“Dramatic Change” Ahead: Robots Are Coming For 200,000 US Banking Jobs

A new report by Wells Fargo & Co., warns that nearly 200,000 US banking jobs are at risk of being displaced by robots.

As we’ve explained in the past, accelerating technological advances in automation, artificial intelligence, and machine learning have the potential to reshape the world in the 2020s through 2030. The collision of these forces could trigger economic disruption far greater than what was seen in the early 20th century.

Across the financial industry, a new wave of investment, somewhere in the tune of $150 billion per year, is being spent on technology, that will “lead to lower costs, with employee compensation accounting for half of all bank expenses,” said Mike Mayo, a senior analyst at Wells Fargo Securities LLC.

The Wells Fargo study, which was first reported by Bloomberg, indicates 20% to 33% of banking jobs will be slashed by 2030. Most affected will be back office, bank branch, call center, and corporate employees. Jobs related to tech sales, advising and consulting will be less affected, according to the study.

“It will be a dramatic change in contact centers, and these are both internal and external,” Michael Tang, a Deloitte partner who leads the consulting firm’s global financial-services innovation practice, said in the Wells Fargo report. “We’re already seeing signs of it with chatbots, and some people don’t even know that they’re chatting with an A.I. engine because they’re just answering questions.”

Wells Fargo joins a handful of other major banks that have already detailed plans to cut a majority of their workforce by 2030 amid the rapid adoption of automation and artificial intelligence.

According to Coalition Development Ltd. data. R. Martin Chavez, an architect of Goldman Sachs’ push to automate its workforce, said last month, front-office headcount for investment banking and trading declined for the fifth consecutive year in 2018.

In an earlier piece, we described how tens of millions of jobs across the world, and across various industries, would be lost because of robots by 2030.

The 2020s will be known as the great transformation period where corporate America abandons its workforce for automation. The coming job losses, due to automation, will be on par with the automation revolution of agriculture (the transition of farm workers into the industrial sector) from 1900 to 1940.

Robots have so far increased three-fold since the Dot-Com bust. Momentum in automation trends suggests robots will multiply even quicker through the 2020s. The collision of automation in the economy will lead to more volatility, economic swings, and social unrest.

I have blogged twicebefore about Ben Penn’s false and misleading article for Bloomberg Law about my colleague, Leif Olson. One month later, the story remains without any retraction. There are several “updates” and “corrections” which make the article incomprehensible. Regrettably, people who Google “Leif Olson” will quickly see this hit job, without knowing the proper context. Penn has not tweeted since his “scoop.” I can only hope he is under investigation, and will face the appropriate discipline.

This post focuses on recent developments in this saga. On September 3, 2019, Penn tweeted:

To Leif Olson’s friends & others who take issue with this reporting, I sent a screenshot of a public FB post to DOL, seeking comment. 4 hours later I received this response: “Today, the Department of Labor accepted the resignation of Leif Olson effective immediately.”

To Leif Olson's friends & others who take issue with this reporting, I sent a screenshot of a public FB post to DOL, seeking comment. 4 hours later I received this response: “Today, the Department of Labor accepted the resignation of Leif Olson effective immediately.” https://t.co/PZbIScDHqe

Is that all Penn did? Did he simply send a screenshot and seek a comment. At the time, I was incredulous. My skepticism was warranted.

Now, we know exactly what Penn wrote to DOL. Shortly after the article was posted, Frank Bednarz and Ted Frank of the Hamilton Lincoln Law Institute submitted a FOIA request to the Department of Labor. They requested any communications from Ben Penn to the agency.

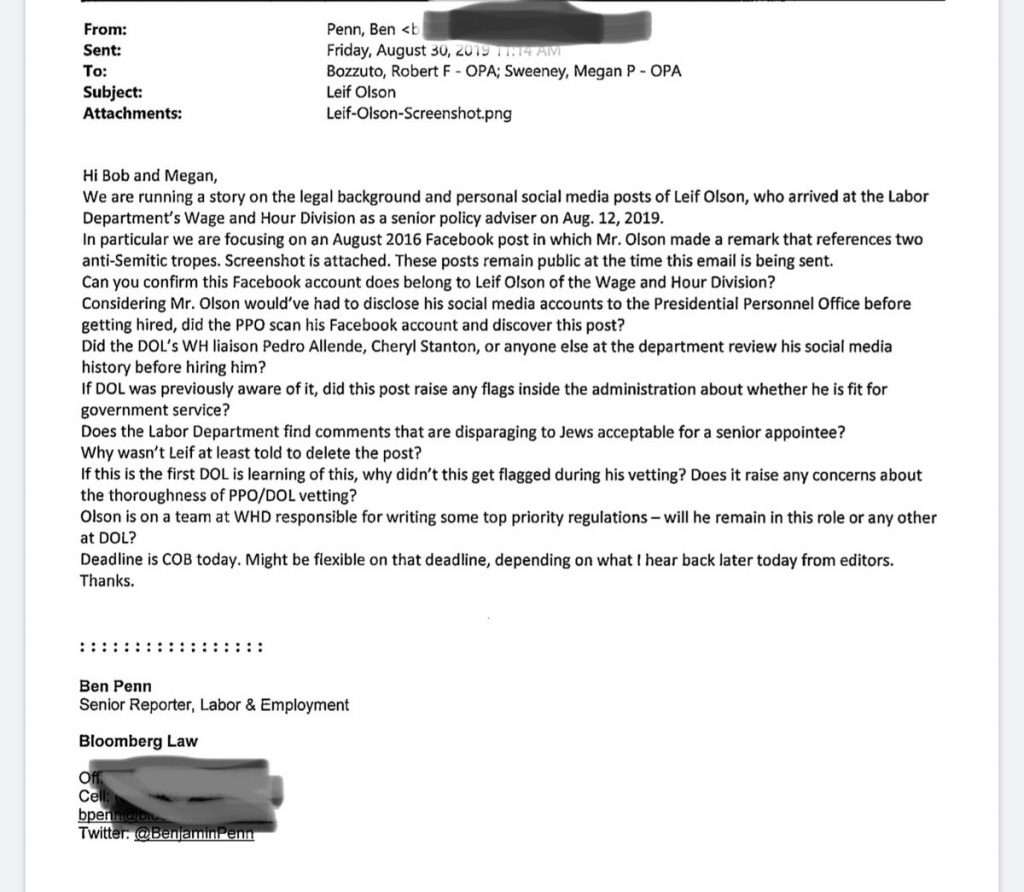

Here is the message, sent on Friday, August 30, four days before Penn’s article was published.

First, Penn wrote:

“In particular we are focusing on an August 2016 Facebook post in which Mr. Olson made a remark that references two anti-Semitic tropes. Screenshot is attached. These posts remain public at the time this email is being sent.”

This message is extremely misleading. Leif’s remarks “referenced two anti-Semitic tropes” to criticize anti-semitism. Penn’s use of the word “reference” was deliberate. He did not say that Leif made anti-semitic comments, or engaged in anti-semitic acts. This precise use of language suggests Penn knew that his claim of anti-semitism was, at best, tenuous.

Second, Penn wrote:

“Does the Labor Department find comments that are disparaging to Jews acceptable for a senior appointee?”

Again, nothing Leif wrote was disparaging to Jews. I doubt the people at DOL had the ability to parse through the grainy Facebook screenshots, and figure out their context. Penn’s failure to provide the context is journalistic malpractice.

At bottom, Penn did not simply send the screenshot, and seek comment. His tweet was, at best, misleading. And he concocted alternative facts to cover up his own gross error. Memo to Bloomberg law: if you were looking for an easy justification to punish Penn, here you go. Journalists should not mislead the public on social media to defend their false stories.

Finally, Penn wrote, “Deadline is COB today. Might be flexible on that deadline, depending on when I hear back later today from editors.” This last statement is perhaps the most troubling. I had largely assumed that Penn was acting on his own, and that a single, overworked editor only glanced at the piece. No. Editors (plural!) were closely involved with the publication process, and had four days to digest this record, and still published the article. Who knows how many hours the editors gave Penn to scroll through a decade of Facebook posts?!

This entire incident reflects so poorly on Bloomberg Law. Both Penn, and the editors approved this story, should face severe consequences. This FOIA’d document provides all the evidence that any journalistic review would require

Finally, Bloomberg should add a clear disclaimer should be put at the top of the article, stating that organization retracts all claims. There is no reason to stand behind this story. Bloomberg has already assaulted Leif’s character; at least it can rehabilitate his Google footprint.

from Latest – Reason.com https://ift.tt/2AHw5p2

via IFTTT

Typically when one hears about flaming, bright objects falling from the sky, one comes to a very simple conclusion—it must be a meteorite, burning as it falls through the Earth’s atmosphere.

However, last week in the south of Chile, residents on the island of Chiloe were shocked when a fireball plummeted all the way down to the ground, starting a number of fires, CNET reports.

Local property owner Bernardita Ojeda was among the residents impacted by what many assumed was a meteorite when a brush fire was sparked by the burning object.

However, on Saturday, officials from the country’s National Geology and Mining Service (Sernageomin) reached the preliminary conclusion that the object could not have been a meteorite—for the simple reason that no evidence of any form of space rock could be found where the fires were started by the “luminous and incandescent object in the sky that fell in that location.”

