellectual property and data. The decision, which rattled global equity markets, has been decried as a dramatic escalation in bilateral tensions as Beijing condemned the order as an outrageous violation of international law. Spokespeople for the Chinese government also slammed the decision as outrageous and unprecedented.

Washington’s order, which according to WSJ was issued just yesterday, marks an “unprecedented escalation” and “a political provocation unilaterally launched by the US,” according to Chinese Foreign Ministry spokesman Wang Wenbin, who addressed the issue during his regular press briefing in Beijing.

“China urges the US to immediately rescind its erroneous decision, otherwise China will undertake legitimate and necessary responses.”

Reuters is now reporting that China is considering closing the US consulate in Wuhan in retaliation. Though we suspect those diplomats wouldn’t mind being stationed elsewhere.

Even Hu Xijin, the typically long-winded editor of the Global Times, could only manage a surprisingly brief “that’s crazy”.

The US asked China to close Consulate General in Houston in 72 hours. This is a crazy move.

State Department Spokeswoman Morgan Ortagus didn’t specify which specific actions, if any, inspired Washington’s decision, though she did say: “President Trump insists on fairness and reciprocity in U.S.-China relations.”

“The United States will not tolerate the PRC’s violations of our sovereignty and intimidation of our people, just as we have not tolerated the PRC’s unfair trade practices, theft of American jobs and other egregious behavior.”

So far, details from official sources are scant. However, it’s probably worth remembering the scene from yesterday’s ‘document fire’ incident: the Houston police and fire departments responded Tuesday night to a reported document fire at the Chinese Consulate. Footage taken from the building next door shows what appears to be barrels with burning material inside of them.

Seems like a totally normal and non-suspicious reaction to a closure order.

Stocks slumped during the Asian trading session; the offshore yuan also slumped against the greenback.

The Foreign Ministry spokesman continued to hammer the US, saying China has always treated American diplomats ‘with respect’ (including monitoring their every move), while this isn’t the first incident involving China’s diplomatic personnel in the US.

“In contrast, the US put restrictions on Chinese diplomats in June and last October, respectively, with no valid reason. [The US] has seized and opened mail and official supplies,” Wang said.

Back in December, Washington quietly expelled two Chinese diplomats suspected of espionage after they were caught driving to a sensitive military base in Virginia. But Chinese foreign ministry spokesman Geng Shuang rejected the claims when asked about them by reporters.

China’s diplomats are widely regarded members of Chinese society, probably holding a higher status than American diplomats hold. State-controlled media has praised China’s diplomats as “Wolf Warriors”. Read more about that here.

The HPD said it began receiving reports just after 2000 local time warning about documents being burned at 3417 Montrose Boulevard, where the consulate is located.

The consulate holds a special significance. According to information available online, the consulate “was the first one to be established” in 1979 when the US and China official re-established diplomatic relations. The consulate’s district covers eight southern US states, namely Texas, Oklahoma, Louisiana, Arkansas, Mississippi, Alabama, Georgia, Florida and an unincorporated territory, the Commonwealth of Puerto Rico.

