Chinese Scientist, Escorted Out Of Canadian Biolab, Sent Deadly Viruses To Wuhan Tyler Durden

Mon, 06/15/2020 – 08:42

“We have a researcher who was removed by the RCMP from the highest security laboratory that Canada has for reasons that government is unwilling to disclose. The intelligence remains secret. But what we know is that before she was removed, she sent one of the deadliest viruses on Earth, and multiple varieties of it to maximize the genetic diversity and maximize what experimenters in China could do with it, to a laboratory in China that does dangerous gain of function experiments. And that has links to the Chinese military.” -Amir Attaran

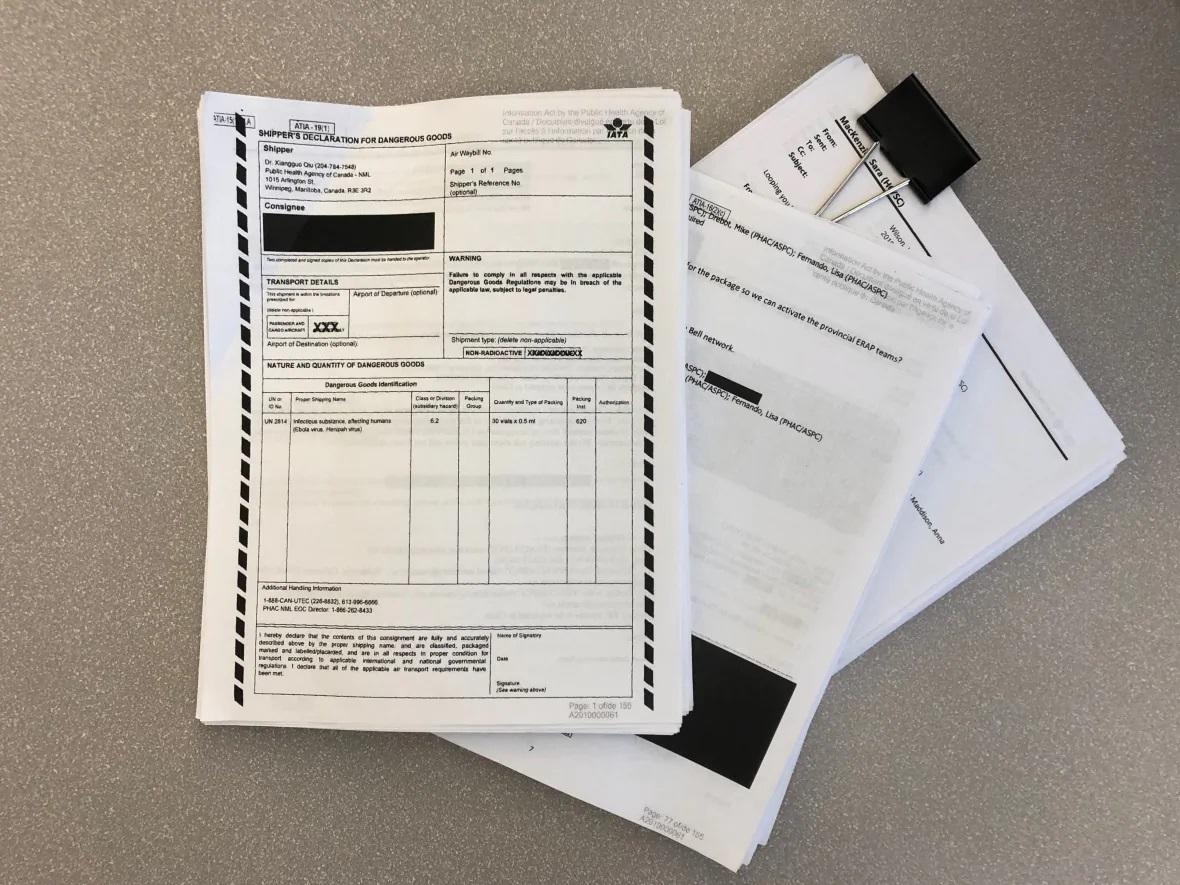

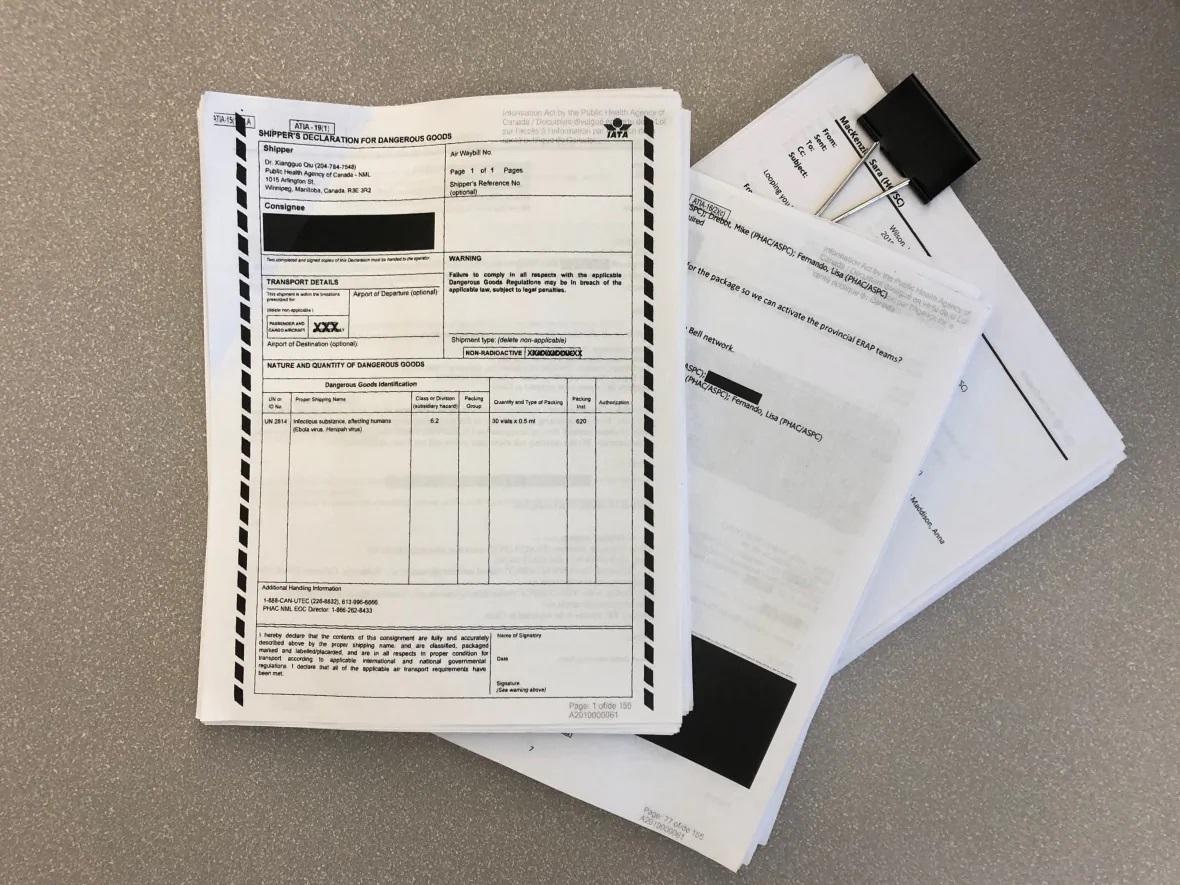

A Chinese scientist who was escorted out of Canada’s only level-4 biolab over a possible “policy breach” shipped dealdy Ebola and Henipah viruses to the Wuhan Institute of Virology, according to the CBC, citing newly-released documents. The shipment is not related to COVID-19 or the pandemic.

Dr. Xiangguo Qiu, her husband Keding Cheng and her Chinese students were removed from the Canadian lab after the Public Health Agency of Canada (PHAC) asked the RCMP to investigate several months earlier. According to PHAC, Qiu’s eviction from the lab is not connected to the shipment.

Dr. Xiangguo Qiu accepting an award at the Governor General’s Innovation Awards at a ceremony at Rideau Hall in 2018. Qiu is a prominent virologist who helped develop ZMapp, a treatment for the deadly Ebola virus which killed more than 11,000 people in West Africa between 2014-2016. (CBC)

“The administrative investigation is not related to the shipment of virus samples to China, said PHAC chief of media relations, Eric Morrissette.”

