Thanks to a generous grant from the Stanton Foundation, and to the video production work of Meredith Bragg and Austin Bragg at Reason.tv, I’m putting together a series of short, graphical YouTube videos—10 episodes to start with—explaining free speech law. Our first four videos were

As usual for our episodes, the full script is also posted right below the video on YouTube.

We’d love it if you

Watched this.

Shared this widely.

Suggested people or organizations whom we might be willing to help spread it far and wide (obviously, the more detail on the potential contacts, the better).

Gave us feedback on the style of the presentation, since we’re always willing to change the style as we learn more.

Please post your suggestions in the comments, or e-mail me at volokh at law.ucla.edu.

Future videos in the series will likely include most of the following, plus maybe some others:

Corporations and speech.

Alexander Hamilton: free press pioneer.

Free speech at college.

Speech and privacy.

Speech on or with government property.

from Latest – Reason.com https://ift.tt/317elPe

via IFTTT

The FOMC will almost certainly cut the funds rate by 25bps to 2.00-2.25% today at 2pm. Whereas banks such as Goldman, BofA and Deutsche Bank expect a 25bp move – because virtually all of the signals from the committee point that way – there are several outliers, such as Morgan Stanley who are expecting the Fed to cut 50bps.

While the Fed leadership hasn’t taken a public position but seems to support 25bp privately, based on an article in the Wall Street Journal and an unusual statement by the New York Fed indicating that a (dovish) speech by President Williams was not a signal about the upcoming meeting. Other FOMC members are mainly debating whether to cut rates at all, with little overt support for 50bp. With that said, we cannot entirely rule out a 50bp move (for reasons listed yesterday).

Markets are currently priced for 30bp of easing, and this number could grow further on any significant disappointments in the economic data or adverse trade news before July 31. If so, the committee might be unwilling to deliver a large hawkish shock, given their apparent focus on bond market pricing.

So with that big picture out of the way, here is a snapshot of what Wall Street expects, courtesy of RanSquawk:

RATES:

The base case is a rate cut of 25bps, lowering the federal funds rate target to 2.00-2.25%, with the FOMC justifying the move as “insurance” to prolong US economic expansion amid global growth and trade uncertainties which continue to weigh on its outlook. Money markets still assign a negligible risk for a 50bps move, though it seems to lack widespread consensus among policymakers, particularly amid upside surprises in some key domestic data.

SIZE OF CUT:

The recent dovish remarks by Fed Vice Chair Richard Clarida and FOMC Vice Chair John Williams boosted expectations of a 50bps move, though pricing pared as the NY Fed walked back comments made by the latter, and analysts interpret the former as an argument for sooner rate cuts before data deteriorates, rather than aggressive rate cuts. A recent report said Fed officials were not prepared to cut by 50bps as recent economic developments were yet to signal an imminent downturn, sources told the WSJ, though these sources did suggest that the Fed could lay out potential stimulus beyond the July meeting. Voter Charles Evans said the argument between 25bps or 50bps of easing was a matter of strategy, while there could be further action ahead; fellow dove Bullard (who dovishly dissented at the June meeting, calling for a rate cut) noted his concerns on inflation and the yield curve for some time, but said 50bps might be excessive.

HAWKISH DISSENT:

In remarks just before the blackout window, voter Eric Rosengren said that as long as the economy continues doing well, accommodation was not needed, and he did not want to loosen policy if the economy is doing well without it; while voter Esther George said she saw nothing in the data to change her outlook, leaving scope for two possible hawkish dissents calling for rates to be left unchanged. George is almost certain to be the lone dissenting voice to today’s rate cut; if more than just one dissenter emerges, stocks will take it as a potentially hawkish surprise.

FUTURE CUTS

It is worth noting that Bullard, Clarida and Evans have all alluded to the ‘insurance’ rate cuts made by the FOMC in 1995 and 1998 as a potential blueprint; the Fed cut rates by 25bps three times during each of those episodes. Markets still expect further easing ahead, with 68bps of easing priced through the end of this year, and around 100bps of easing through 2020. The June ‘dots’ revealed that just under half of participants are comfortable with the notion of 50bps of further cuts through the end of the year. The statement could give a nod to that pricing by maintaining guidance that “the Committee will closely monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion,” language that was inserted into the June statement to supposedly prepare for the July cut.

BALANCE SHEET:

There is a possibility the Fed might announce a sooner than anticipated end to its balance sheet normalisation plans, which will presently conclude in September (and then in October, the Fed will be a net buyer of between USD 10-20bln of Treasuries per month). Powell has previously indicated that the Fed would be prepared to adjust the run-off as necessary. Ending the run-off early would be bullish for Treasuries, TD Securities thinks, since USD 28bln of Treasuries within the Fed’s portfolio mature in August and September; if the runoff ended in July, it would result in USD 28bln of less supply for the private market to digest, TD explains, and additionally, MBS runoff would be reinvested in Treasuries, resulting in between USD 35-40bln of additional Treasury buying over two months.

