The much anticipated G-20 summit, which culminated in the latest trade truce between the US and China, has come and gone, and while the outcome was as largely expected, it will still push US equities to new all time highs just shy of 3,000.

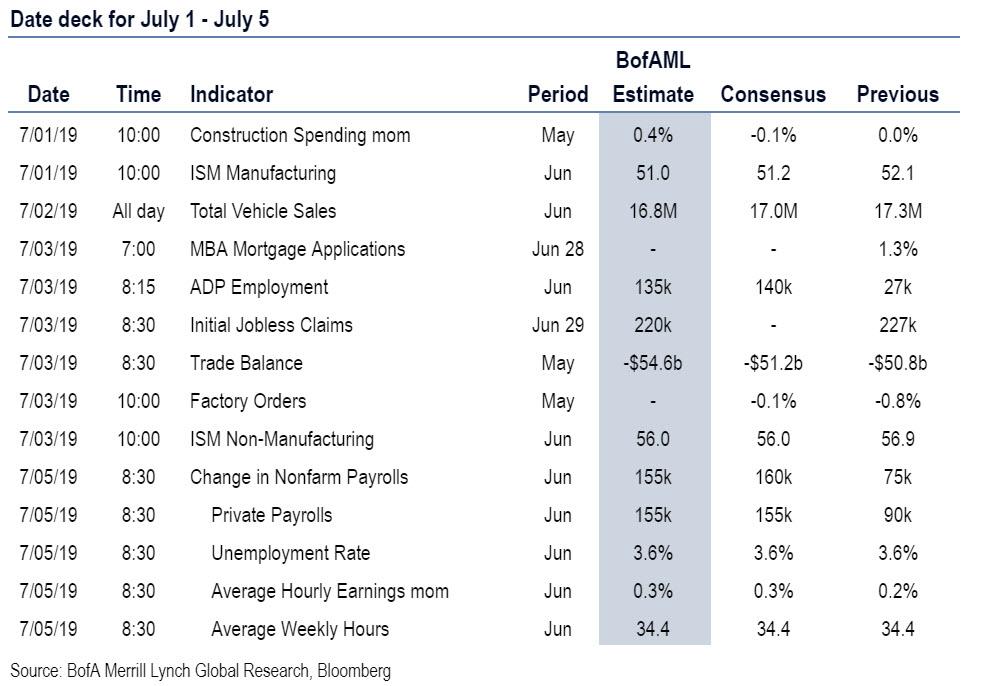

And with the US set for a holiday shortened week, the outcome of the Xi-20 meeting will dictate the tone in markets for the next 56 hours, until the July 4 holiday wreaks havoc with positioning, while the US employment report looms at the end of the week. We will also get PMIs – which are pointing at a global economic contraction – and US ISM data, which may print below 50, to digest along with an OPEC meeting and a scattering of central bank speak throughout.

With the G-20 in the rearview mirror, traders can once again focus on the economic fundamentals, which are not pretty. Across Asia and Europe, factory activity shrank in June, according to reports Monday. China’s manufacturers saw sales, exports and production fall, with unemployment sliding to a decade-low, while Germany suffered from weaker foreign demand. Exports from South Korea plunged almost 14%, and Japan’s Tankan confidence index dropped to a three-year low.

After the G-20, focus will turn to the June employment report in the US on Friday, and as Deutsche Bank’s Craig Nicol writes, the big rates repricing and subsequent dovish turn by the Fed last week has increased anticipation around this report. In terms of expectations, right now the consensus is for a 158k payrolls reading. A reminder that this follows that much weaker than expected 78k reading in May. The unemployment rate is expected to hold at 3.6% while earnings are expected to have risen +0.3% mom which would nudge the annual rate up one-tenth to +3.2% yoy.

That’s not the only significant data that we get next week in the US with the June ISM manufacturing reading due on Tuesday and non-manufacturing on Wednesday. The consensus is for a 51.2 manufacturing reading which would represent a drop of 0.9pts from May. Our US economists have warned about the ISM potentially declining towards 50, with sharp drops in recent regional Fed manufacturing surveys furthering this argument. So it’s a print worth watching.

Meanwhile, we’ll also get the final June manufacturing PMIs on Tuesday and services and composite PMIs on Wednesday across the globe.

Other data worth flagging in the US this week includes May vehicles sales on Tuesday, June ADP, jobless claims and final durable and capital goods for May on Wednesday. In the UK we get money and credit aggregates data for May on Monday and May factory orders data in Germany on Friday.

Elsewhere, the oil market is facing a mini test with OPEC meeting on Monday and OPEC+ (which includes Russia) on Tuesday in Vienna. A press conference is expected on Tuesday with nations expected to set oil production policy for the rest of the year. Reports last week – including in the WSJ – suggested that Saudi Arabia was expected to push to renew cutting output amid slowing global demand.

As for Fedspeak, Clarida is due to speak early on Monday at an event in Helsinki on the topic of monetary policy and the future of EMU. Williams is due to speak on Tuesday morning in Zurich on the global economic and monetary policy outlook while Mester will also speak on Tuesday during the afternoon in London on the economic outlook. Meanwhile, over at the ECB, Mersch is due to speak tomorrow, Guindos is due to speak on Monday, Thursday and Friday, Knot on Tuesday, Villeroy on Wednesday and Lane on Thursday. The BoE’s Cunliffe and Broadbent are also due to speak at separate events on Wednesday and PBoC’s Yi on Monday morning.

Other events worth flagging include the EU leaders meeting in Brussels on Sunday to discuss the next heads of the European Commission, ECB and European Council. Turkey’s Erdogan visiting Beijing on Tuesday. The European Commission potentially deciding to open a disciplinary procedure against Italy on Tuesday. Finally, we should highlight that US markets will be closed on Thursday for the Independence Day holiday. This will also likely include a half-day session on Wednesday for bond and equity markets.

Here is a summary of key events in the next few days, courtesy of Deutsche Bank:

Monday: The final June manufacturing PMIs for Japan, Europe and the US will be the focus of the data releases along with the June ISM manufacturing reading in the US. The June Caixin PMI will also be released in China while the Q2 Tankan Survey is due in Japan. In Europe we’ll also get the June unemployment rate in Germany, M3 money supply data for the Euro Area for May and money and credit aggregates data for May in the UK. In the US the May construction spending print is also due. Away from that OPEC nations meet in Vienna to set oil production policy for the rest of the year. The Fed’s Clarida, ECB’s Guindos and PBoC’s Yi are due to speak also.

Tuesday: Data includes June house price stats in the UK, May PPI for the Euro Area and June vehicle sales in the US. The Fed’s Williams and Mester are also due to speak along with the ECB’s Knot. Meanwhile, OPEC+ meet in Vienna and Turkey’s Erdogan visits Beijing. Tuesday is also the day that the US may begin imposing tariffs on almost all remaining imports from China (pending what happens at the G-20) and the European Commission may decide to open a disciplinary procedure against Italy.

Wednesday: The remaining June PMIs will be the main data highlight. The remaining Caixin PMIs will also be out in China while other data in the US includes the June ADP employment report, May trade balance, jobless claims, June ISM non-manufacturing and final May durable and capital goods orders. The ECB’s Villeroy and Nowotny are due to speak along with the BoJ’s Funo and BoE’s Broadbent. US markets are also expected to close early.

Thursday: US markets will remain closed for the Independence Day public holiday. As for data, the only release due in Europe is May retail sales for the Euro Area. The ECB’s Lane and Guindos are also due to make comments.

Friday: The June employment report in the US will be the main highlight for data. Prior to that we get May factory orders in Germany, May trade balance in France, June house prices data in the UK and Q1 labour costs in the UK. The ECB’s Guindos is also due to speak.

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the ISM manufacturing report on Monday, the ISM non-manufacturing report on Wednesday, and the employment report on Friday. There are several scheduled speaking engagements from Fed officials this week, including one by Vice Chair Clarida on Monday, and one by New York Fed President Williams on Tuesday.

Monday, July 1

02:15 AM Fed Vice Chair Clarida (FOMC voter) speaks: Fed Vice Chair Richard Clarida will speak at a conference on monetary policy and the future of the EMU at the Bank of Finland.

09:45 AM Markit US manufacturing PMI, June final (consensus 50.1, last 50.1)

10:00 AM ISM manufacturing index, June (GS 50.5, consensus 51.0, last 52.1): All regional manufacturing surveys but Richmond declined by more than expected in June, and caused our manufacturing survey tracker — which is scaled to the ISM index — to fall to its lowest level since mid-2016 (-3.1pt to 50.4). Other idiosyncratic factors roughly offset for this month, and we thus expect the ISM manufacturing index to decline by 1.6pt to 50.5 in June. A simple analysis based on the historical deviations between the ISM and our survey tracker suggests slightly more than a one in three chance of the ISM manufacturing index falling into contractionary territory.

