Is This The Other Reason Why Stocks Just Won’t Go Down?

While the world and their pet cat knows that the gush of global liquidity has lifted all stock market boats – blinkering investors to any threats from organic recessions, virus-driven supply-chain collapse, record high leverage, and/or record high valuations.

Source: Bloomberg

But, as the chart above shows, the last week or so has seen stocks soar even further, despite a flattening in central bank liquidity (and despite soaring death-counts from Covid-19).

So what is driving this renewed surge?

Perhaps it is this?

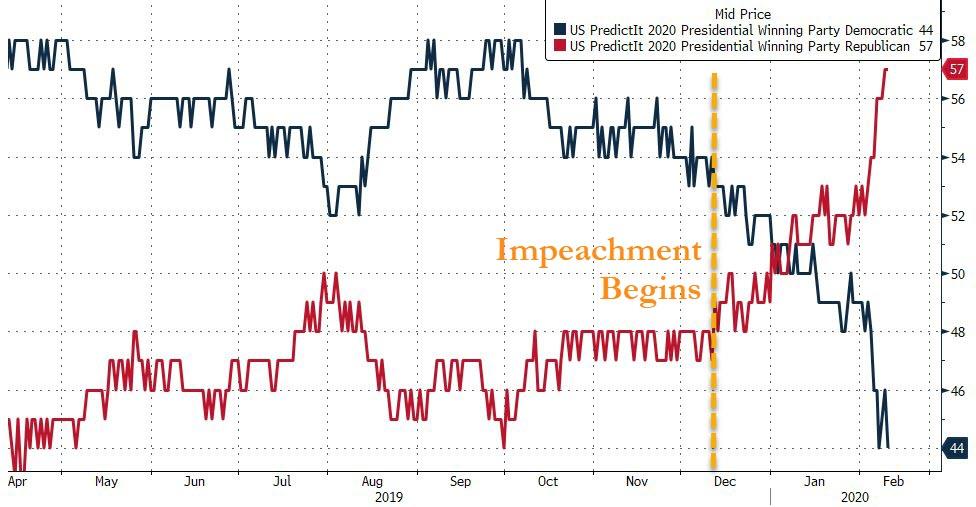

Sanders victory in New Hampshire (and close second place in Iowa) along with the devastation in Warren and Biden’s camps, leaves him the massive front-runner in the Democratic presidential nominee race…

Source: Bloomberg

But… as Sanders soars, so does the odds of a Republican (Trump) victory in November 2020…

Source: Bloomberg

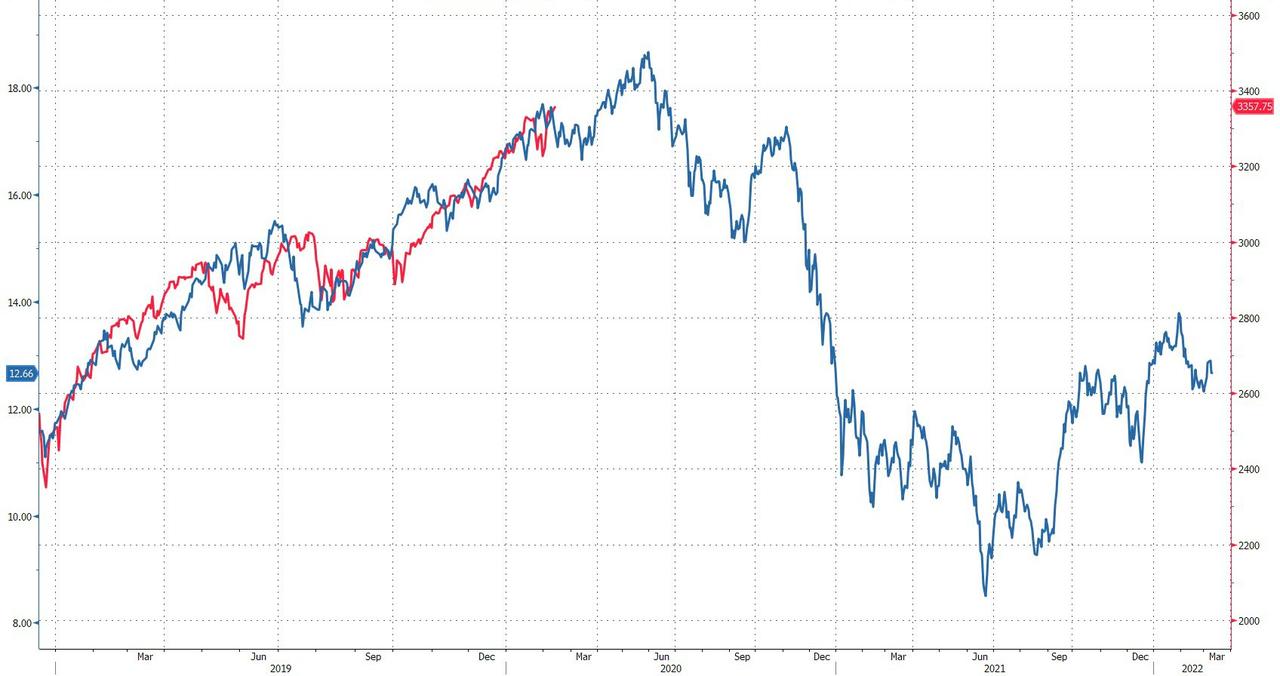

And as the odds of a Trump win have accelerated, so has the stock market…

Source: Bloomberg

Is it as simple as that? The market appears convinced that Sanders will get the Dem nomination and lose in November.

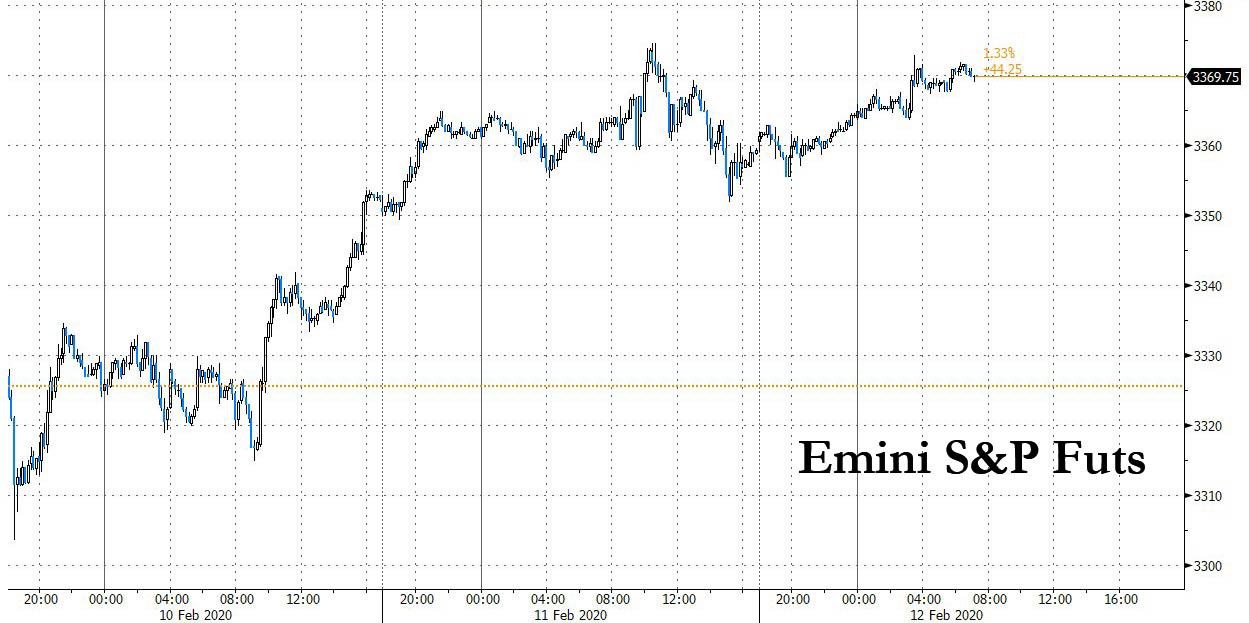

Stocks Panic-Bid To Record Highs Amid Liquidity-Fueled “Stark Reality” Divergence Between Markets & Real World

Authored by Richard Breslow via Bloomberg,

Traders are doing their best to pretend they have a serious handle on how the coronavirus tragedy will play out. They’re racing back and forth anticipating the effects on the global economy, asset prices and central bank policy. It makes for active trading. But at this point, if anyone is making longer-term investing decisions based on the narrative of the day, they are flipping a coin. Even though they would beg to differ.

It seems to be the case that markets are once again driven by the unshakable belief that the central banks will have their backs if necessary. And sooner rather than later. They are apparently not bothered by the warnings of the limited scope for further monetary policy stimulus. The simple reason is the expectation that the less room there is for more traditional responses, the more the likelihood for more extreme measures, as there won’t be any choice. And risk assets will like that even more. What a world.

S&P and Dow surged to record highs today…

I have my own theories of how, in the bigger picture, to look at this situation. And I’m not going to say what it is. At this point it doesn’t really matter. But there’s no reason to abandon the short-term charts and see what can be made out of whatever is the current theme of the day. Especially, since it’s mid-week and we don’t have the weekend effect to take into consideration. Although, this Friday will be another interesting data-point in seeing just how bulled up the bulls are prepared to be.

Looking at the screens, it’s obvious that this moment’s mood in the market is buoyant. Demonstrating once again the stark reality that financial markets and the real world can diverge with no difficulty. If I didn’t see the prices, all I would have to do is read the titles of the commentaries being circulated.

