Trump Leads Biden At The Bookies Amid Surge In Black Americans’ Support Tyler Durden

Wed, 09/02/2020 – 07:45

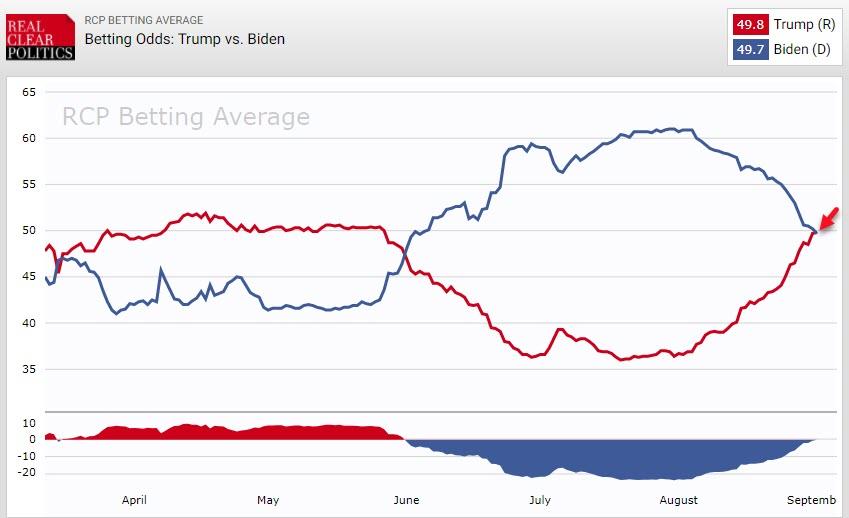

The trend we have been noting for the last week has accelerated overnight and ‘the streams have crossed’, with the average bookie now seeing it more likely that President Trump wins the 2020 election that Joe Biden.

This huge swing comes as Summit News’ Paul Joseph Watson notes that the results of a new national poll reveal that a stunning 28 per cent of black Americans plan on voting for President Donald Trump.

The Atlas Intel poll finds that Biden leads Trump nationally by just three points.

But the real story lies in the percentage of Hispanic and black voters who told the pollsters that they will vote for Trump.

According to the survey, 28 per cent of African-Americans say they plan to vote for Trump, a stunning figure.

Among Black Voters:

Biden 66% (-23 vs 2016 results)

Trump 28% (+20)

29 per cent of black Americans also approve of the job Donald Trump is doing.

This compares to 2016 when Trump attracted 8 per cent of the black vote while Hillary Clinton captured 89 per cent. Joe Biden is down to 66 per cent of the black vote, according to the poll.

Amongst Hispanics, Trump is up 13 points on the 2016 (41%), while Biden is down 10 per cent (56%).

The reason behind the surge in black support for Trump could be the fact that the Black Lives Matter movement seems to be backfiring after 3 straight months of violent riots and unrest.

As we highlighted earlier, a separate poll found that Trump’s support amongst African-Americans has doubled since 2016, although the results of the Atlas Intel poll blows even that figure out of the water.

Activist Candace Owens, who has led the ‘Blexit’ campaign to convince black Americans to get off the Democratic reservation, appears to have achieved a stunning success.

And finally, it appears Democrats may be preparing for just such a scenario, as a top Democratic data and analytics firm told “Axios on HBO” it’s highly likely that President Trump will appear to have won – potentially in a landslide – on election night, even if he ultimately loses when all the votes are counted.

“We are sounding an alarm and saying that this is a very real possibility, that the data is going to show on election night an incredible victory for Donald Trump,” Hawkfish CEO Josh Mendelsohn said.

“[but], when every legitimate vote is tallied and we get to that final day, which will be some day after Election Day, it will in fact show that what happened on election night was exactly that, a mirage.”

We suspect the social unrest will go to ’11’ should such an event occur.

via ZeroHedge News https://ift.tt/3hRmHmP Tyler Durden

“I don’t love the idea of being a house cat, but what’s the solution?”

When you are looking for someone to blame remember this: The Market is not stupid. Participants are.

When Fed heads and economists are warning of more pain still to come, when investors believe the US needs another $1 trillion stimulus, and the FTSE is worth less than Apple… you have to wonder what’s different? Perhaps the main reason stocks remain so insanely high is because there is absolutely nothing else worth chasing returns on…

Usually markets correct because something happens – like funds stopping redemptions in 2007 triggering a cascade effect that culminated in the collapse of Lehman. Maybe this time it will be an outbreak of un-common sense?

The market is the summation of all the multiple views and perceptions of each and every participant. If these views are stupid, perceptions are false, or participants believe in unicorns and whatever else they desperately want to pin their hopes to – don’t blame what’s going to happen on Mr Market. He/She/It doesn’t care. It only exists to help you realise your mistakes, and turn bad ideas into tangible losses.

A bubble market is one where the “whatever-you-want-to-believe” forces overcome well-grounded common sense, causing story stocks to head off on ballistic parabolas. (The clue to how it usually ends is in the words ballistic and parabola.) Even the few stocks that reach escape velocity and go into orbit – eventually see that orbit decay. That decays is due to the gravitational forces called obsolescence and competition. Practically no stock ever remains in the top 10 for more than a decade or two. Creative destruction ensures new firms are constantly emerging to meet consumer demand.

At some point even Apple will just be (once more), something that falls from a tree – although it does look like pent-up lockdown frustrations mean the new iPhone (perhaps later this month) will become the most eagerly desired product in consumer history!

