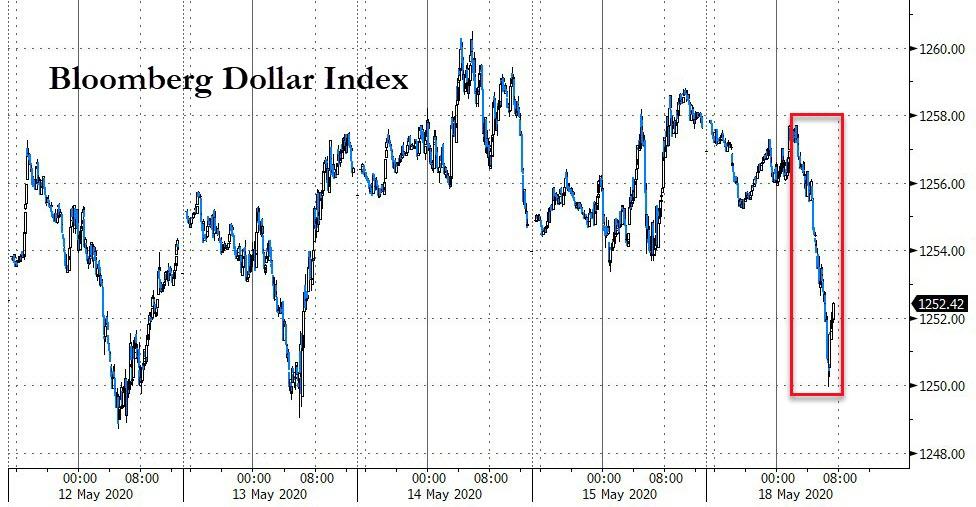

Gold, Silver, Dollar, & Bonds Dumped Because 8 Healthy Young People Didn’t Die From Test Vaccine Tyler Durden

Mon, 05/18/2020 – 10:26

Great news America – 8 healthy, young people did not show any adverse effects from being injected with a potential vaccine for COVID-19…

“All eight initial participants” in the Moderna trial developed neutralizing antibodies to the virus at levels reaching or exceeding those seen in people who have naturally recovered from Covid-19, according to the press release.

Problem solved!? (But, one quick question – isn’t that the whole premise of immune response? How about when someone is injected with this ‘vaccine’ who has any number of the comorbidities that have killed 10s of 1000s… or has the coronavirus.)

But, never mind that! Buy all the stock market things…

And sell bonds…

Sell the dollar…

Sell silver…

And Sell gold…

Sparking a jump in the collapse of the Gold/Silver ratio…

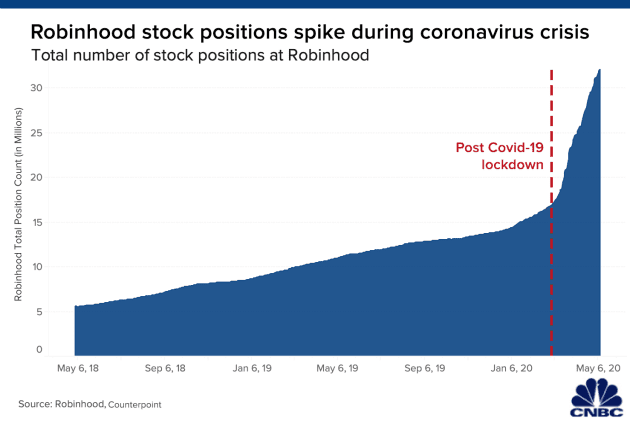

How long can they make this last? One thing is for sure, they better get Robinhood back up and running soon – who are we are all going to sell to otherwise?

via ZeroHedge News https://ift.tt/2WFybl6 Tyler Durden

The contradictions revealed in recent disclosures, including the list of officials seeking to “unmask” the identity of former National Security Adviser Michael Flynn, are shocking. There seems a virtual news blackout on these disclosures, including the fact that both former President Barack Obama and former Vice President Joe Biden followed the investigation. Indeed, Biden’s name is on the unmasking list.

The declassification of material from the Michael Flynn case has exposed more chilling details of an effort by prosecutors to come up with a crime to use against the former national security adviser. This week, however, a letter revealed another unsettling detail. Among over three dozen Obama administration officials seeking to “unmask” Flynn in the investigation was former Vice President Joe Biden. This revelation came less than a day after Biden denied any involvement in the investigation of Flynn. It also follows a disclosure that President Obama was aware of that investigation.

For three years, many in the media have expressed horror at the notion of the Trump campaign colluding with Russia to influence the 2016 election. We know there was never credible evidence of such collusion. In recently released transcripts, a long list of Obama administration officials admitted they never saw any evidence of such Russian collusion. That included the testimony of Evelyn Farkas, a former White House adviser who was widely quoted by the media with her public plea for Congress to gather all of the evidence that she learned of as part of the Obama administration.

The media covered her concern that this evidence would be lost “if they found out how we knew what we knew” about Trump campaign officials “dealing with Russians.” Yet in her classified testimony under oath, she said she did not know anything. Farkas is now running for Congress in New York and highlighting her role in raising “alarm” over collusion. As much of the media blindly pushed this story, a worrying story unfolded over the use of federal power to investigate political opponents.

There is very little question that the response by the media to such a story would have been overwhelming if George Bush and his administration had targeted the Obama campaign figures with secret surveillance.

That story would have been encompassing if it was learned that there was no direct evidence to justify the investigation and that the underlying allegation of Russian collusion was ultimately found to lack a credible basis.

But the motives of Obama administration officials are apparently not to be questioned. Indeed, back when candidate Donald Trump said the Obama administration placed his campaign officials under surveillance, the media universally mocked him. That statement was later proven to be true. The Obama administration used the secret Foreign Intelligence Surveillance Act court to conduct surveillance of Trump campaign officials.

Yet none of this matters as the media remains fully invested in the original false allegations of collusion. If Obama administration officials were to be questioned now, the coverage and judgment of the media may be placed into question, as even this latest disclosure from the investigation of the unmasking request of Biden will not alter the media narrative.

Unmasking occurs when an official asks an intelligence agency to remove anonymous designations hiding the identity of an individual. This masking is a very important protection of the privacy of American citizens who are caught up in national security surveillance. The importance of this privacy protection is being dismissed by media figures, like Andrea Mitchell, who declared the Biden story to be nothing more than gaslighting.

While unmasking is more routinely requested by intelligence officials, with a reported 10,000 such requests by the National Security Agency last year alone, it is presumably less common for figures like Biden or White House chief of staff Denis McDonough. Seeking unmasking information that was likely to reveal the name of a political opponent and possibly damage the Trump administration raises a concern. More importantly, it adds a detail of the scope of interest and involvement in an investigation that targeted Flynn without any compelling evidence of a crime or collusion.

The media portrayed both Obama and Biden as uninvolved. But now we know they both actively followed the investigation.

According to former acting attorney general Sally Yates, she was surprised that Obama knew about the investigation and knew more than she did at the time. Obama called upon former FBI director James Comey to stay after a meeting to discuss the investigation. Comey had mentioned using the Logan Act to charge Flynn, even though the unconstitutional law has never been used successfully in a prosecution since the country was founded.

Biden has repeatedly denied knowledge of the investigation. Just a day before the latest disclosure, George Stephanopoulos asked Biden in an interview what he knew of the Flynn investigation. Biden was adamant that he knew nothing about “those moves” and he called it a diversion. But that is not true if he took the relatively uncommon action for a vice president of demanding the unmasking of Flynn information.

Yet none of this matters. A Democratic administration using a secret court to investigate the opposing political campaign does not matter to many in Congress or in the media anyway. An investigation continuing despite the lack of credible information supporting collusion does not matter to them either. A president and a vice president who take personal interest in the surveillance of their political opponents also does not matter.

