Democratic Party Official Admits He Took Bribes To Stuff Ballot Boxes Tyler Durden

Thu, 05/21/2020 – 16:25

The US Attorney’s Office in Philadelphia obtained a guilty plea from a Democratic Party elections judge, who admitted to taking bribes to stuff ballot boxes in favor of Democratic candidates in 2014, 2015 and 2016.

According to the Department of Justice, 73-year-old Domenick J. DeMuro was indicted for “conspiracy to deprive Philadelphia voters of their civil rights by fraudulently stuffing the ballot boxes for specific Democratic candidates,” as well as violating the Travel Act, which “forbids the use of any facility in interstate commerce (here, a cell phone) with the intent to promote certain illegal activity (here, bribery).”

DeMuro charged up to $5,000 per election to rig the votes for an unnamed “political consultant,” who in turn charged his clients “consulting fees” which were used to pay off multiple Election Board Officials.

The Judge of Elections is an elective office and a paid position. In that role, DeMuro was responsible for overseeing the entire election process and voter activities of his Division. The Judge of Elections is charged with overseeing the Division’s polling place in accordance with federal and state election laws and is required to attend Election Board Training conducted by the Philadelphia City Commissioners.

The voting machines at each polling station, including DeMuro’s station, generate records in the form of a printed receipt documenting the use of each voting machine. The printed receipt, also known as the “results receipt,” shows the vote totals, and the Judge of Elections and other Election Board Officials at each polling place attest to the accuracy of machine results.

During his guilty plea hearing, DeMuro admitted that an unnamed political consultant gave DeMuro directions and paid him money to illegally add votes for certain Democratic candidates. These candidates were individuals running for judicial office whose campaigns had hired the consultant, as well as other candidates for various federal, state, and local elective offices who were preferred by this consultant for a variety of reasons. –DOJ

“DeMuro fraudulently stuffed the ballot box by literally standing in a voting booth and voting over and over, as fast as he could, while he thought the coast was clear,” said US Attorney William M. McSwain. “Voting is the cornerstone of our democracy. If even one vote is fraudulently rung up, the integrity of that election is compromised.”

via ZeroHedge News https://ift.tt/3galFlt Tyler Durden

Bitcoin & Bullion Battered As Stocks, Bonds, & The Dollar Do Nothing Tyler Durden

Thu, 05/21/2020 – 16:01

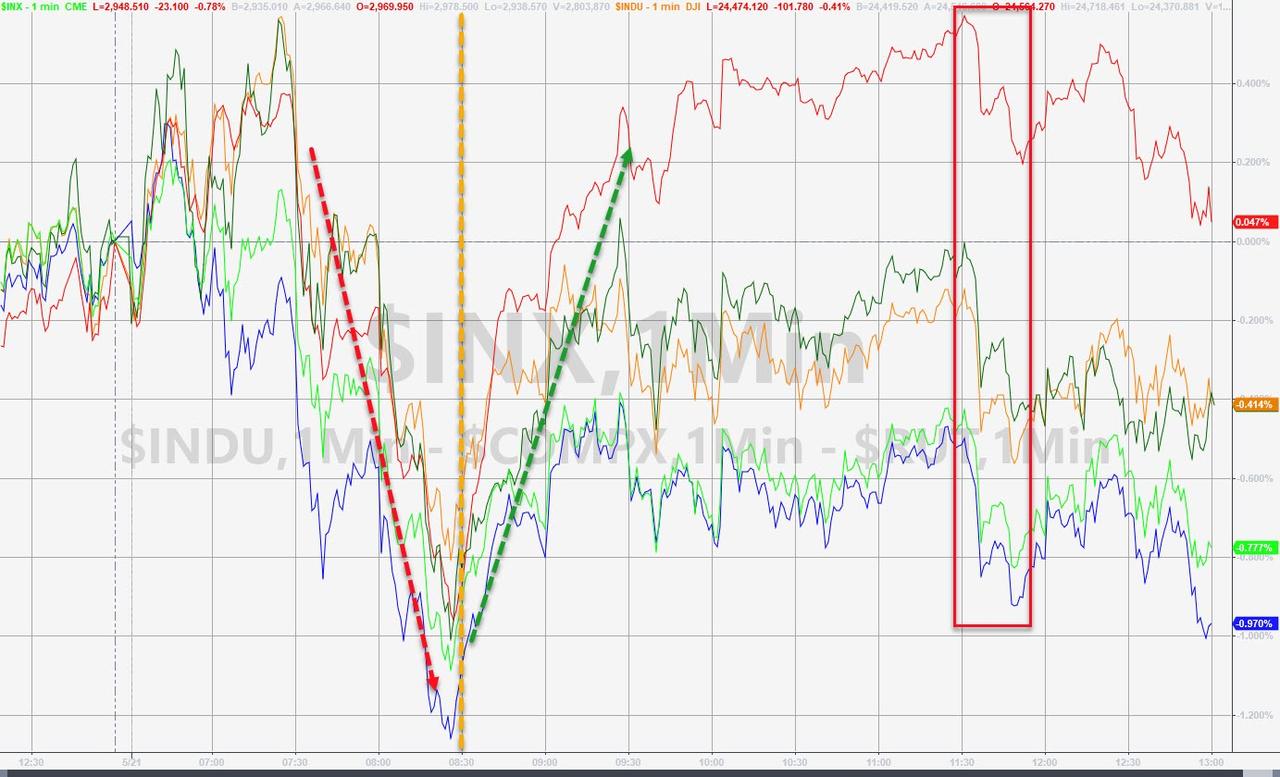

Another 2.4 million Americans added to the jobless rolls, China tensions soar, Leading Indicators were a disaster, Housing Data a shitshow, PMIs bounced but remain historically bad… so buy small cap (domestically focused) stocks, and dump gold, silver, and cryptos…