Although, you can never fool EUR/CHF for very long. It has continued its way lower in almost blatant defiance of the Swiss National Bank. I’m very curious to see if the narrative changes as the currently bid risk assets make their way to their technical resistance levels or we can keep motoring.

Emerging market currencies, not surprisingly, had a rough second half of January after a spectacular run that began last September. After chopping around in a big range so far in February they are trying to regain their composure. A major resistance zone for the MSCI Emerging Market Currency Index is close. Watch how it trades between 1653 and 1655. So far today the high has been 1651.95.

Copper prices melting down was a major story for the markets as this episode developed. The metal is also trying to bounce. Its move down was big and fast enough that it has left behind a few former support zones, that are now resistance. It’s starting to nibble at them. If there are two things that define this market, it’s that when it gets going, it can really motor. And when it fails, it can do so with considerable drama. Whether you are bullish or bearish, it’s in play and bears watching.

The dollar is taking a bit of a breather. It’s a tough call here. So many haters and so many people who need them. I’ll go out on a limb and say it has yet to do anything wrong. But, barring news, it’s probably not today’s trade. A lot of people think the dollar went too far, too fast. Yet, when you look at the euro area’s latest industrial production numbers, it’s another seriously disappointing data point.

It’s not surprising that ECB Chief Economist Philip Lane reiterated yesterday that they hadn’t reached the reversal rate yet. Something for everyone trading this asset class.

I’ll try to resist bonds. The range is well known and agreed upon

Watch Live: Fed Chair Jay Powell Testifies Before Senate Banking Committee

Fed Chair Powell concludes his two-day testimony on The Hill today.

Having been chastised by the Democrat-controlled House Financial Services Committee for attending a party at Jeff Bezos’ house yesterday, and not paying enough attention to varigating rates for minorities and taking account of climate change, today’s testimony before the Republican-controlled Senate Banking Committee, may be a little friendlier.

As Rabobank’s Michael Every noted earlier, today we get to listen to a technocrat describe how well everything is going while trying to decipher the hidden and not so hidden hints in his speech to ensure that one correctly front-runs where the state is about to pour enormous buckets of liquidity.

My colleagues and I strongly support the goals of maximum employment and price stability that Congress has set for monetary policy. Congress has given us an important degree of independence to pursue these goals based solely on data and objective analysis. This independence brings with it an obligation to explain clearly how we pursue our goals. Today I will review the current economic situation before turning to monetary policy.

Current Economic Situation

The economic expansion is well into its 11th year, and it is the longest on record. Over the second half of last year, economic activity increased at a moderate pace and the labor market strengthened further, as the economy appeared resilient to the global headwinds that had intensified last summer. Inflation has been low and stable but has continued to run below the Federal Open Market Committee’s (FOMC) symmetric 2 percent objective.

Job gains averaged 200,000 per month in the second half of last year, and an additional 225,000 jobs were added in January. The pace of job gains has remained above what is needed to provide jobs for new workers entering the labor force, allowing the unemployment rate to move down further over the course of last year. The unemployment rate was 3.6 percent last month and has been near half-century lows for more than a year. Job openings remain plentiful. Employers are increasingly willing to hire workers with fewer skills and train them. As a result, the benefits of a strong labor market have become more widely shared. People who live and work in low- and middle-income communities are finding new opportunities. Employment gains have been broad based across all racial and ethnic groups and levels of education. Wages have been rising, particularly for lower-paying jobs.

Gross domestic product rose at a moderate rate over the second half of last year. Growth in consumer spending moderated toward the end of the year following earlier strong increases, but the fundamentals supporting household spending remain solid. Residential investment turned up in the second half, but business investment and exports were weak, largely reflecting sluggish growth abroad and trade developments. Those same factors weighed on activity at the nation’s factories, whose output declined over the first half of 2019 and has been little changed, on net, since then. The February Monetary Policy Report discusses the recent weakness in manufacturing. Some of the uncertainties around trade have diminished recently, but risks to the outlook remain. In particular, we are closely monitoring the emergence of the coronavirus, which could lead to disruptions in China that spill over to the rest of the global economy.

Inflation ran below the FOMC’s symmetric 2 percent objective throughout 2019. Over the 12 months through December, overall inflation based on the price index for personal consumption expenditures was 1.6 percent. Core inflation, which excludes volatile food and energy prices, was also 1.6 percent. Over the next few months, we expect inflation to move closer to 2 percent, as unusually low readings from early 2019 drop out of the 12-month calculation.

The nation faces important longer-run challenges. Labor force participation by individuals in their prime working years is at its highest rate in more than a decade. However, it remains lower than in most other advanced economies, and there are troubling labor market disparities across racial and ethnic groups and across regions of the country. In addition, although it is encouraging that productivity growth, the main engine for raising wages and living standards over the longer term, has moved up recently, productivity gains have been subpar throughout this economic expansion. Finding ways to boost labor force participation and productivity growth would benefit Americans and should remain a national priority.

Monetary Policy

I will now turn to monetary policy. Over the second half of 2019, the FOMC shifted to a more accommodative stance of monetary policy to cushion the economy from weaker global growth and trade developments and to promote a faster return of inflation to our symmetric 2 percent objective. We lowered the federal funds target range at our July, September, and October meetings, bringing the current target range to 1-1/2 to 1-3/4 percent. At our subsequent meetings, with some uncertainties surrounding trade having diminished and amid some signs that global growth may be stabilizing, the Committee left the policy rate unchanged. The FOMC believes that the current stance of monetary policy will support continued economic growth, a strong labor market, and inflation returning to the Committee’s symmetric 2 percent objective. As long as incoming information about the economy remains broadly consistent with this outlook, the current stance of monetary policy will likely remain appropriate. Of course, policy is not on a preset course. If developments emerge that cause a material reassessment of our outlook, we would respond accordingly.

Taking a longer view, there has been a decline over the past quarter-century in the level of interest rates consistent with stable prices and the economy operating at its full potential. This low interest rate environment may limit the ability of central banks to reduce policy interest rates enough to support the economy during a downturn. With this concern in mind, we have been conducting a review of our monetary policy strategy, tools, and communication practices. Public engagement is at the heart of this effort. Through our Fed Listens events, we have been hearing from representatives of consumer, labor, business, community, and other groups. The February Monetary Policy Report shares some of what we have learned. The insights we have gained from these events have informed our framework discussions, as reported in the minutes of our meetings. We will share our conclusions when we finish the review, likely around the middle of the year.

The current low interest rate environment also means that it would be important for fiscal policy to help support the economy if it weakens. Putting the federal budget on a sustainable path when the economy is strong would help ensure that policymakers have the space to use fiscal policy to assist in stabilizing the economy during a downturn. A more sustainable federal budget could also support the economy’s growth over the long term.

Finally, I will briefly review our planned technical operations to implement monetary policy. The February Monetary Policy Report provides details of our operations to date. Last October, the FOMC announced a plan to purchase Treasury bills and conduct repo operations. These actions have been successful in providing an ample supply of reserves to the banking system and effective control of the federal funds rate. As our bill purchases continue to build reserves toward levels that maintain ample conditions, we intend to gradually transition away from the active use of repo operations. Also, as reserves reach durably ample levels, we intend to slow our purchases to a pace that will allow our balance sheet to grow in line with trend demand for our liabilities. All of these technical measures support the efficient and effective implementation of monetary policy. They are not intended to represent a change in the stance of monetary policy. As always, we stand ready to adjust the details of our technical operations as conditions warrant.

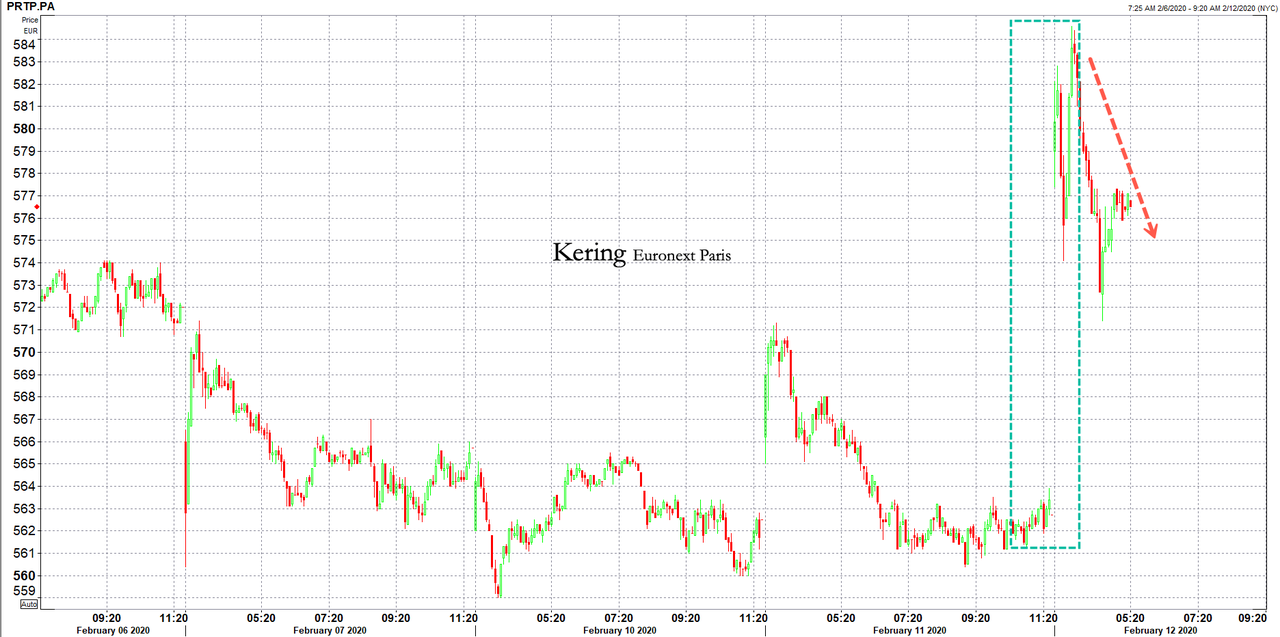

Luxury Hard Landing? Gucci Owner Blames Covid-19 Virus For Deteriorating Outlook

Kering shares on the Euronext Paris jumped several percents on Wednesday following higher-than-expected sales for 4Q19. Traders have since faded the initial pop, due mostly to the company’s warning that the virus outbreak in China could damage sales in 1Q20 for its star brand Gucci, reported Reuters.

