Before leaving the White House on Friday afternoon for Joint Base Andrews where he’s scheduled to board Marine One en route to his golf club in Bedminster, New Jersey, President Trump – as is his custom – stopped on the White House lawn to answer questions from a gaggle of White House reporters.

With so much going on, it’s hardly surprising that the questions covered a lot of ground. But what was surprising was Trump’s distinctly aggressive stance on his trade-deal negotiations with both China and the EU just minutes before the market closed.

First, his comments on the trade talks with China:

TRUMP SAYS HE CAN RAISE CHINA TARIFFS ‘TO A MUCH HIGHER NUMBER’

TRUMP SAYS CHINA HAS TO DO A LOT OF THINGS TO TURN IT AROUND

Less than 24 hours after President Donald Trump announced an escalation of the trade war with China, he got some predictable news: America’s trade deficit has hit a new high.

The gap between how much America exports to China and how much it imports from the Asian nation grew to $30.2 billion in July, up from $30.1 billion the previous month, according to Commerce Department figures. The widening gap was due to a decrease in the value of American exports, Bloomberg notes.

In normal circumstances, this wouldn’t be a big deal. Economists generally agree that trade deficits don’t matter, for the same reason that you wouldn’t worry about running a “deficit” with a grocery store. But Trump has used America’s trade deficit as a key justification for his trade policies, and he has repeatedly promised that tariffs on China would reduce that deficit.

Trump’s tariffs are having an impact. During the first six months of 2018, U.S. exports to China fell by 18 percent relative to the same period last year. Imports from China slipped by 12 percent. Both sides are doing less trading, but the trade deficit persists.

Here are three more recent data points that show problems with Trump’s trade war:

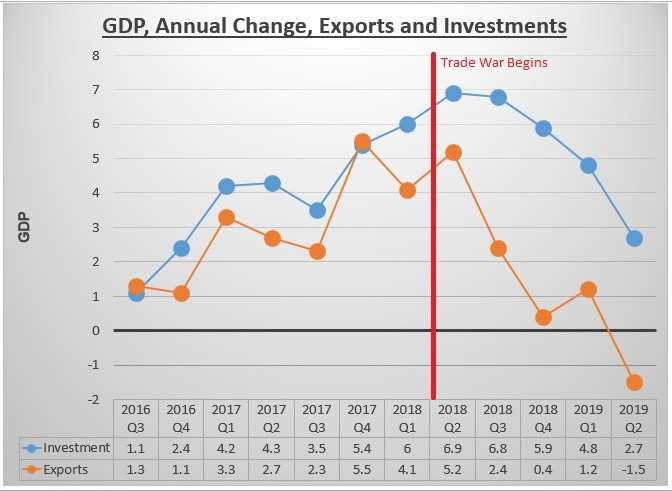

BUSINESS INVESTMENTS

According to the Commerce Department, investment in American businesses has fallen off sharply since the start of Trump’s trade war in mid-2018. Nonresidential domestic investment was buoyed by the tax cuts Trump signed in December 2017, but during the second quarter of 2019 investment dipped into negative territory. That’s a sign that businesses are holding back on hiring or expanding in the face of the uncertainty created by the president’s trade policies.

Equally significant is the recent sharp drop in American exports. This is an expected but perhaps underappreciated consequence of Trump’s policies. “Exporters can be successful only if they are viewed as reliable suppliers,” writes C. Fred Bergsten, a senior fellow at the Peterson Institute for International Economics. “But Trump’s trade policies have rendered US firms among the most unreliable in the world.”

GOODS-PRODUCING JOBS DECLINING

As a perfect encapsulation of where the economy is right now, after a gangbuster 2018, job growth year-over-year in goods is just about where it is for services. Goods has seen a dramatic slowdown, while services has held up better. pic.twitter.com/WvTcdGLjMB

Trump has also tried to justify his bellicose trade policies by citing the importance of American manufacturing jobs . Trump talked about “an extraordinary resurgence of American manufacturing” during a photo op at the White House last month.

But as the chart above indicates, goods-producing jobs have been declining steadily since last summer. The drop-off begins almost exactly when the trade war began.

The latest jobs report continues this trend.

Almost all the US job gains are now coming from the service sector, not blue collar. Manufacturing jobs are basically flat this year.

Here’s a look at July:

Professional services +31,000

Health care +30,000

Social assistance +20,000

Fin Services +18,000#jobs

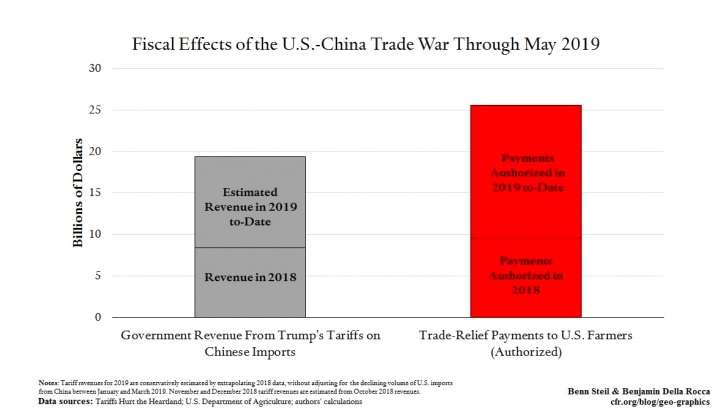

THE TRADE WAR HAS BEEN A NET LOSER FOR THE TREASURY

Another of Trump’s favorite defenses for the trade war is the claim that tariffs are generating billions of dollars for the U.S. Treasury. He’s right about that much—though it’s Americans who are paying, not China.

But the tariffs have also failed as a revenue-generating strategy. As of May, they were on pace to generate about $20 billion in revenue by the end of 2019. By comparison, Trump’s bailouts to farmers hurt by China’s retaliatory tariffs totaled over $25 billion.

Those bailouts, meanwhile, have been a complete mess. A report released this week by the Environmental Working Group, a agricultural policy watchdog, found that 54 percent of those payments went to just 10 percent of all farmers.

With more Chinese tariffs set to take effect in September, it’s possible that Trump’s tariffs and bailouts might balance each other out by the end of the year. If so, an 18-month experiment in economic nationalism will have been, at best, a wash for the Treasury while serving as a massive transfer in wealth from America’s manufacturing and agricultural sectors to a small sliver of farmers. Great success!

from Latest – Reason.com https://ift.tt/2GFoCKr

via IFTTT

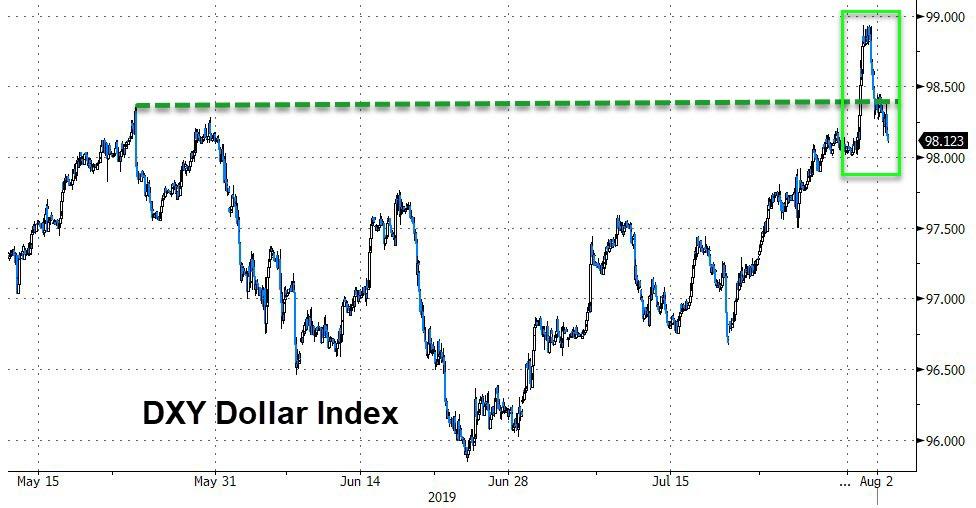

Since Powell dropped the “mid-cycle adjustment” mic, Bonds and Bullion have been bid, the dollar is practically unchanged and stocks have plunged (hurt more by Trump Tariffs)…

