The Trump administration’s new “public charge” rule for immigrants is an attempt to massively cut legal immigration, under the guise of constraining welfare spending. I was thinking of writing a more detailed post on this subject. But David Bier of the Cato Institute has already published an excellent analysis that I cannot hope to improve on. Reason’s Shikha Dalmia has helpfully expanded on Bier’s analysis (see also her discussion of an earlier version of the proposal). As they explain, the new rule would massively cut legal immigration, including by excluding large numbers of people who are net-positive fiscal contributors to the treasury. It does not exclude people based on actual use of welfare benefits, but merely based on a skewed bureaucratic determination that they are likely to use them for pover 12 months during a 3 year period. In addition, the rule would cruelly separate large numbers of American citizens from parents, children, and other relatives.

As Shikha notes, this rule is also a massive executive power grab (unilaterally imposing a major change in immigration policy, unauthorized by Congress), of a sort that Republicans would surely have condemned had a Democratic administration done it. The rule is also, of course, just the latest front in the Trump administration’s longstanding effort to cut legal immigration as much as it possibly can—a record that gives the lie to oft-heard claims that the administration only objects to illegal immigration.

I would add that the administration’s plan to massively restrict immigration based on bureaucratic determinations about potential future welfare usage is based on reasoning similar to that of early 20th century eugenics advocates, who argued that we must use the power of the state to preclude people from having children, if government experts determined that they were likely to become dependent on welfare.

As Justice Oliver Wendell Holmes put it in Buck v. Bell (the notorious 1927 Supreme Court decision upholding mandatory sterilization laws for those deemed mentally unfit), many advocated such measures in order to prevent “those who already sap the strength of the State” from having “socially inadequate offspring” who are likely to become a fiscal burden. For many potential immigrants being forcibly condemned to a lifetime of poverty and oppression in Third World societies (and separated from close family members in the US, to boot), is an imposition comparable in magnitude to the mandatory sterilization once defended by Holmes and others.

The Trump administration’s new “public charge” rule for immigrants is an attempt to massively cut legal immigration, under the guise of constraining welfare spending. I was thinking of writing a more detailed post on this subject. But David Bier of the Cato Institute has already published an excellent analysis that I cannot hope to improve on. Reason’s Shikha Dalmia has helpfully expanded on Bier’s analysis (see also her discussion of an earlier version of the proposal). As they explain, the new rule would massively cut legal immigration, including by excluding large numbers of people who are net-positive fiscal contributors to the treasury. It does not exclude people based on actual use of welfare benefits, but merely based on a skewed bureaucratic determination that they are likely to use them for pover 12 months during a 3 year period. In addition, the rule would cruelly separate large numbers of American citizens from parents, children, and other relatives.

As Shikha notes, this rule is also a massive executive power grab (unilaterally imposing a major change in immigration policy, unauthorized by Congress), of a sort that Republicans would surely have condemned had a Democratic administration done it. The rule is also, of course, just the latest front in the Trump administration’s longstanding effort to cut legal immigration as much as it possibly can—a record that gives the lie to oft-heard claims that the administration only objects to illegal immigration.

I would add that the administration’s plan to massively restrict immigration based on bureaucratic determinations about potential future welfare usage is based on reasoning similar to that of early 20th century eugenics advocates, who argued that we must use the power of the state to preclude people from having children, if government experts determined that they were likely to become dependent on welfare.

As Justice Oliver Wendell Holmes put it in Buck v. Bell (the notorious 1927 Supreme Court decision upholding mandatory sterilization laws for those deemed mentally unfit), many advocated such measures in order to prevent “those who already sap the strength of the State” from having “socially inadequate offspring” who are likely to become a fiscal burden. For many potential immigrants being forcibly condemned to a lifetime of poverty and oppression in Third World societies (and separated from close family members in the US, to boot), is an imposition comparable in magnitude to the mandatory sterilization once defended by Holmes and others.

Today’s insanity was brought to you by the words “delay” and “protests” and by the number “0” as Trump blinked and ‘delayed’ some China tariffs, Hong Kong ‘protests’ in the airport escalated, and all eyes were on the UST curve’s 2s10s spread rapidly plunging toward ‘0’…