STANDING REPO RATE FACILITY (SRF):

The June FOMC meeting minutes showed participants were briefed on a possible new repo facility which could allow the Fed to better manage the effective fed funds rate within the target range, preventing unusual spikes via providing incentives for banks to shift the composition of their portfolios of liquid assets away from reserves and toward high-quality securities. The Fed could use this help to boost liquidity conditions, however, desks have noted that the mechanics of setting up a repo facility will take time – it took over a year for the Fed to set up the reverse repo facility, for instance.

GOLDMAN UNCONVINCED

In a surprising dissent with the coming rate cut, in its preview of the FOMC decision, Goldman said that its own assessment “remains that the justification for rate cuts at the current juncture is tenuous in terms of the Fed’s own mandate.” We were unconvinced of the need for easier policy even at the time of the June 18-19 FOMC meeting, and virtually all of the information since then has come in on the stronger side. President Trump postponed the threatened tariff escalation versus China, all of the major economic reports—including payrolls, retail sales, the manufacturing surveys, core CPI, and UMich 5-10 year inflation expectations—have surprised on the upside, and financial conditions have eased further since the meeting. Our outlook for the next year is for real GDP growth in the 2%-2½% range, unemployment falling below 3½%, and core PCE inflation rising to 2%+.

In other words, when it comes to controlling the Fed, Trump now has more power than even Goldman, a historic regime shift in its own right.

For those wondering what a 25bps rate cut Fed statement will look like, here is Goldman’s take on how the Fed statement changes will look like:

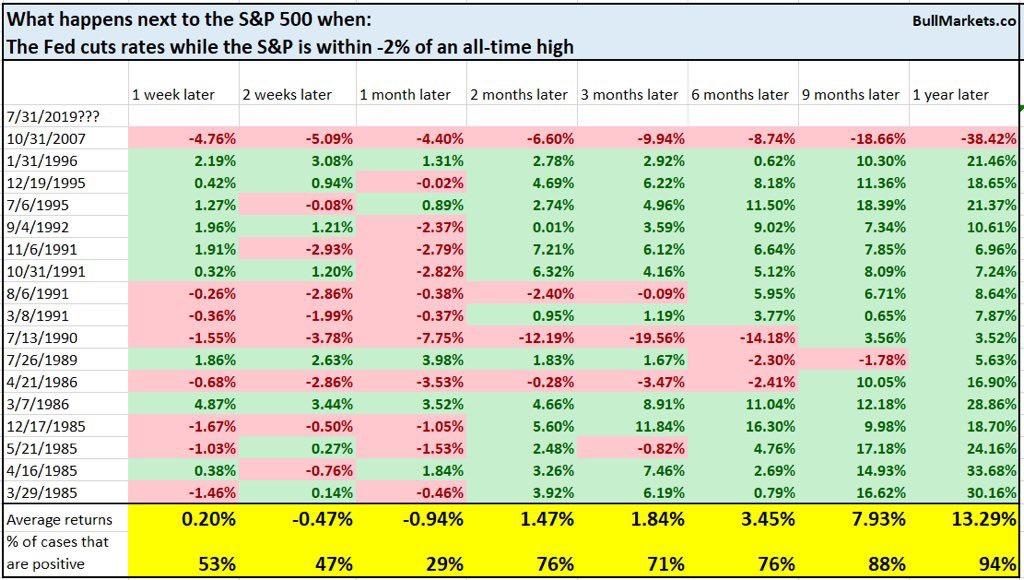

Finally, some historical trivia: courtesy of bullmarkets.com, here is a look at what happened in the past when the Fed cut rates with the S&P within 2% of all time highs.

via ZeroHedge News https://ift.tt/2GG5pIJ Tyler Durden

In case readers have been burried under a pile of negative yielding debt for the past 6 months, today is the long-awaited Fed decision day, where markets are fully pricing in what is expected to be the first rate cut since December 2008.

But, as Deutsche Bank’s Jim Reid notes, exactly what happens today is far from a foregone conclusion, as the question still on investors’ minds is by how much the Fed will cut, and whether there’ll be any messages about the future path of rates going forward. The market currently fully prices a 25bp cut and implies an 16% chance of a larger 50bp cut. And as we discussed last night, although the Fed have given no real encouragement to the notion of a 50bps cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50bp cut (with a recession following three months later), and a similar 50bp cut happened when the Fed began cutting in January 2001 (a recession followed in March).

Of course, rates were higher back then though so the Fed had much more space before hitting the infamous zero lower bound. The last time the Fed started an easing cycle with a 25bps “insurance” cut was in September 1998, when they ultimately cut rates 3 times and successfully prolonged the expansion… until the dot com bubble and recession in 2001.

So in their preview of what the FOMC will do, Deutsche Bank economists predict a 25bp cut, but they say that “the key question is how Chair Powell and the Committee frame the narrative for further easing through year end.” With this in mind, investors will be paying close attention to Chair Powell’s press conference. DB’s economists write that they “do not expect the Committee to pre-commit to another cut in September”, but instead the amount of further easing is going to be data dependent. “Will a market hungry for stimulus accept this”, asks Jim Reid, who then notes that:

Indeed we’re at a fascinating juncture in markets.