10:00 AM Construction spending, May (GS +0.2%, consensus flat, last flat): We estimate a 0.2% increase in construction spending in May, with scope for an increase in private nonresidential construction, but scope for a decrease in residential construction.

Tuesday, July 2

06:35 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will speak on the global economic and monetary policy outlook at an event in Zurich. Prepared text and audience Q&A are expected.

11:00 AM Cleveland Fed President Mester (FOMC non-voter) speaks: Cleveland Fed President Loretta Mester will speak on the economic outlook to the European Economics and Financial Centre in London. Prepared text and audience Q&A are expected.

5:00 PM Wards Total Vehicle Sales (GS 17.1m, consensus 17.0m, last 17.3m)

Wednesday, July 3

08:15 AM ADP employment report, June (GS +125k, consensus +140k, last +27k): We expect a 125k gain in ADP payroll employment, reflecting a drag from lagged payrolls, lower oil prices, and modestly higher jobless claims. While we believe the ADP employment report holds limited value for forecasting the BLS nonfarm payrolls report, we find that large ADP surprises vs. consensus forecasts are directionally correlated with nonfarm payroll surprises.

08:30 AM Trade balance, May (GS -$54.3bn, consensus -$53.5bn, last -$50.8bn): We estimate the trade deficit increased by $3.5bn in May, reflecting a rise in the goods trade deficit.

08:30 AM Initial jobless claims, week ended June 29 (GS 225k, consensus 220k, last 227k): Continuing jobless claims, week ended June 22 (last 1,688k); We estimate jobless claims edged down by 2k to 225k in the week ended June 29, after increasing by 10k in the prior week. There were several auto plant shutdowns.

09:45 AM Markit US services PMI, June final (consensus 50.7, last 50.7)

10:00 AM Factory Orders, May (GS -0.7%, consensus -0.5%, last -0.8%): Durable goods orders, May final (consensus -1.3%, last -1.3%); Durable goods orders ex-transportation, May final (last +0.3%); Core capital goods orders, May final (last +0.4%); Core capital goods shipments, May final (last +0.7%): We estimate factory orders decreased by 0.7% in May following a 0.8% decline in April. Durable goods orders moved down in the May advance report, driven by a further decline in aircraft orders.

10:00 AM ISM non-manufacturing index, June (GS 55.4, consensus 55.9, last 56.9): Our non-manufacturing survey tracker declined by 0.8pt to 53.9 in June, following mixed regional service sector surveys. We expect the ISM non-manufacturing index to decline by 1.5pt to 55.4 in the June report. The index appears elevated relative to other service sector surveys, suggesting some scope for catch-down.

Thursday, July 4

US Independence Day holiday observed. US equity and bond markets are closed.

Friday, July 5

08:30 AM Nonfarm payroll employment, June (GS +175k, consensus +163k, last +75k); Private payroll employment, June (GS +160k, consensus +155k, last +90k); Average hourly earnings (mom), June (GS +0.4%, consensus +0.3%, last +0.2%); Average hourly earnings (yoy), June (GS +3.2%, consensus +3.2%, last +3.1%); Unemployment rate, June (GS 3.7%, consensus 3.6%, last 3.6%): We estimate nonfarm payrolls increased 175k in June, more than double the 75k pace in May. Our forecast reflects low jobless claims, the continued expansion indicated by our employment survey trackers, and an expected rebound in public education payrolls related to the timing of the survey periods. We believe the May report overstates the magnitude of the slowdown in trend job growth, which we believe remains well above potential. We also note that labor supply constraints are historically less binding in June: in years with relatively tight labor markets, payroll growth tends to slow in May then reaccelerate in June and July (as students and recent graduates are absorbed into the labor force).

Source: Deutsche Bank, BofA, Goldman

via ZeroHedge News https://ift.tt/2ZYALl2 Tyler Durden

If you were to have asked me what news reports I definitely did not expect to see when checking my news feed this morning, “Malignant plutocrats join hands across partisan divide to end America’s forever war” would probably have been among my first guesses. And yet, weirdly, here we are.

A new Boston Globe article titled “In an astonishing turn, George Soros and Charles Koch team up to end US ‘forever war’ policy” reports that the two influential billionaires have chipped in a half a million dollars apiece to start a new DC think tank with the goal of doing the exact opposite of the sort of thing that billionaire-funded DC think tanks normally do.

“Besides being billionaires and spending much of their fortunes to promote pet causes, the leftist financier George Soros and the right-wing Koch brothers have little in common,” the report begins.

“They could be seen as polar opposites. Soros is an old-fashioned New Deal liberal. The Koch brothers are fire-breathing right-wingers who dream of cutting taxes and dismantling government. Now they have found something to agree on: the United States must end its ‘forever war’ and adopt an entirely new foreign policy.”

“In concrete terms, this means the Quincy Institute will likely advocate a withdrawal of American troops from Afghanistan and Syria; a return to the nuclear deal with Iran; less confrontational approaches to Russia and China; an end to regime-change campaigns against Venezuela and Cuba; and sharp reductions in the defense budget,” the article reads.

Finally. A think tank that aims to fight the blob and endless war. Hope @stephenWalt will be involved. @stephenkinzer writes, “In an astonishing turn, Soros and Charles Koch team up to end US ‘forever war’ policy” Congrats to @tparsi https://t.co/pvFE4wFJjz

Responses to this news from Twitter’s blue-ticked commentariat have been largely supportive.

“Great to see that avoiding really stupid, costly wars has support across party lines,” tweeted author and professor Max Abrahms.

“Certainly understand skepticism of Soros and Koch money but with a platform of ending endless war and Trita Parsi at the helm, this sounds very promising and is sorely needed as we inch towards catastrophic nuclear war,” said journalist Dan Cohen.

“A new foreign policy think tank that will ‘promote an approach to the world based on diplomacy and restraint rather than threats, sanctions, and bombing.’ YES PLEASE,” tweetedIn The Now’s Rania Khalek.

“Finally. A think tank that aims to fight the blob and endless war. Hope Stephen Walt will be involved,” tweeted foreign policy analyst Joshua Landis.

Hi Joshua,

I’ve got a bridge on sale. You seem very interested in buying such. Gimme a call.

“Hi Joshua, I’ve got a bridge on sale. You seem very interested in buying such. Gimme a call,” Moon of Alabama tweeted at Landis.

Such skepticism is warranted. It is true that the Quincy Institute’s co-fouder Trita Parsi has been a vocal opponent of US imperialism towards Iran and elsewhere, but it is also true that the Kochs and Soros have both acted as toxic facilitators of US imperialism.

The report claims that the new think tank seeks an end to America’s regime change agenda in Venezuela, for example, yet investigative journalist Greg Palast reports that the Koch brothers have been a major driving force behind that very agenda. The group claims to seek a de-escalation against Syria, yet investigative journalist Vanessa Beeley and alternative media outlet Mintpress News have documented extensive ties between George Soros and the various NGOs and narrative management operations which have been facilitating the agenda of toppling Syria’s government.

In 2014 journalist Mark Ames observed that Soros “funded many of the NGOs involved in ‘color revolutions’ including small donations to the same Ukraine NGOs that Omidyar backed. (Like Omidyar Network does today, Soros’ charity arms — Open Society and Renaissance Foundation — publicly preached transparency and good government in places like Russia during the Yeltsin years, while Soros’ financial arm speculated on Russian debt and participated in scandal-plagued auctions of state assets.)”

George Soros is a major funder of the NATO narrative management firm Atlantic Council, which has been a driving force behind the campaign manufacturing consent for escapations against Russia, something the Quincy Institute claims to oppose.

So if you’re interested in viewing world events through a lens that is untainted by corrupt narrative management, some skepticism of this new Quincy Institute is not just appropriate, but absolutely required.

The term “think tank” almost always refers to a group of academics hired by plutocrats to come up with reasons why it is very good and smart to do something very evil and stupid, and then to market those reasons at key points of influence. They are key tools of narrative management for the billionaire class, and the interests of the billionaire class are rarely in alignment with those of ordinary people. This is especially true when said billionaires are operating in a bipartisan manner.

But the good news is that all we have too do to know the truth about this new group’s purposes is watch its behavior over time, and pay attention to who benefits from the narratives it ends up pushing. Just make a mental note of the information you have about it now, and pay attention to what’s happening when you see the words “Quincy Institute” in reports from the political/media class going forward. If this think tank is what it claims to be, we will see this proven over time in the effects it has on dominant narratives and government policy. If it isn’t, we’ll see that, too.