“Once in the Dalcahue area, geologists went to the site to examine the area of the supposed impact. They worked at seven points corresponding to the burnt bushes, where they found no remains, vestiges or evidence of a meteorite falling.

Likewise, and as part of the investigation, they interviewed local residents, who said they had not seen the fall of the supposed object or heard noises associated with the fall of a body of this nature.

Preliminarily, professionals are ruling out the fall of a meteorite in this sector and, therefore, that the cause of burning thickets, has corresponded to that situation.”

So if Chile’s authorities are ruling out a meteorite, what could the falling heavenly body possibly be?

As CNET correctly notes, these are by definition, UFOs:

“Technically, we’re talking about unidentified flying objects. Yes, UFOs. Although nothing big or well-piloted enough to reopen The X-Files for, it would seem.”

So this definitely wasn’t a flying saucer, if only because then we’d have some alien technology lying around, perhaps. Then was it a bit of litter that escaped the near-to-low-Earth orbit, a zone of space that’s known to be teeming with “zombie” satellites, shards from rockets, and all sorts of other debris left behind by the world’s space agencies?

“Since the Soviet Union launched the first satellite, Sputnik, in 1957, the number of objects in space has surged, reaching roughly 2,000 in 1970, about 7,500 in 2000 and about 20,000 known items today. The two biggest spikes in orbital debris came in 2007, when the Chinese government blew up one of its satellites in a missile test, and in the 2009 Iridium–Cosmos collision.”

In this case, a bit of flaming space junk appears to be the most plausible scenario, and one that leading Chilean astrophysicist Jose Maza told to national broadcaster TVN.

The Sernageomin concluded:

“In parallel, geologists collected soil samples for a more thorough and detailed analysis in the institution’s laboratory. Final conclusions will be announced in the coming weeks.”

We wouldn’t be surprised if geologists manage to find small bits of metal and other human-manufactured bits of garbage, be it from old rocket boosters or from the hundreds of dead satellites spinning around our planet. And luckily, space debris very rarely hits the ground—although this may well have been an exception to the rule.

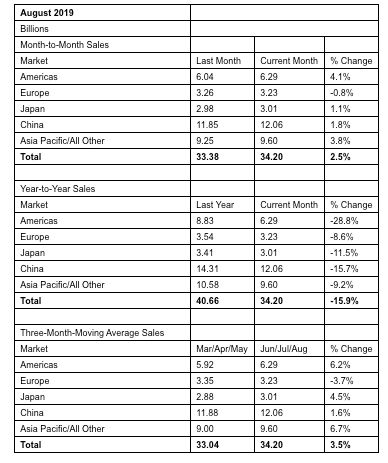

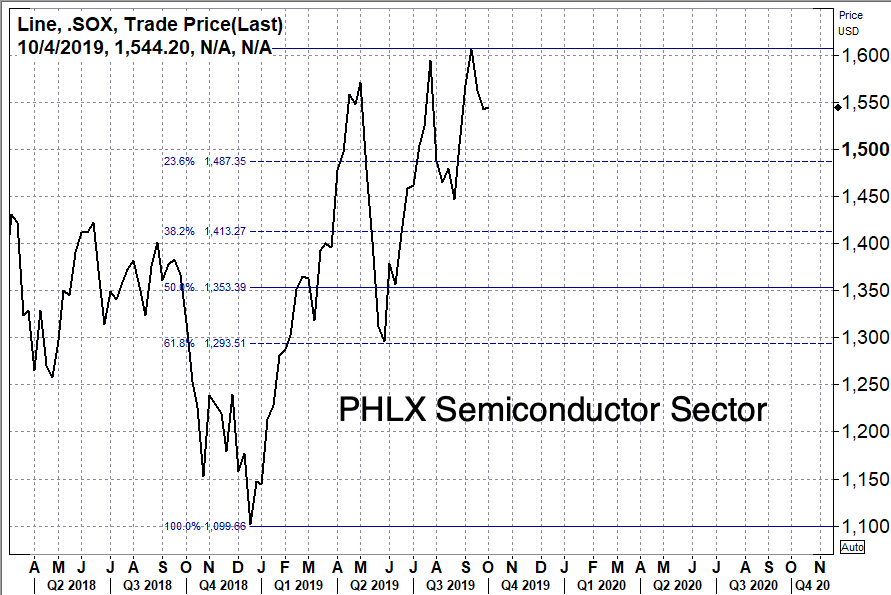

And more evidence of global slowdown was found in the latest report from the Semiconductor Industry Association (SIA) on Tuesday, who warned, semiconductor sales are plunging around the world. SIA said worldwide sales of semiconductors were $34.2 billion in August, a 15.9% drop YoY.

Monthly sales showed the August figure of $34.2 billion, was 2.5% higher than July 2019 total of $33.4 billion, these sales were compiled by the World Semiconductor Trade Statistics (WSTS) organization.

John Neuffer, SIA president and CEO, was rather pessimistic on the global semiconductor industry, indicating YoY changes in sales were disappointing in the Americas.

“While worldwide semiconductor sales remain well behind the totals reached in 2018, month-to-month sales increased in two consecutive months for the first time in nearly a year,” said Neuffer. “Sales into the Americas market were mixed, decreasing significantly year-to-year but increasing more than any other region on a month-to-month basis.”

On a regional basis, MoM sales increased slightly in late summer. The Americas saw a 4.1% MoM increase from July to August, the Asia Pacific/All Other 3.8%, China 1.8%, Japan 1.1%, but a decline -.8% in Europe.

However, it was the YoY sales that frightened Neuffer, who wasn’t completely clear if a bottom would be seen in the global semiconductor industry this year. Semiconductor sales YoY in Europe were -8.6%, the Asia Pacific/All Other -9.2%, Japan -11.5%, China -15.7%, and Americas -28.8% for the August period.

In this cycle, semiconductors are considered an economic bellwether of the global economy, because the chips are central to everything that’s modern or electronic, whether it’s automobiles, smartphones, robots, airplanes, televisions, computers, and fifth-generation cellular networks. So when demand for, let’s say automobiles, severely declines, like Toyota reported a 16.5% YoY drop in September car sales, that would force the car manufacture to slow production, thus delay the need for more semiconductor chips.

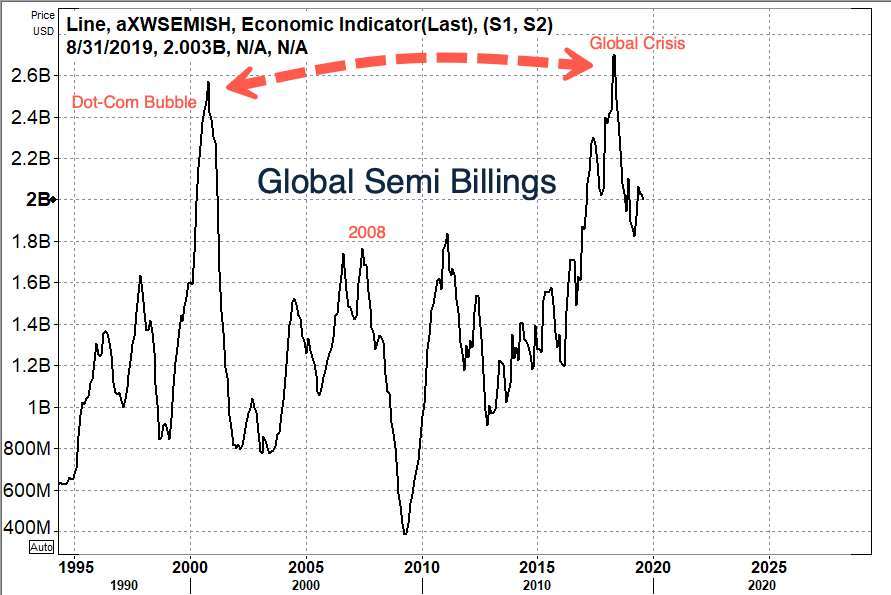

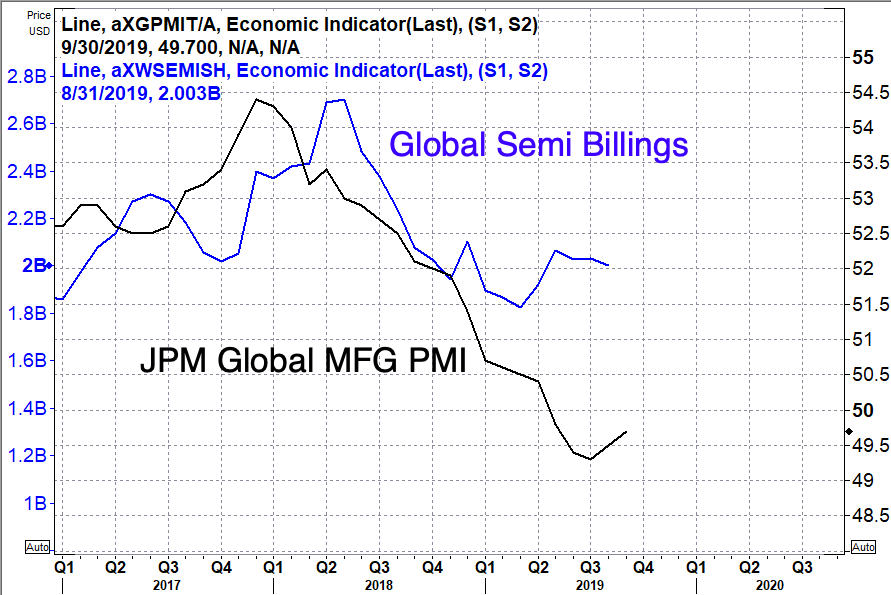

Shown in the chart below, Global semiconductor equipment billings peaked in April 2018.