There was a time, however, when all of this did matter. There was once a time when this would be viewed as the story of the century, including the unmasking of Biden himself in this investigation. But these are not those times, and this cannot be the story. Russian collusion is the story and, as Biden stressed, the rest is just a diversion. It is up to the public to decide who has been ultimately unmasked by the Flynn investigation.

via ZeroHedge News https://ift.tt/3bJpWZs Tyler Durden

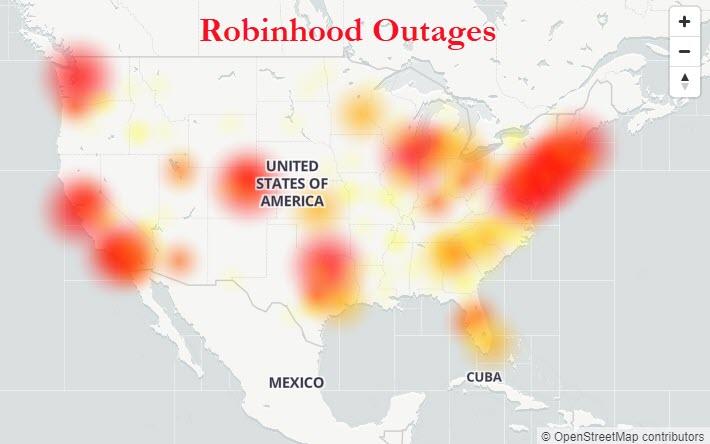

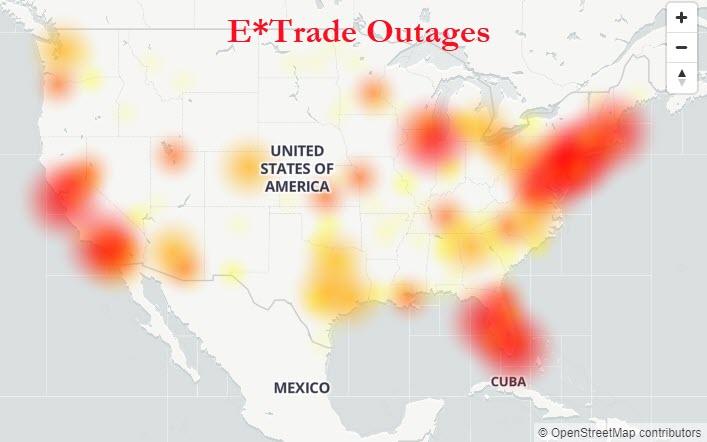

Retail Rout? Robinhood & E*Trade Are Down! Tyler Durden

Mon, 05/18/2020 – 09:48

This is a major problem for the bulls…

“I felt a great disturbance in the farce, as if millions of bullish Millennials cried out in terror and were suddenly silenced. I fear something terrible may happen…”

While Moderna sparked the squeeze, we’re gonna need Millennials back in this market to lift it out of its one-month funk… even if Powell goes back on ’60 Minutes’ this weekend.

via ZeroHedge News https://ift.tt/2AF899c Tyler Durden

Who? None other than Fed Chair Powell – saying on ’60 minutes’ for a mainstream audience that “Assuming there’s not a second wave of the coronavirus, I think you’ll see the economy recover steadily in the second half of this year.” However, he then added “For the economy to fully recover people will have to be fully confident, and that may have to await the arrival of a vaccine,” and that a full recovery could take until the end of 2021. So while no Great Depression in his eyes, no V-shape either, and no return to normality until medicine or nature step up to the plate. That looks a timely call as Friday saw retail sales collapsed the most on record in April.

Powell also reiterated that he was not of the view that negative rates will be useful in the US, but that there is a lot more the government can do, perhaps via direct support to states and municipalities. Moreover, he stressed there is a lot more the Fed can do too – so yield curve control and more QE? At least that’s what he’s most likely to explain to the Senate when he testifies tomorrow. In which case, then Fed will be hoovering up more of the safe (and not so safe!) US assets out there that markets would otherwise be able to get hold of. And failing to do so will see a further USD liquidity squeeze as the rest of the market steps up to buy those safe assets instead.

Meanwhile, the ‘WHO’ is in focus today as geopolitics comes (even more obviously) to the World Health Organisation. We are going to see a motion (with the final vote apparently Wednesday) to push for an international investigation into the origins of COVID-19. The one that the sudden problems exporting Australian beef and barley to China have nothing to do with. (And – who?! The Aussie Trade Minister is now warning about the risks of doing business with China and that firms may want to look at diversification!)

So far at least 62 countries including Russia(!), and perhaps as high as 116 together with a block of African states, are co-sponsoring a motion for a virus investigation. China and its supporters are not. The event has all the makings of a contemporary Khrushchev-bashing-his-shoe-on-the-table-at-the-UN moment.

More so as on Friday the US Commerce Department tightened its limitations on the export of key technology to Huawei, this time with what look like real teeth, to target third parties and third countries; and China’s Global Times immediately reported that Beijing is considering striking back with measures at key US firms, including Boeing. Plus US Secretary of State Pompeo has just warned Hong Kong that “any action to interfere and impinge on Hong Kong’s freedoms” in the form of steps against US journalists, who have already had to leave China in some cases, “would impact” the looming US assessment of Hong Kong’s autonomous status.

The latter will now come after this Friday’s National People’s Congress (NPC) in Beijing, which is expected to announce several key policy decisions with market impact. One will be if there is a GDP growth target for 2020 or not, and if so how high; another will be how to achieve it, with the same fiscal vs. monetary vs. outright monetization debates reportedly taking place in Beijing as in the West, and as debt soars regardless – the IIF now sees China’s total debt-to-GDP ratio at 314% and rising rapidly; a third may be China’s international stance, and whether to continue to with its “Wolf Warrior” diplomatic stance. Recall all these decisions will be taken as the BIS show that CNY only accounts for 4.3% of international currency transactions, up from 4.0% in 2016, vs. 88% for USD, which is also on the other side of 95% of CNY transactions. Indeed, the BIS conclude the Chinese currency has made “marginal progress” in its internationalisation in the past three years. That backdrop does not sit so well with either major monetization of debt or global feather-ruffling.

Can one say the same for the UK and GBP? PM Johnson, taking brickbats at home on several fronts, has said that the virus is going to linger in Britain, which does not suggest a return to full normality. Johnson also apparently refuses to embrace austerity, which is sensible,…but then places the responsibility on the BOE – who are already monetizing a small portion of the new UK debt, pretending that QE is not more of less the same thing in real terms, and are now openly talking about negative rates ahead. All that is happening as the UK and the EU are walking in opposite directions over a new trading relationship, with a non-negligible likelihood that Hard WTO Brexit will follow at the end of the year. Put that kind of major monetization and global feather-ruffling together and we have Cable at 1.2099 when we started at 1.32, so down 8.7%.

So this remains the trend we expect to see: more monetary easing; more fiscal easing; more de facto monetization behind acronym fig-leaves – or maybe without; and hence more downwards pressure on FX and upwards pressure on USD. Oh, and lots more geopolitical rumbling both as cause and effect. Look to Japan and see why.

It is now officially in recession, with GDP in Q1 sinking -3.4% annualised vs. -7.3% in Q4, and the outlook for Q2 is even uglier. The government is talking about a 20% of GDP fiscal stimulus package – and we have both BOJ JGB (and ETF) guzzling and yield curve control. Yet JPY is up 1.5% YTD vs. USD. This is due to the risk-off Yen function; and that is because it runs current-account surpluses.

Apart from the US, who can run a massive current-account deficit and still MMT away happily because of the global need for USD, it’s that magical current-account surplus that will dictate if a country can sustainably use MMT to prop up its post-Covid economy without markets then pricing for a Weimar or Zimbabwe endgame. BUT NOT EVERYONE CAN DO SO AS A SURPLUS IN ONE LOCATION IS A DEFICIT SOMEWHERE ELSE (and the US can’t and won’t be that for everyone. Certainly not for China.) That means more supply-chains shifting, and from a far broader interpretation of ‘national security’ than just who and can’t make masks.

