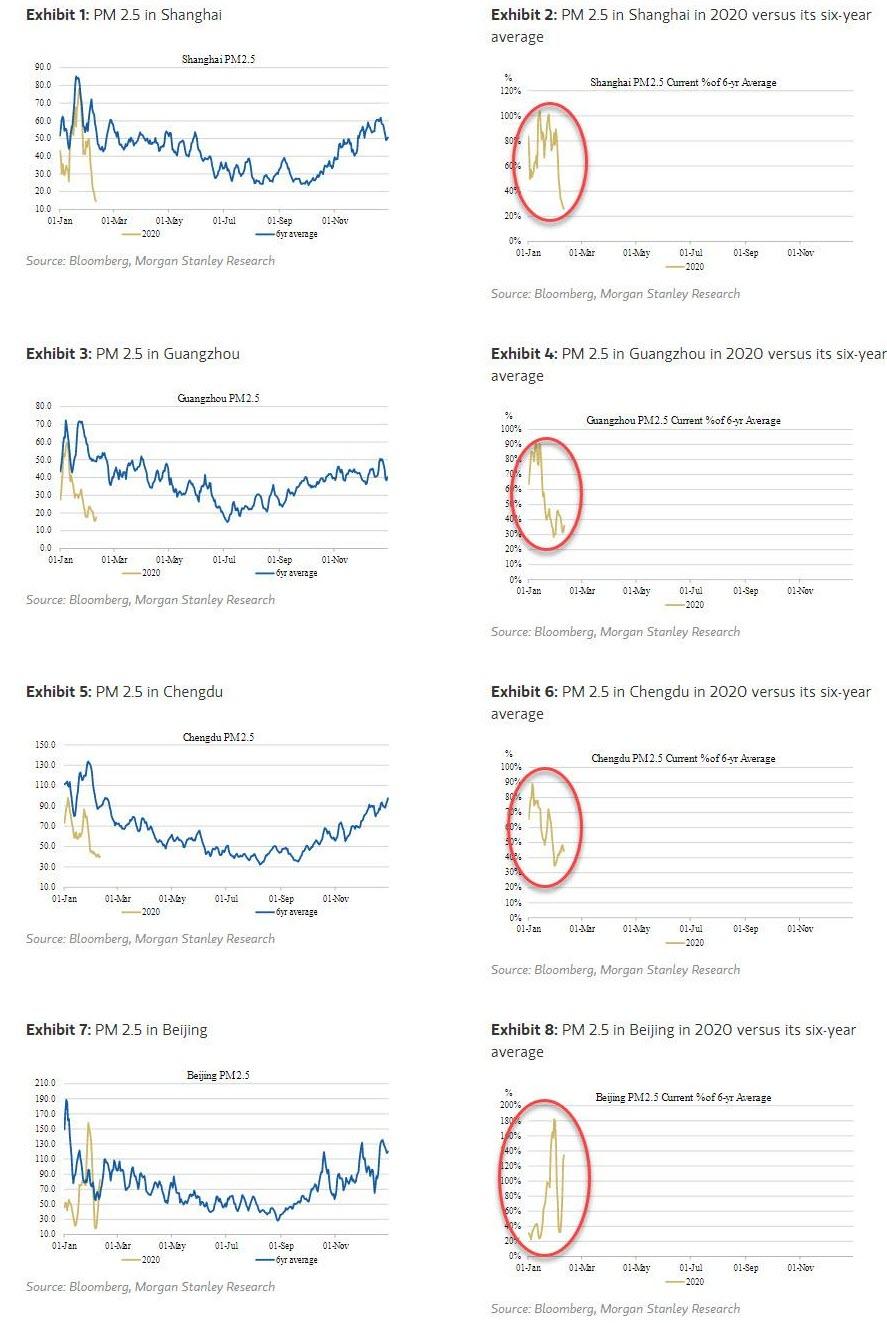

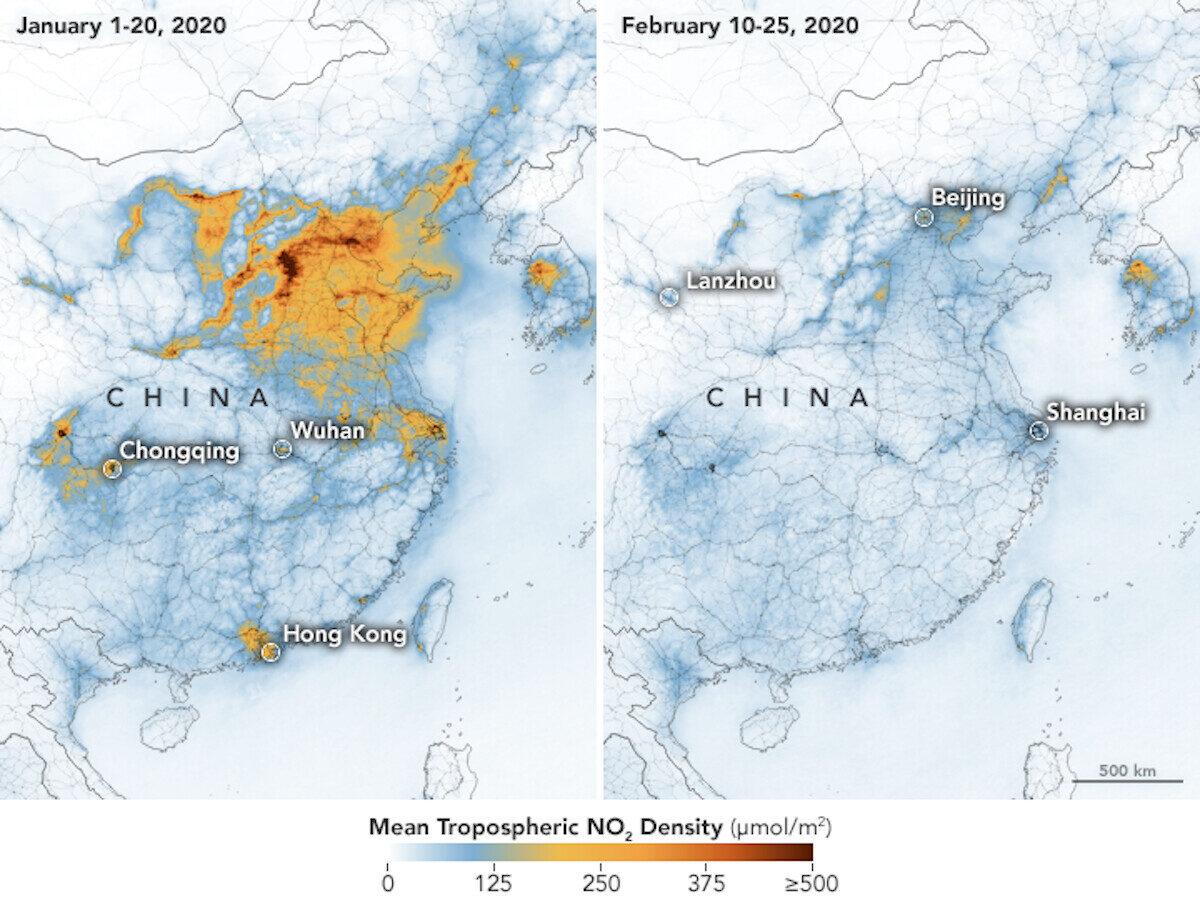

The start of the new year normally sees higher pollution across China due to higher coal/fuel consumption for heating and resumption of industrial production after Chinese New Year.

