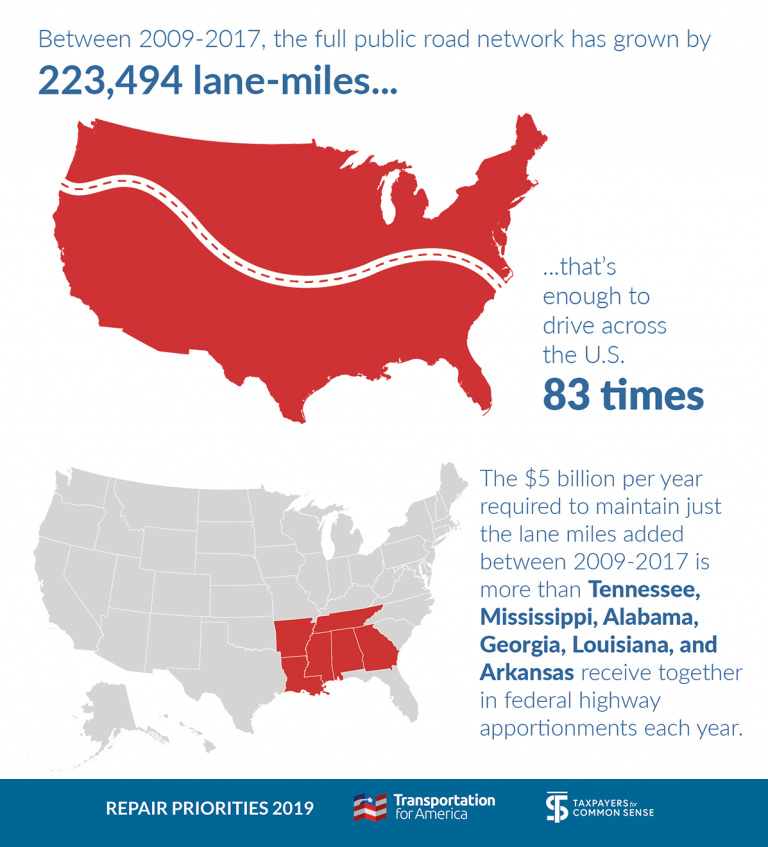

As Statista’s Niall McCarthy notes, it found that states are continuing to push ahead with the expansion of their roads while neglecting to repair and carry out regular maintenance on existing infrastructure, which is creating new financial liabilities. The share of roads in poor condition nationwide increased from 14 to 20 percent between 2009 and 2017. This is particularly concerning given that Congress has provided addtional federal funding for transportation infrastructure twice during that timeframe.

As of 2017, the U.S. would have to spend $231.4 billion annually to keep its existing road network in a decent state and restore the backlog of roads in a poor condition over a six-year period. Between 2004 and 2008, states collectively spent $21 billion per year on road expansion and $16 billion per year on maintenance and preservation. Between 2009 and 2014, spending on new projects came to $21.3 billion while while the collective outlay for maintenance totaled $21.4 billion. Despite that increase, the still considerable financial outlay on new roads will require considerable and possibly unsustainable investment in the years ahead.

When it comes to managing the balance between new roads and the maintenance of existing ones, some states are performing better than others. For example, South Dakota allocated 69 percent of its highway capital budget to road repair between 2009 and 2014. During the same period, Mississippi dedicated 4 percent to repair and 77 percent to expansion. Given how mismanaged funding is, which states had the worst roads in 2017?

According to the report, 53 percent of roads in Rhode Island are deemed to be in poor condition, along with 45 percent in California and 42 percent in Hawaii. Idaho and Tennessee were at the opposite end of the table with only 5 percent of roads in both states deemed to be in poor condition.

via ZeroHedge News http://bit.ly/2HVX3wt Tyler Durden

“It seems that if there was any truth to our language, ‘trust’ would be a four-letter word.”

Joel – “Risky Business”

Trust is the most important aspect of human endeavor.

Without trust there can be no interaction. No communication.

No friendship. No love.

No Commerce.

The key to understanding economics is understanding people. The basis for all human interaction is the basic trust that a trade once completed will be honored.

The global economy runs solely on trust. Without the trust that contracts signed today can be fulfilled tomorrow and disputes settled with a reasonable degree of amity, there can be no iPhones.

No Amazon.

No oil.

When politics become toxic, when the sides refuse to cooperate on the very basic functions of government, uncertainty reigns. And uncertainty filters down to the people getting up everyday, going to work and providing a home for themselves and their families.

It’s like that great scene in the classic movie “Trading Places” where Eddie Murphy talks about the guy who’s worried he won’t be able to buy his kid that “G.I. Joe with the Kung Fu Grip” for Christmas.

That guy was the barometer for the market. That guy knew something about trust.

I had one of those G.I. Joe’s as a kid. My dad rarely let me down in supplying the most important things on my Christmas list.

It’s part of the reason why I loved him and trusted him completely. He was very human, but he kept his promises and I always knew where the boundaries were.

He and mom did what they could without making promises they couldn’t keep.

That example, despite the heartbreaks and the setbacks, shaped my approach to being a husband and a father. I don’t make promises to my daughter or my wife I can’t keep.

The global economy works on the same basic principles as the trust between you and anyone close to you. Trust takes a lifetime to build and a minute to lose.

This is why I watch in horror as company after company betray the basic trust between them and their consumers. From Facebook to Google, Twitter to Mastercard they all now believe it is in their best interest to dictate terms to their customers.

They’ve moved from offering their services to people to judging them as worthy of using their product. They’ve broken the basic trust providing a place to communicate or do business free from bias that was sold to us when they needed us.

Now our opinions are inconvenient to their political and social goals.

But we know it doesn’t come solely from them. We know this pressure comes from powerful political forces intent on holding onto stolen power gained through years of inflation, legislation and media manipulation.

And they will, in the end, empower the competition that will destroy them. Because once you lose someone’s trust. No amount of convenience or enticements will bring them back.

The same holds true, if not more so, for political institutions. Brexit is proving that Britons who wanted out of the European Union were right that the political classes and monied oligarchy I like to call The Davos Crowd view the people as inconveniences to their consolidating power for their own betterment.

Brexit has destroyed the careers of two British Prime Ministers and will likely destroy both the Conservatives (Tories) and Labour before it’s finally done.

Theresa May’s resignation was met with cheers by the working class in the U.K. like England had just won the World Cup.

The media punditry, namely Ryan Heath of Politico, in love with the EU are already writing eulogies for it in anticipation of poor turnout giving voice to Euroskeptics who don’t represent the ideals of a united Europe.

Among Heath’s 12 people who have ruined the EU elections are Helmut Kohl, Angela Merkel and Mark Zuckerberg the very people who weaponized the Deutschemark (euro), immigration and censorship respectively.

Trust in the money, your community and your ability to express yourself are all under basic attack.

Donald Trump is single-handedly attacking the foundations of a global economy at a time when it is in no position to handle the shock of his bipolar personality disorders.

“We have diverted so much money and capital to education that we have cheapened its value in the labor market while encouraging two generations of kids to go heavily into debt to chase some dream of fame or fortune that had an ever-shrinking probability of ever coming true.

$100,000 for a Women’s Studies degree will not train you to run a production line. It won’t get your air-conditioner fixed. And it won’t prepare you to take responsibility for your wasted time and energy.

