I remember getting that phone call 20-some years ago while at my desk at The Lima News, which was a sister newspaper to The Orange County Register. “Would I like to come to California to work at the Register,” the editor asked? “Why, yes,” I eagerly said. “When do I start?” I forgot to ask about the salary.

When I told my wife the exciting news, she asked if we were going to weigh the pros and cons of such a big move from our cozy Ohio town to sprawling Southern California. “No,” I answered. “There’s nothing to discuss.” We’re going to California and, unlike the words in the Led Zeppelin song, it’s not with an “aching in my heart.” After crossing the border near Needles, in the 110-degree desert heat, I fell in love with the place and never looked East again.

Like others from the Midwest and East, I had long dreamed of the Golden State. By then, of course, California already ceased to be the magnet it was in earlier decades. The number of Americans who left California for other states had surpassed those from other states who moved here. Immigration rates and birth rates were still growing, however, which has propelled our population from 30 million in 1990 to nearly 40 million now.

“Nearly” is the key word. California has been inching toward the 40 million mark for some time but hasn’t reached it. Its growth rate last year of 0.47 percent is the slowest in recorded history. The exodus to other states has accelerated. International immigration has slowed. Even births are lower this year than last year. We’re a long way from the Gold Rush, when fortune-seekers from around the world tripled California’s population in a flash.

Based on the latest U.S. Census data, domestic out-migration to places such as Texas, Arizona and Oregon has outstripped domestic in-migration for eight years in a row. Anecdotal stories abound. One friend, who we met shortly after moving to Fullerton, is now a successful Texas Realtor who specializes in relocating Californians to Dallas.

Another California acquaintance, who now lives in Pennsylvania, helps our state’s businesses relocate. At social events, people always talk about the states where they are considering moving. Recent surveys show that 53 percent of Californians are considering moving elsewhere. Such ideas used to be heresy. I’ve lived in seven states plus the District of Columbia and, quite frankly, the rest of the country seems drab in comparison to California. But, lately, I’m starting to think these California refugees have made a wise choice.

We’ve reached the tipping point, where California’s progressive political imperatives are having such glaring real-world repercussions that it’s hard to keep ignoring them. Why are people leaving? Top of the list is home affordability. The national median home price is around $227,000. The median single-family home price in California topped $600,000.

In Orange County, that median price is around $700,000. In the entire Bay Area, the median price for homes and condos is $860,000. In San Francisco, you’ll need a cool $1.7 million (listed price) to get a median-priced abode (and it’s not going to be special). Our cost-of-living is astronomical in many areas. Gasoline prices are $1.29 a gallon more than the national average. Even California’s notoriously overpaid government retirees are moving elsewhere.

This is the fault of public policy. Regulations and fees can add 40 percent or more to the cost of every new house. Slow-growth rules, and the lawsuit-generating California Environmental Quality Act (CEQA), impede housing construction. The state is vastly underbuilding the number of housing units it needs even to keep up with its slowing population. Gas prices are high not only because of our high taxes, but because of the special California-only formulation that limits competition.

We all know about our nationally high tax burdens. Our property taxes are reasonable, thanks to Proposition 13, but liberal groups are gunning for its protections on commercial properties in a 2020 ballot measure. They’ll probably be coming for your home protections next. Regulatory burdens make it tougher to grow a business here than elsewhere.

Recently, Gov. Gavin Newsom signed Assembly Bill 5 into law, which messes with our ability to earn a living. That law forbids many types of contract labor. But many people don’t want to be 9-5 wage slaves and prefer piecing together various contract jobs. Businesses aren’t going to respond by hiring everyone as permanent workers. This will squelch job growth, especially in California’s innovative tech economy.

We’re also facing statewide rent controls, which will further depress housing availability. And just wait until lawmakers make good on their promise to provide single-payer healthcare. I’ve been to all 58 counties and still love the terrain, climate, culture and beaches. But if I were to get that call today, I’d have that long discussion with my wife before agreeing to move here.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/31bDHLz

via IFTTT

2019 has been a pleasant ride so far for high yield investors. Over the past 9 months the global high yield market has delivered a total return of 10.9% and an excess return of 6.4%, in part thanks to the U-turn of major central banks. Despite all the good news, things have occasionally gone wrong.

Recent events have reminded high yield investors that investing doesn’t come without risk. Thomas Cook, the UK tour operator, was grounded after final restructuring negotiations failed. To blame Brexit or the slowdown in global growth for the default would be a hasty conclusion. The business, operating in a structurally challenged industry, had long stretched its financials to the limits. The fragile situation did not go unnoticed by customers, who had stopped booking with the business. As a result of this, 2018 EBITDA (earnings before interest, taxes, depreciation and amortisation) dropped by 14.6% year-on-year which also changed the ability to materially generate positive cash flow. The company produced a negative free cash flow of £148 million in 2018. 2019 half year numbers revealed an even worse picture, with a seasonal outflow of £839 million; £121 million higher than the previous year. Operating with current liabilities that exceeded current assets by £2bn, made the solvency issue even more pressing and, in the end, didn’t allow the company to recover in time. This is a prime example of how quickly things can fall apart if consumers lose trust in a business. With bonds trading currently at 7 cents in the euro, investors only foresee a limited recovery rate for the asset-light business, which is also carrying a large amount of debt structurally senior to the bonds.

Thankfully, these default cases are the exception rather than the rule and we’ve only seen a handful of defaults in Europe this year. Early on in the year, the Retail space made headlines. It was high street retailer New Look who had to capitulate after net leverage skyrocketed well into the double digit region following weak Christmas trading. Shortly after, UK department store Debenhams announced restructuring after a period of operational underperformance combined with structural issues. Debenhams was disproportionately hit by the structural shift to online shopping, given its long-term rents and large store estate hindered the retailer from adopting quickly to the new shopping behaviour that resulted in less footfall.

Rallye, the holding company that effectively controls French food retailer Casino Guichard-Perrachon SA, pushed the Retail default rate up by one. Having sold most non-core assets over the past several years, the core investment of Rallye has been Casino. Rallye started to look insolvent as the Casino share priced dropped, and Rallye debt is now being restructured. This is an important reminder for bond investors to consider the additional risks of lending to a holding company, particularly if it only has one income stream.

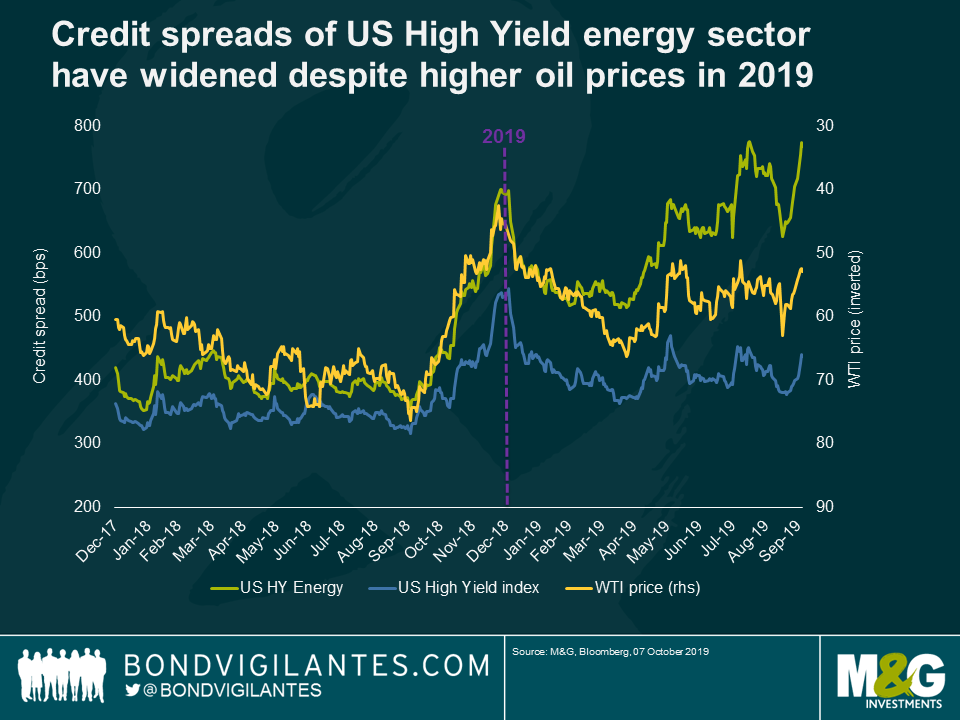

In the US, the Energy sector has been the dominant sector of defaults in 2019, accounting for more than half of the defaulted universe. In fact, the energy sector was the bottom performer in the US high yield market in the first 3 quarters of 2019 delivering an excess return of -2.9%. While the sector is up by 2.5% in total return terms, this makes dull reading compared to the broad US high yield market which generated a return of 11.5% over the same period. In contrast to the wider HY market, credit spreads of the energy sector have actually widened, which might come as a surprise considering that WTI (West Texas Intermediate) is up 17% since the turn of the year, now trading in the mid-50s and above breakeven levels for many oil players. So what is behind the underperformance and defaults in this space?