* * *

The best way to get around the internet censors and make sure you see the stuff I publish is to subscribe to the mailing list for my website, which will get you an email notification for everything I publish. My work is entirely reader-supported, so if you enjoyed this piece please consider sharing it around, liking me on Facebook, following my antics onTwitter, throwing some money into my hat on Patreon orPaypal, purchasing some of my sweet merchandise, buying my new book Rogue Nation: Psychonautical Adventures With Caitlin Johnstone, or my previous book Woke: A Field Guide for Utopia Preppers. For more info on who I am, where I stand, and what I’m trying to do with this platform, click here. Everyone, racist platforms excluded, has my permission to republish or use any part of this work (or anything else I’ve written) in any way they like free of charge.

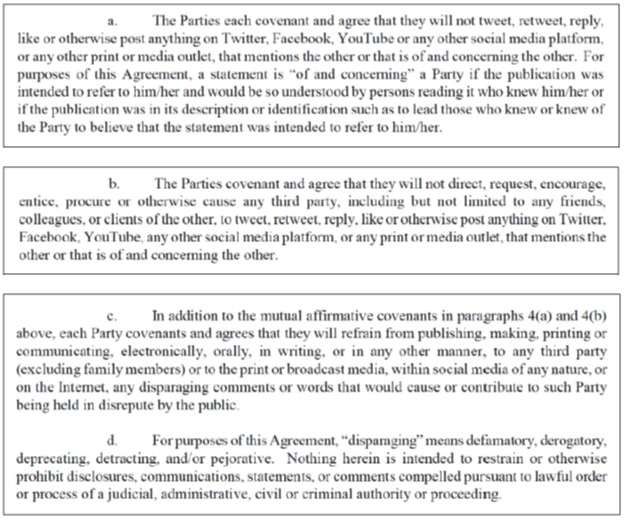

1. Trevor FitzGibbon is a communication strategist who has epresented, among others, Julian Assange. Jesselyn Radack is a whistleblower lawyer and author who has represented, among others, Edward Snowden. Radack and FitzGibbon had been on apparently good terms, and Radack had publicly praised FitzGibbon’s work in August 2015:

FitzGibbon media has “a veritable Who’s Who” of leading organizations and public figures in the progressive world, Radack says: “While big PR firms may have more name cachet, FitzGibbon media makes up for it with genuine concern for client well-being, not just placing a story.”

Then, in early 2016, Radack accused FitzGibbon of raping her in November and December 2015. (FitzGibbon says they had a consensual sexual relationship, and claims that he has messages from after the alleged November incident that reflect the relationship being consensual.) Radack went to the police, but in 2017 prosecutors closed the investigation and decided not to prosecute FitzGibbon.

Radack then continued to criticize FitzGibbon, as well as “liking” and retweeting others’ posts that criticized FitzGibbon with regard to other sexual harassment accusations that had been made against him. FitzGibbon therefore sued her for libel (for more details, see this complaint). During the lawsuit, Radack continued to criticize FitzGibbon further, even though the trial court had ordered her not to use any social media “to publish or republish statements about”:

(a) the character, credibility, or reputation of Plaintiff or Defendant and/or their respective counsel;

(b) the identity of a witness or the expected testimony of Plaintiff, Defendant, or any witness;

(c) the identity or nature of evidence expected to be presented in support of any motion or at trial or the absence of such evidence;

(d) the strengths or weaknesses of the case of either party; and/or

(e) any other information the Defendant knows or reasonably should know is likely to be inadmissible as evidence in this case and that would create a substantial risk of prejudice or confusion if disclosed.

Radack was even held in contempt of court for violating the order, with the judge writing,

Radack acknowledges making the comments which [violated the order] and apologized for them claiming that they were “a desperate, emotionally charged, reflexive attempt to defend herself and respond to attacks that appeared to her to be coming from or orchestrated by the Plaintiff.” … The simple fact is that Radack deliberately violated the July 31, 2018 ORDER (ECF No. 41) by making the communications that she admittedly made. In so doing, she acted in contempt of the ORDER (ECF No. 41).

Neither contrition nor emotional distress nor illness [multiple sclerosis, apparently] nor financial difficulties [a bankruptcy] can excuse deliberate misconduct of this sort by any litigant, much less by a lawyer. And, the record here shows that Radack is a sharp-tongued, mean-spirited, proliferous user of social media. Her conduct here is just more of the same. Neither contrition nor emotional distress nor illness nor financial distress have caused Radack to ameliorate her penchant for nasty social media communication.

The original defamation case had settled, but Radack is apparently continuing to criticize FitzGibbon.

2. Here’s the complication, though: The restraining order in the earlier case would have been unconstitutional, except that Radack had stipulated to it:

Defendant concedes the motion and will not oppose entry of an order consistent with the relief sought in Plaintiff’s Motion for a Restraining Order. As counsel for plaintiff agreed at the hearing on the motion, this concession obviates the need for depositions or a hearing on the motion…. Defendant respectfully suggests that the Court enter an order consistent with that laid out on pages 1-2 of Plaintiff’s Motion for a Restraining Order [which are nearly identical to the order that was actually issued-EV].

She therefore had agreed to the speech restriction, and had it embodied in a court order—and then spoke despite it.

Radack then apparently settled the original case, and Tweeted this about the matter:

Since April 2018, I have been involved in litigation with Trevor Fitzgibbon. We have amicably resolved our differences. As part of the settlement, I retract and withdraw every allegation and statement I have ever made against Trevor Fitzgibbon.

And the settlement agreement (according to FitzGibbon) stated:

Radack’s continued posts about FitzGibbon thus seem to be in violation of that settlement agreement, and Friday FitzGibbon filed suit against her again for, among other things, breach of the settlement agreement as well as defamation.

3. Radack’s consent to the speech restrictions—the restraining order in the first case, and the settlement agreement (assuming FitzGibbon’s follow-up complaint accurately reports it)—was doubtless given under pressure, stemming from the costs and risks of the continuing litigation. Nonetheless, promises not to speak are legally binding (see Cohen v. Cowles Media, Inc. (1991)), and that’s also true of promises extracted under litigation pressure.

I don’t know who’s right and who’s wrong as to the original allegations, or Radack’s later follow-ups. And certainly people generally have a First Amendment right to sharply criticize those who they believe have abused them, subject to the constraints of defamation law. But this is a good illustration that, once people promise not to exercise this right, they’re generally stuck with it (unless there’s some special legal rule that makes such promises unenforceable, and such rules are rare). And this is so even if the restrictions agreed to in the promise are very broad.

from Latest – Reason.com https://ift.tt/2J21wPV

via IFTTT

It what appears to be the first known violation of the terms of the 2015 nuclear deal (JCPOA), Iran’s stockpiles of enriched low-grade uranium have surpassed the limit of 300 kg, Iran’s semi-official Fars News is reporting.

Fars noted further that the International Atomic Energy Agency had confirmed the stockpile measurement on Monday, after in May it had already quadrupled its production of the material, the key component to make nuclear reactor fuel – and potentially nuclear weapons. Following the Fars report which had been based on an unnamed “informed source,” Iranian Foreign Minister Javad Zarif was the first government official to confirm the country has exceeded the ceiling of 300kg, according to Iran’s ISNA.

Iran’s President, Hassan Rouhani, and Foreign Minister, Mohammad Javad Zarif. Image source: Getty

Iran’s leaders warned in the past days and weeks that it was on track to surpass the agreed upon enriched uranium limit set by the JCPOA in reaction to President Trump’s reimposed sanctions, as well as the inability of remaining signatories to deliver on their terms of the deal, which the US unilaterally pulled out of in May 2018.

The Fars report announcing the breach of the nuclear deal limits specifically cited European partners as lagging behind commitments to shield Iran from Washington sanctions, despite the new Instrument in Support of Trade Exchange (INSTEX) going live just days ago.

“For Europeans, there is still time, but if they are asking for more time, it means that whether they are incompetent or they are unwilling to deliver on their commitments,” an official with the Atomic Energy Organization of Iran (AEOI) was cited as saying in the Fars report.

Zarif also called INSTEX – which was officially launched by Europe as a SWIFT alternative on Friday – a “preliminary step” of the European members of the nuclear deal which only “partially delivers” on their commitments.

Zarif said Monday while speaking at a public event: “We will never succumb to international pressure, and together with the people of the world, we will force them to only treat Iran with respect and never threaten an Iranian,” and urged European allies to resist US pressures and aggression.

Last week, President Trump had threatened Iran in a tweet with “great and overwhelming force” and in some areas “obliteration” should it pursue nuclear weapons development. Zarif had responded with his own tweet saying “misconceptions endanger peace” and reiterated that US sanctions amount are tantamount to “war.”

via ZeroHedge News https://ift.tt/2RLRTrq Tyler Durden

1. Trevor FitzGibbon is a communication strategist who has epresented, among others, Julian Assange. Jesselyn Radack is a whistleblower lawyer and author who has represented, among others, Edward Snowden. Radack and FitzGibbon had been on apparently good terms, and Radack had publicly praised FitzGibbon’s work in August 2015:

FitzGibbon media has “a veritable Who’s Who” of leading organizations and public figures in the progressive world, Radack says: “While big PR firms may have more name cachet, FitzGibbon media makes up for it with genuine concern for client well-being, not just placing a story.”