Chinese stocks were lower for the last three days with big caps worst and tech names the least bad… for now…

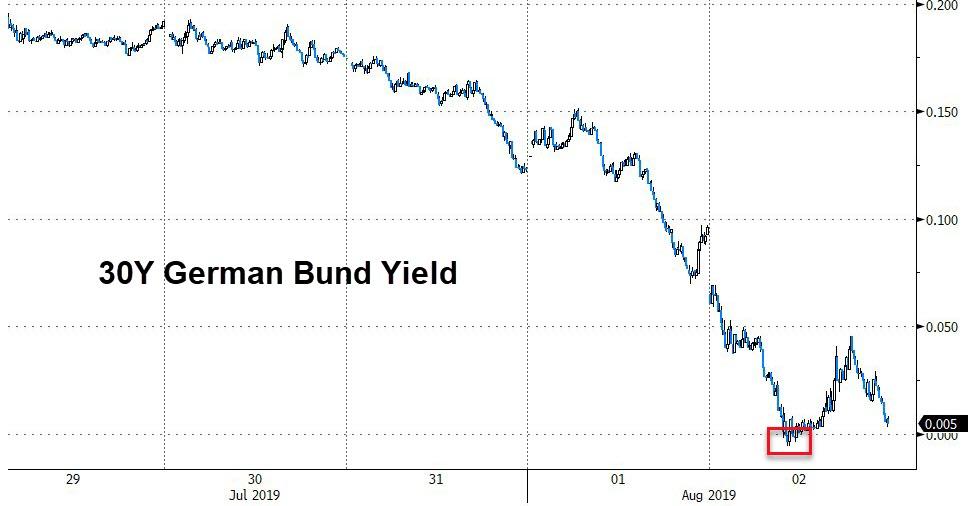

European stocks cratered today – the biggest single-day drop since Dec 2018 – with Germany and France leading the way lower on the week…

For the first time ever, Germany’s entire yield curve (30Y) traded with a negative yield…

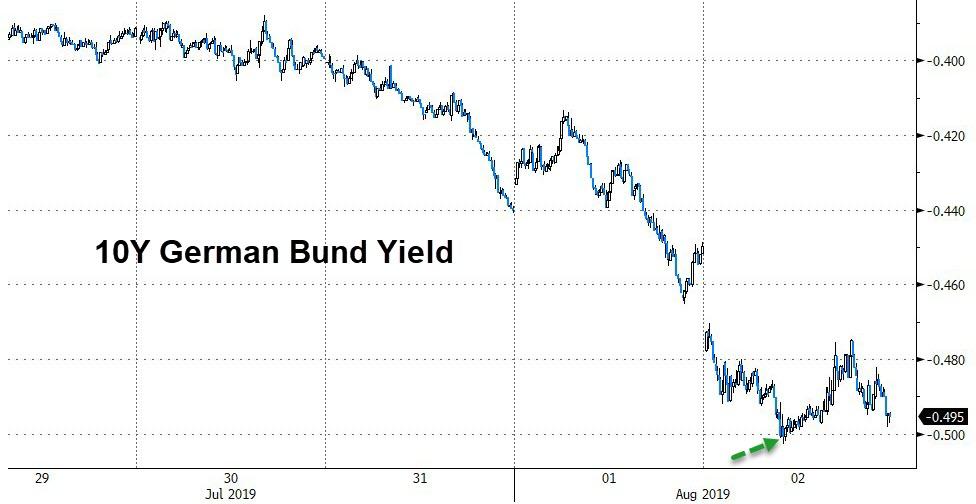

10Y Bunds hit -50bps today!!!!

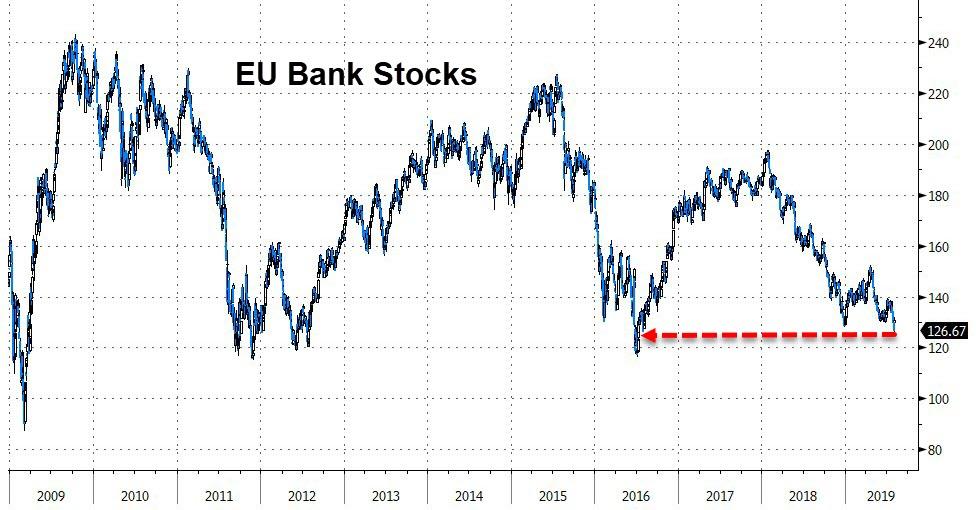

European banks crashed on the week to their lowest since Brexit vote (June 2016)