Guangzhou, Shanghai and Chengdu see a clear pattern –air pollution is only 20-50% of the historical average. This could imply thathuman activities such as traffic and industrial production within/close to those cities are running 50-80% below their potential capacity.

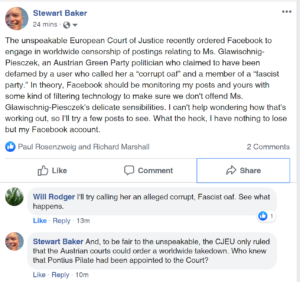

And now, thanks to satellite images published by NASA and the European Space Agency (ESA), we have further confirmation that nothing is back in China.

As The Epoch Times’ Katabella Roberts writes, the images show a dramatic drop in levels of air pollution over China following the outbreak of the new coronavirus, which forced the shutdown of industry and transport.

Images taken by pollution monitoring satellites compare air quality between Jan. 1 and Jan. 20 with air quality between Feb. 10 and Feb. 25, and show a significant decrease in nitrogen dioxide (NO2), a toxic gas that gets into the air from the burning of fuel from vehicles, power plants and factories.

According to NASA scientists, the reduction in NO2 pollution was first apparent near Wuhan, which shut down transportation going into and out of the city, as well as local businesses by Jan. 23, in order to reduce the spread of the disease.

NASA said there is evidence that the change in air pollution is “at least partly related to the economic slowdown following the outbreak of coronavirus.”

“This is the first time I have seen such a dramatic drop-off over such a wide area for a specific event,” research scientist Dr. Fei Liu said.

However, scientists also noticed the reduction in the toxic gas also spread across the rest of China and coincided with the Lunar New Year celebrations in January, which they said usually sees businesses and factories close from the last week of the month to celebrate the festival.

“This year, the reduction rate is more significant than in past years and it has lasted longer,” Liu said.

“I am not surprised because many cities nationwide have taken measures to minimize spread of the virus.”

Additionally, researchers have not seen a rebound in NO2 after the holiday and noted that in 2020, the reduction rate is “more significant than in past years and it has lasted longer.”

Of course, we only need to look at the collapse in the PMIs to know nothing is back… yet. And hope for any v-shaped recovery should be rapidly discounted as not coming anytime soon.

On the bright side, Greta must be cheering the deadly Covid-19’s spread across the world.

While Everyone Waits For Powell, Here’s What Wall Street Thinks Will Happen Next

On Friday morning, with stocks resuming their historic plunge, we said that across Wall Street, there was just one question: “Will The Fed Activate A Coordinated Central Bank Bailout On Sunday.” And indeed, just a few hours later, the Fed Chair did in fact publish an unscheduled statement in an attempy to calm crashing markets:

The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook. We will use our tools and act as appropriate to support the economy.

Unfortunately for the bulls who got steamrolled by last week’s record drop from a record high, this statement wasn’t sufficient to assure them that the Fed would indeed do “whatever it takes” to stem the bleeding. Commenting on Powell’s attempt to ease nerves, JPMorgan’s chief economist Michael Feroli said that the “statement took a page of out Greenspan’s playbook in responding to Black Monday, reminding markets that the Fed is on the job and ready to respond. This may have been particularly necessary since Fed rhetoric this week sounded somewhat unresponsive to the changing situation. Unlike Black Monday, however, the economic fundamentals may truly be changing” according to Feroli, which is ironic because just last week JPM’s head quant, Marko Kolanovic, tripled down on his bullish view of the market. Perhaps he was too concerned as being seen as wrong, than accounting for the “changing economic fundamentals”?

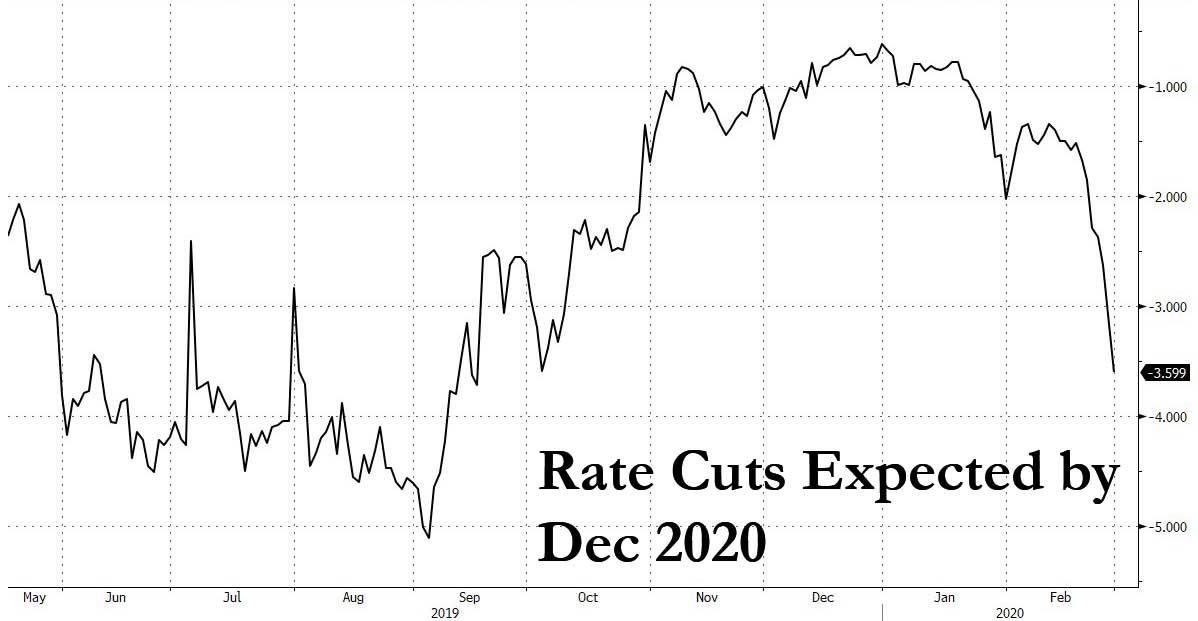

For this reason, Feroli said that “the tool most likely to be considered is the overnight interest rate target, not the discount window or some other liquidity tool”, which makes sense – the market is now pricing in more than 1.5 rate cuts on or before March 18…

… and one could come as soon as this evening. Incidentally the market is also pricing in almost 4 – or 3.6 to be exact – rate cuts by year end, which would send the fed funds rate just above 0.0%, and a second Trump administration may start off with the first ever negative interest rates in US history.

But here JPM had some bad news: the bank said it suspects “the Fed is minded to avoid going inter-meeting, if they can get away with it.” Instead, Friday’s statement by Powell implicitly acknowledges that current policy may no longer be appropriate and that a cut may be the central scenario (Tealbook alternative B) at the March meeting.

As such, Feroli concludes by comically noting that his long-standing call for a cut at the June meeting, which had looked quite dovish just a few weeks ago, “is now looking sadistically hawkish relative to market pricing.”

