While the League remains the most popular political party in Italy, Emilia Romagna is part of the so-called “red belt” – a region of the country that for decades supported the Italian Communist Party (once the largest Communist Party in Europe) before moving to the center-left Democratic Party (or PD) after the fall of communism. Polls ahead of the vote showed that Borgonzoni and Bonaccini were running neck-and-neck, suggesting that the region might be the latest left-wing stalwart to embrace Salvini’s tough-on-immigration agenda. The League also triumphed in the region during the EU parliamentary elections in May, becoming the leading party with 34% of the vote to the PD’s 31%. And after Salvini led the League to an upset in Umbria three months ago, many observers bet that he would repeat that same feat.

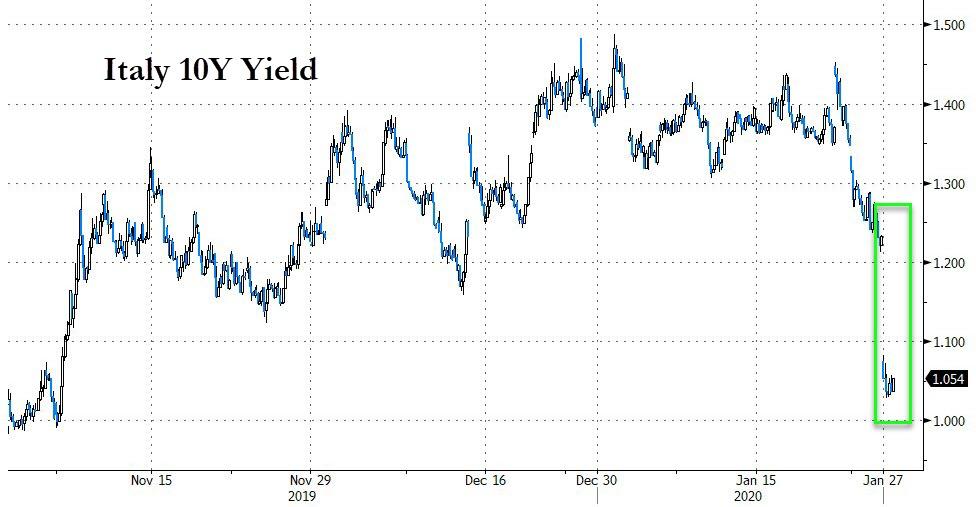

Italian government bonds (known as BTPs) rallied, compressing the spread with German bunds to its tightest level since November. Analysts claimed the risk of imminent collapse for the Italian government had abated – for now, at least.

“With the centre-left win in Emilia-Romagna, the risk of a government crisis in the short term has receded somewhat,” said analysts at Barclays in a note to investors. “Yet many hurdles persist: [among them] the future nature of the coalition with a fractured Five Star Movement, the thin majority in the Senate [and] the regional and referendum votes further into 2020.”

As one WSJ reporter pointed out, this is hardly the first time that fears of political instability led to a blowout in spreads, only for Italian bonds to rally on the big risk-off headline.

Here’s the Italian bond spread after Emilia-Romagna elections. At this point, I’m surprised nobody has set up a “Non-Eurozone Breakup Income Fund” that basically longs any significant widening in euro spreads. Works every time. pic.twitter.com/9oNlUzwosd

To be sure, tensions in Italy’s ruling coalition – between the center-left PD and anti-establishment Five Star Movement – remain tense, even after longtime M5S leader resigned from the leadership last week in a bid to save the coalition. Despite this, Goldman Sachs said it expects BTPs to outperform, seeing more room for yield compression between bunds and BTPs.

The 10-year BTP yield slid 16 basis points lower to 1.08% bringing the spread to the 10-year bund to 142 bps, the narrowest since Nov. 8 as the ruling coalition looks to stay in power until at least the first half of 2021.

But before you pile in to BTPs, the FT’s Tony Barber offers some food for thought: Though this loss was Salvini’s second political miscalculation in the last six months, “the overall political momentum” is still behind him. And the ruling coalition of former sworn enemies has been riddled with gridlock. The only thing they seem to agree on is that they don’t want Salvini to become prime minister.

When I was growing up, my father used to tell me I should “never take advice from anyone who hasn’t succeeded at what they are advising.”

The most truth of that statement is found in the financial press, which consists mostly of people writing articles and giving advice on topics where they have little experience, and in general, have achieved no success.

The best example came last week in an email quoting:

“You recently suggested that you took profits from your portfolios; however, I read an article saying retirees shouldn’t change their strategies. ‘If you’ve got a thoughtful financial plan and a diversified investment portfolio, the general rule is to leave everything alone.’”

This seems to be an entirely different approach to what you are suggesting. Also, since corrections can’t be predicted, it seems to make sense.”

One of the biggest reasons why investors consistently underperform over the long-term is due to flawed investment advice.

Let me explain.

Corrections & Bear Markets Matter

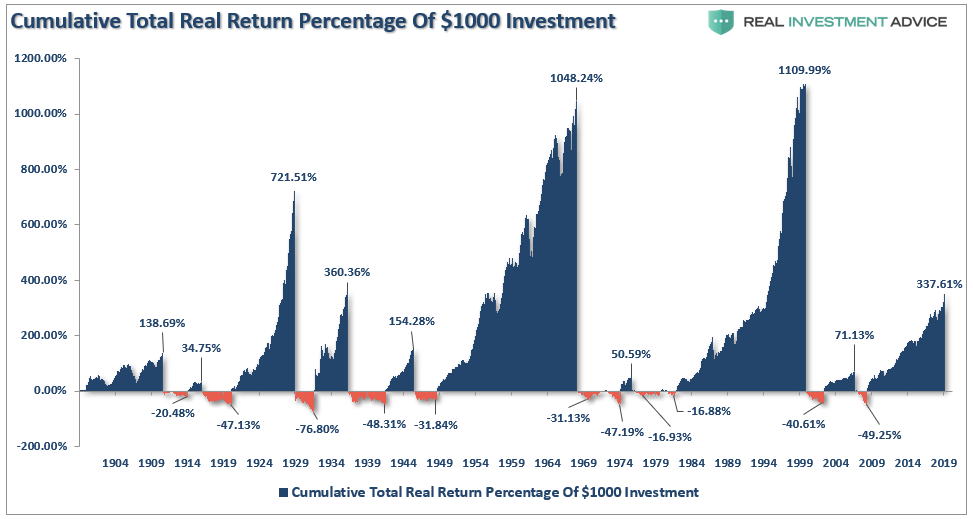

It certainly seems logical, by looking the 120-year chart of the market, that one should just stay invested regardless of what happens. Eventually, as the financial media often suggests, the markets always get back to even. One such chart is the percentage gain/loss chart over the long-term, as shown below.

This is one of the most deceptive charts an advisor can show a client, particularly one that is close to, or worse in, retirement.

The reality is that you DIED long before ever achieving that 8% annualized long-term return you were promised. Secondly, math is a cruel teacher.

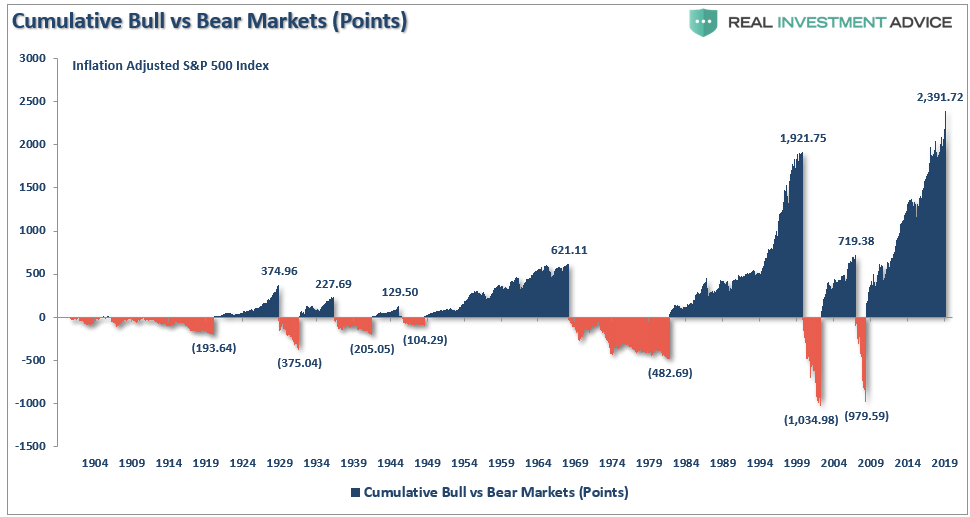

Visually, percentage drawdowns seem to be inconsequential relative to the massive percentage gains that preceded them. That is, until you convert percentages into points and reveal an uglier truth.

It is important to remember that a 100% gain on a $1000 investment, followed by a 50% loss, does not leave you with $1500. A 50% loss wipes out the previous 100% gain, leaving you with a 0% net return.

For retirees, this is a critically important point.

In 2000, the average “baby boomer” was around 45-years of age. The “dot.com” crash was painful, but with 20-years to go before retirement, there was time to recover. In 2010, following the financial crisis, the time to retirement for the oldest boomers was depleted, and the average boomer only had 10-years to recover. During both of these previous periods, portfolios were still in accumulation mode. However, today, only the youngest tranche of “boomers,” have the luxury of “time” to work through the next major market reversion. (This also explains why the share of workers over the age of 65 is at historical highs.)

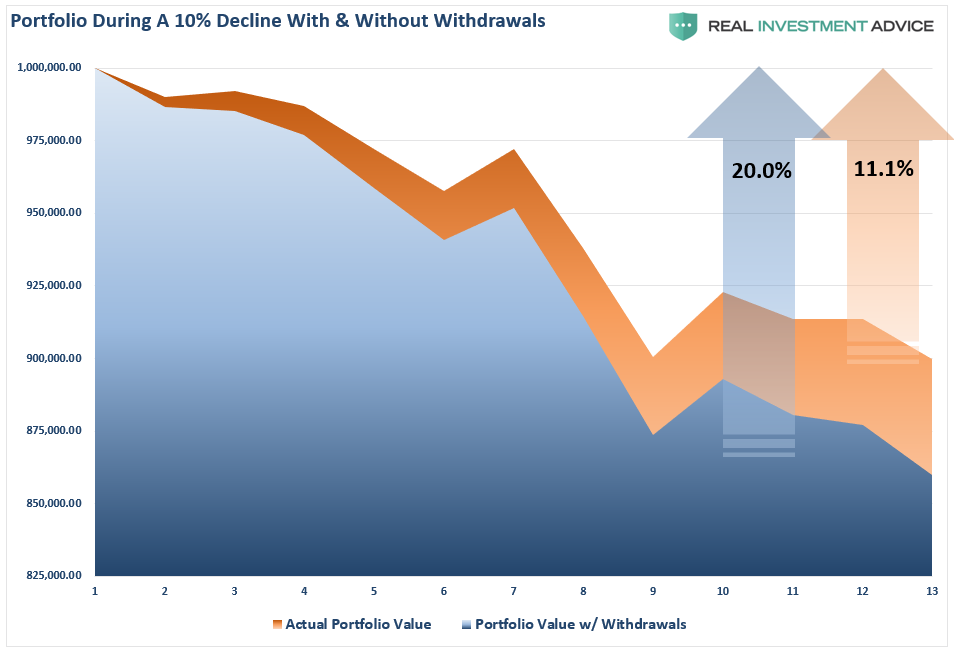

With the majority of “boomers” now faced with the implications of a transition into the distribution phase of the investment cycle, such has important ramifications during market declines. The following example shows a $1 million portfolio with, and without, an annualized 4% withdrawal rate. (We are going into much deeper analysis on this in a moment.)

While a 10% decline in the market will reduce a portfolio from $1 million to $990,000, when combined with an assumed monthly withdrawal rate, the portfolio value is reduced by almost 14%. This is the result of taking distributions during a period of declining market values. Importantly, while it ONLY requires a non-withdrawal portfolio an 11.1% return to break even, it requires nearly a 20% return for a portfolio in the distribution phase to attain the same level.

Impairments to capital are the biggest challenges facing pre- and post-retirees currently.

This is an important distinction. Most articles written about retirees, or those ready to retire, is an unrealized assumption of an indefinite timeline.

While the market may not be different than it has been in the past. YOU ARE!

Starting Valuations Matter

As I have discussed previously, without understanding the importance of starting valuations on your investment returns, you can’t understand the impact the market will have on psychology, and investor behavior.

Over any 30-year period, beginning valuation levels have a tremendous impact on future returns.

As valuations rise, future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay for an asset today, the future returns must, and will, be lower.

This is far less than the 8-10% rates of return currently promised by the Wall Street community. It is also why starting valuations are critical for individuals to understand when planning for both the accumulation and distribution, phases of the investment life-cycle.

Let’s elaborate on our example above.