via ZeroHedge News https://ift.tt/32HKJfl Tyler Durden

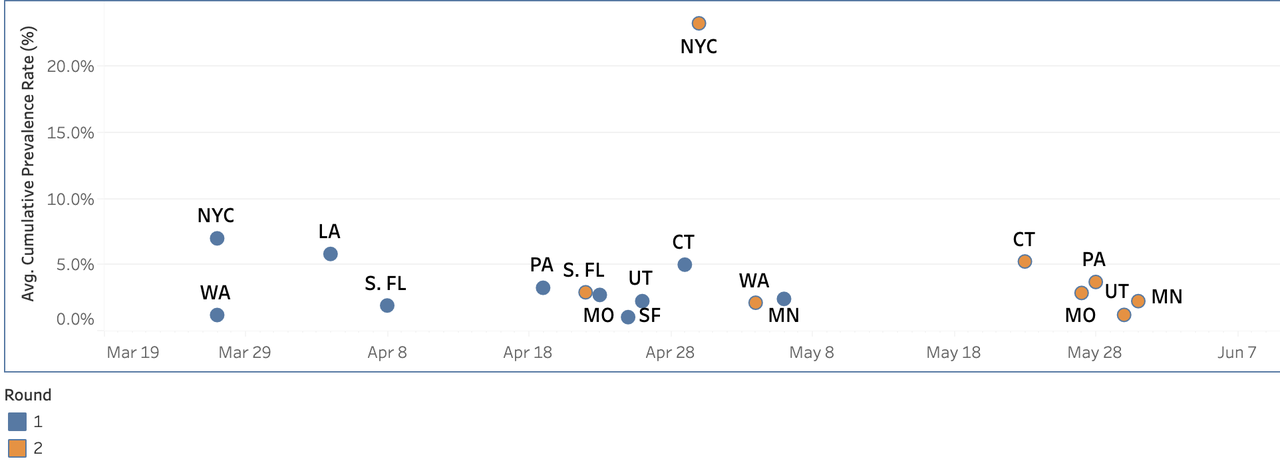

Coronavirus Infections 13x Higher Than Reported In Some Parts Of US Tyler Durden

Wed, 07/22/2020 – 06:30

As scientists get a better grasp on the coronavirus and how it has spread across the US, a new survey from the CDC purports to show that the true number of coronavirus cases is between 2x and 13x the official count, varying from state to state,

Data released by the CDC suggest that large numbers of asymptomatic people may have kept the virus spreading in their communities, directly contradicting the findings of another study cited by the WHO last month.

Following a similar finding by scientists in Sweden,the researchers working with the CDC found that even the hardest-hit area in the study – ie NYC, where 1 in 4 people have been exposed according to antibody surveillance studies – isn’t anywhere near achieve herd immunity, which scientists believe will require 60% infection rate.

If these seroprevalence rates are accurate, then Missouri is suffering from an outbreak that is 13x its reported rate.

The analysis, based on antibody tests, is the largest of its kind to date, and the full breakdown has been released after some surveillance numbers focusing on limited areas were released last month.

Media orgs like the FT, NYT and Washington Post started trying to gauge the number of unconfirmed cases and deaths by calculating the “excess fatality” rate, measure the average deaths during equivalent time periods from the past 5 years vs. the numbers from this year.

On the other hand, the data illustrate how large swaths of the US remain relatively untouched by the virus. Parts of Utah have just over 1% exposure rates, while Minneapolis-St. Paul’s rate is 2.2%.

Nearly 40% of infected people reportedly never develop symptoms, but they can still pass the virus along (though the exact risk factors here are still under investigation) The US now tests roughly 700,000 people a day, per the NYT.

“These data continue to show that the number of people who have been infected with the virus that causes Covid-19 far exceeds the number of reported cases,” said Dr. Fiona Havers, the C.D.C. researcher who led the study. “Many of these people likely had no symptoms or mild illness and may have had no idea that they were infected.”

Dr. Havers emphasized that even those who do not know their infection status should wear cloth face coverings, practice social distancing and wash their hands frequently.

In some areas, like NYC, the gap between the true number of cases (according to CDC estimates) and the number confirmed improved as testing capacity expanded.

In some regions, the gap between estimated infections and reported cases decreased as testing capacity and reporting improved. New York City, for example, showed a 12-fold difference between actual infections and the reported rate in early April, and a 10-fold difference in early May.

“This is not coming as a shock or surprise to epidemiologists,” Carl Bergstrom, an infectious diseases expert at the University of Washington in Seattle, said in an email. “All along, we have expected that only about 10 percent of the cases will be reported.”

Tracking the numbers over time can provide useful insights into the virus’ spread and about a region’s capacity to cope with the epidemic, other experts said.

“The fact that they’re sort of marking it out over time and looking at it over a longer duration will actually be super-informative,” said Dr. Rochelle Walensky, a researcher at Harvard University who wrote an editorial accompanying the JAMA paper.