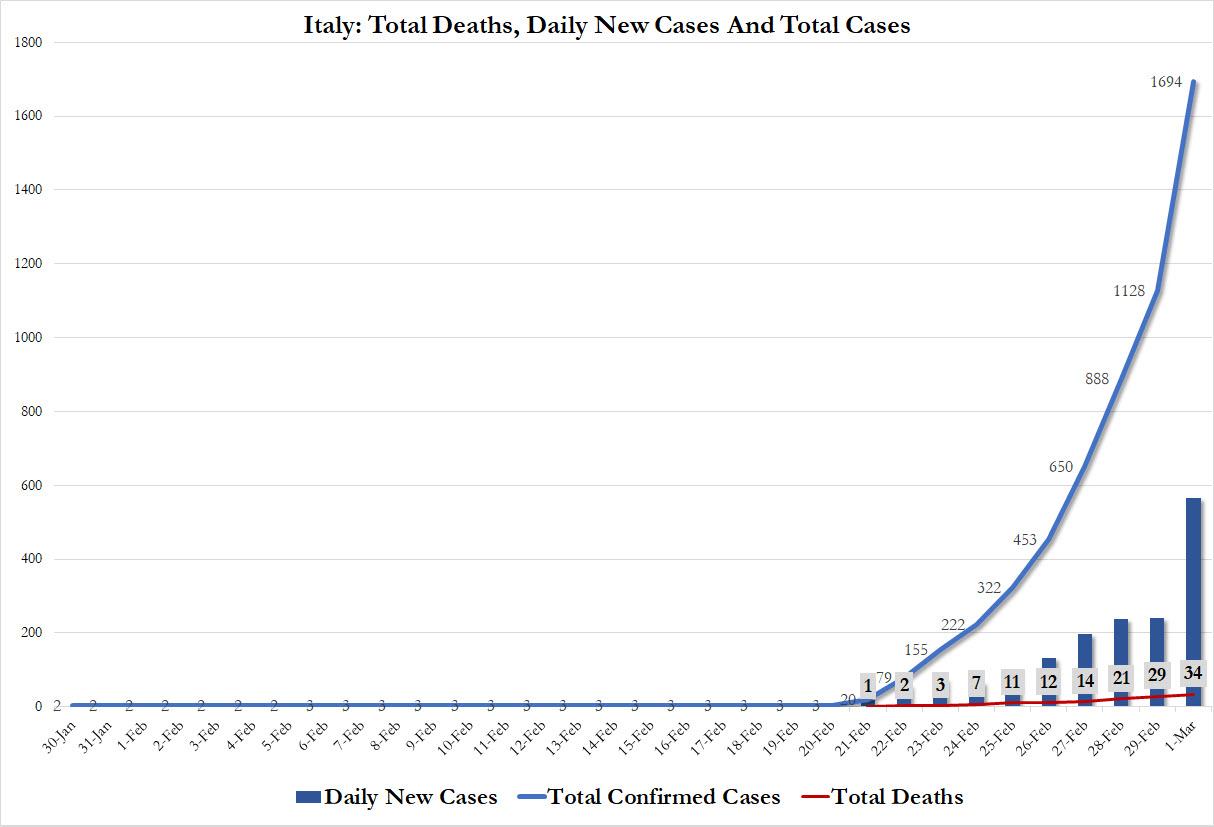

Of course, with events moving fast and furious now, the pandemic situation as of Sunday is far worse than where it was just on Friday morning, as the drumbeat of viral, so to speak, bad has only gotten more feverish: the US had its first coronavirus related death and admitted it may have a potential cluster of new cases in Washington State, Italy reported a 50% surge in new coronavirus cases…

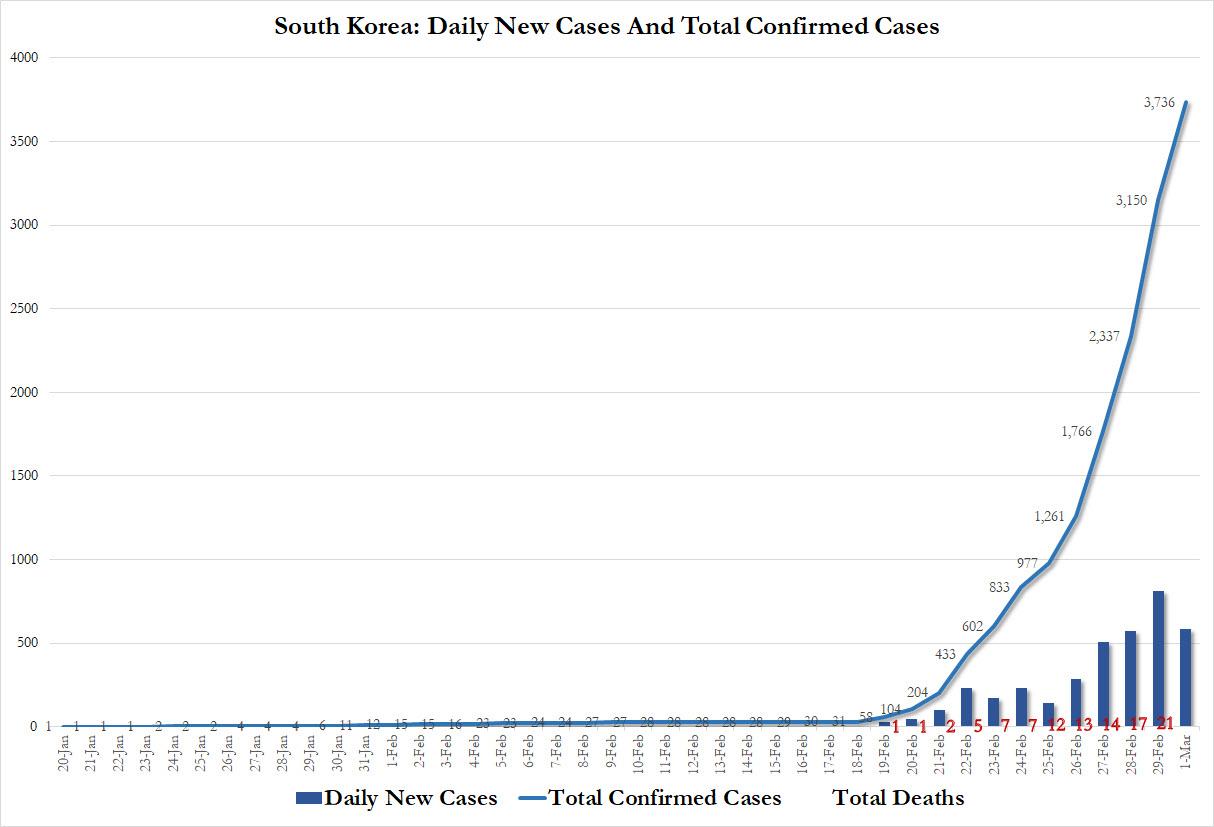

… South Korea also had a surge in new cases…

… and the U.S. and Japan issued “do-not-travel” warnings for affected regions of Italy and South Korea after the U.S., Australia and Thailand reported their first fatalities.