Some story stocks get a boost from events.

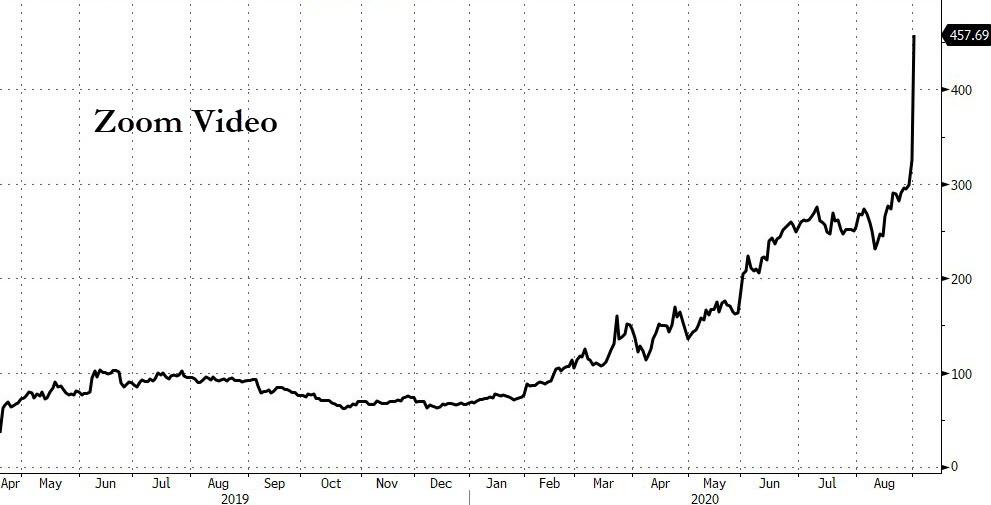

The current market darling is Zoom – profits up by 3300% on the back of the pandemic. It’s achieved the remarkable accolade of becoming the verb for video-meetings – which gives it an incredible leg-up versus its many rival video-conferencing apps. Zoom was a cottage industry a year ago – making a $5mm profit. It made $186 mm in the last 3 months – and, yes, $186mm might seem a little insignificant to justify a $125 bln market cap – but relax… its Zoom. It’s so now… But I don’t know what it will be worth tomorrow.

As far as I can make out the reason Zoom made any profit is companies signing off employee expenses to pay for the pro-version, which you need for a meeting longer than 45 mins. Being a thrifty Scotsman, I wondered about this – and since we already have Teams why pay for another similar video service.. Sure.. there were arguments about quality vs security, and Zoom is easy to use while Teams is frankly a pain in the bottom.

Zoom is not a bad company. Lucky and in the right place at the right time. If the virus has not accelerated adoption of WFH and video-conferencing, I dare say it would have struggled on not making any decent money for years and either vanish or join so many other tech companies we never really heard of.

Other Tech firms do have stories to beguile us with – none more so than Tesla. When Elon tweeted his stock-price was too high a few weeks ago… well now we know what he meant. The stock split was a brilliant idea – enabling his legions of Robinhood fanboys to buy into the suddenly much cheaper 5 for 1 price. Brilliant. The fanboys get the opportunity to own less of the firm for more! And to facilitate them, Tesla quietly raised $5 bln via a new stock sale! The market didn’t even blink.

Of course, daring to criticise Telsa is a dangerous thing. Some 25 year-old self-declared Market Genius will post a video rant demonstrating with dodgy charts why Tesla will rule the world and tell the world what an idiot I am. He will focus on my call last year to sell. YEP. I GOT THAT WRONG. As did many short-sellers. As has been said before, the market can remain irrational longer than you can stay solvent.

Mea Culpa. Tesla is likely to survive. It’s unlikely to implode. They are making good cars that people are buying. I just wonder what its’ really worth. I still don’t buy the Tesla narrative.

Reading the through the posts on a recent negative article on Tesla, the author was taking lots of predictable flack, this time about the Tesla Battery Day on September 22nd. All the posts said the same thing – battery day means one thing: the stock is going even higher.

I’m intrigued – so I tried to find out what could Tesla possibly announce in terms of Battery Tech which will greatly increase profits and push them even further ahead of the competition in terms of Electric Vehicles.

Turns out there are a lot of possible things for Tesla to brag about on Battery Day. Apparently, Elon is going to do a Steve Jobs on speed presentation that will stun everyone into a buying frenzy. Tesla might be close to being able to lighten batteries and increase their power per kilogram, thus enhancing the range. They may be close to a 1 million mile battery that wont need replacing. They may be planning a Terafactory, 28 times the size and productive capacity of the current giga-factories. They might be doing something clever with silicon annodes. And they might be making enhancements on the cost per battery that will significantly improve the bottom line and margins per car.

These all sound like great steps forward – but they are improvements rather than invention or innovation. They sound laudable and fascinating tech projects – but will they justify Tesla’s 2% of the total global auto market being worth 40+% of the sector’s total market cap? Global auto profits were $105 bln last year. Let’s say Tesla made $1 bln profits (which it didn’t), which would suggest it would to sell some 20 mm cars to justify its 40% of total market cap. Let’s half that number to account for Tesla’s exceptionalism – like self-driving, the earnings potential of each car as self-driving taxis and other stuff that’s apparently unique to the EV-maker.