“In response to a request from the Wuhan Institute of Virology for viral samples of Ebola and Henipah viruses, the Public Health Agency of Canada (PHAC) sent samples for the purpose of scientific research in 2019.”

To recap, a Chinese scientist, her husband and her Chinese students were escorted out of Canada’s only Level-4 lab for reasons unknown, and which are not related to her shipment of deadly viruses to the Wuhan Institute of Virology.

“It is suspicious. It is alarming. It is potentially life-threatening,” said University of Ottawa law professor and epidemiologist, Amir Attaran.

Amir Attaran, professor in the Faculty of Law and the School of Epidemiology and Public Health at the University of Ottawa, is concerned about the shipment of dangerous viruses sent from Canada’s only level-4 lab to China. (CBC)

While Canada doesn’t do ‘gain-of-function’ experiments – which are where natural pathogens are mutated in a lab and assessed to see if it has become more deadly or infectious, “The Wuhan lab does them and we have now supplied them with Ebola and Nipah viruses. It does not take a genius to understand that this is an unwise decision,” said Attaran.

“I am extremely unhappy to see that the Canadian government shared that genetic material.“

Attaran pointed to an Ebola study first published in December 2018, three months after Qiu began the process of exporting the viruses to China. The study involved researchers from the NML and University of Manitoba.

The lead author, Hualei Wang, is involved with theAcademy of Military Medical Sciences, a Chinese military medical research institute in Beijing.

All of this has led to conspiracy theories linking the novel coronavirus responsible for COVID-19, Canada’s microbiology lab, and the lab in Wuhan. –CBC

According to the report, the RCMP and PHAC have repeatedly denied any connections between the virus shipments and COVID-19.

According to the newly-released documents, the following virus strains were shipped to the WIV (approximately 15 ml):

Ebola Makona (three different varieties)

Mayinga.

Kikwit.

Ivory Coast.

Bundibugyo.

Sudan Boniface.

Sudan Gulu.

MA-Ebov.

GP-Ebov.

GP-Sudan.

Hendra.

Nipah Malaysia.

Nipah Bangladesh.

The documents also shed light on communications from the months leading up to the shipment – including confusion on how to package the viruses, along with a lack of decontamination of the package prior to its shipment, as well as concerns expressed by NML Director-General Matthew Gilmour to his superiors in Ottawa – particularly over where the package was going, what was in it, and whether its paperwork was in order.

CBC News received hundreds of pages of documents through an Access to Information request, detailing a shipment of Ebola and Henipah viruses sent from the National Microbiology Lab in Winnipeg, to the Wuhan virology lab in China. (Karen Pauls/CBC News)

In one email, Gilmour said Material Transfer Agreements would be required, “not generic ‘guarantees’ on the storage and usage.”

He also asked David Safronetz, chief of special pathogens: “Good to know that you trust this group. How did we get connected with them?”

Safronetz replied: “They are requesting material from us due to collaboration with Dr. Qiu.” –CBC

According to the report, the shipper of the viruses had originally planned to use inappropriate packaging, and only corrected the mistake when the WIV flagged the issue.

“The only reason the correct packaging was used is because the Chinese wrote to them and said, ‘Aren’t you making a mistake here?’ If that had not happened, the scientists would have placed on an Air Canada flight, several of them actually, a deadly virus incorrectly packaged. That nearly happened,” said Attaran.

‘Hope’ Sends New York Manufacturing Survey Soaring Back To ‘Normal’ In June Tyler Durden

Mon, 06/15/2020 – 08:39

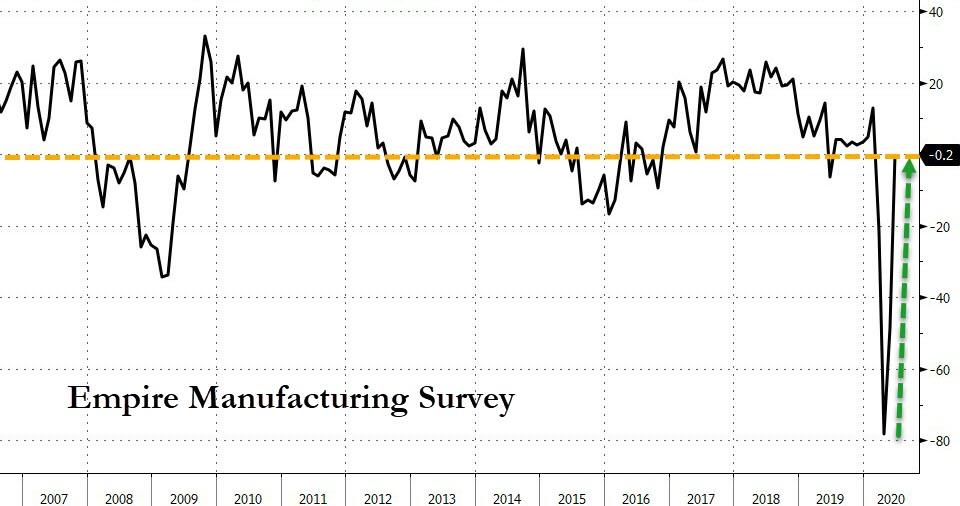

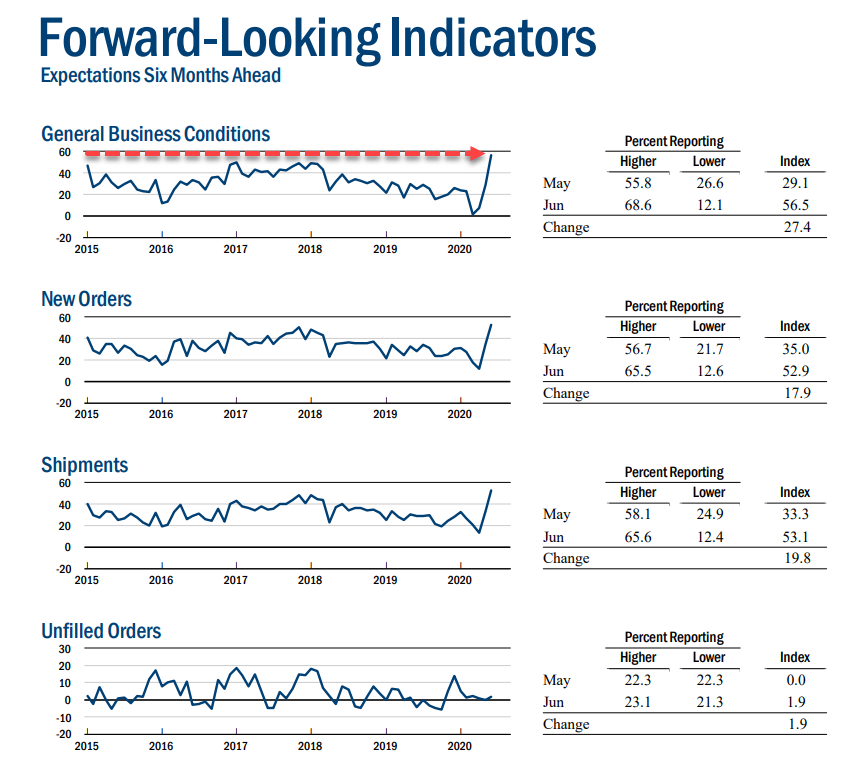

After collapsing to a record low -78.2 in April, The New York Fed’s general business conditions index advanced to -0.2 from -48.5 a month earlier. This is massively better than the -30.0 expectation.

Source: Bloomberg

As a reminder, a reading of zero is the dividing line between expansion and contraction meaning that at -0.2, New York is basically “back to flat” in June.