Even before the latest news, the market was already in freefall – despite a furious last minute short squeeze on Friday ahead of a possible Powell statement – with global stock plunging the most since the 2008 financial crisis last week, while commodities tumbled on concern the spread of the coronavirus will tip the global economy into a recession, crippling both commodity supply and demand. In the Treasury market, both 10- and 30-year yields fell last week to record lows.

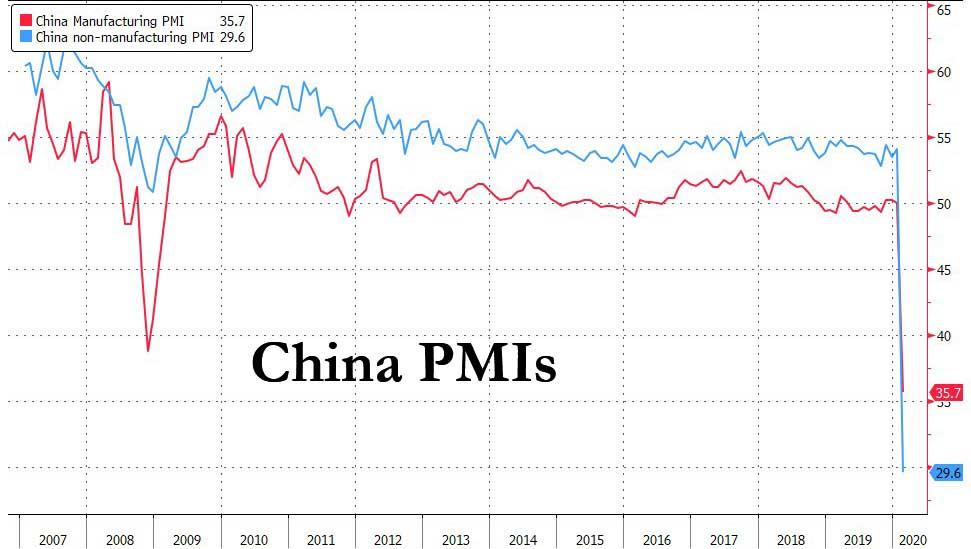

Adding insult to injury, China’s February manufacturing purchasing managers’ index plunged to 35.7 in February from 50 the previous month, much lower than the consensus estimates. The non-manufacturing gauge also fell to 29.6, its lowest ever. Both were far below 50, which denotes not just contraction but potentially recession.

Therefore it is hardly a surprise that virtually every trader is refreshing the federalreserve.gov website every few seconds ahead of what is seen as an inevitable intervention by the Fed, which has always stepped in when there was a sharp market drop in the past 11 years – why would it not do so now?

Sure, one can argue that nothing the Fed can do will actually have a positive impact on what is essentially a rapidly spreading diseases. After all just what will the Fed’s rate cuts do – it’s not like the central bank will print viral antibodies. And yet, the Fed has to do something.

This is the argument made by BMO’s rate strategist Ian Lyngen who over the weekend writes that “The Fed has been boxed into a corner and now effectively must act to prevent financial conditions from tightening even further – this much is obvious even to us. The second-order uncertainty is whether Powell’s put is a quarter-point or a half-point; and, of course, the timing thereof. It goes without saying that the Fed would rather not be pressed into monetary policy service by the market, and if it must, it would be better to do it on the Committee’s terms. This would imply a quarter-point ‘post-preemptive’ ease on the 18th. At this stage however, with the S&P down 15.8% from the peaks and the Dow off 16.5%, such a restrained effort would risk being considered insufficient.”

This, as Lyngen correctly notes, “quickly becomes a self-fulfilling paradox – the easier monetary conditions are, the more investors will require from Powell to remain in risk assets.” Critically, the viral pandemic has now become a test of the Fed’s commitment to using financial conditions as the transparency-inspired decision making policy tool. One thing is certain: there is little chance the Committee reverts to the traditional metrics of domestic growth and inflation expectations; after all, as Bmo concludes, “using those inputs not only would a rate-cut not be on the table for March, but we also wouldn’t have seen the 2019 ‘fine-tuning’ effort which resulted in 75 bp of net easing. Alas, we digress.“

So with the Fed unable to do nothing, consensus is that it will do something. The only questions are what and when?

“There is a sense the Fed will be there for markets, but a lot of that was already priced-in on Friday,” said Steven Englander, Standard Chartered Bank’s head of North America Macro Strategy. Ironically, any sharp easing by the Fed would only result in even lower rates, which could lead to even more selling especially among bank stocks, as yields now indicate a recession is virtually inevitable.

“I can see rates continuing to fall in the near term as there is no sign of a cure or vaccine,” said TD Securities chief rates strategist Priya Misra. “Even though the mortality is lower than SARS, the magnitude and geographical spread of affected people is massive. Add to that travel restrictions and fear.”

And so, with everyone hitting F5 on the Fed’s website, here is a summary of what some of the more notable Wall Street strategists are saying as we countdown the minutes to tonight’s futures reopening which – if the Fed has failed to chime in by then – could be absolutely devastating.

Jason Daw, head of emerging markets strategy at Societe Generale SA in Singapore, wrote in a note:

“Markets might be partially soothed by Powell’s statement that the Fed will act, but unlike other growth or liquidity induced market sell-offs, monetary policy could be ill-equipped to deal with Covid-19”

“Whether the market rout last week develops into a full-blown crisis is an open question (Covid-19 news flow will be critical). But the tail risk event everyone was worried about is possibly here in the form of large negative growth shock and it’s time to be prepared and dust off the crisis playbook”

“If risk assets come under continued pressure, CNY might outperform others, but ultimately there is no safe-haven EM currency in a negative growth shock”

Mansoor Mohi-uddin, a Singapore-based senior strategist at NatWest Markets:

“Risk assets will weaken Monday morning in Asia because China’s PMI data was worse than the consensus expected. If the U.S. ISM survey later in the day also falls back below 50, signaling the coronavirus was already affecting U.S. corporate sentiment in February, then financial market expectations for Fed easing before March’s FOMC meeting will increase further”

“Central banks will wait to see what the Fed does first before using their own limited ammunition”

“The market will focus more on the rapid spread of the coronavirus while Super Tuesday will be seen as a secondary U.S. risk”

Stephen Innes, the Bangkok-based chief market strategist at Axicorp:

“The fallout from the China PMI means we are starting the recovery process from a weaker level than thought. The shift from a more Asia-centric to global perspective means a more protracted economic downturn is also negative”

“Risk-free assets are getting scarce and people will view the best option to stay in cash.”

“The PBOC response should help, given the dreadful PMI. I expect much more policy front-running, with RRR cut and guidance for a 15-basis-point cut in the OMO rate.”