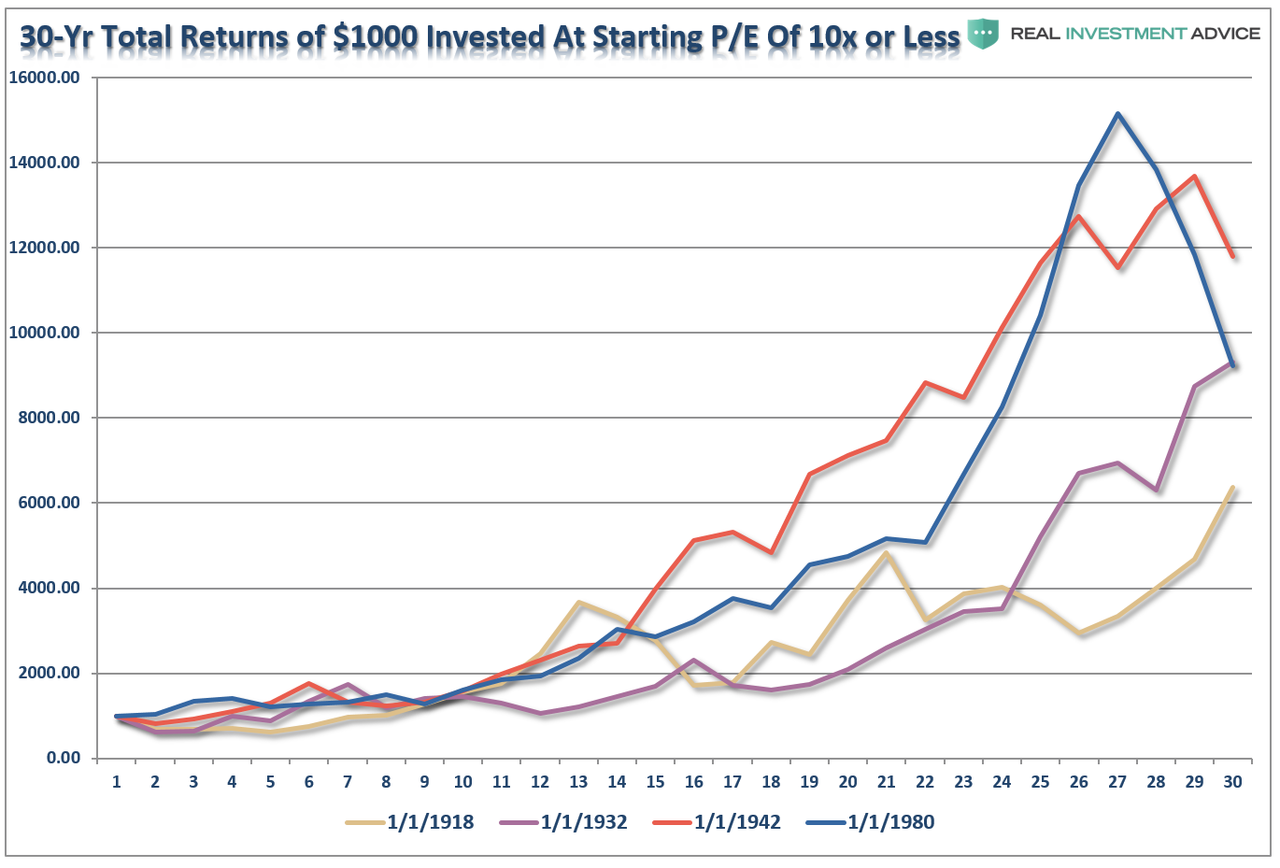

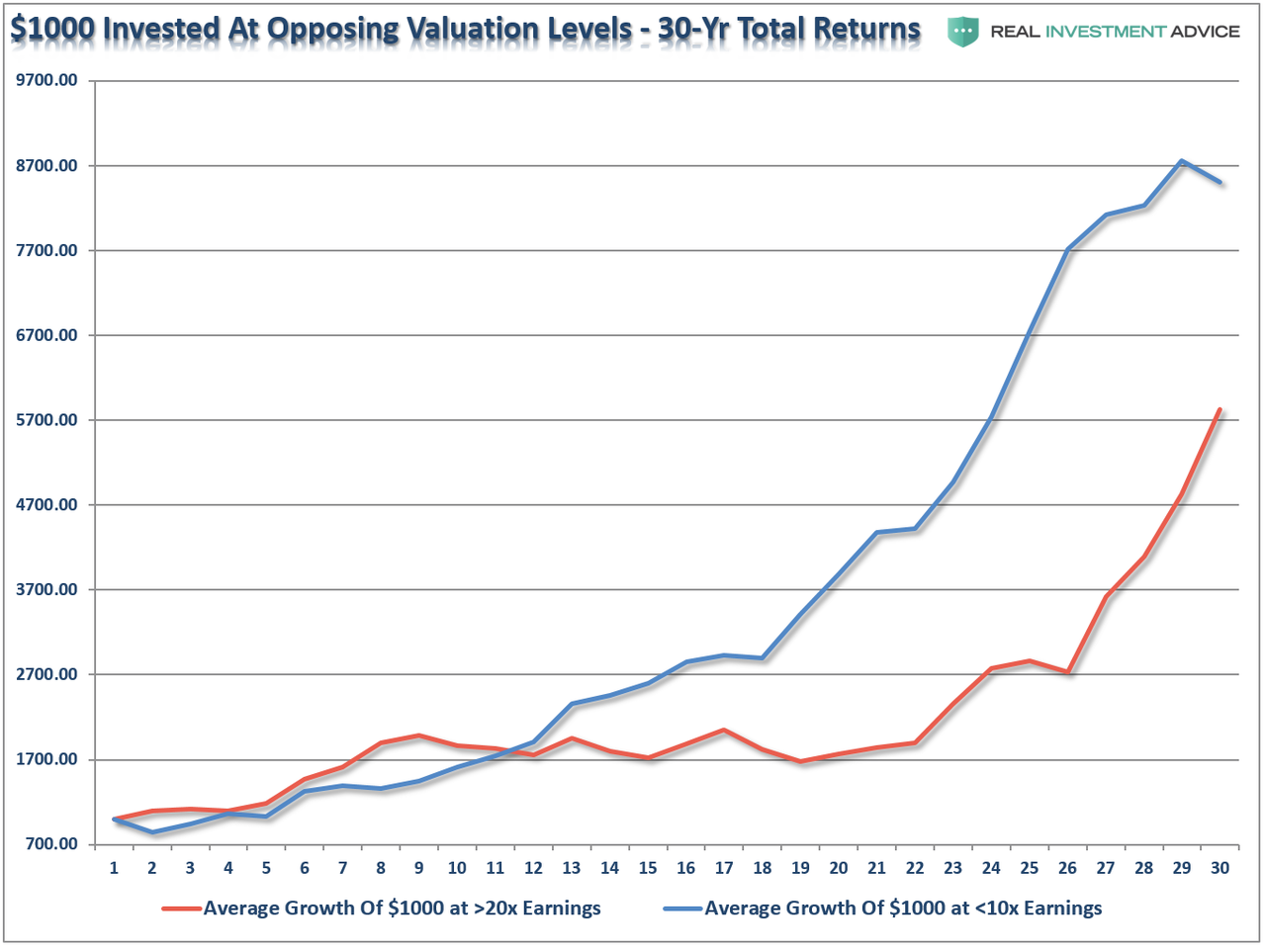

We know that markets go up and down over time, therefore when advisors use “average” or “annualized” rates of return, results often deviate far from reality. However, we do know from historical analysis that valuations drive forward returns, so using historical data, we calculated the 4-periods where starting valuations were either above 20x earnings, or below 10x earnings. We then ran a $1000 investment going forward for 30-years on a total-return, inflation-adjusted, basis.

The results were not surprising.

At 10x earnings, the worst performing period started in 1918 and only saw $1000 grow to a bit more than $6000. The best performing period was actually not the screaming bull market that started in 1980 because the last 10-years of that particular cycle caught the “dot.com” crash. It was the post-WWII bull market that ran from 1942 through 1972 that was the winner. Of course, the crash of 1974, just two years later, extracted a good bit of those returns.

Conversely, at 20x earnings, the best performing period started in 1900, which caught the rise of the market to its peak in 1929. Unfortunately, the next 4-years wiped out roughly 85% of those gains. However, outside of that one period, all of the other periods fared worse than investing at lower valuations. (Note: 1993 is still currently running as its 30-year period will end in 2023.)

The point to be made here is simple and was precisely summed up by Warren Buffett:

“Price is what you pay. Value is what you get.”

To create our variable return assumption model, we averaged each of the 4-periods above into a single total return, inflation-adjusted, index. We could then see the impact of $1000 invested in the markets at both valuations BELOW 10x trailing earnings, and ABOVE 20x. Investing at 10x earnings yields substantially better results.

Starting Valuations Are Critical To Withdrawal Rates

With a more realistic return model, the impact of investing during periods of high valuations becomes more evident, particularly during the withdrawal phase of retirement.

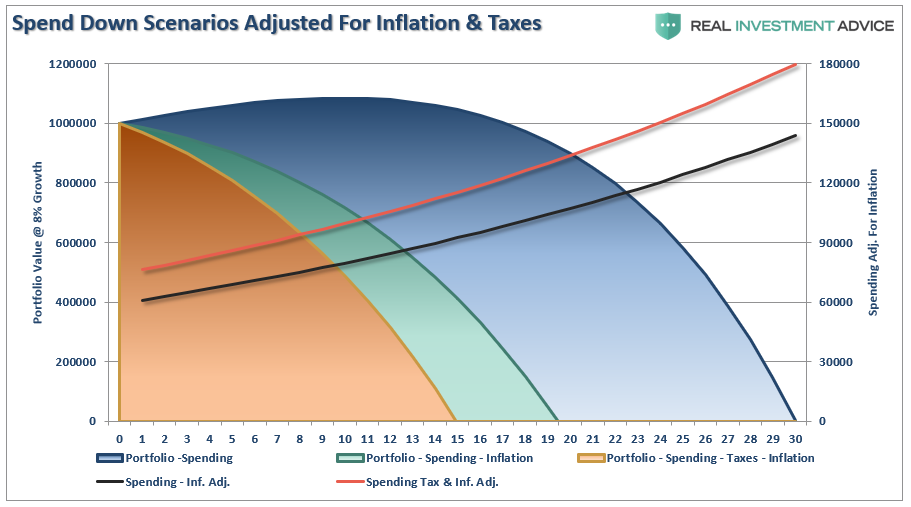

Let’s start with our $1 million retirement portfolio. The chart below shows various “spend down” assumptions of a $1 million retirement portfolio adjusted for an 8% annualized return, the impact of inflation at 3%, and the effect of taxation on withdrawals.

By adjusting the annualized rate of return for the impact of inflation and taxes, the life expectancy of a portfolio grows considerably shorter. Unfortunately, this is what “really happens” to investors over time, but is never discussed in mainstream analysis.

To understand “real outcomes,” we must adjust for variable rates of returns. There is a significant difference between 8% annualized rates of return and 8% real rates of return.

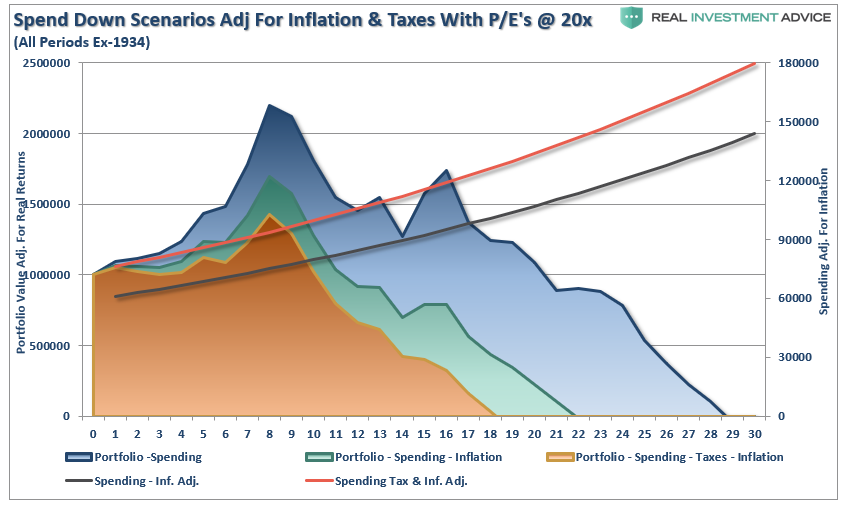

When we adjust the spend down structure for elevated starting valuation levels, and include inflation and taxes, a far different, and less favorable, outcome emerges. Retirees will run out of money not in year 30, but in year 18.