One part of the answer is execution risk, which was also the source of trouble for Alta Mesa, the recent default victim in the US HY market. The company’s acreage turned out to be less robust than anticipated. In addition, the company was having technical difficulties in drilling their wells, a problem that has already befallen several drillers operating in emerging shale basins across the states. For companies with a single asset exposure, this can be fatal. Bond investors need to carefully weight up whether the low entry costs compared to more established drilling areas such as the Permian basin, are worth the risk of missing production forecasts and consequently the failure to generate the cash flow needed to service its bonds.

As always, a major concern of US Exploration and Production companies is the degree of debt that some players are saddled with, making it impossible to grow into their capital structure should production levels disappoint due to operational issues even when WTI is in the 50’s.

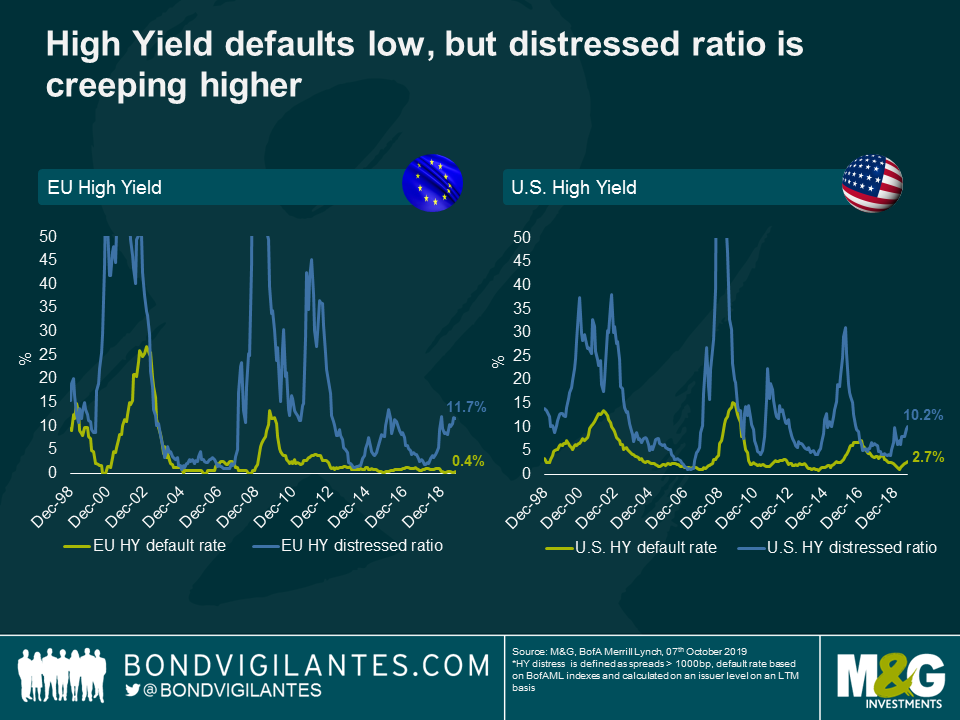

Overall however – particularly outside the Energy and Retail space – defaults remain low in high yield. That being said, the portion of bonds trading at distressed levels, defined by a spread level higher than 1000bps, is on the rise, which tends to be a good leading indicator for future defaults. Therefore, I would expect default rates to increase somewhat from here due to idiosyncratic issues, such as those experienced by Thomas Cook. Bond investors are currently witnessing an increasingly two-tier market. Those that are in favour can borrow cheaply and benefit from the low interest rate environment. Those falling out of favour find themselves locked out of the market with market concerns perpetuating a vicious cycle.

This is John Stossel’s full interview with Democratic Presidential candidate Tulsi Gabbard. To watch an excerpted version, click here.

Rep. Tulsi Gabbard (D–Hawaii) will be in the Democratic debate next week. John Stossel says that’s good, because she’s different from the other Democrats.

One difference is that she served in Iraq, and now pushes for ending wars. “We have to honor our servicemen and women by only sending them on missions that are worthy of their sacrifice,” Gabbard tells Stossel.

Instead, American interventions are often open-ended. “There’s seldom a discussion that I’ve heard about what is our mission,” Stossel says.

“Exactly! That’s exactly the problem…what is the clear, achievable goal?” Gabbard responds. She says her Afghanistan policy would have been: “Go in. Defeat Al-Qaeda. Get out.”

Gabbard also says: talk with our enemies. She met with Syria’s dictator. The media and other Democratic candidates give her grief for that.

CNN’s Chris Cuomo lectured her: “You need to acknowledge that Bashar al-Assad is a murderous despot.”

Kamala Harris called Gabbard an “Assad apologist.”

“What’s going on with your party?” Stossel asks Gabbard. “Democrats used to the antiwar party.”

Gabbard responds that both parties are “heavily influenced by the foreign policy establishment…whose whole power base is built around continuing this status quo. So much so to the point where when I’m calling for an end to these wasteful wars, they’re saying, ‘well, gosh, Tulsi, why are you such an isolationist.’ As though the only way that we can relate with other countries in the world is by bombing them, or by putting crippling economic sanctions in place.”

Stossel also asks Gabbard about taking down a Democratic front-runner. In the fourth debate, she criticized Kamala Harris for her history of jailing people.

“She put over 1,500 people in jail for marijuana violations and then laughed about it when she was asked if she ever smoked marijuana,” Gabbard said in the debate.

That moment changed the race. Harris lead in the betting at ElectionBettingOdds.com, with a 26% chance of winning the nomination. During the debate, she fell seven points. 10 days later, another seven points.

“You killed her off,” Stossel says.

“I’m for the people, man,” Gabbard replies, laughing. “I was speaking the truth, and speaking for a lot of people.”

Gabbard and Stossel argue, too. Like most democrats, Gabbard would spend billions on expensive new programs. She backs Medicare for All and free college.

“Don’t you think colleges already waste a lot of money?” Stossel asks.

Gabbard agrees, “They do. Absolutely. Why is it costing more and more and more every single year?”

“Look how much more it will cost when it’s free,” says Stossel.

Gabbard responds, “We have to deal with…the root cause of the problem. One of which is…how much administrators of a lot of these colleges are being paid or overpaid.”

Stossel and Gabbard also argue over her proposal for a $15 minimum wage.

“How does that not destroy opportunity for a 17-year-old in his first job who isn’t worth $15 an hour?” Stossel asks.

“I think we’re looking at this as an investment in people,” Gabbard answers.

In the end, Stossel says, “I’m glad we could have a civil argument about some of these areas where we disagree. Few politicians want to do that anymore.”

She adds: “Look, I love my country. You love our country. Let’s come together as Americans with appreciation for our Constitution, our freedoms, civil liberties and rights, and have this civil discourse and dialogue about how we can move forward together.”

The views expressed in this video are solely those of John Stossel; his independent production company, Stossel Productions; and the people he interviews. The claims and opinions set forth in the video and accompanying text are not necessarily those of Reason.

from Latest – Reason.com https://ift.tt/2phOOVF

via IFTTT

In prior posts I have offered a dismal view on why it will be difficult for the U.S. to shed the “mass incarceration” label. Nonetheless, even an impossible situation has degrees of badness, and the size of the task is no excuse for not trying to get better. As noted earlier, some progress has been made in reducing inmate populations; but to continue to make gains will require a sustained and coordinated effort from all actors in the system.

