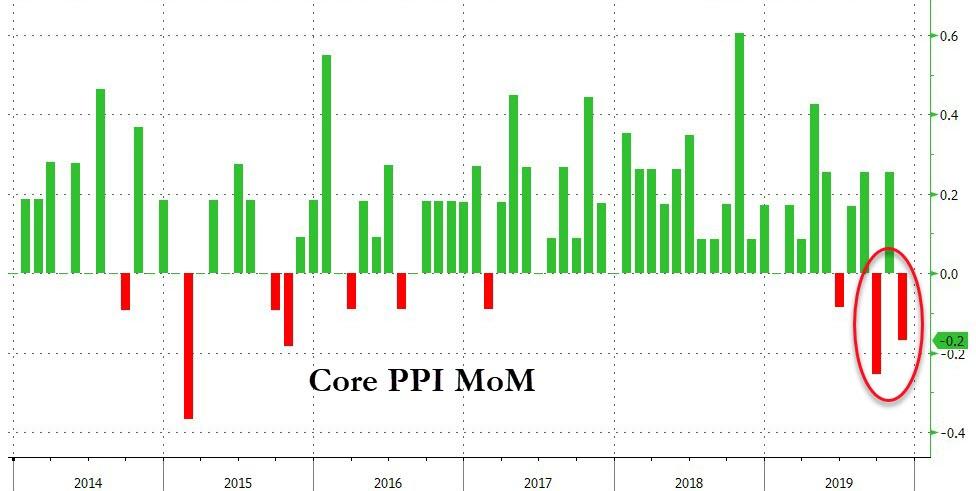

US Producer Prices Grow At Slowest Pace In Over 3 Years

Following yesterday’s bigger than expected rise in consumer prices (driven by surging services costs), US producer prices were expected to accelerate after slowing dramatically in recent months, but it didn’t with core PPI dropping 0.2% MoM and headline PPI holding at just 1.1% YoY – the lowest since September 2016.

Source: Bloomberg

Core PPI fell 0.2% MoM – dispelling more of the narrative that President Trump’s tariff threats will crush the average American with cost increases…

Source: Bloomberg

Notably, while Consumer Services costs surged in November, Producer Services costs slid 0.3% (with Trade -0.6%).

Watch Live: Christine Lagarde’s First Press Conference As ECB President

Having got through the ECB statement release unscathed with no changes or surprises, all eyes are now on Christina Lagarde’s first press conference appearance as ECB president.

The focus will fall on how Lagarde intends to run the central bank, and its upcoming strategic policy review, which will likely be formally announced at the December confab; but there is a risk that this meeting will be light on details, which may possibly result in horizontal price action. Many believe Lagarde’s first task will be uniting a divided Governing Council, where there are mixed views on the efficacy and risks of loose(r) policy, as well as the practicalities of the ECB’s decision-making functions.

Lagarde is also expected to reiterate her call on fiscal authorities to do more to support the Eurozone economy. Elsewhere, updated economic projections may see near-term growth forecasts nudged up slightly, though further forecasts are subject to downside risks; inflation forecasts are seen little changed.

Today’s press conference may reveal more information about this, and could come with a formal announcement on the review. And among many other policy/mission tweaks for the convicted criminal-cum-central banking climate crusader, Rabobank sarcastically adds, “will it include a pledge to also do ‘whatever it takes’ to get to the Eurozone to net-zero carbon emissions?“

Apple Shares Slide After Credit Suisse Reports Plunge In China iPhone Shipments

Apple share were already sliding in the pre-market session as tariff fears re-emerged but a report from Credit Suisse that iPhone shipments fell meaningfully in November sparked considerably more selling pressure.

In fact, CS says iPhone shipments in China dropped a shocking 35.4% YoY in November (following a 10.3% YoY drop in October). This compares to a 0.2% increase in the broader regional smart phone market. Additionally, CS reports that total shipments in China are now down 7.4% since the launch of the iPhone 11 line.

Luckily, Apple stopped reporting iPhone unit sales so this will soon be forgotten (or not).

No Changes Or Surprises From ECB In Lagarde’s First Meeting

In her first policy meeting as head of the ECB, Christine Lagarde left the uber-dovish momentum put in place by her predecessor, Mario Draghi, untouched, and moments ago the ECB kept all its three rates unchanged as expected, noting that rates would remain “at their present or lower levels” until the ECB nears its inflation goal, i.e. never, and that the ECB will continue buying €20BN in bonds until “shortly before it starts raising the key ECB interest rates” (or until it runs out of German bonds to buy, whichever comes first). In short no surprises, and the market reacted accordingly, with the EURUSD and bunds not even pretending to move.

Full statement below:

At today’s meeting the Governing Council of the European Central Bank (ECB) decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

On 1 November net purchases were restarted under the Governing Council’s asset purchase programme (APP) at a monthly pace of €20 billion. The Governing Council expects them to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

And now attention turns to Lagarde’s first press conference and – in continuation of a trope started under her predecessor – what color tie she will be wearing (we jest; we know the only accessory with her will be her money-printing Berkin). As a reminder, in her first speech, Lagarde stated that the ECB’s strategic review would begin soon.

As such, today’s press conference may reveal more information about this, and could come with a formal announcement. And among many other policy/mission tweaks for the convicted criminal-cum-central banking climate crusader, Rabobank sarcastically adds, “will it include a pledge to also do ‘whatever it takes’ to get to the Eurozone to net-zero carbon emissions?“

China Warns It Will Retaliate After Reuters Reports Trump Will Proceed With Dec 15 Tariffs

A report claiming that President Trump would be meeting with senior aides on Thursday to discuss whether the US should move ahead with its next round of tariffs has apparently rankled the higher-ups in Beijing. Because Global Times editor Hu Xijin, a popular mouthpiece for the Communist Party, tweeted a rebuttal Thursday morning, warning that “China will surely retaliate” If Washington moves ahead with the Dec. 15 tariffs.

“Such a trade war escalation scenario has been played several times,” Hu warned, referring to the previous truces declared between China and the US during the 17-month trade fight, before adding that history would reflect poorly on Trump for walking away from the table.

Impose tariffs, China will surely retaliate, such a trade war escalation scenario has been played several times. Washington won’t be so naïve to still believe it can crush China, will it? A trade war that doesn’t result in a trade deal will only be completely denied by history. pic.twitter.com/sZZkODlI1X

The warning from Beijing is clear: If Washington moves ahead with the tariff hikes, there will be hell to pay, and we can forget about a trade deal before next year’s election; meanwhile Beijing will do everything in its power to crash US stocks.

Reuters initially reported that Treasury Secretary Steve Mnuchin, US Trade Rep. Robert Lighthizer, and White House advisers Larry Kudlow and Peter Navarro would be involved in the meeting.

“I’m expecting them to raise the tariffs on Sunday,” one “source” told Reuters, who is very likely Peter Navarro who is using Reuters as a trial balloon conduit, while Larry Kudlow uses Bloomberg and the WSJ. “The administration is preparing its talking points about how that’s the right thing to do. The message is that it will not be painful.”

Recently, Peter Navarro, the Trump advisor and one of the administration’s top trade hawks, warned during an interview with Fox Business that Beijing has recently mastered the art of “shaping the narrative” with strategic leaks to Western media, claiming that trade-related leaks from earlier in the week “came from the Chinese not our side.”