But what this will do is further destroy trust in our leadership as the premier place to do business in the world.

The gap between the U.S.’s legal infrastructure and the rest of the world’s is shrinking. Trust is breaking down. Countries like Russia are rising in trust while the U.S. falters.

In 2012 the U.S. ranked 4th in the World Bank’s Ease of Doing Business. We’ve since fallen to 8th. In 2012 Russia ranked #111 while today they rank 31st, which is better than that of China at #46.

And that rank rose sharply in 2018 along with India, who still has a long way to go.

Commerce seeds ideas and humans are very good at figuring out what is worth copying and what isn’t. The difference between a Frontier/Emerging Market and a Developed one is trust. Putting money into them is easy. Getting that money back out is the barrier to commerce and growth.

Every day Donald Trump wakes up and sanctions another company. Another CEO. And every day the world looks on in horror as the rules of trade change.

Every day is another day where trust frays a little more.

When it’s lost chaos follows. That is what we’re witnessing today and what will shape our investment decisions tomorrow.

Germany’s top official on anti-Semitism has caused a stir by saying that he would not advise Jews wear skullcaps in certain parts of the country, according to AP.

Felix Klein said in an interview published Saturday that his “opinion has unfortunately changed compared with what it used to be” and that he couldn’t “recommend to Jews that they wear the skullcap at all times everywhere in Germany.”

He also said German police were not familiar with how to deal with anti-Semitic crimes:

“Many of them don’t know what’s allowed and what’s not. There is a clear definition of anti-Semitism and cops should be taught it during their training.”

He didn’t elaborate further on details of what he meant, including what times and places he was referring to. Germany is home to about 100,000 Jewish citizens, according to Haaretz.

Israeli President Reuven Rivlin said on Sunday that he was “shocked” by the comment:

“The statement of the German government’s anti-Semitism commissioner that it would be preferable for Jews not wear a kippa in Germany out of fear for their safety, shocked me deeply.”

He continued:

“We will never submit, will never lower our gaze and will never react to anti-Semitism with defeatism — and expect and demand our allies act in the same way.”

The country’s main Jewish leader, Josef Schuster, also said last year that he “would advise people visiting big cities against wearing Jewish skullcaps”. He continued:

“It has long been a fact that Jews are potentially exposed to danger in some big cities if they can be recognized as Jews.” He added that he pointed that out two years ago, “so it is to be welcomed if this situation gets more attention at the highest political level.”

Three years before that, he also cautioned against wearing one in areas with large Muslim populations. His comments in years prior have been met with criticism from religious leaders in Israel. The country’s chief rabbi, David Lau, said that “skullcaps are a Jewish symbol they should continue to bear proudly.”

Last April, Germans wore skullcaps in protest of an anti-Semitic attack in Berlin. Meanwhile, statistics from the German government show that the number of anti-Semitic incidents grew in Germany last year, despite an overall drop in politically motivated crimes.

The German Federal Ministry of the Interior says there has been growth of 20% in anti-Semitic crimes in the country. Extreme right-wing activists were responsible for 90% of the 1,800 incidents in 2018.

Michel Friedman, former vice president of the Central Council of Jews in Germany, said: “When an official government representative tells the Jewish community they can’t be protected from violence, it’s a show of poverty for Germany’s legal and political reality.”

via ZeroHedge News http://bit.ly/2MdXw2k Tyler Durden

The first Chinese commentaries have appeared on the outcome of the general elections in India. The timing is important, since the counting of votes is yet to take place in India. Yet, Chinese commentaries have presumed that the result cannot be contrary to the trend that the exit polls have indicated – that PM Modi is securing a renewed mandate to head another government.

This presumption is broadly in line with the estimations by Chinese commentators in the recent weeks and months. The Chinese commentators have not hidden their acclamation of the Modi government. Contrary to the common opinion among Indians that the Modi government showed a pro-US tilt in foreign policies, the Chinese (and Russian) opinion has been generally positive about Indian policies through the past 5 years.

China was not particularly perturbed that India has a deepening engagement with the US or that India’s non-alignment is in any great danger. This opinion was reinforced following Modi’s informal summit with the Chinese President Xi Jinping last year in April in Wuhan and with Russian President Vladimir Putin a month later in Sochi. It stands to reason that both Xi and Putin have sized up Modi from very close, intimate quarters and decided that they could do business with him even in new Cold War conditions.

In fact, in an extraordinary gesture of camaraderie, the Kremlin announced the decision to confer Russia’s most prestigious national award to Modi after the Indian election got under way.

A commentary by the “Observer” in the Chinese communist party newspaper Global Times on May 20 is self-revealing in its display of a sense of relief that Modi will be at the helm of affairs in Delhi at a critical juncture in the geopolitics of the region. The following excerpts will be of interest:

1. “Modi’s reelection will further stabilise and improve China-India relations. During Modi’s term of office, India’s relations with China show the trend of steady development. The meeting between President Xi Jinping and Modi in 2018 opened a new chapter for the two countries’ bilateral ties and laid the foundation for future relations.”

2. Admittedly, Modi’s actions have also triggered controversy in China — such as his initial bonhomie with the Tibetan leadership based in Dharamsala, his three visits to Arunachal Pradesh or the rising trend of Hindu nationalism (which “somewhat contained Modi’s policies towards China.) But these were actions with an eye of India’s domestic politics with the aim to “drum up support” for the Bharatiya Janata Party, while “generally speaking, Modi’s policies have been sound.”

3. “Modi separated political conflicts from economic cooperation, a wise move that brings reciprocal results to both countries (India and China). Modi knows that tense relations with China are not in line with India’s interests.”

4. “India joined the Asian Infrastructure Investment Bank although the US and Japan strongly opposed… India has stuck to its policy of non-alignment and did not adjust its policies toward China according to Washington’s strategy for Beijing. These are all positive diplomatic achievements of the Modi administration.”

5. Looking ahead, “these policies will continue if Modi is successfully re-elected… Modi’s reelection benefits the continuity of his policies toward China and the two countries’ mutual trust.”

6. “India’s dispute with Pakistan is an important factor that influences China-India relations. China always encourages the two countries to build mutual trust through cooperation in trade, economies, anti-terrorism and other areas. As Pakistan and India are both members of the Shanghai Cooperation Organization, they will have more cooperation within the framework.”

The commentary draws satisfaction with the recent trend that India’s deficit in bilateral trade trade is steadily narrowing. And it envisages that the US-China trade war “provides more chances… (as) China will turn to India when it is looking for a substitute for imports.” Pharmaceuticals and computer software are particularly promising areas. Equally, the commentary is cautiously optimistic that India may take a fresh look at the Belt and Road projects in South Asia.

The Chinese commentators have consistently hailed Modi as a “reformer” who is taking India on a path of modernisation and rapid growth. In their judgment, Modi is far from dogmatic in foreign policies and has an open mind to expand cooperation with China, mindful of the advantages that such cooperation can bring to advance his development agenda.

In strategic terms, China is not overtly anxious that under Modi’s stewardship, India continued to expand its so-called “defining partnership” with the US. But the “red line” will be India’s strategic autonomy, which, in the Indo-Pacific context, narrows down to Modi hitching the Indians wagons to Trump’s regional strategies. In the Chinese assessment, Washington is eager to lure India into its bandwagon, but Modi has been doing a smart trapeze act by getting all good things from the big powers without really giving away anything that might erode India’s freedom of thinking and action.