The move was entirely driven by an explosion in hope…

This reopening euphoria is the highest level of ‘hope’ for 6-month forward expectations since Oct 2009. And that rebound did not end well in 2009.

via ZeroHedge News https://ift.tt/3d21ALh Tyler Durden

From the Senate resolution, which came out about a month ago, but which I only learned about several days ago (underlining added to note some key phrases):

WHEREAS on April 28th, 2020 in the course titled “Introduction to Comparative Studies in Race and Ethnicity,” Professor Rose Salseda was invited to teach and said, “nigga,” while reciting lyrics to the 1988 classic by N.W.A., “Fuck tha Police;” and

WHEREAS on May 4th, 2020, in the course titled “Riot!: Visualizing Civil Unrest in the 20th and 21st Centuries” Professor Salseda wrote “Niggaz” twice while writing the full name of the group N.W.A and discussing their artwork, and …

WHEREAS use of the n-word by a White person or Non-Black person of color is offensive and highly inappropriate, especially in courses whose teachings intend to value and center Black liberation; and

WHEREAS this is not the first incident of racial violence against Black students in which a non-Black lecturer has employed and said the n-word while teaching, but hopefully will be the last; …

THEREFORE BE IT BE RESOLVED BY THE UNDERGRADUATE SENATE

THAT the Undergraduate Senate is appalled by and condemns Professor Rose Salseda’s continuous aggressions against the Black community and Black students, particularly her repeated use of the n-word in Canvas discussion board communications on May 4th, 2020. Reckless actions of this manner and Salseda’s disturbing presence teaching Black art and art history in our intellectual community must be dealt with….

THAT the Undergraduate Senate calls for the Center for Comparative Studies in Race and Ethnicity to reconsider what courses Professor Rose Salseda can teach (i.e Introduction to African-American Art), bring her back to Introduction to CSRE to listen / fully take ownership of her actions, participate in identity and cultural humility training ….

Prof. Salseda, an assistant professor, apologized; nearly everyone does, of course. What have things come to, though, that university professors (and surely also students) can’t accurately quote important music, literature, or film that they are discussing? (Unless, of course, they’re the right color.) Presumably Stanford professors discussing the lyrics would be required to say, “I don’t know if they fags or what / Search a n-word down, and grabbin’ his nuts.” (Or should it be “I don’t know if they f-words or what …”?) I wonder what the members of N.W.A. would think about that.

And of course you can’t simply play the song (or the movie, whether it’s To Kill a Mockingbird or Pulp Fiction or Godfather, Part II or The Shining or Rocky or Platoon or many others), as the UCLA Ajax Peris incident shows: He was faulted both for reading a passage with the word “nigger” from Martin Luther King, Jr.’s Letter from Birmingham Jail and for “show[ing] a portion of a documentary which included graphic images and descriptions of lynching, with a narrator who quoted the n-word in explaining the history of lynching.” Presumably you’d have to edit the song or video to bleep out the word—bleep it out not for the sake of small children, but for the sake of adult university students.

It’s as if the Stanford Undergraduate Senate decided that, to protect Holocaust survivors and their children or grandchildren (perhaps now, or perhaps in 1960, when there was an ever closer connection between some students and the Holocaust), all swastikas in photographs, on maps, or in movies had to be fuzzed out, and when talking about death camps, you’d have to say “Au-place” and “Tre-place” (at least unless you were Jewish). Are swastikas offensive? Of course. Can seeing them be upsetting to people for whom the Nazi reign of terror hit close to home? Sure. But it seems to me that American universities should show and talk about history as it is, without fuzzing or bleeping or expurgating. Likewise for showing and talking about film, music, literature, and legal disputes.

from Latest – Reason.com https://ift.tt/2Nc7S0B

via IFTTT

From the Senate resolution, which came out about a month ago, but which I only learned about several days ago (underlining added to note some key phrases):

WHEREAS on April 28th, 2020 in the course titled “Introduction to Comparative Studies in Race and Ethnicity,” Professor Rose Salseda was invited to teach and said, “nigga,” while reciting lyrics to the 1988 classic by N.W.A., “Fuck tha Police;” and

WHEREAS on May 4th, 2020, in the course titled “Riot!: Visualizing Civil Unrest in the 20th and 21st Centuries” Professor Salseda wrote “Niggaz” twice while writing the full name of the group N.W.A and discussing their artwork, and …

WHEREAS use of the n-word by a White person or Non-Black person of color is offensive and highly inappropriate, especially in courses whose teachings intend to value and center Black liberation; and

WHEREAS this is not the first incident of racial violence against Black students in which a non-Black lecturer has employed and said the n-word while teaching, but hopefully will be the last; …

THEREFORE BE IT BE RESOLVED BY THE UNDERGRADUATE SENATE

THAT the Undergraduate Senate is appalled by and condemns Professor Rose Salseda’s continuous aggressions against the Black community and Black students, particularly her repeated use of the n-word in Canvas discussion board communications on May 4th, 2020. Reckless actions of this manner and Salseda’s disturbing presence teaching Black art and art history in our intellectual community must be dealt with….

THAT the Undergraduate Senate calls for the Center for Comparative Studies in Race and Ethnicity to reconsider what courses Professor Rose Salseda can teach (i.e Introduction to African-American Art), bring her back to Introduction to CSRE to listen / fully take ownership of her actions, participate in identity and cultural humility training ….

Prof. Salseda, an assistant professor, apologized; nearly everyone does, of course. What have things come to, though, that university professors (and surely also students) can’t accurately quote important music, literature, or film that they are discussing? (Unless, of course, they’re the right color.) Presumably Stanford professors discussing the lyrics would be required to say, “I don’t know if they fags or what / Search a n-word down, and grabbin’ his nuts.” (Or should it be “I don’t know if they f-words or what …”?) I wonder what the members of N.W.A. would think about that.

And of course you can’t simply play the song (or the movie, whether it’s To Kill a Mockingbird or Pulp Fiction or Godfather, Part II or The Shining or Rocky or Platoon or many others), as the UCLA Ajax Peris incident shows: He was faulted both for reading a passage with the word “nigger” from Martin Luther King, Jr.’s Letter from Birmingham Jail and for “show[ing] a portion of a documentary which included graphic images and descriptions of lynching, with a narrator who quoted the n-word in explaining the history of lynching.” Presumably you’d have to edit the song or video to bleep out the word—bleep it out not for the sake of small children, but for the sake of adult university students.

It’s as if the Stanford Undergraduate Senate decided that, to protect Holocaust survivors and their children or grandchildren (perhaps now, or perhaps in 1960, when there was an ever closer connection between some students and the Holocaust), all swastikas in photographs, on maps, or in movies had to be fuzzed out, and when talking about death camps, you’d have to say “Au-place” and “Tre-place” (at least unless you were Jewish). Are swastikas offensive? Of course. Can seeing them be upsetting to people for whom the Nazi reign of terror hit close to home? Sure. But it seems to me that American universities should show and talk about history as it is, without fuzzing or bleeping or expurgating. Likewise for showing and talking about film, music, literature, and legal disputes.

from Latest – Reason.com https://ift.tt/2Nc7S0B

via IFTTT

“I’m not ready for Monday – I’m going back to sleep..” (She-who-is-Mrs-Blain, this morning.)

I understand the supply of high-quality recreational pharmaceuticals is fairly limited at present, so if anyone can send me a quarter ounce of whatever Morgan Stanley are smoking I would be profoundly grateful. Apparently the global economy is in a new expansion cycle, and we will surpass pre-coronavirus GDP before the end of this year in a V-Shaped Recovery, say my American former employers (many years ago..) Excellent!

Sadly, no one seems to be sharing Morgan Stanley’s particular bullish insight with the market – which is setting up this morning for a “bit of a tanking” and a third consecutive down day. Markets are going to remain… fraxious… for the next few days. Volatile, risk off and expect to see the bad news mount…

Hard Hats at the ready…

There are two big forces dominating market levels at present:

1) Short-term reactions: the daily news blurb primes the market to make a binary flip between Risk On/Risk Off days – RoRo as some are calling it. The buttons being pressed include the daily threats on new virus hotspots from Brazil, Beijing and Texas, second waves, US authorities warning they will keep borders closed, negative nellies on the TV, and general exhaustion with the news flow. For instance, who cares if Larry Kudlow said Jay Powel was too ”morose”, although he did say US unemployment could remain above 8%.

2) The Global Central Bank Put – how can markets head lower when the authorities simply can’t afford for it happen? It’s a free option, knowing they will intervene with another flood of liquidity and bailouts – if they can get their act together.

These two forces are essentially balancing each other. The danger is it turns chaotic. It feels like it might happen….

The short-term reactive news, and central bank promises, don’t address the real long-term threat issues to the global economy, which include:

Growing Civil Unrest and rising dissatisfaction with governments.

The rising number of bankruptcies.