Kering said Gucci’s success is partly because of the robust Chinese market, with much of the economy shut down, and consumption collapsed, this could have a significant impact on “consumption trends and tourism flows, and their ability to affect economic growth.”

Kering’s CFO Jean-Marc Duplaix said the company “remained very confident about its growth potential in the medium and long term” despite the world’s second-biggest economy shut down, 400 million people in quarantine, factory hubs on idle, and transportation networks froze.

Kering’s revenues increased by 13.8% to $4.76 billion in 4Q, up 11% Y/Y. Duplaix said despite sales halving in Hong Kong last year because of the riots, the company was overly reliant on mainland China to drive new sales. He said Gucci contributes 83% of its recurring operating income.

However, just like global stock markets, Kering’s Chairman P{inault is optimistic…

“Knowing how dynamic and resilient the Chinese people are, we expect things to return to normal promptly once the emergency is over,”

But, Kering admitted it was “impossible” at this time to assess the impact of the virus on business and how fast it will recover, as it has closed around half of its stores in mainland China and is postponing new openings and reviewing product launches in the country due to the impact of Covid-19.

Earlier this week, Italian jacket maker Moncler warned that sales at its stores in China crashed 80% since the virus broke out.

“The company’s initial 2020 outlook currently includes an estimated negative impact of the coronavirus outbreak in China of approximately $50 million to $60 million in sales related to the first quarter of 2020.”

Pandora A/S informed investors this week that its operating segment in China has ground to a halt.

Gucci, Moncler, Under Armour, and Pandora are some of the first consumer companies to realize a demand shock in China could severely damage sales in 1Q.

As we’ve mentioned before, the coronavirus impact on China is global, and it could be a large enough disruption that tilts the global economy into recession.

The Democratic presidential candidates have doubled down on the party’s opposition to the Trump immigration policies while supporting sanctuary cities, noncooperation with ICE on detainers and other issues. In the meantime, the Trump Administration is prevailing in litigation over his travel ban orders and it is now expanding the nations subject to the executive order. Both parties seem to believe that they have the voters on their side, including a new showdown in New York where Gov. Andrew Cuomo has signed the “Green Light Law” allowing undocumented persons to get driver’s licenses. That has set off a major confrontation with Homeland Security which is vowing to suspend enrollment in the Trusted Traveler Programs (TTP).

There was considerable coverage of the travel ban litigation when lower courts were ruling against the Administration. The litigation was no doubt prolonged by an original order that was poorly written and poorly defended. That order went through a series of changes but, as the challengers noted in court, the underlying claim of executive authority remained the same. Some of us believed that the Administration would prevail ultimately and criticized elements of the lower court decisions, including their reliance on campaign statements and tweets by President Trump. Ultimately, the Supreme Court lifted injunctions and signaled that the Administration would prevail on those fundamental claims.

The Trump administration’s latest travel ban, announced on January 31, targets six countries:

Eritrea, Kyrgyzstan, Myanmar and Nigeria – will not be allowed immigrant visas for permanent visas.

Sudan and Tanzania – will be barred from “diversity visas” that is open to countries will historically low levels of immigration.

Since all six have large Muslim populations, the same criticism over religious discrimination will be raised. It is guaranteed to trigger the same controversy — perhaps by design — right before the 2020 election. That will include at least one Supreme Court decision in the area and a number of appellate court decisions. On the travel orders, Trump still holds the advantage on precedent.

The Democrats are equally committed to their course on immigration. Cuomo signed the Green Light Law and joined 14 other states and the Washington D.C. in allowing undocumented persons to obtain driver’s licenses. However, Homeland Security opposes the laws. Thus, Acting Homeland Security Secretary Chad Wolf announced that some 800,000 people will be suspended from the TTP over the next five years. There will be almost 90,000 New Yorkers impacted immediately and barred from programs like Global Entry. Changes will often not occur until the date of renewal for such programs. Cuomo is pledging a lawsuit over the changes.

As with sanctuary cities and ICE detainer conflicts, the travel ban sets up 2020 as an election on immigration policies like no other in modern political history. The only thing that is clear, again, is someone is really, really wrong.