Gold puked on major volume at 10amET…

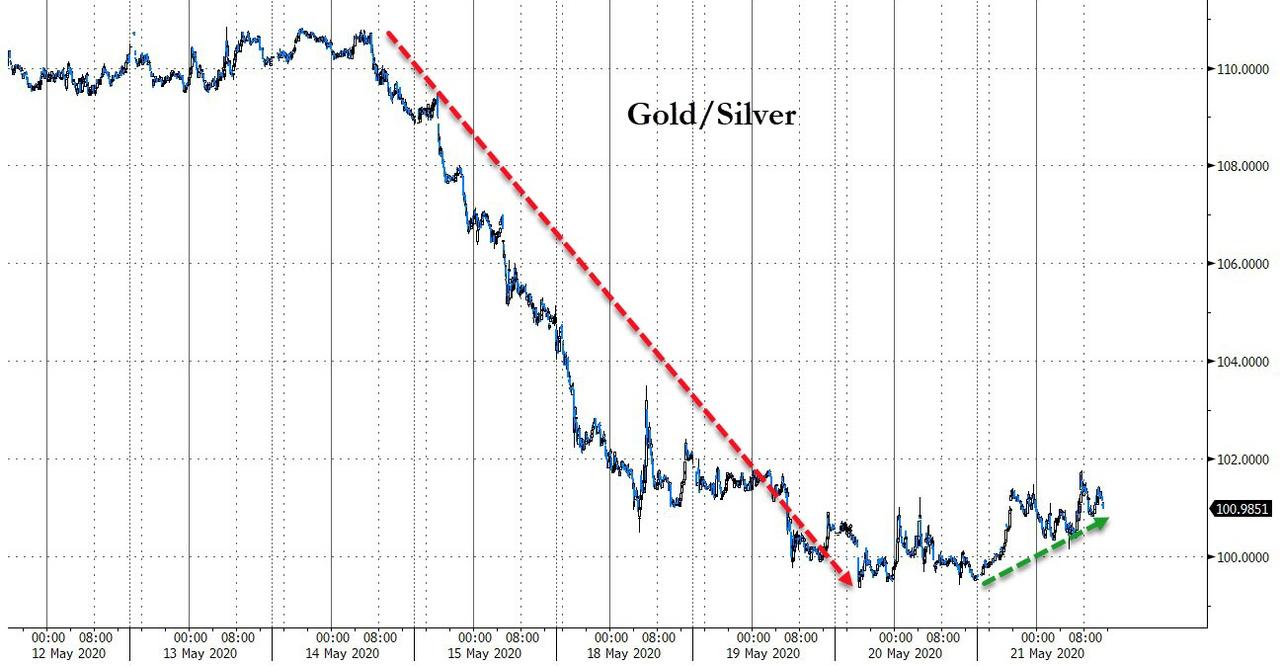

Silver was monkeyhammered even more than gold…

Which stalled the silver outperformance of late…

Source: Bloomberg

Bitcoin was also battered at the same time (around 10amET)…

Source: Bloomberg

Cryptos have erased a lot of the post-Bitcoin-Halving gains…

Source: Bloomberg

Notably, the plunge in bullion and bitcoin coincided with the ugly PMI data and a jolt lower in Fed Rate expectations (back towards negative rates)…

Source: Bloomberg

Nasdaq was the laggard on the day but Small Caps were manically bid off the European Close lows (and took a hit on the China sanction headlines late on)…