Companies, like BP this morning, raising provisions and scaling back investment.

Growing geopolitical tension.

Politics – the outlook for the US November elections has swung away from Trump – causing conniptions across C-Suites!

Disincentives to save as returns crash to zero.

Rising unemployment, growing corporate insolvency threats and a rising sense of wobble.

The market’s extreme detachment from the dismal underlying economic reality has become a major force in itself. The wider it is, the greater the prospect of a major shock/correction if it’s seen to be reversing.

Good luck to the UK this morning as shops reopen –I expect “shopping with confidence” will prove underwhelming, and yet another gaff by our flolloping and accident-prone premier, Boris Johnson.

And then there is the Coronavirus itself. Lockdowns are breaking down. Everyone wants normality. Whatever we think about the apparently reduced threat – it’s not going to magically vanish. Get used to it. It remains a very real threat from top to bottom of the global economy:

It’s going to change the way people shop, work and travel.

It’s going to change government policy – especially in terms of intervention in markets and commerce.

It’s going to change corporate behaviours.

I would guess that by this stage we all know someone who has spent considerable time in hospital with Covid-19. They are now in recovery, but have profound and ongoing medical issues. It’s increasingly clear we still don’t know enough about the virus. Over the weekend I was reading about how it seems to be more a vascular viral infection than an evolved flu. If you get it bad it’s taking out organs, triggering strokes and heart-attacks through blood clots. It requires new treatments.

More than ever, I’m convinced Health and Pharma are areas for investment. The virus could prove a dominant economic theme through this decade. I also fear the vaccine could well be delayed if we discover we’re addressing the wrong symptoms rather than the cause. (Virus hopes are another new-factor fuelling delusional V-Shaped recovery hopes.)

Then there is the bond market. In bonds there is truth. Or at least there used to be. Today bond yields have been depressed to such artificially low rates as to be meaningless. But the key attribute of bond yields is relative value – they set the return rate across financial assets. Ultra-low rates force investors to take greater risk in return for decreasing yields. Which is now illustrated by the amount of money chasing stocks – which are making lower profits and going to pay lower dividends.

When rates are this low and returns are crashing… well… I’m just not very happy to be thinking my pension pot is now going to be paying me pennies, but I will still be taxed to infinity to pay gold-plated final salary pensions to Civil Servants and such. This picture is not getting any better…

The big debates in bonds boil down to sovereign credit. The ability of governments to freely bailout insolvent companies, create jobs through fiscal infrastructure spending and pay rising social security costs is a function of their ability to raise money from the market. Traditionally that’s a function of the credibility of the country – not a problem for the dollar, but a massive problem for Italy.

As countries lose credibility and their ratings and currencies slide – can they bear the costs of the virus? If you believe in the magic of Modern Monetary Theory – that countries can effectively digitalise unlimited money with zero side effects… Phew.. we should be alright. If not.. then back to the old rules; the conventional Reinhart/Rogoff wisdom says sell any country with a debt/gdp ratio higher than 90%.

Am I too late to move to New Zealand?

via ZeroHedge News https://ift.tt/2AsX6QP Tyler Durden

“Just A Huge Bear Market Rally?” Stocks Tumble On Fears Of Second Virus Wave Tyler Durden

Mon, 06/15/2020 – 08:03

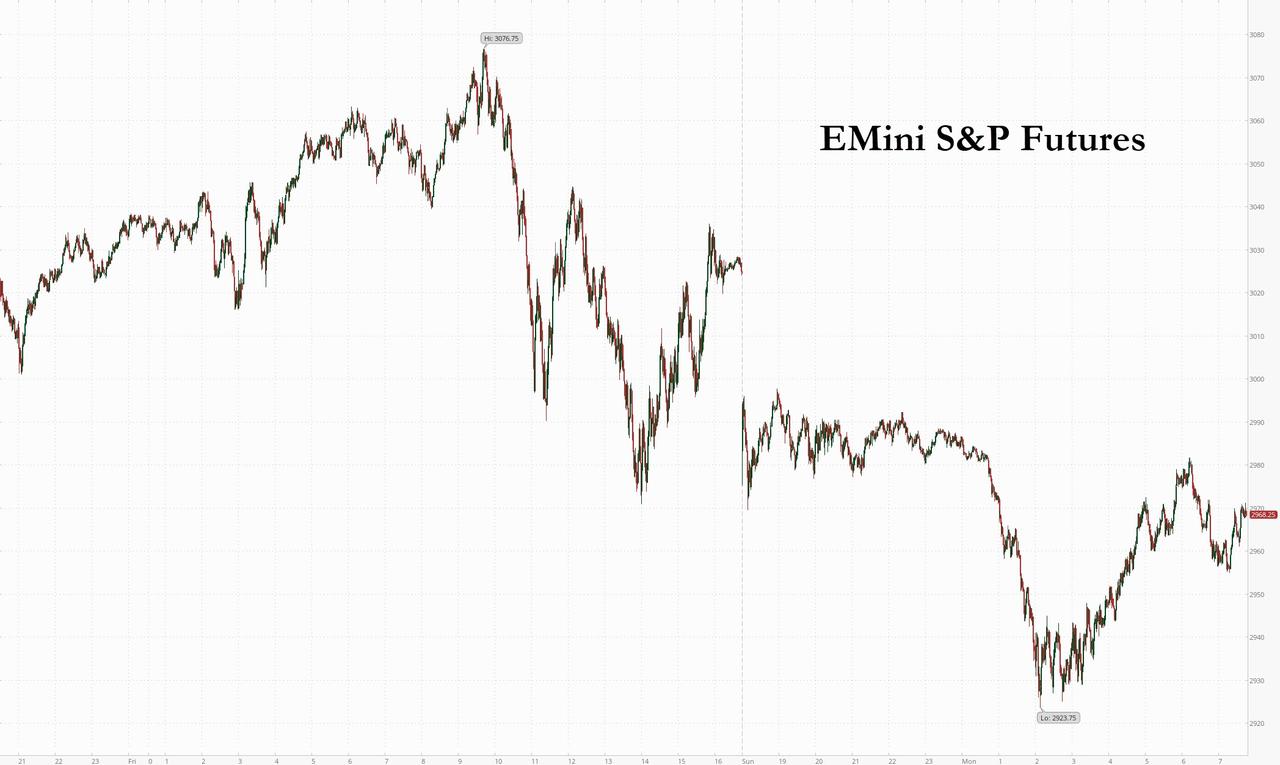

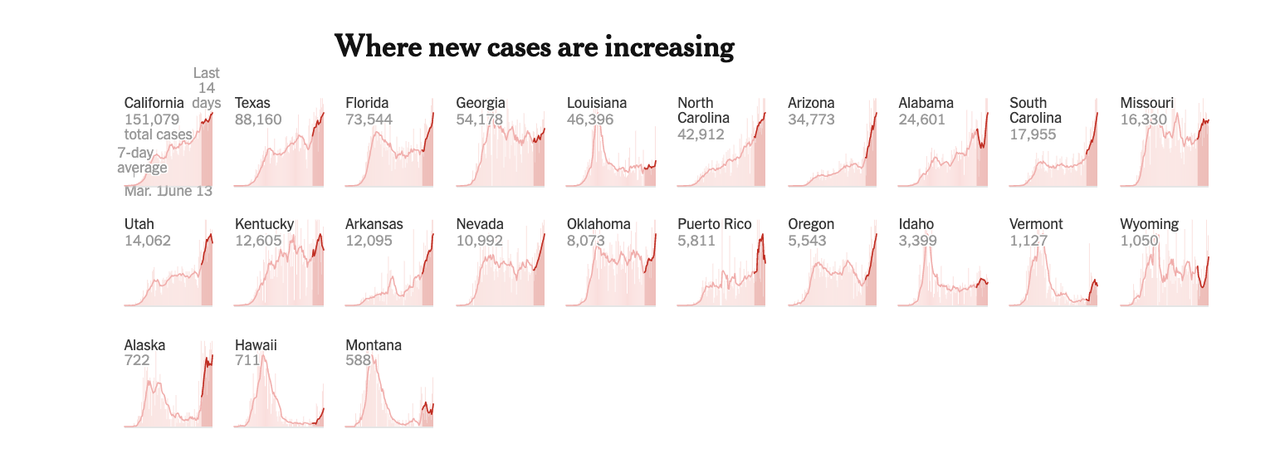

In a continuation of the selloff that started overnight, US equity futures and world stocks are plunging on Monday on signs that a second wave of the pandemic is emerging in parts of the United States and China, dousing investor hopes of a quick economic rebound that had powered the Nasdaq to record levels last week. Beijing closed the city’s largest fruit and vegetable supply center and locked down nearby housing districts after dozens of people associated with the market tested positive for the virus. A record number of new infections and hospitalizations were reported in more U.S. states, including Florida and Texas over the weekend.