J.P.Morgan Global Manufacturing PMI peaked in December 2017, then shortly after, Global semiconductor equipment billings moved sharply lower in 2H18.

PHLX Semiconductor Sector has nearly doubled in the last 38 weeks, moved up 46%. If a return to macro event is underway, and risk assets are repriced into fall/winter, this would mean semiconductors stocks are headed for catastrophe.

The reasons why the Green New Deal won’t really work are fairly subtle. A person really has to look into the details to see what goes wrong. In this post, I try to explain at least a few of the issues involved.

[1] None of the new renewables can easily be relied upon to produce enough energy in winter.

The world’s energy needs vary, depending on location. In locations near the poles, there will be a significant need for light and heat during the winter months. Energy needs will be relatively more equal throughout the year near the equator.

Solar energy is particularly a problem in winter. In northern latitudes, if utilities want to use solar energy to provide electricity in winter, they will likely need to build several times the amount of solar generation capacity required for summer to have enough electricity available for winter.

Figure 1. US daily average solar production, based on data of the US Energy Information Administration.

Hydroelectric tends to be a spring-dominated resource. Its quantity tends to vary significantly from year to year, making it difficult to count on.

Figure 2. US daily average hydroelectric production, based on data of the US Energy Information Administration.

Another issue with hydroelectric is the fact that most suitable locations have already been developed. Even if additional hydroelectric might help with winter energy needs, adding more hydroelectric is often not an option.

Wind energy (Figure 3) comes closest to being suitable for matching the winter consumption needs of the economy. In at least some parts of the world, wind energy seems to continue at a reasonable level during winter.

Figure 3. US daily average wind production, based on data of the US Energy Information Administration.

Unfortunately, wind tends to be quite variable from year to year and month to month. This makes it difficult to rely on without considerable overbuilding.

Wind energy is also very dependent upon the continuation of our current economy. With many moving parts, wind turbines need frequent replacement of parts. These parts need to be precisely correct, with virtually no tolerance for change. Sometimes, helicopters are needed to install the new parts. Because of the need for continued high-technology maintenance services, wind energy cannot be expected to continue to operate for very long unless the world economy, with all of its globalization, can continue pretty much as today.

[2] Depending upon burned biomass in winter is an option, but we already know that this path is likely to lead to massive deforestation.

Historically, people burned wood and other biomass to provide heat and light in winter. If biomass is burned for heat and light, it is an easy step to using charcoal for smelting metals for goods such as nails and shovels. But with today’s population of 7.7 billion people, the huge demand for biomass would quickly deforest the whole world. There is already a problem with growing deforestation, especially in tropical areas.

It is my understanding that the Green New Deal is focusing primarily on wind, hydroelectric, and solar rather than biomass, because of these issues.

[3] Battery backup for renewables is very expensive. Because of their high cost, batteries tend to be used only for very short time periods. At a 3-day storage level, batteries do nothing to smooth out season-to-season and year-to-year variation.

The cost of batteries is not simplytheir purchase price. There seem to be several related costs associated with the use of batteries:

The initial cost of the batteries

The cost of replacements, because batteries are typically not very long-lived compared to, say, solar panels

The cost of recycling the battery components rather than simply leaving the batteries to pollute the nearby surroundings

The loss of electric charge that occurs as the battery sits idle for a period of time and the loss related to electricity storage and retrieval

We can get some idea of the cost of batteries from an analysis by Roger Andrews of a Tesla/Solar City system installed on the island of Ta’u. The island is in American Samoa, near the equator. This island received a grant that was used to add solar panels, plus 3-day battery backup, to provide electricity for the tiny island. Any outages longer than the battery capacity would continue to be handled by a diesel generator. The goal was to reduce the quantity of diesel used, not to eliminate its use completely.

Based on Andrews’ analysis, adding a 3-day battery backup more than doubled the cost of the PV-alone system. (It added 1.6 times as much as the cost of the installed batteries.) The catch, as I pointed out above, is that the cost doesn’t stop with purchasing the initial batteries. At least one set of replacement batteries is likely to be needed during the lifetime of the system. And there are other costs that are more subtle and difficult to evaluate.

Furthermore, this analysis was for a solar system. There seems to be more variation over longer periods for wind. It is not clear that the relative amount of batteries would be enough for 3-day backup of a wind system, or for a combination of wind, hydroelectric and solar. The long-term cost of a solar panel plus battery system might easily come to four times the cost of a wind or solar system alone.

There is also the issue of necessary overbuilding to make the system work. On Ta’u, near the equator, with diesel power backup, the system is set up in such a way that 40% of the solar generation is in excess of the island’s day-to-day electricity consumption. This constitutes another cost of the system, over and above the cost of the 3-day battery backup.

If we also eliminate the diesel backup, then we start adding more costs because the level of overbuilding would need to be even higher. And, if we were to create a similar system in a location with substantial seasonal temperature variation, even more overbuilding would be required if enough capacity is to be made available to provide sufficient generation in winter.

[4] Even in sunny, warm California, it appears that substantial excess capacity needs to be added to avoid the problem of inadequate generation during the winter months, if the electrical system used is based on wind, hydroelectric, solar, and a 3-day backup battery.

Suppose that we want to replace California’s electricity consumption (excluding other energy, including oil products) with a new system using wind, hydro, solar, and 3-day battery backup. Current California renewable generation, compared to current consumption, is as shown on Figure 4, based on EIA data.

Figure 4. California total electricity consumption compared to the sum of California solar, wind, and hydroelectric production, on a monthly average basis. Data used from the US Energy Information Administration through June 30, 2019.

California’s electricity consumption peaks about August, presumably due to all of its air conditioning usage (Figure 5). This is two months after the June peak in the output of solar panels. Also, electricity usage doesn’t drop back nearly as much during winter as solar production does. (Compare Figures 1 and 5.)

Figure 5. California electricity consumption by month, based on US Energy Information Administration data.

We note from Figure 4 that hydroelectric production is extremely variable. It appears that hydroelectric generation can vary by a factor of five comparing high years to low years. California hydroelectric generation uses all available rivers, so any new energy generation will need to come from wind and solar.

Even with 3-day backup batteries, we need the system to reliably produce enough electricity that it can meet the average electricity generation needs of each separate month. I did a rough estimate of how much wind and solar the system would need to add to bring total generation sufficiently high so as to prevent electricity problems during the winter. In making the analysis, I assumed that the proportion of added wind and solar would be similar to their relative proportions on June 30, 2019.

My analysis suggests that to reliably bridge the gap between production and consumption (see Figure 4), approximately six times as much wind and solar would need to be added (making 7 = 6 +1 times as much generation in total), as was in place on June 30 , 2019. With this arrangement, there would be a huge amount of wind and solar whose production would need to be curtailed during the summer months.

Figure 6. Estimated share of wind and solar production that would need to be curtailed, to provide adequate winter generation. The assumption is made that hydroelectric generation would not be curtailed.

Figure 6 shows the proportion of wind and solar output that would be in excess of the system’s expected consumption. Note that in winter, this drops to close to zero.

[5] None of the researchers studying the usefulness of wind and solar have understood the need for overbuilding, or alternatively, paying backup electricity providers adequately for their services. Instead, they have assumed that the only costs involved relate to the devices themselves, plus the inverters. This approach makes wind and intermittent solar appear far more helpful than they really are.

Wind and solar have been operating in almost a fantasy world. They have been given the subsidy of “going first.” If we change to a renewables-only system, this subsidy of going first disappears. Instead, the system needs to be hugely overbuilt to provide the 24/7/365 generation that backup electricity providers have made possible with either no compensation at all, or with far too little compensation. (This lack of adequate compensation for backup providers is causing problems for the current system, but it is beyond the scope of this article to discuss them here.)

Analysts have not understood that there are substantial costs that are not being reimbursed today, which allow wind and solar to have the subsidy of going first. For example, if natural gas is to be used as backup during winter, there will still need to be underground storage allowing natural gas to be stored for use in winter. There will also need to be pipelines that are not used much of the year. Workers will need to be paid year around if they are to continue to specialize in natural gas work. Annual costs of the natural gas system will not be greatly reduced simply because wind, hydro, and water can replace natural gas usage most months of the year.

Analysts of many types have issued reports indicating that wind and solar have “positive net energy” or other favorable characteristics. These favorable analyses would disappear if either (a) the necessary overbuilding of the system or (b) the real cost of backup services were properly recognized. This problem pervades studies of many types, including Levelized Cost of Energy studies, Energy Returned on Energy Invested studies, and Life Cycle Analyses.

