Former Green Beret Who Allegedly Spied For Russia Arrested Tyler Durden

Fri, 08/21/2020 – 19:20

The latest in what has become a steady drumbeat of arrests of foreign spies and double-agents in the intelligence community continued on Friday when federal prosecutors charged a former Green Beret living in northern Virginia with espionage activity dating back to 1996.

The spy was accused of working with Russian Intelligence, and was even assigned a code name by his Russian handlers, implying that he was a de facto part of their organization. He allegedly signed a statement saying he wanted “to serve Russia.”

It’s already the second arrest this week involving a US official caught stealing and transmitting US secrets to a foreign power. On Aug. 17, an ex-CIA officer was charged in Hawaii. Other cases involving corporate America and academia have cropped up earlier this year as well.

The US attorney who brought the case in released a statement promising to hold service member double-agents “accountable”.

“When service members collude to provide classified information to our foreign adversaries, they betray the oaths they swore to their country and their fellow service members,” said G. Zachary Terwilliger, U.S. Attorney for the Eastern District of Virginia., whose office is prosecuting the case. “As this indictment reflects, we will be steadfast and dogged in holding such individuals accountable.”

Debbins was arrested Friday, prosecutors told the AP. However, online court records remain sealed, so details of the case including related to Debbins’ representation are unclear.

The espionage allegedly occurred between 1996 to 2011, prosecutors say, a period where Debbins served in the US Army Special Forces as a Green Beret.

via ZeroHedge News https://ift.tt/3aM8chf Tyler Durden

AG Barr Throws Cold Water On Possible Trump Pardon Of “Traitor” Edward Snowden Tyler Durden

Fri, 08/21/2020 – 19:00

Once again President Trump’s anti-establishment and ‘anti-deep state’ instincts look like they’ll be promptly reigned in by those around him. He shocked leaders in Congress and within his own administration when one week ago he mused openly in a New York Post interview that maybe Edward Snowden should be pardoned. In follow-up he said at a press briefing last Saturday “There are many, many people – it seems to be a split decision that many people think that he should be somehow treated differently, and other people think he did very bad things.” And further that: “I’m going to take a very good look at it.”

The president raised eyebrows and anxiety across the D.C. beltway with his unprecedented remarks: “There are a lot of people that think that he is not being treated fairly. I mean, I hear that,” he had initially told NY Post, before adding: “Many people are on his side, I will say that. I don’t know him, never met him. But many people are on his side.” This immediately raised hopes among those that hail the NSA leaker as a whistleblower who exposed deeply unconstitutional surveillance of the domestic populace that he might one day soon see freedom.

But now Attorney General William Barr is throwing cold water on such a bold prospect, saying to the Associated Press on Friday that he’d be “vehemently opposed” to any initiative to pardon Snowden, who remains on the run from US authorities – but given asylum in Russia. If he were to return to the United States he would face severe charges related to the Espionage Act and spilling of state secrets, which would certainly bring life imprisonment.

“He was a traitor and the information he provided our adversaries greatly hurt the safety of the American people,” Barr said in the new comments. Interestingly, Trump’s own view as expressed years ago was that Snowden was a “traitor”.

Barr’s latest comments frame Snowden’s actions as motivated by money and fame, and not of out of a sense of patriotism or concern for upholding the Constitution: “He was peddling it around like a commercial merchant. We can’t tolerate that,” Barr added firmly.

Recall that last year the DOJ under Barr fought to ensure that Snowden wouldn’t see any money generated from US sales of his tell-all book Permanent Record.

Critics have still claimed that Snowden has raked in millions from his online remote appearances at conferences, and in speaking events and interviews.

This whole latest discussion as to the administration’s stance on Snowden had arisen when in the NY Post interview Trump’s former advisor Carter Page was brought up in connection with allegations of abuse and illegal surveillance under the aegis of the Foreign Intelligence Surveillance Act and the secret FISA court.

After years of the whole sordid ‘Russiagate’ saga, it appears Trump has formed a new perspective and appreciation for just what Snowden was exposing, and what the government contractor was up against.

via ZeroHedge News https://ift.tt/34sCwg1 Tyler Durden

“These Are Staggering Numbers”: Spending By Unemployed Americans Plunges As Fiscal Stimulus Ends Tyler Durden

Fri, 08/21/2020 – 18:40

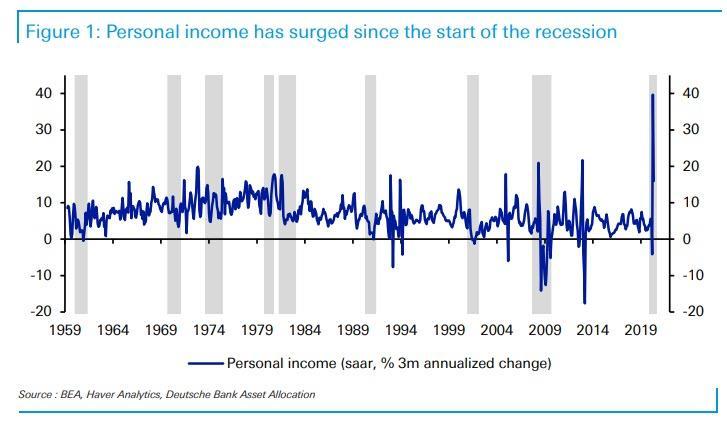

One month ago, with millions of newly unemployed Americans fearful about their future in an economy transformed by the covid pandemic, Deutsche Bank’s Jim Reid made a remarkable observation: “Recessions don’t usually result in personal income soaring, but this one has thanks to government support around the world.” This was shown in the following chart:

This was not a surprise: as Bank of America writes, one of the regular features of US recessions since the 1950s is that they always trigger, with a bit of a lag, an expansion of unemployment benefits. In normal times, benefits in the US are lower than for most other developed market economies, but there is an attempt to close some of the gap during the recession. In recent recessions the additional benefits have tended to be earlier, bigger and last longer. Thus benefits weren’t enhanced until the end of the 2001 recession and provided 13 weeks of additional benefits through Mar 2004. However, for the Great Recession of 2008-9 enhanced benefits were enacted on July 2008, a year before the end of the recession, lasting through December 2013, with the unemployment rate down to 6.7%.