After dropping as much as 1,000 points, Dow futures were down about 600 points at last check, with S&P futures dropping as much as 3.4% in early London trading in what some have dubbed “Meltdown Monday”, although S&P 500 futures managed to trim their losses in half, last down about 1.6%.

Travel stocks which were hit hard as passenger numbers dwindled due to travel restrictions, slumped on Monday with retail favorites such as United Airlines Holdings Inc, American Airlines Group, Carnival Corp, Norwegian Cruise Line Holdings Ltd and Royal Caribbean Cruises Ltd down between 5.1% and 7.4% in premarket trading. Stocks from economically-sensitive sectors including financials and energy also lost ground. U.S. lenders Bank of America, Citigroup and Morgan Stanley dropped 3.1% to 4%. Oil majors Exxon Mobil and Chevron shed 2.8% and 1.5% respectively. The VIX index jumped to its highest level since April 22 at 44.44 points.

In Europe, cash equities steadied after an opening slump of as much as 3%, with miners, travel and tech stocks weighing, while rising health-care shares blunted the retreat across markets. BP Plc slumped as the British oil major predicted the pandemic will hurt long-term energy demand. Travel and Leisures stocks were hit hard: travel operator TUI and caterer Sodexo led declines in Europe’s travel and leisure stocks after analyst downgrades and amid signs of a second coronavirus wave eroding hopes for a quick recovery for the tourism, leisure and travel industries. Europe’s Stoxx 600 Travel & Leisure Index down 2.6% at 9:42 a.m. in London, the region’s second-worst performing sector on Monday. Airlines also declined, led by flagship carriers Lufthansa (-3.8%), which was downgraded to sell at Redburn, and Air France-KLM‘s 2.9% slide after being cut to sell at Redburn.

Asian stocks also fell, led by industrials and IT. All markets in the region were down, with South Korea’s Kospi Index dropping 4.8% and Singapore’s Straits Times Index falling 2.7%. The Topix declined 2.5%, with W-Scope and Casa falling the most. The Shanghai Composite Index retreated 1%, with China Shenhua and Jiangsu Luokai Mechanical & Electrical posting the biggest slides. Emerging-market stocks headed for their biggest drop in more than three weeks.

After a fierce rally sent global equities close to their pre-pandemic levels, sentiment in markets is starting to sour. In China, a string of top-tier data all missed expectations, and while consumer spending and investment continued to improve in May, there are few signs of a broad-based rebound needed to spur a V-shaped recovery.

“Any further sell off from here will likely see some larger unwinds of the more price and momentum driven investment styles,” said James Athey, a money manger at Aberdeen Standard Investments. “People will then start openly asking the question again, ‘Was that just a huge bear market rally?’”

In rates, US Treasury yelds are richer by 1bp to 5bp across the curve, 10-year by 3.6bp at 0.666%, with long-end-led gains flattening 2s10s by ~2bp, 5s30s by ~3bp. Bunds are cheaper by 2bp vs Treasuries while Spain notably outperforms after Fitch affirmed its sovereign rating at A- with a stable outlook Friday. During the Asia session, gains were pared after a block sale of 10-year futures near the highs.

In FX, the dollar rose versus most Group-of-10 peers. Risk aversion saw commodity currencies like the Australian dollar lead losses versus the greenback, after a jump in new coronavirus cases in Beijing, Tokyo and more than 20 U.S. states raised fears of a resurgence of the pandemic. All developing-nation currencies, except for Taiwan’s dollar, were weaker in early as the dollar climbed and U.S. stock index futures fell. Implied currency volatility climbed for a third day while spreads on dollar bonds widened as investors shunned riskier assets

Elsewhere, bitcoin dropped below $9,000 for the first time since May. Commodities also retreated, with gold, oil and copper all lower.

Expected data include the Empire State manufacturing survey and the latest TIC data.

Market Snapshot

S&P 500 futures down 2.1% to 2,970.50

STOXX Europe 600 down 1.6% to 348.56

MXAP down 2.4% to 153.32

MXAPJ down 2.2% to 494.07

Nikkei down 3.5% to 21,530.95

Topix down 2.5% to 1,530.78

Hang Seng Index down 2.2% to 23,776.95

Shanghai Composite down 1% to 2,890.03

Sensex down 1.6% to 33,257.89

Australia S&P/ASX 200 down 2.2% to 5,719.80

Kospi down 4.8% to 2,030.82

German 10Y yield fell 1.5 bps to -0.454%

Euro down 0.01% to $1.1255

Italian 10Y yield fell 5.2 bps to 1.318%

Spanish 10Y yield fell 2.2 bps to 0.572%

Brent futures down 0.8% to $38.42/bbl

Gold spot down 0.5% to $1,722.53

U.S. Dollar Index down 0.2% to 97.16

Top Overnight News from Bloomberg

Beijing shuttered the city’s largest fruit and vegetable supply center and locked down nearby housing districts as dozens of people associated with the wholesale market tested positive

The fragile recovery in China’s economy is pointing to a long road back for the rest of the world too

The European Union fired a warning shot at China over its global trade ambitions with an unprecedented tariff decision to counter Chinese subsidies to exporters

British Prime Minister Boris Johnson will step back into the Brexit fray on Monday as he holds talks with the European Union’s top officials, with both sides looking to reset negotiations that have drifted into stalemate

Asian equity markets traded negative and US equity futures also began the week on the backfoot in which the E-Mini S&P gapped below its 200DMA (3011.20) and the key 3000 focal point, with investor sentiment weighed by coronavirus second wave fears after several US states recently suffered a record number of additional cases including 2 of the 4 largest populated states – California and Florida. ASX 200 (-2.1%) and Nikkei 225 (-3.5%) declined at the open amid the downbeat tone although losses in Australia were briefly reversed amid resilience in tech and with authorities planning to fast track infrastructure projects valued over AUD 72bln to speed up the recovery, while exporter sentiment in Tokyo was dragged by unfavourable currency effects. Hang Seng (-2.1%) and Shanghai Comp. (-1.0%) were subdued after an outbreak prompted a lockdown of some areas in Beijing and following disappointing activity data in which Chinese Industrial Production and Retail Sales both missed expectations, but with pressure in the mainland cushioned after the PBoC conducted a CNY 200bln MLF operation. Finally, 10yr JGBs were relatively flat with prices only marginally benefitting from the weakness in stocks as participants also digested the inline-to-soft enhanced liquidity auction results for longer-dated JGBs and with the BoJ kicking off its 2-day policy meeting.

Top Asian News

Beijing Outbreak Grows to Nearly 100 Cases in Test For China

China’s Recovery Continues But Wary Consumers Show Vulnerability

Turkey Showcases Air Power in Region With Major Attack in Iraq

Warburg Pincus-Backed Group Is Said to Near 58.com Buyout Deal

Europe kicks the week off with sizeable losses [Euro Stoxx 50 -1.2%], albeit well off worst levels, as the region conformed to the global risk aversion amid growing fears of a second wave – with Beijing now seemingly the epicenter of a second outbreak, whilst several US states including Alaska, Arizona, Arkansas, California, Florida, North Carolina, Oklahoma and South Carolina all experienced a record increase in coronavirus cases during the past 3 days. Bourse have drifted off worst levels as the session is underway, potentially due to short covering, but nonetheless remain in firm negative territory. Sectors are predominantly in the red and post an anti-cyclical performance, with energy recouping some losses but still retaining its spot as the laggard whilst healthcare names fare the best, marginally into positive territory. The detailed breakdown pains a similar picture, with Travel & Leisure one of the worst performers amid fears of further sectoral disruption. In terms of individual movers and shakers – BP (-3.5%) shares are pressured (alongside lower oil prices) as it anticipates Q2 charges of USD 13-17.5bln. Additionally, the group are cutting their long-term price assumptions as part of a review of development plans. Meanwhile, Commerzbank (-1.0%) reportedly rejected Cerberus’ demands for two seats on the supervisory board, according to sources; subsequently, Cerberus reportedly said they expected this to happen and will announce next steps in due course. On the flip side, AstraZeneca (+1.0%) are buoyed amid comments from Italy’s Health Minister who stated that Italy, Germany, France & Netherlands have signed a contract for 400mln doses of a COVID-19 vaccine – Co. CEO said the group will know by the end of Summer if a working vaccine is viable.