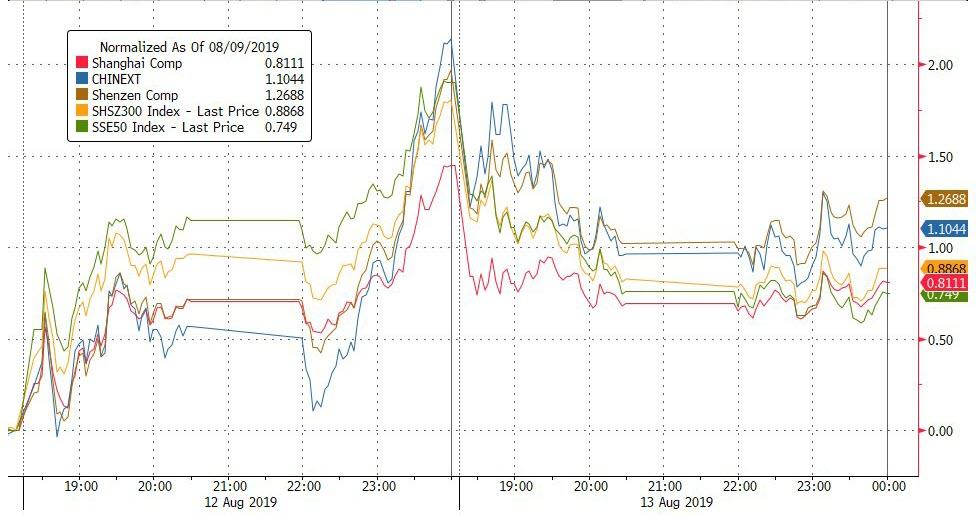

Chinese stocks leaked lower on the day but held gains on the week…

Source: Bloomberg

European stocks surged on the trade headlines but Spain remains red on the week…

Source: Bloomberg

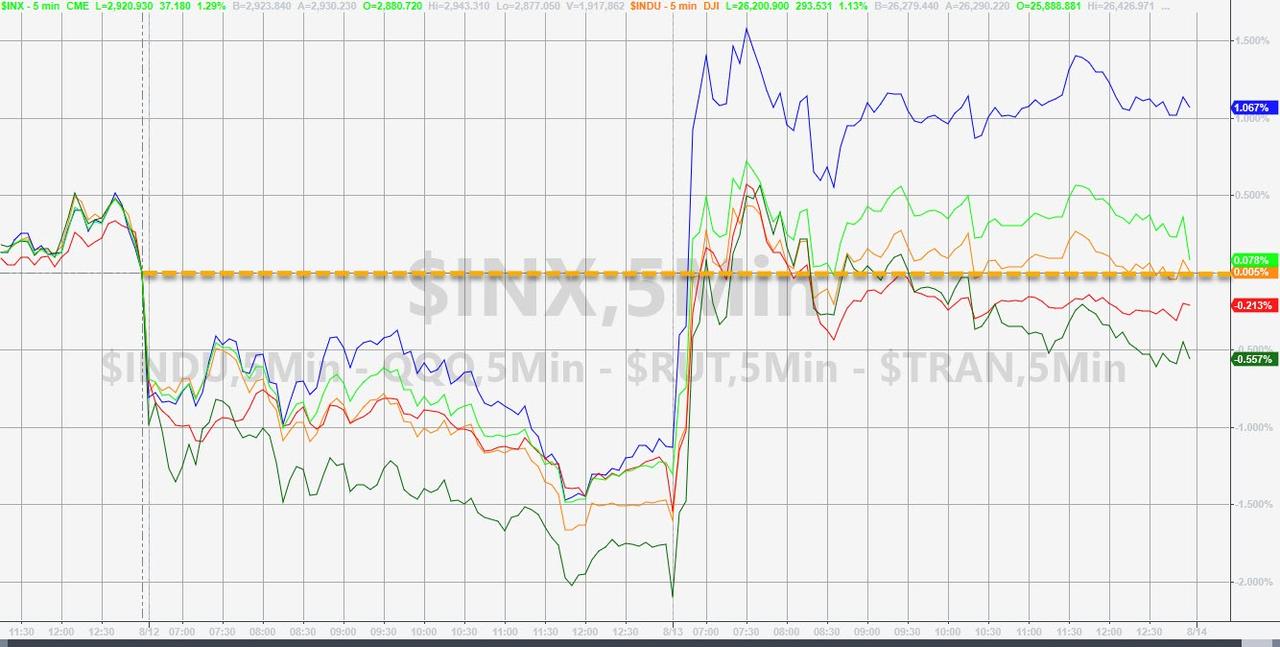

A big day for US equities thanks to trade headlines rescuing another ugly overnight session…

However, The Dow, Small Caps, and Trannies were unable to erase yesterday’s losses (weak close)…

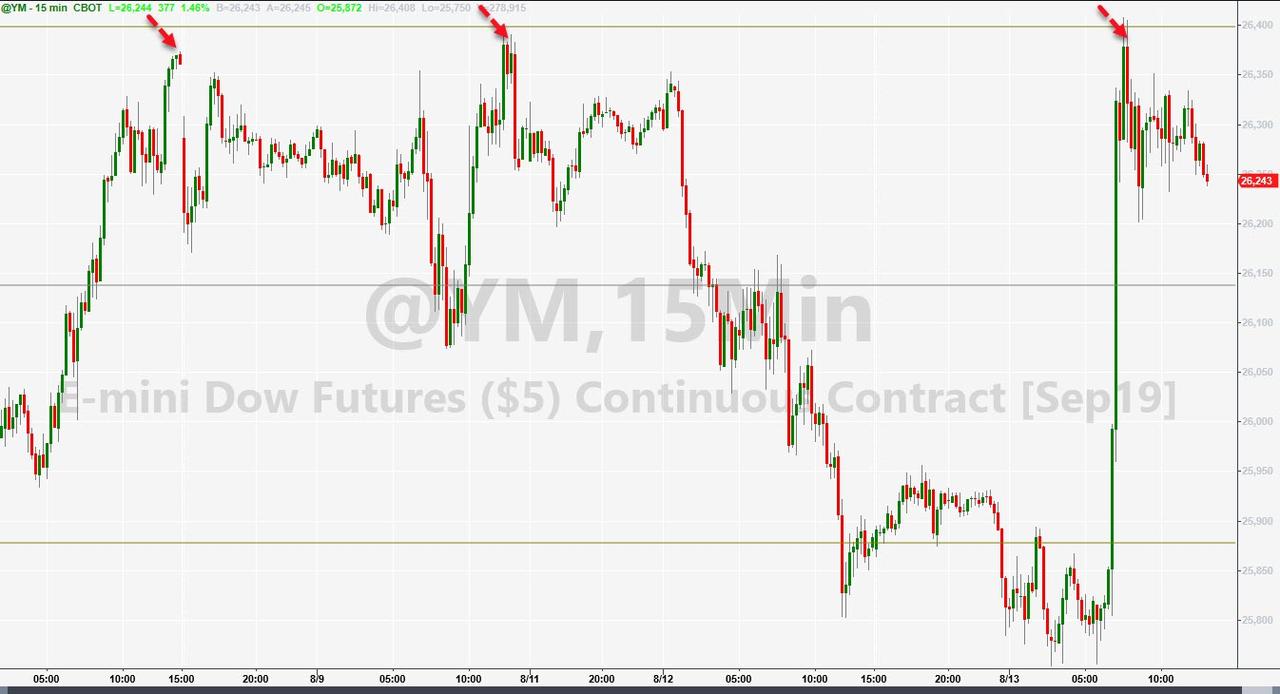

But we note that, stocks were unable to break key resistance levels (Dow futs stalled at the Fib 61.8% retracement level of the July/Aug plunge)

Close-Up…

And all the majors stalled at or below key technical levels…

AAPL was a big driver of markets today, but look where it stalled…

Cyclicals outperformed, as you’d expect, today; but since Friday, Defensives are leading…

Source: Bloomberg

Stocks, as always, more excited than bonds about everything…

Source: Bloomberg

As StanChart’s Steve Englander noted: “The key characteristic of recent episodes of risk-off and risk-rebound is that the equity-market consequences are largely reversed, while the downward moves in fixed income have largely stayed in place.”

Treasury yields were all notably higher on the day, spiking after the trade headlines (but the long-end dramatically outperformed the short-end) – also note that all yields slipped lower in the last hour (only 2Y is higher in yield on the week)…

Source: Bloomberg

But the yield curve refused to stop flattening, with 2s10s falling below 1bps for the first time since May 2007…

Source: Bloomberg

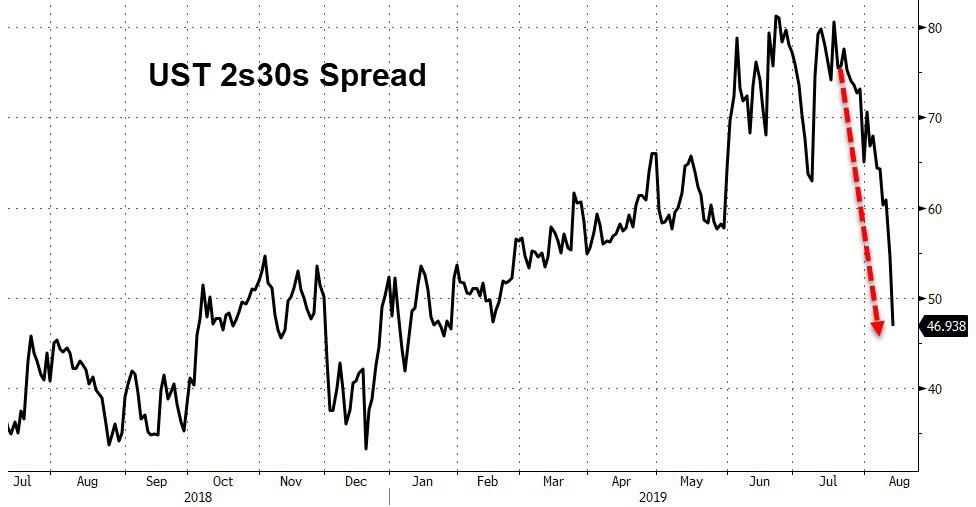

And 2s30s crashed to its lowest levels of 2019…

Source: Bloomberg

The Dollar managed gains on the day but remains within a very narrow range since The Fed cut rates…