Or you could argue Tesla has 19% (let’s call it 20%) of the EV market, and the EV market will be 40% of total sales.. which is 28 million cars, meaning Tesla still has to massively increase production to 6 mm to start to justify its premium. But let’s not worry about that…

The reality is you are entitled to believe or think whatever you like about Tesla – the summation of the market is that it’s the most valuable auto-company and is going higher. Jolly good. Enjoy the ride.

I’m going to wait. I suspect Battery Day is yet more Tesla Hype.

I’ll stick to the perspective that Tesla’s battery secret-sauce is basically evolved 50 year old Lithium Ion tech that’s vulnerable to future alternatives like the hydrogen economy (not just fuel cells) and entirely new battery-tech like Carbon-Ion. I’ll discount the proposed/imagined Tera-factory on the basis it will need about 300% of current lithium supply to reach its production goals. Or that lithium is a mined in terrible conditions, is difficult to recycle and it’s a major threat to the environment, while Carbon-ion is clean, doesn’t require child labour to mine, and is easily recycled, and a clean hydrogen economy is the logical next step in renewable power replacement of fossil fuels.

And I will remain unconvinced that all the trillions of miles of data that Tesla has acquired from every car its ever built means it is about to make every Tesla a high-earning self-drive taxi-asset for owners, or that it’s about to enable fully autonomous driving.

These things will all come tomorrow, or more likely the day after a tomorrow that never comes.

Of course, it’s not just equites that are irrational.

Take the bond market. European bonds are having a blistering September open. I read a report yesterday about tightening secondary spreads and solid demand for new bonds – stronger sentiment and technical factors is apparently driving investors into European bank subordinated paper. Are these people daft? When the crunch comes and companies start defaulting – what will be the first asset class to struggle on the expectation of rising Bank NPLs?

I will definitely buy bank paper – at some point. That’s after the crunch has happened, prices have cratered, and the moment of maximum fear has been reached as everyone expects multiple Lehman events across the continent. At that point I will buy cheap European bank subordinated paper in the sure and certain knowledge the ECB will be forced into one its oh-so-many “do-whatever-it-takes” moments to avoid the banking crisis that might make Europe’s dismal economic outlook even worse.

I won’t be buying banks or corporate subordinated paper at today’s levels – not when spreads are this stupidly incredibly tight, and non-reflective of the underlying risk. Not that I would be able to anyway – there simply isn’t a functional secondary bond market anymore. One deal that is worth mentioning is 10.25% on a new Finnair deal – it steps up to 15.25% if it’s not called. It illustrates just how much pandemic ravaged sectors have to pay. Yet near junk (and generally detested by its customers) BBB rated Vodafone can raise 10-year money at 3%.

Now, I must dash so I can read this prospectus about financing a cheese mining project on the moon. It looks a brilliant idea…. I’m surprised Musk isn’t all over it…

via ZeroHedge News https://ift.tt/3lGHtI7 Tyler Durden

“Demand Is Insane”: NYC Movers Turn People Away, Suburban & Rural Housing Snagged Up, As Big City COVID-Exodus Accelerates Tyler Durden

Wed, 09/02/2020 – 06:50

The pandemic-induced summer of escape from New York continues at a moment violent crime is on the rise, restaurant and public venue closures make the city less appealing, public transit is reeling in debt, and remote working set-ups are giving those with means greater mobility.

More worrisome trends… or rather signs of the times signalling that for many the gentrified Big Apple has as one family recently put it reached its “expiration date”. Two separate NY Times reports on Sunday detailed that moving companies are so busy they’re in an unprecedented situation of having to turn people away, while simultaneously the suburbs are witnessing an explosion in demand “unlike any in recent memory”.

Getty Images

And then there’s fresh data showing that during the pandemic Americans are fast getting the hell out of the more expensive “real estate meccas” of New York and New Jersey.

According to FlatRate Moving, the number of moves it has done has increased more than 46 percent between March 15 and August 15, compared with the same period last year. The number of those moving outside of New York City is up 50 percent — including a nearly 232 percent increase to Dutchess County and 116 percent increase to Ulster County in the Hudson Valley.

“The first day we could move, we left,” a dentist was cited as saying of the moment movers were declared an “essential service” by Gov. Cuomo late March. Her family moved to Pennsylvania where they had relatives.