Initially the response to this crisis continued the trend toward stronger responses. Facing a much deeper and faster recession, enhanced benefits were almost immediately implemented and included a large bonus benefit of $600/week. Unfortunately, 4 months later and policy has taken a 180 degree turn: the benefit has been allowed to expire with an unemployment rate still north of 10%. Needless to say, it seems a bit early to declare mission accomplished.

That said, the US is now caught in an unprecedented dilemma – as BofA also notes, “Absent government support disposable income would have fallen the most in history; with that support it has risen the most in history.”

So what’s Congress – and the President – to do?

Well, while the full impact of this economic transformation has yet to be felt across the country, at least for some the government support ended on July 31 when the infamous “fiscal cliff” hit and has yet to be renewed by Congress (executive orders signed by Trump two weeks ago have offset only a modest portion of the stimulus). The group most directly affected are recipients of unemployment insurance (UI) who have seen a notable reduction in income.

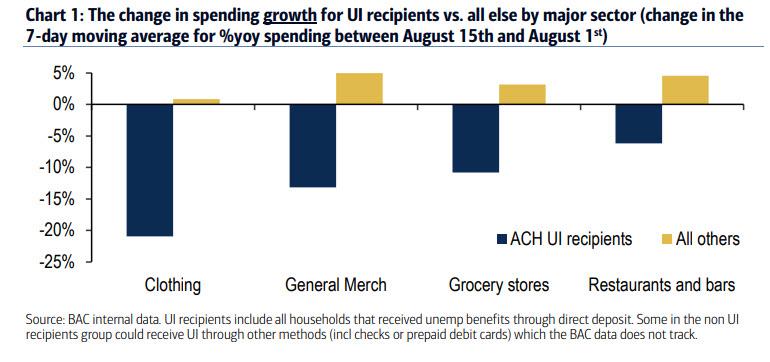

To quantify the impact, Bank of America examined spending trends of the population of card holders who receive UI through ACH

(direct deposit) and compared to all other households. What it found was a dramatic divergence as the YOY rate of growth for UI recipients slowed dramatically but increased for the broader population since Aug 1st.

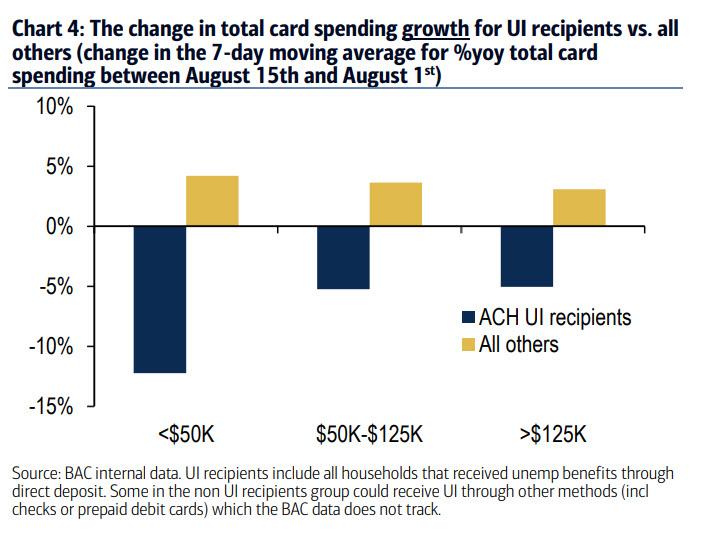

By income, over the past two weeks, the YOY growth rate slowed by 12% for the unemployed cohort (formerly) earning under $50K vs. a roughly 5% drop for the middle and upper income cohorts.