This strange but necessary overbuilding situation also has implications for how much homeowners should be paid for their rooftop solar electricity. Once it is clear that only a small fraction of the electricity provided by the solar panels will actually be used (because it comes in the summer, and the system has been overbuilt in order to produce enough generation in winter), then payments to homeowners for electricity generated by rooftop systems will need to decrease dramatically.

A question arises regarding what to do with all of the electricity production that is in excess of the needs of customers. Many people would suggest using this excess electricity to make liquid fuels. The catch with this approach is that the liquid fuel needs to be very inexpensive to be affordable by consumers. We cannot expect consumers to be able to afford higher prices than they are currently paying for fossil fuel products. Also, the new liquid fuels ideally should power current devices. If consumers need to purchase new devices in order to utilize the new fuels, this further reduces the affordability of a planned changeover to a new fuel.

Alternatively, owners of solar panels might be encouraged to use the summer overproduction themselves. They might set the temperatures of their air conditioners to a lower setting or heat a swimming pool. It is unlikely that the excess could be profitably sold to nearby utilities because they are likely encounter the same problem in summer, if they are using a similar generation mix.

[6] As appealing as an all-electric economy would seem to be, the transition to such an economy can be expected to take 150 years, based on the speed of the transition since 1985.

Clearly, the economy uses a lot of energy products that are not electricity. We are familiar with oil products burned in many vehicles, for example. Oil is also used in many ways that do not require burning (for example, lubricating oils and asphalt). Natural gas and propane are used to heat homes and cook food, among other uses. Coal is sometimes burned in making pig iron and cement in China.

Figure 7. Electricity as a share of total energy use for selected areas, based on BP’s 2019 Statistical Review of World Energy.

Electricity’s share of total energy consumption has gradually been rising (Figure 7).* We can make a rough estimate of how quickly the changeover has been taking place since 1985. For the world as a whole, electricity consumption amounted to 43.4% of energy consumption in 2018, rising from 31.2% in 1985. On average, the increase has been 0.37%, over the 33-year period shown. If we assume this same linear growth pattern holds going forward, it will take 153 years (until 2171) until the world economy can operate using only electricity. This is not a quick change!

[7] While moving away from fossil fuels sounds appealing, pretty much everything in today’s economy is made and transported to its final destination using fossil fuels. If a mis-step takes place and leaves the world with too little total energy consumption, the world could be left without an operating financial system and with way too little food.

Over 80% of today’s energy consumption is from fossil fuels. In fact, the other types of energy shown on Figure 8 would not be possible without the use of fossil fuels.

Figure 8. World Energy Consumption by Fuel, based on data of 2019 BP Statistical Review of World Energy.

With over 80% of energy consumption coming from fossil fuels, pretty much everything we have in our economy today is available thanks to fossil fuels. We wouldn’t have today’s homes, schools or grocery stores without fossil fuels. Even solar panels, wind turbines, batteries, and modern hydroelectric dams would not be possible without fossil fuels. In fact, for the foreseeable future, we cannot make any of these devices with electricity alone.

In Figure 8, the little notch in world energy consumption corresponds to the Great Recession of 2008-2009. The connection between low energy consumption and poor economic outcomes goes back to many earlier periods. Energy consumption growth was unusually low about the time of the Great Depression of the 1930s and about the time of the US Civil War. The vulnerability of the financial system and the possibility of major wars are two reasons why a person should be concerned about the possibility of an energy changeover that doesn’t provide the economic system with adequate energy to operate. The laws of physics require energy dissipation for essentially every activity that is part of GDP. Without adequate energy, an economy tends to collapse. Economists are generally not aware of this important point.

Agriculture is dependent upon fossil fuels, particularly oil. Petrochemicals are used directly to make herbicides, pesticides, medications for animals and nitrogen fertilizer. Huge quantities of energy are necessary to make metals of all kinds, such as the steel in agricultural equipment and in irrigation pumps. Refrigerated vehicles transport produce to market, using mostly oil-based fuel. If the transition does not go as favorably as hoped, food supplies could prove to be hopelessly inadequate.

[8] The scale of the transition to hydroelectric, wind, and solar would be unimaginably large.

Today, wind, hydroelectric, and solar amount to about 10% of world energy production. Hydroelectric amounts to about 7% of energy consumption, wind about 2%, and solar about 1%. This can be seen on Figure 8 above. A different way of seeing this same relationship is shown in Figure 9, below.

Figure 9. World hydroelectric, wind and solar production as share of world energy supply, based on BP’s 2019 Statistical Review of World Energy.

Figure 9 shows that hydroelectric power is pretty well maxed out, as a percentage of energy supply. This is especially the case in advanced economies. This means that any increases that are made in the future will likely have to come from wind and solar. If hydroelectric, wind and solar are together to produce 100% of the world’s energy supply, then wind and solar, which today comprise 3% of today’s energy supply, will need to ramp up to 93% of energy supply. This amounts to a 30-fold increase in wind and solar between 2018 and 2030, based on one version of the Green New Deal’s planned timing. We would need to be building wind and solar absolutely everywhere, very quickly, to accomplish this.

[9] Moving to electric vehicles (EVs) for private passenger autos is not likely to be as helpful as many people hope.

One issue is that it is possible to mandate the use of EVs, but if the automobiles cost more than citizens can afford, many citizens will simply stop buying cars at all. At least part of the worldwide reduction in automobile sales seems to be related to changes in rules that are intended to reduce auto emissions. The slowdown in auto sales is part of what is pushing the world into recession.

Another issue is that private passenger autos represent a smaller share of oil consumption than many people would expect. BP data indicate that 26% of worldwide oil consumption is gasoline. Gasoline powers the vast majority of the world’s private passenger automobiles today. While an oil savings of 26% would be good, there would still be a very long way to go.

One study of EV sales in Norway suggests that, with large subsidies, these cars are disproportionately sold to high-income families as a second vehicle. The new second vehicles are often used for commuting to work, when prior to the EV ownership, the owner had been taking public transportation. When this pattern is followed, the savings in oil use from the adoption of EVs becomes very small because building and transporting EVs also requires oil use.

Figure 10. Source: Holtsmark and Skonhoft The Norwegian support and subsidy policy of electric cars. Should it be adopted by other countries?

If one of the goals of the Green New Deal is to level out differences between the rich and the poor, mandating EVs would seem to be a step in the wrong direction. It would make more sense to mandate walking or the use of pedal bicycles, rather than EVs.

[10] Wind, solar, and hydroelectric have pollution problems themselves.

With respect to solar panels, a major concern is that if the panels are broken (for example, by a storm or near the end of their lives), water alone can leach toxic substances into the water supply. Another issue is that recycling needs to be subsidized, to be economic. The price of solar panels needs to be surcharged at the front end, if adequate funds are to be collected to cover recycling costs. This is not being done in the US.

Wind turbines are better in terms of not being made of toxic substances, but they disturb bird, bat, and marine life in their vicinity. Humans also complain about their vibrations, if the devices are close to homes. The fiberglass blades of wind turbines are not recyclable, and many of them are too big to fit into standard crushing machines. They need to be chopped into pieces, in order to fit into landfills.

Adding huge amounts of 3-day battery backup for wind turbines and solar panels will create a new set of recycling issues. The extent of the recycling issues will depend on the battery materials used.

Of course, if we try to ramp up wind and solar by a huge factor, pollution problems will rise accordingly. The chance that raw materials will prove to be scarce will increase as well.

There will also be an increasing problem with finding suitable sites to install all of the devices and batteries. There are limits on how densely wind turbines can be spaced before the output of one wind turbine interferes with the output of other nearby turbines. This problem is not too different from the problem of declining per-well oil production caused by too closely spaced shale wells.

Afterword

I could explain further, but that would make this make this post too long. For example, using an overbuilt renewables system, there is not enough net energy to provide the high salaries almost everyone would like to see.

Also, the new renewable energy systems are likely to be more local than many have hoped. For example, I think it is highly unlikely that the people of North Africa would allow contractors to build a solar system in North Africa for the benefit of Europeans.

Note

*There are two different ways of comparing electricity’s value to that of total energy. Figure 7 uses the more generous approach. In it, the value of electricity is based on the amount of fossil fuels that would need to be burned to produce the electricity amounts shown. In the case of electricity types that do not involve burning of fossil fuels, these amounts are estimated amounts. The less generous approach compares the heat value of the electricity produced to the total heat value of primary energy sources. Using the less generous approach, electricity corresponds to only about 20% of primary energy supply. The transition to an all-electric economy would be much farther away using the heat value approach.

September Payrolls Preview: Can We Get The First Negative Print In 10 Years?

After the surprisingly poor August payroll report which saw the US economy add only 139K jobs, analysts expect the disappointing trend to continue and forecast a below-trend 145k nonfarm payrolls added to the US economy in September, with earnings growth seen at 0.3% M/M, and the jobless rate seen unchanged at 3.7%.

