Rabobank: “Things Are Getting Real… Everywhere You Look, Decades Are Happening In Weeks”

Tyler Durden

Mon, 06/01/2020 – 09:45

Submitted by Michael Every of Rabobank

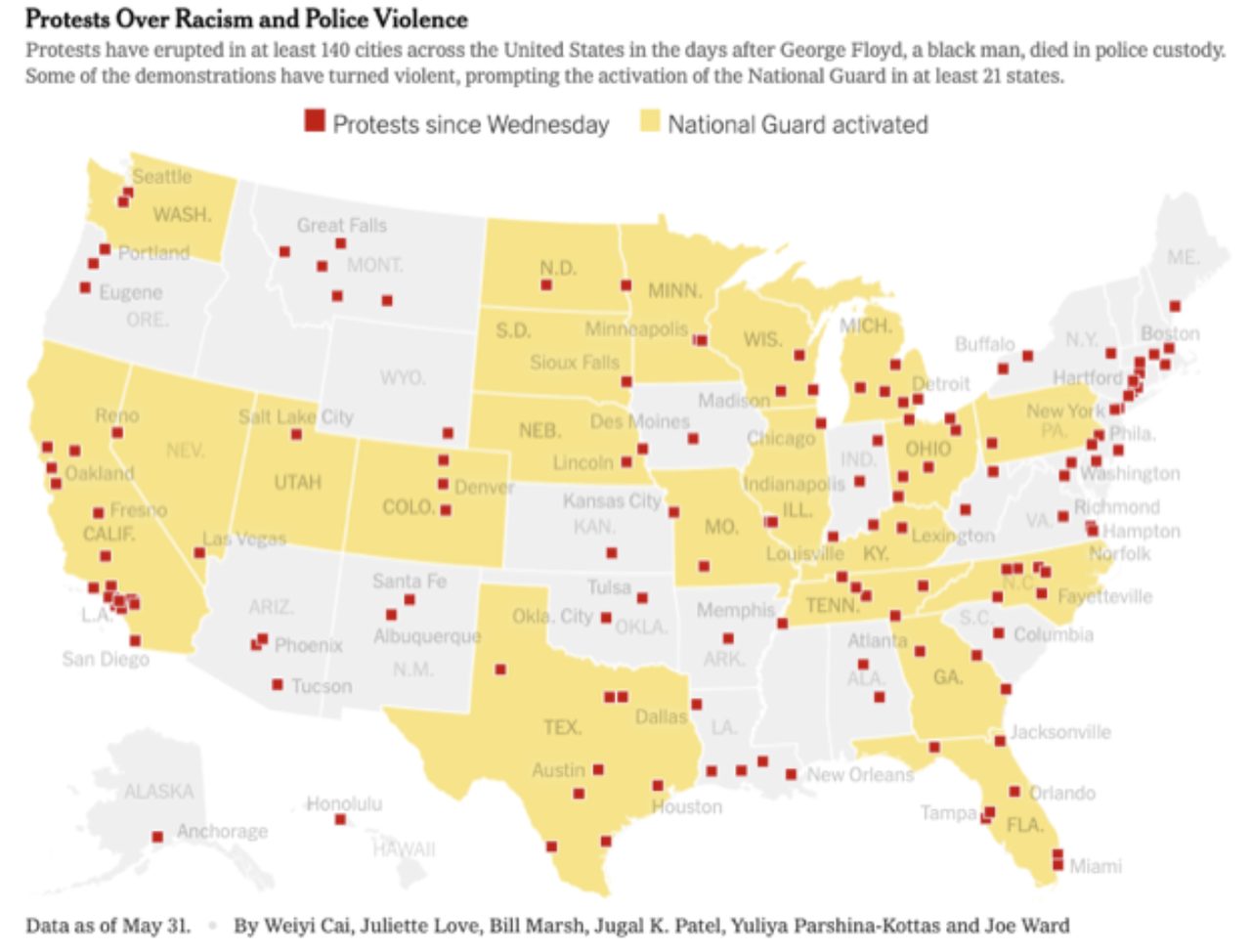

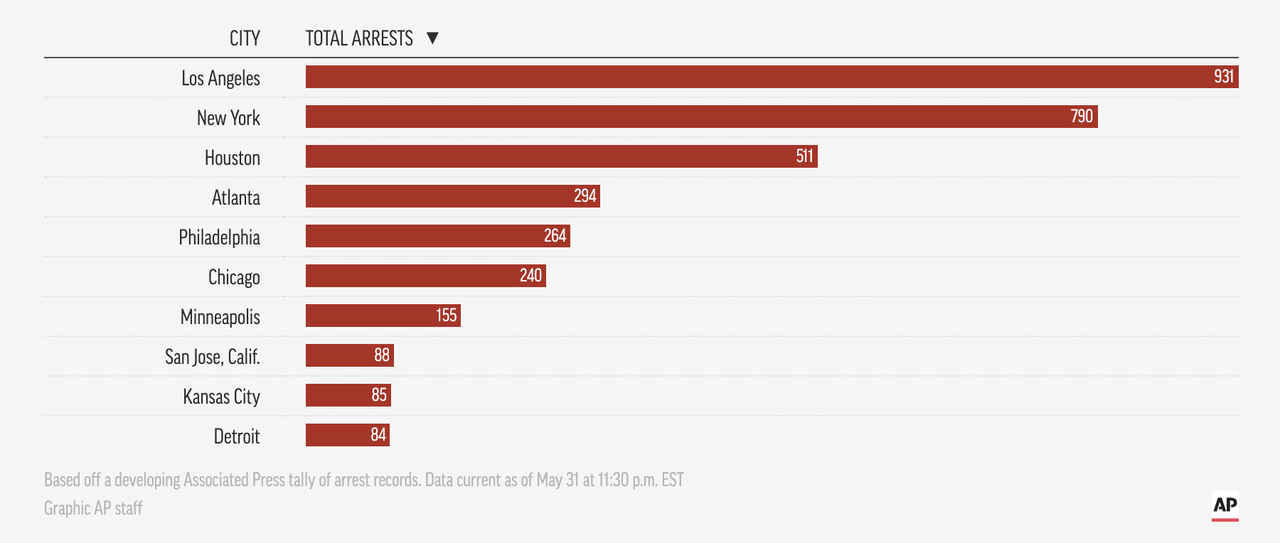

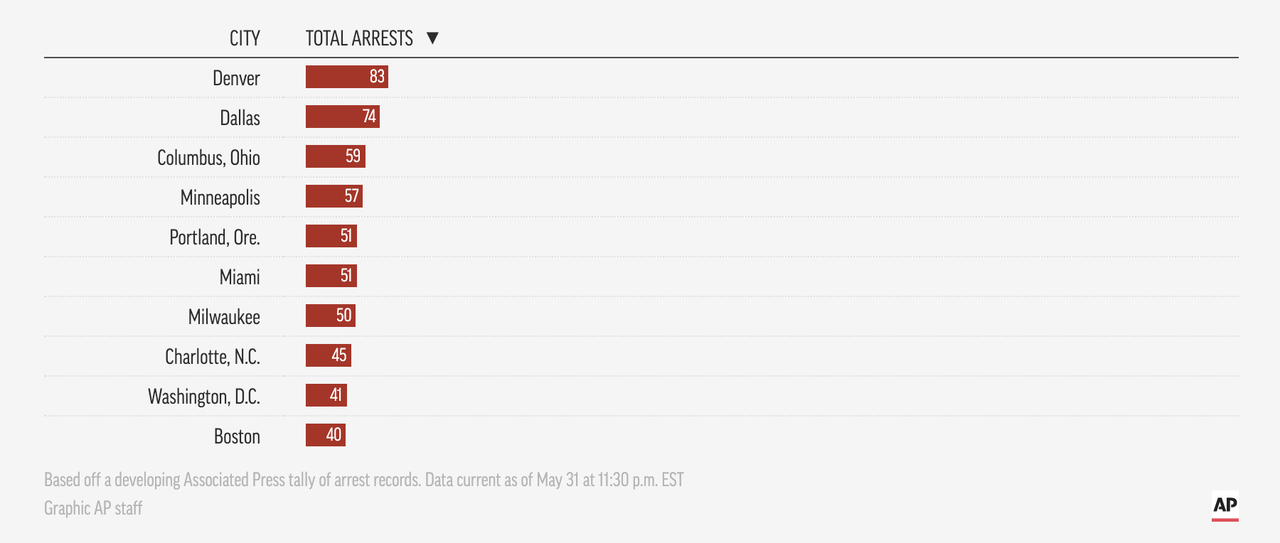

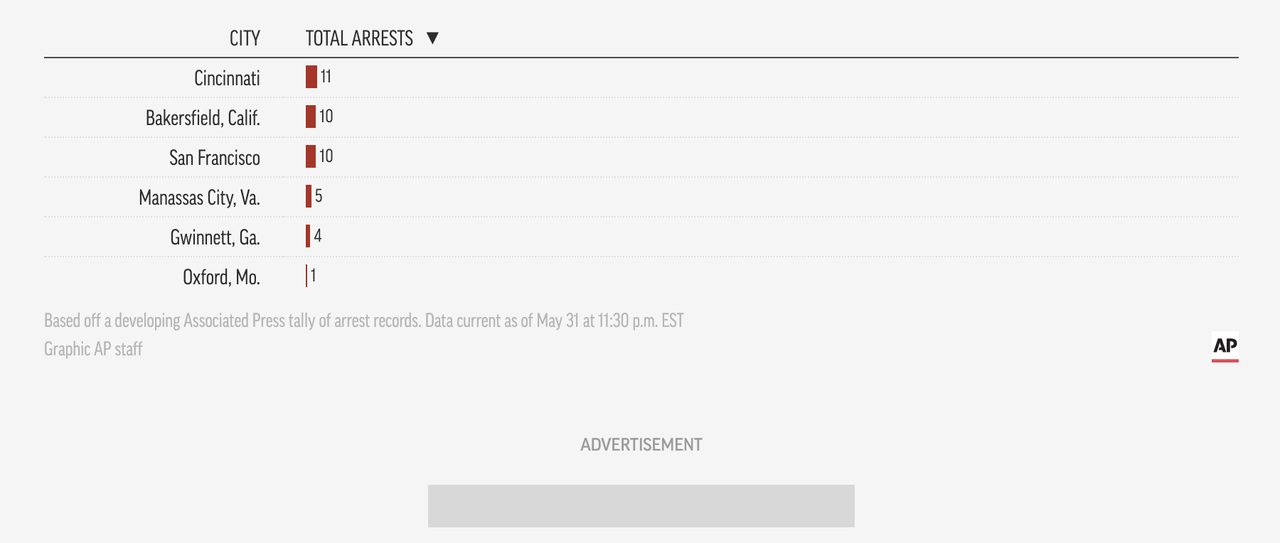

“There are years where nothing happens, and there are weeks where decades happen.” So said Lenin, who knew a thing or two about revolutionary times. The US faces its worst protests/riots since 1968, which are whipped up by the far right, or the Russians, or ANTIFA –newly-designated as a terrorist organisation by President Trump– depending on what you read. The editor of China’s Global Times has trolled this must be Hong Kong