The debate over the Montana Department of Public Health and Human Services’ plan to permanently ban the sale and marketing of all flavored e-cigarettes has focused on two entrenched viewpoints. Supporters argue that these vaping products can lure teens into a lifetime of nicotine addiction, while opponents argue that a ban will harm small businesses and the economy.

The public debated these views last week at a two-hour hearing in Helena. Unfortunately, there’s too little discussion—and no acknowledgment from state health officials—about the ill health effects of banning these products. Quite simply, large numbers of smokers have switched from dangerous combustible cigarettes to far-less dangerous e-cigarettes. Britain’s top health agency notes that vaping is 95 percent safer than smoking.

Banning flavored vape products is essentially a ban on all vape products, given that virtually all e-cigarette liquids contain some kind of flavoring. Even tobacco flavors, which many vape users eschew as they distance themselves from their past cigarette habit, are an additive to vaping liquids. The debate over flavored vapes really is a debate about whether adult smokers will still have access to products that could save their lives.

“While it’s addiction to nicotine that keeps people smoking, it’s primarily the combustion, which releases thousands of harmful constituents into the body at dangerous levels, that kills people,” notes former Food and Drug Administration Commissioner Scott Gottlieb. He argues that e-cigarettes offer smokers a chance to transition to “nicotine delivery products that may not have the same level of risks associated with them.”

Teen vaping certainly is a problem, but it’s nonsensical to use that concern to outlaw products that already may only legally be sold to adults. Vaping, according to a health department statement, “is causing major health consequences for our youth driving a lifelong addiction to nicotine.”

That’s true, but the answer, just as it is for underage alcohol consumption or other already-illegal behavior, is for state officials to enforce existing prohibitions. A sensible society reserves some activities for adults only—and simply enforces age limits and other restrictions.

Ironically, Gov. Steve Bullock’s imposed a “temporary” ban on flavored vaping following a nationwide health scare—debilitating lung diseases that were reportedly the result of vaping. In the ensuing months, the Centers for Disease Control discovered that black-market and cannabis-containing vaping products—not commercially available nicotine-based ones—were almost entirely the source of the illnesses.

The problem centered on illicit products. There’s an important lesson to be learned here. If states ban commercial vaping products, vapers will be more apt to buy them on the black market or, as some news reports have shown, make their own liquids based on online recipes. A flavored e-cigarette ban could thereby increase the dangers to teens and adults who choose that risky path of DIY flavors.

There are other problems with this proposal, as well. Elected lawmakers, not bureaucratic officials, should make decisions of this magnitude. Indeed, the Legislature’s Economic Affairs Interim Committee on July 2 sent a letter to the health department’s director, Sheila Hogan, arguing that the department lacks the statutory authority to impose a ban.

As retailers noted during the hearing, they face serious economic consequences from the proposal. “The Vapor Technology Association found that in 2018 the vapor industry created 554 jobs and $67 million in economic output for Montana and $2.6 million in state and local taxes,” according to a recent Great Falls Tribune report.

Nevertheless, the main overlooked argument centers on public health—and how a ban is a step in the wrong direction. Any proposal designed to battle tobacco-related health diseases ought not to harm people who are choosing a less-dangerous course. Montana health officials need to take such concerns more seriously before they implement this proposed rule.

from Latest – Reason.com https://ift.tt/2D5CsHB

via IFTTT

There are clues in this morning’s financial news about where this goes next.

The headlines are about the stunning success of the Big Four Tech giants – beating expectations and proving themselves largely impervious to the Cornonavirus.

Stand that against the news the US Economy showed a notional 32.9% annualised GDP decline through Q2 – its worst performance since 1947. As virus hotspots erupt around the globe, we’ve got Trump tweeting about cancelling the election – which he actually can’t do. And buried deep in the back pages is news of the coming crisis; proof the whole system is in deep trouble as the UK’s University Superannuation Scheme (“USS”) faces the consequences of QE Infinity.

Back in February, I put down Apple as one of the likely strong stocks most able to survive the coronavirus crisis – arguing an iPhone sale lost in March would simply be a purchase delayed. I was wrong. Apple’s revenues increased 11% as it sold more Macs, iPads and selling phones right through – especially its cheaper ones in China – boosting sales by 35% at a time when competitors like Samsung saw sales decline 14%. What’s happening? I need to go speak to marketing experts, but it looks like firms with a clear domination of their space are getting a boost as consumer behaviour shifts and they make deliberate decisions to prioritise quality over price.

A second factor is the Advertising Industry – lots of firms deliberately cut advertising spending early in the crisis. It’s a decision they probably regret – smart companies went out and spent more to boost their profile. That’s reflected in the increased revenue at Facebook – where the “boycott” by leading firms failed to dent the firm. Facebook saw revenues grow 11%!

Amazon was barely troubled by the crisis protocols – the number of smiley face boxes bearing the logo piled up in the globes litter bins. I suppose there must have been a collapse in waste carboard prices as a result. It may be second place in the cloud computing battle to Microsoft – but Amazon hiking revenues to near $90 bln is pretty impressive.

In contrast – rising unemployment, smaller companies facing the end of support and solvency catastrophe, plus the ongoing virus outbreaks, confirms the global economy is increasingly divided into good and bad. Talking to clients over the past week, it’s become clear no one really believes there will be a solid cross-economy recovery – a common v-shape. You need to look sector by sector, stock by stock to understand the winners and losers, but that’s being made obscure by the effects of the QE Infinity and Zero Interest Rate Policy.

When Fed-head Jay Powell earlier this week said it’s all about the virus, he was being disingenuous. It’s about winners and losers – and the Fed looking the other way as it pretends it not…

There are seriously large icebergs out there.. and I can’t help thinking pushing the QE Infinity engine all the way up to 11 is dangerous…

I’ve been arguing since 2008 that government interventions, regulatory overkill, QE Infinity and ZIPR will have massive and painful consequences. When it comes down to financial assets – liquid listed stocks and bonds, the result is now clearly visible financial asset stagflation: financial assets cost much more and return far less. That’s the way prices work. A stock that cost $1 dollar in 2010 and made $1 in profit costs $10 today, but still makes $1 in profit. A bond that yield (or is it yielded?) 10% in 2010 makes 0.8% today.

University staff in the UK are furious. They are threatening to strike because their gold-plated final salary schemes are at risk. The USS faces a £20 bln funding gap – which will require universities and staff to significantly increase contributions to maintain its pension provision. It’s not just the effect of Financial Asset Stagflation on the final salary scheme that’s causing the crisis – people are living longer, shifting the actuarial goalposts even as the returns plummet.

The brutal reality is that ZIRP and QEI have a voracious appetite for more. As long as markets are distorted, they will consume all the salaries and contributions of the university sector, and there will still be an unfillable hole at the centre of the pension scheme. Consequences.. consequences.

It’s not just the Universities. This is going to happen to every occupational pension scheme. In the case of the USS, we’ve already seen the richer universities pull out – apparently unwilling to share risk. It won’t help the UK’s university sector faces a double whammy from the virus and declining student numbers.

Who can afford the costs of final salary pension schemes in today’s Zero-return market? The maths simply don’t work. Yet, as angry Academics are demonstrating, no-one holding a FSP is willing to give it up. Of course they aren’t – those of us outside defined benefit schemes, and saved our own pension pots face the same problem.. without the benefit of being able to go on strike at the injustice of it all.