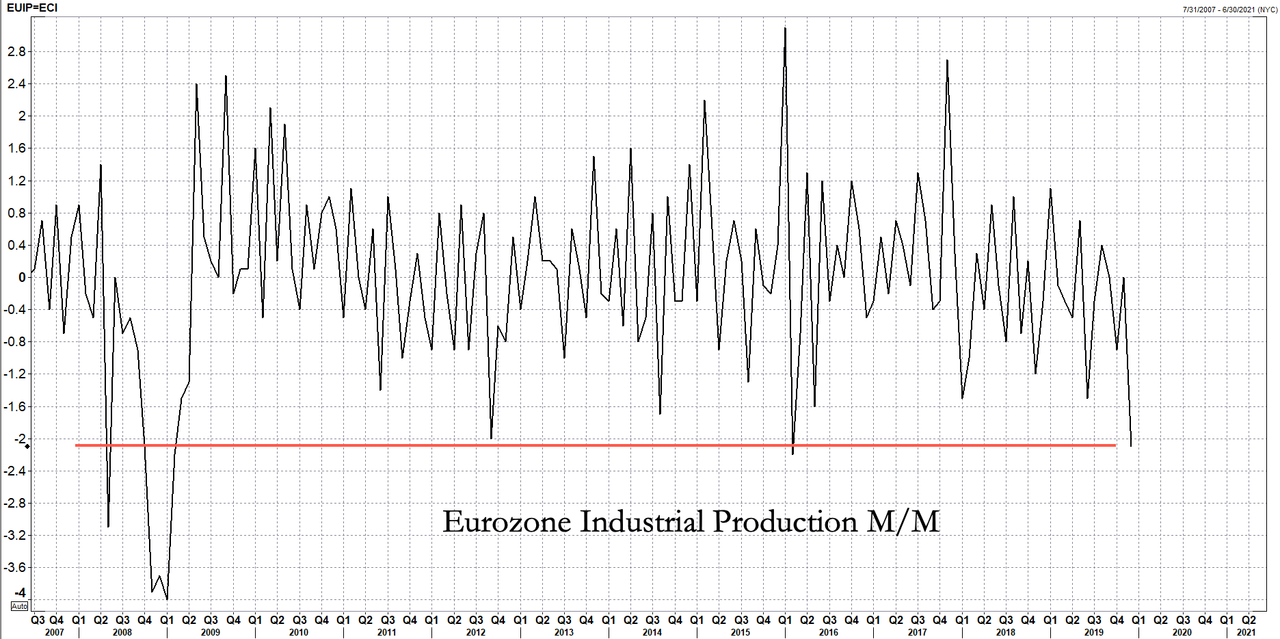

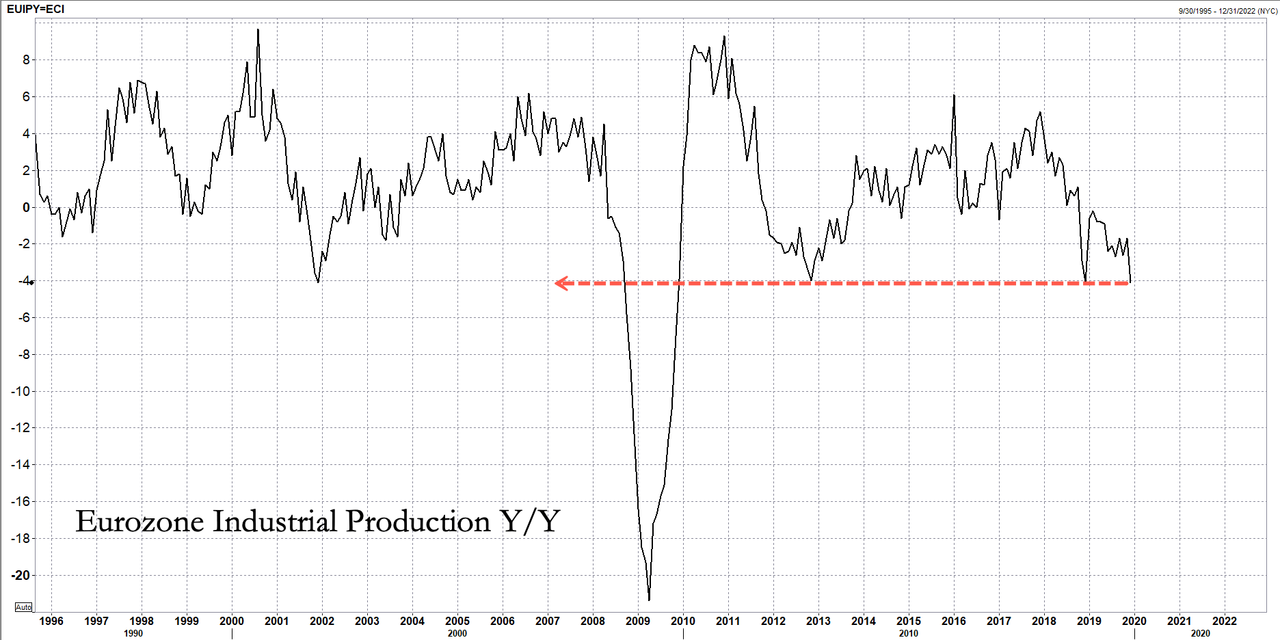

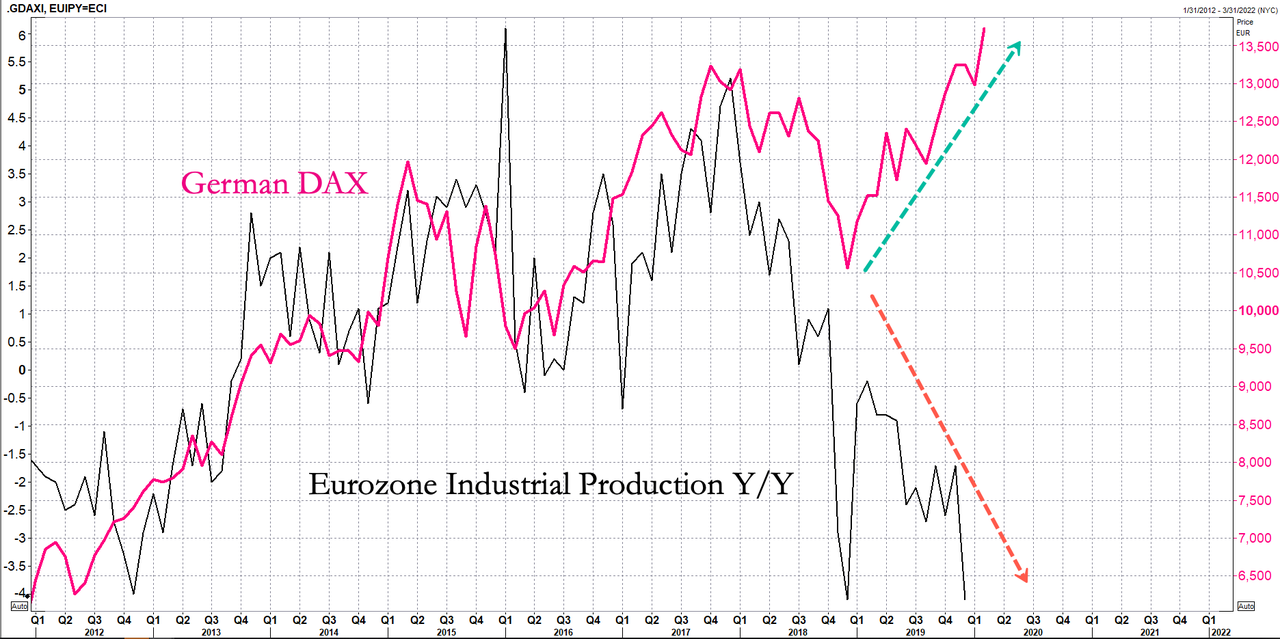

What Rebound? Eurozone Industrial Production Collapses In December

On Wednesday morning, all hope for a recovery in Europe was abandoned when industrial production numbers missed estimates in December.

Industrial production fell -2.1% in December on an M/M basis, according to Eurostat, confirming our suspicions that Germany was “suck in a recession,” with limited signs of an economic rebound.

Eurozone industrial production plunged -4.1% in December on a Y/Y basis, now printing at its weakest level since 2012.

The disappointing news came as investors have been buying European equities hand over fist, essentially frontrunning an industrial recovery, that at this point, could be another example where central banks are forcing risk-taking at a time when many should be playing defensive names.

Though sentiment has improved in the region in the last several months because the European Central Bank (ECB) continues its unprecedented money printing to keep the stock market party alive.

However, no matter how much money the ECB throws at stocks and corporate bonds, industrial production remains in a severe slump, now two-years-old, with no rebound in sight.

Economists have spent the last several weeks revising down their forecasts for Eurozone economic growth in 1Q as the coronavirus shock in China could produce an even more significant downturn in Europe.

“European car manufacturers, in particular, are already warning of potential shortages of components due to factory shutdowns in China,” said Jessica Hinds, an economist at Capital Economics. “So even if the virus is soon brought under control, eurozone industry is likely to remain in recession in at least the early part of this year.”

The longer China’s economy remains offline, the larger the shock will be in Europe and elsewhere.

“The longer it takes for production to resume, the higher the risks,” said Jörg Krämer, chief economist at Commerzbank in Frankfurt.

Automobiles are Germany’s largest export. The industrial slump could produce a negative print for 4Q19 GDP.

The challenges of the imploding automobile industry in Germany have spread across the Continent. Suppliers in other countries were also affected by the industrial slowdown.

“For most countries, Germany is the most important trading partner,” said Carsten Brzeski, chief economist at ING Germany. “If it starts to slow down, other countries will feel it.”

One of the most significant threats to Europe’s economy is part shortages from China. This could effectively cause major production lines in Germany and across the Continent to shut down.

Also, Daimler sold 700,000 Mercedes-Benz cars in China last year, twice as many as it sold in the US. If two-thirds of China’s economy remains frozen, and more than 400 million people are in quarantine, this could severely damage car sales.

Europe’s industrial production downturn continued to accelerate in late 2019, but now, it could crash because of the virus shock seen in China.

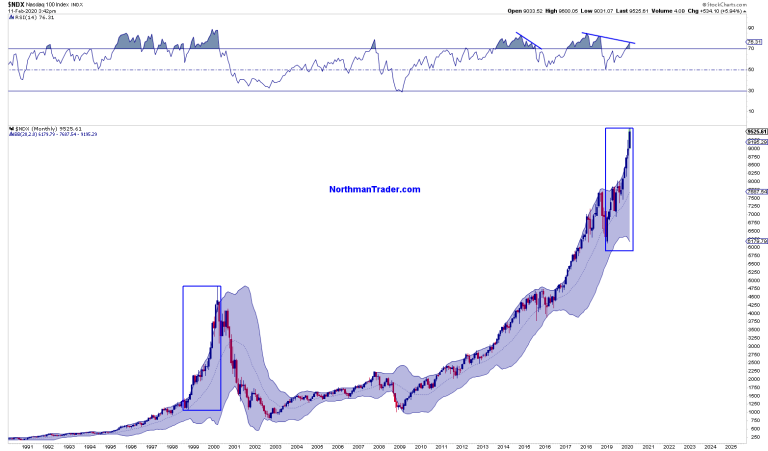

We’ve talked about the year 2000 comparison (Party like it’s 1999). In 2020 markets went onto a similar structural tear just having rammed relentlessly higher. In 2000 markets famously topped in March following the Fed’s Y2K inspired liquidity injections in 1999 as markets had vastly disconnected from fundamental reality.

Now that the truth is out we also know that markets are now vastly disconnected from fundamentals.

And the 2000 comparisons still hold water on a number of measures, price to sales, price to ebitda, market cap to GDP and of course relative weightings in favor of the few as the rally continues to narrow.

The top 2 stocks now have gone complete vertical especially as it relates to their weighting in the S&P:

This chart from Carter Worth on Fast Money last night and even he pointed out how in the lead up to the 2000 top there was some back and forth, but not here, just completely uninterrupted vertical.

One of the 2 stocks being Microsoft, a stock that now has nearly doubled since 2019 with a market cap expansion of over $700 billion for a total market cap of over $1.4 trillion. Historic.

And add the top 4 and their market caps you get this same vertical picture:

Everything screams reversion and correction, but nothing. The market just keeps going up and they keep buying the big cap tech stocks. Risk free. Or so it seems.

And given the large weightings of these few stocks $NDX just keeps ramping up vertically as well, also far outside the monthly Bollinger band:

So yes, one can make year 2000 comparisons on some specific measures and market behavior.

In 2000 we had a top in March. One may consider that to be a sample size of N1, an outlier statistic, but it isn’t. Markets have seen this before.