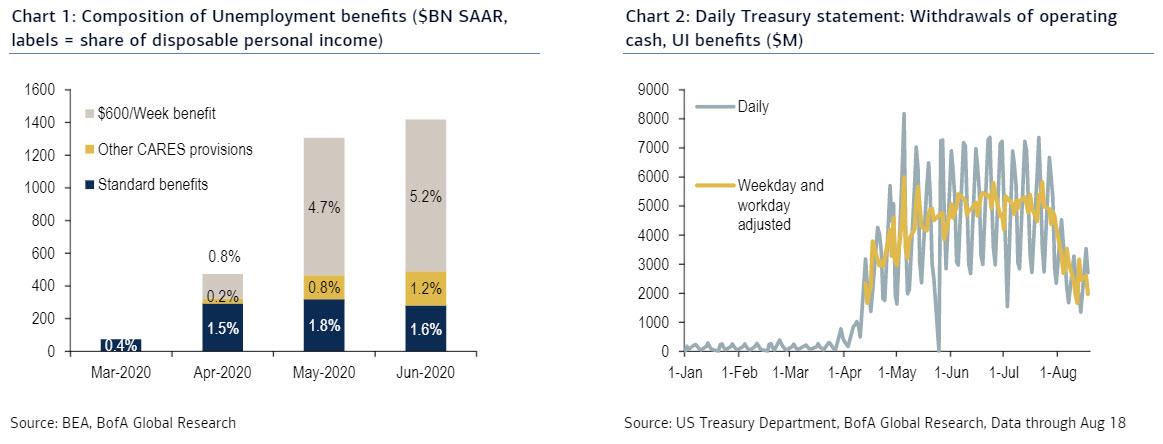

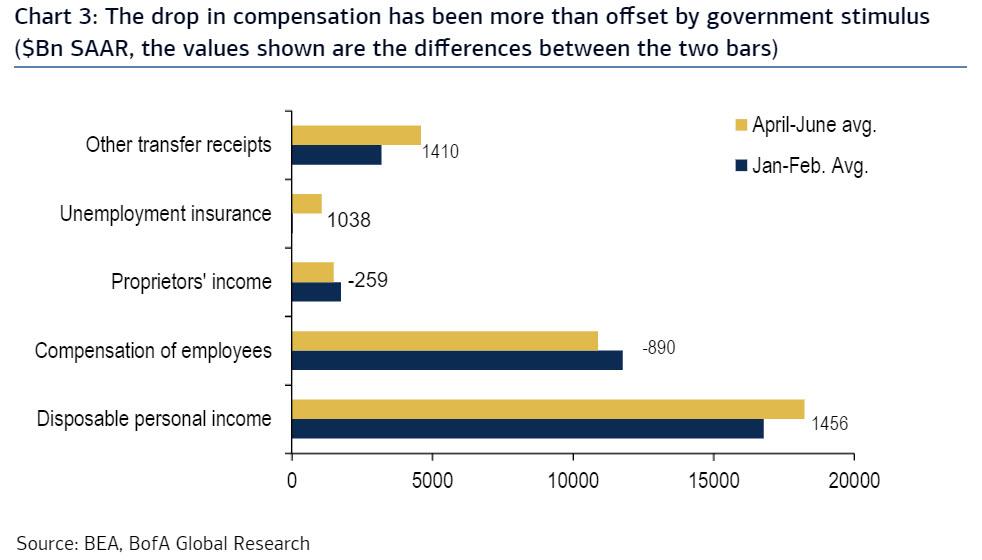

Some more math: a closeer look at the US household income statement underscores the resulting hole in household income as a result of the lapsing of the fiscal stimulu. The $600/week benefit was not a small support to the unemployed, it accounted for more than 60% of unemployment benefits in June (Chart 1). As the numbers on the chart indicate, that means a payment equivalent to about 5% of household income just disappeared. We don’t have data yet for July and August, but the daily treasury statement confirms the collapse in payments (Chart 2). In July the average daily outlay was $4.8bn, in the past five working days it has collapsed to $2.3bn, or a drop of more than half from the peak stimulus period.

These charts show just how reliant on the government much of America has become.

To be sure, much has been made about the resilience of the consumer so far in this crisis. Indeed, while services spending remains depressed, retail sales have fully recovered. However, as shown above, this recovery is deeply dependent on fiscal support. The next chart decomposes the various sources of income in recent months-unemployment benefits, other tax and transfer benefits, labor income, proprietors income and other income.

And here is BofA’s remarkable observation: “Absent government support disposable income would have fallen the most in history; with that support it has risen the most in history.” Note that the role of government stimulus is even bigger because the surge in proprietors income was due to another (now fading) federal program-the Paycheck Protection Program.

So just how much of a hit to consumption – which represents 70% of US GDP – is coming?

Well besides the already noted slump in spending by unemployed Americans, it will take time to see the full effect of the lost payments on consumer spending since presumably some recipients have savings or can postpone rent, credit card and other bills. The early evidence suggests “a moderate shock” according to BofA which again notes – see chart 4 above – that among the unemployed, lower income groups were among the hardest hit, with the YOY growth rate slowing by 12% for the cohort earning under $50K vs. a roughly 5pp drop for the middle and upper income cohorts.

While the bank has not done a formal simulation of the impact of the lost fiscal stimulus, a simple illustrative example from the Petersen Institute can give a sense of the magnitude. First, they assume that 20MM people were unemployed at the end of July and that the $600 benefit has a fiscal multiplier of 1.5 (around the midpoint of the CBO’s range of estimates). The expiration of the $600/weekly benefit would therefore remove about $50bn in income from the economy per month. By their estimate, this would result in about a 2.5% decline in GDP, 2MM less jobs over the next year and a 1.2pp increase in the unemployment rate.

As BofA summarizes “while illustrative, these are staggering numbers.” Moreover, based on the latest claims data there were around 15MM people on standard unemployment benefits as of the week ending August 8 with millions more in other programs such as Pandemic Unemployment Assistance (PUA). Thus, the full impact will likely be even more acute than modeled by BofA.

The final question is whether President Trump’s executive orders can offset the shock to incomes.

Let’s look first at the unemployment benefits and then at executive orders as a group. The executive order earmarks the $44bn in remaining FEMA funds for unemployment benefits of $300/week. In addition, initially it required states to provide $100/week in matching funds, but that requirement was dropped as it became clear that it would deter cash-strapped states from participating. Since the program is new it will take time for states to set up the new system, and indeed as we pointed out earlier this week, only 7 states have so far signed up for the $300 unemployment stimulus plan. Hopefully a number of states will have the program up and running by the September 1 launch date. While this new payment cuts the income shock in half, the funds are likely to only be enough to cover a month or so or into early October, one month ahead of the elections. Moreover, the order is backdated to start on Aug 1. So in practice, the funds may be disbursed quickly after states have set up their programs.