It’s going to get worse. I sometimes wonder if whole UK Government might just be a Ponzi Pension Scheme that’s going to bankrupt us all. Within a few years the UK will be paying about 25% more in gold-plated pensions to government workers than it receives in tax revenues. Meaning, those of us saving for our own pensions will be taxed more to pay theirs. While I understand the need to ensure the retirement of our brave front line medical and service personnel, I’m struggling to feel much sympathy for bureaucrats.

And that, dear readers, is why the Blain yacht is well stocked, seaworthy and able to flee these shores when the revolution erupts led by angry Torygraph and Guardian readers..

via ZeroHedge News https://ift.tt/3hV1c45 Tyler Durden

“It’s Shocking No Matter How You Look At It” – Futures Jump On Blockbuster Tech Earnings; Gold Hits New Record High Tyler Durden

Fri, 07/31/2020 – 08:10

S&P futures rose (but faded much of their earlier gains) alongside European shares with Nasdaq futures jumping nearly 1% as stellar earnings from US tech giants lifted sentiment amid dismal economic data and a resurgent virus. Gold climbed to a record even as the dollar rebounded from two year lows.

The Tech Tsunami helped lifted European shares, with the Stoxx Europe 600 Index rising, even after France and Spain posted record economic contractions. Nokia Oyj soared after earnings beat estimates, while BNP Paribas SA jumped on a blowout performance in fixed-income trading. Following the dismal US GDP print, the Euro Area reported that in Q2, its GDP contracted sharply by 12.1%qoq, in line with expectations, and corresponding to by far the sharpest decline in quarterly GDP growth since records began in 1995. French and Italian GDP both contracted by less than expected—by -13.8% and -12.4%, respectively—whereas Spanish GDP contracted most sharply (-18.5%) across the Euro area countries that have so far reported Q2 GDP. The unprecedented contractions in GDP were primarily attributable to weak domestic demand in both France and Spain, with a comparatively smaller drag from net trade as both exports and imports collapsed. The weakness was broad-based across sectors, with industry and services both registering record quarterly declines.

Asian stocks fell, led by industrials and energy, after falling in the last session. Most markets in the region were down, with Japan’s Topix Index dropping 2.8% and Australia’s S&P/ASX 200 falling 2%, while Shanghai Composite gained 0.7% on widespread retail buying as margin debt increased once again. The Topix declined 2.8%, with SoldOut and DTS falling the most. The Shanghai Composite Index rose 0.7%, with Xi’an Bright Laser and Anji Micro posting the biggest advances.

Apple surged 6% in premarket trading, setting the stock on course to open at a record high, as it delivered year-on-year revenue gains across every category and in every geography. Amazon.com also jumped 5.4% after posting the biggest profit in its 26-year history, while Facebook gained 6% as it reported better-than-expected revenue. Trading in Alphabet was more subdued as quarterly sales fell for the first time in its 16 years as a public company (for a response to tech earnings from some Wall Street analysts see here). Elsewhere, Ford rose 2.7% after signaling ample cash-on-hand for the year even as it forecast a full-year loss. Gilead Sciences fell 3.5% as it posted worse-than-expected quarterly results, hurt by weak sales of its hepatitis C drugs and flagship HIV treatments. Caterpillar Inc. gained after reporting higher-than-expected profit. Bucking the trend, U.S. oil giant Chevron Corp. posted its worst quarterly loss in at least three decades, sending the shares lower.

“It’s shocking no matter how you look at it,” said Randy Frederick, vice president of trading and derivatives for Schwab Center for Financial Research.

“The virus is getting worse in a lot of areas, and some places have started to shut back down again. If you look at earnings in terms of beat rates, the results have actually been pretty good, granted the expectations bar has been set very low.”

A surge in the stock price of the four companies, which make up nearly a fifth of the S&P 500’s value, as well as aggressive fiscal and monetary stimulus have sent the tech-heavy Nasdaq to record highs and set the S&P 500 on course for its fourth straight monthly gain. The S&P is now about 4% shy of its February all-time high, but faltering macroeconomic data and rising COVID-19 cases are making investors cautious again.

The GDP number on Thursday confirmed the sharpest contraction in the US economy since the Great Depression, while rising jobless weekly claims suggested a nascent recovery in the labor market was stalling. Investors betting on more U.S. government stimulus, before an extra $600-per-week federal jobless benefit expires on Friday, have also been disappointed as the Senate adjourned for the weekend and will return on Monday.

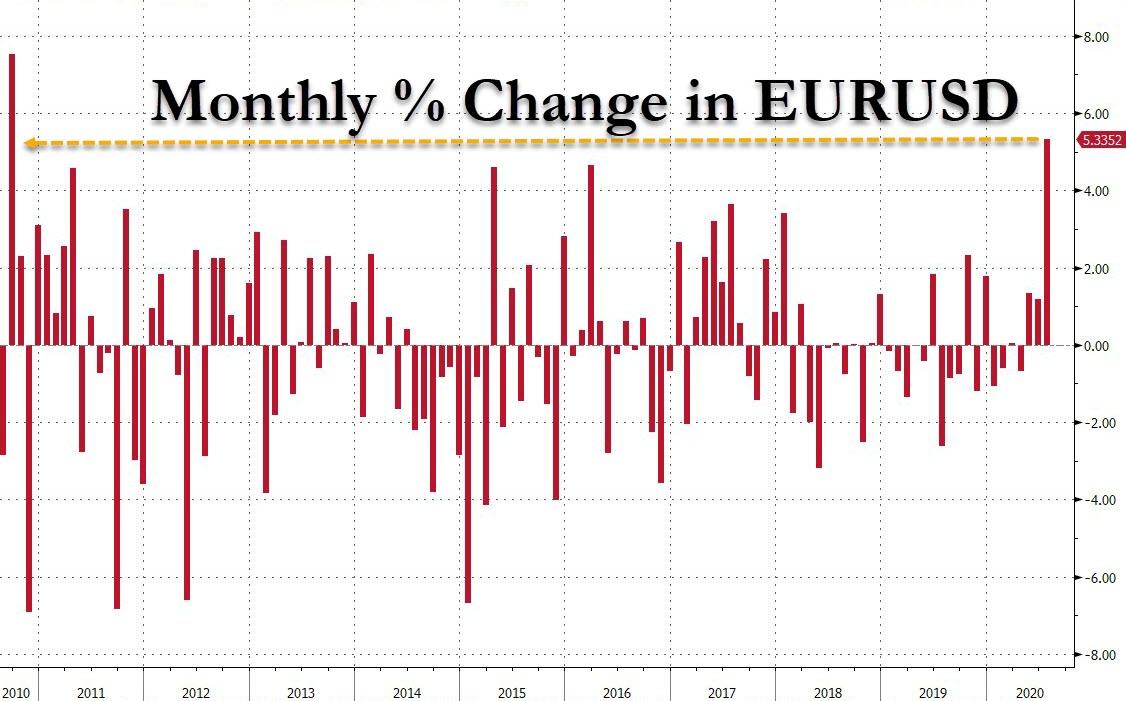

In FX, a gauge of the dollar’s strength weakened to its lowest since May 2018, heading for its sixth week of losses, before rebounding sharply as the EUR slumped. The pound advanced against the dollar, while the euro trimmed its gains following data showing an unprecedented euro-area slump. The two currencies are heading for their best monthly performance for a decade.

The Aussie dollar declined against the greenback as a risk-off mood persisted on reports of surges of the virus across the world, including Australia’s Melbourne.