It’s about who can and can’t make money.

via ZeroHedge News https://ift.tt/2WIbZqo Tyler Durden

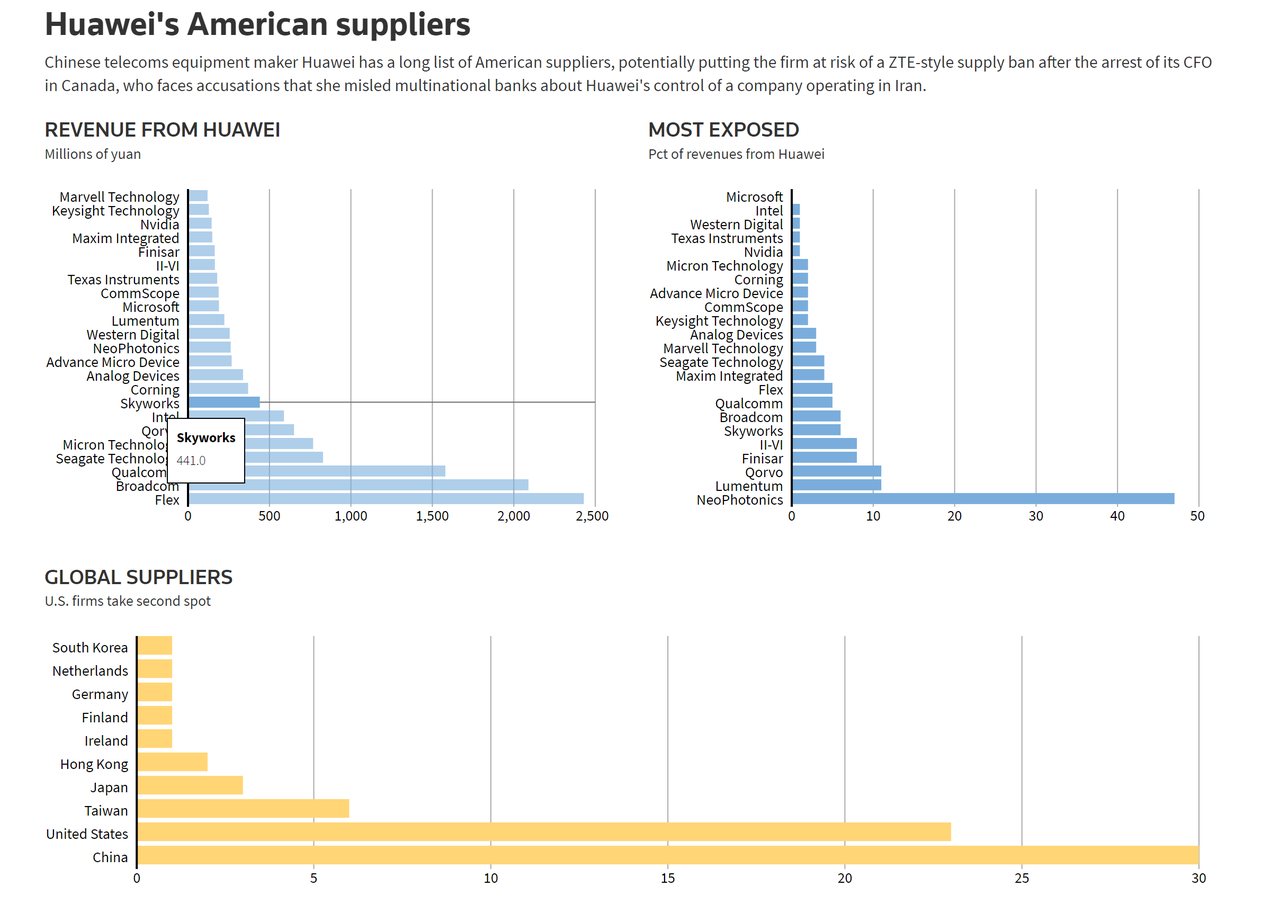

World’s Largest Contract Chipmaker Halts Deliveries To Huawei As New US Sanctions Bite Tyler Durden

Mon, 05/18/2020 – 09:25

The Commerce Department’s decision to tighten restrictions on Huawei announced a few days ago are already throwing a wrench in Huawei’s supply chain, a sign that the US is no longer playing around, and is going all-in on bringing the Chinese telecom giant with strong links to the PLA to its knees.

As we reported on Friday, the Trump Administration reportedly blocked a shipment of American-made semiconductors that was headed to Huawei, eliciting a flurry of retaliatory threats, as Beijing via the mainland press promised to target Boeing, Apple and Qualcomm. Despite the seeming escalation in the US trade and tech wars with China, White House economic advisor Kevin Hassett told CNBC Monday morning that the ‘Phase 1’ trade deal appears to still be intact.

Despite years of aggressive intellectual technology theft coordinated by the Chinese government, Huawei remains surprisingly dependent on products and technology produced by American companies.

When the Commerce Department added Huawei to the national “entities list” – effectively a “blacklist” requiring US companies to seek permission from Commerce to do business with Huawei – it essentially caveated the decision to hell, leaving in loopholes that allowed large American chip companies to continue shipping to Huawei (which, in addition to its telecoms infrastructure business, is also the second-largest maker of smartphone handsets)

However, the latest restrictions unveiled by the Commerce Department late last week and over the weekend will “narrowly and strategically” target a loophole that allows US companies to produce chips overseas with American technology to get around the restrictions. This will no longer be allowed, as even foreign companies that depend on US products will be forced to comply. In response, other global chipmakers are refusing to ship certain products to Huawei. This group includes the world’s biggest contract chipmaker, Taiwan Semiconductor Manufacturing Co, a

According to Nikkei Asian Review reported published Monday morning, TSMC has halted new orders from Huawei in response to tighter US export controls. Prior to the new declaration, some companies evaded existing US sanctions by producing semiconductor chips overseas, using American technology, then selling them directly to Huawei.

From here on out, any company that continues this practice risks being sanctioned by the Treasury Department, sanctions that could restrict their access to the dollar-based financial system, or even ban them entirely, leaving them in the same predicament faced by Iranian companies.

“TSMC has stopped taking new orders from Huawei after the new rule change was announced to fully comply with the latest export control regulation,” a person familiar with the situation said. “But those already in production and those orders which TSMC took before the new ban are not impacted and could continue to proceed if those chips could be shipped before mid-September.”

[…]

“It’s a difficult decision for TSMC as Huawei is the company’s No. 2 customer, but the chipmaker has to follow the U.S. rules,” another person familiar with the matter said.

The Chinese 5G pioneer relies on TSMC for chips that power its smartphones, and TSMC has long been viewed as a “lifeline” for Huawei in the face of US sanctions.

Huawei, the world’s biggest telecom equipment maker and second biggest smartphone maker, relies heavily on TSMC to manufacture its advanced chip designs – including all of the mobile processors used in Huawei’s flagship smartphones. The Taiwanese company, which also produces artificial intelligence processors and networking chips for Huawei, has been viewed as a vital lifeline for the Chinese company in its efforts to resist U.S. pressure since Washington placed it on a trade blacklist last May.

This relationship with Huawei, however, has put the Taiwanese company in the crossfire of Washington-Beijing tensions.

The tighter U.S. controls were announced the

However, TSMC shares tumbled during Asian trade on Monday as investors fretted about how these sanctions would impact the relationship between TSMC and its second-biggest customer (after Apple).

One trade lawyer who spoke to Nikkei explained that virtually every contract chip maker outside the US will need to apply for a license from the US to ship to Huawei, unless they meet certain criteria showing American-made components in a given product fall below a given threshold.

Harry Clark, a Washington-based trade law expert and managing director of U.S. law firm Orrick, said that chip contract manufacturers outside the U.S. will have to apply for license for any shipments that do not meet the above criteria. Violating such laws, he added, could leave a company “exposed to substantial penalties” imposed by the regulators.

Huawei has of course been preparing for another crackdown since the trade war between the world’s two largest economies started, and those preparations were stepped up after the US government targeted Huawei and its fellow Chinese telecoms giant ZTE.

Huawei has been preparing for such a move by the U.S. since the end of last year, including stockpiling more than a year’s worth of networking equipment-related chips, especially for its crucial telecom equipment and carrier business, sources told Nikkei Asian Review.

The company has also explored a wide range of other options, including asking European chipmaker STMicroelectronics, a longtime supplier, to co-design chips, Nikkei reported earlier. However, those efforts may not immediately solve all of its vital chip supply issues, which are critical for Huawei to continue rolling out world-class technologies, analysts said.

China’s Department of Commerce on Sunday said it “strongly objects to the new export controls and warned such restrictions would pose a huge threat to the global supply chain. If Washington doesn’t reverse the action, Beijing warned it would face retaliation.