The other major executive order is the deferral in the employee component of the payroll tax from September 1 until December 31. Objectively, this will provide very little support to consumer spending, and as we also noted earlier, business lobbies are already complaining that the program is “unworkable” – a letter co-signed by a number of groups including the US Chamber of Commerce, the National Retail Federation, the National Association of Manufactures and others argued that (1) the order would result in a significant tax bill in 2021 for employees, (2) the implementation of the order is unworkable and (3) many members expect to decline to actually adopt the deferral.

Even for workers at firms that do implement the deferral the impact on spending will likely be very small. Households that are not in financial distress will save most of the tax cut in anticipation of a big bill at tax year end. Of course, workers that are in distress due to unemployment will not benefit from cutting a tax they are not paying. That leaves a relatively small group of households that remain cash strapped even though they are still employed. Presumably they will spend a good part of the tax cut.

What happens next?

As we have reported almost every day for the past three weeks, Congressional negotiations seem hopelessly bogged down and furthermore, Congress is currently on recess with funding the post office has become a major distraction. Both parties are having their conventions. Both parties are watching to see if the executive orders work. And an election looms.

As BofA’s economists concludes, while they had hoped for a deal this month, “increasingly it looks like one only comes after Labor Day and after demonstrable pain in the economy.” Unfortunately, in a world in which the market no longer reflects the economy, it is unclear just what signal US politicians will seek to determine that the economy is “in pain.” Ironically this will make the disconnect between the soaring market which just hit a fresh all time high and the economy which is about to double dip, even more grotesque.

via ZeroHedge News https://ift.tt/3j4yw9u Tyler Durden

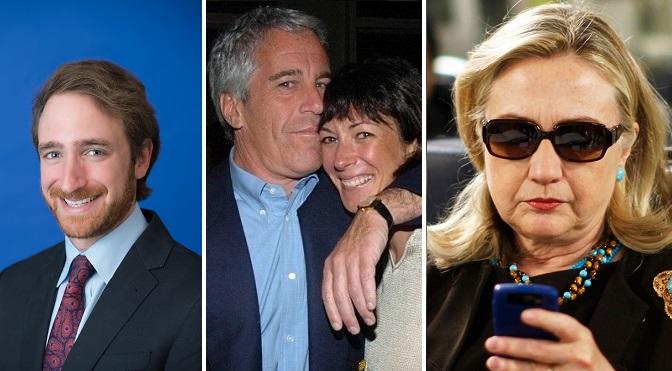

Hillary Clinton Gave Ghislaine Maxwell’s Nephew “Very Powerful” Position At State Department: Report Tyler Durden

Fri, 08/21/2020 – 18:28

Hillary Clinton “gifted” a prestigious job in the Obama State Department to the nephew of accused pedophile and sex trafficker Ghislaine Maxwell, according to OK!Magazine – and whose employment was confirmed by the Daily Beast.

Alexander Djerassi, the son of Maxwell’s sister, went from working on Hillary Clinton’s 2008 Presidential campaign, to a “very powerful and prestigious position” within the state department, working under Clinton in charge of the Bureau of Near Eastern Affairs. He returned to Clinton’s 2016 campaign, according to the Beast.

“Secretary Clinton gave Alex a job in one of the most sensitive areas of Obama’s executive apparatus,” an anonymous source told OK!. “The fact Alex Djerassi, fresh out of college, was put in charge of the State Department’s Bureau of Near Eastern Affairs, covering the Middle East, was an interesting move.”

“He worked directly on the Arab Spring, and Hillary sent Alex as the US representative to the expatriate rebel groups Friends of Libya and Friends of the Syrian People,” the source continued, adding that Djerassi was given “special treatment.”

A State Department spokesperson confirmed Djerassi’s employment with The Daily Beast, though could not comment on whether the job was in fact “gifted” by Clinton.

A year before Mr. Djerassi’s appointment, his aunt’s ex-boyfriend, Epstein, pleaded guilty to a state charge (one of two) of procuring for prostitution a girl below age 18 and was sentenced to 18 months in prison.

Epstein served almost 13 months before being released for a year of probation on house arrest until August 2010.

According to Djerassi’s LinkedIn profile, “He worked on matters relating to democratization and civil society in the Arab world, the Arab uprisings, and Israeli-Palestinian peace. Djerassi has served as a U.S. representative to the Friends of Libya conferences, Friends of the Syrian People conferences, U.S.-GCC Strategic Coordination Forum, and several UN General Assemblies.”

According to the Beast, Derjassi’s name appears in a ‘collection of Clinton’s emails’ published by WikiLeaks – with Assistant Secretary of State Jeffrey Feltman referring to his “special assistant, Alex Djerassi” in November of 2011 and January 2012.

Meanwhile, the Beast also notes his employment on Clinton’s campaign.

From September 2007 to June 2008, Djerassi was a policy associate for Hillary Clinton’s presidential campaign. He listed his job duties as such: “Researched and drafted memos, briefings, and policy papers for candidate, senior staff, and news media on wide range of domestic and foreign policy issues. Prepared for more than 20 debates.” (In late 2007, Epstein was under investigation for trafficking girls in Palm Beach and working on a secret plea deal with federal prosecutors. Maxwell is believed to be one accomplice who was protected under the controversial agreement.)

The Yale and Princeton alum—the son of Maxwell’s sister Isabel—apparently returned for Clinton’s 2016 presidential run. –Daily Beast

Bill Clinton notably flew 26 timeson the infamous “Lolita Express” belonging to Maxwell associate and convicted pedophile Jeffrey Epstein. The former US President was notably fingered as having been seen on Epstein’s “pedo island” according to court documents released three weeks ago.