As RanSquawk cautions, indicators are decidedly mixed with a strong negative bias going into the data: the ADP private payrolls gauge saw a miss against expectations with the prior number revised substantially lower, while initial jobless claims have essentially moved sideways; Challenger’s job cuts data improved, though employers are beginning to see negative effect from trade wars; the employment sub-components within the ISM has pared back in the month; and on wages, consumer wage expectations has become a touch more pessimistic. The data will be released at 8:30 EDT; with the Fed in data-dependent mode, it is also worth noting that Fed chair Powell will deliver remarks at 2:00pm EDT. Today’s market response to the dismal non-mfg ISM (whose employment index suggests we may see the first sub-zero payrolls print since September 2009) was telling: the market is now in full blown “bad news is great news for more Fed easing” mode, and the risk tomorrow is clearly to the upside, with a stronger than expected number likely to offset today’s surge in rate cut odds for the rest of 2019, leading to a adverse market reaction.

Courtesy of RanSquawk, here is what the street expects:

Non-farm Payrolls: Exp. 148k, Prev. 130k (whisper is below 100K)

Private Payrolls: Exp.133k, Prev. 96k.

Manufacturing Payrolls: Exp. 4k, Prev. 3k.

Government Payrolls: Prev. 34k.

Unemployment Rate: Exp. 3.7%, Prev. 3.7%. (FOMC currently projects 3.7% at end-2019, and 4.2% in the longer run).

U6 Unemployment Rate: Prev. 7.2%.

Labour Force Participation: Prev. 63.2%.

Avg. Earnings Y/Y: Exp. 3.2%, Prev. 3.2%.

Avg. Earnings M/M: Exp. 0.3%, Prev. 0.4%.

Avg. Work Week Hours: Exp. 34.4hrs, Prev. 34.4hrs.

SUMMARY:

The Street expects to see 148k nonfarm payrolls (whisper expectations are of a sub-100K print) added to the US economy in September. The three-month trend rate of employment growth is 156k, rising from the 133k going into the prior Employment Situation Report; the six-month trend rate is unchanged at 150k, while the 12-month pace has edged lower to 173k from 186k. In its below-trend preview of the payrolls report, Nomura says that it expects a 115k contribution from private firms and a 10k boost from government payrolls, some of which will likely reflect an influx of temporary Census workers for the second consecutive month.

HOUSEHOLD SURVEY:

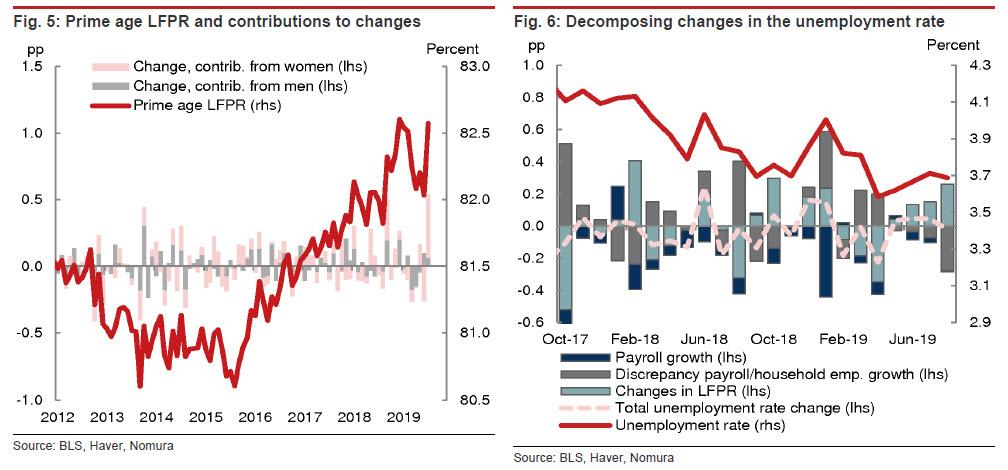

While the establishment survey results in August were somewhat weaker than expected, household survey data was more positive. As Nomura points out, the prime age (25-54) labor force participation rate (LFPR) rose 0.6pp to 82.6%, matching the recent high from January and marking the largest one-month increase since April 1960, driven by a jump in prime age LFPR for women (Figure 5). That helped push aggregate LFPR up 0.2pp to 63.2%. The increase in LFPR helped put upward pressure on the unemployment rate to keep it unchanged at 3.7% (Figure 6).

In September, much of that large increase in prime age LFPR will revert, putting downward pressure on aggregate LFPR and the unemployment rate. Since 1950, prime age LFPR has increased more than 0.4pp 16 times. In the next month, both the mean and median changes showed a 0.2pp decline. A modest drop in the LFPR would be enough to lower the unemployment rate 0.1pp to 3.6%.

US ADP NATIONAL EMPLOYMENT:

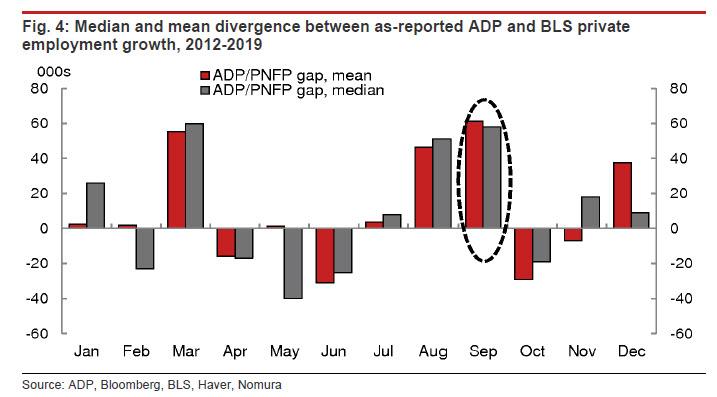

ADP’s gauge of private payrolls showed 135k additions in September, missing the consensus 140k, while the prior was revised lower from 190k to 157k. The average monthly job growth for the past three months is at 145k, last year the average stood at 214k for the same period, showing signs the job market is slowing, ADP said. Pantheon Macroeconomics stated it is not as soft as it seems, however, as it incorporates official payroll data from the prior month, which only saw a rise of 96K, adding constraint to the September ADP headline print. PM notes the data does not change its forecast for the official BLS data: “The downshift in labour demand in all the surveys we follow suggest job gains will be down to just 50-to-75K by the turn of next year.” It also states that with the lower revisions has no implication for revisions to the official data on Friday. Since 2012, ADP has tended to overestimate private employment growth during August and September on an as-reported basis relative to what the BLS shows the following Friday (Figure 4). Goods and service industries were relatively healthy in the ADP report.

JOBLESS CLAIMS:

In the payrolls survey week, weekly jobless claims data printed 210k versus the 211k going into last month’s payrolls data. The underlying trend remains steady around 215k, Pantheon Macroeconomics suggests, arguing that most of the downward pressure on payroll growth is coming from scaled-back hiring, not lay-offs; “that’s normal in the early stages of a downturn, but if the economy continues to weaken, we would expect claims to begin rising, perhaps by the year-end” Pantheon says.

CHALLENGER JOB CUTS:

This month’s layoffs data declined in September, falling 22.3% M/M and 24.8% Y/Y, making it the lowest monthly total since April. The prior months’ data (Aug) was the fourth highest job cut of 2019, and Challenger notes that employers are beginning to feel effects of the trade war, with trade difficulties being attributed to around 10,000 of the job cuts announced in the last month. Challenger notes that employers held off on making any large-scale employment decisions, as “companies will monitor consumer behaviour, government regulation or deregulation, and market conditions during the final quarter of the year in order to make staffing decisions for next year.” The job cuts were led by retail (8132), Industrial Goods (5067), Automotive Companies (4912) with the consultancy noting an expected rise in coming months for this sector if the strikes at General Motors (GM) continues and the fallout impacts suppliers.

BUSINESS SURVEYS:

Within the ISM manufacturing survey, the Employment Index registered 46.3 falling 1.1 points from August, and the lowest since January 2016. ISM noted that comments were generally neutral concerning hiring for attrition, labor force reduction comments were minimal, but it did note that 29% of employment comments were cautious regarding employment expansion. ISM also notes that the manufacturing ISM’s employment sub index above 50.8, over time, is generally consistent with an increase in the BLS data on manufacturing employment. In the non-manufacturing ISM report, the employment sub-component fell by 2.7 points to 50.4; respondents noted that the number of new employees was starting to level-off, and a tightening workforce was leading to a more competitive market for qualified potential employees.

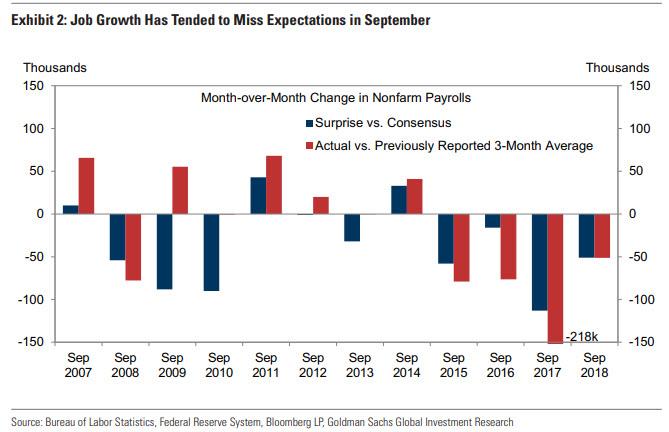

Correlating the ISM Employment print with the monthly change in payrolls would suggest a sub-zero payrolls number. If confirmed, this would be the first negative monthly payrolls number in 10 years, since September 2009.