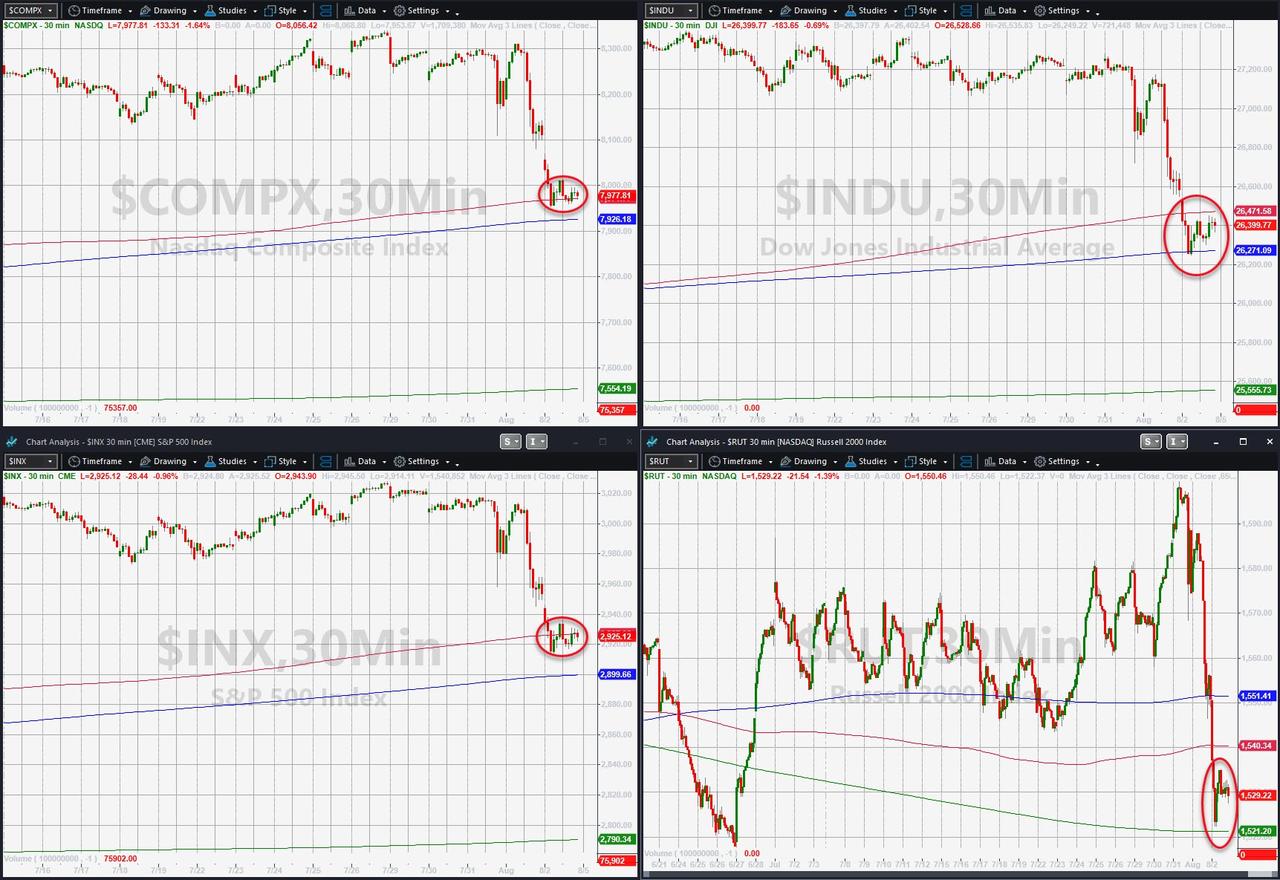

Broadly, this was the worst 3-day drop for US stocks since Christmas Eve and worst week of 2019… Stocks were – as always – bid in the last hour… until Trump said “he could raise China tariffs to a much higher degree.” Nasdaq was the week’s biggest loser (and Dow lost the least of the majors)

US equities plunged to critical technical levels:

S&P 500 tested its 50DMA (2927) and 100DMA (2900)

Nasdaq tested its 50DMA (7971) and 100DMA (7927)

Dow broke below its 50DMA (26472) and tested its 100DMA (26276)

Trannies broke below the 50DMA (10358) and 100DMA (10478) and tested its 200DMA (10281)

Small Caps broke below the 50DMA (1540) and 100DMA (1551) and tested its 200DMA (1520)

VIX topped 20.00 intraday today before fading back…

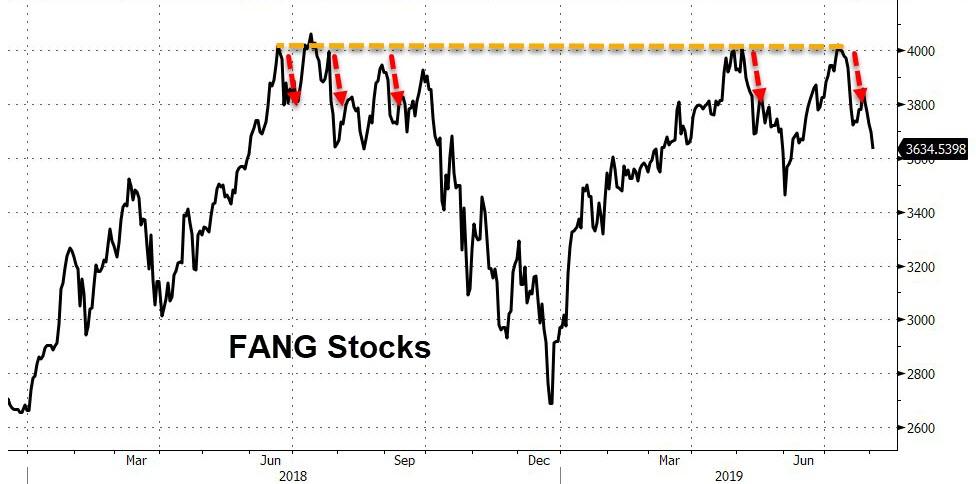

FANG Stocks were down every day this week (2nd worst week of the year)…

Cyclical stocks tumbled, their worst week of the year, dramatically underperforming defensives…

Bank stocks were battered, tracking the collapse of the curve…

Despite this week’s carnage, bonds and stocks remain dramatically decoupled…

Credit spreads blew wider on the week…

It was a bloodbath for bond bears this week (down 12-20bps across the curve with the long-end outperforming)…

10Y crashed to its lowest yield since before Trump’s election…This was the biggest 10Y Yield drop in a week since Dec 2014.

2Y yields were even crazier – initially spiking on Powell then crashing on Trump…

30Y Yields are back at their lowest since Oct 2016…

The yield curve (3m10Y) crashed to cycle lows…

And finally, before we leave bond-land, longer-term inflation expectations have fallen the most in the past two days since 2016, based on 5-year 5-year forward breakeven rates… a total policy-failure

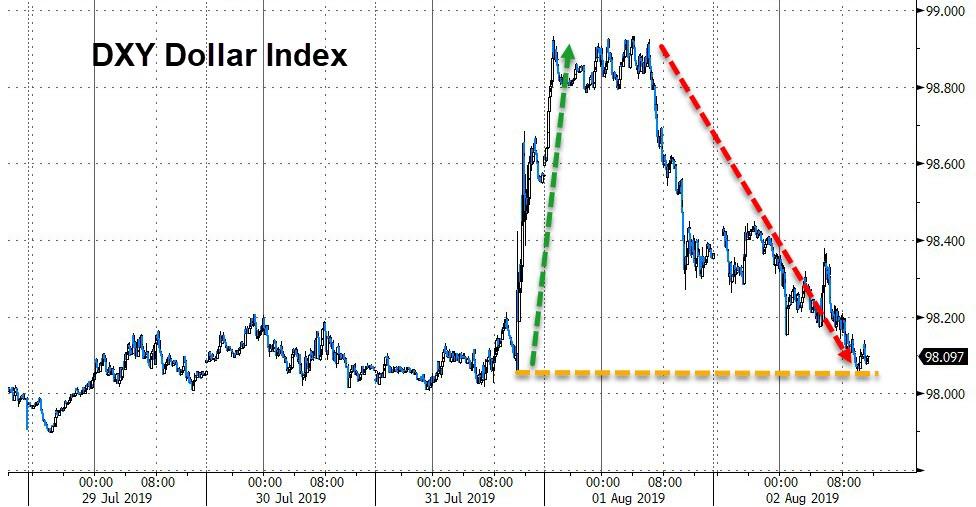

Amid all the chaos, the dollar index ended the week only marginally higher after a huge round trip the last few days

…After a false breakout to the highest since May 2017)…

Cable suffered one of its worst weeks since Brexit, dropping to its lowest weekly close since May 1985…

Yuan dropped five of the last six days closing the week at its weakest since Dec 2016 (Yuan has only closed weaker than this twice before… ever)

Emerging Market FX has really collapsed the last few days (Turkey surprisingly outperformed)…