As shorts were squeezed yet again…

Source: Bloomberg

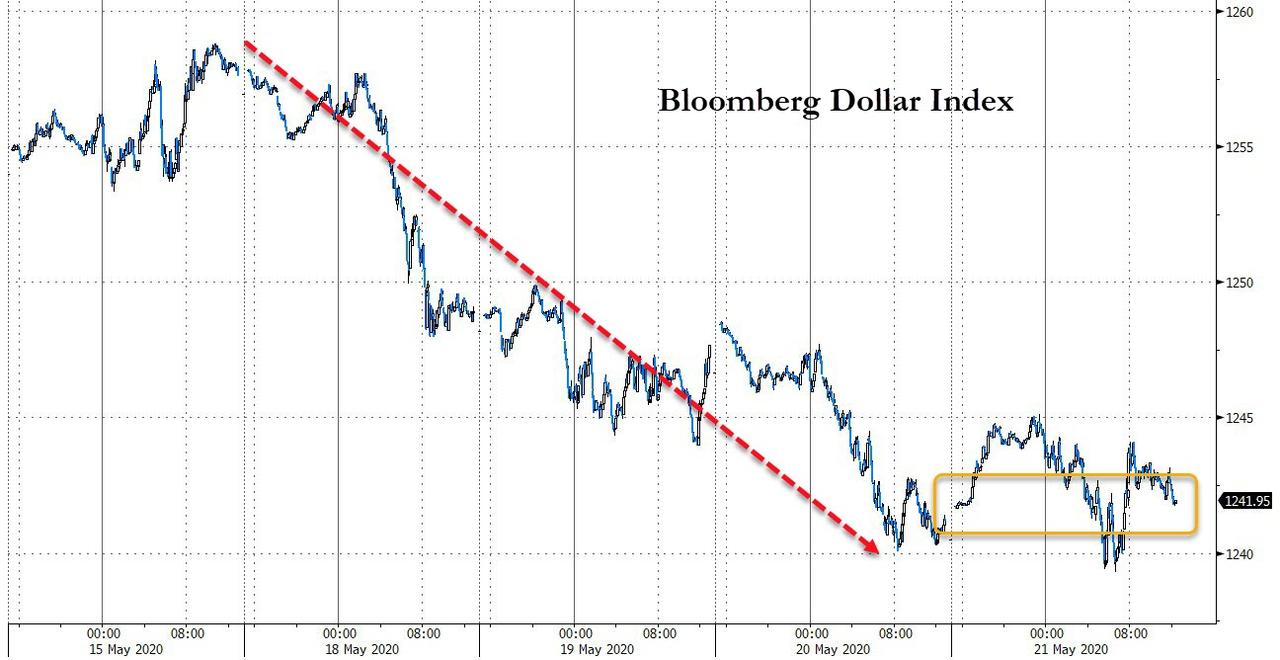

Meanwhile, The dollar did nothing…

Source: Bloomberg

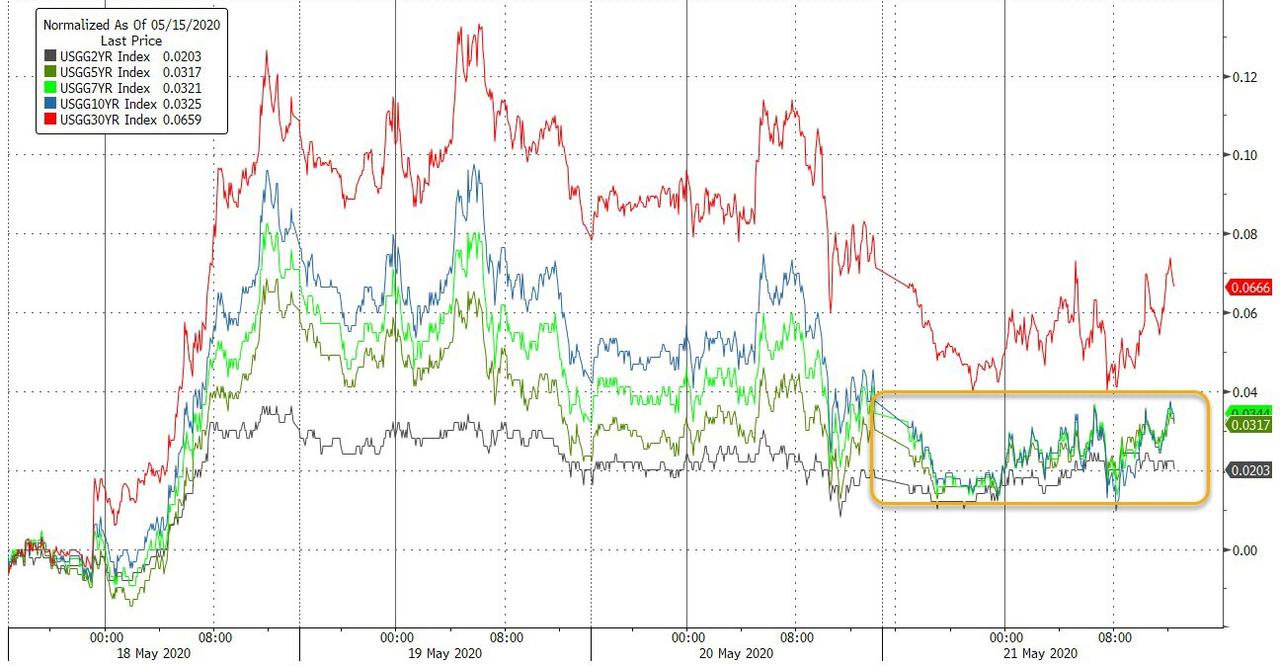

Bonds did nothing… (long-end yields rose around 1bps on a major corporate issuance day)

Source: Bloomberg

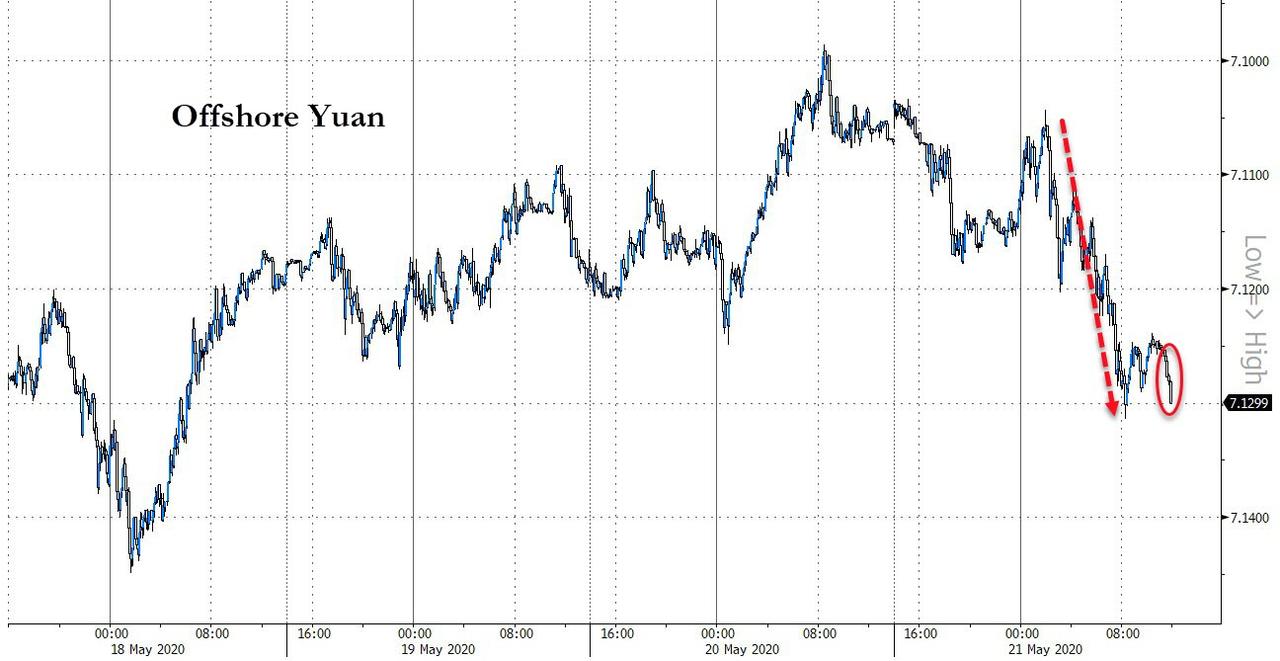

Yuan was dumped as sanctions and threats were traded…

Source: Bloomberg

Finally, whatever The Fed, The Market, The Politicians are doing… it’s not working for sentiment…

Source: Bloomberg

Americans haven’t been this pessimistic about current economic conditions in six years. The Bloomberg Consumer Comfort Index fell to 34.7 last week, a 1.1-point drop from the prior week and its ninth straight weekly decline, matching the longest streak on record.

via ZeroHedge News https://ift.tt/2Tpf6S3 Tyler Durden

The coerced economic “shutdowns” – enforced with fines, arrests, and revoked business licenses – are not the natural outgrowth of a pandemic. They are the result of policy decisions taken by politicians who have suspended constitutional institutions and legal recognition of basic human rights. These politicians have instead imposed a new form of central planning based on an unproven, theoretical set of ideas about police-enforced “social distancing.”

None of that is being considered, however, since it is now fashionable to have governments determine whether or not people may open their businesses or leave their homes. So far, the strategy for dealing with the resulting economic collapse is no more sophisticated than record-breaking deficit spending, followed by debt monetization via money printing. In short, politicians, bureaucrats, and their supporters have insisted a single policy goal—ending the spread of a disease—be allowed to destroy all other values and considerations in society.