“Powell was unusually dovish on Friday and I expect a stream of Fed speak to confirm this pivot before Friday’s blackout period”

“The week will start horrible, but may improve on central-bank pivots, with a coordinated G-20 fiscal pump not out of the question”

Patricia Ribeiro, a New York-based senior portfolio manager at American Century Investments:

“It’s a short-term impact or challenge for the portfolio. The second half of 2020 should get better” as countries respond quickly to contain the outbreak

“The earnings-per-share numbers are still pretty high. You’re going to see a very significant slowdown in the first half of the year and then that will bounce in the second half”

“Rates are already low and that’s positive for emerging markets. It’s beneficial for consumption in all of these countries. For me, it’s less about rates coming down more in the U.S.; it’s more about not going up any time soon. If rates were to stay or be around where they are now, it’s definitely a positive”

Richard Segal, a senior analyst at Manulife Investment Management in London:

“Markets will open down a lot, but more likely because of the virus spreading in the U.S. The Chinese PMI was bad but I don’t think worse than expected. Super Tuesday in the U.S. is also a preoccupation”

“Until last week, investors were apprehensive about the virus and mainly worried about the impact on the Chinese economy given its status as the locomotive of global growth. However, the mood darkened a lot on Monday when it began to spread more widely in Italy and Korea. This led many to sell at any price and ask questions later”

“The mood shifted from hoping it could be controlled and contained to expecting the worst. Mainly though, markets are searching for a new base”

Divye Arora, a portfolio manager at Daman Investments in Dubai:

“Given the increasing spread of virus in the West, we expect global equity markets to remain under pressure. However, the pace of decline would be much lower versus last week as markets seem to have priced in a significant amount of uncertainty in the form of lower consumer demand, travel and supply chain disruptions”

“We also expect some institutional investors to start buying the dip on expectation of fiscal and monetary stimulus, virus spread being more contained in the West versus China due to the timely response from the respective health authorities and declining supply-chain disruptions in China. Overall people will continue to diversify into safe-haven assets such as U.S. treasuries, gold and the U.S. dollar”

Edward Bell, a commodity analyst at Emirates NBD in Dubai:

“The virus has just begun to become rooted in other markets such as Italy and, while the economic hit may not be as sharp as in China’s case, it will nevertheless be significantly negative”

“The fixation for oil markets this week will be the OPEC meeting taking place on March 5, followed by a meeting with partners outside the bloc the next day”

Despite the collapse in prices, speculative net longs in both Brent and WTI rose last week as investors may have expected crude prices to have hit a bottom

“As many of these new long inflows will have burned by the price decline last week we may see another round of selling pressure in the coming days if doubts grow about how committed OPEC+ is to limiting production”

Han Tan, a Kuala Lumpur-based market analyst at FXTM:

“Equities are set to continue hogging the limelight over the immediate term. Although a lot of the coronavirus-related pessimism has been discounted over recent sessions, investors will be wondering if the correction may eventually give way to a bear market, though perhaps not at the same ferocious pace that we saw last week”

“With China reporting its lowest ever manufacturing PMI, the hard economic data from around the world is not expected to provide enough resistance against the rising tide of risk aversion in the markets”

“The risk-off theme is expected to remain dominant, until the coronavirus outbreak can show material signs of stabilizing”(Updates with currency market open)

Finally, courtesy of Macrohive’s George Concalves, here is a twitter thread describing where the Fed finds itself and what its options are:

Many investors are expecting Fed (coordinated or not) to do something soon (perhaps before futures open). There has been a lot of debate that CB easing can’t resolve health issues, but they can help sentiment. Here’s what may happen next.

Backdrop1: Long gone is the façade the Fed will ignore sliding financial conditions (regardless of driver). Its not much, but the Fed has some flexibility on rate policy side but more importantly can come up w/some creative solutions in its use of the powers granted under 13 (3)

Backdrop2: One of the reasons why the Fed needs to be preemptive is because some of its crisis fighting abilities have been damped post GFC due to Federal Reserve Act section 13(3) revisions per DFA. That said, from what I understand they could still launch ABC facilities.

Backdrop3: In the early days of GFC the Fed resorted to tweaks versus all out easing measures or launching new facilities. In August 2007 it cut the discount rate and not the FF rate and in Jan-2008 did a 75 bp intra-meeting ease (followed by another 50bp at the meeting).

Old School Fed: I found this Min-Fed posting (see tinyurl.com/rgyeklr) as a good historical review of potential Fed crisis fighting usage of section 13(3), also see link at the end “Lender of more than last resort” for how the discount window evolved, more later…

Old Fed playbook1: In the ’02 Bernanke report on deflation (see tinyurl.com/qmyto8g) he provides a laundry list of what they can do to stimulate the economy/markets. We have pretty much done all of them except for buying foreign bonds. Meanwhile Fed can buy munis too.

Old Fed playbook2: Since September 2019 the Fed has been providing liquidity with TOMO repo operations and TRM bill purchases (ie notQE). At a minimum the Fed will be inclined to keep these programs for a while longer (and abort tapering repo) while introducing new tools.

New Fed playbook1: In my view there is a risk of an intra-mtg ease (as early as today vs allowing mkts to freefall). First off this is a public health concern, but COVID disruptions run the risk of hitting biz CF/working capital. The Fed can encourage discount window use.

New Fed playbook2: Given JPM & Quarles want to break the DW stigma (see tinyurl.com/qqpbkzx) Fed could announce it reduces the DW rate to 25bp or even 0 over FF (vs 50) for large banks, maybe further for smaller banks if funds are used to help industries hit by COVID

New Fed playbook3: 17 days is a long time to wait for levered investors, so expect FF rate to come down 50bps too (would make DW rate cut be 75-100bp). The Fed could gauge how these measure work as well as monitor COVID into 3/18 where it could always do more if needed.

DEFCON1: Its too early to forecast COVID’s eco-impact and if there is multiple waves. But Fed is on track to move to DEFCON1 in table (see tinyurl.com/sq65skd) if so they will end up with new ABCs, ZIRP (with tiering) eventual YCC, & credit easing (MBS, CP, & munis).

Coronavirus Has Reached ‘Community Spread’ Within United States: Dr. Anthony Fauci

Dr. Anthony Fauci – the director of the National Institute of Allergy and Infectious Diseases (who Joe Biden falsely claimed was being ‘muzzled’), said on Sunday that “community spread” of the new coronavirus in which cases cannot be directly traced to anyone are becoming more common throughout the United States.

As Fox News notes, the term “community spread” is defined as an infection with an unknown origin, or ‘index case,’ as opposed to most of the early coronavirus cases which could be clearly traced from travel or contact with known patients.

According to Fauci, this comes as no surprise.

“This was something that was entirely expected when you have diffuse infections throughout the world – as you’ve just mentioned, South Korea, Iran, Italy, in places like that – sooner or later there are going to be cases in your country that you can’t directly trace to anyone,” he said in an Sunday interview with Fox & Friends Weekend. “That becomes much more challenging about identifying the source.”

Cases such as those in Washington state and Oregon (which may be far more widespread than we know) require officials to do “much more intensive contact tracing in addition to the isolation,” he added.

Fauci, who is also director of the National Institute of Allergy and Infectious Diseases, went on to address whether it is appropriate to compare the coronavirus with the seasonal flu.

“Yes and no,” Fauci said, cautioning that the comparison is suitable in some respects, but not in others.

“It clearly is much more lethal, if you want to call it that, than the typical seasonal flu,” he said. –Fox News

The mortality rate of the flu is around 0.1%, while coronavirus’ mortality rate is approximately 2 to 2.3%, according to Fauci – who suggested that the number might be lower if the total number of cases could be accurately assessed.