The biggest 3-day drop since Aug 2018 to its lowest since May…

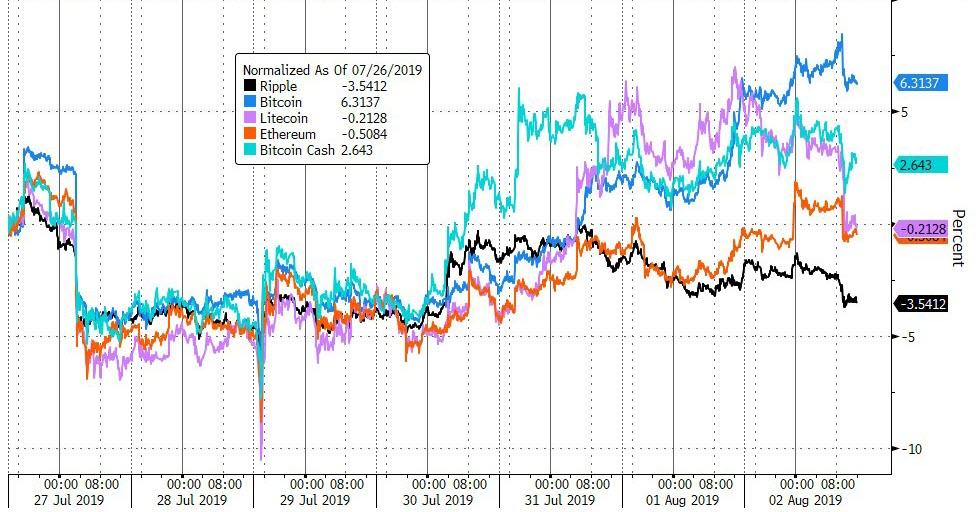

Cryptos had a mixed week – best gains since June for Bitcoin as Ether and Litecoin scrambled back to even…

Bitcoin surged back above $10,000 and extended gains…

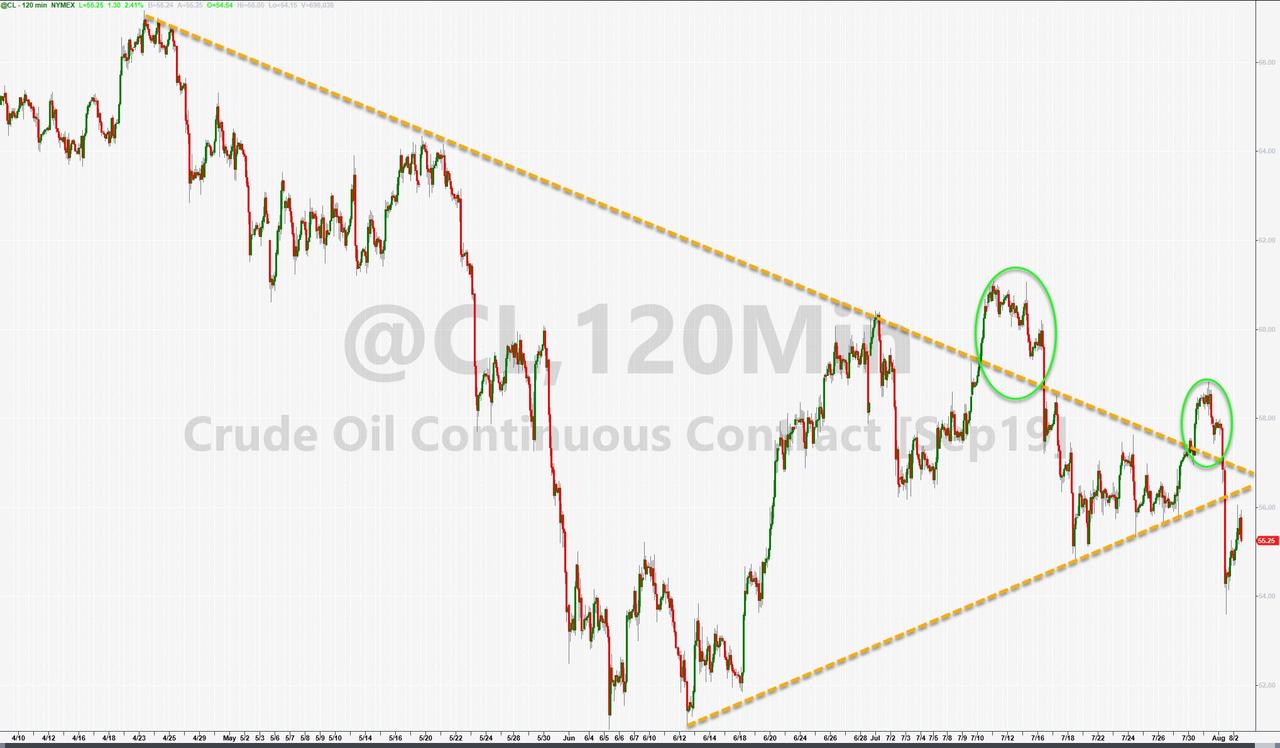

Copper was crushed on the week but Gold outperformed as crude rebounded after its worst day in years…

In fact, Dr.Copper has collapsed to two year lows… what does the PhD economist commodity know?