Has it even worked? Mounting evidence says no.

In The Lancet, Swedish infectious disease clinician (and World Health Organization (WHO) advisor) Johan Giesecke concluded:

It has become clear that a hard lockdown does not protect old and frail people living in care homes – a population the lockdown was designed to protect. Neither does it decrease mortality from COVID-19, which is evident when comparing the UK’s experience with that of other European countries.

At best, lockdowns push cases into the future, they do not lower total deaths. Gieseck continues:

Measures to flatten the curve might have an effect, but a lockdown only pushes the severe cases into the future—it will not prevent them. Admittedly, countries have managed to slow down spread so as not to overburden health-care systems, and, yes, effective drugs that save lives might soon be developed, but this pandemic is swift, and those drugs have to be developed, tested, and marketed quickly. Much hope is put in vaccines, but they will take time, and with the unclear protective immunological response to infection, it is not certain that vaccines will be very effective.

As a public policy measure, the lack of evidence that lockdowns work must be balanced with the fact that we have already observed that economic destruction is costly in terms of human life.

Yet in the public debate, lockdown enthusiasts insist that any deviation from the lockdown will result in total deaths far exceeding those places where there are lockdowns. So far, there is no evidence of this.

In a new study titled “Full Lockdown Policies in Western Europe Countries Have No Evident Impacts on the COVID-19 Epidemic,” author Thomas Meunier writes, “total deaths numbers using pre-lockdown trends suggest that no lives were saved by this strategy, in comparison with pre-lockdown, less restrictive, social distancing policies.” That is, the “full lockdown policies of France, Italy, Spain and United Kingdom haven’t had the expected effects in the evolution of the COVID-19 epidemic.”1

The premise here is not that voluntary “social distancing” has no effect. Rather, the question is to whether “police-enforced home containment” works to limit the spread of disease. Meunier concludes it does not.

The question the model set out to ask was whether lockdown states experience fewer Covid-19 cases and deaths than social-distancing states, adjusted for all of the above variables. The answer? No. The impact of state-response strategy on both my cases and deaths measures was utterly insignificant. The “p-value” for the variable representing strategy was 0.94 when it was regressed against the deaths metric, which means there is a 94 per cent chance that any relationship between the different measures and Covid-19 deaths was the result of pure random chance.

Overall, however, the fact that good-sized regions from Utah to Sweden to much of East Asia have avoided harsh lockdowns without being overrun by Covid-19 is notable.

Another study on lockdowns—again, we’re talking about forced business closures and stay-at-home orders here—is this study by researcher Lyman Stone at the American Enterprise Institute. Stone notes that areas where lockdowns were imposed either had already experienced a downward trend in deaths before the lockdown could have possibly shown effects or showed the same trend as the year prior. In other words, lockdown advocates have been taking credit for trends that had already been observed before lockdowns were forced on the population.

Stone writes:

Here’s the thing: there’s no evidence of lockdowns working. If strict lockdowns actually saved lives, I would be all for them, even if they had large economic costs. But the scientific and medical case for strict lockdowns is paper-thin.

Experience increasingly suggests that a more targeted approach is better for those who actually want to limit the spread of disease among the most vulnerable. The overwhelming majority—nearly 75 percent—of deaths from COVID-19 occur in patients over sixty-five years of age. Of those, approximately 90 percent have other underlying conditions. Thus, limiting the spread of COVID-19 is most critical among those who are already engaged with the healthcare system and are elderly. In the US and Europe, more than half of COVID-19 deaths are occuring in nursing homes and similar institutions.

This is why Matt Ridley at The Spectator quite reasonably observes that testing, not lockdowns, appears to be the key factor in limiting deaths from COVID-19. Those areas where testing is widespread have performed better:

Yet it is not obvious why testing would make a difference, especially to the death rate. Testing does not cure the disease. Germany’s strange achievement of a consistently low case fatality rate seems baffling—until you think through where most early cases were found: in hospitals. By doing a lot more testing, countries like Germany might have partly kept the virus from spreading within the healthcare system. Germany, Japan and Hong Kong had different and more effective protocols in place from day one to prevent the virus spreading within care homes and hospitals.

The horrible truth is that it now looks like in many of the early cases, the disease was probably caught in hospitals and doctors’ surgeries. That is where the virus kept returning, in the lungs of sick people, and that is where the next person often caught it, including plenty of healthcare workers. Many of these may not have realised they had it, or thought they had a mild cold. They then gave it to yet more elderly patients who were in hospital for other reasons, some of whom were sent back to care homes when the National Health Service made space on the wards for the expected wave of coronavirus patients.

We could contrast this with the policies of Governor Andrew Cuomo in New York, who mandated that nursing homes accept new residents without testing. This method nearly ensures that the disease will spread quickly among those who are most likely to die from it.

Meanwhile, Governor Cuomo saw fit to impose police-enforced lockdowns on the entire population of New York, ensuring economic ruin and ruined health for many non-COVID patients who were then cut off from vital treatments. Yet, disturbingly, lockdown fetishists like Cuomo are hailed as wise statesmen who “acted decisively” to prevent the spread of disease.

But this is the sort of regime we now live under. In the minds of many, it is better to abolish human rights and consign millions to destitution in the name of pursuing trendy unproven policies. The prolockdown party has even turned basic fundamentals of policy debate upside down. As Stone notes:

At this point, the question I usually get is, “What’s your evidence that lockdowns don’t work?”

It’s a strange question. Why should I have to prove that lockdownsdon’twork? The burden of proof is to show that they do work! If you’re going to essentially cancel the civil liberties of the entire population for a few weeks, you should probably have evidence that the strategy will work. And there, lockdown advocates fail miserably, because they simply don’t have evidence.

With economic output crashing worldwide and unemployment soaring to Great Depression levels, governments are already looking for a way out. Don’t expect to hear any mea culpas from politicians, but we can already see how governments are quickly moving toward a voluntary social-distancing, nonlockdown strategy. This comes even after politicians and disease “experts” have been insisting that lockdowns must be imposed indefinitely until there’s a vaccine.