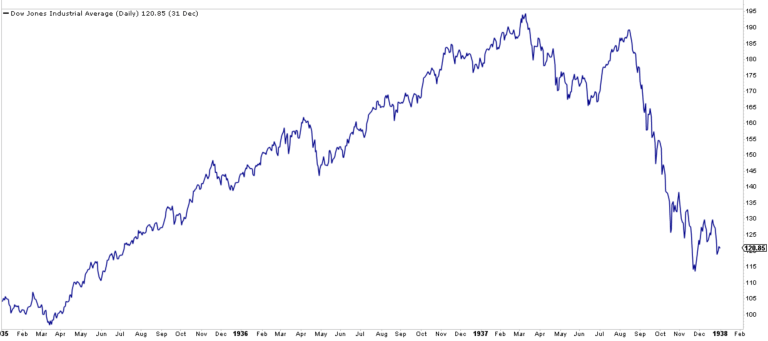

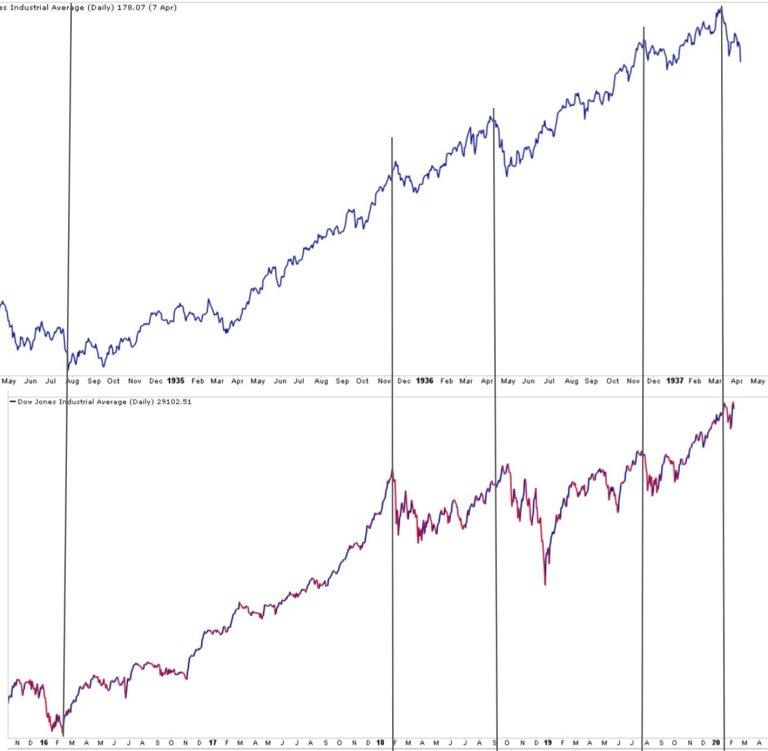

1937:

Markets ran wild for several years following the 1929 crash and optimism was rampant. And look at the structure of the chart. A relentless rally in 1936, followed by another massive squeeze in early 1937 with a final spike into early March, and then all the 1936/1937 gains were given back in the same year as the recession unfolded.

That’s your revisit the lows of 2018 scenario.

No analog is perfect and I could be faulted for moving the scales, but generally speaking I can make the case for an at least similar structure here:

Are we topping here, or one more final burst into 3400/3500 on $SPX into March? April? I can’t say. The analog structure leaves room for the possibility that we may be topping here, but there’s no confirmation as of yet.

All I can say is that these top tech stocks are in technical la la land and present a clear and present danger to not only the stock market but also the economy. See these reverse hard and, because of their outsized weightings, take the indices with them we may see awe-inspiring systemic selling in markets that would bring about a recession.

It’s all theoretical right now, but that’s the larger risk I see in the structural make up of this market.

The market keeps getting narrower in leadership, it keeps getting ever more divergent and artificial liquidity is all that’s keeping it up. And, as markets have rallied relentlessly ignoring all risks, they face the prospect of meeting the fate of history of similar rallies in the past. Not only 2000, but also 1937.

And hence it’s perhaps ironic or telling that $SPX hit its upper trend line resistance today:

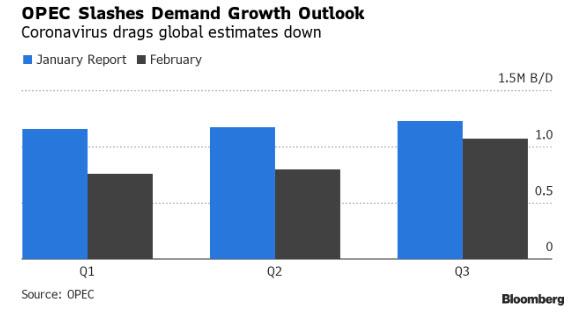

OPEC Slashes Oil Demand Forecast On Coronavirus Crunch

Perhaps buoyed by speculation that oil demand in China is set to plunge as much as 20% if not more on the coronavirus “demand shock”, on Tuesday OPEC slashed it forecast for global oil demand by almost a quarter million barrels per day as the coronavirus pandemic cripples fuel use in China, leaving the cartel facing a renewed glut despite its recent production cuts.

The cartel reduced projections for demand growth in the first quarter by 440,000 barrels a day, or about a third, in its monthly report, and 230,000 for the full year, one day after oil prices sank to a one-year low on Monday as the infection has idled thousand of businesses and left millions quarantined in the world’s biggest crude importer.

The plunge in oil prices has sparked a push by OPEC’s top exporter, Saudi Arabia, to push for an emergency meeting and consider new output cutbacks, following a recent Vienna meeting that ended without a consensus after Russia – the biggest non-OPEC producer – refused to comply with further cuts as it is able to weather lower prices more easily.

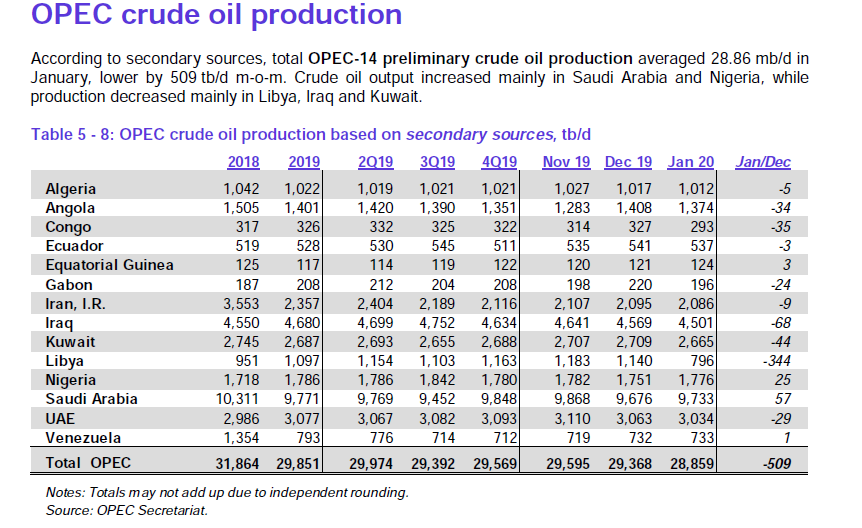

Ominously for Riyadh, the latest OPEC report showed that, even though many OPEC members made a strong start with fresh output curbs that took effect last month, the overhang from the virus will leave them with an even greater surplus. The group collectively pumped 28.86 million barrels a day in January, down 509,000 on the month, and if it maintains that rate there will be a surplus of 570,000 barrels a day during the second quarter, when consumption slows down seasonally.

Furthermore, unlike bullish stock traders, OPEC doesn’t see the effects of the disease confined to the start of the year, and has cut its growth estimate for global oil demand in 2020 as a whole by a whopping 230,000 barrels a day to just under 1 million a day. Yet even with the cut, the increase remains slightly higher than last year’s.

Ironically, despite OPEC’s fatalism, oil prices recovered overnight precisely on the opposite, namely speculation the spread of the disease could be nearing its peak. Even so, Brent trading at $55 a barrel is well below the levels most OPEC members need to cover government spending.

It could have been even worse: since OPEC formed an alliance with non-members such as Russia three years ago, the coalition has restrained supplies to offset a surge of production from the U.S. shale industry, and keep prices supported, indirectly supporting the US shale sector. In January, OPEC launched a new round of cutbacks which served to briefly send oil prices higher before a bear market ensued in the days following on the coronavirus epidemic.

Last week an OPEC+ expert committee recommended reducing output by a further 600,000 barrels a day to offset the impact of the coronavirus. Russia, which held out, said it was “studying” the proposal and its energy minister, Alexander Novak, is consulting with oil companies today. Which may explain the latest gloomy OPEC outlook, which may encourage them to give greater consideration to taking additional measures.

“Clearly, the ongoing developments in China require continuous monitoring and assessment to gauge the implications,” the report said.

“He’ll Ruin Our Economy”: Lloyd Blankfein Warns “Russians Will Reconsider Who To Work For” If Sanders Clinches Nomination

Just when it looked like Bernie Sanders would become the first avowed Democratic Socialist to win the Iowa caucus, the Iowa DNC delivered a political slide tackle with their botched polling map, effectively robbing Sanders of a considerable amount of momentum

But Sanders and his band of white college-educated liberals and hackey-sacking “Bernie Bros” soldiered on from the disaster in Iowa and managed to clinch the first place finish in New Hampshire, sending a jolt of apprehension through corporate America.

As Sanders delivered his triumphant victory speech, one of America’s most famous capitalist, a man who led “the Vampire Squid” Goldman Sachs during one of the most ruthless periods in the bank’s history, decided to weigh in on twitter, which he uses pretty sparingly to share his views on politics and public affairs.

Lloyd Blankfein tweeted that if Sanders wins the nomination, “the Russians will have to reconsider who to work for to best screw up the US.”

If Dems go on to nominate Sanders, the Russians will have to reconsider who to work for to best screw up the US. Sanders is just as polarizing as Trump AND he’ll ruin our economy and doesn’t care about our military. If I’m Russian, I go with Sanders this time around.

Sure, Blankfein might have a point: wasting hundreds of billions of taxpayer dollars to pay off private debts is obviously terrible public policy, unless you’re doing it to stave off a devastating economic crisis. And at least when the banks got bailed out, they paid taxpayers back.