Navarro, a China hawk, also circulated a separate memo in favor of continued tariffs, arguing that China had increased its purchases of U.S. pork and soybeans solely because of its domestic swine fever outbreak, and that tariffs were not having a negative effect on U.S. growth or the stock market.

The Navarro-penned document and separate memos said tariffs imposed by the Trump administration on China over the past year-and-a-half had not been as devastating as critics had argued, a view not shared by many economists.

“The message is that it will not be painful,” said the one source familiar with the administration’s thinking. “People have been proclaiming for a year and half that the sky is falling, and the sky isn’t falling yet.”

Will Lagarde Pledge To Do “Whatever It Takes” To Fix Climate Change?

Authored by Michael Every of Rabobank

Noughts: As Philip Marey notes here, the FOMC kept the target range for the Federal Funds rate unchanged yesterday, and the dot plot continued to show the Fed on hold in 2020, before hiking in 2021 and 2022. In other words, no change for a year, so when we go away for Xmas we can effectively stay away for as long as we want. However, Powell was rather dovish, stressing that there was less reason to hike than after previous mid-cycle adjustments in the 1990s because there is now less upward pressure on inflation. (As headline US CPI printed a tick above expectations at 2.1% y/y and core at 2.3%.)

Powell was sanguine about the problems in the repo markets, despite market chatter that the complete opposite stance was more logical, and said that temporary upward pressures were not uncommon year end, and they appear to be manageable. He also did not seem to be in a hurry to introduce a standing repo facility and said that the Fed was at the moment more focused on treasury bill purchases and looking into supervisory and regulatory issues affecting repo. However, he showed willingness to buy coupons, in addition to T-bills, in the balance sheet expansion program if necessary. Does that make NOT QE into QE, one wonders? Or is it still NOT QE if they claim that’s what it is?

Philip thinks that we may still see some Fed action before year end, of course only ‘technical.’ For example, he has already explained that if the Fed does not develop better tools to control the repo markets – such as a standing repo facility -, it is only a matter of time before we get another episode of repo stress

All in all Philip concludes that while the Fed thinks it has everything under control, the same forecasting framework that helped us pinpoint the end of the Fed’s hiking cycle in 2019 is also indicating that the FOMC will have to cut rates all the way back to zero before the end of 2020. In short, enjoy that Xmas break – because you will need it.

How did the market react? With 10-year Treasuries closing down around 5bp to below 1.80% again, and 2-years around 4bp at 1.61% and hence the curve flattening; equities marginally in the green again; and the broad USD index in the red again.

Crosses:Today is election day in the UK, where millions get to put an X on a bit of paper to try to find the solution to the complex set of socioeconomic problems besetting the not-so United Kingdom. It seems appropriate for a country addicted to schlocky TV reality show ‘Love Island’, and with an education system that has produced a contestant that claims to not understand the difference between a city, a county, a country, and Europe, that this election revolves around issues such as ‘is Liverpool is in Europe?’; and that PM Johnson has an election video calling to “Get Brexit Done” in the style of the movie ‘Love, Actually’. In which case we can portmanteau that the UK is now ‘Love Island, Actually’. There just isn’t a lot of love to go round.

Stefan Koopman has produced a detailed dive into the election, which is available here. He concludes that It is easier for BoJo to win a parliamentary majority in an election than to win a popular majority in a People’s Vote, but that assuming that clarity on Brexit is the only thing that is broadly desired, party allegiances could potentially break down; indeed, the election will be dominated by tactical voting. The greatest likelihood is of a Tory majority, but other outcomes are still easily possible. In short, we either have PM BoJo, heading straight towards a further set of cliff-edge negotiations with the EU over a trade deal and with a risk of Hard Brexit and/or Scottish independence looming this time next year; PM Corbyn, and the kind of socialism that will see champagne socialists in the City clutching their rosary beads, and again a call for Scottish independence; or a hung parliament, and more of the purgatory of the past five years. To quote Woody Allen: “More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly.”

Noughts: Meanwhile, there is another big nought today in the form of the ECB meeting, the first led by President Lagarde. Our ECB watchers Bas van Geffen and Elwin de Groot don’t expect any changes at this juncture – thus the nought (their full preview is here). However, some doubts were expressed about the inflation assumptions in the October ECB meeting. We think that the bleak outlook for 2020 (close to nought for GDP growth and CPI?) will eventually force the ECB’s hand on policy again. In her first speech, Ms. Lagarde stated that the ECB’s strategic review would begin soon. The press conference today may reveal more information about this, and could come with a formal announcement. Among many other policy/mission tweaks, will it include a pledge to also do ‘whatever it takes’ to get to the Eurozone to net-zero carbon emissions?

From Monday’s decision by Judge Jesse M. Furman in Usherson v. Bandshell Artist Mgmt. (S.D.N.Y.):

Pending before the Court in this copyright case is Defendant Bandshell Artist Management’s motion for sanctions against Plaintiff and Plaintiff’s counsel, Richard Liebowitz—a frequent target of sanctions motions and orders imposing sanctions in this District…. “In his relatively short career litigating in this District, Richard Liebowitz has earned the dubious distinction of being a regular target of sanctions-related motions and orders. Indeed, it is no exaggeration to say that there is a growing body of law in this District devoted to the question of whether and when to impose sanctions on Mr. Liebowitz alone.” …

Defendant’s motion turns in large part on the veracity of factual representations that Liebowitz has made to the Court, some under oath. In particular, Liebowitz asserts that a mediator in the Court-annexed Mediation Program gave advance permission by telephone for (1) an associate to appear instead of Liebowitz at an October 31, 2019 in-person mediation, and (2) Plaintiff Arthur Usherson to appear telephonically at the mediation, rather than in person. Defense counsel asserts that those representations are false—and that the mediator (the “Mediator”) has indicated that, if called upon to do so, would testify to that effect. Determining the truth or falsity of Liebowitz’s assertions is critical to the integrity of both the proceedings before the Court and the Court-annexed Mediation Program itself.

[Footnote moved:] Notably, Liebowitz’s veracity has already been found wanting by other Judges on this Court. See, e.g., Nov. 13, 2019 Minute Entry, Berger v. Imagina Consulting, Inc., 18-CV-8956 (CS) (noting a finding on the record at a conference held on November 13, 2019, that Liebowitz had “willfully lied to the Court”); Sands v. Bauer Media Group USA, LLC, No. 17-CV-9215 (LAK), 2019 WL 6324866, at & n.1 (S.D.N.Y. Nov. 26, 2019) (describing several statements made by Liebowitz as “false”).

Determining the truth or falsity of Liebowitz’s assertions, however, requires delving into an area that is usually beyond the scrutiny of the Court and the public. That is, to repurpose a familiar phrase, what happens in mediation is generally supposed to stay in mediation. See, e.g., Rule 2(a), Procedures of the S.D.N.Y. Mediation Program (Dec. 26, 2018) (“Mediation Rules”) (providing that communications made “exclusively during or for the mediation process shall be confidential”), available at https://ift.tt/2PyYIMg; see also, e.g., In re Teligent, Inc., 640 F.3d 53, 57 (2d Cir. 2011) (“Confidentiality is an important feature of the mediation and other alternative dispute resolution processes.”). The general rule of confidentiality is eminently sound. As the Second Circuit has explained, “confidentiality is ‘essential’ to [the] … vitality and effectiveness” of mediation. “Promising participants confidentiality in [mediation] proceedings promotes the free flow of information that may result in the settlement of a dispute, and protect[s] the integrity of alternative dispute resolution generally.”

