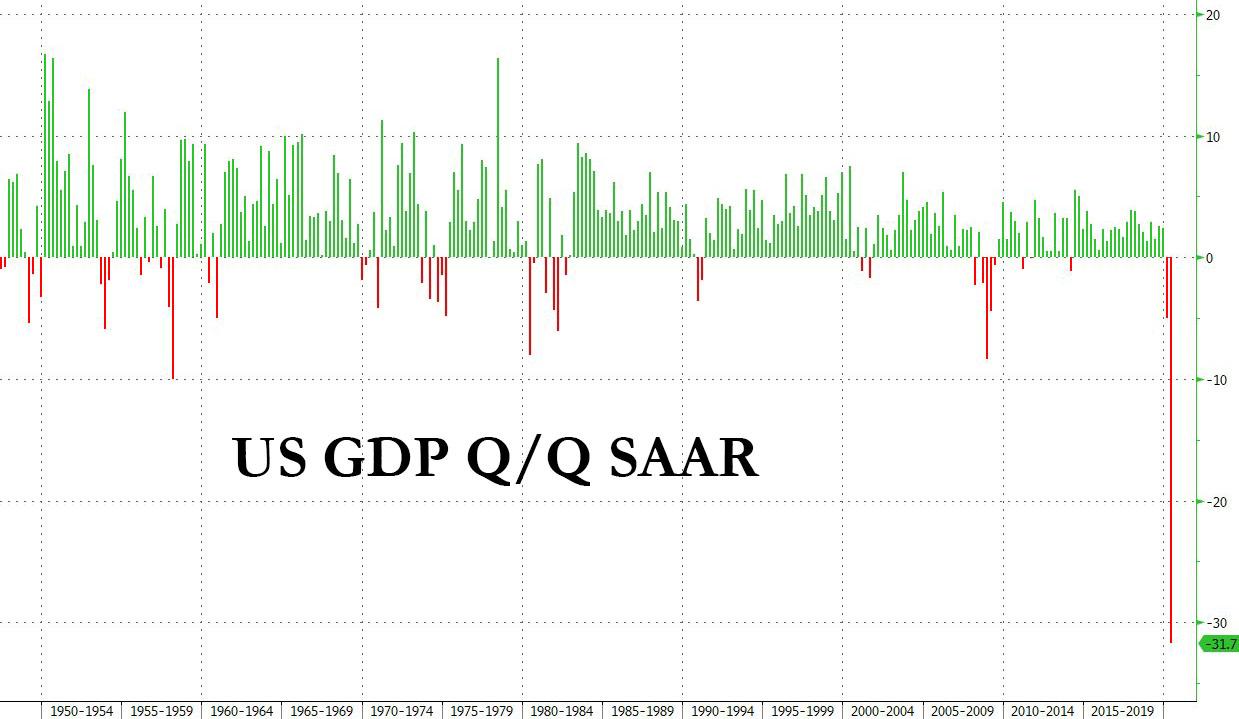

Record GDP Plunge Revised Slightly Higher: US Economy Contracted 31.7% In Q2 Tyler Durden

Thu, 08/27/2020 – 08:35

One month after the worst ever GDP print in US history revealed that in the 2nd quarter the US economy contracted by -32.9%, moments ago the BEA unveiled in its first revision of GDP that the slowdown was just modestly better than expected, coming in at -31.7%, beating expectations of a -32.5% number.

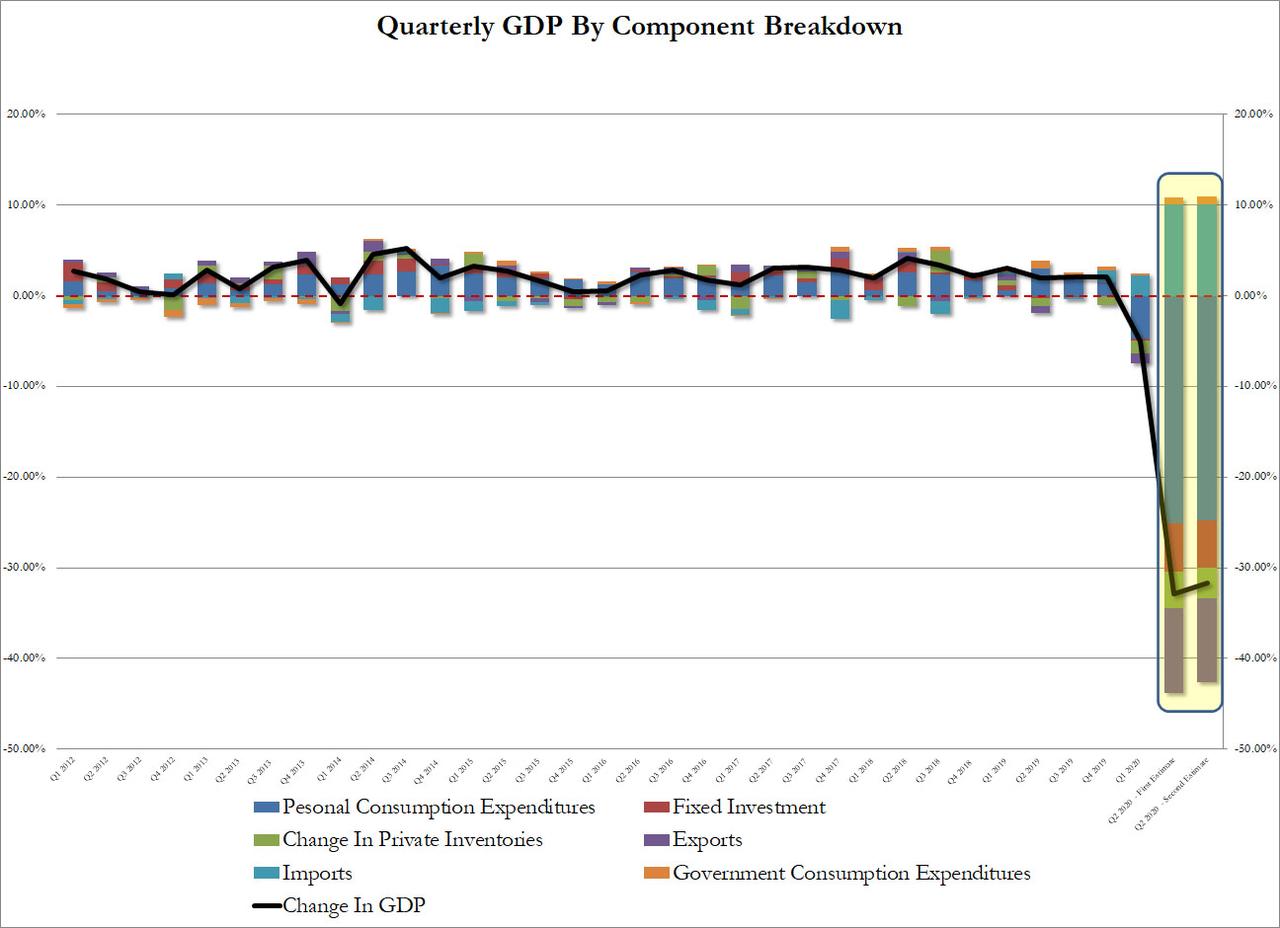

The decrease in real GDP reflected decreases in consumer spending, exports, business investment, inventory investment, and housing investment that were partially offset by an increase in government spending. Imports, a subtraction in the calculation of GDP, decreased.