Reid goes on to summarize the zeitgeist: “It feels like the global macro risks are building for late summer/autumn (hard Brexit, US/China trade uncertainty, US/EU trade issues to come before year-end and global manufacturing effectively in recession) but all of us are reluctant to fight the central banks. Is this a trap? Indeed even our traditionally bullish Binky Chadha has some reservations about the risk/reward from this starting point.”

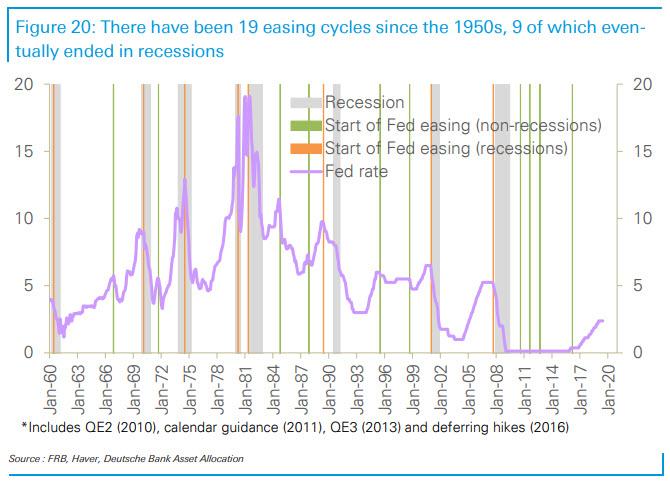

Referring to a note we highlighted on Monday, Reid notes that as Chadha pointed out, there have been 19 Fed easing cycles since the 1950s and this one fits almost exactly inline timing wise with the average slowdown in ISMs and LEIs through history. However, where it differs markedly is that only once (in 1995) has a rate cut occurred when the S&P 500 was around record highs. On average, the market has peaked 4 months before the cutting cycle started and was down a median -12% in between the two points.

Also, he pointed out that 9 of the 19 rate cutting cycles failed to avert a recession.

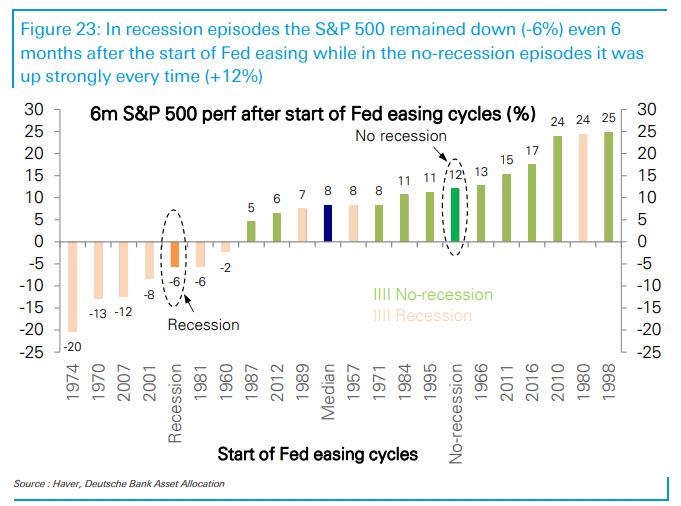

The recessions typically saw a -27% peak to trough drawdown in the S&P (mostly after the first cut) and on average bottomed 5 months after the Fed started cutting. Of the 10 that didn’t end in recessions, growth rebounded quickly – on average after 2-3 months – and although the S&P still fell around -7%, within 6 months of the first cut they had gained 12% from the lows and sat comfortably above pre-cut levels.

So history would suggest quite a binary outcome from here and based on this alone one would have to say that the risk/reward doesn’t look particularly compelling especially as we’re at record highs.

So, as Reid concludes, “while don’t fight the Fed is a famous refrain but nearly 50% of the time they’ve been powerless to stop negative economic and market momentum in a growth slowdown.”