One analyst at Jeffries Equity Research wrote that if the US is successful, the pressure could help “quash China’s 5G ambitions” – the White House’s ultimate goal – though that would come with its own set of repercussions…

“The proposed legislation likely aims to stop Huawei’s tech progress and quash China’s 5G ambitions,” Jefferies Equity Research analysts said in a research note. “We expect China to retaliate if this materializes. The risk of a ‘super’ cold war is mounting.”

…including mounting risk of a “super cold war” as the two economies continue with a decoupling that has been rapidly accelerated by the coronavirus.

via ZeroHedge News https://ift.tt/3bFbgdR Tyler Durden

Is it possible the Fed over-reacted to a natural disaster?

There are two different types of “recessionary” events that occur throughout history. The first is a “business cycle” recession, which happens with some regularity as excesses build up in the economy. These cycles generally take 12-18 months to complete as those excesses are reversed.

Then there are “event-driven” recessions that can occur from “natural disasters.” These are generally much shorter in duration and can be sector specific. One such event was the Japanese earthquake/tsunami in 2011, which led to a temporary manufacturing recession.

Understanding the type of recessionary cycle you are fighting is essential in ensuring the Government applies the correct monetary and fiscal response. As with any illness, the application of the wrong medication can lead to unintended consequences.

There are growing expectations of the COVID-19 economic shutdown, and the subsequent recessionary backlash will be very short-lived. The assumption is that if the economy reopens, the activity will resume, and the economy will quickly regain its footing.

If such an outcome is indeed the case, has the Fed applied the wrong “medication” to cure the economic patient?

“Over the last month, the Federal Reserve, and the Government, have unleashed a torrent of liquidity into the U.S. markets to offset a credit crisis of historic proportions. A list of programs already implemented has already surpassed all programs during the ‘Financial Crisis.’”

03/12 – Federal Reserve supplies $1.5 trillion in liquidity.

03/13 – President Trump pledges to reprieve student loan interest payments

03/13 – President Trump declares a “National Emergency” freeing up $50 billion in funds.

03/15 – Federal Reserve cuts rates to zero and launches $700 billion in “Q.E.”

03/17 – Fed launches the Primary Dealer Credit Facility to buy corporate bonds.

03/18 – Fed creates the Money Market Mutual Fund Liquidity Facility

03/18 – President Trump signs “coronavirus” relief plan to expand paid leave ($100 billion)

03/20 – President Trump invokes the Defense Production Act.

03/23 – Fed pledges “Unlimited QE” of Treasury, Mortgage, and Corporate Bonds.

03/23 – Fed launches two Corporate Credit Facilities:

A Primary Market Facility(Issuance of new 4-year bonds for businesses.)

A Secondary Market Facility(Purchase of corporate bonds and corporate bond ETFs)

03/23 – Fed starts the Term Asset-Backed Security Loan Facility(Small Business Loans)

04/09 – Fed begins several new programs:

The Paycheck Protection Program Loan Facility(Purchase of $350 billion in SBA Loans)

A Main Street Business Lending Program($600 billion in additional Small Business Loans)

The Municipal Liquidity Facility(Purchase of $500 billion in Municipal Bonds.)

Expands funding for PMCCF, SMCCF and TALF up to $850 billion.

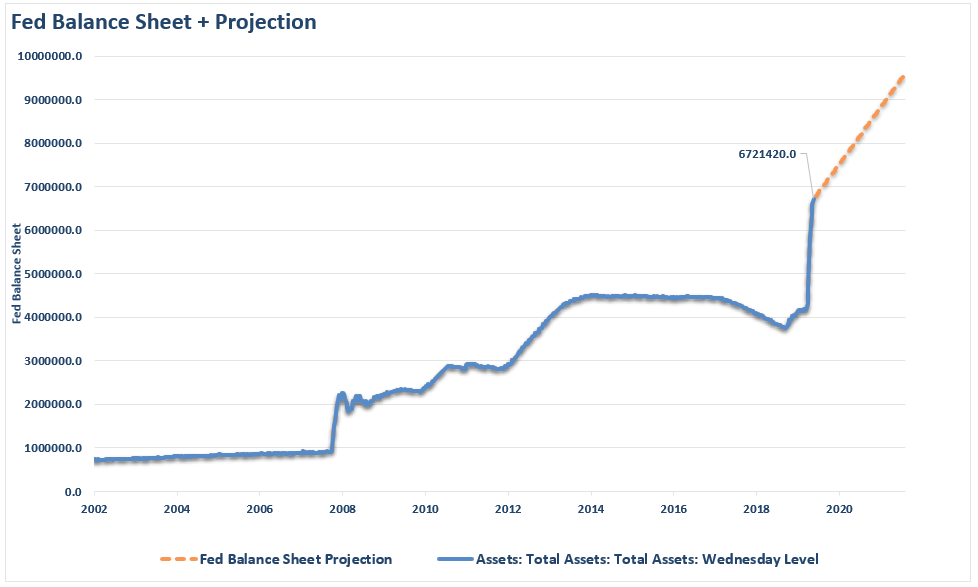

Racking Up The Debt

Here is the Fed’s balance sheet through this past Wednesday (estimated at time of writing)

As investor Paul Tudor Jones stated:

“Investors can take heart that we’ve counteracted this existential shock with the greatest fiscal, monetary bazooka. It’s not even a bazooka. It’s more like a nuclear bomb.”

Was It Too Much?

Jones’s comment was correct. However, was applying a “nuclear bomb” of monetary policy the proper response to a virus? Such is the question for consideration.

Historically, the world has been through several viruses, world wars, financial panics, major natural disasters, inflationary spikes, terrorist events, corporate defaults, attacks, and more. In every case, the economy, markets, and population survived and eventually flourished.

Was COVID-19 going to change history? I doubt it.

In hindsight, it is becoming easier to comprehend that shutting down the entire economy was probably not the right choice. Infection rates and death tolls are far lower than initially estimated, and the economic fallout was a steep price to pay. However, going in to the crisis such a modest outcome was not known and politicians had touch decisions to make.

The magnitude of the Fed’s response was also a function of “panic” based more on “recency bias” than facts. The Fed quickly returned to the “Financial Crisis” playbook to anticipate events that may occur in the credit markets rather than responding to outcomes.

There is a difference.

The Financial Crisis was a problem with the banking system. The COVID-19 pandemic is a health crisis.