Source: Bloomberg

The Yuan exploded higher on the trade headlines, surging below 7.0/USD before fading back to the CNY Fix…

Source: Bloomberg

The Hong Kong Dollar was relatively volatile intraday but remains a few pips away from the 7.85 weak-end of the USD peg band…

Source: Bloomberg

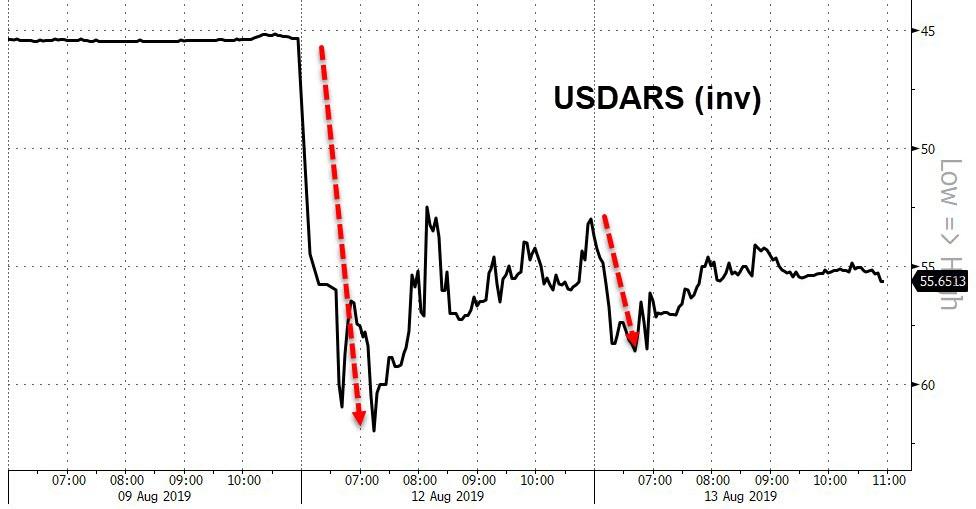

The Argentine Peso did not stop its freefall…

Source: Bloomberg

In cryptos, Bitcoin tumbled on the day as Bitcoin Cash soared…

Source: Bloomberg

Bitcoin fell back below $11,000…

Source: Bloomberg

Oil spiked on the trade headlines (as did copper) and PMs (safe havens) tumbled…

Source: Bloomberg

Gold futures tumbled buyt bounced off $1500…

WTI Crude ramped up to $57 handle ahead of tonight’s API inventory data…

Finally, some context for the headlines today, the market-implied odds of a trade deal initially spiked but faded back as the day wore on…

And Bloomberg’s Tom Orlik explains why: Tariffs are not the only, or perhaps even the main drag from the U.S.-China trade war. That prize goes to head-spinning policy uncertainty.

A gauge of trade policy uncertainty in the U.S. is at levels not seen since Nafta ratification in the 1990s. China and Europe face a similar problem.

via ZeroHedge News https://ift.tt/2Twl6Yf Tyler Durden

Mere hours after President Trump tweeted that US intelligence had confirmed the buildup of Chinese troops on the border with Hong Kong, US defense officials warned that Beijing had refused two US Navy ships permission to make port stops in Hong Kong in the coming weeks, a sign that President Xi is none too pleased with how the US has handled itself during the anti-extradition bill protests that have swept Hong Kong over the past ten weeks.

BREAKING: We just got news China is refusing to grant US Navy ships entry into Hong Kong. We’re watching market reaction NOW @ClamanCountdown

Beijing has repeatedly warned the US to stop interfering with Taiwan and Hong Kong, or else face consequences, including the implicit threat of force.

Meanwhile, China confirmed that it denied the requests made by the US Navy.

Commander Christensen, Deputy Spokesperson, US Pacific Fleet: The Chinese Government denied requests for port visits to Hong Kong by the USS Green Bay and USS Lake Erie, which were scheduled to arrive in the next few weeks.

Three Chinese Navy ships arrived in San Diego as part of a routine port visit that will last from December 6 to 9.

Two Jiangkai II-class frigates Yancheng (FFG 546) and Daqing (FFG 576), and the Fuchi-class oiler Tai Hu (AOR 889) were hosted by the U.S. Navy destroyer USS Cape St. George (CG 71) in San Diego, where sailors from both navies will participate in sporting events and cultural exchanges.

“Practical cooperation, such as port visits and key leader engagements, helps us enhance transparency and mitigate risks when we operate at sea,” said Rear Adm. James S. Bynum commander, Carrier Strike Group Nine.

“Continuous dialogue is necessary to find where we share interests and also to address disagreements candidly if they arise.”

A spokesman for Beijing warned that they’re worried the presence of US ships might embolden protesters, meanwhile, US officials have warned that they prefer not to make shipfall in areas where unrest is brewing.

via ZeroHedge News https://ift.tt/2yVMkxV Tyler Durden

First it was Amazon. Then Apple. Now, to nobody’s surprise, not only was the biggest privacy violator in history, Facebook, also listening in to everything you were dumb enough to say in its proximity, but it also was just as busy writing it all down.

According to Bloomberg, the company which has faced Congressional hearings for virtually every possible and impossible violation of user privacy (and gotten away with it with just a wristslap), Facebook was not only secretly collecting user audio without their knowledge or permission, but was paying “hundreds of outside contractors to transcribe clips of audio from users of its services.” Facebook – and Mark Zuckerberg – also appear to have forgotten to mention this minor detail during their countless sworn testimonies in Congress over the past year.

The work, as Bloomberg notes, “rattled the contract employees”, who are not told where the audio was recorded or how it was obtained — only to transcribe it, said the people, who requested anonymity for fear of losing their jobs.

They’re hearing Facebook users’ conversations, sometimes with vulgar content, but do not know why Facebook needs them transcribed, the people said.

Here’s a lucky guess “why” – because in its attempt to cozy with the government, and replace the NSA, Facebook ran out of in house spies and was forced to hire outside privacy violators in its quest to make a mockery of user privacy.

When approached by Bloomberg, Facebook confirmed that it had been transcribing users’ audio and said it will no longer do so, because somehow that will make it all better.