Fauci added that coronavirus will mostly affect older people with underlying health conditions, but that infections in young, healthy individuals can still occur.

Print your way to prosperity, what could be simpler? Only those who profoundly hate humanity could embrace the idea…

There is nothing new under the sun

Modern Monetary Theory, or “MMT”, has been getting a lot of attention lately, often celebrated as a revolutionary breakthrough. However, there is absolutely nothing new about it. The very basis of the theory, the idea that governments can finance their expenditures themselves and therefore deficits don’t matter, actually goes back to the Polish Marxist economist, Michael Kalecki (1899 – 1970).

MMT as a centralisation tool

MMT says that the national debt means that we owe the money to ourselves, so the central bank in combination with the approval and blessings of the political branch can now together spend as much as they want without facing any consequences. In other words, we can print our way to prosperity. The only real problem according to the theory is that there is not enough money and not that resources are scarce and therefore limited. To understand the basic idea behind this, let’s use the game “Monopoly” as an example. If players decide to double the amount of monopoly-money to play with, the logical outcome will be that people start to pay much higher prices e.g. for the same amount of locations. Whenever more money is chasing the same amount of goods, prices will rise. Another lesson is that the bank will always win, especially when it has the power to change the rules at any time during the game.

The main cause for most of the problems of our days is the current central banking system. But how many people have ever thought about what money is, or how did it came into existence? How many know whether it was always used a debt security by government declaration or if it once was a property title, as it still pretends to be? Well, I can tell you that over the past decades, I haven’t met a lot of people who really thought about these questions. At the same time, our public education system and the mass media ensure that the next generation won’t think about them either. Meaningless distractions, alternative facts and daily doses of fear effectively crush most inquisitive instincts. It’s a process that Immanuel Kant recognized a long time ago and described in the following way:

“First, these guardians make their domestic cattle stupid and carefully prevent the docile creatures from taking a single step without the leading strings to which they have fastened them. Then, they show them the danger that would threaten them if they should try to walk by themselves. Now this danger is really not very great; after stumbling a few times they would, at last, learn to walk.”

However, examples of such failures intimidate and generally discourage all further attempts.”

With MMT, a massive shift in terms of centralization of power will take place. Drastic changes in our current system would be possible, with a massive push away from the private sector and from individual freedom towards more government control. This is extremely dangerous. History is our witness that centralization in the hands of government, particularly when coming from a so-called “morally superior” ideology, never had a good outcome for the people. State officials, institutional actors and those closest to the top of the power pyramid were the only ones to ever benefit from such systems.

MMT essentially gives carte blanche to those interest groups to boost government spending to astronomical levels. At the same, it allows within a very short period of time a government-enforced, massive redistribution of wealth and a gigantic misallocation of capital.

Over the next few years, the biggest growth potential anywhere in the market, besides the military-industrial complex, will be found in everything that is related to climate change. You can be sure that governments will just print massive amounts of money and flood this sector with it, where you will find a tremendous number of formal politicians and bureaucrats creating artificial and well paid government-sponsored jobs. The European Union alone wants to spend EUR1 trillion until 2030 on this new sector. If Trump loses the next election, Americans can also be sure that MMT will finance the same moves over there too, most likely with the “New Green Deal”.

Let me quote Joan Robinson, who used to be a friend of Kalecki, MMT’s inspirer, during his days at Cambridge University. She summarized his theory as follows: “the workers spend what they earn and the capitalists earn what they spend”. Interesting, isn’t it? This is how the original Marxist thinkers defined capitalism. You might have understood that in their eyes the individual is the worker and when everything is under government control, the politicians and bureaucrats become the real capitalist. This is exactly the opposite of my understanding of capitalism, which is also only possible in a free and decentralized society. Of course, it is important to understand that the term “capitalism” has been purposefully misdefined and hijacked from the beginning by Marxist thinkers.

Far-reaching consequences

MMT, also conveniently facilitates other dangerous policies and ideas, that so far seemed unrealistic, like Universal Basic Income and “helicopter money” that have been particularly propagated by government-sponsored economists for the past few years. It sounds pretty cool that people will not have to work to make a living – they can lay back and enjoy money for free provided by the government. But as we all know every coin has two sides, and to me as a fan of history, and monetary history in particular, an old saying comes to my mind: “Gold is the money of kings, silver is the money of the bourgeoisie, barter is the money of peasants – and debt is the money of slaves.”

It would seem that the only thing history actually teaches us is that we learn nothing from it. Nevertheless, there is hope, due to the decentralized and open-source internet and the increasing connectivity and access to knowledge. These ensure the competition of ideas, the emergence and evolution of different schools of thought, and the means for millions of people to learn about the world and to become conscious individuals with their own opinions. In addition to that, our financial system is also being challenged and pushed towards a more positive and healthy direction, as hard assets, blockchain applications and cryptocurrencies are laying the foundation for a decentralized approach, where financial sovereignty is key and privacy is respected.

For now, however, we still live in a two-class society, divided between those who have to pay taxes and those who live off them. As you can imagine, the above-mentioned changes and shifts are not welcome by government and its servants. They see a return to a culture of public debate, based on respect and on the premise that we can “agree to disagree”, with the humble understanding that no one knows the truth, as a threat. Therefore they enforce a de-industrialization agenda in combination with mass-migration, using the climate hoax as an excuse to speed up a cultural suicide. They prefer to have a monoculture and are against the amazing beauty that lies in complexity, in different cultures, in different regions, with different languages and beliefs. By splicing it all together, they destroy all of them at once.

At the end of the day, what MMT, the Green New Deal, QE, NIRP, Helicopter Money or any other sort of government promise or intervention have in common is that they are all collectivistic by definition, aimed against the individual and based on the crazy findings of the “Economic School of Zimbabwe” – where everyone became a trillionaire. Henry Hazlitt described it best, in his “Marxism in One Minute“:

“The whole gospel of Karl Marx can be summed up in a single sentence: Hate the man who is better off than you are. Never under any circumstances admit that his success may be due to his own efforts, to the productive contribution he has made to the whole community. Always attribute his success to the exploitation, the cheating, the more or less open robbery of others.

Never under any circumstances admit that your own failure may be owing to your own weakness, or that the failure of anyone else may be due to his own defects — his laziness, incompetence, improvidence or stupidity. Never believe in the honesty or disinterestedness of anyone who disagrees with you.

This basic hatred is the heart of Marxism. This is its animating force.”

Coronavirus Was Spreading In Washington State For 6 Weeks, Infecting Up To 1,500, Study Finds

Last night the US got its first dose of really bad coronavirus news, when Washington State announced it was the site of the country’s first coronavirus death on Saturday, while additionally reporting that two confirmed cases of covid-2019 were confirmed at a long-term care facility in Kirkland, Washington, prompting the state to declare a state of emergency, even as President Trump issued new foreign travel warnings and restrictions on Saturday afternoon in an effort to stop the spread of the virus, while also urging calm among members of the public.