Manufacturing employment indicators in September were mixed. Employment subindices on a number regional Federal Reserve Bank manufacturing surveys improved during the month. Markit’s manufacturing PMI employment series also improved in September. However, ISM’s manufacturing employment subindex declined further below 50, likely as a result of continued weak global growth, suggesting some downside risk for manufacturing hiring.

WAGES:

In the Conference Board’s measure of consumer confidence, the differential between jobs ‘plentiful’ and jobs ‘hard to get’ fell, auguring poorly for the unemployment rate. Analysts look for average hourly earnings to rise by +0.3% M/M, the pace paring a touch versus last month, but would still be encouraging. The Y/Y is seen remaining at 3.2%. The CB’s consumer confidence report stated that, regarding short-term income prospects, the percentage of consumers expecting an improvement decreased from 24.7 to 19.0 percent, but the proportion expecting a decrease also declined, to 5.6 from 6.3.

REVISIONS:

As in August, September payroll growth tends to be weak in the preliminary release. This may reflect a recurring seasonal bias in early vintages, and Goldman is assuming a 20-30k drag for the monthly pace reported tomorrow. As shown in Exhibit 2, first-print September job growth has decelerated in 4 of the last 5 years, and it has missed consensus in 8 of the last 10. At the same time, the 2017 and 2018 observations probably overstate the bias (due to major hurricanes in both months). There is also the possibility of positive revisions in tomorrow’s report that might reverse some of the August bias (the September employment report has included upward revisions in 5 of the last 8 years, including +87k last year). Given these offsetting considerations, the first-print bias as a roughly neutral factor for tomorrow’s report as a whole.

ARGUING FOR A STRONGER REPORT:

Jobless claims. Initial jobless claims were flat-to-down in the four weeks between the payroll reference periods—averaging 213k—and are consistent with a very low pace of layoffs. Continuing claims declined by 45k from survey week to survey week, the largest sequential improvement since April.

Labor market slack. With the labor market somewhat beyond full employment, the dwindling availability of workers is one factor weighing on job growth this year. In past tight labor markets however, payroll growth has tended to reaccelerate in September (for example in 2000 and 2007). Some firms likely pulled forward hiring into September, anticipating a shortage of applicants in Q4.

Census hiring. While temporary employment related to the 2020 Census has significantly lagged that of 1999 and 2009, it picked up meaningfully in the August report (+25k). Address canvassing continued into September, and we expect the level of Census employment to rise further from 27k in August to 40k or somewhat higher, contributing around 15k to monthly job growth in tomorrow’s report.

Job cuts. Announced layoffs reported by Challenger, Gray & Christmas declined by 15k in September to 41k and were 13k below their September 2018 level. The sequential decrease in announced layoffs primarily reflects reversals in the technology (-12k) and government (-4k) sectors, which rose sharply in August.

ARGUING FOR A WEAKER REPORT:

Employer surveys. September business activity surveys were on net weaker than expected for both the manufacturing and service sectors. The employment components of those surveys rebounded for the manufacturing sector (+1.8 to 51.4) but more importantly, they declined for the services sector (-0.7 to 52.7). As shown in Exhibit 1, the level of these surveys is consistent with an underlying pace of job growth of around 130-160k per month. Service-sector job growth rose 84k in August and averaged 121k over the last six months, while manufacturing payroll employment rose 3k in August, in line with its average over the last six months.

ADP. The payroll-processing firm ADP reported a 135k increase in September private employment, 5k below consensus and in line with the 136k average pace over the three prior months. While somewhat weaker than our estimates, the report still suggests that the underlying pace of job growth remains firm.

POTENTIAL SOURCES OF NOISE:

Will Census workers boost topline NFP again? There will likely be another 5-10k temporary Census workers reported in September according to Nomura. The Census Bureau noted in August that up to 40k temporary field staff had started address canvassing as part of the decennial 2020 census. With only 27k temporary Census workers reported by the BLS, 25k of which came in August, there is room for an additional 5-10k in September.

Will the GM strike affect nonfarm payrolls in September? Probably not. The strike took place after the BLS establishment survey reference period (the pay period containing the 12th of the month). The BLS strike report for September showed no new workers on strike during the CES survey reference pay period. However, if the strike does not end this week, it could show up in the strike report for October, with a reference week of 7 October, and potentially affect October NFP.

Forever synonymous with wealth, gold has been the most coveted mineral on earth since its first recorded use back in 3000 BC.

From Ancient Egypt to the U.S. Treasury its history is one of war, death, love and prosperity.

But how did this most precious of precious metals actually get here? How much gold is there in the world? And, most importantly, how can you get your hands on it?

Gold: Origin

It’s the stuff movies are made of. Literally. From Goldfinger (1964) to The Good, The Bad, and The Ugly (1966), from The Italian Job (2003) to Die Hard: With a Vengeance (1995). Hollywood keeps making movies that depict the irresistible nature of gold and reinforce its mythical status.

But little is known about how gold gained its unrivalled reputation or, more interestingly, how it first came to be.

According to the Greg Moore, the CEO of EuroSun Mining, the origins of gold is still the subject of heated debate in the industry. The only thing that seems certain is that such a heavy metal would require the most extreme conditions in the universe to create – both the highest densities and the highest temperatures.

Here are four of the most popular theories when it comes to the mysterious origins of gold:

#1Sun Sweat

The Aztecs famously believed that gold was the sweat of the sun and that it was literally falling from the sun to the earth, where it could be gathered. This origins story goes a long way to explaining why the Aztecs believed gold held a very strong spiritual value.

While the notion that gold is sun sweat may sound crazy, some scientists believe that the Aztecs weren’t a million miles from the truth…

#2Metal of the Gods

The Romans thought that gold was the metal of the gods, and like the Aztecs, thought that gold had descended from the sun. The Romans thought Pluto, the god of wealth, was the giver of gold and other metals.

They mined most of their gold in the Eastern part of their empire, Romania, which even today is home to a huge amount of this precious metal. In fact, the largest in-development gold mine in Europe can currently be found at EuroSun Mining’s Rovina Valley project.

Modern day miners don’t have much time to worry about the origins of this remarkable metal, but for EuroSun and its fellow junior gold miners, finds of this size will certainly seem like a god send in the current bull market.

#3The Rock Star

Now we don’t want to get bogged down in the detailed astronomical explanations behind this theory. Suffice it to say that some scientists believe gold is created when a “rock star” collapses and becomes a very heavy neutron star (aka, black hole). The extreme density and heat created by this explosive process, called a supernova, is what some scientists think creates these heavy elements such as gold.

#4 Neutron Stars

An alternate cosmic theory is that when two neutron stars touch each other, it creates billion-degree heat and extremely high density, which is powerful enough to eject mass, creating a Jupiter-sized batch of gold in a single go.

Regardless of which cosmic phenomena are responsible for forming the precious metal, most scientists do agree on how that universe-created gold came to earth. It is widely understood that gold arrived on this planet in meteor showers a couple hundred million years after the earth was formed.

As for the involvement of god… well that is a question we are going to leave open to you.

Easy Come, Easy Go

Origins may be elusive, but the meaning is certainly not. We may not know exactly how it came into being, but the mysticism has only added to gold’s use, since the beginning of time, as a currency.

Other currencies have come and gone, but gold has remained as the support for nearly all currencies around the globe. Its long-term value, unlike other forms of currency, has kept it above all other minerals. While dollar bills and other forms of paper currency eventually took over how the world conducts business, gold has backed many currencies, and at one point in history, the United States even backed every dollar that was in circulation with gold.

So where does this leave us? None the wiser, but all the richer.

In the immediate term, it’s about getting gold out of the ground, not finding more. We’ve tapped out Earth’s supplies. Origins, as far as miners like EuroSun in Romania are concerned, is quite a simple concept: It’s in the ground in the Rovina Valley in droves, and now –we need to get it out in an economically viable way. It is now technology that rules supreme in the gold space, with the most efficient extraction process bringing in the huge returns.

In the EuroSun case, their new technology essentially makes gold afraid of water and pushes it to the surface, devoid of all the waste. Whether or not the Roman gods put it there, a large portion of Romania’s gold will soon be extracted.

In a beautiful cyclical manner, it seems that the gold story is likely to end where it began – with the race to mine space already underway. After new technologies have squeezed the last of our gold reserves out of the earth, we must look to the origins of this most precious of metals and search for more in the final frontier.

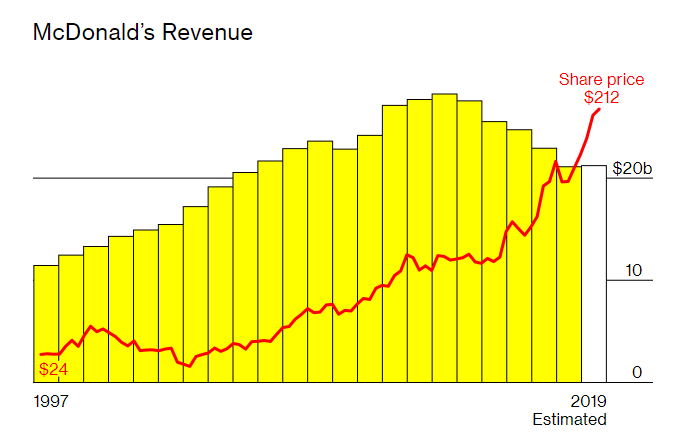

McDonald’s Goes “Big Tech” While Franchisees And Money Losing Delivery Companies Bear The Costs

McDonald’s is trying to turn around its business, like many other companies, by moving to a more “futuristic” business model. And by “futuristic”, of course, we mean benefiting from increased costs it is lopping onto its franchisees and taking advantage of ubiquitous money-losing delivery services.