“We paused human review of audio more than a week ago,” the company said Tuesday. The company said the users who were affected chose the option in Facebook’s Messenger app to have their voice chats transcribed. The contractors were checking whether Facebook’s artificial intelligence correctly interpreted the messages, which were anonymized.

Of course, Facebook can just plead ignorance, and claim all other big tech companies – including Amazon and Apple – were doing the same. Indeed, all three tech giants have recently come under fire for collecting audio snippets from consumer computing devices and subjecting those clips to human review.

Bloomberg first reported in April that Amazon had a team of thousands of workers around the world listening to Alexa audio requests with the goal of improving the software, and that similar human review was used for Apple’s Siri and Alphabet Inc.’s Google Assistant. Apple and Google have since said they no longer engage in the practice and Amazon said it will let users opt out of human review.

Now it’s Facebook’s turn to say it, too, paused the practice following scrutiny of other technology companies’ audio-collection programs.

Which is odd, because the social networking giant which claims it has over 2 billion monthly active users, just completed a $5 billion settlement with the U.S. Federal Trade Commission after a probe of its privacy practices; it has long denied that it collects audio from users to inform ads or help determine what people see in their news feeds. Chief Executive Officer Mark Zuckerberg denied the idea directly in Congressional testimony.

“You’re talking about this conspiracy theory that gets passed around that we listen to what’s going on on your microphone and use that for ads,” Zuckerberg told U.S. Senator Gary Peters in April 2018. “We don’t do that.”

Apparently “we” did.

In follow-up answers for Congress, the company said it “only accesses users’ microphone if the user has given our app permission and if they are actively using a specific feature that requires audio (like voice messaging features.)” The Menlo Park, California-based company did not address what happens to the audio afterward. Now we know: it was all dutifully transcribed and collected.

Some more lies: the Facebook data-use policy, revised last year to make it “more understandable” for the public, includes no mention of audio according to Bloomberg. It does, however, say Facebook will collect “content, communications and other information you provide” when users “message or communicate with others.”

Facebook says its “systems automatically process content and communications you and others provide to analyze context and what’s in them.” It includes no mention of other human beings screening the content. In a list of “types of third parties we share information with,” Facebook doesn’t mention a transcription team, but vaguely refers to “vendors and service providers who support our business” by “analyzing how our products are used.”

Worse, Facebook never disclosed to users that third parties may review their audio. That’s led some contractors to feel their work is unethical, according to the people with knowledge of the matter.

Unethical yes, but criminal? Well, that’s up to Congress to decide. And judging by the non-existent reaction in the stock price following the Bloomberg news…

… nobody will be losing much sleep over yet another flagrant violation of personal privacy by the company which hopes to soon control not only all global media, but also money, thanks to its Libra initiative.

via ZeroHedge News https://ift.tt/2MdR2zG Tyler Durden

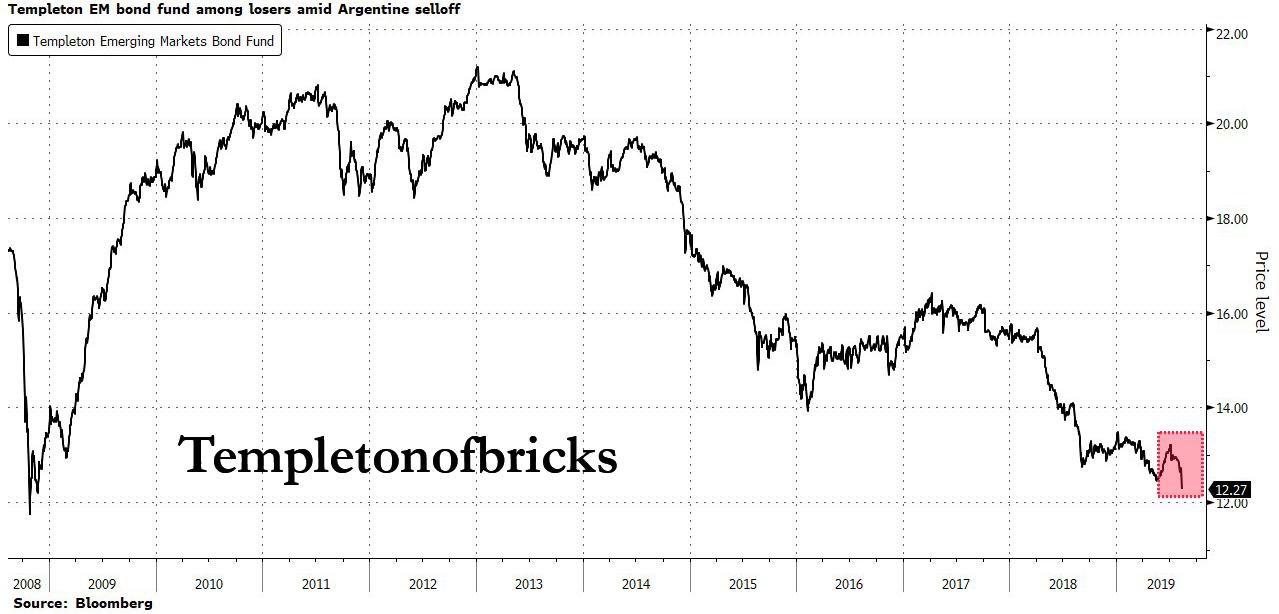

Yesterday, in the immediate aftermath of the historic collapse of all Argentine assets, coupled with the record plunge in the Argentine Peso which only added to the USD-denominated pain of those who were unlucky enough to be long Argentina stocks and bonds, we asked if Michael Hasenstab – the man who may have bought every single sovereign bond dip in history in hopes of being bailed out by central banks – was on Epsteinwatch, for the simple reason that this time a bailout was not forthcoming, resulting in unprecedented losses.

As a reminder, back in May 2018, when it was on the verge of the biggest ever IMF bailout in history (some $57 billion and counting in money that will never be recovered), Argentina received a “vote of confidence” from Franklin Templeton’s Michael Hasenstab after he injected $2.25 billion into the country, which has been battling to save its currency. As the Financial Times reported then, funds run by Hasenstab, including his flagship $38 billion Templeton Global Bond fund, snapped up more than three quarters of a 73 billion peso ($3 billion) ‘Bote’ bond issuance by Argentina in May 2018. .