protestors at work – with no Twitter fact-check; certainly Hong Kong’s “If we burn, you burn with us” fits the real rage on display. So should markets think not of the end of lockdown but the start of breakdown? (We have certainly swapped quarantine for curfew in many places.) Perhaps – but 1968 and 1992 were both followed by the usual US exceptionalism. Indeed, the US private sector just sent the first astronauts into space from US soil in a decade, with plans for a moon landing and a trip to Mars. Then again, we are decades further into neoliberal financialisation now, with all the resultant atrophying of previous US strength: the public sector can no longer put a man on the moon; it has to be outsourced.

Re: decades in weeks and breakdowns, on Friday markets –and this Daily– felt a Rubicon was about to be crossed when Trump tweeted “CHINA!” just before a press conference on the subject. However, despite his aggressive rhetoric on the South China Sea and “Wuhan virus”, the conclusion was a bazooka had not been brought to the table. Trump announced: the beginning of the process of ending Hong Kong’s separate legal status from China; a shift in the US travel advisory; action to limit access to US universities; and a working group to protect the US financial system from China; and sanctions on HK and PRC individual. Yet he did not walk away from the phase one trade deal – Trump opted to leave the WHO entirely instead. Equities and CNH both rallied Friday, and Hong Kong was up strongly today. Wrongly.