In rates, Treasuries bull flattened as yields ticked lower, outperforming German bunds; the two-year yield hovered near May’s record low. The 10-year TSY dropped as low as 0.519%, supported by month-end flows. Yields were lower by 0.5bp to 2bp across the curve with long-end-led gains flattening 2s10s, 5s30s by ~0.5bp; 10-year at 0.535% has breached the 0.54% level where convexity trigger is thought to lie and is also its record low closing level on March 9 Bunds, gilts trade broadly in line with Treasuries; S&P 500 E-minis have pared an 0.8% gain to 0.3% with Euro Stoxx 50 higher by 0.6%.

China’s 10-year government bond yield rose after official data showed manufacturing activity expanded at a faster rate this month, suggesting the country’s economic recovery has gained momentum to start the year’s second half. The yield on 10Y Chinese bonds rose 4bps to 2.98% and is on pace to climb 12 basis points for July, the third straight monthly gain. The official manufacturing purchasing managers’ index rose to 51.1 in July from 50.9 a month earlier, as government-led investment gained traction and global demand recovered. Economists have revised up their forecasts for full-year growth, and now see China’s economy expanding 2% this year. Building strength could further reduce the prospects of more monetary easing and add downward pressure on China’s bonds.

In commodities, WTI and Brent have been rangebound throughout the morning as sentiment more broadly remains modestly elevated, while Gold futures stormed back to its all time high just shy of $2,000.

Looking ahead, on the economic front, core personal consumption expenditures data due at 830am, the Fed’s preferred measure of inflation, is likely to have edged higher by 0.2% in June.

Market Snapshot

S&P 500 futures up 0.3% to 3,257.00

STOXX Europe 600 up 0.7% to 362.11

MXAP down 1% to 165.19

MXAPJ down 0.3% to 551.51

Nikkei down 2.8% to 21,710.00

Topix down 2.8% to 1,496.06

Hang Seng Index down 0.5% to 24,595.35

Shanghai Composite up 0.7% to 3,310.01

Sensex down 0.3% to 37,628.16

Australia S&P/ASX 200 down 2% to 5,927.78

Kospi down 0.8% to 2,249.37

German 10Y yield fell 0.7 bps to -0.549%

Euro up 0.2% to $1.1866

Brent Futures up 0.8% to $43.26/bbl

Italian 10Y yield fell 2.1 bps to 0.845%

Spanish 10Y yield fell 0.8 bps to 0.309%

Brent Futures up 0.8% to $43.26/bbl

Gold spot up 1% to $1,975.84

U.S. Dollar Index down 0.2% to 92.82

Top Overnight News from Bloomberg

The euro-area economy plunged into an unprecedented slump in the second quarter, putting it in a deep hole from which it may take years to fully recover. Spain took the biggest hit in the period, shrinking 18.5%, while French and Italian output also dropped by double digits

Gold rose to another record high on Friday, setting it on track for its strongest monthly performance in eight years, fueled by a weaker dollar and low interest rates

An uptick in virus infections are stoking fears of a resurgence in Europe, with Spain seeing particularly high numbers of new cases and the British government re-imposing lockdown measures in part of the U.K. New York City has kept its Covid-19 infection rates low, but the risk of a resurgence looms over the Big Apple as fall approaches

The Senate left Washington for the weekend after a fourth day of negotiations yielded little substantial progress on narrowing differences between Republicans and Democrats on a plan to bolster the coronavirus- ravaged U.S. economy

The largest U.S. technology companies are thriving in a pandemic that has increased dependence on their products and services, while hammering much of the rest of the economy

Asian equity markets traded lacklustre heading into month-end after somewhat mixed Chinese PMI data with the region failing to take advantage of the momentum from US, where futures were boosted after-hours following big tech earnings in which Apple, Alphabet, Amazon and Facebook all beat on top and bottom lines. ASX 200 (-2.0%) was dragged lower by underperformance in the commodity related sectors and with the top-weighted financials also heavily pressured, while there were reports that Australian PM Morrison recently held emergency discussions with the Victoria state Premier which included possible further restrictions for movement within Melbourne and a shutdown of non-essential businesses. Nikkei 225 (-2.8%) was hampered by unfavourable currency flows and although Industrial Production data beat expectations for June, quarterly output was at a decline of 16.7% which was the largest drop according to comparable data since 2015. Furthermore, the biggest movers were driven by earnings including Panasonic, while SoftBank shares also suffered due to the currency effects despite a share repurchase announcement of up to 12.3% of shares for JPY 1tln. Hang Seng (-0.5%) and Shanghai Comp. (+0.7%) were both initially positive with outperformance in the mainland after the PBoC’s liquidity efforts resulted to a net weekly injection of CNY 120bln, although this eventually faded following the latest mixed data releases in which Chinese Official Manufacturing PMI topped estimates but Non-Manufacturing PMI missed and Composite PMI slowed although all figures remained in expansionary territory. Finally, 10yr JGBs eked mild gains amid the soured risk appetite in the region and with the BoJ present in the market for JPY 450bln of JGBs predominantly concentrated in the belly of the curve.

Top Asian News

Japan Factory Production Rises for First Time in Five Months

China Stocks Will Only Get Wilder After July Whipsaws Investors

Facebook, Google Told They Must Pay Australia Media For News

European equities (Eurostoxx 50 +0.6%) trade modestly firmer across the board in what has been another busy morning of corporate updates whilst incremental macro newsflow remains relatively light since yesterday’s close. Although stocks are attempting to recoup some of yesterday’s heavy losses, the extent of the recovery is relatively mild with the Eurostoxx still lower by some 2.5% on the week heading into month-end. Some of the positivity in Europe is a by-product of the fallout from US mega-cap stocks earnings’ in which Apple, Alphabet, Amazon and Facebook all beat on top and bottom lines and were seen higher in after-market trade, prompting outperformance in Nasdaq 100 futures and the tech sector in Europe this morning. Also supporting the tech sector in Europe today is Nokia (+12.2%) post-earnings in which the Co. raised its guidance. Banking names have posted a strong performance in Europe following earnings from BNP Paribas (+2.1%) and Natwest Group (+1.1%), although gains for the sector have been capped by performance in the periphery following disappointing earnings from Spanish-listed Caixabank (-2.6%) and Sabadell (-2.0%). Elsewhere, travel & leisure names have been unable to join in on the mild positivity seen in Europe this far following earnings IAG (-9.1%) in which the Co. announced a EUR 1.37bln operating loss and proposed a capital increase of EUR 2.75bln; easyJet (-3.0%), Ryanair (-3.2%) and Deutsche Lufthansa (-2.2%) are seen lower in sympathy. Performance for telecom names has been hampered by BT (-3.4%) with the Co. warning over the impact of coronavirus on its revenues and earnings after posting a decline in profits. Looking ahead, asides from US participants continuing to digest the latest updates from Apple, Alphabet, Amazon and Facebook, focus will also be on pre-market updates from Exxon, Chevron, Phillips 66, Caterpillar, Merck and Colgate.