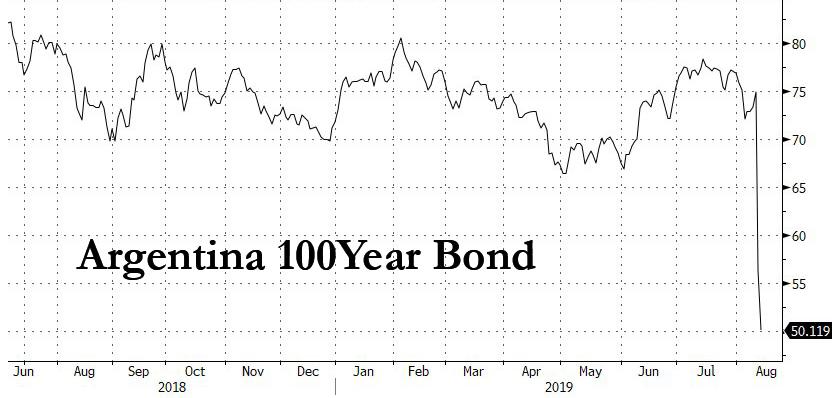

The purchase reportedly made the asset manager Argentina’s single largest creditors, with holdings in most Argentina bond securities, including the country’s infamous 100 year bond due 2117, which has been eviscerated in the past two days as it now appears the country’s market-friendly regime is on its way out, and will be replaced with the second coming of Cristina Kirchner.

Following the $3 billion issuance, Luis Caputo, Argentina’s finance minister and former central bank president, told Bloomberg: “You can’t get a bigger sign of confidence from markets when you place a bond in pesos at a fixed-rate on one of the worst days in emerging markets this year. It is a sign of confidence in president Macri, and the policies he is putting in place.”

A little over one year later, that “sign of confidence” has come back to haunt both Hasenstab and Templeton, because as we first suggested yesterday…

…. today Bloomberg confirms that the record crash in Argentine assets is “wreaking “havoc on some of the largest U.S. money managers, but none more so than Hasenstab’s employer, the $720 billion mutual fund, Franklin Templeton. According to Bloomberg calculations, the biggest loser was the $11.3 billion Templeton Emerging Markets Bond Fund, which fell by 3.5%, a drop that has continued on Tuesday as the selling was nowhere near done. That was its largest daily drop since the October 2008 global financial crisis.

What is perhaps surprising is that the fund’s loss wasn’t even bigger: The Templeton fund had a 12% allocation to Argentina as of June 30, including Treasury bonds and notes linked to the nation’s benchmark rate. As discussed yesterday, Argentine stocks (denominated in USD) lost more than half their value in one day – an unprecedented event – while sovereign and corporate bonds erased $16.8 billion of their value in the Bloomberg Barclays emerging-market index on Monday.

The plunge “shows the painful and long-lasting impact of Argentina’s belligerent treatment of creditors,” said Mike Conelius, a money manager at T. Rowe Price , whose $5.8 billion emerging-market bond fund slumped by 2.2% on Monday, the most in six years. Over 7% of the T. Rowe portfolio was exposed to the country.

To be sure, Templeton wasn’t the only one hammered this week by Argentina’s spectacular implosion: other large funds also suffered, such as the $7.5 billion Ashmore Emerging Markets Short Duration Fund which fell by 3.2%, while the $1.4 billion Fidelity Series Emerging Markets Debt Fund dropped by 3.1%.

Meanwhile, we wonder if for Hasenstab who may have lost more money in one day than he made over the past decade with all his prior, haphazard bets on central bank bailouts, will finally face the proverbial “swimming naked when the tide runs out” moment, or if investors are dumb enough to keep giving him more money.

via ZeroHedge News https://ift.tt/2YJdCqw Tyler Durden

Submitted by Steve Englander, Head, Global G10 FX Research and North America Macro Strategy at Standard Chartered Bank

Currency wars are likely to be won by the countries that can afford the consequences

DM economies are likely to have an advantage over EM

In DM, inflation rates are lower, bond issuance is domestic, and bond yields are less likely to back up

If both the Fed and Treasury want to weaken the USD, we think they are likely to succeed …

… except if the consequent risk-off response generates buying of USD along with other safe havens

Riding the horse is easy, affording the stable is hard

Most analysis of currency wars begins and ends with the view that the country that depreciates the most wins. We argue here that the likely winner is the country that can best handle the consequences of depreciation. A wealthy economy with a current account deficit, low inflation, a flat Phillips curve, room to cut policy rates, long-term rates that track policy rates down, and local currency-denominated debt is at an advantage in winning a currency war, in our view. Keeping in mind that ‘victory’ in a currency war is a sustained weaker currency, our conclusions are:

Developed-market (DM) economies in general have an advantage over emerging-market (EM) economies in dealing with the consequences of currency weakness

The US would likely have an advantage over other DM economies if it aggressively pursued currency depreciation, but not under all circumstances

The USD, JPY, CHF and possibly EUR are safe-haven currencies; a currency war that led to risk selling would likely cause them to strengthen

Currency weakness is often associated with poor outcomes in EM, making it harder for EM policy makers to commit fully to aggressive easing

EM currencies tend to fall in a strongly risk-off environment, but this is hardly a currency war victory because EM asset markets and economies are damaged

Domestic markets are more forgiving when DM currencies depreciate

DM investors tolerate easing better than EM

We define winning a currency war as successfully weakening one’s currency to induce a pick-up in net exports, without significant negative inflation or domestic asset-market consequences. Developed economies have an advantage because their bond markets generally respond favourably to monetary easing, even when the currency weakens.

In EM countries, easing at the short end does not always translate into lower long-term yields (Figure 1). EM rates do not always back up on easing, but this risk creates a headwind to aggressive easing. Winning a currency war that pushes inflation to unacceptable levels, drives up long-term rates, damages business confidence, disturbs financial markets and financial institutions, or leads to undesired capital outflows is a pyrrhic victory.

DM economies do not face the issues of long-term credibility that many EM economies face. Long-term DM yields rarely go in the opposite direction to short-term yields in response to policy moves, even when the currency drops. EM countries face the risk that policy easing and currency weakness will backfire if long-term yields rise. On 7 August, New Zealand and India cut policy rates more than expected; New Zealand’s 10Y yields fell and India’s 10Y yields rose.

We think this phenomenon makes it more difficult for EM countries to maintain weak currencies than for DM countries. As a result, we think that currency wars are broadly a long EM, short DM currency trade unless risk sells off sharply. Like polo, the issue is not whether you can ride the horse, but whether you can afford the upkeep.

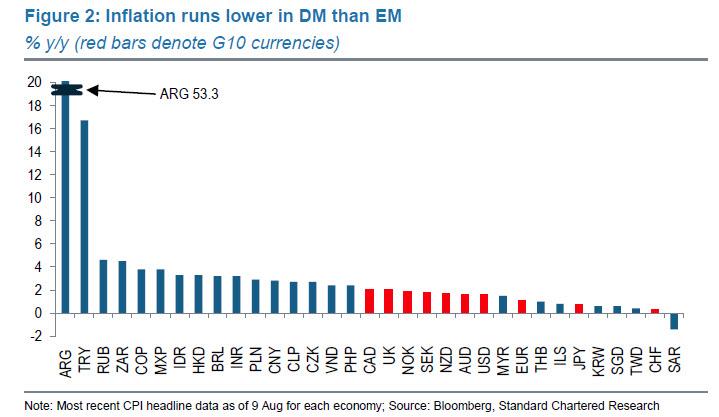

Below-target inflation makes it easier to deal with currency weakness

The credibility of currency wars is enhanced if inflation is below target, so that the weaker exchange rate helps inflation move closer to the target rather than away from it. In the G20, no DM country currently has inflation above 2.25% y/y. In EM, Asia has the biggest concentration of low-inflation EM economies (Figure 2), with Taiwan, Singapore, South Korea, Thailand and Malaysia below 2.25% and the Philippines,

China, India, Hong Kong, Indonesia and Vietnam above 2.25%. Few economies face major inflation constraints at present, but encouraging depreciation is less risky when inflation is approaching the target from below and is unlikely to significantly breach it.