That said, there are important exceptions to the rule of confidentiality in the mediation context…. [T]here are cases in which the strong interest in preserving confidentiality in mediation must—and does—give way to other, even weightier interests.

This is such a case. On October 7, 2019, the Court ordered the parties to comply with the Court’s prior Mediation Referral Order, by participating in an “in-person mediation no later than October 31, 2019.” The parties agreed to hold the mediation on the very last possible day—October 31, 2019—but neither Liebowitz nor his client appeared. Instead, two associates from Liebowitz’s firm—neither of whom had (or has since) entered an appearance on behalf of Plaintiff and neither of whom had much, if any, knowledge of the case—arrived and confirmed that Liebowitz and Plaintiff would not be attending in person. After Liebowitz’s associates, Defendant, and defense counsel spoke briefly with Plaintiff on the phone—the details of their conversation are not relevant to Defendant’s motion and, thus, need not be made public—the mediation ended without a resolution.

Liebowitz does not dispute that he and his client failed to appear in person at the mediation, but he contends that the Mediator gave him advance permission to send an associate in his place and for Plaintiff to appear by telephone. Specifically, at a conference before the Court on November 14, 2019, Liebowitz stated on the record that he had “personally advised” the Mediator “before the mediation” that Plaintiff would not appear in person and that the Mediator had “said that was okay.” {It is worth noting that the November 14, 2019 conference was only one day after Liebowitz had appeared before Judge Seibel in connection with the contempt proceedings in Berger, a proceeding in which he was taken to task for lying to the Court.} Several days later, Liebowitz repeated this claim in a sworn declaration, and further averred that he had obtained the Mediator’s permission for Freeman to appear as counsel instead of himself. Liebowitz made the same claims in Plaintiff’s opposition to the sanctions motion. As noted, defense counsel disputes these assertions, stating in a declaration currently filed under seal that the Mediator told counsel that the Mediator never gave Liebowitz such permission and that the Mediator would testify to that effect if called as a witness.

The need to resolve this dispute—and to rule on Defendant’s motion—justifies a limited inquiry into Liebowitz’s communications with the Mediator. Only the Mediator can clarify whether he did, in fact, give Liebowitz advance permission to depart from the Mediation Program’s rules, which applied to the mediation by virtue of Local Civil Rule 83.9. These Rules mandate attendance by “[e]ach party”; mandate attendance “by the lawyer who will be primarily responsible for handling the trial of the matter”; and allow a party who “resides more than 100 miles from the Courthouse” for whom in-person appearance “would be a great hardship” to participate by telephone, but only with the permission of the assigned mediator. Shedding light on these issues is critical for determining whether Liebowitz complied with the Court’s Orders (which incorporated the Local Rules and the Mediation Rules by reference) and whether Liebowitz was truthful in his representations to the Court—some made under penalty of perjury.

The Court does not call upon the Mediator to involve himself further in this litigation lightly. A mediator should generally not be dragged into litigation beyond the mediation itself—both to protect the confidentiality of mediation communications and (mindful that the lawyers who serve as mediators in this Court’s Mediation Program do so on a volunteer basis) to avoid disincentivizing lawyers from serving as mediators. In the unique circumstances of this case, however, it is necessary to call upon the Mediator to provide evidence.

To minimize the burdens on him (and the Mediation Program generally), the Court will carefully limit the evidence required from the Mediator regarding his communications with Liebowitz. Moreover, rather than holding an evidentiary hearing in the first instance, the Court will proceed in steps, beginning with a declaration from the Mediator. In particular, the Mediator shall submit a declaration detailing any and all communications with Liebowitz regarding Liebowitz’s personal attendance at the mediation and Plaintiff’s participation by telephone in the mediation. The Mediator should specify whether (and if so, when and how) he gave Liebowitz permission (1) not to appear personally at the mediation (and to send an associate instead); and (2) for Plaintiff not to appear at the mediation in person and to appear by telephone instead.

Significantly, limiting the Mediator’s disclosures to these issues protects the confidentiality of the information discussed at the mediation itself, which is the primary focus of the rule of confidentiality. That is, the Court’s inquiry concerns only a narrow set of communications about procedural matters that occurred before the mediation proper—not communications about the substance of the case or the parties’ settlement negotiations. Indeed, although Liebowitz casts aspersions on the conduct and good faith of Defendant and defense counsel during the mediation itself in his opposition papers, the Court will not permit inquiry into such matters. These allegations have no bearing on the veracity of Liebowitz’s representations to the Court or the Court’s resolution of Defendant’s sanctions motion—and impinge more directly on the core of the rule of confidentiality….

Moreover, this case falls squarely within the exceptions to the rule of confidentiality recognized by the Second Circuit …. Liebowitz’s representations to the Court in response to Defendant’s sanctions motion, including some under penalty of perjury, have created a special need for the confidential material. Failing to discover the limited information necessary to resolve this factual dispute would not only result in unfairness to Defendant, but would also threaten the integrity of the proceedings before the Court and the integrity of the Court-annexed Mediation Program itself. Given the nature of the communications sought and the careful restrictions the Court has drawn, any remaining interest in confidentiality is outweighed by the need for the Mediator’s evidence….

There is one more matter impinging on the general rule of confidentiality that the Court must address: whether and to what extent the Mediator’s declaration, the transcript of the November 14, 2019 conference, the motion papers filed thus far, and any future filings and proceedings should be made public. “Given the interest in maintaining the confidentiality of negotiations and discussions conducted as part of the Court-annexed Mediation Program,” the Court issued an Order on November 20, 2019 that temporarily sealed any filings made in connection with the sanctions motion pending a final determination by the Court and directed the parties to file letters stating “their views on whether and to what extent the motion filings should remain under seal given the strong presumption in favor of public access to judicial documents.” Amazingly, Liebowitz did not comply with the Court’s Order by filing a letter. Defendant did comply, stating that sealing is not necessary.

For the most part, the Court agrees with Defendant and concludes that the presumption in favor of public access to judicial documents and judicial proceedings requires that the filings and proceedings relating to the sanctions motion should be public. The presumption in favor of public access is especially weighty here, as Defendant has filed a formal motion asking the Court to exercise its coercive authority in the form of sanctions.

In addition, the public has a strong interest in knowing about the additional aspersions cast on Liebowitz’s truthfulness. Following the Court’s warning to “be very, very, very careful” about any representations made to the Court, Liebowitz repeatedly asserted—both in person and in filings—that his and his client’s absences from the mediation were justified because he had received permission in advance. The public—including other litigants—and other judges who may come into contact with Liebowitz, a frequent litigant in this District, have an interest in the Court’s determination of the veracity of these representations.

By contrast, the considerations cutting against public access here are generally weak. As discussed, the interest in confidentiality with respect to the communications that are relevant to the Court’s inquiry is limited. The parties have also expressed no objections to unsealing. Nevertheless, the Court concludes that some redactions are warranted to preserve the confidentiality of substantive mediation discussions and the integrity of the Mediation Program. Specifically, the allegations made in the parties’ submissions about the parties’ conduct at the mediation proper—and, in particular, the content of their negotiations—shall be redacted, as they have no bearing on the sanctions motion and directly implicate the core purpose of the rule of confidentiality. The same is true of the identities of the Mediator and court employees working in the Court-annexed Mediation Program, which shall also be redacted to protect their privacy. The Court finds that the presumption in favor of public access is much weaker as to those portions of the motion papers, and the countervailing interests are stronger….