Top European News

Johnson Returns to Brexit in Bid to Reboot Faltering Talks

Johnson Tells Brits to ‘Shop With Confidence’ as Shops Open

Immofinanz Seeks to Increase Capital by ~25% with Shares, Notes

Danske Reallocates Roles and Cuts Jobs in Work-From-Home Push

In FX, the Dollar has retained some safe-haven allure alongside Gold and the Yen as 2nd wave coronavirus concerns spark another bout of broad risk aversion, with the DXY holding above 97.000 and well off mtd lows just under 96.000. However, the Greenback is still tussling with bullion and the Jpy given new outbreaks of COVID-19 across several US states and eight seeing a record rise in the number of cases over the last 3 days. Hence, Xau/Usd looks underpinned around the 10 DMA (Usd 1715/oz) and Usd/Jpy appears capped ahead of 107.60, albeit also mindful of decent option expiry interest between 107.20-15 (1.1 bn).

NOK/AUD/CAD – Another downturn in crude prices and a further deterioration in Norway’s trade balance has undermined the Crown, while the Aussie is weaker in wake of Chinese ip and retail sales missing consensus to offset latest fiscal initiatives to support the economy via infrastructure spending. Meanwhile, the Loonie is also tracking oil down ahead of Canadian manufacturing sales, with Eur/Nok elevated within a 11.0187-10.8561 range, Aud/Usd pivoting 0.6800 and Usd/Cad firmly above 1.3600. Ahead, a big week for the Aussie kicks off with RBA minutes tomorrow and culminates in jobs data and retail sales on Thursday and Friday respectively.

NZD/SEK – Also on the back foot, but the Kiwi benefiting to a degree from favourable Aud/Nzd cross flows towards the bottom of 1.0644-1.0583 parameters and the Swedish Krona holding up better than its Scandinavian counterpart by the same token, as Nzd/Usd sits more comfortably on the 0.6400 handle and Eur/Sek in a tighter 10.5835-5070 band.

CHF/EUR/GBP – All pretty flat with the Franc near the middle of 0.9500-50 extremes vs the Buck and even tighter against the Euro between 1.0730-1.0695 after more deflationary Swiss data (import/producer prices) and latest sight deposits showing a big rise in domestic bank accounts in the run up to Thursday’s SNB policy review. Elsewhere, Eur/Usd seems constrained by 1.1225/30 bids and 1.1270 offers, 1.1270 with 1.5 bn option expiries at 1.1260 also keeping the headline pair in check, while Cable has reclaimed 1.2500+ status and Eur/Gbp is back under 0.9000 amidst reports of demand for Sterling via the cross before attention turns to UK PM Johnson’s Brexit call with EC President von der Leyen at 13.30BST.

EM – Widespread declines on the lack of risk appetite, but especially for the Rub, Mxn, and Zar, while the Try is under pressure following Turkey’s airstrikes on PKK targets in Northern Iraq.

In commodities, WTI and Brent front-month futures bear the brunt of the overall risk aversion coupled with demand woes emanating from the resurgence in COVID-19 cases in the US and in Beijing. WTI has since reclaimed the 35/bbl handle (vs. 36.12/bbl high) as has Brent for the USD 38/bbl figure (vs. 38.80 high); as newsflow slows and prices grind higher ahead of US’ entrance. The week could prove to be a volatile period, barring COVID-headlines, the monthly OPEC and IEA oil market reports are due later this week, whilst the JMMC meeting will be underway on the 18th June. The committee will review secondary source data alongside current market fundamentals before proposing policy recommendations. Sources last week said that OPEC+ is to move cautiously to rebalance the market amid easing lockdowns, while anticipated Shale resumptions could also weigh on eastern producers’ minds. Participants may give less credence to the oil market reports as the prospect of rising cases could prove the reports stale. Moving to metals where, spot gold trades lacklustre around USD 1720/oz (vs. 1735 high), as the yellow metal decouples from its safe-haven properties amid early USD strength, although as the Dollar recedes, gold is seemingly weighed on by investors potentially on the sidelines as they observe the state of play. Copper prices have been moving broadly with the risk aversion. Reports noted that CME May copper volumes slid 40%, whilst LME volumes fell 26% as funds fled from high volatility amid the pandemic. Meanwhile, Dalian iron ore futures remained steady despite the second wave-woes amid falling stockpiles of the raw material.

US Event Calendar

8:30am: Empire Manufacturing, est. -30, prior -48.5

4pm: Net Long-term TIC Flows, prior $112.6b deficit

DB’s Jim Reid concludes the overnight wrap

Patient zero in the U.K. was not in my household after all as my wife tested negative for Covid antibodies over the weekend. It must have been the worst flu ever over Xmas then.

New virus cases continue to bubble up in certain parts of the world and we again include our full Covid case and fatality tables in the full report – including the four most troublesome US states at the moment. There were Sunday headlines of China seeing the largest increase in new cases since April and a very localised lockdown around a market in Beijing. However at 57 new cases reported in a country of 1.4 billion people we have to put this into some perspective. This rounded up the 1-day new case growth to 0.1% after 62 days of 0.0% growth. A further 49 cases have been reported overnight with Beijing shutting down housing districts in and around the market in focus.

Meanwhile, the US is still struggling to reduce daily new case growth below 1% as all of Western Europe have. The most problematic states continue to be California, Texas, Florida and Arizona. Over the weekend these 4 states were responsible for over 16,500 new cases, or roughly 37% of the total new cases in the US. The first three are the largest states in the US so it is a worry that cases continue to rise nearly 3 months into the pandemic. Weekend reporting issues might be an issue but the 7 day average rise in daily cases in California and Texas is 2.2% currently, the same as a week ago in California and down slightly in Texas from 2.4%. Arizona and Florida are more worrisome. Arizonian cases rose by 4.5% in the last week on average, up from 4.1% the week prior, while Florida saw cases rose by 2.3% on average up from 1.8% in the period before. Rtlive’s estimates of effective transmission rates, Rt, show Arizona at the highest currently in the US at 1.18. California is now estimated at 1.0 after being slightly under a few days back, indicating that efforts to reopen may be raising the risk of transmission. Overall 16 of the 50 states are now estimated to have an Rt value over 1, while only 9 states have the entire confidence interval of their Rt values under 1.

At DB, we’ve had a lot of internal debate about whether the piecemeal, lack of centrally planned US approach to fighting this virus will eventually be worse for growth than the more synchronised and more thorough lockdown approach of Europe. My personal view is that whilst the latter looks very effective on paper, the fact that more of the US economy has remained open for longer means they’ll probably see a better short to medium term growth outlook. It’s hotly debated here though. The other thing to comment on around the four highest virus growth US states is that death rates still remain relatively low in them as you’ll see in our tables. Overall, it’s possible that globally we are now shielding the vulnerable better and that even if we do see a second wave it might not be as deadly as the first. Anyway, expect the market to be obsessing about these states this week.

The worsening virus newsflow has seen most Asian markets start the week on the back foot. The Nikkei (-0.98%), Hang Seng (-0.62%), Kospi (-0.58%) and ASX (-0.73%) are all down as we go to print. Moves for Chinese bourses have been more muted following the data (more on the shortly). In FX, the Japanese yen is up +0.21% amidst the risk off. Meanwhile, yields on 10y USTs are down -4bps to 0.665% and futures on the S&P 500 are down -1.22%. Elsewhere, WTI oil is down -2.84% to $35.23.