via ZeroHedge News https://ift.tt/2LR6Msf Tyler Durden

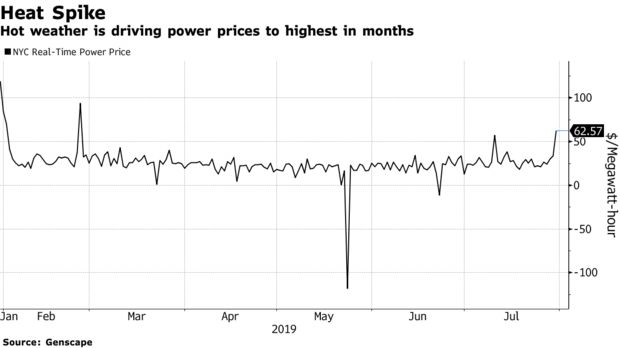

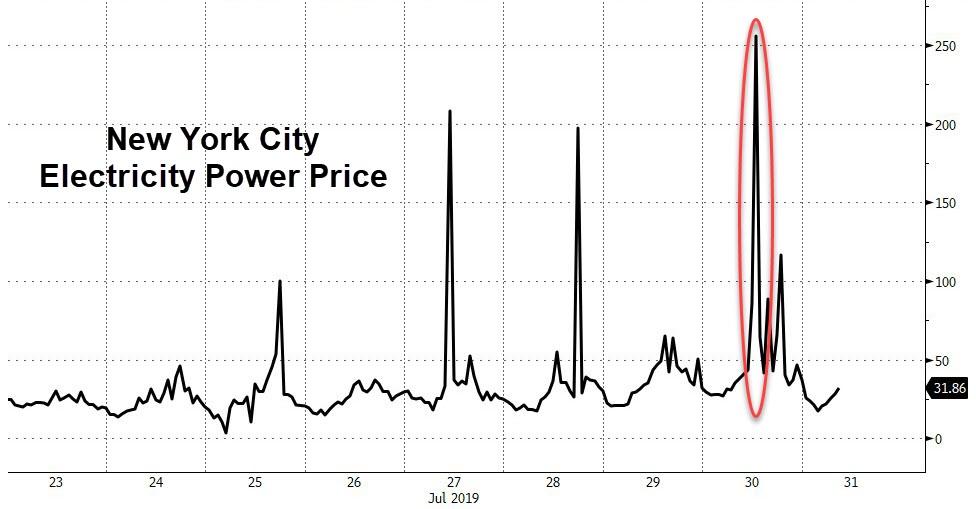

With the summer heat now becoming relentless, New Yorkers are putting their air conditioners to the test, driving demand for electricity to its highest so far this year, according to Bloomberg.

With temperatures steady in the 90’s and on some days approaching 100 Fahrenheit in New York City, electricity demand is estimated to reach 30,400 megawatts, according to the state’s grid operator. This would exceed demand from July 20 and 21, which were the two hottest days of the year so far.

The strain on the electric grid on those two days was tempered by the fact that they fell on a weekend, when office and factory buildings were idle and not using as much power as they would during the week.

Meanwhile, wholesale power prices in New York City nearly doubled on Tuesday this week to $62.57 per megawatt-hour, the highest price since February 25 (even higher intraday).

Power in New England, where there is also a heat advisory, spiked 41% to $51.45 per megawatt-hour.

Imagine what those prices would be if Enron was still randomly shutting down parts of the nation’s grid…

via ZeroHedge News https://ift.tt/2ysOYuK Tyler Durden

A damning new audit of improvements being made to New York City’s ailing subway system found that absentee workers, design flaws, and mistakes made during construction are delaying needed repairs and costing taxpayers and riders millions.

On Monday, New York State Comptroller Thomas P. DiNapoli published an audit of six capital projects being undertaken by the Metropolitan Transportation Authority (MTA)—the state-run transit agency responsible for most of New York City’s buses and trains—costing some $817 million.

All six of the examined projects were finished late, and four were finished overbudget. Cost overruns totaled $43.2 million.

“This audit found numerous problems in the MTA’s capital projects pipeline that led to delays and cost overruns,” said DiNapoli in a press release. “These are red flags that fall within the MTA’s power to fix.”

One driver of cost overruns were additional work orders, or AWOs, which ask contractors to perform work beyond the scope of their original agreements with MTA, often to fix mistakes made during construction or to rectify design flaws.

For example, MTA had to shell out $617,000 on AWOs for one project that was intended to make a subway station accessible to disabled people after it was discovered that the original design had omitted a necessary raising of the subway platform to allow passengers with wheelchairs to enter and exit trains. The New York Post identifies the project as the $21.7 million accessibility overhaul of the 23rd Street and Lexington Avenue station.

Manhattan Institute transportation scholar Nicole Gelinas has argued that these AWOs raise project costs significantly, writing that “the MTA has no leverage in negotiating these change orders; once it has awarded a contract, the winning bidder effectively holds the authority hostage.”

The MTA reported $731 million in change orders in 2018.

The state’s audit also uncovered rampant absenteeism, with large numbers of workers not showing up to work despite being paid to be there.

State auditors compared the number of workers showing up to job sites to contractor work schedules over a 15-day period for all six of the examined projects and found that contractors were short on staff by 29 percent on average.

Some job sites were worse than others. Auditors found that on one project workers were paid for working 378 days despite only showing for about half those days. This absenteeism is a major reason for project delays.

Currently, the MTA is nearing the end of a $33 billion, five-year capital improvement plan, which has cost roughly $3 billion more than projected. The next capital improvement plan is expected to cost $40 billion.

The MTA itself was largely dismissive of Monday’s audit, with an agency spokesperson telling the New York Post that the state comptroller “cherry-picked” examples and that the six projects examined were not representative of the over 2,000 capital projects currently underway.

Transit experts also criticized the report for not doing enough to root out the real causes of the MTA’s cost overruns.

“The DiNapoli audit is a dud because doesn’t aim squarely at the factors that cause high MTA construction costs,” said Ben Fried of TransitCenter to AM New York. “his report sheds a little light on project management but otherwise doesn’t get us any closer to understanding how to wrangle the MTA’s cost problem under control.”