Ugly week for crude…

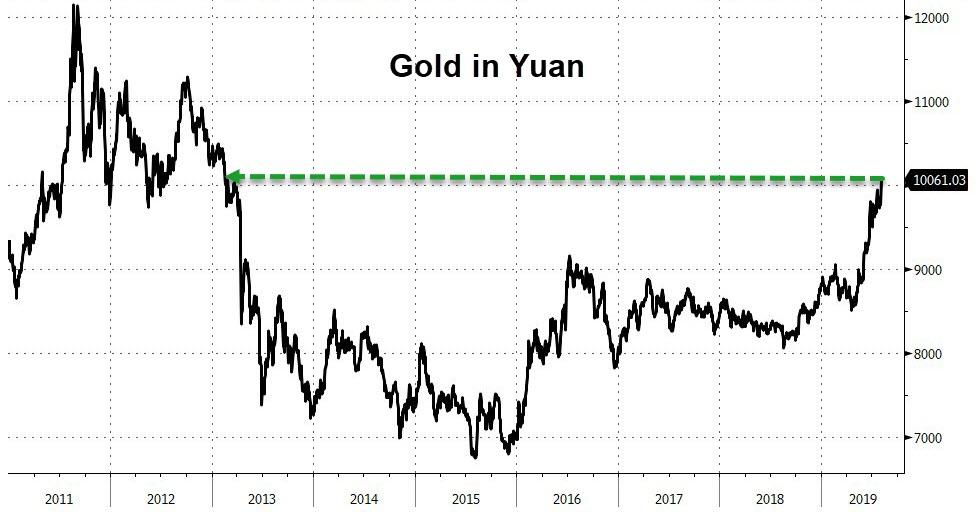

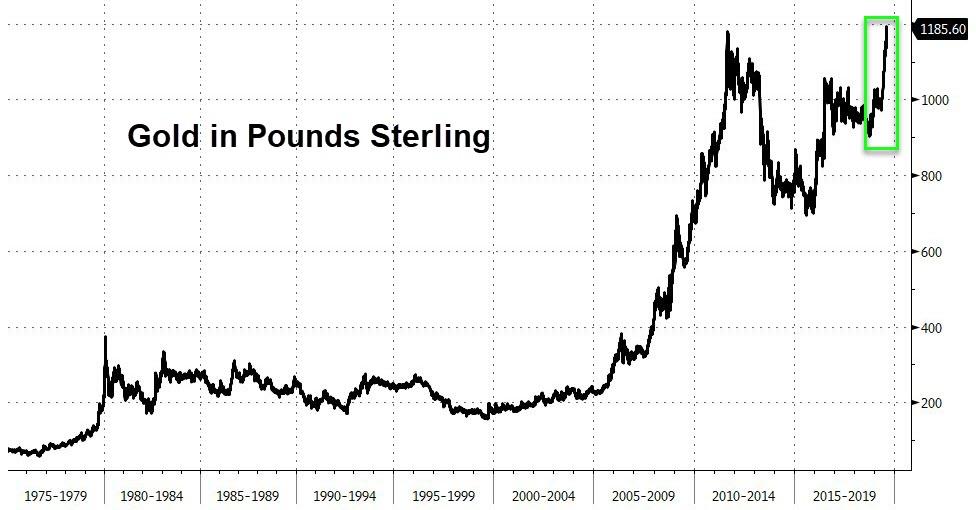

Gold topped CNH10,000 for the first time since Feb 2013…

Gold reached a new record high against the pound sterling…

Soybeans were monkeyhammered (worst week since Aug 2018) to their lowest since May after Trump tariff headlines…

Finally, you are here…

It’s different this time though – remember!

Different, because it’s way more ridiculous (negative-yielding debt tops $14 trillion!!)

And gold and crypto appear to be where investors are going to hide from this policy-maker pandemonium!!

via ZeroHedge News https://ift.tt/2yzXo3y Tyler Durden

A new essential oil blend will help you stay really mad about everything.

Dubbed “Outrage,” the specialized blend contains authentic extract of coffee beans, sweat from Antifa protestors, liberal tears, and a hair plucked from the eyebrows of Alyssa Milano.

Other varieties have essence of scorpions, ferret rabies, vinegar, and organic LaCroix extract.

“Are you finding it difficult to read the day’s news and get really worked up about it day after day?” said a representative for the company.

“Then it’s time for you to take a whiff of ‘Outrage.’ Our patented scent will cause you to find something to be upset about in any mundane news story or interaction with normal humans.”

The rep recommended putting a few drops in your essential oils diffuser or adding one drop to your morning kombucha.

Side effects of Outrage include tweeting to your 134 followers about just how mad you are, arguing about stuff that doesn’t matter on Facebook, and cutting off your relationships with your friends and family who disagree with you. Outrage manufacturers claim this is a feature of the product, not a bug, however, and that if you find yourself burning bridges with everyone you know as you rage about events that no one will remember in a few days, the product is working exactly as intended.

Outrage has been endorsed by political pundits on both the left and the right, garnering rave reviews for its enraging properties.

Upcoming scents include “Existential Dread,” “Imposter Syndrome,” and “Screaming at the Sky.”

via ZeroHedge News https://ift.tt/2YM28lC Tyler Durden

After Democratic 2020 candidate Rep. Tulsi Gabbard (D-HI) dressed down Sen. Kamala Harris (D-CA) over her criminal justice record, Harris hit back – suggesting that Gabbard is somehow ‘below her’ – and an “apologist” for Syrian dictator Bashar al-Assad.

In case you missed the original smackdown:

In response, Harris thumbed her nose at Gabbard, telling CNN‘s Anderson Cooperafter the debate: “This is going to sound immodest, but obviously I’m a top-tier candidate and so I did expect that I’d be on the stage and take some hits tonight … when people are at 0 or 1% or whatever she might be at, so I did expect to take some hits tonight.”

Harris added “Listen, I think that this coming from someone who has been an apologist for an individual, [Syrian President Bashar al] Assad, who has murdered the people of his country like cockroaches. She has embraced and been an apologist for him in the way she refuses to call him a war criminal. I can only take what she says and her opinion so seriously, so I’m prepared to move on.”

Wait a second…

Tulsi wasn’t having it. In a Thursday interview with CNN‘s Chris Cuomo, Gabbard punched back – saying “[T]he only response that I’ve heard her and her campaign give is to push out smear attacks on me, claim that I am somehow some kind of foreign agent or a traitor to my country, the country that I love, the country that I put my life on the line to serve, the country that I still serve today as a soldier in the Army National Guard.”

Gabbard also made clear that she believes Assad is “a brutal dictator, just like Saddam Hussein, just like Gaddafi in Libya,” adding “The reason that I’m so outspoken on this issue of ending these wasteful regime change wars is because I have seen firsthand this high human cost of war and the impact that it has on my fellow brothers and sisters in uniform.“

via ZeroHedge News https://ift.tt/2KiqJ8a Tyler Durden

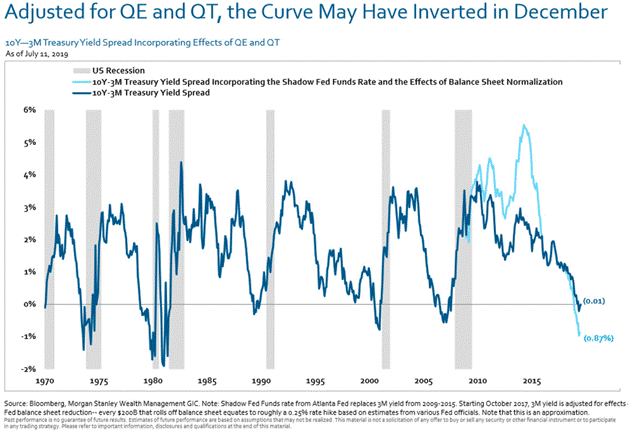

The inverted yield curve is one of the more reliable recession indicators.

I discussed it at length last December. At that point, we had not yet seen a full inversion. Now we have, and it appears the curve was “inverted” back then, and we just didn’t know it.

Now if you assume, as Morgan Stanley does, every $200B balance sheet reduction is equivalent to another 0.25% rate increase, which I think is reasonable, then the curve effectively inverted months earlier than most now think.

Worse, the tightening from peak QE back in 2015 was far more aggressive and faster than we realized.

Worrisome Charts

Let’s go to the chart below. The light blue line is an adjusted yield curve based on the assumptions just described.

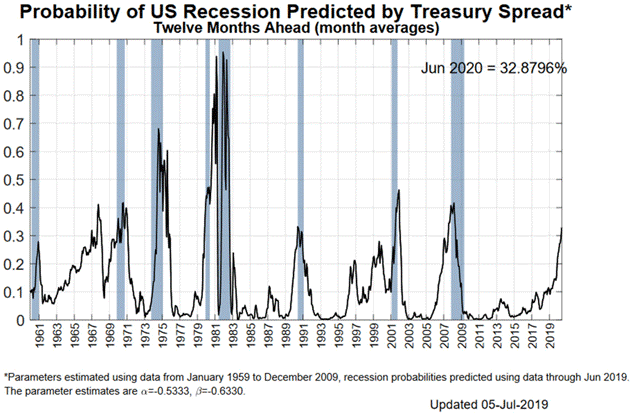

But even the nominal yield curve shows a disturbingly high recession probability. Earlier this month, the New York Fed’s model showed a 33% chance of recession in the next year.

Their next update should show those odds somewhat lower as the Fed seems intent on cutting short-term rates while other concerns raise long-term rates.

But it’s still too high for comfort, in my view.

But note that whenever the probability reached the 33% range (the only exception was 1968), we were either already in a recession or about to enter one.

For what it’s worth, I think Fed officials look at their own chart above and worry. That’s why more rate cuts won’t be surprising.

And frankly, and I know this is out of consensus, I would not rule out “preemptive quantitative easing” if the economy looks soft ahead of the election next year. Just saying…

But that’s not everyone’s view.