The decrease in consumer spending reflected a decrease in services (led by health care) and goods (led by clothing and footwear). The decrease in exports primarily reflected a decrease in goods (led by capital goods). The decrease in business investment primarily reflected a decrease in equipment (led by transportation equipment). The decrease in inventory investment primarily reflected a decrease in retail (led by motor vehicle dealers). The decrease in residential investment primarily reflected a decrease in new single-family housing. The increase in government spending reflected an increase in federal spending related to payments made to banks for processing and administering the Paycheck Protection Program loan applications.

Looking at the 1.2% improvement in the GDP estimate from the original print, it was the result of an increase in government spending reflected an increase in federal spending related to payments made to banks for processing and administering the Paycheck Protection Program loan applications.

Some details:

the decline in personal consumption was revised higher from -25.05% to -24.76%

the decline in fixed investment was revised from -5.38% to -5.20%; Nonresidential fixed investment, or spending on equipment, structures and intellectual property fell 26% in 2Q

the decline in change in private inventories was revised from -3.98% to -3.46%

the boost from net trade was revised from 0.68% to 0.90%

the contribution from government was unchanged at 0.82%

For those keeping tables on inflation, the GDP price index fell 2% in 2Q after rising 1.4% prior quarter; core PCE q/q fell -1% in 2Q after rising 1.6% prior quarter.

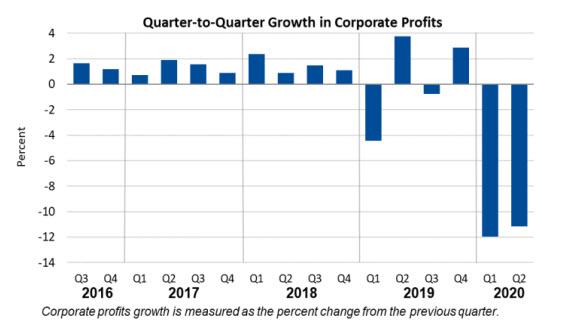

In the first look at corporate profits, the BEA calculates that profits from current production decreased 11.1% at a quarterly rate

in the second quarter after decreasing 12.0% in the first quarter. Corporate profits decreased 20.1% in the second quarter from one year ago.

Profits of domestic non-financial corporations decreased 15.0 percent after decreasing 14.4 percent.Profits of domestic financial corporations increased 9.2 percent after decreasing 8.9 percent. Profits from the rest of the world decreased 20.3 percent after decreasing 8.4 percent.

Overall, while still historic, the GDP number was largely expected within a margin of error, and the question is how far does GDP rebound in the all to key third quarter, the first look of which we will get just days before the presidential election on Nov 3.

via ZeroHedge News https://ift.tt/2G3WS51 Tyler Durden

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/3hzp4up

via IFTTT

Please feel free to write comments on this post on whatever topic you like! (As usual, please avoid personal insults of each other, vulgarities aimed at each other or at third parties, or other things that are likely to poison the discussion.)

from Latest – Reason.com https://ift.tt/3hzp4up

via IFTTT

“No man can taste the fruits of autumn while he is still delighting his scent with the flowers of spring.”

Stock markets continue to grind higher. Why? There are reasons to be cheerful – global earnings haven’t been a bleak as feared, economies are posting some stronger than expected numbers, and the absolute numbers around the pandemic are improving in terms of better outcomes and fewer deaths. There are even a few analysts claiming we’re still headed towards a V-Shaped Recovery – although it won’t now be until mid 2021 – which sounds pretty much their best-case scenario is one year missing from Global Growth.

And that’s the best case?

Most Porridge readers think I’m some kind of Uber-Bear, a Casandra-like misery-guts always warning of impending doom and gloom. Nope. I’m a happy glass-half-full optimist. I believe things are never as bad as you fear – although they seldom turn out as good as you hope.

But, I am getting concerned… This August has been a miserable end to the summer. The massive storm Laura has just hit the US. I have gut-feel the financial weather is heading for a deep low – I have a feeling late-October/early-November is likely to be when a reckoning hits markets…

The enormous efforts to sustain, stimulate, preserve and maintain global economies via furloughs, bailouts and rescues are running out of runway. As markets get fretful about the costs and soaring sovereign debt, the Torygraph puts it rather well as it warns of a brutal autumn as mortgage holidays and furloughs schemes end as massive waves of job losses hit. 2 million Brits are taking a mortgage break and nearly 10 million were furloughed. These people and jobs hit reality in a few weeks time.

And that’s just the UK. The Italian’s say the effective loss of 11% of their economy due to the zero-tourist season is accelerating their descent into madness insolvency. The Chinese claim they’ve recovered, but the anecdotal evidence of job losses and a hard hit working class suggest otherwise. And, lest we forget, there is still the virus – although it sounds like the threat of a devasting second autumn/winter wave is receding.

We all know the soaring stock market looks utterly disconnected from the grim reality of the real economic damage that’s already done. Deep down we all know the rally is nothing to do with improving fundamentals, but is driven by the effectiveness of Central Bank QE Infinity (which will be reinforced later today as the Fed promises lower rates for longer through inflation averaging).

We know ultra-low bond yields force investors to seek higher returns by taking greater risk in stocks.

All that central bank liquidity and rate repression is starving the markets of the oxygen of common sense – hence the current hypoxic euphoria.

It can’t last forever. Wake up, take a deep breath and glug a strong coffee..

There is a lot to worry about.

Just how vulnerable are markets? Thus far their conviction in the ability of central banks to maintain liquidity and thus the upside has gone unchallenged. It’s been supported by the stronger than expected economic releases, and the swift evolution of the global economy in terms of working-from-home, internet deliveries and new tech. Thus far, the gains from sectors having a good crisis have covered for the losses in sectors hit hard by pandemic.

That cosy sentiment could easily be shaken.

I am particularly concerned about what’s occurring in the US. The degree of polarisation across the economy is becoming a major threat. The haves are increasingly few in number, while the middle classes are beginning to sense just how disposable they may be as good jobs from healthcare to airlines evaporate. If the economy was to take a nosedive, you have all the conditions for a repeat of the 1930s.

Think about the 1930s in the context of rising political risk.

The political impasse in congress on a second Pandemic Stimulus Package isn’t even making the front pages – yet Govt support was promised, and its critical for markets in terms of keeping up the strong numbers. The swamp is focused on bargaining: apparently the Republicans will counter the Democrats $1 trillion demands with a $500 bln counter package. They bicker as the pandemic rages on, the dole lines lengthen, and current furlough and stimulus cash runs out. Their deliberations have a direct consequence on business and consumer sentiment – it’s getting wobbly.

The airlines are asking for another $25 bln. Delta is slashing pilot numbers. American Airlines sacking nearly 19,000 pilots and staff. These will be followed by the others. The same is happening across the economy and will be riggering multiplier effects across the economy.