The Director of the Court-annexed Mediation Program is directed to provide a copy of this Memorandum Opinion and Order to the Mediator, who shall submit a declaration, consistent with the directions above, by December 18, 2019…. Upon review of the Mediator’s declaration, the Court will decide what, if any, further proceedings are necessary to resolve Defendant’s motion.

from Latest – Reason.com https://ift.tt/38vYZbw

via IFTTT

From Monday’s decision by Judge Jesse M. Furman in Usherson v. Bandshell Artist Mgmt. (S.D.N.Y.):

Pending before the Court in this copyright case is Defendant Bandshell Artist Management’s motion for sanctions against Plaintiff and Plaintiff’s counsel, Richard Liebowitz—a frequent target of sanctions motions and orders imposing sanctions in this District…. “In his relatively short career litigating in this District, Richard Liebowitz has earned the dubious distinction of being a regular target of sanctions-related motions and orders. Indeed, it is no exaggeration to say that there is a growing body of law in this District devoted to the question of whether and when to impose sanctions on Mr. Liebowitz alone.” …

Defendant’s motion turns in large part on the veracity of factual representations that Liebowitz has made to the Court, some under oath. In particular, Liebowitz asserts that a mediator in the Court-annexed Mediation Program gave advance permission by telephone for (1) an associate to appear instead of Liebowitz at an October 31, 2019 in-person mediation, and (2) Plaintiff Arthur Usherson to appear telephonically at the mediation, rather than in person. Defense counsel asserts that those representations are false—and that the mediator (the “Mediator”) has indicated that, if called upon to do so, would testify to that effect. Determining the truth or falsity of Liebowitz’s assertions is critical to the integrity of both the proceedings before the Court and the Court-annexed Mediation Program itself.

[Footnote moved:] Notably, Liebowitz’s veracity has already been found wanting by other Judges on this Court. See, e.g., Nov. 13, 2019 Minute Entry, Berger v. Imagina Consulting, Inc., 18-CV-8956 (CS) (noting a finding on the record at a conference held on November 13, 2019, that Liebowitz had “willfully lied to the Court”); Sands v. Bauer Media Group USA, LLC, No. 17-CV-9215 (LAK), 2019 WL 6324866, at & n.1 (S.D.N.Y. Nov. 26, 2019) (describing several statements made by Liebowitz as “false”).

Determining the truth or falsity of Liebowitz’s assertions, however, requires delving into an area that is usually beyond the scrutiny of the Court and the public. That is, to repurpose a familiar phrase, what happens in mediation is generally supposed to stay in mediation. See, e.g., Rule 2(a), Procedures of the S.D.N.Y. Mediation Program (Dec. 26, 2018) (“Mediation Rules”) (providing that communications made “exclusively during or for the mediation process shall be confidential”), available at https://ift.tt/2PyYIMg; see also, e.g., In re Teligent, Inc., 640 F.3d 53, 57 (2d Cir. 2011) (“Confidentiality is an important feature of the mediation and other alternative dispute resolution processes.”). The general rule of confidentiality is eminently sound. As the Second Circuit has explained, “confidentiality is ‘essential’ to [the] … vitality and effectiveness” of mediation. “Promising participants confidentiality in [mediation] proceedings promotes the free flow of information that may result in the settlement of a dispute, and protect[s] the integrity of alternative dispute resolution generally.”

That said, there are important exceptions to the rule of confidentiality in the mediation context…. [T]here are cases in which the strong interest in preserving confidentiality in mediation must—and does—give way to other, even weightier interests.

This is such a case. On October 7, 2019, the Court ordered the parties to comply with the Court’s prior Mediation Referral Order, by participating in an “in-person mediation no later than October 31, 2019.” The parties agreed to hold the mediation on the very last possible day—October 31, 2019—but neither Liebowitz nor his client appeared. Instead, two associates from Liebowitz’s firm—neither of whom had (or has since) entered an appearance on behalf of Plaintiff and neither of whom had much, if any, knowledge of the case—arrived and confirmed that Liebowitz and Plaintiff would not be attending in person. After Liebowitz’s associates, Defendant, and defense counsel spoke briefly with Plaintiff on the phone—the details of their conversation are not relevant to Defendant’s motion and, thus, need not be made public—the mediation ended without a resolution.

Liebowitz does not dispute that he and his client failed to appear in person at the mediation, but he contends that the Mediator gave him advance permission to send an associate in his place and for Plaintiff to appear by telephone. Specifically, at a conference before the Court on November 14, 2019, Liebowitz stated on the record that he had “personally advised” the Mediator “before the mediation” that Plaintiff would not appear in person and that the Mediator had “said that was okay.” {It is worth noting that the November 14, 2019 conference was only one day after Liebowitz had appeared before Judge Seibel in connection with the contempt proceedings in Berger, a proceeding in which he was taken to task for lying to the Court.} Several days later, Liebowitz repeated this claim in a sworn declaration, and further averred that he had obtained the Mediator’s permission for Freeman to appear as counsel instead of himself. Liebowitz made the same claims in Plaintiff’s opposition to the sanctions motion. As noted, defense counsel disputes these assertions, stating in a declaration currently filed under seal that the Mediator told counsel that the Mediator never gave Liebowitz such permission and that the Mediator would testify to that effect if called as a witness.

The need to resolve this dispute—and to rule on Defendant’s motion—justifies a limited inquiry into Liebowitz’s communications with the Mediator. Only the Mediator can clarify whether he did, in fact, give Liebowitz advance permission to depart from the Mediation Program’s rules, which applied to the mediation by virtue of Local Civil Rule 83.9. These Rules mandate attendance by “[e]ach party”; mandate attendance “by the lawyer who will be primarily responsible for handling the trial of the matter”; and allow a party who “resides more than 100 miles from the Courthouse” for whom in-person appearance “would be a great hardship” to participate by telephone, but only with the permission of the assigned mediator. Shedding light on these issues is critical for determining whether Liebowitz complied with the Court’s Orders (which incorporated the Local Rules and the Mediation Rules by reference) and whether Liebowitz was truthful in his representations to the Court—some made under penalty of perjury.

The Court does not call upon the Mediator to involve himself further in this litigation lightly. A mediator should generally not be dragged into litigation beyond the mediation itself—both to protect the confidentiality of mediation communications and (mindful that the lawyers who serve as mediators in this Court’s Mediation Program do so on a volunteer basis) to avoid disincentivizing lawyers from serving as mediators. In the unique circumstances of this case, however, it is necessary to call upon the Mediator to provide evidence.

To minimize the burdens on him (and the Mediation Program generally), the Court will carefully limit the evidence required from the Mediator regarding his communications with Liebowitz. Moreover, rather than holding an evidentiary hearing in the first instance, the Court will proceed in steps, beginning with a declaration from the Mediator. In particular, the Mediator shall submit a declaration detailing any and all communications with Liebowitz regarding Liebowitz’s personal attendance at the mediation and Plaintiff’s participation by telephone in the mediation. The Mediator should specify whether (and if so, when and how) he gave Liebowitz permission (1) not to appear personally at the mediation (and to send an associate instead); and (2) for Plaintiff not to appear at the mediation in person and to appear by telephone instead.