Food and energy are relatively small percentages of the DM consumption basket. Rising prices of commodities that are largely priced in global markets do not create social tensions because the impact on living standards is relatively modest. In the US, food and energy make up 11% of the consumption basket and have about a 20% weight in the CPI.

Countries where prices of essentials are closely tied to the exchange rate and where these essentials are a large share of consumption are more vulnerable to depreciation. If domestic food and energy prices are largely driven by world markets, driving the exchange rate down sharply deals a major blow to living standards. In Brazil, food and energy together represent 30% of the CPI. In Vietnam, food and beverages alone are almost 40% of the CPI.

Borrowing abroad makes currency depreciation risky

We think it is less risky to engage in a currency war if domestic debt is almost entirely in local currency. The boost to trade competitiveness from currency depreciation quickly turns sour if depreciation leads to corporate or sovereign debt repayment problems or financial-sector stress. Few DM economies issue in foreign currencies, while many EM economies do. This may limit some EM countries to currency skirmishes, where they try to prevent appreciation or encourage modest depreciation rather than engaging in all-out war to weaken their currencies.

In principle, countries with current account deficits should have an easier time weakening their currencies, particularly if intervention is unsterilised. The logic is that if a country already has a current account deficit and is trying to reduce or eliminate the capital account surplus, it will be hard for the currency to move anywhere but down.

A current account deficit is often accompanied by high interest rates that may make capital flows sticky. However, the combination of a deficit and low rates could be a powerful factor driving both the current and capital accounts into deficit – provided that other factors, such as safe-haven flows, are neutral. The drop in the exchange rate is the mechanism by which the current account-capital account identity is maintained. Along the same lines, if potential capital outflows are hampered by regulation, liberalisation of the capital account would quickly depreciate the currency, but could also have spillover effects on domestic assets.

Safe-haven status is a similar consideration. If the currency war is taking place during, or contributing to, a risk-off episode, safe-haven currencies may find that intervention has limited success in deterring or offsetting capital inflows. The US might find it easier to weaken the USD if investor sentiment were more robust and there was less safe-haven buying of US Treasuries. Again, while easing rates and providing ample liquidity – essentially unsterilised intervention – could mitigate the risk-negative consequences, this is not certain against a backdrop of trade tensions.

Do you want to be a central bank or an asset manager?

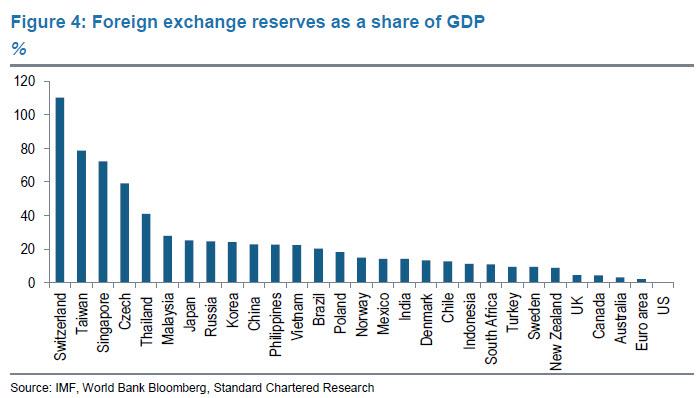

Some reserve managers oversee large FX reserve portfolios (Figure 4). The Swiss National Bank’s (SNB’s) interventions have made it one of the world’s biggest asset managers, with reserves approaching 110% of GDP. If the reserve portfolio is more than 40% of GDP, a 10% capital gain or loss on the portfolio due to currency shifts can represent a big percentage of annual growth. Moreover, after intervention, reserve managers are stuck with a portfolio of foreign currencies that no private portfolio manager would have selected (see US can intervene, but what would it buy?). When the reserve portfolio increases in size, so does the potential for conflict between the portfolio management and monetary policy management roles.

Is it worth winning a currency war?

In the best of circumstances, a weaker currency enables a country’s producers to sell more to the rest of the world, at the cost of the country’s consumers being able to afford a smaller consumption basket. If a currency drops 10%, the country’s producers will likely gain market share, but its consumers will have lower purchasing power abroad. The narrow case for currency weakness is that it may generate employment for workers who would otherwise be unemployed.

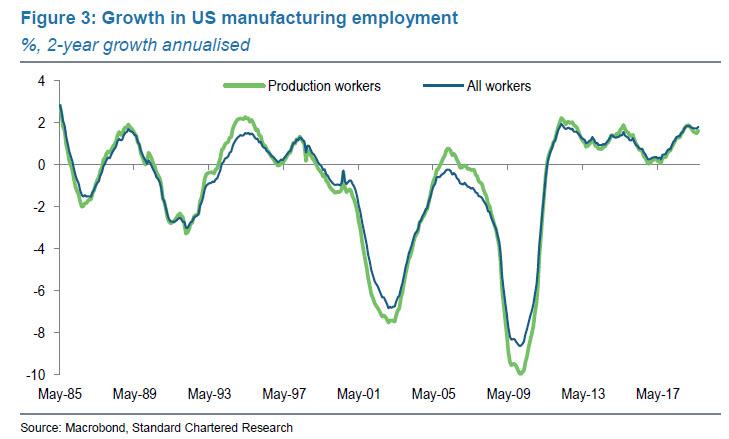

In the US, two-year growth in employment of manufacturing production workers has not exceeded 2.25% since 1985, well before trade with China was an issue (Figure 3). Increasing that growth rate to 3.25% over an extended period would require generating an additional 90,000 production worker jobs a year beyond the peak of the last the 35 years. This is only 7,500 workers per month more on a non-farm payroll basis than otherwise, about one-sixth the standard error of m/m employment growth.

US may have a small currency-war advantage within G10

The US has lots of room to ease compared to others

We think DM policy makers could succeed in broadly weakening their currencies against EM currencies. Within G10, we believe the US has significant advantages, although they are not absolute. The US has low inflation and can force short- and long-end rates down further than other G10 economies without hitting zero-bound constraints; however, Barkis (the Fed) must be willing (see The why and how of a potential Fed FX intervention). The FX intervention literature emphasises that intervention signals central bank objectives. Not participating in Treasury intervention would be a negative signal to markets and other central banks, unless there were a simultaneous easing of policy rates and increase in liquidity.