More recently, photos of Clinton receiving a neck rub from one of Epstein’s accusers (who said he was a perfect gentleman) surfaced in the Daily Mail.

via ZeroHedge News https://ift.tt/2EgfSMT Tyler Durden

Real Vision CEO Raoul Pal is joined by senior editor Ash Bennington to reflect on the future of markets at this unique juncture. Raoul begins by giving Ash a glimpse of how his “unfolding” thesis has evolved, particularly with regard to the dollar. The discussion of currencies naturally leads Raoul and Ash to talk about the ongoing meltdown of the Turkish Lira (TRY). Raoul explains the correlation between Bitcoin and the TRY and explores whether it’s a sign of capital flight by Turkish investors. After a brief detour into New York City’s woes, Raoul and Ash consider how this consumer-led recession is widening the divide between skilled and unskilled workers, as well as between the rich and the poor. They then discuss Joe Biden’s recent nomination, the upcoming presidential election, and the importance of evaluating markets in a non-partisan way. In the intro, Jack Farley notes a stark contrast in the PMI data between Europe and the U.S.

via ZeroHedge News https://ift.tt/3j2zUcx Tyler Durden

Trump Team Assures Big Tech Lobbyists That WeChat Ban Won’t Impact China Business Tyler Durden

Fri, 08/21/2020 – 18:20

A little over a week ago, we shared how President Trump’s decision to expand the scope of his crackdown on Chinese tech firms to include WeChat, Tencent’s ubiquitous platform for everything from payments, to messaging to e-commerce sent a wave of panic through American multinationals like Apple who depend on the Chinese market for growth, and feared being essentially shut out due to an oversight by the administration.

The backlash has been just as intense as could be expected. In a quintuple-byline story published Friday afternoon, Bloomberg reported that an army of corporate lobbyists are working with Team Trump to try and find a way to restrict WeChat’s use in the US without hamstringing every American company that depends on the app to connect with Chinese consumers.

According to sources from within the West Wing, the administration is still “working through the technicals” of how they’re going to restrict WeChat in the US while allowing American companies to liaise with it in foreign markets.

The Trump administration is signaling that U.S. companies can continue to use the WeChat messaging app in China, according to several people familiar with the matter, two weeks after President Donald Trump ordered a U.S. ban on the Chinese-owned service.

The administration is still working through the technical implications of how to enforce such a partial ban on the app, which is owned by Tencent Holdings Ltd., one of China’s biggest companies. A key question is whether the White House would allow Apple Inc. and Alphabet Inc.’s Google to carry the app in its global app stores outside of the U.S., according to the people, who spoke on condition of anonymity.

Over the past week, lobbyists went into “overdrive” and started harassing White House and Commerce Department staffers about Trump’s order, and the “logistics and intention of the WeChat executive order.” Now they’re pushing to “narrow” the scope of the looming ban.

“We are talking to everyone who will listen to us,” said Craig Allen, president of the US-China Business Council, whose group represents companies including Walmart Inc. and General Motors Co. “WeChat is a little like electricity. You use it everywhere” in China, Allen said.

Author Robert Kiyosaki, who wrote the book Rich Dad, Poor Dad says the United States is headed for totalitarianism and that he wants to flee the country with his gold. American is already fascist, regardless of opinions on the matter.

In an interview with Kitco, Kiyosaki explains that Americans have almost lost every smidge of liberty that their ancestors had.

“The freedom of speech is gone. Freedom of speech, freedom of assembly, and also the freedom of religion,” he said.

Kiyosaki has prepared for a time when he would have to leave the U.S., he said, by holding safe-haven assets like gold and silver.

“Way back when I started storing gold in Switzerland and in Singapore, so in case I had to run, plus I had different passports. Gold and silver are flight capital, and as you know, the only people making money today in America are moving vans,” he said.

Regardless of the price of gold, whether it’s $1000 or $15,000, Kiyosaki says he will continue to buy more because it’s one way to protect yourself from the central banks. Kiyosaki wants to remind people that he fought for capitalism, not socialism. But the U.S. is becoming Marxist quickly.

In a tweet on Aug. 21, the author of Rich Dad Poor Dad told followers that there was no time to “think about” investing in safe havens.

“Major banking crisis coming fast”

The reason, he said, was that Warren Buffett had chosen to dump bank stocks.

“WHY BUFFET is OUT OF BANKS . Banks bankrupt. MAJOR BANKING CRISIS COMING FAST,” he wrote.

“Fed & Treasury to take over banking system? Fed and Treasury ‘helicopter fake money’ direct to people to avoid mass rioting? Not a time to ‘Think about it.’ How much gold, silver, Bitcoin do you have?”

WHY BUFFET is OUT OF BANKS . Banks bankrupt. MAJOR BANKING CRISIS COMING FAST. Fed & Treasury to take over banking system? Fed and Treasury “helicopter fake money” direct to people to avoid mass rioting? Not a time to “Think about it.” How much gold, silver, Bitcoin do you have?

He added that bitcoin also qualifies as a safety asset because it’s “international currency; it operates outside the Fed and the Treasury. Kiyosaki says he holds gold because it’s “God’s money” and Bitcoin because its the “people’s money.” He seems to be attempting to remove himself from the system of enslavement set up by the Federal Reserve.

via ZeroHedge News https://ift.tt/2Eu9PE8 Tyler Durden

“It’s Just Absolutely Incredible”: What’s Going On In The Corporate Bond Market Is Stunning Tyler Durden

Fri, 08/21/2020 – 17:40

In a recent report from hedge fund giant Brevan Howard, the investor pointed out the biggest flaw in the policy response to the covid pandemic: “Many businesses face solvency risks that are not addressed by borrowing; a debt overhang cannot be cured by more borrowing no matter how cheap it may be.“