Top European News

NatWest Adds $2.8 Billion Provision for Pandemic Loan Losses

He Built It But No One Came: China Chills the Next Canary Wharf

Fortiana Buys Out Abramovich in Bid for Russian Gold Miner

Spanish-Led Outbreaks Fuel Concerns About Further Economic Pain

In FX, it seemed to start with a tweet, but Dollar losses accumulated after Thursday’s plunge in Q2 GDP and IJC data into the NY close and as APAC participants entered the fray for their final trading day of July to push the index further below 93.000 where it remains. The latest rise in unemployment benefit claims is especially worrying as Congress remains at odds over the next fiscal support package that looks certain to leave an overhang when the current jobless insurance measures expire, and with White House Chief of Staff Meadows not confident about reaching a deal next week. All this on top of the ongoing resurgence of COVID-19 across many US states plus the prospect of even more Greenback selling for month end, especially around the 4 pm London fix, amidst a growing number of bank models flagging bearish portfolio rebalancing signals. However, the DXY is holding between 92.539-969 parameters as the Buck pares some declines across the board.

EUR/GBP/JPY – The aforementioned sell Dollar for the July/August turn dynamic is said to be strongest against the Euro and has propelled the single currency through touted resistance between 1.1815-51 to just over 1.1900 temporarily, but Sterling is keeping pace and actually forming a firmer base on its next psychological/round number level at 1.3100. Similarly, the Yen has broken free of tethers that were restraining rallies beyond 105.00, but has retreated ahead of 104.00 following the first signs of alarm about FX developments from Japan’s MoF. Back to Eur/Usd, decent option expiry interest at the 1.1900 strike (1 bn) may be capping attempts to the upside.

CAD/CHF/AUD/SEK/NOK – All narrowly mixed vs their major counterparts in consolidative mode, with the Loonie just below 1.3400 and eyeing a tentative recovery in crude prices, but perhaps more intently aware that unusually large expiries run off at the big figure (2.2 bn) after Canadian GDP and PPI. Elsewhere, the Franc has drifted back towards 0.9100 from circa 0.9057 in wake of a marked slowdown in Swiss retail sales and the Aussie has lost momentum above 0.7200, but the Scandinavian Crowns are benefiting from the Euro’s fade from best levels to maintain upward trajectories within 10.3155-2840 and 10.7825-7240 respective ranges.

NZD – The major underperformer or laggard, as the Kiwi loses grip of the 0.6700 handle and retreats from 1.0750+ in Aud/Nzd cross terms, perhaps taking heed of a stark warning from ANZ overnight about a double dip NZ recession in Q4.

EM – Broad depreciation vs the Usd but the Yuan is extending gains from a firmer PBoC Cny fix and end of month 7-day liquidity injection to supplement mixed, but comfortably above 50 Chinese PMIs, while the Lira has rebounded from lows presumably with the aid of yet more Turkish state bank intervention.

In commodities, WTI and Brent have been rangebound throughout the morning as sentiment more broadly remains modestly elevated as we close out the busiest week of earnings season, with a number of energy names still on the schedule ahead including Exxon & Chevron. As it stands, the benchmarks are going to finish the week in the red by some USD 1/bbl for WTI; albeit, such a close would leave it just about in positive territory for the month as a whole. Aside from the aforementioned earnings, the energy schedule is again very light and we haven’t see any new thus far aside from inflammatory rhetoric from Iranian Supreme Leader Khameni against the US, following the sanctions yesterday, who also said they should not be dependent on oil exports. Moving to metals, in which spot gold is bolstered once more after soft APAC trade and the continuing decline for the USD; albeit, the DXY is currently modestly firmer. Yellow metal resides in the top half of a USD 30/oz range so far but off the USD 1984/oz session peak thus far. At present, spot gold is up by ~10% for the month and is on target for the biggest monthly gain in over 4-years; even given the recent upside desks still believe the rally has further to go with Goldman Sachs envisaging USD 2300/oz; however, JP Morgan believe the pace will decline later into the year. For reference, BofA Flow Show saw the second largest inflows into gold ever, totalling USD 3.9bln.

US Event Calendar

8:30am: Personal Spending, est. 5.2%, prior 8.2%; Real Personal Spending, est. 5.0%, prior 8.1%

8:30am: Personal Income, est. -0.55%, prior -4.2%

8:30am: PCE Deflator MoM, est. 0.44%, prior 0.1%; YoY, est. 0.9%, prior 0.5%

8:30am: PCE Core Deflator MoM, est. 0.2%, prior 0.1%; YoY, est. 1.0%, prior 1.0%

9:45am: MNI Chicago PMI, est. 44.5, prior 36.6

10am: U. of Mich. Sentiment, est. 72.9, prior 73.2; Current Conditions, est. 85.5, prior 84.2; Expectations, est. 65.5, prior 66.2

DB’s Jim Reid concludes the overnight wrap

As the first week of potty training the twins comes to an end my knowledge of the progress is best summed up by the fact that Eddie has 27 stickers on his “well done” chart whereas poor Jamie only has 10. I’ve been trying to keep a low profile in my office as my wife patrols the battlefield waiting to deal with the many casualties. I fear I’m going to be given a lot of the cloths and disinfectant spray this weekend. To be honest I probably am going to get double duties due to the language I used last night when my wife told me how much she spent kitting out Maisie for her first school uniform yesterday. I was gobsmacked and I’ve still got two more to do next year! Oh and then repeat every year or two. Yikes!

If only I had set up a school uniform fund with tech stocks a few years ago. If I had I would now be buying them all gold encrusted blazers rather than asking my wife why she didn’t go to the second hand sale. On tech, the big news after the US closing bell last night was with four of the biggest five companies in the US (and pretty much the world outside of Aramco) reporting. These big four tech companies represent c.16% of the S&P 500 and over a third of the Nasdaq 100. In terms of results all but one ended up higher in after-hours trading. Apple (+6% after-market trading) reported quarterly revenues ahead of analysts’ estimates as iPhone and laptop demand surged, causing revenues to come in 11% higher than a year earlier. Facebook (+6% after-market trading) saw Q2 sales beat even the most bullish analyst’s estimate, with revenues rising 11%. Amazon (+5% after-market trading) beat on profits even after increasing costs substantially through the pandemic. Q2 revenues were up 40% from the same quarter last year, which offset over $4bn in incremental covid-1 related costs. Lastly, Google’s parent company, Alphabet, had falling revenues for the first time as companies lowered ad-spend during the pandemic. That resulted in shares trading flat after market.

Staying with this theme, yesterday we highlighted Amazon in a Chart of the Day (link here), where we showed how its recent rise has coincided with more Americans buying online than ever before during the pandemic. We’re keen to see whether this trend will continue so we’ve set up a 10 second survey to gauge the frequency of your Amazon purchases pre-, during and (likely) post pandemic. All responses welcome including those who don’t use or are unlikely to do so going forward.

Unsurprisingly, NASDAQ futures are trading well overnight, up +0.81% while S&P 500 futures are up a more modest +0.20%. It’s a more mixed picture in Asia however where gains for the Hang Seng (+0.22%) have been offset by moves lower for the Shanghai Comp (-0.05%), Kospi (-0.20%) and most notably, the Nikkei (-2.15%) and ASX (-1.88%). The underperformance in those markets appears to be related to the latest virus data, with Tokyo expected to report more than 400 cases on Friday according to NHK, and the State of Victoria in Australia continuing to see a high number of new cases. Away from that, we’ve also had China’s July PMIs, where the manufacturing reading came in slightly ahead of expectations and the strongest since March (51.1 vs. 50.8 expected; 50.9 previously) and non-manufacturing slightly below (54.2 vs. 54.5 expected; 54.4 previously).