But of course, no US politician is actually focused on the virus anymore. All eyes are on the election. And that is looking massively more scary. If you were still expecting an easy win for Biden – forget it. This election is going to be won and lost on the hugely polarised battlefield of race vs law and order.

The events in Wisconsin defy belief – what possible justification is there for shooting a man in the back, seven times? Listening to the chief of police last night he was arguing the state has to go through proper process and therefore can’t de-escalate tensions by arresting or even sacking the two officers. As riots engulfed the town, two more people died – but it turns out they were shot by vigilantes, and the guy arrested was a 17 year old from out of town dressed in makeshift militia gear.

In terms of the election, forget the state of the economy, forget the trade wars with China, forget the pandemic response. Suppressing uppity rioters has become the central issue of the election.

Their grievances of BLM will be stomped over as Trump goes long Law and Order, and support for the Police, while scaring the electorate that Biden is a pawn of the left-wing defunders. Trump’s betting his rock solid 44% support will be unshaken, and all he needs is small number of scared Dems to think Biden is weak. The timing could not have been better – for Trump in this election.

It couldn’t be worse for solving the divisions across the US to ensure its long-term economic success. There is something deeply depressing about the news from the US. It feels like a Reichstag Fire moment for divided American politics. BLM will be repressed – but not for long. It will come back even more divisive.

Americans will vote as they see fit, but what will it mean for markets? Trump’s global unpopularity may seem unimportant to voters in Peoria, but perceptions matter. If Trump wins because he’s “trumped” the perceived oppression of the Black minority by playing the Law and Order card, it will simply accelerate the already shifting power of US global influence, weaken alliancies, weaken the dollar equation and further shake the dollar foundations of the global economy, while opening doors to China.

Around the globe folk will increasingly wonder about the degrees of difference between Trump’s America and the soon to be Chairman Xi’s China? Sad, but it feels the golden age of US influence is waning.

All these factors – the pace of recovery, the ability of governments to sustain bailout and jobs support programmes, the rising debt mountain, the escalating cumulative economic damage already done, the threat of a second pandemic wave, and the US election – come due in October/November. Have your hard hats ready in case it gets rowdy.

via ZeroHedge News https://ift.tt/31A4nJj Tyler Durden

Futures Dip Ahead Of Powell’s Landmark Speech Tyler Durden

Thu, 08/27/2020 – 08:06

US equity futures and global stocks fell on Thursday and the dollar tried to stage a rebound after two days of losses, as tensions between Washington and Beijing dampened the mood ahead and as investors braced for Powell’s speech at the virtual Jackson Hole conference at 910am ET, at which he is expected to unveil the Fed’s “new policy” of tolerating higher inflation.

Trading on Thursday was weighed down by U.S. sanctions on China over military action in the disputed South China Sea after both Wall Street and the MSCI World index hit new record highs on Wednesday with the endless supply of cheap cash from central banks pushing up big-cap tech companies. The S&P 500 and the Nasdaq had risen for the past five session to new highs, largely driven by investors pouring into heavyweight technology-related stocks.

Among early movers, Abbott Laboratories soared 9.2% in the premarket after gaining clearance for a portable $5 15-minute Covid test. NetApp jumped 10.2% in premarket trading after it posted better-than-expected quarterly results, powered by demand for its cloud services.

The MSCI world equity index dipped 0.1% while the MSCI’s main European Index was down 0.3%. Europe’s Stoxx 600 was down 0.2% led by losses in the bank and insurance sectors. Rolls-Royce Holdings tumbled, leading decliners across Europe after a record half-year loss and writedown on its main jet-engine arm as the coronavirus crisis battered air travel. WPP Plc climbed after suggesting the pandemic’s worst impact may have passed for the world’s biggest advertising group.

Earlier in the session, Asian stocks were little changed, with energy and utilities falling, after rising in the last session. Markets in the region were mixed, with Shanghai Composite and Jakarta Composite rising, and South Korea’s Kospi Index and Singapore’s Straits Times Index falling. The Topix declined 0.5%, with Takasho and Aeon Fantasy falling the most. The Shanghai Composite Index rose 0.6%, with Whirlpool China and Shanghai Industrial Development posting the biggest advances.

CMC Markets UK analyst David Madden told Reuters the week’s pattern was a classic case of “buy the rumor, sell the fact” as investors unwound their bullish positions from earlier in the week.

“If you’re a trader starting the week on Monday you think Powell is speaking on Thursday, we’re all expecting him to have some sort of dovish stance, so you buy Monday, Tuesday, Wednesday, when he’s actually giving the talk on Thursday you wind down your positions,” he said. “You trade in advance in the expectation that a dovish speech will be delivered and then you square up your position a few hours before hand.”

Powell is likely to make a case for low interest rates and higher inflation in an overhaul of the central bank’s policy approach in his remarks at the Jackson Hole symposium, being held virtually this year. Before his address at 9:10 a.m. EDT investors will get a look at the weekly jobless claims report, the most timely U.S. economic indicator, which is expected to have dipped to 1 million for the week ended Aug. 22.

In rates, benchmark 10-year Treasury yields edged lower in a move eclipsed by European peers. The dollar turned higher versus a basket of its biggest counterparts from a level near its two-year low. European bond yields fell, with Germany’s benchmark 10-year Bund yield down 4 bps at -0.451%.

In FX, the Bloomberg Dollar Index steadied following two days of declines. Against a basket of currencies, it was up 0.1% at 92.955. The riskier Aussie and Kiwi dollars gained versus the U.S. dollar, while the euro was slightly lower at $1.18055. Australia’s Victoria state which has become the epicenter of the nation’s second wave of COVID-19 infections, reported its lowest one-day rise in new cases in nearly two months.

The offshore Chinese yuan hit a 7-month high versus the dollar overnight, but erased losses as the European session progressed.

In commodities, oil prices were mixed, with Brent crude futures for October, which expire on Friday, up 0.1% at $45.61 a barrel by 1055 GMT. U.S. West Texas Intermediate crude futures were down 0.4% at $43.21 a barrel. Oil prices were mixed, with Brent crude futures for October, which expire on Friday, up 0.1% at $45.61 a barrel by 1055 GMT. U.S. West Texas Intermediate crude futures were down 0.4% at $43.21 a barrel. Hurricane Laura, a massive Cat 4 hurricane in the Gulf of Mexico pushed the market higher this week, but the storm is not expected to affect supplies much because oil and product inventories are high. Gold prices fell as investors took profits before Powell’s speech, with spot gold down 0.8% to $1,9340 per ounce.

Looking ahead, a bevy of central bankers and economists speak at the Jackson Hole economic symposium in a few hours via webcast entirely viewable by the public for the first time. Powell’s appearance will be closely watched for insight into the Fed’s new monetary policy framework review. “We think the Fed’s message is clear: it will want to keep rates low across the yield curve, in line with its desire to keep financial conditions ultra-loose,” Mark Haefele, chief investment officer at UBS Global Wealth Management, wrote in a note. “Investors should keep cash holdings to a minimum and will need to search harder for yield.” Also in focus is the conclusion of the Republican National Convention. U.S. President Donald Trump will speak live from the White House on Thursday. Quarterly reports from retailers Abercrombie & Fitch Co, Dollar Tree Inc, Dollar General Corp and cosmetic maker Coty are also due premarket.