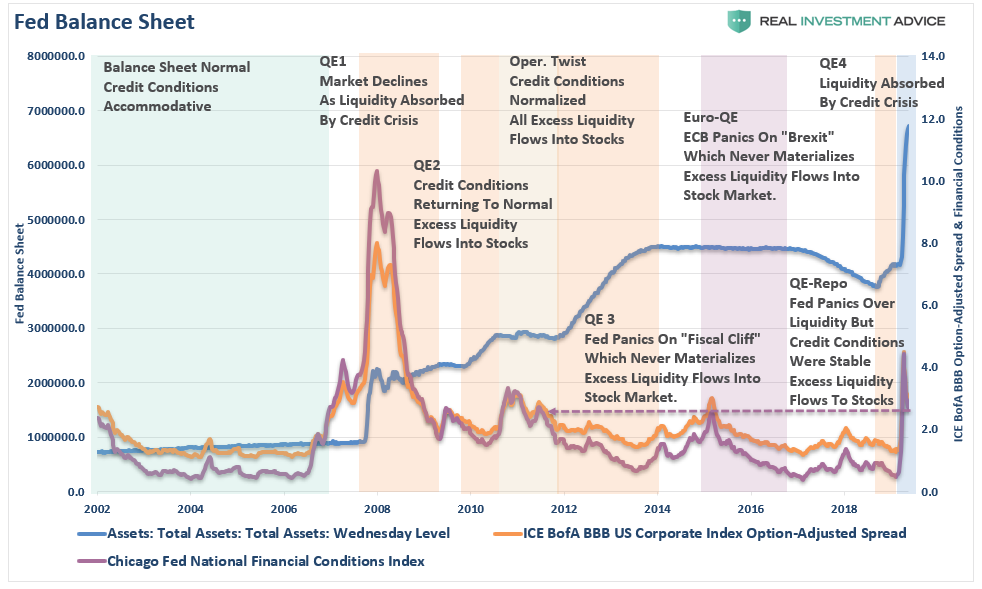

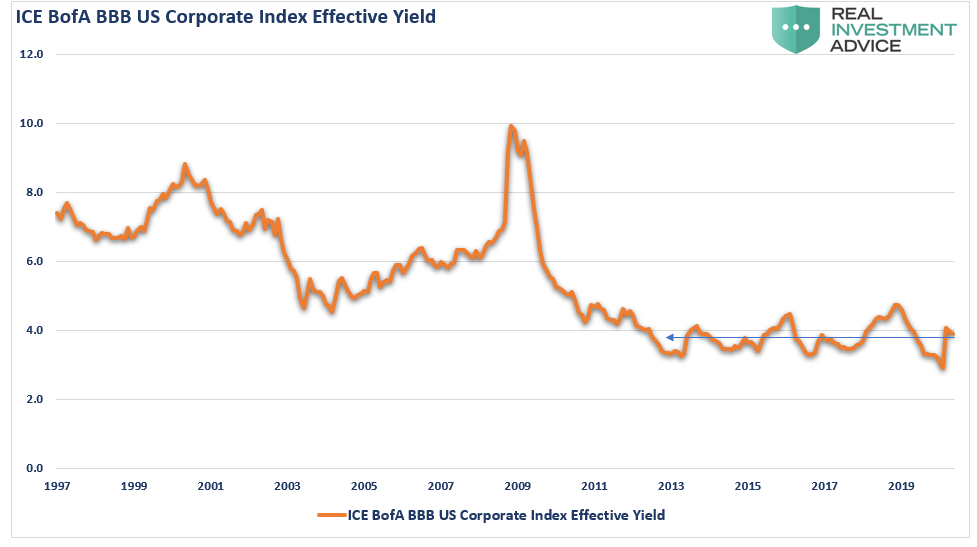

Notice the difference between the 2008 crisis and today concerning yield spreads, financial conditions, and the Fed’s balance sheet.

The Yield Tale

The singular purpose of the Fed’s actions was to ensure the proper functioning of the credit markets. While yields did initially spike, that ignition was quickly quenched by the “fire hose” of liquidity from the Fed.

However, the Fed has not ceased their actions. Last week, the Fed began its process of buying corporate and high-yield bond ETF’s. These purchases are being done under the SMCCF program (Secondary Market Corporate Credit Facility) with the sole purpose of ensuring corporate credit markets function smoothly.

“Purchases are focused on reducing the broad-based deterioration of liquidity seen in March 2020 to levels that correspond more closely to prevailing economic conditions,” the document said. It listed an array of metrics that would guide investments, including transaction costs, bid-ask spreads, credit spreads, volatility, and “qualitative market color.”

“Once market functioning measures return to levels that are more closely, but not fully, aligned with levels that correspond to prevailing economic conditions, broad-based purchases will continue at a reduced, steady pace to maintain these conditions.”

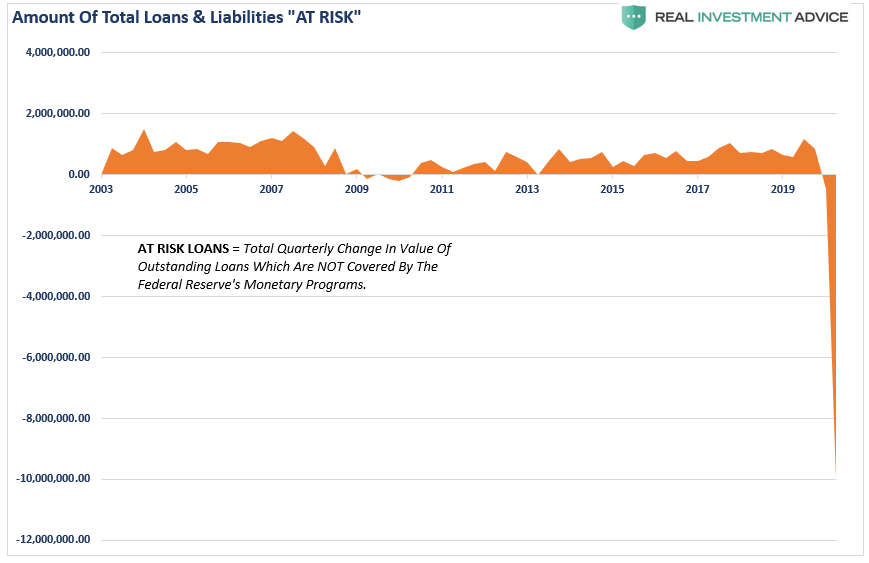

Such is interesting as credit condition never blew out and have already returned to levels more closely aligned with previous economic conditions. In fact, in the one area where there is the densest concentration of bonds “at risk,” effective yields haven’t risen much at all.

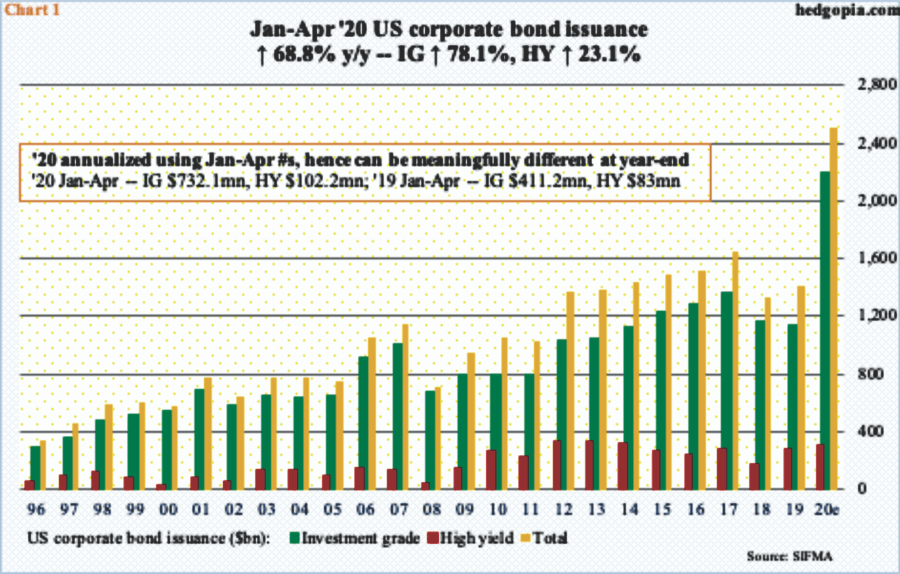

More Debt

Corporate issuers also have had NO trouble issuing debt as of late. In fact, over the past couple of months, there has been a record amount of debt issuance in investment-grade bonds, with high yield issuance close to previous levels.

If yields are within more normal ranges, and bond issuance isn’t a problem, then why is the Federal Reserve continuing to act as if a credit crisis is in process?

Do they see issues in the credit markets the data doesn’t show? Or, are they trying to “front-run” any potential credit disruptions which may occur as the economy reopens?

There Will Be Consequences

If the Fed is correct, and a credit crisis is in process, then the current levels of stimulus may fall short. As noted on April 10th:

“We are now looking at a potential decline of 20% in GDP, which will equate to roughly a $10 Trillion reduction in debt as defaults, bankruptcies, and restructurings rise.

There is a real possibility the Fed is ‘filling in a hole’ that is growing faster than they can fill it. (The Fed is injecting $6 Trillion via the balance sheet expansion versus a potential $10 Trillion shortfall.)”

Unfortunately, that estimate of the decline in GDP was a bit optimistic. Last week, the Atlanta Fed’s real-time economic indicator was predicting a -42.8% decline, or nearly twice the current levels of most estimates.

However, if this turns out to be a short-lived crisis and economic activity comes surging back, then the Fed’s stimulus may be too much, leading to a surge in inflation and downward pressure on the middle class.

Regardless of the eventual outcome, there is one consequence of massive debt and deficit expansions that will not change – slower economic growth.

No Other Choice

With the economy facing an “economic depression,” and in the middle of an election year, the Federal Reserve had a choice to make.

Allow capitalism to take root by allowing corporations to fail and restructure after spending a decade leveraging themselves to the hilt, buying back shares, and massively increasing their executives’ wealth while compressing the wages of workers. Or,

Bailout the “bad actors” once again to forestall the “clearing process” that would rebalance the economy, and allow for higher levels of future organic economic growth.