This follows a difficult day for risk but one that recovered progressively after a bad first hour of US trading and one that was back in positive territory after hours with the strong beats seen above. Sentiment initially wasn’t helped by challenging data even if the GDP weakness was well flagged and in the ballpark of expectations. On this, the US’s sharpest quarterly downturn since the 1940’s was confirmed with an annualised rate of -32.9% (vs consensus at -34.5%) or a -9.5% quarterly rate. While this is the worst data point in the official quarterly data going back to 1947, as we showed in yesterday’s second “Chart of the Day” (link here), it was not the worst over the last century. Elsewhere, yesterday’s German GDP print of -10.1% (vs. -9.0% expected) was the biggest drop in at least 50 years and is an ominous sign for the Spanish, French and Italian GDP prints due this morning. These countries had much longer lockdowns than Germany.

Investor sentiment was not helped by the initial weekly jobless claims in the US, which covered the week ending July 25. The data showed a second straight weekly increase in claims with 1.434m (vs. 1.443m expected) registered. On the continuing claims front for the previous week (ending July 18), 17.02m (vs. 16.2m expected) Americans filed to continue to receive benefits, up 867k from the week before. That was the largest weekly increase since the early part of May.

Following the expectedly bad GDP data in the US and the less expected poor continuing claims data, the S&P 500 fell -1.67% within the first half hour of US trading. However by the close the index had pared much of those loses ahead of those largest US tech companies reporting. With technology stocks leading the way, the S&P finished with a -0.39% loss on the day and the NASDAQ finished +0.43%.

European stocks dropped further and closed before the full comeback, with the STOXX 600 retreating -2.16% for the worst daily performance in over a month. The only industry group to finish higher was Travel & Leisure (+0.20%) led by Francaise des Jeux rallying +18.84% after the company announced that overall activity since mid-June had returned to a level comparable to 2019. The worst performing sector was banks (-4.26%) following Lloyds announcing a loan loss provision that cancelled out the lender’s quarterly profit, while BBVA fell after posting worse-than-expected revenues from lending and also set aside larger provisions than expected.

Whether the poor economic data yesterday in the US and Europe led to a risk-off sentiment or simply the feeling the central banks will need to do more, core sovereign bonds rallied. 10yr German bund yields fell -4.4bps to -0.54%, while US 10yr Treasuries fell -2.8bps to 0.546%, about half a basis point above all-time closing lows. US yields barely sold off as risk sentiment improved though. Elsewhere the dollar fell another -0.46%, but the drop in yields and the dollar move could not keep gold positive. The yellow metal fell (-0.72%) for the first time in 10 sessions yesterday.

There was a flurry of positive coronavirus vaccine news yesterday, though not enough to offset the negative economic data. There is also the possibility that the likelihood of a vaccine in the medium term is already priced in. Nearly 10,000 people in the UK were given a dose of the AstraZeneca and University of Oxford experimental vaccine after an early study showed promising signs in primates. In the US, Johnson & Johnson announced intent to start their phase 3 trials of its covid-19 vaccine in September. A study in Nature showed that the Johnson & Johnson candidate caused a strong protectionary immune response against the infection.

There continues to be calls for covid vigilance across Europe though, even as countries are mostly reopened. In Sweden, one of the most critiqued nations for their handling of the crisis, Prime Minister Lofven urged residents to continue working from home this autumn. Amsterdam has joined other metropolitan regions in the continent requiring face masks in public spaces where previously they were only required on public transport. While in the UK, the government announced that they have lengthened the self-isolation period for coronavirus patients to ten days from seven. Prime Minister Johnson warned citizens that the pandemic was ongoing and that other European nations are seeing “signs of a second wave of the pandemic”. Spain and France in particular have both seen an uptick in cases, with Spain reporting over 1000 infections on 2 consecutive days for the first time since the start of May. French cases are increasing by just under 1,000 a day on average over the last week, compared to under 500 per day at the end of June. The U.K. also saw its highest numbers of cases (846) since 28 June and there have been a tightening of household interactions in northern England.

These growing case numbers are still low compared to the US where cases rose by over 60,000 yesterday for the fourth day in a row. Florida reported a third straight day of record fatalities with 253 new covid-19 deaths. Arizona also saw a record rise of deaths with 172, yet 78 of those were belatedly reported numbers after prior clerical errors. Regardless, the country as a whole is seeing over 7200 deaths per week, up from the 4100 recorded at the beginning of July, but about half as bad as was seen during the height of the pandemic in April (peak of 15,400 fatalities in a week).

These data points should get Congress’s attention, as the US fiscal stimulus situation in the US becomes more fraught. The senate held a procedural vote to try and extend lapsed supplemental unemployment insurance, however Democrats held out saying that the measure should be included in comprehensive stimulus legislation. The senate is on recess until Monday, but expect negotiations over the weekend with the base case remaining a deal is done with additional unemployment benefits less than the $600 per week it was at and some aid to state and local governments to deal with the costs of the pandemic.

Lastly to the day ahead, where the highlights should be French, Italian and Euro Area preliminary Q2 GDP and CPI prints. Along with those there is Italian retail sales and a bevy of US data, including June personal income, personal spending, July MNI Chicago PMI and the final July University of Michigan sentiment. While there are no big central bank speakers, the busiest week of earnings season will end with results from Chevron, Charter Communications, Merck, AbbVie, Phillips 66, ExxonMobil, BNP Paribas, Caterpillar, Nokia, NatWest Group and Fiat Chrysler.

via ZeroHedge News https://ift.tt/39J9p8u Tyler Durden

A Stunned Wall Street Responds To Apple And Google’s Stellar Earnings Tyler Durden

Fri, 07/31/2020 – 07:39

At a time when the “big four” mega tech companies are in the public spotlight for anti-trust, anti-competitive behavior, watching their collective market cap explode by a quarter trillion dollars may not have been the most prudent outcome. But that’s what happened when Apple, Amazon, Facebook and Google reported generally blockbuster earnings last night, sending the price of the first three stocks higher by at least 5% in the premarket, and pushing the collective market cap of the four gigacaps to nearly $5 trillion.

Below we summarize Wall Street’s reactions to Apple and Google’s earnings which were broadly indicative of the mood set by big tech last night, and which has carried over into this morning’s futures:

Apple:

Apple shares are poised to open at a record level following second-quarter results that prompted multiple price-target increases from Wall Street analysts, and reassured that the iPhone-maker’s business was weathering any impact from the pandemic. Apple’s shares jumped 6.3% in U.S. premarket trading, putting the stock on track to open at $409, above the all-time high of $394 reached just last week. Analysts at Goldman Sachs said that they had underestimated how much people were spending to support their working and studying from home, as well as the amount of cash that had been freed up as consumers cut back spending on areas like entertainment and gas. Piper Sandler analysts said they see further strength for Apple’s business, which should benefit from the launch of its new 5G-enabled iPhone, expected later this year.

Google:

Alphabet Inc. shares dipped in premarket trading on Friday, after the Google-parent reported its first-ever decline in revenue, pressured as the pandemic weighed on digital advertising. The company said that ad sales were picking up again by the end of the quarter, but the comments failed to excite, especially in comparison with earnings seen at other major internet and technology stocks, like Facebook Inc., Amazon.com Inc. and Apple Inc. RBC Capital Markets wrote that the quarter showed a “recovery in moderation,” adding that “fundamentals were clearly weak” due to the pandemic. While analysts see a steady recovery in the digital ads market, prompting a number of firms to raise their price targets, Susquehanna cautioned that a full recovery “will only come when the economy begins performing better.” Shares fell 0.9% before the bell. Based on its most recent close, Alphabet’s stock is up more than 45% from a March low. Morgan Stanley, Brian Nowak

Courtesy of Bloomberg, here’s what analysts are saying about Apple’s earnings:

Piper Sandler, Harsh Kumar

The most notable item in Apple’s June quarter results was the business holding up “extremely well,” with the pandemic having little impact on the core business.