Market Snapshot

S&P 500 futures down 0.3% to 3,471

STOXX Europe 600 down 0.3% to 372.15

MXAP down 0.02% to 174.06

MXAPJ up 0.2% to 578.36

Nikkei down 0.4% to 23,208.86

Topix down 0.5% to 1,615.89

Hang Seng Index down 0.8% to 25,281.15

Shanghai Composite up 0.6% to 3,350.11

Sensex up 0.3% to 39,206.14

Australia S&P/ASX 200 up 0.2% to 6,126.23

Kospi down 1.1% to 2,344.45

German 10Y yield fell 3.4 bps to -0.449%

Euro up 0.05% to $1.1836

Italian 10Y yield fell 0.9 bps to 0.891%

Spanish 10Y yield fell 2.8 bps to 0.348%

Brent futures little changed at $45.66/bbl

Gold spot down 0.5% to $1,945.61

U.S. Dollar Index down 0.2% to 92.87

Top Overnight News

Hurricane Laura made landfall near Cameron, Louisiana in the early hours of Thursday as one of the most powerful storms to hit the state on record. Authorities ordered evacuations and warned the storm surge will be “unsurvivable”

Covid-19 cases surpassed 24 million worldwide with India seeing a record spike and South Korea, Italy and France reporting the most new daily infections in months

Japanese Prime Minister Shinzo Abe should be able to serve out his term as party leader ending about a year from now, his top aide said, after concerns about the PM’s health

A quick look around global markets courtesy of newssquawk.com

Asian equity markets traded mixed after failing to take full impetus from the fresh record highs stateside which was led once again by a surge in big tech, with the region kept tentative by ongoing US-China tensions and ahead of the looming Jackson Hole Symposium. ASX 200 (+0.2%) was led higher by metal miners following the prior day’s advances in precious metals and with sentiment also supported amid better than expected Private Capex data which included upward revisions to yearly capex estimates. Conversely, Nikkei 225 (-0.4%) was pressured as exporters suffered from the ill effects of recent currency strength, while the KOSPI (-1.0%) also weakened after virus cases rose by the most since March and following the BoK rate decision where the central bank maintained rates at 0.50% as expected but downgraded its 2020 growth forecast in which it now anticipates a wider contraction of 1.3% for the economy. Elsewhere, Hang Seng (-0.8%) and Shanghai Comp. (+0.6%) were cautious as US-China tensions were stoked after the US blacklisted more Chinese firms including several subsidiaries of China Communications Construction Company which saw shares in the parent drop nearly 5%. Other notable stock movers today included HSBC (-1.6%) which was pressured by recent accusations from US Secretary of State Pompeo that it is aiding Beijing’s crackdown on Hong Kong and continues to provide services to people sanctioned by the US, although Xiaomi (+13.0%) shares have surged after it more than doubled its Q2 profit. Finally, 10yr JGBs were positive following the bull steepening stateside in the wake of a strong 5yr US auction, with the slightly soured Asia-Pac tone also providing a tailwind for bond prices, although some of the gains were later pared after mixed results at today’s 2yr JGB auction.

Top Asian News

China Cash Shortages Push Up Funding Costs, Pressuring Bonds

Japan’s Abe to Serve Out Term as LDP Leader, Top Aide Says

South Korea Extends Ban on Short-Selling Amid Virus Flareup

Biggest Malaysian Bank’s Profit Falls to Least in a Decade

Subdued trade across the European equity space (Euro Stoxx 50 -0.5%), as bourses drifted lower since the cash open despite a lack of fresh catalysts and a mixed APAC lead, but with possible positioning/profit-taking ahead of Fed Chair Powell’s address (full Jackson Hole schedule available on the newsquawk headline feed). Participants will be eyeing any nuances regarding the Fed’s framework review and average inflation targets ahead of the September meeting (full preview available in the newsquawk Research Suite). Sectors are mostly lower with a defensive bias, although IT bodes somewhat better than other cyclical names following the tech outperformance on Wall Street yesterday. Meanwhile, Banks reside at the bottom of the pile amid the low-yield environment. In terms of individual movers, WPP (+4.3%) leads the gains in the Stoxx 600 after overall solid earnings. Conversely, Rolls-Royce (-6.8%) resides on the other side of the spectrum after reporting dismal numbers whilst noting the COVID-19 has significantly impacted the group in H1. The newest DAX-component Delivery Hero (-2.9%) is pressured by its earnings which eroded YY. Finally, positive broker moves see Ambu (+1.5%) and Swedbank (+1.0%) in the green.

Top European News

Europe Rejects Hardline Lockdowns to Contain Resurgent Virus

Hedge Funds Press for Crackdown on Front-Running Loophole in EU

The Hut Group’s Planned $1.2 Billion IPO Breaks London Lull

U.K. to Pay People on Low Incomes If Self-Isolating in Pandemic

In FX, the Aussie and Kiwi are outpacing G10 peers, with the former probing resistance around 0.7250 vs its US counterpart in wake of Q2 Capex data showing a less steep decline than anticipated, while Aud/Usd is also deriving more upward momentum from the ongoing incremental strength in the YUAN that is now testing 6.8700 against the Greenback. Meanwhile, Nzd/Usd is eyeing 0.6650 next having established a firmer base above 0.6600 and gleaning some support from latest reports on the COVID-19 situation in Auckland as NZ’s Health Minister states that the outbreak is now relatively contained.

DXY – The broad Dollar and index have unwound more of Wednesday’s pre and post US durable goods gains after another solid Treasury auction prompted a retreat in yields alongside some curve realignment from pronounced steepening, which in turn helped Gold and other precious metals to rebound sharply (Xau currently back up around Usd 1950/oz compared to just above Usd 1900 at one stage). In fact, the DXY is now hovering shy of 93.000 within a 92.991-783 range awaiting top tier data, Fed speakers at the symposium and the final issuance of the week, while also conscious of the fact that today is spot month end and portfolio rebalancing models are negative on balance for the Buck.

CHF/EUR/GBP/JPY/CAD – All narrowly mixed vs the Greenback, as the Franc holds above 0.9100 and perhaps takes heed of Swiss Q2 GDP not contracting quite as much as expected, while the Euro continues to bang its head against 1.1850 and the 200 HMA in close proximity, but hold above 1.1800 and around the 21 DMA with a decent spread of option expiries outside of those parameters (from 1.1750-60 through 1.1900 to 1.19050-55). Elsewhere, the Pound is consolidating at newfound higher levels – Cable around 1.3200 and Eur/Gbp either side of 0.8950 – the Yen is straddling 106.00 and Loonie pivoting 1.3150 ahead of Canadian current account data and average earnings.