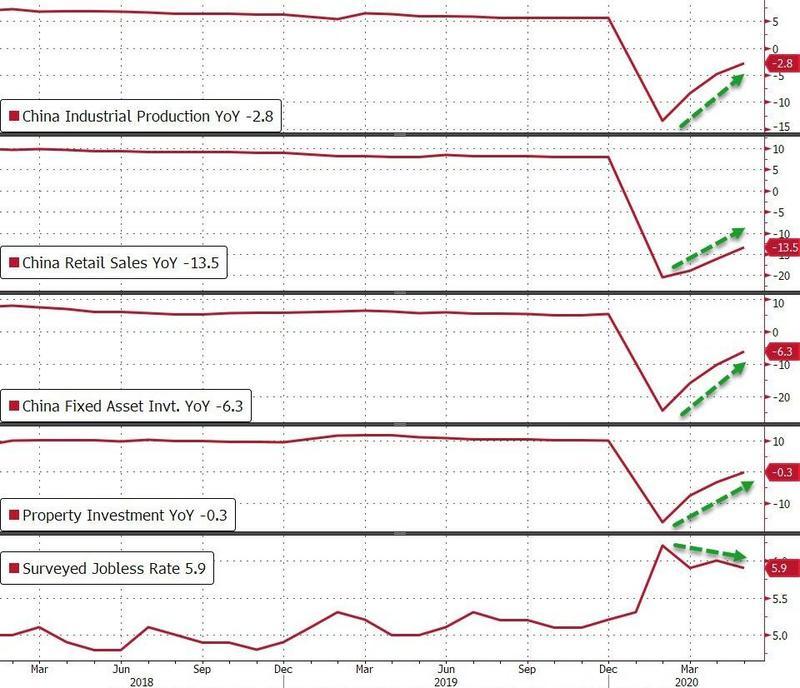

In terms of that data, China’s activity data for May did suggest an improving growth outlook albeit slightly disappointing relative to expectations. Industrial production rose to +4.4% yoy (vs. +5.0% yoy expected and +3.9% yoy last month) while retail sales rose to -2.8% yoy (vs. -2.3% yoy expected and -7.5% yoy last month) and YtD fixed asset investments ex rural printed at -6.3% yoy (vs. -6.0% yoy expected). Finally the surveyed jobless rate in May came in line with expectations at 5.9%.

In other weekend news, US infectious disease expert Anthony Fauci suggested that bans on travel to the US may remain until a vaccine arrives. Elsewhere, Italian news daily La Repubblica noted over the weekend that the Italian government may request up to EUR 36bn in credit lines linked to the ESM by the end of July. The report added that PM Conte has received preliminary approval from Foreign Minister Luigi Di Maio of the Five Star movement, which has been against tapping the fund and said that Italy would aim to request an ESM loan along with other EU members including Spain and Portugal.

In terms of this week, central banks will feature highly on the agenda, with decisions from the Bank of Japan (tomorrow), the Bank of England (Thursday) and a number of others, while Fed Chair Powell will also be testifying before Congress (tomorrow and Wednesday). Elsewhere, European politics will be in focus, with a European Council meeting taking place on Friday where the recovery fund will be discussed, as well as talks between Prime Minister Johnson and EU leaders on today about their future relationship. Meanwhile we’ll get an increasing number of hard data releases for May, offering further insight into how different economies have fared as various lockdown measures have been eased.

Starting with central banks while the BoJ (tomorrow) is likely to see no policy change, the Bank of England (Thursday) are expected by DB to ramp up QE by a further £125bn with more QE likely over the course of the year. Their decision comes against the backdrop of Friday’s data showing UK GDP contracting by -20.4% in April, following its -5.8% decline in March, and with the country still only slowly easing lockdown restrictions.

Another central bank highlight will be Fed Chair Powell’s appearances before the Senate Banking Committee tomorrow and the House Financial Services Committee on Wednesday. He’ll be delivering a testimony as part of the semiannual Monetary Policy Report that’s submitted to Congress. It’ll be interesting to hear what he has to say on the outlook and how he sees the recovery progressing given his remarks in the most recent press conference that “we’re not thinking about thinking about raising rates”. So close to last week’s FOMC there is unlikely to be much new news but his tone will be closely watched as many in the market have criticised his downbeat nature at last week’s press conference. Rightly or wrongly, markets like a bit of sparkle from their central bank leaders and didn’t feel they got enough last week. Finally, central banks elsewhere will also be making a number of decisions next week, including in Switzerland, Norway, Indonesia, Russia and Brazil.

At the end of the week, the European Council summit on Friday will be of particular importance, with EU leaders due to discuss the recovery fund to deal with covid-19, along with the EU’s new long-term budget. Last month, Commission President von der Leyen presented a proposal for a €750bn recovery fund, which would include a mixture of grants and loans to member states. As part of this, the Commission would borrow from markets on behalf of the EU. However, the plans would require unanimity among the member states, and there are differences of views between them, not least on the extent to which the fund should be balanced between grants and loans. However, talks on the issue are expected to keep going into July, when Germany will take over the rotating EU Presidency.

Staying on European politics, and Brexit will return to the headlines as a high-level meeting between UK Prime Minister Johnson and the Presidents of the European Commission, Council and Parliament takes place by video conference this afternoon. The two sides have now agreed to an intensified timetable for negotiations on a free-trade agreement, with talks in each of the 5 weeks from the week commencing 29 June to the week commencing 27 July. The question will be whether today’s high-level talks can provide fresh impetus for the negotiations.

On the data front, it isn’t a particularly eventful week. The US will be releasing more hard data for May, with retail sales, industrial production and capacity utilisation figures coming out tomorrow, before housing starts and building permits for May are released on Wednesday. Our economists believe the trough of activity was in early May where their tracker showed YoY growth of -11%. It’s now around -9%. Moving across the Atlantic, here in the UK, this week sees inflation, retail sales and unemployment data released. For more on the rest of the week’s calendar see the day by day week ahead at the end.

Looking back at last week now, global equity markets in the US and Europe fell the most since the worst days of this covid-19 crisis. While Fed Chair Jerome Powell indicated midweek that the Fed would continue to use its tools to support the US recovery, the central bank’s bleak long term forecast and rising virus cases in the largest US states caused a reversal in investor risk sentiment. The S&P 500 (+1.31% Friday) nearly erased all of the previous week’s gains, falling -4.78% on the week, with the largest one-day fall coming on Thursday (-5.89%). The tech-focused NASDAQ went back to outperforming the S&P after two weeks of lagging the broader index, down “just” -2.30% over the 5 days (+1.01% Friday). For both the S&P 500 and the NASDAQ it was the worst weekly performance since the height of the crisis in the week ending 20 March. European equities fell even more on the week as the cyclical-over-growth outperformance trade of the past 1-2 weeks unwound. Banks were at the forefront of this on both sides of the Atlantic – US Bank stocks fell -11.17% while European Banks fell -9.76%. The Stoxx 600 as a whole fell -5.66% (+0.28% Friday) over the five days. The DAX was down -6.99% (-0.18% Friday), while the CAC fell -6.90% (+0.49% Friday), the IBEX retreated -7.37% (+0.20% Friday), and the FTSE MIB dropped -6.44% (+0.43% Friday). Asian indices did not fall as much, with the Nikkei down -2.44% over the week (-0.75% Friday) while the CSI 300 was largely unchanged at +0.05% (+0.18% Friday), and the Kospi fell -2.27% (-2.04% Friday).

With worries of a protracted first wave or potential second wave dampening economic activity, oil fell for the first week since late April. While OPEC+ agreed to extend production cuts at the start of the week, the global demand picture has not materially improved yet. And on a week where risk assets repriced the risks around reopening the economy, the commodity traded sharply lower. WTI futures fell -8.32% (-0.22% Friday) to $36.26/barrel and Brent crude retreated -8.44% on the week (+0.47% Friday) to $38.73/barrel.

As risk assets traded lower and volatility spiked, credit spreads both in the US and Europe widened on the week. European HY cash spreads were +44bps wider on the week (unchanged Friday), while European IG spreads were +13bps wider (+1bp Friday). US HY cash spreads were +78bps wider (-12bps Friday), while IG widened +9bps on the week (-1bp Friday).

Peripheral debt widened across the board as well, with Spanish 10yr yields +19.9bps wider to German bunds over the week, while Italian BTPs were +19.7bps wider, Greek 10yr yields widened less at +8.6bps, and Portuguese bonds widened +19.4bps. With risk assets falling sharply toward the end of the week, core sovereign bonds rallied with US 10yr Treasury yields falling -19.2bps (+3.4bps Friday) to finish at 0.703%, while 10yr Bund yields fell -16.2bps over the course of the week (-2.5bps Friday) to -0.44%. With yields lower and investors seeking havens, Gold rise +2.71% on the week (+0.18% Friday). The largest one week move for the metal since late April.