Curiously, Russia also shares the Chinese view. To what extent Indian policies have figured in the Sino-Russian discourses we do not know — and we may never get to know. But India being a “swing state” in the contemporary world situation, its policies impact the Eurasian integration processes, which are at the core of the Russian and Chinese strategies. It is entirely conceivable, therefore, that Moscow played a significant role behind the scenes in getting the Chinese block removed on the Masood Azhar denouement.

Prime Minister Narendra Modi and Chinese President Xi Jinping at the informal summit in Wuhan, China, April 2019

Without doubt, the delisting of the Azhar controversy from the litany of India-China discords is a defining moment in the trajectory of relations between the two countries. Conceivably, a period of creative diplomacy lies ahead as China takes over the chair of the Financial Action Task Force for the coming one-year period starting in July. (Xiangmin Liu, who currently serves as director-general of the legal department at the People’s Bank of China (China’s central bank) and concurrently as the vice-president of the FATF, picks up the baton of presidency for an one-year term from the US’ Marshall Billingslea at the meeting of the grouping at Orlando, Florida on June 16-21.)

Between the Shanghai Cooperation Organisation (SCO) and the FATF, there is scope for dialectical thinking to arrive at a reasonable reconciliation of the seemingly contradictory and intractable issue of terrorism in India-Pakistan relations. This is where China’s unique position to promote reconciliation comes into play. The FATF plenary is of vital importance for Pakistan, as a decision will be taken whether the country should be moved out of the “grey list” or kept there due to any residual shortcomings. Of course, this would have significant bearing on Pakistan’s standing with multilateral lenders like the IMF, World Bank, ADB, etc. and in risk rating by agencies such as Moody’s, S&P and Fitch. Islamabad is attaching high importance to the FATF designation.

Significantly, EAM Sushma Swaraj is attending the SCO foreign ministers meeting in Bishkek on May 20. Swaraj will certainly run into her Chinese and Pakistani counterparts in Bishkek. The SCO summit meeting is due to be held on June 13-14. Suffice to say, if China is successful in cutting the Gordian knot of terrorism in India-Pakistan relations, a new vista opens up in the Sino-Indian relationship and we may see a new dawn in the politics of the region.

Quite obviously, China is conscious that the China-Pakistan-India triangle is at an inflection point. An influential “India hand” in Beijing’s strategic community, Ma Jiali, a senior research fellow at the China Institute of Contemporary International Relations, has been quoted in a Global Times report yesterday as saying that “the growing US presence would have limited influence on overall China-India relations” and in regional security, he underscored that China will continue playing a mediating role in India-Pakistan relations. Ma added China highly values its relations with both India and Pakistan. China will keep furthering its relations with Pakistan, and also attach great importance to India’s concerns.

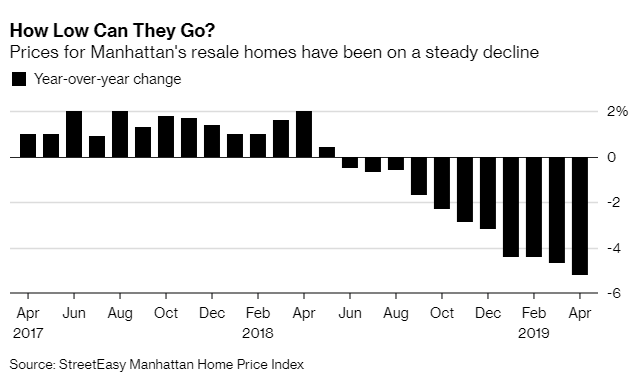

Proving that higher prices aren’t always better news, housing in Manhattan may finally be catching a bid after a nearly yearlong slump in prices has plunged far enough to finally attract buyers. Additionally, inventory growth finally looks to be slowing down.

Manhattan home prices were thrashed again in April, falling the most since 2010 – but this time, there may be somewhat of a silver lining. The falling prices caused buyers to “pounce”, resulting in 1,193 homes under contract during the month – more than any month since April of 2015, according to data provided by Bloomberg and StreetEasy. Perhaps deflation is not so evil after all.

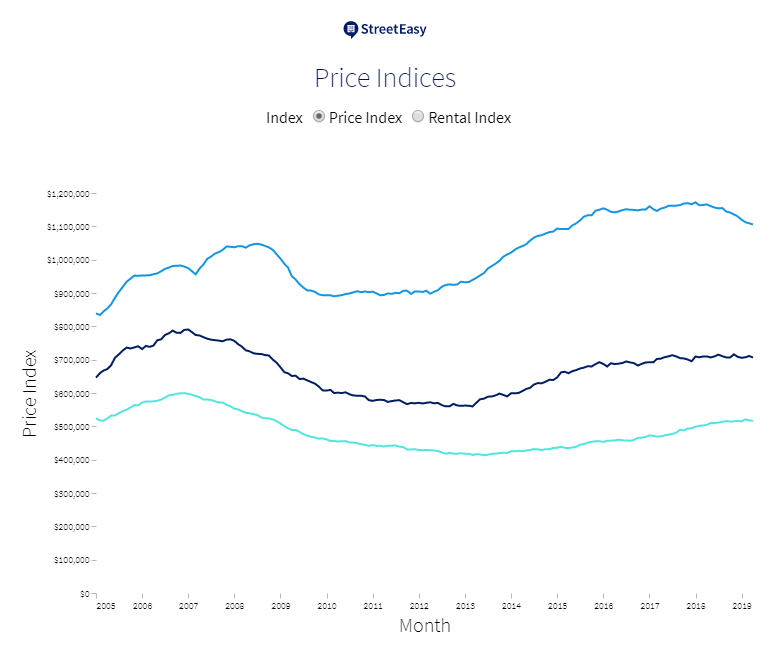

StreetEasy’s price index fell 5.2% from a year ago to $1.11 million. The index measures change in resale prices for the same properties over time. It was the largest decline in the index since April 2010, when the index dropped 6.1%.

The newfound bid for homes could be a sign that Manhattan’s market may be emerging from a drought of buyers, who had been previously been sitting on the sidelines, scared of overpaying for properties. As prices move toward more realistic buyer expectations, capital has been put to work.

Grant Long, senior economist at StreetEasy said: “Sellers are finally getting that many of their price expectations were not realistic. They’re lowering their prices to a point that’s attractive to buyers.”

Here are some of StreetEasy’s additional findings:

The most homes went into contract since 2015. The number of pending sales in Manhattan increased 26.6% from last year, up by more than 250. The number of homes entering contract in Upper Manhattan doubled year over year, from 66 to 132.

Inventory growth slowed. While sales inventory growth remained in the double digits at 10.8%, it still moved at the slowest pace in 13 months. The volume of new inventory hitting the market shrank by 9.6% over last year.

As sellers priced homes more strategically from the start, fewer made price cuts. The share of homes with a price cut fell slightly for the first time in 13 months. Some 14.1% of Manhattan homes saw a price decrease in April — down 0.6 percentage points from last year. The share of price cuts fell the most in the Upper West Side — down 2.1 percentage points to 14.2%.

Luxury home inventory dropped slightly. The number of homes for sale priced within the top 20% of the market fell by 0.3%, the first year-over-year decrease in inventory since February 2018.