SCANDI/EM – Retail sales beats and improvements in Swedish sentiment (both industrial and consumer) haven’t given the Nok or Sek much lasting impetus, as the respective Eur crosses hover around 10.5300 and 10.3100, though the latter may receive something more sustainable from Riksbank’s Floden shortly . However, EM currencies are largely firmer at the Dollar’s expense, even the Rub awaiting a major interview by Russian President Putin at 12.00BST and the Try despite Turkey announcing live fire drills for next Tuesday and Wednesday in the Eastern Med that is almost certain to irk Greece, the international community and investors.

In commodities, WTI and Brent front month futures remain uneventful within a tight range, albeit near session lows, awaiting the main even later today at the Jackson Hole Symposium. Prices have largely priced in the temporary impacts of Hurricane Laura – which has made landfall near Cameron Louisiana as a Cat 4 hurricane, but has since been technically downgraded to a major Cat 3 hurricane – with BSEE leaving their shuttered production estimates unchanged D/D at 84.3%, equating to around 1.56mln BPD (some 13% of total US output). WTI Oct resides sub-43.50/bbl, having touched the figure to the upside in APAC trade, but remains within a tight USD 0.40/bbl range thus far. Brent Oct similarly trades sideways under USD 46/bbl having had printed an overnight base at 45.57/bbl. Elsewhere, spot gold trades softer at the whim of the Buck just under the USD 1950/oz mark, moving within a USD 20/oz range, whilst spot silver sees similar price action and remains contained under USD 27.50/oz. In terms of base metals, nickel prices hit November highs after solid stainless-steel demand and supply concerns from top producer Indonesia, while copper traded flat overnight in tandem with the mixed risk appetite.

US Event Calendar

8:30am: GDP Annualized QoQ, est. -32.5%, prior -32.9%

Personal Consumption, est. -34.2%, prior -34.6%

Core PCE QoQ, est. -1.1%, prior -1.1%

8:30am: Initial Jobless Claims, est. 1m, prior 1.11m; Continuing Claims, est. 14.4m, prior 14.8m

9:45am: Bloomberg Consumer Comfort, prior 43.5

10am: Pending Home Sales MoM, est. 2.0%, prior 16.6%; Pending Home Sales NSA YoY, est. 10.75%, prior 12.7%

11am: Kansas City Fed Manf. Activity, est. 5, prior 3

DB’s Jim Reid concludes the overnight wrap

If like me you’ve been in the market for a Canada Goose Jacket for a few years but have balked at their cost then you may want to check out eBay today for some cut price deals. Yes shockwaves will have been felt through that industry as Davos has been moved from its traditional January slot to the summer of 2021. At least those of us going can rejoice at now arriving at a snowless Davos Forum and not be thinking that we’ve contributed to global warming.

From Davos to a virtual Jackson Hole where the Fed host their annual symposium today and tomorrow. I don’t think I’ve ever been asked to speak at a symposium so please invite me if you have one. I looked the word up in the Oxford English Dictionary to get the exact definition and I’ll leave you to decide which is likely to take place over the next two days. 1) A conference or meeting to discuss a particular subject. 2) A drinking party or convivial discussion, especially as held in ancient Greece after a banquet.

Number two sounds more fun but whichever it is, an array of central bankers will be gathering virtually this year for the annual shindig. There’ll likely be a lot of material to digest over the next 48 hours, but the main highlight will likely come later today from Fed Chair Powell, who’ll be speaking on the Fed’s monetary policy framework review. As Henry mentioned here on Monday, our US economists think that although it’s possible the policy review results will be released along with Powell’s appearance, it’s more likely that he’ll summarise the key findings and outline the likely implications for the Fed moving forward, with the policy review results not released until the September meeting.

Ahead of this, the recent selloff in core sovereign bonds has paused for now. Although US Treasury yields rose a further +0.5bps to 0.689% yesterday, they are down -1.1bps overnight. They were up over +2bps intra-day yesterday before a late session slide in yields. The recent general move higher in rates continues to be driven by a rise in inflation expectations rather than real yields, with US 10yr breakevens closing up another +2.6bps to 1.73% yesterday. That’s the highest level they’ve been at since January 21st, which incidentally was the first time that the coronavirus pandemic was mentioned in the EMR. The move in yields hasn’t been exclusive to the US however, with the bund-treasury spread having remained within a 10bps range for all of August. Before the small reversal in US bonds, 10yr bund yields were also up +1.6bps yesterday to -0.42%, almost closing at a one-month high.

At the risk of sounding repetitive now, global equity markets had yet another strong performance yesterday, with the S&P 500 up again to reach its 4threcord high in a row, thanks to a +1.02% advance. Tech stocks led the rally, helping the NASDAQ to hit a new high as well, with an even stronger +1.73% move upwards. Europe saw a similarly strong showing, with the STOXX 600 moving up +0.91%, while the DAX’s +0.98% advance put the index less than half a per cent away from moving into positive territory on a YTD basis. The MCSI global equity index also hit a new record, surpassing its 12 Feb highs. Even on a day when there was some positive vaccine news, the risk-on rally saw a growth over cyclical rotation. The Media (+4.43%) and Software (+3.15%) industries led the S&P higher at the expense of Energy (-2.23%), Banks (-1.63%) and Autos (-0.63%). Europe was more of a rising tide lifting all boats market with all but two of the 19 sectors finishing higher, though Tech (+2.20%) led as well.

The drop in US energy stocks comes as the Texas-Louisiana region braces for Hurricane Laura, which has been upgraded to a category 4 storm and is approaching category 5 with maximum winds increasing to 150 mph (241km/hr). It is estimated to make landfall between 12:30 am to 1:30 am CDT (about the time this hits inboxes). The region last saw a Cat-4 storm (Harvey) back in 2017, which caused over $130bn of damages. According to a Bloomberg report, more than 80% of the Gulf of Mexico’s oil production has been shut and the destruction to refineries alone could surpass $5bn. Brent (-0.48%) and WTI (+0.09%) were largely unchanged just ahead of the storm with news of declining stockpiles coinciding with decreased demand from shuttering refineries, though both measures are up over +2.5% on the week.

Overnight, markets in Asia are trading a bit more mixed with the Nikkei (-0.30%), Hang Seng (-0.63%) and Kospi (-0.55%) all down while the Shanghai Comp (+0.29%) and Asx (+0.54%) are up. Futures on the S&P 500 are also trading lower (-0.16%) while those on the Nasdaq 100 are down -0.25%. Spot gold and silver prices are also down -0.71% and -1.41% respectively this morning. Elsewhere, the BoK held its policy rate steady while slashing the 2020 GDP growth forecast to -1.3% yoy (vs. -0.2% yoy earlier) at its monetary policy meeting today. In terms of overnight data, China’s July industrial profits came in at +19.6% yoy (vs. +11.5% yoy last month), however the data series is fairly volatile.