The longer the lockdown-created economic destruction continues, the greater will be the threat of social unrest and even economic free fall. The political reality is thst the current situation cannot be sustained without threatening the regimes in power themselves. In an article for Foreign Policy titled “Sweden’s Coronavirus Strategy Will Soon Be the World’s,” authors Nils Karlson, Charlotta Stern, and Daniel B. Klein suggest that regimes will be forced to retreat to a Swedish model:

As the pain of national lockdowns grows intolerable and countries realize that managing—rather than defeating—the pandemic is the only realistic option, more and more of them will begin to open up. Smart social distancing to keep health-care systems from being overwhelmed, improved therapies for the afflicted, and better protections for at-risk groups can help reduce the human toll. But at the end of the day, increased—and ultimately, herd—immunity may be the only viable defense against the disease, so long as vulnerable groups are protected along the way. Whatever marks Sweden deserves for managing the pandemic, other nations are beginning to see that it is ahead of the curve.

via ZeroHedge News https://ift.tt/2WOEK4S Tyler Durden

“Feeding Fednzy”: Powell To Announce $2.5 Billion In Bond ETF Purchases Today Tyler Durden

Thu, 05/21/2020 – 15:38

One week ago we reported that after avoiding the capital markets for weeks, the Federal Reserve finally started waving corporate bond ETFs in, and as of May 13 owned $305 million in corporate bond ETFs under the Corporate Credit Facility, i.e., the corporate bond ETF buying program.

With the Fed set to provide its latest weekly balance sheet update at 4:30pm today, some are curious how many more bond ETFs (i.e., LQD and HYG) the Fed purchased in the past week to make sure stocks can only go up as companies use the mispriced bond market to issue even more bonds (up to $1 trillion YTD at last check) and repurchase their stock, if much more quietly.

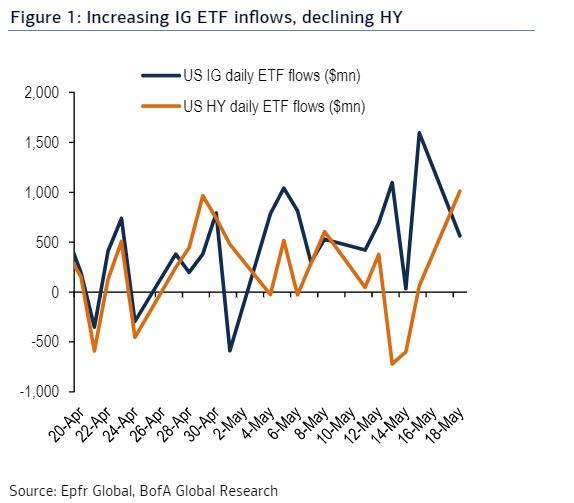

According to BofA’s credit strategist Hans Mikkelsen, the Fed has continued buying at roughly that average daily pace and the bank’s expectation is that the Fed will report holding around $2.5bn of corporate bond ETFs as of Tuesday this week.

Looking at daily IG ETF inflows they have risen to about $780bn after the Fed began buying from $360bn the prior period. Meanwhile, HY ETF inflows actually declined.

Trace data shows an estimated $5.3bn increase in dealer inventories after the Fed began buying ETFs, no doubt in part artificial because ETF creations are unreported and thus not subtracted from Trace…

… when dealers feed the Fed. IG and HY ETFs are trading at 0.44% and 0.30% premiums, respectively, on average, suggesting some limitations on specific ETFs the Fed can buy.

In short: the Fed likely purchased $2.5 billion in bond ETFs in the past week, once again steamrolling over even the faintest pretense that price discovery remains in a market where the perpetually high LQD and JNK prices mean companies can and will issue trillions in debt which they will promptly turn around and use to fund even more buybacks, as the Fed now fully owns the final bubble, the one where Soviet-style central planning is on full display.

via ZeroHedge News https://ift.tt/2ZwjYZP Tyler Durden

The U.S. government is asking the Supreme Court to block a federal judge’s injunction ordering a federal prison in Ohio to release elderly and at-risk inmates due to the threat of COVID-19.

U.S. District Judge James Gwin filed the injunction on Tuesday, after finding that the Bureau of Prisons (BOP) had not made enough progress with a previous order to identify inmates eligible for early release or transfer. By “thumbing their nose at their authority to authorize home confinement,” he wrote, prison officials “threaten staff and they threaten low security inmates.”

On Wednesday, U.S. Solicitor General Noel Francisco filed an application to the Supreme Court seeking a stay of the injunction. Arguing on behalf of the federal government, he said that letting Gwin’s injunction stand “would undermine BOP’s systemic response to the COVID-19 pandemic; intrude the Judicial Branch on policy decisions that have been assigned to expert prison administrators; and require BOP to defy the CDC’s guidance to restrict prisoner movements during the pandemic to avoid unnecessary risk of spreading the virus.”

The prison in question is FCI Elkton, a low-security institution in Ohio that houses approximately 2,500 inmates. So far, nine Elkton inmates have died of COVID-19, the most of any federal prison. According to the BOP’s latest reported numbers, 119 inmates and 8 staff are infected with the virus.

The American Civil Liberties Union (ACLU) of Ohio and the Ohio Justice & Policy Center filed the class-action lawsuit in April on behalf of four men incarcerated at Elkton. The suit argues that Elkton “failed to provide meaningful protection against the spread of the disease,” violating inmates’ Eighth Amendment protections against cruel and unusual punishment.

On March 27, following calls from lawmakers and advocacy groups to address the threat of COVID-19 in federal prisons, Attorney General William Barr issued a directive ordering the BOP to identify elderly and at-risk inmates who met certain criteria and release them, either through an early transfer to home confinement or through compassionate release.

Although the BOP has approved the early release of nearly 3,000 inmates, the rollout was hampered by contradictory rules; criminal justice advocates and families of inmates say the BOP only half-heartedly complied with it. In a letter to Congress earlier this month, a group of federal public defenders warned that the Department of Justice and the BOP “have made little use of these authorities to reduce prison populations and enable social distancing.”

On April 22, Gwin issued a preliminary injunction ordering Elkton officials to identify all elderly and at-risk inmates and evaluate them for early release within two weeks.

The Sixth Circuit Court of Appeals denied the Justice Department’s appeal of Gwin’s order on May 4.

On Tuesday, Gwin ruled that Elkton had made poor progress expanding testing and had made “only minimal effort to get at-risk inmates out of harm’s way.” Of the 837 elderly and at-risk inmates that Elkton officials identified, only five were pending transfer to home confinement. Meanwhile, one in four inmates had been infected by COVID-19.