Significantly, limiting the Mediator’s disclosures to these issues protects the confidentiality of the information discussed at the mediation itself, which is the primary focus of the rule of confidentiality. That is, the Court’s inquiry concerns only a narrow set of communications about procedural matters that occurred before the mediation proper—not communications about the substance of the case or the parties’ settlement negotiations. Indeed, although Liebowitz casts aspersions on the conduct and good faith of Defendant and defense counsel during the mediation itself in his opposition papers, the Court will not permit inquiry into such matters. These allegations have no bearing on the veracity of Liebowitz’s representations to the Court or the Court’s resolution of Defendant’s sanctions motion—and impinge more directly on the core of the rule of confidentiality….

Moreover, this case falls squarely within the exceptions to the rule of confidentiality recognized by the Second Circuit …. Liebowitz’s representations to the Court in response to Defendant’s sanctions motion, including some under penalty of perjury, have created a special need for the confidential material. Failing to discover the limited information necessary to resolve this factual dispute would not only result in unfairness to Defendant, but would also threaten the integrity of the proceedings before the Court and the integrity of the Court-annexed Mediation Program itself. Given the nature of the communications sought and the careful restrictions the Court has drawn, any remaining interest in confidentiality is outweighed by the need for the Mediator’s evidence….

There is one more matter impinging on the general rule of confidentiality that the Court must address: whether and to what extent the Mediator’s declaration, the transcript of the November 14, 2019 conference, the motion papers filed thus far, and any future filings and proceedings should be made public. “Given the interest in maintaining the confidentiality of negotiations and discussions conducted as part of the Court-annexed Mediation Program,” the Court issued an Order on November 20, 2019 that temporarily sealed any filings made in connection with the sanctions motion pending a final determination by the Court and directed the parties to file letters stating “their views on whether and to what extent the motion filings should remain under seal given the strong presumption in favor of public access to judicial documents.” Amazingly, Liebowitz did not comply with the Court’s Order by filing a letter. Defendant did comply, stating that sealing is not necessary.

For the most part, the Court agrees with Defendant and concludes that the presumption in favor of public access to judicial documents and judicial proceedings requires that the filings and proceedings relating to the sanctions motion should be public. The presumption in favor of public access is especially weighty here, as Defendant has filed a formal motion asking the Court to exercise its coercive authority in the form of sanctions.

In addition, the public has a strong interest in knowing about the additional aspersions cast on Liebowitz’s truthfulness. Following the Court’s warning to “be very, very, very careful” about any representations made to the Court, Liebowitz repeatedly asserted—both in person and in filings—that his and his client’s absences from the mediation were justified because he had received permission in advance. The public—including other litigants—and other judges who may come into contact with Liebowitz, a frequent litigant in this District, have an interest in the Court’s determination of the veracity of these representations.

By contrast, the considerations cutting against public access here are generally weak. As discussed, the interest in confidentiality with respect to the communications that are relevant to the Court’s inquiry is limited. The parties have also expressed no objections to unsealing. Nevertheless, the Court concludes that some redactions are warranted to preserve the confidentiality of substantive mediation discussions and the integrity of the Mediation Program. Specifically, the allegations made in the parties’ submissions about the parties’ conduct at the mediation proper—and, in particular, the content of their negotiations—shall be redacted, as they have no bearing on the sanctions motion and directly implicate the core purpose of the rule of confidentiality. The same is true of the identities of the Mediator and court employees working in the Court-annexed Mediation Program, which shall also be redacted to protect their privacy. The Court finds that the presumption in favor of public access is much weaker as to those portions of the motion papers, and the countervailing interests are stronger….

The Director of the Court-annexed Mediation Program is directed to provide a copy of this Memorandum Opinion and Order to the Mediator, who shall submit a declaration, consistent with the directions above, by December 18, 2019…. Upon review of the Mediator’s declaration, the Court will decide what, if any, further proceedings are necessary to resolve Defendant’s motion.

from Latest – Reason.com https://ift.tt/38vYZbw

via IFTTT

Global Stocks On Verge Of All Time High After Powell Give The All Green

It was all systems go this morning, after Fed Chair Powell made it clear that Fed won’t be hiking rates for a long, long time, maybe ever, and could potentially expand QE to coupon Treasuries, sending bond yields and the dollar lower, and sparking a rally for global shares which took a fresh run at record highs on Thursday, as the Fed set traders up another news packed day of bank meetings and a Brexit-defining election in Britain, although the rally started to sputter around the time US traders walked in to their desks with US equity futures barely changed.

As expected, on Wednesday the Fed kept U.S. interest rates unchanged, but it was a message that it would take an unexpected and “persistent” rise in inflation to lift them again that inspired bulls and shoved the dollar to its lowest since August. It helped Asian shares rally almost 1%, despite reports Washington will press on with new China tariffs, and solid 0.2%-0.5% gains in Europe early on left MSCI’s broadest index of world shares just 0.1% shy of its January 2018 all-time high.

“The Fed’s accommodative stance does support equities, but the chance of a disruptive election outcome in Britain is very real,” said CMC strategist Michael McCarthy.

S&P 500 futures faded an early gain that pushed the index up briefly as high as 3,150 after the cash index rose for the first time this week in the wake of the Federal Reserve’s final policy gathering of the year. The yield on 10-year Treasuries fluctuated around 1.79% amid bets the bar will be high for any future U.S. rate hikes.

In Europe, the Stoxx Europe 600 Index pared an earlier gain, government bond yields in the region dipped and the euro was little changed before the European Central Bank delivers its decision at 745am in new ECB head Christine Lagarde’s inaugural meeting. The Swiss franc fluctuated after Switzerland’s central bank left rates unchanged and reiterated a threat to intervene in currency markets if needed.

Earlier in the session, Asian stocks gained after the Fed signaled it would stay on hold throughout 2020 amid a “solid economy.” Markets in the regions were mixed, with Taiwan and South Korea rallying. The Taiex ended 1.2% higher as it extended gains from its highest level since 1990, while South Korea’s Kopsi Index capped its best day since the end of August. India’s S&P BSE Sensex Index rose for a second day. Asia tech shares followed a global chip-stocks rally buoyed by positive comments from analysts at Bank of America and Citigroup

In FX, the Bloomberg Dollar Spot Index was little changed as currencies stayed in tight ranges, including the Swiss franc after the SNB kept interest rates at rock bottom.

Meanwhile, in the UK, sterling was hovering at its highest in more than two years versus the euro and close to an eight-month high versus the dollar as voting began in an election that will determine whether Britain exits the European Union next month. Expectations are that the ruling Conservatives, led by Boris Johnson, will score a majority that allows his Brexit deal to be passed by a new parliament, but the latest polls have shown the lead shrinking. Exit polls for Britain’s election will begin around 2200 GMT, after voting closes, with clarity over whether their will be a clear winner or another hung parliament likely between 0400 GMT and 0600 GMT.

As Reuters notes, following a 10% surge by the pound in the last few months, Traders and investors are now hedging their bets. Union Bancaire Privée’s Global Head of Forex Strategy Peter Kinsella said a Conservative majority remained his expectation, however: “We think a move to levels of around $1.35 or even $1.37 is entirely feasible,” if there is a decent Conservative majority, whereas with another hung parliament “you are definitely back down to $1.26-1.27.” It was last at $1.3107, just shy of its highest since March and close to a May 2017 peak against the euro at 84.32 pence.