On the virus, Italy recorded a further 1,366 cases in the past 24 hours, which was the highest one day rise since mid-May. However the Italian health minister cited a lack of strain in healthcare services and the low average age (30) of those testing positive in the past two weeks as reasons why the country would not need to impose a new round of national lockdowns. This follows similar comments from Spanish and German officials earlier in the week. France has now reported 5,429 cases in the last 24 hours and have added nearly 29,000 cases in the last week. The country has not seen that many new infections in a week since mid-April and PM Castex will hold a press conference today to discuss the health situation. In more positive news however, a phase 1 trial from Moderna showed that the antibody response among those over 55 was comparable to that experienced by younger adults. The firm’s share price was up +6.42% yesterday in response. In other encouraging news on the virus, Bloomberg reported that Abbott Laboratories has won US clearance for a 15-minute Covid test that will be priced at just $5.

Elsewhere, cases in the US continue to drive lower as the summer hot spots in the Sun Belt continue to see lower case loads, especially Arizona (0.3% average 7-day increase) and Florida (0.6% average 7-Day increase). Across the other side of world, South Korea reported another 441 cases in the past 24 hours, marking the biggest single day gain since early March. In other COVID related overnight news, the FT reported that a WHO team that was meant to investigate the origin of the coronavirus concluded their trip to China without a visit to Wuhan, China’s epicenter of the outbreak, citing the UN agency.

Outside of Jackson Hole, the other main highlight today will come from President Trump’s speech to the Republican National Convention later, which comes with less than 10 weeks to go now until US voters go to the polls. Though early in-person voting starts in less than a month in some US states, including potential swing states like Michigan and Minnesota. We discussed the election in our chart of the day yesterday (see here), where we pointed out how since the Second World War, only one other incumbent president has managed to win re-election with an approval rating as low as President Trump’s is 2 months before an election. Trump’s approval currently stands at 42%, but in the 11 post-WWII elections where an incumbent President has been a candidate, the only one who managed to win with an approval rating lower than this was Harry Truman in 1948 (at 40%). So while there’s still some time left to see a recovery in his numbers before election day, on that measure alone it looks historically challenging for Trump to win re-election on November 3rd.

Looking at yesterday’s data, the main highlight came from the US as July’s durable goods orders rose +11.2% (vs. 4.8% expected), while core capital goods orders excluding aircraft and military hardware was up +1.9% (vs. +1.7% expected). Meanwhile in France, the INSEE’s consumer confidence reading remained stable in August at 94, in line with expectations, though it remained below the 104 readings in January and February before the impact of the pandemic hit.

To the day ahead now, and the aforementioned economic symposium at Jackson Hole will likely be the highlight, including remarks from Fed Chair Powell, ECB chief economist Lane, and Bank of Canada Governor Macklem. Otherwise, data highlights include the Euro Area’s M3 money supply for July, while from the US we’ll get the second estimate of Q2 GDP, July’s pending home sales, August’s Kansas City Fed manufacturing activity index, and the weekly initial jobless claims. Finally, tonight sees President Trump speak at the Republican National Convention.

via ZeroHedge News https://ift.tt/2QwfNqV Tyler Durden

“Any Excuse To Riot” – Minneapolis Descends Into Chaos Over Police Shooting “Fake News” Tyler Durden

Thu, 08/27/2020 – 07:55

In these heady times, it seems, incidents are quickly magnified and wildly distorted, leading to mass public outrage when really none should be warranted: Case in point, the state of Minnesota was forced to declare a “state of peacetime emergency” in Minneapolis last night after violent protests erupted following the death of a local black man.

Violence erupted once again in the larger of the twin cities last night, with video showing angry “demonstrators” burning down businesses, rioting and looting, following “misinformation” about the killing of a black homicide suspect. Rumors spread online said he had been killed in a police shooting, but really, he shot himself in the head, according to surveillance video.

Before watching the video below, be advised: It depicts a man shooting himself in the head, before a nearby officer rushes to his aid. Then off camera, bystanders can be heard accusing the cops of shooting the now-dead victim.

It later emerged that the man shot himself in the head as police were moving in to make an arrest. He had committed the murder just hours earlier, at around 2pm local time in a nearby parking garage

That was apparently enough to spark a wave of rioting and looting.

Doesnt look locked down to me…

Looting is now taking place at the Nicollet Mall in Minneapolis after a man committed suicide while being pursued by police. Any excuse to riot. pic.twitter.com/LGVY7DVX6E

More looting in downtown Minneapolis. They’ve now breached the Saks 5th Avenue store on 6th and Nicollet and people are making out with lots of goods. pic.twitter.com/tgUIyoIMvf

Minneapolis Mayor Jacob Frey imposed a curfew following what he described as mass looting of businesses, destruction of property and unrest. Gov Tim Walz, also a Democrat, declared the state of emergency, before taking to twitter to beg those committing the violence to stop.

Minneapolis, it’s time to heal. We must rebuild and recover. Dangerous, unlawful behavior will not be tolerated. The State Patrol is headed to Minneapolis to help restore order. I remain in close contact with the city and every state resource stands ready to help bring peace.

Minneapolis Police Chief Medaria Arradondo said his officers were not involved in the suicide death, saying it was not officer-related.

“I will not allow to add more trauma to a city that’s still grieving from May 25,” referencing the death of George Floyd, whose death while in Minneapolis police custody sparked ongoing nationwide protests and riots.

One officer was injured in the incident, but not seriously.

Hennepin County Sheriff David Hutchinson said his deputies were helping the Minneapolis Police Department to quell the unrest. He urged people to go home and gather the facts before just jumping to conclusions.

“When the police do things wrong we need to hold them accountable, but this is not the case,” he told reporters. “We as the police, the Sheriff’s Office did nothing wrong tonight.”

Minneapolis Mayor Jacob Frey imposed a curfew across the city after the mass looting, destruction of property and unrest.

via ZeroHedge News https://ift.tt/2En4teA Tyler Durden

Night 4 Of Kenosha Protests Mostly Peaceful As City Calls In Reinforcements Tyler Durden

Thu, 08/27/2020 – 07:50

Protests in the city of Kenosha Wisconsin remained peaceful Thursday night as city officials and the governor called in more national guardsmen and police from around the state, adding another 500 officers to the small army that stood by and watched the situation descend into mayhem earlier this week.

Last night, 3 men were shot, 2 fatally, and a 17-year-old whom left-wing politicians have tried to tar as a “white supremacist” (based on zero evidence) has been arrested in Illinois and charged with fleeing justice and first degree murder.

Also on Wednesday, state authorities finally released the identity of the officer who shot Blake on Sunday. He is a 7-year department vet named Rusten Sheskey. Sheskey shot Blake while holding onto his shirt after officers first unsuccessfully used a Taser to try and subdue him. Officials said last night that Blake appeared to be reaching for a knife under the seat of his car when he was shot.

In a statement, Wisconsin’s Democratic Governor Tony Evers asked those who wanted to exercise their First Amendment rights to “please do so peacefully and safely” and urging others to “please stay home and let local first responders, law enforcement and members of the Wisconsin National Guard do their jobs.”

“A senseless tragedy like this cannot happen again,” Evers said.

Unsurprisingly, CBS News dedicated some of its report on the night’s events to an alleged “eyewitness” (whose testimony contradicts myriad video evidence) peddling a false narrative of Tuesday night’s shooting.