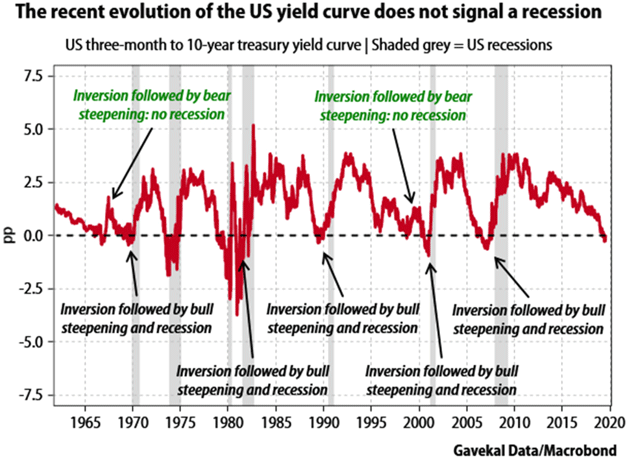

The Other Side of the Argument

Gavekal Research gives us this handy chart showing inversions don’t always lead to recession right away. (I noted 1968 above and I think 1998 is a separate issue. But then again, that’s me.)

Fair enough; brief inversions don’t always signal recession. But as noted, when you consider the balance sheet tightening, this one hasn’t been brief.

Note also that an end to the inversion isn’t an all-clear signal. The yield curve is often steepening even as recession unfolds.

One thing seems certain: While the yield curve may not signal recession, it isn’t signaling higher growth, either. The best you can say is that the mild expansion will continue as it has. That’s maybe better than the alternative, but doesn’t make me want to pop any champagne corks.

The Fed has always been behind the curve. To Powell’s credit, he may be trying to get in front of it, at least this time.

* * *

The Great Reset: The Collapse of the Biggest Bubble in History – New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

via ZeroHedge News https://ift.tt/2ywXbht Tyler Durden

Woodstock: Three Days That Defined a Generation. PBS. Tuesday, August 6, 9 p.m.

It’s perfectly reasonable to wonder why anybody feels the need for another documentary about Woodstock. We’ve already got the film of the same name that was released in 1970, a staggering 224 minutes of dope, drizzle, and dishabille, which won an Oscar and is part of the Library of Congress’ National Film Registry.

But there are a few reasons you might want to take a peek at PBS’s new effort, Woodstock: Three Days That Defined a Generation. For instance, its revelation of the novel funding idea of Artie Kornfeld, one of 1969 rock festival’s principal organizers.

Told that construction crews hadn’t been able to get fences built in time and Woodstock would have to be declared a free concert, Kornfeld asked: “Can’t we get a whole bunch of girls and put them in diaphanous gowns and give them collection baskets and send them out into the audience?”

Then there’s the video of that bumper sticker posted on one of the food stands that dotted the perimeter of the concert ground: “DON’T WORRY BE HAPPY,” a full 19 years before Bobby McFerrin’s record drove a nation to homicidal madness.

Oh, and a reminder that rodents were rocking their own Age of Aquarius: A glimpse of the log kept at the medical tents remembered mostly for taking care of the consumers of Woodstock’s infamous brown acid reveals they also had 11 patients suffering from rat bites. I blame Nixon.

To be fair, this Woodstock is very different than the film, which lacked interviews or narration and was more immersion than explication. Director Barak Goodman (Oklahoma City) conducted interviews with several of Woodstock’s organizers that he uses to trace the festival’s evolution from its conception as a recording studio for Bob Dylan to an outdoor concert for 5,000 people to (at least for a weekend) a city that was the 10th-biggest and most-stoned in America.

(Actually, I assume that Goodman’s crew did the interviews, but that may not be true. Several of the interviewees, including Joe Cocker and Jefferson Airplane guitarist Paul Kantner, have been dead for years, and the film’s credits don’t reveal where their comments came from.)

The result is a story in equal parts amusing and appalling. The organizers spent weeks lurking around the bathrooms in Yankee Stadium and Madison Square Garden and timing the occupants to determine how many Porta Potties would be needed at Woodstock. Answer: “Tens of thousands … just impossible numbers.” They went ahead anyway.

Pretty much the same degree of planning went into food, security, shelter and everything else about Woodstock. Even the power lines into the festival site—literally the life blood for all the guitars, amps, speakers and soundboards necessary for the show—were installed chaotically. During the apocalyptic rainstorm that struck on the second day, a 50,000-volt cable was unearthed, which—as one of the organizers admits—could easily have resulted in a mass electrocution. “Fortunately,” he observes breezily, “that didn’t happen.”

It’s narrow misses like that one that make the documentary’s subtitle—”three days that defined a generation”—so arrogantly infuriating. Woodstock, it’s true, did not live up to the famous New York Times headline, “Nightmare in the Catskills.”

But that was mostly due to the eternal saviors of teenagers, Mommy and Daddy. The National Guard helicopters ferried in food (nearly all of it donated by the middle-aged townsfolk of nearby Bethel, N.Y., who were home watching Lawrence Welk instead of Jimi Hendrix) and carried out medical casualties. Without their help, and a generous amount of blind luck like the power line not zapping everyone, Woodstock might have more literally resembled what the crew that stayed behind two weeks after the festival to clean up compared it to: a Civil War battlefield.

The most notable thing about the PBS Woodstock is the contortionist specter of a generation blowing smoke up its own ass. The last 15 minutes or so are mostly devoted to people who attended Woodstock declaring it a utopically transformative event that changed everything. Really? Jimi Hendrix and Janis Joplin would be dead of drug overdoses within a year. The Vietnam War continued for another three. The next president elected was not George McGovern but Richard Nixon, and when Baby Boomers finally did start electing presidents, the result was Afghanistan and Iraq. And raise your hand if you think race relations are any better today than they were in 1969.

You could as easily make the argument that what defined a generation was not Woodstock but Altamont or the Manson Family. Baby Boomers didn’t change the world at Woodstock, or create a New Man. Their only accomplishment was to stand up in public, half a million strong, and chant the word “Fuck!” without getting spanked. It’s sad that, 50 years later, they still can’t tell the difference.

from Latest – Reason.com https://ift.tt/31bGa8T

via IFTTT

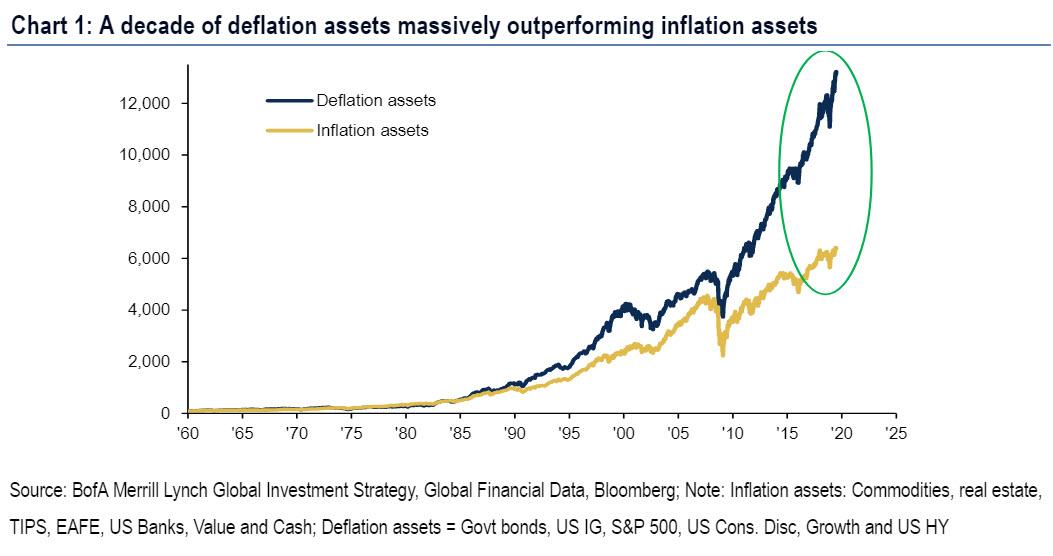

Fishing for some fascinating trivia about the “New Abnormal” period we live in? Here are ten remarkable observations from BofA’s Micharl Hartnett that demonstrate that we live in a time like no other.