Gwin’s injunction orders the prison “to make full use of the home confinement authority beyond the paltry grants of home confinement it has already issued.” It also requires officials to give detailed explanations for denials.

ACLU of Ohio Senior Staff Attorney David Carey said in a statement that the ruling “confirms the urgent need to comply with the Court’s order and respond to the crisis in an efficient and expedient manner.”

“The federal government has attempted to stall and delay the release of medically-vulnerable individuals at every single turn,” he continued.

The ACLU and other advocacy groups have filed numerous lawsuits against prisons and jails across the country since COVID-19 hit American shores. Earlier this month, a U.S. District judge in Connecticut ordered officials at Danbury federal prison to speed up their process for identifying inmates eligible for release, finding that their foot-dragging amounted to “deliberate indifference to a substantial risk of serious harm to inmates in violation of the Eighth Amendment.”

But Gwin’s injunction goes farther, and in fact requires Elkton officials to go beyond Barr’s directive. It orders them to disregard such criteria as the amount of sentence served, citizenship status, and violent offense restrictions, if the offense happened more than five years ago and would otherwise be the sole reason for disqualification.

The Justice Department, in its Supreme Court application, argues the BOP has mitigated the risk of COVID-19 at Elkton and that risk of the virus “could not remotely justify the peremptory order to remove more than 800 inmates from Elkton.”

from Latest – Reason.com https://ift.tt/3gaZBaj

via IFTTT

The U.S. government is asking the Supreme Court to block a federal judge’s injunction ordering a federal prison in Ohio to release elderly and at-risk inmates due to the threat of COVID-19.

U.S. District Judge James Gwin filed the injunction on Tuesday, after finding that the Bureau of Prisons (BOP) had not made enough progress with a previous order to identify inmates eligible for early release or transfer. By “thumbing their nose at their authority to authorize home confinement,” he wrote, prison officials “threaten staff and they threaten low security inmates.”

On Wednesday, U.S. Solicitor General Noel Francisco filed an application to the Supreme Court seeking a stay of the injunction. Arguing on behalf of the federal government, he said that letting Gwin’s injunction stand “would undermine BOP’s systemic response to the COVID-19 pandemic; intrude the Judicial Branch on policy decisions that have been assigned to expert prison administrators; and require BOP to defy the CDC’s guidance to restrict prisoner movements during the pandemic to avoid unnecessary risk of spreading the virus.”

The prison in question is FCI Elkton, a low-security institution in Ohio that houses approximately 2,500 inmates. So far, nine Elkton inmates have died of COVID-19, the most of any federal prison. According to the BOP’s latest reported numbers, 119 inmates and 8 staff are infected with the virus.

The American Civil Liberties Union (ACLU) of Ohio and the Ohio Justice & Policy Center filed the class-action lawsuit in April on behalf of four men incarcerated at Elkton. The suit argues that Elkton “failed to provide meaningful protection against the spread of the disease,” violating inmates’ Eighth Amendment protections against cruel and unusual punishment.

On March 27, following calls from lawmakers and advocacy groups to address the threat of COVID-19 in federal prisons, Attorney General William Barr issued a directive ordering the BOP to identify elderly and at-risk inmates who met certain criteria and release them, either through an early transfer to home confinement or through compassionate release.

Although the BOP has approved the early release of nearly 3,000 inmates, the rollout was hampered by contradictory rules; criminal justice advocates and families of inmates say the BOP only half-heartedly complied with it. In a letter to Congress earlier this month, a group of federal public defenders warned that the Department of Justice and the BOP “have made little use of these authorities to reduce prison populations and enable social distancing.”

On April 22, Gwin issued a preliminary injunction ordering Elkton officials to identify all elderly and at-risk inmates and evaluate them for early release within two weeks.

The Sixth Circuit Court of Appeals denied the Justice Department’s appeal of Gwin’s order on May 4.

On Tuesday, Gwin ruled that Elkton had made poor progress expanding testing and had made “only minimal effort to get at-risk inmates out of harm’s way.” Of the 837 elderly and at-risk inmates that Elkton officials identified, only five were pending transfer to home confinement. Meanwhile, one in four inmates had been infected by COVID-19.

Gwin’s injunction orders the prison “to make full use of the home confinement authority beyond the paltry grants of home confinement it has already issued.” It also requires officials to give detailed explanations for denials.

ACLU of Ohio Senior Staff Attorney David Carey said in a statement that the ruling “confirms the urgent need to comply with the Court’s order and respond to the crisis in an efficient and expedient manner.”

“The federal government has attempted to stall and delay the release of medically-vulnerable individuals at every single turn,” he continued.

The ACLU and other advocacy groups have filed numerous lawsuits against prisons and jails across the country since COVID-19 hit American shores. Earlier this month, a U.S. District judge in Connecticut ordered officials at Danbury federal prison to speed up their process for identifying inmates eligible for release, finding that their foot-dragging amounted to “deliberate indifference to a substantial risk of serious harm to inmates in violation of the Eighth Amendment.”

But Gwin’s injunction goes farther, and in fact requires Elkton officials to go beyond Barr’s directive. It orders them to disregard such criteria as the amount of sentence served, citizenship status, and violent offense restrictions, if the offense happened more than five years ago and would otherwise be the sole reason for disqualification.

The Justice Department, in its Supreme Court application, argues the BOP has mitigated the risk of COVID-19 at Elkton and that risk of the virus “could not remotely justify the peremptory order to remove more than 800 inmates from Elkton.”

from Latest – Reason.com https://ift.tt/3gaZBaj

via IFTTT

YouTube on Wednesday reinstated a video it has previously censored in which several medical doctors suggested that the drug hydroxychloroquine might be useful in treating coronavirus, with the company reportedly claiming at the time of censorship that the presentation was “dangerous.”

The video report, presented by Sharyl Attkisson at Full Measure News, examined the possible benefits of hydroxychloroquine as a treatment for COVID-19 and the possible financial interest some parties have in downplaying the drug and promoting a separate treatment called remdesivir.

One of the doctors interviewed in the video, William O’Neill, tells Attkisson, also a Just the News contributor, that there is “some value” to hydroxychloroquine and “it has to be tested.”

O’Neill, a cardiologist in Detroit, has prescribed the drug to multiple patients and “saw improvement in all of them,” Attkisson reported.