But we digress: There are many legitimate reasons to criticize Sanders. But a billionaire banker supervillain spreading hysterical nonsense about Russia to try and scare Americans away from supporting a socialist is just a little too on the nose, as Tom Wright, the WSJ reporter who blew the lid off the 1MDB scandal, reminds us:

This from a CEO who oversaw Goldman’s role in the subprime crisis, the Libya scandal and 1MDB fraud, and whose pay is still suspended as the bank investigates 1MDB. https://t.co/xQ87DHn3M2

Health insurers have seen brief dips in their shares, but outside that, Wall Street hasn’t exhibited too much concern about Sanders. The prevailing thinking, from what we can tell, is that if the Democrats don’t kneecap him, he’ll lose to Trump, unless the coronavirus outbreak really does plunge the world into a deep recession between now and November.

Blankfein, a registered Democrat, tweeted three months ago that Elizabeth Warren unfairly vilified Wall Street, even embedded a clever little dig at Warren’s “native American heritage”.

Speaking on CNBC Wednesday morning, Democratic political strategist Frank Luntz said he had a piece of advice for Blankfein: “Delete your twitter account…it’s not a good look.”

And not because Luntz disagrees. It’s because a billionaire slamming Sanders plays right into the candidate’s rhetoric about terrified billionaires lashing out and running scared. We must admit…he has a point.

World Stocks Storm To Record High As Traders “Believe All Will Be OK With The Coronavirus Situation”

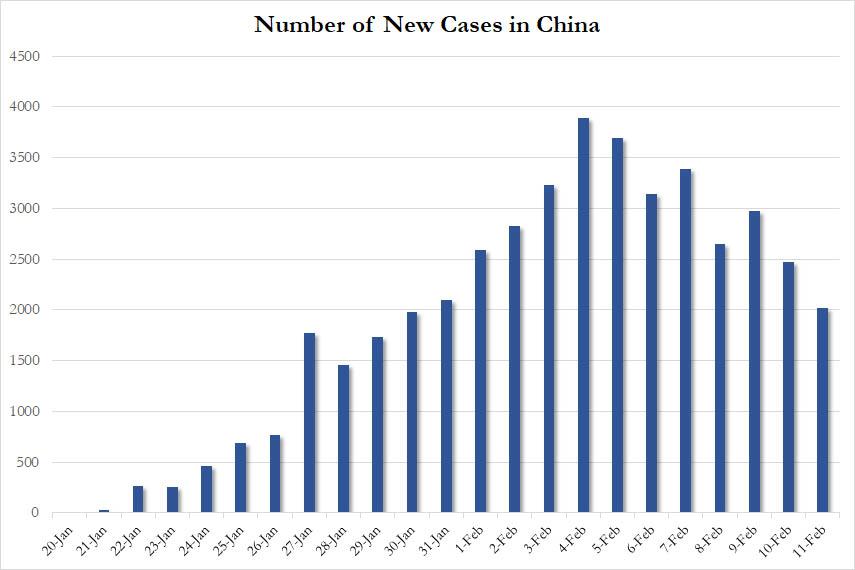

Another drop in the number of new coronavirus cases and Powell’s cheerful view of the economy (with the backstop of more easing should the coronavirus epidemic turn out worse than expected) boosted global stocks for a third day on Wednesday and sparked a 2% rally in oil prices, on hopes the epidemic’s effects would be contained.

S&P futures indicated Wall Street would extend gains from Tuesday, when the S&P 500 and Nasdaq posted record closing highs, gaining overnight along with European stocks on Wednesday…

… after China reported its lowest number of new coronavirus cases since late January, lending weight to a prediction from its senior medical adviser that the outbreak might be over by April.

The drop encouraged investors to get back into equities at the expense of safe-haven assets such as bonds, gold and the Japanese yen which benefited as the virus death toll mounted. Riskier, higher-yielding bonds also rallied, with yields on 10-year Greek governments bonds slipping under 1% for the first time ever .

“If you look at the share indexes and other risky assets it seems like people now believe all will be okay with the coronavirus situation,” said Francois Savary, chief investment officer at Swiss wealth manager Prime Partners.

MSCI’s global equity index rose 0.2% to stand just off Tuesday’s record highs. The pan-European Stoxx 600 index rose to a record as automobile stocks — which depend on exports to China — jumped 1.2%. Carmakers and miners led the advance in Europe even as data showed a deep slump in euro-area industrial output at the end of last year.

Earlier in the session, Asian stocks gained, led by communications and technology stocks. The MSCI Asia Pacific Index advanced for a second day. Markets in the region were mixed, with Taiwan’s Taiex Index and Hong Kong’s Hang Seng Index rising and Indonesia’s Jakarta Stock Price Index falling. Chinese shares rose almost 1% and the offshore-traded yuan reached two-week highs after the death toll from the coronavirus reached 1,115. President Xi Jinping vowed that China would meet its economic goals while winning the battle against the deadly pandemic.

Despite the clear return of market euphoria, many analysts still caution against complacency over the economic fallout. Some Chinese firms have reported job cuts caused by damage to manufacturing supply chains. Savary at Prime Partners agreed, noting the dollar is near four-month highs, 10-year U.S. yields are some 30 basis points below early-January levels and demand for Swiss francs is high.

“Investors are not completely convinced the coronavirus is under control … they are trying to hedge their equity bets by taking exposure to safe-havens at the same time,” he said.

In short, we are back to the good news is good, bad news is better regime that defined much of the past decade.

Markets also got a boost from signs President Donald Trump might be re-elected in November, since centrist candidates for the Democratic nomination appear to be struggling and Biden’s candidacy is now in tatters after his disastrous performance in New Hampshire where we didn’t win a single delegate.

“Trump had a great start into the U.S. election season. After the early end of the impeachment trial in the Senate and the Iowa caucus chaos for the Democrats, betting markets suggest that Trump has a 58% probability of winning re-election on 3 November,” Berenberg said.

Summarizing the New Hampshire primary results this morning, after 86% of the precincts reported, Sanders has been declared the winner with 25.8% of the vote, followed by Buttigieg in second with 24.4%, and then Klobuchar at 19.7%. Both Warren and Former Vice President Biden finished in a distant 4th and 5th at 9.3% and 8.4% respectively. In terms of the narrative and expectations, Klobuchar significantly outperformed her polls following a strong debate performance last Friday, with exit polls showing that roughly 50% of NH voters deciding in the last 3 days. Buttigieg also seems to have outperformed in a second straight state. Klobuchar’s outperformance may have come at the other Moderate’s expense – keeping Buttigieg from beating Sanders overall and keeping Biden under the 15% threshold to win proportional delegates. The Moderate wing of the primary continues to outperform the Left wing – Biden/Buttigieg/Klobuchar with 52.5 % and Sanders/Warren with 35.1% respectively – but it is not clear whether voters will jump between those groups. Biden left NH early in the day to start campaigning in South Carolina, indicating that the disappointing results in the first two states will not stop his primary campaign. It seems that we will not have the traditional winnowing seen after Iowa and New Hampshire, with all five major candidates moving on to Nevada and South Carolina. The field will likely only finally clear once over a third of delegates are awarded after Super Tuesday, but even then Former New York City Mayor Mike Bloomberg has already been campaigning in those delegate-rich states.

In geopolitics, the US Army is planning to set up a new military command post to cooperate with European allies in countering potential threats from Russia. The US said it was prepared to sign a deal with the Taliban that would see the withdrawal of US troops and the start of peace talks between the insurgents and the Afghan government, although a deal would only proceed if the Taliban adhere to a pledge to reduce violence over a 7-day period. Elsewhere, Turkish President Erdogan will do whatever is necessary; includes air and ground means – Erdogan accuses Russian forces of a massacre in Idlib – Erdogan and Russian President Putin discussed the situation via a phone call. Erdogan adds that Turkey will hopefully see inflation below 8.5% year-end target, trend of falling interest rates will continue.

In rates, yields on Treasuries and German Bunds rose around 2 basis points, the former rising to 1.62%; ten-year U.S. yields are now 12 bps off the four-and-a-half-month lows reached in late January. Yields rose on Tuesday after Fed Chair Jerome Powell said the U.S. economy was “resilient”. Powell also said he was monitoring the coronavirus, because it could lead to disruptions that affect the global economy.

In FX, the dollar was steady while currencies such as the Thai baht and Korean won, reliant on Chinese tourism and trade, gained 0.3% to 0.5%, as the yen slipped 0.3% to a three-week low against the dollar. The day’s big currency mover was the New Zealand dollar, which rose more than 1% against the greenback after the Reserve Bank of New Zealand kept rates unchanged and indicated it would remain on hold barring an outsized impact from the coronavirus outbreak. Traders pared odds for an RBNZ rate cut by May to around 30% from almost 50% before the decision; the Aussie advanced with the kiwi. Sweden’s krona shrugged off a downward revision of the Riksbank’s inflation forecast as the central bank kept its rate path intact, signaling a repo rate at zero in the coming years. The pound rose and gilts slid as money markets trimmed bets on BOE easing.

In commodities, oil rallied back above $50 a barrel as investors waited to see whether Russia would accept an OPEC+ plan for production cuts to cope with demand destruction from the coronavirus.

Looking at the day ahead, we’ll hear from Fed Chair Powell once again as he appears before the Senate Banking Committee, while there’ll also be remarks from Philadelphia Fed President Harker and the ECB’s Chief Economist Lane. Data releases to look out for include the MBA’s weekly mortgage applications and the monthly budget statement for January.