New York City’s subway system, like many legacy transit systems, has experienced major performance problems and drops in ridership as a result of deferred maintenance. Fixing and improving the subway is going to be an expensive proposition. If taxpayers are going to be asked to foot the bill, the transit agency has a responsibility to get costs under control and deliver projects on time.

from Latest – Reason.com https://ift.tt/2YCOWiw

via IFTTT

Ten years ago, at the peak of the global financial crisis, the Board of Trustees which oversees Social Security in the United States issued a stark warning:

They projected that Social Security’s enormous trust funds would completely run out of money in 2039.

Naturally nobody paid attention. Back in 2009 the economy in shambles, so focusing on a future economic crisis that was more than three decades away was a low priority.

And for the past decade, the US government has continued to ignore its Social Security problem.

But it’s become much worse.

Ten years later, the Board of Trustees now projects that Social Security’s primary trust fund will run out money in 2034.

That’s five years earlier than they projected back in 2009. And it’s only 15 years away.

Now, 15 years might seem like a long time. But take a minute to grasp the magnitude of this problem:

According to the US government’s own estimates, Social Security and Medicare combined are underfunded by $100 TRILLION.

$100 trillion is literally more than FIVE TIMES the size of the entire US economy. And this giant fiscal chasm is actually growing.

The big problem for Social Security is that tax revenue is no longer enough.

Every worker who is legally employed in the United States currently pays roughly 15% of his/her wages each month to help fund Social Security and pay benefits to retirees.

But there are now so many people receiving Social Security benefits that all the payroll tax revenue is no longer enough.

Social Security also derives a portion of the income it needs to pay benefits from the investment returns on its $3 trillion worth of assets.

Problem is– Social Security is forbidden by law to invest in anything EXCEPT United States government bonds.

Most countries who have large Sovereign Wealth Funds or Pension Funds have the latitude to invest that capital in a variety of asset classes.

I personally know several national pension fund and sovereign wealth fund executives in Europe and Asia, and they typically buy a wide variety of assets– real estate, private equity, stocks, bonds, etc., with a target annualized return of between 6% to 8%.

(Norway’s sovereign wealth fund earned an average 7.6% between 2010 and 2017. And California’s state employee pension fund, CALPERS, earned 6.7% last year.)

But Social Security doesn’t have this investment freedom. Instead, Social Security is required BY LAW to invest in US government bonds, which yield less than 3%.

In fact Social Security’s investment return last year was 2.9%.

You’re probably starting to see the problem–

At the moment, Social Security is the #1 owner of US government debt, having spent years stockpiling $3 trillion of dollars worth of US Treasury bonds.

Month after month, as payroll tax revenues exceeded the total retirement benefits paid out, Social Security invested its surplus into government bonds.

But now that flow of money is about to reverse.

We know that Social Security’s payroll tax revenue is no longer sufficient to pay out benefits. There are simply too many retirees.

We also know that the 2.9% invest return is pitiful and not going to help at all.

This means that Social Security is about to start burning through the trust funds in order to meet its monthly benefit obligations.

The Board of Trustees has already acknowledged this fact. And they project the trust funds will be fully depleted in 15 years.

But it could likely come much sooner than that.

Before they can use the trust funds to cover their financial shortfall, Social Security will first have to convert its government bonds into cash.

Doing that will require that they either let the bonds mature (and demand the government to repay them in full). Or it will require them to dump tens of billions… hundreds of billions of dollars worth of bonds on the open market.

Either way, Uncle Sam loses its biggest lender. Instead of borrowing money from Social Security, the Treasury Department is going to have to pay Social Security back.

We’re talking $3 TRILLION. That’s not exactly pocket change. And it’s coming at a time when the US government is already losing more than $1 trillion per year.

The Congressional Budget Office already forecasts that the federal government will have to borrow $12.7 trillion in additional debt through the end of 2029.

Now, on top of that already-prodigious figure, the Treasury Department will have to find some sucker willing to lend an additional $3 trillion to repay Social Security… not to mention tens of trillions of dollars more down the road.

That’s extremely unlikely.

What’s far more likely is that the US government simply freezes the repayments to Social Security.

Maybe they pay back a trillion or two. But not the full amount. The rest of it would be frozen, which means that the trust funds would be effectively depleted MUCH earlier than expected.

Prudential, one of the largest financial institutions in the world, estimates that 86% of current retirees, 88% of baby boomers who are about to retire, and 71% of Gen-Xers, rely or expect to rely on Social Security when they retire.

But the Social Security trustees themselves tell us that the funds will run out of money in 15 years. And as I’ve just shown, it could happen a lot sooner than that.

So it’s clear that a LOT of people will have their lives turned upside down.

Look, maybe I’m totally wrong.

Maybe the Treasury Department does find a sucker to bail out Social Security. Maybe that sucker is us. Bank deposits, managed IRAs, etc. are all fair game for Uncle Sam. They could seize anything they want.