A threshold problem is that the list of actors who need to coordinate their efforts is long. As James Foreman, Jr., puts it:

The police make arrests, pretrial service agencies recommend bond, prosecutors make charging decisions, defense lawyers defend (sometimes), juries adjudicate (in the rare case that doesn’t plead), legislatures establish the sentence ranges, judges impose sentences within these ranges, corrections departments run prisons, probation and parole officers supervise released offenders, and so on. The result is an almost absurdly disaggregated and uncoordinated criminal justice system.

In an effort to influence these scattered decisionmakers, reform efforts have targeted legislators, urging them to eliminate mandatory minimum sentences, lower the punishment for drug or property crimes, or soften the impact of three-strikes and truth-in-sentencing laws. Other proposals target judges, encouraging them to use risk-assessment tools when sentencing or setting bail, or to more closely consider alternative sanctions rather than incarceration. Still other reforms address probation and parole officers, police, and prison officials, all recommending changes in practice that will reduce the number of people being sent to prison, speed up the release time, or both.

Remarkably, the actor who is least likely to be the target of the reforms is almost surely the most important one—the prosecutor. The prosecutor has complete discretion to decide who is charged and for what; has near complete control over which cases end in a guilty plea and on what terms; and has a significant role in deciding who is jailed prior to trial and who is released, all of which channel and shape the ultimate punishment a defendant will face. And yet, as John Pfaff has observed, while prosecutors “have used [their] power to drive up prison populations, ….[t]o date … no state- or federal-level proposal aimed at cutting prison populations has sought to explicitly regulate this power…. [P]rosecutors have remained untouched.”

It’s not hard to figure out why. Prosecutors have clout, and it is hard to get changes made to the justice system in the face of prosecutorial opposition (particularly if those changes involve greater regulation of prosecutors). Prosecutors also have a judicially-enforced zone of discretion, within which they are free to act without fear of being overruled, even by the courts themselves.

So if prosecutors want to make frequent use of statutory three-strike provisions, or seek particular sentence enhancements, or file higher charges rather than lower charges, or recommend against probation as a sentence, they can do so regardless of the impact on incarceration rates. Legislatures can channel this discretion to a degree by changing their sentencing laws or their substantive offenses, but the broad and overlapping reach of most criminal codes allows prosecutors to reach most of the ends they seek, including an appropriately severe sentence, in most criminal cases.

Despite this broad authority, incarceration reform efforts have not attempted to limit the charging power, have mostly maintained the prosecutor’s role in the sentencing process, and have left intact the near-complete power over the plea bargaining process—the straw that stirs the drink in the criminal system. As a result, prosecutors may, if they wish, take steps to reduce incarceration rates, but they are not compelled to do so.

Of course, even if we leave prosecutors outside the reform efforts this does not mean that they necessarily will exercise their discretion in ways that increases the severity and frequency of incarceration. “Prosecutors” are not monolithic in their actions and attitudes,(recall the recent war of words between the Philadelphia D.A. and the U.S. Attorney for the Eastern District of Pennsylvania), and there are many prosecutors who have expressed their unhappiness with the status quo.

Still, prosecutors suffer the same confirmation bias as everyone else; like most of us, they believe that they do their jobs honorably and properly, and that their professional choices make things better, not worse. And so the moral basis for sentencing reform—that is “unnecessary” (and therefore unjust) to lock up this many people for this number of years—is likely to be less convincing to prosecutors, especially when they collectively have played such a significant role in creating the current state of affairs.

This is not to argue that prosecutors are the sole or even the dominant cause of high incarceration rates; Jeffrey Bellin, for example, has cogently argued that the “primary culprits” of the incarceration problem are judges and legislatures. The point is simply that prosecutors play a highly important role, that that states have struggled to find ways to harness the prosecutors’ powers to bring about change, and that unlike other actors in the system, prosecutors are involved in the effort to reduce incarceration levels as a matter of grace, not as a matter of command.

Conclusion

James Forman, Jr., has noted that “[m]ass incarceration wasn’t created overnight; its components were assembled piecemeal over a forty-year period.” Unwinding the missteps and excesses is likely to take at least that long. But even assuming societal patience with the task, there is nothing inevitable about a long-term decrease in incarceration. Extremely hard choices have to be made—are we willing to release those who commit violent crimes earlier than we do now?—and the declining crime rate of the last 20 years that have made reform politically feasible will not last forever.

The recent decrease in incarnation levels is encouraging, but sustained change will surely require a greater engagement by prosecutors. Formal restrictions on their role are not likely to materialize (and may not, in the long run, even be a good idea), which leaves persuasion and cooperation as the tools of engagement. If prosecutors are convinced that incarceration is an over-used tool, there is reason to hope that the prison system can become permanently smaller and more effective. If not, it seems likely that the label of mass incarceration will continue to apply for a very long time to come.

from Latest – Reason.com https://ift.tt/2ODFypD

via IFTTT

I remember getting that phone call 20-some years ago while at my desk at The Lima News, which was a sister newspaper to The Orange County Register. “Would I like to come to California to work at the Register,” the editor asked? “Why, yes,” I eagerly said. “When do I start?” I forgot to ask about the salary.

When I told my wife the exciting news, she asked if we were going to weigh the pros and cons of such a big move from our cozy Ohio town to sprawling Southern California. “No,” I answered. “There’s nothing to discuss.” We’re going to California and, unlike the words in the Led Zeppelin song, it’s not with an “aching in my heart.” After crossing the border near Needles, in the 110-degree desert heat, I fell in love with the place and never looked East again.

Like others from the Midwest and East, I had long dreamed of the Golden State. By then, of course, California already ceased to be the magnet it was in earlier decades. The number of Americans who left California for other states had surpassed those from other states who moved here. Immigration rates and birth rates were still growing, however, which has propelled our population from 30 million in 1990 to nearly 40 million now.

“Nearly” is the key word. California has been inching toward the 40 million mark for some time but hasn’t reached it. Its growth rate last year of 0.47 percent is the slowest in recorded history. The exodus to other states has accelerated. International immigration has slowed. Even births are lower this year than last year. We’re a long way from the Gold Rush, when fortune-seekers from around the world tripled California’s population in a flash.

Based on the latest U.S. Census data, domestic out-migration to places such as Texas, Arizona and Oregon has outstripped domestic in-migration for eight years in a row. Anecdotal stories abound. One friend, who we met shortly after moving to Fullerton, is now a successful Texas Realtor who specializes in relocating Californians to Dallas.

Another California acquaintance, who now lives in Pennsylvania, helps our state’s businesses relocate. At social events, people always talk about the states where they are considering moving. Recent surveys show that 53 percent of Californians are considering moving elsewhere. Such ideas used to be heresy. I’ve lived in seven states plus the District of Columbia and, quite frankly, the rest of the country seems drab in comparison to California. But, lately, I’m starting to think these California refugees have made a wise choice.

We’ve reached the tipping point, where California’s progressive political imperatives are having such glaring real-world repercussions that it’s hard to keep ignoring them. Why are people leaving? Top of the list is home affordability. The national median home price is around $227,000. The median single-family home price in California topped $600,000.

In Orange County, that median price is around $700,000. In the entire Bay Area, the median price for homes and condos is $860,000. In San Francisco, you’ll need a cool $1.7 million (listed price) to get a median-priced abode (and it’s not going to be special). Our cost-of-living is astronomical in many areas. Gasoline prices are $1.29 a gallon more than the national average. Even California’s notoriously overpaid government retirees are moving elsewhere.

This is the fault of public policy. Regulations and fees can add 40 percent or more to the cost of every new house. Slow-growth rules, and the lawsuit-generating California Environmental Quality Act (CEQA), impede housing construction. The state is vastly underbuilding the number of housing units it needs even to keep up with its slowing population. Gas prices are high not only because of our high taxes, but because of the special California-only formulation that limits competition.

We all know about our nationally high tax burdens. Our property taxes are reasonable, thanks to Proposition 13, but liberal groups are gunning for its protections on commercial properties in a 2020 ballot measure. They’ll probably be coming for your home protections next. Regulatory burdens make it tougher to grow a business here than elsewhere.