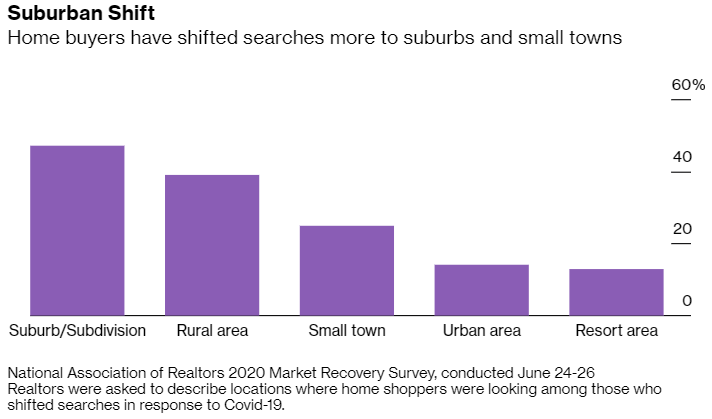

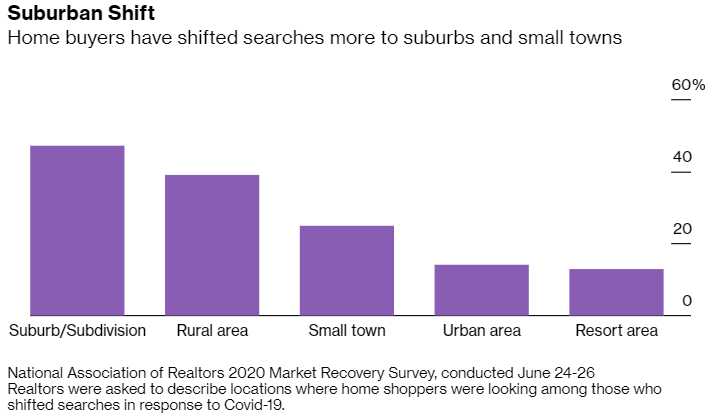

And second, the Times details the unprecedented boom in the suburban real estate as an increasingly online workforce is fed up with closures in the city, losing its appeal and vibrancy.

National trends via Bloomberg

July alone witnessed a whopping 44% increase in home sales among suburban counties near NYC compared to the same month last year, as the report details:

Over three days in late July, a three-bedroom house in East Orange, N.J., was listed for sale for $285,000, had 97 showings, received 24 offers and went under contract for 21 percent over that price.

On Long Island, six people made offers on a $499,000 house in Valley Stream without seeing it in person after it was shown on a Facebook Live video. In the Hudson Valley, a nearly three-acre property with a pool listed for $985,000 received four all-cash bids within a day of having 14 showings.

Since the pandemic began, the suburbs around New York City, from New Jersey to Westchester County to Connecticut to Long Island, have been experiencing enormous demand for homes of all prices, a surge that is unlike any in recent memory, according to officials, real estate agents and residents.

They’re not just fleeing for the suburbs or upstate, but also to the significantly cheaper and lower cost of living areas of the country like Texas, Florida, South Carolina, and Oregon, or to rural areas.

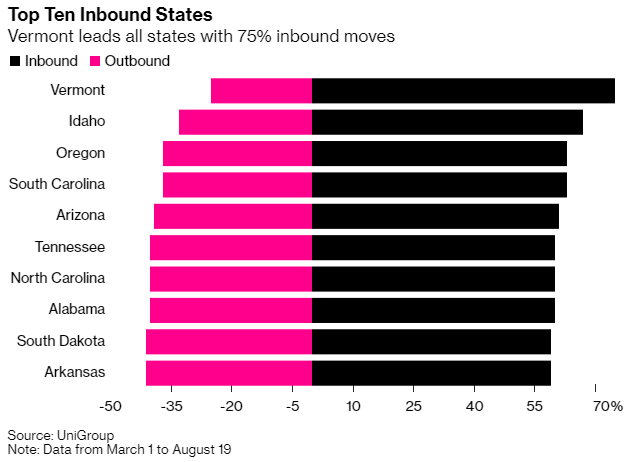

COVID-19 is fast reviving American mobility on scales reminiscent of the mid-20th century. Bloomberg describes separately that“Far more people moved to Vermont, Idaho, Oregon and South Carolina than left during the pandemic, according to data provided to Bloomberg News by United Van Lines.”

Two charts via Bloomberg:

“On the other hand, the reverse was true for New York and New Jersey, which saw residents moving to Florida, Texas and other Sunbelt states between March and July,” the report finds.

General fear of living in densely populated areas, better enterprise video communications platforms making possible fully remote workplaces which in some cases are ‘canceling’ the traditional office space altogether, and a lack of nightlife or entertainment allure of big cities is driving the exodus.

In addition to the aforementioned states, “Illinois, Connecticut and California, three other states with big urban populations, were also among those losing out during the pandemic,” according to United Van Lines data.

via ZeroHedge News https://ift.tt/2Gneysr Tyler Durden

“Does money buy happiness?” asked economist Richard Easterlin in a famous 1973 essay in The Public Interest. His conclusion was that once a certain level of economic development had been achieved, greater wealth and income did not lead to greater overall happiness. At an aggregate level, more money does not buy more happiness, he claimed.

A new study in the journal Emotion presents a challenge to the Easterlin finding. Jean Twenge, a psychologist at San Diego State University, and A. Bell Cooper, a data scientist at Lynn University, examined data collected from 44,000 adult respondents to the General Social Survey (GSS) between 1972 and 2016 and found that more money does, in fact, correlate with more happiness.

The survey asks respondents to report their happiness on a three-point scale: “Taken all together, how would you say things are these days—would you say that you are very happy, pretty happy, or not too happy?” The researchers then parsed the data by income deciles, reporting that “twenty-one percent of those in the lowest decile described themselves as ‘very happy’ compared with 45 percent of those in the top decile; thus, those at the top of the income scale were more than twice as likely to be very happy than those at the bottom.”

Others have challenged Easterlin before. In 2012, Daniel Sacks of the University of Pennsylvania and Betsey Stevenson and Justin Wolfers of the University of Michigan published an analysis in Emotion finding that richer people are happier than poorer people within individual countries and that people in richer countries are happier than people in poorer countries. Over time, they found, increased economic growth leads to increased happiness. “The data show no evidence for a satiation point above which income and well-being are no longer related,” the trio concluded.

Nevertheless, Easterlin and other scholars continue to argue that the “Easterlin Paradox” is real. Some cite 2010 research in the Proceedings of the National Academy of Sciences by Princeton economist and Nobelist Angus Deaton and his colleagues that supposedly found happiness does not increase once an individual’s income reaches about $75,000 per year. What the study actually found is that more money does not affect the level of day-to-day joy, stress, and sadness but does correlate strongly with rising measures of overall life satisfaction.