But even if I’m totally wrong, it certainly doesn’t hurt to have a Plan B… to take back control of your own retirement.

via ZeroHedge News https://ift.tt/2yuZzFq Tyler Durden

A damning new audit of improvements being made to New York City’s ailing subway system found that absentee workers, design flaws, and mistakes made during construction are delaying needed repairs and costing taxpayers and riders millions.

On Monday, New York State Comptroller Thomas P. DiNapoli published an audit of six capital projects being undertaken by the Metropolitan Transportation Authority (MTA)—the state-run transit agency responsible for most of New York City’s buses and trains—costing some $817 million.

All six of the examined projects were finished late, and four were finished overbudget. Cost overruns totaled $43.2 million.

“This audit found numerous problems in the MTA’s capital projects pipeline that led to delays and cost overruns,” said DiNapoli in a press release. “These are red flags that fall within the MTA’s power to fix.”

One driver of cost overruns were additional work orders, or AWOs, which ask contractors to perform work beyond the scope of their original agreements with MTA, often to fix mistakes made during construction or to rectify design flaws.

For example, MTA had to shell out $617,000 on AWOs for one project that was intended to make a subway station accessible to disabled people after it was discovered that the original design had omitted a necessary raising of the subway platform to allow passengers with wheelchairs to enter and exit trains. The New York Post identifies the project as the $21.7 million accessibility overhaul of the 23rd Street and Lexington Avenue station.

Manhattan Institute transportation scholar Nicole Gelinas has argued that these AWOs raise project costs significantly, writing that “the MTA has no leverage in negotiating these change orders; once it has awarded a contract, the winning bidder effectively holds the authority hostage.”

The MTA reported $731 million in change orders in 2018.

The state’s audit also uncovered rampant absenteeism, with large numbers of workers not showing up to work despite being paid to be there.

State auditors compared the number of workers showing up to job sites to contractor work schedules over a 15-day period for all six of the examined projects and found that contractors were short on staff by 29 percent on average.

Some job sites were worse than others. Auditors found that on one project workers were paid for working 378 days despite only showing for about half those days. This absenteeism is a major reason for project delays.

Currently, the MTA is nearing the end of a $33 billion, five-year capital improvement plan, which has cost roughly $3 billion more than projected. The next capital improvement plan is expected to cost $40 billion.

The MTA itself was largely dismissive of Monday’s audit, with an agency spokesperson telling the New York Post that the state comptroller “cherry-picked” examples and that the six projects examined were not representative of the over 2,000 capital projects currently underway.

Transit experts also criticized the report for not doing enough to root out the real causes of the MTA’s cost overruns.

“The DiNapoli audit is a dud because doesn’t aim squarely at the factors that cause high MTA construction costs,” said Ben Fried of TransitCenter to AM New York. “his report sheds a little light on project management but otherwise doesn’t get us any closer to understanding how to wrangle the MTA’s cost problem under control.”

New York City’s subway system, like many legacy transit systems, has experienced major performance problems and drops in ridership as a result of deferred maintenance. Fixing and improving the subway is going to be an expensive proposition. If taxpayers are going to be asked to foot the bill, the transit agency has a responsibility to get costs under control and deliver projects on time.

from Latest – Reason.com https://ift.tt/2YCOWiw

via IFTTT

Rep. Alexandria Ocasio-Cortez (D-NY) jumped into action after a New York Times editor slammed AOC’s progressive Democrat ‘Squadmates’ Rashida Tlaib (D-MI) and Ilhan Omar (D-MN) as not representative of the Midwest.

In a now-deleted tweet, New York Times deputy Washington editor Jonathan Weisman responded to a comment by Justice Democrats spokesman Waleed Shahid – who was opining on a debate comment made by 2020 Democratic candidate Claire McCaskill (D-MO) that “free stuff from the government doesn’t play well in the Midwest.”

Weisman replied, suggesting that saying Tlaib and Omar are from the Midwest “is like saying @RepLloydDoggett (D-Austin) is from Texas or @repjohnlewis (D-Atlanta) is from the Deep South” (which they are).

AOC had her girls’ backs, tweeting that her colleagues “literally are” Midwestern. While Tlaib was born in Detroit, Michigan, Omar was born in Mogadishu, Somalia but was brought to Minnesota as a child.

They literally are, &this comment is what erasure looks like. HIGH TURNOUT from DEEP BLUE SEATS &being competitive everywhere is the core of a winning strategy.

It’s disturbing to see this Trump talking pt that dense, diverse communities “aren’t the REAL [America/Midwest/etc].” https://t.co/S97RillWbU

Shahid, meanwhile, responded “The people who shape our national conversation should be telling the story of how we are all Americans, not repeating Trump’s racism. They do us all a disservice when they echo Trump’s dog whistles that tell us some people are more ‘American’ or ‘Midwestern’ than others — that our lives and our votes matter less than others,” adding “We must change the idea that people of color can’t exemplify the region — or the nation — in which we live.”

To which Weisman, choosing this hill to die on before deleting his tweet, replied “[P]lease don’t tell me that Atlanta is synonymous with Georgia. It isn’t.”

via ZeroHedge News https://ift.tt/2ysCdAA Tyler Durden

If the two-plus years of President Donald Trump’s tenure have taught us anything, it’s that even a scandal-plagued, generally incompetent chief executive who lacks strong congressional allies can have tremendous influence over trade policy.