Loss of US recognition will not directly impact Hong Kong much, as China says, yet:

-

The shift on visas prevents Chinese nationals studying STEM at post-grad level in the US if they attended a military university (around 4% of the total in the US) OR have links to a firm signing up to Beijing’s policy of ‘Military-Civilian Fusion’: that covers anything larger than an SME.

-

The working group on financial markets is almost certain to recommend delisting Chinese equities from the US, a process already underway, and escalate restrictions on US capital flows into China, also underway.

-

We should expect the list of sanctioned individuals to be lengthy and embarrassing. Some will have at least one account with a Western bank, which will have to be closed and moved to a Chinese bank, causing a backlash (last week saw former Hong Kong CEO CY Leung call for a boycott of a bank that could not be more ‘Hong Kong’). Moreover, once Chinese banks are doing that banking instead, US sanctions will then apply to them. We will still end up with restrictions on USD usage in Hong Kong/China that the market think we have dodged.

-

Trump was never going to walk away from a trade deal even if many observers already see it as dead: why bother? If China sticks to it, great – but it won’t change the political direction of travel; and if they don’t, it’s more fuel on the anti-China fire in the near future.

In short, Trump put US-China decoupling on the table – and STILL pushed the stock market up. Those who don’t see that might want to look at Hong Kong’s money changers, who are having to turn away hundreds of customers due to a lack of USD in the face of massive demand; and this is matched by inquiries over emigration and foreign property purchases. The Hong Kong Finance Secretary has even had to come out and say there are no plans to change the city’s HKD peg to the USD or to impose capital controls: that this had to be said speaks volumes. The South China Morning Post likewise points out Beijing may be holding back on a massive stimulus package because it is keeping its power dry and asks: is it for looming US decoupling? It’s certainly not because the economy is doing well from the latest PMI data (manufacturing 50.6 with new export orders 35.3 and 54% of firms seeing insufficient demand; services at 53.6; and Caixin manufacturing 50.7.)

Meanwhile, the tectonic shift on the US-China front runs through all other markets. Mexico has questioned the US over the phase one trade deal given USMCA Article 32.10 states an FTA with a non-market economy allows the other two parties to terminate or update it. Obviously it isn’t a FTA –it’s barely a deal anymore– but Mexico is stirring the pot given much of the US trade lost to China is likely to be gained by it, underlining the new regionalisation underway.

Far more significantly, Trump postponed the G7 meeting set for June because Germany’s Angela Merkel refused to attend. In response to this slight, as well as the milquetoast EU reaction to Hong Kong, who are still set to proceed with a September EU-China investment summit, Trump has shifted the “out of date” G7 date to September – and invited Australia, South Korea, India, and Russia to join. Yes, Russia used to be in G8, and Australia, South Korea, and India are all in the G20. Yet this overlooks the fact that all of the above except Russia feel threatened by China, and are establishing new national security mechanisms to deal with those concerns, including trading arrangements (India may be buying the Aussie barley China no longer is, for example). Moreover, reverse Nixon-ing to bring in Russia from the cold would be the requisite move to encircle China. That’s realpolitik over liberal ideals.

Please listen to Lenin, Europe (where watches are still set back to 2005). The EU debt/budget debate would have been timely 15 years ago, but the block looks to be drifting into a geo-strategic headache if the US and Russia were to build bridges over the top of it, or if the global architecture fragments, WHO style. Even the UK may opt for the US over an EU FTA (and for Australia, India, etc.). This is a real risk of that building in the British determination to walk away from deadlocked EU trade negotiations within weeks; and in the UK dumping Huawei and angling for a new “D10” (D for Democracy) of countries to unite behind a Western technological 5G alternative; and as the UK says 2.9m Hong Kongers are eligible for British residency – this from a government seen as having won the Brexit debate over immigration.

Everywhere you look, decades are happening in weeks. Are they taking us towards US collapse or renaissance? Towards European solidarity or division and (further) European irrelevance? Towards a Chinese century – or very rapidly away from it?

Does this matter for your market/asset? How can it not?! Bond yields are very low; volatility is very low; equities are very high; and the USD is well off its highs. Not all of these can be correct if those tectonic plates are about to shift: only one can.

via ZeroHedge News https://ift.tt/2TWmBAc Tyler Durden