Then, in early 2016, Radack accused FitzGibbon of raping her in November and December 2015. (FitzGibbon says they had a consensual sexual relationship, and claims that he has messages from after the alleged November incident that reflect the relationship being consensual.) Radack went to the police, but in 2017 prosecutors closed the investigation and decided not to prosecute FitzGibbon.

Radack then continued to criticize FitzGibbon, as well as “liking” and retweeting others’ posts that criticized FitzGibbon with regard to other sexual harassment accusations that had been made against him. FitzGibbon therefore sued her for libel (for more details, see this complaint). During the lawsuit, Radack continued to criticize FitzGibbon further, even though the trial court had ordered her not to use any social media “to publish or republish statements about”:

(a) the character, credibility, or reputation of Plaintiff or Defendant and/or their respective counsel;

(b) the identity of a witness or the expected testimony of Plaintiff, Defendant, or any witness;

(c) the identity or nature of evidence expected to be presented in support of any motion or at trial or the absence of such evidence;

(d) the strengths or weaknesses of the case of either party; and/or

(e) any other information the Defendant knows or reasonably should know is likely to be inadmissible as evidence in this case and that would create a substantial risk of prejudice or confusion if disclosed.

Radack was even held in contempt of court for violating the order, with the judge writing,

Radack acknowledges making the comments which [violated the order] and apologized for them claiming that they were “a desperate, emotionally charged, reflexive attempt to defend herself and respond to attacks that appeared to her to be coming from or orchestrated by the Plaintiff.” … The simple fact is that Radack deliberately violated the July 31, 2018 ORDER (ECF No. 41) by making the communications that she admittedly made. In so doing, she acted in contempt of the ORDER (ECF No. 41).

Neither contrition nor emotional distress nor illness [multiple sclerosis, apparently] nor financial difficulties [a bankruptcy] can excuse deliberate misconduct of this sort by any litigant, much less by a lawyer. And, the record here shows that Radack is a sharp-tongued, mean-spirited, proliferous user of social media. Her conduct here is just more of the same. Neither contrition nor emotional distress nor illness nor financial distress have caused Radack to ameliorate her penchant for nasty social media communication.

The original defamation case had settled, but Radack is apparently continuing to criticize FitzGibbon.

2. Here’s the complication, though: The restraining order in the earlier case would have been unconstitutional, except that Radack had stipulated to it:

Defendant concedes the motion and will not oppose entry of an order consistent with the relief sought in Plaintiff’s Motion for a Restraining Order. As counsel for plaintiff agreed at the hearing on the motion, this concession obviates the need for depositions or a hearing on the motion…. Defendant respectfully suggests that the Court enter an order consistent with that laid out on pages 1-2 of Plaintiff’s Motion for a Restraining Order [which are nearly identical to the order that was actually issued-EV].

She therefore had agreed to the speech restriction, and had it embodied in a court order—and then spoke despite it.

Radack then apparently settled the original case, and Tweeted this about the matter:

Since April 2018, I have been involved in litigation with Trevor Fitzgibbon. We have amicably resolved our differences. As part of the settlement, I retract and withdraw every allegation and statement I have ever made against Trevor Fitzgibbon.

And the settlement agreement (according to FitzGibbon) stated:

Radack’s continued posts about FitzGibbon thus seem to be in violation of that settlement agreement, and Friday FitzGibbon filed suit against her again for, among other things, breach of the settlement agreement as well as defamation.

3. Radack’s consent to the speech restrictions—the restraining order in the first case, and the settlement agreement (assuming FitzGibbon’s follow-up complaint accurately reports it)—was doubtless given under pressure, stemming from the costs and risks of the continuing litigation. Nonetheless, promises not to speak are legally binding (see Cohen v. Cowles Media, Inc. (1991)), and that’s also true of promises extracted under litigation pressure.

I don’t know who’s right and who’s wrong as to the original allegations, or Radack’s later follow-ups. And certainly people generally have a First Amendment right to sharply criticize those who they believe have abused them, subject to the constraints of defamation law. But this is a good illustration that, once people promise not to exercise this right, they’re generally stuck with it (unless there’s some special legal rule that makes such promises unenforceable, and such rules are rare). And this is so even if the restrictions agreed to in the promise are very broad.

from Latest – Reason.com https://ift.tt/2J21wPV

via IFTTT

Update: Russian Energy Minister Novak has stated that the extension of six to nine months is a consolidated agreement and other countries are in favour of such an extension.

Novak’s comments, and Russia agreeing to extend the OPEC+ deal, have removed a uncertainty from the discussion surrounding the deals future; as until these comments it was not known precisely what Russia’s position around an extension was and whether or not they would support one.

It is becoming increasingly clear that Russia is taking a larger and larger role in controlling OPEC (behind the scenes) as Bloomberg’s Javier Blas notes:

What’s most amazing about how #Russia is shapping every decision within #OPEC is how Moscow is also controlling the message. The below is from our live blog from Vienna on @TheTerminal | Follow TLIV [GO] for more | #OOTTpic.twitter.com/HLJCjWIMbh

Oil prices are up notably, after Friday’s plunge, as confidence builds that the OPEC+ alliance is poised to extend production cuts into 2020.

At the start of two days of meetings in Vienna, Bloomberg reports, that the world’s leading oil exporters are likely to extend production cuts as they fret about a weakening outlook for global demand growth and the relentless rise in output from America’s shale fields.

Of course, the OPEC+ meeting is actually moot since Russia and the Saudis already agreed the cuts would be extended at the G-20 meeting over the weekend.

“The market is going to like the nine months extension,” said Mohammad Darwazah, oil analyst at consultant Medley Global Advisers, who’s in Vienna monitoring the oil talks.

“Everyone now is realizing that in 2020 supply growth will exceed demand growth. And the Saudis and the Russians are trying to get ahead of that situation.”

And it is, for now…

However, as Bloomberg notes, it is not a completely done-deal as despite the broad consensus for a six-to-nine month extension, the meeting could prove contentious as Iran appears determined to make an issue of the growing dominance of Saudi Arabia and non-member Russia in the policy decision making of the cartel.

via ZeroHedge News https://ift.tt/2NmO9hq Tyler Durden

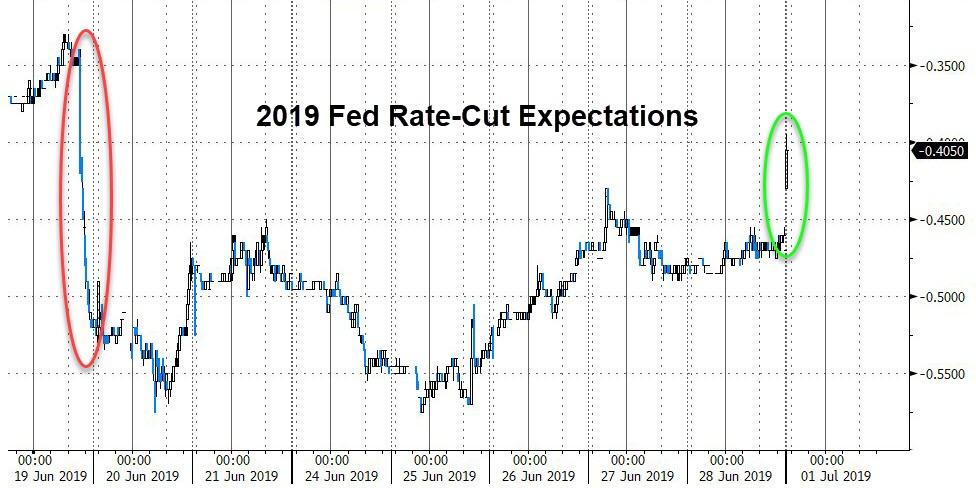

Global bonds retreated on Monday (although losses were pared) as the U.S. and China agreed to restart trade talks, leading investors to pare wagers on aggressive policy easing by the major central banks.

That, however, did not prevent stocks from surging out of the gate, with S&P futures set to open at new all time highs just 20 or so point below 3,000 even though as Bloomberg points out, the outcome of the G-20, or rather G-2, meeting was just as consensus expected.

Stocks are jumping even as none of the market Gremlins have left, with Hong Kong protests turning violent again on Monday (incidentally, there was zero mention of China’s growing pains in Hong Kong, just as Beijing wanted),while global PMI continued plumbing new cycle lows, and after both Chinese manufacturing surveys missed expectations, printing in contraction just below 50…

… the picture turned even uglier in Europe, where the UK PMI missed expectations, sliding to a three year low of 48, while Spain’s mfg PMI printed in contraction, or 47.9, for the first time in five and a half years.