Recently, Gov. Gavin Newsom signed Assembly Bill 5 into law, which messes with our ability to earn a living. That law forbids many types of contract labor. But many people don’t want to be 9-5 wage slaves and prefer piecing together various contract jobs. Businesses aren’t going to respond by hiring everyone as permanent workers. This will squelch job growth, especially in California’s innovative tech economy.

We’re also facing statewide rent controls, which will further depress housing availability. And just wait until lawmakers make good on their promise to provide single-payer healthcare. I’ve been to all 58 counties and still love the terrain, climate, culture and beaches. But if I were to get that call today, I’d have that long discussion with my wife before agreeing to move here.

This column was first published in the Orange County Register.

from Latest – Reason.com https://ift.tt/31bDHLz

via IFTTT

Donald Trump Presents: ‘Plotting Lovebirds’ And The Search For ‘Loser’ Hunter Biden

President Trump delivered a fiery performance in Minnesota on Thursday night, where he pulled few punches laying into his political opponents. After a brief warmup, Trump kicked things off by reminding the crowd he’s still the outsider in DC – who’s now being attacked with a “phony” Democrat narrative which has formed the basis of a House impeachment inquiry.

“Our bold pursuit of this pro-America agenda has enraged the failed ruling class in Washington,” said Trump, adding “not easy to get ’em out but we’re doing it slowly but surely.”

“These corrupt politicians and the radical leftists got rich bleeding America dry, and they knew that my election would finally end their pillaging and looting of our country. And that’s what they were doing. And that’s what they continue to try and do.”

Trump then proclaimed “from day one, the wretched Washington swamp has been trying to nullify the results of a truly great and democratic election – the election of 2016. They’re trying, but they’re not getting very far. They want to erase your vote like it never existed. They want to erase your voice. And they want to erase your future.”

Trump then did a dramatic recreation of FBI ‘lovebirds’ Peter Strzok and Lisa Page discussing how they were going to bring Trump down.

The two high-ranking FBI officials were busted exchanging anti-Trump / pro-Clinton text messages while investigating both Trump and Clinton.

“Remember he and his lover Lisa Page,” Trump said, before mocking the pair.

“Oh I love you so much. I love you, Peter! I love you too Lisa! Lisa, I love you. Lisa, Lisa, Oh God, I love you, Lisa.

“And if [Hillary Clinton] doesn’t win, Lisa, we’ve got an insurance policy, Lisa! We’ll get that son of a bitch out.”

Trump then turned to ‘crooked’ Adam Schiff (D-CA), who “had to make up a fake conversation that never happened” about Trump’s phone call with Ukrainan President Volodomyr Zelensky, after the White House released a transcript of the call which proved that Trump asked – not pressured, Ukraine to look into corruption allegations against Joe and Hunter Biden. Trump then tore into House Speaker Nancy Pelosi (D-CA) for insisting Schiff was using Trump’s own words.

“These people are sick,” Trump said of the Democrats. “I’m telling you. Had they waited one day longer, they would have had the actual transcript of the call. Instead, they went early. You know why? Because they never thought in a million years that I was going to release a transcript of the call”

“So Nancy Pelosi upon hearing a false story from a whistleblower that has no clue what was going on in that call – or somebody gave hervery bad advice – but also hearing it from ‘shifty’ Schiff. Nancy Pelosi said a day before seeing a transcript of the call with the Ukrainian President “WE’VE GOT TO IMPEACH HIM!”

And then she saw the call and she said to her people “what the hell? Nobody ever told me this was the call!”

Then, after calling polls crooked ‘like the media,’ Trump tore into Joe and Hunter Biden – calling the former Vice President “totally owned, and totally controlled by the Washington swamp for many years.”

“Two months after President Obama put Joe in charge of Ukraine policy – he put Joe Biden in charge of Ukraine policy (and the press will not write it) … Joe’s son Hunter got thrown out of the Navy and then he became a genius on Wall Street in about two days.”

“By the way, what ever happened to Hunter? Where the hell is he?” Trump asked, before pitching an idea for a ‘Where’s Hunter’ T-shirt (which is now for sale at the official Trump campaign website).

“Hunter, you know nothing about energy, you know nothing about China, you know nothing about anything, frankly. Hunter, you’re a loser. Why did you get $1.5 billion dollars Hunter?“

Then, as if speaking to to Hunter, Trump said: “Your father was never considered smart … He was never considered a good senator. He was only a good vice president because he understood how to kiss Barack Obama’s ass.“

“The Bidens got rich, and America got robbed,” Trump added.

Hunter Biden served on the board of Ukraine’s largest private gas company, Burisma, for nearly five years. While Hunter’s position raised eyebrows at the time, controversy erupted earlier this year after footage emerged of Joe Biden bragging about threatening the President of Ukraine by withholding $1 billion in US loan guarantees if he didn’t fire the country’s lead investigator, Victor Shokin, who was leading an inquiry into Burisma at the time.

Trump also laid into Rep. Ilhan Omar (D-MN), who represents the Minneapolis district in which the rally was held – telling the crowd “Leaders in Washington brought large numbers of refugees to your state from Somalia without considering the impact on schools and communities and taxpayers,” adding “Congresswoman Omar is an America-hating socialist.”

Looked at one way, Gemini Man is a classic tale of man versus himself: The Bourne-esque sci-fi thriller pits a middle-aged Will Smith against a younger, computer-generated clone, constructed partly from images of Smith as a 20-something movie and TV star. Smith’s technology-enhanced dual role anchors the movie, and gives it a reason for being. The idea for the film reportedly languished in development for decades, and was only made once Smith signed on. Where there’s a Will, there’s a way.

As a big-budget tech demo, Gemini Man is ambitious and fascinating: Finally! A way to appease all those viewers who’ve been clamoring for cinematic technology that lets the Fresh Prince of Bel-Air face off against Genie from Aladdin. As a movie, it’s flat stilted, an extended visit to the uncanny valley.

Hollywood has always cast aging stars opposite fresh-faced talent, but in this case, the face is literally Smith’s own. In an industry that has always treated any perceptible sign of aging as a mortal threat to one’s career, there is arguably something courageous about submitting to such a concept, which offers a visceral reminder of the toll of time. Here, the movie seems to say, is the competition: Will Smith used to be young, and beautiful, and…look oddly like a character out of a video game. I can’t wait to play him when he inevitably becomes an avatar in Overwatch.

Which is why the better way to view Gemini Man may not be as a story of man versus himself, but of humans versus technology. Spoiler alert: Nobody wins.

Junior, the name given to the movie’s younger Smith, was not conventionally de-aged like Samuel L. Jackson in Captain Marvel, a process more like applying digital make-up, so much as virtually replicated. Junior is better understood as a full-body digital costume wrapped around a motion-capture performance, then tweaked and tailored by an army of digital artists. Smith plays a younger version of himself by donning what is effectively a Young Will Smith mask and suit.

Smith’s on-screen opponent is thus a sort of digital clone, a virtual person constructed using a cinematic process that mirrors the biological cloning portrayed in the film. But while technically impressive in some ways, Junior still tends to come across as less than fully real. There’s a slightly unnatural quality to the character’s brow and eyes, to the way his lips don’t quite seem to be in sync with his words; he’s more pixel than person, an animated presence rather than a flesh-and-blood actor. No, the younger Smith isn’t Genie-blue, but there were times when I half expected him to shout a jokey catchphrase and disappear into a cloud of cerulean smoke.

Some of the disjointedness can be attributed to director Ang Lee’s decision to shoot the film using an ultra-high frame rate, in which a digital camera collects vastly more images per second than the 24-images-per-second that has been standard since the days of film. Less advanced versions of this process have been employed before, on Peter Jackson’s first Hobbit film, and on Lee’s last movie, Billy Lynn’s Long Halftime Walk, but Lee’s preferred projection method is so advanced that not one theater in the United States will be able to show it exactly as he intended. Directors who shoot in high frame rates sometimes cast it as a system for creating cinematic hyper-reality, but the results so far are always distracting and weird, like watching a television with motion smoothing turned up to the max. Here, the entire movie exudes a sense of plastic falseness; too many of the images feel synthetic, stilted, or simply off in some difficult-to-precisely-identify way.