Recall, in early May, we wrote that inflated and overpriced retail real estate in Manhattan was turning the city into a “wasteland”. Later, the Post wrote an article confirming our writeup from late March which pointed out that high prices were driving businesses out of town:

If you want to see the future of storefront retailing, walk nine blocks along Broadway from 57th to 48th Street and count the stores.

The total number comes to precisely one — a tiny shop to buy drones.

That’s right: On a nine-block stretch of what’s arguably the world’s most famous avenue, steps south of the bustling Time Warner Center and the planned new Nordstrom department store, lies a shopping wasteland.

It appears that, despite what central bankers think, the only logical, and natural, response to high prices is, gasp, low prices. Unfortunately, while the Federal Reserve may be willing to ease back on US home prices, it has so far refused to do the same to the stock market. And just like unsustainably high prices resulted in the bursting of the housing bubble in 2007, so the inability of the market to deflate to a fair value will be the reason behind the next great bubble burst.

via ZeroHedge News http://bit.ly/2EzUYW6 Tyler Durden

In its escalating confrontation with Iran, the US is making the same mistake it has made again and again since the fall of the Shah 40 years ago: it is ignoring the danger of plugging into what is in large part a religious conflict between Sunni and ShiaMuslims.

I have spent much of my career as a correspondent in the Middle East, since the Iranian revolution in 1979, reporting crises and wars in which the US and its allies fatally underestimated the religious motivation of their adversaries. This has meant they have come out the loser, or simply failed to win, in conflicts in which the balance of forces appeared to them to be very much in their favour.

It has happened at least four times. It occurred in Lebanon after the Israeli invasion of 1982, when the turning point was the blowing up of the US Marine barracks in Beirut the following year, in which 241 US military personnel were killed. In the eight-year Iran-Iraq war during 1980-88, the west and the Sunni states of the region backed Saddam Hussein, but it ended in a stalemate. After 2003, the US-British attempt to turn post-Saddam Iraq into an anti-Iranian bastion spectacularly foundered. Similarly, after 2011, the west and states such as Saudi Arabia, Qatar and Turkey tried in vain to get rid of Bashar al-Assad and his regime in Syria – the one Arab state firmly in the Iranian camp.

Now the same process is under way yet again, and likely to fail for the same reasons as before: the US, along with its local allies, will be fighting not only Iran but whole Shia communities in different countries, mostly in the northern tier of the Middle East between Afghanistan and the Mediterranean.

Donald Trump looks to sanctions to squeeze Iran while national security adviser John Bolton and secretary of state Mike Pompeo promote war as a desirable option. But all three denounce Hezbollah in Lebanon or the Popular Mobilisation Units in Iraq as Iranian proxies, though they are primarily the military and political arm of the indigenous Shia, which are a plurality in Lebanon, a majority in Iraq and a controlling minority in Syria. The Iranians may be able to strongly influence these groups, but they are not Iranian puppets which would wither and disappear once Iranian backing is removed.

Allegiance to nation states in the Middle East is generally weaker than loyalty to communities defined by religion, such the Alawites, the two-million-strong ruling Shia sect in Syria to which Bashar al-Assad and his closest lieutenants belong. People will fight and die to defend their religious identity but not necessarily for the nationality printed on their passports.

When the militarised Islamist cult Isis defeated the Iraqi national army by capturing Mosul in 2014, it was a fatwa from the Shia Grand Ayatollah Ali al-Sistani that sent tens of thousands of volunteers rushing to defend Baghdad. Earlier in the fighting in Homs and Damascus in Syria, it was the non-Sunni districts that were the strongpoints of the regime. For example, the opposition were eager to take the strategically important airport road in the capital, but were held back by a district defended by Druze and Christian militiamen.

This is not what Trump’s allies in Saudi Arabia, UAE and Israel want Washington to believe; for them, the Shia are all Iranian stooges. For the Saudis, every rocket fired by the Houthis in Yemen into Saudi Arabia – though minimal in destructive power compared to the four-year Saudi bombing campaign in Yemen –can only have happened because of a direct instruction from Tehran.

On Thursday, for instance, Prince Khalid Bin Salman, the vice minister for defence and the brother of Saudi Arabia’s de facto ruler Crown Prince Mohammed Bin Salman, claimed on Twitter that drone attacks on Saudi oil pumping stations, were “ordered” by Iran. He said that “the terrorist acts, ordered by the regime in Tehran, and carried out by the Houthis, are tightening the noose around the ongoing political efforts”. He added: “These militias are merely a tool that Iran’s regime uses to implement its expansionist agenda in the region.”

There is nothing new in this paranoid reaction by Sunni rulers to actions by distinct Shia communities (in this case the Houthis) attributing everything without exception to the guiding hand of Iran. I was in Bahrain in 2011 where the minority Sunni monarchy had just brutally crushed protests by the Shia majority with Saudi military support. Among those tortured were Shia doctors in a hospital who had treated injured demonstrators. Part of the evidence against them was a piece of technologically advanced medical equipment – I cannot remember if it was used for monitoring the heart or the brain or some other condition – which the doctors were accused of using to receive instructions from Iran about how to promote a revolution.

This type of absurd conspiracy theory used not to get much of hearing in Washington, but Trump and his acolytes are on record on as saying that nearly all acts of “terrorism” can be traced to Iran. This conviction risks sparking a war between the US and Iran because there are plenty of angry Shia in the Middle East who might well attack some US facility on their own accord.

It might also lead to somebody in one of those states eager for a US-Iran armed conflict – Saudi Arabia, UAE and Israel come to mind – that staging a provocative incident that could be blamed on Iran might be in their interests.

But what would such a war achieve? The military invasion of Iran is not militarily or politically feasible so there would be no decisive victory. An air campaign and a close naval blockade of Iran might be possible, but there are plenty of pressure points through which Iran could retaliate, from mines in the Strait of Hormuz to rockets fired at the Saudi oil facilities on the western side of Gulf.

A little-noticed feature of the US denunciations of Iranian interference using local proxies in Iraq, Syria and Lebanon is not just that they are exaggerated but, even if they were true, they come far too late. Iran is already on the winning side in all three countries.

If war does come it will be hard fought. Shia communities throughout the region will feel under threat. As for the US, the first day is usually the best for whoever starts a war in the Middle East and after that their plans unravel as they become entangled in a spider’s web of dangers they failed to foresee.

via ZeroHedge News http://bit.ly/2QpnGNZ Tyler Durden

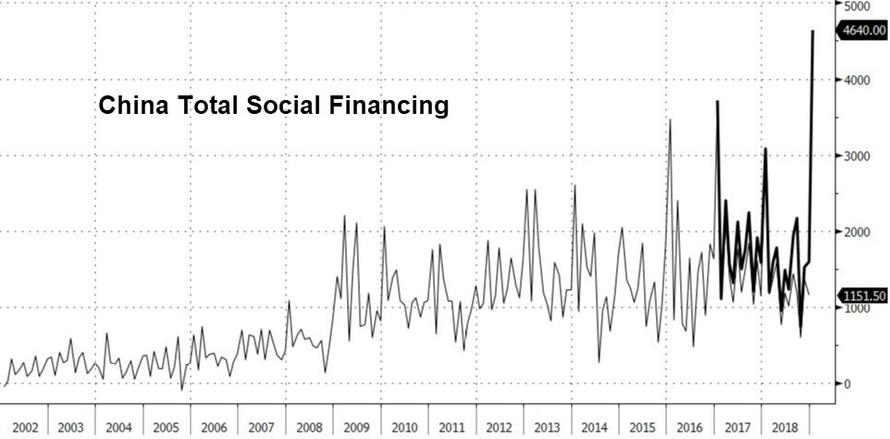

For several months at the start of 2019, analysts, pundits and the media argued that the year was shaping up as a mirror image of 2016, and specifically a repeat of the Shanghai Accord in January 2016 which resulted in a global credit explosion emanating from China and meant to arrest the global bear market. To be sure, in January of 2019 we saw a similar “gargantuan” credit tsunami out of China after the injection of an unprecedented 4.64 trillion yuan in January.