Surveys from Japan and South Korea showed similar slowdowns as did the 19-country euro zone’s reading which contracted for fifth month running and at a faster pace than previously thought.

“Euro zone manufacturing remained stuck firmly in a steep downturn in June, continuing to contract at one of the steepest rates seen for over six years,” said Chris Williamson, chief business economist at IHS Markit. “The disappointing survey rounds off a second quarter in which the average PMI reading was the lowest since the opening months of 2013.”

None of this had an impact on stocks, however, with European markets rising over 1%, chasing the outperformance in Asia, as US equity futures ramped higher, even as the dollar firmed across the board, as traders reined in bets for a half-point rate cut from the U.S. Federal Reserve this month. And yet, the Fed’s dovishness which was responsible for the market’s gain in June (as a reminder PE multiple expansion accounted for 90% of the June surge), is being widely ignored on Monday, with the market’s attention focused on the G-20 outcome instead, where as we noted overnight (and this morning), nothing has been resolved.

To be sure, trader sentiment about the outcome was mixed: “It (Trump-Xi G20 meeting) played as well as possible,” said SEB Investment Management’s global head of asset allocation Hans Peterson. “So It gives us time to digest and get a bit better activity in the global economy.”

On the other hand, Bloomberg’s Cameron Crise was more skeptical, noting that “a truce is a long way from a deal, and it may be worth recalling that the sharp rally after the previous G-20 meeting between Trump and Xi lasted a mere 24 hours, albeit under a somewhat different backdrop. While there’s no guarantee that the rally fades by the end of the day, therefore, it wouldn’t come as a surprise to see a little late-session selling once the euphoria starts to cool off.”

For now, however, risk is certainly higher, with Europe’s STOXX 600 and Japan’s Nikkei climbed 1% and 2.1% respectively to hit two-month tops and MSCI’s global index added 0.2% having only just missed out on its best first half to a year.

In Asia, Chinese blue chips jumped 2.6% to their highest since late April, Germany’s export-heavy DAX sprang 1.5% to its highest since August, Wall Street futures were up over 1% while the combination of the Huawei hiatus and M&A activity hoisted Europe’s the tech sector to a one-year high.

In the US, E-Mini futures for the S&P and Nasdaq rose 1.1% and 1.7%, with the former breaking out above resistance, and just whispers away from 3,000 whereas in the bond market Treasury futures slid 10 ticks as yields on 10-year notes edged up 4 basis points to 2.04%.

Ironically, the S&P may hit 3,000 on the day the ISM dips below 50 (expectations for the Mfg ISM is for a 51.0 print).

As noted last night, Fed funds dropped over 5 ticks as the market scaled back the probability of a half-point rate cut this month to around 15%, from nearer 50% a week ago. “I think the Fed expectations in the market are very aggressive. Possibly a bit too aggressive,” SEB’s Peterson added.

The reaction in currency markets was to strip some recent gains from safe harbors like the yen and Swiss franc. The dollar crept up 0.4% on the yen to 108.26 and 0.7% on the franc to 0.9830. The dollar strengthened versus all its Group-of-10 peers, while haven currencies weakened. Weaker-than-forecast manufacturing PMIs from the euro zone weighed on the euro and capped losses in the region’s bonds. The pound slipped following disappointing U.K. manufacturing data and before Conservative leadership contender Jeremy Hunt is expected to detail contingency plans for a hard Brexit

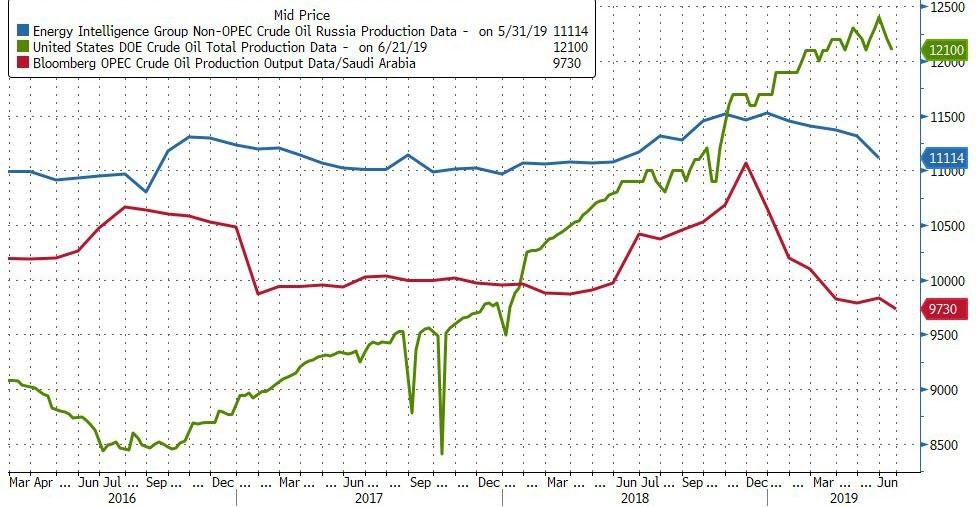

In commodities, oil prices sprang higher on news OPEC and its allies look set to extend supply cuts at least until the end of 2019 as Iraq joined top producers Saudi Arabia and Russia in endorsing the policy. Brent crude futures rose $1.85 or 2.8% to $66.40, while U.S. crude gained $1.84 or 2.75% to $59.90 a barrel.

Expected data include manufacturing PMIs. No major company is scheduled to report earnings

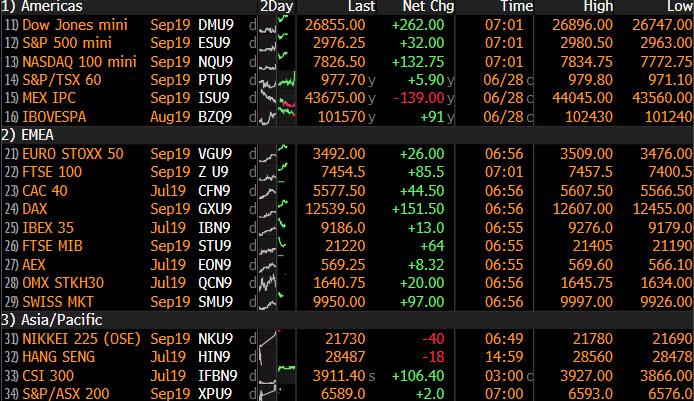

Market Snapshot

S&P 500 futures up 1.1% to 2,976.25

STOXX Europe 600 up 0.7% to 387.73

MXAP up 0.8% to 161.38

MXAPJ up 0.4% to 529.96

Nikkei up 2.1% to 21,729.97

Topix up 2.2% to 1,584.85

Hang Seng Index down 0.3% to 28,542.62

Shanghai Composite up 2.2% to 3,044.90

Sensex up 0.8% to 39,716.91

Australia S&P/ASX 200 up 0.4% to 6,648.10

Kospi down 0.04% to 2,129.74

German 10Y yield unchanged at -0.326%

Euro down 0.4% to $1.1331

Italian 10Y yield fell 3.2 bps to 1.74%

Spanish 10Y yield fell 1.3 bps to 0.382%

Brent futures up 2.8% to $66.53/bbl

Gold spot down 1.5% to $1,388.10

U.S. Dollar Index up 0.4% to 96.51

Top Overnight News

President Donald Trump declared the U.S. was “winning” the trade war a day after reaching a temporary truce with Chinese President Xi Jinping. Gauges of activity in China’s manufacturing sector showed the economy remains fragile, underlining the need for the truce with the U.S. forged at the weekend to be a lasting one

Manufacturers in the euro area remained firmly stuck in a slump last month as new orders slid and business confidence remained subdued

Tension returned to Hong Kong’s streets Monday as protesters attempted to break into the city’s legislature and thousands more began marching in opposition to the city’s China- backed government

Sentiment among Japan’s large manufacturers deteriorated to the lowest level in almost three years amid trade tensions that are adding to uncertainties for the economic outlook

Jeremy Hunt and Boris Johnson, the candidates competing to become U.K. prime minister, reiterated their willingness to take the nation out of the European Union without a deal if necessary, as both insisted they have the fiscal space to fund their spending plans

The ECB presidency won’t be decided at the EU summit in Brussels, a high-ranking German official said, who declined to be identified because the matter is confidential. That decision will be postponed until September in an attempt to move it away from the highly political nominations for the commission and council presidencies

Oil raced higher after Russian President Vladimir Putin struck a deal with Saudi Crown Prince Mohammed Bin Salman at the G-20 to extend output cuts for the rest of this year and potentially into early 2020, while the U.S. and China called a temporary truce in the trade war

Factory sentiment across Asia became even more frigid in June, signaling a worsening in the region’s growth outlook as U.S.-China trade tensions continue to simmer