The euro was also climbing against the weakened dollar. It rose as far as $1.1144, close to a five-week high before Christine Lagarde’s first meeting as President of the European Central Bank. She is almost certain to keep rate rates on hold, but her style and signals will be closely watched by economists, especially with the bank due to update its forecasts and make some changes to its policy framework next year.

Switzerland’s central bank had got up early and already held its rate meeting meanwhile. Negative interest rates remain central to its plans, the SNB’s Chairman Thomas Jordan said as it maintained its ultra-expansive monetary policy. The Swiss franc barely budged.

In summary:

The SNB maintained rates at -0.75%, as expected. SNB reiterated their language around the CHF and their willingness to intervene in FX markets. In terms of forecasts 2019 growth has been increased, while the 2020 and 2021 inflaton forecasts have been cut slightly. This was not enough to prompt a significant move in EUR/CHF, as focus for the CHF will be on external factors today namely the ECB and UK General Election; most notably, the SNB maintained their rate projection for the forecast period at -0.75%.

The CBRT cut by 200bp to 12.0% vs. Exp. 12.5% (Prev. 14.0%) Maintained their cautious stance and noted the disinflation process in on track, forecast show that inflation is likely to materialise closer to the lower bound of October’s projections. Following the decision the TRY saw some modest strength.

Brazil’s Central Bank cut the Selic rate by 50bps to 4.50% as expected via unanimous decision and stated the economic recovery is gaining steam but current stage of the cycle warrants caution in its next steps. BCB added it sees two-way risks to inflation and that stimulative policy is still required but noted that data shows the economy has gained traction from Q2 onwards and it assumes recovery will continue at a gradual pace.

It’s not just central banks, there were fresh U.S.-China developments to digest too: U.S. President Donald Trump is expected to meet top advisers on Thursday to discuss tariffs on nearly $160 billion of Chinese consumer goods that are scheduled to take effect on Dec. 15, three sources told Reuters. Trump is expected to go ahead with the tariffs, a separate source told Reuters, which could scuttle efforts to end a 17-month long trade dispute between the world’s two-largest economies.

“The fact is the big event risk remains in place, with the world watching to see if the 15% tariffs kick in,” Pepperstone’s Chris Weston wrote on Thursday. “What the Fed has delivered is about as much as we could have hoped for in this period.”

In rates, Treasury yields had fallen in reaction to the Fed’s comments, but they rebounded slightly in Asia and Europe. The yield on benchmark 10-year Treasury notes rose to 1.7966%.

In commodities, WTI edged up 0.15% to $58.85 a barrel, while Brent crude rose 0.39% to $63.97 per barrel. A report by OPEC released on Wednesday suggested that oil markets are tighter than previously thought. Traders are also focused on state oil company Saudi Aramco. Its value briefly rose above $2 trillion on Thursday as its shares surged again following its Riyadh stock market debut on Wednesday, however they closed at half their intraday gain, up around 4% and below $2 trillion.

To the day ahead now where datawise this morning we get final November CPI readings in Germany and France and October industrial production for the Euro Area. The ECB and SNB meetings follow, before we get November PPI in the US and the latest initial jobless claims data. Expect plenty of focus on the election in the UK too, especially with the exit polls this evening. Finally, EU leaders are due to gather in Brussels to discuss the EU budget and climate neutrality. Initial jobless claims are among Thursday’s economic data. Scheduled earnings include Oracle, Adobe, Costco and Broadcom.

Market Snapshot

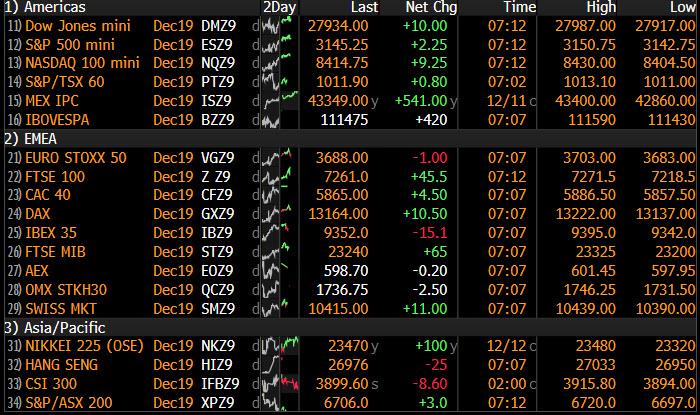

S&P 500 futures up 0.2% to 3,148.75

STOXX Europe 600 up 0.2% to 407.17

MXAP up 0.6% to 166.68

MXAPJ up 1% to 534.06

Nikkei up 0.1% to 23,424.81

Topix down 0.1% to 1,712.83

Hang Seng Index up 1.3% to 26,994.14

Shanghai Composite down 0.3% to 2,915.70

Sensex up 0.6% to 40,649.98

Australia S&P/ASX 200 down 0.7% to 6,708.83

Kospi up 1.5% to 2,137.35

German 10Y yield fell 0.2 bps to -0.323%

Euro down 0.03% to $1.1127

Italian 10Y yield fell 3.9 bps to 0.858%

Spanish 10Y yield unchanged at 0.413%

Brent Futures up 0.7% to $64.16/bbl

Gold spot down 0.09% to $1,473.52

U.S. Dollar Index up 0.04% to 97.16

Top Overnight News from Bloomberg

The Federal Reserve left interest rates unchanged and signaled it would stay on hold through 2020, keeping it on the sidelines in an election year. Jerome Powell told reporters that the committee might consider widening reserves management-related Treasuries purchases to include short-term coupon-bearing securities, if necessary, to ease liquidity strains in money markets

Senate Republicans say there is an early consensus building within their ranks for a short impeachment trial that could see the GOP-led chamber vote on a likely acquittal of President Donald Trump without hearing from any witnesses

The pound earlier touched an eight-month high — the move understates uncertainty about whether U.K. Prime Minister Boris Johnson’s Conservative Party will win a majority in Thursday’s election. Sterling’s overnight implied volatility has soared to the highest since February 2017 as demand for downside protection jumped in Asian trade

The Swiss National Bank held interest rates at rock bottom and reiterated its intervention threat, steering a steady course even as its policy comes under increasing public criticism

Christine Lagarde finally has the chance to shake off the shadow of her predecessor on Thursday, at her debut press conference as ECB president. She faces a press conference in which she’ll be judged on how convincingly she communicates the institution’s plan to restore price stability

Saudi Aramco jumped for a second day, pushing the oil giant’s value beyond the $2 trillion mark that alienated global investors and potentially making further share sales abroad more difficult

A major Chinese commodities trader became the biggest dollar bond defaulter among the nation’s state-owned companies in two decades, in a moment of reckoning for Beijing as it struggles to contain credit risk in a weakening economy

Israel is headed to its third election in less than a year, an astonishing if foretold development that’s closely intertwined with Benjamin Netanyahu’s legal troubles and may not resolve the political crisis

The U.S. sees “deeply troubling indications” that North Korea may be poised to engage in a major provocation, United Nations Ambassador Kelly Craft warned

Uncertainty surrounding the U.K.’s general election and Brexit are paralyzing the housing market, according to the Royal Institution of Chartered Surveyors

Asian equity markets were varied for most of the day as ongoing trade uncertainty heading into this week’s tariff deadline and today’s looming risk events slightly dampened the momentum from Wall St where sentiment was mildly underpinned following the FOMC meeting. Nonetheless, ASX 200 (-0.7%) and Nikkei 225 (+0.2%) traded mixed as the former suffered from broad losses across its sectors including underperformance in tech and financials, while the Japanese benchmark was kept afloat by a predominantly weaker currency but with gains also limited by a surprise 4th consecutive contraction in Machinery Orders which represented the longest streak of declines in over a decade. Elsewhere, Hang Seng (+1.3%) outperformed and topped the 27k level with the index led by a surge in Chinese tech names, although sentiment in the mainland was less optimistic with Shanghai Comp. (-0.3%) subdued by the tariff-threat overhang and as participants await statements from China’s Central Economic Work Conference which is expected to finish today. Finally, 10yr JGBs tracked the post-FOMC gains in T-notes and with prices also underpinned following the abysmal Machine Orders data from Japan, despite slightly weaker demand at the enhanced liquidity auction for longer-dated JGBs.