At the Henry Ford Health System, where O’Neill works, officials are working with hydroxychloroquine and remdesivir. The doctor said the media campaign against the drug, which began around the time President Trump first started touting it, has left patients “scared to use the drug without any scientifically valid concern.”

“We’ve talked with our colleagues at the University of Minnesota who are doing a similar study, and at the University of Washington,” he said.

“We’ve treated 400 patients and haven’t seen a single adverse event. And what’s happening is because of this fake news and fake science, the true scientific efforts are being harmed because people now are so worried that they don’t want to enroll in the trials.”

Another physician, Dr. Jane Orient, the executive director of the Association of American Physicians and Surgeons as well as a clinical lecturer at the University of Arizona College of Medicine, urged viewers to “look at the money” when it comes to the two drugs.

“There’s no big profits made in hydroxychloroquine,” said Orient.

“It’s very cheap, easy to manufacture, been around for 70 years. It’s generic. Remdesivir is a new drug that could be very expensive and very lucrative if it’s ever approved. So I think we really do have to consider there’s some financial interest involved here.”

‘These are organized efforts’

Sharyl Attkisson on Wednesday afternoon told Just the News that it wasn’t immediately clear when the video was removed

It was originally uploaded to YouTube two days ago. Attkisson said YouTube had removed the presentation with a note claiming that it was “dangerous,” without offering any explanation as to why.

She said Full Measure News appealed the removal, after which YouTube subsequently reinstated it.

“These are organized efforts,” she said, arguing that politically biased parties are behind efforts to remove or censor contrarian information on social media.

“They know they can use these systems to limit information. It’s very frightening because I feel like if something’s not done, in five years, we’re going to be telling our kids, ‘There was once a time we could get any information we wanted on the Internet.’ That’s changing. We can’t anymore.”

She noted recent efforts by Democratic Rep. Adam Schiff, the chairman of the House Intelligence Committee, to pressure social media companies to censor and downgrade “harmful” coronavirus-related material and push users instead toward information from the World Health Organization.

“Nobody appointed Adam Schiff to police our content on social media.”

Full Measure News noted that it tried to contact White House coronavirus task force member Dr. Anthony Fauci, the drug company Gilead (which manufactures remdesivir), and numerous doctors who have “criticized or are skeptical of hydroxycholoroquine.” None responded to the interview requests.

via ZeroHedge News https://ift.tt/3gaSizp Tyler Durden

Senators Introduce Bill Sanctioning Chinese Officials, Banks Over Hong Kong Crackdown Tyler Durden

Thu, 05/21/2020 – 15:03

Shortly after it became clear that China has run out of patience with Hong Kong, when as reported earlier China’s National Congress adopted a resolution calling for a new National Security law in Hong Kong, US senators immediately responded to China’s attempt to further crackdown on Hong Kong autonomy as Beijing moves to stop widespread pro-democracy protests that have challenged leader Xi Jinping, by introducing a bipartisan bill that would sanction Chinese party officials and entities who enforce the new national-security laws in Hong Kong, with the legislation also would penalizing banks that do business with the entities, according to the WSJ.

The latest bill in a recent barrage of legislation targeting China comes one day after the Senate also passed a bill that could force the de-listing of Chinese companies in the US.

Senators Chris Van Hollen (D., Md.) and Pat Toomey (R., Pa) said they had been working on the bill already but Thursday’s developments made the legislation more urgent, and said they would urge Senate leaders to take up the matter quickly.

“We would impose penalties on individuals who are complicit in China’s illegal crackdown in Hong Kong,” Van Hollen said quoted by the WSJ. He called the move by Beijing “a gross violation” of China’s agreement with the U.K. to preserve more freedom and autonomy in the territory. Toomey called the move by China “very, very deeply disturbing.”

Last year, Trump signed a bill designed to show solidarity with pro-democracy protesters in Hong Kong, despite expressing concerns it could complicate U.S.-China trade talks.

So far stocks have continued to ignore the constant escalation in tensions between the US and China clearly convinced that it is all just political theater, but when it comes to Hong Kong and US intervention in what Beijing deems “local matters”, not to mention the ongoing feud over the origin of the coronavirus crisis, China couldn’t be more serious, and with the China’s National People’s Congress starting tomorrow, a harsh response is inevitable.

via ZeroHedge News https://ift.tt/2XmmyPn Tyler Durden

Initially, we were told that the coronavirus lockdowns would just “temporarily” disrupt the U.S. economy, but now it is becoming clear that a lot of the damage will be permanent.

We are starting to see businesses go belly up all over the country, and this includes some of the most iconic names in the retail world. When J.C. Penney announced that it would be declaring bankruptcy and closing hundreds of stores, I warned that would just be the tip of the iceberg, and that has definitely turned out to be the case. In fact, on Wednesday many analysts were absolutely shocked when news broke that Victoria’s Secret has decided to shut down about 250 stores…

Victoria’s Secret plans to permanently close approximately 250 stores in the U.S. and Canada in 2020, its parent company L Brands announced Wednesday.

L Brands also plans to permanently close 50 Bath & Body Works stores in the U.S. and one in Canada, according to information the company posted online as part of its quarterly earnings.

If this pandemic had passed quickly, perhaps those stores wouldn’t have needed to be shut down. But at this point it has become obvious that this virus is going to be with us for a long time to come. In fact, the WHO just announced that on a global basis we just witnessed the largest number of newly confirmed cases on a single day so far.

Pier 1 Imports, which previously said it would close half of its fleet of stores, now plans to close all of its locations.

The retailer, based in Fort Worth, Texas, announced in a news release Tuesday that it was seeking bankruptcy court approval to begin an “orderly wind-down” when stores are able to reopen “following the government-mandated closures during the COVID-19 pandemic.”

I was never a huge fan of Pier 1 Imports, but my wife liked to visit and see what they had, but now we will never be able to do that again.

Something about that really saddens me.

Of course it isn’t just retailers that are collapsing. Car rental giant Hertz “is on the verge of bankrutpcy”, and things are not looking good at all…

Hertz is on the verge of bankruptcy. At the end of April, it disclosed it had missed a large amount of lease payments on its rental cars. Since then, it has entered into forbearance and waiver agreements with these lenders that give it until May 22 to come up with the money and a plan. Its cars, now parked at various parking lots around the country, are collateral for this debt.