Market Snapshot

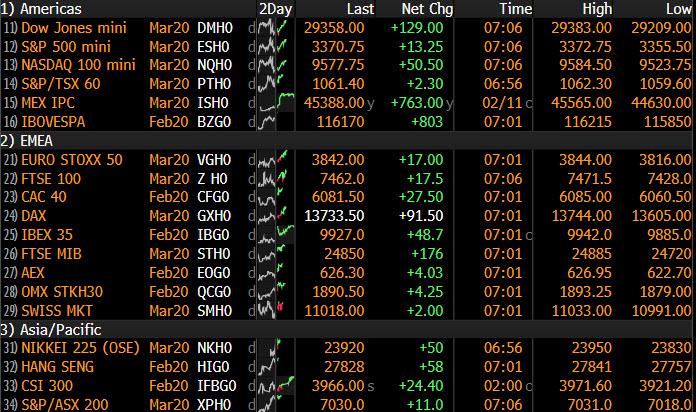

S&P 500 futures up 0.3% to 3,367.50

STOXX Europe 600 up 0.3% to 429.84

MXAP up 0.5% to 170.72

MXAPJ up 0.8% to 555.01

Nikkei up 0.7% to 23,861.21

Topix down 0.04% to 1,718.92

Hang Seng Index up 0.9% to 27,823.66

Shanghai Composite up 0.9% to 2,926.90

Sensex up 0.9% to 41,584.82

Australia S&P/ASX 200 up 0.5% to 7,088.20

Kospi up 0.7% to 2,238.38

German 10Y yield rose 2.0 bps to -0.371%

Euro down 0.03% to $1.0913

Italian 10Y yield rose 1.6 bps to 0.802%

Spanish 10Y yield rose 4.8 bps to 0.316%

Brent futures up 1.8% to $55.00/bbl

Gold spot little changed at $1,566.82

U.S. Dollar Index little changed at 98.73

Top Overnight News from Bloomberg

The coronavirus outbreak in China could become a negative shock to global economic growth in the short term, ECB Governing Council member Gabriel Makhlouf says

A deep slump in euro-area industrial output at the end of last year highlights the scale of the challenge the sector will face in 2020. The 2.1% drop — the steepest in almost four years — will raise doubts about a meaningful rebound in momentum

Some of the world’s major bond funds are rekindling their love for Chinese government debt, as an unexpected rally in recent weeks took the 10-year yield to the lowest level since late 2016

President Recep Tayyip Erdogan vowed to strike Syria should there be any new aggression against Turkish soldiers deployed across the border, escalating threats against Damascus after winning rare support from the U.S.

Fidelity International is increasing long positions in U.S. and Australian sovereign bonds while reducing exposure to credit in some sectors amid the widening fallout from the coronavirus

The promise of yields when many bonds pay holders close to nothing is driving a boom in sales of hybrid securities which combine elements of both debt and equities. 3.7 billion euros worth of hybrid bonds have been issued since the start of the year in Europe. This marks the fastest pace of issuance since at least 2014, based on data compiled by Bloomberg

New Zealand’s central bank left interest rates unchanged and signaled it won’t need to cut them further unless the coronavirus outbreak has a bigger-than-expected impact on economic growth

Bernie Sanders won the New Hampshire primary Tuesday. With 84% of the precincts reporting, Sanders had 25.9% of the vote and Buttigieg had 24.4%. Klobuchar was third with 19.7%, according to the Associated Press, which called the race. Elizabeth Warren finished fourth with 9.4%, while longtime front runner Joe Biden had 8.4%

President Xi Jinping vowed China would meet its economic goals while winning the battle against the deadly coronavirus that has claimed 1,115 lives. Japan found 39 new cases of the coronavirus aboard a cruise ship, bringing the total number of cases from the vessel to 174

Preliminary genetic sequence data indicating the presence of a SARS-like virus in central China was known about two weeks before key information was publicly released, scientists said

All four U.S. government prosecutors who backed a long prison stay for Trump ally Roger Stone resigned from the case, a stunning rebuke to the Justice Department after it cut his recommended sentence by more than half

Oil edged back above $50 a barrel as investors waited to see whether Russia would accept an OPEC+ plan for production cuts to cope with demand destruction from the coronavirus.

Asian equity markets were mostly higher but with gains initially limited as coronavirus fears lingered and following the lack of conviction on Wall St. where US stocks notched fresh record highs at the open before gradually fading the moves throughout the day. ASX 200 (+0.5%) traded positively with the biggest movers driven by earnings releases including the largest of the Big 4 banks CBA, resulting in outperformance in the top-weighted financials sector, while Nikkei 225 (+0.7%) was also lifted as it played catch up on return from holiday and with SoftBank sitting on double-digit percentage gains following the federal court approval of the merger between its unit Sprint with T-Mobile. Elsewhere, Hang Seng (+0.9%) and Shanghai Comp. (+0.9%) were kept afloat but with the mainland initially indecisive after the PBoC refrained from liquidity operations for a neutral daily position and as participants contemplated over the ongoing outbreak in which the number of cases and death toll continued to mount albeit at a slower pace with the additional number of cases at 2015 which is the lowest since January 30th. Finally, 10yr JGBs were lower amid the gains in Japanese stocks and following the mixed results at the 10yr inflation-indexed auction, while pressure was also seen in New Zealand bonds in the aftermath of the less dovish statement from the RBNZ.

Top Asian News

Top Indian Iron Ore Miner Targets 50% Output Jump Next Year

China Life Group Said to Seek Hong Kong Listing Via Unit

Erdogan Escalates Threats Against Assad Loyalists in Idlib

Rewards Outweigh Risks for Assad in Drive to Retake Idlib

European equities are mostly higher [Eurostoxx 50 +0.6%] following on from a similar APAC session, which saw Japanese markets return from yesterday’s holiday and close with firm gains. Bourses are largely in the green with the exception of the SMI (-0.2%), led lower by heavyweights Roche (-0.7%), Nestle (-0.6%) and Novartis (-0.3%) – which together account for ~55% of SMI – as sectors reflect risk appetite (healthcare, consumer staples lag and utilities lag). In terms of individual movers – dismal earnings see ABN AMRO (-7.0%) at the foot of the pan-European index after net income and dividend printed sub-par, with interest income falling and impairments rising. On the flip side, Heineken (+6.2%) stands as a top Stoxx 600 gainer following their earnings in which net profit and consolidated beer volume topped estimates, leading to the best performance in over a decade. Kering (+2.2%) shares also benefit from their numbers after metrics beat estimates across the board including the much-watched Gucci Q4 comparable sales growth. Kering also noted that the uncertainties in China do not call into question the Co’s fundamentals in the luxury industry. Thus, European luxury stocks receive tailwinds: Swatch (+1.5%), Richemont (+1%) and LVMH (+0.6%) all trade higher in tandem.

Top European News

ECB’s Makhlouf Sees Risk of Negative Growth Shock on Coronavirus

Euro-Area Industrial Output Slumps Most in Almost Four Years

U.K. to Regulate Internet in Crackdown on Social Media Firms

Google Claims EU Crackdown Is a Threat to Internet Innovation

Riksbank Clings On to Zero Despite Cutting Inflation Outlook

In FX, the Kiwi is flying and leaving G10 rivals far behind on the back of another shift from the RBNZ towards ending its easing cycle. Nzd/Usd has rebounded sharply following February’s policy guidance tweaks and updated OCR projections that signal no change for the foreseeable future compared to 10 bp easing previously. In fact, the rate path is now pointing to a 1.10% benchmark price by mid-2021 vs 0.9% out to March next year last time, and the only caveat appears to be severe economic contagion from China’s virus. Nzd/Usd is now eyeing resistance ahead of 0.6500 from sub-0.6400 lows and the Aud/Nzd cross has snapped back towards 1.0400 following transitory forays just above 1.0500 of late. However, the Aussie is also outpacing its US peer that is largely consolidating after failing to extend its winning run when the DXY hit a brick wall inches before 99.000, as Aud/Usd probes firmer ground on the 0.6700 handle with some independent impetus from improved Westpac consumer confidence overnight.

GBP/CHF/CAD/EUR – All benefiting from the aforementioned flagging Greenback, albeit to varying degrees, with Cable also capitalising on Tuesday’s UK GDP data rather than any dovish BoE nuances and extending recovery gains beyond 1.2980 towards 1.3000 and the 10 DMA that falls just shy of the big figure (1.2997). Meanwhile, Eur/Gbp is hovering a few pips above 0.8400 as the single currency remains leggy around 1.0900 against the Buck after yet another Eurozone data miss via pan IP and Eur/Usd runs into headwinds at 1.0925. Note also, heavy option expiry interest between the round number and 1.0910 in 1.6 bn may be capping the headline pair ahead of the NY cut. Elsewhere, the Franc is still straddling 0.9750, but trending bullishly vs the Euro around a 1.0650 axis that prefaces multi-year peaks or troughs for the cross, while the Loonie is gleaning more underlying support from oil’s revival to hold above 1.3300 against its NA neighbour.

SCANDI – In contrast to the RBNZ, nothing new at all emanated from the Riksbank’s latest policy meeting as the repo trajectory matched December’s (flat) profile and accompanying statement underlined the likelihood that zero percent will prevail until the end of the forecast horizon. Nevertheless, Eur/Sek has drifted down towards 10.5000 as none of the regular Board dissenters entered reservations and Governor Ingves reiterated the on hold message in the ensuing press conference. However, Eur/Nok has fallen further on the crude price rebound noted above to test bids/support in front of 10.0500.