As the Fed’s balance sheet heads toward $10 Trillion, the Fed opted to impede the “clearing process.”By not allowing for debt to fail, corporations to be restructured, and “socializing the losses.” They have removed the risk of speculative practices and ensured a continuation of “bad behaviors.”

Unfortunately, given we now have a decade of experience of watching the “wealth gap” grow under the Federal Reserve’s policies, the next decade will only see the “gap” worsen.

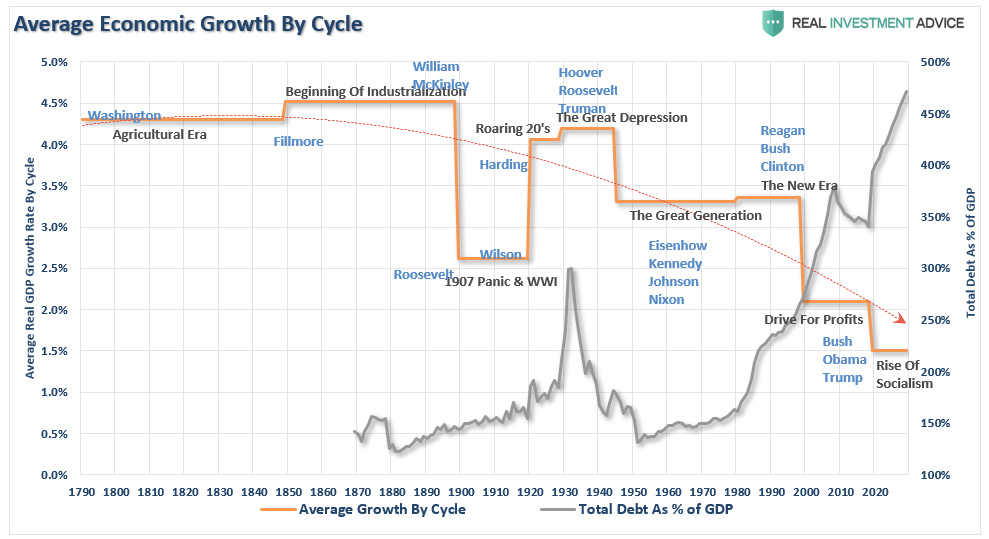

Furthermore, given that we now know surging debt and deficits inhibit organic growth, the massive debt levels added to the backs of taxpayers will only ensure lower long-term rates of economic growth. The chart below shows the 10-year annualized run rates of economic growth throughout history with projected debt and growth levels over the next decade.

The End Game

History is pretty clear about future outcomes from the Fed’s current actions. More importantly, these actions are coming at a time where there were already tremendous headwinds plaguing future economic growth.

A decline in savings rates

An aging demographic

A heavily indebted economy

A decline in exports

Slowing domestic economic growth rates.

An underemployed younger demographic.

An inelastic supply-demand curve

Weak industrial production

Dependence on productivity increases

Yes, another $4-6 Trillion in QE will likely be successful in inflating a third “bubble” to counteract the last deflation.

The problem is that after a decade of pulling forward future consumption to stimulate economic activity, a further expansion of the wealth gap, increased indebtedness; low rates of economic growth will weigh on future economic opportunity for the masses.

Supporting economic growth through increasing levels of debt only makes sense if “growth at all cost” uniformly benefits all citizens. Unfortunately, we are finding out there is a big difference between growth and prosperity.

The United States is not immune to social disruptions. The source of these problems is compounding due to the public’s failure to appreciate it. Until the Fed’s policies are discussed publicly and reconsidered, the policies will remain, and the problems will grow.

Was the “medicine” applied by the Fed to counteract a “virus” the correct prescription? If the patient ultimately dies, we will have our answer.

via ZeroHedge News https://ift.tt/2LFnSY8 Tyler Durden

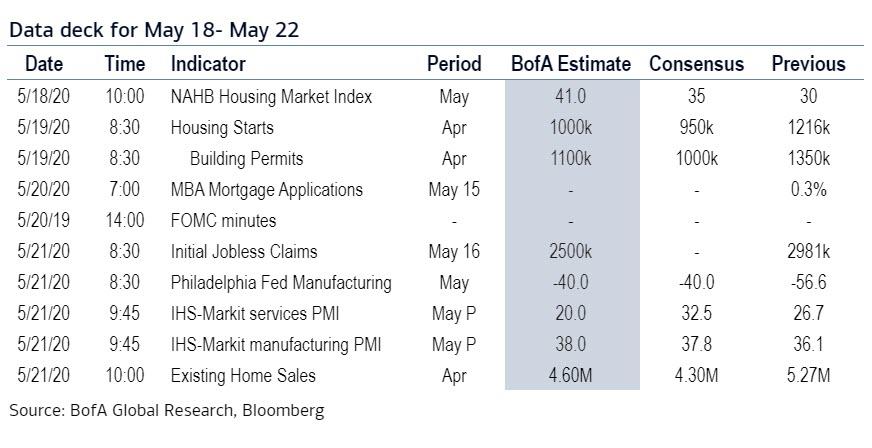

Key Events This Week: Things Quiet Down Tyler Durden

Mon, 05/18/2020 – 09:10

After several weeks of economic, political and corporate earnings, things finally quiet down this week as Q1 earnings season comes to an end with a handful of retailers (at least the ones that aren’t bankrupt yet) set to report. The main data release this week will be the flash PMIs for May from around the world on Thursday and Friday, according to DB’s Jim Reid. The consensus is expecting services in Europe to bounce from low teens to the mid-twenties area and manufacturing to go up a few points in the thirties. The PMIs are diffusion indices, with respondents simply saying whether things are better or worse than the previous month so they are a little difficult to calibrate to growth at such extreme levels of activity but they will be a big curiosity nonetheless.

There’s a raft of central bank events this week, including a number from the Fed. The highlights are likely to be the two sets of remarks from Fed Chair Powell that we mentioned above. Aside from that, there’ll also be remarks to digest from Vice Chair Clarida and New York Fed President Williams on Thursday, as well as other regional Fed Presidents throughout the week. Finally on the Fed, it’ll be worth keeping an eye out for the release of the minutes from April’s meeting on Wednesday. On Friday, the ECB will also be publishing their account of the most recent monetary policy meeting.

Earnings season continues to wind down over the week ahead, with over 90% of the S&P 500 companies having now reported. This week will only see a further 22 companies from the S&P 500 and 30 from the STOXX 600 announce earnings. In terms of the highlights, today we’ll hear from Ryanair, Lufthansa and Panasonic. Then tomorrow we have Walmart and Home Depot, before Wednesday sees Lowe’s, Target and Experian report. On Thursday, there’s Nvidia, Medtronic, Intuit, TJX and Hewlett Packard Enterprise, and finally on Friday there’s Deere & Company and Alibaba.

Finally on Friday, the National People’s Congress will open in China. The central government is expected to unveil more fiscal measures, aimed at supporting households and encouraging consumption. Another thing that will be interesting to see is whether a numerical GDP target for this year is made, since Bloomberg reported previously that one option that could be done instead is to have a description of the GDP goal.