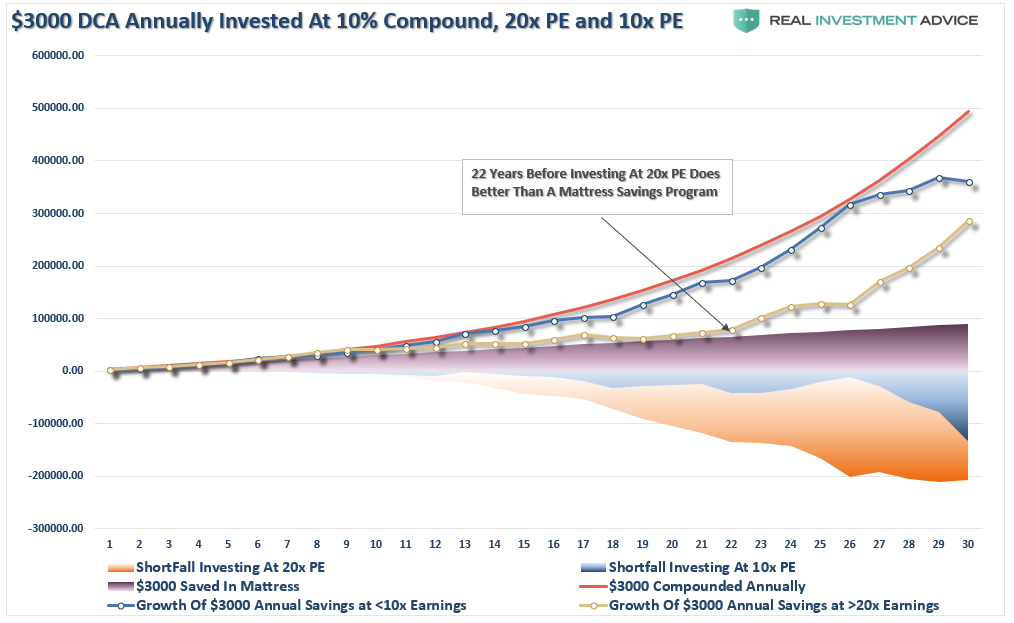

With this understanding, let’s revisit what happens to “buy and hold” investors over time. The chart below shows $3000 invested annually into the S&P 500 inflation-adjusted, total return index at 10% compounded annually, and both 10x and 20x valuation starting levels. I have also shown $3000 saved annually and “stuffed in a mattress.”

The red line is 10% compounded annually. While you don’t get compounded returns, it is there for comparative purposes to the real returns received over the 30-year investment horizon starting at 10x and 20x valuation levels. The shortfall between the promised 10% annual rates of return and actual returns are shown in the two shaded areas. In other words, if you are banking on some advisor’s promise of 10% annual returns for retirement, you aren’t going to make it.

Questions Retirees Need To Ask About Plans

What this analysis reveals is that “retirees” SHOULDbe worried about bear markets.

Taking the correct view of your portfolio, and the risks being undertaken is critical when entering the retirement and distribution phase of the portfolio life cycle.

Most importantly, when building and/or reviewing your financial plan, these are the questions you must ask and have concrete answers for:

What are the expectations for future returns going forward given current valuation levels?

Should the withdrawal rates be downwardly adjusted to account for potentially lower future returns?

Given a decade long bull market, have adjustments been made for potentially front-loaded negative returns?

Has the impact of taxation been carefully considered in the planned withdrawal rate?

Have future inflation expectations been carefully considered?

Have drawdowns from portfolios during declining market environments, which accelerates principal bleed, been considered?

Have plans been made to harbor capital during up years to allow for reduced portfolio withdrawals during adverse market conditions?

Has the yield chase over the last decade, and low interest rate environment, which has created an extremely risky environment for retirement income planning, been carefully considered?

What steps should be considered to reduce potential credit and duration risk in bond portfolios?

Have expectations for compounded annual rates of returns been dismissed in lieu of a plan for variable rates of future returns?

If the answer is “no” to the majority of these questions. then feel free to contact one of the CFP’s in our office who take all of these issues into account.

With debt levels rising globally, economic growth on the long-end of the cycle, earnings growth weak, valuations high, and potential risk of a recession, the uncertainty of retirement plans has risen markedly. This lends itself to the problem of individuals having to spend a bulk of their “retirement” continuing to work.

Yes, not only should you worry about bear markets, you should worry about them a lot.

Canada Says Wife Of First nCoV Patient Also Has Virus

Another alarming development in the global coronavirus outbreak has been confirmed: Public health officials in Ontario are preparing to announce that the wife of Canada’s first coronavirus patient has also been stricken with the virus.

The significance of this news may be lost on some casual observers, as it was no doubt lost on the reporters from the Canadian Press News who got the scoop: But this might constitutes evidence of human-to-human transmission outside of China – a sign that the virus has reached a new stage of contagion that some epidemiologists and researchers dismissed as extremely improbable just last week.

It’s unclear whether the woman traveled to China with her husband, so it’s still not certain whether she contracted the disease from the same source as her husband, or whether he actually passed it to him. The CPN reported that she has been in self-imposed isolation with her husband since arriving in Toronto (presumably for him to get treatment) last week.

On Thursday, the WHO declined to designate the outbreak as a global pandemic, arguing that China had the resources to contain the virus, and that it had not yet become a global problem. WHO Director-General Tedros Adhanom Ghebreyesus said they needed more information to reach a consensus on whether to declare a PHEIC (Public Health Emergency of International Concern). Specifically, the organization wanted to see evidence of human-to-human transmission outside of China before declaring a global emergency.

Person to person transmission offshore. This was the catalyst the WHO needed to declare a global emergency https://t.co/38K6iEzT2d

Global Stocks Crash As Coronavirus Pandemic Infects 3,000; China, Yuan Plummet

Global markets are a freefalling, sea of red mess, as algos finally realized that last week’s optimism that “China’s coronavirus epidemic is contained” was actually dead wrong, and the result is Dow down over 400 points and S&P futures plunging below 3,250…

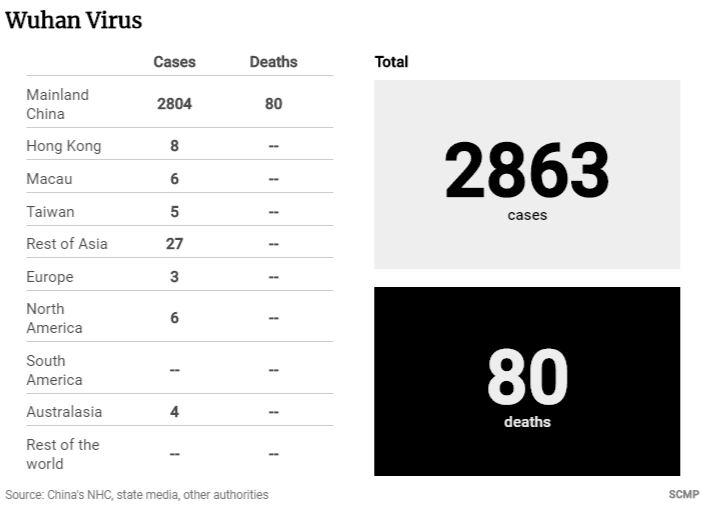

… because with nearly 3,000 people infected around the globe and over 80 dead, one thing is certain: the epidemic is anything but contained.

And so, after denying reality for over a week, global stocks finally tumbled on Monday with S&P futures plunged the most since October 2, as investors grew increasingly anxious about the economic impact of China’s spreading virus outbreak, with demand spiking for safe-haven assets such as the Japanese yen and Treasury notes.

“Any economic shock to China’s colossal industrial and consumption engines will spread rapidly to other countries through the increased trade and financial linkages associated with globalization,” Stephen Innes, chief Asia market strategist at Axitrader, wrote in a note Monday. “I’m starting to think cash is the right place to be for the next few weeks” Innes added making a mockery of Ray Dalio’s cash forecast for the second time in three years.

As Saxobank notes, equities are finally beginning to contemplate the possibility that the virus 2019-nCoV in China will have significant economic impact as the lockdown is now affecting 56 million people. China has imposed travel bans, school closings in major cities and is extending the Lunar New Year. The market reaction already started Friday with the US equities declining as more news disseminated, but in today’s session Chinese related markets are hit hard.

“Investors will react quickly to any sign of negativity and this is no exception as China announces that the issue has become an emergency. This could keep oil prices fragile until the coronavirus shows signs of slowing down,” said Mihir Kapadia, chief executive at Sun Global Investments.

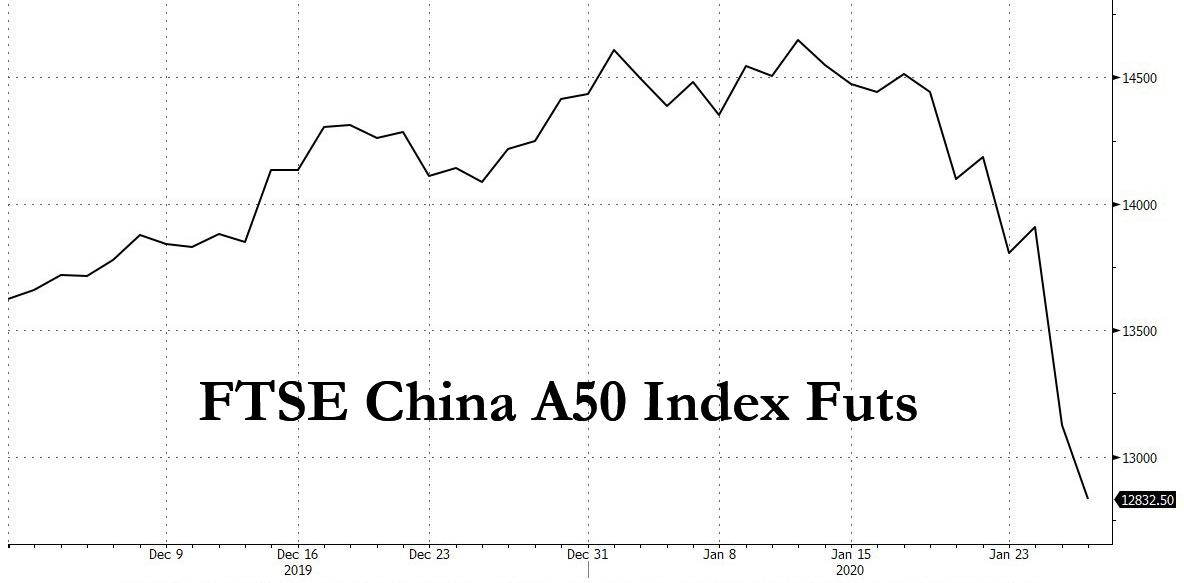

In Asian trading, the MSCI index of Asia-Pacific shares ex-Japan was off 0.4%, although trade in the region has already slowed for the Lunar New Year and other holidays, with financial markets in China, Hong Kong, Taiwan, South Korea, Singapore and Australia closed on Monday. Japan’s Nikkei average slid 2.0%, the biggest one-day fall in five months. Amid the Lunar New Year holiday, many markets in Asia were closed with China expected to be closed until at least Feb 3, however those who wanted to get out of China could do so thanks to the Singapore-tarded China proxy, the FTSE China A50 future, has plunged over 11% since the disease outbreak was reported.

The risk-off sentiment continued in European trading, where volumes and volatility surged, as Europe reacted to Asian equity weakness driven by weekend updates on the coronavirus spread. The Stoxx Europe 600 Index headed for its worst decline since October, with the mining group dropping by 4%. All Euro Stoxx 600 sectors are in the red with miners, travel and tech names posting the heaviest losses; a key measure of risk for the debt of Europe’s most fragile companies jumped to the highest in nearly two months. Adding to Europe’s pain, Germany’s IFO survey disappointed, confirming that the economic rebound in Germany is not a straight line as we have seen in previous rebounds since 2008. It all adds to uncertainty.