A week before Steve Easterbrook was named McDonald’s CEO, the company had suffered one of its worst years in decades. Customers were ditching McDonald’s for Chipotle burritos and Chik-fil-A sandwiches en masse, according to a new Bloomberg Businessweek profile.

To add insult to injury, the company lost hundreds of thousands of customers to Burger King during the week of Spain’s Real Madrid vs. Barcelona match – one of the most important fixtures in all of soccer. Customers were choosing Burger King’s delivery option, which McDonald’s didn’t have. Hundreds of other burger competitors were popping up on food delivery apps across the U.K., as well, pushing Easterbrook to address the weakness.

Lucy Brady, who oversees McDonald’s global strategy and business development teams said: “He looked at me and said, ‘We’re not going to go through the traditional market pilot and study delivery for six months. We’re just going to do it’.”

Easterbrook then commanded each country’s manager to nominate their best executive to build out an online delivery business that would be operational in just two week’s time. Brady suggested a target of having 3,000 delivery restaurants online by July 1. Easterbook came back by saying he wanted to get 18,000 locations online – about half of the company’s locations around the globe.

Easterbrook made it so that management’s compensation was tied to the speed of the roll out and McDonald’s quickly teamed with Uber Eats for the widest possible deployment. The partnership was so meaningful to Uber, that it devoted two pages to its delivery agreement with McDonald’s in a roadshow prospectus ahead of Uber’s IPO.

Easterbrook, who let go 11 of the 14 most senior executives he inherited, now says he uses the service when he travels to get a gauge of its quality. McDonald’s expects the delivery business to account for about $4 billion in sales by the end of this year.

But catching up to Burger King on delivery wasn’t the only goal Easterbrook had. Easterbrook seeks to reconfigure all of his restaurants into data processors, utilizing things like machine learning and mobile technology.

It’s a great vision for McDonald’s, but it hits the wallets of franchisees hard. Franchisees have mostly balked at the costs that it would require to equip their stores with things like license plate scanners and touchscreen kiosks.

And what would futuristic sounding bullshit be if Wall Street didn’t eat it up? For McDonald’s stock, the strategy is working. As the article notes, only a couple of companies in the S&P 500 have outperformed McDonald’s since 2015. Easterbrook has said he seeks to reclaim the company’s image as a “beacon of innovation”.

Currently, the company has a market cap of $159 billion and feeds about 1% of the human population daily. But its share of the US market has shrunk to 13.7% from 15.6% in 2013, ceding ground to casual dining chains like Panera and burger joints like Shake Shack and Five Guys.

The company’s earnings started to stagnate in 2013 and fell by almost 20% to $4.7 billion the following year. The company’s former CEO, Dan Thompson, said upon leaving that the company had “failed to evolve at the same rate as our customers’ eating out expectations”.

Easterbrook became the company’s global chief brand officer in 2013 and sat down with Apple CEO Tim Cook to become a partner for the Apple Pay launch system. This resulted in a digital add-on installed on every machine at McDonald’s 14,000 locations in the US.

In 2014, the company launched the “experience of the future” concept which was an initiative that Easterbrook had worked on.

It reimagined the entire store from the ground up: from how orders were placed, to what services were offered. Some franchisees have benefited so much from the ideas that restaurant sales are growing at double digit rates.

But other franchisees have banded together to try and force the company to slow the program’s roll out two years past its original target. These franchisees are objecting to the massive cost of the project, which can run into the tens of millions of dollars for owners of select locations – even after McDonald’s pays for 55% of the remodels.

Adding an Uber Eats counter for delivery, touchscreen kiosks, modern furniture and power outlets means that franchisees can incur costs up to $750,000 per restaurant, according to McDonald’s.

But the enhancements are achieving what they set out to do. Annual profits are inching higher again and McDonald’s posted its fastest global sales gain in seven years last quarter. Changes like including all day breakfast have also brought customers back and the company has introduced a curbside pick up system that allows customers to order through the app and notify the store when they are within 300 feet of the property.

But the company’s workers and franchisees who have long complained about low hourly wages and poor conditions have taken a dim view of the overhaul. Workers claim that new items, self order kiosks and app orders have them “riddled with anxiety”, even causing some workers to flee to competing fast food restaurants.

Eli Asfaw, who operates seven franchises in the Denver area said: “I would like to make the kitchen as stress-free as it possibly can be. For a start, scaling back rollouts mandated by the company, such as all-day breakfast, would make it easier for us to keep people and make our people happy.”

Staff welfare continues to be a major issue for the company in the United States, where the median pay for food workers is $10.45 an hour. Complaints of endemic sexual-harassment and poor working conditions have been a national conversation and part of the political fabric, with 2020 Democratic presidential candidates sending a letter to Easterbrook about his “unsafe and intolerable” work conditions and “unacceptable” behavior at the chain’s restaurants.

One franchisee, who owns 21 stores near Washington DC, says the modernization has succeeded in attracting new customers, but the revamp was a burden: “There’s training that’s involved. We have to get the employees ready for it—mobile order and pay and Uber Eats and kiosks. All these different things are happening at the same time, and it really took a toll on us.”

Meanwhile, McDonald’s shows no signs of slowing down, acquiring AI startup Dynamic Yield for $300 million in March and Silicon Valley startup Apprente Inc. in September. The acquisitions will help add learning software to drive-thrus and use voice recognition software to hopefully cut down on lines in restaurants.

“We were just going so hard at it, it proved to be a bit of a handful,” Easterbrook concedes of the roll out.

You can read Bloomberg’s full writeup on Steve Easterbrook here.

Trump Dares Pelosi To Hold Impeachment Inquiry Vote After She Says It Is “Not Required”

Is president Trump about to be impeached without the House even holding a vote authorizing the very impeachment inquiry to which he is subject? Well no – he won’t be impeached as the Senate will promptly vote the entire political theater down – and that precisely why Pelosi, who until last month was vehemently against starting impeachment proceedings, refuses to hold a vote.

In a letter to Pelosi, House GOP Leader McCarthy today asked 10 questions including, among those: Do you intend to hold a vote of the full House authorizing your impeachment inquiry? Pelosi response: not at all.

Speaking this morning an interview, Pelosi dismissed the impeachment vote as “not required” and added “we haven’t, but we could.” She said they could hold a vote “because it is a Republican talking point.” For now, however, she is dismissing this as a political move – one in response to her own political move, of course – and pressing ahead with the investigation.

Of course, it’s hardly a secret why Pelosi is eager to impeach Trump without actually voting to authorize a formal inquiry: such a move not only insulates vulnerable Democrats running in red districts but shuts down the GOP’s ability to wage a legal offensive of its own.

On paper at least, House Democrats who support Trump’s impeachment have more than enough votes to follow through, with 226 now backing his ouster compared to just 9 holdouts, according to a Politico tally.

So far, however, Pelosi has declined to hold a vote on moving forward with the inquiry, and her aides make a point of saying it’s not required.

“There is no requirement under the Constitution, House Rules or House precedent that the House has to take a vote before proceeding with an impeachment inquiry,” Pelosi spokeswoman Ashley Etienne told RealClearPolitics in a statement. “The Committees of the House now have robust authority under the House’s existing rules to conduct investigations for all matters within their jurisdiction, including impeachment investigations. For several decades, impeachment investigations have frequently been conducted without a full vote,” Etienne added.

On Thursday Pelosi doubled down, maintaining in a Thursday letter to the House’s Republican Leader, Kevin McCarthy, that there “is no requirement under the Constitution, under House Rules, or House precedent that the whole House vote before proceeding with an impeachment inquiry.”

But Republicans are quick to point out that in the only presidential impeachment investigations to have taken place over the last four decades – those against Presidents Bill Clinton and Richard Nixon — the House voted on the inquiry, thus authorizing the Judiciary Committee to investigate.

Why do Republicans want a vote, besides have Democrats – especially those in states won by Trump – be put on the record? Because, as RealClearPolitics explains, holding a formal vote on impeachment would allow Republicans to subpoena documents and witnesses and investigate all the revelations surrounding the whistleblower’s complaint about Trump’s interactions with Ukraine, as well the roles of Joe Biden and his son Hunter in Ukrainian corruption allegations.

“Republicans would have the opportunity to get information from all sources and get it on the table,” Cleta Mitchell, a conservative political law attorney, told RealClearPolitics. “The process they are proceeding under through their committee attorney means they are the only ones who have the rights to gather information.”

Rep. Doug Collins, who serves as the top Republican on the Judiciary Committee, argued Monday that if Pelosi were proceeding in a serious and “somber” manner, as she has claimed, she would bring the impeachment inquiry up for a floor vote.

“Formal impeachment would actually afford due process and ensure both sides are heard,” Collins tweeted Monday.