The American editor Beatrice Kaufman once declared, “I’ve been poor and I’ve been rich. Rich is better.” It turns out that she was right.

from Latest – Reason.com https://ift.tt/3bi1HDj

via IFTTT

“Does money buy happiness?” asked economist Richard Easterlin in a famous 1973 essay in The Public Interest. His conclusion was that once a certain level of economic development had been achieved, greater wealth and income did not lead to greater overall happiness. At an aggregate level, more money does not buy more happiness, he claimed.

A new study in the journal Emotion presents a challenge to the Easterlin finding. Jean Twenge, a psychologist at San Diego State University, and A. Bell Cooper, a data scientist at Lynn University, examined data collected from 44,000 adult respondents to the General Social Survey (GSS) between 1972 and 2016 and found that more money does, in fact, correlate with more happiness.

The survey asks respondents to report their happiness on a three-point scale: “Taken all together, how would you say things are these days—would you say that you are very happy, pretty happy, or not too happy?” The researchers then parsed the data by income deciles, reporting that “twenty-one percent of those in the lowest decile described themselves as ‘very happy’ compared with 45 percent of those in the top decile; thus, those at the top of the income scale were more than twice as likely to be very happy than those at the bottom.”

Others have challenged Easterlin before. In 2012, Daniel Sacks of the University of Pennsylvania and Betsey Stevenson and Justin Wolfers of the University of Michigan published an analysis in Emotion finding that richer people are happier than poorer people within individual countries and that people in richer countries are happier than people in poorer countries. Over time, they found, increased economic growth leads to increased happiness. “The data show no evidence for a satiation point above which income and well-being are no longer related,” the trio concluded.

Nevertheless, Easterlin and other scholars continue to argue that the “Easterlin Paradox” is real. Some cite 2010 research in the Proceedings of the National Academy of Sciences by Princeton economist and Nobelist Angus Deaton and his colleagues that supposedly found happiness does not increase once an individual’s income reaches about $75,000 per year. What the study actually found is that more money does not affect the level of day-to-day joy, stress, and sadness but does correlate strongly with rising measures of overall life satisfaction.

The American editor Beatrice Kaufman once declared, “I’ve been poor and I’ve been rich. Rich is better.” It turns out that she was right.

from Latest – Reason.com https://ift.tt/3bi1HDj

via IFTTT

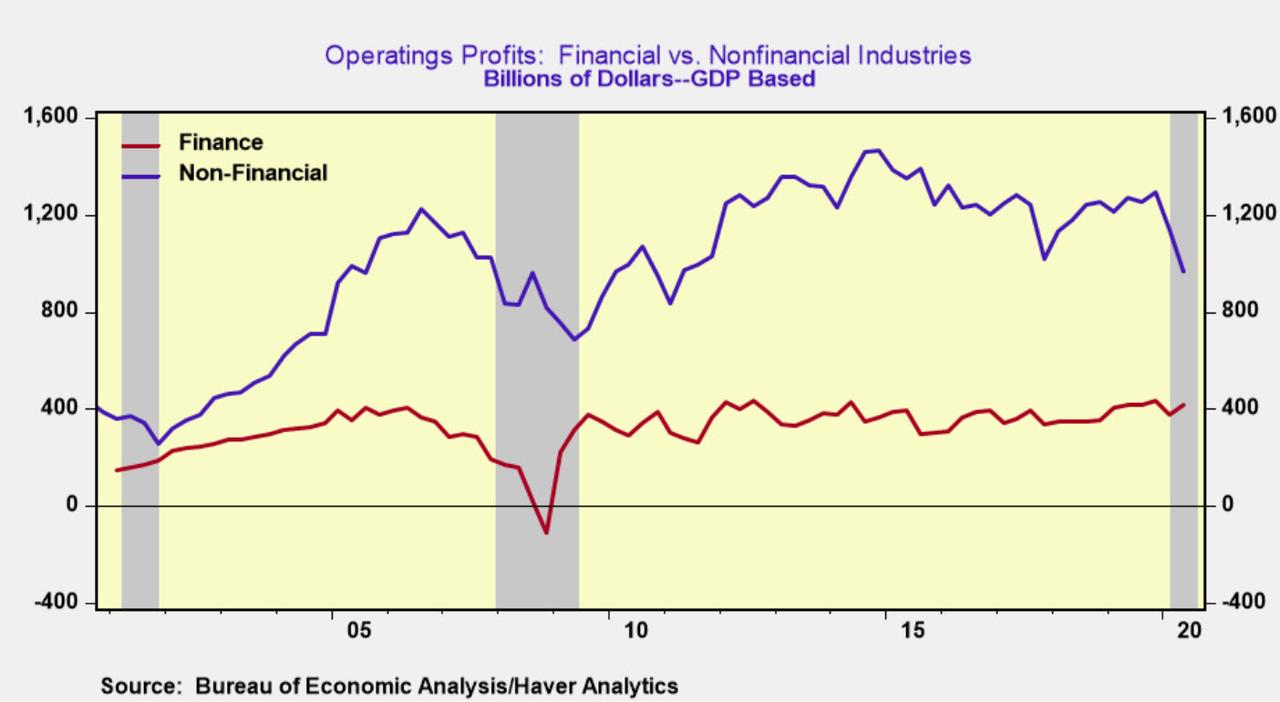

2020 Plunge In Operating Profits Mirrors 2008: Different Mix Shows The Need For More Fiscal Support Tyler Durden

Wed, 09/02/2020 – 06:20

Submitted by Joseph Carson, former chief economist at AllianceBernstein

The sharp drop in operating profits in 2020 mirrors the decline of 2008. But the mix of profits is markedly different, with the bulk of the decline centered in non-financial industries. The crisis of 2020 is centered more so in the general economy unlike the financial/banking crisis of 2008. That means the policy response requires more fiscal stimulus than monetary ease.