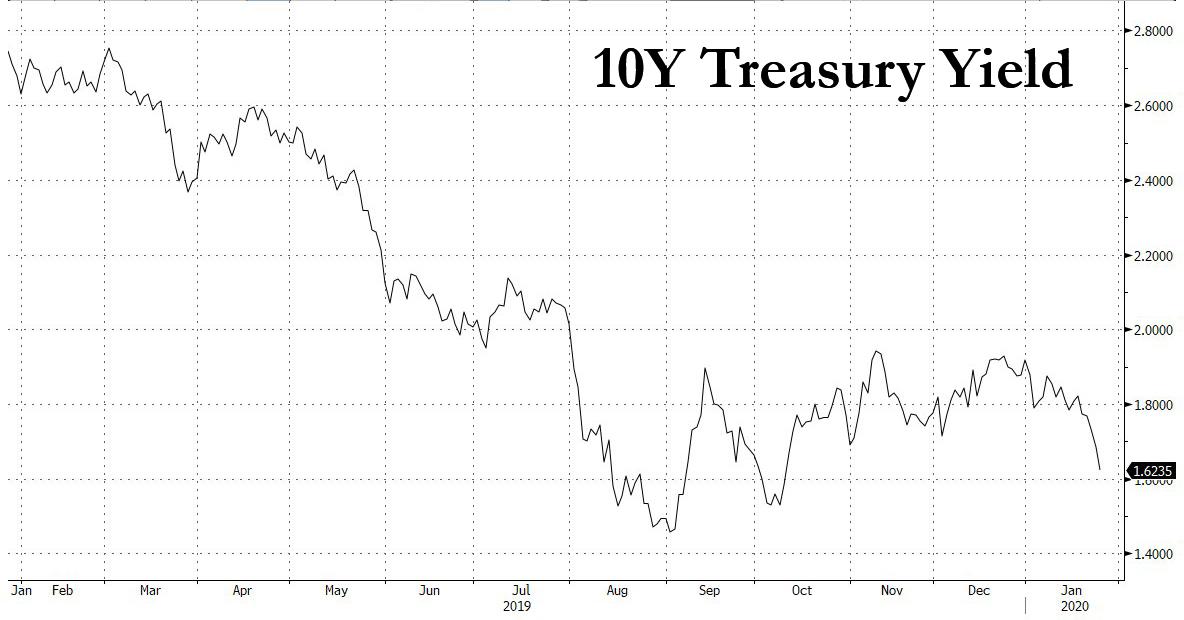

U.S. Treasury prices advanced, pushing down yields further, with the benchmark 10-year notes dropping to a 3-1/2-month trough of 1.627% in early Asian trade.

As yields plunged, so did oil and Brent crude futures fell to three- and five-month lows, respectively, with Brent plunging below $60 for the first time since October.

In Rates, German bonds rallied after closing their opening gap in early London trade with the curve bull flattening, spurred by a large block trade in bobl futures. One-way traffic in Italian bonds, 10y BTP rally ~230 ticks, tightening ~17bps to core after the weekend regional election. Amusingly, in Greece 10-year GGB yields drop to record lows after Friday’s upgrade by Fitch. Treasury curve bull steepens, 10-year yield drops ~6bps, with 2y and 5y supply due later today.

Emerging market equities are down 4.1% and cyclical sectors are leading the declines with especially travel, luxury goods, semiconductors and mining related stocks being hit the hardest.

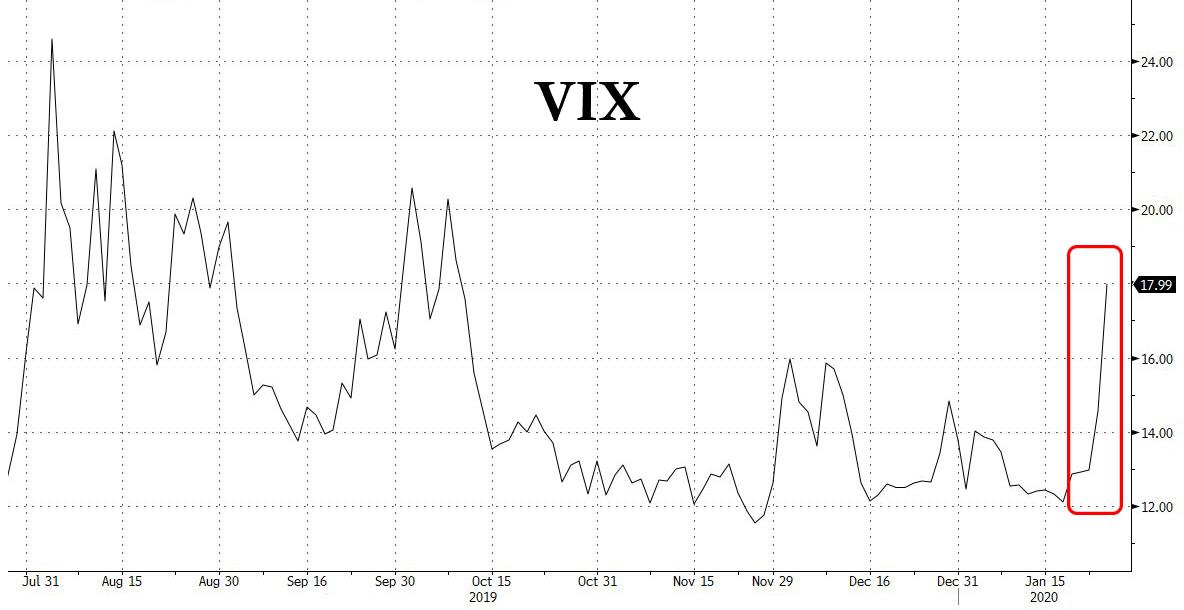

Adding to risk-off sentiment we observe the VIX Index is close to 18, the highest level since October, which means that the equity market is shifting in a different state with lower expected returns and higher volatility. Remember as we have said many times in the past that the 22 level is the magical level where equity markets downside dynamics become very ugly. So stay alert and pay attention to news out of China and watch the VIX.

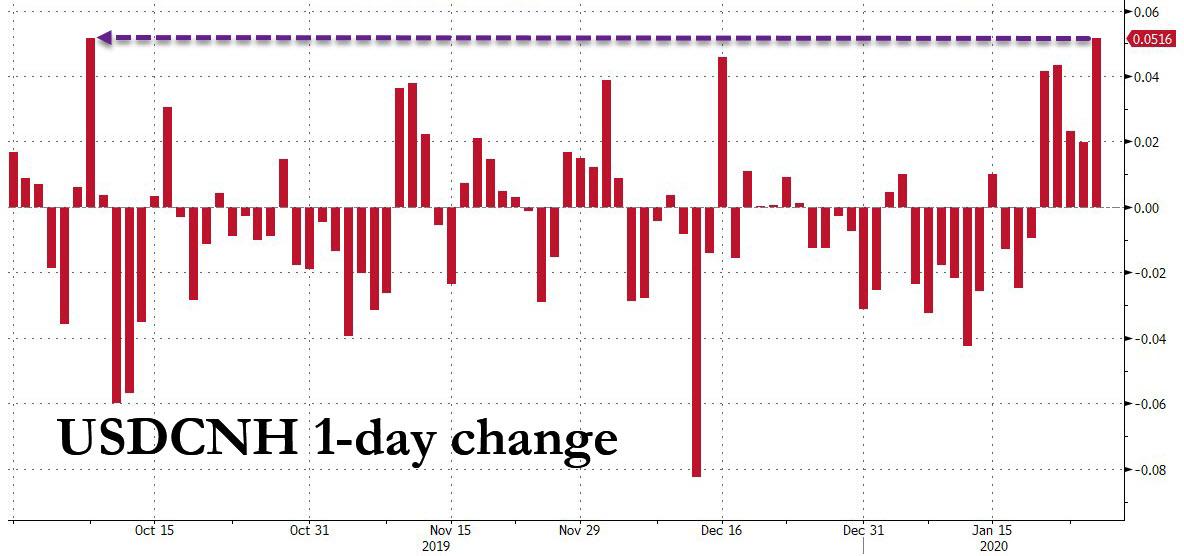

In the currency market, the concerns about the virus supported the yen, which strengthened as much as 0.5% to 108.73 yen per dollar, its 2-1/2-week high. The euro last stood at $1.1028 versus the dollar, having fallen to its eight-week low of $1.1019 on Friday. The offshore yuan dropped more than 0.5% to 6.9776 against the dollar, its weakest level since Jan. 6 and its biggest drop since October.

In other commodities, base metals slump, LME Nickel over 2% lower to underperform peers. Spot gold rose as much as 1.0% to $1,585.80 per ounce, the highest level since Jan. 8, as rising concerns over the spread of a virus outbreak in China and its potential economic impact prompted investors to buy the safe-haven metal.

In geopolitical news, Iran nuclear agency deputy chief said they have the capacity to enrich uranium at any percentage if the government decides to. There was an attack on the US embassy in Baghdad, Iraq where 3 rockets hit the embassy which left one individual injured although the injuries were only minor and the person later returned to duty, while the US embassy is said to have informed the Iraqi government that there will be a military response according to Twitter sources.

New home sales are among economic data due. Scheduled earnings include Sprint, Whirlpool

Market Snapshot

S&P 500 futures down 1.3% to 3,250.25

MXAP down 0.7% to 170.81

MXAPJ down 0.5% to 556.16

Nikkei down 2% to 23,343.51

Topix down 1.6% to 1,702.57

Hang Seng Index up 0.2% to 27,949.64

Shanghai Composite down 2.8% to 2,976.53

Sensex down 1% to 41,210.97

Australia S&P/ASX 200 up 0.04% to 7,090.54

Kospi down 0.9% to 2,246.13

Brent futures down 3.4% to $58.62/bbl

Gold spot up 0.8% to $1,583.27

U.S. dollar Index up 0.06% to 97.91

STOXX Europe 600 down 1.7% to 416.42

German 10Y yield fell 2.7 bps to -0.362%

Euro down 0.07% to $1.1017

Brent Futures down 3.2% to $58.75/bbl

Italian 10Y yield fell 2.2 bps to 1.064%

Spanish 10Y yield fell 5.2 bps to 0.296%

Top Overnight News from Bloomberg

Traders see nearly 60% chance of a Bank of England cut this week as of Monday. Economists are more cautious, predicting a 6-3 vote to keep rates on hold as the government prepares to negotiate a trade deal with the European Union that will help define the post-Brexit economy

Japanese Prime Minister Shinzo Abe’s upcoming choice of candidate to join the Bank of Japan board could shed light on the leader’s current thinking on the importance of achieving a stubbornly difficult inflation goal. be’s nomination to replace Yutaka Harada is scheduled to take place Tuesday morning, according to a document seen by Bloomberg

China’s escalating viral outbreak may end up hitting Japan’s fragile economy harder than the SARS outbreak of 2003, according to economists

Traders are pricing in a full quarter- point Federal Reserve rate cut this year amid fears of headwinds to global growth from the spread of the coronavirus. Economists for their part see the Fed holding rates steady this year and next, according to a survey by Bloomberg

A broad risk-averse tone resumed across asset classes following on from last Friday’s declines on Wall St. where the S&P 500 posted its worst weekly performance since August amid ongoing coronavirus fears, with the number of confirmed cases stateside now at 5. Furthermore, the latest official update from China stated the number of infected rose to 2744 with the death toll at 80, and China also warned that the coronavirus is getting stronger and the amount of cases could increase. This heavily pressured US equity futures which slipped around 1% in early trade and spurred safe-haven bids for T-notes and gold, while Nikkei 225 (-2.0%) sold off due to the virus outbreak fears, detrimental currency flows and against the backdrop of thinned conditions with nearly all major bourses in the region closed for holiday. India’s NIFTY (-1.0%) was also lower after large-scale protests yesterday regarding the Citizenship Amendment Act, but with losses limited amid corporate earnings including ICICI Bank. Finally, 10yr JGBs were underpinned on safe-haven buying due to the coronavirus jitters which also spurred T-notes to gap higher by about 10 ticks at the re-open, although the upward momentum for JGBs has since petered out amid the lack of BoJ presence in the market and absence of most regional participants.

Top Asia News

Abe’s Pick to Replace BOJ Board Member Could Come on Tuesday

Coronavirus Seen Hitting Japan’s Economy Harder Than SARS

Bidders Must Absorb $3.3 Billion Debt to Buy Air India

European stocks see hefty losses across the board [Eurostoxx 50 -2.2%] following muted but negative APAC session as the region experiences mass holiday closures. For reference, the pan-European Stoxx 600 index sees around 95% of its stocks in negative territory. UK’s FTSE 100 (-2.5%) sees slightly more pronounced downside amid heavy-bleeding from large-cap miners and energy names, in-fitting with price action in the respective complexes – Rio Tino (-4.8%), Antofagasta (-4.3%), Anglo American (-4.5%), Glencore (-4.5%), BP (-2.0%) and Shell (-2.0%). Meanwhile, Italy’s FTSE MIB (-0.7%) fares better in light of the aftermath from the Emilia Romagna regional elections which diminished the chances of an Italian snap election, thus Italian banks cushion losses in the index with tailwinds from favourable BTP price action – Ubi Banca (+0.1%), Banco BPM (+0.1%), Intesa Sanpaolo (-0.1%). Sectors are broadly, but firmly in the red, with Materials (-2.8%) lagging amid the base-metal price action. Defensives meanwhile see losses to a lesser extent than their cyclical peers. Consumer discretionary names also remain a laggard amid the demand implications from the virus outbreak for luxury goods and travel names, such as: Swatch (-3.6%), Richemont (-3.0%), IAG (-6.0%) and easyJet (-5.5%). In terms of individual movers; William Hill (-1.7%) saw losses at the open amid a breakdown in expansion talks with CBS Sports. Bayer (-1.5%) conforms to losses seen in the region despite a pushback from a spokesperson regarding last-week’s sources reports of an imminent settlement to its Roundup weedkiller scandal. On the flip side, positive broker moves see RWE (+0.1%), Uniper (+0.1%) Orsted (+0.1%) and Italgas (+1.4%) in the green.