The European Central Bank could be headed for its first-ever female president as European Union leaders haggle over top policy positions

Asian equity markets began H2 with gains across the board as global sentiment was buoyed following the US-China trade truce at the G20, while President Trump also met with North Korea leader Kim at the Demilitarized Zone and became the first sitting US President to step into North Korean territory. ASX 200 (+0.4%) was lifted by the trade sensitive sectors, as well as energy names after oil prices were buoyed by news of a Russia and Saudi agreement regarding the output cut deal. Advances in Nikkei 225 (+2.2%) were exacerbated by favourable currency moves and the KOSPI (U/C) was subdued by domestic tech weakness amid a dispute with Japan related to wartime forced labour in which the latter is to restrict chip material exports to South Korea. Elsewhere, the Shanghai Comp. (+2.2%) was buoyed by the US-China trade truce and after comments from President Trump which raised hopes of a potential U-turn on Huawei. This underpinned tech and telecom stocks with mainland Chinese markets the regional outperformers despite the miss in Chinese Manufacturing PMI data and absence of Hong Kong participants for holiday. Finally, 10yr JGBs were lower as they mirrored the slump seen in T-notes and heavy losses across safe-havens, while the BoJ also recently announced its bond buying intentions last week in which it reduced the amounts of JGBs with 3yr-5yr and 10yr-25yr maturities.

Top Asian News

Applied Materials Said to Buy Kokusai Electric From KKR

Turkish Assets Rally After Trump Seen Softening Sanctions Threat

Iron Ore Tests $120 as Australia Lays Bare Global Market Squeeze

Dubai’s DP World Acquires Topaz Energy in $1.1b Deal

Major European bourses are posting gains this morning [Euro Stoxx 50 +0.9%] as the positive sentiment generated by the US and China temporary trade truce rolls over from the Asia-Pac session. Sectors are mixed, though predominantly in the green, outperformance is seen in Energy names which are also bolstered by the broader complex; in terms of the laggards, the defensive sectors, i.e. utility and consumer staples sectors are in negative territory. Towards the top of the Stoxx 600 are a number of semiconductors for example, STMicroelectronics (+5.5%), Dialog Semiconductor (+4.4%) and ASML (+3.3%) on the aforementioned US-China updates; however, also of note for chip names is that Japan are to restrict chip material exports to South Korea amidst a dispute concerning the countries ruling on wartime forced labour. Other notable movers include, ArcelorMittal (+3.0%) after the Co. has completed the sale of several steel-making assets to Liberty House Global for EUR 740mln. At the other end of the spectrum is Ericsson (-0.5%), who opened lower by around 1.5% as US President Trump commented that the US is to ease restriction on Huawei; as previously the likes of Huawei and Nokia have benefited from the Huawei restrictions.

Top European News

ECB May Cut Rates by 20bps, Restart QE in September: Goldman

Generali Is Said to Lead Bidding for Apollo’s Tranquilidade

LafargeHolcim Is Said to Join Race for BASF Mortars Unit

Germany’s DAX Set to Enter Bull Market as Trade Clouds Clear

In currencies, the Franc has slumped across the board and only in part on a loss of safe-haven demand after the US-China trade truce forged on Saturday, as Swiss retail sales and manufacturing PMI both misses consensus by considerable margins, and the SMI kicks off H2 on its own after the EU severed links with the Swiss bourse. Usd/Chf is back up near 0.9850 and Eur/Chf has rebounded further above 1.1100 to just over 1.1150 vs recent lows of sub-1.1000 and circa 1.1055 respectively.

GBP – Sterling has also succumbed to all round selling in wake of the latest UK manufacturing PMI that was weaker than forecast and deeper in contraction territory, while output fell sharply from 50.3 to 47.2 and the worst level since October 2012. Cable recoiled from around 1.2707 at best through 1.2665-63 support that held several times in late June before breaching 1.2650 and a 1.2646 Fib on its way to a 1.2635 base, while Eur/Gbp has jumped towards 0.8970 from close to 0.8925 at one stage even though the single currency was pressured by disappointing Eurozone manufacturing PMIs as well.

JPY/AUD/EUR – The Yen has succumbed to the broad post-G20 recovery in risk sentiment, but not to the same extent as the Franc noted above, with 108.50 vs the Greenback tested and marginally topped before a relatively deep pull-back towards 108.25. A decent 1 bn option expiry may have capped the headline pair, while the DXY also faded after edging above 96.600 and a lack of follow-through buying to test near term resistance at 96.711 (June 21 peak). However, the Aussie remains on the backfoot just under 0.7000 ahead of Tuesday’s RBA policy meeting with a firm majority anticipating back-to-back 25 bp rate cuts, and the Euro is holding near the bottom of a hefty expiry zone from 1.1320 to 1.1335 (1.6 bn) having lost grip of the 200 DMA (a few pips below 1.1350) in the run up to the aforementioned poor PMIs and then breaching the 10 DMA (at 1.1328) to a 1.1315 low.

CAD/NZD/SEK/NOK – The Loonie and Kiwi are both down vs their US counterpart, but holding up better than most major rivals, bar the Scandi Crowns, with Usd/Cad only just above 1.3100 and Nzd/Usd hovering close to 0.6700. A firm rebound in oil prices is impacting, and also boosting the Nok (through 9.7000 vs the Eur), while the Kiwi is eyeing the impending NZIER Q2 survey for independent impetus. Note, Eur/Sek is back below 10.5500 in response to a rare manufacturing PMI beat from Sweden that will likely keep the Riksbank in hawkish mood on Wednesday.

EM – The Lira has extended gains made on the back of a relatively cordial meeting between Turkish President Erdogan and his US peer Trump on the G20 sidelines that assuaged concerns about sanctions over Russia’s imminent S-400 delivery with additional momentum coming in the form of a less contractionary manufacturing PMI. Usd/Try reversed from 5.7910 to 5.6735 in response before settling around 5.6950.

In commodities, WTI (+2.7%) and Brent (+2.7%) have started the week firmly on the front foot, with WTI having breached the USD 60/bbl level to the upside. Gains in the oil complex are stemming from a sentiment-driven gains (from constructive US-China G20 and North Korea outcomes) alongside an agreement between Russia and Saudi Arabia to extend the OPEC+ deal. The leaders discussed an extension of six to nine months at the level it is currently at (1.2mln BPD), with Russian Energy Minister Novak stating that the extension is a consolidated agreement and other countries are in favour of such an extension. Novak’s comments, and Russia agreeing to extend the OPEC+ deal, have removed a uncertainty from the discussion surrounding the deals future; as until these comments it was not known precisely what Russia’s position around an extension was and whether or not they would support one. In terms of scheduling for today we have both the JMMC and the OPEC meeting, with the closed session of the JMMC having commenced as of 10:00BST, and OPEC’s opening session is due to begin at 13:00BST, closed session at 14:00BST and a presser at 16:00BST, where we may get further insight into the OPEC+ extension; though an official decision will not be released until the presser following tomorrows OPEC+ meeting at 12:00BST. Note, the timing of the various sessions for JMMC, OPEC & OPEC+ is at best an indicative guide only.

Elsewhere, Gold (-1.3%) is suffering due to a firmer USD and a safe-haven unwind, as are other havens including JPY and CHF, with the yellow metal giving up the USD 1400/oz handle after this weekend’s positive trade/geopolitical developments; having printed a session low of USD 1381/oz after the metals largest intraday fall for a year. In contrast, the trade truce has supported copper prices which are just shy of the 6-week high posted earlier in the session at USD 2.72/lb. Finally, iron ore prices have rallied in excess of 4.0%, supported by the overall risk sentiment and underpinned by supply woes.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 50.1, prior 50.1

10am: ISM Manufacturing, est. 51, prior 52.1; ISM Employment, prior 53.7; ISM New Orders, est. 52.5, prior 52.7

10am: Construction Spending MoM, est. 0.0%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

Welcome to July and a very happy 10th birthday to this economic expansion. Today takes us into unchartered territory in the US with this upswing now being the longest on record of all the 34 back to the 1850s. A reminder that we published a note a couple of weeks ago looking at the long cycle world we’ve been in since the 1980s and how it’s only been possible due to a massive global levering up, unparalleled money printing, and likely lower productivity. See the link here .

Before we get to a big weekend for news, Craig has published the latest performance review for H1, Q2 and June. June saw all 38 of our non-FX assets in our survey higher – only the second time in 150 months since we started collating the data in 2007 with January this year being the other. Indeed for H1 2019, 37 out of 38 assets were higher – the highest H1 ratio over the same period. See the full report here .