Like most studies, the CDC data aren’t perfect. For example, critics have warned that samples analyzed by the researchers might overrepresent the presence of COVID since only the most ill people, who might not be representative of the general population.

via ZeroHedge News https://ift.tt/30zfC2R Tyler Durden

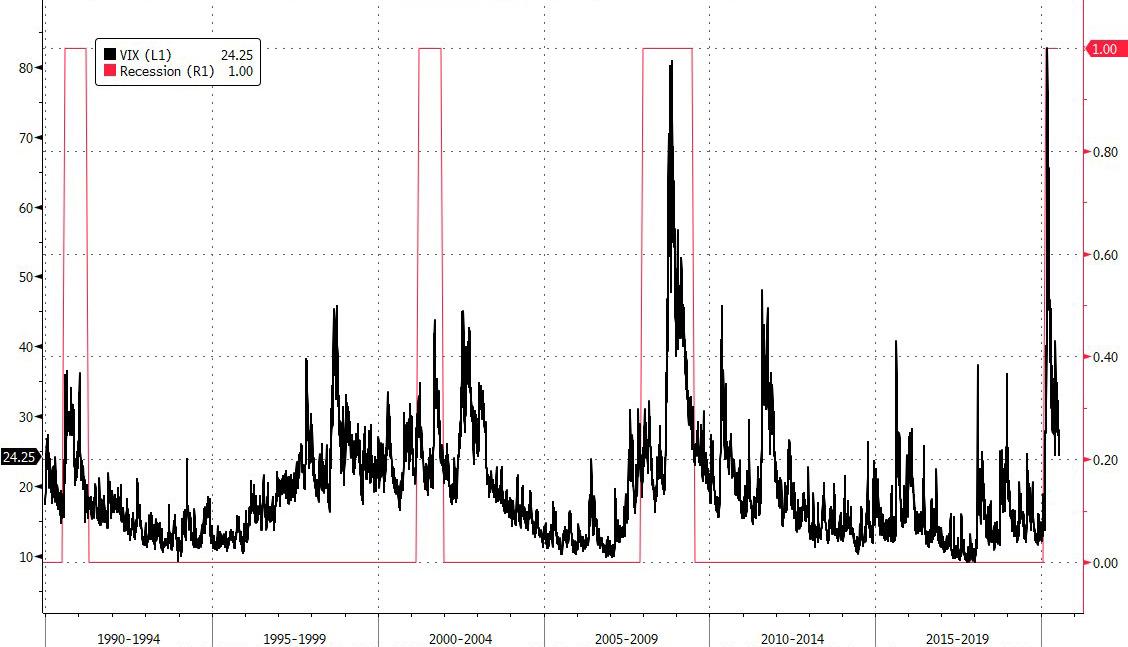

There is growing concern that US stocks are replaying the tech-driven bubble phase of the late 1990s. Today’s S&P rally fits that narrative. The CBOE VIX Index will tell us if it will be our fate to live through 1999 again. Back then, the VIX generally held above 20. In every other sustained rally back to 1990, it went below 20 and generally stayed there for years.

Just one “Markets” topic today: the CBOE VIX Index. The mathematical mechanics of the VIX are grimy, of course. To the letter of the law, it is the implied volatility priced into short term options on S&P futures contracts. Metaphysically, the VIX is the one variable in the Black-Scholes pricing model you can’t measure elsewhere but rather the number that falls out of the equation once you plug in asset and strike prices, interest rates and time to expiration.

But the world simply knows it as the Fear Index… When the VIX is rising quickly you can be sure stock prices are likewise falling. And when the VIX is heading lower after a spike, you know the S&P is recovering from a recent drop.

And that’s where we find ourselves today: the VIX declined to 24.46 and the S&P rallied to 3,252, respectively a post-COVID Crisis fresh low and high. And if one looks at the VIX’s long run distribution of observations, there would seem to be reason to think the rally can continue:

The average of all CBOE VIX closes back to its start in 1990 is 19.4.

The standard deviation of the VIX over that time is 8.1 points.

At today’s 24.46 VIX level we’re well within 1 standard deviation (27.5 being the upper band), indicating that the options market thinks we are not set up for another bout of market volatility in the near future.

As comforting as that message may be, we need to acknowledge that Monday’s breakout in the S&P and correlated break down in the VIX was entirely due to the Tech sector plus Facebook/Google (Communication Services) and Amazon (Consumer Discretionary). No other industry groups were in the green. US mid-caps and small-caps also ended the day lower.

There was, of course, another period in market history with similar fundamentals, so let’s look at the VIX across multiple cycles to see what we can learn. The chart below shows monthly VIX data back to 1990, with the January 2000 VIX level highlighted as a way to focus our attention on this potentially analogous historical period.