Next fiscal year appears to be a “banner year” for Apple as the firm will benefit from the delayed 5G iPhone launch falling in the December quarter.

Kumar raised his price target to $450 from $310 and reiterated his overweight rating.

Cowen, Krish Sankar

Apple’s June quarter results are “robust” and its outlook is “encouraging.”

While there was no formal September guidance, positive iPad and Mac momentum and encouraging back-to-school trends are expected.

Sankar raised his price target to $470 from $400 and reiterated his outperform rating.

Goldman Sachs, Rod Hall

This is a “very strong” quarter for Apple as consumers and institutions were clearly spending even more than expected to support both work-from-home and study-from-home.

Also likely underestimated short-term impact of stimulus and disposable income freed up by lack of spending on things like entertainment and gas.

“This is a quarter to give Apple credit where credit is due for excellent execution and performance in the midst of unprecedented difficulty,” Hall said in a note.

However, continues to believe caution is warranted looking into 2021.

Hall raised his price target to $314 from $299 and kept his sell rating.

Raymond James, Chris Caso

June was “significantly better” than expectations for Apple as the impact on demand from the pandemic improved more quickly than expected.

Apple did admit “somewhat surprisingly” to new iPhone availability “a few weeks later” compared to last year, which Caso expects will serve to push iPhone revenue from Sept. to Dec.

Caso raised his price target to $440 from $400 and reiterated his outperform rating.

Deutsche Bank, Jeriel Ong

While Apple’s decision not to provide a forward-quarter guidance could be interpreted as a sign of uncertainty, Apple did provide more segment commentary.

Apple also guided to select line items more within its control.

Positives outweigh the minor negatives in the quarter, while Apple’s confidence that trends continue into the Sept. quarter could understate the reality that they could actually strengthen.

Ong raised his price target to $440 from $400 and maintained his buy rating.

And here is Google:

Morgan Stanley, Brian Nowak

Overweight, PT to $1,760 from $1,700

Alphabet’s ad recovery “is progressing largely in-line with our expectations,” though it “remains slower than [Facebook]” given Alphabet’s size, exposure to travel, and growth in social-media e-commerce

Any structural reduction in opex or capex could “translate to material earnings power”

The stock is a “strongmulti-year compounder”

RBC Capital Markets, Mark Mahaney

Outperform, PT raised to $1,700 from $1,500

The results showed a “recovery in moderation”

While most metrics came in ahead of consensus expectations, “fundamentals were clearly weak and negatively impacted by COVID”

Fundamentals are stabilizing, but the Alphabet’s management “remains cautious for [the second half of the year] on macro uncertainties”

Susquehanna Financial Group, Shyam Patil

Positive, PT to $1,850 from $1,550

Advertising trends improved throughout the quarter, and “barring an unexpected turn for the worse in the macro, GOOGL should continue to steadily recover” over the rest of the year

A full recovery “will only come when the economy begins performing better”

The stock should see tailwinds from Alphabet’s cloud business, expense management, “a more shareholder-friendly capital allocation approach,” and the long-term growth in digital ads, especially from YouTube and mobile search

Baird, Colin Sebastian

Outperform, PT raised to $1,675 from $1,650

The results “keep us constructive at current levels,” especially as online advertising trends improved in May, June and into July

Growth in the company’s cloud business “remained stable even as competitors decelerated a bit”

The company has “multiple levers of growth within online advertising, video, commerce, cloud and ‘other bets’”

Bloomberg Intelligence

The company “continues to be carried through a muted ad climate by cloud’s robust momentum,” along with growth in YouTube and productivity tools

If this quarter ends being the worst, in terms of its pandemic impact, “extended improvement in July could aid recovery optimism and boost 2H consensus”

via ZeroHedge News https://ift.tt/2XdStBY Tyler Durden

Hong Kong Cancels Fall Election As Coronavirus “Third Wave” Intensifies Tyler Durden

Fri, 07/31/2020 – 07:35

President Trump’s mere “suggestion” that the US ought to think about delaying the November election (Nov. 7, 2024 sounds like a pretty safe date) unleashed a torrent of hysterical commentary as the president’s dedicated #resistance critics accused the president of wilfully subverting our great democracy – despite the fact that even WaPo is worried about the USPS “backlog” and the risk that some mail-in ballots won’t arrive by November.

The hysteria dominated yesterday’s news cycle, despite the fact that Trump’s tweet was in all likelihood intended to distract from the abysmal Q2GDP data released Thursday morning…

Trump’s ‘let’s delay the election’ tweet was clearly intended to distract from the Q2 GDP print on a slowish news day…yawn https://t.co/Capw9L5VuP

…now, in an amusing coincidence, Hong Kong chief executive Carrie Lam on Friday announced that the city state would postpone its elections set for the fall as the “third wave” of SARS-CoV-2 causes more outbreaks than the prior two waves (prompting HK to crack down on indoor dining/bars and impose the most restrictive social distancing measures yet).

Hong Kong’s embattled leader has invoked emergency powers to postpone the Legislative Council elections scheduled for September 6, citing health risks from the resurgent Covid-19 crisis as the primary reason.

Flanked by the ministers for justice, health and constitutional affairs, Chief Executive Carrie Lam Cheng Yuet-ngor told a press conference on Friday evening the decision was the most difficult she had made in the last seven months.

“Since January, we have been fighting the pandemic for seven months. This pandemic has dealt a heavy blow to our economy,” she said.

“We have not been complacent. We need to be on high alert all the time and respond.

“We are facing a serious situation … The World Health Organisation’s chief recently said we sometimes need to make some hard choices, and my decision today is the hardest of all.”

Lam said she was invoking the Emergency Regulations Ordinance in doing so, and her decision was supported by the central government.

Beijing supports canceling September’s legislative elections? Color us shocked. Domestic pro-democracy critics immediately slammed the HK government for using COVID-19 as a ruse to crack down on freedoms in the city, where a new ‘national security’ law has given authorities sweeping powers to punish anybody for political dissent that is now legally tantamount to terrorism. Yesterday, we reported that 4 teens in the city had been arrested for political social media posts.

The decision comes as Hong Kong reports a record single-day jump in new COVID-19 cases, extending the streak of 100-plus single-day infection numbers.

Americans should probably pay closer attention to what’s happening in Hong Kong – because President Trump clearly was. Lam’s decision to cancel the September vote followed a decision on Thursday to disqualify at least a dozen opposition hopefuls who managed to qualify for the vote, per the SCMP.

In a statement released earlier, 22 pan-democrat lawmakers, including four barred from seeking another term, said the Legislative Council elections were a core element of Hong Kong’s constitutional foundation.

“According to the Legco Ordinance, the polls can only be postponed by 14 days,” the statement said. “To postpone it [beyond that] is to trigger a constitutional crisis in the city.”

“After a year of democratic movement, it is urgent for Legco to undergo a baptism of public opinion, that is the root of the city’s governance…The government and the whole of society must make every effort to make sure that the general elections can be held as planned.”