However, several months later, it appears that China’s determination to reflate at all costs fizzled, Europe failed to piggy back on China’s spike in the credit impulse, and suddenly comparisons to 2016 were quietly scrubbed. This is how Horseman Global’s Russell Clark explained the shift in sentiment:

Markets turned around in 2016 when it became obvious that the Chinese policy of cutting capacity and pushing up commodity prices was the real deal. This was Chinese policy to create inflation internally to the benefit of corporates and the financial sector. However, it seems these polices have been reversed, and share prices of Chinese steel companies and banks are beginning to reflect these problems again. If the US dollar stays strong, and China cannot create inflation internally, then they are going to be forced to devalue. Many of the long positions of the fund began to reflect this at the end of April, including mining stocks and currencies.

As a result, Clark writes that “the likelihood of sustained inflation is beginning to disappear” and “deflation again looks more likely, just as it did from 2011 to 2016.”

So if 2016 is not the appropriate comp for 2019, what is? Well, in a far more unpleasant – for the bulls – shift in the narrative, the year that is now discussed as the most likely comparison to what is taking place now, is 2018.

But is that also going to end up being a false comp?

To help answer this question, JPMorgan’s Nikolaos Panagirtzoglou has dedicated his last two “Flows and Liquidity” weekly reports to dissecting first the three biggest similarities and then the three biggest differences between 2019 and 2018.

Starting with the similarities, he observes that the current market environment to be in a similar state of flux to that seen during the last three quarters of 2018, caused by

elevated trade war risks,

dollar strengthening, and

a deteriorating inversion at the front end of the US curve that was signaling a Fed policy mistake.

Meanwhile, in the optimistic, or “differences” column, Panagirtzoglou writes that we find that “there are three main differences between the current environment and last year:

bond yields are falling this year rather than rising,

the US repatriation flow is much reduced and

there is less growth divergence between US and non-US economies.

Drilling down first on the similarities, the JPM strategist writes that while “global merchandise trade volumes posted a rare decline in the fourth quarter of last year”, the recent re-escalation of trade wars “risks another leg down in global trade volumes later this year, which if it materializes, would represent the most severe cumulative retrenchment in global trade since the Lehman crisis.” To be sure, we showcased this ominous development two weeks ago, in “Global Trade Collapsing To Depression Levels” where we showed the following striking chart:

Separately, forward looking indicators of global merchandise trade, such as the new export orders component of the global manufacturing PMI, looked vulnerable even before the re-escalation of the past two weeks. This is shown in the next chart, “which shows that the New Export Orders index of the Global Manufacturing PMI has been persistently weak, hovering below the 50 level since last September with little signs of a pickup in the most recent release for the month of April. The next monthly reading for May due on June 3rd will reveal the impact that the recent escalation of trade war risks had on this forward looking indicator of global trade.”

Additionally, uncertainty also hurts trade also via businesses postponing investment. While it is difficult to quantify uncertainty or its impact on trade, the proxy for uncertainty JPM has used before is the one constructed by Baker, Bloom and Davis (www.policyuncertainty.com). To a large extent, their proxy quantifies newspaper coverage of policy-related economic uncertainty as well as disagreement among economic forecasters. This uncertainty proxy shown below has been rising steeply over the past year and is still flashing red, raising the risk of persistent capex weakness.

The second comparable factor, i.e. dollar strength, started intensifying since April, and according to JPMorgan is driven by the Fed’s Quantitative Tightening (QT). Up until the end of March, the Fed’s QT or balance sheet shrinkage was masked as it was offset by the decline of the US Treasury’s account balance at the Federal Reserve. As Panagirtzoglou notes, as the Treasury account balance normalized in April, the Fed’s balance sheet shrinkage manifested abruptly via a sharp $170bn decline in dollar reserves within three weeks. This caused abrupt tightening in the reserve and dollar liquidity space, pushing the Fed funds rate to well above the Fed’s effective policy rate, i.e. the Interest on Excess Reserves (IOER) rate. While a previous spike in both the median and 75th volume-weighted percentiles of the Fed funds rate to 3bp above the IOER rate around first quarter-end was quickly unwound, these rates spiked again over the past four weeks to 3bp-6bp above the IOER rate creating a more persistent and concerning upmove (Figure 5). In turn, this persistent upmove is raising questions about whether dollar reserves are in tight territory already.

JPM also notes that during May, the dollar got an additional boost from the eruption of trade war risks and the announcement of additional tariffs, similar to what happened in April/May 2018. And similar to last year, this positive dollar impulse is already hurting EM, with EM assets trading particularly weak vs. their DM counterparts over the past month.

The third, and final, similarity is the worsening of Fed rate cut expectations and the inversion at the front of the US curve. Last year, JPMorgan first – correctly – argued that the inversion at the front end of the US yield curve, since it first emerged in April 2018 between the 2- and 3-year forward points of the 1m OIS rate, was “a bad omen for equity and risky markets more broadly last year.” This indicator had been worsening since April 2018 not only by turning progressively more negative, but also by shifting forward between the 1- and 2-year forward points since mid-November. And this worsening continued up until the end of last year. With the Fed pivoting at the beginning of January, Fed rate cut expectations at the front end of the US curve got stabilized during the first quarter of this year at around zero (no rate cut) for 2019 and around 25bp by the end of 2020.

However, in the aftermath of the March 20th FOMC meeting, these Fed rate cut expectations saw a steep deterioration declining further into negative territory. As in April, JPM once agian argued at the time that this bad omen was resurfacing creating downside risk for risky markets. It certainly did, and the S&P tumbled into a very brief bear market before posting a near record rebound in the first 4 months of 2019.

* * *

Enough for the similarities; how about the differences? To address this, the JPM strategist writes that in his client conversations, has has been discussing three key differences in particular.

The first, and arguably most important one, is that bond yields are falling this year rather than rising. During the first three quarters of last year, before the risky market correction erupted in Q4 2018, the yield on the Global Agg Bond index had risen by 52bp. However, it was instead down by 22bp in the first four months of this year before risky markets started correcting in May. The difference is even more striking if one focuses on US bond yields. The yield on the US Agg Bond index was up by 76bp during the first three quarters of last year and was down 30bp in the first four months of this year.

What may explain this difference in bond market performance this year vs. last year? According to JPM, both retail and institutional flows played a role. Retail investors stopped buying bond funds after the February 2018 equity market correction helping to push yields up during Q2 and Q3 of last year. But retail investors started becoming strong buyers of bond funds from the beginning of 2019, most likely in response to strong equity market gains that mechanically increased their equity weights and in turn made them underweight in bonds. And this retail flow helped to push bond yields significantly lower this year. At the same time momentum traders such as CTAs have been likely exacerbating this bond momentum as shown by the decline of bond futures momentum signals during the summer of 2018 and their steady reversal since Q4 of last year.