Economic data on Friday continued to show the economic hardship brought on by the coronavirus, with Euro Area industrial production falling by -17.1% in April, following its -11.9% decline in March. In the US, the University of Michigan consumer sentiment survey bounced back 6.6pts to 78.9 (vs. 75 expected), which is still near 7 year lows.

via ZeroHedge News https://ift.tt/3hrXoI9 Tyler Durden

Virus Resurgence A Match For Liquidity? Tyler Durden

Mon, 06/15/2020 – 07:29

Submitted by Eleanor Creagh, Australian Market Strategist at Saxo Bank

Summary: Following the relentless run up in risky assets off the March lows, we are seeing 2-way price action return to the market. USD strength is resuming as risk sentiment sours and gravity is visible once again in risk assets.

Last week’s price action underscored that despite the aggressive rebound off March lows, a degree of fragility remains. Of course, markets are all about 2-way price action and it is fair to say, prior to last week’s sell off, price action had been very one-sided, with sentiment and positioning reaching extremes. Bankrupt companies were flying, the put-call ratio was close to 10-year lows and sports betters were morphing into fully-fledged portfolio managers. Speculation was rife and complacency a foot.

However, the pullback we saw on Thursday, although warranted given extremes in positioning, revealed more than just the extreme speculation driving markets higher in recent weeks. The realized move in the S&P 500 was far greater than the implied daily move in the S&P 500 from the VIX index. Here, there are a number of conclusions we can draw:

We know markets are not normally distributed in any case, but last week’s 4 standard deviation move in the S&P 500 confirms active fat tail risk is in play

Despite meeting the technical definition of a bull market (20% off lows), price action is not characteristic of a secular bull market, revealing an underlying fragility

However, these are unusual and uncertain times. We know that fundamentals are wildly disconnected from market pricing, something my colleagues and myself have discussed at length in recent weeks. However, does that mean we are ready to call time on the liquidity induced mania revealed in recent weeks.

At this stage we would argue that although fundamentals will eventually trump liquidity, the liquidity driven narrative has proved strong and tough to break, particularly as the lack of appealing alternatives and the expectation that rates will remain low for an extended period drives investors up the risk spectrum into equities (TINA). Conditioned by the central bank put to “buy the dip” these investors are reaching for yield and piling into risky assets (FOMO). The existence of this dynamic perversely dictates one need not be positive on the expectations of a swift economic recovery, to be long stocks (and by default short cash/efficient markets/price discovery). Post consolidation/retracement these factors are likely to remain key drivers of continued upside and will persist in lending an underlying support to risky assets.

As we said last Tuesday, prior to Thursdays sell off, for short-term traders, now is the time to tighten stops and book gains. We maintain this defensive stance on risk.

The news cycle has certainly turned for the worse and it is clear the world still has a COVID-19 problem.Fresh lockdowns in Beijing, an uncontrolled first wave in the US and EM’s (India, Peru, Brazil, Chile, Pakistan) struggling to control the pandemic locally corroborate a cautious stance. In Beijing, “The risk of virus spread is very high, and resolute and decisive measures are needed to prevent further spread,” vice premier Sun Chunlan said during a state council meeting on Sunday, as reported by state media.

Without a vaccine, as lockdowns are lifted a persistent and growing first wave presents a clear risk for a true second wave resuming in the Northern Hemisphere once colder weather remerges. This would be a real hurdle that extended valuations fail to reflect. These risks are now being more adequately considered, but for how long is the question. In the current paradigm, when the only bull market is in intervention, the cynic in me wonders how long until the newswire, “a vaccine is close” crosses!

via ZeroHedge News https://ift.tt/30MWccr Tyler Durden

Brazilian COVID-19 Death Toll Surpasses UK, China Blames Latest Outbreak On Imported Salmon: Live Updates Tyler Durden

Mon, 06/15/2020 – 06:51

Summary:

China blames outbreak on imported salmon

Official warns risk of resurgence is high

World nears 8 million case mark

Brazil surpasses UK death toll; now second only to US

23 US cases see new infections climb

UK allows many retailers to reopen for first time in 3 months

* * *

US equity futures initially broke below 3,000 last night after dozens of new coronavirus cases were reported in Beijing and Guangdong Province over the weekend. During a press briefing organized by China’s National Health Commission, Vice Premier Sun Chunlan spooked traders by claiming the risks for a resurgence of the coronavirus in Beijing were “high” due to the outbreak at the Xinfadi seafood market, billed as the largest wholesale market for seafood and meat in Asia. On Saturday, China reported 57 new infections, its largest resurgence in 2 months, before confirming dozens of additional cases on Sunday (remember, cases are always reported with a 24 hour delay).

40,000 Beijing residents are reportedly on lockdown, with at least half of the districts in Beijing reporting new cases. Officials in Beijing blamed flights from India and Bangladesh for carrying more infected individuals (some of them foreigners) to Guangdong, with 14 of the patients confirmed in the province flying from Bangladesh and three from India. Beijing’s warning about a “high” risk of resurgence follows a warning from Saturday when officials warned that the part of Beijing surrounding Xinfadi (situated in the southwestern part of the capital city) had assumed a “wartime posture”, as nearly a dozen neighborhoods were placed back on lockdown.

In total, some 80 new cases were reported in China over the weekend.

As we await the latest batch of infection data out of China, the Global Times reported Monday that the closure of Xinfadi “will impact seafood sales worldwide”, and as a result, sales of salmon had already been suspended across China after a sample of the virus was detected on a chopping board owned by a fishmonger selling imported salmon.

The linkage to the imported salmon and the national ban on salmon sales are, of course, bits of political theater to convince the Chinese people that new cases of the virus are tied to foreign sources. Here’s an excerpt from a Global Times editorial published Monday in China.

We must also admit that we still know little about COVID-19. Our knowledge is still limited about where the virus comes from, how it spreads and how COVID-19 patients should be treated.

This determines that when there are still many countries affected by the epidemic, it is impossible for China to completely eradicate the virus. The epidemic may break out from unexpected directions, and we must be able to withstand such situations and respond effectively. What happened in Beijing is very likely not the end of China’s domestic COVID-19 spread.

Moving on from China, we begin the week on the cusp of the latest grim milestone for the international outbreak: With the world still reporting roughly 100k new COVID-19 cases a day, with at least 40k of these coming from Latin America alone, the global tally passed 7.9 million mark Monday. And while roughly half of those, some 3.8 million, have already recovered, another 433,394 have succumbed to the deadly virus.

Yesterday, authorities in Tokyo confirmed they had uncovered the biggest cluster of cases in more than a month. Adding to the alarm, local TV news station FNN reported early Monday that another ~50 cases had been confirmed in Tokyo, the biggest jump since May 5, although the number is roughly equivalent to the number of cases confirmed over the weekend. Of these new cases, approximately 20 were linked to a popular nightlife district in the city.

Those who have been monitoring the rankings for countries with the highest number of COVID-19-linked fatalities might notice a change: As of Monday, Brazil has officially surpassed the UK total for COVID deaths, moving into second place behind only the US.

After its latest update on deaths and new confirmed cases last night, Brazil has counted 43.3k deaths since the outbreak began, and many on the ground have warned that this figure greatly underestimates the true number of deaths. Mexico has also been accused of undercounting fatalities in hotspots like Mexico City.

In the US, roughly half of the states are seeing new cases rise, many alongside hospitalizations. Texas has seen hospitalizations hit record highs, while Florida, NC, SC, Arizona, Nevada and many other states are seeing an increase in new cases reported daily.

Even Georgia, which was heralded for its ability to reopen aggressively without sparking a massive resurgence in new cases, has reported a discomfiting spike over the past few days, according to the NYT.

Meanwhile, as we noted last night, in New York, Gov Cuomo is threatening to shut down Manhattan and parts of the Hamptons if he keeps receiving complaints about COVID-19-related violations. In Tennessee, authorities in Nashville have cited a number of businesses for breaking social distancing rules, including one bar where patrons were packed in shoulder to shoulder.

{kind=link}

{kind=link}

{kind=link}