Some of you old timers might remember the old Hertz commercials featuring O.J. Simpson. Those were much simpler times, and to be honest I really miss them.

Unfortunately, times have really changed, and I seriously doubt that Hertz will be able to survive much longer in this very harsh economic environment.

Needless to say, a lot of businesses are going to die in the weeks and months ahead of us. As I discussed the other day, it is now being projected that approximately one out of every four restaurants in the United States will be closing down permanently.

Can you imagine what this is going to look like?

We are going to have abandoned buildings all over the place, and this will especially be true in our more impoverished communities.

The only chance we have of pulling out of this economic death spiral is if there is a full scale return to normal economic activity all across America, but that isn’t going to happen any time soon.

Fear of COVID-19 is going to paralyze small and big businesses alike for the foreseeable future, and every new outbreak is going to spark more overreactions.

Just days after reopening its American assembly plants, Ford temporarily shut down two separate factories because employees tested positive for Covid-19.

One plant in Chicago that builds the Ford Explorer, the Lincoln Aviator and the Ford Interceptor police car stopped operations Tuesday afternoon after two employees tested positive for Covid-19. Then, Ford’s plant in Dearborn Michigan that makes its bestselling F-150 pickup, shut down Wednesday.

If we keep shutting things down every time someone gets sick, our economic problems are just going to get worse and worse.

A new study suggests the number of Americans who will die after contracting the novel coronavirus is likely to more than triple by the end of the year, even if current social distancing habits continue for months on end.

The study, conducted by the Comparative Health Outcomes, Policy and Economics Institute at the University of Washington’s School of Pharmacy, found that 1.3 percent of those who show symptoms of COVID-19 die, an infection fatality rate that is 13 times higher than a bad influenza season.

Of course it certainly doesn’t help that we continue to allow people from other countries where COVID-19 is raging to fly into the U.S. without any special screening whatsoever…

A glamorous Russian blogger says she has proved that the US is open for foreign tourism again, despite the pandemic, according to video obtained by DailyMail.com.

Sofia Semyonova, 33, a fitness model, told how she traveled on a crammed Aeroflot flight with 500-plus passengers with ‘no social distancing’ from Moscow to New York City.

She used her B2 tourist visa to enter America from Russia’s coronavirus epicentre ‘in 30 seconds without any extra questions’.

I don’t know how this could possibly be happening, but apparently it is.

Eventually, COVID-19 will literally be just about everywhere, and almost everyone in the entire country will be exposed to it.

And fear of this virus will paralyze our economy for the foreseeable future.

So the truth is that the “for lease” and “space available” signs that you are now seeing are just the start.

A lot more are coming, and it is going to be a very dark chapter for our nation.

via ZeroHedge News https://ift.tt/3bRyUEf Tyler Durden

On March 19, the Ohio Department of Health ordered the closure of “hair salons, nail salons, barber shops, tattoo parlors, body piercing locations, and massage therapy locations” as part of the state’s efforts to combat the spread of COVID-19. Nearly two months later, Gov. Mike DeWine announced that hair salons and barber shops would be allowed to reopen shortly, so long as they followed various social distancing and public health requirements.

There was no mention of letting tattoo artists get back to work. “We were closed with salons, barbers, tanning salons and the like,” the Oxford, Ohio, tattooist Steve Cupp told WLWT5. “And we assumed once they opened, considering the proximity they have to their clients and the proximity that we have to ours, that we would be reopened with them. But we were excluded.” The state eventually announced that tattoo shops would finally be allowed to reopen on May 15.

This sort of government action raises some interesting legal questions, especially for the numerous tattoo parlors that remain shuttered in other states. Do tattoo artists have a case to make against coronavirus closure orders? Does the Constitution protect a tattoo shop’s right to remain open—at least in some limited fashion—during the pandemic?

The idea is not so far-fetched. Both state and federal courts have recognized tattooing as a constitutionally protected form of free expression. Up until the year 2000, for example, it was a crime in Massachusetts, punishable by up to one year in prison, for any person except a doctor to mark “the body of any person by means of tattooing.” But in Lanphear v. Commonwealth of Massachusetts, the Massachusetts Superior Court struck down that statewide ban on the grounds that “the act of tattooing is inseparable from the display of the tattoo itself and is expression protected by the First Amendment.”

The U.S. Court of Appeals for the 9th Circuit reached the same conclusion in Anderson v. City of Hermosa Beach (2010). At issue was that city’s ban on tattoo shops within city limits. “The tattoo itself, the process of tattooing, and the business of tattooing are forms of pure expression fully protected by the First Amendment,” declared a unanimous 9th Circuit panel.

Which brings us back to the idea of a tattoo artist mounting a legal challenge to a coronavirus closure order. In United States v. Carolene Products Co. (1938), the U.S. Supreme Court said that when the courts review a regulation “affecting ordinary commercial transactions…the existence of facts supporting the legislative judgment is to be presumed.” In other words, judges were told to be extremely deferential towards the government when it is regulating economic activity.

But Carolene Products did not endorse judicial passivity on all fronts. “More exacting judicial scrutiny,” the Court said, would still be appropriate in some cases. For example, judges should not defer to the government by rote in matters involving “a specific prohibition of the Constitution, such as those of the first ten amendments.” Lawyers now call this exacting approach “strict scrutiny.” In the words of Black’s Law Dictionary, for a law or regulation to survive strict scrutiny review, it “should only be as restrictive as is necessary to accomplish a legitimate governmental purpose.”

“The business of tattooing,” as the 9th Circuit put it, is “fully protected by the First Amendment.” Which means that any regulation of a tattoo shop should trigger strict scrutiny review when that regulation lands in court.

A public health order designed to curb the spread of an infectious disease like COVID-19 would seem to pass the “legitimate governmental purpose” prong of the strict scrutiny test. But what about the second prong, which requires the regulation to be the least restrictive means of pursuing that legitimate state end?

Here is where the tattoo shops may have a case. So long as they can operate safely during the coronavirus outbreak—by requiring artists and clients to wear masks and gloves at all times, by routinely cleaning equipment and surfaces, by carefully practicing social distancing, by limiting the number of people allowed inside the shop, etc.—a total shutdown of the business would not seem to qualify as the least restrictive means available for achieving a legitimate government purpose, even amid a pandemic.