The story, meanwhile, is a pastiche of globe-trotting thriller cliches—a private corporation run by a villainous Clive Owen wants to make ultra-reliable super-soldiers because blah blah who cares reasons—that appears to have been written by feeding every Jason Bourne movie script and novel into an AI screenwriting-bot and filming whatever came out. At best it’s an ironic metaphor for Hollywood’s own desire to endlessly clone its star properties, forcing them into soulless service. But the clunker-packed screenplay never rises above the expository, state-the-theme dullness of lines “I need to get you to Budapest” and “Deep down it’s like my soul has been hurt.” (Which, same.)

Officially, the writing is credited to Shattered Glass writer Billy Ray, Game of Thrones showrunner David Benioff, and Shrek Forever‘s Daren Lemke. Yet as with Smith’s computer-generated quasi-performance, it’s sometimes hard to believe any real person, much less three of them, was involved.

That’s a problem for the entire film, which generally comes across as grim, lifeless, and technologically overdetermined. What both Smith’s digitized younger self and the movie are missing is a distinctive personality, a sense that there’s something human behind the scenes. There’s no soul, nor even the winning screen persona of Smith at his best. Gemini Man delivers a digitized double dose of its leading man, but it can’t replicate his essential charm. The movie’s real problem, you might say, is a lack of Will.

from Latest – Reason.com https://ift.tt/2M4D0iH

via IFTTT

Looked at one way, Gemini Man is a classic tale of man versus himself: The Bourne-esque sci-fi thriller pits a middle-aged Will Smith against a younger, computer-generated clone, constructed partly from images of Smith as a 20-something movie and TV star. Smith’s technology-enhanced dual role anchors the movie, and gives it a reason for being. The idea for the film reportedly languished in development for decades, and was only made once Smith signed on. Where there’s a Will, there’s a way.

As a big-budget tech demo, Gemini Man is ambitious and fascinating: Finally! A way to appease all those viewers who’ve been clamoring for cinematic technology that lets the Fresh Prince of Bel-Air face off against Genie from Aladdin. As a movie, it’s flat stilted, an extended visit to the uncanny valley.

Hollywood has always cast aging stars opposite fresh-faced talent, but in this case, the face is literally Smith’s own. In an industry that has always treated any perceptible sign of aging as a mortal threat to one’s career, there is arguably something courageous about submitting to such a concept, which offers a visceral reminder of the toll of time. Here, the movie seems to say, is the competition: Will Smith used to be young, and beautiful, and…look oddly like a character out of a video game. I can’t wait to play him when he inevitably becomes an avatar in Overwatch.

Which is why the better way to view Gemini Man may not be as a story of man versus himself, but of humans versus technology. Spoiler alert: Nobody wins.

Junior, the name given to the movie’s younger Smith, was not conventionally de-aged like Samuel L. Jackson in Captain Marvel, a process more like applying digital make-up, so much as virtually replicated. Junior is better understood as a full-body digital costume wrapped around a motion-capture performance, then tweaked and tailored by an army of digital artists. Smith plays a younger version of himself by donning what is effectively a Young Will Smith mask and suit.

Smith’s on-screen opponent is thus a sort of digital clone, a virtual person constructed using a cinematic process that mirrors the biological cloning portrayed in the film. But while technically impressive in some ways, Junior still tends to come across as less than fully real. There’s a slightly unnatural quality to the character’s brow and eyes, to the way his lips don’t quite seem to be in sync with his words; he’s more pixel than person, an animated presence rather than a flesh-and-blood actor. No, the younger Smith isn’t Genie-blue, but there were times when I half expected him to shout a jokey catchphrase and disappear into a cloud of cerulean smoke.

Some of the disjointedness can be attributed to director Ang Lee’s decision to shoot the film using an ultra-high frame rate, in which a digital camera collects vastly more images per second than the 24-images-per-second that has been standard since the days of film. Less advanced versions of this process have been employed before, on Peter Jackson’s first Hobbit film, and on Lee’s last movie, Billy Lynn’s Long Halftime Walk, but Lee’s preferred projection method is so advanced that not one theater in the United States will be able to show it exactly as he intended. Directors who shoot in high frame rates sometimes cast it as a system for creating cinematic hyper-reality, but the results so far are always distracting and weird, like watching a television with motion smoothing turned up to the max. Here, the entire movie exudes a sense of plastic falseness; too many of the images feel synthetic, stilted, or simply off in some difficult-to-precisely-identify way.

The story, meanwhile, is a pastiche of globe-trotting thriller cliches—a private corporation run by a villainous Clive Owen wants to make ultra-reliable super-soldiers because blah blah who cares reasons—that appears to have been written by feeding every Jason Bourne movie script and novel into an AI screenwriting-bot and filming whatever came out. At best it’s an ironic metaphor for Hollywood’s own desire to endlessly clone its star properties, forcing them into soulless service. But the clunker-packed screenplay never rises above the expository, state-the-theme dullness of lines “I need to get you to Budapest” and “Deep down it’s like my soul has been hurt.” (Which, same.)

Officially, the writing is credited to Shattered Glass writer Billy Ray, Game of Thrones showrunner David Benioff, and Shrek Forever‘s Daren Lemke. Yet as with Smith’s computer-generated quasi-performance, it’s sometimes hard to believe any real person, much less three of them, was involved.

That’s a problem for the entire film, which generally comes across as grim, lifeless, and technologically overdetermined. What both Smith’s digitized younger self and the movie are missing is a distinctive personality, a sense that there’s something human behind the scenes. There’s no soul, nor even the winning screen persona of Smith at his best. Gemini Man delivers a digitized double dose of its leading man, but it can’t replicate his essential charm. The movie’s real problem, you might say, is a lack of Will.

from Latest – Reason.com https://ift.tt/2M4D0iH

via IFTTT

“Sea Of Green” As Trade Deal, Brexit Optimism Send Futures, World Markets Soaring

So far, Friday has been a rerun of the Thursday session, where early “trade war” gloom turned to euphoria with the market convinced a mini trade deal between the US and China will be announced momentarily, just as soon as Trump and Liu He are scheduled to meet at 2:45pm in the White House. Throw in some Brexit optimism and there’s your reason why US equity futures jumped over 30 points overnight…

… and why global stock markets were a sea of green.

The MSCI world index jumped 0.8% to head toward its first weekly gain in four weeks. The broader Euro STOXX 600 surged 2.5%, led by a 3.4% surge in the German DAX. Tech shares led European gains, with the Stoxx 600 Technology Index surging 3.2%, most since April 24, led higher by SAP. Banks also rose, with the index rising 2.4%, most in a month, while S&P 500 futures jumped 0.9% Asian shares had rallied earlier, with an index of Asia-Pacific shares outside Japan climbing 1.3%.

The improvement in appetite for riskier bets came after U.S. President Donald Trump on Thursday called the first day of trade talks with China in over two months “very, very good.” Trade optimism was bolstered overnight after a Chinese state newspaper said on Friday that a “partial” trade deal would benefit China and the United States, and Washington should take the offer on the table, reflecting Beijing’s aim of cooling the row before more U.S. tariffs kick in.

China’s top trade negotiator, Vice Premier Liu He, said on Thursday that China is willing to reach agreement with the United States on matters that both sides care about so as to prevent friction from leading to any further escalation. He stressed that “the Chinese side came with great sincerity”.

Adding to that, the official China Daily newspaper said in an editorial in English: “A partial deal is a more feasible objective” adding that “Not only would it be of tangible benefit by breaking the impasse, but it would also create badly needed breathing space for both sides to reflect on the bigger picture.”

Additionally, and not coincidentally, hours ahead of an expected meeting between China’s Liu and U.S. President Donald Trump at the White House, China’s securities regulator unveiled a firm timetable for scrapping foreign ownership limits in futures, securities and mutual fund companies for the first time, suggesting that professional US gamblers will be welcome to invest, and lose, other people’s money in Chinese fraudcaps. China previously said it would further open up its financial sector on its own terms and at its own pace, but the timing of Friday’s announcement suggests Beijing is keen to show progress in its plan to increase foreigners’ access to the sector, which is among a host of demands from Washington in the trade talks.