Top Asian News

Hong Kong’s Dollar Jumps Into Strong Half of Its Trading Band

China to Unveil Plan to Make Macau Finance Hub, Reuters Says

Hong Kong Property Stocks Battered by Protests Look Cheap

Philippine Central Bank Holds Interest Rate as Growth Rebounds

European bourses trade choppy but tread water in modest positive territory [Eurostoxx 50 +0.3%) ahead of looming risk events (ECB, UK General Election) with FOMC now out of the way. UK’s FTSE 100 modestly outperforms (+0.5%) with banks, and homebuilders supported as election voting gets underway – with exit polls expected around 22:00GMT (Full preview available on the Newsquawk Research Suite). Sectors have shown somewhat of a recovery since the open and now trade mostly in the green vs. a mixed start – defensives retreat whilst cyclicals gain traction. In terms of individual movers, Tullow Oil (+11.8%) continues to pare back from its recent 70% slump with the aid of rising oil prices acting as tailwind. Elsewhere, Balfour Beatty (+4.2%) benefits from its latest trading update which sees FY profit from operations ahead of expectations. Similarly, a positive trading update sees Ocado (+2.5%) supported. Nestle (+0.5%) shares are underpinned by source reports that it is mulling the sale of its ice cream business, which could be valued at USD 4bln. On the flip side, Germany’s Metro (-1.7%) is subdued post-earnings, whilst AB InBev (-1.5%) hovers near the bottom of the Stoxx 600 after Australia competition watchdog ACCC expressed concern about Asahi Group’s proposed purchase of AB InBev’s Carlton & United Breweries unit.

Top European News

Nordea Hiring Freeze Includes Wealth Management Unit

Latvian Parliament Elects New Head for Scandal-Hit Central Bank

Chip Stocks Lead Tech Gains After Strength in Asian, U.S. Peers

In FX, the DXY is clinging to the 97.000 handle amidst broad-based Greenback depreciation in wake of the FOMC that contained enough dovish elements to keep the index depressed, including a muted view of inflation, flat 2020 dot plots and Fed Chair Powell raising the bar for any reversal of the mid-cycle insurance easing. On that note, US PPI data comes hot on the heels of the last 2019 policy meeting and yesterday’s mixed CPI metrics, while initial claims provide the first post-NFP snapshot of the labour market that may not be as tight as the Central Bank previously perceived.

CHF/EUR/TRY- All paring gains vs the Buck, with the Franc taking some heed of more NIRP and currency intervention backing from the SNB that is flagging no rate normalisation for the duration of the forecast horizon. Usd/Chf has nudged up to circa 0.9830 from 0.9810 and Eur/Chf is near the top of a 1.0924-48 range even though the Euro has drifted down against the Dollar within 1.1145-25 parameters ahead of the ECB. The single currency may be wary about key technical resistance just above 1.1150 in the form of the 200 DMA (1.1155) rather than any fundamental change in language or policy insight from new head Lagarde, while flow-wise decent option expiry interest between 1.1120-25 and 1.1090-1.1100 (1 bn and 2.2 bn respectively) could be exerting some downside pressure. Meanwhile, the TRY firmed in light of the latest CBTR decision which kept its cautious stance despite a deeper than forecast 200bps cut. Further, the Central Bank noted of signs that inflation is close to materialise close to lower bound of its October projects. USD/TRY breached 5.7800 to the downside to low of 5.7740 (vs. 5.7980 pre-announcement) before stabilising around 5.7800.

AUD/GBP/SEK/NOK – The Aussie continues to outperform across the board, as Aud/Usd squeezes higher and through a longer term downtrend to target 0.6900 and Aud/Nzd consolidates around 1.0450 given a more subdued Kiwi vs its US counterpart after losing altitude on the approach to 0.6500, while Sterling is meandering on GE day, with Cable pivoting 1.3200 and Eur/Gbp straddling 0.8430. Note, a hefty 1.1 bn option expiry at the 1.3200 strike may keep the Pound tethered awaiting the vote outcome. Elsewhere, another swing in sentiment for the Scandi Crowns after dismal Swedish jobs data vs a boost in Norwegian oil investment. Eur/Sek nudging 10.4500, Eur/Nok off near 10.1500 highs.

In commodities, a relatively slow session initially for commodities in the aftermath of the FOMC which saw crude future nurse some EIA-induced wounds. WTI and Brent futures saw a very modest pop higher shortly after the release of the IEA Monthly Oil Market report – which aligned itself more with the OPEC report as they both kept global demand growth forecasts unchanged for 2019 and 2020 whilst EIA saw a modest revision higher of 50k BPD to its 2020 forecast. The report also noted that global oil demand rose by 900k BPD in Q3 2019 – highest annual growth in year. WTI and Brent futures meander around session highs above 59/bbl and 64/bbl respectively as the complex eyes awaits its next catalyst(s) and have seen some upside on the recent geopolitical rhetoric out of China. Elsewhere, spot gold is flatlining around USD 1475/oz ahead of its FOMC high of USD 1478.90/oz and on stand-by for upcoming events. Copper meanwhile touched resistance just under USD 2.8/lb amid a strengthening USD and some consolidation following six sessions of consecutive gains. Finally, nickel prices hit their highest in almost two weeks – with touted FOMO the main driver.

US Event Calendar

8:30am: 8:30am: PPI Final Demand YoY, est. 1.3%, prior 1.1%; Final Demand MoM, est. 0.2%, prior 0.4%;

8:30am: PPI Ex Food and Energy YoY, est. 1.7%, prior 1.6%; Ex Food and Energy MoM, est. 0.2%, prior 0.3%;

8:30am: Initial Jobless Claims, est. 214,000, prior 203,000; Continuing Claims, est. 1.68m, prior 1.69m

9:45am: Bloomberg Consumer Comfort, prior 61.7

12pm: Household Change in Net Worth, prior $1.83t

DB’s Jim Reid concludes the overnight wrap

Plenty of stuff to get through today. The General Election here in the UK, a wrap-up of the Fed last night and a preview of the ECB meeting.