It feels that the weekend saw positive progress on a lot of things. A US/China trade truce, a constructive surprise Trump meeting with Kim Jong Un, positivity over US/Turkey relations, a Russian/Saudi OPEC+ agreement on extending cuts (official OPEC/OPEC+ meetings today/tomorrow), and in the background the EU and Mercosur (South American trading block) brokered a trade deal after 20 years of negotiating. That timespan is something to consider when thinking about Brexit! On the flip side China’s manufacturing PMI stayed at 49.4 – a tenth below expectations with new export orders edging down 0.2pts to 46.3, the weakest since February. The non-manufacturing PMI slipped a tenth to 54.2 (54.3 expected) bringing the composite to 53.0 (vs. 53.3 expected). China’s Caixin manufacturing PMI also printed this morning at 49.4 (vs. 50.1 expected and 50.2 last month), the weakest since January, with both the new orders and new export orders components falling into contractionary territory, after rising in May.

The main G-20 summit was a sideshow really and the released communique was unanimous only by being bland and not committing anyone to anything. Disagreements on trade and climate change continue. As for the main event, although expectations were building ahead of the Trump/Xi meeting, on balance they exceeded them even if it still feels like a fragile equilibrium. At the moment I’m relieved we went back to being more constructive on credit a couple of weeks ago as news of this meeting broke at the same time as Draghi’s very dovish Sintra speech. The two most positive things from the weekend were that President Trump won’t put the additional tariffs on China for the “time being” and that he softened his stance on Huawei. He will allow US companies to sell some equipment to Huawei, as long as it was “no great national security problem”. At the moment there is no clarity on whether this means Huawei will be taken off the ‘entity list’ of the US Commerce Department, but Trump has promised to discuss this soon and suggested they’ll leave this controversial issue to the end of trade negotiations which is likely to be seen as a positive as its now not standing in the way of an outline deal. However, Trump’s decision to grant Huawei some temporary relief has drawn criticism back home with Senator Marco Rubio tweeting “If President Trump has agreed to reverse recent sanctions against #Huawei he has made a catastrophic mistake.”

Trump also said Xi promised that China will buy “tremendous” amounts of US agricultural products, and that the US will “give them a list of things” they would like China to buy. However, Chinese official media reports are not as clear on this and suggested only that Trump hopes China will import more American goods as part of the trade-war truce. Meanwhile, there has been no official communication from China. So whether China sees things the same way is not clear, but on balance it seems a more positive backdrop for talks to continue even if there is not currently any roadmap. Elsewhere, Trump continued his criticism of the Fed over the weekend saying the Federal Reserve “has not been of help to us at all” in his trade spat with Beijing and added “Despite that, we’re winning, and we’re winning big because we have created an economy that is second to none”.

Meanwhile, in an interview on Fox News, Larry Kudlow, the White House National Economic Council director, said that Mr Trump isn’t offering a “general amnesty” to Huawei Technologies as part of an agreement to restart trade talks while adding that there are no firm promises and no timetable for completion of a potential sweeping trade agreement, and that China still needs to address the issues that the U.S. has said caused the discussions to fall apart in early May. He repeated that the U.S. and China are 90% done on a trade deal but the final 10% will be the hardest.

Asian markets have started the week on a firm footing buoyed by the trade war truce. Chinese markets are leading the advances with the CSI (+2.47%), Shanghai Comp (+1.88%) and Shenzhen Comp (+2.93%) all up along with the Nikkei (+1.91%). The Kospi (-0.06%) is trading down on news that Japan plans to slap export restrictions on some tech items sent to South Korea, a sign of escalating tension between the pair over recent compensation claims for Korean workers dating back from the colonial period. Samsung electronics is down -1.17% on the news. Meanwhile safe haven assets are trading down this morning with the Japanese yen trading weak (-0.39%) and gold prices down -1.19%, the largest drop since March this year. The Chinese onshore yuan is up +0.49% this morning to 6.8332 while the Turkish Lira is up +1.03%. Elsewhere, futures on the S&P 500 are +0.87% with WTI oil prices +2.38% on the likely extension of output cuts. US treasury yields are around 2-3bps higher across the curve. Markets in Hong Kong are closed for a holiday.

Yesterday also saw an EU leaders summit to discuss the important top jobs about to need filling. They have so far failed to agree on candidates with talks getting dragged into a second day. Meanwhile, here in the UK, the Telegraph has reported that in a speech today, Conservative Leadership Candidate Jeremy Hunt will announce plans for a £20 bn “war chest” for a no deal Brexit which would see dramatic tax cuts designed to turbo-charge the economy. Under the plan, Hunt would set aside £6 bn to help farmers and fishermen and spend £13bn cutting corporation tax from 19% to 12.5% to help businesses amongst other measures. So in addition to Mr Johnson’s plans, a no-deal Brexit will likely unleash a huge fiscal spending spree in the UK – another show to drop in the global fiscal movement. Staying with the UK, yesterday Nigel Farage’s Brexit Party announced that it was ready to fight a general election as it unveiled 100 people it said would be candidates.

As for this week, US Independence Day on Thursday will break up the week and activity with US bond and equity markets closing at half time Wednesday and all of Thursday. However we do have some important data including the remainder of today’s global manufacturing PMIs/US ISM, Wednesday’s services equivalent, and Friday’s US employment report which will be important as evidence starts to slowly build of a softening of the strong US labour market. Consensus is at +158k vs +78k last month. The weekend truce will take the edge of any weak numbers in today’s PMIs with hopes that business confidence can slowly start to rebuild again with the caveat that the truce could break at any time. The rest of the week ahead is at the end today.

In advance of the G-20, equity markets ended last week on a positive foot but mixed overall on the week. The S&P 500 ended the five days -0.32% lower (+0.55% on Friday) while the Stoxx 600 was close to flat at +0.03% (+0.70% Friday). On both sides of the Atlantic, financials outperformed, with US and European bank shares up +2.22% and +1.79% (+2.37% and +0.75% Friday) respectively. The moves mostly came after all major banks passed the Fed’s stress tests on Thursday night. US tech firms had more muted price action, with the NASDAQ down -0.32% (+0.48% Friday) and the NYFANG index +0.54% (+0.18% Friday). The DOW lagged slightly trading down -0.45% (+0.28% Friday), as its largest member Boeing dropped (-2.09% on the week and flat on Friday) on new revelations about safety issues with its 737 Max plane. In Europe, performance was a bit bifurcated, with the DAX outperforming +0.48% (+1.04% Friday) while Italy’s FTSE MIB and Spain’s IBEX lagged, down -0.72% and -0.31% (+0.59% and +0.56% Friday) respectively.

The rally in fixed income markets continued relentlessly, with 10-year treasury yields down -4.9bps on the week (-0.9ps Friday). That marks the 8th consecutive weekly rally, the longest streak since 2012. Two-year yields fell less sharply, dropping -1.7bps (+0.6bps Friday), which caused the curve to flatten -3.0bps (-1.3bps Friday). Similar dynamics were at play in Europe, where bunds and schatz rallied -4.2bps and -1.3bps (-0.7bps and -1.4bps Friday), respectively. Action in currency markets was relatively muted, with the dollar index trading listlessly to end the week flat. EM currencies fell -0.30% (+0.06% Friday), though there was heterogeneity within the asset class, e.g. the Brazilian real fell -0.56% (-0.61% Friday), but the South African rand appreciated +1.77% (+0.59%).

via ZeroHedge News https://ift.tt/2ZZIeAm Tyler Durden

That was truly an extraordinary weekend. Trump vs Xi agreed to resume trade negotiations. No more tariffs, but the old ones still in place. Huawei ban to be reconsidered. Trump also met Kim in the DMZ. It was also the end of H1 2019, with stock markets posting their most impressive gains since 1997 even as bonds proved the top returning assets – which should have everyone wondering and worrying how!

I reckon that puts us in a very interesting position for the next 18 months. Trade wars will remain a major distraction and concern – whatever happened in Osaka over the weekend, about the only thing we can confirm is nothing is really fixed! Instead, the dominant factor in coming months could be the US Federal Reserve – and how it is likely to come under increasing pressure from Trump, who is now in full electioneering mode. That puts a whole new complexion on the Game of Markets.

(I am travelling next few days, but I would be fascinated to read any research on how markets perform in the lead up to US elections? I suspect its highly unlikely Trump will countenance any kind of market instability that could damage his prospects ahead of Nov 2020 – therefore expect lots of Fed Bashing as an electoral weapon!)

Let me try to put it all in context. We are posed with far more questions than answers. Its complex:

The renewed trade negotiations between China and US will have little effect on market direction. The news will decrease expectations of an imminent global recession, but it also reduce the pressure on the Fed to cut US rates. Hence it is Market Neutral.

This week’s US Payroll number on Friday is expected to be back in the 150k range, confirming last month was an anomaly and the US is still seeing strong/moderate growth, suggesting little immediate pressure to ease rates.