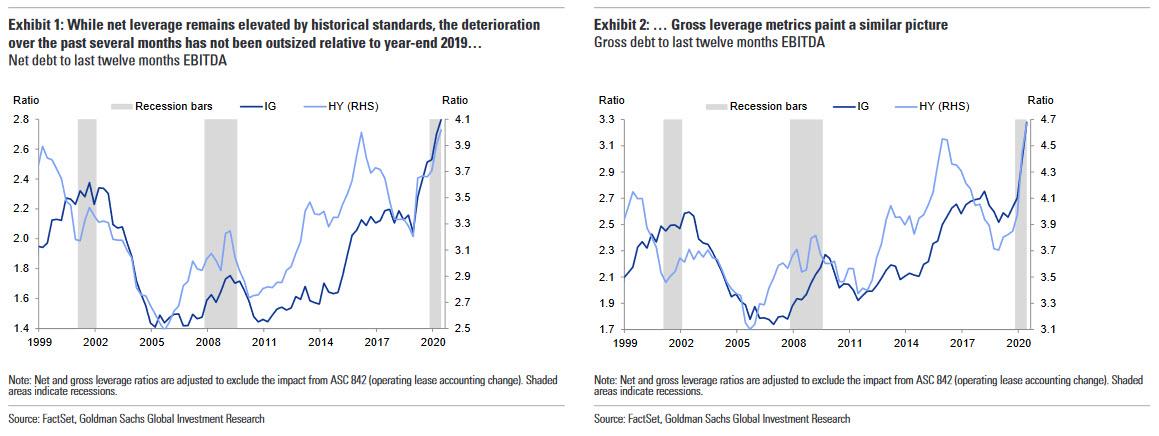

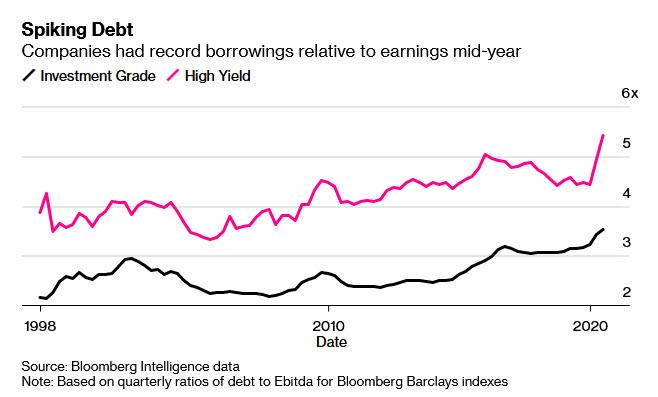

While that statement is absolutely true, and it applies not only to the aftermath of the covid shutdowns but everything that has happened in the past decade, it hasn’t stopped both government and corporations from going on a historic borrowing spree, in the former case thanks to “helicopter money” whereby central banks now directly monetize all the debt government treasurys have to sell, and in the latter as company CFOs take advantage of record low rates to borrow as much as possible before the window closes. This can be seen in the Goldman chart below which shows that both investment grade and high yield leverage is at all time high levels:

The numbers are staggering: on Friday, BofA Chief Investment Strategist Michael Hartnett calculated that US corporate bond issuance is currently annualizing a mindblowing $2.5 trillion this year, between $2.1TN for IG and $0.4TN for high yield. As Bloomberg writes today, while much of that fresh cash – more than $1.6 trillion in total – has helped scores of companies stay afloat during the pandemic lockdown, “it now threatens to curb an economic recovery that was already showing signs of sputtering” as many companies will have to divert even more cash to repaying these obligations at the same time that their profits sink, leaving them with less to spend on expanding payrolls or upgrading facilities in months ahead.

The paradox is that this is all by design: in doing everything in its power to prevent the corporate debt bubble – which was already at a record size before the covid pandemic – from bursting, the US central bank unleashed monetary policies that have terminally decoupled the bond market from all fundamentals, while also arresting default risks by taking over credit risk without punishing investors and moving into lower-rated debt than ever before, which started off the risk-on period as Nordea’s Andreas Steno Larsen writes today and shows in the following chart:

In a sign of just how pronounced the borrowing overhang has become, Bloomberg points out that the average junk-rated company had debt levels relative to earnings that were so high in the middle of the year, according to a new analysis by Bloomberg Intelligence, that they almost would have tripped do-not-touch alerts from banking regulators a few years ago. Those warnings back then only applied to a handful of borrowers. Had regulators not opted to drop these warnings, they could today apply to far more.

Corporations have also been borrowing heavily as the Fed has slashed short-term interest rates to near zero and supported credit markets through, for example, buying company bonds. Lower rates have spurred investors to buy higher-yielding, riskier securities, which has allowed even junk-rated firms to borrow more to tide them over during the crisis. High-grade issuers have already sold more bonds in 2020 than any other full year in history. Junk corporations have surpassed 2019’s total already.

Some specifics: leverage (i.e., the ratio of total debt to Ebitda) for investment-grade companies was 3.53x in the second quarter for the Bloomberg Barclays U.S. Corporate high-grade index. That’s the highest in data going back to 1998, and is up from 3.42 in the first three months of the year, when the impact of the pandemic was only just beginning to show up in earnings. It compares with a 20-year average of 2.65.

For high yield, leverage stood at a record 5.42 at the end of June, up from 4.93 at the end of March and 4.44 at the end of 2019. Avis Budget Group Inc., the car rental company, had debt equal to 27 times earnings as of June 30, up from five times at the end of March, as it burned cash in the second quarter, although that figure could improve later this year as its earnings start to rebound. In 2016, banking regulators pushed back against leveraged buyouts that left companies with ratios above six.