Top European News

Populists Humiliated in Italy Vote as Conte Gets a Respite

Axa Narrows Bids for Eastern Europe Unit to Generali, Austrians

Slovenian Prime Minister Resigns, Floats Holding Early Elections

Turkey Starts Probe of ‘Provocative’ Social Media Posts on Quake

In FX, broad losses experienced in the EM-sphere, led by downside in the Yuan as the coronavirus crisis claims more lives and spreads further towards the West (full analysis available on the Newsquawk feed). USD/CNH has gained traction and breached 6.9800 to the upside (vs. 6.9400 low), topping its 200 and 55 DMAs at 6.9817 and 6.9843 respectively – with talks of potential stimulus measures by the Chinese Government to cushion the economic impact of the outbreak. TRY and ZAR feel the Yuan contagion with USD/TRY looking for a test of 5.9500 to the upside whilst USD/ZAR inches closer to 14.6000, but could see mild resistance at 14.5970 (21st Jan high) with reported stops above the round figure and ahead its 200 DMA at 14.6105.

CAD, NOK, RUB – Energy-related FX succumb to losses seen in the complex as jitters materialise regarding the implications of the virus outbreak on global oil demand. The Rouble remains the most impacted as USD/RUB surpasses 62.50 (vs. 62.24 open) before stopping short of its 200 DMA (62.63). The Loonie meanwhile extends losses vs. the Buck as the pair found support ~1.3150 before taking out its 55 and 100 DMAs (at 1.3158 and 1.3178 respectively) ahead of the psychological 1.3200. Similarly, Norway’s oil-correlated Crown drifted lower since the open – EUR/NOK reclaimed 10.0000 (which also coincides with its 55DMA) to the upside and topped its 100 DMA (10.0183) – with potential resistance touted at 10.0500.

AUD, NZD – The antipodeans also drift in tandem with the risk aversion and headwinds from detrimental base metal price action amid the aforementioned virus woes. AUD/USD has given up its 0.6800-status as losses exacerbated amid the domino-effect coronavirus would have on the Australian economy via China’s anticipated economic slowdown – with reports noting that Chinese GDP could see a reduction of as much as 1ppt. The pair remains the marked G10 underperformer thus far and eyes 0.6755 (26th Nov low and 76.4% Fibo of the Oct to Dec move) to the downside for a potential support level, and with some AUD 800mln in options seen expiring at strike 0.6765. Meanwhile, its Kiwi counterpart looks to test its 55 DMA to the downside at 0.6550.

JPY, DXY – Safe haven flows have seen an early bid in the Japanese currency, as USD/JPY gapped below 109.00 at the open vs. Friday’s 109.25 close. Since then, the pair has fluctuated on either side of the round figure having found a base around 108.75, and with technicians eyeing 108.67 (100 DMA) and 108.52 (200 DMA) should the base fail to hold, and with 109.00 seeing circa USD 800mln in options expiries. DXY meanwhile remains flat intraday having notched a current range of 97.800-941 and with little by way of schedule data/speakers to sway the state of play.

EUR, GBP – Mixed session for the Sterling and Single Currency, but relatively muted action compared to some of its G10 and EM peers. EUR/USD saw some pressure amid a downbeat German Ifo Survey which reaffirmed that the German economy has a subdued start to the year, but somewhat echoed Markit’s assessment that the manufacturing sector is slowly emerging from its downturn. EUR/USD failed to glean much reprieve from the development in Italy after the Centre-Left bloc defeated Salvini’s league in regional elections, thus dimming the chances of a snap election. The pair hovers just above 1.1000, having clocked in a current range of 1.1015-35. Meanwhile, Cable found an overnight base at 1.3050 and took advantage of some weakness seen in the Single Currency. EUR/GBP drifts further below 0.8450 whilst GBP/USD meanders just under 1.3100, having eclipsed the level in recent trade.

In commodities, WTI and Brent front-month futures continue their downward trajectory amid the materialising concerns surrounding the virus outbreak’s impact on global growth, oil demand and overall sentiment. While some desks have drawn comparisons to the SARS virus in 2003, which trimmed 0.15ppts off of global growth, some believe that the comparisons may be slightly unfair, albeit some economists note that Chinese GDP could see a reduction of as much as 1ppt. WTI Mar’20 futures gapped lower at the open before downside exacerbated and prompted the contract to test levels close to USD 52/bbl to the downside, levels last seen in October 2019. Similarly, Brent Mar’20 surrendered the USD 60/bbl handle and currently posts loses around USD 2/bbl; the contract did find some support at USD 58.50/bbl. Elsewhere spot gold is bolstered by the flows in to safe-havens, with prices testing USD 1590/oz to the upside during APAC trade vs. Friday’s ~USD 1570/oz. The overall demand/global growth aspect of the outbreak of the coronavirus has led to sharp losses in base metal prices: copper slumped around 2% at one point and dipped below USD 2.62/lb vs. Friday’s ~USD 2.67/lb close, whilst iron ore futures fell as much as 6% at one point.

US Event Calendar

10am: New Home Sales MoM, est. 1.53%, prior 1.3%

10am: New Home Sales, est. 730,000, prior 719,000

10:30am: Dallas Fed Manf. Activity, est. -1.6, prior -3.2

DB’s Jim Reid concludes the overnight wrap

There’s a reasonable amount of drama to anticipate this week. The progress of the coronavirus will be the overwhelming key short term driver (latest below) as more and more concerns rise to the surface. As an aside the week ends with a landmark moment in history as at midnight CET on Friday the U.K. will finally leave the EU 43 months after the vote. Staying with the U.K., a finely balanced BoE meeting the day before might be the highlight elsewhere. The FOMC (Wednesday) will attract the usual interest even if the Fed seemingly have a high bar to act in either direction at the moment. Also watch today’s German IFO with expectations that it will match the strongest level since June. China’s official PMIs (Friday but possibly delayed as the holiday season has now been extended until February 2) could be a very important release for the globe but the reality is that the virus will impact these numbers from next month making trends difficult to decipher. Q4’s GDP numbers from both the US (Thursday) and the Euro Area (Friday), as well as the European flash CPI (Friday) will also garner some interest.

We also have some very high profile earnings this week with four of the five largest US companies reporting (Apple, Microsoft, Amazon, Facebook). On Friday night our US equity strategists reiterated their view of very stretched positioning in the market. They now see it in the 98th percentile of their historical dataset with systematic funds at all time high exposure. They also show that 3-5% pull backs typically happen every 2-3 months and we’ve now been without one for 3.5 months. In another two weeks this will put us in the 90th percentile through history (86th currently). See their report here.

Staying with the US and with great importance to US equity markets, it seems that Bernie Sanders has edged into the lead in the Democratic nomination race over the weekend with a probability of between 35-40% in bookmaker markets. He was 5th in the race and only just above 5% in mid October. Joe Biden probabilities range from c.31-37%. So pretty tight with Sanders climbing rather than Biden falling. This time next week Iowa will vote in the first primary so we’ll soon be giving this race a lot more macro attention. The polls (Emmerson College and YouGov) suggest he’s edged into a very narrow lead there, the same as with New Hampshire that polls 8 days later. A reminder that in our last monthly investor sentiment poll, 90% thought a Sanders Presidency would be negative for US equities. Should more risk premium be priced into markets therefore? Especially with positioning and valuations as stretched as our strategists believe.

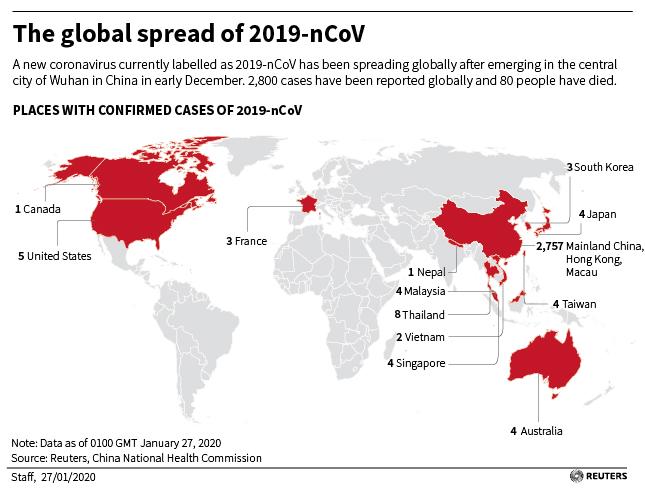

Before we go through the two main central bank events of the week in more detail and review last week in markets we should go straight to Asia and for updates on the coronavirus. The latest is that there are now 80 confirmed deaths (up from 25 on Friday) and 2,774 confirmed cases (up from 835) with around 30,000 people under observation. Meanwhile, France became the first country in Europe to report cases of the virus. As of now, the global tally is 7 in Thailand, 3 in Japan, 3 in South Korea, 3 in the US, 1 in Canada, 2 in Vietnam, 4 in Singapore, 3 in Malaysia, 1 in Nepal, 3 in France, and 4 in Australia along with 8 in Hong Kong, 5 in Macao and 4 in Taiwan. Elsewhere, on Saturday China said that it is imposing a ban on all outgoing overseas group tours from today after banning all domestic group tours on Friday. China has now also banned wildlife trade across the country with the government saying that the shipping and sale of wild animals won’t be allowed, and breeding sites will be quarantined and warned citizens against the consumption of wild animals. Also about 56 million people in China are now under severe transport curbs.

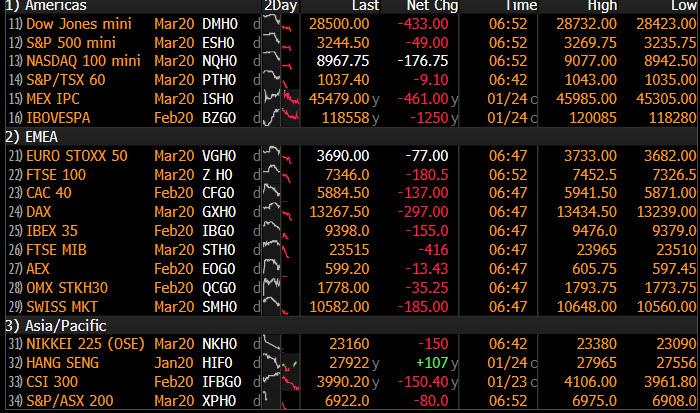

Risk off continues to be the theme in Asian markets this morning as the concerns over the coronavirus continue to rise. Safe heaven assets are up with gold (+0.48%) and the Japanese yen (+0.18%) both higher while yields on 10y USTs are down -4.2bps to 1.643% and crude oil prices are down c. -2.35%. Meanwhile, Asian equity markets are declining with the Nikkei (-1.97%) and India’s Nifty (-0.43%) both down. Markets in Hong Kong, China and South Korea are closed for the NY holiday. As for Fx, the offshore Chinese yuan is down c. -0.50% to 6.9669 while most emerging market currencies are also trading weak. Elsewhere futures on the S&P 500 are down -0.98% while those on the Chinese equity market (SGX FTSE China A50) are down -5.19%.

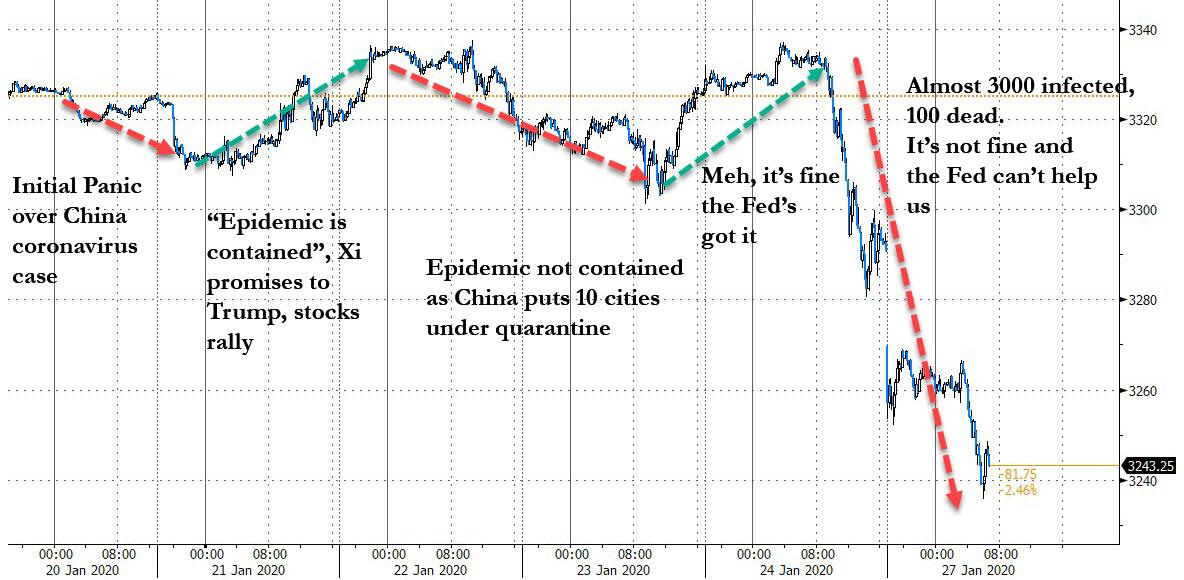

In other news, the Italian government led by Prime Minister Giuseppe Conte were boosted by a victory in a regional election in Emilia-Romagna with interior ministry figures showing that support for the center-left bloc led by the Democratic Party was at around 50% while the group headed by Salvini’s Lega Party trailed at only 45%. Meanwhile, the support for the M5S dropped to only 5%. The election results should help the performance of BTPs albeit in a risk off environment.