Both Trump and XI were playing for time – Trump’s demands about opening up China to US agri-goods is simple play for an electoral boost. XI needed the promise of no further tariffs and a Huawei rethink as a sign he’s got concessions. Neither side has much to gain politically from pushing swift agreement, (economically is a very different matter, both China and US will still suffer), meaning trade doubts drag on and remain a major market concern through rest of year.

The debate over Huawei is also a distraction – whatever is now agreed, Huawei is a damaged brand in the West. The US and China are likely to increasingly diverge down separate tech paths. However, Trump’s readiness to trade the Huawei card could cause him domestic political issues.

In the Long Term little was solved in Osaka. The US and China remain on collision course.

Trump – played the G20, Xi Meeting and Korea meeting with Kim to play to US electorate. Trump is in full election mode which is bad for Fed.

The issue for markets is Trump’s willingness to play the short electoral game. The fact he was willing to trade Huawei for an agreement was fascinating. A few weeks ago he was parading advice on the danger Huawei presents to long-term communications systems and therefore the whole economy. The US neo-cons will be furious. They have argued the US has just a few short-years to take-on China economically before it’s transforming economy is settled, and before the Chinese military becomes an effective deterrent to US geopolitical might. Any delay now makes that long-term reckoning less certain to play towards the US.

What is going to be critical is how market reacts – the big danger is that market believes Fed is going to deliver, and it doesn’t. That’s why I think it’s all about how Powell stands up to Trump in coming months. It’s hardly an encouraging time for markets when it’s the expectations of further Fed easing that’s the dominant factor keeping them afloat, and a President who thinks stocks = economic health!

The current market doesn’t speak of strong companies making sound business decisions. Nor does the downwards direction of global yields make any sense if the economy was strong enough to justify stock prices… Nope it speaks of a Fed feeding markets by easing when it should be normalising rates.

Now why would the Fed ease? Someone should tattoo “Hold Fast” on Powell’s knuckles.

Such is the world we live in. Tomorrow, European leaders and all that stuff.

via ZeroHedge News https://ift.tt/2xneIIt Tyler Durden

Just when local (Chinese-beholden) authorities thought it was safe to continue their totalitarian shift to the motherland, the citizens of Hong Kong are rising up once again.

Reuters reports that Hong Kong protesters stormed the Legislative Council on the anniversary of the city’s 1997 return to Chinese rule on Monday amid widespread anger over planned laws that would allow extraditions to China, plunging the city deeper into chaos.

“In the past few years, people have been getting more active, because they found the peaceful way is not working,” said a 24-year-old protester surnamed Chen.

A small group, mostly students wearing hard hats and masks, used a metal trolley, poles and pieces of scaffolding to hack through reinforced glass and charge at the government compound near the heart of the financial center.

Riot police in helmets and carrying batons fired pepper spray in response in a standoff that was lasting into the sweltering heat of the evening.

Tens of thousands marched in temperatures of around 33 degrees Celsius (91.4°F) from Victoria Park in an annual rally that organizers hoped would get a boost from the anger over the extradition bill.

A tired-looking Lam appeared in public for the first time in nearly two weeks, flanked by her husband and former Hong Kong leader Tung Chee-hwa.

“The incident that happened in recent months has led to controversies and disputes between the public and the government,” she said.

“This has made me fully realize that I, as a politician, have to remind myself all the time of the need to grasp public sentiment accurately.”

In a statement, a government spokesman has criticised demonstrators for storming “the Legislative Council with extremely violent methods, and destroying the glass door of the Legislative Council with offensive weapons such as an iron cart and iron poles”.

The statement said:

“The government strongly condemns it and expresses deep regret.

“Hong Kong is a society of the rule of law, and violence has never been accepted by society. Demonstrators who use violence must stop immediately, and the police will take appropriate law enforcement actions to ensure social order and public safety.”

More than a million people have taken to the streets at times over the past three weeks to vent their anger.

via ZeroHedge News https://ift.tt/2XgNKS8 Tyler Durden

When I’m having a bad day, I trawl the internet for videos of happy cyborgs. My favorites are clips of hearing-impaired people getting their cochlear implants turned on for the first time. The videos follow a soothingly predictable pattern. Mumbly background chatter and shaky cam—the cinematography is rarely good—then a pregnant pause, wide eyes, and finally that peculiar kind of sobbing that human beings do when we are overwhelmed. The pattern is the same whether it’s a babe in arms or a full-grown man.

If you catch the right algorithmic wave on YouTube or the right hashtag on Instagram, you can surf for hours in this genre: videos of Parkinson’s patients as their tremors are calmed by a new therapy, paraplegics walking with the help of adaptive prosthetics, infants getting their first pair of coke-bottle glasses, and more.

Adorable kittens and soppy love stories do little to warm my cold, dead heart. But show me a part-robot baby flipping out because he heard his mom say “hello” for the first time, and it’s onion city.

I’m not deaf or hard of hearing, but I am aware that cochlear implants are not without controversy in that community. As with almost everything you see on the internet, behind the scenes there is invisible labor, difficult setbacks, and the occasional disaster. Hardly anyone posts those on their YouTube channel.

Still, entire religions were once built around the spectacle of someone banishing a severe disability with the wave of a hand. Today any certified R.N. in the right audiologist’s office can be a secular saint. When my own worthless eyeballs were corrected with lasers, making me a blind(ish) woman given the gift of sight, I didn’t fall to my knees and worship the ophthalmologist. I just got out my credit card. We live in an age of reliable, scalable, profitable miracles.

People are ungrateful wretches, of course. Once anyone can reliably perform a miracle, it immediately ceases to seem miraculous. Babies generated without sex—actual virgin births—are humdrum. We carry nearly all of human knowledge in our pockets. Within a decade, burgers made without meat will be commonplace (page 10). And the memory of a time when HIV was a death sentence will soon fade to almost nothing (page 30).

As a species, we’re brilliant at focusing on the negative. There are some very useful evolutionary implications of this trait, but an unfortunate side effect is that we always feel like the sky is falling, even when it’s 70 degrees and sunny.

But historically speaking, it’s a beautiful day.

In 1820, nearly 84 percent of the world’s population lived in extreme poverty (roughly less than $1.90 per day per person). In 1981, according to the World Bank, that number was still 42 percent. Today, it’s hovering around 8 percent.

Also in 1820, 90 percent of the world’s population was illiterate. Today that number is inverted: 90 percent can read.

Since 1990, an additional 2.6 billion people have secured access to clean water.

And in 1990, zero percent of the world’s population had access to the World Wide Web. By 2020, more than half will.

In other words, the people around us are healthy and long-lived. They have words to read and videos to watch. The water is clear and blue. Food is plentiful and delicious. And the soundtrack—whether it’s piped in through the latest medical technology or just an ordinary pair of earbuds—is gorgeous.

All of these heartening facts and figures (and much of my hope for humanity) are drawn from an upcoming book, Ten Global Trends Every Smart Person Should Know, by Reason Science Correspondent Ronald Bailey and the Cato Institute’s Marian L. Tupy (page 12).

These are mere material gains, the determined pessimist might say. True enough. We are the children of Steven Pinker’s “long peace” and the grandchildren of Deirdre Nansen McCloskey’s “great enrichment.” We are safe and wealthy beyond the imagining of our ancestors, the beneficiaries of an astonishingly lengthy stretch of success for liberal institutions, international trade, and the free exchange of ideas.

These institutions are not automatically self-sustaining. But they are self-reinforcing. People aren’t perfectible, and they are prone to both personal and political error. Everything could always go pear-shaped.

But so far, billions of healthier, wealthier, better-educated, and better-connected people have also proven themselves better able to understand and defend the values of the free society.

Politics, of course, is crap. But politics has consistently been crap throughout the last couple of centuries, and yet here we are in the greatest period of global peace, enrichment, and innovation in human history. Truth be told, even the crappiness of politics is way down over the last 200 years. The modes of amplifying the shouting have gotten better, so the whole enterprise is noisier. But it’s far less fatal than it used to be. Not every downward trend line is an inflection point.

“Put not your trust in princes,” the psalmist warns us, “nor in the son of man in whom there is no help. His breath goeth forth, he returneth to his earth; in that very day his thoughts perish.” The first bit couldn’t be more true. But the rest is absolute rubbish.

Human beings are doing remarkably well lately, especially for such fragile, mortal creatures. As with the cochlear implants, a lot of messiness, horror, and hopelessness are hidden from view. It’s wrong to dismiss or ignore suffering just because it’s not part of a broader trend. But it is also wrong to despair.

The combined efforts of the sons of man have wrought astonishing changes. And their thoughts do not perish when they die but live on through their inventions and institutions. The dead of the last two centuries have bettered the world not just for themselves but for those of us who came after them. Their legacy is a world rife with boring, ordinary miracles.

from Latest – Reason.com https://ift.tt/2xn1kUJ

via IFTTT

{kind=link}