Chinese officials are offering to increase annual purchases of U.S. agricultural products as the two countries seek to resolve their trade dispute, the Financial Times reported on Wednesday, citing unidentified sources. The U.S. Department of Agriculture (USDA) on Thursday confirmed net sales of 142,172 tonnes of U.S. pork to China in the week ended Oct. 3, the largest weekly sale to the world’s top pork market on record.

A (very unlikely) U.S.-China currency agreement is also being floated as a symbol of progress in talks between the world’s two largest economies, although that would largely repeat past pledges by China, currency experts say, and will not change the dollar-yuan relationship that has been a thorn in the side of Trump.

There were also overnight reports that the White House is reportedly mulling Public Company Accounting Oversight Board (PCAOB) dispute over access to China audits, according to reports. Officials are fixating on why Chinese companies can sell shares in the US when American regulators are prohibited from inspecting their books.

Analysts have noted China sent a larger-than-normal delegation of senior Chinese officials to Washington, with commerce minister Zhong Shan and deputy ministers on agriculture and technology also present. Separately, the SCMP reported that China’s Vice Premier Liu has a letter from President Xi, which may or may not be given to US President Trump in their meeting today.

The sudden optimism about a potential de-escalation is in stark contrast to much more gloomy predictions in business circles just days ago on the heels of a series of threatened crackdowns on China by the Trump administration. On Tuesday, the U.S. government widened its trade blacklist to include Chinese public security bureaus and some of China’s top artificial intelligence startups, punishing Beijing for its treatment of Muslim minorities. Surprised by the move, Chinese government officials told Reuters on the eve of talks that they had lowered expectations for significant progress.

Friday’s China Daily editorial also warned that “pessimism is still justified”, noting that the talks would finish just three days before Washington is due to raise tariffs on $250 billion worth of Chinese imports. The negotiations were the “only window” to end deteriorating relations, it added.

Investors cautioned that markets were hoping for, at best, a deal limited in scope, and they noted that sunny rhetoric had in the past failed to translate into more meaningful moves. “I would caution that we have been here before, where we have seen positive talk,” said Mike Bell, global market strategist at J.P. Morgan Asset Management. “It’s possible they will be able to do a smaller deal around tariffs, where there is some room for movement.”

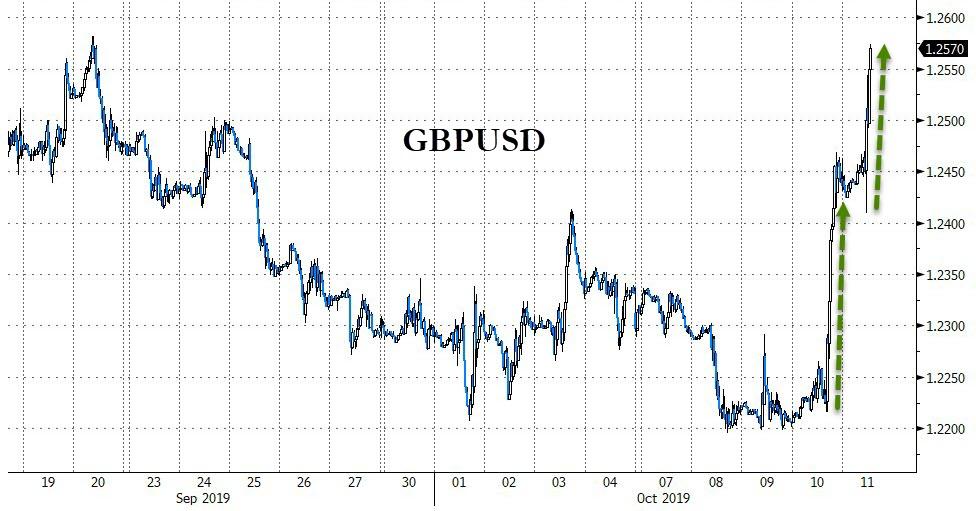

Elsewhere, Brexit optimism was also rampant and the pound soared higher on Friday – its largest daily percentage gain in seven months and biggest 2-day jump since June 2016 – after Donald Tusk, EU council president, said he had seen “promising signals” about the chance of a fresh Brexit agreement between the UK and the EU, even if the country hasn’t come forward with a workable, realistic plan. Optimism that a deal could be reached has been increasing following a meeting between Boris Johnson, UK prime minister, and Leo Varadkar, Irish taoiseach, on Thursday, after which the two said they could see a “pathway” to a possible Brexit deal.

After meeting British Prime Minister Boris Johnson for talks, Irish Prime Minister Leo Varadkar said on Thursday that a deal to let Britain leave the European Union in an orderly fashion could be sealed by the end of the month. Varadkar called the talks “constructive,” while the two leaders said in a joint statement that they could “see a pathway to a possible deal”. But it remained unclear what the pair agreed on.

But with Britain due to leave the world’s biggest trading bloc on Oct. 31, the fate of Brexit is still in the balance. Market players said investors remained skittish. Moves in sterling reflected a tendency to jump on any signs of progress.

“We are moving to a glimmer of hope, rather than strong expectation that things will get done,” Tim Drayson, head of economics at Legal & General Investment Management. Yet Drayson said that any deal struck between Dublin and London would then face the hurdle of the British parliament, even after securing agreement from the European Union. “I think the odds are that we don’t reach an agreement, but I’m not expecting a crash out on October 31.”

“We still think that markets are probably underpricing the likelihood of a hard Brexit scenario,” said Salman Baig, a cross-asset investment manager at Unigestion whose pound short appears to have been steamrolled by a backbreaking short squeeze.

In geopolitics, US House Republicans said they will introduce sanctions against Turkey in response to its offensive against Kurds in Northern Syrian, according to newswires. Subsequent reports indicate European response could be debated as early as next week

In commodities, oil prices jumped by 2% after Iranian news agencies said a state-owned oil tanker was struck by two missiles in the Red Sea near Saudi Arabia, raising the prospect of supply disruptions from a crucial producing region. Brent crude was up around 2.1% at $60.36 per barrel.

Expected data include the University of Michigan Consumer Sentiment Index. Fastenal is reporting earnings

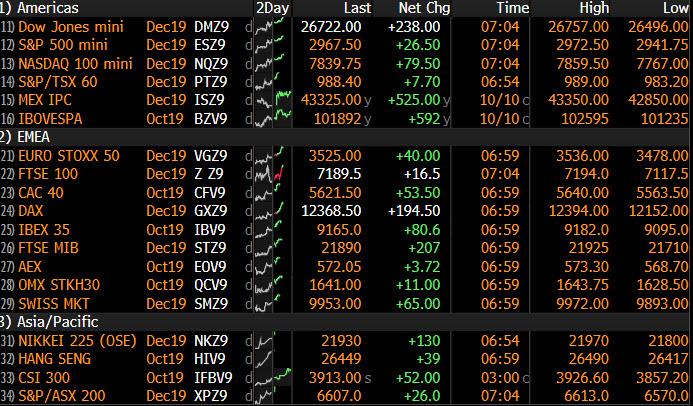

Market Snapshot

S&P 500 futures up 0.7% to 2,962.75

STOXX Europe 600 up 1% to 386.50

MXAP up 1.2% to 157.15

MXAPJ up 1.4% to 504.43

Nikkei up 1.2% to 21,798.87

Topix up 0.9% to 1,595.27

Hang Seng Index up 2.3% to 26,308.44

Shanghai Composite up 0.9% to 2,973.66

Sensex up 0.9% to 38,227.49

Australia S&P/ASX 200 up 0.9% to 6,606.81

Kospi up 0.8% to 2,044.61

German 10Y yield fell 1.4 bps to -0.483%

Euro up 0.05% to $1.1010

Italian 10Y yield rose 8.7 bps to 0.616%

Spanish 10Y yield fell 3.3 bps to 0.194%

Brent futures up 1.5% to $59.96/bbl

Gold spot up 0.4% to $1,499.17

U.S. Dollar Index down 0.2% to 98.52

Top Overnight News from Bloomberg

Trump said the first day of high-level trade negotiations between the U.S. and China on Thursday went “very well” and that he plans to meet with the top Chinese negotiator Friday

The U.K. and the European Union took a step closer to agreeing the terms of Brexit after a positive meeting between the British and Irish leaders identified a “pathway” to a potential deal. The pound jumped by the most in seven months. No-Deal Brexit to cost Ireland 73,000 jobs, central bank Says