As for the UK election today, I’ll be voting on the dot at 7am as soon as the polls open to ensure my side goes 1-nil up with only around 35 million more to come in as I try to defend my team’s lead. The first point of call will be the exit polls expected out at 10pm GMT. The results will then filter in over the next few hours after that so we should have a good idea of how things stand in the early hours of tomorrow morning. A reminder that Tuesday night saw the YouGov MRP forecast a much smaller 28 seat majority for the Conservatives versus 68 seats in the previous iteration. While much was made of this, to be fair that better reflects the BritainElects moving average of polls reducing to just below 10pts for a Tory lead versus closer to 12pts the first time the survey was run. The handful of polls over the last 24 hours have generally agreed with this although a SavantaComRes poll last night did show a 5% lead only – the narrowest of this election campaign. This morning Sterling is hovering around $1.322.

Turning to the Fed last night, the main headline was that the FOMC unanimously voted to leave rates unchanged, in line with the market’s expectations following a run of 3 successive 25bp cuts. Indeed, this was actually the first unanimous decision since May. Looking at the statement, the language on the economy was unchanged, with the Fed continuing to say that “the labor market remains strong and that economic activity has been rising at a moderate rate.” In a slightly hawkish lean however, they also removed their comment from the previous meeting’s statement that “uncertainties about this outlook remain.”

Examining the dot plot, the median dot for next year saw policy remaining unchanged, with just 4 members wanting a 25bp increase, while the median dot for 2021 saw a 25bp hike. That said, there was some variation around this, with 5 members seeing no change in policy, 4 with a 25bp increase, 5 with a 50bp increase, and 3 with a 75bp increase from present levels. But notably, not a single FOMC member opted for a cut, signalling that the Fed has finished its period of insurance cuts. In his press conference however, Chair Powell pushed back against any inferences that this meant the Fed now had a tightening bias, saying that “a significant move-up in inflation” was needed in order to support rate hikes.

Our US economists published their full summary of the meeting here. In their view, the most-important conclusion from it was Chair Powell’s strong signal of a low-for-longer outlook for the policy rate with rate hikes very unlikely for the foreseeable future. In contrast to the signal from a year ago when normalization was the driving force for the policy outlook, Powell stressed below-target inflation creates challenges, slack remained in the labor market despite a fifty-year low in unemployment, and a “persistent” and “significant” rise in inflation was needed to justify higher policy rates. These signals reinforce our team’s view the Committee is cognizant of the benefits of a hot labor market and is therefore likely to adopt an inflation makeup strategy as a result of the policy review. As Powell made clear, this change will require a credible commitment to be successful.

Markets were buoyed following the decision and press conference, with the S&P 500 advancing +0.29%, while the DOW and NASDAQ finished +0.11% and +0.44%. The trade-sensitive Philadelphia semiconductor index had its best session in over two weeks, closing up +2.23%. Sovereign debt also rallied a couple of bps following the decision, with 10y treasuries ending the session -5bps at 1.791%, with the 2s10s curve flattening -1.6bps. The dollar didn’t perform so well however, down -0.33% against the euro with the move lower largely post-FOMC. Elsewhere Gold performed strongly to end +0.72%,

This morning in Asia, with the exception of the Shanghai Comp which is down -0.12%, that post FOMC momentum has continued for the most part with the Kospi (+1.35%) and Hang Seng (+1.18%) leading the way followed by the Nikkei (+0.24%). Futures on the S&P 500 are also up slightly.

Moving on. With the Fed out of the way it’s the turn of the ECB today and while we’re not expecting any big announcements, given that its Lagarde’s first as the new ECB President, expect there to be plenty of focus. In their preview note our economists highlighted that staff forecasts for GDP growth, headline inflation and core inflation are likely to be stable for the first time since the exit from the APP was announced in mid-2018. The Council will likely remain cautious and view the balance of risks as still tilted to the downside. The accommodative policy stance will remain appropriate. However, Lagarde is likely to oversee one immediate change. That is, they expect the willingness to use “all instruments” to be conditioned on an assessment of the possible side effects of policy. All eyes on that this afternoon then. On a related topic our European economists put a piece out yesterday suggesting why the ECB pain trade cannot persist with regards to monetary policy and bank performance (link). Eventually they expect financial profitability will influence policy. Lagarde’s sensitivity to “side effects” is the signal and the coming ECB strategic review is the opportunity. Absent other changes (e.g. strong fee generation), the reversal of negative policy rates to counteract the side effects cannot be ruled out over time.

Back to yesterday, where the data highlight was the November CPI report in the US. The headline reading of +0.3% mom was a tenth ahead of expectations however the core reading of +0.2% mom (+0.23% unrounded) was in-line which left the year-over-year rate at +2.3% yoy. Later on the November monthly budget statement saw the deficit widen to $208.8bn (vs. $206.2bn expected).

There was no substantive data out in Europe yesterday, with newsflow also fairly light. The EU outlined its plan to become climate-neutral by 2050 while French President Macron finished his awaited clarification on pension reform proposals in which he signalled the dropping of aiming to pursue spending cuts in the short run. For completeness European stocks were a touch firmer yesterday with the STOXX 600 closing +0.22%. European bond markets were also slightly stronger with bunds -2.6bps

To the day ahead now where datawise this morning we get final November CPI readings in Germany and France and October industrial production for the Euro Area. The ECB and SNB meetings follow, before we get November PPI in the US and the latest initial jobless claims data. Expect plenty of focus on the election in the UK too, especially with the exit polls this evening. Finally, EU leaders are due to gather in Brussels to discuss the EU budget and climate neutrality.

Russia’s Only Aircraft Carrier Has Erupted In Flames

According to TASS News and social media footage, a fire has erupted onboard Russia’s only aircraft carrier, Admiral Kuznetsov, at a naval dock in Murmansk, northwest Russia. The aircraft carrier was undergoing repairs and maintenance when fuel tanks caught fire.

RT News reports a “blaze was sparked by welding in the first power section on the ship’s deck, after which the fire spread to a space of 600 square meters.”

Footage of the fire onboard aircraft carrier Admiral Kuznestov shows black smoke rising above the decks of the ship.According 🇷🇺# Russian state news agencies,one worker remains unaccounted for.The same wires suggest the fire is spreading and now covers 600 sq metres of the ship. pic.twitter.com/H840i8uwhI

Russian aircraft carrier “Admiral Kuznetsov” caught fire during repair works at Zvezdochka plant. 8 workers rescued, 1 unaccounted. Fire at least at 120m2 in engine room https://t.co/EhBCrUKBg8#Russiapic.twitter.com/011TFOQSrk

The Emergencies Ministry told TASS that “three people have been injured. All of them are receiving medical assistance,” adding that, “Eight people have been rescued by the emergencies services and firefighters, and one person has gone missing.”

3 wounded in fire at Admiral Kuznetsov. Firefighters say that fire in wires system of the vessel, and they cannot get to it. Governor of Murmansk region is heading to the site https://t.co/qUQi5yxO83#Russiapic.twitter.com/KU5WNbs9dM

Fire at “Admiral Kuznetsov” continues to burn. Now decision taken to flood it with water. First reports suggest that fire started during welding works at energy compartment https://t.co/aex4as5zzi#Russiapic.twitter.com/mphumclbDR

Aleksey Rakhmanov, head of the state-run United Shipbuilding Corporation, told Interfax that the fire was possibly sparked by “a human factor.”

Russia’s only aircraft carrier had been undergoing repairs and maintenance since the second half of 2017, after performing combat missions in the eastern Mediterranean Sea, providing air support for the Bashar al-Assad government of Syria in the country’s near-decade civil war.