There was worse news: researchers who studied two cases in the state say that the virus may have been spreading there for weeks, suggesting the possibility that up to 1,500 people in the state may have been infected. Specifically, the researchers compared two cases to learn more about how the coronavirus spreads. The viral mutations suggest that it has been spreading in the state for close to six weeks, according to one of the scientists who compared the sequences, Trevor Bedford, an associate professor at the University of Washington.

If that is true, it could mean that 150 to 1,500 people “have either been infected and recovered or currently are infected now,” said Mike Famulare, a researcher at the Institute for Disease Modeling in Bellevue, Wash., who performed the analysis. Those cases, if they exist, have thus far been undetected.

And most problematic of all, many of those people might not yet have symptoms even if they are contagious. Dr, Famulare characterized his estimate of community cases as a “best guess, with broad uncertainty.” Another method, based on census data and estimated sampling, produced similar results, he said.

This case, WA2, is on a branch in the evolutionary tree that descends directly from WA1, the first reported case in the USA sampled Jan 19, also from Snohomish County, viewable here: https://t.co/gxyo0PsJ7x 2/9 pic.twitter.com/LBH26A0AFC

It’s possible that this genetic similarity is a coincidence and these are separate introductions. However, I believe this is highly unlikely. The WA1 case had a variant at site 18060. This variant is only present in 2/59 viruses from China. 4/9 pic.twitter.com/Rb9N5uvgwg

I believe we’re facing an already substantial outbreak in Washington State that was not detected until now due to narrow case definition requiring direct travel to China. 6/9

An update, because I see people overly speculating on total outbreak size. Our best current expectation is a few hundred current infections. Expect more analyses tomorrow.

Through Sunday, there were only 71 confirmed cases in the United States, although that is mostly a function of testing limitations; over the weekend the Food and Drug Administration announced that testing for the coronavirus would be greatly expanded in the country, a move that is expected to improve the pace of detecting infections and help identify patterns of suspected or confirmed cases. It may also result in hundreds if not thousands of new confirmed cases, and has already prompted a furious hoarding of provisions in what may be a harbinger of the panicked response that could descend upon the nation once the CDC admits there are thousands of domestic cases.

Telling people their lives suck is no way to win an election. As James Carville says, they’re losing their damn minds…

The chaos of the primaries, the lack of a clear party vision in the last debate – are Democrats a progressive party, a party of moderates, a plaything for billionaires, or just people sniping each other for virtue points? It is time for concern.

Politics is always about the biggest story you tell and how voters see themselves in that story. If the Democrats lose in November, one of the main reasons—and the competition is strong—will be that they’ve gotten trapped inside a set of false narratives. Or they’re, in the words of James Carville, “Losing our damn minds.”

Think how powerful the narratives of “Morning in America” and “Hope and Change” were, and contrast those with the Dems’ “things suck more than you realize, people,” and you see where this is headed.

At the top of the list is the economy. The Democratic narrative is that the economy is bad, with a recession just around the corner (or maybe the corner after that, keep looking). Yet outside the debate hall, 59 percent of Americans say they are better off than they were a year ago. Overall quality of life is satisfactory for a massive 84 percent. Unemployment is at historic lows. Wages are up a bit.

The reality is bad enough for Dems. But the narrative problem is that they’re confusing a strong economy with economic inequality. The economy does benefit everyone, but it benefits a small percentage at the top much more. They have not gotten this message across to an electorate that is happy to have any job, content with some rise in wages, and, for the half of Americans who own some stock, want to see just enough growth in their 401(k) to suggest at least part of retirement won’t be dependent on canned soup being on sale. The Dems are running on a narrative that the economy is failing; Americans believe that if it is failing, it’s failing less than it did before, and that’s good enough.

Holding Democrats back is their false narrative of all-you-can-eat white privilege. Economic inequality across America is not primarily racial, though it does have a racial component. But Dems are still telling the same old story, as if whites across the Midwest have the same union factory jobs that raised them and blacks never did. The powerful message of “we’re all in this together” is being thrown away for black victimization narrative votes that may or may not turn out on Election Day.

Dems also insist on lumping blacks, Hispanics (30 percent of whom support Trump), Chinese, and everyone non-lily into “People of Color,” a classic case of one size fits none. It would be an award-winning SNL skit to watch Larry David’s Bernie try to convince a Chinese friend, a medical doctor with kids in the Ivies, that as a “POC,” his personal concerns have significant crossover with what’s happening to a guy uptown as played by guest host Samuel L. Jackson. It’s about money, stupid, not color.

Dems seem to be working this narrative into the ground in an effort to alienate as many voters as possible. Poor whites, too meth-addled to see Trump making false promises, deserve to be replaced by driverless delivery trucks. Poor blacks, it’s not your fault, because racism. Everyone else not white, whatever, go with the black folk on this one, ‘kay? An issue that could unite 90 percent of Americans gets lost. And if you don’t agree racism is the root cause of everything, from “top to bottom,” as Bernie says, well, you’re a racist! James Carville says for the Democratic Party to win it has to drive a narrative that “doesn’t give off vapors that we’re smarter than everyone or culturally arrogant.” Instead the strategy seems to be Dems turning from criticizing ideas to criticizing voters.

Much of the rest is a mighty credibility issue for the Dems. They have stuck with so many proven false narratives so long, no one believes them anymore. Trump did not work with Putin to get elected, yet Maddow on MSDNC is still pushing something similar even today. Do we really need to talk about how few Americans cared so little about impeachment? Trump did not start World War III. Roe v. Wade is still firmly the law.

But the transpeople! Dems have clung to the narrative that trans rights are somehow a major issue among voters. Biden tweeted, “Let’s be clear: Transgender equality is the civil rights issue of our time.” While most voters want to see transpeople treated decently, there is no national election issue here. Same for all the other virtuous baggage Dems drag around the social media. For example, rights and benefits for illegal immigrants. It makes them seem out of touch with mainstream America, a particular liability in an election likely to hinge on purple voters in swing states.

Dems also cling too hard to the narrative of Barack Obama. Maybe he deserves accolades for this or that, maybe not, but that the guy who seems to be the talk of the Democratic Party isn’t one of the people on the ballot does not indicate strength. Barack’s and Michelle’s formal portraits are touring the nation, apparently so Democrats can worship them like artifacts from some lost cargo cult, a “communal experience of a particular moment in time,” according to the National Portrait Gallery. Five equally desperate candidates, with Biden in the lead Art Garfunkel role, are airing ads featuring St. Barack.

Health care is a kitchen-table economic issue. A majority of Americans, regardless of party affiliation, rank cutting health care and drug costs as their top priority. That polls as far more important than passing a major health system overhaul like Medicare for All. Americans are not interested in converting the entire economy over to some flavor of socialism just so they can see a doctor. The bigger the change the Dems sell, the more it frightens people away.

Same for all the other free stuff Dems are using to troll for votes (college, loans, reparations). Each good idea is wrapped in a grad school seminar paper requiring America to convert its economy from something people have grown to live with into something they aren’t sure they understand. It is a hell of a narrative: Democrats turning an election against Trump into a sub-referendum on socialism lite at a time when Americans’ personal economic satisfaction is at a record high.