Fed cut makes it 729 global central bank cuts since Lehman bankruptcy.

Soaring US consumer confidence at highest level vs. plunging German business confidence since Q4’98…when Fed cut rates “mid-cycle” igniting bubble of ’99.

EM equities at lowest level vs. US equities since 2003…China weak, US$ strong.

Wall St (US private sector financial assets) now 5.5x the size of Main St (US GDP)… between 1950 & 2000 the norm was 2.5-3.5x…Wall Street is now “too big to fail”.

Global debt now 3.2x the size of global GDP, an all-time high.

Fresh China tariffs in Sept would raise average US tariff on total imports to 5.6% from 4.5%, highest since 1972…was 1.5% before Trump.

US companies spent $114 on buybacks for every $100 of capex in past 2 years… between 1998 & 2017 they spent $60 for every $100 of capex.

Inflows to bond funds ($278bn) rising at a record pace in 2019.

Past 10 years $4.1tn into passive investment funds vs. $1.5tn out of active funds.

Just 6% of MSCI ACWI stocks account for 53% of YTD global equity return.

As Hartnett summarizes, “the above reflect a decade of Maximum Liquidity & Minimal Growth, of tech disruption, aging demographics & Chinese rebalancing, of polarized outperformance by deflation assets (US stocks, HY bonds, growth stocks) vs. inflation assets, of expectations for higher inflation, yields, volatility consistently being dashed.

His contrarian recommendations for 2020s:

“long inflation” & “short Wall St” driven by populism, protectionism, policy impotence, popping bond bubbles, peak globalization.

In short: brace for the deflationary ice age end of the world as we know it.

via ZeroHedge News https://ift.tt/2ZrzlQ5 Tyler Durden

Woodstock: Three Days That Defined a Generation. PBS. Tuesday, August 6, 9 p.m.

It’s perfectly reasonable to wonder why anybody feels the need for another documentary about Woodstock. We’ve already got the film of the same name that was released in 1970, a staggering 224 minutes of dope, drizzle, and dishabille, which won an Oscar and is part of the Library of Congress’ National Film Registry.

But there are a few reasons you might want to take a peek at PBS’s new effort, Woodstock: Three Days That Defined a Generation. For instance, its revelation of the novel funding idea of Artie Kornfeld, one of 1969 rock festival’s principal organizers.

Told that construction crews hadn’t been able to get fences built in time and Woodstock would have to be declared a free concert, Kornfeld asked: “Can’t we get a whole bunch of girls and put them in diaphanous gowns and give them collection baskets and send them out into the audience?”

Then there’s the video of that bumper sticker posted on one of the food stands that dotted the perimeter of the concert ground: “DON’T WORRY BE HAPPY,” a full 19 years before Bobby McFerrin’s record drove a nation to homicidal madness.

Oh, and a reminder that rodents were rocking their own Age of Aquarius: A glimpse of the log kept at the medical tents remembered mostly for taking care of the consumers of Woodstock’s infamous brown acid reveals they also had 11 patients suffering from rat bites. I blame Nixon.

To be fair, this Woodstock is very different than the film, which lacked interviews or narration and was more immersion than explication. Director Barak Goodman (Oklahoma City) conducted interviews with several of Woodstock’s organizers that he uses to trace the festival’s evolution from its conception as a recording studio for Bob Dylan to an outdoor concert for 5,000 people to (at least for a weekend) a city that was the 10th-biggest and most-stoned in America.

(Actually, I assume that Goodman’s crew did the interviews, but that may not be true. Several of the interviewees, including Joe Cocker and Jefferson Airplane guitarist Paul Kantner, have been dead for years, and the film’s credits don’t reveal where their comments came from.)

The result is a story in equal parts amusing and appalling. The organizers spent weeks lurking around the bathrooms in Yankee Stadium and Madison Square Garden and timing the occupants to determine how many Porta Potties would be needed at Woodstock. Answer: “Tens of thousands … just impossible numbers.” They went ahead anyway.

Pretty much the same degree of planning went into food, security, shelter and everything else about Woodstock. Even the power lines into the festival site—literally the life blood for all the guitars, amps, speakers and soundboards necessary for the show—were installed chaotically. During the apocalyptic rainstorm that struck on the second day, a 50,000-volt cable was unearthed, which—as one of the organizers admits—could easily have resulted in a mass electrocution. “Fortunately,” he observes breezily, “that didn’t happen.”

It’s narrow misses like that one that make the documentary’s subtitle—”three days that defined a generation”—so arrogantly infuriating. Woodstock, it’s true, did not live up to the famous New York Times headline, “Nightmare in the Catskills.”

But that was mostly due to the eternal saviors of teenagers, Mommy and Daddy. The National Guard helicopters ferried in food (nearly all of it donated by the middle-aged townsfolk of nearby Bethel, N.Y., who were home watching Lawrence Welk instead of Jimi Hendrix) and carried out medical casualties. Without their help, and a generous amount of blind luck like the power line not zapping everyone, Woodstock might have more literally resembled what the crew that stayed behind two weeks after the festival to clean up compared it to: a Civil War battlefield.

The most notable thing about the PBS Woodstock is the contortionist specter of a generation blowing smoke up its own ass. The last 15 minutes or so are mostly devoted to people who attended Woodstock declaring it a utopically transformative event that changed everything. Really? Jimi Hendrix and Janis Joplin would be dead of drug overdoses within a year. The Vietnam War continued for another three. The next president elected was not George McGovern but Richard Nixon, and when Baby Boomers finally did start electing presidents, the result was Afghanistan and Iraq. And raise your hand if you think race relations are any better today than they were in 1969.

You could as easily make the argument that what defined a generation was not Woodstock but Altamont or the Manson Family. Baby Boomers didn’t change the world at Woodstock, or create a New Man. Their only accomplishment was to stand up in public, half a million strong, and chant the word “Fuck!” without getting spanked. It’s sad that, 50 years later, they still can’t tell the difference.