No matter how one slices the data the message is clear: “An overburdened corporate sector is likely to grow less rapidly and that could slow the whole recovery down,” said Kathy Jones, chief fixed-income strategist for Charles Schwab.

Of course, none of that matters now when rates are at all time lows, but fast forward a few years when inflation kicks in and suddenly corporate America is facing another unprecedented crisis as it has to not only rollover record amounts of debt but has to refi into ever higher rates.

Quoting Lale Topcuoglu, senior fund manager at JO Hambro Capital Management in New York, Bloomberg warns that a slower recovery could have wide-reaching implications in financial markets. Many securities prices reflect investors’ expectation that profits will normalize next year, when in fact it could take at least two or three years. Not surprisingly, she believes that many junk bonds as being overpriced.

“It just seems absolutely incredible how much people are closing their eyes and buying,” Topcuoglu said.

The good news is that unlike last year when much of the new debt issuance went to fund stock buybacks, much of the debt sold in recent months has refinanced maturing borrowings allowing companies to lock in even lower rates for the next 5 to 10 years; furthermore many of the companies are holding on to the money they raised as cash and may end up not spending it.

And while the fact that companies managed to stay afloat during the pandemic is “a good thing compared with the alternative of even more corporations having gone bankrupt” not all companies have been able to access that credit, with smaller borrowers often getting shut out as a DoubleLine Portlio Manager wrote WEdnesday in “Large Firms Reap Benefits From Central Bank Easing As Small Ones Suffer.”

To be sure, even the large companies face a day of reckoning or as Bloomberg puts it simply “a hangover” as many corporations were already groaning under their debt loads even before the Covid-19 pandemic, and now will have to work harder to cut borrowings as earnings remain depressed. Even if companies are hanging on to the money they borrowed, they must still pay interest on it, and could eventually use the cash if the pandemic drags on. Many will simply revert to using the debt proceeds to repurchasing their stock and make quick profits for management and shareholders as we pointed out earlier this week. Ultimately it is the economy, and the middle class workers who will suffer the most as chief JPM economist Michael Feroli wrote, warning that with corporations shunting more of their earnings toward paying interest and paying down debt, they will struggle to hire and invest as much as they would at the end of a more conventional recession.” That could translate to a relatively sluggish recovery instead of the fast, “V-shaped” one many investors hope for.

“The debt overhang is going to be a headwind for capital spending and for hiring, not just in the second half of the year but probably into next year as well,” Feroli said.

Another paradox is that as corporate leverage is rising to all time highs, rates continue to sink as investors have no choice but to buy their debt, which in turn forces even more debt issuance, even higher leverage and so on, until the Fed is tasked with yet another corporate debt bailout:

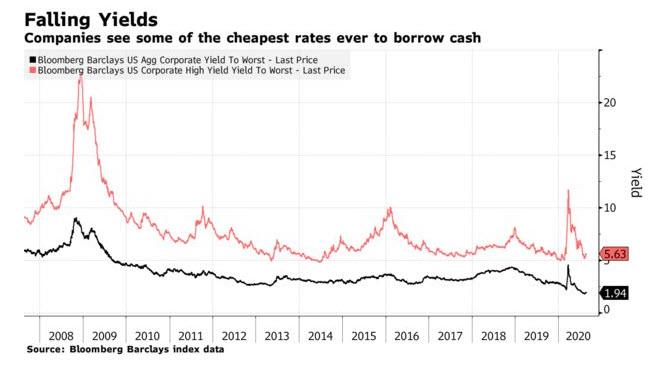

With short-term interest rates having fallen to near-zero levels, borrowing is cheaper for most companies than it was just a year ago. Average yields on U.S. investment-grade corporate bonds touched all time lows of 1.82% earlier this month, and are still hovering near those levels, according to Bloomberg Barclays index data.

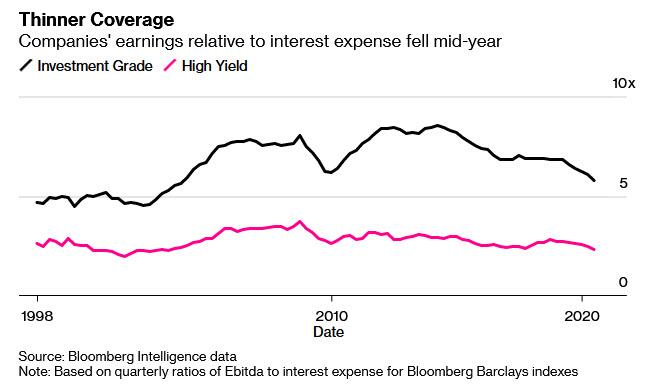

As a result of record low rates, even as leverage soars, interest coverage, or EBITDA to total interest expense, has fallen to 5.8 in the second quarter for investment-grade companies, compared with a 20-year average closer to 7. The June 2020 level was the lowest since 2003. For junk-rated companies, the interest coverage ratio fell to 2.3 in June, also the lowest since 2003.

Unlike the 2008 bubble, ratings firms have taken note of the broad downward trend in credit quality, with S&P downgrading more high-yield debt in the second quarter, relative to upgrades, than any time in at least a decade, according to data compiled by Bloomberg. That too has not stopped investors from piling on: just recently junk-rated Ball Corporation sold debt for the lowest ever yield for a “high” yield bond at 2.875%.

Meanwhile, corporate earnings per share fell by about a third in the second quarter from the same period last year, and are likely to fall in the third and fourth quarters as well and may not recover their 2018 levels until the end of 2021. As a result, strategists expect leverage and interest coverage to erode further.