We also got news over the weekend that three rockets hit the US embassy in Iraq’s capital Bhagdad on Sunday with Bloomberg reporting that at least one person was wounded in the attack. It is not clear how serious the injuries are or whether the person was an American national or an Iraqi staff member. This indicates that geopolitical risks are likely to linger this year.

Now to the knife-edge BoE decision on Thursday (Mark Carney’s last meeting). This meeting follows a run of fairly weak economic data over the last few weeks but with last week’s strong employment data and better than expected flash PMIs (more later) confusing the picture. Our economists have expected a cut for a good couple of months now but markets are closer to 50:50. Sterling is at $1.3058 in Asia (-0.11%) as we approach the big day. It started the year at $1.3257 so net net the weak data in 2020 has impacted pricing.

As for the FOMC on Wednesday, our US economists write in their preview (link here) that the FOMC should hold rates steady, and that “the current stance is likely to be unchanged barring a “material reassessment to the outlook.” However, they do foresee a 5bp upward technical adjustment to the interest rate on excess reserves (IOER), though they write that “it is a close call given the communication challenges of such a move.” All eyes will be on Chair Powell’s press conference following the meeting for any new information. The full day by day week ahead is at the end.

Earnings seasons ramps up this week, with a number of large companies reporting. Tuesday sees reports from Apple, LVMH, Pfizer and SAP. Then on Wednesday we’ll get an array of companies, including Microsoft, Facebook, Mastercard, AT&T, Novartis, Boeing, McDonald’s, PayPal, General Electric and Banco Santander. On Thursday, releases come from Amazon, Visa, Roche Holding, Verizon, The CocaCola Company, Royal Dutch Shell, Unilever, Amgen and Samsung. Finally on Friday, we’ll hear from Exxon Mobil, Chevron and Caterpillar.

Now for last week where we ended weak as fear grew over the coronavirus. Global equity markets sold off with the S&P 500 coming off record highs to end the week down -1.03% (-0.90% Friday), with its decline on Friday actually its worst daily performance since early October. It was a similar story elsewhere, with the NASDAQ also down -0.79% (-0.93% Friday), and the STOXX 600 down -0.22% (+0.86% Friday before the late US sell-off). Chinese assets in particular suffered last week, though they were closed on Friday for the New Year holiday, with the Shanghai Composite index down -3.22% in its worst week since August, while the CSI 300 was down -3.63% in its worst week since May. Other risk assets also underperformed, with Brent crude down -6.41% (-2.18% Friday) in its worst weekly performance since December 2018 and its 3rd successive weekly decline. So probably not where a lot of investors thought we’d be for oil following the heightened geopolitical tensions that started the year between the US and Iran.

Safe havens were the beneficiaries, with 10yr bund yields falling every day last week, down -12.0bps (-2.7bps Friday), which is actually their biggest weekly decline since May 2018. 10yr Treasury yields were also down -13.8bps (-4.9bps Friday) in their biggest weekly fall since October, down to 1.684%, their lowest level since October. Other safe haven assets outperformed as well, with gold up +0.92% (+0.55% Friday) and the Japanese Yen +0.79% (+0.19% Friday) against the US dollar.

The main data release on Friday came from the PMIs, which were a mixed set of results, though their impact on markets was rather outweighed by the virus. For the Euro Area as a whole, the composite PMI surprised slightly to the downside, remaining at 50.9 against expectations for an increase to 51.2. The French composite PMI fell back this month, down to 51.5 (vs. 52.0 expected) amidst the ongoing strikes in the country, while the German reading surprised to the upside, with the composite PMI up to 51.1 (vs. 50.5 expected), which is the strongest reading since August. Here in the UK, the PMIs also surprised on the upside, with the composite PMI coming in at 52.4 (vs. 50.7 expected), and up from a contractionary 49.3 in December. Following the news, investors dialled back their expectations of a rate cut from the Bank of England this week, which now stand at around a 46% chance, down from 70.5% chance a week ago. For completeness, over in the US the composite PMI rose to a 10-month high of 53.1, in spite of the fact that the manufacturing PMI declined for a second successive month, down to 51.7 (vs. 52.5 expected).

From Stavridanoudakis v. U.S. Dep’t of Fish & Wildlife, decided Friday by Judge Lawrence J. O’Neill (E.D. Cal.):

The Migratory Bird Treaty Act (“MBTA”) codifies the protections of migratory birds as outlined in various conventions between the United States and four foreign countries: Canada, Mexico, Japan, and Russia. The MBTA only applies to migratory birds native to the United States, which includes several types of Falconiformes (vultures, kites, eagles, hawks, caracaras, and falcons) and Strigiformes (owls). The MBTA authorizes the Secretary of the Interior (“Secretary”) to adopt suitable regulations to determine, inter alia, when, and to what extent, it may be permissible to hunt, take, capture, possess, sale, and transfer protected birds, bird parts, nests, and eggs.

Pursuant to the authority of the MBTA, the Secretary promulgated regulations to regulate falconry standards and falconry permitting …. 50 C.F.R. § 21.29(f)(9)(i) prohibits photographing or filming falconry raptors for “movies commercials, or in other commercial ventures.” 50 C.F.R. § 21.29(f)(9)(ii) prohibits falconers from photographing or filming their birds for “advertisements; as a representation of any business, company, corporation, or other organization; or for promotion or endorsement of any products, merchandise, goods, services, meetings, or fairs”—unless the promotion or endorsement is of “a nonprofit falconry organization or association” or “products or endeavors related to falconry.”

50 C.F.R. § 21.29(f)(8)(v) dictates that during conservation education programs, falconers “must provide information about the biology, ecological roles, and conservation needs of raptors … although not all of these topics must be addressed in every presentation.” …

In Count III of the FAC, Plaintiffs claim that 50 C.F.R. § 21.29(f)(9)(i) is a content-based restriction that violates the First Amendment. Section 21.29(f)(9)(i) states “You may not use raptors to make movies, commercials, or in other commercial ventures that are not related to falconry.”

In Count IV, Plaintiffs contend that 50 C.F.R. § 21.29(f)(9)(ii) is an unconstitutional restriction on commercial speech. ECF No. 16 at 15-16. 50 C.F.R. § 21.29(f)(9)(ii) states that falconers may not use their raptors for “commercial entertainment; for advertisements; as representation of any business … or for promotion … of any products [or] services … with the following exceptions: (A) … to promote … a nonprofit falconry organization … [and] (B) … to promote … products … related to falconry ….”

In Count V, Plaintiffs challenge 50 C.F.R. § 21.29(f)(8)(v) which requires falconers giving conservation education programs to provide “information about the biology, ecological roles, and conservation needs of raptors.”

In Count VI, Plaintiffs challenge the prohibitions on charging fees that exceed the amount required to recoup costs under 50 C.F.R. § 21.20(f)(8)(iv)….

The Supreme Court has recognized that various forms of entertainment and visual expression are purely expressive activities—including movies. Therefore, 50 C.F.R. § 21.29(f)(9)(i)’s restrictions on movies and § 21.29(f)(9)(ii)’s restriction on commercial entertainment go beyond restricting expressive conduct and restrict purely expressive activity.

The restriction compelling the content of falconers’ conservation education program under 50 C.F.R. § 21.29(f)(8)(v) is clearly a content-based restriction because it explicitly restricts the topic of the speech that can be discussed: “you must provide information about the biology, ecological roles, and conservation needs of raptors ….” … The regulation unequivocally discriminates based on the topic of the educational presentation.

“A statute is presumptively inconsistent with the First Amendment if it imposes a financial burden on speakers because of the content of their speech.” Simon & Schuster, Inc. v. Members of N.Y. State Crime Victims Bd., 502 U.S. 105, 115 (1991). 50 C.F.R. § 21.29(f)(8)(iv) limits the fee that falconers can charge when giving a conservation education program. Therefore, this regulation imposes a financial burden on falconers depending on the content of their presentation….

The Federal Defendants do not argue in the motion to dismiss that the regulations restrict excludable speech (i.e. obscenity), or that the regulations are valid time, place, and manner restrictions. See Ward v. Rock Against Racism, 491 U.S. 781, 791 (1989). It is inconsequential that falconers could merely use nonnative raptors to engage in the prohibited activities. Because the restrictions are content based, they are not subject to reasonable time, place, and manner restrictions. Id. (the government may impose reasonable time, place, and manner restrictions, provided the restrictions are justified without reference to the content of the regulated speech). The Federal Defendants provide no such support that the restriction on use of native raptors is no less a restriction on falconers’ speech.

In addition, the Federal Defendants make no argument in the motion to dismiss that the content-based restrictions pass strict scrutiny. Thus, the Federal Defendants’ motion to dismiss Counts III, IV, V, and VI on the grounds that the regulations do not restrict protected speech is DENIED….

Next, the Federal Defendants contend that, assuming the speech restricted by the regulations is protected speech, the regulations do not violate the First Amendment because they are permissible regulations on commercial speech. {As discussed below, even assuming the speech regulations are aimed at only commercial speech, the Court finds that Defendants are not entitled to dismissal. In light of that finding and because the First Amendment test for commercial speech is less stringent, at this stage, the Court is not required to determine definitively the commercial or noncommercial nature of speech being restricted.} …

In the present case, the limits on “commercials,” under §§ 21.29(f)(9)(i) and “advertisements,” under subsection (ii), standing alone, are restrictions on commercial speech. However, restrictions on film (movies), photography, or on commercial entertainment are not restrictions on commercial speech. See ETW v. Jireh Pub., Inc., 332 F.3d 915, 925 (6th Cir. 2003) (holding “prints,” or copies, of paintings were not commercial speech because they did not propose a commercial transaction); see also Anderson, 621 F.3d at 1060 (recognizing various forms of entertainment and visual expression—including movies—are purely expressive activities). Thus, §§ 21.29(f)(9)(i) & (ii) place restrictions on commercial speech— advertisements, commercials, and promoting a business or product—and on non-commercial, fully-protected speech….

The Court evaluates restrictions on commercial speech using the four-part test in Central Hudson: “(1) if the communication is neither misleading nor related to unlawful activity, then it merits First Amendment scrutiny as a threshold matter; in order for the restriction to withstand such scrutiny, (2) [t]he State must assert a substantial interest to be achieved by restrictions on commercial speech; (3) the restriction must directly advance the state interest involved; and (4) it must not be more extensive than is necessary to serve that interest.” …

Plaintiffs argue that Defendants cannot make the showing on the fourth prong that the restrictions fit the government’s interest at the motion to dismiss stage. Where the challenged regulation is a content-based restriction subject to strict scrutiny, the issue of whether the challenged restrictions adequately fit the government interest was a question for summary judgment or trial. Frudden v. Pilling, 742 F.3d 1199, 1207-08 (9th Cir. 2014). The summary judgment process requires defendants to show a compelling government interest and permits plaintiffs an opportunity to present countervailing evidence.

The Court acknowledges Defendants have a substantial interest in protecting native raptors. In arguing that the regulations meet the fourth prong as a matter of law, the Federal Defendants claim that “the regulations are directed specifically at commercial endeavors, with a limited carve-out for falconry related undertakings.” ECF No. 24-1 at 19. However, in light of Frudden, the present record is not developed sufficiently. Accordingly, the Federal Defendants’ motion to dismiss the challenges to 50 C.F.R. § 21.29(f)(9)(i) and (ii) (Counts III & IV) on the theory that they are permissible commercial speech restrictions is DENIED….

In Count VI (Second Count), Plaintiffs claim that the California regulation, 14 C.C.R. § 670(h)(13)(A), violates the First and Fourteenth Amendments in the same way that the federal regulations do. This regulation states: “Education and Exhibiting. A licensee may use raptors in his or her possession for training purposes, education, field meets, and media (filming, photography, advertisements, etc.), as noted in 50 CFR 21, if the licensee possesses the appropriate valid federal permits, as long as the raptor is primarily used for falconry and the activity is related to the practice of falconry or biology, ecology or conservation of raptors and other migratory birds. Any fees charged, compensation, or pay received during the use of falconry raptors for these purposes may not exceed the amount required to recover costs.”