from Latest – Reason.com https://ift.tt/31bGa8T

via IFTTT

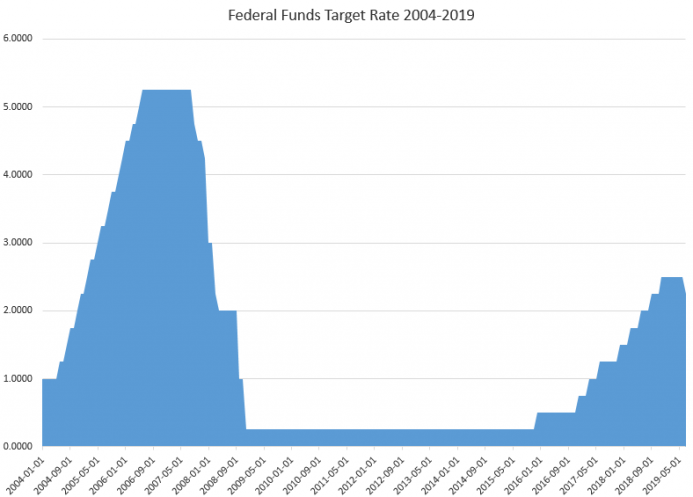

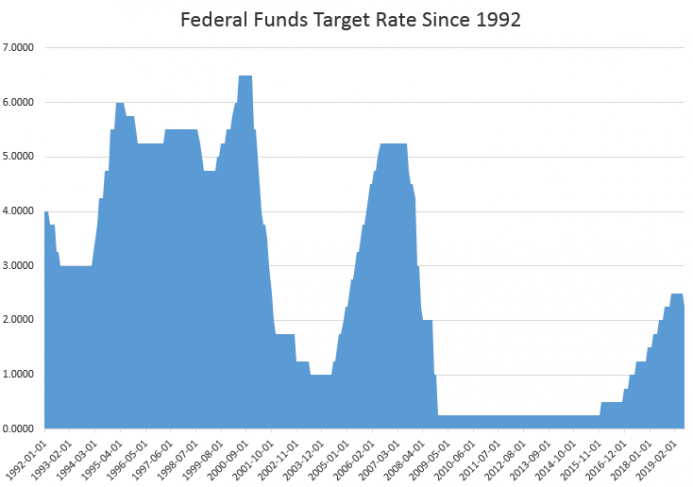

This week, the Fed’s Federal Open Market Committee lowered the target federal funds rate by 25 basis points, dropping it to 2.5 percent. The Fed had last changed its target rate in December of 2018, when it raised the rate from 2.25 percent to 2.50 percent.

It now looks like 2.5 percent is the highest the rate is going to get for the foreseeable future. After all, according to the Fed, the current state of the economy is “moderate” and the job market “strong.” If the economy needs a rate cut under these conditions, it’s hard to imagine a situation in which the Fed will be enthusiastic about another rate increase.

On the other hand, it’s entirely possible the rate cut is not motivated primarily by economic data, but by politics. Donald Trump has repeatedly and publicly pressured the Fed for a rate cut for many months.

It could be that the political pressure has had the desired effect. Economists — who are generally childlike in their naïve and fanciful views of how the political system works — actually appear to think the Fed is “independent” from the political system, or that it at least has been in the past.

But that’s not the reality, and the Fed, for all its protestations of independence, may simply be doing what it has always done. If this alleged independence appears to have diminished in recent times, of course, the difference is really only that Trump is simply more public about the pressure he applies. Past presidents and policymakers have tended to stick to applying pressure behind closed doors.

Fed Admits Economy Weaker than It Says

But, for the sake of argument, let’s assume that the rate cut comes primarily as a result of Fed economists’ consideration of the data.

If the conclusion was that a rate cut was now warranted, this tells us that the economy is not really as strong as the Fed has long pretended it to be. This has been obvious for years, of course.

For a decade, the Fed told us the “recovery” was proceeding nicely, but “oh by the way, we don’t dare allow interest rates to increase to anything resembling even 1990s-type rates.”

Thus, the fed funds rate sat at 0.25 percent from 2008 to 2015. And it was barely allowed to inch up much after that. And now it seems that even 2.5 percent is too much for the fed to stomach.

Inflation and the Phillips Curve

To explain this all away, the Fed has invented the “two-percent” which is a totally arbitrary number at which the economy is functioning with a healthy inflation rate. The fact that years of “strong” job growth hasn’t led to the “official” inflation rate reaching 2 percent suggests that either the method of measuring inflation is wrong, or the economy is weaker than the Fed thinks it is.

It’s possible that both factors are contributing. It’s possible that real wage growth is insufficient to drive sizable inflation. This, after all, is what has long been gospel among mainline economists: strong employment leads to higher inflation. But that doesn’t seem to be the case anymore, and Chairman Powell has even admitted this relationship — described by the Phillips Curve — doesn’t apply anymore.

This is a big admission by a Fed chairman given the importance of the Phillips Curve to the Fed’s economic analysis. The fact the Fed is confused by the apparent irrelevance of the Phillips Curve means the Fed is flying blind.

On the other hand, it could be that the inflation measure is simply wrong. The CPI has long been a measure based on a lot of arbitrary judgment calls, such as those that go into hedonic pricing. This method is used to push down inflation rates by claiming price increases aren’t as big as they seem because products have increased in quality. The reality for most people is that cars simply cost more now — although hedonic pricing would suggest the price of cars hasn’t really increased. But saying those aren’t real prices increases because they reflect increases in quality is a pretty tone-deaf way of looking at inflation.

So, it’s hard to know exactly what’s driving the thinking behind the rate cut. Is it politics? Do Fed members believe their inflation data? Or is the economy truly weaker than the headline data suggests?

We can only guess at the moment. We only know that the Fed is mostly blowing smoke when it tells us that the economy is fine, but we also need a rate cut. Either the Fed doesn’t know what’s going on, or it’s lying about the economy being “strong.” Or it’s just doing what Trump is telling it to do.

Keeping Interest Rates Low as Debt Rises

Another issue that must be mentioned in the importance of keeping interest rates low in an environment of runaway government spending.

As the national debt continues to rise above $22 trillion, and as the annual deficit — in a period of “expansion,” mind you — inches back toward one trillion per year, it becomes ever more important to keep debt service low by pushing down interest rates. As debt payments rise toward half a trillion dollars per year in the coming years, interest rates must be kept low, or federal programs will face real cuts in order to make payments on the debt. That means cuts to things like the Pentagon and Social Security. Those cuts would be politically unpopular. Thus, policymakers will need the Fed to keep debt payments down by manufacturing demand for government debt — via artificially low interest rates.

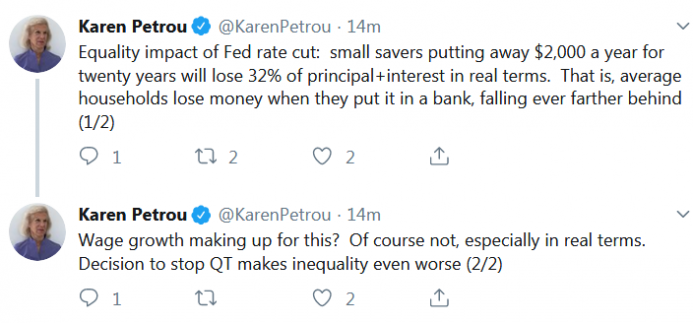

For ordinary and conservative savers, the effect of more than a decade of ultra-low rates has already been devastating. Thanks to the Fed, we now live in an economy designed for the ultra-rich on Wall Street who can afford to chase yield through high-risk investment instruments. For ordinary families who must save through lower-yield and lower-risk methods like savings accounts, this means they will continually lose purchasing power.

Fed policy has long been a war on ordinary families and savers. It’s a policy for the wealthy, and it worsens income inequality, as Petrou notes.

Future Problems

With the target rate now inching back toward 2 percent, the Fed will have even less room to maneuver when the next recession comes. But we don’t even need to wait for that. As Brendan Brown recently explained, we can already see the effect of ultra-low rates in increasing anemic economic growth numbers, and in withering real world savings and capital accumulation. We may not see a dramatic, crash, but simply see growth continue to under-perform.

In any case, the future doesn’t look good for people on fixed income, middle-income savers, or people in general who aren’t already property-owning millionaires.

via ZeroHedge News https://ift.tt/2Mzw9yr Tyler Durden