EM – Ongoing recovery gains across the region and the Rand only partially hampered by another SA data miss (retail sales), but no respite for the Lira as Turkish President Erdogan ramps up his verbal threats to repel attacks by Syrian Government sources to prevent the Try maintaining an attempt to regain 6.0000+ status.

In commodities, WTI and Brent front-month futures continue their upward trajectories with the contracts piggy-backing the broad risk appetite across the market, amid the slowing rate of COVID-19 cases/deaths coupled with reports of positive therapies and resumptions in Chinese operations. WTI Mar’20 futures reside north of USD 50.50/bbl with prices eyeing USD 51.00/bbl ahead of potential resistance at the USD 51.50/bbl mark, which coincides with the 7th Feb high. Brent Apr’20 futures came across mild resistance in early EU trade at USD 55.38/bbl (7th Feb high) ahead of further potential resistance around USD 55.55/bbl (6th Feb high). On the OPEC front, a definite OPEC+ meeting date remains in question, with desks noting that the longer we wait, the more likely that the meeting will take place in March as opposed to late-February. Russian Energy Minister Novak will today be meeting with domestic oil companies to discuss Moscow’s stance on deeper/prolonged output reductions. Elsewhere, yesterday’s APIs, which showed a larger-than-forecast build (+6mln vs. Exp. +3mln), did little to provide sustained pressure in prices as sentiment underpins the benchmarks – participants will be on the lookout to see if the weekly DoE numbers align with those of the API. Yesterday also saw the release of the EIA STEO ahead of today’s OPEC monthly oil report. The STEO cut 2020 oil demand growth by 310k BPD, downgraded US crude output forecasts and noted the uncertainty surrounding the virus outbreak, again little sustained reaction. Next up, OPEC’s monthly report will garner interest as this is the report that will encapsulate coronavirus forecasts as well as OPEC output since the December meeting. In terms of metals, spot gold trades lacklustre on either side of the 21 DMA (USD ~1566/oz), in-fitting with the current risk appetite. Copper prices remain supported by the risk tone but within yesterday’s ranges awaiting the next catalyst. Finally, Dalian iron ore futures hit three-week highs as coronavirus cases/deaths slowed and following a 22.4% YY drop in Vale’s Q4 iron ore production.

US Event Calendar

7am: MBA Mortgage Applications, prior 5.0%

2pm: Monthly Budget Statement, est. $10.0b deficit, prior $8.68b

DB’s Jim Reid concludes the overnight wrap

We’re jumping straight to the New Hampshire primary results this morning where, after 86% of the precincts reported, Sanders has been declared the winner with 25.8% of the vote, followed by Buttigieg in second with 24.4%, and then Klobuchar at 19.7%. Both Warren and Former Vice President Biden finished in a distant 4th and 5th at 9.3% and 8.4% respectively. In terms of the narrative and expectations, Klobuchar significantly outperformed her polls following a strong debate performance last Friday, with exit polls showing that roughly 50% of NH voters deciding in the last 3 days. Buttigieg also seems to have outperformed in a second straight state. Klobuchar’s outperformance may have come at the other Moderate’s expense – keeping Buttigieg from beating Sanders overall and keeping Biden under the 15% threshold to win proportional delegates. The Moderate wing of the primary continues to outperform the Left wing – Biden/Buttigieg/Klobuchar with 52.5 % and Sanders/Warren with 35.1% respectively – but it is not clear whether voters will jump between those groups. Biden left NH early in the day to start campaigning in South Carolina, indicating that the disappointing results in the first two states will not stop his primary campaign. It seems that we will not have the traditional winnowing seen after Iowa and New Hampshire, with all five major candidates moving on to Nevada and South Carolina. The field will likely only finally clear once over a third of delegates are awarded after Super Tuesday, but even then Former New York City Mayor Mike Bloomberg has already been campaigning in those delegate-rich states.

Prior to those results, the S&P 500 (+0.17%) and NASDAQ (+0.11%) posted another round of new record highs yesterday however it wasn’t without a bit of a pullback into the close. Indeed, the gloss was taken off after the Federal Trade Commission issued orders to Google, Apple, Facebook, Amazon and Microsoft to turn over a decade’s worth of information on past small acquisitions. That could provide insights into antitrust issues and the Commission noted could lead to enforcement action. Microsoft (-2.26%) and Facebook (-2.76%) were the biggest movers post the news.

Nevertheless, the moves yesterday still mean both indices have climbed on six out of the last seven sessions for cumulative gains of +4.07% and +5.33%% respectively. For the NASDAQ, the last time we had a better seven-day performance was October 2014. In credit US HY spreads were also 14bps tighter with the other micro story yesterday being the big rally across the Sprint complex following the announcement that T-Mobile had won court approval for its $26.5bn merger with the wireless company. For what it’s worth, Sprint is currently the second biggest issuer in the US HY index with around $20bn of bonds with the 2028 bonds as an example up around 18pts yesterday post the news.

As for bonds markets, they were comparatively less eventful with 10y Treasuries +3.1bps higher yesterday with a fairly muted reaction to the slew of Fedspeak – more on that shortly. The main measures of the yield curves were also little changed while in commodities it was a better day for oil with Brent and WTI pulling back from their one-year lows the previous day, up +1.39% and +0.75% (while being up a similar amount this morning and copper was up +1.27%.

A quick refresh of our screens shows that Asian markets are higher this morning too with the Nikkei (+0.54%), Hang Seng (+0.86%), Shanghai Comp (+0.39%) and Kospi (+0.61%) all advancing. In FX the big mover has been the New Zealand dollar which is up +0.84% after the RBNZ left rates on hold and forecasts showed no further rate cuts in this year. As for the latest on the coronavirus, the death toll in China now stands at 1,113 with confirmed cases at 44,653. Japan also found 39 new cases of the virus on the quarantined cruise ship bringing the total tally on-board to 174. Meanwhile, in an encouraging sign that the virus outbreak might be plateauing in China – Hubei province reported 1,638 additional cases overnight, the lowest daily level this month.

To be fair, there wasn’t a huge amount of news to report yesterday away from the New Hampshire results with central bankers providing most of the material. Fed Chair Powell was the main highlight as he testified before the House Financial Services Committee. In his opening statement, he referenced the coronavirus, saying that “we are closely monitoring the emergence of the coronavirus, which could lead to disruptions in China that spill over to the rest of the global economy.” However, in response to questions, he said that it was too early to say about the effects on the US. In his opening statement, Powell also said that “Putting the federal budget on a sustainable path when the economy is strong would help ensure that policymakers have the space to use fiscal policy to assist in stabilizing the economy during a downturn. A more sustainable federal budget could also support the economy’s growth over the long term.” You can read our piece last week (link here) on the latest huge increase in long-term debt projections from the CBO.

A number of Powell’s colleagues also spoke yesterday. Quarles supported the Fed’s continued purchasing of Treasury bills, while reiterating that it was important for the central bank’s balance sheet to shrink following a recession. Bullard addressed concerns with Coronavirus, saying that “previous viral outbreaks suggests that the effects on U.S. interest rates can be tangible and last until the outbreak is clearly contained. He explicitly pointed to the effects on the 10-year Treasury yield of other viral outbreaks, such as SARS, swine flu, avian flu, and Ebola. Bullard has been amongst the most dovish committee members – he was ahead of the curve last year in pushing for a shift to cutting rates – so it is notable that he is not pushing for a cut yet due to the virus. Kashkari also spoke later in the day on the need to possibly adjust monetary policy if the virus hits the country in scale, though he expressed uncertainty in its ability to contain it.

On the other side of the Atlantic, ECB President Lagarde was speaking before the European Parliament yesterday, where she said that “monetary policy cannot, and should not, be the only game in town. The longer our accommodative measures remain in place, the greater the risk that side effects will become more pronounced.” She also called for “a more complete EMU”, with banking union, capital markets union and a central stabilisation function to defend against shocks.

Away from all that and in terms of the data, the number of job openings in the US fell to a 2-year low of 6.423m in December (vs. 6.925m expected), which marked the first annual decline in the number of job openings since 2009. That said, the quits rate remained at 2.3% for the 4th consecutive month, while hirings rose for a second month running to 5.907m. Separately, data from the UK out yesterday showed GDP in Q4 was unchanged from the previous quarter, in line with expectations, while the monthly reading for December showed the economy grew by +0.3% (vs. +0.2% expected).

Staying on the UK, Brussels fired a warning shot ahead of the upcoming trade negotiations yesterday, with European Commission President Ursula von der Leyen saying that the “unique ambition in terms of access to the Single Market”, with a zero tariffs and zero quotas for trade in goods, would “require corresponding guarantees on fair competition and the protection of social, environmental and consumer standards.” So, the EU are sticking to the line that the level playing field is required for a trading relationship like this, even though Prime Minister Johnson explicitly said last week that there was “no need for a free trade agreement to involve accepting EU rules on competition policy, subsidies, social protection, the environment, or anything similar”. There was also some news on financial services, with chief negotiator Michal Barnier saying that “Certain people in the UK should not kid themselves about this: there will not be general, ongoing open-ended equivalence in financial services”.

To the day ahead, where we’ll hear from Fed Chair Powell once again as he appears before the Senate Banking Committee, while there’ll also be remarks from Philadelphia Fed President Harker and the ECB’s Chief Economist Lane. Data releases to look out for include the Euro Area’s industrial production for December, and from the US there’s the MBA’s weekly mortgage applications and the monthly budget statement for January. Finally, the Riksbank will be announcing their latest interest rate decision.