One of the protesters in Kenosha Wednesday night was also there Tuesday night during the shooting. He told CBS Milwaukee affiliate WDJT-TV Kenosha police pushed peaceful protesters into the way of counter-protesters and police should be held accountable for what happened.

“I watched a man get shot down yesterday,” Cairo Thomas said. “I watched that. Nobody chastised him. Nobody was trying to burn down a property. They were literally cutting through the parking lot. And that 17-year-old murderer, which he is, he’s a murderer, that 17-year-old murderer decided to open fire and shoot this man in the head.”

In an interview shared by the Daily Caller, the alleged shooter said he had brought his gun only for “self defense”, and that he hoped to “help people” by treating the injured.

“So people are getting injured, and our job is to protect this business,” the young man said. “And part of my job is to also help people. If there is somebody hurt, I’m running into harm’s way. That’s why I have my rifle – because I can protect myself, obviously. But I also have my med kit.”

It’s legal in Wisconsin for people 18 and over to openly carry a gun without a license.

via ZeroHedge News https://ift.tt/31xK1QR Tyler Durden

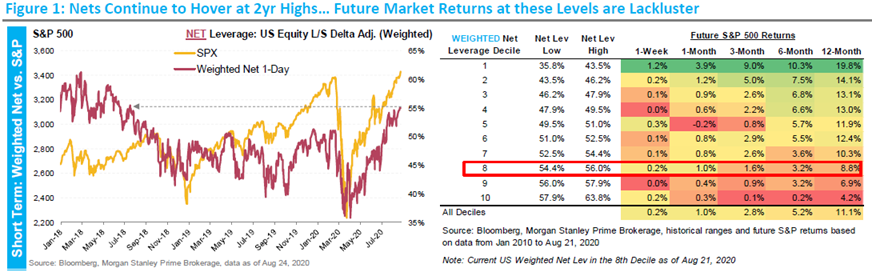

Powell is on deck tonight and here’s where we stand…

Between rising US-China tensions, unemployment insurance benefits expiring and dwindling volumes the last month, one would have thought, a pullback would have come to fore. But that’s also probably the reason why it didn’t. In fact, it’s been the opposite has happened with global equities making new all-time highs.

As we move into September, which has been SPX’s worst month on average since ’00, while the same risks remain, the positioning set up is quite different. Further, what is concerning now is that we have “peak Fed” and potentially a growth/rates scare around the corner. According to Mike Wilson, this is likely to drive a tactical pullback in the coming weeks (but it is also the reset the market needs before the next leg of the bull market).

Per our PB Content team, US Equity L/S weighted net leverage has rebounded significantly and surpassed levels seen throughout all of 2019 and 2020 thus far and currently stand at the highest levels since July ’18. For context, the last time nets were last at these levels (July ’18), they were actually slowly starting to decline as the market was also inching towards all-time highs, but ultimately dropped around the 4Q18 market sell-off.

The rebound in net leverage this year has come from a mix on short covering, some long additions, coupled with the market continuing to make new highs. Net leverage is currently at 55% which is the 75th %-tile since 2010 – typically when nets are at these levels, future S&P returns for the next few months are usually pretty lackluster.

For the Fed specifically, Ellen Zentner believes Powell’s update at Jackson Hole tonight will mark an important moment in monetary policy. Her confidence is bolstered by a series of appearances that have been scheduled for the aftermath – Clarida, Brainard, Williams, even Yellen and Bernanke – all key personnel you would expect to see on a major framework announcement.

She expects this will include information on flexible average inflation targeting, which will formerly be adopted in the FOMC statement in September, and opens up another runaway for Powell to deliver new forward guidance in December.

All in, expectations are pretty high heading into the testimony and so are valuations. Per Jonathan Garner today:

Additionally, SPX 14 RSIs are back to highs last seen in Jan’20 and Jan ‘18

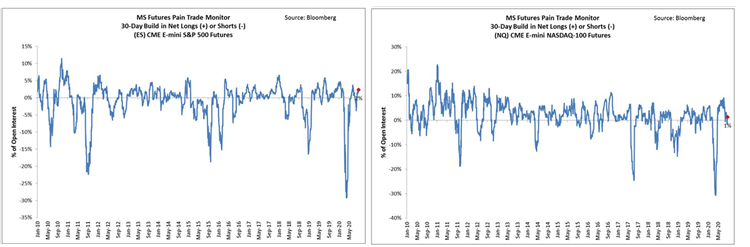

And futures positioning, is a long ways from the short skew earlier this year

From Mike Wilson’s perspective, backend rates are likely going up in meaningful way between now and next year (btw, this is the part of the call he gets the most pushback).

Contributing to that view, he thinks a growth scare which is likely to prompt action from Congress to deliver a larger than expected package, which will in turn help drive rates higher. While it’s prettyimpossible to call when Nasdaq tops given the wall of money into top 5 names, a taper tantrum could be the catalyst .

Moving beyond this reset, he still maintains the big money will be made in next 12 months by buying interest sensitive stocks. He believes materials, basic resources, banks, consumer cyclicals, hotels, airlines are still priced for no vaccine or herd immunity and rates not moving. Our reopening baskets = MSXXOPN1 and MSXXOPN2 are well placed here.

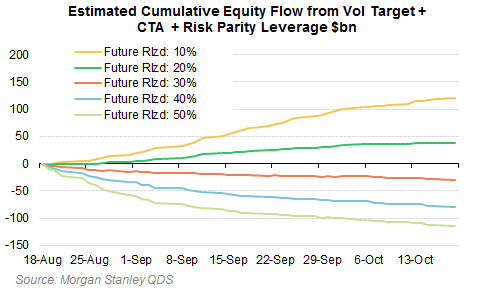

Finally, while systematic strategies are a market support right now (with ~$30-35bn expected buying over next two week), it will not prevent a correction if there was some external market shock (i.e. taper tantrum?).

Our QDS team notes that with low realized vol (like it is now, near 10%), systematic strategies will continue to buy. But if there was a shock to the market, they would actually flip to sellers. The below chart shows future realized vol = SPX realized vol. So you can see they would continue to contribute to equity demand in a low vol environment, but if there were some shock and vol rose, that would flip to selling.