Like the federal regulations in Counts III, IV, V, and VI, this regulation is also a restriction of expressive activity based on content. It demands that when using the raptors in presentations or media, the content must be related to falconry. Section 670(h)(13)(A) also imposes a restriction on compensation that corresponds to the federal regulations. The State Defendants argue that § 670(h)(13)(A) does not ban speech. For the same reasons stated above that the federal regulations are content-based restrictions on expressive activity, the Court rejects this argument. Because the regulations are content based, they are presumptively unreasonable and subject to strict scrutiny review.

Next, the State Defendants contend that should falconers desire to use raptors for exhibiting or commercial uses not authorized in § 670(h)(13)(A), they may obtain the appropriate permit to engage in such activity. It is somewhat unclear what State Defendants are pecking at. The Court has reviewed the falconry regulations raised by the parties. It is possible there is a separate regulatory regime that supports State Defendants’ argument that falconers can obtain a separate permit to engage in the prohibited activities. State Defendants have not identified any such alternative regulations or laws.

The language of the regulations does not support the State Defendant’s position.14 C.C.R. § 670(h)(13)(A) provides “A licensee may use raptors in his or her possession for training purposes, education field meets, and media (filming, photography, advertisements, etc.), as noted in 50 CFR 21, if the licensee possesses the appropriate valid federal permits, as long as the raptor is primarily used for falconry and the activity is related to the practice of falconry or biology, ecology or conservation of raptors and other migratory birds.” By this provision’s plain language, it does not appear that a falconer could seek a permit to give a talk with the raptor that is unrelated to the practice of falconry. For instance, even with an exhibiting permit under 14 C.C.R. § 671.1(b)(6), a falconer could not give a presentation using her raptor about her political or religious views, or throw a Harry Potter party for a relative, because these topics are not related to the practice of falconry or the biology, ecology, or conservation of raptors. Furthermore, it is notable that the provision requires the licensee to possess the “appropriate valid federal permits.” Thus, the Court rejects the State Defendants’ argument that Count VI (Second Count) fails to state a claim for relief on the theory Plaintiffs could simply get a separate federal permit….

[T]he strength of the government’s interest for the challenged regulations and the fit of those interests to the speech restrictions at issue are material to the Court’s preliminary injunction analysis for all three categories of the First Amendment challenges.

The Court tentatively finds that the government has a strong interest in protecting the native raptor species, but because the briefing has failed to sufficiently discuss any aspect of fit, and because the Court is responsible for evaluating how a preliminary injunction would impact the public interest, the Court must hear from the Federal and State Defendants before it takes any action.

For example, it is unclear from the present record whether prohibiting falconers from earning money for educational presentations is a narrowly-tailored solution to combat a marketplace for the protected birds. Federal and State Defendants must discuss why the restrictions on falconers’ ability to give presentations and to film and photograph their birds meet strict scrutiny.

As with analyzing the restrictions on falconers’ ability to give presentations and film their birds, the Court will need supplemental briefing to thoroughly analyze whether the compensation restrictions are narrowly tailored to achieve the government’s interest. Federal and State Defendants must discuss why the compensation restrictions meets strict scrutiny.

As to the third category relating to commercial speech, the Federal Defendants contend that the regulations affecting commercial transactions of falconers are necessary to prevent a market for the protected birds from developing. Federal Defendants argue that lifting the regulations would undermine the goal of falconry raptor preservation and cause detrimental effects on the protected species….

Under Central Hudson, the restriction must not be more extensive than necessary to serve the government interest. The test is sometimes phrased as requiring a “reasonable fit” between the government’s legitimate interests and the means it uses to serve those interests, or that the government narrowly tailors the means to meet its objective….

At present, the Federal and State Defendants’ briefing does not explain how the regulations are not more extensive than necessary to serve an important state interest…. The State Defendants similarly do not address how the restrictions on commercial speech are not more extensive than necessary to promote the health and welfare of raptors. Therefore, on the present record, the Court cannot determine if the restrictions on commercial speech are not more extensive than necessary to serve these interests.

The Court will order the Federal and State Defendants to submit supplemental briefing with respect to these narrow issues. The Defendants should discuss the nature of the government interest involved and how the three categories of speech restrictions (falconers’ presentations and media, compensation, and commercial speech) are drawn to meet such interest. Lastly, Defendants should provide an analysis for the third and fourth prongs of the Winter test: the balance of equities and the public interest. Plaintiffs will then have an opportunity to respond….

The State and Federal Defendants are ordered to file supplemental briefs addressing the state interest(s) in the regulations challenged under the First Amendment and how those speech restrictions are tailored to achieve those interests, and relatedly, the balance of equities and the public interest prongs under Winter…. The Defendants shall have 30 days from the date of this order to file the briefs. Toucan, of course, play at this game, so Plaintiffs will then have 30 days from the date they are served with both State Defendants’ and Federal Defendants’ briefs to file a responsive brief….

from Latest – Reason.com https://ift.tt/2GrUDWc

via IFTTT

From Stavridanoudakis v. U.S. Dep’t of Fish & Wildlife, decided Friday by Judge Lawrence J. O’Neill (E.D. Cal.):

The Migratory Bird Treaty Act (“MBTA”) codifies the protections of migratory birds as outlined in various conventions between the United States and four foreign countries: Canada, Mexico, Japan, and Russia. The MBTA only applies to migratory birds native to the United States, which includes several types of Falconiformes (vultures, kites, eagles, hawks, caracaras, and falcons) and Strigiformes (owls). The MBTA authorizes the Secretary of the Interior (“Secretary”) to adopt suitable regulations to determine, inter alia, when, and to what extent, it may be permissible to hunt, take, capture, possess, sale, and transfer protected birds, bird parts, nests, and eggs.

Pursuant to the authority of the MBTA, the Secretary promulgated regulations to regulate falconry standards and falconry permitting …. 50 C.F.R. § 21.29(f)(9)(i) prohibits photographing or filming falconry raptors for “movies commercials, or in other commercial ventures.” 50 C.F.R. § 21.29(f)(9)(ii) prohibits falconers from photographing or filming their birds for “advertisements; as a representation of any business, company, corporation, or other organization; or for promotion or endorsement of any products, merchandise, goods, services, meetings, or fairs”—unless the promotion or endorsement is of “a nonprofit falconry organization or association” or “products or endeavors related to falconry.”

50 C.F.R. § 21.29(f)(8)(v) dictates that during conservation education programs, falconers “must provide information about the biology, ecological roles, and conservation needs of raptors … although not all of these topics must be addressed in every presentation.” …

In Count III of the FAC, Plaintiffs claim that 50 C.F.R. § 21.29(f)(9)(i) is a content-based restriction that violates the First Amendment. Section 21.29(f)(9)(i) states “You may not use raptors to make movies, commercials, or in other commercial ventures that are not related to falconry.”

In Count IV, Plaintiffs contend that 50 C.F.R. § 21.29(f)(9)(ii) is an unconstitutional restriction on commercial speech. ECF No. 16 at 15-16. 50 C.F.R. § 21.29(f)(9)(ii) states that falconers may not use their raptors for “commercial entertainment; for advertisements; as representation of any business … or for promotion … of any products [or] services … with the following exceptions: (A) … to promote … a nonprofit falconry organization … [and] (B) … to promote … products … related to falconry ….”

In Count V, Plaintiffs challenge 50 C.F.R. § 21.29(f)(8)(v) which requires falconers giving conservation education programs to provide “information about the biology, ecological roles, and conservation needs of raptors.”

In Count VI, Plaintiffs challenge the prohibitions on charging fees that exceed the amount required to recoup costs under 50 C.F.R. § 21.20(f)(8)(iv)….

The Supreme Court has recognized that various forms of entertainment and visual expression are purely expressive activities—including movies. Therefore, 50 C.F.R. § 21.29(f)(9)(i)’s restrictions on movies and § 21.29(f)(9)(ii)’s restriction on commercial entertainment go beyond restricting expressive conduct and restrict purely expressive activity.

The restriction compelling the content of falconers’ conservation education program under 50 C.F.R. § 21.29(f)(8)(v) is clearly a content-based restriction because it explicitly restricts the topic of the speech that can be discussed: “you must provide information about the biology, ecological roles, and conservation needs of raptors ….” … The regulation unequivocally discriminates based on the topic of the educational presentation.

“A statute is presumptively inconsistent with the First Amendment if it imposes a financial burden on speakers because of the content of their speech.” Simon & Schuster, Inc. v. Members of N.Y. State Crime Victims Bd., 502 U.S. 105, 115 (1991). 50 C.F.R. § 21.29(f)(8)(iv) limits the fee that falconers can charge when giving a conservation education program. Therefore, this regulation imposes a financial burden on falconers depending on the content of their presentation….

The Federal Defendants do not argue in the motion to dismiss that the regulations restrict excludable speech (i.e. obscenity), or that the regulations are valid time, place, and manner restrictions. See Ward v. Rock Against Racism, 491 U.S. 781, 791 (1989). It is inconsequential that falconers could merely use nonnative raptors to engage in the prohibited activities. Because the restrictions are content based, they are not subject to reasonable time, place, and manner restrictions. Id. (the government may impose reasonable time, place, and manner restrictions, provided the restrictions are justified without reference to the content of the regulated speech). The Federal Defendants provide no such support that the restriction on use of native raptors is no less a restriction on falconers’ speech.

In addition, the Federal Defendants make no argument in the motion to dismiss that the content-based restrictions pass strict scrutiny. Thus, the Federal Defendants’ motion to dismiss Counts III, IV, V, and VI on the grounds that the regulations do not restrict protected speech is DENIED….

Next, the Federal Defendants contend that, assuming the speech restricted by the regulations is protected speech, the regulations do not violate the First Amendment because they are permissible regulations on commercial speech. {As discussed below, even assuming the speech regulations are aimed at only commercial speech, the Court finds that Defendants are not entitled to dismissal. In light of that finding and because the First Amendment test for commercial speech is less stringent, at this stage, the Court is not required to determine definitively the commercial or noncommercial nature of speech being restricted.} …

In the present case, the limits on “commercials,” under §§ 21.29(f)(9)(i) and “advertisements,” under subsection (ii), standing alone, are restrictions on commercial speech. However, restrictions on film (movies), photography, or on commercial entertainment are not restrictions on commercial speech. See ETW v. Jireh Pub., Inc., 332 F.3d 915, 925 (6th Cir. 2003) (holding “prints,” or copies, of paintings were not commercial speech because they did not propose a commercial transaction); see also Anderson, 621 F.3d at 1060 (recognizing various forms of entertainment and visual expression—including movies—are purely expressive activities). Thus, §§ 21.29(f)(9)(i) & (ii) place restrictions on commercial speech— advertisements, commercials, and promoting a business or product—and on non-commercial, fully-protected speech….

The Court evaluates restrictions on commercial speech using the four-part test in Central Hudson: “(1) if the communication is neither misleading nor related to unlawful activity, then it merits First Amendment scrutiny as a threshold matter; in order for the restriction to withstand such scrutiny, (2) [t]he State must assert a substantial interest to be achieved by restrictions on commercial speech; (3) the restriction must directly advance the state interest involved; and (4) it must not be more extensive than is necessary to serve that interest.” …

Plaintiffs argue that Defendants cannot make the showing on the fourth prong that the restrictions fit the government’s interest at the motion to dismiss stage. Where the challenged regulation is a content-based restriction subject to strict scrutiny, the issue of whether the challenged restrictions adequately fit the government interest was a question for summary judgment or trial. Frudden v. Pilling, 742 F.3d 1199, 1207-08 (9th Cir. 2014). The summary judgment process requires defendants to show a compelling government interest and permits plaintiffs an opportunity to present countervailing evidence.

The Court acknowledges Defendants have a substantial interest in protecting native raptors. In arguing that the regulations meet the fourth prong as a matter of law, the Federal Defendants claim that “the regulations are directed specifically at commercial endeavors, with a limited carve-out for falconry related undertakings.” ECF No. 24-1 at 19. However, in light of Frudden, the present record is not developed sufficiently. Accordingly, the Federal Defendants’ motion to dismiss the challenges to 50 C.F.R. § 21.29(f)(9)(i) and (ii) (Counts III & IV) on the theory that they are permissible commercial speech restrictions is DENIED….

In Count VI (Second Count), Plaintiffs claim that the California regulation, 14 C.C.R. § 670(h)(13)(A), violates the First and Fourteenth Amendments in the same way that the federal regulations do. This regulation states: “Education and Exhibiting. A licensee may use raptors in his or her possession for training purposes, education, field meets, and media (filming, photography, advertisements, etc.), as noted in 50 CFR 21, if the licensee possesses the appropriate valid federal permits, as long as the raptor is primarily used for falconry and the activity is related to the practice of falconry or biology, ecology or conservation of raptors and other migratory birds. Any fees charged, compensation, or pay received during the use of falconry raptors for these purposes may not exceed the amount required to recover costs.”