[…]

election officials cited the city’s new national security law and the pan-democrats’ previous calls for foreign governments to sanction Beijing and Hong Kong as reasons for barring four incumbent lawmakers – the Civic Party’s Alvin Yeung Ngok-kiu, Dennis Kwok and Kwok Ka-ki, as well as accountancy sector lawmaker Kenneth Leung.

Other disqualified opposition figures included Joshua Wong Chi-fung, Ventus Lau Wing-hong, Gwyneth Ho Kwai-lam and Alvin Cheng Kam-mun, along with district councillors Cheng Tat-hung, Lester Shum, Tiffany Yuen Ka-wai and Fergus Leung Fong-wai.

Returning officers cited similar reasons for their invalidation and their earlier vow to vote down the government’s budget and other bills, should the bloc win an unprecedented majority in the legislature.

Opposition lawmakers accused the central government of trying to deprive HKers of their right to vote, and noted that more than 60 elections have been held worldwide since the start of the outbreak, either right on schedule or after a brief delay. But Beijing was never going to risk an embarrassing electoral defeat in the LegCo. Opposition lawmakers probably understood that going in, now that Hong Kong’s freedoms have been stripped away by the new Nat Sec law.

via ZeroHedge News https://ift.tt/3gho79r Tyler Durden

Let us now praise the Go-Go’s, glittering jewels of the New Wave moment of the 1980s .

Praise has been in meager supply since the band’s first album, Beauty and the Beat, streaked up the charts in 1981, fueled by the irresistible hits “We Got the Beat,” “Our Lips Are Sealed,” “How Much More,” and “Skidmarks on My Heart” (all heavily assisted by the newborn MTV). Today, after nearly 40 years of eligibility for induction into the Rock and Roll Hall of Fame, the Go-Go’s remain un-inducted.

In the beginning, there was a certain amount of critical skepticism as to whether the group – chief songwriters Charlotte Caffey (lead guitar and keyboards), Jane Wiedlin (rhythm guitar), and Kathy Valentine (bass), along with singer Belinda Carlisle and drummer Gina Schock—actually played the instruments heard on their records. But they had started out on the tough LA punk scene; and as a terrific new Showtime documentary, The Go-Go’s, irrefutably demonstrates—in period footage from old club gigs and big arena shows—they definitely could play. “We got onstage and happened to be a group of women who really kicked ass,” Schock says.

Some notable fellow musicians were impressed. “They had the most important ingredient in musicianship, which is feel,” says Stewart Copeland, drummer for the Police, which recruited the Go-Go’s as an opening act for a 1981 tour. “They established a groove that worked, that you could lock into. They just created something that exploded on the stage.” A little earlier, the English ska group Madness had the Go-Go’s open for them on a UK tour. “Their musicianship was second to none,” says band member Lee Thompson. “They taught me a thing or two.”

The Go-Go’s’ heyday was brief, for the usual reasons. Despite their sunshiny sound, the group had some dark problems. Carlisle was plagued by decades-long drug and alcohol issues (she recalls the group’s “cross-eyed drunk” performance on Saturday Night Live), Caffey was a full-blown heroin addict, Wiedlin was bipolar, and Schock had a heart condition that eventually required surgery. But in the end it was the music business that tore them apart. Their smash-hit debut album kept them on the road for a year, leaving little time to write new material for their second record, Vacation, which got over mainly on the strength of its title track. Their third LP, Talk Show, featured two classics, “Head Over Heels” and “Turn to You,” but it didn’t crack the Top 10. The magic was leaking away.

But the Go-Go’s’ main problem, which proved insurmountable, was money. Songwriters Caffey, Wiedlin, and Valentine got most of the song-publishing checks, and Schock—a great drummer and the band’s lowest-paid member—grew increasingly resentful. A separate financial injustice propelled Wiedlin out of the group at the end of 1984; Caffey and Carlisle bailed shortly thereafter. And that was it. The Go-Go’s stopped speaking to each other for the next five years. “Money wrecks everything,” Schock says.

There have been several reunions since that time, though, and the best of them—like a 2001 concert in New York’s Central Park, which launched a comeback album called God Bless the Go-Go’s—have shown that the old songs still dazzle, and that the band still has the power and precision to put them over onstage. The Showtime doc—a blend of new interviews and old footage wonderfully well-assembled by director Alison Ellwood—is a rousing tribute to the first self-contained female band (they write, they play) to score a number-one album. God bless ’em.

(The Go-Go’s premieres on Showtime at 9pm Friday, July 31.)

from Latest – Reason.com https://ift.tt/2XhJyzM

via IFTTT

Let us now praise the Go-Go’s, glittering jewels of the New Wave moment of the 1980s .

Praise has been in meager supply since the band’s first album, Beauty and the Beat, streaked up the charts in 1981, fueled by the irresistible hits “We Got the Beat,” “Our Lips Are Sealed,” “How Much More,” and “Skidmarks on My Heart” (all heavily assisted by the newborn MTV). Today, after nearly 40 years of eligibility for induction into the Rock and Roll Hall of Fame, the Go-Go’s remain un-inducted.

In the beginning, there was a certain amount of critical skepticism as to whether the group – chief songwriters Charlotte Caffey (lead guitar and keyboards), Jane Wiedlin (rhythm guitar), and Kathy Valentine (bass), along with singer Belinda Carlisle and drummer Gina Schock—actually played the instruments heard on their records. But they had started out on the tough LA punk scene; and as a terrific new Showtime documentary, The Go-Go’s, irrefutably demonstrates—in period footage from old club gigs and big arena shows—they definitely could play. “We got onstage and happened to be a group of women who really kicked ass,” Schock says.

Some notable fellow musicians were impressed. “They had the most important ingredient in musicianship, which is feel,” says Stewart Copeland, drummer for the Police, which recruited the Go-Go’s as an opening act for a 1981 tour. “They established a groove that worked, that you could lock into. They just created something that exploded on the stage.” A little earlier, the English ska group Madness had the Go-Go’s open for them on a UK tour. “Their musicianship was second to none,” says band member Lee Thompson. “They taught me a thing or two.”

The Go-Go’s’ heyday was brief, for the usual reasons. Despite their sunshiny sound, the group had some dark problems. Carlisle was plagued by decades-long drug and alcohol issues (she recalls the group’s “cross-eyed drunk” performance on Saturday Night Live), Caffey was a full-blown heroin addict, Wiedlin was bipolar, and Schock had a heart condition that eventually required surgery. But in the end it was the music business that tore them apart. Their smash-hit debut album kept them on the road for a year, leaving little time to write new material for their second record, Vacation, which got over mainly on the strength of its title track. Their third LP, Talk Show, featured two classics, “Head Over Heels” and “Turn to You,” but it didn’t crack the Top 10. The magic was leaking away.

But the Go-Go’s’ main problem, which proved insurmountable, was money. Songwriters Caffey, Wiedlin, and Valentine got most of the song-publishing checks, and Schock—a great drummer and the band’s lowest-paid member—grew increasingly resentful. A separate financial injustice propelled Wiedlin out of the group at the end of 1984; Caffey and Carlisle bailed shortly thereafter. And that was it. The Go-Go’s stopped speaking to each other for the next five years. “Money wrecks everything,” Schock says.