“We have candidates talking about open borders and decriminalizing illegal immigration. You’ve got Bernie Sanders talking about letting criminals and terrorists vote from jail cells. It doesn’t matter what you think about any of that, or if there are good arguments—talking about that is not how you win a national election…

By framing, repeating, and delivering a coherent, meaningful message that is relevant to people’s lives and having the political skill not to be sucked into every rabbit hole that somebody puts in front of you.”

Where once you had hope and change, now there’s the always exasperated Warren, the out-of-breath grumpy Bernie, that frozen Pete grin, Steyer giving his TED talks, Biden looking like the last surviving member of a rock band playing a Holiday Inn gig remembering when he and Barack once filled arenas, man. And now, Mike Bloomberg, cosplaying a Democrat. Oh well. The Beto revival of 2024 isn’t that far away.

If I were writing ad copy for the Republicans, I might try this: “Voters, do me a favor. Look out the window. Do you see a republic on the edge of collapse, Rome, the U.S. in 1860? Is your life controlled by an authoritarian? That’s what Democrats say is out there. But you don’t see that, do you? You see more people with jobs. You have a little more. And more kids down the block are home from war than are gearing up to fight in places like Libya and Syria that none of us really care about. Your choice is pretty straightforward at this point. Have a good night, and a good day at work tomorrow.”

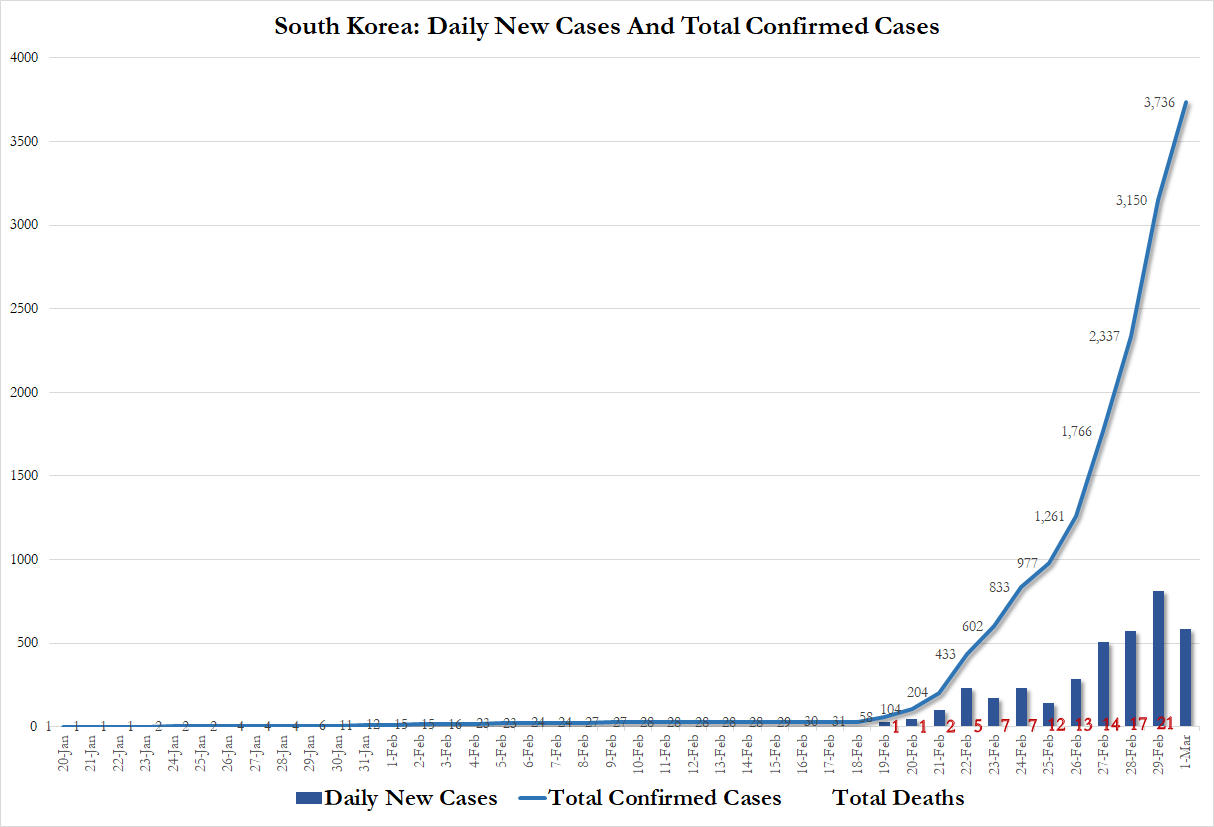

South Korean Cult Leader Faces Murder Investigation Over Church’s Role In Coronavirus Outbreak

The leader of the Christian “doomsday cult” at the center of the outbreak in the South Korean city of Daegu is now facing a murder investigation as the country’s death toll from COVID-19 hits 21, the BBC reports. The push for the investigation comes as public fury toward the church has exploded thanks to its role in sparking the Daegu outbreak.

City officials in Seoul have asked prosecutors to charge Lee Man-hee, the messianic founder of the Shincheonji Church, along with 11 other church leaders, with murder after a member of the church became South Korea’s biggest “super spreader”, infecting dozens of others and kicking off the country’s outbreak in earnest just as public health officials were beginning to suspect that the virus was fizzling out.

The 61-year-old woman attended multiple church services because she believed she was only suffering from a bad cold, having not left the country recently. The woman also reportedly made frequent trips to Seoul. She initially refused to be taken to the hospital to be tested, though reports claim she had visited early in her illness, before it was apparent that she may have been infected with the virus.

Somehow, doctors didn’t catch the virus the first time she visited the hospital.

South Korea has reported 3,730 cases and 21 deaths, the biggest outbreak outside mainland China. More than half of the patients are members of Lee’s Shincheonji Church. It’s believed that church members infected one another after leaders urged members not to report symptoms.

Officially, all 12 church leaders have been charged with homicide, causing harm and violating the Infectious Disease and Control Act.

All 230,000 members of the church have been interviewed, and nearly 9,000 have shown symptoms of infection. The government plans to test every member for the virus. Church founder Lee, who claims to be Jesus Christ returned to earth, is awaiting the results of a test to see if he has the virus. Shincheonji means “new heaven and earth” and the group was founded by Lee in 1984. It has members across Asia, including in Wuhan. The church claims to have more than 20,000 followers outside South Korea.

The government has shuttered all Shincheonji churches across South Korea. Additionally, Roman Catholic churches, major Protestant groups and even the Buddhists have cancelled church or religious gatherings.

One helluva weak week for the stock market. Three of the five largest Dow point flops in history. Yes, we have already been lectured like a little schoolboy by the Twitterati geniuses “it is the percentage drops that count.” No shit.

Cheap? You gotta be fricking kidding me. Not even close. Look at our favorite valuation metric – market cap-to-GDP. But, interest rates are going to zero, yada, yada, yada! That is not exactly a positive, in our opinion.

Note the above chart is a ratio of the total stock market capitalization to nominal gross domestic product (GDP) and cannot continue to move higher forever. It gyrates from an upper limit of extreme overvaluation to the lower limit of extreme undervaluation.

Oversold? Yes, and the S&P finally carved out a daily green candlestick, to close higher than its opening trade… but weekend trading suggests that is all gone already…