That’s all the more reason for Democrats to focus on exactly that issue.

Former congressmen Beto O’Rourke of Texas and John Delaney of Maryland are both struggling with fundraising and in the polls, but both did their part during Tuesday’s primary debate in Detroit to highlight an important schism in the Democratic field. On one side are candidates who recognize the value of international trade, and on the other, those who dismiss it as a tool of capitalists bent on hollowing out the American working class.

The latter camp is where you can find frontrunners like Sens. Bernie Sanders (I–Vt.) and Elizabeth Warren (D–Mass.), the two highest-polling candidates to participate Tuesday night. They are pitching protectionist trade policies that effectively mirror much of what Trump has done. Sanders on Tuesday bragged of his track record in opposing the North American Free Trade Agreement (NAFTA) and other trade deals. He railed against corporations for trying to “save five cents by going to China, Mexico, or Vietnam, or anyplace else, that’s exactly what they will do” and bizarrely tried to blame Detroit’s economic depression on Trump-era trade policies.

Meanwhile, in a policy paper unveiled this week, Warren effectively rules out signing trade deals with developing nations until they adopt American standards for labor laws, environmental rules, and more. On Tuesday night, she defended that stance. “People want access to our markets all around the world,” she said. “Then the answer is, let’s make them raise their standards.”

That sounds a lot like Trump, doesn’t it? Warren is seeking progressive ends rather than chasing a supposedly unfair trade balance, but the fundamental thought process is the same: use America’s collective economic might to force other nations to change their behavior.

Like Trump, she misses the big picture. Trade is not conducted country-to-country but by the individual choices of millions of people along complex supply chains that stretch around the world. Governments can’t dictate the demands of consumers, all they can do is determine how easy or difficult it will be for goods to pass across national borders. Clearly, Warren and Sanders (like Trump) seek to make it more difficult.

But Democrats don’t have to settle for Trumpism wrapped in progressive rhetoric. Delaney attacked Warren’s trade policies from a position many Democrats held just a few years ago. He pointed out the Obama administration’s efforts to open up greater trade through the ill-fated Trans-Pacific Partnership (Trump yanked America out of the TPP shortly after being inaugurated), and called for Democrats to oppose those who want to “build economic walls.”

Warren’s plan, he said, “would prevent the United States from trading with its allies. We can’t go and—we can’t isolate ourselves from the world.”

Delaney’s right. Cutting off trade is not the way to improve labor standards and working conditions in developing countries. Indeed, the United States puts trade embargoes on countries as a way to punish them, not help them. Warren’s plan relies on magical thinking and fundamentally misunderstands how trade works.

Beto jumped into the fray to make another important point that hits closer to home. Tariffs, he said, “are a huge mistake” that “constitute the largest tax increase on the American consumer, hitting the middle class and the working poor especially hard.”

“When have we ever gone to war, including a trade war, without allies and friends and partners?” O’Rourke asked, nodding towards both the TPP (envisioned as a way to counteract China’s economic rise) and Trump’s trade isolationism.

Trade policy should be a central concern for Democratic primary voters—for both political and practical reasons.

Politically, whichever candidate wins the primary will have an opportunity to hit one of Trump’s obvious weaknesses by stressing how tariffs are harming Americans more than they are helping—exactly the type of argument O’Rourke deployed Tuesday night.

But Warren can’t make that case when her own trade policy paper says “tariffs are an important tool” as part of a “broader strategy” to reshape global trade. Sanders can’t, either, given his longstanding hostility to trade deals like NAFTA and TPP, which are predicated on lowering tariffs and easing cross-border trade.

It’s worth noting, too, that most Democratic voters seem to side with O’Rourke and Delaney. Polling data released this week by the Pew Research Center shows that 65 percent of Americans—and majorities of both Democrats (73 percent) and Republicans (59 percent)—say that signing free trade agreements is a good thing. Among Democrats, that figure is the highest since Pew started asking about trade in 2009.

Practically, trade matters more than other policies because it’s an area where the president can make an immediate impact regardless of other political considerations.

In other words, a victorious Democrat taking office in January 2021 will struggle to implement Medicare for All or any other national health care plan unless voters also hand Democrats a veto-proof majority in the Senate; yet that outcome seems highly unlikely given the Senate seats in play in 2020. But thanks to a decades-long trend of Congress handing unilateral trade authority to the president—a trend that has not been reversed during Trump’s tenure, even as he has abused those powers—a future President Warren or President O’Rourke will have the power to reshape how the world’s largest economy deals with every other nation on the planet, and he or she will be able to do it with limited congressional oversight.

Democratic voters, even if they aren’t inclined to vote for O’Rourke or Delaney, should demand better than Warren’s trade policy of warmed-over Trump-style protectionism with a veneer of magical progressive thinking and the promise of being executed in a less incompetent way.

from Latest – Reason.com https://ift.tt/2YCLWmg

via IFTTT

If the two-plus years of President Donald Trump’s tenure have taught us anything, it’s that even a scandal-plagued, generally incompetent chief executive who lacks strong congressional allies can have tremendous influence over trade policy.