In addition, the strong bond fund flows this year are boosting credit and US HY in particular. The biggest US HY ETFs saw a collapse in the borrow fee this year in contrast to a persistently high borrow fee during most of last year. This is another important difference to last year, which as JPM warns, “makes US HY credit look more vulnerable currently relative to last year.”

What does this difference in bond market performance this year vs. last year mean? One suggested proposal is that this year’s strong bond market performance is currently creating easier financial conditions relative to last year, especially in the US where 30-year mortgage rates (at 4% currently) are down by 50bp YTD compared to a 100bp increase between January and October last year. So it is less likely, the argument goes, this time to see a repeat of the Q4 2018 correction given that current financial conditions are so much easier than the tight financial conditions and high bond yields prevailing in September 2018 ahead of the Q4 correction.

JPM does not buy this argument, and points out that a casual inspection of the Chicago Fed’s Adjusted National Financial Conditions Index (shown below), which adjusts for the state of the business cycle and the level of inflation to isolate a financial-only element of conditions, shows that US financial conditions were even easier in September 2018 , ahead of the Q4 correction, than they are at the moment. In other words, the picture of Figure 5 is not consistent with the idea that higher bond yields had caused tight financial conditions by September 2018, potentially inducing the Q4 correction.

The conclusion: while the JPM strategist accepts that falling bond yields is one important difference to last year “we do not believe that this difference is enough of a reason to change the balance of risks for risky markets from negative to positive.

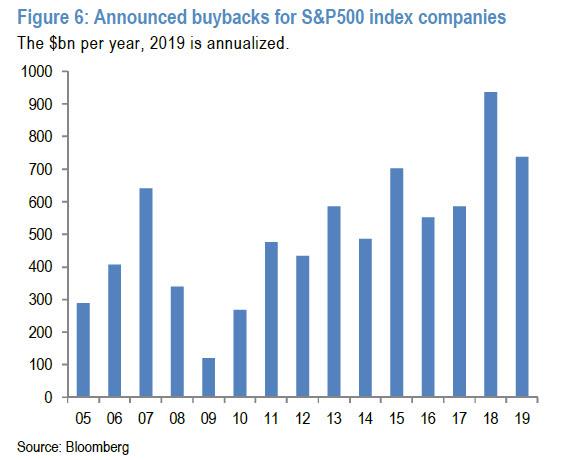

A second key difference to last year is the US repatriation flow. The US repatriation flow was an important factor last year boosting both US equity and bond markets, the former via more US share buybacks and the latter via reduced net issuance of US HG corporate bonds. As a reminder, JPM had previously estimated that of the $430bn that was repatriated last year according to US Flow of Funds, around 2/3rds or $276bn was used for increased US share buybacks, with the rest split between corporate bond withdrawal and capex. Assuming the US repatriation flow is largely behind us, this creates downside risk to US share buybacks and capex growth this year relative to last year and upside risk to US corporate bond issuance. Indeed, announced US share buybacks in the first five months of the year are tracking a pace that is more than 20% below the pace for the same period of last year

And US HG corporate bond net issuance is flat YTD relative to the same period of last year at $115bn. I.e. the strong annual decline in net issuance seen last year does not appear to be repeated this year, again pointing to much reduced US repatriation flow.

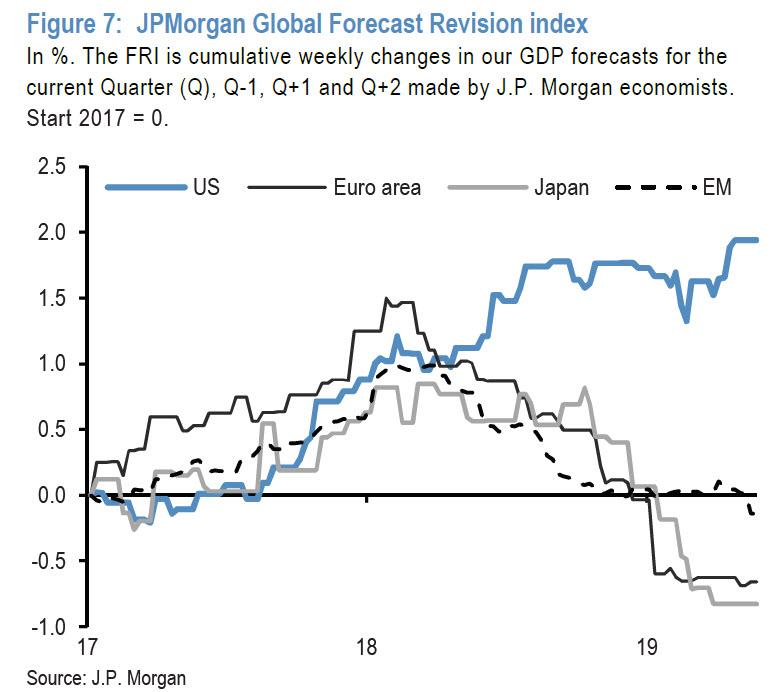

A third, and final, difference is the divergence between US and non-US growth. Boosted by the fiscal stimulus, the US economy had entered a sugar-high phase last year decoupling from the weakness seen in Europe, Japan and EM, which were suffering from their structurally higher sensitivity to the downturn of the global manufacturing cycle. This is shown in the chart below of JPM’s Forecast Revision Indices (FRI) for the US, Euro area, Japan and EM. The US FRI was rising last year while the other three regions FRIs were falling. In contrast, this year, all four FRIs are exhibiting a similar flat pattern.

Last year this growth divergence had been reflected in the performance of US vs. non-US equities as seen in the next chart. But this year a similar relative performance gap has been opening between US and non-US equities despite less divergence in the FRIs across regions. In other words, while JPM acknowledges that less growth divergence between US and non-US economies is an important difference to last year, this has not reflected in the relative performance of US vs non-US equities. As a result US equities outperformed strongly in dollar terms this year similar to the first three quarters of last year. In JPMorgan’s – or at least the opinion Nikolaos Panigirtzoglou, if not that of Marko Kolanovic – “this makes US equities more vulnerable than their non-US counterparts to an equity correction from here, similar to September 2018.”

Putting all this together, JPMorgan finds that in addition to three key similarities, there are also three key differences of the current environment to last year: bond yields are falling this year rather than rising, the US repatriation flow is much reduced and there is less growth divergence between US and non-US economies.

But, as the bank’s “bad cop” strategist summarizes, “these differences do little in altering the state of flux and the downside risk for risky markets emanating from similarities to last year such as elevated trade war risks, dollar strengthening, a deterioration in the inversion at the front end of the US curve and the strong outperformance of US equities relative to their non-US counterparts.”

In short, JPMorgan has once again covered all the bases, with the bank’s official or “house” call still for the S&P rising to 3,000, a call that has been pounded during almost every major market uptick by the bank’s head quant Marko Kolanovic. And yet, at the same time JPMorgan’s far more skeptical, if not permabearish analyst Nikolaos Panigirtzoglou is there to take the under, and with each passing week sees the most likely outcome as one of further market weakness. While this is bad news for anyone hoping for consistency in JPM’s calls, at least it will make for an entertaining cage match between the Greek and Croatian quants.