Below, courtesy of Deutsche Bank, is a day-by-day calendar of events:

Monday

Data: Japan preliminary Q1 GDP, March tertiary industry index, China April new home prices, US May NAHB housing market index

Central Banks: Remarks from the Fed’s Bostic, ECB’s Hernandez de Cos and the BoE’s Tenreyro

Earnings: SoftBank, Ryanair, Lufthansa, Panasonic

Tuesday

Data: Japan March capacity utilisation, final March industrial production, UK March unemployment, employment, average weekly earnings, EU27 April new car registrations, Germany May ZEW survey, US April housing starts, building permits

Central Banks: Remarks from Fed Chair Powell, the Fed’s Rosengren, Kashkari and the ECB’s Lane, Bank Indonesia monetary policy decision, Reserve Bank of Australia release minutes from May policy meeting

Earnings: Walmart, Home Depot

Wednesday

Data: Japan March core machine orders, UK April CPI, Euro Area March current account balance, Euro Area final April CPI, US weekly MBA mortgage applications, Canada April CPI, Euro Area advance May consumer confidence

Central Banks: FOMC release meeting minutes, remarks from BoE’s Bailey, Broadbent, Cunliffe and Haskel, Fed’s Bullard and Bank of Canada’s Lane

Earnings: Lowe’s, Target, Experian

Thursday

Data: Manufacturing, services and composite PMIs from Australia, Japan, UK and US, Japan April trade balance, US May Philadelphia Fed business outlook survey, weekly initial jobless claims, April leading index, existing home sales

Central Banks: Remarks from Fed Chair Powell, Vice Chair Clarida and New York Fed President Williams, monetary policy decisions from the Central Bank of Turkey and South African Reserve Bank

Data: Manufacturing, services and composite PMIs from France, Germany and the Euro Area, Japan April nationwide CPI, nationwide department store sales, UK April retail sales, public sector net borrowing, Canada March retail sales

Central Banks: ECB releases account of monetary policy meeting

Earnings: Deere & Company, Alibaba

Politics: China’s National People’s Congress begins

Key highlights via BofA:

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the Philly Fed manufacturing index and the jobless claims report on Thursday. In addition, minutes from the April FOMC meeting will be released on Wednesday. There are several scheduled speaking engagements from Fed officials this week, including Chair Powell on Tuesday and Thursday, and New York Fed President Williams and Vice Chair Clarida on Thursday.

Monday, May 18

10:00 AM NAHB housing market index, May (consensus 34, last 30)

02:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will take part in a virtual discussion about the economy and the coronavirus hosted by the Nashville Chamber of Commerce. Audience Q&A is expected.

Tuesday, May 19

08:30 AM Housing starts, April (GS -26.0%, consensus -24.1%, last -22.3%); Building permits, April (consensus -25.9%, last -6.8%); We estimate housing starts declined by 26.0% in April due to coronavirus-related declines in construction activity.

10:00 AM Fed Chair Powell appears before the Senate Banking Committee: Fed Chair Jerome Powell will testify alongside Treasury Secretary Steven Mnuchin on the Quarterly CARES Act report to Congress before the Senate Banking Committee. Prepared text is expected.

10:00 AM Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will discuss the economy in a virtual town hall hosted by General Mills.

02:00 PM Boston Fed President Eric Rosengren (FOMC non-voter) speaks: Boston Fed President Eric Rosengren will discuss the impact of the coronavirus on the New England economy and the actions taken by the Fed in response in a virtual talk hosted by the New England Council.

Wednesday, May 20

10:00 AM Atlanta Fed President Raphael Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will speak on the Fed’s response to the coronavirus in a webinar with the JAXUSA Partnership.

12:00 PM St. Louis Fed President James Bullard (FOMC non-voter) speaks: St. Louis Fed President James Bullard will take part in a virtual discussion on the coronavirus and the economy hosted by the Missouri Growth Association.

02:00 PM Minutes from the April 28-29 FOMC meeting: At its March meeting, the FOMC left the target range for the policy rate unchanged at 0-0.25%, as widely expected. The FOMC did not make changes to IOER, the forward guidance, the asset purchase plan, or the credit facilities. In the minutes, we will look for further discussion of the economic outlook and the Fed’s toolkit.

Thursday, May 21

08:30 AM Philadelphia Fed manufacturing index, May (GS -35.0, consensus -40.0, last -56.6): We estimate that the Philadelphia Fed manufacturing index increased by 21.1pt to -35.0 in May.

08:30 AM Initial jobless claims, week ended May 16 (GS 2,500k, consensus 2,425k, last 2,981k): Continuing jobless claims, week ended May 9 (consensus 23,500k, last 22,833k); We estimate initial jobless claims declined but remain elevated at 2,500k in the week ended May 16

09:45 AM Markit Flash US manufacturing PMI, May preliminary (consensus 38.0, last 36.1): Markit Flash US services PMI, May preliminary (consensus 32.3, last 26.7)

10:00 AM Existing home sales, April (GS -21.0%, consensus -18.4%, last -8.5%): After falling by 8.5% in March, we estimate that existing home sales fell another 21.0% in April. Existing home sales are an input into the brokers’ commissions component of residential investment in the GDP report.

10:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will take part in a webinar video conference hosted by the Buffalo Niagara Partnership, CenterState CEO, and the Greater Rochester Chamber of Commerce. Prepared text and audience Q&A are expected.

01:00 PM Fed Vice Chair Clarida (FOMC voter) speaks: Fed Vice Chair Richard Clarida will take part in an online discussion on the US economy and monetary policy hosted by the New York Association for Business Economics. Prepared text and a moderated Q&A are expected.

02:30 PM Fed Chair Powell (FOMC voter) speaks: Fed Chair Jerome Powell will make opening remarks at a virtual Fed Listens event on how the coronavirus is affecting US communities. Fed Governor Lael Brainard will moderate the discussion.

Friday, May 22

There are no major economic data releases scheduled today.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News https://ift.tt/36bZwOQ Tyler Durden

Oil Soars, Prompt WTI Contango Disappears As Chinese Oil Demand “Almost Back To Pre-Crisis Levels” Tyler Durden

Mon, 05/18/2020 – 08:53

After plunging more than 20% in Q1 due to the economic shutdown from the coronavirus pandemic, Chinese oil demand is now “all but back to levels last seen before Beijing imposed a national lockdown to fight the coronavirus outbreak” Bloomberg reported citing people with inside knowledge of the country’s energy industry, who may or may not be long oil futures.

Gasoline and diesel are leading the recovery in China as commuters prefer the safety of their own cars, rather than using public transport, while jet-fuel demand has remained subdued.

The quick turnaround in China, the world’s second largest oil consumer behind only the U.S., has helped tighten the petroleum market sooner-than-expected, and the result is a sharp rally in West Texas Intermediate crude, which a month ago plunged into negative prices and last traded above $32 a barrel.

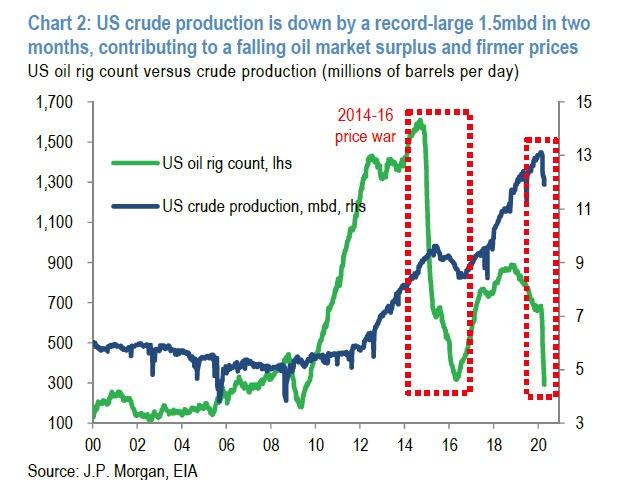

Helping the impressive rebound in oil is the accelerating shutdown in US crude production, which as shown below is down by a record 1.5mmb/d in the past two months, helping reduce supply and firm prices.

According to Bloomberg sources, Chinese consumption of gasoline and diesel has fully recovered as factories reopen and commuters drive rather than use public transport, according to the people, who are long crude asked not to be named because they aren’t authorized to discuss the matter publicly.

The same “people” adds that while pinpointing the exact level of Chinese oil demand in real time is a difficult exercise, executives and traders who monitor the country’s consumption said it was at about 13 million barrels a day, just shy of the 13.4 million barrels a day of May 2019 and 13.7 million barrels a day of December 2019. The overall number would be higher were it not for jet-fuel demand, which is still running well below a year’s ago level, as a result of a continued slump in both domestic and international air travel.

Unlike the “unnamed people” who may or may not be long oil on Monday (before they dump it and change their mind), the International Energy Agency is far more pessimist about Chinese consumption. In a report last week, it predicted that the Asian giant will consume less oil every month for the rest of the year than it did during the same period of 2019.

To reach their optimistic conclusion, the “people” are likely looking at rush hour traffic data (provided publically by TomTom International) in multiple Chinese cities , which has surged in the last couple of weeks, in many cases running either at or even above year-ago levels, according to data from navigation company TomTom International BV. The traffic has particularly intensified in cities other than Beijing and Shanghai, which typically have more space for the drivers that are now using their cars to commute into work.