That’s all the more reason for Democrats to focus on exactly that issue.

Former congressmen Beto O’Rourke of Texas and John Delaney of Maryland are both struggling with fundraising and in the polls, but both did their part during Tuesday’s primary debate in Detroit to highlight an important schism in the Democratic field. On one side are candidates who recognize the value of international trade, and on the other, those who dismiss it as a tool of capitalists bent on hollowing out the American working class.

The latter camp is where you can find frontrunners like Sens. Bernie Sanders (I–Vt.) and Elizabeth Warren (D–Mass.), the two highest-polling candidates to participate Tuesday night. They are pitching protectionist trade policies that effectively mirror much of what Trump has done. Sanders on Tuesday bragged of his track record in opposing the North American Free Trade Agreement (NAFTA) and other trade deals. He railed against corporations for trying to “save five cents by going to China, Mexico, or Vietnam, or anyplace else, that’s exactly what they will do” and bizarrely tried to blame Detroit’s economic depression on Trump-era trade policies.

Meanwhile, in a policy paper unveiled this week, Warren effectively rules out signing trade deals with developing nations until they adopt American standards for labor laws, environmental rules, and more. On Tuesday night, she defended that stance. “People want access to our markets all around the world,” she said. “Then the answer is, let’s make them raise their standards.”

That sounds a lot like Trump, doesn’t it? Warren is seeking progressive ends rather than chasing a supposedly unfair trade balance, but the fundamental thought process is the same: use America’s collective economic might to force other nations to change their behavior.

Like Trump, she misses the big picture. Trade is not conducted country-to-country but by the individual choices of millions of people along complex supply chains that stretch around the world. Governments can’t dictate the demands of consumers, all they can do is determine how easy or difficult it will be for goods to pass across national borders. Clearly, Warren and Sanders (like Trump) seek to make it more difficult.

But Democrats don’t have to settle for Trumpism wrapped in progressive rhetoric. Delaney attacked Warren’s trade policies from a position many Democrats held just a few years ago. He pointed out the Obama administration’s efforts to open up greater trade through the ill-fated Trans-Pacific Partnership (Trump yanked America out of the TPP shortly after being inaugurated), and called for Democrats to oppose those who want to “build economic walls.”

Warren’s plan, he said, “would prevent the United States from trading with its allies. We can’t go and—we can’t isolate ourselves from the world.”

Delaney’s right. Cutting off trade is not the way to improve labor standards and working conditions in developing countries. Indeed, the United States puts trade embargoes on countries as a way to punish them, not help them. Warren’s plan relies on magical thinking and fundamentally misunderstands how trade works.

Beto jumped into the fray to make another important point that hits closer to home. Tariffs, he said, “are a huge mistake” that “constitute the largest tax increase on the American consumer, hitting the middle class and the working poor especially hard.”

“When have we ever gone to war, including a trade war, without allies and friends and partners?” O’Rourke asked, nodding towards both the TPP (envisioned as a way to counteract China’s economic rise) and Trump’s trade isolationism.

Trade policy should be a central concern for Democratic primary voters—for both political and practical reasons.

Politically, whichever candidate wins the primary will have an opportunity to hit one of Trump’s obvious weaknesses by stressing how tariffs are harming Americans more than they are helping—exactly the type of argument O’Rourke deployed Tuesday night.

But Warren can’t make that case when her own trade policy paper says “tariffs are an important tool” as part of a “broader strategy” to reshape global trade. Sanders can’t, either, given his longstanding hostility to trade deals like NAFTA and TPP, which are predicated on lowering tariffs and easing cross-border trade.

It’s worth noting, too, that most Democratic voters seem to side with O’Rourke and Delaney. Polling data released this week by the Pew Research Center shows that 65 percent of Americans—and majorities of both Democrats (73 percent) and Republicans (59 percent)—say that signing free trade agreements is a good thing. Among Democrats, that figure is the highest since Pew started asking about trade in 2009.

Practically, trade matters more than other policies because it’s an area where the president can make an immediate impact regardless of other political considerations.

In other words, a victorious Democrat taking office in January 2021 will struggle to implement Medicare for All or any other national health care plan unless voters also hand Democrats a veto-proof majority in the Senate; yet that outcome seems highly unlikely given the Senate seats in play in 2020. But thanks to a decades-long trend of Congress handing unilateral trade authority to the president—a trend that has not been reversed during Trump’s tenure, even as he has abused those powers—a future President Warren or President O’Rourke will have the power to reshape how the world’s largest economy deals with every other nation on the planet, and he or she will be able to do it with limited congressional oversight.

Democratic voters, even if they aren’t inclined to vote for O’Rourke or Delaney, should demand better than Warren’s trade policy of warmed-over Trump-style protectionism with a veneer of magical progressive thinking and the promise of being executed in a less incompetent way.

from Latest – Reason.com https://ift.tt/2YCLWmg

via IFTTT