And if Morgan Stanley is right in warning that the longer we go without a trade war resolution, the more likely that the market outcome is a crash, then we eagerly look forward to whether JPM’s Croatian “Gandalf” will blame his co-worker for manipulating market sentiment and unleashing “FUD”, which once again results in the market failing to reach his overly optimistic S&P target.

via ZeroHedge News http://bit.ly/2JEzefX Tyler Durden

A series of tiny quakes rattling California and the Pacific Northwest may signal an upcoming catastrophic earthquake, seismologists say, KOIN reported. Or experts say they might just be another reminder that the pressure’s always building on fault lines beneath the West Coast, KATU reported.

“Those are just reminders,” said Scott Burns, a Portland State University geology professor, according to the station. “We don’t know what they mean. They are reminders that we are in earthquake country, and they may be precursors to the ‘big one.’”

But, as SHTFplan.com’s Mac Slavo details, for the first time since 2011, three distinct zones in the Pacific Northwest have been “going off” all at once. According to King 5 News, scientists say that the theory is that the sub-ducting ocean plate is being stretched like taffy in the heat that is the mantle of the earth.

“Any signal you get is interesting,” said Tim Melbourne, a who runs the Northwest Geodetic Array, which is based at Central Washington University in Ellensburg.

“If you have something out in the dark, and you know it’s dangerous, you know it’s menacing, and every now and then you get a flash of light from it. Any flash of light doesn’t tell you a lot, but you piece them all together and you can start to put together all the angles, and you can start to see the dragon, and it’s a big dragon,” Melbourne said.

Melbourne’s metaphorical “dragon” is the Cascadia Subduction zone. Sections of the ocean floor are being pushed under the western edge of the North American continent creating pressure. Where the two plates join is a huge fault line, and the cooler upper portions of that fault are locked together. When they give way, typically between about 300 and 500 years, the result is a massive tsunami-triggering earthquake. The one scientists expect to occur off of our coast is expected to be a magnitude nine. And some government agencies have already been preparing for the inevitable event.

Episodes of tremors and plate slippage have been affecting the Pacific Northwest about every 14 months since at least the 1990s. Shaking from these events typically aren’t felt and don’t mean an earthquake is imminent. However, researchers believe the slip events are building up the pressure at the fault, which will eventually lead to a long-predicted magnitude 9 earthquake.

Though it appears several slip events are occurring, the latest data doesn’t seem to indicate the “main” event or “the big one” has started north of Seattle. But it’s still a good idea to be prepared.

via ZeroHedge News http://bit.ly/2XacJCK Tyler Durden

When I look around at the state of public discourse in ‘the West’ what strikes me is that everyone says they want to have a reasoned and rational debate but say that the reason it doesn’t happen is because the ‘other side’ is irrational and so they can’t be debated with. The ‘other side’, their opponents say, always avoids the debate, is never willing to just answer a reasonable question and generally just refuse to have the debate they claim to want. Does this resonate with you?

I see impasse everywhere I look. In the UK between Brexit and Remain supporters and in the USA between Trump and Non-Trump supporters. I see it between Alt-right advocates and Progressives, and between all the various groups within and around identity politics and those they see as their enemies. I see it in every discussion of immigration. I see it between globalists and those they call populists or nativists.

How is this possible? How can all sides in every debate want to have a reasoned and rational discussion and yet all claim the ‘other side’ is irrational and unwilling to discuss?

Here are some thoughts.

It seems to me that in every one of our contentious social and political debates each ‘side’ comes to the debate with a set of assumptions which they are absolutely sure are the correct and in fact only way of framing the debate. The problem with me suggesting this, is that the people I am talking about will read that sentence and nod happily, feeling quite certain that this is a correct and lamentably true description of people other than themselves. Their own assumptions, if they are aware of having them at all, seem to them to be so basic, so self evident, that it would be wrong to describe them as ‘assumptions’. Sure, other people may have deeply embedded assumptions, but what ‘we’ have is a clear-eyed and unbiased statement of reality.

Sometimes the assumptions which provide the framework for every other thought, statement and debate, are held, I think, almost unconsciously. If you grow up in a fundamentalist religious culture then Allah, or Jehovah or Christ and his rules are unquestioned and held as unquestionable.

Such assumptions are then nearly always buttressed by an accompanying belief that questioning or denying these most unquestionable assumptions and the version of reality they describe, will lead to utter disaster. In the religious case because god will get peeved and visit some sort of divine anger upon the heads of the unbelievers and possibly even those around them who did nothing to stop the blaspheming.

So far so smug.

But the same logic is there in lots of more secular or ‘rational’ people. For some Capitalism and the workings of the Free Market are so basic, so much just a reflection into human affairs, of the basic nature of reality, that to go against them is ‘irrational’. On the other side there are those for whom a more communist view of human relations seems equally undeniable. Both sides usually claim their view is the only conclusion you can rationally come to if you start from an unbiased and scientific view of human nature. Both exaggerate.

An important part of the fierceness with which people defend their assumptions is often, I think, that they work through what their assumptions lead to and like what they see. But when they look at what ‘the other side’ espouses and put those things into their own framework of assumptions they find it leads to all sorts of things they find deplorable. The key thing is they always use their own framework of assumptions to evaluate what the other side’s beliefs ‘must lead to’. Never the assumptions the other side uses. Each side says to the other – you believe this and that means you must also believe… or that you must be a… . Very often the word fascist comes in to the shouting match at this point.

My view is that everyone comes to the debate wearing mental glasses which show them what they take to be ‘reality’ but which is in fact, a construction, created by the glasses they may be unaware they are even wearing.

So what?

My view is that this means everyone comes to the debate with a framework which includes what they are absolutely sure the ‘other side’ must think. Why? Well, if you have a framework of assumptions which tells you what the correct answer is then that same framework of assumptions will also tell you what the wrong answers are. It will tell you what the ‘other’ side, the wrong side of the debate thinks. You will ‘know’ before they open their mouths what they are going to say – more or less – because you are a rational thinking person who has ‘thought it through’. The problem is, the ‘it’ you thought through, which you attribute to the ‘other side’, is what your set of assumptions say the other side must think.

You hear what the other side’s opinion is, find that opinion within the framework of your own thinking and then look at the train of thoughts that – if they were using your assumptions, they must have gone through to get to their conclusion. And you also look around at the other thoughts that – in your logic – would go along with or be a consequence of their expressed view. And you then accuse the other side of those further ideas. Along the lines of – ‘Well if you say that then you must be in favour of…. You must be a ….!’

How many times in a contentious debate do both sides get really angry because they say – with some justification – that the other side is putting words in their mouth and are making assumptions about what they think or believe? Both sides claim the other is doing this and both get angry at the way the other side ‘distorts’ things and doesn’t listen. And both sides then reply, “No we’re not. We’re just showing anyone listening what you ‘really think’ but don’t like to say out loud.”

What I see, is both sides wanting to control how the debate is to be framed. And both sides feel this is legit because they ‘know’ their view is the rational and clear one. The other side is blinded by assumptions.

All sides say they want a rational and reasoned debate but both sides come to the debate assuming that their way of framing the debate, their set of assumptions, are the correct, rational and in fact the only legitimate ones. Each side comes with its assumptions and expects, demands, the other side to fit into them …not because they are bullies or irrrational – heaven forfend – but because their’s is the right framework. And to disagree is, by definition, to be irrational.