via ZeroHedge News https://ift.tt/2D8PrZe Tyler Durden

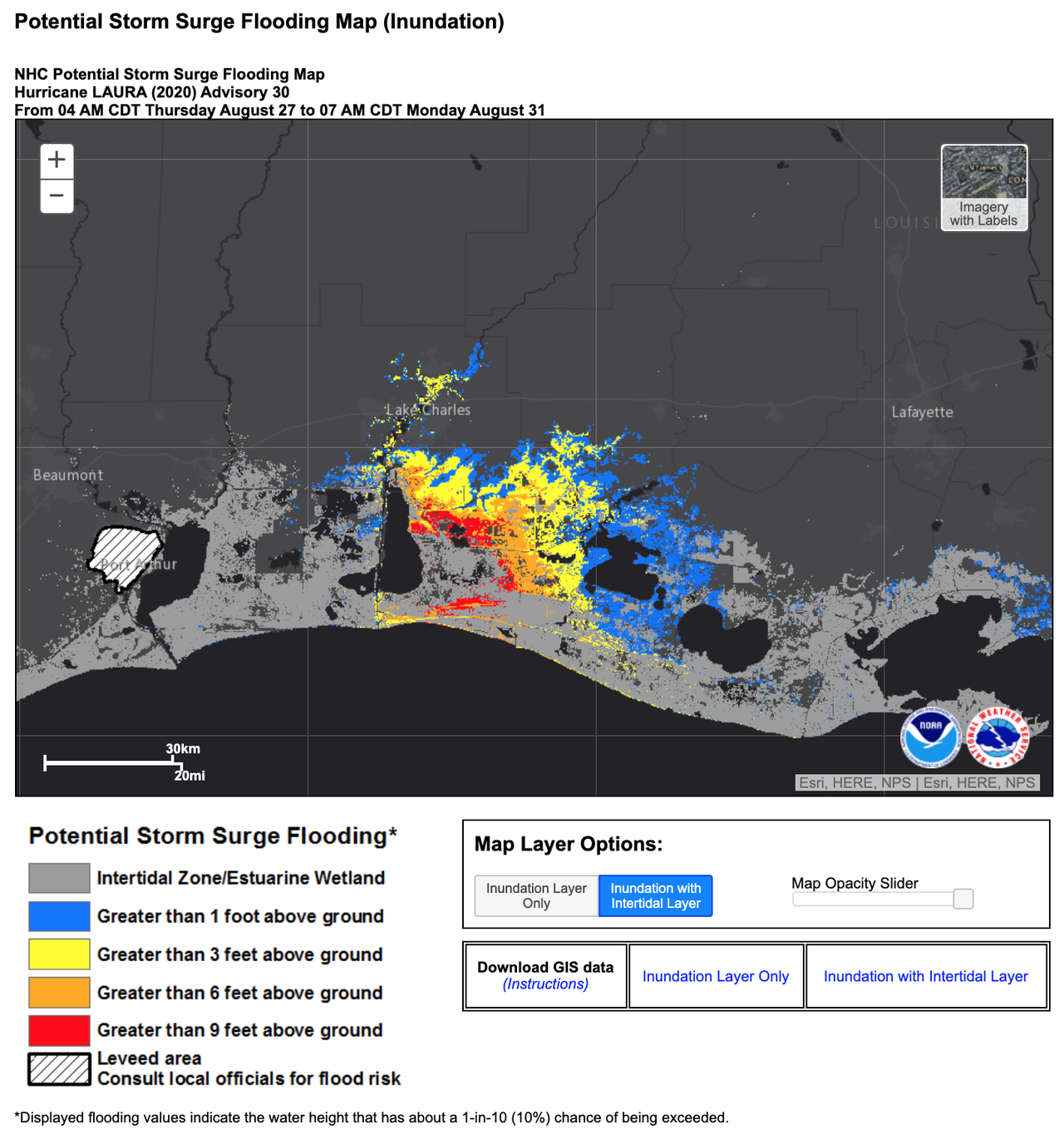

“This Is Insane” – Hurricane Laura Makes Landfall As “Extremely Dangerous” Category 4 Storm Tyler Durden

Thu, 08/27/2020 – 07:13

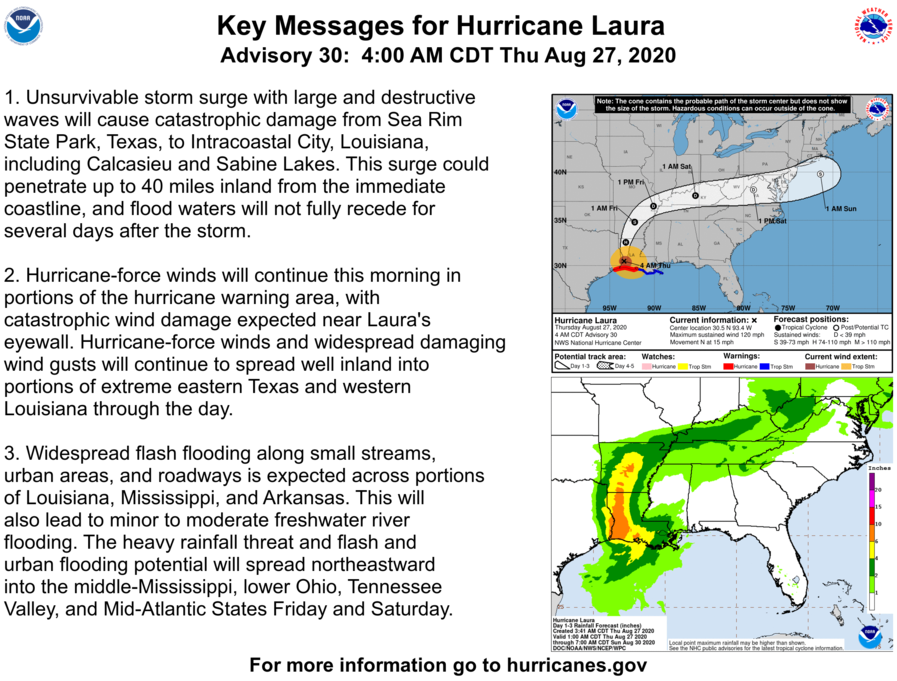

The ‘extremely dangerous’ Hurricane Laura made landfall early Thursday morning as a Category 4 near Cameron, Louisiana, with maximum sustained winds of 150 mph. The eye of the storm pushed inland across southwestern Louisiana around 3:00 ET, with “catastrophic storm surge, extreme winds, and flash flooding,” the National Hurricane Center (NHC) said.

Around 0500ET, the NHC downgraded Laura to a Category 3 storm with winds up to 120 mph. The storm is moving northward through Louisiana as an “unsurvivable storm surge with large and destructive waves” batters the region.

NHC’s Latest Update

It’s too early to speculate the total dollar amount of damage caused by Laura. Still, with floodwaters expected to penetrate 40 miles inland and take “several days” to recede, it could be in the billions of dollars, like other major storms to hammer the region in recent years.

Storm Surge

Storm Surge Map

“Hurricane-force winds and widespread damaging wind gusts will continue to spread well inland into portions of extreme eastern Texas and western Louisiana through the day,” NHC said.

A 132 mile per hour wind gust was recorded at the Lake Charles Regional Airport within Hurricane #Laura‘s northeastern eye wall. pic.twitter.com/oxxaggURyt

More widespread damage is being reported around Lake Charles.

Damage is widespread in Lake Charles. It’s also very difficult to get around due to all of the downed power lines and trees. The interstates have multiple blockages of power lines and light poles with the smaller roads even worse. #HurricaneLaura#lawxpic.twitter.com/TSA5OY6sM4

NEW: A look at some of the damage being found around Lake Charles after Hurricane Laura made landfall nearby as a Cat 4 storm. Roofs of buildings torn off, trucks toppled, debris and trees all over. @WPTVpic.twitter.com/ujlp3ZMgX7

A piece of the Lake Charles skyline has collapsed, here is a view of the KPLC tower. Photo credit to Charlie Haldeman of ABC 13 in Houston. #lawxpic.twitter.com/N908vVP4Qm