A risk-off currency war weakens small G10 and EM

The US’ problem is that the USD is in the top tier of safe havens: not quite the JPY and CHF, but ahead of other G10 and EM currencies. So a currency war that raises risk-off tensions would limit broad USD weakness. The USD’s liquidity and reserve status may also make foreigners more willing to hold it, even at lower rates.

Negative-rate currencies may depreciate faster on easing

The European Central Bank (ECB) and the Bank of Japan (BoJ) already have rates in negative territory and may find it harder to cut rates significantly. Sterilised intervention would mean selling the EUR or JPY for foreign currency and selling an equivalent amount of domestic assets to offset the liquidity injection from the intervention. The outcome would be a shift in the composition of the BoJ or ECB monetary base to holding more foreign assets and fewer domestic assets. Sterilised intervention could be surprisingly effective, as foreign investors may be reluctant to hold more negative-yielding EUR or JPY assets without a hefty discount.

Unsterilised intervention would entail flooding the FX market with newly printed money to buy foreign currencies. The ECB or BoJ balance sheet would have more foreign assets, foreigners would have fewer domestic assets and more EUR or JPY assets, and the overall supply of EUR or JPY in asset markets would be higher. Such an intervention may work very well to weaken the EUR or JPY, but poorly in terms of the impact on domestic financial markets and the financial system if it makes rates more negative. Fiscal stimulus makes more sense, but there are institutional and policy barriers to this in both countries.

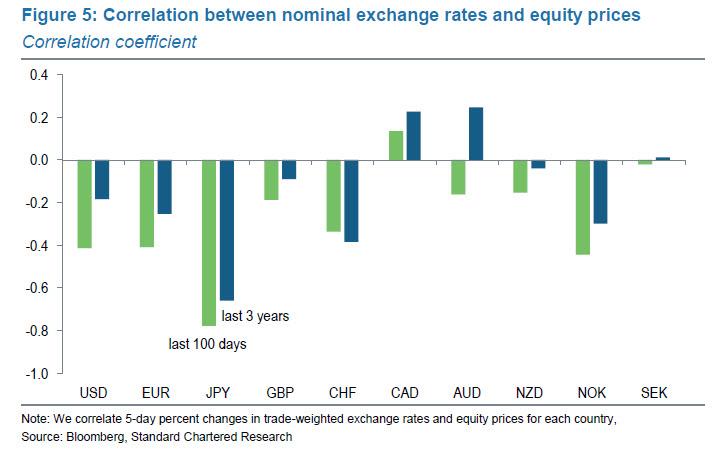

Japanese equity markets are typically very responsive to up-and-down moves in the trade-weighted JPY (Figure 5). This is another way currency weakness could have positive effects for Japan. Euro-area, US, Swiss and Norwegian equity markets also generally respond positively, but the US and euro-area equity-market response is somewhat more variable. We think most of the equity impact would be via valuation effects on corporate profits rather than higher export volumes. Commodity-currency equity prices show less consistent effects from currency depreciation – possibly because their exchange rates and equity prices often respond to common commodity-price shocks. We suspect that the EM equity price response resembles that of DM commodity currencies more than G3 currencies.

The ECB is unlikely to initiate a currency war due to the risk of US retaliation and the soft EUR. USD-JPY is already under downward pressure as a consequence of low US rates and broad risk-off sentiment. Under G20 rules, it would be hard for the BoJ to justify intervening on the basis of rate differentials narrowing and supporting the JPY. There is a reasonable case that central banks of safe-haven currencies should intervene counter-cyclically, but this would likely provoke heavy US criticism and possibly countermeasures. Most likely, the Japanese authorities would stop short of intervention but intervene verbally as long as USD-JPY were falling gradually. A sharp drop towards and past the 100 level for USD-JPY could prompt limited intervention aimed at smoothing, but this could fail if investors see US opposition limiting Japan’s ability to respond.

The Bank of England (BoE) and Bank of Canada (BoC) are not far off their inflation targets – they could act resolutely in pushing rates down, but may have to deal with inflation consequences down the road. Fiscal stimulus, accompanied by central bank balance-sheet expansion, makes more sense than targeting the currency. With Swiss reserves having risen to almost 110% of GDP in Q1-2019 from less than 10% in 2008, it is unclear how much more appetite for intervention the SNB has.

Of the remaining G10 countries, Norway and Sweden have already-weak currencies, plenty of fiscal room, and inflation close to target. Australia and New Zealand have been encouraging their currencies weaker for some time, but also have plenty of fiscal room.

via ZeroHedge News https://ift.tt/2Z1XADI Tyler Durden

“Financial technology firms” and clueless left wing lawmakers are now attempting to change the infrastructure behind payday so that workers get paid “faster”, according to the Wall Street Journal.

There is a group of technology start ups with more than $300 million in venture funding that have worked on ways to “front workers’ wages” – (also known as a payday loan?) – and then collect later when payday arrives. They are experimenting with using certain types of fees or selling companies’ future payroll obligations to investors. Some start up companies are also advertising faster paycheck access.

And these new payday loanssuper technologically savvy inventions are, of course, being back by Senator Elizabeth Warren and Representative Ayanna Pressley, among other Democrats. They’re looking to push change that will get workers paid a day or two faster, which they claim could make a “big difference”.

In other words: they want to get a broke consumer their money faster, so they can spend it and stay broke quicker.

Aaron Klein, a fellow at the Brookings Institution, noted that there’s a program at Wells Fargo that waives overdraft fees for people who receive a direct deposit the day after spending more than they have. Under this program, more than 2 million customers have already avoided fees in 2018.

Klein believes that slow payments can “cost workers billions of dollars a year in overdraft fees”. We’re wondering if he has ever thought of the simple idea of people just not spending money they don’t have.

Meanwhile, $30 billion is lent out every year in payday loans and functions that once took days or weeks to manage involving payroll can now sometimes take minutes using software.

And even though direct deposit has become the new norm, payday could supposedly still be faster. Senator Elizabeth Warren has taken exception with the fact that paychecks sometimes “take a day or two to clear”. She’s been advocating for the Federal Reserve to build a new payment network that can move money instantly. Because of course, what we need is the Federal Reserve handling our paychecks and getting involved.

But it looks like that’s what’s going to happen.

The Federal Reserve said earlier this month that it plans to build this type of network over the next few years to compete with other real time systems offered by banks. Other banks that have built their own instant payment systems have lobbied against it.

Today, the norm is for companies to put their payroll through a couple of days early to accommodate the delay in clearing for their employees. And so, with instant payments, companies might just hold onto employees’ money a day or two longer.

ADP held an average of $24.3 billion of money in transit from companies but not yet paid to employees in the fiscal year ending June 2018. That generated $466.5 million in interest revenue for them. The company is now starting to work with clients that want faster options for pay and is discussing it with lawmakers and regulators.