There have been several reunions since that time, though, and the best of them—like a 2001 concert in New York’s Central Park, which launched a comeback album called God Bless the Go-Go’s—have shown that the old songs still dazzle, and that the band still has the power and precision to put them over onstage. The Showtime doc—a blend of new interviews and old footage wonderfully well-assembled by director Alison Ellwood—is a rousing tribute to the first self-contained female band (they write, they play) to score a number-one album. God bless ’em.

(The Go-Go’s premieres on Showtime at 9pm Friday, July 31.)

from Latest – Reason.com https://ift.tt/2XhJyzM

via IFTTT

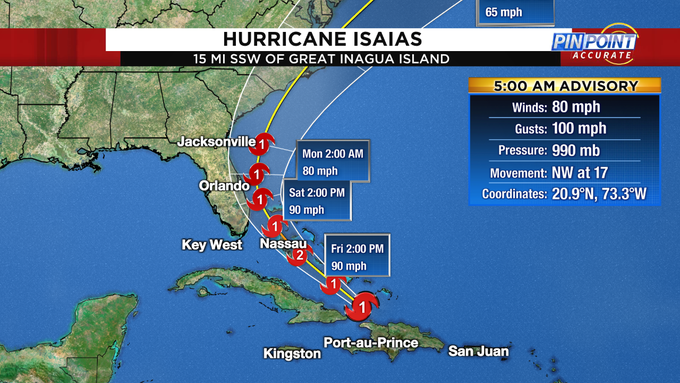

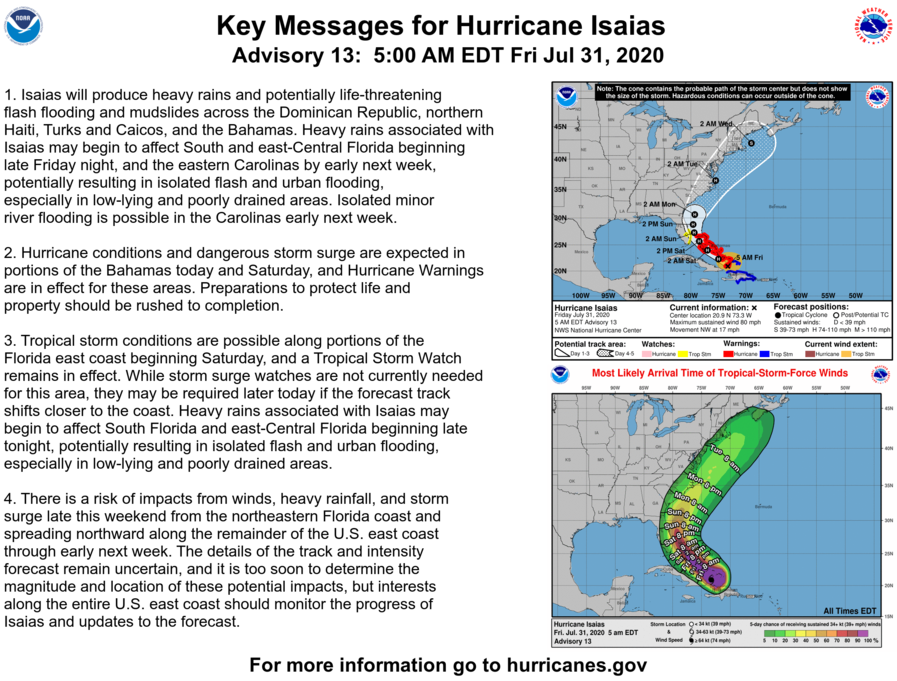

Isaias Strengthens To Category 1 Hurricane With South Florida In Sight Tyler Durden

Fri, 07/31/2020 – 07:02

Tropical Storm Isaias was upgraded in the overnight hours to a Category 1 hurricane.

Hurricane Isaia has maximum sustained winds at 80 mph and is quickly moving northwest at 17 mph, located 15 miles south-southwest of Great Inagua Island, reported CBS Orlando.

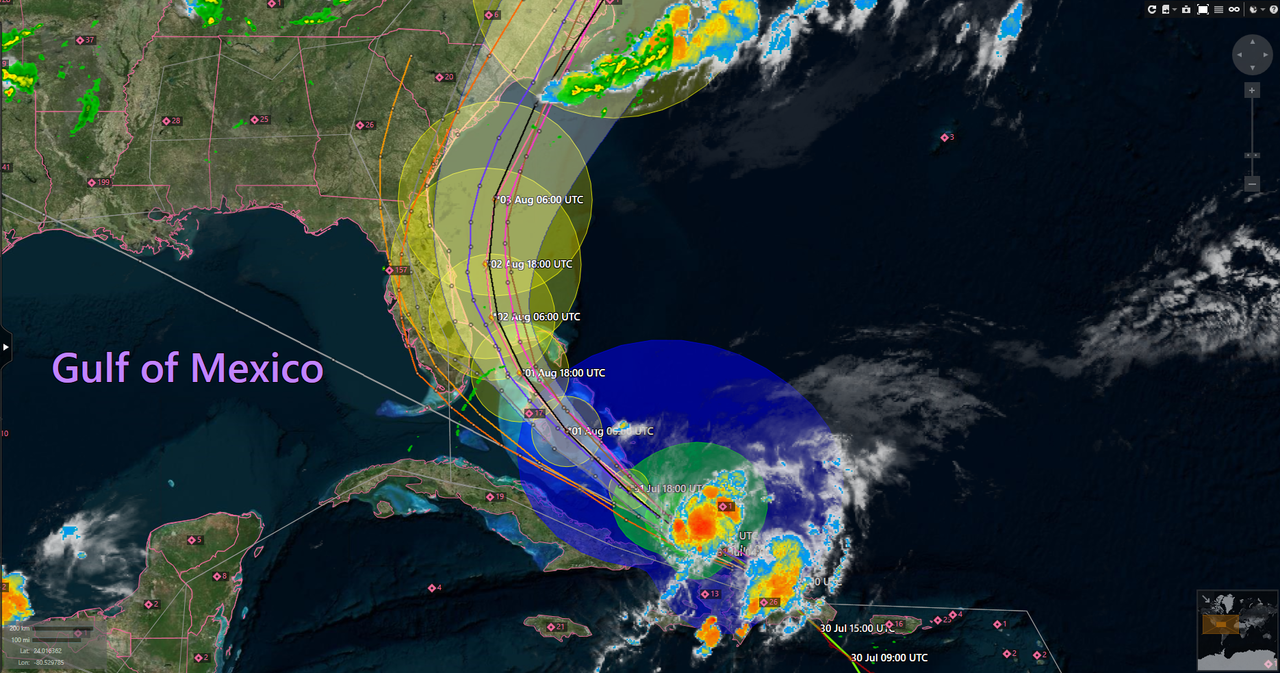

Isaia is expected to pass over the southeastern Bahamas early Friday, then central Bahamas Friday evening, and should close in on South Florida by Saturday. The storm is expected to hug the Florida coast through the weekend.

Most spaghetti models show the hurricane could move up the East Coast and head to the Outer Banks by late Monday. A couple of models show the storm tracks more into the Atlantic. There’s even a model of the storm heading into the Gulf of Mexico.

“As of now, the center of Isaias is expected to remain off the coast of Florida,” News 6 meteorologist Jonathan Kegges said. “The worst of the weather is on the northern and western side of the storm.”

A more precise track will be determined later in the day on Friday.

via ZeroHedge News https://ift.tt/39GWRyu Tyler Durden