Like the federal regulations in Counts III, IV, V, and VI, this regulation is also a restriction of expressive activity based on content. It demands that when using the raptors in presentations or media, the content must be related to falconry. Section 670(h)(13)(A) also imposes a restriction on compensation that corresponds to the federal regulations. The State Defendants argue that § 670(h)(13)(A) does not ban speech. For the same reasons stated above that the federal regulations are content-based restrictions on expressive activity, the Court rejects this argument. Because the regulations are content based, they are presumptively unreasonable and subject to strict scrutiny review.

Next, the State Defendants contend that should falconers desire to use raptors for exhibiting or commercial uses not authorized in § 670(h)(13)(A), they may obtain the appropriate permit to engage in such activity. It is somewhat unclear what State Defendants are pecking at. The Court has reviewed the falconry regulations raised by the parties. It is possible there is a separate regulatory regime that supports State Defendants’ argument that falconers can obtain a separate permit to engage in the prohibited activities. State Defendants have not identified any such alternative regulations or laws.

The language of the regulations does not support the State Defendant’s position.14 C.C.R. § 670(h)(13)(A) provides “A licensee may use raptors in his or her possession for training purposes, education field meets, and media (filming, photography, advertisements, etc.), as noted in 50 CFR 21, if the licensee possesses the appropriate valid federal permits, as long as the raptor is primarily used for falconry and the activity is related to the practice of falconry or biology, ecology or conservation of raptors and other migratory birds.” By this provision’s plain language, it does not appear that a falconer could seek a permit to give a talk with the raptor that is unrelated to the practice of falconry. For instance, even with an exhibiting permit under 14 C.C.R. § 671.1(b)(6), a falconer could not give a presentation using her raptor about her political or religious views, or throw a Harry Potter party for a relative, because these topics are not related to the practice of falconry or the biology, ecology, or conservation of raptors. Furthermore, it is notable that the provision requires the licensee to possess the “appropriate valid federal permits.” Thus, the Court rejects the State Defendants’ argument that Count VI (Second Count) fails to state a claim for relief on the theory Plaintiffs could simply get a separate federal permit….

[T]he strength of the government’s interest for the challenged regulations and the fit of those interests to the speech restrictions at issue are material to the Court’s preliminary injunction analysis for all three categories of the First Amendment challenges.

The Court tentatively finds that the government has a strong interest in protecting the native raptor species, but because the briefing has failed to sufficiently discuss any aspect of fit, and because the Court is responsible for evaluating how a preliminary injunction would impact the public interest, the Court must hear from the Federal and State Defendants before it takes any action.

For example, it is unclear from the present record whether prohibiting falconers from earning money for educational presentations is a narrowly-tailored solution to combat a marketplace for the protected birds. Federal and State Defendants must discuss why the restrictions on falconers’ ability to give presentations and to film and photograph their birds meet strict scrutiny.

As with analyzing the restrictions on falconers’ ability to give presentations and film their birds, the Court will need supplemental briefing to thoroughly analyze whether the compensation restrictions are narrowly tailored to achieve the government’s interest. Federal and State Defendants must discuss why the compensation restrictions meets strict scrutiny.

As to the third category relating to commercial speech, the Federal Defendants contend that the regulations affecting commercial transactions of falconers are necessary to prevent a market for the protected birds from developing. Federal Defendants argue that lifting the regulations would undermine the goal of falconry raptor preservation and cause detrimental effects on the protected species….

Under Central Hudson, the restriction must not be more extensive than necessary to serve the government interest. The test is sometimes phrased as requiring a “reasonable fit” between the government’s legitimate interests and the means it uses to serve those interests, or that the government narrowly tailors the means to meet its objective….

At present, the Federal and State Defendants’ briefing does not explain how the regulations are not more extensive than necessary to serve an important state interest…. The State Defendants similarly do not address how the restrictions on commercial speech are not more extensive than necessary to promote the health and welfare of raptors. Therefore, on the present record, the Court cannot determine if the restrictions on commercial speech are not more extensive than necessary to serve these interests.

The Court will order the Federal and State Defendants to submit supplemental briefing with respect to these narrow issues. The Defendants should discuss the nature of the government interest involved and how the three categories of speech restrictions (falconers’ presentations and media, compensation, and commercial speech) are drawn to meet such interest. Lastly, Defendants should provide an analysis for the third and fourth prongs of the Winter test: the balance of equities and the public interest. Plaintiffs will then have an opportunity to respond….

The State and Federal Defendants are ordered to file supplemental briefs addressing the state interest(s) in the regulations challenged under the First Amendment and how those speech restrictions are tailored to achieve those interests, and relatedly, the balance of equities and the public interest prongs under Winter…. The Defendants shall have 30 days from the date of this order to file the briefs. Toucan, of course, play at this game, so Plaintiffs will then have 30 days from the date they are served with both State Defendants’ and Federal Defendants’ briefs to file a responsive brief….

from Latest – Reason.com https://ift.tt/2GrUDWc

via IFTTT

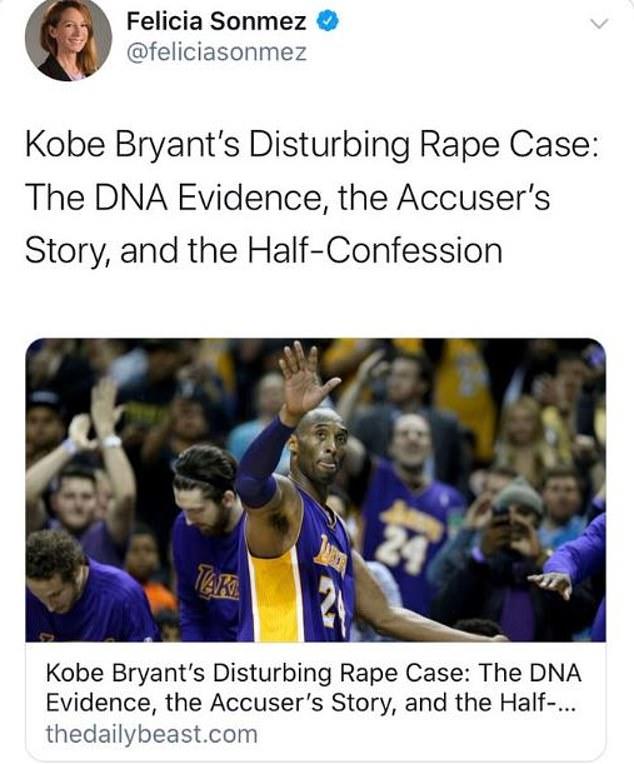

WaPo, CNN Reporters Spark Massive Backlash With ‘Kobe Was A Rapist’ Tweets

What kind of sensible person would feel compelled to call Kobe Bryant a rapist and trash his legacy in the hours after the devastating helicopter crash that left the NBA legend and his daughter, Gianna, dead? Unsurprisingly, the answer to that question is staff reporters at CNN and the Washington Post, among other media outlets.

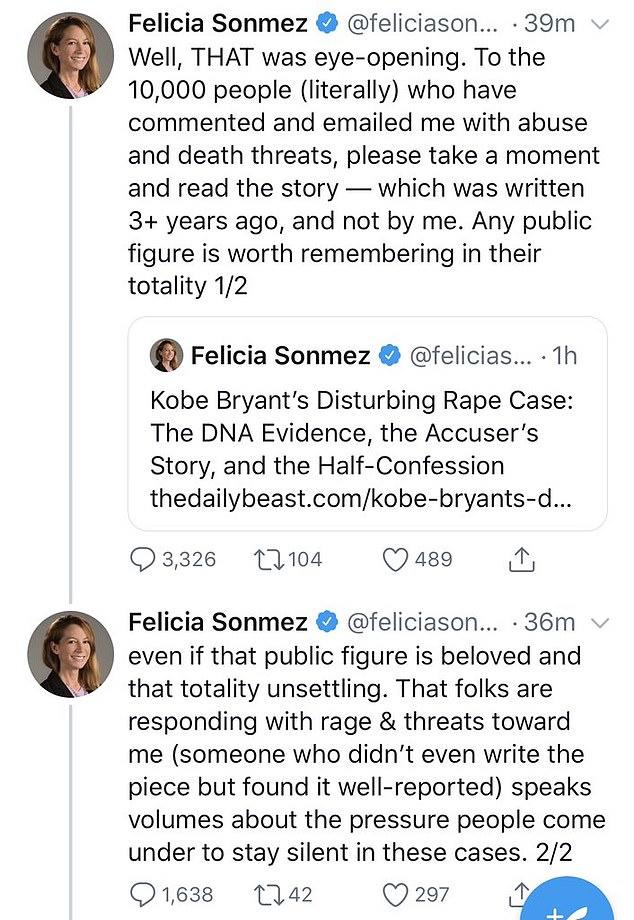

Bryant and his daughter were on their way to a travel basketball game. The victims in the crash also included another player and a parent. But that didn’t stop the Washington Post’s Felicia Somnez from sending a controversial tweet reminding the world about Bryant’s “disturbing” rape case. The tweet was deleted, but a screenshot was preserved and published by the Daily Mail.

Sonmez said she received death threats after posting the tweet, and added that she was inundated with more than 10,000 harassing and insulting messages in the wake of her tweet.

We find it difficult to believe that she didn’t anticipate this reaction. And unfortunately for her, this play for sympathy in the aftermath has decidedly backfired.

Of course, Bryant is a ‘rapist’ at the moment of his death, but Fidel Castro was simply “Cuban dictator” – where were the reminders of the atrocities committed by his government?

According to the Mail, Sonmez, a political reporter at WaPo, has been suspended from her position.

In response to Sonmez’s claims that she was merely remembering Bryant’s legacy “in totality,” one twitter user cut right to the heart of why her tweet infuriated thousands of people.

The backlash was just as intense after CNN’s Nathan McDermott tweeted about the “very credible rape allegation” made against Bryant, neglecting to mention that the charges were dropped and the victim admitted she went on to have sex with another man less than a day after the incident with Bryant.

Yes Kobe Bryant was one of the greatest basketball players of all time, but he’s also faced a very credible rape accusation where the woman was choked and submitted to a rape-kit test which found injuries “not consistent with consensual sex.”https://t.co/HsItwC7VaC

Think whatever you want about him, but if you think this is immaterial and shouldn’t be talked about in the aftermath of his death, well, I think you’re wrong.

Even reporters with obscure sports media organizations managed to incite a massive backlash (and boost their own profile) with their critical Kobe tweets. One reporter with College Hockey News decried the “sick” people on twitter for inundating her with insults after she had the “audacity” to suggest that “sexual assault victims deserve compassion too” in the hours after the crash.

We can have multiple feelings – be heartbroken over a tragic death, send thoughts & prayers to a family and also hold compassion for survivors

You people are incredibly sick and have a true talent for truly not interpreting things correctly. You’re way off base here for many reasons and you can also keep your thoughts to yourself because no one asked you https://t.co/BbifKKsXp3

Actress Evan Rachel Wood called Bryant a “rapist”.

What has happened is tragic. I am heartbroken for Kobe’s family.

He was a sports hero. He was also a rapist.

And all of these truths can exist simultaneously.

Your gonna turn #MeToo into a joke. These things need to be taken seriously and your just looking for attention after him and his daughter JUST died. Wow. ERW, Amazing Actress, shes also an narcissistic disappointment.

It looks like the account that tweeted this had to delete for harassment, so I’ll just quote it. “My thoughts are with Kobe Bryant’s rape victim who will spend the next week hearing about how beloved and great her rapist was.”

As a reminder of how much Bryant meant to millions of fans:

Want to know what Kobe Bryant meant to LA? My neighbor who loves playing basketball has been out here like this for a good 20 minutes with his Lakers basketball. #RIPMAMBApic.twitter.com/pdvm0LEk4U

Oh, and let’s not forget the New York Times,LA Times and other media organizations highlighting Bryant’s “complicated” legacy. WaPo also caught some flack for describing Bryant as a “controversial” figure in the opening paragraphs of its obituary.

Washington Post treated Soleimani and Al Baghdadi with more respect than they gave Kobe

You want to show compassion for ‘survivors’ living with trauma? How about showing some compassion for the Bryant family and the millions of people devastated by the deaths of Bryant and his 13-year-old daughter?

Wuhan Mayor Offers To Resign As Coronavirus Death Toll Accelerates, Supply Shortages Intensify

Investors who dismissed the threat to their P&Ls posed by China’s coronavirus outbreak are suddenly realizing that they’ve made a grave miscalculation. What few Asian markets were open on Monday (most were closed for the LNY holiday) saw equities tank, and in the US, futures are pointing to a steep drop at the open – a sign that the market has found the excuse it needed to give back some of its torrid January gains.

With so much going on – the Bolton revelations, the deaths of Kobe Bryant and his daughter, the busiest week of earnings season, and the upcoming Fed meeting – the virus remains the most dominant theme – and with good reason.