For example, right now ADP works with a start up company called DailyPay, Inc. which competes to offer instant pay access to employees. ADP is also working on starting a program that will enable workers who are viewing their pay online to explore new ways of getting access to their money. But of course, just like with any service, there’s costs associated with it. ADP might earn less interest for holding cash and more fees for faster service, but the shift is still in its early days.

Some experts view these programs as intermediate steps, with the ultimate shift being companies just paying workers more frequently. Now, gig economy workers, like those for Uber, can get paid up to five times a day by getting the money out put on debit cards – but few other workers have that option.

About 60% of US private businesses pay employees every two weeks and another 5% pay monthly.

Todd Baker, a senior fellow at Columbia University’s Richman Center for Business, Law and Public Policy said:

“You’ve got an enormous embedded infrastructure of payroll tied into doing things, and the cost of replacing it is pretty significant.”

via ZeroHedge News https://ift.tt/33t87Ln Tyler Durden

You know, the woman Jeffrey Epstein referred to as his “best friend” and who’s accused of acting as his madam in this whole sordid affair. She seems to have disappeared off the face of the earth and very few people seem interested.

As Vanity Fair’s Vanessa Grigoriadis notes, is it possible prosecutors have lost track of Ghislaine Maxwell, Jeffrey Epstein’s alleged co-conspirator in his pedophile ring?

For the past few weeks, rumors have circulated that she’s 400 pounds and living in Florida, or that she’s living the high life in London or the Continent, but according to the Washington Post, authorities are having a hard time locating her.

Those who know her say that it’s possible she is as much of a Houdini as Epstein. Both of them liked having secrets, and the way those secrets kept people off balance. “Jeffrey always wanted to give the impression that he was an international man of mystery—‘I control everyone and everything, I collect people, I own people, I can damage people,’” says an ex-girlfriend.

…

A source close to Maxwell says she spoke glibly and confidently about getting girls to sexually service Epstein, saying this was simply what he wanted, and describing the way she’d drive around to spas and trailer parks in Florida to recruit them. She would claim she had a phone job for them, “and you’ll make lots of money, meet everyone, and I’ll change your life.” The source continues, “Ghislaine was in love with Jeffrey the way she was in love with her father. She always thought if she just did one more thing for him, to please him, he would marry her.”

Maxwell had one other thing to tell this woman: “When I asked what she thought of the underage girls, she looked at me and said, ‘they’re nothing, these girls. They are trash.’”

This is why Liberty Blitzkrieg’s Mike Krieger rages that the top question right now should be – Where is Ghislaine Maxwell (and why isn’t she in custody)?

London — The death of Jeffrey Epstein is putting new attention on his alleged co-conspirators, who could still face charges. The number one person on that list is Ghislaine Maxwell, who’s accused of finding teenage girls for Epstein and his friends — including a member of Britain’s royal family.

As CBS News correspondent Holly Williams reports, documents unsealed on Friday contain allegations that Maxwell, a close acquaintance of Epstein’s, played an “important role” in the late billionaire financier’s “sexual abuse ring,”directing an underage girl to have sex with Epstein and others. Maxwell strenuously denies the allegations. Her current whereabouts are unknown.

Strange, sure, but it gets even more bizarre once you understand who her late father, Robert Maxwell, was. There’s even a book written about him.

No, not strange at all. Totally normal, nothing to see here.

Rule of law in America? Don’t be ridiculous. There are rulers and the ruled. Which bucket do you think you’re in?

* * *

Liberty Blitzkrieg is now 100% ad free. To make this a successful, sustainable thing consider the following options. You can become a Patron. You can visit the Support Page to donate via PayPal, Bitcoin or send cash/check in the mail.

via ZeroHedge News https://ift.tt/2McZEGR Tyler Durden

Last October, if you happened to be near the scene where some right-wing Proud Boys got into a fight with Antifa activists on New York City’s Upper East Side, the Manhattan District Attorney’s office may have collected your phone number and location at the time—without your knowledge.

Two members of the Proud Boys are on trial and several others have already pleaded guilty to rioting and disorderly conduct charges in connection with the fight. During the trial last week, an investigator with the DA’s office testified that they had gotten what’s called a “reverse location” search warrant demanding that Google cough up location information on people who had Android phones or used Google Maps near the scene. This warrant included many people who have no connection to the case—the technological equivalent of doing a house-to-house search for evidence connected to a crime in that neighborhood.

Gothamistreported that Google sent them an anonymized list of Google device identifications. Investigators cross-referenced location data and the IDs in order to narrow down those with multiple appearances in the area. They got the list to just two or three records that matched what they were looking for. On further investigation, though, they discovered that even those individuals were not connected to the case.

While this is the first time the public has been informed that these types of searches are happening in New York, the city didn’t pioneer this technique. Aaron Mak over at Slatereported in February on the growing trend of police and prosecutors turning to Google with warrants in hand, demanding data. Authorities are collecting phone numbers and locations in large numbers, and then trying to narrow down the information to likely suspects.

Mak notes that these types of searches are more powerful and far-reaching than the StingRay devices police secretly use to trick phones into connecting to them rather than phone cell towers, allowing police to track location data. With these warrants, Mak explains,

They can retrieve much more reliable data from users of Android phones or certain Google apps. Google’s location-tracking functions are often more precise than those of cell towers for tools like Maps and even Gmail. Plus, the company collects tracking data from phones that aren’t connected to cell towers, such as those using GPS satellites or Wi-Fi. When police request location data from Google-connected devices, they’ve also been known to ask for more personal information, like browsing history and past purchases.

We do not have reliable numbers about how frequently this is happening. Mak notes police in Raleigh, North Carolina, state investigators in Orange County, California, and police across Minnesota use this technique.

Google has responded to Makthat they resist overly broad requests when possible and require warrants for their cooperation. And police defend their actions by noting that they’re agreeing to the anonymized process until they narrow down to a couple of actual suspects.

Still, we should be concerned that police and prosecutors are quietly, secretly demanding phone data as a fishing expedition and that they’re getting private information about thousands upon thousands of people who are not suspected of a crime. Gothamist and Slate both spoke with privacy advocates who have concerns. From Gothamist:

Albert Fox Cahn, executive director of the Surveillance Technology Oversight Project at the Urban Justice Center, said the case illustrates what privacy advocates have long feared.

“When we sign up for Google, we shouldn’t be signing away our core constitutional rights,” he said. “When law enforcement uses these sort of digital dragnets they often will get it wrong, and innocent people will be swept up in the mix.”

In a city as dense as New York, such digital sweeps could gather data on thousands of innocent cell phone users, noted Jerome Greco, a staff attorney in the Legal Aid Society’s Digital Forensics Unit.

“That’s like saying, we suspect that somebody hid a gun in an apartment in a building, so we’re going to search everybody in the building, even though we know only one apartment actually has this,” he said. He argued law enforcement warrants should be more focused.

Meanwhile, according to New York press reports, Apple doesn’t track the location of their devices and therefore cannot provide this information to the police or prosecutors.

from Latest – Reason.com https://ift.tt/2z0aRSk

via IFTTT