Painting By The Numbers

In Q2, the GDP measure of operating profits showed a decline of 11% and that comes on the heels of a 12% drop in Q1. The two-quarter decline of 23% nearly matches the 25% decline in operating profits in Q4 2008 during the Great Financial Recession.

But there are two key differences; first, the 2020 occurred over two quarters, while the decline in 2008 occurred in one; and second, the 2020 decline is almost entirely concentrated in non-financial companies while finance accounted for the bulk of the decline in 2008.

S&P 500 companies operating profits show a bigger decline, a different quarterly pattern, but a similar mix. According to the data compiled by S&P, operating profits for the largest companies declined 33% over the past two quarters. But the decline was concentrated in Q1, dropping 50% from the Q4 levels, while Q2 profits showed a gain of 36% over Q1.

The detailed industry profit data from S&P shows that the big turnaround from Q1 to Q2 is centered in finance. The financial sector lost money in Q1 but posted an increase in Q2. The GDP profit data also shows operating profits in finance rebounded sharply in Q2, rising 11%.

Trading gains and losses are considered part of S&P operating profits, but not in the GDP measure of operating profits. But the financial sector posted gains under both accounting frameworks. So trading gains are not the primary reason for the Q2 rebound in profits in finance.

The 25% decline in non-financial industries operating profits over the past two quarters is much more severe than the 15% drop in Q4 2008. Industry details from S&P show the weakest performers are energy, consumer discretionary, and industrials. Detailed non-financial industry data from GDP are not yet available.

The GDP data does show that the aggregate level of operating profits for non-financial companies stood at $966 billion in Q2. That’s a decline of $330 billion from Q4 2019 and represents the lowest level of operating profits since 2011. Real profit margins for non-financial companies are estimated at 10.5%, the lowest level since 2009.

At mid-year 2020, non-financial firms employ nearly 10 million more workers compared to 2011. But that’s after they have already shed more than 10 million workers since the start of the year.

Reports that previously laid-off workers are being told that they will not be rehired should not come as a surprise. Many firms don’t have the level of profitability to support re-hiring. Lack of confidence in the future trends in business conditions also plays a role as the pandemic continues to disrupt businesses as does the on-and-off-again support from governmental policies.

Congress appropriated more than $3 trillion in fiscal stimulus, a record amount, to people and businesses. But that federal support abruptly ended on July 31st when Congress and the White House could not agree on a second round of stimulus. Failure to extend federal stimulus payments removes at least $750 billion a month from what people were seeing in terms of cash flow in Q2.

Equity investors have been betting that the combination of monetary ease and fiscal stimulus will build a strong and long bridge to keep the economy running until a vaccine is medically approved. With broad equity averages at record highs, the bulls have won the argument for now.

But what happens as the fiscal well runs dry, companies are operating with record debt levels and the monetary spigot is not pouring out liquidity, as fast as it was a few months back?

Cracks in the bull case are quickly starting to emerge. The consumer confidence index for August dropped 7 points to 84.8. That’s a new low for 2020, reversing the federal stimulus-related gains of the prior three months.

People’s assessment of labor markets turned sharply negative, consistent with the million-plus jobless claims being filed week after week. People are also expressed concern about their financial well being at the same time the S&P 500 hit a new record high.

The equity market is not the economy, but the direction of the economy will ultimately determine if the equity market can maintain the lofty levels for the simple reason investors are banking on better news in corporate earnings.

But without a new round of fiscal stimulus, it’s hard to see how corporate earnings can meet bullish investor optimism.

via ZeroHedge News https://ift.tt/32KDK3D Tyler Durden

”It Happened So Fast” – Baltimore Man Smashed By Brick, Disturbing Video Shows Tyler Durden

