ECB Cuts Rates By 25bps (As Expected); Projects Worsening Stagflation

As expected, The ECB cut rates by 25bps today to 3.50%.

In its statement (below), the central bank confirmed it will continue to follow data dependent path, cut its PEPP by €7.5 bn a month…hiked inflation expectations and cut growth expectations…

The ECB staff increased its inflation expectations:

-

ECB Sees 2024 Inflation Ex-Food/Energy at 2.9% vs 2.8%

-

ECB Sees 2025 Inflation Ex-Food/Energy at 2.3% vs 2.2%

-

ECB Sees 2026 Inflation Ex-Food/Energy at 2% vs 2%

-

ECB Sees 2026 Inflation at 1.9%; Prior Forecast 1.9%

And cuts its growth expectations:

-

GDP 2024 0.8%, previous 0.9%

-

GDP 2025 1.3%, previous 1.4%

-

GDP 2026 1.5%, previous 1.6%

This is a slight downward revision compared with the June projections, mainly owing to a weaker contribution from domestic demand over the next few quarters.

So more stagflationary!

But forward guidance remains absolutely unchanged:

“The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach… The Governing Council is not pre-committing to a particular rate path.”

However, some market participants sense some reluctance to be too dovish as inflation is not tamed,…

‘inflation data have come in broadly as expected’

…

‘Domestic inflation remains high as wages are still rising at an elevated pace.

The euro is basically unchanged after the statement.

Watch Lagarde explain her decision here (due to start at 0845T):

Read the full ECB Statement below:

The Governing Council today decided to lower the deposit facility rate – the rate through which it steers the monetary policy stance – by 25 basis points. Based on the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, it is now appropriate to take another step in moderating the degree of monetary policy restriction.

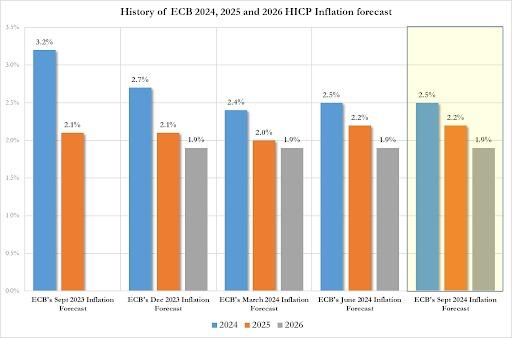

Recent inflation data have come in broadly as expected, and the latest ECB staff projections confirm the previous inflation outlook. Staff see headline inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, as in the June projections. Inflation is expected to rise again in the latter part of this year, partly because previous sharp falls in energy prices will drop out of the annual rates. Inflation should then decline towards our target over the second half of next year. For core inflation, the projections for 2024 and 2025 have been revised up slightly, as services inflation has been higher than expected. At the same time, staff continue to expect a rapid decline in core inflation, from 2.9% this year to 2.3% in 2025 and 2.0% in 2026.

Domestic inflation remains high as wages are still rising at an elevated pace. However, labour cost pressures are moderating, and profits are partially buffering the impact of higher wages on inflation. Financing conditions remain restrictive, and economic activity is still subdued, reflecting weak private consumption and investment. Staff project that the economy will grow by 0.8% in 2024, rising to 1.3% in 2025 and 1.5% in 2026. This is a slight downward revision compared with the June projections, mainly owing to a weaker contribution from domestic demand over the next few quarters.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

As announced on 13 March 2024, some changes to the operational framework for implementing monetary policy will take effect from 18 September. In particular, the spread between the interest rate on the main refinancing operations and the deposit facility rate will be set at 15 basis points. The spread between the rate on the marginal lending facility and the rate on the main refinancing operations will remain unchanged at 25 basis points.

Key ECB interest rates

The Governing Council decided to lower the deposit facility rate by 25 basis points. The deposit facility rate is the rate through which the Governing Council steers the monetary policy stance. In addition, as announced on 13 March 2024 following the operational framework review, the spread between the interest rate on the main refinancing operations and the deposit facility rate will be set at 15 basis points. The spread between the rate on the marginal lending facility and the rate on the main refinancing operations will remain unchanged at 25 basis points. Accordingly, the deposit facility rate will be decreased to 3.50%. The interest rates on the main refinancing operations and the marginal lending facility will be decreased to 3.65% and 3.90% respectively. The changes will take effect from 18 September 2024.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the PEPP, reducing the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

Tyler Durden

Thu, 09/12/2024 – 08:28

via ZeroHedge News https://ift.tt/sk8YArg Tyler Durden