The Georgia lawmaker, one of Trump’s strongest allies in Congress, accused Pelosi of abusing her power by failing to hold that formal. “It’s not America when you can simply ramrod a hearing without allowing the person who is being accused or the minority to have more rights. … This is just not fair and the American people will see through this,” he predicted during an interview on Fox News.

* * *

Which brings us to late on Thursday, when Trump himself figured out that his position would be strengthened by having a formal vote, because according to Axios, the White House is planning to send Nancy Pelosi a letter as soon as Friday arguing that President Trump and his team can ignore lawmakers’ demands until she holds a full House vote formally approving an impeachment inquiry.

In addition to the above considerations, Axios notes that by putting in writing the case that Trump and his supporters have been making verbally for days, “the White House is preparing for a court fight and arguing to the public that its resistance to Congress’ requests is justified.”

Trump wants to force House Democrats in vulnerable races to be on the record if they favor pursuing impeachment, these sources tell us.

Republicans also say the minority party can exert more influence over hearings and other aspects of an inquiry once it is formalized with a vote.

By calling this an inquiry without holding a vote, Pelosi and the Democratic committee chairmen are having it both ways, one official said. “They want to be a little bit pregnant.”

A letter could be filed as soon as Friday, because according to Axios sources, several White House lawyers spent a good chunk of their Thursday reviewing the language in the letter, expecting that it could find its way before a judge.

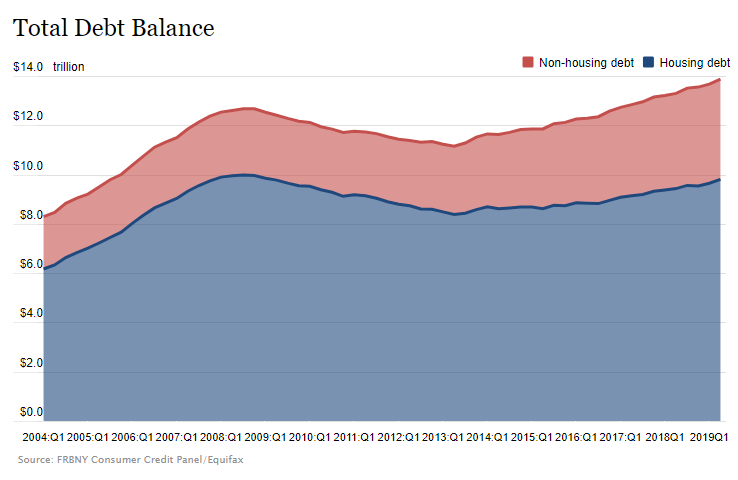

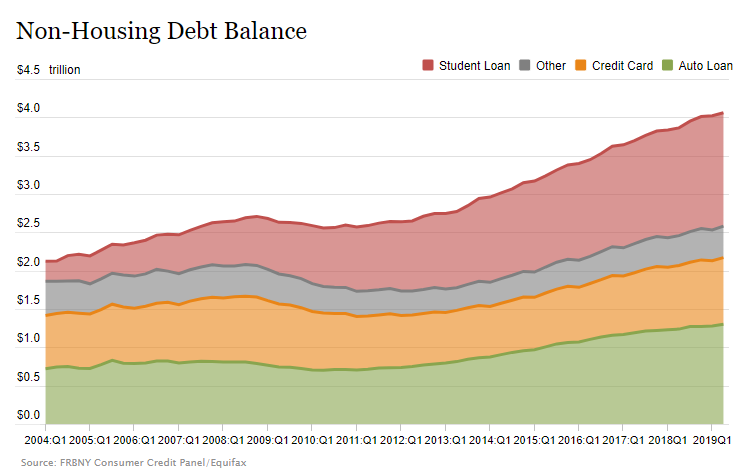

Millennials Are Now Putting Everyday Items, Like Shoes & Sweaters, On Payment Plans

In what is certainly a microcosm of how dire the consumer credit situation in this country has become, startups like Affirm are now offering credit to millennials who want to buy products priced much lower than those traditionally bought with financing, according to the Wall Street Journal.

Yes, installment plays and layaway – constantly the butt of jokes for those who were always far too broke to afford whatever they were buying – have now become an everyday reality. But not for big ticket items, for everyday purchases, like shoes.

Take, for example, Sean Gauthier. He recently used an offer from Affirm to buy a “pair of white, pink and green Nikes” and pay for them over 6 months. He says he could have bought them outright (sure he could have) but said that the $5 that the company charges in interest is worth it to be able to make flexible payments.

And these types of everyday installment purchases are being encouraged at merchants like Walmart, Urban Outfitters and H&M, all of whom will be offering payment plans at checkout.

It’s a way for merchants to address a consumer debt bubble in the country that has grown significantly out of control, despite the “good economy”. Everyday consumers continue to rely on borrowing to fund their daily lives and consumer debt is higher than ever as a result of products and services getting more expensive while wages stagnate.

And growth for these payment plans is booming. Affirm’s point of sale loans have doubled to about $2 billion last year and are expected to double again this year. The market is tiny compared to the $450 billion in spending limits on new U.S. credit cards, but more than half of merchants surveyed this year said they plan on offering these installment options – or already do.

Meanwhile, about 40% of consumers surveyed “said the ability to finance a purchase at checkout made it more likely they would complete a transaction“.

And the big investment banks smell blood: JP Morgan, Citigroup and American Express are all introducing, or have introduced, payment programs for cardholders that resemble installment loans.

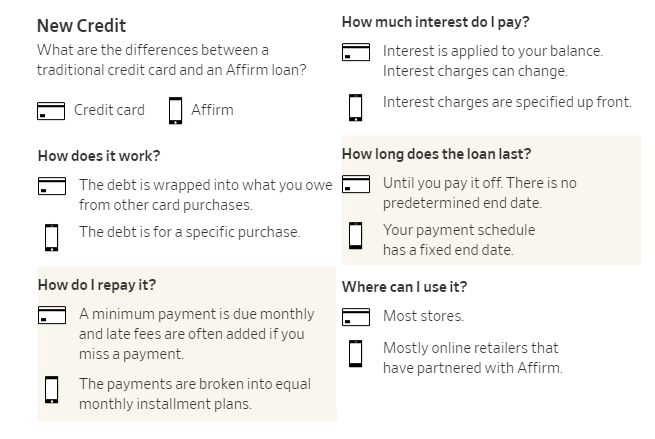

The Journal explained how Affirm works:

Say a borrower buys a $100 outfit. With a credit card, he will need to pay that off by the next due date or carry a card balance, which can last months if he makes only the minimum payments and racks up interest charges. With an installment loan, he pays a fixed amount with each payment—say, $25 each month over the following four months, or more depending on interest or other charges—and knows ahead of time what the total will be.

Some borrowers even claim that installment plans force them to be more disciplined to pay back the money. With this type of savvy financial acumen, we’re wondering why they never thought of not borrowing $50 to buy a sweater in the first place.

Guy Stephens, who has used Affirm, said:

“When you put something on a credit card, it vanishes into a big black ball of debt. There are balances I’ve had over time where I don’t even know what I bought.”

Larger purchases can require larger installment payments. For example, a $400 purchase, could require four $100 installments. With a credit card, the minimum due would be significantly lower. The plans are offered when customers are browsing products or about to purchase an item. Retailers hope the services will draw in new customers and – surprise – get them to spend beyond their means more.

The loans aren’t secured, which means that lenders have little recourse against a borrower who won’t pay. They can, however, be referred to debt collectors.

Some borrowers use the plans because they can’t get approved for credit cards – usually for good reason.

For example, Heidi Peyser said she was rejected for several credit cards because she stopped paying her bills. To Affirm, that is a perfect client. She was offered an installment plan to buy a mattress on Purple.com. “I thought ‘Well, let’s see how this goes,’ ” she said.

She has since signed up for 5 Affirm plans since 2017 to buy such crucial “must have” items like like woodworking tools and a gel to help with joint aches. She paid off her loans recently.

Another consumer, Erica Padilla, has used Afterpay 19 times.

“It makes it easier to think, ‘OK, I have to pay $25 now’ [rather] than spending $100 upfront,” she said, deluding herself as to the actual cost of items she was buying. She used the app over Christmas to buy “$75 of videogame T-shirts for her 13-year-old son at Forever 21 and $60 of rock-themed tops for her toddlers.” She, too, has paid off her balances.

Without Afterpay, she said: “We definitely would have bought less.”

Catherine Tabor, 24, has used the American Express arrangement nine times to buy such “much have” items like concert tickets and an opera house tour. She commented: “I’m not making a whole lot of money, so this is really helpful.”

Back in August of 2017, we reminded the world that millennials couldn’t afford anything without financing, reporting that they were financing purchases from airplane tickets to luxury bedsheets with loans from payment companies like PayPal and Affirm. Indeed, millennials’ seeming inability to pay for anything outright has caused revolving debt in the US to balloon past $1 trillion.

We followed up in November of 2018, reporting that three other notable finance technology companies had hit the scene with installment services – a business model that established players such as Discover has warned might get dicey if the economy goes sideways and defaults spike.

But we know it’s not a question of “if”, it’s a question of “when”.