Wed, 09/02/2020 – 05:50

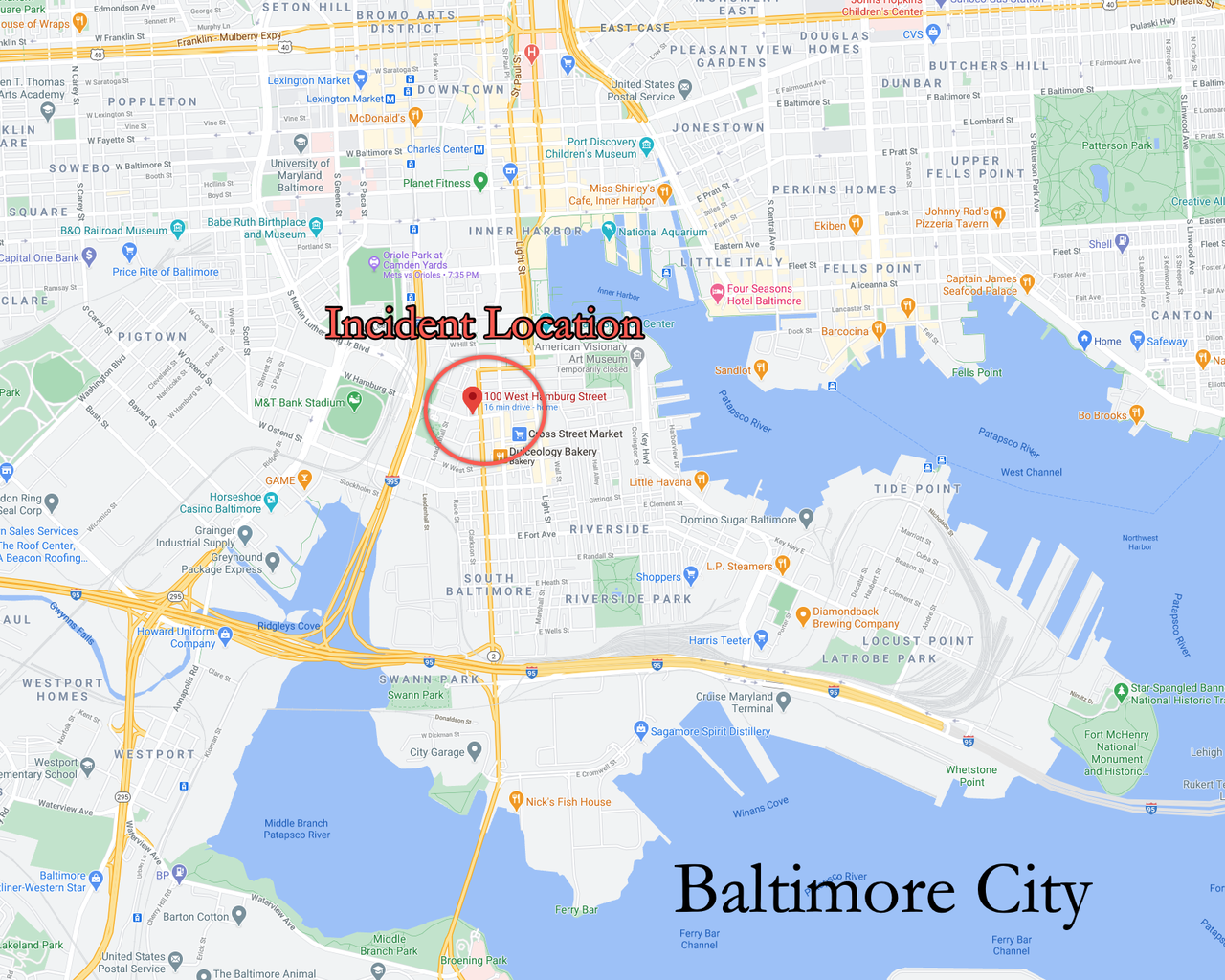

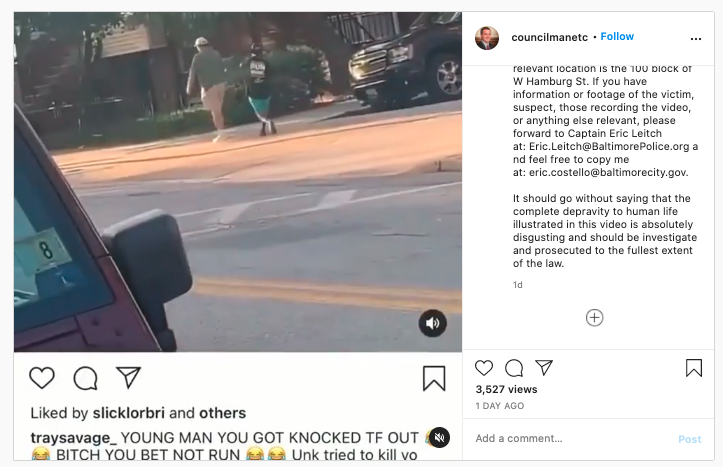

A disturbing video has surfaced on social media showing a man striking another unsuspecting man with an apparent brick in Baltimore City.

The short video shows a man running up with a brick in hand and then smashing it over the head of an older white man on Sunday afternoon around the 100 block of West Hamburg Street in South Baltimore.

While the video shows the suspect blindsided the victim, Fox News said the assault occurred after both men were involved in a “loud argument.”

Officers arrived on the scene around 6:40 p.m. Sunday to Hamburg Street and found a “pool of blood” on the sidewalk where the victim laid on the ground for several minutes.

“It happened so fast,” one witness, who did not want to be identified, told CBS WJZ. “When I saw him running, I thought he was running to talk to the guy.”

Baltimore City Councilman Eric Costello condemned the “disgusting” attack in an Instagram post:

“It should go without saying that the complete depravity to human life illustrated in this video is disgusting and should be investigated and prosecuted to the fullest extent of the law,” Costello wrote.

The councilman repeated those comments with WJZ on Monday.

“It’s a depraved act, it’s disgusting,” he said.

Police have yet to identify the suspect or the victim. Still, the video lends credibility to President Trump’s claim that Democratically-controlled cities, like Baltimore, are lawlessness areas full of violent crime.

via ZeroHedge News https://ift.tt/34Vmzip Tyler Durden

The cracking sound of ice breaking in the frozen US-China relationship is audible with the two big powers holding a high-level “virtual meeting” last week to discuss trade and related issues. In spite of everything, the US and China are finally talking.