In this 30 years of VIX history we see 3 things that are relevant to understanding today’s US equity market:

Put aside the idea that US equities can only rally in a sleepy, grinding way once a crisis has passed. This is the most common pattern, to be sure; look at how the VIX chart makes a smile shape through every market cycle. But it isn’t the only way stocks rally…

Instead, focus on what happened from 1997 – 2000; that’s why we highlighted January 2000’s 24.95 average level. This was a relatively unusual period of market history, with higher than average VIX readings (reliably above 20) pairing up with stellar S&P 500 returns (1997 +33.1%, 1998 +28.3%, 1999 +20.9%).

Consider how similar the setup in 2020 is to the 1997 – 2000 time period, except that now a handful of very profitable Big Tech companies dominate important verticals and provide market leadership rather than the free-for-all that drove stock prices higher during the late 1990s dot com bubble.

We totally understand why this is not necessarily a welcomed interpretation of current market psychology. It does, however, fit the facts and it certainly describes the S&P’s break out on Monday anchored purely on Big Tech’s strength. There have been 10 turns of Moore’s Law since the year 2000, but those in conjunction with the disruption wrought by COVID-19 may finally be delivering the tech-driven world many imagined in 1999.

The good news is that the VIX will tell us if we’re in another speculative bubble, because if that’s the hand we have to play we will see the Fear index stay mostly above 20. This won’t be a sell signal, just as it wasn’t in 1997. But it will be a sign that we’re in a different sort of market from the ones we usually see after a crisis.

via ZeroHedge News https://ift.tt/3fWPYf2 Tyler Durden

Global Pop Star Dua Lipa ‘Cancelled’ Over Tribute To Albanian Nationalism Tyler Durden

Wed, 07/22/2020 – 05:30

As celebrities continue to grapple with the explosion of SJW culture into the mainstream – all of a sudden, wealthy white celebrities are talking about ‘colonizers’ and the ‘erasure’ of indigenous cultures – their awkward embrace of international struggle against oppression has led to a handful of accidental controversies.

On Tuesday, the BBC reported on a ‘scandal’ involving British-Albanian pop singer Dua Lipa. Lipa, who occasionally tweets about her Albanian ‘heritage’, shared a map of ‘Greater Albania’ – an ultra-nationalist vision of a new Albanian state encompassing territory belonging to Albania’s neighbors that is occupied by mostly ethnic Albanians. Kosovo is perhaps the most glaring example. Having declared independence from Serbia in 2008, Serbia, Russia and their geopolitical allies still refuse to recognize Kosovo as an independent state.

au•toch•tho•nous adjective

(of an inhabitant of a place) indigenous rather than descended from migrants or colonists pic.twitter.com/OD9bNmLcZ4

Lipa’s tweet included a definition of the word “autochthonous” – pronounced ah-tak-then-us – not exactly a common component of the popular lexicon. Its essentially a fancy synonym for “indigenous”.

Albanians believe their claim to the land in and around Albania dates back centuries to long before the Serbs arrived in the region.

According to the BBC, Lipa was accused of supporting Albanian expansionism after posting the map which forms part of hard-line nationalist dreams of creating a Greater Albania encompassing all ethnic Albanians. Taken a certain way, one could argue that this nationalist ‘dream’ is vaguely reminiscent of Hitler’s justification for invading Poland and the Sudetenland – that German-speaking peoples were in danger.

Some on twitter accused Lipa of being a “fascist” and even trotted out the hashtag #CancelDuaLipa. However, considering that most Americans probably don’t even know what Kosovo is (older Americans might remember the NATO bombing campaign, but that’s about it), we doubt Ms. Lipa will experience any lasting financial backlash over the controversy. We wouldn’t be surprised to learn that her ‘critics’ are pro-Serbian bots.

Lipa’s parents are from Kosovo, but she was born in London after they moved to the UK. She pursued a successful modeling career in her teens and went on to achieve pop superstardom with a series of hit singles over the past few years. She is currently dating Anwar Hadid, the brother of model sisters Bella and Gigi.

via ZeroHedge News https://ift.tt/3hqfRnw Tyler Durden