At the same time, diesel demand is also recovering strongly as Beijing encourages farmers to plant more to guarantee the country’s food security and industrial consumption recovers. The uptick in China’s gasoline and diesel consumption has prompted state and independently-owned refiners to crank up run rates to convert more crude oil into fuel. That means Chinese crude stockpiles are actually being drawn down.

As Bloomberg also notes, Chinese oil refiners had in recent days embarked on a buying spree, snapping up barrels in the physical market, prompting prices to recover. “The Chinese are buying everything in sight,” said a senior executive at a major trading house.

The price of crude that’s popular with Chinese refiners, including Lula from Brazil, Djeno from the Republic of Congo, and Oman has rallied so far this month. A month ago, Lula changed hands at a discount of about $6 a barrel under the benchmark Brent. On Monday, one Chinese company bought a cargo at around $1-$1.50 a barrel premium to Brent, traders said.

“China’s oil demand is starting to show optimistic signs of full recovery, led by diesel,” said Liu Yuntao, a London-based analyst with consultant Energy Aspects.

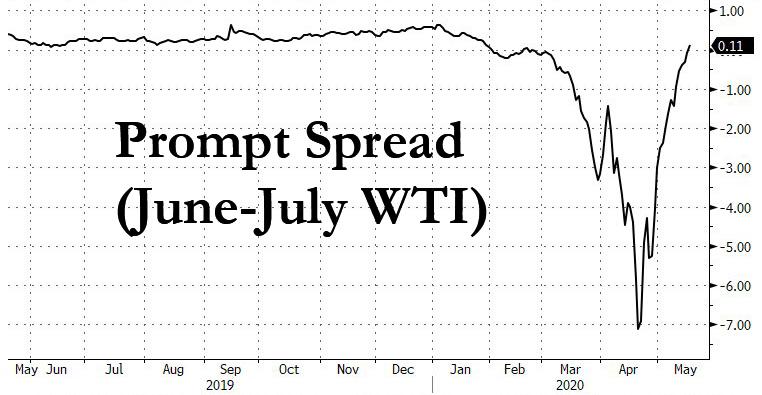

And as optimism returns to the oil market, and as prices soar, what was until a few weeks ago a super contango in the prompt Jun-July spread is now back to backwardation, which is making the storage of oil on tankers increasingly unprofitable.

via ZeroHedge News https://ift.tt/3cL2ufK Tyler Durden

‘Tidal Wave’ Of Delinquent Mortgages Set To Surpass Great Recession Tyler Durden

Mon, 05/18/2020 – 08:35

With nearly 4 million homeowners in some type of mortgage forbearance plan – representing 7.54% of all mortgages, delinquencies are set to eclipse the great recession which peaked at 10%.

According to a new report from UK-based forecasting firm Oxford Economics, 15% of homeowners will fall behind on their monthly mortgage payments in a ‘tidal wave’ of delinquencies.

Stimulus legislation signed by President Donald Trump allows any borrower with a federally-backed mortgage to request forbearance for up to 12 months, meaning the homeowner can skip or make reduced payments during that time.

Given the risk mortgage companies are facing right now, many lenders have imposed more stringent requirements for loan applicants. “The uncertainty in the mortgage market has contributed to a significant tightening of lending standards that may persist even once a recovery is underway,” Oxford Economics wrote. –MarketWatch

An while the pace of requests for forbearance has slowed in recent weeks – however that could change. “Although the pace of forbearance requests slowed this week, call volume picked up — which could be a sign that more borrowers are calling in to check their options now that May due dates have arrived,” said Mortgage Bankers Association chief economist, Mike Fratantoni.

Keep in mind that Oxford Economics’ forecast is half of the potential mortgage bloodbath predicted by Moody’schief economics, Mark Zandi, who said that as many as 30% of Americans with home loans – or around 15 million households, may stop paying if the US economy remains closed through the summer or beyond.

We assume that a large percentage of Americans refusing to return to pre-pandemic consumption habits would have similar effects.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania in comments last month. She also points out another way the current crisis is different from the 2008 GFC: “The great financial crisis happened over a number of years. This is happening in a matter of months – a matter of weeks.”

via ZeroHedge News https://ift.tt/3cIEmKW Tyler Durden

Business and markets are arbitraging government support packages and central bank QE Infinity to stay “insanely high” despite the massive economic hit of the virus. If the proverbial Martian visited the stock market today, he’d struggle to understand just why markets are so high when prospects look so low.

At which point we come back to earth with a bump. The papers this morning are full of doom and gloom – particularly re the UK. My email is full of analyst gibberish about why I should be buying Bitcoin, Tesla and other crap. I shall ignore them all, and focus on the real picture

Even if the global economy was to magically reopen tomorrow, we’d still see earnings for 2020 massively impacted, reduced credit worthiness as companies leveraged themselves with more debt to see them through the crisis, and an increasingly protectionist trade uncurrent.

That’s not a favourable market for anyone. And we all get it – the world has changed.

Understanding the nuances of this new markets is going to be critical.

It’s not just about listening to what Fed Head Jay Powell was saying when he warned about how assets prices could be impacted by the pandemic, and how it might take 18 months for the US economy to recover. It’s not just understanding the consequences of how UK long-term unemployment might rise to 9%. It’s not even all about the 11.2% decline in US industrial production through April, or the 70% crash in car production – and the knock on effects these have across the economy.

It’s also about understanding behavioural economics – how will people and politicians (note the distinction) respond in this changed environment. What impacts will politically driven decisions and consequences have on markets going forward.

Much has been said about the welfare and mental health crisis the virus lockdown has unleashed. Anxiety and fears for the future are impacting just about everyone – which I why I recommend sailing to everyone. Getting back on the water this weekend has given my feel-good an enormous boost. People are going to cut spending plans if they fear their jobs and livelihoods are under threat because of the virus and the virus recession.

How much damage can Coronaphobics and Coronanazis do to recovery? In the first bracket are the genuinely scared – frightened by the excitable news flow, and what the virus will do to them and their families. How to reassure them?

The CoronaNazi camp is more dangerous.

There seem to be an increasing number of players willing to play politics to delay reopening to prize concessions and control. Corbynistas (yes, there is still a nest of them at the extreme end of the UK political spectrum) are demanding the unions are given control of workplaces to ensure worker safety is a complete red herring – but try to criticise it, and you will be trolled! (Some of the tweets are hilarious.) All political actions have consequences – and when the government has to play to the fears of Corona-phonics and respond to the Virus-Nazis, we are going to get sub optimal outcomes.

Much of the growing China vs US trade war rhetoric is politically inspired. You can’t threaten trade sanctions again a microscopic bug, but you win voters by blaming Beijing!

It’s clear much of government response has been about anticipating the coming blame-game. Just how did the staggeringly well-paid public health managers across the UK so conclusively fail the logistics and preparation tests for the virus? Because the buck doesn’t stop with them – it will be the health minister that takes the can. Bureaucracies have a tendency to become even more entrenched during times of crisis. Although the NHS desperately needs root and branch fundamental reform, and being dragged into the modern age though AI and apps, its unlikely to happen any time soon… Cost constraints etc will ensure the bureaucracy will probably grow.

What businesses and sectors stand to win or lose short, medium and long-term? Clearly some stocks are going to do very well – companies that crack the vaccine and new treatments. But just how secure is the rest of the health sector? We’re hearing talk of being prepared for a second wave of the virus in the autumn/winter, but are governments going to keep the spending spigots open? Or do they start slash and burn cuts on health care to pay the costs of the virus? How vulnerable are any sectors that rely on government spending? Defence? Policing? Health? Education?

There is a well-circulated post doing the internet rounds how the UK’s furlough scheme is costing over £14 bln a month – £168 bln over a year. Put that in context of replacing our nuclear Trident deterrent at £205 bln, the money already spent on the HS2 railway to no-where (£100bln) or how much it’s cost to bail the banks out in 2008 – £500 bln!

The debate about how much governments can afford to leverage up before crisis is going to be an ugly one between the traditionalists who will demand a sharp scale back, and the MMT factions arguing for even greater spending. Somewhere in that argument between spending our way of out recession, and calls for financial orthodoxy, some important lessons are going to be lost. And markets will arb these events.

That’s what they do…

via ZeroHedge News https://ift.tt/2zJPJ6P Tyler Durden