The “jury is out” on whether the current slowdown in the U.S. economy will turn more severe amid weaker global growth and uncertainty over trade policy that’s chilling investment, according to Federal Reserve Bank of Dallas President Robert Kaplan. Federal Reserve Bank of Cleveland President Loretta Mester says U.S. central bankers should wait for fresh economic information before deciding their next policy move

The Bank of Japan’s promise to keep pumping extra money into the economy will eventually clash with its efforts to control interest rates, according to Hiromi Yamaoka, the former head of the central bank’s financial markets department. Yamaoka said the pledge to expand the monetary base until inflation is above 2% should be changed to make it easier for the BOJ to keep yields where it wants them

Asian equities took their cue from the rally on Wall Street which saw the DJIA close just below 26,500 as US President Trump said he will meet with Chinese Vice Premier Liu He. ASX 200 (+0.9%) was supported by energy and mining names, whilst Nikkei 225 (+1.2%) felt tailwind for a weaker Yen. Elsewhere, Hang Seng (+2.4%) outperformed as heavyweight financials and oil-related stocks bolstered the index amid a high-yield and firmer oil price environment. Meanwhile, Shanghai Comp. (+0.9%) swung between gains and losses with the mainland remains on-guard as sticking points remain between the two largest economies. Hong Kong Protesters reportedly are mulling whether to scale back on vandalism and violence as it risks alienating more moderate supported, according to reports. Japanese Typhoon Hagibis is forecast to be the most powerful typhoon to hit Tokyo since 1958, according to the meteorological agency.

Top Asian News

Malaysia Widens Budget Deficit Target to Weather Trade War

Tencent Gets ‘Wakeup Call’ From China’s Assertions of Patriotism

Violent Typhoon Heads for Japan, Canceling Over 1,000 Flights

Major European bourses are firmer thus far this morning as US-China newsflow remains light ahead of Trump and Liu He’s meeting at 19:45BST today; and following a positive Asia-Pac session where sentiment remained buoyed going into day two of talks. Sectors clearly illustrate the mornings heavy newsflow. With IT the notable outperformer following SAP (+7.6%) reporting earnings which were above Prev. and news that the CEO is to step down with immediate effect being well received. Also, firmer this morning are energy names following an Iranian tanker incident this morning, which is outlined in the Commodity section below. However, consumer discretionary names are suffering on the back of Hugo Boss (-13.3%) cutting their FY19 EBIT target citing persistent macroeconomic uncertainties; alongside, a number of downgrades at brokerages. Elsewhere, the FTSE 100 is this morning’s clear laggard given the recent upside in Sterling on positive Irish/UK PM comments regarding Brexit. However, in-spite of the index’s weakness the upbeat Brexit commentary has lent support to politically sensitive Co’s such as housebuilders and banks; although most recent comments from EU Council President Tusk have brought yet more urgency into the talks stating if there are no sufficient proposals today then he will have to announce there is no chance for a deal at next week’s summit. International Air Safety Panel have faulted the FAA for their certification of the Boeing (BA) 737 Max; FAA failed to sufficiently assess the MCAS system, did not sufficiently consider now design features of the craft, some regulations are out of date.

Top European News

Equinor Green-Lights $550 Million Subsidized Floating Wind

European Equities To Fall 8% in No-Deal Brexit Scenario: BofAML

Two Out of Three Options Trades Now Look for a Stronger Sterling

EU Will Discuss Sanctions Against Turkey Next Week: Syria Update

In FX, Aud/Usd has extended gains beyond 0.6750 and through the 50 DMA (0.6778) to within a whisker of 0.6800 on a wave of US-China trade optimism after day one of talks in Washington and generally positive updates from both sides on the status of trade negotiations thus far.

GBP – Yet another white knuckle ride for Sterling after a more pronounced short squeeze on Irish backstop breakthrough hype inspired by Thursday’s meeting between UK PM Johnson and Ireland’s Varadkar, and the latest catalyst came via EU’s Tusk rather Britain’s Brexit Minister Barclay or EU kingpin Barnier that have now completed their rendezvous to discuss the situation. In short, Tusk said the deadline for alternative border/customs proposals is today and as yet they have not been submitted, prompting an abrupt/sharp Pound plunge, but then revived bullish momentum by noting that promising signs from the Irish PM mean a deal can still be done. In terms of market moves, Cable collapsed to almost 1.2400 before regrouping and flying back up to 1.2500+ awaiting the debriefing from Barnier to EU states and fading just short of 1.2550, while Eur/Gbp has whipsawed between 0.8867-0.8789 and is poised just above 0.8800, but below the 200 DMA (0.8830).

NZD/EUR/CAD – All firmer vs a flagging Greenback (DXY only just holding above 98.500), with the Kiwi piggy-backing its Antipodean counterpart and climbing towards 0.6350, Euro consolidating above 1.1000 and Loonie maintaining a bid over 1.3300 ahead of Canadian jobs data and as oil prices rally in wake of an Iranian tanker missile attack . Back to Eur/Usd, decent option expiries at the 1.1000 strike may figure (1.4 bn), while tech levels could also influence trade/direction given Fibs at 1.1021 and 1.1055 and DMAs at 1.1054 and 1.0987 (55 and 21 respectively).

CHF/JPY – More safe-haven unwinding has nudged the Franc a bit nearer parity vs the Dollar and a test of 1.1000 against the single currency, while the Yen has slipped under 108.00 to expose September’s peak a fraction below 108.50.

EM – The Cnh is also anticipating good news from the President Trump-VP Lui He date at the White House that will officially close the latest round of talks, with the offshore Yuan hovering around 7.0900, but the Try has retreated in wake of US sanctions over Turkey’s military actions in Syria awaiting the EU’s response at next week’s summit – Lira back down towards 5.8750.

In commodities, Brent and WTI have been lifted this morning to gains of over USD 1/bbl at best on the back of early geopolitical newsflow that a Iranian tanker was on fire after a explosion near Saudi’s Jeddah port which led to heavy tanker damage and reports that oil was leaking into the Red Sea. TankerTrackers believe this tanker could be the SINOPA tanker which was on route to Syria and had a cargo of 1mln barrels on board. Subsequently, newsflow noted that the explosion was due to missiles and there were some reports that this originated from Saudi Arabia; however, Iran’s National Tanker Co. have denied reports that they said the missiles originated from Saudi Arabia though the Foreign Ministry confirm two hits on the tanker. The updates evidently led to a crude bid on further geopolitical tensions, particularly as reports note this is the 3rd Iranian tanker to be hit in around 6-months in this area; focus now turns to clarity on where the missiles originated from. Separately, today’s IEA report marked the end of the monthly trio where they cut their demand forecast form 2019 in stead with the other two reports. In terms of metals, spot gold was lifted above the USD 1500/oz mark on the middle-east geopolitical premium with the upcoming US-China trade talks also in focus; although it has since dropped back below.

US Event Calendar

8:30am: Import Price Index MoM, est. 0.0%, prior -0.5%; Import Price Index YoY, est. -2.1%, prior -2.0%

8:30am: Export Price Index MoM, est. -0.05%, prior -0.6%; Export Price Index YoY, prior -1.4%

10am: U. of Mich. Sentiment, est. 92, prior 93.2; Current Conditions, est. 109, prior 108.5; Expectations, est. 82.5, prior 83.4; 1 Yr Inflation, prior 2.8%; 5-10 Yr Inflation, prior 2.4%

11:45am: Bloomberg Oct. United States Economic Survey

DB’s Jim Reid concludes the overnight wrap

What does or doesn’t happen over the next few days could have major ramifications for global politics for years to come. At the start of the week things looked bleak on prospects of any kind of US/China trade deal and even bleaker on the prospect on a Brexit deal. However we close out the week with renewed hopes on both of these with the latter being the more surprising of the two.