The only problem is the other side doesn’t see the world the same way. The two sides aren’t starting with an agreed set of assumptions. So each side sees the other as irrational and obstructive. Each side begins by asking a question or making a statement which seems to them to be the correct, legitimate and clear-eyed way of proceeding only to find the other side refusing to go along with the programme. Refusing to answer the questions or trying to avoid it by asking a totally different question. Each side sees the other being obstructive. And each side says of the other side, “Either they’re stupid or they’re doing this because they know they are wrong and would lose!”

And in truth both are correct. For good reason. If you do accept the starting assumptions of the other side in this sort of polarised debate, then by definition you will lose. The logic the other side come with, already contains your beliefs, but in their mental framework ‘your’ beliefs are connected to all sorts of awful ideas. They can’t understand how you can’t see this. It’s so clear. Of course it is only clear because they are looking at it only from within the framework of their own assumptions.

Each side knows how easy it is to follow the logic which runs from their own assumptions to the ‘correct’ conclusion. And each side wonders how the other refuses to see this. It’s a short step from there to decide that perhaps the other side aren’t that stupid which means they must be malignly, knowingly, deplorably advocating a position they know is wrong.

The other side must be other irrational or evil. Or sometimes both. Et voila! Mutual hatred, intollerance and a strong sense of self-righteous superiority on all sides.

Everyone sincerely believes their assumptions are the correct starting point for any debate and insist the other side fit into the role which the starting assumptions have laid down for them. Which conveniently mean they – the other side – will soon see the error of their ways, lose the debate and come to see how stupid or misguided they have been. Not surprisingly people quickly sense this is what is in store for them if they continue to allow the debate to be framed by the other side’s assumptions. And so at some point, usually fairly early on, people start to not allow the other side to dictate the framework of the debate. At which point both sides then feel frustrated that the other side is ‘irrationally’ sabotaging the debate by avoiding perfectly good questions and insisting of other irrelevant, unconnected, distracting questions.

Sorry this is a lot of words to say what might be blazingly evident.

But I think we are going to have to begin to admit we have deeply held assumptions and step back from them far enough to talk about them. I believe the debate we need at this point has to be about our assumptions and the debate has to happen at this deeper level. We are going to have to be willing to listen to why other people have different assumptions. And not rule them as somehow illegitimate or unspeakable or deplorable. We need to do this so we can follow the logic of the other side to understand how they get to where they are, why they think that they think. Why they have the fears they do. We need to do this for their assumptions and for our own. And we need to allow them to do the same.

It is the opposite of de-platforming. It’s the other path from using emotive labels to shut people down.

I think there are people who really do not want others to debate and discuss. They don’t want people to come to a better understanding of each other. They want, instead, to keep very tight control over what can and can’t be said and can and can’t be debated. They want people to be angry at each other and to distrust each other. They want to divide people against each other while claiming to be ardent opponents of divisiveness. It’s a clever ploy. But a dangerous and I think an evil one.

Such people don’t want to ever be accused of shutting down debate. They want to be seen as the champions of debate – rational debate, but all the while managing to prevent it. And the way they do it is by insisting they do not have assumptions. Only the ‘other’ side does. The ‘good’ side has science or evidence or just the moral high ground as their platform. This is a profound danger. Everyone has assumptions. The essential thing is to admit it, and be willing to discuss them.

There are plenty of people who hold views I find deeply distasteful. But rather than refuse to debate or try to insist that any debate happen within assumptions I have laid down, I prefer to try to get at what logic has led them to their views. What assumptions do they start with and why? What are the fears or the hopes which their assumptions seem to them to provide good answers to?

via ZeroHedge News http://bit.ly/2JF7nML Tyler Durden

Authored by Michael Zezas, Chief Public Policy strategist at Morgan Stanley

Investors are obsessed, trying to figure out what happens next in the US/China trade dispute. Will the US call China? What do the negotiators really think? Does this last three weeks or three months? Our answer: you could be starting with the wrong questions.

First, let’s look back. It all seemed to be going so well. After market sell-offs sent signals to the US and China about the costs of trade tensions, they sat down at the G20 in November, called a truce, and appeared close enough to a deal to start planning for a signing ceremony. Then came the week of May 5. The US claimed China had moved the goalposts on key issues and announced another tariff increase, with preparations to levy tariffs on another ~US$300 billion of imports. China responded with counter-tariffs and heated rhetoric. Escalation was back, but the market response was relatively muted. After a 3-4% down move in the S&P from all-time highs and about a 7% down move in the Shanghai Composite, both indices remain well above pre-G20 levels. This suggests the recognition of heightened uncertainty, but no clear idea of what comes next.

It appears that investors are trying to gauge trade risks by focusing on near-term catalysts. We’re often asked what key players are saying, what might happen at the next G20, where that meeting fits in the timelines for tariff events, and what unconventional action each side might take. But these questions can be counterproductive. Answers require us to intuit the intentions of key players around specific details, while we can only parse their broad intentions from public statements and reporting. Furthermore, this approach risks overemphasizing isolated bits of evidence.

Rather than guess at the next headline or meeting, define the dynamic at play.

Game theory takes us back to what shaped our call in 2018. Both sides will continue to escalate until clear market or economic weakness pushes them to reengage. Hence, investors should act as if the next escalation will happen until markets price it in. The situation resembles a repeated Prisoner’s Dilemma game. Both sides start by escalating, perceiving better payoffs for doing so. They can cooperate later on if they realize that the rewards for payoffs from cooperation are greater than from further escalation. Consider:

This isn’t posturing, meaningful disagreements exist: Early speculation the week of May 5 was that the game hadn’t changed, rather both sides were framing their compromises for domestic audiences. But the US soon highlighted new areas of disagreements, confirmed by the Chinese side, around IP protections and how quickly to remove existing tariffs.

These conflicts reset the payoffs, suggesting that escalation is preferable at this point to meeting the other’s demands: For one side, and possibly both, the payoff for cooperation had diminished as it became clear that their counterpart wasn’t agreeing to key conditions.

Market and/or economic weakness could change the game: In 4Q18, we believe that the US administration’s market sensitivity and China’s short-term economic exposure played a key role in bringing them to the table amid weakness in global markets and softer data in China. The payoffs for cooperation became clearer and preferable to escalation. A repeat of these pressures could mend this new rift.

We expect this dynamic to pressure risk assets and US bond yields lower. If risk markets don’t drive cooperation soon, escalation will likely cause enough economic erosion to move the markets before long. Consider the impacts of further escalation laid out by our economists in their midyear outlook. A three-to-four month extension of current tariffs could dampen growth in China and the US by 20bp and 30bp, respectively, barely avoiding recession. A longer period of tension, including fresh tariffs on ~US$300 billion of remaining China exports to the US, puts 100bp of global growth at risk and pushes the Fed into repeated cuts. Neither of these outcomes is in the price, in our view, and recent conversations with investors suggest that they under-appreciate the downside impact of such scenarios.

Where could we be wrong? Perhaps the US and China will follow the path lauded by game theorists and marriage counselors alike – communication! Given domestic politics and negotiating stances, we think that it will take weak markets or fundamentals to pry open a channel. Still, any news of fresh, substantive dialogue between the countries should be seen as a positive.

via ZeroHedge News http://bit.ly/2K5VX3U Tyler Durden