The backdrop is that in the so-called phase I of their trade pact, signed in January, which was aimed to bring to an end the US-China trade war that began in 2018, Beijing had agreed to purchase record levels of American products in 2020 and 2021 in exchange for the US cutting trade war tariffs.

But halfway through 2020, largely due to the pandemic, the pace of China’s purchases is behind where it should be. It fuelled speculation that the agreement was at risk of falling apart. The focus at today’s meeting was to review progress, but “other topics” also, inevitably, figured in the discussion.

The meeting took place at the initiative of the American side. It was originally slated for August 15 but Trump delayed the talks, presumably with an eye on the Democratic and Republican party conventions where perceptions mattered.

China fielded its economic czar, Vice Premier Liu He (who is also a member of the Politburo of CCP Central Committee) while the US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin (both cabinet rank) participated from the American side.

The talks mark a rare moment of cooperation between the two powers. After the talks, officials on both sides sought to assure the public—and the markets—that phase 1 is on track. The Chinese media reported that it was a “constructive dialogue on how to strengthen bilateral coordination on macroeconomic policies, and on implementation of the phase one economic and trade agreement.”

Importantly, “The two sides also agreed to create conditions and an atmosphere conducive to pushing forward the implementation of the trade deal.” The US readout also said “Both sides see progress and are committed to taking the steps necessary to ensure the success of the agreement.”

“The parties addressed steps that China has taken to effectuate structural changes called for by the Agreement that will ensure greater protection for intellectual property rights, remove impediments to American companies in the areas of financial services and agriculture, and eliminate forced technology transfer. The parties also discussed the significant increases in purchases of U.S. products by China as well as future actions needed to implement the agreement.”

The Chinese experts have interpreted that “the subtext of both sides agreeing to foster an atmosphere conducive to the implementation of the trade deal could be positive news for Huawei, which is currently under attack from the Trump administration.”

Indeed, American microchip companies have been badly hit too, as Huawei has been their biggest customer by far, importing tens of billions of dollars worth microchips annually.

Conceivably, the Trump administration’s easing of its earlier order banning Huawei from buying microchips from US companies comes as China ramps up imports of US agricultural and energy products from the US. To be sure, there is growing pressure from US farm and energy lobbies on the US administration, which are important for Trump’s campaign in the November election.

Trump is facing a tough reelection campaign as the election is only three months away amid the raging pandemic and a historic decline in GDP, which largely explains his intensifying multifaceted campaign against China. However, the meeting on Tuesday underscores the continued importance of trade and economic relations in the overall matrix.

All through the recent turbulent period in the relationship, Beijing has remained unwaveringly committed to ensuring the stability of China-US economic and trade relationship. The pandemic slowed down China’s purchase of US products but China has nonetheless acted on all of the 50 items it was expected to work on through the first four months of implementation of the trade deal.

China has continued to buy American commodities, such as agricultural products. Interestingly, notwithstanding the Trump administration’s bullying of TikTok, Beijing is opening up the Chinese market for American companies, especially financial companies.

The US oil exporters say they are readying to send a record level of crude exports to China in September, and USagricultural officials say that agricultural exports to China have been on the rise in the last few weeks.

The plain truth is that, as a recent paper by the Peterson Institute for International Economics estimates, “US-China financial decoupling is not happening.” In July, a survey by the American Chamber of Commerce in China showed that 84 percent of US enterprises are unwilling to withdraw from China, and 38 percent of them will maintain or increase their investment in China. Of course, Chinese companies have also remained very eager to increase their investments in the US.

China’s balancing of the relationship with the US through a period of exceptionally high tensions is proving to be successful. Basically, it stuck to the maxim that diplomacy is the “art of possibility” and kept doggedly working to reduce and avoid conflict and confrontation, while at the same time seeking to achieve with constructive and rational tools its strategic missions, which in this case is about the country’s peaceful development and sustainable growth. Suffice to say, the rationality of China’s goals and methods stands out as exceptional.

China clinically analysed that the criticality of the present moment is to be attributed to a large extent to the overlapping of Trump’s desperate need to get re-elected for a second term with the China hawks’ agenda to advance moves to suppress China, while, the political reality is also that the US is not solidly united as a single behemoth.

Therefore, China didn’t fall into the trap of “tit-for-tat” measures in the face of Trump’s (rather, state secretary Mike Pompeo’s) strident anti-China campaign. Instead, it showed restraint while holding its ground where resolute responses were needed.

Certainly, from Beijing’s perspective, it also helped that the Trump administration’s hysteria over China eventually backfired within the US and also abroad, with hardly any support for the hype of a new cold war in the international community.

And, most important, there is a paradigm shift insofar as the Chinese economy is back on a sustainable growth trajectory. And that hasn’t gone unnoticed in the US, which is itself in a deep recession amidst a raging pandemic.

Maintaining cooperation with the US amid this current strategic competition poses a huge challenge for China, but the leadership’s long-term vision for the country’s development demands that the all-important relationship with the US should not be hijacked by the “China hawks” and right-wing forces in the US whose agenda is to drag China into a new cold war. That strategy is working.

Last week’s talks represented a rare friendly encounter between the US and China — perhaps, the first of its kind — in months and, shortly after the news broke, markets worldwide signalled relief. The talks signal the recognition by both Washington and Beijing that the trade deal is the glue that is holding the relationship together in a period when other channels of communication aren’t working well.

via ZeroHedge News https://ift.tt/31NNtXz Tyler Durden

{kind=link}

{kind=link}