None of this fazes investors who have gone “balls to the wall” buying corporate debt with the Fed’s blessing now that the central bank is buying both investment grade and high yield ETFs and bonds in the open market. To justify the euphoria, investors have given companies a break for about a year and are looking ahead into mid-2021 or even later to evaluate where they will perform after, for example, the world finds and distributes a Covid-19 vaccine. That to Bloomberg explains why cruise companies that are burning cash, such as Royal Caribbean Cruises Ltd. and Carnival Corp., have been able to borrow repeatedly, and have seen most of their new bonds trade well above the price at which they were originally sold.

But even if bond prices are broadly rising, investors need to be cognizant of the risks they’re buying, said Schwab’s Jones.

“This cycle is very different because we’ve had so much support from central banks and we have so much liquidity in the market,” Jones said. “But the old saying ‘liquidity does not equate to solvency’ is something people need to keep in mind when they’re investing.”

Brevan Howard would most certainly agree.

We give the final word to GnS Economics’ founder Tuomas Malinen who today writes that “we have stock markets that have decoupled from real economic activity to an unprecedented degree and a moribund European banking sector practically doomed to collapse. The constant resuscitation and bailouts of the central banks since the last crisis in 2009 have pushed us to the brink of ‘Financial Armageddon’, initiated this time by the repo-market implosion and the coronavirus pandemic.”

His conclusion: “When it truly gets going, as it likely will, do not blame the virus. Blame the reckless central bankers.“

via ZeroHedge News https://ift.tt/329FuDc Tyler Durden

Smith is apparently involved with Jennings’ ex-wife, who is in a bitter custody battle with Jennings. Jennings, Smith alleged, had written posts falsely stating that Smith was a “pedophile” and a “known predator” (see the application for the TRO for more), so Smith sued Jennings for libel.

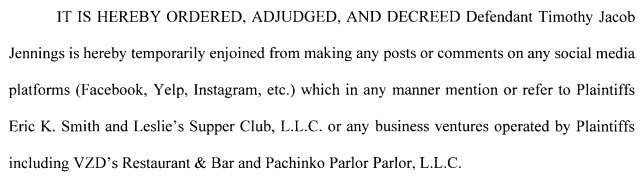

So far so good: Smith might have a valid libel claim. But instead of just getting damages, or even an injunctions against future libels, the court issued this pretrial restraining order (Smith v. Jennings(Okla. Dist. Ct.), dated Wednesday):

That can’t be constitutional, it seems to me.

But beyond that, Oklahoma is one of the several states that still forbids injunctions in libel cases, even narrow injunctions that ban repeating statements found to be libelous after a trial on the merits. See House of Sight & Sound, Inc. v. Faulkner, 912 P.2d 357, 361 (Okla. Civ. App. 1995); First Am. Bank & Trust Co. v. Sawyer, 865 P.2d 347, 352 (Okla. Civ. App. 1993). There is a narrow exception for “conspiracy, intimidation, or coercion,” but it is narrow indeed, and First Am. Bank & Trust Co. made clear that the “coercion” element is not satisfied simply by speech being aimed at pressuring a business to give the speaker a refund or similar benefit.

And I’ve seen plenty of other cases that issue such clearly unconstitutionally overbroad injunctions. Just a reminder, I think, that things happen in trial courts that are hard to reconcile with the appellate precedents—and if the losing party doesn’t have the money, energy, or time to fight the case on appeal, the trial judge’s decision stands.

from Latest – Reason.com https://ift.tt/2COg19P

via IFTTT

A coalition of New York City police, firefighter, and prison guard unions have lost their bid to block the city’s planned release of a huge trove of police misconduct records. The ruling clears the way, at least for the moment, for New York City’s Civilian Complaint Review Board (CCRB) to post officers’ complaint histories, and for the New York Police Department to release separate disciplinary records it holds.

All those records had been confidential for the past 40 years under Section 50-a, a notorious police secrecy law. But the New York legislature repealed the law in June—a stinging defeat for police unions, who are still bitterly fighting to claw back what records they can. Today U.S. District Judge Katherine Polk Failla declined to grant a preliminary injunction barring New York City from releasing unsubstantiated misconduct allegations.

“Whoa!” an unidentified person on an unmuted line shouted during the telephonic court hearing, as Failla announced she was almost totally rejecting the police unions’ request.

Last month, Failla temporarily blocked New York City from disclosing the records while she weighed the unions’ arguments that the release of unsubstantiated complaints would lead to retaliation against police officers and harm their reputations and future employment prospects.

But before the unions filed their lawsuit, the review board released misconduct records to the New York Civil Liberties Union (NYCLU) and ProPublica, the latter of which published its own database of more than 4,000 complaints. A court initially blocked the NYCLU from releasing its records, but yesterday the 2nd Circuit Court of Appeals lifted that stay as well.

The NYCLU immediately published a database of more than 320,000 complaints filed against the city’s police officers since 1985. The New York Timesreports that only 3 percent of those complaints were substantiated.

Today Failla ruled that the unions had failed to demonstrate the release would cause concrete harms or risks for officers.

“Plaintiffs have presented speculation only that these disclosures will increase risk of officer harm,” Failla said, noting that such records are public in a dozen other states.

Failla did, however, grant a narrow injunction blocking the city from releasing records on certain low-level disciplinary offenses that can be expunged under the officers’ collective bargaining agreement.

CCRB Chair Fred Davie said in a press release today that this outcome “is not only legally justified, but is the only logical path forward for preserving what New Yorkers and lawmakers intended through the repeal of 50-a. I applaud today’s decision—the fight for transparency has been delayed, but not deterred.”

The unions have until Monday afternoon to appeal Failla’s ruling to the 2nd Circuit Court of Appeals.

from Latest – Reason.com https://ift.tt/3l0CUYK

via IFTTT