Indeed the Irish and U.K. PM’s joint statement “agreed that they could see a pathway to a possible deal.” The Irish Times suggested that there had been “significant movement” from the UK on the customs issue. If there has been a concession on NI customs this could very easily alienate the DUP and they’ve suggested they won’t back it. However where this would become clever is if Mr Johnson agreed to back down on this and agree a deal only on the basis that the EU refuse to back an extension if U.K. MPs vote this deal down. In this scenario ironically the very people who forced the government into the Benn Act (that takes no deal off the table) would be the ones responsible for a no deal if they voted the deal down. This calculation does rely on the ERG group staying with PM Johnson and not going back to rebelling but their bar to rebel seems to be higher under Johnson than May. So far we’ve got no details from the U.K. side and only cautious positive soundbites from the Irish (a big improvement relative to where we’ve been though). However no leaked news is probably good news for now and it’s remarkable that I’ve woken up this morning with nothing on the wires to flesh out the progress. Sterling rallied +1.97% against the dollar yesterday – the most in 7 months. In terms of next steps, the UK’s Brexit Secretary Stephen Barclay will be meeting the EU’s chief negotiator Michel Barnier today as the two sides look to move closer towards a deal ahead of Thursday’s EU Council summit. A long long way to go but unexpected hope after yesterday.

Prior to the Brexit developments the mood in markets started to pick up after a tweet from President Trump just after the US open, as he confirmed he would meet with Vice Premier Liu He at the White House today at 2:45pm. The fact that the President is meeting the Vice Premier directly can be seen as a positive sign for the path of negotiations, offering hope that some sort of ‘partial deal’ of the sort that has been briefed out might be possible. After US markets had closed, Trump said that the discussions were going “very well,” helping S&P 500 futures to trade +0.37% higher this morning. As part of this reported partial deal, Bloomberg reported that the White House is looking at rolling out a currency agreement with China that they’d previously agreed before the talks broke down earlier in the year, while not going ahead with the tariff hikes planned for October 15. For their part, China is reportedly asking for no further tariff hikes, as well as the elimination of sanctions on their national champion shipping company, COSCO. The US had barred American firms from doing business with the Chinese shipping giant last month, accusing the firm of transporting Iranian crude oil.

As a final point on the trade war, it’s worth reading this report (link here ) from our US economists from earlier this week. They delve into regional data to show that the trade war has had an outsized negative effect on counties that rely more on manufacturing. Interestingly, those counties also tended to be the ones which supported President Trump more in the 2016 election, meaning there are clear political implications to the current trade war.

Trade-sensitive stocks saw the biggest gains for the second consecutive day, with the Philadelphia semiconductor index up +0.97%, while the S&P 500 and the NASDAQ closed up +0.64% and +0.60% respectively. Meanwhile bonds continued their earlier sell-off following the tweet, with 10yr Treasuries +7.9bps, and we saw another slight steepening of the curve, with the 2s10s closing +0.3bps, its 3rd consecutive move steeper. Bunds (+7.8bps) and BTPs (+8.9bps) also lost ground, with 10yr bund yields closing above -50bps for the first time in in over 3 weeks. Gilt yields rose +12.7bps, their biggest one-day increase in over a year.

The initial catalyst for the Euro government move seemed to be the FT story we mentioned as we went to press yesterday that the ECB monetary policy committee was at odds with the governing council. As we’ll see below the minutes backed up the splits at the ECB but nothing that came out yesterday should be a surprise. The market just decided to react to it more yesterday, and the selloff was given further boosts by the improvement in risk sentiment and a move higher in oil prices (+2.03%) after OPEC Secretary General Barkindo committed to do “whatever it takes” to prevent a drop in prices.

Asian markets are higher this morning on the more positive trade sentiment with the Nikkei (+1.08%), Hang Seng (+2.19%), Shanghai Comp (+0.44%) and Kospi (+1.00%) all up alongside most other markets. Yields on 10yr JGBs are up +2.7bps to -0.190%. Elsewhere, WTI crude oil prices are also up a further +0.56% and most agriculture (CBT Soybean +0.68%) and base metal (Copper c. 1%) commodity futures are also up.

Overnight we also got some Fed speak with Cleveland Fed President Loretta Mester, a hawk, saying that US central bankers should wait for fresh economic information before deciding their next policy move. She also said that she did not support the central bank’s decision to cut interest rates in July and September as her preferred strategy “was to take action only if there were evidence of a material deterioration in the outlook and not merely on heightened risks”. Meanwhile, on the Fed’s ongoing framework review, she said that she understands the argument for a so-called make-up strategy, like average-inflation targeting, for addressing below-target inflation, but says the Fed would be challenged to commit credibly to such an approach and added that it would be better for the Fed to not overreact to variations of inflation around the 2% target. Elsewhere, in an interview with the WSJ, Minneapolis Fed President Neel Kashkari, a dove, said that if data continues to come in the way it has, he will support another rate cut of 0.25%.

Back to yesterday and the positive sentiment also supported European equities, with the STOXX 600 up +0.65% and bourses across the continent ending in the green. Amidst the sterling rally, the FTSE 100 underperformed other European bourses rising only +0.28% despite the positivity in the air. Brexit sensitive stocks like U.K. financials were strong after the joint statement with the more domestically-focused Lloyds and Barclays gaining +3.89% and +2.90% respectively, while the more international and sterling-exposed HSBC retreated -1.09%.

In terms of the data yesterday, there were signs that the UK might have avoided a recession this quarter. Although monthly GDP data for August showed a -0.1% contraction (vs. unch expected), the July figures were revised up a tenth to +0.4% mom. After the -0.2% contraction in Q2, there has been nervousness that the economy would enter a technical recession, but the quarterly growth for the 3 months to August was at +0.3% qoq (vs. +0.1% expected). In spite of this, a number of the sector readings disappointed, with industrial production contracting by -1.8% yoy, the biggest yoy contraction since August 2013.

This contraction in industrial production was a theme elsewhere in Europe, with data from France also disappointing. Industrial production fell -1.4% yoy (vs. +0.1% expected), which is the biggest contraction of 2019 so far. It was a similar story in Italy, where industrial production fell -1.8%, as expected, but also the biggest yoy fall this year so far.

Turning to the US, CPI came in slightly below forecasts, with the September reading showing no mom change in prices (vs. +0.1% expected), which meant that the yoy reading remained at +1.7% (vs. +1.8% expected). Core inflation was also slightly below expectations, +0.1% mom (vs. +0.2% expected), with the yoy reading remaining at +2.4% (vs. +2.4% expected). Meanwhile weekly initial jobless claims were better than expected at 210k last week (vs. 220k expected), with the 4-week moving average ticking up slightly to 213.75k (vs. 212.75k previously).

Back to Europe, and the release of the minutes from September’s ECB meeting confirmed much of what we already knew, in that a number of members on the Governing Council had been opposed to the package of easing the ECB unveiled. Although the account revealed that “a few members” had been prepared to cut the deposit facility rate by 20bps, “in particular as part of a package that would exclude net asset purchases”, there were others who were against even the smaller 10bp cut, “as they were concerned about the possibility of increasingly adverse side effects from additional rate cuts.” With President Draghi departing at the end of the month, there’s going to be work to do in bringing unanimity back to the Governing Council under the ECB’s next leadership.

Speaking of EU leadership, France’s candidate for the next European Commission, Sylvie Goulard, was rejected by the European Parliament yesterday. She currently serves as the Deputy Governor at the Banque de France, and is the 3rd candidate for the next Commission to have been rejected so far in the confirmation hearings.

The Eurogroup of finance ministers also met yesterday, and agreed on a new common budget instrument, the budgetary instrument for convergence and competitiveness or BICC. However, this instrument is small at around 0.2% of GDP and draws its funding from the EU budget, so it does not represent a new fiscal commitment by European authorities. Also, Commissioner Moscovici, who has been watched for signals that the EU would allow countries to loosen their purse-strings this year, said “if there is a more marked downturn, we should not tighten our policies.” That’s an extremely tentative signal that the Commission would allow for easing if growth deteriorates further.

Looking at the day ahead, the data highlights include the final September CPI readings from Germany, while the main US release will be October’s preliminary University of Michigan sentiment indicator. Elsewhere, we’ll have the US import price index for September, as well as the Canada’s unemployment rate for September. Central bank speakers include the Fed’s Kashkari, Rosengren and Kaplan, along with the ECB’s de Guindos, Hernzndez de Cos and Costa. Finally, the winner of this year’s Nobel Peace Prize will be announced.